Abstract

In 2020, Nebraska sought to provide property tax relief through an income tax credit against public school property tax levies. Millions of dollars of the tax credit were offered and went unclaimed. The state responded by mailing notifications to 6,000 taxpayers that informed them of the opportunity to claim the missed credit using a simplified form. Treatment effects estimated using taxpayer microdata show that the credit take-up rate of notified taxpayers was 20 percentage points greater than that of 9,905 taxpayers selected for potential notification but received no contact. Taxpayer subgroups, such as self-preparers, married taxpayers that filed jointly, and rural taxpayers were among those most responsive to notification.

Introduction

When a new income tax exclusion, deduction, or credit is enacted and implemented, do taxpayers understand when and how to claim it? In this research, we investigate Nebraska's experience with implementing a refundable income tax credit against school district property tax levies. Soon after enactment of the credit, the Nebraska Department of Revenue (Department) found that take-up of the income tax credit was much lower than predicted: Millions of dollars of income tax credits were made available to taxpayers but went unclaimed. To help increase take-up of the tax credit, the Department embarked on an awareness campaign which included the mailing of a postcard notification to certain taxpayers. The Department mailed the notification to taxpayers it estimated would be most likely to claim the credit retroactively, and it developed a special form intended to simplify the process of claiming the credit that would not require filing an amended income tax return.

Using methods of matching notified taxpayers to non-notified taxpayers to estimate the causal effect of the postcard mailings, we estimate that the notification campaign increased the income tax credit take-up rate by about 18–20 percentage points among those that were notified by the Department relative to taxpayers that were not notified. Our research contributes to the taxpayer notification literature by providing a contrast to previous investigations of correspondence sent to taxpayers intended to increase take-up rates of the federal refundable income tax credits, such as the earned income tax credit (EITC). Unlike the EITC, Nebraska's refundable income tax credit against public school property tax levies is not means tested and is likely to be claimed by relatively higher-income taxpayers. Also, taxpayers eligible to claim the credit are likely to regularly file a state income tax return. Statistics of Income reported by the Department for Tax Year 2021 show that 58.4 percent of the income tax credits against school district levies were claimed by taxpayers with federal adjusted gross incomes of $100,000 or greater (Nebraska Department of Revenue 2022).

The process of claiming Nebraska's income tax credit against public school levies required taxpayers to extract and report information related to parcel identification numbers and property taxes paid from an external database. By contrast, the federal EITC can be automatically calculated and applied to a taxpayer's liability using electronic income tax filing software for taxpayers that meet the EITC qualification criteria. Therefore, the case of Nebraska's refundable income tax credit provides evidence that relatively higher income, property-owning taxpayers are also prone to failing to claim income tax credits for which they qualify. Even some professional tax preparers failed to claim the credit on behalf of their clients: About 14 percent of taxpayers that hired a professional preparer to complete and file their Nebraska income tax returns missed the credit. These taxpayers then retroactively claimed it. The evidence presented in this paper suggests that the taxpayers notified by the Department about the missed credit are more responsive to notification than those targeted for increased take-up of the EITC. Subsamples of taxpayers, such as married taxpayers filing jointly, self-preparers, and rural taxpayers are among the most responsive to notification.

Public finance scholars have studied taxpayer notification campaigns that generally correspond with one of the two following goals: To increase tax compliance or to increase the take-up of social benefits offered through the income tax code. Tax administration agencies frequently communicate with taxpayers via written correspondence, such as through deficiency determination notices. Several scholars test the subsequent behavior of taxpayers to experimental messages that range from those including threats of legal action, an appeal to civic pride, or to social norms. Slemrod, Blumenthal and Christian (2000) find that notifications that suggest the taxpayer's return will be “closely examined” increased reported taxable income among lower- and middle-class taxpayers, while treated high-income taxpayers reported less taxable income. Little treatment effect was found among reported taxable income from a letter intended to evoke civic pride (Blumenthal, Christian and Slemrod 2001). Castro and Scartascini (2015) test messages related to deterrence, reciprocity, and peer-effects among Argentinian property taxpayers, finding that only the deterrent message elicits a statistically significant response among taxpayers receiving the message.

Anderson (2017) studies Nebraska's postcard notification to taxpayers in 2009, which informed them of the circumstances under which use tax liability arises and how they may satisfy that outstanding liability through the individual income tax return. He finds that the postcards raised a negligible amount of use tax revenue – just enough to pay for the printing and mailing of the postcards. Hallsworth et al. (2017) find a positive effect on payment rates of delinquent taxes arising from the inclusion of social norm messages (gain framing) included in notices sent to taxpayers in the United Kingdom. Meiselman (2018) finds that messages that emphasize the penalty of failing to file a City of Detroit income tax return saw the greatest increase in compliance among recipients of the notice, while Chirico et al. (2016) found modest effects of notices sent to taxpayers with delinquent property taxes in Philadelphia. Perez-Truglia and Troiano (2018) contact delinquent taxpayers from publicly-posted lists and find that increasing the visibility of one's delinquent taxes increases their settlement rates for those with delinquent tax amounts up to $2,500. Angaretis et al. (2024) find that letters sent to candidates for inclusion on California's “Top 500” delinquent taxpayer online publication induced a strong compliance response among receipients.

Another thread of taxpayer notification research relates to nudges intended to encourage taxpayers to claim social safety net benefits through the income tax code. This research is motivated by concern that socioeconomic barriers may prevent potential beneficiaries of social programs from claiming them, such as lack of awareness of means-tested credits, administrative complexity arising from the process of claiming them, or a lack of engagement with the income tax system, particularly when the mandatory income threshold for filing an income tax return exceeds the taxable income of the taxpayer. This thread of research seeks to identify what form of notification or outreach helps increase credit take-up by informing potential program beneficiaries that they may qualify for benefits and/or how to claim them.

Bhargava and Manoli (2015) find that taxpayers who did not claim the federal EITC when their income tax returns were initially filed were responsive to follow-up notifications encouraging them to claim the EITC. However, while some taxpayers qualify for refundable income tax credits, they do not file an income tax return, and therefore are more difficult to reach for notification. Goldin et al. (2022) study an IRS outreach initiative with the goal of increasing refundable income tax credit take-up by encouraging low-income taxpayers to file an income tax return, finding modest effects of the intervention on credit take-up. Using lists of California SNAP beneficiaries who have not filed California state income tax returns, Linos et al. (2022) attempt to contact potential EITC recipients and direct them to guided taxpayer assistance. They find that no method of notification or assistance made a significant difference in the EITC take-up rates of notified taxpayers.

