Abstract

Drawing on institutional theory, this study tests how the ethical behaviors of firms, in interaction with public officials and through the strength of accountability regulations, influence sustainability reporting practices in the hospitality and tourism (H&T) sector. The results indicate that firms operating in a highly ethical business environment are less likely than those in a less ethical environment to disclose a sustainability report. However, accountability yields the opposite result; firms established in environments characterized by high accountability are more likely than low accountability environments to issue a sustainability report, which implies a complementary effect between the strength of the accountability and the firms’ sustainability disclosures. This verifies that the weakness or strength of informal and formal institutional forces exert considerable influence on firms’ desire to carry out sustainability reporting. However, this influence is not true of the acquisition of external assurance statements and following Global Reporting Initiative guidelines, with which accountability has a negative and insignificant association, respectively.

Keywords

Introduction

The hospitality and tourism (H&T) sector is among the biggest industries in the world and an important pillar for economic development. Tourism generates one in every 10 jobs worldwide and contributes 10% of the global gross domestic product (United Nations Environment Programme, UNEP, 2021). 1 Despite its economic and social benefits, the H&T sector is criticized for its negative environmental impact, including waste problems, pollution, and depletion of natural resources (De Grosbois, 2012; Scott et al., 2010). The United Nations argues that the H&T industry can increase pollution, lead to soil erosion, and destroy natural habitats and biodiversity (UNEP, 2021). 2 For example, tourism contributes more than 5% of global greenhouse gas emissions, 90% of which is from transportation. Every year, many millions of tons of plastic enter the ocean, to which the H&T sector contributes significantly. By 2030, the tourism emissions of carbon dioxide (CO2) are expected to increase by 25% compared to 2016, with 1998 million tons emitted compared to 1597 million tons in 2016. 3 By 2050, tourism is expected to generate an increase of 131% in greenhouse gas emissions, 251% in solid waste disposal, and 154% and 152% in energy and water consumption, respectively (UNEP, 2021). 4

To address these concerns, various initiatives have been undertaken, such as the One Planet Sustainable Tourism Program led by the UNEP and the United Nations World Tourism Organization (One Planet Sustainable Tourism Program, 2021) 5 . H&T firms undertake sustainability practices to become “greener” in ways that also offer potential environmental and economic benefits. Expedia Group and Accor, for example, signed an agreement with the United Nations Educational, Scientific, and Cultural Organization (UNESCO) to promote sustainable tourism (Hospitality on, 2021). 6

As the H&T sector has evolved over the years, the mentalities of its stakeholders have changed considerably. The corporate social responsibility (CSR) approach has gradually entered the culture of customers, suppliers, employees, and all stakeholders. Consumers increasingly question whether the products and services of the H&T industry meet certain social and environmental standards. The H&T sector’s contribution to the development of sustainability has become a central issue in the modern H&T industry. This context exerts pressure on H&T companies to act in socially and environmentally responsible ways (Guix et al., 2018; Uyar et al., 2020) and to invest in sustainability activities (Camilleri, 2016; Kang et al., 2012; Tan et al., 2017). Once these steps are taken, companies could publish information on their sustainability investments and practices to legitimize their activities (Benavides-Velasco et al., 2014; DiMaggio and Powell, 1983; Kim et al., 2017; Palacios-Florencio et al., 2018), establish a good alliance with their stakeholders (Ettinger et al., 2018), obtain a competitive advantage (Assaf et al., 2012; Cantele and Zardini, 2018; Horng et al., 2017), and enhance customer satisfaction (Palacios-Florencio et al., 2018; Gerdt et al., 2019). Although H&T companies make efforts to fulfill stakeholders’ expectations in terms of environmental and social information, there is a lack of consistency in the activities undertaken, reporting scope, and CSR accounting methodologies (Bonilla-Priego et al., 2014; Burns and Cowlishaw, 2014; De Grosbois, 2012). There are also gaps in the social and environmental information that companies provide to stakeholders (Perez and Rodríguez Del Bosque, 2014). For example, only 12 out of 80 cruise companies and 18 out of the 50 largest hotel groups in the world disclose CSR reports covering social, environmental, and economic information (Bonilla-Priego et al., 2014; Guix et al., 2018). Previous research has also indicated areas for improvement on sustainability reporting in the H&T context (De Grosbois, 2016; Kılıç et al., 2021; Koseoglu et al., 2021; Uyar et al., 2021a) and divergence among the factors that stimulate sustainability reporting (Kılıç et al., 2021; Koseoglu et al., 2021).

Drawing on institutional theory, numerous studies have attempted to understand why companies’ tendencies to report sustainability activities diverge (Briem and Wald, 2018; Kılıç et al., 2019; Martínez-Ferrero and García-Sánchez, 2017). Researchers have argued that companies publish sustainability reports in response to coercive, mimetic, and normative pressures (DiMaggio and Powell, 1983; Kılıç et al., 2019; Martínez-Ferrero and García-Sánchez, 2017). While previous studies on country-level institutional factors and firm sustainability decisions have been inconclusive, certain researchers have suggested a complementary relationship between firm sustainability initiatives and country-level institutional factors. Faced with high institutional pressures, companies disclose sustainability reports (García-Sánchez et al., 2016; Pucheta-Martínez and Gallego-Álvarez, 2020) with external assurance (Martínez-Ferrero and García-Sánchez, 2017) and following Global Reporting Initiative (GRI) standards (Nikolaeva and Bicho, 2011; Bravo et al., 2012) to comply with the institutional environment in which they operate. Other researchers, however, argue that firms use sustainability practices as a substitute for ineffective institutions when they operate in a poor institutional environment (Barkemeyer et al., 2018; Boiral et al., 2019; Kılıç et al., 2019).

Despite the increasing number of studies on sustainability, researchers have paid little attention to the H&T sector compared to other environmentally harmful sectors, such as industrial, manufacturing, chemical, and mining (Benavides-Velasco et al., 2014). Moreover, while it is necessary to understand the determinants of H&T sustainability reporting to better address reporting gaps, few studies have examined sustainability reporting in the H&T context (De Grosbois, 2012, 2016; Ettinger et al., 2018; Kılıç et al., 2021; Koseoglu et al., 2021; Uyar et al., 2021a). Both the significant environmental impact of the H&T sector and the various gaps in H&T companies’ CSR disclosures and practices, therefore, necessitate further consideration of sustainability reporting in the H&T context.

