Abstract

This study investigates a chain of effects to understand the causal path from customer informational inquiries (CIIs) and firm-initiated contacts (FICs) to customer profitability. Drawing on social exchange theory, our framework identifies a set of attitudinal (perceived relationship investment and relationship quality), behavioral (customer cross-buy and service usage), and financial (customer profitability) consequences of CIIs and FICs and also explores the extent to which customer-perceived financial risk and customer involvement shape attitudinal reactions to CIIs and FICs. Using longitudinal data for a sample of 1,990 customers measured in four different periods, the framework is tested in financial services by applying seemingly unrelated regression techniques. Our results reveal that FICs and CIIs are a particularly valuable tool for strengthening the relationship with customers with a low level of involvement but high perception of financial services risk. For highly involved customers, FICs and CIIs are not very effective; CIIs can even backfire if the customer also perceives the risk to be low. Our results highlight the importance of market segmentation for marketers to more effectively manage when and to whom they should target marketing activities (FICs) and steer CIIs.

Keywords

Introduction

Customer-firm interactions are the starting point of the relationship between these parties and contribute to determining the relationship’s future (Dwyer, Schurr, and Oh 1987). These interactions can be initiated either by firms or by customers. Firm-initiated contacts (FICs) are interactions or contacts that the company initiates in order to communicate with its customers and stimulate future customer behaviors (Wiesel, Pauwels, and Arts 2011). E-mail campaigns, catalog mailing, flyer and fax campaigns, economic reward programs, social programs, and advertising are common marketing activities initiated by companies (Bolton, Lemon, and Verhoef 2004; Wiesel, Pauwels, and Arts 2011).

Companies have traditionally taken the initiative to contact customers; however, nowadays, the growing importance of the customer in value-creation processes has changed the rules of the game. Customer-initiated contacts (CICs), understood as any communication with a company that is initiated by a customer (Bowman and Narayandas 2001, p. 281), are an important source of information about customers’ concerns, preferences, tastes, and questions (Lemon and Verhoef 2016; Ramani and Kumar 2008). According to Bowman and Narayandas (2001), CICs encompass “inquiries about a product’s use, availability, and reformulation; request for refunds; and complaints about performance” (p. 282); however, as Bowman and Narayandas note, complaints have been the most widely analyzed of all CICs. However, other types of CICs, such as those related to getting information on the firm’s products and services, are increasingly prevalent in the marketplace (Bolton 1998; Bowman and Narayandas 2001), as customers are willing to become more involved in the company’s activities (Beckers, Risselada, and Verhoef 2013) and have become central to the development of successful customer-firm relationships (Wiesel, Pauwels, and Arts 2011). Thus, in this research, we focus on customer informational inquiries (CIIs) about the company’s products and services—that is, any contact initiated by the customer with the purpose of gathering information on the products and services (prices, performance, expert opinion, etc.). CIIs offer customers the opportunity to contact the company at their own convenience to request precisely the content they need, without being spammed by company messages. Furthermore, new communication channels have increased the number of contact points between customers and companies as well as the quality of these interactions (Lemon and Verhoef 2016). In light of this new reality, companies need to better understand the potential consequences of FICs and CIIs for firms in order to manage them properly.

However, despite the importance of this topic, more research is needed to clarify the effectiveness of FICs and CIIs (Hennig-Thurau, Gwinner, and Gremler 2002; Hogan et al. 2002; Palmatier et al. 2006). Most research assumes that FICs, which are primarily understood as relationship marketing efforts, contribute to building stronger customer relationships that improve customer profitability (Palmatier et al. 2006). However, other authors express doubts regarding the effectiveness of FICs (Colgate and Danaher 2000) and caution that customers may feel annoyed by too-frequent contact or information that is not in line with their needs (Wiesel, Pauwels, and Arts 2011). Therefore, it is stressed that FICs are not considered effective in every situation (Day 2000). This discussion reflects the need for further research to determine when FICs may be especially effective and when they are not. Regarding CIIs, researchers primarily focus on directly studying their financial consequences for firms (Wiesel, Pauwels, and Arts 2011). Shankar and Malthouse (2007) highlight the need for further research on nonpush marketing contact to increase understanding of how and under what circumstances CIIs influence behavior and profitability. Again, the impact of CIIs on the customer-firm relationship may critically vary between different customers.

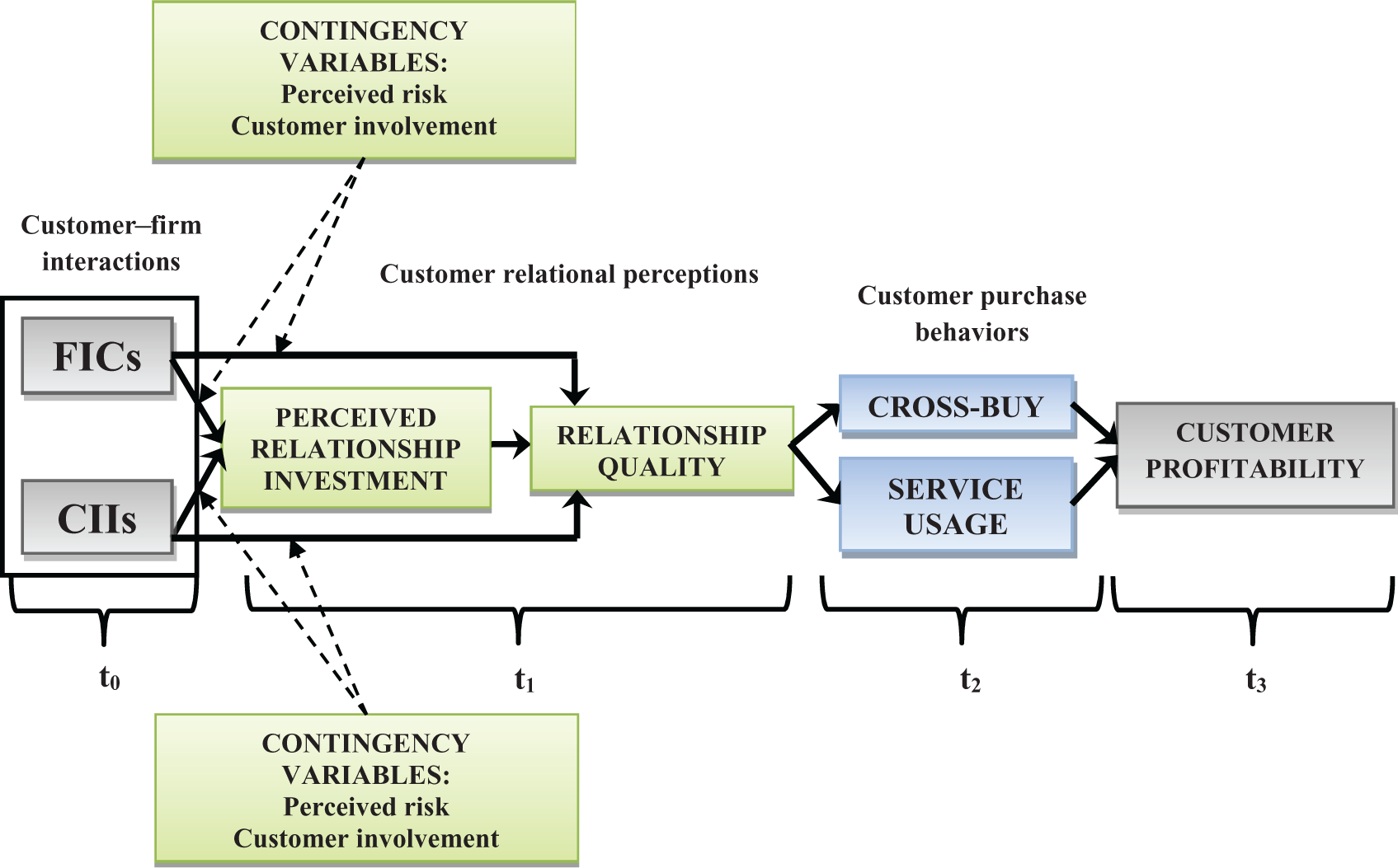

Taking into account these research gaps regarding FICs and CIIs, we propose an integrating conceptual framework that investigates the path through which customer-firm interactions translate into customer profitability. We follow Bolton, Lemon, and Verhoef (2004) who propose a causal sequence of the effects of marketing instruments (FICs): (1) FICs influence relationship perceptions, (2) which influence customer behaviors, and (3) which, in turn, affect financial outcomes. However, we go a step further and empirically analyze the chain of effects following FICs and CIIs. Furthermore, we include two contingency variables that can help in understanding how these customer-firm interactions (FICs and CIIs) contribute to building stronger relationships (perceived relationship investment [PRI] and relationship quality [RQ]), which, in turn, drive purchases (customer cross-buy—i.e., number of different categories owned by the customer—and service usage) and customer profitability. According to the literature, perceived risk and customer involvement determine the depth, complexity, and extensiveness of all cognitive, relational, and behavioral processes during the information search and decision-making processes (Dholakia 2001) and jointly motivate consumer responses (Dholakia 2001; Laaksonen 1994; Laurent and Kapferer 1985).

We therefore include perceived risk as a first contingency variable because different customers may have different risk perceptions associated with a purchase decision, which may become salient to the customer’s information processing and decision-making (Dholakia 2001; Dowling and Staelin 1994). The literature shows that customers’ varying levels of perceived risk lead their searches for information to differ from one another and that it is germane to individual information adoption and purchase decisions (Dowling and Staelin 1994; Shun-Yao and Ching-Nan 2015; Tang, Jang, and Morrison 2012). Risk perceptions result in anxiety and stimulate the development of risk reduction strategies, such as searching for information, which consequently encourage customer-firm interactions (Shun-Yao and Ching-Nan 2015). As a second contingency variable, we include customer involvement because it plays a key role in customers’ willingness to maintain relationships. Hence, there is an established theoretical and empirical consensus about its importance in moderating consumer information processing and decision-making (Alexander and Nicholls 2006; Kinard and Capella 2006; Rodríguez-Molina, Frías-Jalimena, and Castañeda-García 2015; Varki and Wong 2003). Thus, as we propose a sequential chain of effects, we are interested in capturing how differences in perceived risk or involvement may make customers react differently to customer-firm interactions, as well as how this translates into customer relational perceptions, behavior, and profitability.

