Abstract

This research examines the relationship between environmental, social, and governance (ESG) performance and bankruptcy risk for hospitality and tourism (HT) firms, in comparison to other industry sectors. It further examines this proposed relationship within the contingencies of the Covid-19 pandemic and four corporate governance attributes. Fixed-effects regression analyses with 21,563 firm-year observations indicate that firm bankruptcy risk decreases as ESG performance improves. However, relative to both non-HT firms in general and firms in other service sectors, HT firms demonstrate a weaker effect of ESG performance on mitigating bankruptcy risk, especially after the Covid-19 outbreak. In addition, smaller boards and a lower proportion of institutional ownership enhance the relationship between ESG and bankruptcy risk, while CEO duality and board gender diversity attenuate this relationship. This study highlights the uniqueness of the HT industry, and its findings suggest corporate governance practices that can strengthen the impact of ESG initiatives.

Keywords

Introduction

Firms in the hospitality and tourism (HT) industry have been increasingly committed to corporate social responsibility (CSR) initiatives to pursue sustainable business growth (Su and Chen, 2020). A firm’s performance on three dimensions -- environmental, social, and governance (ESG) -- quantifies its efforts in following CSR guidelines for decision-making (C.D. Chen et al., 2022). While the relationship between sustainable business practices and firm financial performance has been documented by many hospitality studies (Babajee et al., 2022; Su and Chen, 2020), the effect of such practices on firm bankruptcy risk has just received increasing interest due to businesses struggling amid the Covid-19 pandemic (Almeida, 2023). Bankruptcy risk refers to the likelihood that a firm will be unable to meet its debt obligations, thereby rendering it insolvent (Bărbuță-Mişu and Madaleno, 2020). Broad environmental factors, including economic recession, high unemployment rate, and excessive population density, increase the risks of firms going bankrupt (Boratyńska, 2021). Internal factors, such as low profit, low operating cash flow, and high leverage ratio, heighten firms’ bankruptcy risks (Gu, 2002; Kim and Gu, 2006; Park and Hancer, 2012). The Covid-19 pandemic challenges global businesses, especially the HT industry (Rastegar et al., 2023). The financial performance of the travel, catering, accommodation, and transportation sectors was severely impacted by the radical decline in consumer demand during the pandemic (Shen et al., 2020). As a matter of fact, 9.7% of restaurants and 4.6% of entertainment establishments in the U.S. filed for either Chapter 7 liquidation or Chapter 11 reorganization in 2020 (Collins-Thompson et al., 2021). Publicly traded firms such as Hertz Global Holdings (Hertz Car Rental), The Restaurant Group, and Cirque Du Soleil, among others, were not immune to the financial distress caused by the pandemic and subsequently filed for bankruptcy in 2020 (BBC, 2021; Hertz, 2020; Valinsky, 2020). Using a predictive model, Matejić et al. (2022) showed that the heightened bankruptcy risk of HT companies due to the Covid-19 pandemic would persist till 2026. Indeed, 17 restaurant chains in the U.S., including Red Lobster, filed for bankruptcy in 2024, showing the prolonged damage caused by the pandemic (Maze, 2024). These incidents highlighted the importance and urgency of investigating factors that lower bankruptcy risk and examining whether the effect was compromised due to the Covid-19 pandemic. Although financial failure is not a new phenomenon, studying such a topic becomes highly relevant in the post-pandemic era for building resilience in HT businesses.

Examining the linkage between ESG performance and bankruptcy risk is critical, especially for HT companies. Unlike necessity goods, the sales of HT products highly depend on consumers’ discretionary income. Compared to low-impact industries such as agriculture and mining, the HT industry experienced a substantially greater decline in financial performance amid the economic recession (Shen et al., 2020). However, studies comparing the performance of HT and non-HT firms have been limited. A previous study found that the stock prices of hospitality firms are more sensitive to changes in ESG practices than those of non-hospitality firms (Su and Chen, 2020). Nevertheless, no study has addressed the industry differences regarding firms’ chances of survival. Therefore, an interesting question arises: Will ESG performance affect bankruptcy risk differently for HT firms versus non-HT firms?

