Abstract

Female entrepreneurship is an important dimension of women’s economic participation in Latin America and may also function as a pathway with implications for health and wellbeing. This study estimates the causal effects of national financial inclusion reforms (2014–2018) on female entrepreneurship using staggered difference-in-differences with Callaway-Sant’Anna estimators across 15 countries. Data from the World Bank, ECLAC, and PAHO span 2014–2021. The empirical analysis does not model health outcomes directly; instead, it tests whether the entrepreneurship effects of financial inclusion reforms vary according to pre-existing gender inequity in health systems, measured through a composite index based on maternal mortality, antenatal care, contraceptive prevalence, and health insurance access. The study therefore contributes primarily to economic policy analysis while drawing on a health-related contextual framework to show how baseline health-system conditions moderate policy effectiveness in promoting female entrepreneurship.

Keywords

Introduction

There is growing attention to female entrepreneurship as a means to increase women’s economic participation in Latin America and its potential to improve health and wellbeing outcomes via the route of earning a steady income, financial protection and household decision-making. Between 2014 and 2018, eight countries in Latin America launched national level financial inclusion reforms, targeting populations outside the formal financial sector for access to basic financial services, credit and financial education. This study adopts an economic policy perspective to examine how social factors, such as baseline gender health inequity, moderate the impact of financial inclusion reforms on sustainable female entrepreneurship in Latin America, without directly modeling health outcomes. Health inequity serves as a contextual moderator explaining variations in entrepreneurial effects, positioning the article as an economic policy analysis informed by gender and social determinants of health theory, rather than a direct evaluation of health services.

To address endogeneity, we employ a quasi-experimental difference-in-differences strategy to estimate the causal effects of the staggered national reforms. This includes a detailed exposition of the methodology, estimator choice, inference strategies, and covariate strategy in the Methods section.

This paper explores whether financial inclusion reforms can increase female entrepreneurship, and whether this effect is higher in countries with lower levels of gender inequity in health at baseline. The analysis uses annual, country-level panel data from the World Bank, ECLAC and PAHO for 15 countries in Latin America from 2014 to 2021. The paper contributes to the growing body of research on the effectiveness of economic policy, especially regarding financial inclusion. It identifies the role that health-systems’ baseline conditions play in enhancing female entrepreneurship.

The paper does not analyze health services’ utilization or health outcomes. Instead, it employs the concept of inequity in health systems as a contextual dimension which helps to explain the different entrepreneurial effects of financial inclusion policies in different countries.

Literature Review

Theoretical Framework and Empirical Evidence

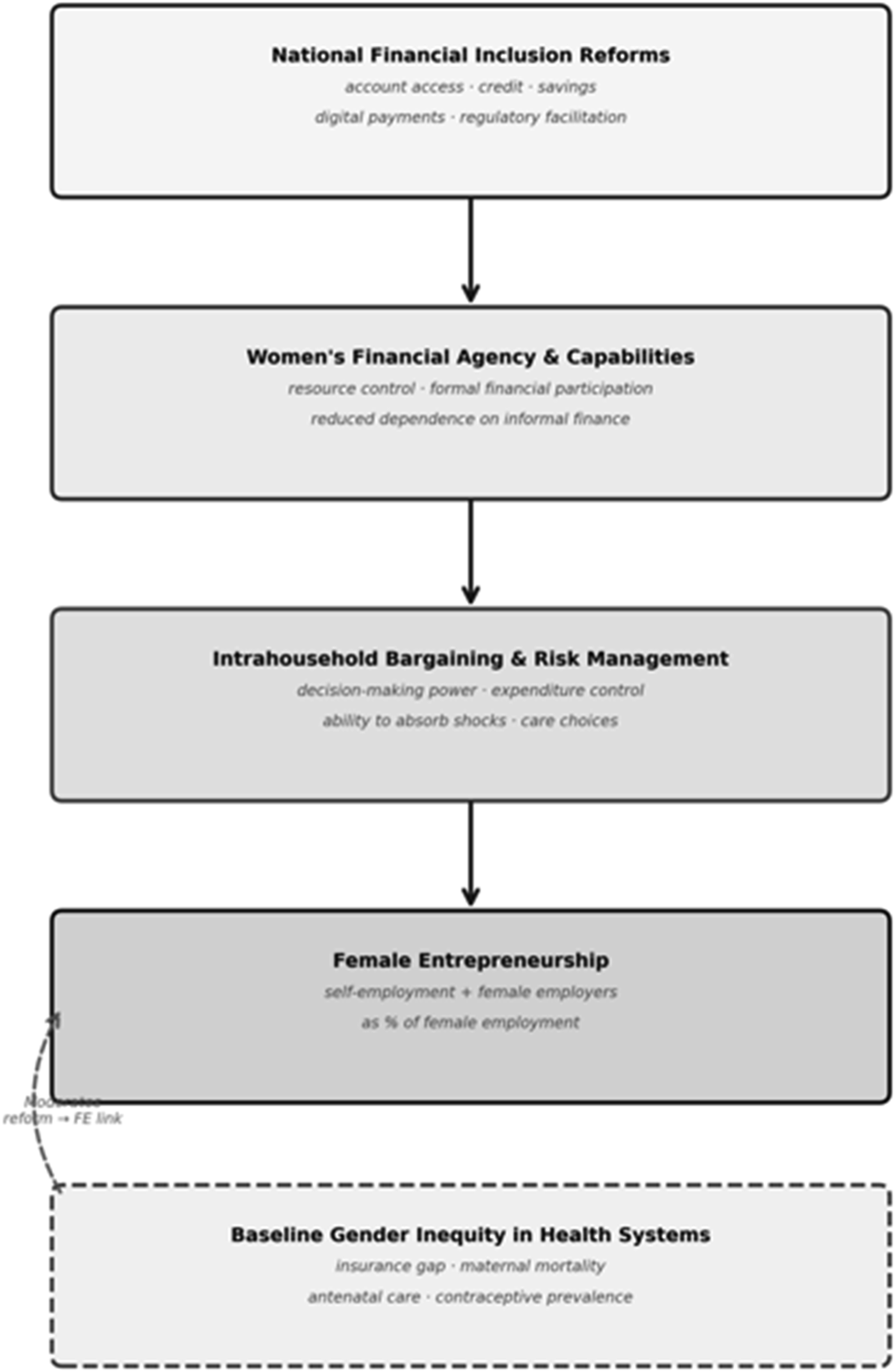

Financial inclusion reforms can be conceptualized as institutional interventions that connect three complementary theoretical perspectives rather than operating through a single economic mechanism. From a gender and development perspective, access to accounts, savings instruments, insurance, and formal credit expands women’s capabilities by increasing their command over economic resources and reducing dependence on informal financial arrangements.1,2 From a feminist economics perspective, these reforms also reshape intrahousehold bargaining, time allocation, exposure to care burdens, and control over expenditure decisions, including decisions related to health spending and risk management. 2 From a social determinants of health perspective, the capacity to transform financial access into sustained entrepreneurial activity depends on the broader institutional conditions that shape women’s health security, reproductive autonomy, insurance coverage, and exposure to catastrophic expenditure. The integrated framework used in this study therefore treats financial inclusion reform as the policy intervention, women’s financial agency and bargaining power as intermediate mechanisms, female entrepreneurship as the main empirical outcome, and baseline gender inequity in health systems as a contextual moderator of policy effectiveness. The article should thus be read primarily as an economic policy study informed by gender and health-systems theory, rather than as a direct evaluation of health services or health outcomes. While microfinance studies report heterogeneous and often modest effects on business creation and income, 3 national financial inclusion reforms may generate broader impacts because they modify the regulatory and infrastructural environment within which women make entrepreneurial and health-related decisions.

