Abstract

The recent surge in Chinese outbound foreign direct investment in Europe has been met with anxiety often invoking national security concerns. Using the national security framework developed by Moran and Oldenski, we try to ascertain which transactions justify apprehension. Our case study is the acquisition by a subsidiary of wholly state-owned State Grid Corporation of China of a 35% stake in CDP Reti S.p.A. (CDP Reti) that controls Italy’s electricity grid via its subsidiary Terna S.p.A. Although State Grid Corporation of China can nominate two members of CDP Reti’s board of directors, we find that there is no direct threat to national security. We then tackle the geopolitical dimension of investments in electricity grids. Using the ‘thought experiment’ developed by Scholten and Bosman, the contribution we make is that, in a world where the importance of renewable energy increases, a framing power rather than control over the strategic development of a country’s grid is sufficient to exert geopolitical power. Since State Grid Corporation of China’s exponents on CDP Reti’s board can at least partly influence the company’s investment decisions, we conclude that the transaction grants China geopolitical influence over Italy’s grid. Furthermore, in the future this type of geopolitical influence could also lead to indirect security concerns. The interconnection of European electricity flows extends this conclusion to the EU’s electricity grid as a whole.

Introduction

In recent years China has made headlines with acquisitions that targeted important Western enterprises. In 2004, Lenovo bought the iconic computer manufacturer IBM. The British car producer MG Rover Group was purchased by Nanjing Automotive. COSCO made an important investment in the Port of Piraeus in Athens, Greece. In 2015, ChemChina bought the tire-maker Pirelli, a piece of pride of the Italian economy. Chinese firms were also allowed to participate in the construction of a nuclear power plant at Hinkley Point C in the UK. Finally, in 2017, there was the acquisition of German robotics producer KUKA by Midea. The shock with which these acquisitions were met in the West is comprehensible: everything is happening so fast, and the economic and geopolitical implications are still being digested.

At the turn of the millennium, China was nowhere to be seen in the world of outbound foreign direct investment (OFDI). From representing virtually zero of global OFDI flows in the late 1990s, Chinese OFDI surged to comprise about 10% in 2015. In the same year, China’s OFDI stock exceeded US$1tn. However, representing only 4.8% of world total, this is still negligible compared to the stock held by Europe and the USA (UNCTAD, 2018). Thus, the surge in OFDI conducted by Chinese businesses should not be overstated.

The motivation behind the present research lies precisely therein. It aims, first and foremost, at contributing to the growing literature on Chinese OFDI by trying to clearly ascertain where to draw the line between deals that should cause apprehension and those that should be seen with more positive eyes. Particularly, the discourse on national security that has accompanied much of the discussion surrounding Chinese OFDI requires careful examination. As we shall see, national security arguments give governments a sort of final judgement call with which to block incoming investments, sometimes arguably for political rather than security concerns (Tingley et al., 2015).

There are valid reasons for apprehension, as the latest discussion about Huawei’s 5G technology shows (Guarascio and Yun Chee, 2018). Chinese companies, be they private or state-owned, are strongly linked to the government. State-owned enterprises (SOEs) in particular are subject to strict government scrutiny, not least because personnel and career decisions are to a large extent taken by the government, whereas senior executives of the most important SOEs are appointed by the Chinese Communist Party (Leutert, 2016). Chinese OFDI provokes fear for reasons of military strategy as China is not a member of the West’s security alliances (Meunier, 2019). The country’s fame for breaching intellectual property (IP) rights and carrying out cyberattacks against Western private and public entities does not do it any good either (Konrad and Kostka, 2017; NBAR, 2017).

Apprehension is severe when Chinese investments target a country’s critical infrastructure, i.e. assets or networks that constitute a vital backbone of the economy and the functioning of the public sector (OECD, 2008). Recently, Australian lawmakers, following a series of Chinese acquisitions in the nation’s electricity grid, had none of it and required tougher scrutiny of such investments (Masters and McBride, 2016). Even in Germany, traditionally open to international capital, the debate around national security with respect to Chinese OFDI is gaining pace (Stanzel, 2017).

To answer where security considerations begin to truly materialize, we have conducted an in-depth investigation of a concrete Chinese investment (our case study). In 2014, a subsidiary of State Grid Corporation of China (SGCC), the largest utility company on the globe, acquired a 35% stake in the Italian holding company, CDP Reti, which controls, among other things, the national electricity grid. The minority stake cost SGCC €2.1b, making it the largest investment undertaken by the Chinese utility. The transaction is of relevance, not only because of CDP Reti’s strategic position within the Italian and European energy system, but also because of several provisions accompanying the deal that grant SGCC representation on the board of directors of CDP Reti and its most important subsidiaries. This gives rise not only to security concerns, but also raises the question whether the investment was motivated by financial considerations or rather followed a geopolitical agenda.

On the basis of our research, the paper makes a number of contributions. First, it uncovers whether the investment was grounded on financial terms. The conclusion will be affirmative. CDP Reti distributes dividends that are in line with the above-average dividends that utilities traditionally hand out (Ross, 2014). Hence, this confirms the strand of the literature that finds Chinese OFDI in Southern Europe’s energy sector to be motivated by market and asset-seeking strategies (Pareja-Alcaraz, 2017).

Second, the paper analyses the deal for its national security risks. The inquiry extends to the EU level. This is justified by the fact that energy markets, particularly electricity grids, cross borders. The literature has voiced concerns over the presence of Chinese representatives on the boards of critical European companies (Kamiński, 2017). However, as will be shown later, in the case of SGCC’s investment in CDP Reti such threats do not materialize yet. This finding should alleviate some of the concerns in Italy (and beyond) surrounding national security.

Nonetheless, in the final part of the paper we also tackle the geopolitical dimension of the acquisition. Rather than investigating what the transaction means for the present day, we explore the increasing importance of electricity grids in the geopolitics of energy. Based on a ‘thought experiment’, the contribution that we are trying to make is that control over electricity grids is not an indispensable precondition for a country to exert geopolitical power over another nation. Rather, what is needed is a framing power over the strategic development of a country’s grid. When the terms of a foreign investment grant the foreign country with such influence over a nation’s electricity grid, FDI therein can in the future effectively represent a means of geopolitical influence. Since the board members that represent SGCC can in the present case at least partly influence what investments CDP Reti and its subsidiaries should undertake in the future, we argue that the transaction under scrutiny does grant China geopolitical influence over Italy’s and Europe’s electricity grid. Moreover, this potential future influence could also indirectly introduce national security risks through the backdoor.

The paper is structured as follows. The section ‘FDI and ‘national security’’will focus on the literature that has covered the field of FDI and national security. It will provide the framework of analysis against which the investment by SGCC in CDP Reti will be examined. The section ‘Our case study: the acquisition of a 35% participation in CDP Reti by SGCC’ will analyse the acquisition of the 35% stake in CDP Reti by SGCC. It will do so against the national security framework provided by Moran and Oldenski (2013). Finally, drawing on the work of Scholten and Bosman (2016) the case study will be used to analyse the future of energy geopolitics with respect to influence over electricity grids. Finally, the section ‘Conclusion’ will wrap up with concluding remarks.