The remainder of this article is organized as follows. In the next section, we show the whole sequence of the chain of effects that constitutes our conceptual framework, explain how social exchange theory can help us to understand the proposed chain, and develop the research hypotheses. The following section describes the data, variables, and method we use. Finally, we present the findings of this research, including the main conclusions and implications of our research for theory and practice. Further research lines are also detailed in the last section to encourage academics to investigate this topic in the future.

Conceptual Framework and Development of Hypotheses

We propose a causal path from customer-firm interactions to customer profitability, where we develop a chain of effects consisting of four steps to understand the dynamic process through which initial customer-firm interactions may generate value for firms. Furthermore, we investigate the roles of perceived risk and customer involvement in shaping customer reactions to customer-firm interactions. We ground our model in social exchange theory. This theory helps to explain the relational interdependence that develops over time through customer-firm interactions (Schiele, Calvi, and Gibbert 2012; Venkatesan, Kumar, and Ravishanker 2007). It is based on the reciprocity principle (Bagozzi 1995; Bowman and Narayandas 2001; De Wulf, Odekerken-Schröder, and Iacobucci 2001; Groth 2005) and identifies the conditions under which people feel obliged to reciprocate behaviors when they receive some benefit from others. Interactions require a bidirectional exchange—that is, something has to be given and something has to be returned. Investments made by one party in a relationship generate the desire to reciprocate (Bagozzi 1995). Therefore, customers who value the investment made by the company may reciprocate by having positive relational perceptions toward the firm or loyal behavior.

Our conceptual framework (Figure 1) takes as its reference Bolton, Lemon, and Verhoef’s (2004) theoretical research that establishes that FICs (direct mailings, relationship marketing instruments such as economic reward programs, and advertising) influence relationship perceptions, leading to customer behaviors that, in turn, drive financial outcomes such as revenues and customer lifetime value. We go a step further by distinguishing two types of customer-firm interactions—FICs and CIIs (Bowman and Narayandas 2001; Wiesel, Pauwels, and Arts 2011)—and investigate their effect on customer relational perceptions: PRI and RQ (De Wulf, Odekerken-Schröder, and Iacobucci 2001; Mimouni-Chaabane and Volle 2010; Anderson and Weitz 1992; Bolton and Drew 1991). PRI is conceptualized as the “consumer’s perception of the extent to which a retailer devotes resources, efforts, and attention aimed at maintaining or enhancing relationships with regular customers that do not have outside value and cannot be recovered if these relationships are terminated” (De Wulf, Odekerken-Schröder, and Iacobucci 2001, p. 35), and RQ is defined as “an overall assessment of the strength of a relationship” (p. 36).

Conceptual framework.

According to social exchange theory, each interaction generates a social exchange that builds a customer opinion. Bagozzi (1979) affirms that an exchange is influenced by contingency variables such as perceived risk and customer involvement. We therefore propose that FICs and CIIs will differently affect PRI and RQ depending on contingency variables; in particular, the amount of risk that customers perceive and their involvement with the service (Dholakia 2001; Dowling and Staelin 1994; Gordon, McKeage, and Fox 1998; Martin 1998). While related, perceived risk and involvement are different constructs, as they capture different aspects of consumer decision-making. Perceived risk is defined as “the nature and amount of risk perceived by a consumer in contemplating a particular purchase decision” (Cox and Rich 1964, p. 33). It refers to the uncertainty and adverse consequences that customers feel regarding the possible negative consequences of using a product or service (Featherman and Pavlou 2003) because, as overall customer behavior involves risk, any action of a customer will produce consequences that he or she cannot anticipate (Dowling and Staelin 1994). Involvement has been defined as “a person’s perceived relevance of an object based on inherent needs, values, and interests” (Zaichkowsky 1985, p. 342). This variable refers to an internal motivational state that shows arousal, interest, or drive induced by a particular stimulus or occasion (Bloch 1982).

We argue that these two constructs will influence the way in which customers perceive and respond to customer-firm exchanges. Consistent with the basic principles of social exchange theory (such as reciprocity), in situations of high risk and great uncertainty, we propose that customers may feel even more gratitude toward the company after each customer-firm interaction (Bowman and Narayandas 2001; Forsythe and Shi 2003; Shun-Yao and Ching-Nan 2015; Stone and Granhaug 1993). Interactions provide customers with valuable information, and they may therefore value the company’s investment in the relationship and in turn reciprocate with gratitude and higher perceptions of RQ (Bagozzi 1995). Involvement has an “established theoretical and empirical importance in moderating consumer information processing and decision making, both of which can be expected to temper consumer interest in relationships” (Varki and Wong 2003, p. 84). In addition, in situations of high involvement, interactions do not provide any relevant additional information for customers, and relational bonds of trust and familiarity between both parties have already been achieved. In this case, customers will not feel as much gratitude, and they will not feel obliged to reciprocate the company’s efforts (Groth 2005). As a consequence, customer-firm interactions for high-involvement customers will not contribute to increasing the perception of investment in the relationship or building a quality relationship.

Following the remaining steps in the proposed chain of effects, we expect the investment in the relationship to influence RQ (De Wulf, Odekerken-Schröder, and Iacobucci 2001). Relationship quality will, in turn, drive behaviors such as cross-buy (i.e., number of different categories owned by the customer) or service usage. We include cross-buy and service usage as indicators of customer purchase behaviors. The higher the RQ, the more likely it is that customers will purchase another service from the same provider and will continue doing business with the company (Palmatier et al. 2006). Cross-buying refers to a customer buying additional products and services from an existing service provider that he or she uses (Kumar, George, and Pancras 2008), and service usage refers to a customer’s purchases and use of the services offered by a firm (Lemon and Wangenheim 2009). In addition, more service usage or cross-buying will lead to higher profits. The literature reveals that cross-buying is an important driver of customer lifetime value and multichannel shopping behavior and leads to a higher share of wallet and higher customer value (Kumar, George, and Pancras 2008). Introducing customer profitability into the model enables us to connect the whole chain of effects with a performance measure and, thus, to offer a link between interactions, perceptions, behavior, and profitability. These linkages can be of high relevance to marketing managers who are eager to identify the return on their marketing investments (Kumar and Shah 2009). As there is broad consensus in the literature about these relations (Bolton and Lemon 1999; Bolton, Lemon, and Verhoef 2004; De Wulf, Odekerken-Schröder, and Iacobucci 2001; Kumar, George, and Pancras 2008; Palmatier et al. 2006), we will not theoretically propose specific hypotheses for them.

Effect of Customer-Firm Interactions on Customer Relational Perceptions

PRI

FICs may have a positive effect on PRI, which reflects the customer’s perception of the company’s effort and interest in maintaining the relationship (De Wulf, Odekerken-Schröder, and Iacobucci 2001). FICs are at the beginning of an information flow between the company and the customer and encourage feelings of trust, closeness, and special status (Anderson and Narus 1990). The customer may feel that he or she is important to the company and hold positive relational perceptions toward it (Bolton and Drew 1991). When customers receive regular information from the company, they may perceive that the company invests in the relationship (and is not just focused on an increase of short-term purchases) and makes efforts to keep them as customers. Only a social exchange encourages feelings of personal obligation, gratitude, and trust (Cropanzano and Mitchell 2005). Thus, according to social exchange theory, customers will feel gratitude toward the company’s investment in the relationship and will become more likely to reward the company in the future (Bagozzi 1995; Groth 2005). Hence, we suggest that:

Conversely, CIIs may negatively influence PRI. CIIs imply that customers contact the company because they are interested in obtaining specific information that is relevant to them, so it is the customer who takes the initiative with the contact. When customers initiate the contact, they may feel that the main effort in starting and building the relationship is made by them and will not perceive a balance between what they invest in the relationship and what the company invests in it. When there is no previous perception of investment in the relationship, customers initially will not feel gratitude or willingness to reward the company (Bagozzi 1995). Thus, we propose that:

Relationship Quality

Consistent with the literature, we conceptualize RQ through a set of related dimensions: trust, satisfaction, and commitment (De Wulf, Odekerken-Schröder, and Iacobucci 2001). Most research has assumed that FICs generate strong customer relationships (Crosby, Evans, and Cowles 1990; Morgan and Hunt 1994; Palmatier et al. 2006). When contacts between company and customer are frequent, both parties may get to know each other better, and the customer’s level of trust in the company may increase. As a consequence, the customer may feel a sense of satisfaction, friendship, or belonging (commitment) to the company (Reynolds and Beatty 1999). In addition, as social exchanges generate trust and a high level of familiarity between both parties (Bagozzi 1995), when customers receive relevant information from the company, they will reciprocate with higher evaluations of RQ (Venkatesan, Kumar, and Ravishanker 2007).

However, the literature also cautions that FICs may have a dark side and can be perceived as intrusive or annoying, particularly, if they occur too frequently or do not match the customer’s information needs (Wiesel, Pauwels, and Arts 2011). Despite this, given that the majority of the literature so far has found a positive effect of FICs on relationship perceptions (Crosby, Evans, and Cowles 1990; Morgan and Hunt 1994; Palmatier et al. 2006), we suggest that:

CIIs may also contribute to the level of RQ because more informed customers have higher levels of trust due to the more frequent interactions in the relationship. As the literature suggests that social exchanges are based on trust and make customers become familiar with an organization and/or its employees, solid customer-firm relationships can develop (Groth 2005; Venkatesan, Kumar, and Ravishanker 2007). CIIs therefore provide customers with more information on the company and are essential to improving the customer’s perception of the RQ (Reynolds and Beatty 1999). Furthermore, as the initiative for interaction is taken by the customer, CIIs avoid potential negative side effects such as feelings of intrusiveness or annoyance (Wiesel, Pauwels, and Arts 2011). We therefore posit that:

The Moderating Roles of Perceived Risk and Customer Involvement

Perceived risk

Following the basic principles of social exchange theory, it is proposed that customers who feel high risk will show even more gratitude toward the company after each FIC that provides them with valuable information, and they will reciprocate it through acknowledgment of the relationship investment (Dowling and Staelin 1994; Stone and Granhaug 1993). Customers who perceive a product or service as very risky will perceive any additional information provided by the company (FIC) as useful and will be more prone to carefully analyze it (Shun-Yao and Ching-Nan 2015) in order to reduce their fears (Featherman and Pavlou 2003). Therefore, customers who perceive the risk as high will be more likely to see FICs as an investment from the company’s side and less likely to perceive them as annoying or intrusive.