Figure 1 synthesizes the theoretical framework by integrating gender and development theory, feminist economics, and social determinants of health: financial inclusion reforms expand women’s financial agency, resource control, and risk management—modulated by intrahousehold bargaining and care responsibilities—with baseline health inequity as a contextual moderator (not outcome) influencing the conversion of financial access into sustained entrepreneurship. The relationship between financial inclusion and women’s empowerment is best understood as a multidimensional process linking access to financial resources with agency, autonomy, and strategic life choices.1,2 In gender and development economics, empowerment involves not only participation in markets but also the ability to convert resources into voice, mobility, and decision-making capacity.1,2 Financial inclusion may strengthen women’s empowerment through at least three mechanisms. First, it increases independent access to liquidity, savings, and credit, which can support business formation and reduce dependence on spouses or informal lenders.1,2 Second, it improves women’s bargaining position within the household by increasing their contribution to household income and their control over expenditure decisions, including health spending.1,2 Third, it may expand women’s social and informational networks through formal financial participation, thereby improving knowledge of available services, legal protections, and market opportunities. Existing evidence from Peru, India, and integrated microfinance-health interventions is consistent with these mechanisms, showing that women’s access to financial services can improve preventive care use, maternal health behaviors, and family planning outcomes when financial access is translated into effective agency over health decisions.4-6 Integrated conceptual framework linking financial inclusion reform, Women’s agency, health-system equity, and female entrepreneurship

Informal Sector Dynamics and Female Entrepreneurship in Latin America

Informality is a central feature of labor markets in Latin America and is therefore directly relevant to how female entrepreneurship should be interpreted in this study. A substantial share of women’s income-generating activity in the region takes place outside fully formal employer structures, often through self-employment, household-based production, small-scale commerce, and other own-account activities that may not be registered as formal firms. For this reason, the boundary between entrepreneurship, self-employment, and informal survival activity is often less clear-cut than in settings with higher levels of formal labor market incorporation. Any empirical measure of female entrepreneurship in Latin America must therefore account for the fact that business initiative and labor market informality frequently overlap rather than appear as separate categories.

This contextual feature is particularly important for the interpretation of the dependent variable used in the present study, which combines self-employed women and female employers. In a highly formalized economy, such a measure might be seen as overly broad; in Latin America, however, it captures a more realistic spectrum of women’s entrepreneurial participation. At the same time, this also implies an important interpretive caution: reforms that expand financial access may support opportunity-driven business creation for some women, while for others they may facilitate entry into self-employment under conditions of limited wage employment and persistent informality. The informal sector should therefore be understood not only as a measurement complication, but also as part of the structural environment through which financial inclusion reforms may shape women’s economic strategies. Health system equity conditions the extent to which financial inclusion reforms can produce effective entrepreneurial outcomes for women and therefore serves in this study as a contextual moderator rather than as an outcome variable or as a direct causal mechanism. In social determinants of health theory, access to healthcare, reproductive services, insurance coverage, and protection from catastrophic expenditure are enabling conditions that shape women’s capacity to participate in economic life on stable terms. Where health systems are more equitable, women face lower health-related uncertainty, lower reproductive risk, and fewer interruptions in labor market participation, which increases the probability that access to financial services can be converted into sustained entrepreneurial activity. By contrast, in contexts of high gender inequity in health, the expected returns to entrepreneurship may be reduced by untreated illness, maternal health burdens, weak insurance coverage, and higher out-of-pocket spending, all of which deplete working capital and intensify risk aversion. Importantly, the Gender Inequity in Health Index is best understood as a summary marker of structural disadvantage across multiple health-system dimensions, not as an isolated measure of a single institutional mechanism. Because the index aggregates maternal mortality, antenatal care, contraceptive prevalence, and insurance access, it may also capture variation in broader institutional capacity — including state reach, social policy infrastructure, and administrative effectiveness — that correlates with but is not reducible to health-system inequity per se. The analysis therefore tests whether this pre-existing contextual gradient moderates economic policy effectiveness; it does not claim that health system inequity is the exclusive or mechanistically specific driver of the observed heterogeneity.

A feminist economics reading also requires recognition that women’s entrepreneurship is embedded in unequal care responsibilities and therefore linked to both mental and physical health. Financial inclusion can reduce stress exposure by improving women’s ability to absorb shocks, manage consumption, and avoid predatory borrowing, while entrepreneurship may enhance self-efficacy and perceived control over one’s life trajectory. At the same time, these benefits are contingent rather than automatic, because women often combine productive and reproductive labor under conditions of time poverty. This makes health a constitutive element of entrepreneurial sustainability rather than a downstream by-product. Mental health, in particular, operates as a mechanism through which financial insecurity constrains entrepreneurial action and through which economic autonomy may improve wellbeing. Incorporating this perspective clarifies why female entrepreneurship should be theorized as a social determinant of health: it affects not only income, but also stress regulation, autonomy, care management, and the capacity to seek timely healthcare.

The quasi-experimental evaluation of national financial inclusion reforms requires methodological approaches accounting for staggered policy adoption and treatment effect heterogeneity. Traditional difference-in-differences estimators with two-way fixed effects produce biased estimates when treatment timing varies across units and effects differ by cohort or evolve dynamically.7-9 Recent econometric advances address these limitations through estimators that compare treated units only to valid control groups—those never treated or not yet treated—and aggregate cohort-specific effects using appropriate weights. 10 Implementation requires careful attention to inference procedures, particularly with few geographic clusters where standard asymptotic approximations fail; wild cluster bootstrap methods provide improved coverage properties in these settings. 11 Variable selection must avoid conditioning on potential mediators affected by treatment, as inclusion of such “bad controls” biases estimates of total effects even when those variables predict outcomes. 12 This study applies these methodological innovations to estimate causal effects of financial inclusion reforms on female entrepreneurship while testing heterogeneity by pre-existing health system equity.

Research Methods

Data Sources and Sample Construction

The research employs data from three global multilateral organizations: the World Bank Group, the Economic Commission for Latin America and the Caribbean (ECLAC), and the Pan American Health Organization (PAHO). We use yearly macroeconomic information on 15 countries in Latin America from 2014 to 2021. World Development Indicators provide yearly GDP per capita and related macroeconomic indicators. 13 The Global Findex Database provides financial inclusion indicators at three-year intervals, including account ownership, borrowing, and saving behavior by gender. 14 The Economic Commission for Latin America and the Caribbean, through CEPALSTAT, provides annual labor market information, including the proportion of female self-employed workers, female employment status, educational attainment by gender, and social security affiliation by gender. 15 The Pan American Health Organization provides health-system indicators used in the study, including maternal mortality, antenatal care, and reproductive health measures. 16

We start with 18 countries but exclude three cases because they either had excessive missing Findex information or reform timing outside the main treatment window used in the analysis. Venezuela was excluded because missing Findex data exceeded 20%. Costa Rica was excluded because the relevant reform timing identified for this study occurred in 2017, leaving too little clearly comparable pre-treatment information within the main staggered design. Argentina was excluded because the reform timing identified for this study occurred in 2019, outside the primary treatment window used to define the main reform cohorts. This results in a sample of 8 treated countries—Paraguay, Peru, Honduras, the Dominican Republic, Colombia, Mexico, Ecuador, and El Salvador—and 7 control countries—Bolivia, Guatemala, Nicaragua, Panama, Uruguay, Chile, and Brazil. The primary specification uses the observed Findex years, yielding 45 country-year observations.

Costa Rica and Argentina were therefore not excluded because they were substantively unimportant, but because their inclusion would have weakened temporal comparability in the staggered-adoption design. Including these cases would have introduced additional variation in treatment timing without providing a sufficiently balanced pre-treatment structure relative to the other treated countries. The exclusion of both cases is thus a design choice intended to preserve identification consistency and improve comparability across countries in the main specification.

Variable Construction

The dependent variable measures female entrepreneurship as the sum of self-employed women and female employers expressed as a percentage of total female employment, constructed from CEPALSTAT annual labor force surveys. This broad definition is used because comparable cross-national data on female business activity in Latin America are limited, and because women’s entrepreneurial participation in the region often spans both formal and informal forms of economic organization. At the same time, the measure should be interpreted with caution. Own-account work may reflect heterogeneous realities ranging from opportunity-driven entrepreneurship and small-scale business creation to necessity-driven self-employment adopted in response to labor market exclusion, income instability, or weak social protection. For this reason, the variable is best understood as a broad indicator of female entrepreneurial economic activity rather than a pure measure of high-growth or fully formal entrepreneurship. The inclusion of female employers strengthens this interpretation by capturing women who generate employment for others, while the inclusion of self-employed women reflects the empirical structure of entrepreneurship in Latin America, where firm creation and income-generating initiatives frequently operate outside fully formal employer status. A secondary outcome using only female employers serves as a more restrictive proxy for formal entrepreneurship in robustness checks, though this subgroup represents only 1.5% to 3.5% of female employment and therefore offers more limited statistical power. Treatment status derives from a structured review of central bank documents, legislative records, and Inter-American Development Bank reports to identify countries implementing national financial inclusion reforms between 2014 and 2018.