Aiming to bridge the gaps, this research examines the linkage between ESG and bankruptcy risk with multiple objectives. It first analyzes the relationship between ESG performance and the bankruptcy risk of publicly traded U.S. firms and examines if the relationship differs between HT and non-HT firms. Second, it further examines whether the relationship changes after the Covid-19 outbreak and whether the effect of the HT industry interacts with the impact of the Covid-19 pandemic. In addition, as corporate governance is closely related to the survival of companies (Charkham, 1994), this study investigates the moderating effect of corporate governance characteristics on the relationship between ESG and bankruptcy risk. The current research contributes to crisis management studies by revealing the effectiveness of ESG in alleviating firm bankruptcy risk. It also adds to the literature by exploring the uniqueness of the HT industry. The findings provide valuable insights to company executives in ESG-related decision-making. The study also suggests potential interventions on the corporate governance structure that enhance the impact of ESG initiatives.

Literature review

ESG and firm bankruptcy risk

Although scholars have not reached a consensus on theories governing the bankruptcy phenomenon, existing research findings agree that liquidity, profitability, and leverage are the main triggers of firm bankruptcy (Lukason, 2019). Successful strategies and operational efficiency are key factors that reduce firm bankruptcy risks (Almeida, 2023). Hospitality and tourism (HT) research unveiled that media coverage (Li et al., 2022; Yuan et al., 2022), good management practice (Gemar et al., 2019; Kaniovski et al., 2008), and avoiding business misconduct (Q.X. Chen et al., 2022) contribute to the survival of firms. Researchers studying strategies to reduce bankruptcy risk from a stakeholder theory perspective argue that firms should strive to provide value for all stakeholders, including owners, customers, employees, and communities. A main path to achieving this goal is to demonstrate social responsibility through the implementation of ESG initiatives (Mushafiq and Prusak, 2022). ESG initiatives help a firm build social support and trust by demonstrating that it prioritizes stakeholders’ interests (Mao et al., 2023). Stakeholder involvement in business drives sales growth and operational efficiency, thereby enhancing the firm’s value and increasing shareholders’ wealth (Mao et al., 2023). Meanwhile, ESG initiatives strengthen brand image and customer loyalty, which have been found to significantly lower the risk of restaurant shutdown amid the pandemic (Arachchi and Samarasinghe, 2023). Although the impact of ESG strategy on a firm’s topline performance has been studied in the HT field, its connection with bankruptcy risk has not been empirically tested in the U.S. market. Using data from Asian and European countries, researchers have found that investment in ESG enhances firms’ value and reduces bankruptcy risk (Z. Lin, 2023; Nilsson and Wallin, 2023; Wong et al., 2021). The following hypothesis is developed to capture the relationship between ESG and firm bankruptcy risk.

Firms with stronger ESG performance bear lower bankruptcy risks.

The moderating effects of the HT industry and the Covid-19 pandemic

Mixed findings have been revealed regarding the impact of ESG performance on business operations. Across 11 industries 1 , the ESG score exhibits a non-linear relationship with corporate efficiency, with positive associations observed only among companies with moderate levels of ESG engagement (Xie et al., 2019). Firms with either low or high ESG engagement show a negative relationship between ESG performance and corporate efficiency, suggesting that implementing ESG initiatives does not come without a cost. It is controversial whether these initiatives, such as energy-saving and waste-reduction programs, are associated with higher or lower business profits (Bohdanowicz, 2006). While some studies suggest that the long-term cost savings associated with environmentally responsible operations outweigh the short-term expenditures, business operators often express concerns about the substantial investment required, particularly in uncertain market conditions (Bohdanowicz, 2006). Prior literature emphasizes the importance of accounting for industry-specific factors when evaluating the effects of ESG initiatives on firm outcomes (Eccles et al., 2012), as each industry faces unique risks shaped by its external environment (Endrikat et al., 2014). HT firms typically operate within a context of polycrisis, an environment marked by the convergence of multiple risk factors, thereby leading to heightened demand uncertainty (Gössling and Scott, 2024). As a critical determinant of firm survival (Chen and Yeh, 2012), demand uncertainty in the HT industry amplifies the risk of financial distress, which may weaken the potential of ESG engagement in mitigating bankruptcy risk. For example, Ortiz-Villajos and Sotoca (2018) find that while strong corporate social responsibility (CSR) performance significantly enhances the longevity of manufacturing firms, this effect does not hold for service firms. Drawing from these insights, the current study posits that the relationship between ESG performance and bankruptcy risk is likely weaker for HT firms. Accordingly, the following hypothesis is proposed.

