Abstract

Funding original children’s television has never been easy because this is rarely a commercially attractive proposition unless you target a global audience and tap into ancillary revenues from licenced merchandise. As a case of market failure, policy makers who wish to ensure the production of a diverse range of quality content for children have therefore pursued a range of interventions to ensure sustainable levels of local content in the face of strong competition from US-owned media services. The aim of this article is to evaluate different funding options for public service children’s content in a more challenging and competitive multiplatform media environment in countries with a strong tradition of public service content for children. Focussing on interventions that go beyond public service broadcasting (PSB) (quotas, alternative funds), it assesses the extent to which these interventions reflect a future-oriented approach, or one that is mired in the status quo and vested interests.

Introduction

Securing funding for domestically produced children’s television (TV) content outside the United States has never been easy. This is because the highly fragmented, age-segmented children’s audience is rarely commercially attractive, unless global audiences are being targeted, which can generate ancillary revenues from licenced merchandise, typically from animation (Alexander and Owers, 2007: 70–73). Moreover, for children older than 12 years, there is little provision from either public service or commercial broadcasters because the market is considered too small.

Reacting to market failure in children’s TV, policy makers in developed markets who wish to promote diverse quality children’s content, including drama and factual programming, have sought to ensure sustainable levels of domestically produced material. In several countries, a key policy intervention for achieving this goal has been public service broadcasting (PSB), which caters for children in the face of intense competition from well-resourced US-owned transnational channels, which invest little in local content, relying instead on the global distribution of their own branded franchises (Steemers and D’Arma, 2012).

The aim of this article is to evaluate different funding options for public service children’s content in an increasingly challenging and competitive multiplatform media environment in countries with PSB. Recent developments show that funding for children’s TV is becoming more difficult because of advertising restrictions on junk food and fizzy drinks around children’s broadcast content, pressures on PSB funding, declining commissions from commercial broadcasters and continuing fragmentation of the child audience by age, and across multiple platforms and services (YouTube, Netflix, catch-up services).

Comparing and contrasting policy in countries with PSB, this article first asks what forms of alternative financial support already exist for domestically produced children’s content beyond provision by PSB institutions, and how effective are these mechanisms for supporting ‘greater diversity of providers and greater plurality in public services provision’ (Department of Culture, Media and Sport (DCMS), 2015: 114–115)? Second, the article explores emerging policy responses to the challenges of funding public service children’s content in a multiplatform environment beyond PSB.

Findings are based on further analysis of documents and interviews with respondents in Australia, Canada, Denmark, France, Ireland, New Zealand and the United Kingdom. These were originally collected for the purposes of a stakeholder report (Steemers and Awan, 2016), designed to contribute to the British Broadcasting Corporation (BBC) Charter Review debate in 2015–2016. Analysis in these countries provides an opportunity to focus on responses in markets of varying size with a PSB tradition and a range of alternative supports for domestically produced children’s content.

The first section of this article provides contextual background about how children’s TV has been promoted in the past through PSB and quota regimes, which have often demanded that commercial players variously (a) invest specific amounts in domestic production, (b) schedule specific amounts of children’s TV content at times when children are available to view, or (c) schedule specific amounts of domestically produced content for children. The second section, in response to the first research question concerning alternative financial support for children’s content beyond PSB, analyses the effectiveness of existing alternative funding approaches for public service content including so-called ‘contestable’ funding. The third section, in response to the second research question about emerging responses to the funding of children’s content, critically evaluates the extent to which these alternative funding arrangements enable the production of diverse domestically produced children’s content on platforms other than linear broadcasting.

PSB, children’s TV and the decline of quotas

Provision for children and young people is crucial to the survival of PSBs as they seek to engage future audiences, but there are challenges in funding broadcast TV, online and mobile content simultaneously, when PSBs face financial pressures as well as political initiatives to limit their scope and scale. With the on-going or virtual withdrawal of commercial free-to-air broadcasters from the children’s market in many countries, publicly funded PSBs have become the principal commissioners of domestically produced children’s content in Australia, France and the United Kingdom, with reinforced dominance in Denmark and Ireland. However, PSBs are certainly not the main funders of costly animation and drama, which are financed from multiple sources, including international presales, equity investors, grants and tax breaks (Steemers and Awan, 2016: 101–104). These complex funding arrangements blur definitions of what national origination means, particularly when projects are developed for international markets and ‘produced’ in more than one country (Cunningham and Flew, 2015).