The same may happen with RQ; customers who perceive high risk will experience more gratitude toward the company after each FIC and will compensate it with a superior consolidated relationship based on high levels of trust, satisfaction, or commitment (Cho and Lee 2006). FICs should have a stronger effect on relationship perceptions for customers who perceive a service as risky compared to customers who do not. Customers who perceive a service as risky will positively value the company’s transparency in giving reliable information to customers (Shun-Yao and Ching-Nan 2015). After receiving that information, customers seem more likely to satisfy their particular information needs, making the relationship become closer and more trusting, so that it can be reinforced (Shun-Yao and Ching-Nan 2015; Stone and Gronhaug 1993). These customers will also be less likely to become irritated or annoyed by company-initiated communication messages (Wiesel, Pauwels, and Arts 2011). Thus, we propose that:

A high level of perceived risk may mitigate the negative relationship that we proposed between CIIs and PRI. The literature shows that there is more search activity in high-risk categories (Beatty and Smith 1987; Dowling and Staelin 1994; Shun-Yao and Ching-Nan 2015). When the level of perceived risk is high, customers tend to engage in extensive information search, perceive information as useful, and rely heavily on their sources for risk reduction (Cho and Lee 2006). Thus, customers will not pay so much attention to which party initiates the contact or invests more in the relationship; they will mainly focus on getting the necessary information to reduce their level of perceived risk (Shun-Yao and Ching-Nan 2015). Customers will then be less demanding regarding the relationship and will not experience disappointment regarding a company’s investment in the relationship when they have to contact the company first because, through these contacts, they safeguard their own personal security.

In addition, with high perceived risk, the positive relationship between CIIs and RQ can become stronger (Flanagin et al. 2014). CIIs lead to customers being better informed and trigger a more familiar and closer relationship. When customers perceive high risk, these CIIs will especially help to reduce the uncertainty, make them perceive the search for information as useful, and increase their levels of trust in the relationship (Shun-Yao and Ching-Nan 2015). In addition, as the perception of risk is a serious concern for many customers (Forsythe and Shi 2003; Shun-Yao and Ching-Nan 2015; Stone and Gronhaug 1993), they will not pay as much attention to which party initiates the contact and will be reciprocal. Hence, we posit that:

Involvement

When involvement is high, customers focus attention on product-related information, establish emotional ties, have higher levels of awareness, and exert greater cognitive effort to comprehend advertising (Dholakia 2001; Gordon, McKeage, and Fox 1998; Martin 1998). Involvement motivates higher levels of attention; consequently, involved customers will be highly informed (Mende and van Doorn 2015). As involved customers know the company well and have sufficient information about all the products and services it offers, FICs do not provide these people with any relevant additional information (Rodríguez-Molina, Frías-Jalimena, and Castañeda-García 2015). The positive relationship between FICs and PRI can become weaker for high-involvement customers because an FIC will have less value for them and they will perceive FICs to a lesser extent as a company investment in the relationship, compared to customers with low involvement. For low-involvement customers, on the other hand, any contact from the company will make them feel that the company is investing in the relationship.

Along the same line of reasoning, the positive link between FICs and RQ may also be mitigated by higher levels of involvement. When the level of involvement is high, customers know exactly what kind of information they are looking for (Rodríguez-Molina, Frías-Jalimena, and Castañeda-García 2015). Thus, for highly involved and informed customers, each informative FIC will not be as effective as for low-involvement customers and will contribute less to gaining customer trust or reinforcing the relationship than for low-involvement customers. Furthermore, when involvement is high, FICs not only will not provide relevant additional information for customers but also will not generate stronger relational bonds in terms of trust or familiarity (Groth 2005). Thus, we suggest that:

Regarding the negative relationship between CIIs and PRI, the fact that involved customers have to initiate the contact (CIIs) can deteriorate their perception of investment in the relationship from the company (Rodríguez-Molina, Frías-Jalimena, and Castañeda-García 2015). Involved customers scrutinize the relationship to a greater extent because it is more important to them (Punj and Moore 2009). Therewith, they also pay more attention to which party contributes what to the relationship, and they notice it more when there is an imbalance (Celsi and Olson 1988).

Furthermore, for customers with high involvement, the positive effects of CIIs on RQ are expected to be weaker because these customers are already fairly well informed (Rodríguez-Molina, Frías-Jalimena, and Castañeda-García 2015). With high involvement, each CII can have a lower positive influence on RQ, also weakening the positive relationship between CIIs and RQ. For high-involvement customers, the increase in RQ will be lower after additional customer contacts; they will, to a lesser extent, increase the level of trust and familiarity and will contribute less to reinforcing the relationship (Groth 2005). Hence, we propose that:

Empirical Study

Data

We used customer data from a major bank in a European country. This database contained monthly customer information between March 2011 and March 2013. For these customers, we had access to different sets of information: (1) interactions-related data, which offered information about the number of CIIs and FICs; (2) transactional data, which included information about service usage, cross-buy, and customer profitability; and (3) customer-level information (including demographics). Most of the FICs that the financial entity develops are aimed at stimulating purchases that have a clear commercial goal. Hence, in this study, we focus on the effect of commercial FICs on relational customer perceptions, behaviors, and profitability. CIIs refer to informational inquiries, excluding other types of CICs such as request for refunds or customer complaints.

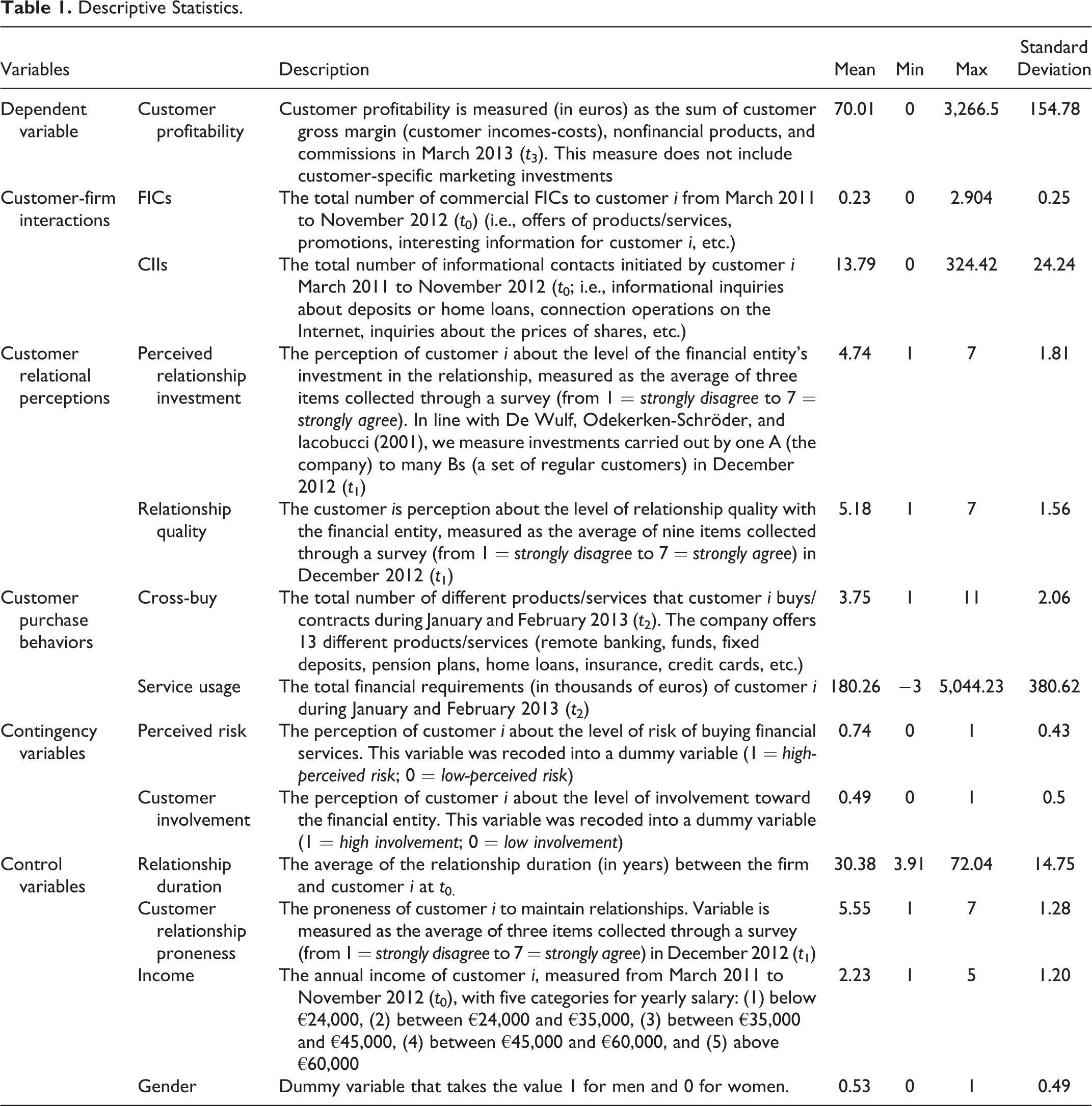

In December 2012, we carried out a survey including scales consolidated in the literature to obtain information about customers’ perceptions of their relationship with the company. To measure PRI and the multidimensional construct of RQ, we used the scales proposed by De Wulf, Odekerken-Schröder, and Iacobucci (2001; scales are shown in Appendix Table A1). Respondents were asked to rate the statements about the company from 1 (strongly disagree) to 7 (strongly agree). We measured customer perceived risk and customer involvement (measured vis-à-vis a specific company—the bank), building on the work of Meuter et al. (2005) and Dholakia (2001). In line with previous research, to facilitate interpretation of the moderating effects, perceived risk and customer involvement were recoded into dummy variables (1 = high perceived risk and high involvement; 0 = low perceived risk and low involvement; Mende and van Doorn 2015). Customers who gave high ratings on these variables (values >4) were considered as having high levels of perceived risk or involvement, and lower values (values ≤4) indicated that customers had lower levels of risk or involvement. 1

The market research company that usually works with the financial entity was responsible for carrying out this survey. The market research company phoned a total of 5,848 customers. We obtained a final effective sample of 2,000 questionnaires, which constitutes a response rate of 34.19%. To carry out this study, we merged the objective data provided by the financial entity and the subjective data from the questionnaire. After removing customers with incomplete information or missing values in some of our key variables, we had a final sample of 1,990 customers. Descriptions of the variables we measured in this research, and their descriptive statistics, are displayed in Table 1 (Appendix Table A1 shows the Cronbach’s αs of the constructs, which all exceed the critical threshold of .7; Nunnally and Bernstein 1994). We also performed an exploratory factor analysis, where all the items loaded on their respective scales (see Appendix Table A2 for the correlation matrix for these variables). Although the correlation value between perceived risk and customer involvement seems high, the results of the exploratory factor analysis carried out via SPSS 22, including all of the scales, led to a two-factor solution in which all items loaded on the scales as they should have. Additional analyses suggest that there are a significant number of individuals (more than 25% of the consumers in our sample) for which there is a negative correlation between involvement and perceived risk (perceiving either high involvement-low risk or low involvement-high risk), suggesting that, while related, the two constructs capture different aspects of decision-making.

