Abstract

Mobile payment technology platforms are quickly gaining popularity. Despite this growth, academic research offers little insight into how adopting mobile payment technology impacts firm value. Further, extant studies are silent on the factors that determine the outcome of pursuing this strategy. Results from an event study of 152 announcements of mobile payments show an increase in firm value by an average of 1.03%, highlighting their effectiveness. Further analysis reveals characteristics of mobile payments that can augment this change in firm value. Specifically, positive firm value accrues when retailers promote the use of mobile payments to their customers. The authors also find that, compared with retailers whose target market comprises older customers, retailers targeting younger customers benefit more from adopting mobile payments. Finally, this study reveals an early-mover advantage, which is maximized in conjunction with an expansive, national rollout strategy. In fact, although a national rollout can be more beneficial early, the results show that for retailers that adopt mobile payments later, there is no difference between using an expansive rollout or a more limited, phased rollout strategy.

The use of mobile payment apps such as Apple Pay, Samsung Pay, PayPal, and Venmo has become increasingly popular with both customers and retailers. For example, in 2020, CVS began offering payments via PayPal and Venmo at its brick-and-mortar stores. Similarly, among others, retailers such as Macy's, Kroger, and Walgreens now allow customers to make in-store payments using mobile devices such as smartphones, smart watches, and tablet computers in addition to traditional payment methods such as cash, credit, or debit cards. According to Kats (2021), mobile payments in the United States are growing; they reached 92.3 million users in 2020 and are projected to grow at an annual rate of 20% through 2025. Adoption of mobile payment technology is driven by customers who value hygiene, convenience, and security. Compared with traditional payment methods, mobile payments are perceived as more hygienic, as customers do not handle cash or touch shared devices such as point-of-sale systems (Fennell et al. 2022). Furthermore, mobile payment technology can facilitate a faster checkout process, provide added convenience for customers (Boden, Maier, and Wilken 2020; Shin 2009), and be considered more secure than traditional transaction methods (Arvidsson 2014; Pal et al. 2017).

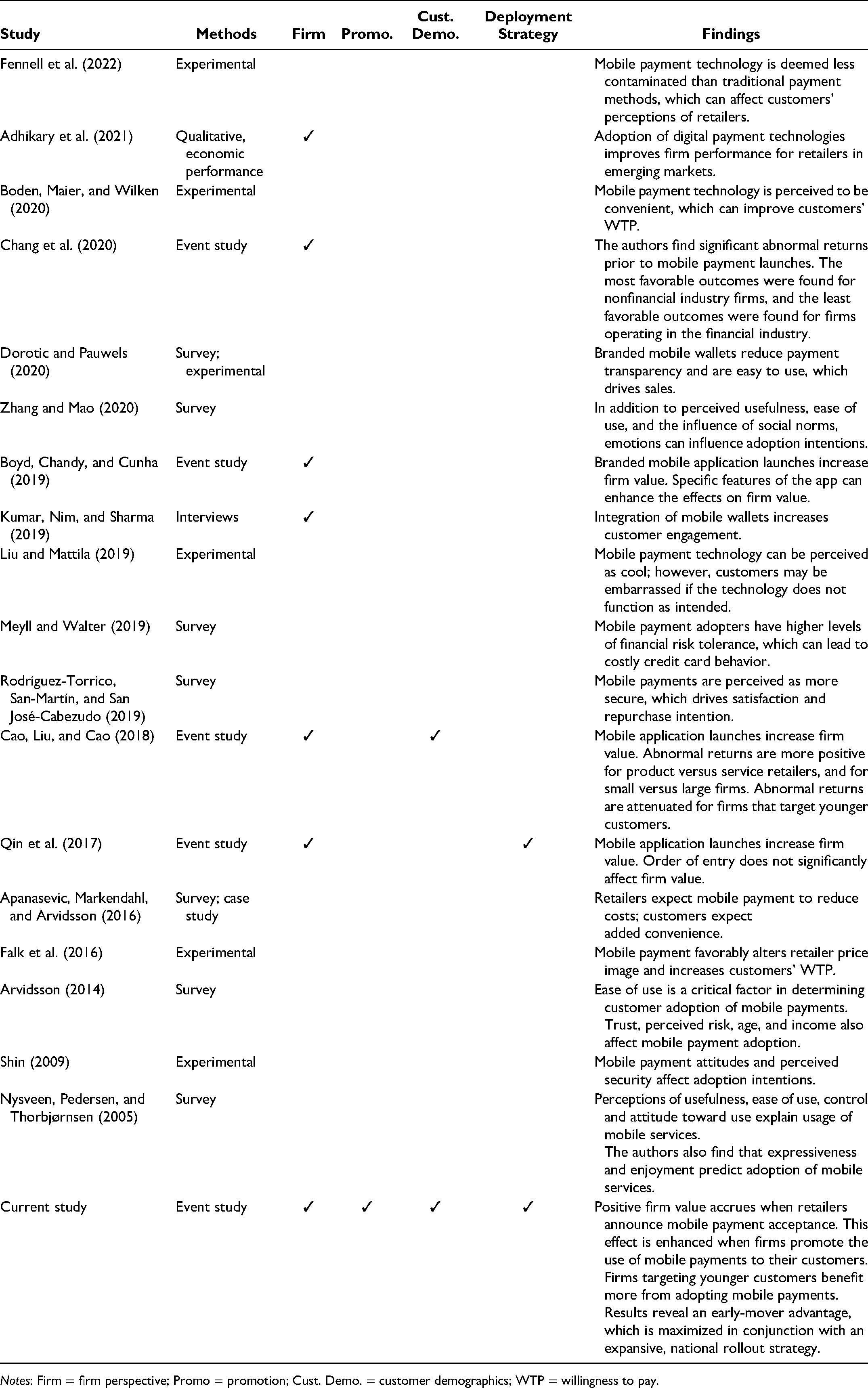

Research on technology adoption in general, and mobile payment methods more specifically, tends to focus on the drivers of adoption, such as customer characteristics (e.g., age, education, income) and attitudes toward the technology (e.g., Meuter et al. 2005; Nysveen, Pedersen, and Thorbjørnsen 2005; Shin 2009; Zhang and Mao 2019). Other research explores how mobile payments affect customers’ transaction satisfaction (Liu and Mattila 2019) and purchase intentions (Dorotic and Pauwels 2020; Rodríguez-Torrico, San-Martín, and San José-Cabezudo 2019). Although research on technology adoption in general explores the pioneering advantage, few studies attempt to understand how adopting mobile payments impacts firm value, let alone strategic factors influencing this outcome. First, although Chang, Shih, and Chien (2020) examine the impact of mobile payments on firms in Taiwan, their study focuses primarily on financial institutions, ignoring adoption consequences for retailers. Similarly, Son and Kim (2018) investigate how the adoption of mobile payments collectively impacts upstream companies (e.g., banks, credit unions, and platform operators), which derive unique benefits from mobile payments. These findings highlight the need for empirical analysis to identify whether mobile payment adoptions are beneficial to retailers. Kumar, Nim, and Sharma (2019) and Adhikary et al. (2021) attempt to address this question by examining the relationship among mobile payments, customer engagement, and firm performance; however, these studies examine mobile wallets (e.g., Google Pay, WeChat Pay) from a handful of small, unorganized retailers in emerging markets (i.e., India, China). Furthermore, these studies do not directly measure the impact of mobile payment adoption on firm value. Our investigation provides unique insight by investigating the financial implications for retailers adopting mobile payment technology. Specifically, we measure the change in firm value resulting from mobile payment adoption using a forward-looking metric based on shareholder value. We then delve deeper to understand factors influencing these effects.

In this study, we directly focus on two specific questions that have theoretical relevance as well as managerial significance. First, we explore whether there are any changes in the firm value of retailers that adopt mobile payment technology. Second, we examine tactics that can moderate the effects of mobile payment technology on firm value. To address these questions, we employ a three-step method. First, we refer to pain-of-payment research and the diffusion of innovations theory to build a conceptual framework for evaluating investors’ reactions to announcements of mobile payment additions by retailers. This framework indicates that investors should react positively to mobile payment technology adoption. Further, this favorable response should be more pronounced when retailers (1) employ promotions to incentivize their customers to adopt mobile payment technology, (2) target younger customer segments, and (3) adopt mobile payments early, depending on the scale of the rollout strategy. We then proceed to develop and test our hypotheses based on this conceptual framework. Second, we use the event study methodology to calculate changes in firm value after retailers announce mobile payments. We then estimate a model considering the context of the mobile payment app's announcement (promotion), retailers’ target customers (customer segment), and deployment strategy (speed of adoption and rollout intensity) on firm value using data from 152 announcements.