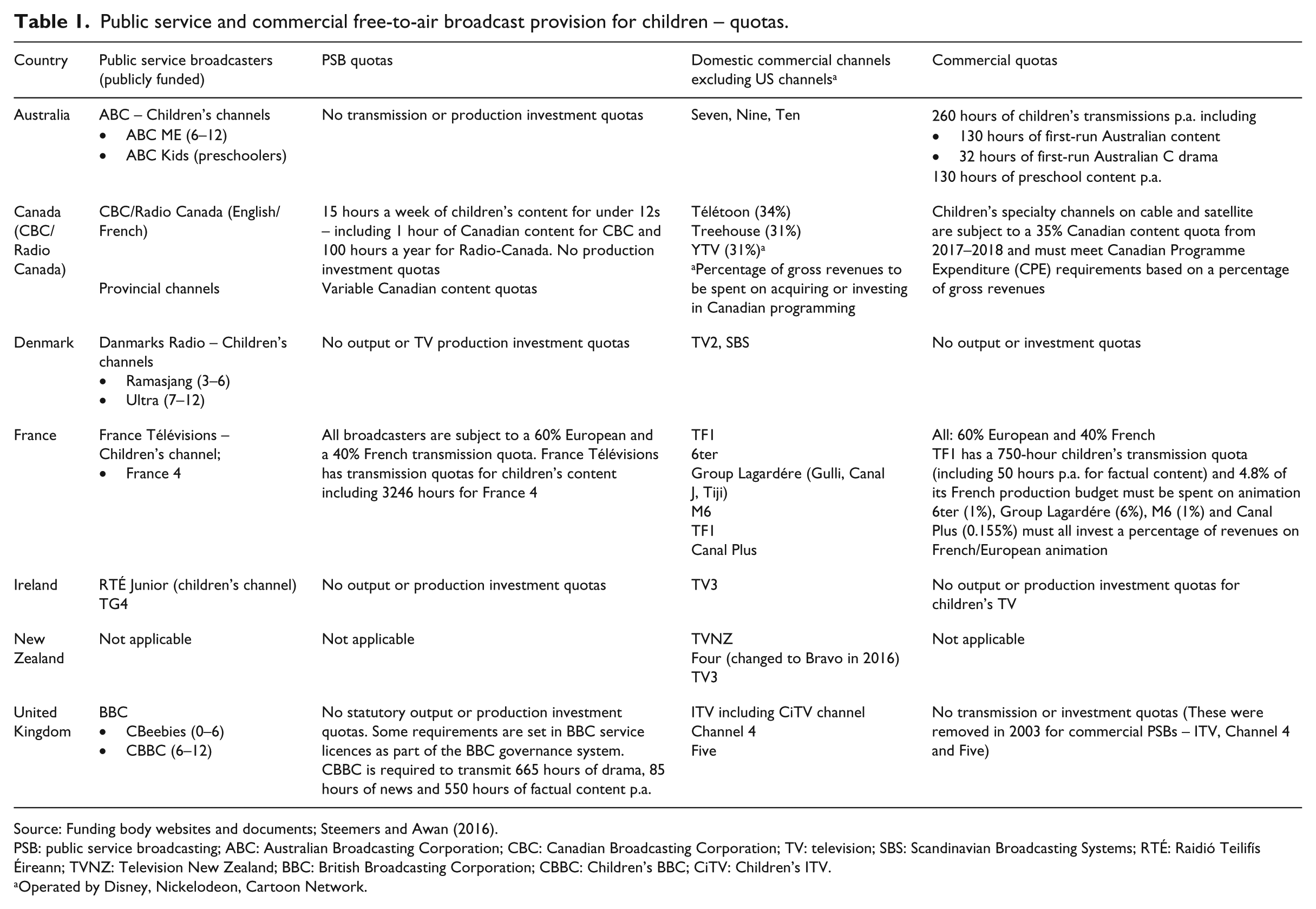

Children’s content forms part of PSB institutional remits, encompassing programming that is meant to appeal to diverse child audiences. Nevertheless, specific obligations are rarely set out in detail in terms of investment levels (production investment quotas), amounts commissioned (often relating to specific types of content), amounts transmitted (output or transmission quotas) and the balance between different content forms (animation, live action), and genres (fiction, factual, entertainment) for different age groups (younger and older children) (D’Arma and Steemers, 2010: 119–121). In Australia, Canada, and France, domestic commercial channels have been subject to much stricter formal obligations on transmissions or expenditure or both than their PSB counterparts (see Table 1).

Public service and commercial free-to-air broadcast provision for children – quotas.

Source: Funding body websites and documents; Steemers and Awan (2016).

PSB: public service broadcasting; ABC: Australian Broadcasting Corporation; CBC: Canadian Broadcasting Corporation; TV: television; SBS: Scandinavian Broadcasting Systems; RTÉ: Raidió Teilifís Éireann; TVNZ: Television New Zealand; BBC: British Broadcasting Corporation; CBBC: Children’s BBC; CiTV: Children’s ITV.

Operated by Disney, Nickelodeon, Cartoon Network.

