Abstract

Homecare workers joined the “Fight for $15” in Boston, Massachusetts on September 4, 2014.

©2014 Marilyn Humphries

Several years ago, I participated in a hearing before a Humboldt, California “fact-finding” commission convened to determine whether the county had bargained unfairly when it refused to give a seventy-five-cent raise to home care workers who were earning $7.75 per hour. A county legislator argued, “These jobs aren’t really jobs and these women aren’t really workers, they are just providing companionship and they are just working for pin money.”

Since the Fair Labor Standards Act was passed in 1938, lawmakers and interested parties have repeatedly argued that home care is not a vocation to justify exempting home care workers from the minimum wage and overtime protections of the Fair Labor Standards Act (FLSA), even as all the other occupations originally excluded from the Act have been covered. 1 In 2011, the Department of Labor began a rule-making process, intended to overturn the so-called “companionship exemption,” which resulted in a new “home care rule,” which would have, for the first time, brought home care workers under the wage and hours protections of the FLSA. In a three-week period immediately prior to and following January 1, 2015, when the new rule was scheduled to take effect, a Federal Court judge gutted two provisions of the new rule, including one that would have required third-party employers—home care agencies and public entities linked to state or county social services—to pay minimum wage and overtime and another that would have sufficiently narrowed the definition of “companionship” to exclude most home care workers from the exemption. 2 This, despite evidence that home care is one of the fastest growing occupations and the highly profitable home care industry is among the fasting growing industries in the country.

The Labor Department’s efforts to recognize home care as a significant and growing occupation, deserving of recognition, is but one front in the effort to bring justice and equity to these “invisible” workers. Over the past twenty-five years, the SEIU, AFSCME, and other unions and affiliates have mounted successful campaigns, especially among the roughly one million home care workers employed through public programs, to raise wages and provide health insurance benefits. That has landed home care right at the front of the right-to-work campaigns now sweeping through the legislatures of Midwestern states. Andy Stern, past president of the SEIU argued, speaking of the mid-1990s home care organizing campaigns, The victory for Los Angeles home care workers, in a campaign named “Invisible No More,” was the largest union election in modern labor history. It started a wave that transformed hard-working independent contractors (in home care and then in child care) into an organized, collective voice for quality care and by offering a union pathway to good jobs. Harris v. Quinn constitutes the Supreme Court’s undercutting of these workers’ strength, by prohibiting agency fee/fair share arrangements for home care and child care workers and by foreshadowing an extension of this union-eroding precedent into the entire public sector.

3

Among the conservative forces fighting to impede regulatory reform and union successes in home care is the newest and most rapidly expanding sector of the home care industry, for-profit and private pay home care franchises. Plaintiffs in the case brought against the Department of Labor (DOL) to strike down the home care rule included the International Franchise Association (IFA), the Home Care Association of America (HCAOA), and the National Association for Home Care & Hospice (NAHC).

This article provides a brief overview of the industry to show that home care is no longer a marginal service provided by friends, neighbors, and families, mainly for free but occasionally for pin money. Rather, it is a highly profitable, rapidly expanding industry.

The Hodgepodge Structure of Home Care

The past forty years have seen a spectacular transformation in the Long-Term Services and Supports industry that cares for elderly persons and persons with disabilities. Before the mid-1970s, most people who needed significant levels of support were housed in nursing homes, mental hospitals, and state institutions for persons with developmental and intellectual disabilities. Since that time, changes in federal Medicaid policies, driven by fiscal pressures as the proportion of the population needing care grows, have combined with cultural and legal shifts to favor deinstitutionalization and aging in place.

