Abstract

Digital services and products are often described as immaterial or virtual. However, they are responsible for a vast amount of environmental damage and destruction. The creation, processing, storage and movement of data relies on extensive natural and finite resources including electricity, water, metals, elements and chemicals as well as the production of human-made materials including plastics and glass; the disposal of these materials can produce toxic waste which is often illegally hidden and shipped around the world to bypass responsibility. Despite clear evidence of the materiality of digital flows, corporate rhetoric artfully acts to conceal the environmental risks and costs of digital flows, while state and international policy and regulation has thus far been unable to produce an effective response. This article seeks to examine the roots of this problem by reviewing the historical global policy discourse on the digital economy. The article is also grounded in Asia – which now accounts for almost half of the world’s Internet users – by looking close up at State policies in the second most economically advanced country in the region: Singapore. The article concludes with a discussion of what needs to happen if states are to reduce the environmental burden of the digital economy and ensure the costs are more justly distributed.

Introduction: the materiality of data flows in the Asia

In just 15 years, data flows have moved from having a near-negligible impact on the global economy to today exerting a larger impact on GDP growth than the centuries-old trade in material goods (McKinsey Global Institute, 2016). This is the result of ever more business models using the Internet to sell non-digital and digital goods and services. The Internet and digital devices – such as mobile phones, tablets and computers – support the movement of data, which in turn increases international connectivity and cross-border business activity. Cross-border bandwidth is accelerating: it grew 45 times larger between 2005 and 2014 (McKinsey Global Institute, 2016). The growth of Internet uptake and use has been particularly dramatic in the Asia Pacific region in recent years: the region accounted for 52% of the global fixed broadband subscribers in 2016, up from 38% in 2005 (UNESCAP, 2016). 1 Mobile broadband subscribers in the Asia Pacific also jumped steeply: from 30 to 47 subscribers per 100 people between 2014 and 2016 (ITU, 2017).

The increasing use and dependence on the Internet in Asia, as elsewhere, is contributing to a growing demand for ICT devices including mobile phones, printers, servers and computers. However, other technology developments are also driving the need for both ICT devices and data storage. Billions of ‘Internet of Things’ devices (excluding smartphones, tablets and computers) now collect data for analysis and storage; most of these units are household consumer items (Gartner, 2017). At the same time, artificial intelligence and machine learning require vast computing power and data processing and require computer storage. CISCO (2016) estimates that cloud storage use will rise more than threefold between 2016 and 2021 with big data and the Internet of Things being identified as key factors driving this growth (CISCO, 2018).

Creating, moving, processing and storing an ever-increasing amount of data around the world require vast digital infrastructures. Drawing on Larkin (2013, 328), digital infrastructures can be defined as the material and energetic sociotechnical systems that allow us to create, enable, record, process and distribute data across time and/or space (Reading and Notley, 2017). These sociotechnic systems rest on a complex assemblage of human and non-human infrastructures built from global supply chains involving natural and man-made resources, capital and labour.

A growing number of scholars who examine the media and communication industries, infrastructures and practices now acknowledge the serious issue of environmental impact. However, it is important to note that this remains a topic that only a small minority of scholars in this or related fields engage with in any way in their research or writing. Maxwell and Miller’s (2012) Greening the Media, is a seminal text that pieced together disparate and patchy global data in an attempt to highlight the environmental impact of the media industries, digital and otherwise. Sociologist Jennifer Gabrys (2011) examined the multiple forms of waste that electronics create and considered the uneven, unjust way this waste is deposited. Mosco’s (2014) To the Cloud was pioneering in the way it connected corporate rhetoric and lobbying about cloud storage to the problems associated with environmental impacts (particularly energy use). Peters (2015) placed digital communication infrastructure into a historical trajectory. ‘Storage’ he argues ‘is one of the most complex legacies of civilization because of its ability to multiply power and extend time’ but also ‘The bigger the infrastructure, the more likely it is to drift out of awareness and the bigger the potential catastrophe’. (42). Starosielski and Walker’s (2016) edited book, Sustainable Media: Critical Approaches to Media and Environment brings together a collection of articles to illuminate the many different ways media are implicated in environmental destruction. Sean Cubbit’s Finite Media (2016) considers the philosophy underpinning our political systems – colonialism, industrialization and neoliberalism – have worked to ensure that the media industries promote and thrive on over-consumption. The title of his book reminds of the finite natural resources the earth has and the reliance of media technologies on these finite resources. He argues that fundamental changes are needed to our political systems if we are to reverse the upward trend where digital technologies are responsible for excessive and unnecessary resource depletion and exploitation.