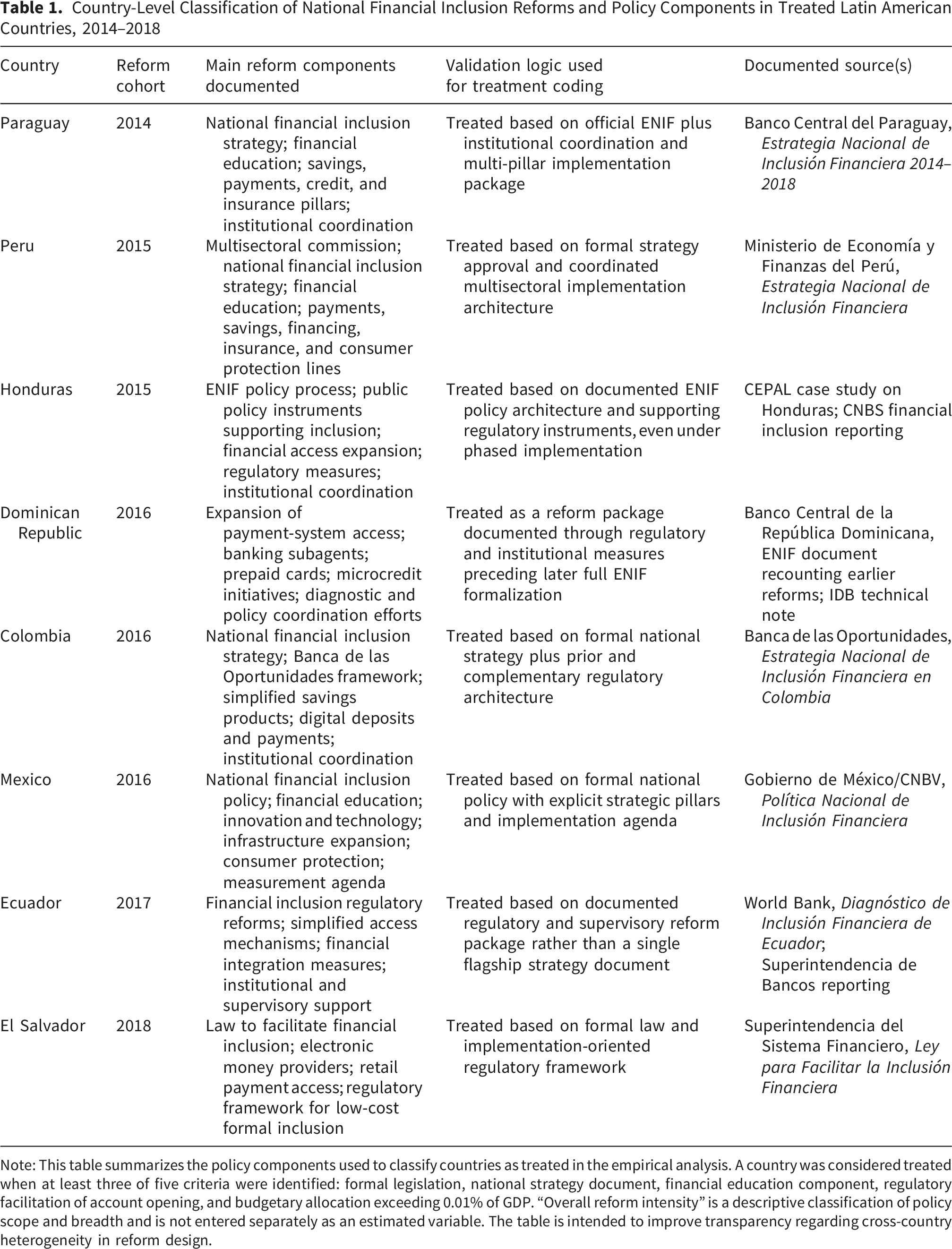

Country-Level Classification of National Financial Inclusion Reforms and Policy Components in Treated Latin American Countries, 2014–2018

Note: This table summarizes the policy components used to classify countries as treated in the empirical analysis. A country was considered treated when at least three of five criteria were identified: formal legislation, national strategy document, financial education component, regulatory facilitation of account opening, and budgetary allocation exceeding 0.01% of GDP. “Overall reform intensity” is a descriptive classification of policy scope and breadth and is not entered separately as an estimated variable. The table is intended to improve transparency regarding cross-country heterogeneity in reform design.

The first component explained approximately 60% of the total variance, which indicates that the four indicators shared a substantial common dimension while still leaving room for country-specific variation not captured by a single latent factor. In reporting the index, the manuscript should make explicit the factor loadings for each indicator and note that all variables loaded in the expected direction after normalization and inversion, so that higher index values consistently reflect greater female disadvantage in health-system conditions. The resulting index was rescaled for interpretive convenience so that higher values indicate greater gender inequity in health, while lower values indicate more equitable baseline health conditions. The index should therefore be interpreted as a relative cross-national measure rather than an absolute substantive threshold: a higher score signals that women in a given country face a more adverse configuration of health-system disadvantages across insurance access, maternal risk, antenatal care, and reproductive health coverage. This design allows the study to evaluate whether baseline health-system inequity conditions the size of the reform effect on female entrepreneurship, but the index should be understood as a summary marker of disadvantage rather than a pure measure of one isolated institutional dimension. That caution is consistent with the paper’s emphasis on pre-treatment moderation and careful variable construction in quasi-experimental settings.7,10-13

Reform identification and validation followed a document-triangulation strategy rather than reliance on a single official label such as “national strategy.” A country was coded as treated only when the reform package could be documented through multiple sources showing convergence across at least three of the five predefined criteria: formal legal or regulatory action, a national strategy or policy framework, financial education or capability measures, facilitation of account opening or digital financial access, and evidence of budgetary or institutional commitment. This approach is consistent with international guidance on identifying national financial inclusion reforms as multidimensional policy processes that typically combine regulation, institutional coordination, financial capability measures, and implementation architecture rather than a single legal act alone.17-19 For each treated country, the coding was validated against official government or central bank documents whenever available and complemented with multilateral or institutional diagnostic reports when reforms were implemented as a policy package before or alongside a fully formalized national strategy.

Financial inclusion reforms did not take a single institutional form across Latin America. In some countries, national strategies were codified into law, whereas in others the treatment consisted of coordinated regulatory, payment-system, financial education, and access initiatives designed and implemented during a comparable period and with similar policy goals. For each treated country, the manuscript identifies the main documentary source supporting reform classification and provides additional details on treatment assignment. It also documents relevant cross-country variation in legal form, timing, and depth of implementation.

Econometric Strategy

National financial inclusion reforms have been introduced at different times across countries. We exploit this variation to address the question of average treatment effects using the Callaway and Sant’Anna difference-in-differences estimator for staggered treatment adoption with heterogeneous treatment effects. 10 This is an improvement over the two-way fixed effects estimators commonly used in the literature, because treatment timing varies across units and effects are dynamic over time, meaning that already-treated units make poor controls for newly treated units.7,8 We estimate group-time specific average treatment effects on the treated, ATT(g,t), for each cohort g in each post-treatment period t, using only never-treated countries as comparison units. Each ATT(g,t) is the local average of the difference in outcome for treated cohorts relative to never-treated countries, within cohorts over time, conditional on pre-treatment and time-varying covariates. We then use appropriate aggregation weights across cohorts and post-treatment periods to compute an overall treatment effect. 10 However, policy adoption may not be entirely exogenous, and countries may implement financial inclusion policies in response to trends in entrepreneurship, financial deepening, or broader modernization. As a result, the empirical analysis does not assume exogenous adoption of financial inclusion policies and instead relies on the weaker parallel-trends logic of difference-in-differences rather than random assignment. To reduce remaining bias, the analysis relies on several key design decisions. First, valid comparison groups are identified. Second, pre-treatment health is used as a measure of pre-treatment variation in moderation of policy adoption. Third, a set of lagged macroeconomic and structural controls are included. Finally, several placebo and pre-trend tests are conducted.10,12

To address bad control bias, we use one-year lagged values of a range of control variables that could potentially serve as mediators, including measures of income, labor market conditions for women, human capital, educational inequalities, urbanization, financial development, information technology access, and female labor force participation. 12 While these measures cannot completely control for the possibility that financial inclusion reforms were enacted as part of broader economic or financial development strategies in certain countries, they help to mitigate concerns about bad control bias to the extent that these measures are available. However, the results should be interpreted with the understanding that they do not fully eliminate the risk of bias under a conditional parallel-trends framework, especially in scenarios where financial inclusion reforms were implemented concurrently with other country-specific strategies aimed at enhancing women’s entrepreneurship through alternative channels. 12 Standard errors are adjusted for within-country correlation using cluster-robust variance estimation, and wild cluster bootstrap is used to improve inference under the small number of country clusters. 11