The relationship between ESG performance and firm bankruptcy risk is weaker for HT firms compared to non-HT firms. The cost burden of ESG initiatives can be exacerbated during periods of turbulence. In the U.S., the Covid-19 pandemic drastically reduced industrial production, personal consumption, capital investment, and stock prices (Thorbecke, 2020). Previous research showed that ESG performance negatively affected hospitality firms’ return on assets (ROA) during the first quarter of 2020 (i.e., the Covid-19 outbreak) due to the high costs (Lin et al., 2023). While ESG investment could lower a firm’s bankruptcy risk, the Covid-19 pandemic may weaken its effectiveness due to the significant cost burden it imposes during a severe decline in revenue. Likewise, Habermann and Fischer (2023) suggest that although investments in socially responsible practices could reduce the likelihood of bankruptcy during times of crisis, the risk of financial default increases when the costs of these initiatives outweigh their immediate benefits. Therefore, this study proposes that Covid-19 weakens the relationship between ESG performance and firm bankruptcy risk.

The relationship between ESG performance and firm bankruptcy risk is weaker following the Covid-19 outbreak than it was before. Given that the HT industry and the Covid-19 pandemic could both attenuate the positive influence of ESG initiatives, this study further proposes that the interaction of these two moderators weakens the relationship between ESG performance and firm bankruptcy risk to a greater extent. The increased likelihood of failure among HT firms amid the pandemic can be attributed to several industry-specific characteristics. First, the HT industry is capital-intensive and typically operates with high leverage ratios (Li and Singal, 2022), making steady net cash inflows essential to meet financing obligations. Second, the HT industry is especially vulnerable to external shocks due to its reliance on discretionary consumer spending. Third, the delivery of HT service depends heavily on human interaction, which was significantly restricted during the pandemic. These characteristics collectively made HT firms more vulnerable amid the Covid-19 pandemic (Aydogan et al., 2023). The distinctive nature of the industry makes it more vulnerable to crises. As such, the following hypothesis is proposed.

Compared to non-HT firms, the moderating effect of the Covid-19 pandemic on the relationship between ESG performance and firm bankruptcy risk is more profound for HT firms.

The moderating effects of corporate governance attributes

The effectiveness of corporate decisions depends substantially on the corporate governance structure (Cutting and Kouzmin, 2000). Corporate governance quality is closely related to the survival and failure of companies (Charkham, 1994). Existing research has identified board monitoring capability, board diversity, and executives’ power as key attributes that influence the strategic decisions made by the board of directors. The current research measures firms’ governance based on these attributes.

Board monitoring factors: Institutional ownership and board size

Stronger board monitoring emphasizes the interests of shareholders (Cutting and Kouzmin, 2000). Existing literature suggests institutional owners significantly influence a firm’s strategic decisions by monitoring management’s decision-making and strategy implementation (Ozdemir et al., 2023). Institutional ownership refers to a company’s equity owned by large institutions (i.e., banks, insurance companies, pension funds). Scholars suggest that firms with high levels of institutional ownership exhibit stronger ESG performance because institutional owners facilitate the acceptance of long-term-oriented projects (Wang and Sun, 2022) and encourage top management to engage in ESG initiatives, thereby building a responsible and trustworthy brand image (Park et al., 2019). However, when the firm is financially distressed, which is a precursor to bankruptcy, institutional owners are inclined to prioritize short-term benefits over supporting long-term value creation (Hutchinson et al., 2015). Indeed, empirical evidence suggests that institutional owners tend to raise more concerns about ESG projects because the costs and benefits are often unclear (Nofsinger et al., 2019). Therefore, this study proposes a negative moderation effect of institutional ownership on the relationship between ESG performance and bankruptcy risk.