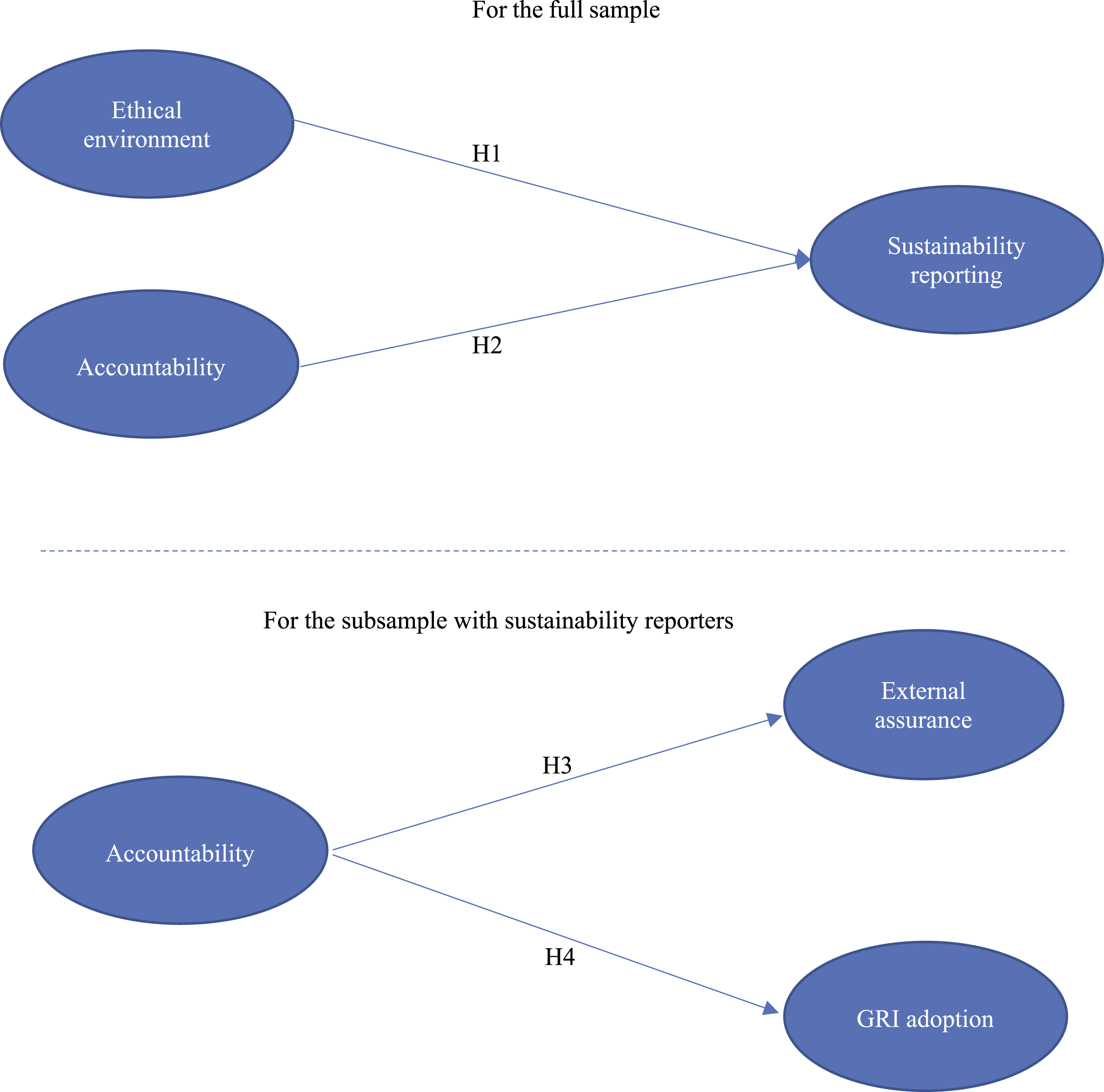

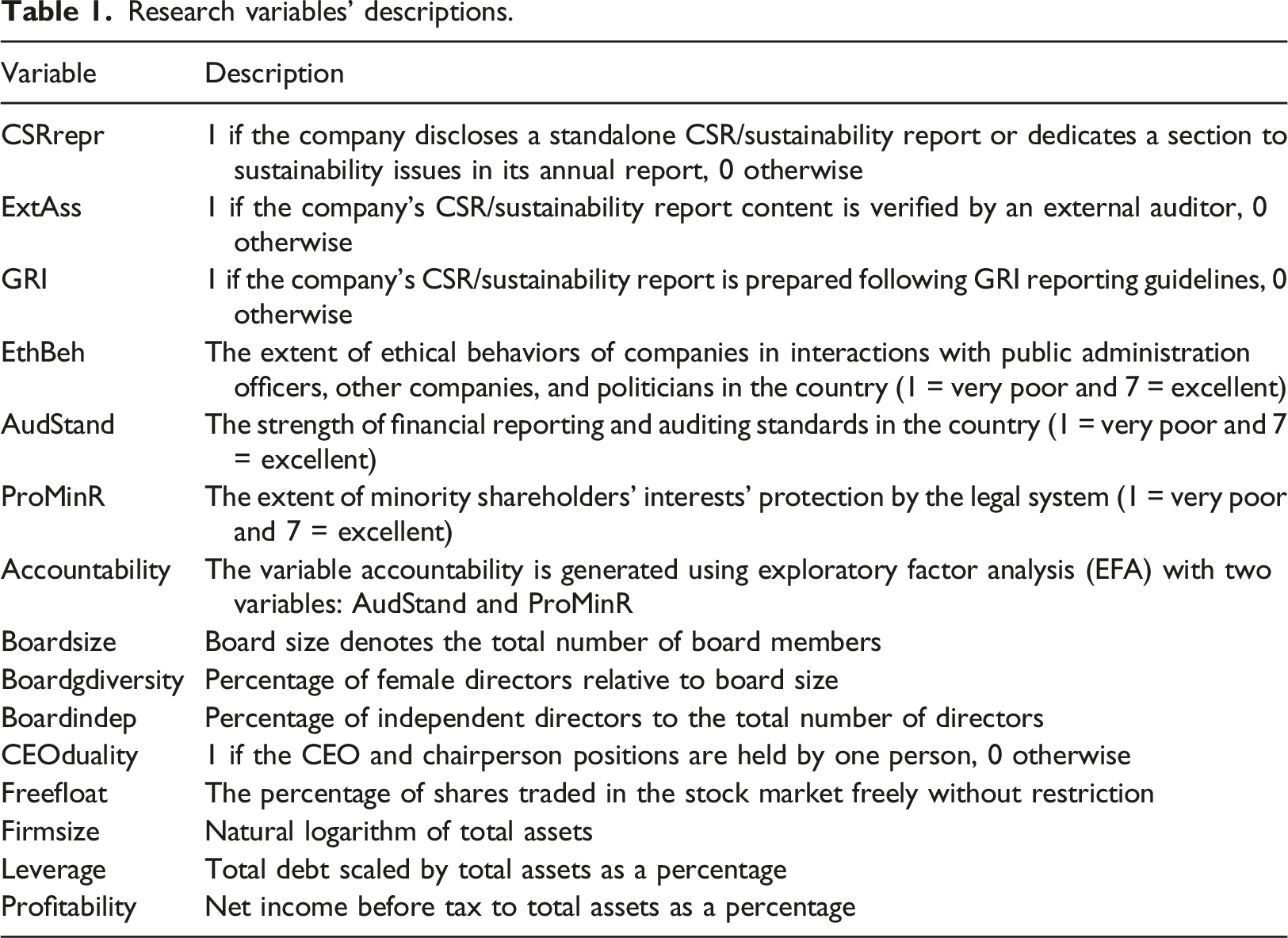

The present study extends the previous literature and aims to elucidate the institutional determinants of sustainability reporting by H&T companies. Using institutional theory, it tests how the ethical behaviors of firms, in interaction with other firms, public administrators, and politicians and under the pressure of accountability, influence (1) sustainability reporting, (2) the acquisition of the external assurance statement, and (3) the implementation of GRI guidelines. We focus on the firms’ ethical environment and accountability because both emphasize the need “to do what is right.” Accountability entails companies being obliged or willing to take responsibility for the ecological, social, and economic impacts of their activities and to report such information. The CSR of H&T companies is similarly affected by the ethical environment in which they operate as when managers are genuinely dedicated to upholding high ethical standards, their conscience to act in socially and environmentally responsible ways is likely to be reinforced. Firms are also likely to issue accurate and credible sustainability reports visibly when accountability and transparency constitute their key values. The ethical behaviors of firms and accountability are two country-level institutional proxies measured by the World Economic Forum (WEF, 2019). We further separate accountability into two individual indicators, namely, the protection of minority shareholders’ rights and the strength of financial reporting and auditing standards, to suggest specific implications for each metric.

A relationship exists between the growth in CSR reporting rates, the use of external assurance services, and the adoption of the GRI framework (KPMG, 2013). It appears that stakeholders not only request that companies disclose sustainability information but also look for greater credibility and transparency in company reports: “Many companies now face significant pressure to give stakeholders confidence in what they say and assurance can help provide this credibility” (KPMG, 2013: p.12). Because the adoption of assurance and GRI guidelines is voluntary in most countries, practices differ among companies (Owen et al., 2009; Perego, 2009; Junior et al., 2014). Moreover, the absence of specific regulations about the assurance process for sustainability reports and divergence among the assurance services offered by different assurance providers invite questions about the determinants of assurance statements and their efficacy in enhancing transparency and accountability to stakeholders (Junior et al., 2014). Therefore, to better understand sustainability reporting, it is important to recognize the key factors that prompt H&T companies to choose external assurance and adopt the GRI framework.

This paper contributes to the existing literature in four ways. First, studies on the relationship between sustainability reporting and country-level factors drawn from ethical values and accountability are still relatively scarce. Prior studies have largely drawn on firm-level financial or board characteristics (Correa-Garcia et al., 2020; Kılıç et al., 2015; Michelon and Parbonetti, 2012), which provide valuable but limited insights into firms’ sustainability reporting practices. Second, to the best of the authors’ knowledge, this is the first study to test how accountability and ethical behaviors of firms concurrently influence the three following principal sustainability reporting initiatives: reporting, external assurance, and adoption of the GRI framework. By including these sustainability reporting decisions in the same study, we aim to shed light on the credibility and integrity of sustainability reporting with external assurance and GRI framework adoption practices. These three sustainability reporting dimensions may not react to institutional forces in the same way. However, the findings of the study justify this approach as the sustainability reporting and external assurance indicators demonstrate opposite reactions to the accountability quality of the environment. Drawing on these three sustainability reporting practices, we suggest implications of their efficacy on companies’ transparency and accountability for policymaking, firms, and assurance firms. Third, we use institutional theory, rather than stakeholders’ theory, as a conceptual framework, which places companies in a broad context that includes country-level factors, such as markets, norms, regulations, and formal and informal rules, in addition to stakeholders (Brammer et al., 2012). This approach highlights a wide range of factors that are likely to influence corporate sustainability decisions. Fourth, we provide evidence of sustainability reporting in the H&T sector—a sector in which companies’ interest in CSR issues continues to increase (Kang et al., 2010). The H&T industry is also among the industries that have historically had the most dramatic impact on the environment through the depletion of natural resources, creation of hazardous waste, and consumption of water and energy (Stottler, 2018), making the H&T sector a timely framework for meaningful analysis of sustainability initiatives.

The following sections are structured as follows. The next section focuses on the conceptual framework of institutional theory and reviews the literature relevant to the research question. The third section describes the research methodology implemented in the empirical study, which is followed by the results in the fourth section. The final section comprises the discussion, conclusion, and implications of the results.

Institutional theory: The conceptual framework

Institutional theory has been increasingly adapted to explore and explain the divergence among companies in undertaking sustainability reporting practices depending on the context (Briem and Wald, 2018; Kılıç et al., 2019; Martínez-Ferrero and García-Sánchez, 2017). Unlike other theories, such as stakeholders’ theory or agency theory, institutional theory pays much closer attention to the ways in which companies’ actions are affected by their environment. It tends to emphasize the reason leading firms adopt homogeneous forms of behavior in an organizational field (Roy and Goll, 2014). Therefore, it suggests placing companies in a broad field that includes markets, norms, regulations, and formal and informal rules (Brammer et al., 2012). According to this theory, firms interact with their stakeholders within contexts formed by country-level institutional factors that influence their behaviors (Campbell, 2007; Kılıç et al., 2019). Hence, firms operating in the same institutional environment will act homogeneously (Claessens and Fan, 2002; Campbell, 2007; La Porta et al., 1998) and comply with the norms of this context to gain legitimacy and enhance their stability and survival (DiMaggio and Powell, 1983). This process is termed homogenization isomorphism (DiMaggio and Powell, 1983). Institutional isomorphic change occurs due to formal mechanisms, such as coercive pressures (exerted by regulatory structures, rules, political laws, etc.), from informal mechanisms, such as normative pressures (driven by ethical values, profession, education, etc.), and from mimetic forces (for example, in an uncertain context, companies operating in the same industry tend to adopt the same behavior; DiMaggio and Powell, 1983; Kolk and Perego, 2010; Kılıç et al., 2019; Martínez-Ferrero and García-Sánchez, 2017). All these mechanisms exert pressure on companies to converge in their behaviors according to the environment in which they operate. From this perspective, institutional theory is a relevant approach to explore the relationship between ethical environment, accountability, and firms’ sustainability reporting practices. It suggests that firms influenced by formal and informal institutional factors disclose sustainability reports to ensure their legitimacy.

Business ethical environment and sustainability reporting

According to institutional theory, moral and ethical values are among the normative factors exerting pressure on companies to comply with their environment, which may influence their decision-making processes (Drew et al., 2006) and, inter alia, their sustainability reporting. The moral and ethical values of managers as members of a society are influenced by the moral and ethical values held by that society (Oliver, 1991). When managers have high professional ethical standards, the firms in which they work are more likely to be ethical and socially responsible and engage in sustainable practices (Valentine and Fleischman, 2008) to conform to the ethical behavior of society (DiMaggio and Powell, 1983). Moreover, ethical and socially responsible companies experience lower principal-agent problems (Kuzey et al., 2021), which can establish a better relationship with their stakeholders and, subsequently, a more auspicious climate for transparency regarding sustainability information.

In ethical business environments, organizations should also act socially and responsibly and maintain sound organizational ethics not due to organizational or financial benefits but because it would be unthinkable to do otherwise (Oliver, 1991). In such environments, companies are particularly susceptible to public scrutiny, and unethical practices are strictly punished. Firms engaging in unethical practices and in noncompliance with social and cultural standards are more sensitive to political costs (Meek et al., 1995). From this perspective, companies tend to use sustainability reporting to remove their potential political costs, such as anti-pollution taxes and consumer boycotts (Gamerschlag et al., 2011), to obtain economic benefits, and to avoid political rivalry (Frias-Aceituno et al., 2014).

Empirical studies show that companies orient their practices in terms of sustainability reporting according to the institutional environment within which they function (García-Sánchez et al., 2016; Martínez-Ferreron and García-Sánchez, 2017). For instance, national culture and ethics influence companies’ sustainable behaviors and environmental practices/disclosure (Pucheta-Martínez and Gallego-Álvarez, 2020). Therefore, firms operating in countries that encourage ethical and socially responsible practices will comply with this context and experience a high degree of CSR disclosure (García-Sánchez et al., 2016; Pucheta-Martínez and Gallego-Álvarez, 2020) along with more transparency and credibility of sustainability reports (Martínez-Ferrero and García-Sánchez, 2017).