This article builds on this growing body of work but is instead focused on critiquing international policy discourse on the digital economy. I argue that a holistic global policy response to this issue has been stymied, in part because the public’s ability to see and therefore know the full scale of the environmental impact of the digital economy has been made impossible. To provide one example that illustrates this challenge of seeing: well over a million kilometres of fibre-optic cable is used to carry the vast majority of Internet data across the ocean floor in order to support connectivity across continents, islands and countries (Carter et al., 2009). These fibre-optic cables are made of fine hair-like optical fibres made from glass or plastic, which are surrounded by a layer of wire to provide strength, a copper conductor to power the repeaters or amplifiers that process the light signal, and a case of polyethylene dielectric. Wire armour and tar-soaked jute or nylon is added for protection (Carter et al., 2009). These materials are produced in multiple places from materials, which in turn are sourced from multiple places. The production of these materials involves mining and the use of chemicals and machinery in factories. Human labour is required to extract, refine, process and dispose of all these materials and to make them operational. Then there is the issue of the ongoing impact of the cable in the sea. The laying and repairing of cables can cause pollution or harmful changes to the marine environment and policing this is difficult. The cables are lowered on the seabed far out to sea, yet this practice is subject to the domestic law and regulations of the relevant coastal country (Jurdana et al., 2014). Thus, talking about the full environmental impact and regulation of even a single material critical to the digital economy is difficult – if it were not in fact impossible since, for a start, the supply chains of this and other digital infrastructure are rendered invisible to those who seek to trace them. Thus, addressing this issue in a holistic way requires regulation that in the very first instance will make the issue more fully visible and therefore knowable.

Certainly, the invisibility of supply chains and their associated environmental impact is not necessary or inevitable and, as I argue below, environmental accountability can be demanded and regulated by state policies and global agreements. The transition to digital economies has been promoted and propagated aggressively by governments and global organisations alongside, and in support of, the vested industry interests. However, despite the long-evident materiality of all digital infrastructure state policies to address, associated environmental issues have – for decades – been completely lacking, ad hoc, piecemeal or otherwise entirely inadequate. In the following section I consider how and why the digital economy has not been closely associated with environmental costs, both in policy terms and in the public imagination. To do this, I consider the initial framing of policy rhetoric and national discourse on the digital economy.

The foundations of digital economy discourse and policy

In policy terms, tentative steps towards digitally orientated economies and societies – in Asia, as with the rest of the world – began with a series of economic policies in Japan and the United States implemented in the 1970s that were underpinned by claims that information and knowledge would become key drivers of economic growth and social change. However, it was not until the World Wide Web began to grow in uptake in the early to mid-1990s that the idea of an ‘information society’ and ‘knowledge economy’ became firmly embedded in most national government policies (May, 2002; Webster, 2004). By this time, information society and knowledge economy national policies were being encouraged and pushed by international organisations, including the International Telecommunications Union (ITU), the Organisations for Economic Cooperation and Development (OECD) and various United Nation organisations.

While some national information society policies attempted to restructure or make changes to diverse sectors including education, the public sector and commercial enterprises, increasing Internet access and use was a key focus for policies during this period (Notley, 2008). Household access to computers and the Internet, and later the individual uptake of mobiles phones, were used as key primary indicators of a nation’s or region’s information economy or knowledge society infrastructure. This was in many ways a justified route for analysis, since it quickly became apparent that the Internet and mobile phones had very significantly altered – and were becoming critical to – the economics and practices of information and knowledge production, analysis, circulation and distribution (Castells, 2001; OECD, 2006). Thus, in the early information society policies, it appears the key risk considered by policy was the risk of some citizens being left disconnected. This meant policies focused on connecting and providing skills-based training to citizens, schools or businesses (Notley, 2008). Other costs or risks associated with an ever-increasing number of ICT devices collecting and sharing data – for example, ethical risks to humans or environmental risks and costs – have only been put onto the policy agenda more recently – driven by concerned citizens, organisations and groups.

In addition, communication technologies can contribute to multiple and conflicting impacts on the natural environment. As noted, negative environmental consequences are associated with the production, use and disposal of information and communication technologies, since toxic materials are included in their making while very significant CO2 emissions result from their use. However, communication technologies are also used in efforts to address environmental issues by increasing access to information and knowledge, which can result, for example, in reduced water or energy consumption or more efficient public transport networks. In addition, ICTs can be used by countries to transition towards less polluting industries (Higón et al., 2017). In terms of CO2 emissions, a study by Lee and Brahmasrene (2014) that examined nine countries from the Association of Southeast Asian Nations found that for the period 1991–2009 ICT adoption had a significant positive on both overall economic growth and overall in reducing CO2 emissions. Similarly, Higón et al. (2017) examined the impact of ICT on CO2 emissions across 142 countries for the period 1995–2010 and found that ICT can positively contribute to the reduction of CO2 emissions once a threshold level of ICT development has been achieved. They explain this by noting that ICT adoption can support ‘a change in the structure of the economy, moving from manufacturing to less energy-intensive sectors like services,’ which is likely to result in reductions in CO2 emissions (p93). Thus, claims about the environmental benefits of ICT use may have detracted from discussions about the very serious environmental costs they are associated with.

Evaluating the environmental impact of the digital economy: where are the data?