FDI and ‘national security’

The surge in Chinese investment in Europe has not gone unnoticed in Brussels. In delivering the 2017 State of the Union speech, the President of the European Commission, Jean-Claude Juncker, called for the creation of an EU-wide screening process for foreign takeovers (European Commission, 2017). Energy infrastructure was explicitly mentioned as one of the ‘strategic’ sectors that deserve protection. In this sense, the most relevant development for our research is China’s interest in acquiring relevant shares in the companies that control the electricity grid of EU Member States. It did so in Greece, Italy, and Portugal (AEI and Heritage Foundation, 2017).

Needless to say, investments of this kind have been met with anxiety. For instance, Konrad and Kostka (2017: 645) highlight that there are ‘growing concerns among policymakers and business managers in Europe, ranging from worries about unfair competition and economic risks to concerns about national security’ in multiple aspects.

First, there is the risk of state intervention. SOEs are predominant actors in Chinese outbound foreign direct investment (COFDI). For example, Hanemann and Huotari (2015) found that in 2015, out of €46b of Chinese OFDI pouring into the EU, €31b came from SOEs. A major concern with respect to the role of SOEs is their close connection with the government. To this date the Central Organization Department (COD) nominates the executives of the most important SOEs, whereas the State-Owned Assets Supervision and Administration Commission in cooperation with the COD does so for the remaining SOEs (Leutert, 2016). Hence, even firm-level investment decisions can be ‘in line with the national environment and strategy’ (Wang and Huang, 2012: 15).

Furthermore, the financing of COFDI also grants the government influence over SOEs investing abroad. Le Corre and Sepulchre (2016) argue that, contrary to how Western businesses operate when investing abroad, the Chinese overseas investment spree is characterized by reliance on debt rather than firms’ own capital. Three different entities are particularly relevant in this respect: China Development Bank, Chinese State funds, and the four largest state-owned Chinese banks: Industrial and Commercial Bank of China, Bank of China, China Construction Bank and the Agricultural Bank of China. These entities stand ready to help Chinese enterprises that cannot get sufficient financing from European banks.

Second, there is apprehension that the ‘government-guided and state-supported attack on European technology leadership will hurt Europe’s long-term competitiveness and harm competition-driven global innovation dynamics’. Third, there are investment imbalances between Europe and China, also in the energy sector. Fourth, national security concerns arise given that ‘[e]nergy infrastructure is a sector with direct security implications’ (Konrad and Kostka, 2017: 646–647). Such concerns are exacerbated by the growing digitalization of energy systems. Moreover, the fact that China operates outside of Europe’s alliance schemes (in particular NATO) together with its reputation for cyberattacks and the country’s notoriety for IP theft increase the need for suspicion (NBAR, 2017).

Fifth, there is a risk of political influence by China over Member States that are exposed to Chinese investments in the energy sector. Specifically, Meunier (2014) argues that with persistent sluggish growth, China can use FDI towards Europe to ‘divide and conquer’ a fragmented EU. Hence, Chinese OFDI could affect the European institutional processes, should some Member States become dependent on Chinese OFDI. This would give China considerable leverage to steer in its favour political decisions taken at the European level. In recent years we have seen how Chinese investments in Europe linked to its ambitious Belt and Road Initiative (BRI) have already made countries such as Greece and Hungary unwilling to join the rest of Member States in taking a harder line against Beijing in the South China Sea disputes (Seaman et al., 2017).

Finally, the installation of Chinese board members on European energy companies is looked at with suspicion. Kamiński (2017: 735–737) analysed a case where the agreement accompanying a Chinese acquisition granted the Chinese investor the right to designate two of the seven members of the board of directors, which, according to the author, gives it ‘access to the company’s secrets, sensitive information as well as direct influence on the management’. This leads Kamiński to describe Chinese SOEs as ‘tools of economic statecraft’ potentially used for ‘sabotage of critical energy infrastructure’.

All the aforementioned concerns were also voiced with respect to the case study of this research. To make just one example, the Italian news outlet, Il Giornale, points to a reference made by Alberto Forchielli, founder of Mandarin Capital Partners, that the goal of Beijing is to create a divide between Europe and the USA (Filippi, 2014).

Despite all these challenges, several authors argue that COFDI is far from ‘malicious’. Cernat and Paraplies (2010) of the European Commission posit that Chinese OFDI is mainly driven by commercial considerations. Seaman et al. (2017) also see the benefits in terms of financing, employment and research and innovation. Others believe that it is important to avoid that national security considerations are used as a means to block Chinese investments from happening altogether (Ranger, 2017).

In this regard, it is interesting to note that Tingley et al. (2015: 27–29), referring to the USA, ‘find that there is more likely to be opposition to Chinese M&A attempts in security sensitive industries, economically distressed industries, and sectors in which US companies faced restrictions in China’s M&A markets’. Given that Europe has similar endowments to the USA in terms of economy, technology and market-size, it is reasonable to believe that similar trends are arising in European political circles.

Legislation that limits foreign investment on security grounds must be finely tuned against the macroeconomic benefits that FDI is generally believed of creating. Foreign investments are ‘often regarded as generators of employment, high productivity, competiveness, and technology spillovers’ (Denisia, 2010: 53). Moreover, policies that scrutinize foreign investments over national security considerations ‘defy a straightforward cost-benefit analysis and can mask economic protectionism’ (Jackson, 2013: 19). On the other hand, as Lenihan (2018) points out, government intervention in cross-border acquisitions is a rising trend as this form of economic statecraft acts as a vehicle of internal balancing and preservation of economic strength through non-military means. In keeping with this view, she also indicates that this form of intervention derives from economic nationalism or pressing geostrategic concerns, which is effectively the new International Relations context we are experiencing.

Limitation of FDI on ‘national security grounds’

The mood and rhetoric around inward FDI in many capitals has changed in recent years. For instance, Australia increased the security vetting of foreign acquisitions following a wave of Chinese deals targeting its critical infrastructure such as electricity grids (Masters and McBride, 2016). Public views of foreign acquisitions are also strikingly negative, especially in advanced economies. A 2014 Pew Research survey of 44 countries found that at the median level only 45% of respondents considered foreign takeovers to be positive. In Germany, only 19% of the population thought such deals were good, whereas an impressive 79% voiced concerns. In Italy, the country of our case study, the values stood at 23% and 73%, respectively. In the USA, 67% of the public viewed the acquisition of local companies by foreign entities negatively (Pew Research Center, 2014).