We proceed by providing context and background that explains the origins of Nebraska's income tax credit against public school levies and the circumstances that led to its enactment. We then describe the process by which the Department selected taxpayers to notify with the goal of maximizing the size of tax credits claimed. Because the taxpayers were not randomly selected, we use propensity score matching and coarsened exact matching to estimate the effect of the postcard on the credit take-up rates of those notified. The postcard notification campaign was largely successful in increasing credit take-up among those who were selected for notification: The postcard increased the credit take-up rate by about 18–20 percentage points among notified taxpayers. We conclude by reporting the legislative fate of the income tax credit.

Background

Public School Reliance on Property Taxes in Nebraska

According to the U.S. Census Bureau, public school districts in Nebraska receive a disproportionately large share of their total revenue from local sources – specifically, the property tax – relative to other states. 1 The Census Bureau's per pupil spending figures rank Nebraska as the 13th most reliant on local revenue sources to fund public elementary and secondary education. Meanwhile, Nebraska's state per pupil contribution ranks 46th. Anderson (2018) finds that Nebraska's per capita property taxes are the 13th highest in the United States, while total property tax as a percentage of state-local revenue is 11th highest. The Tax Foundation ranks Nebraska as having the seventh-highest ratio of property taxes paid as a percentage of owner-occupied housing value (Fritts 2021).

Given that the property tax is among the most salient taxes facing taxpayers (Cabral and Hoxby 2015), Nebraska's high reliance on property taxes to fund public education often motivates its public officials to call for property tax relief. This theme routinely dominates the campaign platforms of each gubernatorial candidate and the policy priorities of each session of the Nebraska Legislature. The Speaker of Nebraska's Unicameral Legislature, John Arch, suggests that while many agree that the state should rebalance revenue sources at the local level, there is little agreement over what revenue source is best suited to offset a reduction in property taxes. The debate is aptly summarized: “Battles over taxes have been raging in Nebraska for nearly 60 years, dating back to the enactment of the state sales and income taxes to replace property taxes that used to pay for state government.” 2

The Property Tax Credit Act of 2007

In 2007, the Nebraska Legislature created the Property Tax Credit Cash Fund. The goal of this account is to receive transfers from the state general fund for the purpose of reducing individual taxpayer property tax bills. The fund's proceeds are distributed to counties according to the ratio of the valuation of real property in the county relative to that of the state (Nebraska Legislature 2023). A property tax credit is then determined and applied to taxpayer statements according to the taxpayer's ratio of taxable property to that of the county. Like other components of the property tax calculation, application of credit requires no action on the part of taxpayers. The Legislature enacted minimum transfers to the Property Tax Credit Cash Fund of $395 million in FY 2023, rising to $475 million by FY 2028. There is concern among state policy makers that the property tax credit is not sufficiently visible to taxpayers. According to one Nebraska state senator, “many people don’t realize that they are getting a credit from the state” because total property tax liability is shown on taxpayer statements after the credit is deducted. 3

Rising Agricultural Land Valuations and 2018 Ballot Initiative

During the years after the Great Recession, Nebraska's agricultural land prices increased from $1,013 to $3,315 per acre between 2006 and 2014, respectively, before surging again in 2020 (Jansen and Stokes 2023). The surging agricultural land valuations exposed its owners to rising property tax bills, increasing from 28 percent to 47 percent of Nebraska farmer and rancher net income in 2016 and 2017, respectively (Aiken 2019). Nebraska assesses the taxable value of agricultural land at 75 percent of its market value. As such, the proportion of the Property Tax Credit allocated to agricultural property increased from 25 percent in 2008 to 48 percent in 2017 (Nebraska Legislature 2021).

Typically, an expansion in the local property tax base associated with increased taxable land valuations is balanced by decreasing property tax rates which generates the amount of property tax revenue necessary to fund each school district's budget. However, the state education equalization formula decreases aid to school districts as local resources increase, ceteris paribus. Therefore, real property owners in non-equalized school districts saw rising property tax bills to offset reduced state equalization aid to school districts (Patent 2015). Agricultural landowners and their representatives in the Nebraska Legislature argued that they paid a disproportionately large share of local education expenses while paying income taxes that support equalization aid for the state's urban school districts. 4 Most rural school districts in Nebraska do not receive state equalization aid because their formula resources exceed the district's formula needs (Nebraska Department of Education 2024). 5

In 2018, a constitutional amendment was proposed via ballot initiative which would have created a refundable income tax credit at a rate of 50 percent against property taxes paid to school districts, a tax expenditure whose cost would exceed one billion dollars. Progress of the ballot initiative was impeded over concern that the Nebraska Legislature, which reserves the right to override such initiatives, would have intervened when faced with such a costly proposal. Ultimately, the initiative did not garner enough signatures to qualify for its placement on the November 2018 ballot. 6 Subsequent plans were announced to introduce a constitutional amendment that would allow taxpayers to claim a 35 percent income tax credit against property taxes during the 2019 Legislative Session. 7

The Nebraska Property Tax Incentive Act of 2020

During the 2020 Legislative Session, the Nebraska Legislature enacted the Nebraska Property Tax Incentive Act, which introduced a refundable income tax credit against property taxes paid to school districts in a form that largely resembled that of the previous income tax credit proposals discussed above. In addition to achieving the goal of forcing the state to subsidize property taxes paid to school districts through credits against the income tax, a motivation for the taxpayer-active approach to property tax relief on the part of state lawmakers was “in part to make the state tax break more visible to taxpayers.” 8 Taxpayers were allowed to claim the credit against income tax liability for the first time during the 2020 tax year. The statute authorizing the credit requires the Department to set a rate for the credit that would fully utilize a certain level of tax expenditure in a given tax year. In 2022, the Nebraska Legislature expanded the income tax credit to property taxes paid to community colleges. The credit may not be claimed against bonded indebtedness of the school district, levy overrides approved by voters, or against property taxes five or more years delinquent. 9

For Tax Year 2020, the Department set a credit rate of 6.0 percent on the basis of a statewide total of $2.6 billion in school district property taxes levied with the goal of exhausting $125 million in tax credits (Nebraska Department of Education 2019). This credit rate implies 100 percent credit take-up. However, the Department observed that credit rate of 6 percent fell far short of fully exhausting the tax credit target for Tax Year 2020: Only $67.7 million of the credits were claimed that year. As the tax credit limit increased to $548 million in Tax Year 2021, the Department increased the credit rate to 25.3 percent on the basis of $2.6 billion in statewide school district property tax levies, again assuming 100 percent take-up of the credit. These credits were available to claim when taxpayers filed their 2021 Nebraska state income tax returns during the 2022 income tax filing season. Actual credit take-up rates again fell short of the targeted credit amounts, as $274.5 million of the $548 million available was claimed for Tax Year 2021. This led the Department to increase the credit rate to 30 percent for Tax Years 2022 and 2023 with the goal of reaching the tax credit goal while assuming less than 100 percent take-up of the tax credit. Despite the increased credit rate, claims of the income tax credit increased to $357.8 million for Tax Year 2022, still falling short of the $548 million allocated by statute (Nebraska Department of Revenue 2022).