In addition to general CSR guidelines, various international codes specifically applicable to H&T companies 7 may influence their CSR policies/disclosure. Regarding the H&T industry, Holcomb et al. (2007) analyze CSR activities on corporate websites, in annual reports, and in CSR reports for the top 10 hotel companies. Their findings document significant diversity in the hotels’ CSR reporting policies and show that the hotels do not report substantially on environmental information. According to the authors (Holcomb et al., 2007), the gaps in the hotels’ CSR reporting are explained by the lack of unified ethical codes in the H&T industry. Huimin and Ryan (2011) suggest that the application of CSR policies in Chinese hotels is facilitated or inhibited by the ethical stance of their managers.

Most prior literature argues that moral and ethical values within society create homogeneity in and compliance with sustainability reporting by companies. However, this statement of normative isomorphism is not shared by all researchers. It appears that in unethical business environments, companies that are involved in socially responsible actions are perceived ethically by customers (Ferrell et al., 2019) and are disposed to have their sustainability reports assured (Boiral et al., 2019; Kılıç et al., 2019).

The literature reviewed points to both positive and negative effects of ethical business environments. Thus, we formulate the following hypothesis: H1: An ethical business environment has a significant impact on the likelihood that H&T firms issue sustainability reports.

Accountability and sustainability reporting

Institutional theory is a promising avenue through which to understand how accountability affects companies’ practices/disclosures (Filatotchev et al., 2013; Kılıç et al., 2019). In an institutional environment with a high level of accountability, stakeholders are especially sensitive to companies’ transparency and accountability and may constantly question them. In such a context, companies need to engage in social or community activities and publish their endeavors (Gamerschlag et al., 2011) to convince stakeholders that they are trustworthy in their corporate dealings (Nwagbara and Ugwoji, 2015). Along similar lines, firms in countries with a high level of voice and accountability tend to provide extensive CSR disclosure (Blanc et al., 2017; Barkemeyer et al., 2018; Gerged et al., 2021).

Stakeholder theory supports the prediction of coercive isomorphism, stating that most companies committed to public accountability are likely to divulge a higher level of information. Sustainability disclosure and, inter alia, sustainability reporting can serve as tools to convey companies’ commitments to public transparency and accountability norms (Coy and Dixon, 2004; Gordon et al., 2002; Nelson et al., 2003; Ntim et al., 2017) and, subsequently, to obtain the support of stakeholders (Donaldson and Preston, 1995; Freeman and Reed, 1983; Freeman, 1984; Michelon and Parbonetti, 2012; Ntim et al., 2017). In general, managers have a greater commitment to public transparency and accountability (Ntim et al., 2017), which incites them to disclose substantial sustainability information (Coy et al., 2011; Donaldson & Davis, 1991, 1994; Ntim et al., 2017).

In the H&T context, companies have kept pace with the global trend of increased sustainability reporting (World Travel and Tourism Council [WTTC], 2017). Government reporting directives and stock exchange regulations are among the factors that have contributed to this trend (WTTC, 2017). Likewise, some initiatives and regulations, such as companies’ annual CSR reports and the International Tourism Partnership, have affected the involvement of H&T companies in CSR practices/disclosure (Franco et al., 2020). Ghaderi et al. (2019) argue that it is necessary for hotels to adhere to official laws and regulations as failure to do so could adversely affect their financial and non-financial performance. This implies that H&T companies need to respond to criticisms of their negative environmental impact through various CSR programs that protect the environment and save costs (Alexander and Kennedy, 2002; Ghaderi et al., 2019). These companies issue sustainability reports in response to stakeholders’ requirements for accountability and environmental commitment.

However, in line with the substitution hypothesis, firms are likely to issue sustainability reports in contexts characterized by poor regulations (Durnev and Kim, 2005) in an attempt to fill the void arising from the poor institutional environment. In other words, the private sector tries to compensate for the poor regulatory environment caused by the poor quality of public governance (Durnev and Kim, 2005).

In light of the literature reviewed above, we propose the following hypothesis: H2: Accountability has a significant impact on the likelihood that H&T firms issue sustainability reports.

Accountability and the adoption of external assurance

The lack of transparency, accuracy, and credibility in sustainability reports has given rise to the need for external assurance services (Ruiz-Barbadillo and Martínez-Ferrero, 2020; Simnett et al., 2009). Previous studies have argued that stakeholders’ confidence in the credibility of sustainability reports is affected by the assurance level offered by companies (Hodge et al., 2009; Low and Boo, 2012; Ruiz-Barbadillo and Martínez-Ferrero, 2020). However, the absence of universal assurance standards and of a legal obligation to adopt external assurance implies variability in the assurance process (Fuhrmann et al., 2017; Ruiz-Barbadillo and Martínez-Ferrero, 2020). In 2013, the study by KPMG revealed that most companies that choose to assure their CSR reports opt for limited levels of assurance. In the H&T context, Kılıç et al. (2021) reveal that only 31.48% of firm-year records include external assurance for their sustainability reports.

Because the external assurance of sustainability reports remains voluntary in most countries (KPMG, 2013), the factors stimulating their adoption can diverge among companies. Several studies have investigated the country-level institutional factors associated with the request for assurance services for sustainability reporting. Faced with amplified normative, coercive, and mimetic pressure, companies use the external assurance of sustainability reports as a legitimization tool, certifying the credibility of the information disclosed (Martínez-Ferrero and García-Sánchez, 2017). Significant attention has been paid to the role of accountability in explaining the adoption of sustainability assurance statements. In 2013, the study of KMPG found that accountability is essential in making sustainability reports credible and accurate and that companies that take CSR seriously have the highest level of accountability. Empirical studies provide evidence that companies operating in countries that place strong emphasis on corporate transparency and accountability utilize more assurance services for their sustainability reports than those in countries that do not enforce these values (Kolk and Perego, 2010; Ruiz-Barbadillo and Martínez-Ferrero, 2020). However, this finding is not unanimously supported in previous studies. It appears that the assurance of sustainability reporting occurs more frequently in environments characterized by lower investor protection (Herda et al., 2014) and/or weaker legal enforcement systems (Zhou et al., 2016). Similarly, as discussed above, Kılıç et al. (2019) show that in poor accountability environments, firms have more reason to assure their integrated reports in the absence of powerful institutions. In the same vein, organizations undergo the external assurance process out of a desire for legitimization and customer loyalty rather than in-depth verification of their sustainability practices (Boiral et al., 2019).

Sustainability reporting assurance is weak in the H&T industry compared to other industries (Janković and Krivaĉić, 2014). For example, Jones et al. (2014) observe that there is little evidence of independent external assurance of sustainability reporting by hotel companies. Koseoglu et al. (2021) similarly highlight room for improvement in assurance statements in the H&T context. Several studies explain these gaps as resulting from the absence of statutory regulation (Jones et al., 2014, 2017) and suggest that independent external assurance services seem essential for H&T companies looking to contribute to the Sustainable Development Goals (SDGs). This implies that the regulatory environment may drive H&T companies’ choice of external assurance.

The extant literature, therefore, reveals diverging opinions regarding the role of accountability in the adoption of external assurance services. The external assurance of sustainability reporting may serve as a complementary or substitutive mechanism of accountability. Thus, we formulate the following hypothesis: H3: Accountability has a significant impact on the likelihood that H&T firms issue sustainability reports with external assurance.

Accountability and the adoption of the GRI framework

The GRI plays an important role in improving transparency and credibility sustainability reporting (KPMG, 2013) and was developed to provide guidelines on how to present a clear vision of the ecological and human impacts of a company (Marimon et al., 2012). Within a few years of its establishment, the GRI has become the most important institution in the context of sustainability reporting (Moneva et al., 2006) and the global standard most widely used by firms (Gamerschlag et al., 2011), meaning that it also influences stakeholders’ decision-making (Alonso-Almeida et al., 2014). The adoption of the GRI framework exceeds national standards and other guidelines (KPMG, 2013). For example, in Korea, most companies strongly believe that the GRI guidelines are more credible than those of individual companies or local organizations (KPMG, 2013). However, in the H&T context, Koseoglu et al. (2021) find that non-GRI followers represent 51.54% of CSR reporters, suggesting that they follow their own guidelines or those of another organization. Kılıç et al. (2021) likewise show that less than half of the H&T companies (48.41% firm-year records) follow the GRI guidelines in preparing sustainability reports.

The adoption of the GRI framework is driven by regulatory and non-regulatory institutional forces (Nikolaeva and Bicho, 2011). Two possible scenarios may explain how the adoption of the GRI framework is associated with accountability. First, in a higher accountability environment, corporate transparency and accountability are highly valued by society (Kılıç et al., 2020), and companies’ practices are constantly subject to public scrutiny (Bravo et al., 2012). The increased coercive pressure may incite companies to adopt GRI standard reporting to demonstrate their commitment to society’s transparency and accountability standards (Nikolaeva and Bicho, 2011). Adopting the GRI framework can help companies establish truthful communication and legitimize their activities (Bravo et al., 2012). Further, pressure from stakeholders leads companies to publish comprehensive and transparent sustainability reports following the GRI guidelines (Fernandez-Feijoo et al., 2014). These guidelines may also allow consistent and comparable sustainability reports to be produced across periods and companies, which may facilitate stakeholders’ decision-making (Alonso-Almeida et al., 2014). In the H&T industry, Kılıç et al. (2021) show that the establishment of CSR committees increases the likelihood of H&T firms engaging with sustainability issues and issuing sustainability reports using the GRI framework. The establishment of the CSR committees demonstrates upper-level management’s attention to GRI-formatted CSR reports.

The second scenario is that in a poor accountability environment, companies may engage voluntarily in self-regulation and transparency exercises as a substitute for the ineffective institutional context (Kılıç et al., 2019). This suggests that the company’s commitment to transparency and the integrity of their sustainability reports through GRI adoption are not a result of institutional pressures but, rather, discretionary initiatives (Kılıç et al., 2019). Thus, adopting the GRI framework could be used to compensate for the absence or ineffectiveness of the governmental institutions. The history of GRI, as illustrated by Brown et al. (2009), confirms this suggestion and shows how the GRI standard did not emerge from institutional pressure but from the initiative of entrepreneurs looking for accountability and transparency. Anti-corruption engagement (Osuji, 2011) provides another relevant example of a specific expression of CSR developed at the initiative of companies rather than as the result of institutional pressures (Barkemeyer et al., 2018).

The literature reviewed above reveals that the association between accountability and the adoption of the GRI framework can be complementary or substitutive. Consequently, we propose the following hypothesis: H4: Accountability has a significant impact on the likelihood that H&T firms issue sustainability reports adopting the GRI framework.