Our study contributes to two distinct literature streams. In contrast to previous mobile payment research that focuses on how adopting mobile payments impact customer responses such as avoidance of contamination (Fennell et al. 2022), convenience, satisfaction (Liu and Mattila 2019; Rodríguez-Torrico, San-Martín, and San José-Cabezudo 2019), store price image, willingness to pay (Falk et al. 2016), and purchase intentions (Dorotic and Pauwels 2020), the focus of this article is on the impact of mobile payments on firm value, an underexamined topic in this literature stream. Another body of research investigates how mobile payments impact firms. Studies in this area focus either on how mobile payments jointly impact all the firms in the distribution channel (e.g., Chang, Shih, and Chien 2020; Son and Kim 2018) or on how mobile payments indirectly impact retailers’ operations in emerging markets (e.g., Adhikary et al. 2021; Kumar, Nim, and Sharma 2019). This stream of work does not currently address how mobile payment technology adoption directly affects firm value; nor does extant research examine managerial factors that can influence this effect on firm value. In this regard, we are the first to investigate the financial implications of mobile payment adoption on retailers in developed markets and, perhaps more importantly, factors that affect the benefits realized for retailers. Second, although overwhelming evidence shows that channel expansions achieved through the addition of mobile apps improve firm value, studies in this area (e.g., Boyd, Kannan, and Slotegraaf 2019; Cao, Liu, and Cao 2018; Qin et al. 2017) primarily examine how the addition of different types of mobile apps such as search-oriented mobile apps (i.e., mobile apps that customers use to gather information), social-oriented mobile apps (i.e., mobile apps through which customers interact with both retailers and other customers), and transaction-oriented mobile apps (i.e., mobile apps that facilitate in-app transactions) impact retailers. Importantly, none of the mobile apps studied in this literature stream can be used by customers for in-store transactions, an area our research addresses. Finally, we add to the innovation diffusion literature by identifying factors that drive the diffusion and adoption of in-store innovations by retailers. In doing so, we provide implications for practitioners to consider when adopting shopper-facing technology in a retail setting (Inman and Nikolova 2017).

The remainder of this article is structured as follows: In the next section, we establish the conceptual framework and hypotheses. Subsequently, we proceed to describe the research methods and present our findings. We then provide theoretical and managerial implications and present the conclusions from our study.

Conceptual Framework and Hypothesis Development

Retailers adopting mobile payments benefit from their ability to generate additional cash flows, which in turn improves firm value. Previous research on payment methods, outlined in Table 1, explains how mobile payments can enhance the firm value of retailers. Specifically, research in this area recognizes that purchase contexts involve the trade-off of giving up or parting with money to receive a product or service, and that this parting with money induces a pain of payment—the discomfort or anguish customers feel when making monetary expenditures (Prelec and Loewenstein 1998). Critically, this pain of payment varies by payment method (e.g., cash, credit card, mobile payment), even when the amount spent by the customer is held constant (Dorotic and Pauwels 2020; Prelec and Loewenstein 1998; Raghubir and Srivastava 2008). This is because payment methods vary in terms of the degree of payment transparency or the relative salience of the amount of money required in a specific transaction (Soman 2001). In general, when a payment method is more transparent, it reminds the customer that their wealth is being depleted, which in turn increases the pain of payment. In this regard, compared with traditional payment methods, mobile payments are the least transparent and, subsequently, the least painful form of payment (Dorotic and Pauwels 2020). In fact, prior studies show that using a less painful payment method increases not only customers’ willingness to pay for products but also the amount they spend per shopping trip (Dorotic and Pauwels 2020; Lee et al. 2019; Prelec and Simester 2001; Sheehan and Van Ittersum 2018). In principle, this suggests that retailers should generate higher cash flows and increased revenue following the adoption of mobile payments, which in turn increases their firm value.

Literature on Mobile Payment Technology.

Notes: Firm = firm perspective; Promo = promotion; Cust. Demo. = customer demographics; WTP = willingness to pay.

In addition, research shows that mobile payments simplify the checkout process, contributing to a frictionless retail experience (Zhu, Cohen, and Ray 2021). These technologies also allow retailers to combine marketing actions on a single platform, affording retailers an opportunity not only to acquire detailed information about their customers but also to personalize their promotions, increasing customers’ transaction frequency (Kumar, Nim, and Sharma 2019; Xu, Ghose, and Xiao 2018). Altogether, this leads to greater convenience for the customers and higher operational efficiencies for retailers, resulting in higher and more predictable cash flows for retailers. As a result, the demand for the retailers’ stock should increase, enhancing their firm value. Thus, we predict:

However, for retailers to benefit from mobile payments, customers must adopt this form of payment and use it extensively. According to the diffusion of innovations theory (Rogers 2003), before adopting innovations, customers must first acquire initial knowledge about the innovation and formulate attitudes toward the innovation. During the knowledge acquisition phase, retailers can use a myriad of promotional materials (e.g., advertising, billboards, brand advocates) to increase awareness about the innovation (Helmes, Schlosser, and Weber 2013). In the attitude formation stage, the characteristics of the innovation, the availability of the innovation, the reputation of the firm offering the innovation, and the benefits customers accrue from using the innovation influence not only customers’ evaluation of the innovation but also their adoption intentions (Demoulin and Zidda 2009).

Furthermore, drawing on the technology acceptance model (Davis 1989) and the unified theory of acceptance and use of technology (Venkatesh, Thong, and Xu 2016), research in retail innovations shows that their adoption is driven by customers’ demographic characteristics such as age, income, and education (Hew et al. 2015). Thus, we anticipate that the adoption of new in-store innovations such as mobile payments will depend on promotional programs designed to motivate customers to use the innovation (promotion), the characteristics of the retailers’ targeted customer segments (customer segment), and the deployment strategy employed by the retailers (speed of adoption and rollout). Altogether, these factors drive the shifts in firm value for retailers that adopt mobile payments, and therefore we develop hypotheses on their impact.

Promotion

Promotion involves the use of communications to motivate and facilitate customer responses such as referral intentions (Wolters, Schulze, and Gedenk 2020), online advertisement click-through rates, store visits (Song et al. 2018), and purchases (Chandon, Wansink, and Laurent 2000). The promotions themselves can offer additional benefits to customers through vehicles such as free shipping, gifts with purchase, sweepstakes, price discounts, in-pack coupons and rebates, and gamified promotional programs (Chandon, Wansink, and Laurent 2000; Zichermann and Cunningham 2011). For example, marketers have widely employed gamification elements such as goal and progress tracking, points accumulation, badges, leaderboards, and progress bars to develop a myriad of loyalty programs that aid in not only driving purchases, but also engaging and retaining customers (Högberg et al. 2019; Jang, Kitchen, and Kim 2018).

Promotions have been frequently employed to promote the use of mobile payment technology. For example, when Marriott launched Apple Pay, its customers who used the mobile app could earn additional rewards from their purchases. The Children's Place offered $10 off, 1-800-Flowers offered $15 off, and Ray-Ban offered 30% off purchases utilizing the mobile payment technology Apple Pay. Similarly, for a limited time following its launch, customers who used Google Pay at Domino's Pizza were rewarded with free pizza every time they used the mobile app. The same was the case for users of the Starbucks mobile app; they earned rewards in the form of badges for making purchases using the mobile app. Starbucks customers were also granted status levels based on their use, enjoying unique benefits at each level.

Extant research reveals that promotions can stimulate curiosity and enhance the perceived usefulness of novel products (Orsingher and Wirtz 2017). We contend that incentivizing mobile payment usage by using promotional elements increases customer curiosity about the innovation, eventually increasing their usage of mobile payment technology. Bearing in mind that existing studies also show that customers spend more when using mobile payments (e.g., Dorotic and Pauwels 2020; Falk et al. 2016), we expect that such usage by customers should increase retailers’ cash flows, resulting in higher firm value for retailers. Therefore, we hypothesize:

Customer Segment

Compared with older customers, younger customers tend to be not only more tech savvy but also more comfortable with technology and more likely to enjoy the benefits of using it. This is because they have greater access to technology and are more open to new ways of engaging with it (Lam and Shankar 2014; Pagani 2004). Furthermore, since they grew up with mobile technologies such as laptops, tablets, and smartphones, younger customers are also the largest users of these mobile devices and may have no experience of being without them (Wilken and Goggin 2011). In fact, when it comes to the use of mobile apps, prior work finds that mobile app users are usually younger customers who value convenience (Cao, Liu, and Cao 2018; Jih 2007; Sultan, Rohm, and Gao 2009). This stream of research also shows that since these younger customers are mobile savvy, they also have a higher probability of responding to mobile marketing strategies (Shankar et al. 2016; Wang, Krishnamurthi, and Malthouse 2015).