Against this background, we analyse the security concerns that might arise in our case study under the framework developed by Moran and Oldenski (2013). The authors provide a benchmark made up of three threats against which to assess foreign investments for their national security implications. These threats are (a) denial of goods or services crucial to the functioning of the economy (Threat I); (b) leakage of sensitive technology (Threat II); and (c) infiltration, espionage and disruption (Threat III). While the framework is originally referred to the USA where national security issues are prominent in the literature due to the vetting process of foreign investments by the Committee on Foreign Investments in the United States (CFIUS), it can easily be transposed to European national settings and to the EU level.

Under Threat I, the target enterprise is vital in the supply of crucial goods or services for its host country. A takeover would make the country dependent on a foreign entity that now controls these goods or services. Under Threat II, the country of the investor acquires technology or know-how that can be used to harm the national interests of the target country. Finally, under Threat III, a takeover enables the investor and/or its home country to infiltrate, surveil or sabotage critical elements of the target country’s economy (Moran and Oldenski, 2013).

The analysis that crystallized around Threat I focuses on whether a foreign takeover could cause an excessive degree of dependence of the host economy on a foreign supplier. This happens if (a) the goods or services now provided by foreigners are critical for the economy to function and (b) the provision of the goods or services can realistically be withheld or made conditional.

As for Threat II, Moran and Oldenski point out that it is almost inevitable that management or manufacturing expertise flows to the foreign entity with an acquisition. Similarly, it is basically unavoidable that this newly acquired expertise increases the foreign country’s defence and even military capabilities. Therefore, the test on Threat II must investigate the extent to which the newly obtained know-how is already available and whether the acquisition is decisive for the foreign government to acquire it. Mostly, it will be exclusive capabilities that can trigger a plausible threat if their deployment can damage the host country’s national interests. Finally, with respect to Threat III, concerns arise if a foreign government can use a takeover for covert espionage or disruption.

‘Critical infrastructure’

With respect to the scrutiny of foreign investments over national security concerns, critical infrastructure has become a prominent area of attention. The OECD grants governments broad operational margins in the definition of ‘critical infrastructure’ (OECD, 2008).

In the USA, the Foreign Investment and National Security Act of 2007 included critical infrastructure in the definition of national security that triggers the review of incoming FDI by CFIUS (Jackson, 2013). Importantly, the definition of critical infrastructure encompasses the energy sector, including electricity grids (Department of Homeland Security, 2016). Consequently, a potential grid-related foreign takeover has to withstand the scrutiny by CFIUS (Akin Gump Strauss Hauer & Feld LLP, 2018).

The EU takes a substantially different approach. Even the recently adopted FDI screening regulation 1 establishes that Member States alone will be responsible for the maintenance of national security (Article 1(2)) and are not required to establish an FDI vetting system (Article 3(1)). It simply aims at providing a ‘framework for the screening by the Member States of’ FDI into the EU ‘on the grounds of security or public order’ (Article 1(1)). However, under certain circumstances Member States and the Commission are able to, respectively, comment or issue an opinion on an FDI into another country which the latter has to take into due consideration (Articles 6 and 7).

The fact that the ultimate responsibility for an FDI screening mechanism rests at the national level and its optionality reflect the compromise that was necessary to appease the opposing views on COFDI among Member States. Some countries (e.g. Germany, France, the UK, Italy, Spain and Poland) are in favour of a screening mechanism, whereas others (e.g. Greece, Hungary, Austria, the Czech Republic, Finland and Malta) are more wary thereof (Le Corre, 2018). The different positions stem from the fact that the EU is broadly divided into three groups of countries: the poorer countries from central eastern and southern Europe which are eager to attract more FDI, especially from China; the northern, export-oriented countries, which are concerned about a protectionist spiral and are, therefore, suspicious of more intrusive investment vetting mechanisms at the European level; and the larger economies, which have great interest in limiting the influence of external powers, again, particularly China, but also Russia, in the periphery of the continent and want to protect their high-tech and industrial sectors (Seaman et al., 2017).

For what matters here, the FDI screening regulation makes the potential effects of an FDI on critical energy infrastructure relevant in determining whether security or public interest is affected (Article 4(1)(a)). Critical infrastructure, in turn, is defined by Directive 2008/114/EC of 8 December 2008 as ‘an asset, system or part thereof located in Member States which is essential for the maintenance of vital societal functions, health, safety, security, economic or social well-being of people, and the disruption or destruction of which would have a significant impact in a Member State as a result of the failure to maintain those functions’. One can speak of ‘European critical infrastructure’ (ECI) when the disruptive effects also impact other Member States (Article 2).

Most importantly, the FDI screening regulation allows the Commission to issue an opinion if it considers that an incoming investment ‘is likely to affect projects or programmes of Union interest on grounds of security or public order’ (Article 8(1)). In this case, the Member State concerned has to ‘take utmost account of the Commission’s opinion’ (Article 8(2)(c)). In this regard, the relevant Union projects include the Trans-European Networks for Energy, which aims at ‘linking the energy infrastructure of EU countries’ including electricity grids (European Commission, n.d.).

In sum, the primary responsibility for screening inward FDI within the EU rests with the individual Member States. In Italy, such a screening mechanism is in place and focuses on the so-called ‘golden powers’ that the government can exercise with respect to certain transactions involving strategic companies (Inzaghi and Piermanni, 2012). The strategic sectors cover, on the one hand, defence, national security and, on the other, energy, transport and communications (Camera dei Deputati, n.d.).

In the energy sector, the government can veto decisions concerning strategic assets or impose conditions with respect to company acquisitions by non-EU subjects and, in exceptional cases, even oppose such investments (Camera dei Deputati, n.d.). The national electricity grid is among the relevant strategic assets that could warrant the exercise of these golden powers (Article 1(2)(c), Decree of the Council of Ministers 25 March 2014, no. 85). There are three further powers of the government worth mentioning. First, the bylaws of companies operating in strategic sectors, including energy, and that are controlled by the state can foresee a limit to shareholding possessions by a single shareholder of no more than 5%. Second, in companies with a government participation, the latter can effectively neutralize attempts of hostile takeovers by creating special classes of shares that can be used to increase capital against such takeover attempts (so-called ‘poison bill’). Finally, Cassa Depositi e Prestiti (CDP) can take on participations in strategic companies (Di Benedetto, 2015).

Geopolitical implications of the acquisition

We believe that the analysis underlying our case study will help future research in further uncovering the geopolitical component of FDI in critical infrastructure. The insights that can be gained from this are essential in untying part of the geopolitical ramifications of COFDI in sensitive industries that increasingly cause anxiety. To begin with, geopolitics deals with analysing how geographical aspects of an actor, traditionally a state, and its political processes influence each other and how this impacts the actor’s relationship with other actors (Cohen, 2003). With respect to energy relations, the definition focuses on ‘the way countries influence one another through energy supply and demand’ (Paltsev, 2016: 390). The key, therefore, is influence.