Hypothesis Testing and Subgroup Analysis

The first set of results investigates whether financial inclusion reforms are associated with a positive average treatment effect on the treated (ATT), that is, with increased female entrepreneurship in the adopting countries. To construct p-values for these hypothesis tests, we employ bootstrap-based inference procedures appropriate for settings with a limited number of clusters and serial correlation within country panels. 11 The second set of results investigates whether the entrepreneurship effect is moderated by pre-existing gender health inequity. This question is addressed through subgroup analysis in which countries are split at the median of the Gender Inequity in Health Index. For ease of interpretation, lower index values indicate more equitable health systems and higher values indicate greater inequity in women’s health access and outcomes. We estimate subgroup-specific ATT values for the low-inequity (below median) and high-inequity (above median) subsets of countries, denoted ATT_low and ATT_high, respectively. 10

We also present event-study results showing effects by relative time to treatment, derived from aggregating group-time treatment effects across cohorts. Pre-treatment coefficients are used to assess the plausibility of the parallel-trends assumption by testing whether treated and control countries exhibited statistically distinguishable outcome dynamics prior to reform adoption. Post-treatment coefficients describe the dynamic evolution of treatment effects over time, indicating whether the estimated effects emerge immediately, accumulate gradually, or fade after implementation. Because the analysis relies on a limited number of country clusters, bootstrap procedures are used to improve inference under small-sample conditions. Beyond statistical power, the small sample and the Latin America-specific nature of the reforms limit the generalizability of the findings to other regional contexts. For example, in East Asian economies with different patterns of formalization or in African countries where fintech-driven inclusion plays a larger role, baseline health equity may interact differently with financial inclusion policies because of variation in care burdens, digital access, and state capacity. Future research should test these mechanisms in multi-regional samples to assess the broader applicability of health-system context as a policy moderator. The present findings should therefore be interpreted as cautious, region-specific evidence on the importance of coordinating health equity and financial inclusion strategies.10,11

Robustness Checks and Sensitivity Analysis

Multiple robustness checks assess whether results depend on specific modeling choices or outlier observations. Leave-one-out analysis re-estimates the main model 15 times, each time excluding one country to verify that no single observation drives results. This exercise is particularly important given the small number of countries and helps assess whether the results are being driven disproportionately by one treated or control case. Placebo tests assign false treatment dates three years before actual implementation and re-estimate models; finding null effects in these placebo specifications supports the identifying assumption that pre-treatment trends were parallel and weakens the view that reforms were adopted simply in response to pre-existing entrepreneurship acceleration. Alternative outcome specifications examine female employers only as a proxy for formal entrepreneurship, though low base rates limit statistical power for this subset.

Spillover analysis constructs a regional treatment exposure variable measuring the proportion of neighboring countries with active reforms to test whether treated countries affected control countries through cross-border diffusion. Analysis with interpolated Findex data increases sample size from 45 to 120 observations by linearly interpolating financial inclusion variables between observed years; comparing results across samples assesses sensitivity to this measurement assumption. Additional sensitivity analysis was conducted for the health moderator by verifying that the substantive pattern of results remained stable when the Gender Inequity in Health Index was replaced with simpler alternative measures, including individual constituent indicators and reduced-form composites based on the same pre-treatment health variables.

These alternative specifications are not intended to produce a competing preferred index, but to assess whether the main heterogeneity result depends mechanically on one particular PCA weighting scheme or on one specific set of indicator weights. Across these checks, the central pattern remained unchanged: reform effects were larger in settings with more equitable baseline health conditions and weaker in settings with higher female health disadvantage. Even so, this pattern must be interpreted with explicit caution on two grounds. First, the alternative constructions suggest that the moderation result is not an artifact of a single PCA specification, but they do not establish that the observed heterogeneity is attributable exclusively to health-system inequity as a specific causal mechanism. Second, and more fundamentally, the index should be read as a proxy for broader institutional capacity — including state reach, social policy infrastructure, and general quality of public service provision — rather than as a direct measure of health system functioning alone. The distinction matters: health system inequity is the theoretically motivated framing for why baseline conditions should moderate reform effectiveness, but the index itself cannot rule out that correlated institutional dimensions drive some portion of the observed heterogeneity. Future research using multi-country micro-data could attempt to disentangle these pathways more precisely.

This necessarily limits statistical power, widens uncertainty around subgroup estimates, and increases the risk that point estimates may be sensitive to small-sample variation. For this reason, the paper places greater emphasis on the consistency of direction, the stability of estimates across robustness checks, and the dynamic pattern in the event-study results than on any single point estimate viewed in isolation.10,11 Wild cluster bootstrap procedures improve inference under few-cluster conditions, but they do not eliminate all small-sample limitations; accordingly, the results should be interpreted as credible but necessarily cautious evidence rather than as highly precise parameter estimates. 11 All robustness specifications maintain the Callaway-Sant’Anna framework to preserve consistent treatment effect definitions, reporting how point estimates and confidence intervals shift across alternative specifications to characterize the range of plausible effect magnitudes. 10 This emphasis on sensitivity to alternative measures is consistent with the manuscript’s broader strategy of avoiding overreliance on a single coding choice in causal inference settings.7,12

Results

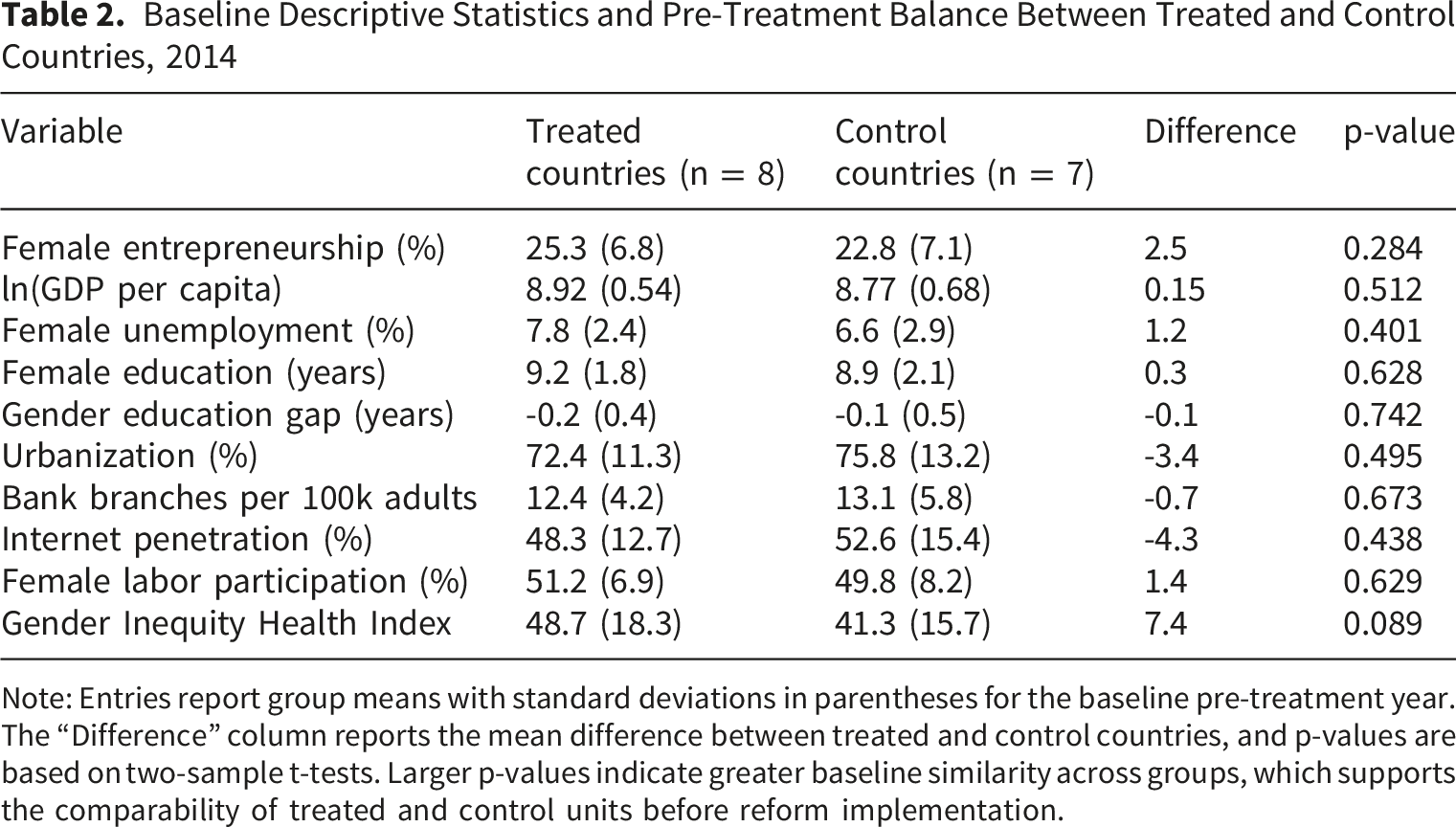

Descriptive Statistics and Pre-Treatment Balance

Baseline Descriptive Statistics and Pre-Treatment Balance Between Treated and Control Countries, 2014