Similarly, extant research also finds that because they are more innovative than the general population, younger customers also adapt to change easily, which results in them not only having a favorable attitude toward new innovations but also adopting them early (San-Martín, Prodanova, and Jiménez 2015). This early adoption is also driven by the fact that younger customers are also less risk averse (Kimmel 2015; Liu et al. 2019), more innovative (Kimmel 2015), and generally enthusiastic about new technology (Kimmel 2015), which suggests that they are more likely to adopt and use mobile payment apps. Taken together, this research shows that the customer segment served by the retailer (i.e., whether it serves young or older customers) is an influential factor for mobile payment adoption rates, such that when the retailer mostly targets younger customers, mobile payment adoption rates will be high. Therefore, for reasons previously discussed, high usage rates of mobile payments should result in increased cash flows and revenues for retailers, suggesting that investors may believe that retailers targeting younger customers accrue more benefits from launching mobile payments through the generation of additional demand. In view of this, we hypothesize:

Deployment Strategy

Being among the first firms to offer new retail technologies is a planned decision that can give competitive advantages to retailers that preempt the competition. Broadly speaking, being first in the market with a new retail technology allows retailers to gain immediate customer awareness, which contributes to brand loyalty. In addition, being an early mover provides retailers the capability to mold customer preferences by creating an industry standard, which in turn allows them to gain market share by virtue of having temporary exclusive access to customers (Kerin, Varadarajan, and Peterson 1992; Lieberman and Montgomery 1988; Lilien and Yoon 1990). Existing studies find that these advantages accrue from the preemption of scarce assets, the establishment of significant supply chain relationships, and, more relevant to the current investigation, technology leadership. Each of these advantages can serve as barriers to entry for new competitors, offering the opportunity to capture greater market share (Kerin, Varadarajan, and Peterson 1992; Lieberman and Montgomery 1988).

Regarding mobile payments, the advantages that retailers accrue from being an early mover stem from technology leadership, which allows retailers that pioneer new mobile payments to not only create a new market segment but also appeal to tech-savvy customers of rivals that do not offer mobile payments. Altogether, offering mobile payments early grants retailers unshared access to customers who value the benefits of mobile payments. As a result, it also permits retailers to mold customer preferences, in that customers will come to view trailblazing retailers as examples against which later entrants will be assessed. Furthermore, being an early mover in the offering of mobile payment capabilities also allows retailers to gain a reputation as technology leaders, which should improve their brand image (Venkatesh, Thong, and Xu 2016). On the contrary, retailers that are late in offering mobile payment capabilities risk being viewed as stagnant and outdated, which may result in the loss of goodwill among their customers and investors. In turn this may adversely impact the retailer's revenue. Thus, offering mobile payments early signals to investors that the retailer is willing to make the necessary investment to achieve rapid growth and preempt the position of the competition.

However, the implementation strategy (i.e., rollout strategy) employed by retailers can determine whether they can accrue advantages by being among the first to offer new technologies (Klingebiel, Joseph, and Machoba 2022). Depending on the retailer's intention, a nationwide rollout or a phased rollout—in which the new retail technology is first introduced to a subset of the market—can be used to launch a new retail technology (Kalish, Mahajan, and Muller 1995; Kimmel 2015). A phased rollout strategy helps retailers reduce the risks of failure, as they can continuously examine and iterate the technology during implementation (Pennings and Lint 2000). However, this strategy occurs over an extended period, suggesting that retailers may concede the benefits associated with the early-mover advantage. In fact, even though a national rollout is resource intensive, this strategy has a shorter implementation time, which allows retailers to create brand awareness and quickly gain market share. This contention is in line with extant research showing that the speed of adoption advantages are not unlimited, but rather they are dependent on industry life cycles, launch strategies, and economic conditions (Klingebiel, Joseph, and Machoba 2022; Lieberman and Montgomery 1988; Robinson, Fornell, and Sullivan 1992). In other words, the combination of a firm being an early mover with a national rollout strategy should provide maximum benefits. Pioneering firms employing a limited or phased rollout strategy may attenuate the benefits associated with the early-mover advantage. In addition, late entrants into the market may not benefit from a national versus a phased rollout strategy. From this, we posit that the early-mover advantage is greatest when a national rollout strategy is employed. Thus, we hypothesize:

Data and Methodology

Our sample is derived from announcements detailing each retailer's launch of mobile payments in large daily news sources and wire services such as Bloomberg, PR Newswire, Newswire, Business Wire, and others between 2011 and 2020. This sample included 178 announcements from publicly traded retailers. From this sample, we then eliminated announcements from international retailers and announcements with missing Center for Research in Security Prices and Compustat data required to create relevant control variables (McWilliams and Siegel 1997). This action removed 21 events, resulting in a final sample of 152 mobile payment announcements from 130 U.S. publicly traded retailers.

Dependent Variables

Our primary measure of firm value is how the stock market reacts to mobile payment announcements. We estimate this reaction using the event study approach. This methodology relies on the efficient market hypothesis, which contends that asset prices reflect all information available about a retailer's future cash flows (Fama 1970). As a result, in an efficient market, the availability of new information (in our case, the launch of mobile payments) leads to investors expecting changes in future cash flows. If investors anticipate that the new information will increase (decrease) a retailer's projected cash flows, there will be more (less) demand for the retailer's stock, and subsequently an increase (decrease) in the stock price. Therefore, the effect of launching mobile payments on firm value is measured by the stock's abnormal return (i.e., the stock's expected return minus the stock's actual returns; Kothari and Warner 2007).

We focus on abnormal returns that are obtained on the day of the event. Specifically, we estimate abnormal returns

Operationalization of Variables.

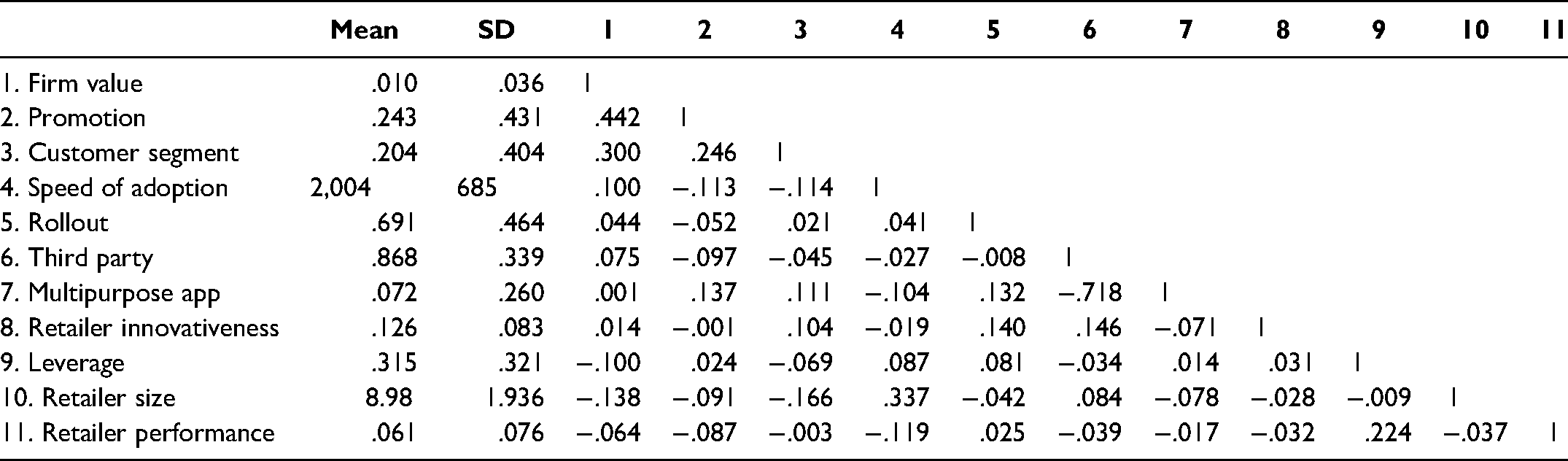

Descriptive Statistics and Correlation Matrix.