The claim that ICT adoption can help reduce CO2 emissions because it leads to structural changes to the national economy or can lead to more environmentally friendly practices or behaviours is problematic when it is used to justify or to overshadow the environmental costs of growing ICT consumption. This is especially the case when such claims are being made by ICT companies that use business models that rely on planned obsolescence as a part of their business model to force unnecessary ICT consumption. The Global e-Sustainability Initiative (GeSI) – which comprises more than 30 software and telecommunications companies including Microsoft, Huweai, Verizon, Bell, Erikson and Nokia – has produced dozens of reports on ICTs and environmental impact and claims to be a ‘leading source of impartial information, resources and best practices for achieving integrated social and environmental sustainability through ICT’ (Gesi, n.d.). None of their report summaries 2 highlight or focus on the damage created by ICTs. Rather, almost uniformly, these reports promote good news stories that claim ICTs can help solve climate change, reduce CO2 emissions, contribute to sustainability, help achieve the Millennium Development Goals and grow a low-carbon economy (see http://gesi.org/gesi/default/report). One report finds that mobile phones are responsible for savings of more than 180 million tonnes of carbon emissions a year while another claims that ‘ICT solutions’ can enable global carbon reductions of up to 15%, save €600 billion and create 15 million green jobs globally by the year 2020. However, as noted, all of these GeSI publications are closed access for paid members. Membership fees are US$30,000 per year and need to be board approved. Only a short summary of the reports is provided to the general public with press releases being made for journalists. Without having access to the full content of these reports (I’ve made numerous requests but have been told they are for members-only), it is impossible to critique the veracity of these claims. It also seems entirely unreasonable that all advancements made by scientists, states, citizens, research organisations and others to address CO2 emissions, pollution and other environmental issues should be attributed to ICTs simply because they were used in these efforts. In addition, the fact that not 1 of the 26 reports (at the time of writing) focuses on addressing planned obsolescence or e-waste reinforces the idea that vested interests are likely to be at work. This highlights the problem of leaving environmental research on ICTs to industry since corporate interests can – and clearly do – lead to what has elsewhere been called ‘greenwashing’ (Bowen and Aragon-Correa, 2014). Indeed, any claims that ICT use can do more environmental good than harm (an argument made by GeSI) are founded on a strawman argument (Jones, 2018). Advocates for better environmental practice are not suggesting people should stop using ICTs – rather that unnecessary consumption should be prevented and responsible production and disposal needs to be enforced.

A number of environmental organisations have also carried out research to investigate the contribution ICTs are making to CO2 emissions. Drawing on a range of sources, Greenpeace (2016) became one of the first international organisations to draw major public attention to the issue of technology and energy use in 2010 with their report, Make IT Green. In the report, they examined the contribution data centres are making to global CO2 emissions. Greenpeace has since produced an annual report on this topic. The latest report from Greenpeace (2016) claims that in 2012, global IT use was responsible for 7% of all global electricity. Of this use, 21% was used to run data centres, 29% for the networks that move data, 34% for devices and 16% for manufacturing infrastructure and devices. The report also found that video streaming is a tremendous driver of data demand, accounting for 63% of the global Internet traffic in 2015. The report’s uneven and at times dated data sources highlights the issue of a lack of up-to-date information from states and companies on sector and industry energy, ICT and bandwidth use.

Other researchers and organisations have focused on examining ICT energy use at the national level. For example, a study by the Berkeley Lab’s Energy Technologies Area found that following a steep increase from 2000 to 2010 in energy use by US-based data centres, this use appeared to have stabilised to 1.8% of the total national energy use (Shehabi et al., 2016). Improvements in energy use were at least in part attributed to the development of very large and hyperscale data centres, which are generally far more energy efficient compared with smaller operations. In this case, even though the research was supported and funded by the US Department of Energy, the data for the study still had to be pieced together in a very complicated way – for example, from historical server shipment data and using details about the energy use of servers as well as data from a market research firm to work out the number, type and operating size of data centres and their energy use. With appropriate regulation, it wouldn’t be this difficult to have accurate reporting and projections on the number and type of data centres and their energy use.

A lack of data is also a serious impediment that stands in the way of analysing and addressing e-waste (electronic waste). The ITU’s partnership with the United Nation’s University and the International Solid Waste Association to produce three global and regional e-waste reports since 2014 (http://ewastemonitor.info) is a notable exception and the first step here in the right direction. After noting that only 41 countries in the world collect statistics to document the movement of e-waste (Balde et al., 2015), in 2017 these partners launched the Global Partnership for E-waste Statistics to ‘help countries produce e-waste statistics and to build a global e-waste database to track developments over time’ and they framed this as part of an effort to address a number of environment, work, industry and health related Sustainable Development Goals, including Goal 12, ‘Responsible Production and Consumption’ (p. 2). The latest report finds that in 2016 the world generated an estimated 44.7 million metric tonnes (Mt) of e-waste and only 20% of this was recycled through legal channels. Close to one-quarter of this waste (10.5 million metric tonnes) is from ICTs (including laptops, computers, mobiles, tablets, routers and printers, but also including a few non-digital economy equipment like telephones and televisions). Asia was the region that generated by far the largest amount of e-waste, while Singapore is one of the top producers of e-waste in the world per capita at around 18 kg per inhabitant per year (Balde et al., 2015). This ICT component of e-waste contains toxic metals including mercury, cadmium and chromium, as well as valuable materials that can be reused, including gold, silver, palladium and rare-earth metals (Huisman et al., 2015; ILO, 2012; Reading and Notley, 2017). The health and environmental risks of the toxins found in discarded ICT equipment include impaired mental development, cancer and damage to the liver and the kidneys (Balde et al., 2017; ILO, 2012; Reading and Notley, 2017). These effects and risks are very unevenly distributed, but they are also hard to monitor. A 2016 report by the Basel Action Network reports on a project, which placed Wi-Fi tracking devices on 205 monitors and printers that were sent to be recycled in the United States. The project found that these items passed through the hands of 168 different identifiable US recyclers, while almost half (45%) were a part of a movement that went offshore with 93% ending up in developing countries (83% in Asia). The report found that it is likely that 96% of these exports were illegal based on the Basel Convention. Out of the 27 unique companies positively identified as ‘last’ holders of the items (apparent exporters), 17 were non-certified. Informal electronic disassembly junkyards in Hong Kong’s New Territories received more than half of the total exports. The research project found these junkyards expose workers and the environment to toxins. All of this happened despite the United States being a signatory of The Basel Convention, a multilateral treaty aimed at suppressing environmentally and socially detrimental hazardous waste trading patterns. Thus, it is clear that international agreements are essential to address the environmental impact of the digital economy – but these are only going to be meaningful if backed up by serious penalties and policing.