Of course, electricity grids can only assume a relevant geopolitical role if they are susceptible of being a tool of influence. It must be pointed out that in the current energy regime, traditional energy relations are conducted through a neo-realist lens focusing on conflict and, specifically, the hunt for oil and gas (Westphal, 2006). An exemplification is given by Klare (2001) who makes clear that conflict over resources is common place globally and involves all major powers which have a key interest in the continuous flow of energy and especially oil supplies.

However, it is important to note the dynamism of energy markets and their foreign policy and global governance (Pascual, 2015). They change over time and adapt to new circumstances, as we might be currently witnessing. This time, though, instead of resources it will be energy infrastructure to occupy the centre stage. In this setting, it is reasonable to expect geopolitics to follow suit and increase the importance of both electricity grids and renewable energy.

The geopolitical implications of both renewables and electricity grids are increasingly being explored in academia. Fischhendler et al. (2016: 533) carried out a study that aimed at identifying ‘the geopolitical dimension of cross-border electricity grids’ and found ‘that electricity geopolitics has been used both as a platform for deeper international cooperation and as a stick against neighboring states. When policies are driven by a peace dividend, proposals for grid connection appear to evolve and overcome the dependency and the security-economy bottlenecks’. We build on their work by investigating not the geopolitical consequences of physical electricity grids, but of foreign investments made therein. Banks and Ebinger (2010) argue that ‘China’s growing influence is not all about military power; it is also about how China is going to find the energy and water needed to feed its rapid economic growth, and specifically how will it find clean electricity’.

As for renewable energy, writings on its geopolitical dimensions have gone so far as to see a ‘green energy race’ under way between the USA and China (Eisen, 2011). More convincingly, Paltsev (2016: 390) argues that with the rise of renewable energies, ‘supply-side geopolitics are expected to be less influential than in the fossil-fuel era’. In fact, ‘low-carbon energy geopolitics may depend on many additional factors, such as access to technology, power lines, rare earth materials, patents, storage, and dispatch, not to mention unpredictable government policies’. Therefore, it is plausible to expect countries engaged in developing alternative energy sources to gain the upper hand in the balance of power. Moreover, the countries that can produce low-carbon energy most efficiently are likely to enjoy a particularly substantial degree of geopolitical power. It appears that the EU is anticipating such a shift of power. Valdés et al. (2016: 1043) find ‘that variables related to energy security play a significant role in the development of renewable energy in the EU’, even more so than environmental considerations.

Hübner (2016: 3) also points out that with the energy transition what counts are ‘networks and energy storage possibilities’. Importantly, he argues that ‘[i]n the internal relations of a regional cooperation, control over energy grids and storage capacities will decide who will become a player in energy policy’ (Hübner, 2016: 7–8). Finally, he points out that the shift towards renewable energy could ‘redraw the global energy map permanently’ 2 .

Our research delves precisely into the redrawing of the energy map. The analysis does not focus on whether energy dependencies are going to be eroded or not. Rather, what is proposed is a new layer of energy interconnection driven by international investments in energy infrastructure. We argue that such investments can create a form of interconnection where two or more countries are linked not by physical infrastructure, but by the stake that one or more of them have in the infrastructure of the other.

While ‘the geopolitics of both traditional and renewable energy will coexist for quite a while’ (Paltsev, 2016: 394), one should not overlook the fact that the capacity of renewable energy sources is far from fully exploited (Criekemans, 2011). For instance, the International Energy Agency (IEA) in 2016 released a special edition of the World Energy Outlook that found that ‘[r]enewable energy technologies are now a major global industry’ and have ‘overtaken coal as the largest source of power generation capacity and are the second-largest source of electricity supply’ (International Energy Agency, 2016: 397). Moreover, one of the scenarios considered by the IEA (2016) makes renewable energy the major source of electricity supply before 2030.

Against this backdrop, Scholten and Bosman (2016: 273) carried out a ‘thought experiment’ to assess the geopolitical consequences of a world that is entirely powered by renewable energy. They point out that given the ‘easy’ conversion of powerful renewables into electricity, electricity will be ‘the dominant energy carrier, implying a more physically integrated infrastructure with stringent managerial requirements’ (Scholten and Bosman, 2016: 277). The authors then distinguish between a national and a continental scenario. In the latter which is the one of interest for our case, one can expect ‘a strategic focus on the infrastructure (and accompanying markets) [. . .]. Consequently, producer, consumer, and transit countries will have an interest in physical grid assets as it allows to exert influence over electricity flows, and in turn markets’ (Scholten and Bosman, 2016: 279). With a shift in power from the source of energy to the distribution thereof, the influence over the latter will be crucial.

Scholten and Bosman (2016: 279) mention two major consequences stemming from a situation where electricity grids become a fundamental focal point. First, energy security issues, which connect countries on different continents such as securing shipping lanes, will become irrelevant. Instead, geopolitical interconnection will play out at a more regional level with the emergence of ‘grid communities’. Second, ‘power struggles will focus on acquiring ownership and decision rights with regard to the grid and its management’. A key question will then be ‘[w]ho finances projects?’ This discussion is even more relevant today given that under the macro geostrategy of the BRI, China has put forward the ambitious plan to establish a Global Energy Interconnection (GEI) initiative, with more than $100b already invested in more than 80 projects in Latin America, Africa and Europe (Kynge and Horby, 2018), and with the establishment in 2016 of the Global Energy Interconnection Development and Cooperation Organization (GEIDCO), ‘which works towards promoting the establishment of a global energy interconnection system (GEI) to meet the global demand for electricity in a clean and green way, as well as to implement the United Nations Sustainable Energy for All initiative’ (UNFCCC, 2019).

Based on our case study, we argue that when the right circumstances are met, FDI in electricity grids can give the investing country significant leverage over the development of the beneficiary’s infrastructure. We learned that when FDI is carried out by a company closely linked to the government, as is the case with Chinese SOEs, it is reasonable to expect that the home country of the investor exerts a guiding power over the company. The government of the investing firm, then, can exert influence over the target company if the terms of the investment give the investor some leverage over the management of the enterprise. This leverage does not have to come in the form of direct control. Leverage over management translates into influence over the development of the electricity grid in countries where the target company enjoys a near-monopoly position with respect to the electricity transmission system.