Home care, as measured by employment and number of persons served, is the largest component of the long-term services and supports industry. The industry is almost entirely the creature of federal and state policies, since about 80 percent of paid services are supported by public funds, especially Medicaid, the state-federal means-tested aid program that provides medical assistance to low-income people. 4

The nursing home industry, as we know it, began with Medicaid’s inception in 1965 and the requirement that state Medicaid plans provide institutional long-term care and home health care to be eligible for federal matching funds. Medicare funds much of home health, but Medicaid is the principal source of payments for institutional long-term care. Two amendments to Medicaid in 1975 and 1981 that gave states the option to meet their long-term care obligations in a non-institutional setting laid the conditions for the beginnings of the home care industry. Approximately two-thirds of the elderly and persons with disabilities who are getting paid long-term care now receive it through home- and community-based services, including group homes, adult day service centers, and in private homes. 5

These policy changes spawned whole new industries, including home health and home care agencies, adult day services, and large public programs that paid for consumer-directed home care.

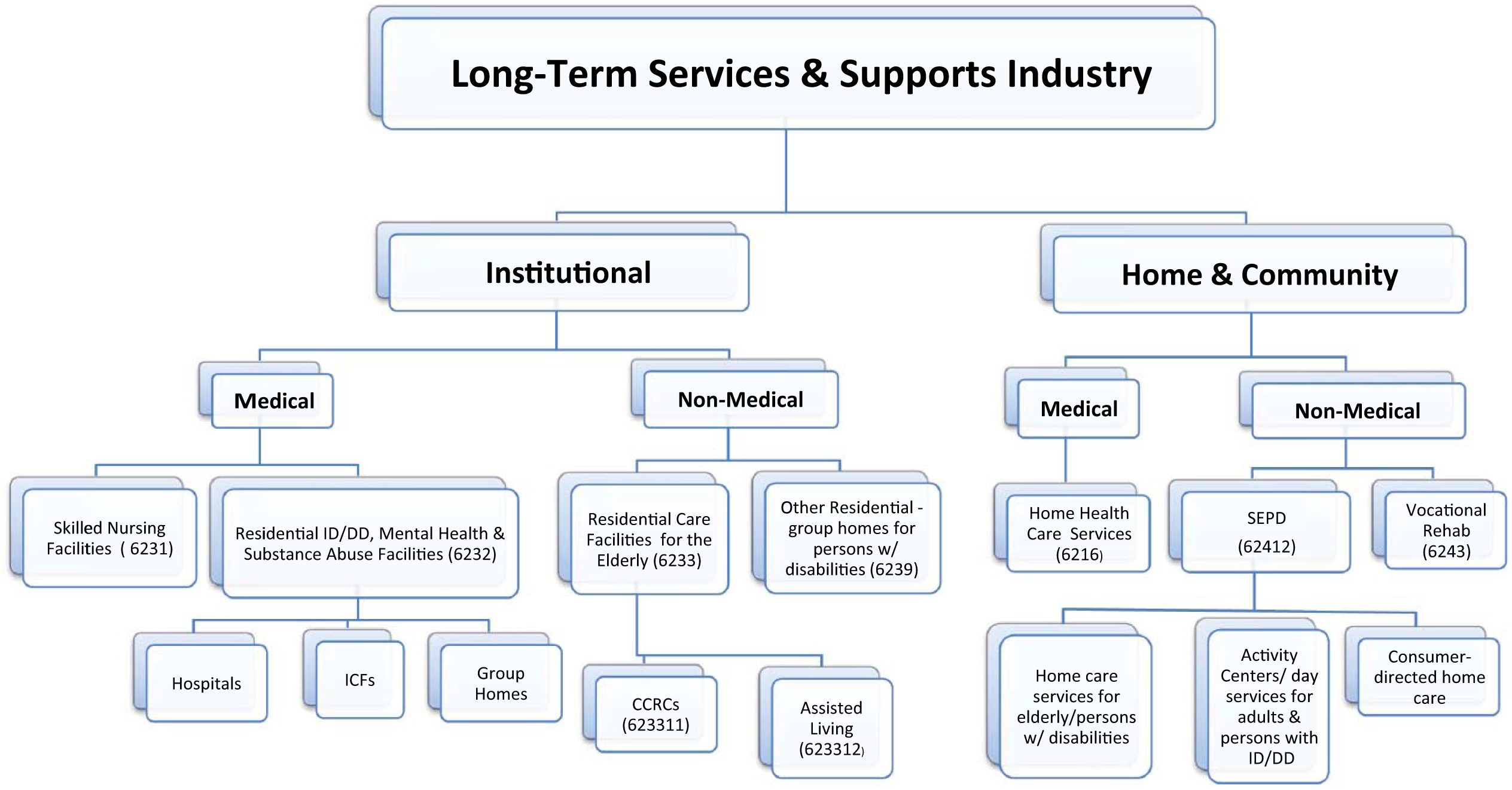

The Long-Term Services and Supports industry is now comprised of six industries that I categorize along two dimensions—whether they provide institutional or non-institutional care and whether they provide medical- or non-medical-based care services (Figure 1; LTSSI organizational chart). The Long-Term Services and Supports industries generated $318 billion in revenue in 2012; about $1 billion was in non-residential care. 6

The long-term services and supports industry. CCRCs = Continuing Care Retirement Communities; ID/DD = intellectual disability/developmental disability; ICFs = intermediate care facilities; SEPD = Services for the Elderly and Persons with Disabilities.

Two main sectors make up the home care industry: Home Health Care Services and Services for the Elderly and Persons with Disabilities. Firms in the Home Health Care Services industry (HHCS) are licensed (by states) to provide home-based medical care, including skilled nursing services; most also provide extensive non-medical services such as physical, speech, and occupational therapy; personal care assistance; and homemaker and companionship services.

Home care companies, which technically provide only non-medical personal care services and housekeeping and companionship services, are the heart of the Services for the Elderly and Persons with Disabilities (SEPD) industry, which also includes adult day services. Just as home health care agencies cross the boundary into non-medical services, home care agencies are expanding into medical services.