Another key challenge related to understanding this problem and its scale is that most studies, policies or campaigns that examine the environmental impacts that result from the digital economy tend to focus on one issue only (e.g. energy use, mining and supply chains, production or e-waste), and often they focus on one location (such as China, India or Hong Kong where so much e-waste ends up). This is likely, in part at least, to be the result of patchy data but it is also due to the complex and varied conditions, practices and risks that are associated with the extraction, production, use and disposal of computers, servers, tablets and mobile phones (for example, see ILO, 2015 or Bales, 2015). The extent of illegal activities that take place through informal markets also seriously complicate the collection of evidence for research and discussion and challenge efforts for cohesive policies or agreements. In addition, often the focus is on the production or disposal of ICT devices themselves, rather than on the impact of having an ever-increasing amount of data, always on and available via an increasing use of and reliance data collecting devices and on cloud services.

Cloud services happen and are stored in data centres. Data centres are critical to the digital economy and they are a fast-growing industry. They provide the space, electricity, cooling and Internet connectivity for servers. While it has become a common trope for engineers or data centre executives to describe data centres as ‘where the Internet lives’ or ‘the brains of the Internet’, data centres also do much more than store Internet data. Big data analysis, deep learning and artificial intelligence all require vast computing processing power and storage capacity that is usually located inside data centres. The stock market is now largely operationalised on servers located in data centres, as is the analysis of up-to-date satellite data on planetary changes. Businesses, universities and governments are all data centre clients and for all of these the movement from using on-site servers for computing power and storage to off-site cloud services and data centres has happened quite rapidly over the past decade.

Data centres vary in size and may be for single purpose (for a single client) or provide co-location (where they provide space to many different clients). A few hundred data centres (around 400 at the time of writing) are what is defined as ‘hyperscale’ facilities that may have tens of thousands of servers housed in hangar-sized buildings, such as those operated by companies like Google and Amazon (Jones, 2018; Smolaks, 2016).

Global spending on cloud infrastructure, software and services was valued at 180 billion in 2015 and is growing quite rapidly (Columbus, 2017). The increasing use of cloud services has the potential to provide significant positive environmental impact, since sharing computing across organisations should reduce the overall number of servers needed for processing and storage. In addition, this market concentration provides greater incentives for companies to specialise to reduce the energy their servers require to power and cool them because doing so will reduce costs (electricity costs constitute the largest operational cost of data centres). However, the flip side of this is that cloud service providers benefit from individuals and organisations storing ever more data while end users and companies are increasingly removed and distant from the material realities associated with their data use. Google and Facebook, for example, have business models that use cloud data for machine learning. This means that users are not provided with options to temporarily store their data on these services and removing data from them can be quite onerous. However, most users of these services do not think about the servers that hold and move their data because they cannot see them. Indeed, in most cases, when using ‘free’ public cloud services, Internet users are denied the ‘right’ to know where their own data are being stored or by whom. At the same time the considerable advancements made by ‘cloud-based’ companies like those of the major technology giants are kept a secret to ensure storage efficiencies are kept as trade secrets. Thus, there are competing interests at play when we consider the environmental footprint of cloud data. Cloud companies want to make their services run efficiently (and cheaply) so that they require less servers and less energy. Yet, they also want users to forget about the risky and complicated parts of their use of these services because they are selling the belief that these services are free, safe and convenient. Furthermore, where they are providing free cloud services, they want more and more data to be amassed where these data provide a financial opportunity or gain.

Data centre companies and industry analysts now widely cite a figure that claims 1%–2% of all global energy is consumed by data centre operations with some suggesting the figure to be as high as 3% and doubling every 4 years (Bawden, 2016). However, data are not stored and processed on a country-by-country basis and a range of factors have led to concentrations of data centres in particular locations. For example, although Singapore is a small island state of just 581 sq km, it has at least 70 large or very large co-location data centres (Broad Group, 2016). This kind of concentration also impacts Singapore’s energy use and related CO2 emissions. The latest government figures available for Singapore’s data centres energy use are from 2015. They indicate that data centres accounted for 9% of Singapore’s overall energy use with a projection that this will reach 12% by 2020. The government also suggests that a single typical data centre consumes as much power as around 60,000 typical households (IMDA, 2017). This is a real problem for a country that imports over 90% of its total power supply and has very low levels of renewable energy (EMA, 2017). Yet, as the following section explains, this concentration of data centres in Singapore is not simply market-driven: it is closely connected to government policies that seek to advance the digital economy.