The credit appears on line 36 of the Nebraska Individual Income Tax Return (Form 1040N). To calculate and claim the credit, taxpayers must complete Form PTC, which requires the use of a web-based look-up tool which lists school district property taxes paid according to parcel identification number. Parcel information and property taxes paid are copied by the taxpayer to Form PTC individually for each parcel subject to school district taxes during the given tax year. For taxpayers filing electronically, the taxpayer must be aware that the tax credit exists and select it from a list of several tax credits. For Tax Year 2021, TurboTax labeled the credit, “Property Owned by an Individual Tax Credit.”

Publicizing the Income Tax Credit after the 2021 Tax Filing Season

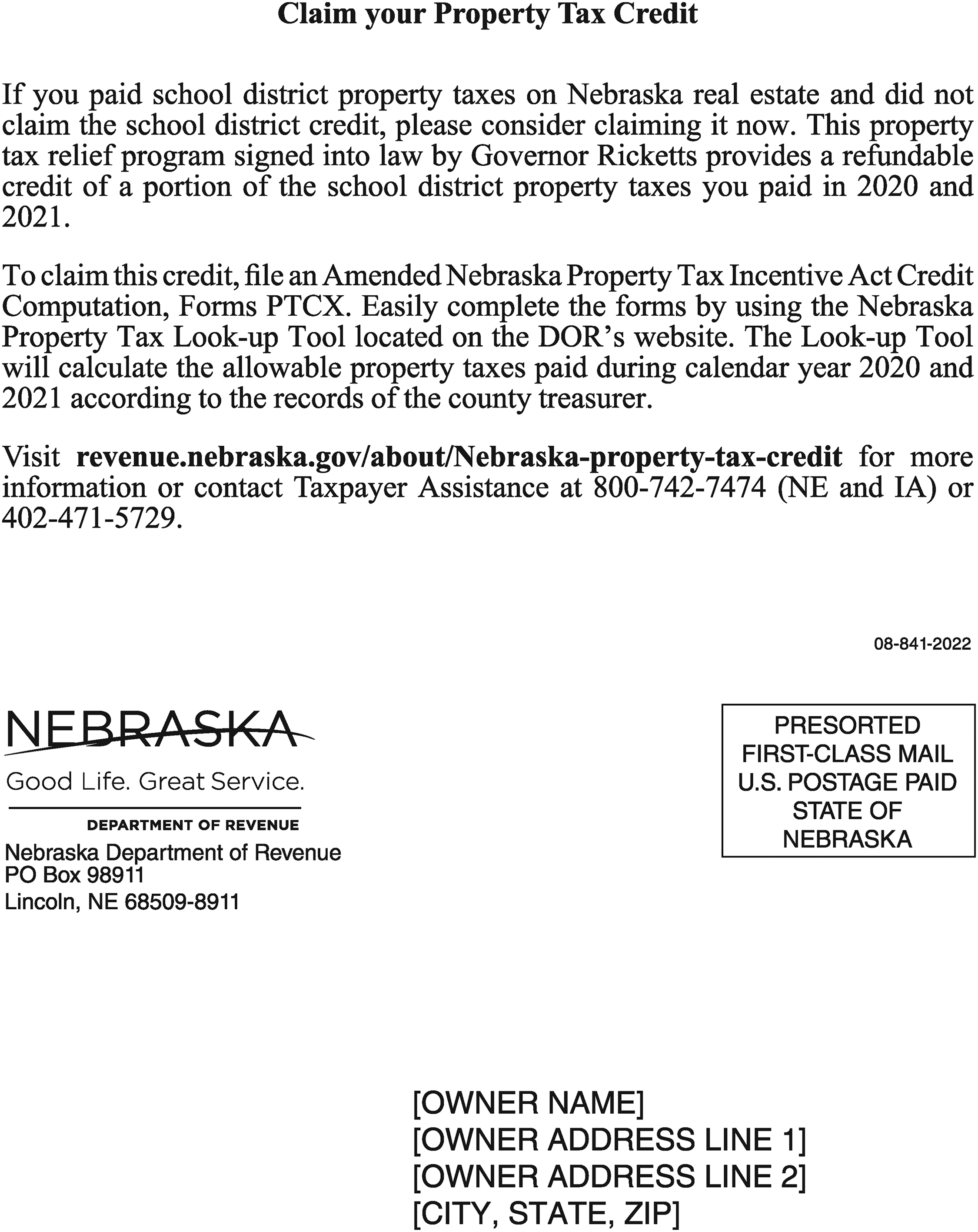

Amid lower-than-expected take-up of the income tax credit after the Tax Year 2021 filing season, Governor Pete Ricketts and the Department launched an information campaign to promote awareness of the tax credit and to increase its take-up rate. This campaign included a press conference held on September 15, 2022, which was covered by local news outlets across the state. To further expand awareness and increase take-up of the credit, the Department mailed postcards to 6,000 taxpayers who did not claim the income tax credit on their 2020 and 2021 Nebraska income tax returns. The postcard is displayed in Figure 1. As shown on the postcard, taxpayers who did not claim the income tax credit but paid school district property taxes in 2020 and 2021 were not required to file an amended income tax return to claim the credit. Instead, eligible taxpayers may file Nebraska Form PTCX to claim the credit if the taxpayer failed to do so on the original return.

Property tax credit postcard mailed to selected taxpayers.