Without specific obligations, children’s departments, particularly those funded by advertising, are vulnerable to cutbacks. For example, following the United Kingdom’s 2003 Communications Act, which removed the regulatory option of imposing transmission quotas and original production targets for children’s programming on advertising-funded commercial PSBs, 1 investment largely by ITV (but also Five and Channel 4) in first-run original UK children’s content declined 95% from £59 million to £3 million between 2003 and 2014 (Ofcom, 2015c: 13). With little competition for UK originations from ITV, BBC investment also fell by 24% to £84 million in the same period (Ofcom, 2015c: 13). This took place as the BBC decided to pursue a ‘fewer, bigger, better’ strategy for children, ostensibly focussing on ‘quality rather than quantity’ (BBC Trust, 2009: 7).

A similar withdrawal by national commercial broadcasting has taken place in Denmark, reinforcing the role of licence fee funded PSB, Danmarks Radio (DR), as the principal commissioner of Danish children’s content. Commercially funded state-owned broadcaster, TV2, is no longer bound by quotas (Kultur Ministeriet, 2014) and, shorn of its obligations, reduced its commitment to children’s transmissions to the bare minimum, mainly at weekends ‘because there’s more money in adult TV than children’s TV’ (Vridstoft, 2014). In Ireland, PSB, Raidió Teilifís Éireann (RTÉ), has no quotas, but remains the only commissioner of domestically produced English language TV for Irish children, competing with the BBC and US channels.

Only recently has Australian PSB, the Australian Broadcasting Corporation (ABC), recognised that children’s content underpins its future relevance (Potter, 2015: 82), but this commitment, following the launch of dedicated children’s channel ABC3 in 2009, is fragile, with declining budgets and Australian hours. In 2015, the target for Australian content transmissions on ABC3 (since rebranded as ABC ME) was reduced from 40% to 25%, precisely at a time when commercial broadcasters are lobbying to extricate themselves from the transmission and production quotas enshrined in the Children’s Television Standards (Australian Children’s Television Foundation (ACTF), 2015: 4; Buckland, 2016; Screen Australia, 2013: 3). The local content quotas require commercial free-to-air channels (Seven, Nine and Ten) each to invest in 32 hours of original Australian children’s C drama (which can include animation) a year (Australian Communications and Media Authority (ACMA), 2009). However, with no expenditure rules, commercial investment fell from, approximately, AUD$30 million to AUD$10 million between 2007 and 2012 (Screen Australia, 2013: 9) as Seven, Nine and Ten sought to satisfy their quotas with internationally co-produced animation, which counts as Australian drama, requires a lower financial commitment because of international funders and benefits from Australian tax breaks (ACTF, 2015: 4; Potter, 2015; Steemers and Awan, 2016: 33–34).

In Canada and France, more interventionist strategies combining levies, quotas and tax relief schemes have sought to protect domestic production on both public and private TV. Free-to-air PSB Canadian Broadcasting Corporation (CBC)-Radio Canada’s obligation to transmit 15 hours a week of Canadian content for children under 12 years, and the expectation of 5 hours for youth aged 12–17 years, is less than obligations imposed on commercial ‘speciality’ children’s channels (Teletoon, Treehouse, YTV, Vrak) on cable and satellite. However, a reduction in Canadian content transmission quotas for all speciality channels from 60%–70% to 35% from 2017–2018 (CRTC, 2015b: para. 195) threatens future commissions, even though production investment quotas (Canadian Programme Expenditure) remain. Producers are concerned that the 35% quota, combined with a failure to include online services like Netflix within the Canadian content quota regime, and the decision to allow consumers to select cable channels rather than take ‘bundles’ that include children’s channels (CRTC, 2015a), will undermine Canadian children’s content in the longer term (Augustin, 2016; Dillon, 2015).

In France, production investment quotas on both public and private channels are designed to incentivise animation, an industry also sustained by generous tax credits because of the ‘strong power relationship between the political powers, regulatory authority, the CSA (Conseil Supérieur de l’Audiovisual), the channels and the producers of animation’ (French Producer, 2016). Yet, it is PSB, France Télévisions, which has emerged as the main force in children’s TV with the launch of the France 4 children’s channel in 2014. France Télévisions surpassed commercial broadcasters as an animation investor in 2014, accounting for 62% of broadcast investment (€29.1 million), just as investment by commercial free-to-air broadcasters fell 53% to €10.4 million (CNC, 2015: 94).

In New Zealand, there are neither public service broadcasters nor quotas. All funding for public service content is allocated by NZ On Air, a state-financed agency, which supports New Zealand content on free-to-air commercial platforms creating ‘a natural tension between broadcasters, programme-makers and NZ On Air’s role on behalf of the audience’ (Wrightson, email correspondence, 10 May 2016). However, the amount of local children’s content on TV2, New Zealand’s main channel for children’s first-run originations has declined 51% since 2006 to 184 hours (NZ On Air, 2016b: 33), underscoring the challenges of incentivising reluctant commercial players to support children’s production without regulatory leverage (Zanker, 2012: 89).