Singapore: digital infrastructure policies and environmental impact

In many regards, Singapore is leading global developments in the digital economy. McKinsey’s Global Institute (2016) Global Connectedness Index found Singapore to overall be the most connected nation (of 118) when the cross-border movement of goods, services, finance, people, and data was assessed. This ranking can – at least in part – be attributed to state policy. Singapore’s post-independence government policies in the 1960s first directed industry towards manufacturing and shipping. Later, following the 1997 Asian Financial Crisis, the government increased efforts to develop Singapore as a ‘knowledge economy’ and as a regional hub for finance. To achieve this, policies were used to attract skilled international talent while financial incentives were used to attract foreign direct investment (Chua, 2011; McKinsey Global Institute, 2016). At the time of writing, new policy efforts are being proposed and implemented in Singapore to create a new regional industry hub focused on deriving value and economic growth from the creation, processing, movement and storage of data.

According to media scholar Terence Lee, the Singapore Media Fusion Plan (SMFP), announced in 2009, marked a paradigm shift from media policy focused on promoting national identity and unity to media policy focused on economic benefits (Lee, 2016). In many ways, this shift can be seen as a practical one. As John Durham Peters (2015) puts it, while the 20th century broadcast media was about creating content to distribute messages and meaning as a way of organising and controlling societies, ‘digital media [today] serve more as logistical devices of tracking and orientation’ as a route to securing social, cultural and economic power (p7). The merging in 2016 of The Media Development Authority and the Infocomm Development Authority into a single, centralised body – Infocomm Media Development Authority (IMDA) – provides one indication of Singapore’s faith that information and data will provide the new business model for media operations.

In order to develop Singapore as a leading regional digital media hub, the development of a robust, sustainable and competitive digital media infrastructure has been critical. However, there are a number of additional reasons why the Singaporean government has a vested interest in ensuring the country’s digital infrastructure is up-to-date, advanced and efficient. First, the government’s investment arm, Temasek Holdings, has been increasingly moving investments into the technology sector since being affected by the 2007 global financial crisis, and Temasek has openly discussed moving investments over to newer industries such as artificial intelligence and biotech: already 23% of its total investment portfolio in the telecommunications, media and technology sector (Temasek, 2017). In this way, the State has a direct and growing financial stake in the growth of the data and ICT industries (a situation not unique and indeed increasingly common to many national investment strategies and portfolios). Second, in 2014 the government announced an extensive, all-of-government policy called Smart Nation (https://www.smartnation.sg/), which pledged to deploy an extensive number of sensors and cameras across the country to allow the government and corporate partners to monitor everything, from the cleanliness of public spaces to the density of crowds, to the precise movement of every locally registered vehicle (Maxwell-Watts and Pernell, 2016). While still in its early stages, 110,000 lamp posts are to be fitted with multiple sensors to advance the policy (OpenGov Asia, 2017). Government officials have, on a number of occasions, stated that the policy needs robust digital infrastructure including data centres to be operationalised, while also speaking in public about the need to promote and incubate labs, innovation districts and technology start-ups (Tegos, 2017; Spring, 2017). It has been proposed that much of the data collected for Smart Nation will be fed into an online three-dimensional (3D) platform called Virtual Singapore. The platform’s development is being led by the National Research Foundation (n.d) and according to their website it is meant to support experimentation, ‘test-bedding’, planning and decision making, research and development (see https://www.nrf.gov.sg/programmes/virtual-singapore).

Barns et al. (2017) have considered the way that the widespread uptake of smart city strategies has led to an important ‘shift in the framing of digital infrastructure’, since these strategies often involve the government working closely in partnership with global companies in ways that are, in many cases, unprecedented. For example, many large global tech companies – IBM, Cisco, Siemens, Oracle and Google (via a subsidiary of its parent company Alphabet) – have developed ‘city operating systems’ while companies are also often putting themselves forward to offer ‘philanthropic services’ to cities that also allow them to benefit from testing new concepts and software on citizens (Barns et al., 2017). Academics and citizen groups have expressed that they are wary about new and emerging ‘digital city’ projects being designed and implemented in New York, Toronto and elsewhere in partnership with governments by Sidewalk Labs, a subsidiary under the Alphabet umbrella company that also houses Google. The New York Project, Hudson Yards, says Shannon Mattern (2016, n.p): equips Alphabet and Sidewalk Labs to ‘build, deploy, and service any digital technology in the physical world’, which they can then test ‘at scale’ and offer on a subscription, fee, or commission model to private parties or governments anywhere.