Independent Variables

Promotion

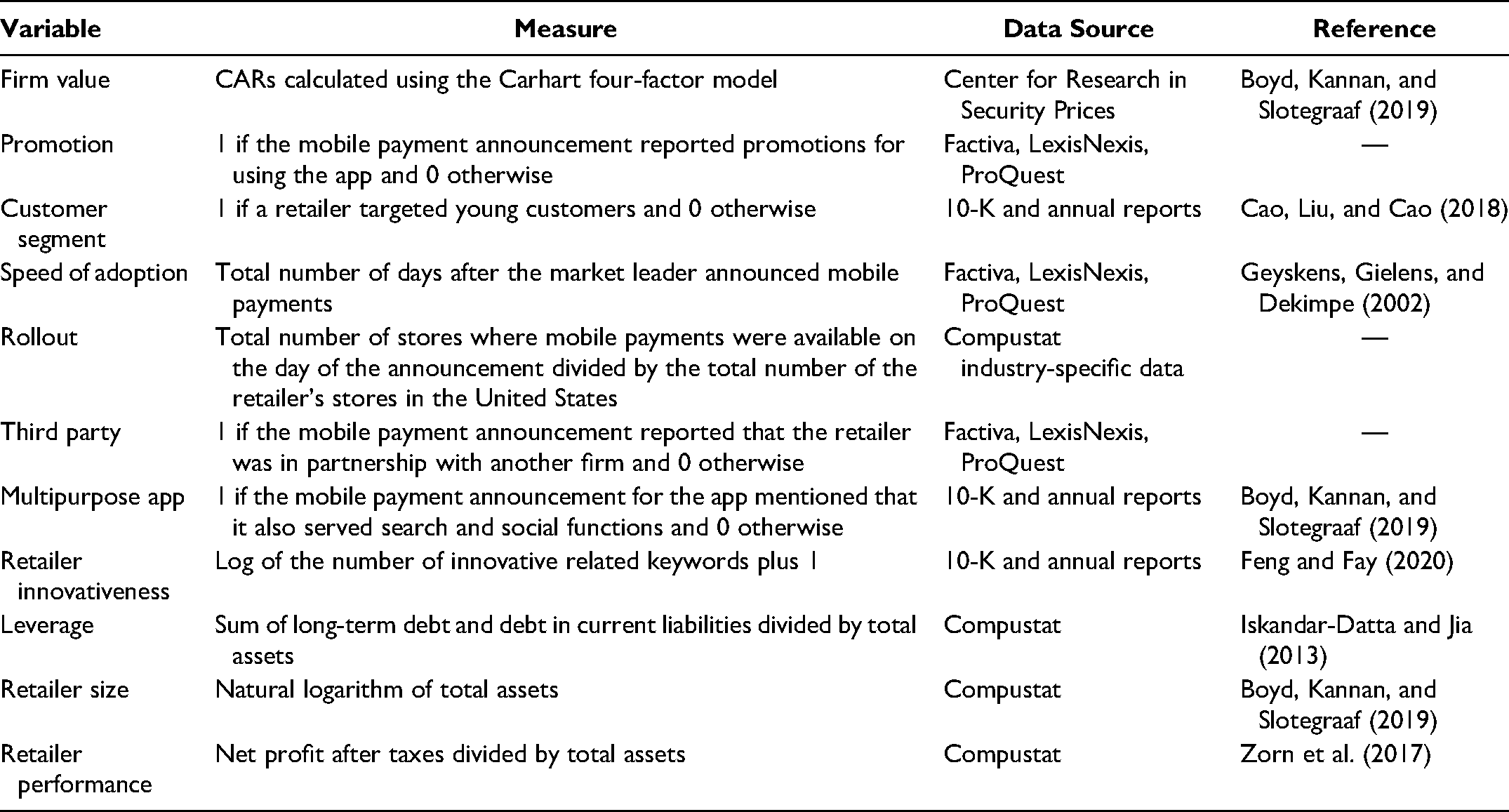

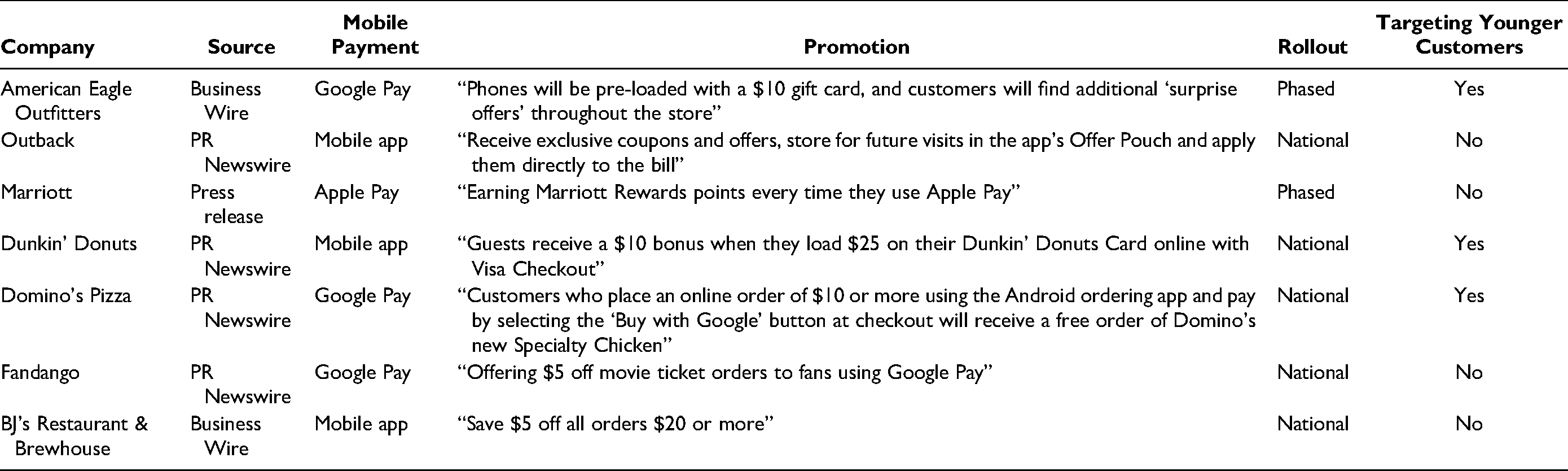

We measured promotion using a dummy variable that indicates whether the mobile payment app had promotional elements assigned to it by the retailer at the time of launch. Specifically, we code promotion as 1 if the mobile payment launch announcement highlighted that customers could win prizes (e.g., gift cards, free products), receive additional coupons and discounts, and earn redeemable reward points when they used mobile payments, and 0 otherwise. Examples of the promotions communicated by the retailers are provided in Table 4. Consistent with extant research (e.g., Robinson et al. 2015), we employed judges to determine this classification. Specifically, two judges manually analyzed the text content of the announcements to determine whether retailers communicated to customers any incentives for using mobile payments. The responses from the judges had an acceptable interrater reliability of .82 (Rust and Cooil 1994), and discrepancies were resolved through discussion.

Selected Examples of Announcements.

Customer segment

Following prior research (e.g., Cao, Liu, and Cao 2018), we used a dummy variable to measure customer segment. That is, in our model this variable takes the value of 1 if the retailer appears to target young customers or to explicitly state that its target customers’ ages were below 35, and 0 otherwise. We acquired the data to measure this variable by having two independent judges manually analyze the text of retailers’ 10-K reports, which U.S.-based publicly traded firms use to provide an overview of a firm's main operations, including the products and services the firm sells, as well as specific financial information about the firm over the previous five years. In addition, we also conducted computer-aided text analysis of the same 10-K reports. The interrater reliability was .70, which was satisfactory for our purposes (Rust and Cooil 1994).

Speed of adoption

Consistent with extant research (e.g., Geyskens, Gielens, and Dekimpe 2002), we measured speed of adoption as the length of time between the market leader's entry into the marketplace and the focal retailers’ mobile payment announcement. In other words, we created this variable by counting the number of days it took the retailer to launch mobile payments after the entry of the market leader in our sample.

Rollout

Last, we measured rollout by dividing the retailer's total number of locations where mobile payments were going to be available on the day of the announcement by the retailer's total number of locations in the United States. Inherently, this variable measures the retailer's mobile payment rollout intensity (i.e., the percentage of the retailers’ stores where mobile payments would be available at the time of the announcement).