Descriptive Statistics.

Method

We developed a five-equation seemingly unrelated regression (SUR) model to empirically test the proposed conceptual framework and its associated hypotheses. The SUR model is a system of linear equations with errors that are correlated across equations for a given individual (Zellner 1962). The model consists of j = 1,…, m linear regression equations for i = 1,…, N individuals.

There are a number of benefits to using the SUR modeling approach. The first is to gain efficiency in the estimation by combining information from different equations. A system of multiple equations produces more efficient estimations when the error terms of the regressions considered are allowed to correlate. When a joint relationship between the disturbances across a system of j equations is not taken into account, the results are inconsistent and biased (Ogundari 2014). Secondly, “since some variables are dependent and independent variables in different regressions, this technique allows us to alleviate endogeneity problems” (Autry and Golicic 2010, p. 95).

To ensure causality in the proposed chain of effects, we consider information on the different components of our model at different points in time: we used interactions-related data (FICs and CIIs) and customer-level information (including demographics) from the period March 2011 to November 2012 (t 0); customer relational data come from the questionnaire in December 2012 (t 1); customer purchase data, which included information about service usage and cross-buy behavior, were measured in January 2013 (t 2); and customer profitability was measured in February and March 2013 (t 3). We also controlled for the effect of additional relevant variables in the explanation of the relational, behavioral, and financial variables by including relationship duration, intended to capture the accumulated experience of the customer in the relationship with the firm, customer relationship proneness (De Wulf, Odekerken-Schröder, and Iacobucci 2001), which was measured at a general level, as a personality trait to understand the customers’ willingness to maintain relationships with companies, and a set of demographic variables such as income and gender.

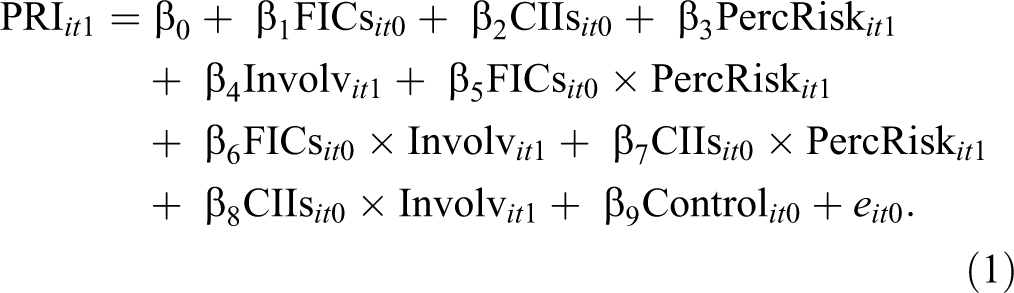

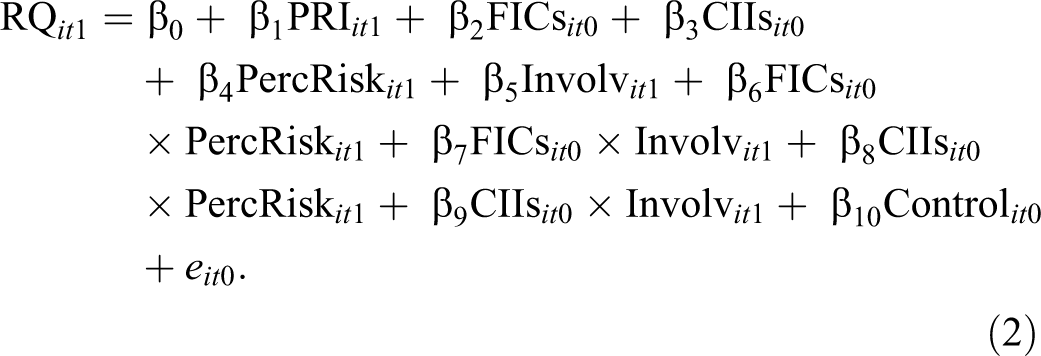

The model consists of j = 5 linear regressions, where the first linear regression has PRI as its dependent variable, the second explains RQ, the third explains customer cross-buy behaviors, the fourth explains customer usage, and the fifth includes explanatory variables to measure their impact on customer profitability. The linear regressions for the SUR model are represented as follows:

where CIIs it 0 represents the number of contacts initiated by customer i in period t 0; FICs it 0 represents the total number of contacts that customer i receives in period t0; RQ it 1 and PRI it 1 are the relational variables (RQ and PRI, respectively), and PercRisk it 1 and Involv it 1 are the moderating variables (perceived risk and customer involvement, respectively) measured through the questionnaire that reflect the level of perceived risk and customer involvement of customer i in t 1 (December 2012); CB it 2 represents the cross-buy behavior of customer i in period t 2, and Us it 2 represents the level of service usage of customer i in period t 2; CP it 3 represents customer profitability of customer i in period t 3; and Control it 0 represents a vector of control variables: relationship duration of customer i in period t 0, relationship proneness of customer i in period t 1, the income of customer i in t 0, and the gender of customer i in t 0. Finally, ∊ it is the error term for customer i in month t. To estimate our model, we used Stata 10. 2

Findings

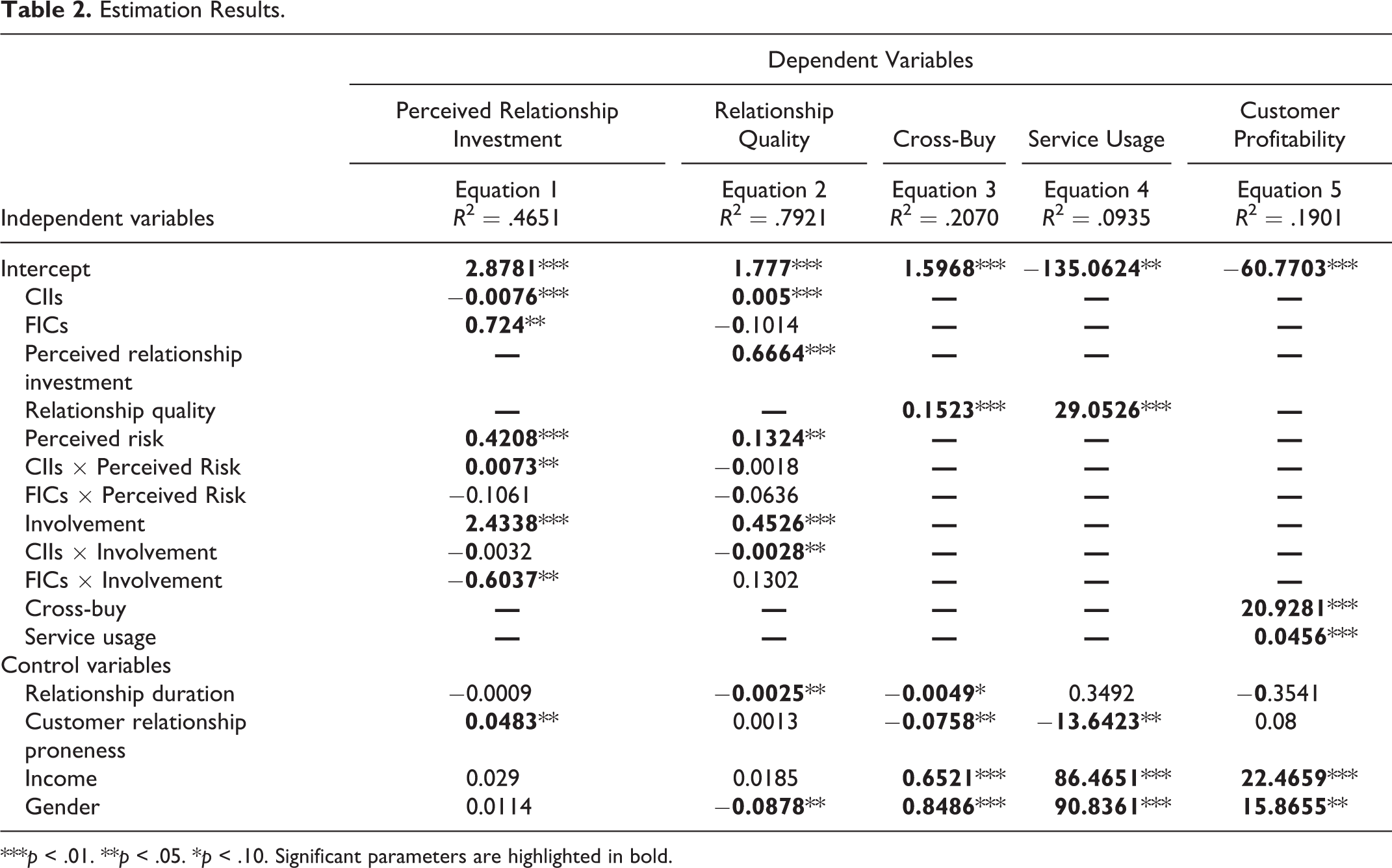

Overall, we find strong support for our proposed chain of effects, as most of the parameters are significant and point in the expected direction (Table 2).

Estimation Results.