As discussed above, stakeholders not only request the disclosure of sustainability reports but also constantly demand accountability and transparency from companies. Faced with this pressure, companies are incited not only to issue sustainability reports but also to convince stakeholders of their credibility (KPMG, 2013). External assurance and GRI guidelines serve as mechanisms through which H&T companies reassure their stakeholders that their sustainability reporting respects credibility and transparency standards. However, few H&T companies use external assurance and the GRI framework, suggesting gaps in their sustainability reporting practices (Uyar et al., 2020; Kılıç et al., 2021; Koseoglu et al., 2021). Therefore, it is inadequate to examine determinants of sustainability reporting without addressing factors that stimulate H&T companies to choose to obtain external assurance and adopt the GRI. In this study, we focus on the relationship between accountability, external assurance, and GRI as accountability has become a central concept of corporate governance, drawing the attention of scholars and policymakers.

In this study, we link external assurance and GRI adoption to accountability rather than ethical environment for the following reasons. While ethics relates closely to the disclosure of environmental and social issues, it is less relevant to assurance and GRI adoption issues, which pertain more to regulations and the format of sustainability reports. The development of verification mechanisms for sustainability reports is mainly influenced by the emergence of international standards, such as the GRI, AccountAbility AA1000 Assurance Standard, and ISAE3000 standard, aimed at improving credibility, comparability, and stakeholders’ responsiveness in sustainability reporting (Perego and Kolk, 2012). Accounting and auditing standards mainly regulate the domains of financial auditing and sustainability report assurance practices. GRI guidelines prescribe what should be included in the sustainability report and how the report should be structured, which ensures that stakeholders receive easily readable and comparable reports. Therefore, assurance and GRI adoption are linked to accountability rather than ethical environment in this study.

Figure 1 highlights the study’s theoretical framework and hypotheses. The theoretical framework of the study. We justify the sample selection of above two models in the “empirical methodology” section.

Research methodology

In this section, multiple statistical analysis methods, including univariate and multivariate approaches, are utilized. First, the sample is preprocessed, involving data organization, missing values analysis using multiple imputation, possible outlier detection, and winsorization. This is followed by a summary of the included variables of interest using descriptive statistics, frequency analysis, Spearman’s correlation analysis, and logistic panel data regression analysis. Finally, a robustness test, rare events logistic regression (RE-Logit) analysis, and logistic regression analysis for panel data using a one-firm-year lag of the testing variables to address the endogeneity issue are performed.

Research variables

In this study, we use three dichotomous variables for CSR reporting undertakings: CSRrepr (CSR reporting), ExtAss (external assurance statement on CSR report), and GRI (following GRI reporting guidelines in the report content; Koseoglu et al., 2021). All three were retrieved from the Thomson Reuters Eikon database. In line with Koseoglu et al. (2021), these variables take 1 if the reporting practices exist or 0 if they do not exist. The ethical behaviors of firms (EthBeh) and accountability indicators, namely, auditing and financial reporting standards (AudStand) and minority shareholders’ rights’ protection (ProMinR), were retrieved from the WEF (2019). While EthBeh assesses the extent of companies’ ethical behaviors in interactions with public administration officers, other companies, and politicians in the country, AudStand evaluates the strength of financial reporting and auditing standards in the country (WEF, 2019). ProMinR measures the extent of legal protection for minority shareholders’ interests (WEF, 2019). These three variables are measured on a scale of 1 (very poor) to 7 (excellent) (WEF, 2019). These indicators were at the country-level and used in prior studies as proxies of the institutional environment (Kılıç et al., 2019). We obtained a composite score from the AudStand and ProMinR variables via factor analysis and labeled it “Accountability,” which is further explained in the following sections. Finally, we incorporated several control variables into the research model, such as board, financial, and ownership characteristics, which could affect firms’ CSR reporting and assurance practices. Those variables include Boardsize (number of board members), Boardgdiversity (proportion of female directors on the board), Boardindep (proportion of independent directors on the board), CEOduality (CEO duality), Freefloat (percentage of free float shares), Firmsize (firm size), leverage, and profitability (Kılıç et al., 2019; Koseoglu et al., 2021). The data concerning the control variables were also obtained from the Thomson Reuters Eikon database.

Research variables’ descriptions.

Sample

The initial sample of this study comprises 940 firm-year observations from 2011 to 2018 from H&T sector firms listed in the Thomson Reuters Eikon database. Before further analysis, various data screening processes are employed, such as missing data analysis, detection of possible outliers, winsorization, and data imputation.

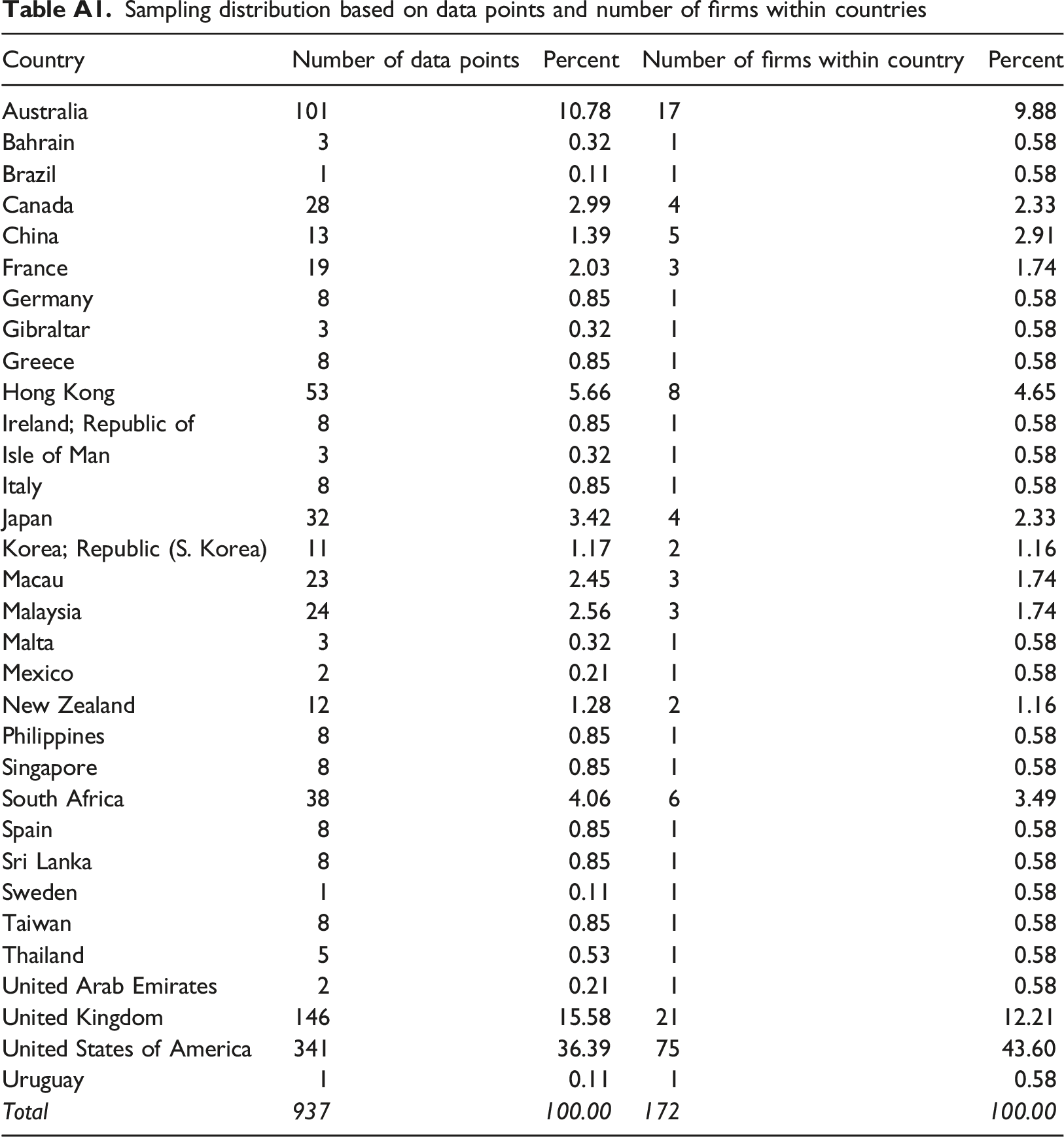

Some variables indicated significant skewness, with extreme values in their distributions following the initial descriptive statistical analysis. The control variables “Leverage” and “ROA” are included in the winsorization step, for which these extreme values are winsorized at the one percent of the bottom and top sections of the data by replacing them in both tails. Outlier detection steps are also used. For this step, the multivariate outlier method using the minimum covariance determinant (MCD) approach (Verardi and Dehon, 2010) is performed. The results show that three firm-year outliers are eliminated, and 937 firm-year records are left in the final sample for further analysis for the eight years between 2011 and 2018. The distribution of the sample based on data points and the number of firms within countries is presented in Table A1 in the appendix. The sample distribution represents a worldwide H&T sample and strengthens the generalizability of the results across countries.

In the next step of the data preprocessing, missing data analysis as well as multiple imputation steps are employed. The initial analysis of the missing data results reveal that EthBeh had 29 (3.09%), AudStand had 29 (3.09%), and Accountability had 29 (3.09%) firm-year missing records, comprising less than 5% in each case, which is considered inconsequential (Schafer, 1999). Finally, data imputation analysis is used, with Markov chain Monte Carlo (MCMC) performed to replace the missing values.

Following the data screening process, the final sample size is 937 firm-year records. Of these records, 79 are from 2011, 89 from 2012, 92 from 2013, 96 from 2014, 114 from 2015, 139 from 2016, 156 from 2017, and 172 from 2018. As the distribution indicates, the sample structure is in panel data type format, where the firm is the panel variable and the year is the time variable. Factor analysis for “Accountability”

The Accountability variable is generated using exploratory factor analysis (EFA) with two variables: AudStand and ProMinR. The composite values of AudStand and ProMinR are used to generate the Accountability variable following the factor analysis. For the EFA setting, principal component analysis (PCA) is selected as the extraction method, while varimax is chosen as the rotation method. The results show that Bartlett’s Test of Sphericity was 1403.66 (df: 1; p-value <. 001), the Kaiser-Meyer-Olkin Measure of Sampling Adequacy was 0.710, the Eigenvalue was 1.882, and the cumulative percentage of variance was 94.08. Based on these results, AudStand and ProMinR are loaded under a single factor called “Accountability.”

Empirical methodology

This section presents the empirical methodology, including the formulation of the research models as a mathematical functional representation. Logistic panel regression analysis for panel data is chosen as the main analysis tool for the following reasons: (i) there is a time-variant association characteristic among the target (dependent) and predictor (independent) variables; (ii) the structure of the sample is in a firm-year longitudinal format for testing the research models; and (iii) the likelihood-ratio (LR) test of

Due to the binary categorical variable type of the dependent variables and the time-variant aspect, logistic panel data regression is used. The following functional relationships in equation (1) show the formulation of the research models with the binary categorical dependent variables (CSRrepr, ExtAss, and GRI):

In the functional relationships (Equation (1)),

The models with CSRrepr as the dependent variable incorporate the full sample (N = 937), while the models with ExtAss and GRI as dependent variables incorporate the subsamples of the firm-year records with the existence of CSRrepr (N = 460). This is because the existence of a CSR report makes it a priority to assess whether the report is externally assured by a third party and prepared in accordance with GRI guidelines. It would be meaningless to measure the ExtAss and GRI variables for observations that do not have a CSRrepr.