Research Design

Taxpayer Selection

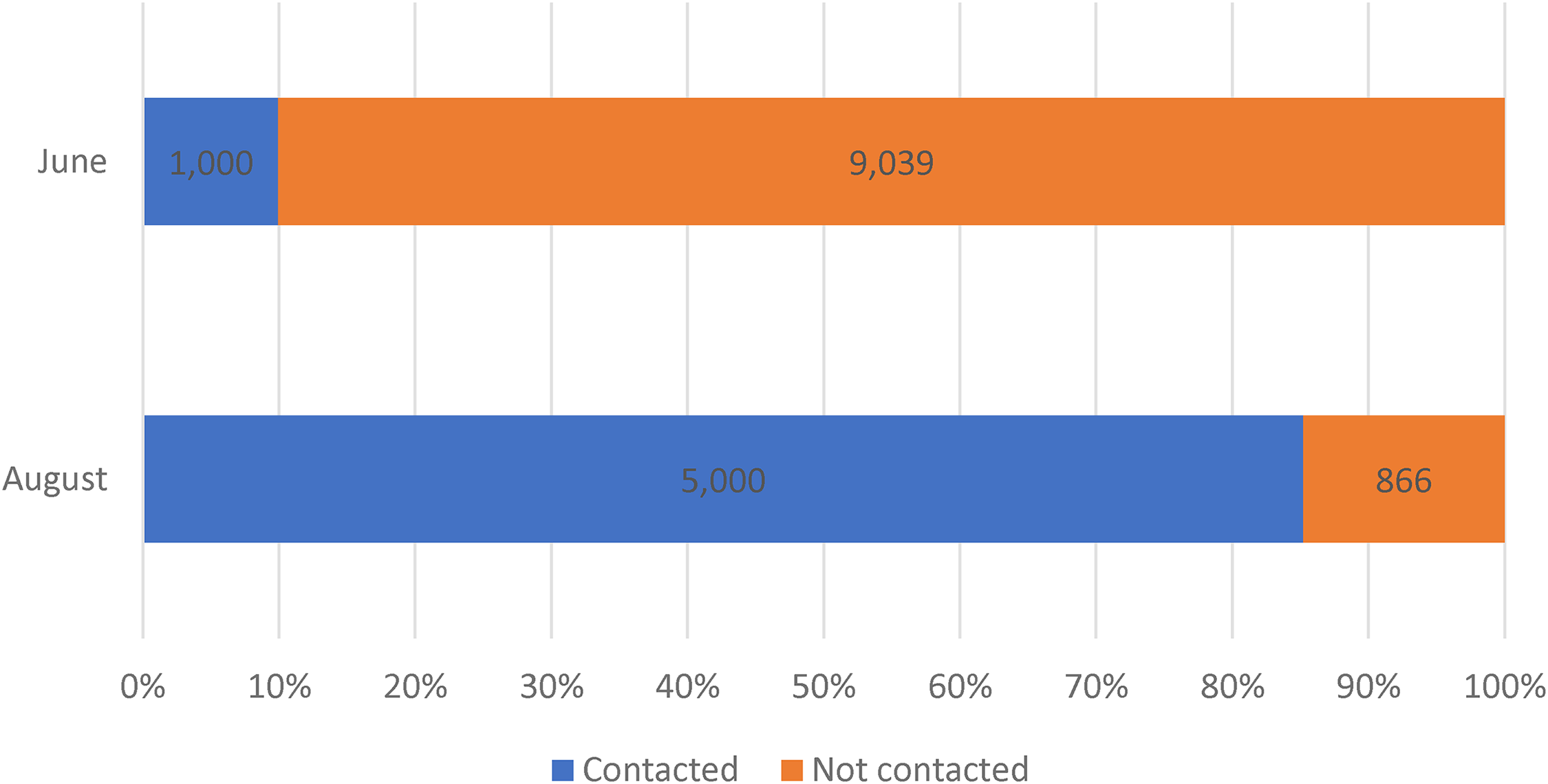

The Department sought to identify taxpayers for notification that did not claim the income tax credit on their income tax returns for Tax Years 2020 and 2021. Further, the Department set a goal of maximizing the potential size of tax credit claimed per notification sent. To accomplish this, the Department estimated the size of these unclaimed income tax credits by matching each taxpayer's name and address fields in its income tax database with the property owner name and address fields in property tax data obtained from counties. 10 This matching process enabled the Department to estimate the size each taxpayer's missed income tax credit by observing the estimated property tax liability of each income taxpayer that did not claim the credit. The Department sorted the list of income taxpayers in descending order by the size of the taxpayers’ estimated unclaimed income tax credits. 11 On June 23, 2022, the Department identified the top 10,039 potential income tax claimants. The top 1,000 taxpayers with the largest estimated unclaimed income tax credits among the 10,039 initially selected were then mailed a postcard notification. This first phase of the notification process was intended to serve as a preliminary test of the selection and notification process before implementing the notification campaign on a wider scale. The remaining 9,039 taxpayers that were selected but not notified in June were excluded from the subsequent August round of selection, sorting, and notification, and therefore become part of the non-notified taxpayer group. As the postcard notification campaign was funded by the Department's general operating budget, the number of postcards mailed was a function of short-term budgetary decisions made by the Department administration.

The sorting and notification procedure was repeated on an expanded basis on August 3, 2022. The Department selected 5,866 taxpayers that it identified as having the largest unclaimed tax credits. The Department then mailed postcards to the top 5,000 taxpayers that the Department estimated as having the largest missed credits, leaving an additional 866 non-notified taxpayers. 12 In total, 6,000 postcards were mailed to taxpayers, and 9,905 taxpayers were selected as eligible candidates for notification but were not contacted. The second batch of postcards was mailed just over one month before Governor Pete Ricketts held a press conference on this matter on September 15, 2022. Figure 2 offers a visual depiction of the notification status for both the June and August cohorts of taxpayers selected for potential contact. The figure clearly shows that most taxpayers selected in the June cohort were not contacted, and most taxpayers selected in the August cohort were contacted.

Taxpayer notification by cohort.