Regardless of their motivations, we can say that the Singaporean government has taken a number of active steps to develop national digital infrastructure over the past decade. First, they have supported the development of pervasive high-speed broadband infrastructure. Singapore was an early Internet adopter: however, with the transition to broadband in the early 2000s, it quickly fell behind Korea (which led the world) and Hong Kong in terms of user uptake. In 2007 the government announced a S$750 million tender to support a high-speed Next Generation Network (NGN) with speeds of 1 Gbps to be made available to all homes and buildings by 2010 (Zhen-Wei Qiang, 2010). As part of the agreement, to ensure widespread uptake, wholesale costs for unlimited broadband per household and business were set and the tender provider was required to waive installation charges for home and building owners. By 2016, 97% of Singaporean households had active broadband subscriptions (IMDA, 2016b).

Second, the Singapore government has supported the development and maintenance of new undersea cables and they manage these cables in three cluster sites. Singtel, a public listed company (through Temasek Holdings) with majority ownership by the Singaporean government, listed in 2015 that it part-owns 33 cables, including 11 (most) of those that come into Singapore. 3 In this way the Singapore government plays a direct role in building and maintaining the country’s undersea cables. Having so many undersea cables landing in Singapore means that data industries in the country have a distinct advantage in terms of current and future capacity to move and receive data to and from the rest of the world. As Nicole Starosielski (2015, p1) puts it: ‘Cables drive international business: they facilitate the expansion of multinational corporations, enable the outsourcing of operations, and transmit the high-speed financial transactions that connect the world’s economies’.