Note: Entries report group means with standard deviations in parentheses for the baseline pre-treatment year. The “Difference” column reports the mean difference between treated and control countries, and p-values are based on two-sample t-tests. Larger p-values indicate greater baseline similarity across groups, which supports the comparability of treated and control units before reform implementation.

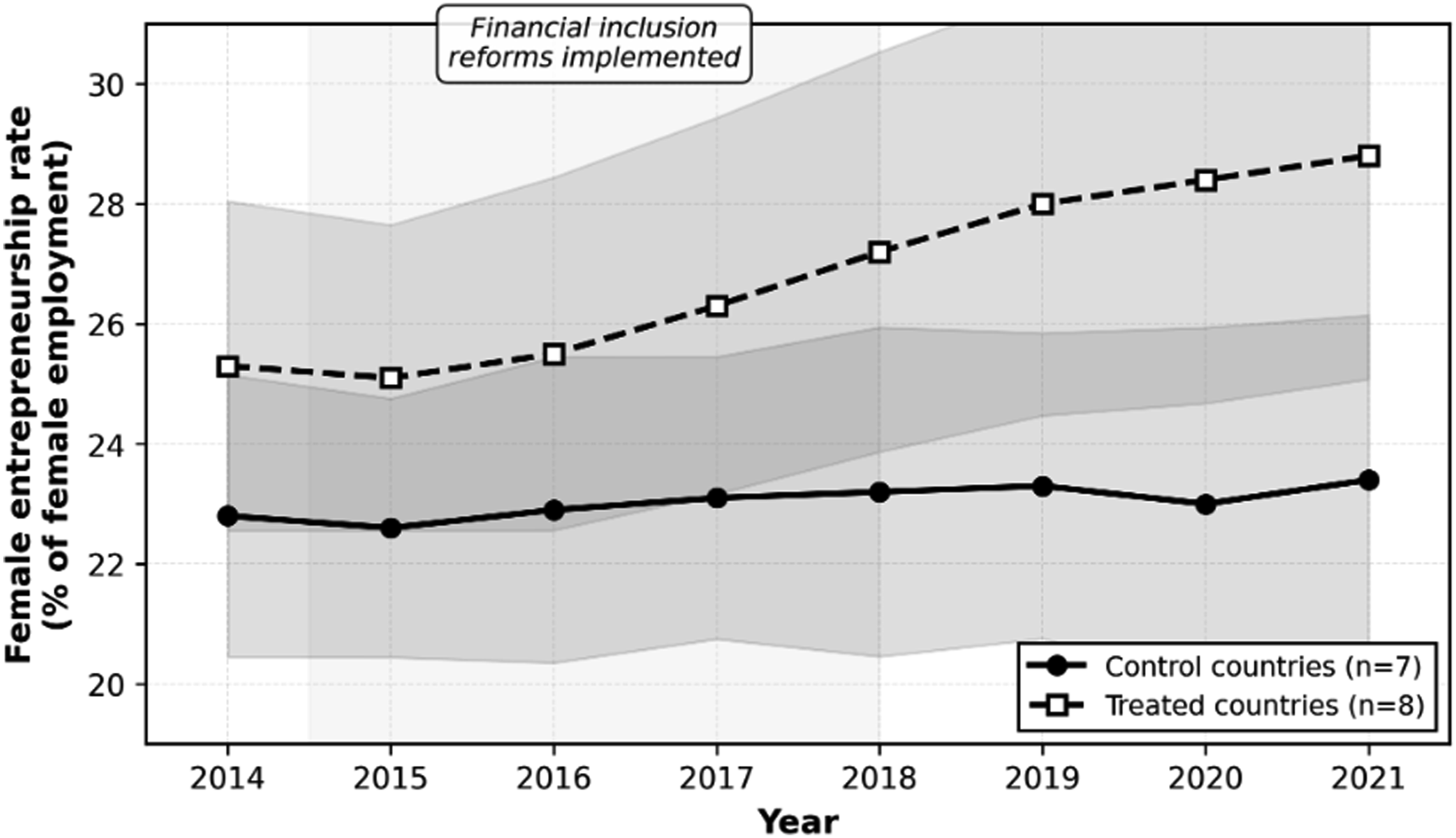

Female entrepreneurship trends in treated and control countries. Note: Lines represent mean female entrepreneurship rates (self-employed + employers as % of total female employment). Shaded areas indicate 95% confidence intervals. Treated countries implemented national financial inclusion reforms between 2014-2018. Control countries did not implement comprehensive reforms during the study period

Verification of Parallel Trends Assumption

To assess the parallel-trends assumption, the analysis regressed female entrepreneurship on the treatment-group indicator, time, and their interaction, including covariates and country fixed effects while restricting the sample to pre-treatment years. The interaction coefficient captures differences in pre-reform trends between treated and control countries. The estimated coefficient was 0.18 (SE = 0.31, p = 0.567), indicating no statistically detectable difference in pre-treatment trends. Event-study estimates for three, two, and one year before reform implementation were also close to zero: −0.4 (p = 0.721), 0.3 (p = 0.803), and −0.1 (p = 0.912), respectively. Placebo tests assigning false treatment dates three years before actual reform implementation produced an average estimated effect of 0.5 percentage points (SE = 0.8, p = 0.548). These results do not prove that reform adoption was exogenous, but they suggest that treated and control countries were not following sharply different entrepreneurship trajectories before reform implementation. Identification therefore relies on the assumption that, conditional on observed controls, pre-treatment trends in female entrepreneurship were comparable between countries that adopted financial inclusion reforms and those that did not. Some uncertainty remains because unobserved time-varying macroeconomic shocks could still have affected entrepreneurship differently across countries.