Our case study: the acquisition of a 35% participation in CDP Reti by SGCC 3

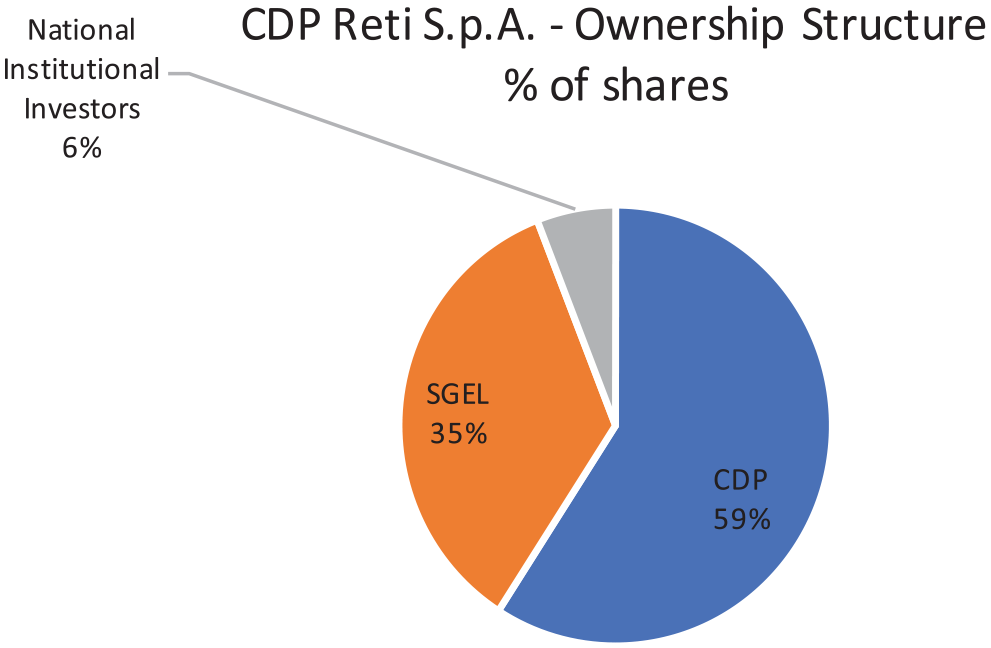

On 27 November 2014 CDP announced the transfer of a 40.9% stake of CDP Reti S.p.A., of which 35% to State Grid Europe Limited (SGEL), entirely owned by SGCC, and the rest to a series of national institutional investors 4 (CDP, 2014; see Figure 1 for the ownership structure of CDP Reti). This investment marks the entry of a Chinese institutional player (SGCC), wholly owned by the Chinese state, in the national electricity grid of Italy. The acquisition is accompanied by provisions that grant SGEL the power of appointing members of the board of directors of CDP Reti and its subsidiaries.

Source: CDP (n.d.)

The installation of board members reminds us of the concerns expressed by Kamiński who described Chinese SOEs as ‘tools of economic statecraft’ (2017: 735–737). This prospect, in turn, raises two of the three national security threats identified by Moran and Oldenski (2013): Threat II concerning the leakage of sensitive technology and Threat III regarding infiltration, espionage and disruption. Moreover, it also raises the issue of protecting the critical infrastructure of both Italy and the EU.

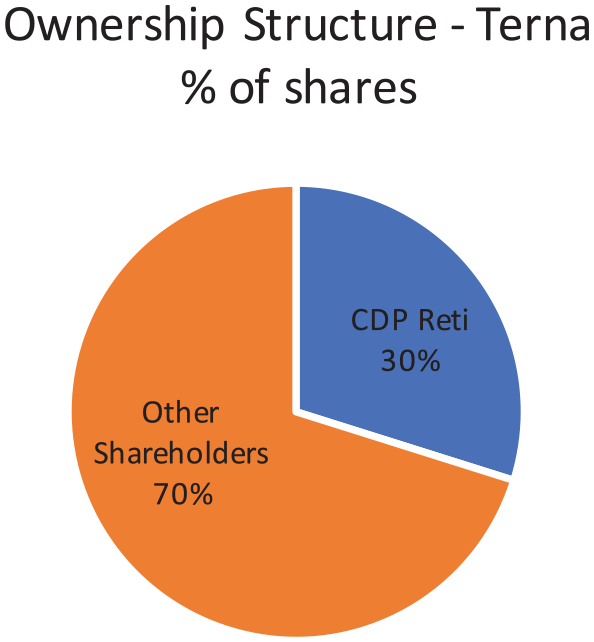

CDP Reti runs Italy’s electricity (and gas) infrastructure via its subsidiaries (mainly Terna, Snam and Italgas). Among them, Terna (see Figure 2 for its ownership structure) is of particular relevance since it operates and owns 99.6% of the high-voltage electricity National Transmission Grid of Italy 5 via its subsidiary, Terna Rete Italia. In terms of Italy’s electricity supply chain, Terna operates in the level of transmission and dispatching. With more than 72,000 km under management, it is one of the largest electricity operators in the world (CDP Reti, 2017). The nature of activities carried out by CDP Reti and its subsidiary would have enabled the Italian government to exercise its ‘golden powers’ with respect to the acquisition by SGEL. However, it decided not to do so (Senato della Repubblica, 2016).

Ownership structure of Terna.

The company is also active abroad, for instance, in the construction and operation of the Italy–Montenegro Interconnection, which will grant Terna the possibility to control the transmission of renewable energy from the Balkans to central Europe (CDP Reti, 2017).

On the other side, SGCC prides itself with being the ‘largest utility of the world’ servicing 1.1b people in China (SGCC, n.d.). The company ranks second on the Fortune Global 500 of 2018 where it is reported to generate revenues of US$348b. Its core business is that of the construction and operation of power grids, also abroad.

Interestingly, the company is behind the goal of establishing the GEI initiative under the BRI mentioned earlier. And SGCC’s long-standing Chairman, Liu Zhenya, was quoted to have stated that this project could lead to ‘a community of common destiny for all mankind with blue skies and green land’ (Minter, 2016). The seriousness of the project was demonstrated by the fact that the President of China, Xi Jinping, himself announced the opening of a ‘discussion on establishing a global energy network’ at the 2015 United Nations Sustainable Development Summit in New York (MFAC, 2015), which eventually led to the creation of the aforementioned GEIDCO, which is now chaired by the same Liu Zhenya after leaving SGCC.

The installation of board members by State Grid Corporation of China

The articles of association (AoA) of CDP Reti (CDP Reti, 2016b) and the shareholder agreement (SA), which entered into force on 27 November 2014 and which were subsequently amended in 2017 (Snam and Terna, 2014, 2017), grant SGEL extensive corporate governance rights. They cover CDP Reti as well as Snam, Italgas and Terna.

With respect to CDP Reti, the agreements are worded in such a manner that SGEL has the right to nominate two out of the five members of the company’s board (Article 15(5) AoA). However, the chairman and the CEO are selected from the board members designated by CDP (Article 16(1)). The current members of CDP Reti’s board nominated by SGEL are Yanli Liu and Yunpeng He (Bloomberg, 2019). SGEL can also name members on the boards of Terna, Snam and Italgas. Currently, Yunpeng He figures in all three of these subsidiaries (Italgas, n.d.; Snam, 2017; Terna, n.d.).

It is important to mention that Article 4(1) of the SA states that with respect to the board members of Snam, Italgas and Terna designated by SGEL, the Chinese investor pledged that they would abstain themselves from obtaining information and/or documents relating to matters where SGEL could have a conflict of interest. These members will also abstain themselves with respect to operations by Snam, Italgas and/or Terna where SGEL could be a competitor. The board members nominated by SGEL cannot take part in the relevant meetings of the board. Moreover, SGEL cannot buy any participation in Snam, Italgas and/or Terna without the previous written consent by CDP (Article 4(2) SA).