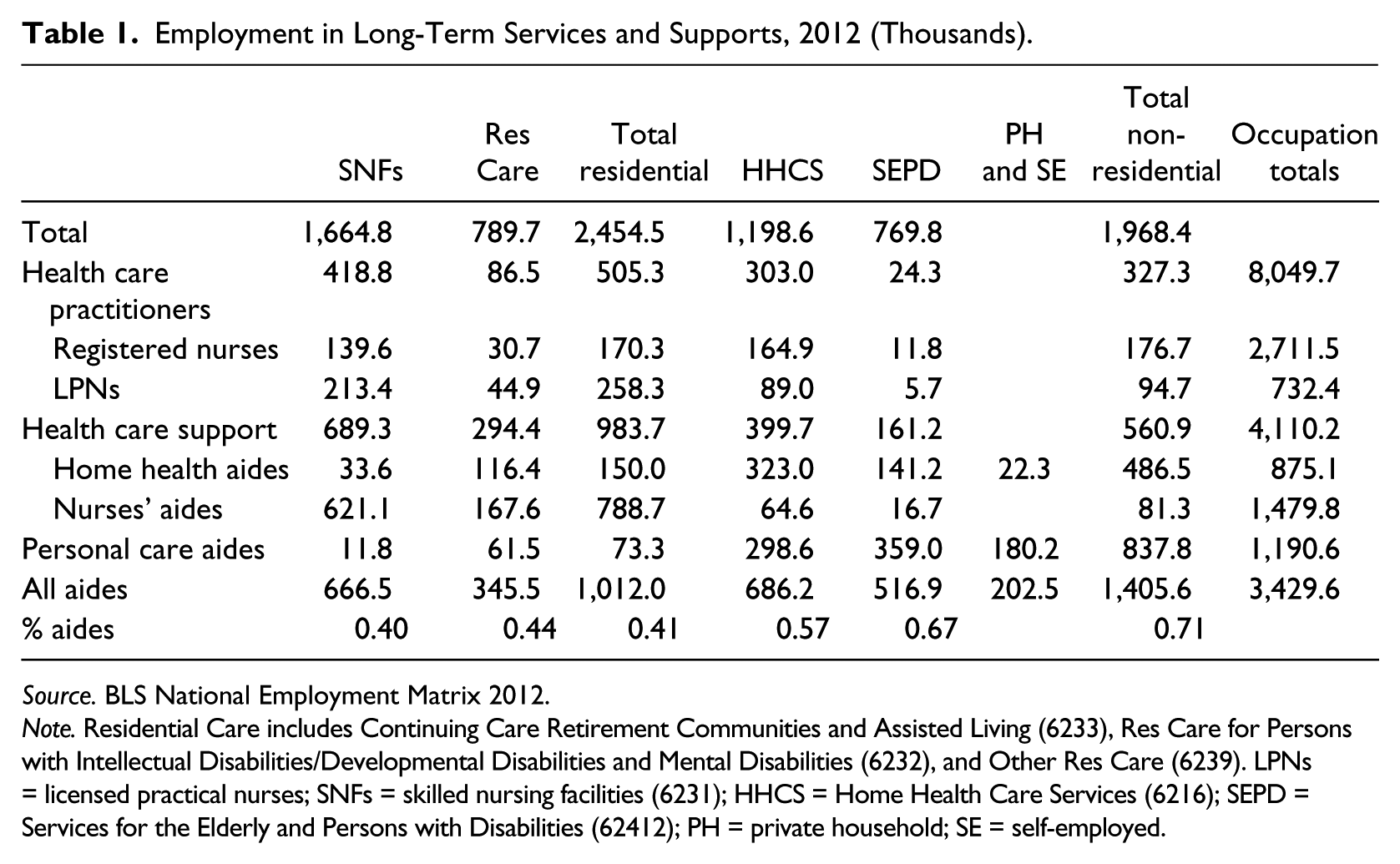

Most home health care aides and personal care assistants work for home health and home care agencies, but many also work in Continuing Care Retirement Communities, Assisted Living facilities, and group homes. Many personal care assistants also work as “independent providers” outside the agency model, either in publicly funded, consumer-directed programs, or directly for private pay consumers (see Table 1).

Employment in Long-Term Services and Supports, 2012 (Thousands).

Source. BLS National Employment Matrix 2012.

Note. Residential Care includes Continuing Care Retirement Communities and Assisted Living (6233), Res Care for Persons with Intellectual Disabilities/Developmental Disabilities and Mental Disabilities (6232), and Other Res Care (6239). LPNs = licensed practical nurses; SNFs = skilled nursing facilities (6231); HHCS = Home Health Care Services (6216); SEPD = Services for the Elderly and Persons with Disabilities (62412); PH = private household; SE = self-employed.

Agencies can be further distinguished by whether or not they are certified by Medicare and/or Medicaid or licensed by the state, by whether they are public, private for-profit, or private not-for-profit. Related to these distinctions is whether their revenue originates primarily from public or private sources. Although some home care agencies, especially in the Franchise sector, try to specialize in private pay consumers, it seems that most rely on reimbursements from Medicaid.