Control Variables

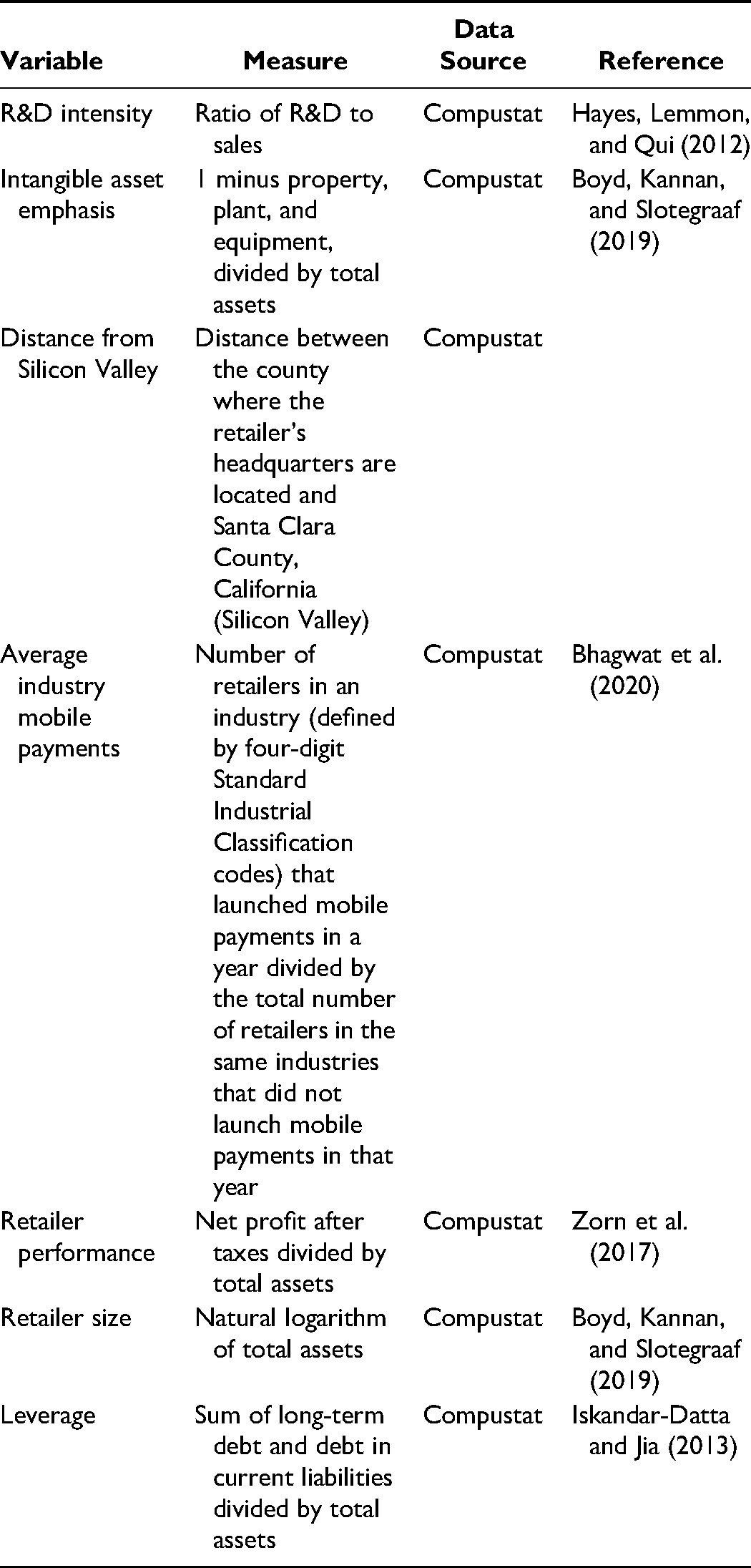

In addition to our independent variables, we also include in our model several control variables—third party, multipurpose app, retailer innovativeness, leverage, retailer size, and retailer performance—as well as industry-specific and time-specific variables. To control for the differences in firm value between mobile payment announcements in which retailers partnered with third-party mobile payment platforms (e.g., Apple Pay, Samsung Pay, Venmo) and mobile payments that were solely launched by the retailers (e.g., mobile payment apps that use QR codes), we include a dummy variable for third-party payments in our model. We also include a dummy variable for multipurpose app, which captures whether a mobile payment app also offered search functions or social features. Formal announcements are cross-referenced with other information sources, such as firms’ websites, social media feeds, and primary media outlets, to ensure consistency in the type and amount of information presented to the market. To account for the fact that innovative retailers are expected to introduce novel technologies (e.g., Dotzel and Shankar 2019), we include a variable for retailer innovativeness in our model. To measure this variable, we analyzed the text in the retailers’ 10-K reports. Specifically, in line with prior studies (e.g., Bhattacharya, Misra, and Sardashti 2019; Feng and Fay 2020) we use computer-aided text analysis to calculate the incidence of innovativeness-related keywords 1 found in the reports. Subsequently, we use the number of these keywords as a proxy for retailer innovativeness. To account for the large variance of this measure, we log transform and add 1 to the variable. Our model also includes additional variables that control for the retailers’ financial status at the time of the mobile payment announcement. Specifically, we control for firm leverage, retailer size, and retailer performance as they affect firm value (Maloney, McCormick, and Mitchell 1993). We measure leverage as the sum of the total long-term debt and debt in current liabilities divided by total assets (Iskandar-Datta and Jia 2013), retailer performance using the ratio of net income to total assets, and retailer size by taking the log of total assets (e.g., Boyd, Kannan, and Slotegraaf 2019; Zorn et al. 2017). Last, we control for other unobserved industry-specific and time-specific factors by adding industry and year dummy variables to our model.