Data

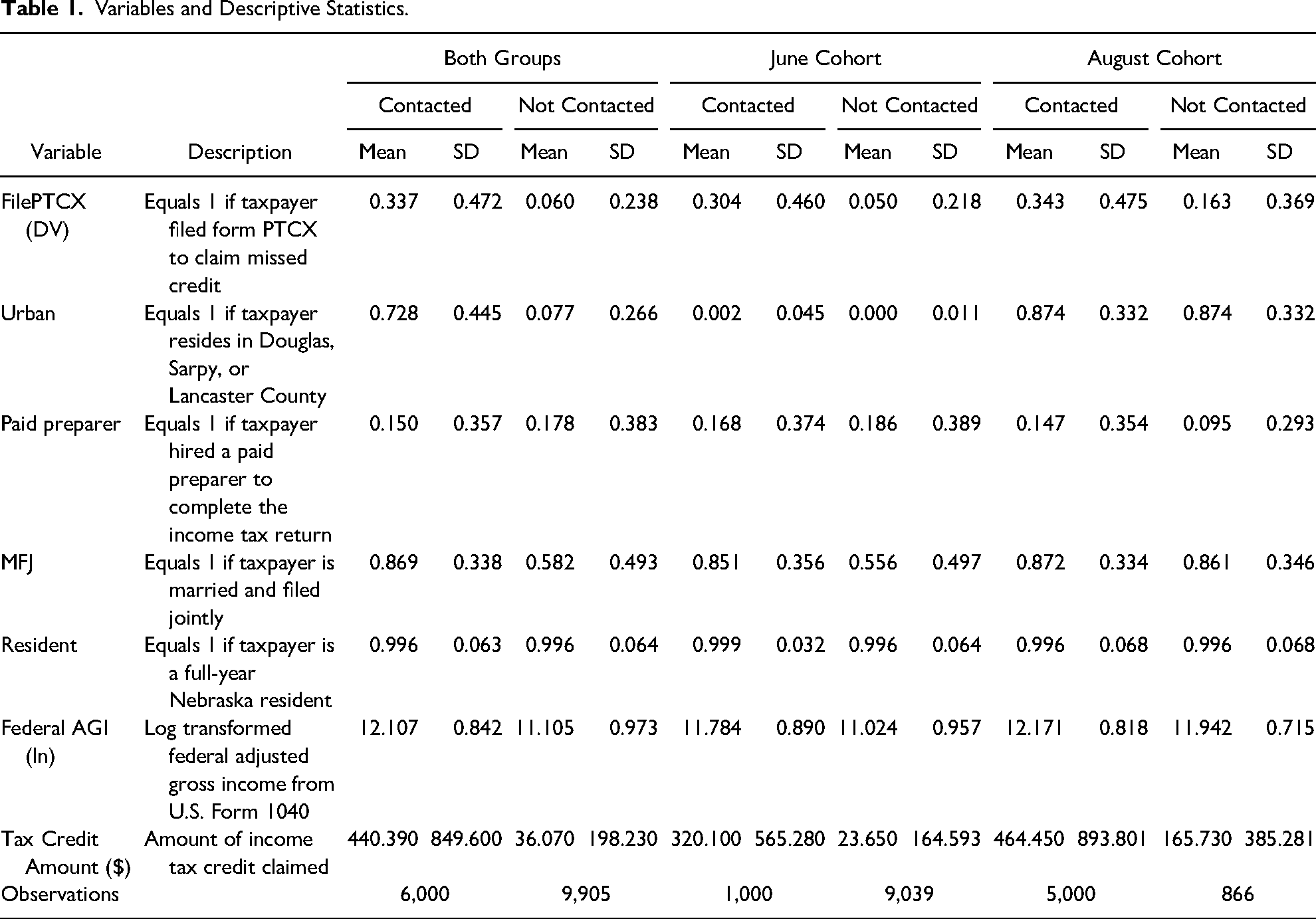

The dataset used for this research consists of the lists of taxpayers selected by the Department discussed in the previous section. The dataset includes the following variables displayed in Table 1 which are derived directly from individual income tax returns associated with Tax Year 2021. The summary statistics of the raw data shown in Table 1 make clear that the notified and non-notified taxpayers are systematically different. A striking result of the sorting by cohort process is that very few urban taxpayers were selected for potential notification in the June cohort, implying that nearly all of those with the largest unclaimed credits are rural taxpayers outside of the Lincoln and Omaha metropolitan areas. In the June cohort, only 0.2% of notifications were sent to taxpayers with the top 1,000 estimated unclaimed credits in the state's urban counties. However, the August cohort of contacted taxpayers disproportionately represent the state's three urban counties: About 87% of those selected for notification were located in urban counties which have a combined population of about 1.1 million as of 2022, totaling about 56% of the state population. Overall, taxpayers that were selected in June cohort were more relatively more responsive to notification than members of the August cohort.

Variables and Descriptive Statistics.

Overall, contacted taxpayers are more likely to file their initial returns jointly with a spouse, and they reported higher adjusted gross incomes than those who were not contacted. These imbalances are artifacts of the Department's nonrandom taxpayer selection process that prioritized notification of taxpayers with the largest estimated income tax credits. As discussed earlier, the Department faced the classic constrained optimization problem: The objective of the postcard notifications was to maximize taxpayer claims of the income tax credit, subject to the Department's budget constraint. The Department mailed the postcard to taxpayers who arguably had the most to gain by claiming the credit. Among them, the June cohort of contacted taxpayers had more to gain from claiming the credit than the August cohort, according to the taxpayer sorting and selection process. Therefore, an ordinary least squares regression of credit claims on notification and taxpayer controls is likely to overstate the effect of the notification. However, the non-notified taxpayer group consists of the taxpayers that are among the most comparable to the notified taxpayers given the sorting process that placed them among the top 15,905 taxpayers with the largest estimated tax credits.

Empirical Methods

Because neither the notified and non-notified taxpayers were randomly selected from the universe of Nebraska income taxpayers, we use three statistical methods to develop a range of estimates related to the causal effect of the postcard mailing on tax credit take-up rates. First, we estimate an ordinary least squares regression of credit take-up on notification and taxpayer covariates, recognizing that this method likely suffers from biased estimates of credit take-up due to imbalances among the two taxpayer groups. Table 1 presents the extent of imbalance between the notified and non-notified taxpayer groups that must be addressed. Next, we implement propensity score matching with the goal of addressing imbalances in observable characteristics between notified and non-notified taxpayers. However, the limitations of the propensity scores as a matching method are well documented. King and Nielsen (2019, p. 2) argue that the blocking methods accomplished through coarsened exact matching provide a superior alternative to the use of propensity scores as a matching method, and they argue that propensity scores randomly prune observations that increases imbalance.

Recognizing the limitations of using propensity scores as a matching method, we also implement coarsened exact matching as a third method, which we believe produces the most empirically sound estimates of causal effect. Therefore, estimates of causal effect estimated from the coarsened exact matching process present a necessary robustness check against the use of propensity scores as a matching method. Iacus, King and Porro (2012, p. 2) demonstrate that coarsened exact matching improves upon propensity scores as a matching method by addressing treatment and control group imbalances while possessing several desirable statistical properties, such as its ability to reduce model dependence and estimation error.