Furthermore, SGEL can influence decisions of corporate strategy, such as the taking on of debt (including guarantees to third parties) if (a) the amount exceeds €100m and/or (b) the operation violates certain financial covenants and ratios. Such operations have to be approved by at least one of CDP Reti’s board members nominated by SGEL (Article 19(5) AoA). In addition, in terms of access to information both CDP and SGEL can obtain a copy of the non-audited accounting entries (Article 23(2) AoA).

Financial considerations of the acquisition

As was mentioned, SGEL spent €2.1b for the 35% stake in CDP Reti. The significance of this disbursement raises the question whether the investment is at all financially motivated or rather follows political and/or strategic goals only. Typically, China’s investments in the energy markets of Southern Europe are considered to be motivated by market and asset-seeking (Pareja-Alcaraz, 2017). Is this true in the present case?

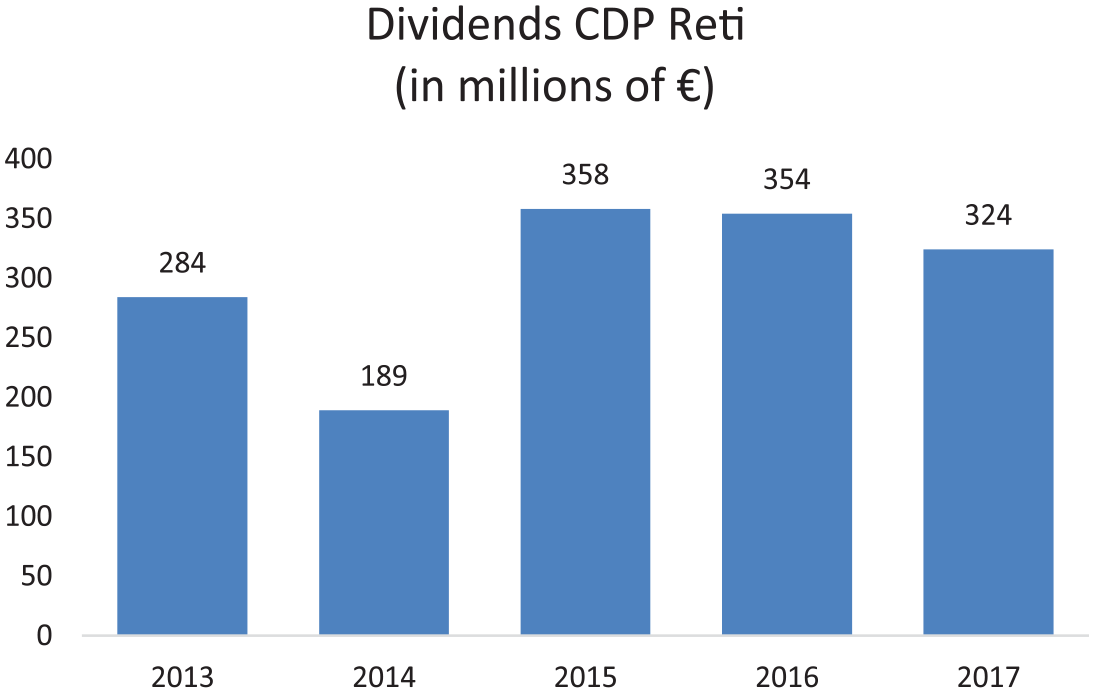

Given that CDP Reti was established only in October 2012, only limited financial data is available. However, the financial statements published thus far suggest that the company’s dividend policy is rather generous and, therefore, in line with a general trend in the utility sector (Figure 3). It should be noted that in 2017 alone, an interim €113m were paid to SGEL (CDP Reti, 2018).

Sources: CDP Reti (2014, 2015, 2016a, 2017, 2018).

The fact that SGEL can expect a steady and significant annual flow of dividends makes it possible to say that the investment in CDP Reti is motivated by financial considerations. Of course, the question arises whether the expectation of a return on the investment constituted the sole reason for the transaction. It is not unconceivable that the installation of board members follows a logic of an attempt by China, via its SOE, to gain influence over Italy’s and Europe’s electricity grid. It is important, therefore, to answer the question whether the investment under scrutiny falls within the security threats identified by Moran and Oldenski (2013).

National and European security considerations of the acquisition

Even though there is no definition of ‘national’ security at EU level 6 , the present case allows one to treat security considerations of Italy and the EU in conjunction. As was mentioned, Directive 2008/114/EC includes electricity transmission in the definition of ECI. Moreover, electricity grids in Europe are not confined to national boundaries (Global Energy Network Institute, 2016; see also Figure 4).

Physical energy flows in gigawatt hours (in Southern Europe).

Threat I: Denial of goods or services vital for the economy

It appears that the denial of crucial goods or services is not a menace in this case. To be sure, CDP Reti’s subsidiaries represent the national distribution network of electricity and gas. Therefore, the condition that the service provided by the target company be crucial for the functioning of the Italian economy is given. However, we saw that for Threat I to materialize it is necessary that the goods or services can realistically be withheld. The presence of exponents of SGEL on the board of CDP Reti and its subsidiaries might spark dismay in this regard. However, they are not in direct control of the company. In fact, the respective CEOs and/or chairmen, who cannot be exponents of SGEL, are in charge of operational matters. Moreover, SGEL cannot buy any participation in Snam, Italgas and/or Terna without the prior written consent by CDP (Article 4(2) SA). Therefore, it is difficult to imagine that SGEL can ever control Italy’s electricity and gas distribution infrastructure to the point of withholding it. Since disruption is not a concern in Italy, Threat I does not materialize on the European level either.

Threats II and III: Leakage of sensitive technology; infiltration, espionage and disruption

Of more concern are Threats II and III. It is not unreasonable to think that exponents of a state-owned Chinese strategic company might, directly or indirectly, use their position to acquire sensitive information and/or carry out espionage on the critical infrastructure of Italy and, in turn, Europe. This is all the more conceivable given the increasing progress the EU is making in building smart grids. Importantly, the communication by the Commission of 28 August 2013 specifically declares smart grid threats as a high-priority concern (European Commission, 2013).

The problem arises because the operation and control of smart grids rely on information and communication technology. This makes them vulnerable to cyberattacks. As a matter of fact, such incidents have already occurred (Xie et al., 2016). In addition, there are concerns over the privacy of consumers as smart grids constantly collect data to enhance the efficiency of energy supply (He et al., 2016). It is important to note that Terna is actively involved in smart grid innovation projects, which constituted a key element in its 2015–2018 strategic development plan (Terna, 2016).