Institutional ownership percentage negatively moderates the relationship between ESG performance and firm bankruptcy risk, so the relationship is stronger when the firm has a lower proportion of institutional owners. Likewise, the board’s monitoring capacity increases as the board size increases (John and Senbet, 1998). Board size refers to the number of directors on the board, and research studying HT companies shows a positive effect of board size on firm ESG performance (Arici et al., 2024; Husted and Sousa-Filho, 2019). However, intensive monitoring from a large board results in companies avoiding risk-taking investments when experiencing financial difficulties (Nakano and Nguyen, 2012). In addition, a larger board tends to consider a broader range of viewpoints from its directors when evaluating proposed strategies, which can slow down the decision-making process. Given the inherent uncertainty surrounding the risk and return of ESG projects, this study proposes that a larger board size has a negative impact on the relationship between ESG performance and firm bankruptcy risk.

Board size negatively moderates the relationship between ESG performance and firm bankruptcy risk, so the relationship is stronger when the firm has fewer directors on its board. In summary, firms with a higher percentage of institutional ownership and larger boards are subject to increased monitoring and control over investment decisions. This often results in a more cautious approach to ESG investments, particularly when financial returns are uncertain. Such heightened oversight may diminish the effectiveness of ESG initiatives in reducing bankruptcy risk.

Board gender diversity

Another board attribute — gender diversity — also significantly impacts firms’ sustainability practices. Gender diversity refers to a fair representation of people of different genders. In the corporate governance context, gender diversity is reflected through the ratio of female representation on the board of directors. The social role theory posits that individuals in the workplace are expected to behave consistently with culturally rooted perceived characteristics associated with their genders (M.H. Chen et al., 2021; Harrison and Lynch, 2005). For example, female executives are more communal and participative and care more about contributing to society (Gerged et al., 2023). Empirical evidence indicates that firms with greater board gender diversity show stronger ESG performance (Romano et al., 2020), and board gender diversity enhances the positive effect of ESG performance on firm ROA (Alodat and Hao, 2024). Research studying the impact of ESG during the Covid-19 pandemic also suggests that firms with greater gender diversity are more effective in coping with the shock through ESG programs (Savio et al., 2023). Building on these findings, this study proposes that a higher proportion of female directors on the board enhances a firm’s ability to reduce bankruptcy risk through ESG investments.

Board gender diversity positively moderates the relationship between ESG performance and firm bankruptcy risk, so the relationship is stronger when a larger proportion of females are on the board.

CEO duality

Authoritative figures within a company exercise concentrated power in strategic decision-making, thereby influencing the firm’s ESG performance (Chen et al., 2021). For example, research with a broad sample finds that CEOs who also chair the board of directors (i.e., CEO duality) tend to reduce ESG investment due to cost considerations (Abdullah and Hashmi, 2024). Arici et al. (2024) studied HT firms in particular and found that the negative effect of CEO duality was observed on the company’s environmental performance but not on social and governance performance. According to stewardship theory, when CEOs chair the board, they are strongly incentivized to maximize shareholder value (Donaldson and Davis, 1991). While the stronger alignment of owners’ and managers’ interests enhances the value of HT firms (Guillet et al., 2013), it may also lead CEOs to prioritize project returns more (Chari et al., 2019). Since ESG initiatives are often associated with minimal financial returns (Halbritter and Dorfleitner, 2015), this study proposes that CEO duality negatively impacts the relationship between ESG performance and firm bankruptcy risk.