In further analysis, the proposed models are subject to a robust standard error to eliminate the heteroskedasticity problem (Wooldridge, 2013). Finally, the research sample consists of unbalanced longitudinal data, in which unequal records of the firms within years exist due to missing financial information. However, the Stata Module (StataCorp, 2015) of the random-effects panel data regression analysis can handle unbalanced panel data.

Findings

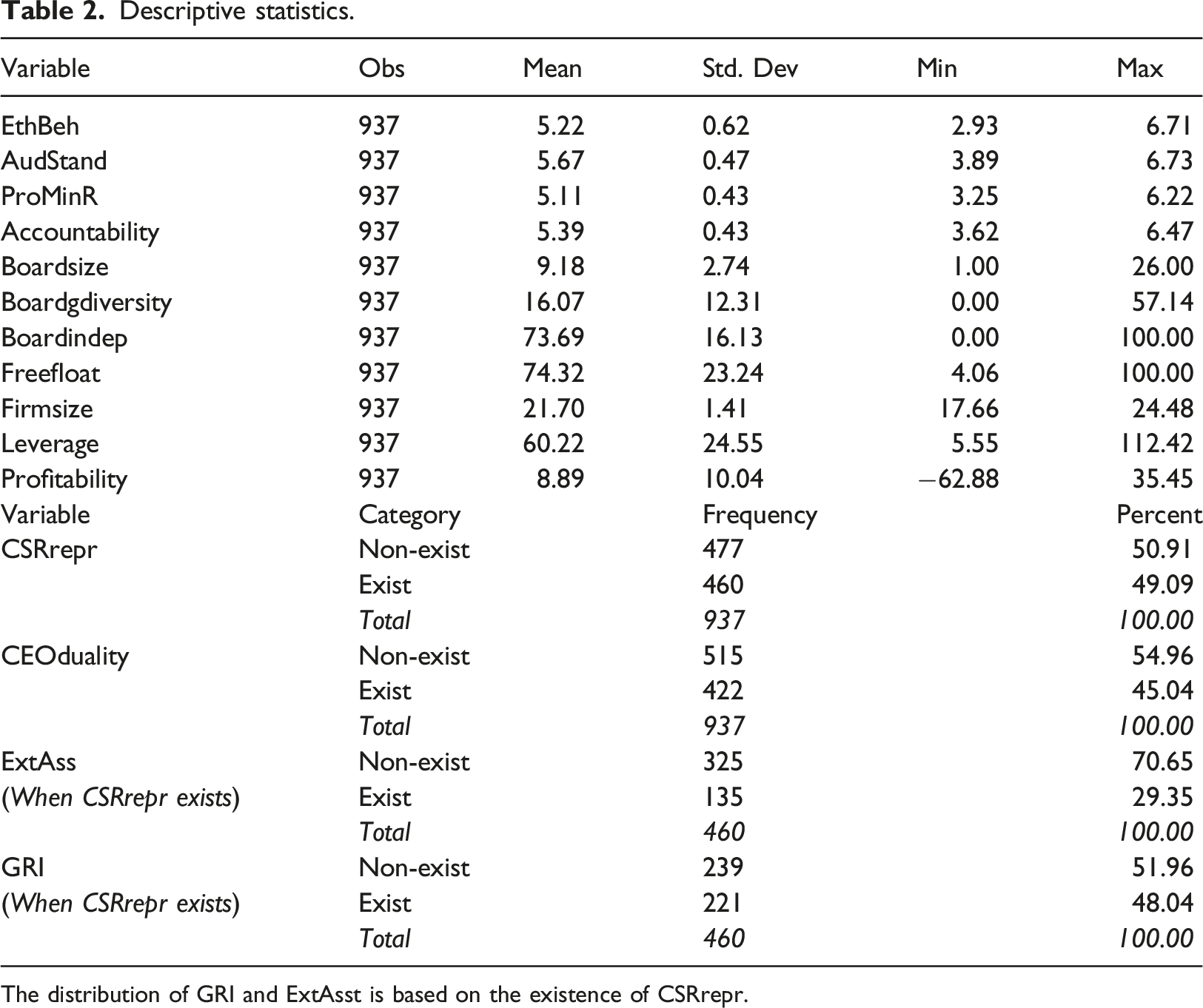

Variables’ descriptive statistics

Descriptive statistics.

The distribution of GRI and ExtAsst is based on the existence of CSRrepr.

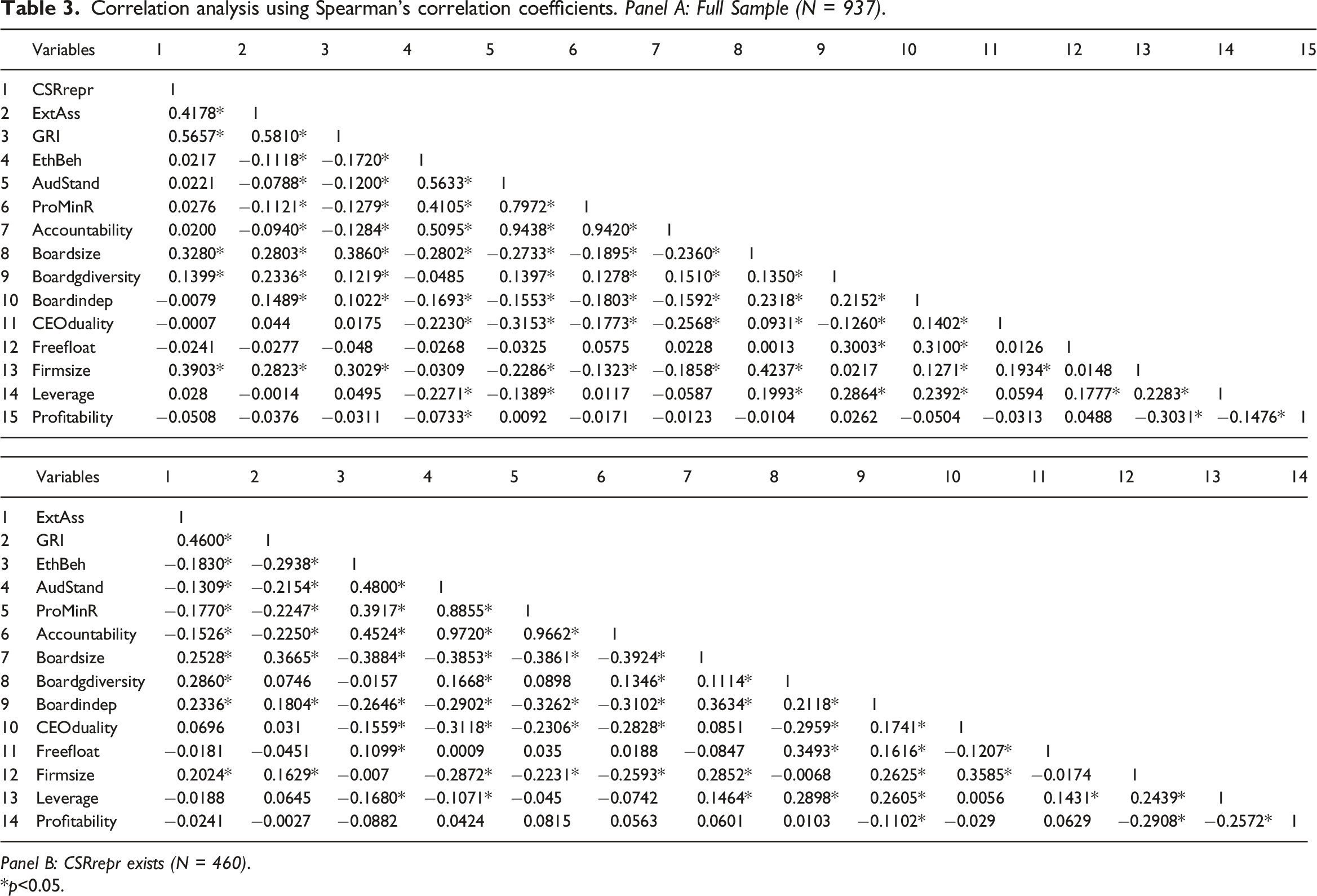

Correlation analysis

Correlation analysis using Spearman’s correlation coefficients. Panel A: Full Sample (N = 937).

Panel B: CSRrepr exists (N = 460).

*p<0.05.

Multicollinearity: The multicollinearity issue among the independent variables is investigated using variance inflation factor (VIF) analysis. The VIF values range between 1.10 and 1.48, which are smaller than the suggested cut-off value of 10 (Hair et al., 2019).