Model Specification

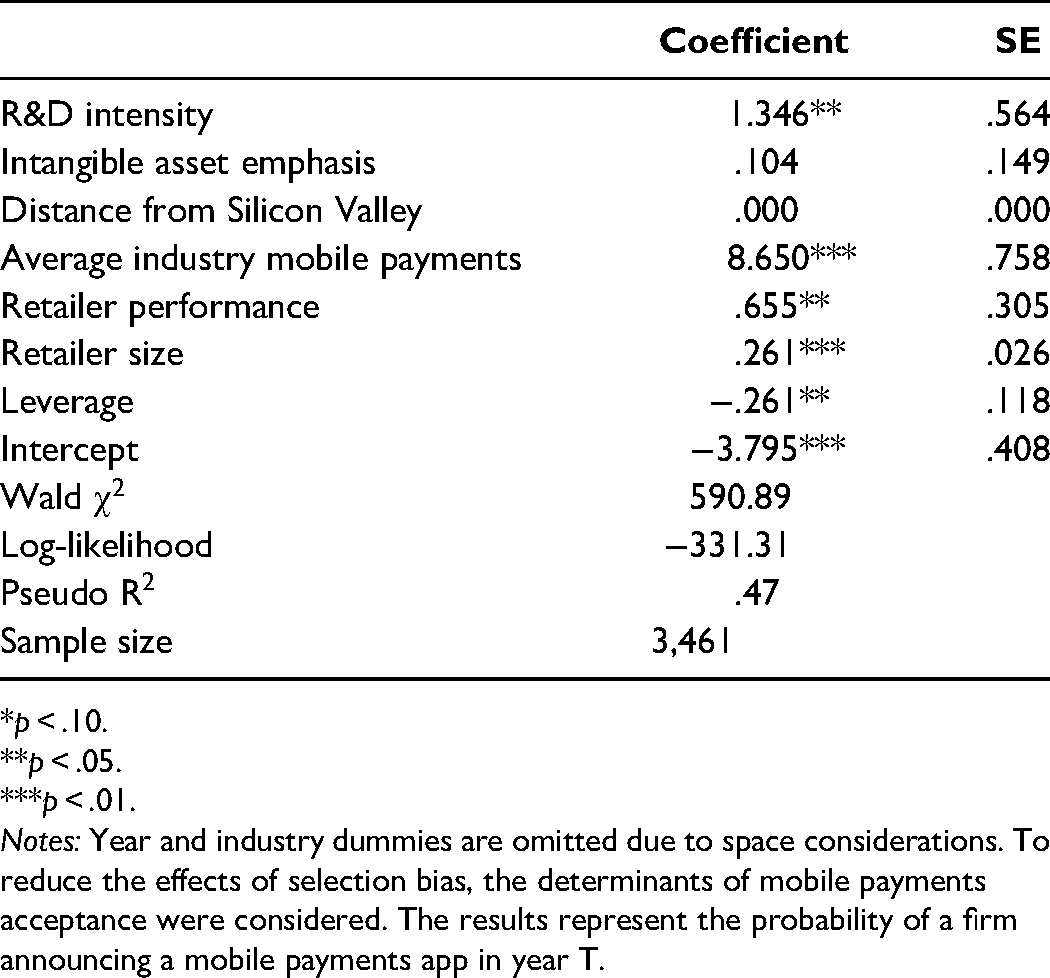

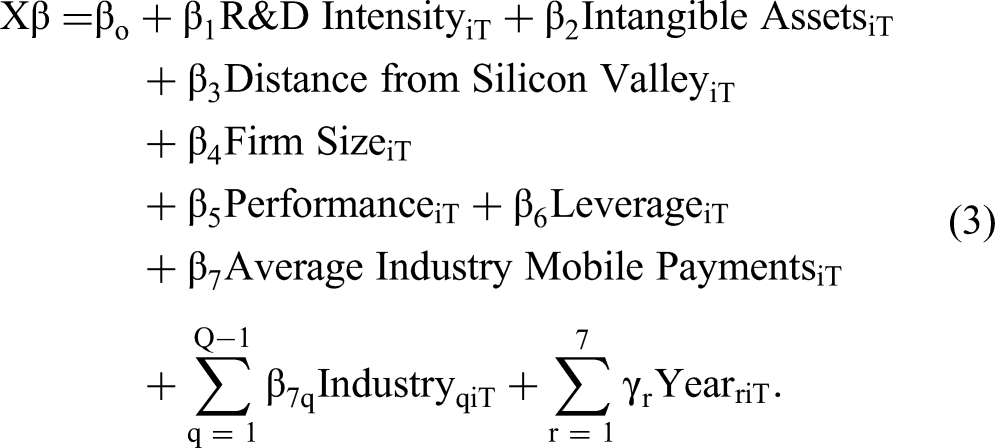

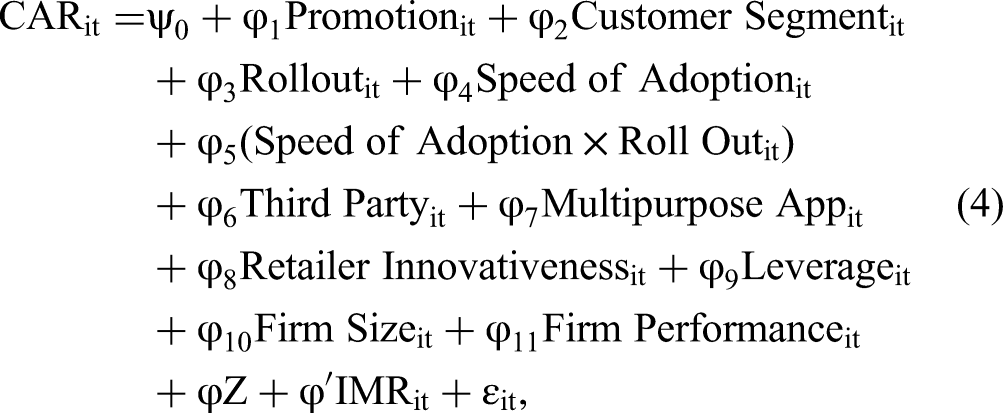

To test our first hypothesis (H1), we examine the CARs that retailers accrued from launching mobile payments, and to test H2 to H4, we then regress these CARs on our hypothesized explanatory variables and control variables. However, because the retailers in our sample all chose to adopt mobile payments, there may be systematic differences between retailers that launched mobile payments and those that did not. This type of self-selection could cause endogeneity in our model, biasing our results. To remedy this potential issue, we employ Heckman's (1979) two-stage correction approach. In the first stage of the model, we estimate a probit model in which the response variable is the retailer's decision to adopt mobile payments (a dummy equal to 1 if the retailer launched mobile payments in year

In the first stage, as explanatory variables we include factors that influence the retailer's decision to adopt mobile payments. Specifically, we include research and development (R&D) intensity; the retailer's intangible asset emphasis; the distance of the retailer's headquarters from Silicon Valley, California; the average industry mobile payment activity; and control variables for leverage, retailer size, and retailer performance. We include R&D intensity, the ratio of R&D to sales, to serve as a proxy for innovation (Daughety and Reinganum 1995; Mizik and Jacobson 2003). Prior work shows that innovative retailers are more likely to introduce innovative in-store technologies (Dotzel and Shankar 2019; Lamey et al. 2021), which suggests that they are more likely to launch mobile payments. As was done in the study by Boyd, Kannan and Slotegraaf (2019), we include the retailer's intangible asset emphasis (1 minus property, plant, and equipment, divided by total assets), as a retailer's intangible investments are likely to impact its decision to launch mobile apps. Existing research (e.g., Gagliardi and Iammarino 2018; Gordon and McCann 2005; Jo and Lee 2014) also finds that when it comes to technological innovations, geographical proximity not only allows retailers to develop strong social networks, which facilitates reciprocal exchanges of tacit knowledge, but also promotes the generation and diffusion of innovative technology. Retailers with headquarters in close geographical proximity to mobile payment technology platforms may be more likely to collaborate with mobile payment platforms, making them more likely to adopt novel payment technologies. Many mobile payment technology firms are headquartered in Silicon Valley, California. 2 Thus, to control for this proximity-based influence, we include a variable measuring the distance between the county where a retailer's headquarters is located and Santa Clara County, California, where many mobile payment technology companies are headquartered.

Similar to prior work (e.g., Bhagwat, Warren, and Beck 2020; Germann, Ebbes, and Grewal 2015; Srinivasan, Wuyts, and Mallapragada 2018), our model includes the average industry mobile payment activity. We operationalize this variable by dividing the number of retailers in an industry (i.e., retailers with the same four-digit Standard Industrial Classification codes) that launched mobile payments each year by the total number of retailers in the same industry that did not launch mobile payments. This variable, which facilitates identification, also meets relevance and exclusion restrictions in that it is reasonable to assume that retailers in the same industry generally tend to imitate each other's marketing strategies; thus, when their competitors launch mobile payments, the remaining retailers in the industry will likely follow suit (Haleblian, Kim, and Rajagopalan 2006; McNamara, Haleblian, and Dykes 2008). Furthermore, we provide statistical evidence that the average industry mobile payment activity meets the exclusion restriction. Specifically, following Certo et al. (2016), we evaluate the correlations between the IMR and our explanatory variables, which reveal weak correlations between the IMR and our variables of interest: promotion

Operationalization of Selection Equation Variables.

Probability of a Retailer Adopting Mobile Payments in Year T.

*p < .10.

**p < .05.

***p < .01.

Notes: Year and industry dummies are omitted due to space considerations. To reduce the effects of selection bias, the determinants of mobile payments acceptance were considered. The results represent the probability of a firm announcing a mobile payments app in year T.