We estimate the average treatment effect of the postcard notification on the treated with Stata command teffects psmatch using the probit estimation method and matching notified taxpayer observations against the nearest neighbor non-notified taxpayer observations with replacement. We also use the coarsened exact matching (cem) algorithm developed by Blackwell et al. (2010). We use the automated coarsening process because our data lacks obvious cutoff points that could be used for user-defined coarsening break points. 13 The coarsened exact matching process assigns each observation to a stratum of taxpayers with similar observable characteristics. The algorithm calculates coarsened exact matching weights which are used in regressions of credit take-up on treatment and covariates to estimate the treatment effect.

We use the propensity scores and coarsened exact matching algorithm to preprocess the taxpayer microdata and match notified taxpayers with similar observed characteristics to non-notified taxpayers with the goal of estimating the average treatment effect of the postcard mailings on taxpayer claims of the missed income tax credit. The dichotomous treatment variable,

We proceed by implementing the following regression using ordinary least squares, with nearest neighbor propensity scores, and coarsened exact matching. In the following regression specification,

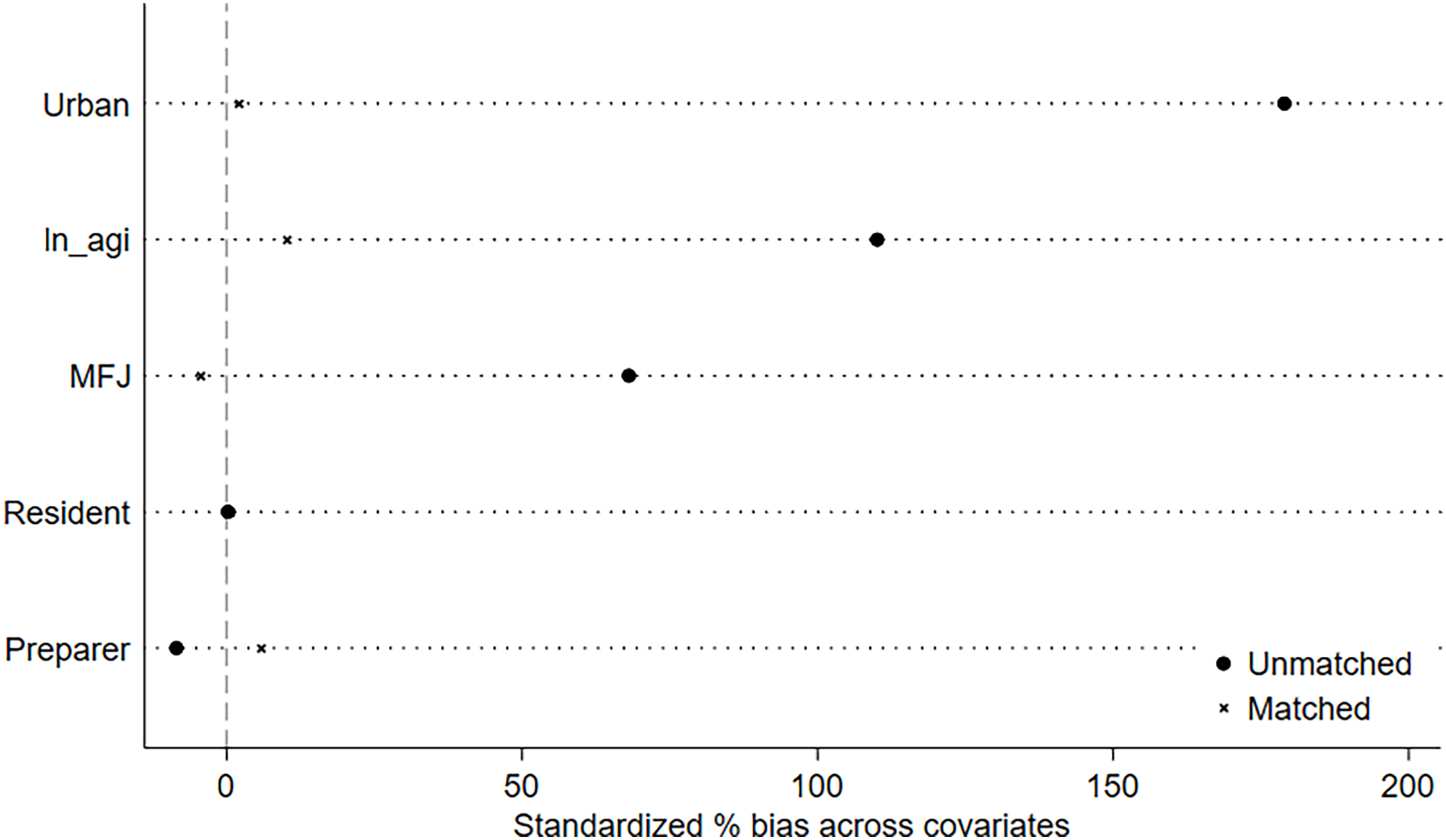

Figure 3 demonstrates the extent to which nearest neighbor matching reduces standardized bias between the groups of notified and non-notified taxpayers. While the two groups are much more balanced after nearest neighbor matching, two control variables, filing status and the use of paid preparers, continue to show statistically significant bias.

Reduction in bias between notified and non-notified taxpayers using nearest neighbor propensity score matching.