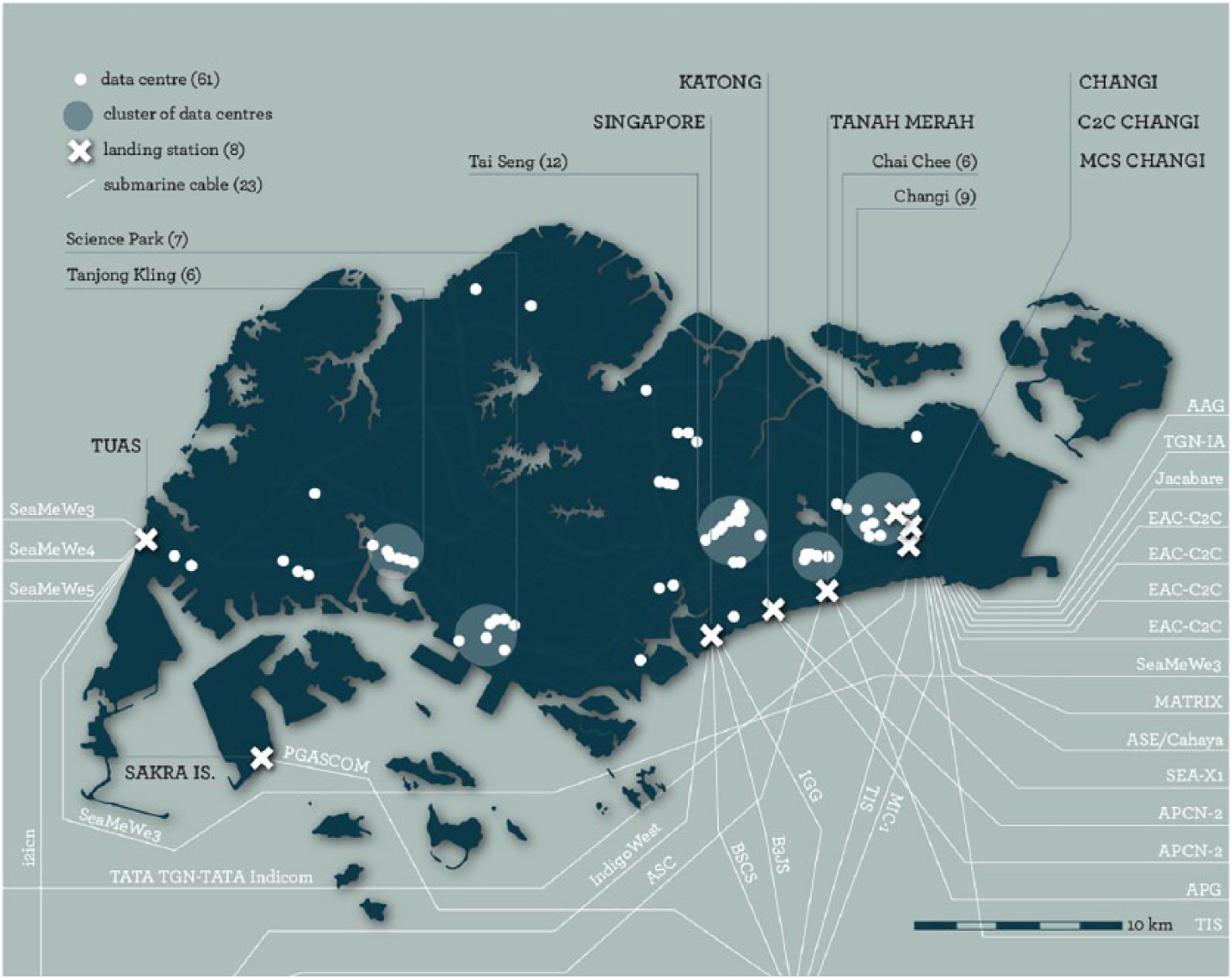

Third, data centres have been a focus of Singaporean policy in what might be considered unexpected ways. By 2016, an estimated 70–75 very large data centres in the country were estimated to hold about half of all the total data that are stored in South-east Asia’s data centres (BroadGroup, 2016). The Singaporean government has supported the development of data centres by setting aside 13 ha for a data centre park to be located in the south-west region of Jurong, where a number of data centres were already located (Google, Digital Realty and Equinix). In 2018, Facebook, which at the time had its regional headquarters and 1000 employees located in Singapore, announced that it would build its first data centre in the country: an 11-storey 170,000 sq m building (Cheok, 2018). The data centre park is an important development that supports the growth of the data centre industry away from the city centre. As Figure 1 shows, most data centres in the country are clustered in the south-east around the city centre. This is no surprise: companies often prefer to have the data centres they use close to them or to particular data sources. Most undersea cables also land in the south-east and many companies have incentives to be as close as possible to the cables that are most important to their global data flows. However, it makes sense to try and have data centres out of the city centre in places where there is more space. Outside the city centre, it is also often possible to make use of natural air-flow. Concentrations of data centres in city centres may also contribute to city micro-climates where the temperature is hotter as a result of the exhaustion of heat from air-conditioning. Here policy interventions, like the data centre park implemented by the Singaporean government, can provide an important way to minimise environmental impact.

Singapore’s co-location data centres and undersea cables as of 2016.

As noted, in 2015 Singapore’s data centres accounted for 9% of all electricity use in the country which – remarkably – is many times higher the percentage used in the United States by data centres. It is unfortunate that more current figures or greater detail on this have not (at the time of writing) been forthcoming from the government. Since the Singaporean government owns the national electricity provider, they are in a position to provide annual and company-specific data to the public on this. The Singaporean government has announced that it will introduce a carbon emissions scheme from 2020. If implemented well, this may provide industry with serious incentives to reduce their energy use (Straits Times, 2017). However, there are many other ways to push for reforms. For example, the government has said they want households to see their own energy consumption through smart nation sensors. Given that industries use far more energy compared with that of citizens, why should the policy focus not be on this information instead? Annual data centre energy and emissions reports could be written to encourage improvements and to allow citizen-consumers and data centre reliant companies to lobby for change and to more critically choose where they store their data. This too has limitations: most of the data amassed and processed in data centres in Singapore do not belong to Singaporeans. However, citizens and companies should be given the ability to critique the impact of their own data storage and of the data industries that reside in and use the resources of their country. If this is to be achieved, governments will need to introduce legislation that will force companies to first tell people where their data are stored and, second, to reveal details about the energy use of these data centres.

At the same time, it is important to note that, while usually couched in concerns about cost and competitiveness, rather than environmental concern, the Singaporean government has taken a number of measures to reduce data centre energy use. First, in 2009, the Infocomm Development Authority of Singapore (IDA) initiated the Green ICT programme with the aim of improving the energy efficiency and competitiveness of the Singapore data centre industry. In 2011 they released a Green Data Centre Standard that provided benchmarks and auditing system to rate the energy efficiency of data centres followed by the ‘Green Mark for Data Centres’, a rating scheme designed to encourage the adoption of energy efficient design, operation and management. One government source says since the launch of the scheme in 2012, until mid-2017 around one-quarter of the data centres in the country’s 18 data centres have been certified: 15 Platinum and 3 GoldPlus (Interview A 2017).

In 2014 the government introduced the ‘Green Data Centre Technology Roadmap’ 4 that made recommendations for research and development investments while proposing methods, models and guidelines to reduce energy use. In 2016, they announced they would provide funding to support technology companies to trial a ‘tropical data center’ model to assess the viability of operating data operating rooms at temperatures of up to 38 C with ambient humidity exceeding 90% (as opposed to the norm of operating at between 20 C and 25 C with 50%–60% relative ambient humidity) (IMDA, 2016a). However, evaluation data has not yet been provided for any of these programmes or trials. (My repeated requests to government agencies for this information and interviews regarding were either ignored or declined.)

In terms of e-waste policies Singapore really falls short and has a very light-hand touch compared with that of many other nations. Companies and organisations are encouraged to adopt SS 587, the Singapore Standard for the management of end-of-life ICT equipment, or at least to implement the best practices for e-waste recycling contained in it (National Environment Agency, n.d.-a). It is not mandatory for companies to adopt this policy, although some financial incentives are offered to small and medium businesses that agree to be certified. Similarly, individuals are ‘encouraged to make use of … recycling programmes’ but it is not mandatory to dispose of ICT equipment through these programmes (National Environment Agency, n.d.-a; n.d.-b). At the same time, the government has made some effort to ensure recycling is accessible and achievable by providing a map of all the collection points. So-called ‘technology hubs’ such as Mediapolis, Fusionopolis and Biopolis also have e-waste bins placed visibly at the front entrance (Figure 2). However, as Lepawsky and Connolly (2016) point out, Singapore can be used as a test case to highlight many of the flaws in the Basel Convention, which is the key international binding treaty to currently regulate e-waste. Because of its location, it is automatically categorised the same way as a developing country that is vulnerable to the import as hazardous waste rather than more appropriately being treated as a major producer and large exporter of e-waste. Furthermore, they note that the Convention permits bi- and multilateral trade agreements (and Singapore has many) to supersede the Convention on the condition that they meet or exceed the Convention’s requirements of environmentally sound management of hazardous waste, which is left as a vague and unclear category that therefore cannot be regulated (Lepawsky and Connolly 2016).

e-waste recycling bins outside Fusionopolis buildings in Singapore.