It could be argued that access to information, particularly sensitive documentation, can constitute an important threat. Holding confidential information on the operative mechanisms of the Italian and, therefore, partly European electricity distribution network can facilitate potential cyber and/or physical attacks against this network. It is, therefore, fundamental to establish whether SGEL can easily access such information. Given SGCC’s close ties with the government, this could be used by China for both transfer of technology (Threat II) and espionage and, potentially, infiltration (Threat III).

Under Italian law, the information streams between executive and non-executive board members (the position of SGEL) are regulated by Article 2381(6) of the Italian Civil Code. This provision states that ‘[a]ll directors must perform their duties in an informed way’. In addition, each board member can ask the delegated bodies to provide ‘specific information about the company’s management in board meetings’. In this respect, it is the chairman’s responsibility to make sure that sufficient and accurate information is provided to the members of the board ahead of meetings (Ferrarini et al., 2013).

The wording of Article 2381(6) is such that it is the executive member of the board who has direct and unlimited access to the integral company documentation. Other board members simply have the power – not the right – to explore, ask for and obtain the information and elements that are required for an appropriate awareness of the management of the company (Perone, 2013). Most importantly, non-executive board members do not have the power to inspect individually the company documents and/or to ask for them directly to the employees of the corporation. This interpretation of Article 2381(6) Civil Code enjoys the support of the Italian jurisprudence. The mainstream view, heralded by the Court of Milan, holds that the possibility for non-executive board members to ask executive directors for supplemental information encounters serious limitations (Tribunale di Milano, 2012). For instance, Meruzzi (2010) posits that the content of the information streams must be adapted to potentially accommodate other principles necessary for the pursuit of the corporate interest.

The provisions of the SA (Article 4(1)) that oblige SGEL’s board members to abstain themselves from obtaining information and/or documents relating to potential conflicts of interest of SGEL further support the impression that the risk of leakage of sensitive information is limited. That Article 23(2) AoA gives SGEL the right to obtain a copy of the non-audited accounting entries does not do away with this 7 .

These considerations indicate that, absent illicit behaviour on behalf of the board members designated by SGEL and/or collusion with their Italian counterparts, SGEL faces a difficult legal environment for obtaining confidential information. Moreover, as the largest utility of the world, it is difficult to imagine that SGCC can gain expertise from the investment in CDP Reti that it could not also get elsewhere.

On Threat III, a further concern could be that SGEL’s exponents use their position to inject malware into the Italian grid undermining its proper functioning. However, given that they are not in charge of operational matters (see the earlier text), it appears unrealistic that they would be able to carry out such an operation on their own. The conclusion could be different if SGEL’s exponents were assigned an operational portfolio as part of their membership in the board of directors of CDP Reti and particularly its subsidiaries or if they were actively entrusted with overseeing hiring practices in sensitive company segments. From CDP Reti’s publications on its website, this does currently not seem to be the case 8 .

In sum, the conditions for Threats II and III do not appear to be met in the present circumstances. Since none of the threats seem to materialize (at least for now), one can rebuke the views of those who opposed the transaction on national security grounds.

Future geopolitical implications

However, we argue that the investment made by SGEL in CDP Reti fulfils the requirements to consider it a geopolitically relevant investment in a future world where renewable energy takes on more relevance. First, as was already mentioned, SGEL is closely linked to China’s government. Second, CDP Reti, i.e. Terna, enjoys a de facto monopoly over Italy’s electricity grid. Third, while the investment made by SGEL does not provide it with a direct control or veto power over the management of the CDP Reti Group (the approval of the group’s strategic plans does not require the consent of at least one exponent of SGEL), it does grant it leverage over certain resolutions.

On the one hand, certain investment plans made by the board of CDP Reti do require the consent of at least one of the exponents of SGEL. This is the case when the ensuing debt exceeds €100m (Article 19(5) AoA). This gives SGEL and, in turn, China considerable leverage over major investment projects in the Italian grid. In fact, it should be remembered that the development and maintenance of the electricity and gas infrastructure is the very corporate purpose of CDP Reti.

On the other hand, this leverage is further increased by the Italian legislation dealing with the inclusion, by minority board members, of elements in the agenda of board meetings. Italian jurisprudence and doctrine generally admit that every single board member can ask the chairman to include specific matters to be discussed by the board in the agenda (Morandi, 2011). Therefore, SGEL’s board members in the CDP Reti Group will have the power to ask for elements of debate, such as investment projects, to be included in the agenda of each board meeting. While not resulting in a direct decision-making power, this gives SGEL and, therefore, China a partial framing power with respect to, and thus influence over, what investments Italy’s national electricity grid will make.

The inclusion of topics in the agenda of board meetings has substantial implications. As a hypothetical scenario we can imagine that SGEL proposes to make investments in Italy for the GEI. Leaving aside legal requirements for public tenders, let us also assume that the investments would be channelled from SGEL to a subsidiary of the CDP Reti Group. Finally, let us imagine that the project brings substantial and undisputed economic benefits to the beneficiary.

To be sure, the Italian legislation on executive liability, in application of the business judgement rule, grants managers significant discretionary power: their decisions cannot be judged ex post on the sole basis of the economic outcomes (Corte di Cassazione, 1965, 1972). This would mean that an executive could simply decline the investment opportunity. However, Italian jurisprudence allows judges to decide on the method used by the manager to come to his/her conclusion. The executive has to use diligent means of instruction before taking decisions (Corte di Cassazione, 2004). Moreover, Italian courts have made it clear that executives can be held liable for conspicuously unreasonable actions (Tribunale di Milano, 1996) 9 . While it is not certain that a CEO would be necessarily held liable for rejecting an investment project as hypothesized earlier, it appears reasonable to expect him/her to accept the offer. This would give China considerable leverage over future developments in the Italian national electricity grid: it sits right where important decisions are debated and can influence these, even if not directly.

In reality, these considerations are in line with the second major consequence of the move towards renewable energy outlined by Scholten and Bosman earlier. Namely, that ‘power struggles will focus on acquiring ownership and decision rights with regard to the grid and its management’ where a key question will be ‘[w]ho finances projects?’ (2016: 279). China already holds some decision rights with regard to the grid and its management. The financing of investment projects could then become a means through which China exercises its influence over Italy’s critical electricity infrastructure. This type of influence is energy geopolitics at work. Moreover, since electricity grids cross borders, such transactions also reverberate through Europe and will indirectly impact fundamental decisions on the EU’s electricity distribution system.

Moreover, it is worthwhile to consider that with the framing power over Italy’s investments in the electricity grid SGEL, and thus China, might be able to deploy Chinese equipment that could be used for sabotage (e.g. by deploying malware into the system). Similarly, such equipment could be used for surveillance purposes (e.g. by measuring the electricity consumption or peak hours of key industries). In essence, Threat III that we excluded as a direct concern above could be ‘re-introduced’ through the backdoor – in the future.