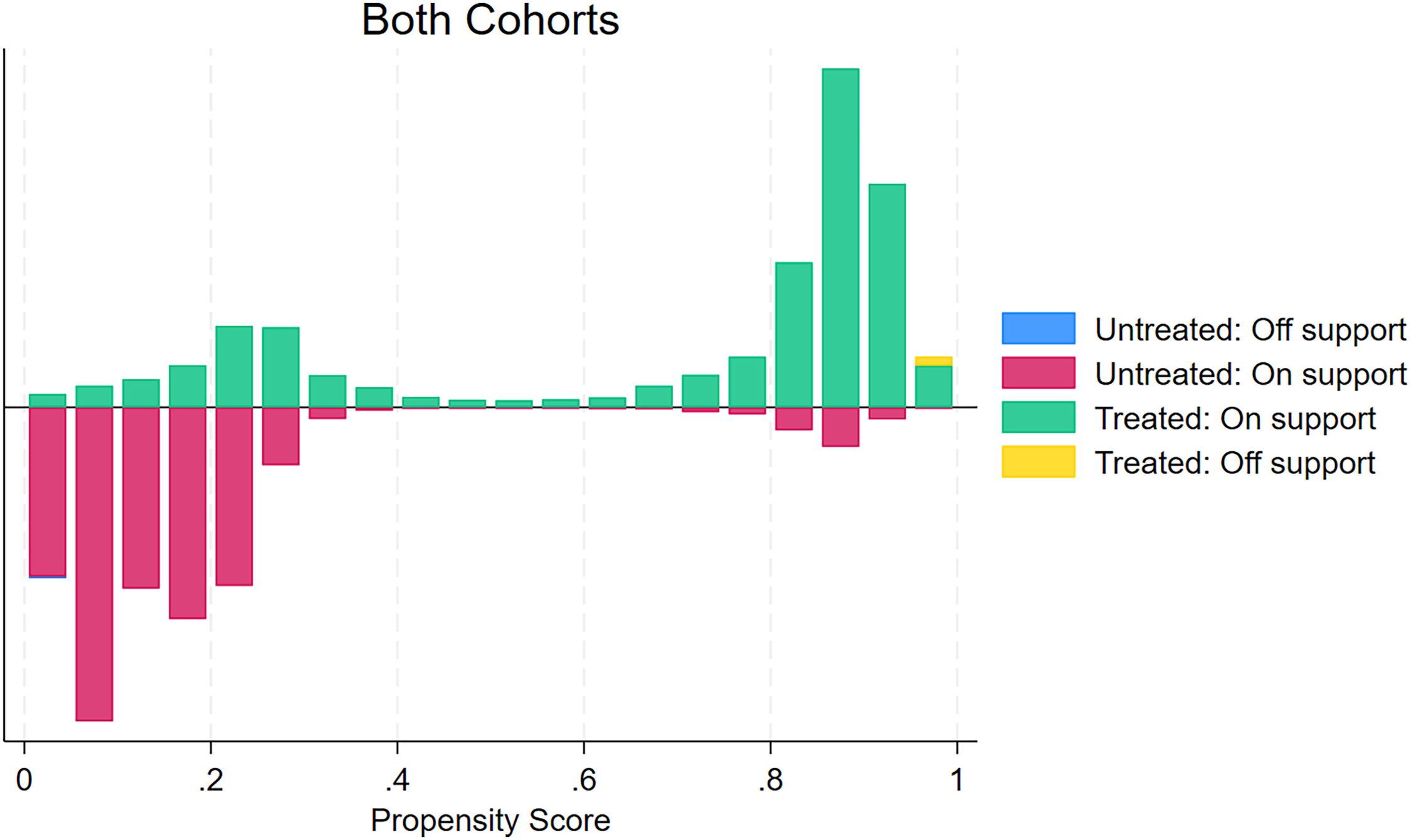

Figure 4 shows the extent of matching by propensity score among treated and untreated observations and whether the observations used satisfy the common support assumption. It is worth noting that the distribution of treated and untreated observations is largely driven by the fact that most members of the June cohort were not treated and most members of the August cohort are treated. We use the nearest neighbor propensity score matching method with replacement, which matches a treated taxpayer with a controlled taxpayer with the closest propensity score that is not ultimately chosen for notification. After matching, we use the propensity scores and CEM weights among matched observations to compare the estimated average treatment effect on the treated (ATT) between treated and controlled taxpayers.

Results of nearest neighbor matching by propensity score.

Results

Treatment Effects of All Sampled Taxpayers

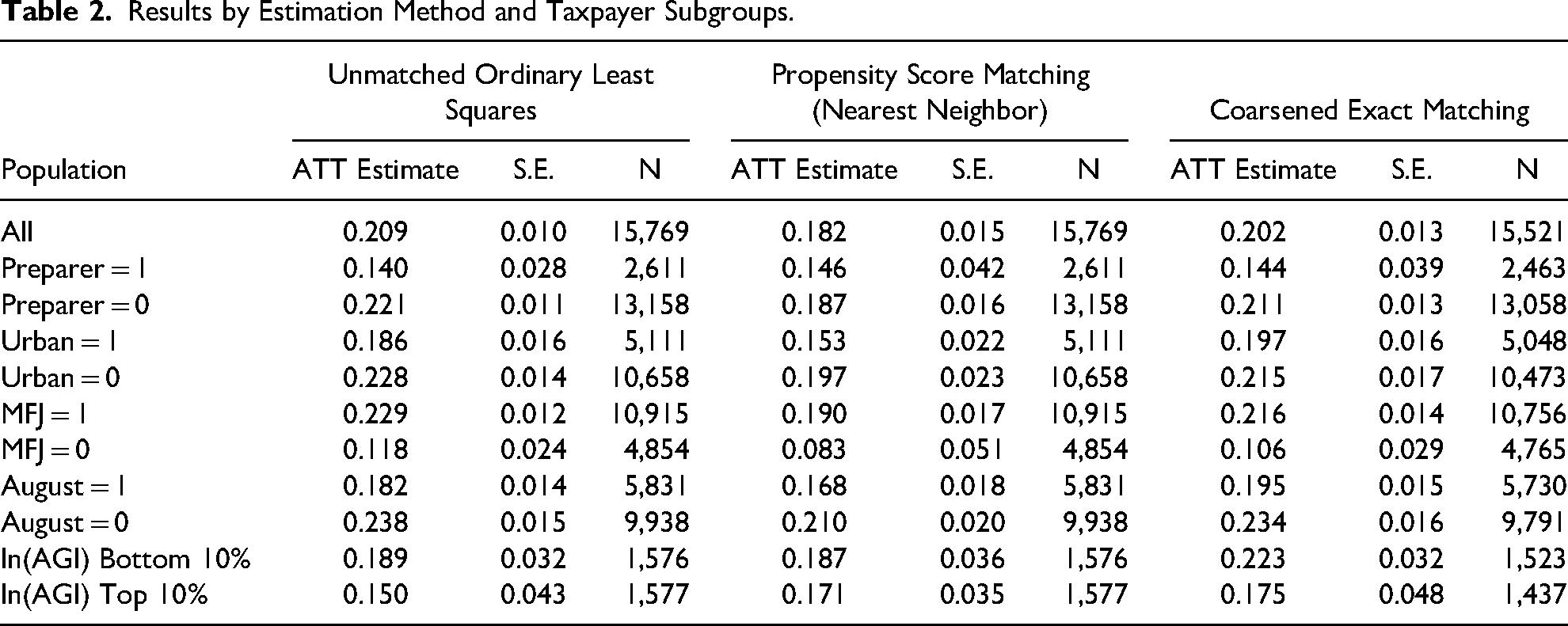

Table 2 compares the treatment effect on the treated results for OLS, nearest neighbor propensity score matching, and coarsened exact matching. The treatment estimate derived from OLS indicates that the income tax credit take-up rate was about 20.9 percentage points higher among notified taxpayers than the non-notified taxpayers. For comparison, nearest neighbor propensity score matching yields a treatment effect on the treated estimate of an 18-percentage point increase in credit take-up rate among the treated, while the coarsened exact matching method leads to treatment effect estimates of increased credit take-up rate by 20.2 percentage points as a result of notification. While readers should be concerned about the potential for bias in the OLS treatment estimate given nonrandom selection, the matching methods serve as important robustness checks and improve causal inference. The results also show that the treatment effect estimate is not especially sensitive to the choice of matching algorithm.