Medicare- and Medicaid-certified home health care companies make up the formal sector of the fast-growing home health/home care sector. These firms are commonly known as home health agencies and visiting nurses associations. In 2009, 87 percent of the industry’s agencies were freestanding; the remainder was attached to hospitals, rehabilitation facilities, and skilled nursing facilities. Among the freestanding agencies—which also included Visiting Nurses Associations—and other voluntary, public, and not-for-profit agencies, 62 percent were private for-profit, including a growing presence of chains. In 2012, there were 12,200 Medicare-certified home health care agencies. Less than twenty years earlier, in 1990, there were fewer than 5,700 agencies, and only 33 percent were private for-profit. Virtually all of home health services growth has been driven by proprietary hospitals and freestanding private for-profit agencies. 7

Within the SEPD industry, some certified or licensed and many non-certified agencies provide mainly non-medical services, though many agencies have started to add services such as skilled nursing, which will qualify them for Medicare certification. Slightly more than four thousand agencies make up the adult day services component of the SEPD industry. There is a much larger public and non-profit presence in adult day services than in home health services. 8

The number of establishments in the SEPD sector has grown sevenfold in less than a decade. 9 Industry sources claim that private pay agencies make up a substantial share of the industry, while the Wages & Hours Division finds little evidence that private pay agencies comprise more than a small fraction of the total industry. 10 The dispute is important because the industry claims the home care rule will raise costs substantially and drive the private pay agencies out of business. Approximately two-thirds of private home care agencies are for-profit. 11