Finally, there is the issue of the production of technology and the associated issues of mineral mining and processing. In this regard, Singaporean citizens and companies based in Singapore are in the same position as those located elsewhere. International agreements have been introduced to ensure people are told where clothes are made or where food is produced. The Kimberley Process Certification Scheme has effectively restricted the trade of ‘blood diamonds’ by using documentation to prevent sales from financing violence by rebel movements and their allies seeking to undermine legitimate governments. However, it remains impossible for technology users in Singapore and anywhere else – whether individuals or companies – to know the source of the various components of their own devices, even though many of these components are made from toxic materials mined in places that are known to use child labour. While there are a few remarkable efforts such as the Fair Phone, 5 which advocates for ethical supply chains and provides consumers with details about each component used in the phone, these are the rare exceptions. It would not be difficult for international agreements to enforce full supply chain disclosure. Already, companies privately hold this information through commercially developed initiatives like GeSI’s E-Task. 6 Only when they have this information will technology users be able to make informed decisions and the digital economy be made environmentally accountable.

Greening the digital economy

Historically, digital economy policies have failed to recognise, let alone address, the environmental impact of technologies. Initially, policies sought to drive ICT uptake and use and this ensured negative side effects were not been accounted for in policy. As this article demonstrates, technology companies are now making claims that suggest ICTs do more good than harm when it comes to the environment: these claims seek to take credit for the many efforts made by governments, scientists and others to reduce carbon emissions simply because they used ICTs in this work. These claims must be rejected as corporate greenwashing. To counter this, some environmentally focused organisations and advocates have made important progress in tracking, monitoring and lobbying against the environmental destruction caused by digital infrastructures, but these efforts are restricted because companies and governments fail to provide the data required to full grasp the scale of the problem while numerous governments – including Singapore – fail to acknowledge or take responsibility for global black markets which conceal significant impacts.

Singapore, like most other governments, can and should do far more. Like many other Asian governments, the Singaporean government has worked very hard to attract global technology companies. In this way, the case of Singapore highlights that complicated economic entanglements between states and industry may be a leading cause of inadequate and half-hearted efforts to curb the environmental impact of digital infrastructures and the data industries. Singapore has taken a few progressive steps to reduce data centre inefficiencies. However, since the Singaporean government is in the unique position of owning the single electricity supplier in the country, they can and should provide annual data about data centre energy use. They could introduce policies to ensure data centres are forced to reduce carbon emissions and they can be more involved in decisions about the locations of data centres and their design. They can also monitor and heavily penalise illegal e-waste activities and be proactive by providing tax breaks or rebates to both citizens and for companies that effectively process old equipment or use renewable energy sources while policing and regulating the flourishing informal and illegal trade of ICTs in ways that maximise reuse, but also discourage over-consumption (Lepawsky and Connolly, 2016). First however, the government must provide transparency so that citizens and businesses are aware of how much e-waste is being accumulated and can find out where this e-waste is being sent.

Most of all though, this article’s examination of Singapore shows that for real progress to be made binding, international conventions that support the progressive greening of digital technologies are required. While a lack of required reporting means that capturing the full environmental impact of the digital economy is currently made impossible, a vast body of evidence now exists to show how serious this issue is. The past 20 years have shown that companies cannot be left to altruistically develop the best environmental practices. This means governments must take the lead. In the 1990s, countries around the world, led by the most advanced nations, came together to develop initiatives and targets that would advance their own digital economies and remove barriers for the global flow of digital goods and services. Governments now need to come together to reduce the environmental costs of these economies. International agreements, such as the Basel Convention, show that unless serious policing and repercussions exist companies will habitually absolve themselves of responsibility with the result being that the worst effects being concentrated in some of the poorest regions in the world with serious health and environmental consequences for local citizens. Finally, fragmenting discussions and policies about the environmental impact of ICTs does not support consumer or corporate ethical decision-making, while it also means policies can only be piecemeal in terms of addressing the problem. Thus, a binding international environment, technology agreement and regulatory body is required to ensure policies are made meaningful and result in real impacts. The digital economy is a vital and growing part of international relations and prosperity. Governments need to take action to reduce the environmental impact of the digital infrastructures required for this economy to function sustainably. In Asia this should be an imperative since the region is the source of much ICT production and waste, while it also bears the consequences for much of it as well.

Footnotes

Acknowledgements

This paper emerges from an Australian Research Council funded Discovery project titled, Data Centres and the Governance of Labour and Territory.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The funding for this article was received from the Australian Research Council Discovery Program for the project ‘Data Centres and the Governance of Labour and Territory’.