We estimate our first-stage probit model for retailer

Results

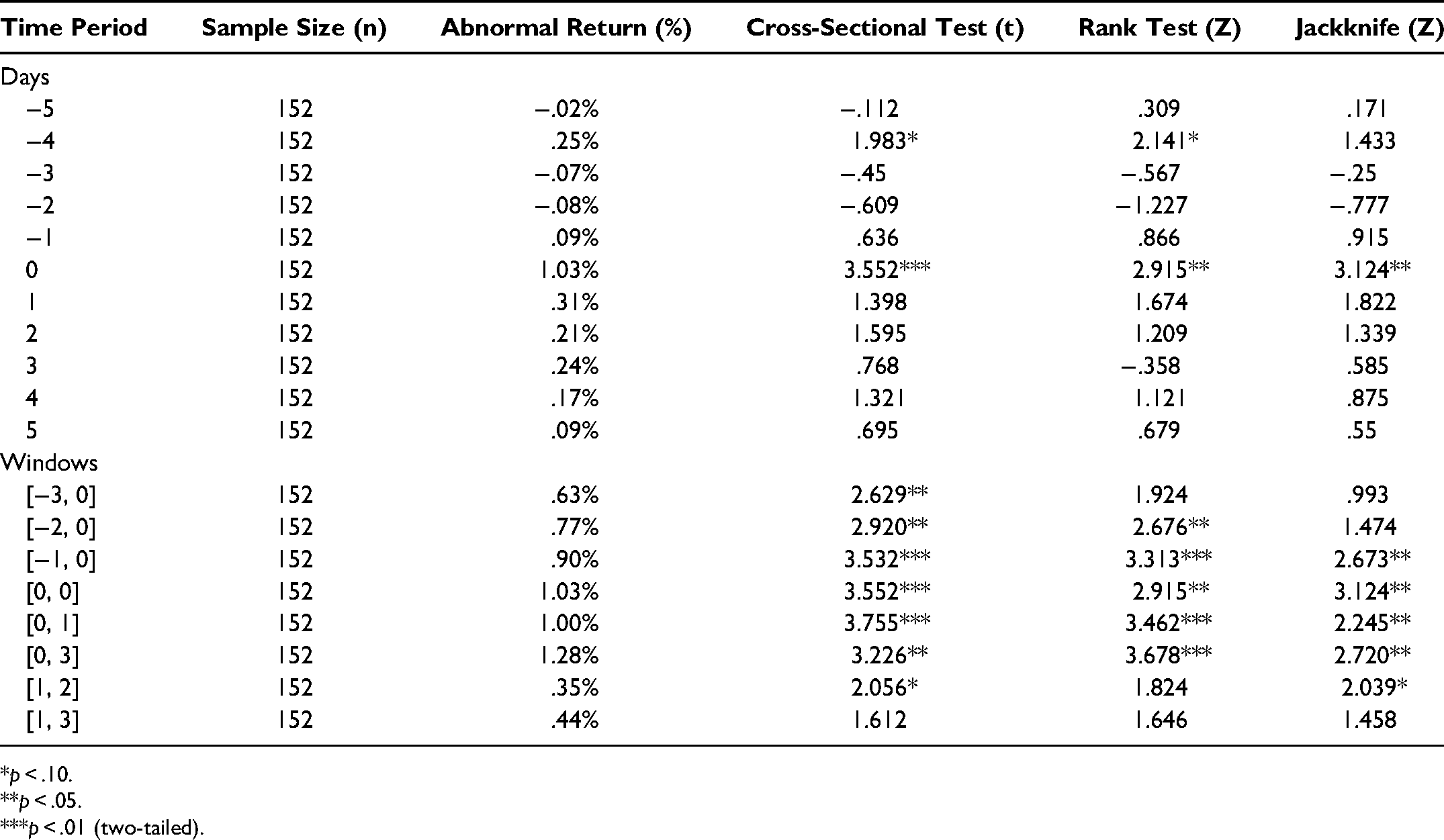

The average abnormal returns of the 152 mobile payment announcements on the day of the announcement and the five days before and after the announcement are presented in Table 5. Across three tests—a cross-sectional error t-test (Brown and Warner 1985), a nonparametric rank test (Corrado 1989), and a jackknife test (Giaccotto and Sfiridis 1996)—and consistent with H1, we find that mobile payments announcements generate significant positive abnormal returns of 1.03% (

Table 7 displays the cumulative average abnormal returns for several windows surrounding the event day. Of all the windows examined, we find that there are no significant cumulative effects after the third day, which indicates a quick correction in firm value after mobile payment announcements. The short event window with significant effects and the lack of significant cumulative effects following the three-day period agree with the assumed efficiency of the stock market (Fama 1970). To test H2–H4, we regress the abnormal returns from the most significant event window, [0, 0], on our explanatory and control variables (Boyd, Chandy, and Cunha 2010; Boyd, Kannan, and Slotegraaf 2019).

Abnormal Returns for Days and Windows Surrounding Mobile Payment Announcements.

*p < .10.

**p < .05.

***p < .01 (two-tailed).

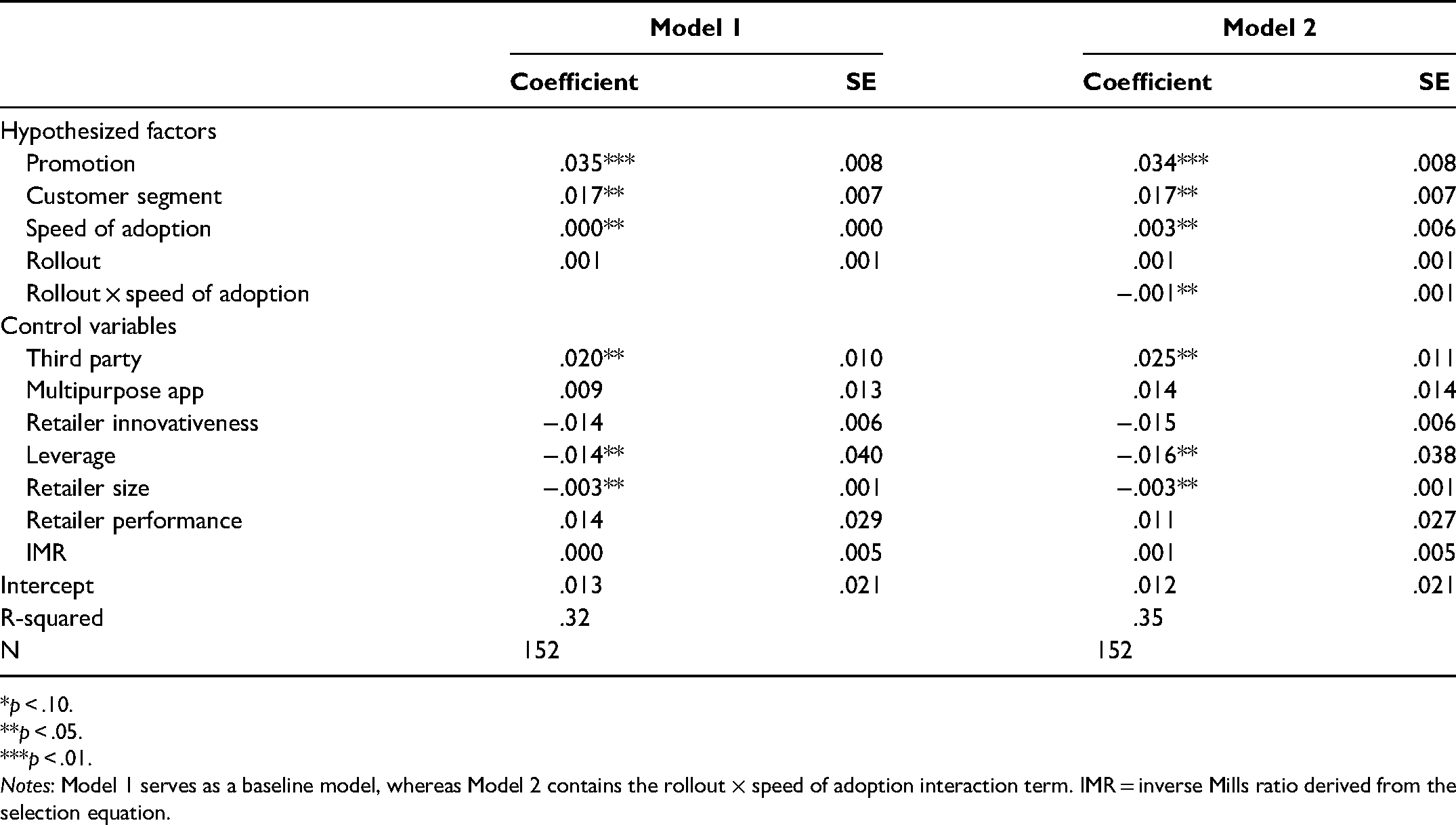

The results in Table 8 show that, in support of H2, there is a significant positive relationship between promotion and abnormal returns,

Cross-Sectional Regression Results.

*p < .10.

**p < .05.

***p < .01.

Notes: Model 1 serves as a baseline model, whereas Model 2 contains the rollout × speed of adoption interaction term. IMR = inverse Mills ratio derived from the selection equation.