Finally, it is noteworthy that the scenario outlined earlier could truly materialize with respect to Italy, given its potential for developing renewable energy capabilities. For instance, a recent paper ‘outline[d] a realistic energy transition roadmap for Italy in which the whole energy demand by 2050 is met by electricity generated by low cost renewable sources, mainly solar photovoltaic, wind, and hydroelectric, along with the highly sustainable solar thermal technology to generate low temperature heat’ (Meneguzzo et al., 2016: 23).

That China’s influence is only minor and not threatening in terms of national (and European) security does not do away with the fact that Beijing’s entry into Europe’s energy market adds an extra layer of complexity and could indirectly lead to security concerns. It appears that SGCC and China grasped the future importance of electricity grids and wanted to make sure to have a say in Europe. They effectively utilized the precarious financial situation of Southern Europe to invest in the electricity grids of Italy, Portugal and Greece. In Portugal, SGCC owns a 25% stake of REN, Portugal’s national electricity and gas transmission company, making it the largest single shareholder. In Greece, SGCC recently acquired a 24% participation in ADMIE, the operator of the Hellenic Electricity Transmission System, worth €320m (Bouras, 2016). Out of the currently nine members on ADMIE’s board, three, including the deputy CEO, are exponents of SGCC (ADMIE, n.d.). All these investments bring China’s ambition ‘to create an interconnected southern European grid’ one step closer (Kynge and Hornby, 2018) and thus are likely to raise even more eyebrows in Brussels in the coming years.

Conclusion

COFDI has recently caused heated debates among European commentators, policymakers and academics. This is not surprising. It is the first time that an emerging economy is investing heavily in a broad array of key industries of industrialized nations. In addition, for Western countries, the fact that China is not part of its military alliance scheme, that it has a poor record in the protection of human rights, its notoriety for cyber-espionage and its reputation for breaching IP rights make COFDI even harder to swallow. The heavy presence of Chinese SOEs in COFDI only adds to the worries since it is generally believed that the state holds firm control over their strategic management and that it could use its immense financial capacity for geopolitical gains in what is increasingly called China’s debt-trap diplomacy along the BRI. Finally, it is important to point out that China’s shopping spree is happening amidst growing concerns over China’s rise as a superpower (Mearsheimer, 2006).

Against this background, it is of paramount importance to analyse Chinese acquisitions of companies in key segments of the economy under a threefold lens. First, it is crucial to understand what drives such investments. When there is a financial motivation, concerns can be alleviated somewhat. Second, it is necessary to set clear parameters under which a Chinese acquisition can constitute a security threat. It should not be forgotten that FDI brings economic benefits and has the potential of bringing the world closer together. Third, given the changing dynamics of the international system, a critical inquiry must be conducted on the geopolitical implications of sensitive investments.

This research aimed precisely at carrying out such an analysis. It did so via a case study of an investment made in 2014 by SGCC, a Chinese SOE, in CDP Reti, an Italian holding company that controls the nations’ critical energy infrastructure, particularly the electricity and gas distribution networks, and is also active abroad. The case scrutinized here is particularly interesting because of the terms of the transaction. Although SGCC acquired only a 35% stake in CDP Reti and is, therefore, not the major shareholder, the Chinese company was granted the right to be represented on the board of directors (and the board of auditors) of key enterprises of the CDP Reti Group. This circumstance creates a distinct set of complexities, which sparked heated debates in Italy helping to push the Gentiloni government in 2017 to join France and Germany in asking the European Commission to start screening foreign investments in Europe. Therefore, it requires addressing the question as to what powers these Chinese board members have and, in turn, what that means for national and European security and geopolitics.

Our research first identified that the transaction is grounded on financial motivations. CDP Reti distributes generous dividends to its shareholders. In 2016 alone, SGCC perceived an interim €113m in dividends. This is in line with the literature that finds China’s investments in Southern Europe’s energy markets to be motivated primarily by market and asset-seeking strategies.

In a second step, drawing on the work of Moran and Oldenski (2013) – who argue that FDI can endanger national security when it leads to (a) denial of goods or services crucial to the functioning of the economy (Threat I); (b) leakage of sensitive technology (Threat II); and (c) infiltration, espionage and disruption (Threat III) – we have demonstrated that these threats do not materialize in our case study. SGCC does not have operational control over the critical infrastructure operated by CDP Reti and its subsidiaries and is not granted unlimited access to sensitive information.

Finally, our research has identified the potential geopolitical dimension of the transaction under examination. It has done so by placing the consequences of the investment in a hypothetical future scenario where renewables will be the prime source of energy. This scenario was outlined by a ‘thought experiment’ conducted by Scholten and Bosman (2016) who found that in such a context electricity grids will be of critical importance. In this regard the transaction analysed here could constitute a form of potential geopolitical influence. We found that the specific peculiarities of the CDP Reti case, particularly the powers granted to the board members that represent SGCC, can indeed lead to a geopolitical influence of China over Italy’s and, hence, Europe’s electricity grid development.

However, it is important to highlight that this influence is different from control, which would lead to a direct security threat. This distinction is of upmost relevance as it constitutes a novel insight into the world of geopolitics. In this regard, we argue that geopolitical influence is not confined to the physical control of resources and assets. Rather, it can come in the form of virtual and limited influence over key decisions on the development of important economic sectors. The distinctiveness of this form of influence centres on the fact that it is carried out not by military might, but by international capital movements, of which FDI constitutes a manifestation. Moreover, we argue that this type of geopolitical influence could lead to indirect security concerns.

Of course, this hypothetical future scenario constitutes a major constraint in our research. It will not materialize any time soon and might never do so. Nevertheless, some indications point towards an increasing trend that sees electricity grids acquiring ever more central importance, as the recently created, and very ambitious, GEI initiative led by China with its ultra high voltage (UHV) cable technology demonstrates. Moreover, in a world that is undergoing rapid and constant change and where the human species is racing against the incremental progress of technology, which also affects electricity distribution, it is pivotal to commence academic and policy debates about potential future trends in energy geopolitics. Future research should conduct similar case studies, primarily in Portugal and Greece where it should determine the motivation of the investments (financial and/or geopolitical), their fitness in terms of national (and European) security and their geopolitical implications. The future evolution of Italy will also remain important. Several observers have pointed out that the new Italian government is keener to cooperate more closely with China (Godement, 2018). It is too early to indicate whether this signifies a structural geostrategic shift away from Brussels and closer to Beijing. It might also be that the ‘China card’ is used as a negotiating tool to extract concessions from Brussels in terms of laxer fiscal discipline. For now, despite the political noise, we are not seeing major concrete moves by Rome other than symbolic gestures like agreeing to sign a memorandum of understanding regarding the BRI. In any case, Italy will remain a key country to observe in the grand scheme of the geopolitics of energy.

Footnotes

Acknowledgements

We would like to thank the two anonymous reviewers for their very useful comments and Ana María Barrenechea Kerin for her excellent research assistance.

Authors’ note

This paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.