***p < .01. **p < .05. *p < .10. Significant parameters are highlighted in bold.

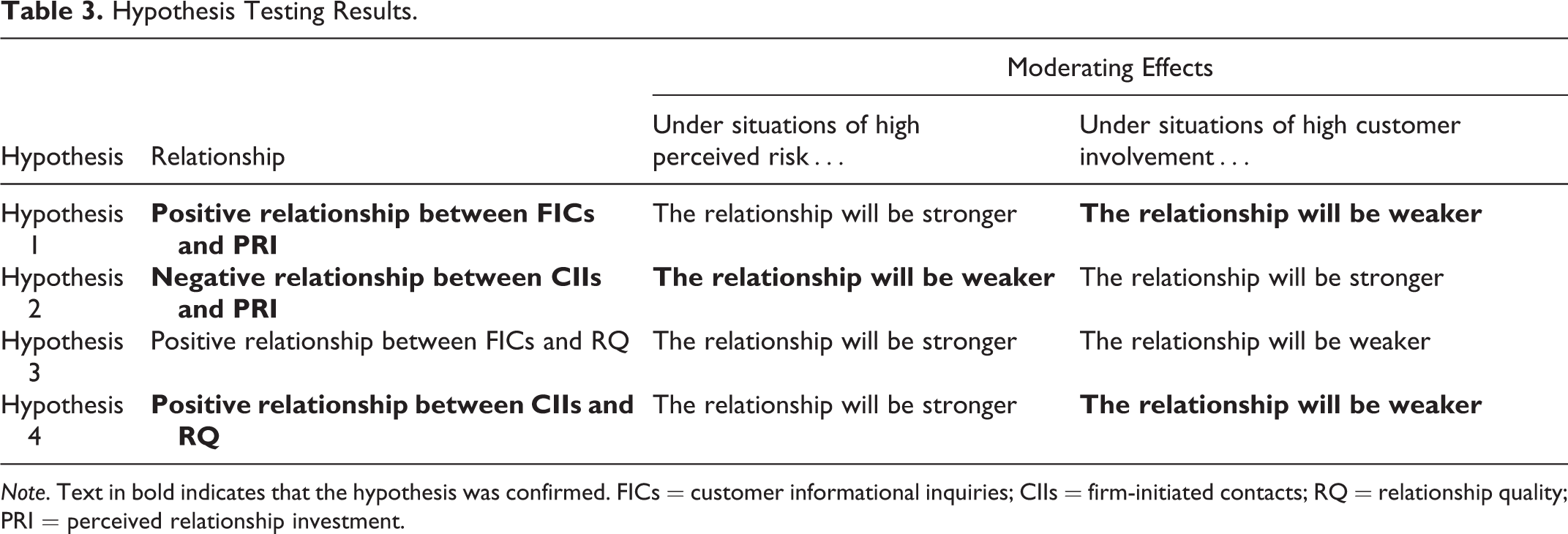

The results confirm that CIIs have a negative effect on PRI (β = −.0076, p < .01), and FICs have a positive one (β = .724, p < .05). These results are in line with Hypotheses 1 and 2. CIIs have a positive influence on RQ (β = .005, p < .01), confirming Hypothesis 3. FICs, however, do not have a significant influence on RQ (β = −.1014, p > .10), so we cannot confirm Hypothesis 4.

Regarding the moderating effect of perceived risk, the results confirm that the relationship between CIIs and PRI is positively moderated by perceived risk (β = .0073, p < .05), supporting Hypothesis 2a. However, we cannot confirm Hypotheses 1a, 3a, and 4a. In addition, customer involvement negatively moderates the relationships between FICs and PRI (β = −.6037, p < .05) and between CIIs and RQ (β = −.0028, p < .05). These results enable us to confirm Hypotheses 1b and 4b, although we did not find support for Hypotheses 2b and 3b. The positive coefficients associated with perceived risk (β = .4208, p < .01 for relationship investment, β = .1324; p < .01 for RQ) and involvement (β = 2.4338, p < .01 for relationship investment; β = .4526, p < .01 for RQ) reveal that customers who perceive risk to be high and/or are highly involved perceive relationship investment and quality as higher.

In line with previous literature, our results also reveal that when customers feel that the company invests in the relationship, the level of RQ increases. Relationship quality positively influences customer cross-buy and service usage—that is, customer purchase behaviors. Finally, cross-buy and service usage behaviors positively contribute to increasing customer profitability. Table 3 offers a summary of the hypothesis testing results.

Hypothesis Testing Results.

Note. Text in bold indicates that the hypothesis was confirmed. FICs = customer informational inquiries; CIIs = firm-initiated contacts; RQ = relationship quality; PRI = perceived relationship investment.

Mediating Effects

To better understand the relationships in this chain of effects, we also tested whether the central variables of the conceptual framework—PRI, RQ, customer cross-buy (CB), and service usage (US)—act as mediators in the model.

We followed the bootstrapping method with 5,000 subsamples, as proposed by Preacher and Hayes (2008), and used their SPSS routine to calculate the total, direct, and indirect effects, as well as the 95% confidence interval (CI) for the mediating variables. When an interval for a mediating effect does not contain 0, the indirect effect is significantly different from 0 with a 95% confidence level. Taking into account the CIs obtained, when the value 0 is not contained in paths, we can confirm that the indirect effect is statistically significant.

The results confirm that PRI acts as a complete mediator in the relationship between FICs and RQ (with a CI [.0425, .4953], significant at 95%) and in the relationship between CIIs and RQ (with a CI [−.0051, −.0002], significant at 95%). While FICs do not significantly influence RQ directly, they indirectly influence it via relationship investment. Therefore, the contingency effects also occur on the level of relationship investment, and not quality, which may explain the disappointing results we obtained. This finding reinforces the importance of the idea of designing a causal chain of effects.

In addition, although CIIs already influence RQ directly, there is an indirect effect of CIIs on RQ through PRI. This points to another interesting conceptual difference between FICs and CIIs (Wiesel, Pauwels, and Arts 2011), with the former being particularly relevant for relationship investment and the latter for both relationship investment and quality.

Furthermore, the results show that RQ plays a partial mediating role in the relationship proposed in the chain of effects between FICs and customer cross-buy (with a CI [.0041, .0612], although this is only just significant at 90%). The relationship between FICs and service usage is significant at 95% (with a CI [.2119, 9.6311]). This result reflects that FICs have an indirect effect on customer purchase behaviors through RQ (complete mediation). However, RQ does not play a mediating role in CIIs’ relationships with customer cross-buy and service usage (with CIs [−.0005, .0003] and [−.0579, .0336], respectively). CIIs do not have an indirect influence on purchase behaviors through RQ. Therefore, it is important that CIIs positively impact RQ because this perception of RQ will lead the customer to cross-buy or increase service usage. Relationship quality also acts as a complete mediator in the relationships between PRI and cross-buy (with a CI [.1185, .2953], significant at 95%) and as a partial mediator between PRI and service usage (with a CI [3.1269, 33.1169], which is just significant at 90%). Thus, RQ is a key step in the proposed chain of effects because it enables the PRI to indirectly lead to positive customer behaviors, which contribute to profitability.

We also checked for log transformation of FICs, CIIs, service usage, and customer profitability, as well as for potential nonlinearity of customer-firm interactions in our model. 3 However, the results of the Bayesian information criterion and the Akaike information criterion to compare among models revealed that the model with contingency variables was the one that best fit the data.

Discussion and Implications for Theory and Management

In this research, we provide a comprehensive conceptual framework in the form of a chain of effects to understand the causal path from customer-firm interactions (CIIs and FICs) to customer profitability, considering perceived risk and customer involvement as contingency variables that shape customers’ reactions to CIIs and FICs.

Theoretical Implications: Effectiveness of the Chain of Effects

The design of the proposed chain of effects has been especially useful for understanding the process through which interactions generate value for firms and has enabled us to contribute interesting findings to the literature. The starting point of the chain of effects is customer-firm interactions, initiated either by the firm (FICs) or by the customer (CIIs), and we investigate their impact on customer profitability through a dynamic, causal process of different constructs. Moreover, we add to the extant literature by investigating the role of customer perceived risk and involvement in this chain of effects (Bolton, Lemon, and Verhoef 2004; Bowman and Narayandas 2001; De Wulf, Odekerken-Schröder, and Iacobucci 2001; Ramani and Kumar 2008; Wiesel, Pauwels, and Arts 2011).

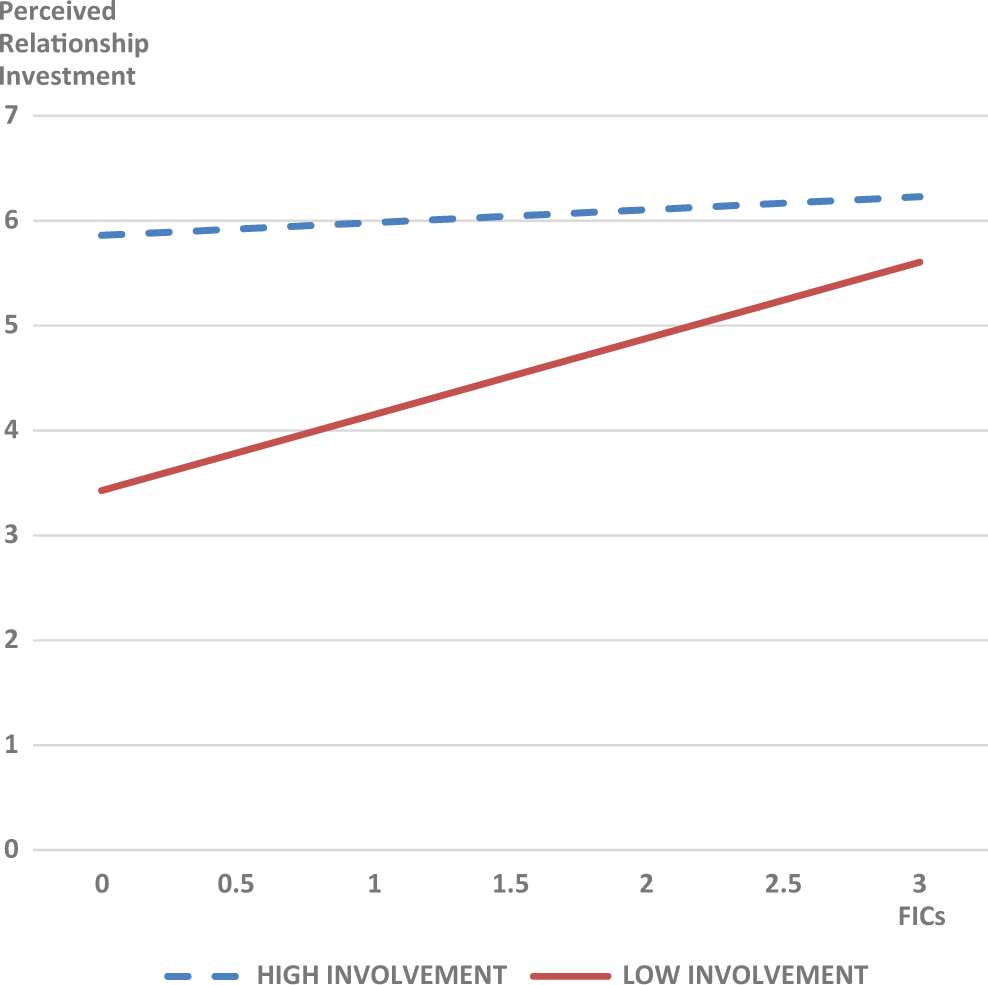

When companies contact customers (FIC), the latter perceive the former to be investing in the relationship and making significant efforts toward building solid relationships with them, which is in line with our theoretical reasoning based on social exchange theory (Groth 2005). However, this effect is weaker for customers with higher levels of involvement. For involved customers, the general effect of FICs on PRI is positive; however, as FICs increase, the improvement in the PRI reduces up to a certain point, where it is almost insignificant. In line with our hypotheses, involved customers have sufficient information about all the products and services of the company, and each FIC has less value for them (Rodríguez-Molina, Frías-Jalimena, and Castañeda-García 2015). Figure 2 4 shows these results graphically.