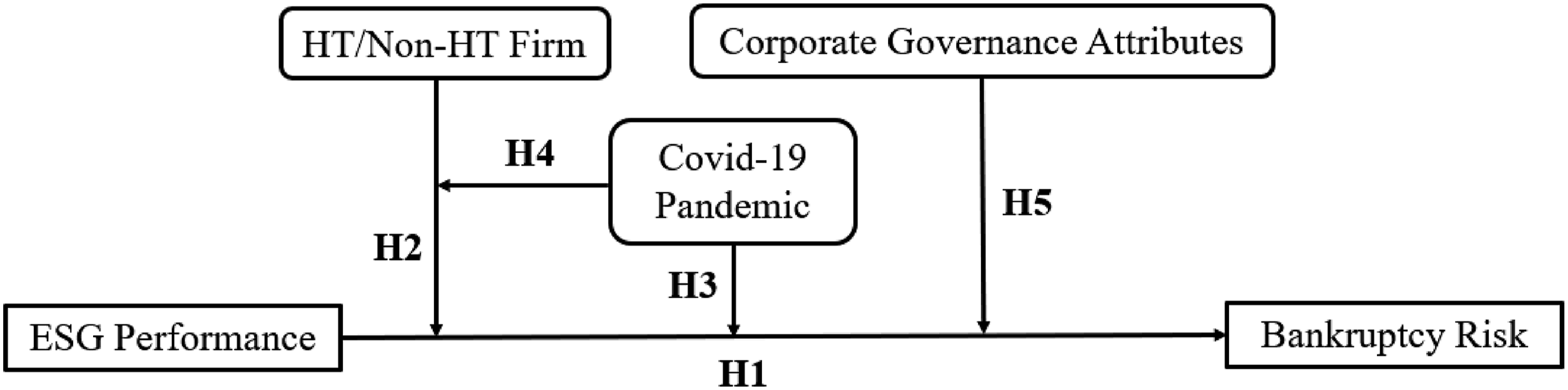

CEO duality negatively moderates the relationship between ESG performance and firm bankruptcy risk, so the relationship is weaker when the CEO chairs the board of directors. Figure 1 presents the research framework of this study with the proposed hypotheses.

Conceptual framework.

Methodology

Data

The ESG performance ratings were obtained from Thomson Reuters’ ESG database, which provides an aggregated ESG score at the firm level, as well as pillar scores for each dimension of ESG: environmental, social, and corporate governance. The ESG performance data was merged with annual firm financials obtained from the Compustat database. After merging datasets, excluding financial services and utility companies, and cleaning for missing observations, the final panel dataset comprised 21,563 firm-year observations across 2634 publicly traded companies for the primary analyses. 2 Corporate governance variables, including board size, board gender diversity, and CEO duality, were also retrieved from Thomson Reuters’ ESG database. Institutional ownership data was retrieved from FactSet. Table 1 presents the industry segments included in the analyses, along with the number of observations for each industry during the analysis period from 2002 to 2023. Hospitality and tourism (HT) firms are classified under the service category and contributed 564 observations, while firms in other service sectors contributed 4041 observations. HT firms include hotels and motels, eating and drinking places, airlines, and leisure and amusement parks according to the Standard Industrial Classification (SIC).

Empirical model

A series of regression equations was estimated to examine the relationship between ESG performance and firm bankruptcy risk, as well as the role of the HT industry and the Covid-19 pandemic on this relationship. Corporate governance variables were introduced to the models as moderators to examine how they alter the relationship between ESG performance and bankruptcy risk. All models are presented below. Equation (1) tests the main effect of ESG performance on bankruptcy risk. Equations (2) and (3) test the moderating effects of the HT industry and the Covid-19 pandemic, respectively. To further explore whether the moderating effect of industry changes its magnitude due to the pandemic, equation (4) incorporates a three-way interaction term (ESGC × HT × Covid) to examine whether the relationship between ESG performance and bankruptcy risk differs for HT firms before and after the Covid-19 pandemic.

To estimate the moderating effect of corporate governance on the relationship between ESG performance and bankruptcy risk, governance attributes variables were added to equation (1) to derive equation (5). Although the role of the HT industry in this relationship was not explicitly hypothesized, governance quality variables were incorporated into equation (3) to derive equation (6), allowing exploration of this effect specifically for HT companies.