There are, of course, no shortages of children’s programming in any of these wealthy countries, with US-owned transnational channels broadcasting mainly US animation and sitcoms. With their emphasis on transnational content and without regulatory obligations, subscription video on demand (SVOD) players (Netflix) and video-sharing platforms (YouTube) are not compensating for declines in domestic commissioning (Ofcom, 2015b: 8). Policy arguments in favour of indigenous PSB content, however, can be hard to make, because US content (Disney, Nickelodeon) is immensely popular. Buckingham et al. (2009) argues there is ‘little definitive evidence’ (p. 140) about the cultural or social benefits of home-grown PSB children’s content, but Messenger Davies and Thornham (2007) note the cultural and educational value derived from a range of genres on incidental learning, socialisation, citizenship and identity (pp. 1–2). In the absence of definitive evidence, the case for domestic production often relies on claims that children, like adults, appreciate and deserve access to content that reflects their diverse voices, stories and lives (D’Arma and Steemers, 2013: 124). This lack of demonstrable public value has an impact because policy makers find it difficult to support initiatives for public service children’s content unless they can see tangible outcomes. In the absence of clear demonstrable benefits for children from home-grown content, it is often industry stakeholders, pointing to the vulnerability of domestic production, who drive calls for alternative funds and more competition because of the perceived dominance of publicly funded PSB institutions over children’s commissioning (Steemers, in press).

Alternative funding for public service content

In response to perceived PSB dominance over some forms of content and to promote more diverse provision, there have been initiatives for alternative funds that sit outside public service institutions either as contestable funds subject to competitive producer bids for funding, or automatic funding schemes, where access is activated by producers successfully securing commissions from a range of broadcasters (as in Canada and France). Most schemes are not for children’s content alone, but children’s TV is usually a beneficiary because it is difficult to fund.

This desire to enhance competition with PSB incumbents became clear in the United Kingdom when contestable funding became an issue during BBC Charter Review in 2016. The UK Government proposed a small £20 million annual pilot fund over 3 years to ‘deliver quality and pluralistic public service content’ and ‘to ensure the highest quality for the best value for money’ in competition with the BBC, which was adjudged to have a monopoly over children’s content commissions (DCMS, 2016: 71). The proposed Public Service Content Fund, financed from leftover licence fee funds, ‘top-sliced’ in 2010 by Government to cover other non-BBC expenditure, is designed to support genres in decline, including children’s, arts and religious content and content for underserved minority and regional audiences. Deemed too little, too late by industry and children’s advocacy representatives, it represents a ‘ticking time bomb’, according to Lord Waheed Alli, chair of Silvergate Media, speaking at the 2016 Children’s Media Conference in Sheffield, because it reinforces the view that the licence fee is not solely for the BBC. There are concerns that, when the money runs out, governments will be tempted to ‘top-slice’ again, undermining BBC independence, without adding extra funds for children’s content.

What Is contestable funding?

Contestable funding is based on the principle that competition for funding can lead to more diverse content from a greater array of providers. Efficiency, quality, innovation and value for money are thereby enhanced because funding is focussed on satisfying specific outcomes associated with particular services, genres and audiences rather than supporting PSB institutions with large overheads (Raats and Donders, 2015: 105–106). Crucially, it allows funding to be allocated to organisations other than PSBs, including commercial organisations, other cultural institutions, grass roots organisations and emerging private enterprises.

However, there are doubts about contestable models, particularly in smaller markets like Belgium and Ireland, where competition has failed to generate more high-quality domestic broadcast content from alternative providers in spite of the end of spectrum scarcity (Donders and Raats, 2015: 147–149; Flynn, 2015). Raats and Donders (2015) argue that there is evidence that contestable models are ideologically driven, and do not deliver on contestability, efficiency or sustainability (pp. 106–107). Focussing on a small number of difficult to fund broadcast genres (usually drama, documentaries, children’s), contestable funds are divorced from the benefits of a more holistic public broadcasting service, built around overarching social and cultural values such as universality, quality, diversity and creativity (Raats and Donders, 2015: 106–107). In the case of children’s content, where children have less consumer power than adults, it could be argued that institutional PSBs deliver significant advantages of ‘discoverability’, safe age-appropriate curation, accumulated institutional expertise about children’s content, and the ability to promote valuable shared audience experiences across a range of genres including entertainment. However, not all PSBs have served children well in respect of quality, diversity or popularity and many, for a variety of reasons (prohibitions on expansion, funding, lack of initiative), are not pioneers in digital content (Steemers and D’Arma, 2012: 70). Finally, it is not a given that commercial players will actually apply for contestable funding if the amounts it offers and the content it supports do not fit their commercial priorities (Raats and Donders, 2015: 107).