Moderating effect of involvement in the relationship between firm-initiated contacts and perceived relationship investment.

Contrary to our expectations, we do not find a positive effect of FICs on RQ. The reason for this may be that while FICs increase the number of interactions between the customer and the company, thereby potentially increasing the level of trust and commitment (Crosby, Evans, and Cowles 1990; Morgan and Hunt 1994; Palmatier et al. 2006), they may also have a dark side, namely, when the FICs are perceived as intrusive, the customer feels annoyed by too-frequent contact or information that is not in line with his or her information needs (Wiesel, Pauwels, and Arts 2011). These two opposing effects may cancel each other out, leading to an overall null effect. Furthermore, other consumer traits that we did not observe in this study may shape customers’ reactions to FICs. Based on attachment style theory (Mende and Bolton 2011; Mende, Bolton, and Bitner 2013), one could, for instance, argue that customer attachment avoidance may lead to FICs being valued less, or even being detrimental to customer satisfaction, while customer attachment anxiety could lead to a strong appreciation of FICs.

However, the results of the mediating effects reveal that FICs have an indirect effect on RQ through PRI. These results stress the importance of PRI for customer relations. According to social exchange theory, when customers perceive a high degree of investment in the relationship by the company, they are grateful and willing to reward/reciprocate the company’s efforts (Bagozzi 1995; Groth 2005). Therefore, the perception of relationship investment is just a first step to future customer purchases due to customer reciprocity.

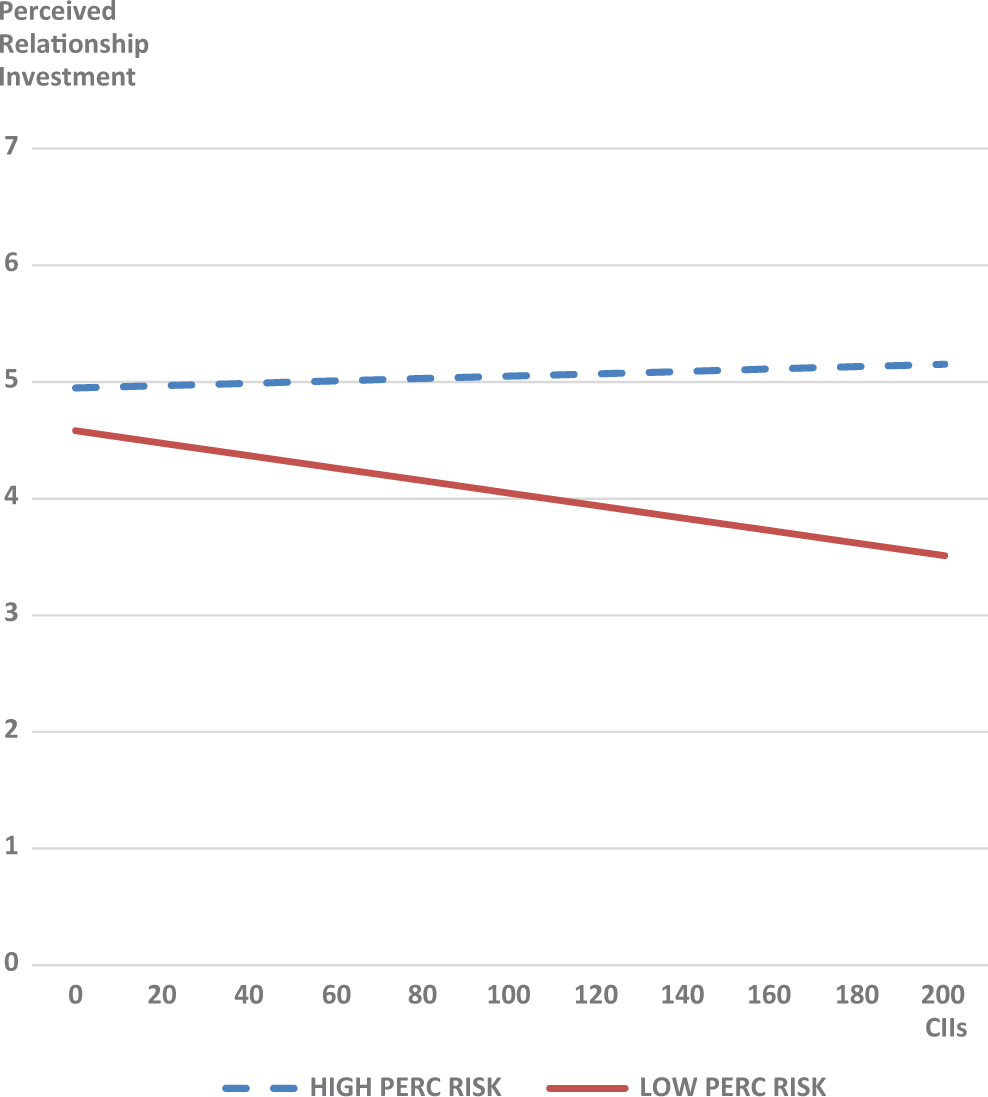

CIIs, on the other hand, negatively influence PRI. This result may be the consequence of customers perceiving that they are investing in building the relationship more than the company is by taking the initiative to make the first contact. Bearing these results in mind, the perception of relationship investment will depend not only on what the company invests in the relationship but also on what the customer invests through his or her CIIs. At this point, it is important to highlight that although social exchange theory establishes that investments made by one party in a relationship are reciprocated by the other party, when customers initiate the contact, they do not perceive any investment in the relationship by the company and, consequently, do not feel the desire to reciprocate. The only exception is when customers perceive high risk (Shun-Yao and Ching-Nan 2015). These customers probably pay less attention to which party initiates the contact because they are more focused on gathering sufficient information to lower their perceived risk (Cho and Lee 2006; Flanagin et al. 2014). Therefore, they may be less demanding regarding the relationship compared to customers who do not perceive the risk to be high; these latter customers react more negatively if they have to take the initiative too frequently. Figure 3 shows these results graphically.

Moderating effect of perceived risk in the relationship between CIIs and perceived relationship investment.

The number of CIIs also positively affects RQ. CIIs enable the customer to contact the company precisely how and when he or she wants, and this fact positively contributes to RQ (Lemon and Verhoef 2016). Every contact that the customer initiates reinforces the relationship and increases its quality by .00146, as customers experience feelings of trust, satisfaction, and commitment toward the company.

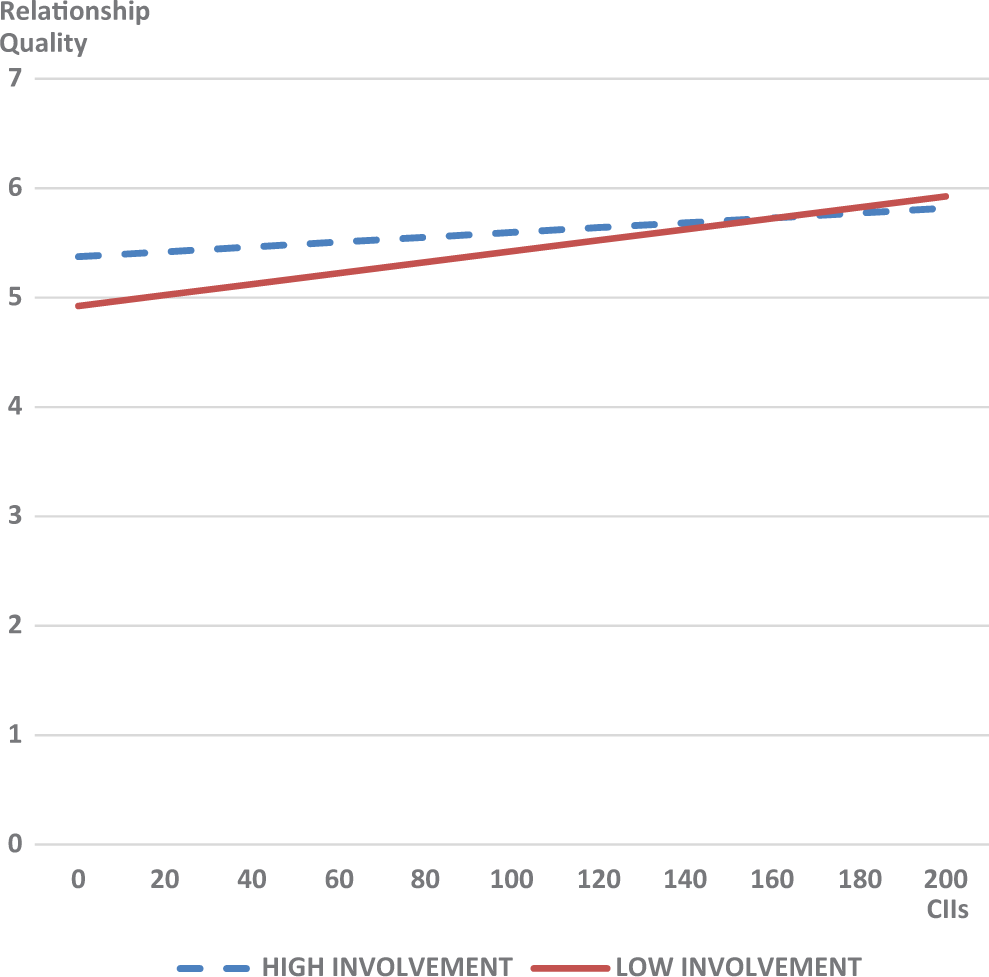

However, for involved customers, the effect of CIIs on RQ is less pronounced. For high-involvement customers, the increase in relational variables such as trust, satisfaction, and commitment is lower after additional customer contact because the customers already have positive feelings toward the relationship and, consequently, this contact contributes less to reinforcing the relationship. Confirmation of these results deserves attention because prior research, by contrast, has proposed that high involvement engenders an ongoing commitment on the part of the consumer that reinforces the RQ (Gordon, McKeage, and Fox 1998). Figure 4 shows the obtained results graphically.