Models are primarily estimated with fixed-effect regression, and robust standard errors are clustered at the firm level to ensure that they are heteroscedastic and autocorrelation-consistent (Hoechle, 2007). Models that include an HT dummy, a time-invariant dummy variable, are estimated using random-effects regression to prevent collinearity between firm fixed effects and the HT dummy. In a similar vein, the moderating effect of CEO duality is assessed using random-effects regression, given the limited within-firm variation in the CEO duality construct and to prevent potential collinearity with firm fixed effects. In the model,

Dependent variable

The dependent variable of this study is bankruptcy risk, which is proxied by Atman’s Z-score (hereafter referred to as Z-score). Z-score has been the dominant failure indicator used worldwide due to its 75%-90% predictive accuracy (Altman et al., 2017). Using tourism and cruise firms as samples, Goh and Roni (2022) demonstrate that the Z-score is a reliable indicator for predicting bankruptcy risk. Z-Score is a composite indicator of bankruptcy risk, which relies on five financial ratios calculated using information from balance sheet and income statement (working capital to total assets ratio (WC/TA); retained earnings to total assets ratio (RE/TA); earnings before interest and taxes to total assets ratio (EBIT/TA); market value of equity to book value of total liabilities ratio (MV/TL); and sales revenue to total assets ratio (Sales/TA)). The discriminant function proposed by Altman et al. (2017) is as follows:

A Z-score below 1.8 indicates that the company is facing financial distress, with a high likelihood of reorganization or dissolution within 2 years. A Z-score above 2.99 suggests minimal bankruptcy risk, while a score between 1.8 and 2.99 indicates moderate risk (Goh and Roni, 2022). Therefore, a higher Z-score represents a lower risk of financial distress and bankruptcy.

Independent and moderating variables

The independent variable in the primary analysis is the annual ESG controversy score (ESGC), which provides a comprehensive evaluation of a company’s ESG performance based on the three pillars of the ESG. ESGC ranges from 0 to 1, with higher values reflecting stronger ESG performance. 3 The individual pillar scores -- environment (E) (emissions, innovation, and resource usage), social (S) (human rights, workforce, product responsibility, and community), and governance (G) (shareholders, management, and CSR Strategy) were used in the robustness tests. A dummy variable, “Covid”, was created to indicate whether the firm-year observation occurred after the Covid-19 outbreak in the U.S. at the beginning of the 2020 calendar year. Specifically, Covid was coded 1 for firm-year observations from 2020 onward and 0 otherwise. Similarly, the dummy variable named HT was created to investigate the effect of the HT industry. It was coded as 1 for firms in the HT industry and 0 otherwise.

Four corporate governance quality measures (i.e., institutional ownership, board size, board gender diversity, and CEO duality) were constructed and examined for their moderating effect on the relationship between ESGC and bankruptcy risk. Institutional ownership is operationalized as the percentage of equity shares held by institutional owners relative to total shares outstanding (Lin and Fu, 2017). Board size (BrdSize) is measured by the number of directors on the board. Board gender diversity (BrdGenDiv) is the ratio of female board members to the total number of board members (Reguera-Alvarado et al., 2017). A dummy variable, CEODual, takes the value of 1 if the CEO is also the chairman of the board of directors, and 0 otherwise. These variables replace “CorpGov” in equations (5) and (6).

Control variables

A set of firm-level control variables was included in the regression model. Firm size (FSize) was controlled for because larger firms are less likely to go bankrupt (Darrat et al., 2016). FSize is measured as the natural logarithm of the book value of total assets. Return on assets (ROA) was added to the models to capture firm profitability, as companies with superior profitability are less likely to experience bankruptcy (Cooper and Uzun, 2019). ROA is calculated as the ratio of net income to total assets. Since high liquidity reduces the chance of financial distress and bankruptcy, the impact of liquidity was also accounted for by including the ratio of cash and cash equivalents to the total assets (Cash/TA) as a control variable. In addition, the effect of leverage (Lev), measured as the ratio of total liabilities to total assets, was controlled for, as high leverage increases bankruptcy risk (Cooper and Uzun, 2019).