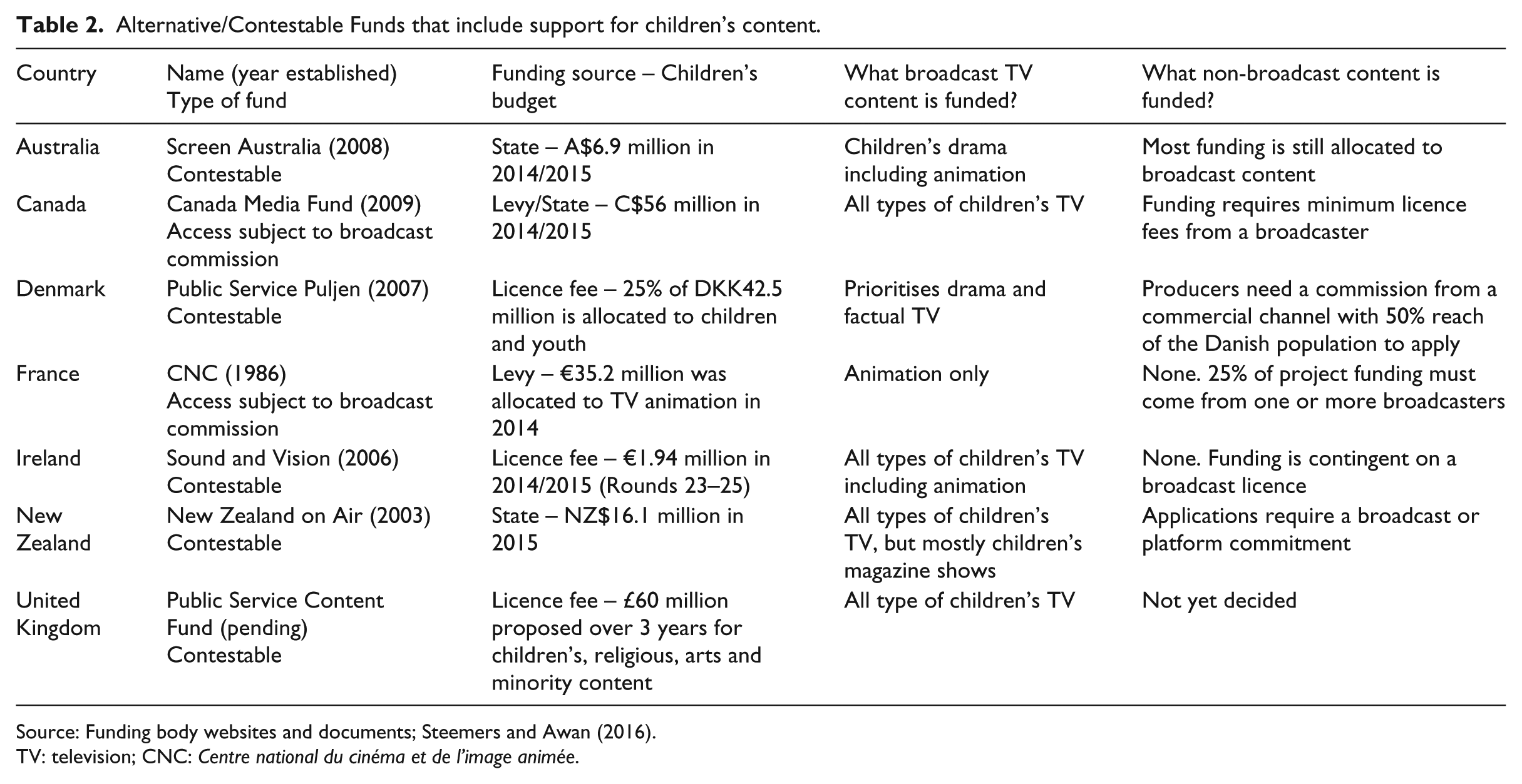

Not all content funds are contestable. Canadian and French schemes allocate funding automatically, subject to producers securing a broadcast commission (see below). Others apply selection criteria based on quality, the target audience, producer track record and, in Denmark’s case, the explicit ability to offer content that the market would not normally provide. Funds established by government policy in these countries are not devoted to children’s content alone although Canada (Shaw Rocket Fund) and Australia (ACTF) operate small independent funds for children’s content. 2 One distinguishing factor of the larger funds is the policy choice over the type of funding, which can be established by licence fee, by state funding, or by a combination of state funding and industry levies (Table 2).

Alternative/Contestable Funds that include support for children’s content.