Findings

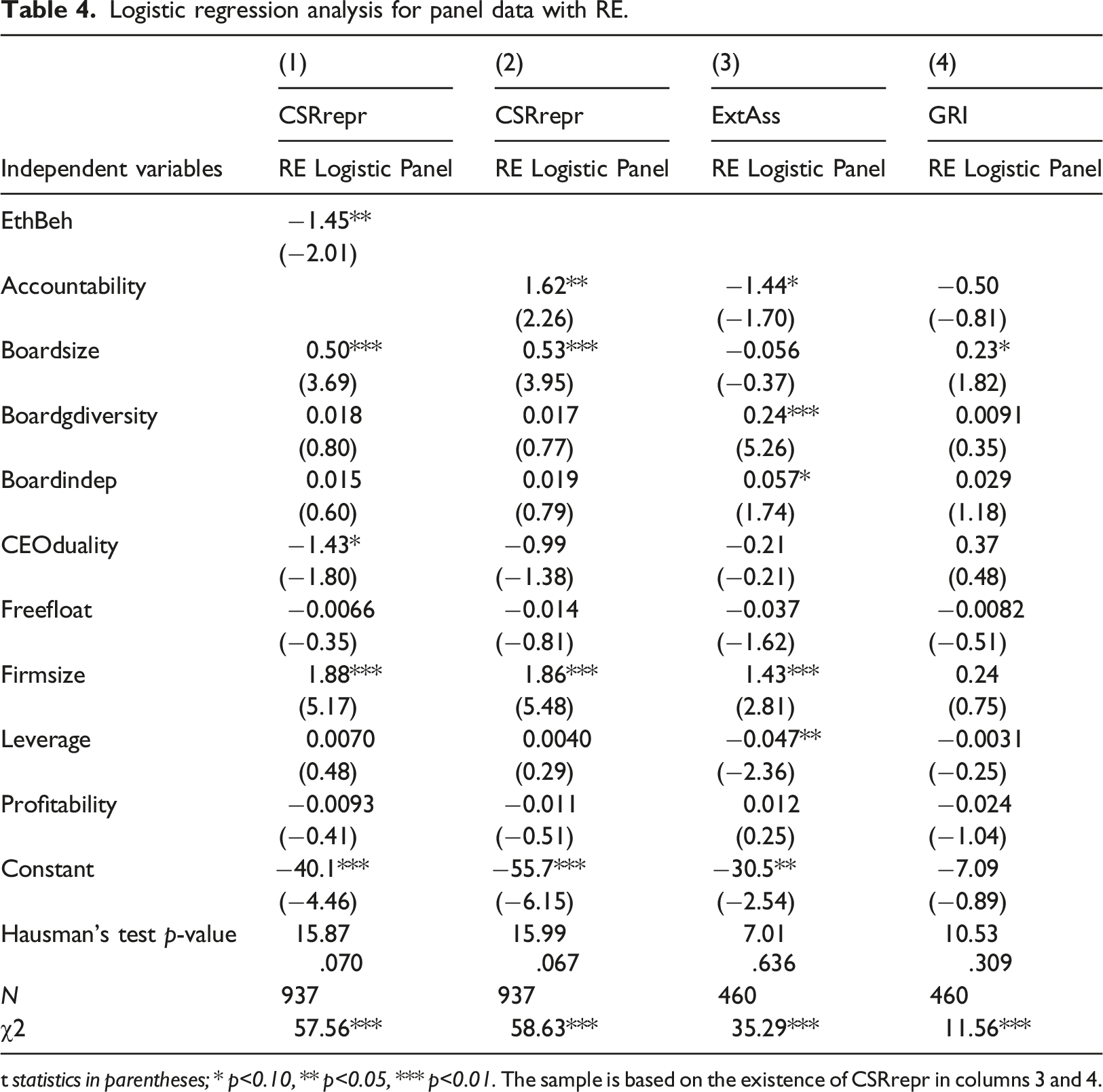

Logistic regression analysis for panel data with RE.

t statistics in parentheses; * p<0.10, ** p<0.05, *** p<0.01. The sample is based on the existence of CSRrepr in columns 3 and 4.

In Model 1, EthBeh (p<0.05) has a negative and significant relationship with CSRrepr. Furthermore, the coefficients of Boardsize (p<0.01) and Firmsize (p<0.01) are positive and significant such that they have a significant relationship with CSRrepr. Moreover, CEOduality (p<0.10) has a weakly significant and negative relationship with CSRrepr. Hence, H1 is accepted, implying that firms located in high ethical business environments are less likely than weak ethical business environments to disclose a sustainability report.

Regarding Model 2, where CSRrepr is the binary dependent variable, the coefficients of Accountability (p<0.05), Boardsize (p<0.01), and Firmsize (p<0.01) are positive and significant. This finding lends support to H2, suggesting that firms located in a higher accountability environment have a greater tendency than a poor accountability environment to disclose a sustainability report.

In Model 3, where ExtAss is the binary dependent variable, the coefficients of Accountability (p<0.10) and Leverage (p<0.05) are negative and significant. Furthermore, the coefficients of Boardgdiversity (p<0.01), Boardindep (p<0.10), and Firmsize (p<0.01) are positive and significant. This finding confirms H3 highlighting that firms located in an environment of weaker accountability are more likely than an environment of strong accountability to issue a sustainability report with external assurance.

Finally, regarding Model 4, where the dependent variable is the binary GRI, the results reveal that Accountability does not have a significant association with GRI, while the coefficient of Boardsize is weakly significant and positive (p<0.10). This result rejects H4.

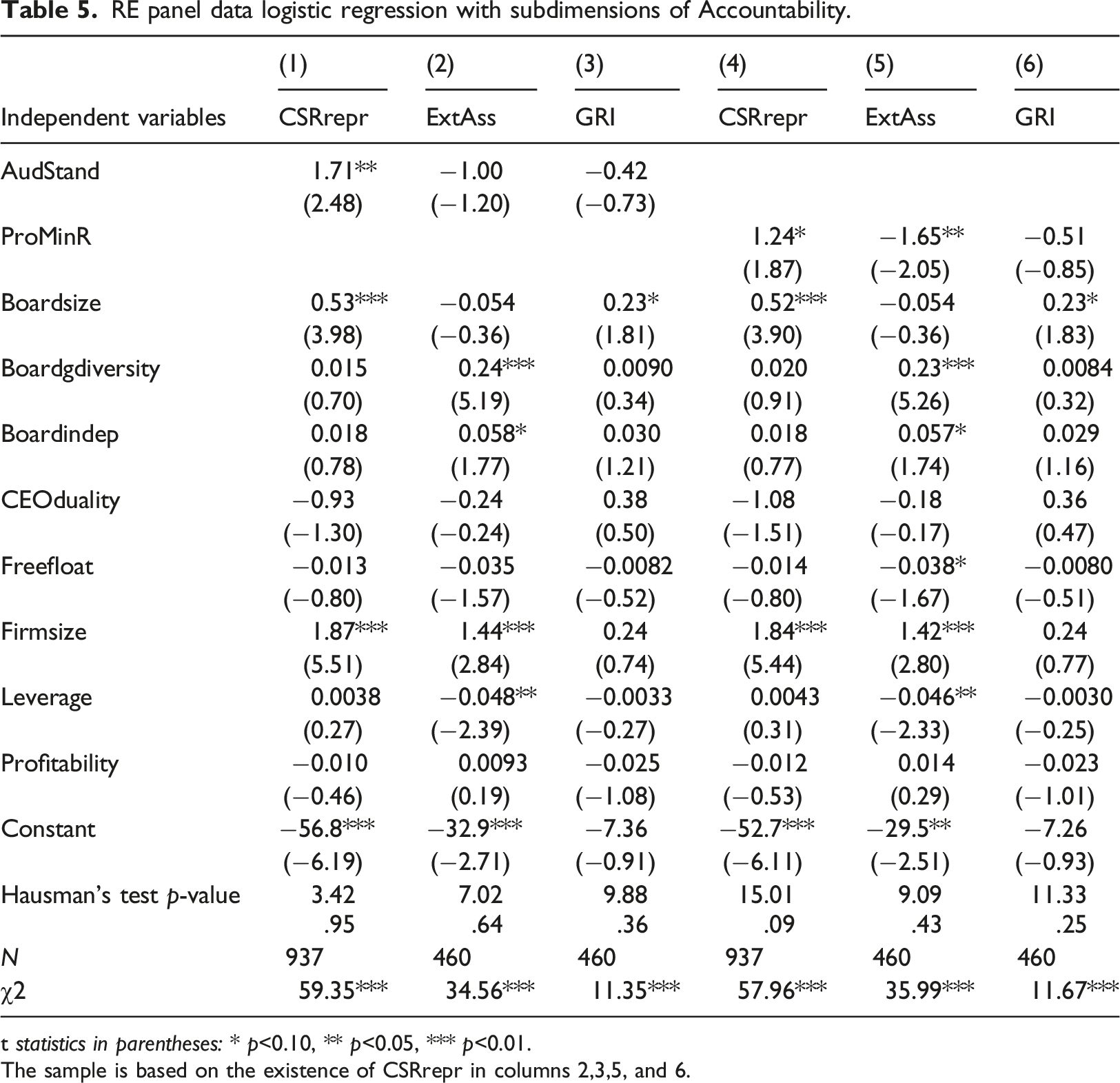

RE panel data logistic regression with subdimensions of Accountability.

t statistics in parentheses: * p<0.10, ** p<0.05, *** p<0.01.

The sample is based on the existence of CSRrepr in columns 2,3,5, and 6.

The results highlight that AudStand has a positive and significant relationship with CSRrepr (p<0.05) whereas it does not have a significant relationship with ExtAss and GRI. Furthermore, ProMinR has a weak positive and significant relationship with CSRrepr (p<0.10) but has a negative and significant relationship with ExtAss (p<0.05), and no significant relationship with GRI. Hence, the outcome confirms the results obtained in Table 4 with a minor deviation.

Robustness check

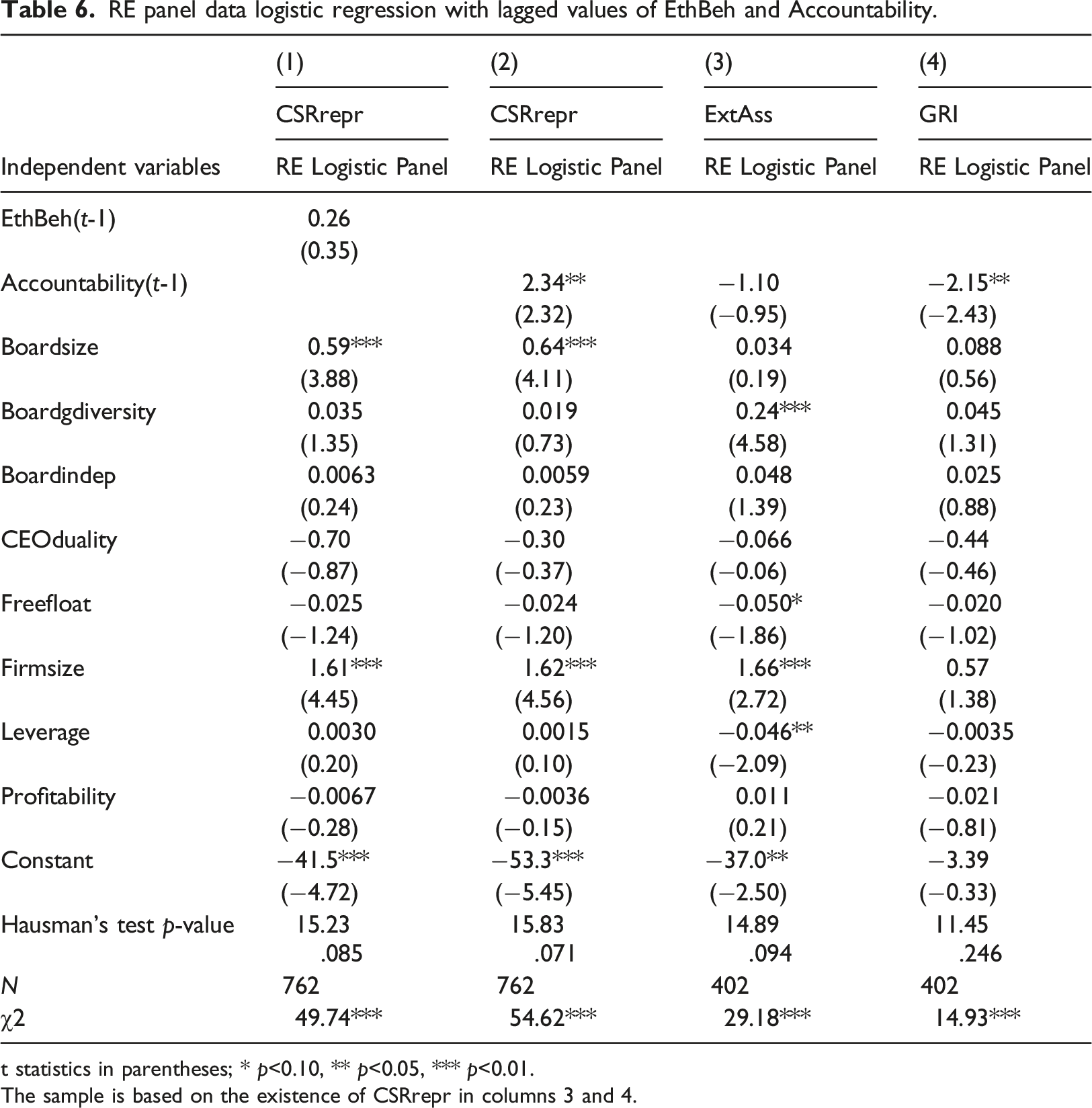

RE panel data logistic regression with lagged values of EthBeh and Accountability.

t statistics in parentheses; * p<0.10, ** p<0.05, *** p<0.01.