Results

Descriptive statistics

Table 2 presents the descriptive statistics of the variables. The sample covers 21,563 firm-year observations for primary analyses. The Z-scores of the sample firms range from −1 to 3.86, with an average of 0.91 and a standard deviation of 0.67. The mean ESG compiled score (ESGC) is 0.38, with a high of 0.82, a low of 0.08, and a median of 0.35. The mean profitability, measured in terms of ROA, is −1%, implying that the sample firms experience a net loss on average. The liquidity measure (Cash/TA ratio) ranges from 0 to 0.96. The average leverage ratio is 0.55. Regarding the potential moderators, institutional owners hold an average of 75% of the sample company’s shares. The average board size for the sample is 9.16 (roughly nine board members), with an average gender diversity ratio of 51%. In addition, 57% of the boards are chaired by the company’s CEO.

Empirical findings

The result of the direct relationship between ESGC and bankruptcy risk is presented in column 1 of Table 3. The significant positive coefficient of ESGC (β = 0.089, p < 0.01) suggests that the bankruptcy risk decreases (Z-score increases) as ESG performance improves, supporting H1. The moderating effects of the HT industry and the Covid-19 pandemic were then examined using separate regression models, and the results are presented in columns 2 to 4. As indicated by the negative coefficient on the interaction term ESGC*HT (ß = −0.303, p < 0.1) in column 2, the decline in bankruptcy risk due to improved ESG performance is less pronounced for HT firms. Supporting H2, these results suggest that HT firms benefit from their ESG performance in reducing bankruptcy risk, but not as much as firms in other industries. The negative coefficient on the interaction term ESGC*Covid (ß = −0.067, p < 0.05) in column 3 implies the risk reduction effect of ESG performance on a company’s survival decays after the Covid-19 outbreak. Therefore, H3 is supported. Lastly, the three-way interaction term ESGC *HT*Covid in column 4 is negative and significant (β = −0.387, p < 0.05), indicating that HT companies experienced a more pronounced decline in the effect of ESG performance on reducing bankruptcy risk due to the Covid-19 pandemic, thereby supporting H4. The results of the control variables indicate that larger firms and firms with weaker profit-generating capabilities are more likely to face bankruptcy. Contrary to expectations, liquidity is negatively associated with the Z-score, suggesting that firms holding more liquid assets may be at a greater risk of bankruptcy.

Table 4 presents the results of the moderation analyses that incorporate four corporate governance measures. Each moderating variable was examined separately using two regression models, where the moderator first interacted with ESGC and then with ESGC*HT, to provide additional insights into whether the moderation effects differ between the HT and non-HT industries. The negative coefficient of ESGC*InstOwnPerc (ß = −0.305, p < 0.01) and ESGC*InstOwnPerc*HT (ß = −1.540, p < 0.05) in columns 1 and 2 suggest that a higher percentage of institutional ownership is associated with a weaker effect of ESG performance on bankruptcy risk, and this moderating effect is stronger for HT companies. The negative coefficient of ESGC*BrdSize (ß = −0.023, p < 0.05) in column 3 shows that a larger board attenuates the relationship between ESG performance and firm bankruptcy risk. This effect is more profound for HT companies, evidenced by the positive coefficient on the three-way interaction term ESGC*BrdSize* HT (ß = 0.081, p < 0.1) in column 4. The negative coefficient of ESGC*BrdGenDiv (ß = −0.327, p < 0.01) in column 5 suggests that a more diverse board attenuates the effect of ESG performance on bankruptcy risk. Yet, the non-significant interaction ESGC*BrdGenDiv* HT (ß = −0.336, p > 0.1) in column 6 implies that the effect does not differ by industry. Regarding the role of CEO duality, the negative coefficient of ESGC *CEODual (β = −0.080, p < 0.05) suggests that when the CEO is also the board chair, the linkage between ESG performance and bankruptcy is compromised. In addition, the moderating effect of CEO duality is more pronounced for HT companies, as evidenced by the positive coefficient on the interaction term ESGC*CEODual*HT (β = 0.523, p < 0.05) in column 8. Consequently, H5(a), H5(b) and H5(d) are supported while H5(c) is rejected.