Source: Funding body websites and documents; Steemers and Awan (2016).

TV: television; CNC: Centre national du cinéma et de l’image animée.

Effectiveness of licence fee financed funds

Licence fee funded contestable funds, where licence fee revenues are allocated away from the incumbent PSB, operate in Denmark and Ireland, two small countries where two PSBs, DR and RTÉ, dominate commissions of public service children’s content. In both countries, the sums involved are small, but differences in how the funds are operated impact effectiveness.

In Denmark, the Public Service Puljen fund is financed from a licence fee surplus (less than 1% of the total), administered by the Danish Film Institute. The local PSB, DR, is barred from applying, as are ‘expensive pay channels’ and channels that do not reach half of Danish households (Danish Film Institute, 2016a). Twenty-five percent of the fund is allocated to children’s content, mainly drama and documentaries, judged on originality, cultural and social significance, and quality in excess of what the market provides (Danish Film Institute, 2016b). However, effectiveness has been limited because commercially funded broadcasters (TV2 and Scandinavian Broadcasting Systems (SBS)) have been reluctant to commission as advertising-funded content and shows for the over 14s (including commercially attractive family programming) are excluded (Danish Film Institute, 2014: 35; N. Mailand-Mercado, 2016). Between 2011 and 2013, the fund only supported four productions for children, including two dramas at a cost of DKK19.5 million (£2 million), developing four more (Danish Film Institute, 2014).

In Ireland, 7% of the licence fee is allocated to Sound and Vision, administered by Irish regulator, the Broadcasting Authority of Ireland (BAI). Originally devised to encourage public service content from other Irish broadcasters, and address competition concerns about RTÉ’s advertising income, 6.2% (€2 million) of the fund was allocated to animation and 1.3% (€429,716) to children’s educational programming under Sound and Vision II between 2010 and 2012 (Crowe Horwath, 2013: 54). Yet, unlike Denmark, where DR is barred, this scheme simply redistributes licence fee revenues back to children’s commissions from RTÉ, which, in the absence of other buyers (except Irish language channel, TG4), remains the main commissioner of Irish children’s content. In 2015 to 2016 (Rounds 23–25), 8 out of 10 children’s awards went to RTÉ commissions, with animation projects accounting for six out of 10 awards and 77% of children’s funding (Broadcasting Authority of Ireland (BAI), 2016). Where Sound and Vision has become significant is as one of the key forms of backing for Irish animation producers, who use it as one component in a range of financial supports including the Irish Film Board, the EU’s Creative Europe scheme and Section 481 Irish tax credits.

Effectiveness of state-financed content funds

State-supported contestable funds operate in Australia (Screen Australia) and New Zealand (New Zealand On Air). However, whereas Screen Australia limits its financial support to children’s drama (including animation) commissioned by any broadcaster, in New Zealand funding for all types of public service content is contestable. State-financed initiatives present similar issues around limited demand from broadcasters, but are additionally vulnerable to downturns in state funding.

Screen Australia, the Australian Federal Government’s main funding body for Australian screen production, provides, approximately, AUD$8 million a year in state subsidies for Australian children’s drama including animation, but has suffered funding cuts in recent years (Groves, 2015). In order to access funding, producers need an Australian presale of at least AUD$100,000 (£50,000) per half hour, rising to AUD$115,000 per half hour from a combined presale to a free-to-air broadcaster, pay channel or video-on-demand provider. In practice, free-to-air broadcast commissions are the main beneficiaries, with producer commissions from the ABC now accounting for most awards. 3 The share of awards to ABC commissions has grown since 2007 because the ABC is more likely to pay the minimum licence fees that allow producers to access Screen Australia funding. By contrast, free-to-air commercial broadcasters can satisfy their statutory obligations to commission 32 hours of Australian children’s drama annually by paying far less for content. Without a minimum licence fee from commercial channels, producers cannot access Screen Australia funding, but they do use the Producer Offset tax rebate scheme, which does not require minimum licence fees. The existence of the Producer Offset has encouraged a shift towards cheaper internationally co-produced animation, which counts as drama, but has a ‘look and feel’ that is international rather than Australian (ACTF, 2015: 4), while still satisfying the 32-hour annual origination quota. This shift towards animation is evident in Screen Australia data, which reveal that animation accounted for nine of the 11 children’s drama series shot in Australia in the twelve month period of 2013–2014 (Screen Australia, 2016).

In New Zealand, government funding agency, New Zealand on Air, supports almost all domestically originated children’s programmes, to the tune of NZ16.1 million in 2015 (NZ On Air, 2016a: 33). Like other markets, there are few broadcast buyers and, without investment or output quotas combined with limited funding, NZ On Air has ‘traded, juggled and explored’ (Zanker, 2015: 33) with free-to-air commercial broadcasters, TV2 and Four, to accommodate children’s content. With few buyers in the marketplace, 70% of NZ On Air children’s content funding went to programming commissioned by Television New Zealand’s (TVNZ) TV2 in 2014–2015, with three long-running magazine shows, produced by two companies accounting for 81% of funded hours (NZ On Air, 2015a: 12).