Moderating effect of involvement in the relationship between customer informational inquiries and relationship quality.

Compared to existing research to date, through this chain of effects we have obtained a more complete view of the consequences of FICs and CIIs (Bolton, Lemon, and Verhoef 2004; Bowman and Narayandas 2001; De Wulf, Odekerken-Schröder, and Iacobucci 2001; Ramani and Kumar 2008; Wiesel, Pauwels, and Arts 2011) by simultaneously investigating a broader set of relational, behavioral, and financial variables after customer-firm interactions take place, as well as two new contingency variables. Compared to Bolton, Lemon, and Verhoef’s (2004) research, we have empirically validated their conceptual framework and considered CIIs and FICs (rather than the latter alone) as the starting point of our chain of effects. We also go a step further than De Wulf, Odekerken-Schröder, and Iacobucci’s (2001) research by including CIIs in the financial impact of customer behaviors and the moderating roles of perceived risk and involvement in the conceptual framework. Ramani and Kumar’s (2008) investigation measured the relational and behavioral consequences of an interaction orientation, but only from the firm perspective and without considering any contingency variables. Thus, we contribute by measuring a causal sequence of consequences from the customer’s perspective. We also extend the contribution of Wiesel, Pauwels, and Arts’s (2011) research by not only analyzing the influence of FICs and CIIs on profits but also providing an extensive explanation of the overall path that these interactions follow before being profitable for firms and the roles of two contingency variables.

The proposed chain of effects has also confirmed that relational investments made by the company increase RQ because customers positively value the company taking care of them and paying attention to their specific needs in a personalized way. This result is also consistent with the literature (De Wulf, Odekerken-Schröder, and Iacobucci 2001; Mimouni-Chaabane and Volle 2010). Relationship quality, subsequently, is confirmed to be the main driver of customer purchase behaviors. In situations where the customer feels that the relationship is of a high quality (based on trust, satisfaction, and commitment), he or she will not have doubts about continuing to do business with the company or carrying out purchase behaviors such as cross-buying or service usage (Palmatier et al. 2006). With respect to the last step of the proposed chain of effects, our findings confirm that customer cross-buy behaviors and customer service usage are two key variables that positively influence customer profitability (Kumar, George, and Pancras 2008; Bolton and Lemon 1999).

Managerial Implications

Through our analysis of this chain of effects, we are able to propose specific guidelines for managers in order to improve customer-firm relationships and increase the value that each customer can provide to the firm.

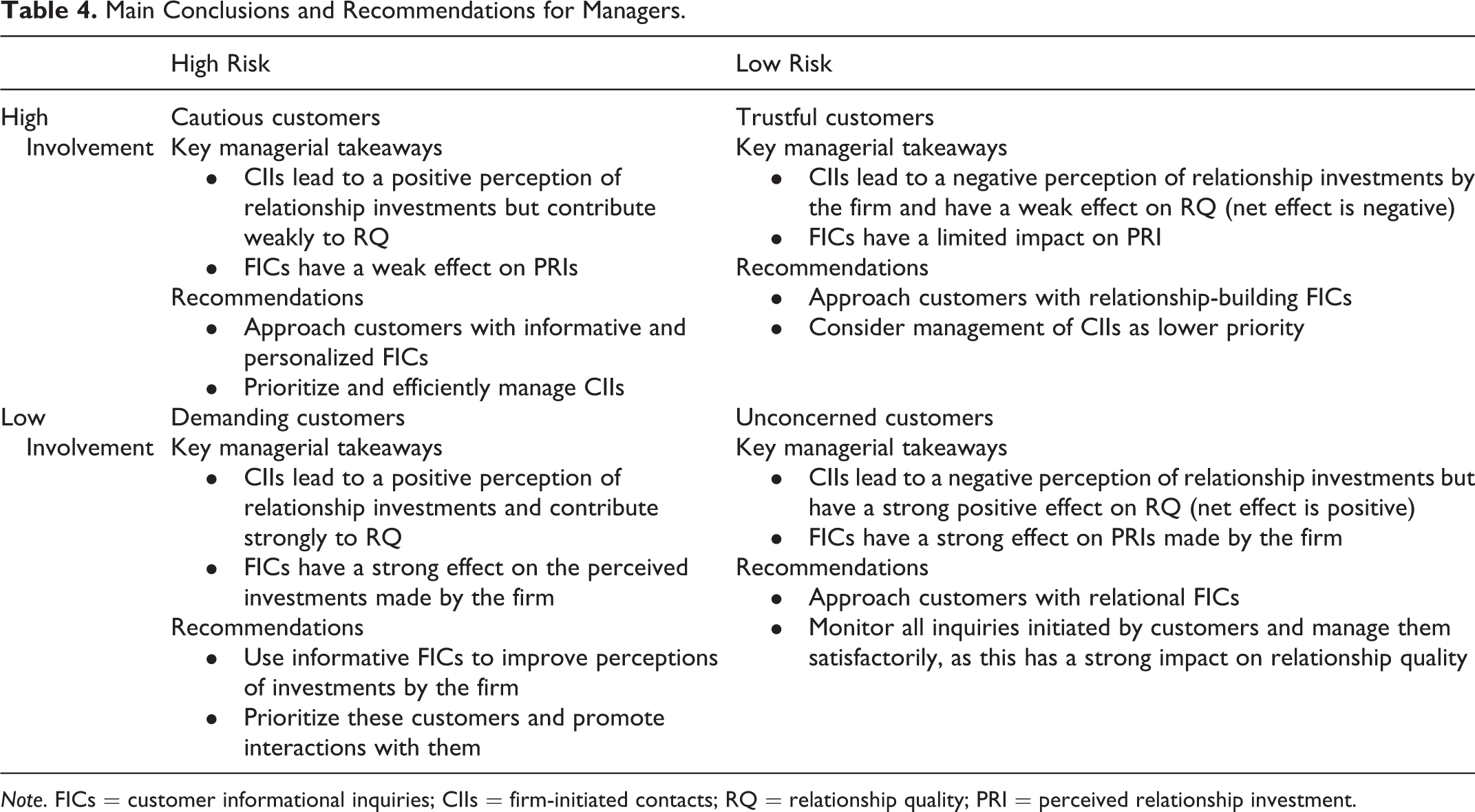

Our contingency framework reveals that the impact of FICs and CIIs may vary between different customers depending on their levels of perceived risk and customer involvement. Based on these two variables, we can identify four customer segments: (1) high-involvement customers who perceive the risk to be high (cautious customers), (2) high-involvement customers who perceive the risk to be low (trustful customers), (3) low-involvement customers who perceive the risk to be high (demanding customers), and (4) low-involvement customers who perceive the risk to be low (unconcerned customers). For each of these segments, a different approach regarding CIIs and FICs is advisable. Table 4 offers a summary of the key managerial takeaways for each segment and recommendations for firms on how to manage customer-firm interactions.

Main Conclusions and Recommendations for Managers.

Note. FICs = customer informational inquiries; CIIs = firm-initiated contacts; RQ = relationship quality; PRI = perceived relationship investment.

Given that for the “demanding customers,” both FICs and CIIs have a positive effect on perceived investment and RQ, companies are advised to prioritize these customers and promote interactions with them. Companies should develop FICs and proactively manage CIIs, as such efforts will constitute a valuable and profitable investment in the long term. For example, a specific recommendation can be to develop informative FICs, as receiving valuable information from the company on its products and services will help reduce risk.

“Unconcerned customers” should be targeted with FICs that strongly increase perceptions of relationship investments in this segment. Relational FICs can serve as a means to reinforce the quality of the relationship (which has a strong effect on subsequent behavior and on customer profitability). Relational FICs may be potentially effective in creating emotional bonds toward the company and increasing customer-firm RQ. For this segment, investing in FICs is of particular importance because FICs can mitigate the negative effect of CIIs on relationship investment. Given that CIIs ultimately strengthen the relationship and positively affect RQ, firms are advised to monitor all inquiries initiated by their customers and manage them satisfactorily, as this has a strong impact on RQ.

For the “trustful customers,” FICs contribute to a lesser extent to PRI, and therewith quality, compared to the other two segments. CIIs may even have a negative effect, given that they lead to a negative perception of the investment made by the firm in the relationship and only modestly improve RQ. Hence, increasing commercial FICs will be less effective in this segment compared to other segments. A useful recommendation is to use different types of FICs, such as relational FICs, as a means to further develop the relationship and make these customers feel special. These FICs may naturally produce favorable outcomes through positive attitudes and perceptions.

Finally, for “cautious customers,” neither FICs nor CIIs harm the customer relationship, but there are also no strong benefits in terms of PRI and RQ. The challenge for managers in this segment is to develop marketing strategies that help reduce consumers’ perceptions of risk. As commercial FICs have a weak effect on PRIs (and no effect on RQ), firms may limit FICs’ use, as they may not produce a large return on investment. However, this result may arise from the use of an inappropriate FIC. Hence, informative FICs addressed in a personalized way may contribute to reducing consumers’ perceived levels of risk and may be more effective in terms of RQ perceptions than other types of FICs. With regard to addressing consumers’ CIIs, the company should prioritize consumers in this segment: As they perceive higher levels of risk, a rapid and useful company response may make customers positively reconsider perceptions about their relationship with company.

Our results reinforce the notion that firms need to collect more information about their customers in order to have a rich enough database to develop more efficient marketing-mix segmentation. This is the only way to be accurate in designing the strategy. This research has shown that each customer perceives each interaction in a specific way depending on their own characteristics (their perception of risk and their involvement). As these perceptions are crucial, given that they will lead to specific customer behaviors and profitability, we strongly recommend that companies pay more attention to the role that customer characteristics can play before designing and developing any strategy. It may also be worthwhile for managers to gather additional information about these customers; for instance, identifying their attachment style (Mende and Bolton 2011; Mende, Bolton, and Bitner 2013) could provide more fine-grained predictions about how these customers may react to an FIC.