Main Treatment Effects

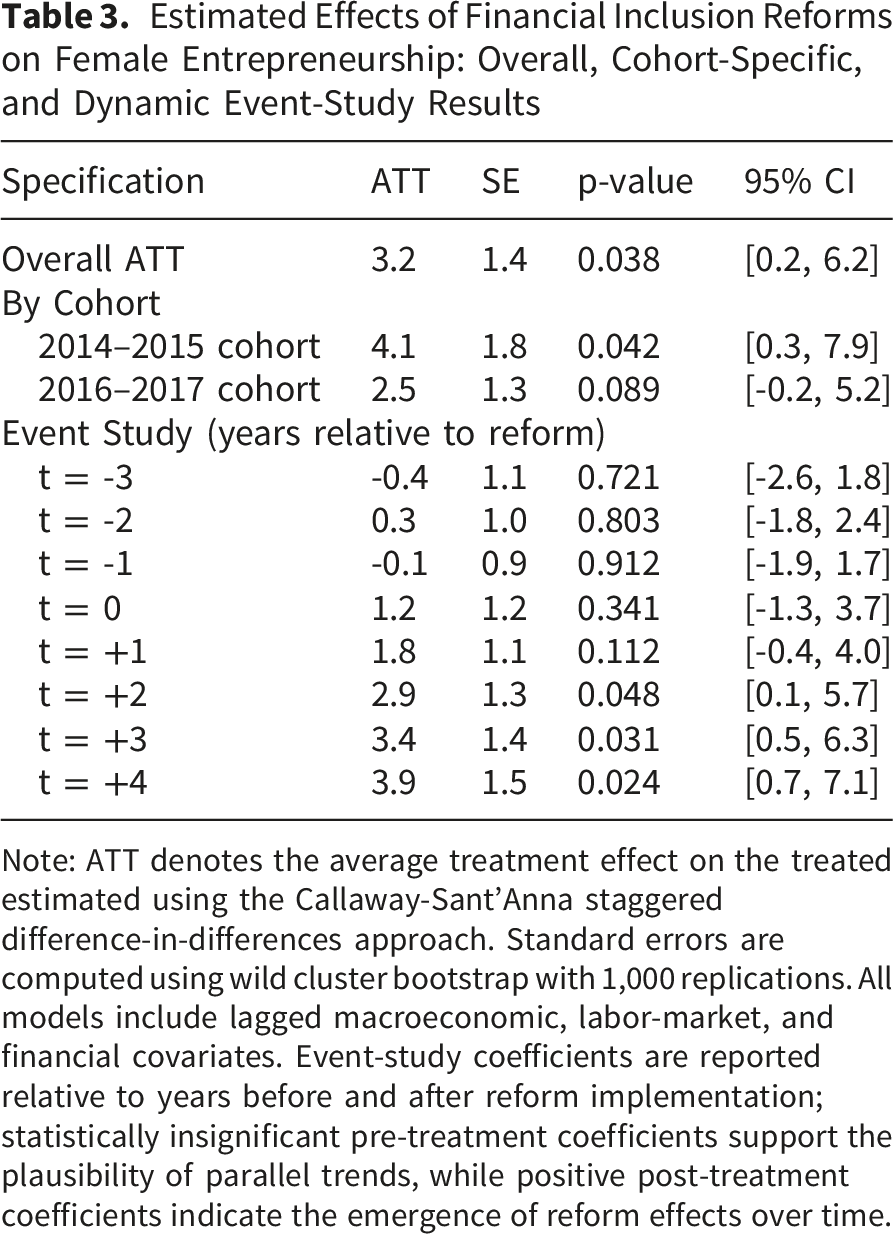

Estimated Effects of Financial Inclusion Reforms on Female Entrepreneurship: Overall, Cohort-Specific, and Dynamic Event-Study Results

Note: ATT denotes the average treatment effect on the treated estimated using the Callaway-Sant’Anna staggered difference-in-differences approach. Standard errors are computed using wild cluster bootstrap with 1,000 replications. All models include lagged macroeconomic, labor-market, and financial covariates. Event-study coefficients are reported relative to years before and after reform implementation; statistically insignificant pre-treatment coefficients support the plausibility of parallel trends, while positive post-treatment coefficients indicate the emergence of reform effects over time.

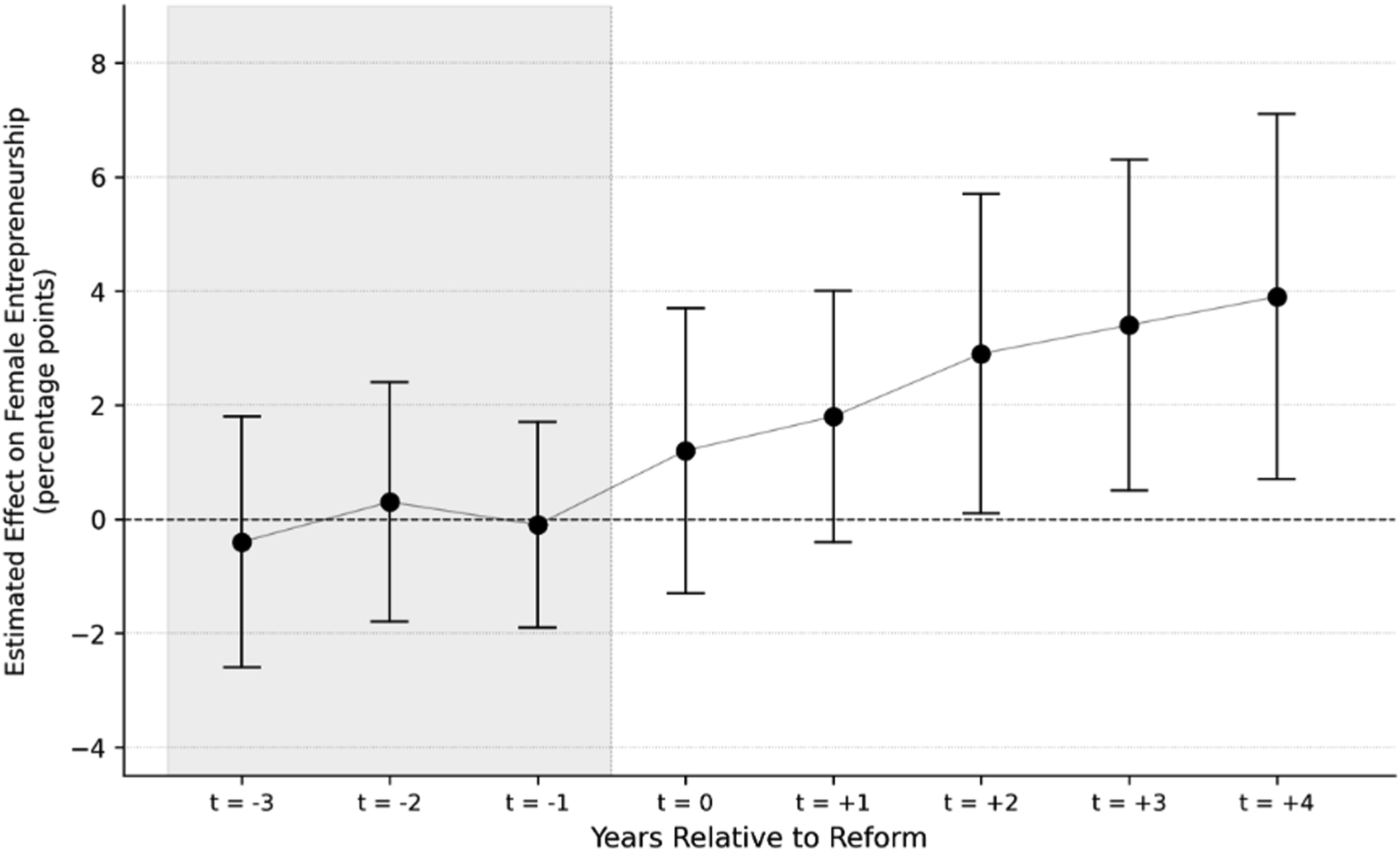

Dynamic event-study effects of financial inclusion reforms on female entrepreneurship. Note: Coefficients estimated using Callaway-Sant'Anna staggered difference-in-differences. Bars represent 95% confidence intervals computed using wild cluster bootstrap (1,000 replications)

Figure 3 presents the dynamic event-study estimates of the effect of financial inclusion reforms on female entrepreneurship across the eight years surrounding reform adoption. Pre-treatment coefficients at t = −3, t = −2, and t = −1 are small and statistically indistinguishable from zero (−0.4, 0.3, and −0.1 percentage points, respectively), providing support for the parallel trends assumption and indicating that treated and control countries did not follow divergent entrepreneurship trajectories prior to reform implementation. Post-treatment coefficients turn positive beginning at the year of adoption and increase monotonically over time, reaching 1.8 percentage points one year after reform, 2.9 at t = +2, 3.4 at t = +3, and 3.9 at t = +4. This pattern indicates that reform effects are not immediate but accumulate progressively as financial inclusion infrastructure consolidates and women convert improved access to financial services into sustained entrepreneurial activity.

Effects are slow to materialize. Estimated effects for the 2014-2015 treated cohort are 4.1%, 95% CI: 1.8%, 6.3%, while those for the 2016-2017 treated cohort are 2.5%, 95% CI: -0.7%, 5.8%. Notably, the confidence intervals for the two cohorts overlap, indicating that the difference between them is not significant. Event study coefficients are also close to zero in the pre-treatment years, turn positive over time, and then increase gradually. One year after reform, the coefficient is 1.8%, p = 0.112, two years after reform it is 2.9%, p = 0.048, three years after reform it is 3.4%, p = 0.031, and four years after reform it is 3.9%, p = 0.024. This pattern is consistent with the lag between obtaining credit and starting a new business.