Franchises, which have grown rapidly just in the last few years but particularly since 2008, are largely concentrated in the for-profit sector. The nature of the services provided focus mainly on non-medical services. 12 A single office of a “senior care” franchise, as they are called in the industry, requires an investment of less than $150,000 and as little as $50,000; Forbes reports that the median franchise revenue is now $2 million; gross margins of 30 to 40 percent are common. When compared to the slim margins and the $500,000 average initial investment for food and retail franchises, it is not surprising that Forbes includes three home care brands among its top ten franchises for investments under $150,000. Today, there are fifty-six franchise brands, up from thirteen, in 2000. Sixty-five percent of individuals who start franchises are over forty-five years of age, 86 percent are Caucasian, and 74 percent are females with a BA, similar to the demographics of real estate agents and brokers. Seventy-six percent started their business in the last five years, and 85 percent entered after looking for home care for a relative. 13

Revenue in the home care industries has more than doubled since 2001, with growth in the for-profit firms far out-stripping the not-for-profit segment of the industries.

Consumer-Directed Home Care Services

Most states now either allow or require that some form of consumer-directed publicly funded home care be offered through their Medicaid program. 14 Under this model, individuals choose their own providers, including family members or friends. The client may either pay the provider directly, using cash support from Medicaid, or the provider is paid by the state or an intermediary, such as a “public authority.”

By far, the largest consumer-directed program is California’s In-Home Supportive Services (IHSS), in which nearly 425,000 consumers are cared for by roughly 400,000 in-home workers. 15 Under a unique arrangement devised in 1992 to create the IHSS Public Authorities that would serve as the “employer of record,” the model allowed home care workers to be reclassified from “independent contractor” to “employee” status, to be covered by the National Labor Relations Act (NLRA), to join a union and engage in collective bargaining. 16

Within the SEPD industry, it is in the consumer-directed, publicly funded home care programs that unions have had their greatest successes. The vast territory of home care companies, especially in the franchise sector, are largely untouched. For that reason, despite rapid growth in the SEPD industry, wages and conditions of work have not improved. In nominal terms, average annual employee income has grown from $17,100 to $18,900, since 2001; in real terms, that represents a 15 percent decline. 17

Virtually all the growth in the Long-Term Services and Supports industry is in home and community-based services that are increasingly being dominated by the fast-growing for-profit home care agency industry where franchises are making substantial inroads. In contrast to nurses’ aides in hospitals and nursing homes, who are doing essentially the same jobs, home care workers employed by these agencies and by public entities are not covered under the FLSA, or in most cases by the NLRA, making it unlawful for them to join unions and denying them the right to minimum wage and overtime protection.

As the declining real incomes in the SEPD industry suggest, home care workers have had little success in improving their conditions of employment. The notable exception has been in states like California where unions were able to organize consumer-directed home care workers in Medicaid-funded home care programs.

Collective bargaining in Medicaid-funded home care programs is a good first strategy. In fact, home care workers’ wages have increased only where there is collective bargaining or local minimum or living wage ordinances, or both, as in San Francisco. An advantage to targeting workers in these programs is that, with the state paying the worker directly, consumers are not price sensitive. In counties, or states, where consumer-directed care is a very large proportion of long-term care, wage increases in the public programs can have a significant impact on wages in the private sector.

The same does not hold true in areas where publicly funded home care services are provided by agencies that are usually reimbursed on a per-visit or hourly basis but have considerable discretion to set wages. The agency has an incentive to keep wages and benefits as low as the market can sustain. The incentive structure created by reimbursement policies in the absence of unionization explains why wages remain low. It may also explain why much of the resistance to eliminating the companionship exemption came from the for-profit industry.

Consumers and workers have expressed a clear preference for consumer-directed home care as a viable alternative to institutional and agency-based models. And yet industry resistance may be one of the major impediments to expanding the consumer-directed model and raising the floor on wages for home care workers.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.