The sample is based on the existence of CSRrepr in columns 3 and 4.

The results show that the one-year lag of EthBeh does not have a significant association with CSRrepr. The one-year lag of Accountability has a positive and significant relationship with CSRrepr (p<0.05) and a negative and significant relationship with GRI (p<0.05). However, it does not have a significant relationship with ExtAss.

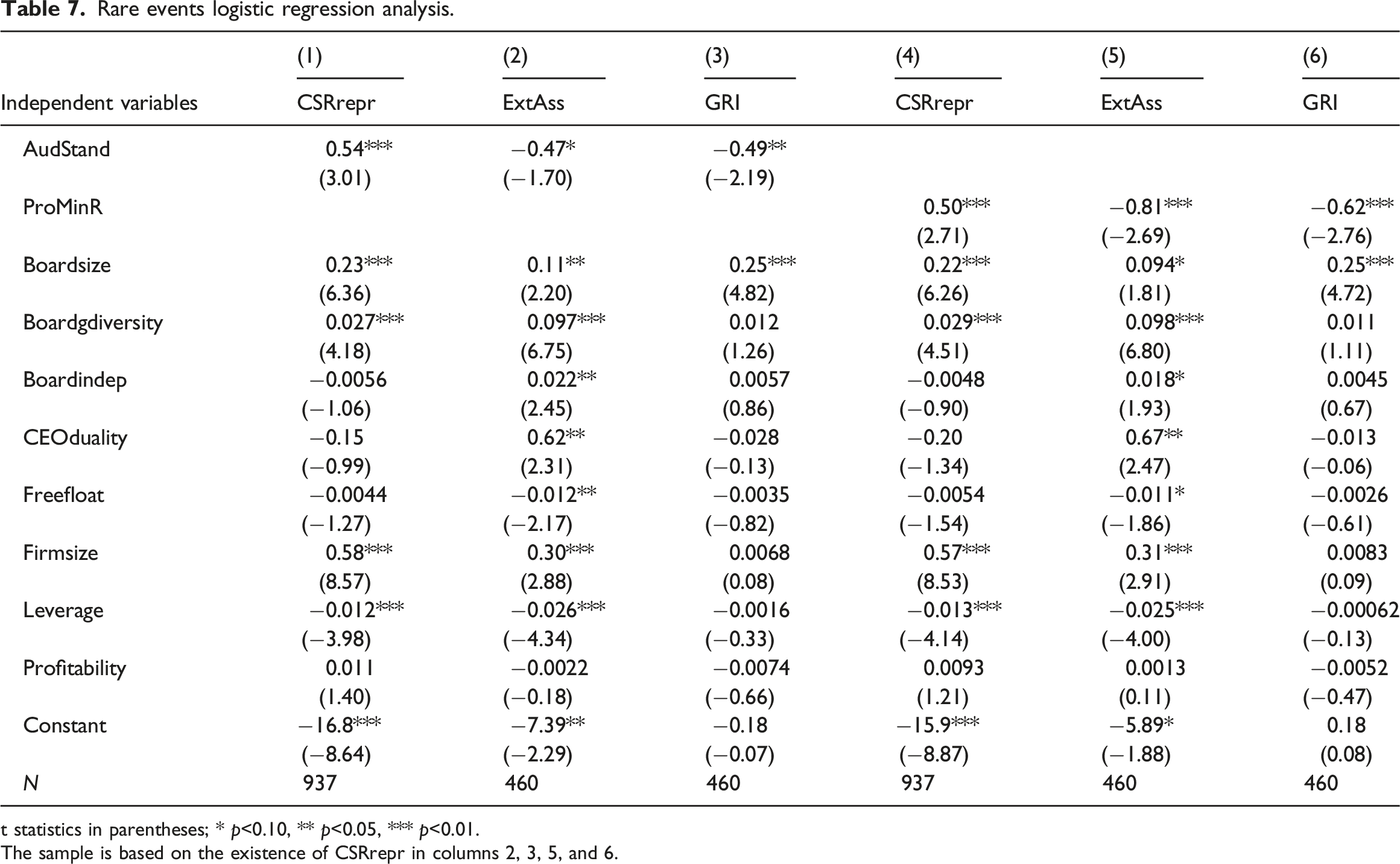

Second, AudStand and ProMinR, as the subdimensions of Accountability, are subject to rare events logistic regression analysis (King and Zeng, 1999a) because the distribution of ExtAss indicates a relatively large difference between the categories of the ExtAss (Kılıç et al., 2020). The rare events logistic regression estimator generates largely unbiased and lower-variance estimates of logit coefficients as well as the variance-covariance matrix of the logit coefficients by correcting for small samples and rare events (King & Zeng, 1999a, 1999b). Common statistical analysis approaches, such as binary logistic regression, can underestimate the probability of rare events. Therefore, corrections by the rare events logistic regression estimator outperform the existing methods such as binary logistic regression (King and Zeng, 1999a). The rare events logistic regression analysis utilizes a finite sample correction developed by McCullagh and Nelder (1989) and extends to simultaneous correction for selection on the dependent variable developed by King and Zeng (1999a, 1999b). It also calculates and reports robust variance estimates known as the Huber/White/sandwich estimator (Huber, 1967; White, 1980).

Rare events logistic regression analysis.

t statistics in parentheses; * p<0.10, ** p<0.05, *** p<0.01.

The sample is based on the existence of CSRrepr in columns 2, 3, 5, and 6.

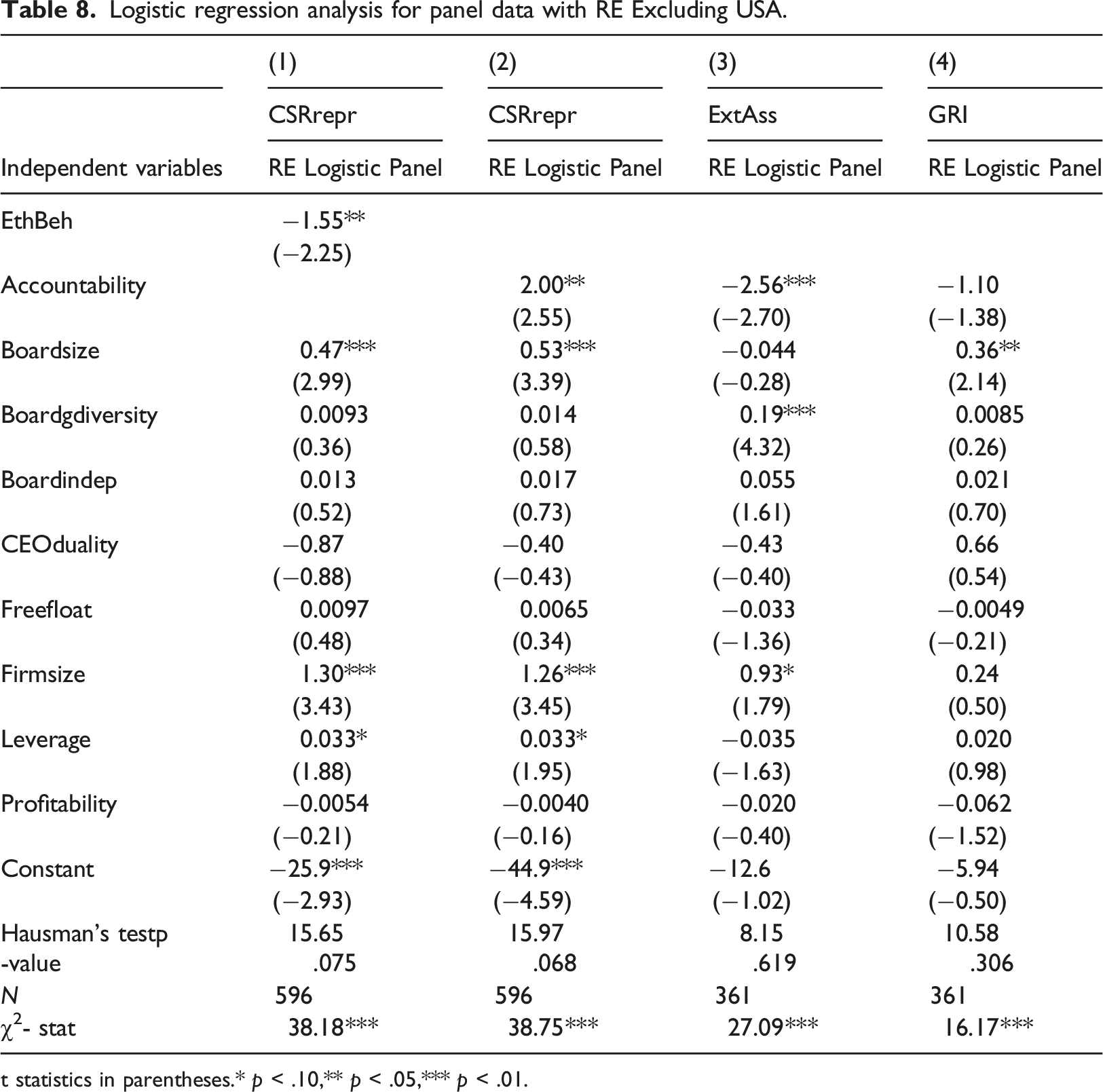

Logistic regression analysis for panel data with RE Excluding USA.

t statistics in parentheses.* p < .10,** p < .05,*** p < .01.

The robustness tests largely overlap with the baseline analyses, although there are two exceptions. The negative association between EthBeh and CSRrepr obtained in the baseline analysis is not supported by the analysis with lagged values. Hence, it appears that while the ethical environment affects the sustainability report dissemination of H&T firms negatively in the current period, it does not affect it in the subsequent reporting period. Thus, the significant association between the two variables should be considered in the concurrent periods. Alternatively, it could be inferred that H&T firms’ sustainability reporting practices are not affected by the prior period’s ethical environment but by the current period’s ethical environment. As incremental evidence, Accountability and its two components’ relationship with GRI are found to be negatively significant in the robustness tests, which are insignificant in the baseline analysis. These inconsistent outcomes could be explained as firms’ decisions to adopt GRI being a reflection not of the current period’s accountability environment but of the previous period’s accountability environment. However, it should be noted that this relationship is adverse as in a weak accountability environment, firms are stimulated to issue a GRI-based sustainability report one year later. This may be due to the time required for GRI adoption as firms prepare, learn, and implement standards, which are realized one year after. The other findings are in line with the baseline results.