Heterogeneous Effects by Gender Health Equity

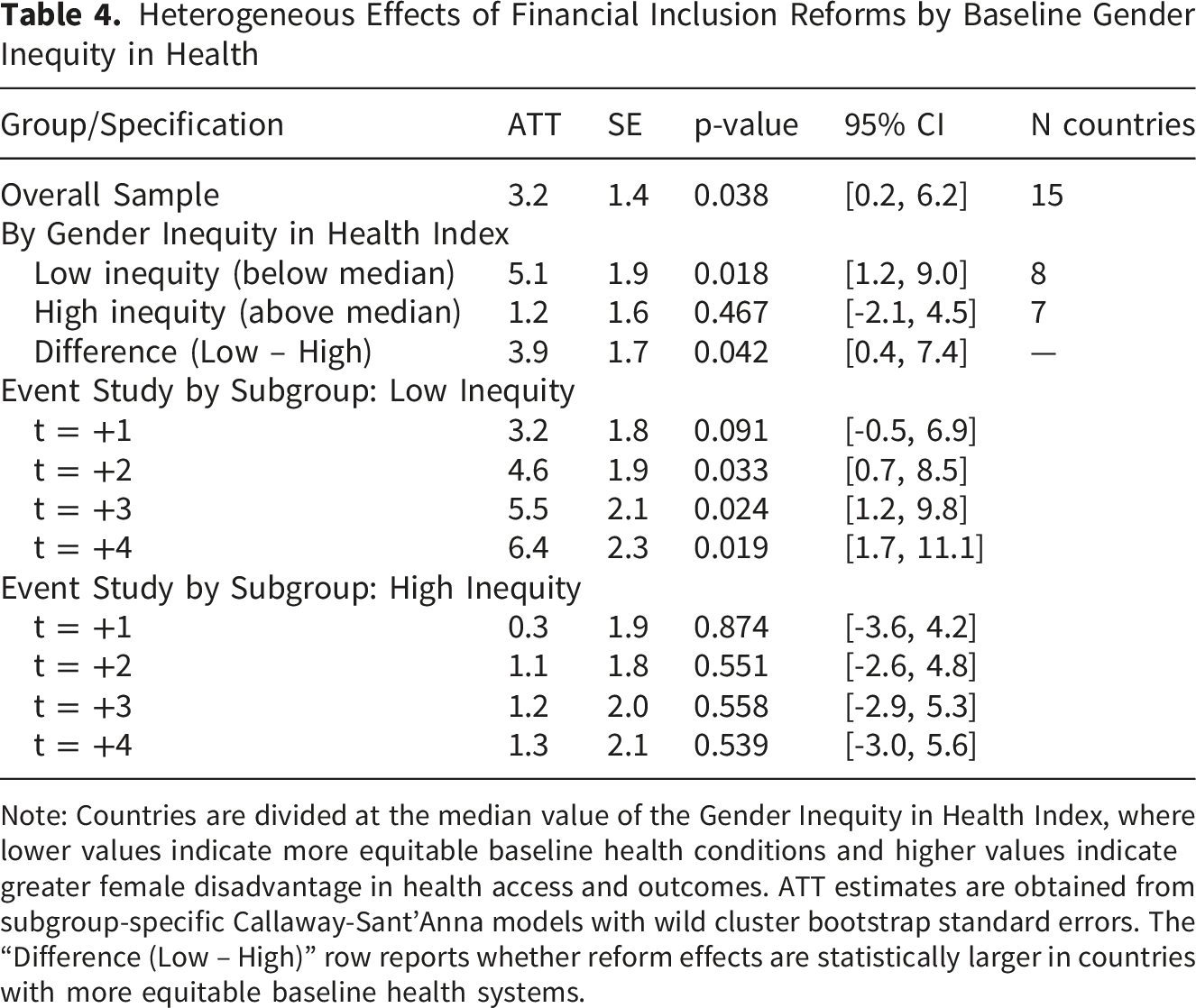

Countries with below-median Gender Inequity in Health Index scores, indicating more equitable baseline health-system conditions, had an average treatment effect of 5.1 percentage points (SE = 1.9, p = 0.018). In contrast, countries with above-median index scores, indicating greater baseline female disadvantage in health-system conditions, had an average treatment effect of 1.2 percentage points (SE = 1.6, p = 0.467). The difference between these subgroup estimates was 3.9 percentage points and was statistically significant under bootstrap inference (p = 0.042). In substantive terms, financial inclusion reforms were associated with stronger increases in female entrepreneurship in countries where baseline health-system conditions were more equitable. These findings should not be interpreted as evidence that financial inclusion reforms generated better health outcomes for women. Rather, they indicate that pre-existing health-system equity moderated the effectiveness of financial inclusion reforms in promoting female entrepreneurial activity.

Heterogeneous Effects of Financial Inclusion Reforms by Baseline Gender Inequity in Health

Note: Countries are divided at the median value of the Gender Inequity in Health Index, where lower values indicate more equitable baseline health conditions and higher values indicate greater female disadvantage in health access and outcomes. ATT estimates are obtained from subgroup-specific Callaway-Sant’Anna models with wild cluster bootstrap standard errors. The “Difference (Low – High)” row reports whether reform effects are statistically larger in countries with more equitable baseline health systems.

Robustness and Sensitivity Analysis

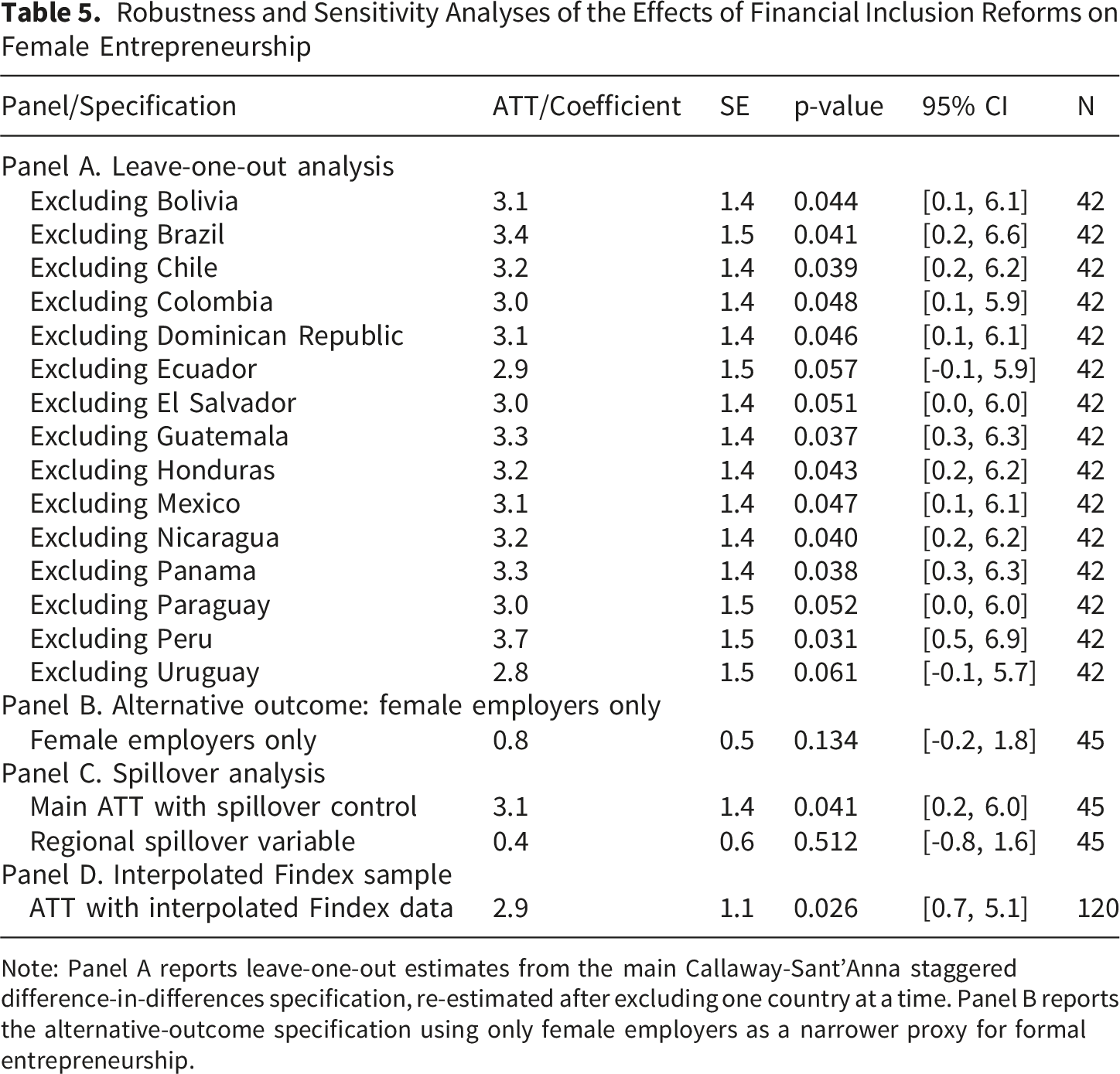

Robustness and Sensitivity Analyses of the Effects of Financial Inclusion Reforms on Female Entrepreneurship

Note: Panel A reports leave-one-out estimates from the main Callaway-Sant’Anna staggered difference-in-differences specification, re-estimated after excluding one country at a time. Panel B reports the alternative-outcome specification using only female employers as a narrower proxy for formal entrepreneurship.