Results by Estimation Method and Taxpayer Subgroups.

Treatment Effects of Taxpayer Subgroups

We also use information from each taxpayer's income tax return to segment the population into groups. Table 2 shows the average treatment effect on the treated estimates for the entire population of selected taxpayers and for restricted samples of taxpayers. The results show that notified taxpayers whose income tax credit take-up rates increased the most include those who did not hire a professional preparer to complete their income tax return, taxpayers outside of the state's three urban counties, and married taxpayers who filed jointly. Among taxpayers that filed from rural counties, the take-up rate of contacted taxpayers was about 25 percentage points higher than those that were not contacted. Further, among taxpayers who self-prepared their income taxes, the take-up rate of the credit among notified taxpayers was 28 percentage points higher than those who were not contacted. A similar effect is found among married taxpayers who filed their income taxes jointly, whose take-up rate was also 28 percentage points higher than married taxpayers that were not contacted. The take-up rate was relatively lower among members of the August cohort, which may be explained by the fact that the estimated size of their unclaimed credits was lower than those who were selected for notification in the June cohort. Meanwhile, tax credit take-up rates among notified taxpayers are not meaningfully different between the bottom and top decile of federal adjusted gross incomes.

Limitations

The clearest limitation that we confront is the imbalances in observable characteristics between the notified and non-notified taxpayers. We attempt to mitigate the problems inherent in causal identification amid imbalanced treatment and control groups through various taxpayer matching methods.

The results presented in this paper may be subject to measurement error due to the following limitations. First, we cannot be certain that the postcard itself was the causal mechanism that influenced the behavior of taxpayers to file Form PTCX to claim the missing income tax credit. The postcard may not have been properly delivered, unread and discarded by a household member, etc. Second, the postcards were mailed the just before Governor Pete Ricketts launched a public awareness campaign about the tax credit, with the second shipment of postcards sent about five weeks before the press conference. It is possible that the taxpayer was motivated by the campaign, or by subsequent word-of-mouth about the credit, to file Form PTCX.

Discussion and Conclusion

Nebraska's refundable income tax credit against school district property tax levies was initially proposed as a method of state subsidization of local property taxes through the individual income tax, a proposal advocated by the state's rural land owners. However, implementation a new tax credit that requires a taxpayer-active method of claiming was met with challenges related to promotion and take-up of the credit, which eventually led to the mailing of postcards to increase awareness. Although the Department was subject to a budget constraint to support the taxpayer notification campaign, the evidence presented in this paper shows that the postcards were largely successful in motivating taxpayers to file Form PTCX and claim the missing income tax credit.

We believe there are several contributing factors that explain why the postcard notification program caused a sizable take-up effect among notified taxpayers. First, the June cohort of 1,000 notified taxpayers included mostly rural taxpayers that were plausibly had the most to gain by claiming the credit. The income tax credit proposal emerged among rural taxpayers exposed to large school district property tax liabilities who may have been more motivated to claim the credit once notified by the Department. Second, the development of Form PTCX by the Department likely helped contribute to the increased take-up rate. This simplified form enabled taxpayers to retroactively claim the credit without filing an amended income tax return, an effort by the Department to simplify the credit claiming process to the greatest extent administratively feasible. Third, the Department's ability to target certain taxpayers according to their estimated unclaimed credits may have helped facilitate take-up rates higher than that of a randomly-selected taxpayer.

Our research contrasts with previous work that investigates the effectiveness of taxpayer notification and the take-up rates of federal income tax credits that are major components of the federal social safety net. First, although the average claimant of the tax credit under investigation in this research is likely to be a regular income tax filer and earn more income than the average EITC claimant, both groups of taxpayers are prone to failing to claim the credit due to a lack of knowledge about the credit. However, the results presented in this research shows that contacted taxpayers – those who own property and previously filed a state income tax return – were much more responsive to notification than experimental evidence associated with EITC take-up. This contrast underscores the challenges that tax administrators and policymakers face in increasing access to means-tested income tax credits targeted to qualifying taxpayers.

In August 2024, Nebraska Governor Jim Pillen called the Nebraska Legislature into special session to consider new approaches to providing property tax relief against school district property taxes. This effort culminated in the enactment of the Property Tax Growth Limitation Act and the School District Property Tax Relief Act, which was signed into law by Governor Pillen on August 21, 2024. The legislation repealed the income tax credit against school district property taxes. Instead, the state will transfer $750 million to the newly-created School District Property Tax Relief Cash Fund for distribution to county treasurers that will apply the credits directly to property tax statements for property taxes levied by school districts beginning in Tax Year 2024. Annual state allocations for this property tax relief program are statutorily scheduled to increase to $902 million by Tax Year 2029 and increase 3% each year thereafter. The legislation also limits the annual growth rate in property tax levying authority to 5% per year for any political subdivision with property tax levying authority (Nebraska Legislature 2024).

The reformed property tax relief program resolves the problem of incomplete credit take-up. While the idea to pursue a taxpayer-active approach to extending property tax relief through the individual income tax originated among rural taxpayers who sought to force the state to subsidize their school district property taxes amid decreased state aid payments to rural school districts, the approach ultimately failed in part because the state's urban taxpayers were less aware of the credit and may have lacked the motivation of their rural counterparts to claim it, despite the simplified mechanism to retroactively claim the credit. Therefore, this episode in tax design and administration serves as an important lesson for policy makers who wish to explore methods of maximizing tax credit take-up.

Footnotes

Acknowledgements

Helpful comments were received from Denvil Duncan, Justin Ross, Luis Navarro, Luke Spreen, Tim Hodge, Deborah Carroll, Jacob Goldin, and from attendees of the 2024 Spring Public Finance Conference at the University of Nebraska at Omaha and the 2024 National Tax Association Conference.

Disclaimer

The views expressed in this paper do not necessarily represent the views of the Nebraska Department of Revenue or the State of Nebraska. Any errors or omissions in this work are our own.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.