Effectiveness of levy-financed content funds

Levy-financed funds operate in France and Canada, and redistribute funding away from private and public broadcasters to promote domestic production as part of a wider policy toolkit that includes output and investment quotas. This has generated more stable commitment from commercial broadcasters alongside PSB, reinforcing a more balanced but heavily subsidised production ecology.

In France, the Centre national du cinéma et de l’image animée (CNC), funded chiefly from a tax on TV services (75% of its funding), operates an automatic subsidy system (Cosip) for drama, documentaries and animation. In 2014, it redistributed €35.2 million directly to French animated TV productions, about 20% of TV animation funding, which is also supported by investment quotas for commercial broadcasters (Table 1), tax breaks and regional subsidies (CNC, 2015: 93–94). Combined, these measures are designed to incentivise exportable French animation rather than children’s drama or factual programming, demonstrating ‘the prioritisation of industrial over cultural goals’ by French policy makers (D’Arma and Steemers, 2013: 130).

The Canada Media Fund (CMF), financed from a levy on cable and satellite operators (one third of funding) and government subsidy (two-thirds) (CMF, 2015: 2), made up 12% of Canadian children’s TV production financing in 2014–2015, mainly through automatic access to the CMF’s Performance Envelope Program, triggered by a broadcast commission and a minimum licence fee threshold. The CMF represents one component of a wide-ranging support system including smaller independent funds, both federal and provincial tax credits, investment and output quotas, which allowed up to 90% of children’s production to be funded in Canada and 51% from public sources in 2014 to 2015 (Canadian Media Producers Association (CMPA), 2016: 60). However, deregulation, including reductions in Canadian content quotas to 35% for speciality channels, and new measures that allow consumers to ‘pick and pay’ for cable channels, rather than ‘bundling’ children’s channels as part of a basic cable package, threaten to undermine the longer term financial stability of the children’s production sector (Augustin, 2016).

Evaluating alternative funding arrangements for the future of children’s content

What is noticeable about the alternative funding arrangements, described above, is that they are mostly designed to fund TV content for linear broadcasting at a time of declining levels of broadcast funding and commissions for children. Flynn (2015) asserts that contestable funding especially fails to engage with new types of public service content because it was designed to address market failure in the ‘existing broadcast market’ (p. 141). The existence of these schemes reveals stark contradictions between the policy objective of sustaining a content production industry that lobbies for public subsidy (often for internationally attractive animation) and the countervailing objective of sustaining home-grown content that is innovative, culturally diverse, accessible and relevant to children living in a particular country.

Even if funds cater for content on other platforms, as is the case with Screen Australia and NZ on Air, in practice, content funds still prioritise distribution by linear broadcasting (Table 2). This contrasts with the more disruptive future-oriented concepts of contestability formulated by UK regulator, Ofcom, in 2007, whose consumer-driven Public Service Publisher (PSP) model was designed as a way of preserving non-BBC public service content in an uncertain digital future by concentrating on user participation, digital media and non-linear content (Ofcom, 2007).

None of the countries in this study have yet managed to find a solution for funding different types of public service content for children on platforms other than broadcasting. While children continue to watch TV, declines in their viewing on TV sets have been noted in all countries surveyed for this article because of viewing on catch-up, streaming and on-demand services (Steemers and Awan, 2016). This issue needs tackling with some urgency as the ways in which content (including large amounts of ‘television’) are distributed to and discovered by children undergo significant change and when there are far fewer public service content options available online than commercial offerings. In this transitional phase, children are still viewing TV on a TV set and probably quite a lot of TV online as well. 4 However, there are scant data about how much public service content children consume online, how long they spend on it, or its impact on informing, educating and entertaining them (Livingstone and Local, 2016). As Livingstone and Local point out, it would be premature to make decisions about the funding of public service content without answers to these questions.

Even in Canada and France, which have the widest range of policy interventions, only small amounts of funding have been allocated to digital first content although there is lobbying in Canada against the broadcast first rule in order to promote standalone digital content in those spaces and platforms where children are accessing it (Augustin, 2016). In August 2016, the broadcast first rule was relaxed for Canadian Independent Production Funds (CIPFs), including the Shaw Rocket Fund, which focusses on children’s content, but CIPFs account for far less funding than the CMF. 5 In France, the interlocking system of broadcast-based statutory quotas, industry levies, tax credits and subsidies was characterised by one French producer (2016) as ‘very stable and reliable’ because it promotes investment in French animation, a valuable export commodity. However, while the CNC has channelled subsidies to animation, only limited funding is awarded through Web COSIP for the development and production of TV works on the Internet (CNC, 2015: 180). In Ireland, interventions have benefitted not only the RTÉ children’s department (by directing funding to its commissions), but also the international growth of the Irish animation industry, including companies such as Brown Bag Films (acquired by Canadian 9 Story Media Group in 2015) and Jam Media. Tax credits are part of these support measures available not only to Irish animation producers, but also overseas projects, which accounted for 78% (€38.9 million) of the total value of tax credits in 2015 (Irish Film Board (IFB), 2015).