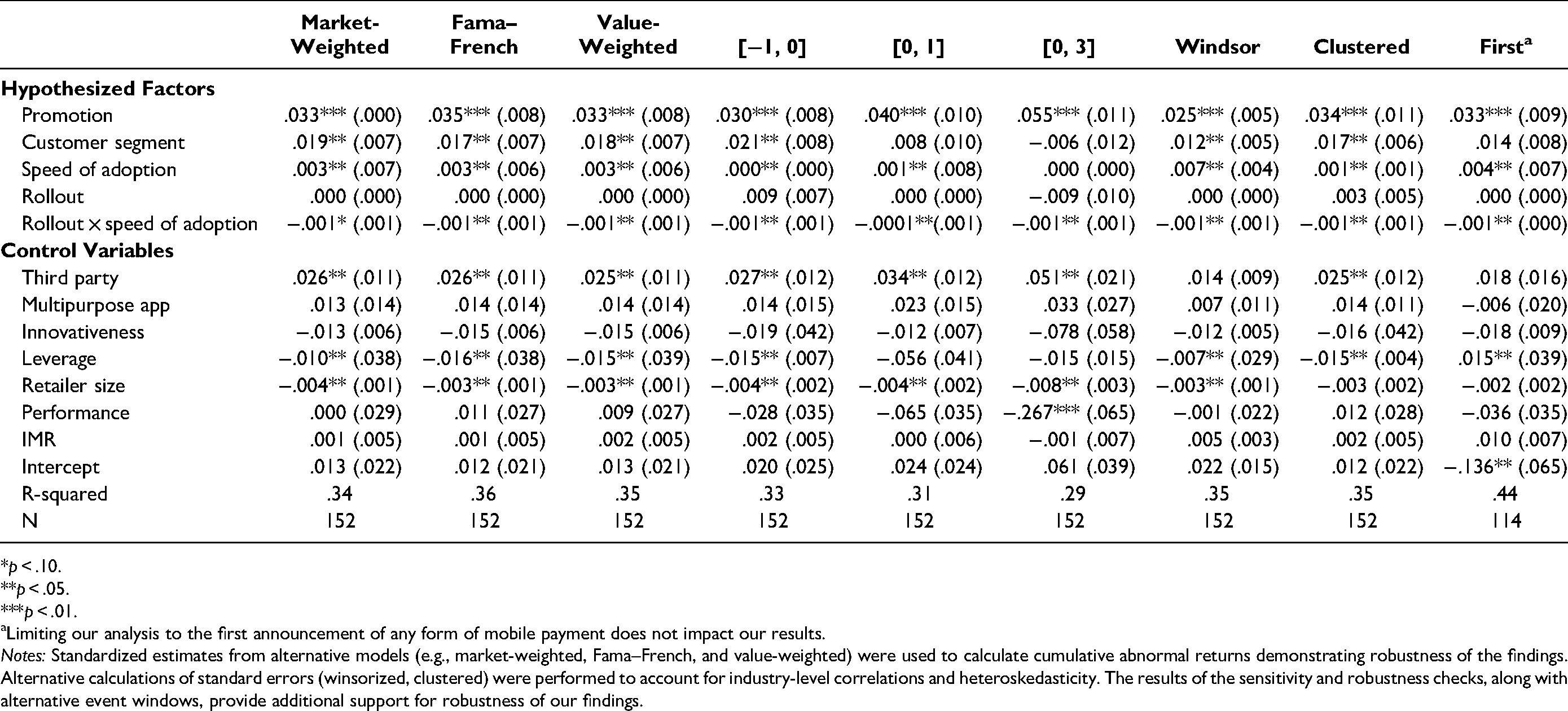

To verify the robustness of our results, we conduct a series of sensitivity assessments. First, similar to event studies in the marketing literature (e.g., Pasirayi and Fennell 2021), we examine the robustness of our results to expected return models. Namely, we utilize abnormal returns obtained from the estimation of the market model and the Fama–French three-factor model (Fama and French 1993), and our results remain unaffected. Our results are also persistent when we use a value-weighted index to compute abnormal returns. Second, we test the sensitivity of our results to other event windows. Specifically, we examine the robustness of our results using the following windows: CAR

Robustness Tests.

*p < .10.

**p < .05.

***p < .01.

Limiting our analysis to the first announcement of any form of mobile payment does not impact our results.

Notes: Standardized estimates from alternative models (e.g., market-weighted, Fama–French, and value-weighted) were used to calculate cumulative abnormal returns demonstrating robustness of the findings. Alternative calculations of standard errors (winsorized, clustered) were performed to account for industry-level correlations and heteroskedasticity. The results of the sensitivity and robustness checks, along with alternative event windows, provide additional support for robustness of our findings.

General Discussion

Our results reveal that investors reward retailers that adopt mobile payments. Specifically, we find that adopting mobile payments increases firm value by an average of 1.03%, indicating that there are efficiencies derived from the strategy. In addition, we highlight that increases in firm value are significantly greater than those of mobile app additions (.34%; Boyd, Kannan, and Slotegraaf 2019; Cao, Liu, and Cao 2018), and internet channel additions (.71%; Cheng et al. 2007; Geyskens, Gielens, and Dekimpe 2002), stressing the value this technology offers retailers. Although we find that most of the retailers in our sample obtained positive abnormal returns after adopting mobile payments, there was considerable variation in the returns obtained by retailers. For example, in comparison with Office Depot, whose firm value rose by 3.31% after adopting Apple Pay, Rite Aid's firm value increased by only .04%. This finding raises a crucial question as to the circumstances that could lead to an increase in the firm value of retailers when they choose to adopt mobile payments, and our study responds to this question.

We find that firm value improves when retailers use promotions to incentivize customers to adopt mobile payments. Promotional efforts likely increase the adoption rates of mobile payment apps, and because customers who use mobile payments have higher willingness to pay, have a favorable brand image of the retailer, and generally spend more per shopping trip (Dorotic and Pauwels 2020; Falk et al. 2016; Fennell et al. 2022; Liu and Mattila 2019), this likely increases retailers’ cash flows and subsequently their firm value. Our results also show that mobile payments generate more positive stock market reactions for retailers that target younger customers as opposed to those that target older customers. A possible explanation for this result is that younger customers are less risk averse and are more likely to adopt mobile payment technology. This suggests that retailers targeting younger customers are more inclined to realize the benefits linked to mobile payments. This finding is consistent with studies showing that younger customers not only are the largest users of mobile technology but also benefit the most from its use (Shankar et al. 2016; Wang, Krishnamurthi, and Malthouse 2015).

Our study also highlights first-mover advantages associated with mobile payment technology adoption. However, these benefits are more pronounced for retailers that enter the market using an expansive mobile payment rollout strategy (i.e., national rollout) as opposed to those that use a more conservative, phased rollout strategy. An expansive, pioneering rollout strategy not only allows a retailer to increase its demand by capturing the early adopters of mobile payments but also endows the retailer with a position of technological leadership in the industry. In principle, this leadership should aid in establishing the retailer as the industry archetype, a position that is shown to increase market share (Kerin, Varadarajan, and Peterson 1992; Lieberman and Montgomery 1988). More generally, our study highlights that novel mobile payment methods increase firm value.

Academic Contributions

The results from this study add to the marketing literature in a few notable ways. Although mobile payment research is sweeping, studies investigating the viability and evaluating the appeal of this approach for retailers are limited. Our study is the first to highlight that in a retail environment, mobile payments augment firm value. From this standpoint, we empirically confirm that mobile payments are a sound strategy for most retailers. This study is also the first to highlight the relationship between promotional incentives and mobile payment adoption, an area that is not addressed in previous work. Although the adoption literature shows that retailers can use several methods (e.g., telemarketing, direct mail marketing, billboards, TV and radio advertising, personal selling, public relations) to increase the adoption rates of new technology (Kalish 1985; Prins and Verhoef 2007), it does not consider the role of promotional incentives or how they can be used to improve adoption rates of new shopper-facing retail technology. Taken together, the findings from our study make a significant contribution to the existing research, which only considers the link between mobile payments and attitudinal behaviors (e.g., Falk et al. 2016; Liu and Mattila 2019; Zhang and Mao 2020), failing to explore how mobile payments impact objective measures such as firm value.

Managerial Implications

This study provides meaningful managerial implications. Overall, our findings suggest that, if it is financially feasible, retail managers should integrate mobile payments into their point-of-sale systems. From a broader perspective, we also highlight the benefits of novel mobile payment methods, implying that managers should look for opportunities to quickly embrace them as they become available. Our study also backs the use of promotions to incentivize mobile payment adoption by retail managers. This is because in a broader sense, promotions increase customer curiosity, which in turn increases customer interest in novel innovations, ultimately increasing their adoption rates, which may also have an added advantage of enhancing customer engagement (Harmeling et al. 2017).

Considering customer engagement, we also find that mobile payments are valued by investors of retailers targeting younger customers. We encourage managers of these types of retailers to actively adopt mobile payments. When evaluating the cost–benefit trade-off associated with the acquisition of mobile payment technology, practitioners should evaluate their expected returns in light of their customer base. Lastly, this study also reveals first-mover advantages tied to adopting mobile payments. However, for retailer managers to take full advantage of adopting mobile payments early, our study points out that they should use an expansive rollout strategy. In fact, we show that for retailers that adopt mobile payments late, the rollout strategy employed does not impact firm value. This finding implies that when retailers adopt mobile payments, they should not only do it rapidly but should also use an expansive rollout strategy. However, practitioners should carefully evaluate the cost–benefit trade-off associated with this inherently riskier approach to determine the optimal decision for their firm.

Limitations and Future Research

Like nearly all research, our study has shortcomings despite its contribution to the existing literature. The primary drawback results from its reliance on stock returns data to test our hypotheses, restricting our sample to publicly traded retailers. Many retailers that have adopted mobile payments are private retailers (e.g., Poshmark, J.Crew, Boxed, Seamless); thus, future research could investigate whether private retailers receive the same benefits as publicly traded retailers. The results of our event study suggest that, at least in the short run, adopting new technology can improve firm value. Beyond the short window of our event study, future investigations could measure firm value more longitudinally.

Another limitation of this study is that, due to limited data, we measure promotion using a binary variable that categorizes promotional activities (e.g., prizes, gift cards, free products, coupons, discounts, redeemable reward points) together without considering the distinctiveness of each program, suggesting that additional research in this area could prove fruitful. For example, research could examine whether certain features, or even the number of features, of a promotion could also lead to unique effects for the firm. In addition, because we concentrate on firm value, our work does not reveal how adopting mobile payments impacts other measures such as customer retention or sales, which may affect their outcome. Future research may also consider examining how customer buying behavior changes (i.e., items purchased, basket size) after the adoption of mobile payments by the retailer. Lastly, future researchers could also explore the fit between the firm and technology adoption (Fennell et al. 2022). For example, retailers like Best Buy predominantly sell tech products, whereas a grocer like Kroger does not. Given the technology associated with mobile payment at the register, differences may exist in the market reaction between such retailers based on the type of products sold.

Footnotes

Editor

Arvind Rangaswamy

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.