Segmenting customers will be necessary from a managerial point of view to establish when, how often, with what message (informative, commercial or relational), through what channels, and so on, companies should contact each segment (via FICs). In addition, this segmentation will help to determine basic guidelines to decide which CIIs should be prioritized, as the effect of a CII likely depends on whether and how a company responds to it (Bolton and Drew 1991)—we did not observe this aspect in our study due to data limitations. Definitively, the company should fit its resources to the specific needs of each customer segment; some segments (that are in more critical or uncertain situations) will be more demanding (petitioners) of the company than others.

Limitations and Further Research

Although this study has demonstrated the importance of customer-firm interactions as antecedents of a set of relational variables that led to other behavioral and financial outcomes during a period of 2 years, it is not without limitations. We only focused on developing our research in the financial services industry. This industry has specific characteristics, such as the relevance of customer-firm interactions and a personalized relationship with employees, but it would be interesting for further research to replicate the same chain of effects in other contexts to compare the results and extract solid conclusions for the literature. In addition, although we used longitudinal data from a European bank, as we conducted a survey to measure customer perceptions at time t 1, we transformed the initial longitudinal customer data into cross-sectional data (including the averages of each period of time in the database). Therefore, for future research, it would be interesting to collect more data in order to replicate our study while taking into account all (monthly) customer information.

Furthermore, we did not distinguish between different types of FICs, as most of the contacts of the financial entity are aimed only at stimulating purchases and have a clear commercial goal. However, for future research, it would be of interest to analyze different types of FICs (commercial, relational, informative, etc.) separately. Similarly, although CIIs can be highly heterogeneous and can differently affect the company, in this research, CIIs are defined as informational customer contacts regarding the company’s products and services. Hence, future research may focus on analyzing the consequences of positive (informational contacts) versus negative (complaints) customer contacts on performance. In addition, although our conceptual framework is one-way and linear, we encourage academics to analyze these variables through feedback loops that show the relationship developing over time, as this is a dynamic and iterative process. Furthermore, firms may allocate FICs based on expected customer profitability; hence, there may be some endogeneity, resulting in an inflation of the positive effects of FICs. Future research could therefore analyze how different expected levels of profitability from customers may make companies vary their investments in terms of FICs.

Future research could also approach the direct influence of customer-firm interactions (FICs and CIIs) in each link of the chain of effects. Thus, it would be interesting to investigate whether FICs and CIIs influence cross-buy, service usage, or even profitability in a direct way. Following the conceptual framework proposed by Bolton, Lemon, and Verhoef (2004), there is a causal sequence of the effects of marketing instruments (FICs): (1) FICs influence relationship perceptions, (2) which influence customer behaviors, (3) which, in turn, affect financial outcomes. Although we have gone a step further with the inclusion of CIIs and two determinant moderating effects, we have followed the original structure of the conceptual framework, measuring only the direct influence of customer-firm interactions (FICs and CIIs) on the first sequence of effects: relationship perceptions (PRI and RQ). Furthermore, it is conceivable that other consumer traits also shape customers’ response to CIIs and FICs; in particular, taking into account customer attachment styles (Mende and Bolton 2011; Mende, Bolton, and Bitner 2013) may be a fruitful avenue for future research.

We also propose that future studies include additional steps in the proposed chain of effects that cover customer nontransactional behaviors. These nontransactional behaviors may be determined by the RQ and may influence purchase behaviors and even customer profitability. If the customer perceives a high level of RQ, he or she will be more likely to share positive word of mouth or engage in co-creation (Bijmolt et al. 2010). Recommendations or suggestions to other customers, or even to the company, after satisfactory interactions may generate value for companies that can result in more sales and income for the company in the future. In the chain of effects studied here, we only included customer purchase behaviors such as cross-buy or service usage. However, the current literature has highlighted the importance of also considering customer nonpurchase or nontransactional behaviors (Kumar et al. 2010; van Doorn et al. 2010). These behaviors, despite not having a direct influence on the company’s profits in the short term, contribute to building stronger customer relationships, which, in future, may influence financial outcomes.

Footnotes

Appendix

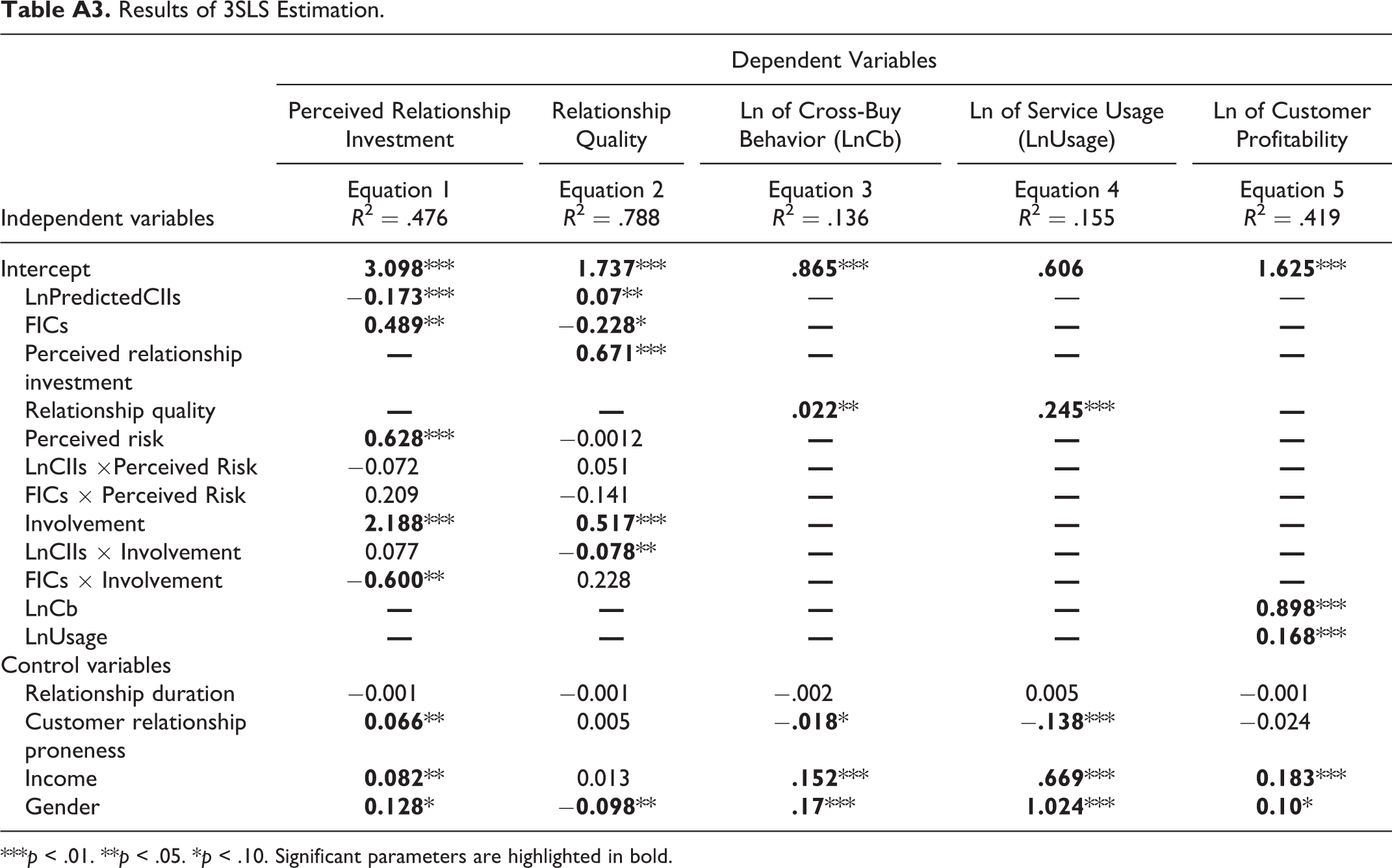

Results of 3SLS Estimation.

| Independent variables | Dependent Variables | ||||

|---|---|---|---|---|---|

| Perceived Relationship Investment | Relationship Quality | Ln of Cross-Buy Behavior (LnCb) | Ln of Service Usage (LnUsage) | Ln of Customer Profitability | |

| Equation 1 R 2 = .476 | Equation 2 R 2 = .788 | Equation 3 R 2 = .136 | Equation 4 R 2 = .155 | Equation 5 R 2 = .419 | |

| Intercept |

|

|

|

|

|

| LnPredictedCIIs |

|

|

— | — | — |

| FICs |

|

|

|

|

|

| Perceived relationship investment |

|

|

|

|

|

| Relationship quality |

|

|

|

|

|

| Perceived risk |

|

−0.0012 |

|

|

|

| LnCIIs ×Perceived Risk | −0.072 | 0.051 |

|

|

|

| FICs × Perceived Risk | 0.209 | −0.141 |

|

|

|

| Involvement |

|

|

|

|

|

| LnCIIs × Involvement | 0.077 |

|

|

|

|

| FICs × Involvement |

|

0.228 |

|

|

|

| LnCb |

|

|

|

|

|

| LnUsage |

|

|

|

|

|

| Control variables | |||||

| Relationship duration | −0.001 | −0.001 | −.002 | 0.005 | −0.001 |

| Customer relationship proneness |

|

0.005 |

|

|

−0.024 |

| Income |

|

0.013 |

|

|

|

| Gender |

|

|

|

|

|

***p < .01. **p < .05. *p < .10. Significant parameters are highlighted in bold.

Authors’ Note

The authors have signed the paper in alphabetical order.

Acknowledgment

The authors want to show their gratitude to the collaborating bank for providing the data for the analyses.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Jesus Cambra-Fierro, Iguacel Melero-Polo, and F. Javier Sese are members of the research group Generes (![]() ), and they appreciate the financial support received from the projects ECO2014-54760 (MICINN, FEDER), and S09-PM062 (Gobierno de Aragon and Fondo Social Europeo) as well as from the program “Ayudas a la Investigación en Ciencias Sociales, Fundación Ramón Areces”.

), and they appreciate the financial support received from the projects ECO2014-54760 (MICINN, FEDER), and S09-PM062 (Gobierno de Aragon and Fondo Social Europeo) as well as from the program “Ayudas a la Investigación en Ciencias Sociales, Fundación Ramón Areces”.