The Danish Film Institute is seeking a relaxation of content fund rules to stimulate demand, targeting the 50% penetration rule and the possibility of funding Danish content on video-on-demand services. According to Nanna Mailand-Mercado (2016) Head of Talent, Games and Media at the Danish Film Institute, ‘If you set up a fund, you have to at least keep it open enough for development, so you don’t lock yourself to something that is too old’.

NZ On Air put forward proposals for a single contestable multimedia fund and ‘online home’ for children’s content in 2015, but had yet to implement any changes by August 2016 (NZ On Air, 2015b: 3). For NZ On Air, there are considerable distribution and discovery issues without a branded ‘online home’:

It is difficult to launch online content successfully outside an existing website or online aggregator of substance. This is because both discovery and repeat visits are very difficult to achieve. (NZ On Air, 2015c: 5)

In Australia, the debate about the future of public service children’s content beyond broadcasting seems to have been largely avoided as broadcasters, producers, funding bodies and advocacy groups engage in what Anna Potter (2015) has called ‘intramural conversations’ about access to subsidies and tax incentives for broadcast content, rather than dialogue about the future of Australian children’s content in a multiplatform, mobile environment (p. xi). In the United Kingdom, also, government proposals for a public service content fund appear to be mainly focussed on delivering funding for broadcast content, driven largely by industry arguments about the future of children’s TV production, rather than any engagement with what children need or want from public service content across broadcast, online platforms and mobile devices (Steemers, in press).

Evaluation and conclusion

Findings here suggest that alternative or contestable funding as currently constituted is not enough to support public service children’s content beyond public service institutions. Experience in France and Canada suggests other interventions and state subsidies are necessary to promote more diversity among providers and increased investment. Alongside PSB, there needs to be a range of policy interventions to stimulate commercial demand, including output and investment quotas, industry levies and tax breaks. Without production investment quotas, in particular, there is strong evidence that commercial players are reluctant to invest in domestically produced children’s content – as seen in Denmark, Ireland, New Zealand, and the United Kingdom. If there is little demand from broadcasters, limited amounts of contestable funding are unlikely ever to lead to greater diversity of providers or greater plurality in public services provision.

More seriously, there is little evidence of future-oriented funding strategies to support different types of public service content for children other than broadcast programmes, particularly in a transitional phase, where we have no clear answers about how much time children spend accessing TV and other services online. Other content forms might include short-form video, interactive formats, apps, games and participatory tools that provide a crossover space to inform future policy. The BBC, as part of its response to BBC Charter Review, suggested something along these lines with its iPlay initiative, an online portal for children (BBC, 2015: 74–75), but this discussion was eclipsed by debates about contestable funding (Steemers, in press). A policy predisposition towards broadcast TV and PSB institutions over other cultural institutions and content producers, combined with a reluctance in some countries to burden commercial players with quotas and levies (see proposals in favour of levies from Goldsmiths, University of London, 2016), suggests an unwillingness by governments to engage sufficiently with how the public interest and the marketplace are balanced in relation to children’s content provision.

It is important, also, that any alternatives for funding public service content are informed by research about the use by and impact of public service content on children. Children’s TV wherever and however it is consumed is still enormously important. However, there needs to be more thought about how children are navigating through and discovering public service content (including TV programmes) as their media engagement shifts from viewing on a TV set to viewing on other devices, from TV remote controls to search engines favouring popular over niche content, and from broadcasting to on-demand and online platforms, which remain largely unregulated in respect of local content and the promotion of commercial products (Kunkel, 2015). In addition to funding children’s content, policy makers need to pay more attention to what a public service commitment to children is likely to mean in future across both TV and a variety of digital platforms and services. With funding policy often focussed on buttressing domestic TV production and animation industries, there is little evidence yet that larger issues concerning the distribution, discovery and social value of public service content for children are being fully recognised, addressed and evaluated by policy makers and stakeholders. Until these are tackled, the diversity of providers and greater plurality in provision for domestically produced content will continue to be an issue, which no amount of tinkering with small-scale alternative funding mechanisms is likely to solve.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Some of the research in this article was funded by the University of Westminster, the author’s previous place of employment.