Discussion and conclusion

Most prior studies have tested how internal (i.e., firm-level) characteristics affect sustainability reporting practices but have largely ignored the role of external forces (i.e., institutional characteristics) on those practices. Without considering the external context, firm-level attributes may not be sufficient to explain the behaviors of organizations as external forces may exert explicit or implicit enforcement. Hence, this study addresses the gap outlined in the literature and tests whether H&T firms undertake sustainability reporting practices as a result of the ethical environment and strength of accountability in the countries in which they are situated. Drawing on institutional theory, Uyar et al. (2021a) previously investigated the effects of institutional environments’ on the tourism sector’s sustainability reporting tendency. However, they ignored the assurance dimension of sustainability reporting. Unlike our study, which focuses on the ethical environment and strength of accountability, they tested the influence of the quality of country-level environmental, social, and governance (overall public governance) on the tourism sector’s sustainability reporting tendency. A very recent study also suggests that institutional factors in CSR studies focusing on the H&T sector should be considered, implying that country-level context may matter in sustainability practices (Uyar et al., 2021b). In addition to sustainability reporting, we study the assurance of sustainability reports to draw the attention of the H&T industry to the topic for two reasons: first, it enhances the credibility of sustainability reports, and, second, the H&T sector’s assurance adoption rate is very low (Jones et al., 2014). We also focus on the GRI framework both because, as a widely accepted framework, it helps firms disclose consistent and comparable sustainability reports (Uyar et al., 2021a) and because H&T firms’ GRI adoption rates are not at a satisfactory level (Guix et al., 2019).

The study’s outcomes confirm the validity of institutional theory in explaining corporate sustainability reporting practices in the H&T sector. While ethical behavior represents informal institutions, the strength of auditing and financial reporting standards constitutes formal institutions. The results indicate that firms domiciled in a highly ethical environment are less likely than weak ethical environment to issue a sustainability report, implying a substitution effect between the ethical sensitivity of the context and the sustainability reporting tendency of the firms. In line with mimetic isomorphism (DiMaggio and Powell, 1983), therefore, firms domiciled in environments with ethical sensitivity behave similarly by not disclosing sustainability practices. However, accountability yields the opposite result as firms in environments characterized by high accountability are more likely to issue a sustainability report, implying a complementary effect between the strength of the accountability and the firms’ sustainability disclosure. This confirms that regulatory forces associated with coercive isomorphism (DiMaggio and Powell, 1983) exert considerable influence on the desire of firms to carry out sustainability reporting. This finding is supported by the two proxies of accountability: the strength of auditing standards and the protection of minority shareholders’ rights. However, this relationship is not true of acquiring an external assurance as accountability has a negative association with the assurance statement. This means that H&T firms established in weakly regulated contexts feel more obliged than strongly regulated contexts to assure their sustainability reports externally (Kılıç et al., 2020). The weak regulatory environment may fuel agency conflicts between shareholders and managers, to which assuring corporate reports may be a positive, mediating response (Choi and Wong, 2007) that justifies assurance costs (Perego, 2009). The insignificant association between accountability and adoption of the GRI framework may reflect two contradictory views. On the one hand, firms may feel stronger pressure from stakeholders and are more motivated to follow GRI guidelines in a higher accountability environment (Kılıç et al., 2020). On the other hand, in a poor accountability environment, firms may try to compensate for ineffective institutional mechanisms through structured sustainability reporting that follows GRI (Kılıç et al., 2019). Thus, these two opposing views might not yield a precise negative or positive direction in the analysis outcomes. Another explanation could be that because following GRI guidelines is not mandated by national regulations, firms may not be encouraged to adopt the guidelines regardless of the context and consider free-format sustainability reporting sufficient for dissemination. Overall, the results confirm that H&T firms take formal and informal institutions into consideration when engaging in sustainability reporting and assurance practices (Uyar et al., 2021a).

Practical implications

The findings suggest several implications for firms and policymakers. Firms can incorporate the findings into their decision-making on whether to report sustainability practices, to assure their sustainability report externally, and to follow GRI guidelines in sustainability reporting depending on the contingencies. Rather than clearly indicating that a report should or should not be published, the results suggest consideration of the contexts, which is the distinctive contribution of this study relative to past studies. As presumed, the context matters in stimulating H&T firms to engage or not engage with sustainability reporting and assurance practices. The findings suggest that H&T firms should disclose sustainability reports in weak ethical environments but may not need to disclose sustainability reports in high ethical environments. In highly ethical environments, H&T firms may not feel obliged to publish a formal sustainability report to communicate with stakeholders and may share their sustainability practices in a transparent and timely manner by using other communication mechanisms, such as social media.

However, the positive link between accountability and sustainability reporting signals that the regulatory environment concerning auditing and financial reporting standards drives sustainability reporting. National auditing and financial reporting standards lay institutional foundations for corporate reporting, and the strength of those standards indicates that the state is striving to save the rights of shareholders and stakeholders by improving the quality of corporate reports. Moreover, the positive association between protecting minority shareholders’ rights and sustainability reporting implies that corporate transparency and disclosure are important mechanisms in safeguarding minority shareholders’ investments against the abuse of managers and major shareholders in the H&T sector. Nevertheless, the negative association between accountability (i.e., minority shareholders’ rights protection) and the external verification of sustainability report content may be attributable to the cost associated with obtaining independent verification. Overall, the results may help H&T firms shape their corporate transparency and accountability strategies, considering the differential roles of informal and formal institutional mechanisms in sustainability reporting practices.

The findings suggest to policymakers that formal and informal institutional foundations are closely related to H&T firms’ sustainability reporting and assurance practices. The unethical behaviors of public officials and/or politicians, such as accepting bribery, spoil the ethical business environment and force H&T firms to make extra efforts to assure stakeholders that they are working for the good of the environment and society. Furthermore, formulating sound public policies to save shareholders’ and stakeholders’ rights encourages H&T firms to respect the rights of those parties by disseminating sustainability information. This mirror effect, in turn, may motivate the public domain to undertake legislative revisions to better address environmentalists’ and communities’ concerns.

Overall, the results bear important economic implications for the H&T sector’s sustainable development. The studied sustainability reporting and assurance practices may have financial consequences concerning the costs and, eventually, profitability of firms. Reporting sustainability initiatives by collecting the associated data and obtaining an assurance statement on the sustainability reports may incur substantial costs 8 for H&T firms and tighten their profit margin. Considering the contextual factors, therefore, the results may help firms set corporate policies regarding sustainability reporting and assurance practices. For example, while they may benefit from disclosing a sustainability report in a weak ethical environment, they may decide against disclosing it in a high ethical environment and avoid associated costs. Likewise, they may decide to assure their sustainability report in low accountability environments to ensure the report’s credibility, but they can avoid assuring it in high accountability environments. However, the results highlight the irrelevancy of the institutional environment in whether firms adopt GRI guidelines, which does not justify the associated costs of tracking and synthesizing the sustainability data by adhering to the GRI framework. In this case, the results may help H&T firms effectively allocate their scarce financial resources among sustainability reporting, assurance initiatives, and other areas, such as marketing, that may strengthen their competitive position. Hence, the results can enhance the H&T sector’s economic and sustainable development by taking the particularities of the context into consideration. Finally, while firms engage with sustainability issues to appease stakeholders, their attempts to align with shareholders’ interests are likely to affect the capital flow of the H&T sector obtained from the stock market. This occurs because the H&T industry is presumed to be capital-intensive (Chen, 2012; Merkert and Swidan, 2019), and shareholders closely track the sector’s discretionary expenses associated with sustainability investments due to tight profitability (Park et al., 2017). Hence, the findings may help H&T firms align with shareholders’ concerns while pleasing stakeholders by highlighting contextual factors that may eventually foster the sector’s economic development.

The sample of this study includes publicly traded H&T firms listed in the Thomson Reuters Eikon database for the years 2011–2018. This dataset may put a constraint on generalizing the findings to non-publicly traded and non-H&T firms, as well as beyond the sample period. The study, however, suggests several future research avenues. A study focused on firms established in developing countries may reveal interesting results and implications, given that their institutional characteristics are different from those in developed countries. Another potential study might examine whether stock market regulations stimulate H&T firms to engage with sustainability reporting, assurance, and the GRI framework. Other potential studies might incorporate certain institutional characteristics as the main variables of interest or moderators into the study, such as political stability, rulemaking, and enforcement mechanisms, which are likely to influence the sustainability reporting decisions of H&T firms.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Appendix

Sampling distribution based on data points and number of firms within countries

| Country | Number of data points | Percent | Number of firms within country | Percent |

|---|---|---|---|---|

| Australia | 101 | 10.78 | 17 | 9.88 |

| Bahrain | 3 | 0.32 | 1 | 0.58 |

| Brazil | 1 | 0.11 | 1 | 0.58 |

| Canada | 28 | 2.99 | 4 | 2.33 |

| China | 13 | 1.39 | 5 | 2.91 |

| France | 19 | 2.03 | 3 | 1.74 |

| Germany | 8 | 0.85 | 1 | 0.58 |

| Gibraltar | 3 | 0.32 | 1 | 0.58 |

| Greece | 8 | 0.85 | 1 | 0.58 |

| Hong Kong | 53 | 5.66 | 8 | 4.65 |

| Ireland; Republic of | 8 | 0.85 | 1 | 0.58 |

| Isle of Man | 3 | 0.32 | 1 | 0.58 |

| Italy | 8 | 0.85 | 1 | 0.58 |

| Japan | 32 | 3.42 | 4 | 2.33 |

| Korea; Republic (S. Korea) | 11 | 1.17 | 2 | 1.16 |

| Macau | 23 | 2.45 | 3 | 1.74 |

| Malaysia | 24 | 2.56 | 3 | 1.74 |

| Malta | 3 | 0.32 | 1 | 0.58 |

| Mexico | 2 | 0.21 | 1 | 0.58 |

| New Zealand | 12 | 1.28 | 2 | 1.16 |

| Philippines | 8 | 0.85 | 1 | 0.58 |

| Singapore | 8 | 0.85 | 1 | 0.58 |

| South Africa | 38 | 4.06 | 6 | 3.49 |

| Spain | 8 | 0.85 | 1 | 0.58 |

| Sri Lanka | 8 | 0.85 | 1 | 0.58 |

| Sweden | 1 | 0.11 | 1 | 0.58 |

| Taiwan | 8 | 0.85 | 1 | 0.58 |

| Thailand | 5 | 0.53 | 1 | 0.58 |

| United Arab Emirates | 2 | 0.21 | 1 | 0.58 |

| United Kingdom | 146 | 15.58 | 21 | 12.21 |

| United States of America | 341 | 36.39 | 75 | 43.60 |

| Uruguay | 1 | 0.11 | 1 | 0.58 |

| Total | 937 | 100.00 | 172 | 100.00 |