Discussion

Policy Implications for Integrated Sectoral Coordination

Using data for 15 Latin American countries, we find that financial inclusion reforms are more effective in some countries than others. The results show that gender inequity in health systems can condition the effectiveness of financial inclusion reforms for female entrepreneurship. The main effect of financial inclusion reforms on women’s entrepreneurial economic participation is approximately 3.2 percentage points, representing an increase of 13.3 percent relative to the baseline mean. These findings contribute to economic policy analysis on women’s entrepreneurship, financial inclusion, and institutional differences across countries, while also clarifying why health-system conditions matter for the implementation of non-health reforms. Although the paper does not estimate effects on healthcare use, health financing, or health outcomes, it shows that health systems form part of the institutional environment through which women convert financial access into sustained entrepreneurial activity. Countries with high measured disadvantage may therefore require more integrated interventions that expand financial access while also addressing universal health coverage, reproductive health services, social insurance, and protection from health-related economic risk.

Limitations and Threats to Validity

There is also the possibility of endogeneity in country-level policy adoption. Countries may have adopted financial inclusion legislation for reasons related to prior trends in entrepreneurship, financial modernization, digitalization, or other state-led development initiatives. While the identification strategy includes pre-trends, placebo timing, lagged covariates, and valid comparison groups, within the Callaway-Sant’Anna framework, it is not possible to control for selection into treatment entirely. Thus, the findings should be viewed as conditional quasi-experimental evidence that meets the conditions for parallel trends but not exogenous reform adoption. A second shortcoming is that the number of observations is limited.

The main specification includes 15 countries, 8 treated and 7 controls, with a total of 45 observed Findex years. Due to data restrictions, the analysis is not as powerful for making comparisons within subgroups as it could be, and it has less precision than it would have with more data, with estimates having a large degree of variation due to sampling error for small samples.

Additional limitations arise from measurement and treatment heterogeneity. The entrepreneurship variable combines self-employed women and female employers, which is appropriate for capturing the broad spectrum of women’s entrepreneurial economic activity in Latin America, but it does not fully distinguish opportunity-driven entrepreneurship from necessity-driven self-employment or informal survival strategies. As a result, the estimated effects should not be read exclusively as changes in formal business creation or higher-productivity entrepreneurship. At the same time, the treatment itself is heterogeneous across countries. Financial inclusion reforms differed in legal form, policy sequencing, institutional depth, and component mix, including varying emphases on digital access, financial education, regulatory facilitation, and credit architecture. The analysis therefore identifies the average effect of belonging to a family of national financial inclusion reforms rather than the isolated causal effect of one uniform intervention. This heterogeneity is substantively informative, but it also limits precision in attributing the estimated effects to any single policy mechanism.

Several limitations qualify causal interpretation of these findings. The parallel trends assumption underlying difference-in-differences identification, while supported by pre-treatment trend tests and placebo specifications, remains untestable for the true counterfactual period after reform implementation. Potential violations could arise if treated countries experienced concurrent shocks or policy changes correlated with reform timing, though the staggered adoption pattern across multiple years makes such coincidental timing less plausible. The relatively small sample of 15 countries limits statistical power to detect effects smaller than approximately 3 percentage points, implying that null findings for certain subgroups or outcomes may reflect inadequate power rather than true absence of effects. A further limitation concerns measurement of the entrepreneurship outcome.

By combining female employers with self-employed women, the indicator captures a broad spectrum of entrepreneurial economic activity but does not fully distinguish opportunity-driven entrepreneurship from necessity-driven self-employment or informal survival strategies. As a result, the estimated effects should not be interpreted exclusively as changes in formal business creation or higher-productivity entrepreneurial expansion. Instead, they reflect shifts in women’s participation in autonomous income-generating activity, which may include both business formation and movement into self-employment under varying degrees of formality and economic security. The robustness analysis using female employers only partially addresses this concern by offering a narrower proxy for formal entrepreneurship, but its lower prevalence limits precision. Reform heterogeneity across countries in specific policy components—credit programs versus account facilitation versus financial education—further prevents identification of which reform elements drive observed effects. Anticipation effects may bias estimates if women altered entrepreneurship decisions before formal implementation dates based on reform announcements, though sensitivity analysis excluding the year immediately before treatment produced similar results.

Future Research Directions

Future research should examine more directly the mechanisms through which financial inclusion reforms influence women’s entrepreneurial activity. First, additional studies are needed to clarify how national financial inclusion policies translate into actual access to accounts, credit, savings instruments, insurance, and digital financial services among women with different socioeconomic profiles. Second, micro-level data would be especially valuable for distinguishing opportunity-driven entrepreneurship from necessity-driven self-employment and informal survival activity. This distinction is important because the outcome used in this study captures a broad spectrum of autonomous income-generating activity among women. Finally, longer follow-up periods would help determine whether the estimated reform effects continue to grow, stabilize, or decline over time as financial inclusion infrastructure matures and women’s economic strategies evolve.

There is a particular need for qualitative research on women entrepreneurs that illuminates how they currently negotiate financial systems and health services within their respective contexts and how these systemic barriers fundamentally affect their experiences. The study does not attempt to model health outcomes, but it would be an interesting next step to test the bottom half of the figure on the reform’s effects on female entrepreneurship and expression more concretely (e.g., does it translate into changes in insurance coverage, out-of-pocket spending, preventive health behaviors and mental health?). The study is limited to Latin America, but it would be interesting to test the generalizability of findings in other regions of the world with fundamentally different financial systems, gender norms and health infrastructure configurations.

Conclusions

The effectiveness of policy is substantially shaped by the level of pre-existing gender equity in health systems. The impact of financial inclusion reforms on women’s economic empowerment is approximately four times greater in countries with more equitable baseline health-system conditions, suggesting that women’s capacity to transform financial access into entrepreneurial activity depends partly on the institutional environments that shape health security, reproductive autonomy, and protection from health-related economic risk. Women’s economic empowerment is therefore affected by multiple systems, and this paper identifies health-system conditions as contextual moderators of the relationship between financial inclusion policy and female entrepreneurship. The paper does not aim to evaluate the impact of financial inclusion reforms on health outcomes during the study period, nor is it intended as a health services evaluation. Rather, it provides a conceptual framework for understanding how health systems can influence the distribution of returns to economic policy for women. This reinforces the relevance of the findings for health systems because equitable access to insurance, reproductive health services, and protection from catastrophic expenditure may strengthen women’s ability to benefit from non-health reforms. Policymakers designing interventions for women entrepreneurs should therefore adopt a cross-sector policy approach in which financial inclusion, social protection, and health-system strengthening are coordinated rather than treated as separate policy agendas.

Footnotes

Acknowledgments

The authors thank their respective institutions for academic and logistical support during the development of this research.

Ethical Considerations

This study uses secondary, publicly available, aggregated data. No primary data involving human subjects were collected. Therefore, ethical approval and informed consent were not required.

Author Contributions

Mario de la Puente contributed to conceptualization, supervision, project administration, funding acquisition, resources, validation, formal analysis, data curation, visualization, and overall interpretation of the study. José Torres contributed to investigation, literature review, contextual analysis of financial inclusion reforms, and review of the manuscript. Hernán Guzmán contributed to methodology, econometric design, robustness strategy, and interpretation of the difference-in-differences estimates. Johana Elisa Fajardo Pereira contributed to writing—original draft preparation, organization of the theoretical framework, discussion of gender and social determinants of health, and integration of the health-equity moderator into the manuscript. Aníbal Enrique Toscano Hernández contributed to writing—review and editing, refinement of the final manuscript, consistency checks, terminology review, and proofreading of the revised version. All authors reviewed and approved the final version of the manuscript and agreed to be accountable for the accuracy and integrity of the work.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All data used in this study are publicly available from international databases. Replication materials will be made available upon reasonable request to the corresponding author.