Robustness test

Individual effects of ESG pillars

Robustness tests were conducted using ratings in each dimension of ESG as independent variables. The effects of three ESG pillars — environmental, social, and governance — on bankruptcy risk were examined. The results of fixed-effect estimations are presented in Table 5. Results in columns 1 through 4 with the environmental pillar as a single item (ß = −0.081, ß = −0.141, ß = −0.095, ß = −0.131, p < 0.01) suggest that the environmental performance of the sample companies is positively related to Z-Score, indicating a decrease in bankruptcy risk as companies engage more in environmentally responsible practices. Consistent with the analysis using ESGC as the predictor, the effect of environmental performance on non-HT companies is more pronounced compared to HT companies, as evidenced by the negative coefficient on EnvPillar*HT (ß = −0.319, p < 0.01) in column 2. In addition, the positive association between environmental initiatives and bankruptcy risk has become less pronounced since the Covid-19 outbreak, as shown in column 3 (ß = −0.052, p < 0.01). Results are similar for the social pillar. The coefficient on SocPillar in column 5 is positive and significant (β = 0.078, p < 0.01), suggesting that increased social responsibility performance reduces bankruptcy risk. This effect is less significant for HT companies, as evidenced by the negative coefficient on SocPillar*HT (β = −0.333, p < 0.05) in column 6. Lastly, columns 9 through 12 present the results of the governance pillar of ESG. Column 9 shows a positive and significant coefficient of GovPillar regressing on Z-Score (β = 0.063, p < 0.01), suggesting that increased governance quality is associated with a decline in bankruptcy risk. While this effect is strong, there is no statistical difference between HT and non-HT firms before and after the Covid-19 outbreak.

Findings pertinent to service firms

To provide evidence relevant to the service industry in particular, and further support the uniqueness of the HT business compared to other service sectors, the model estimation equations (1) to (6) were replicated and tested using only the service firms as the sample, which were dummy-coded as 1 for HT firms and 0 for non-HT service firms. The key results are consistent with those of the full sample analysis, indicating a significant risk-reduction effect of ESG on bankruptcy, with the effect being less pronounced for HT firms compared to non-HT service firms (ESGC*HT β = −0.360, p < 0.05), and this less pronounced effect is further exacerbated during the Covid-19 pandemic (ESGC*HT*Covid β = −0.439, p < 0.05). The revealed moderation effects largely align with those of the full-sample analysis, although differences are observed in the case of CEO duality. Consistent with the results of full sample analysis, institutional owner percentage moderates the relationship between ESGC and Z-score (ESGC*InstOwnPerc ß = −0.767, p < 0.01), and this moderation effect decays for HT compared to non-HT service firms (ESGC*InstOwnPerc* HT (ß = −1.260, p < 0.1). Board gender diversity shows a significant moderation effect (ESGC*BrdGenDiv ß = −0.388, p < 0.01), yet no difference is found between HT and non-HT service firms (ESGC*BrdGenDiv*HT ß = −0.346, p > 0.1). Board size remains a significant moderator, as in the full-sample analysis, although the difference between HT and non-HT service firms is not observed. Differing from the full sample, CEO duality is not a significant moderator between ESGC and bankruptcy risk (ESGC*CEODual ß = 0.069, p > 0.1) for service firms, nor is there a significant difference when comparing HT to non-HT service firms (ESGC*CEODual*HT ß = 0.347, p > 0.1). The individual ESG pillar analyses were also replicated using only service firms, and the significance levels of the effects are consistent with the full-sample analyses. Detailed statistics for service firms only are presented in the Appendix.

Discussion

Conclusion

The current research examined the association between ESG performance and firm bankruptcy risk, comparing hospitality and tourism (HT) to non-HT firms before and after the Covid-19 outbreak. Data from 2634 U.S. publicly traded companies spanning the period from 2002 to 2023 were analyzed to examine whether the effect of ESG performance on bankruptcy risk is moderated by the HT industry and the Covid-19 pandemic. The moderating role of corporate governance attributes in the relationship between ESG performance and firm bankruptcy risk was also investigated.

This study finds that enhanced ESG performance is associated with a reduced risk of bankruptcy. Compared to other industries, ESG engagement provides less protection against financial distress for HT firms, which may be attributed to the inherent characteristics of the industry. Given that most HT firms are capital-intensive and have high fixed costs, investors may prioritize short-term financial returns over the long-term benefits of ESG programs, supporting the “cost-consuming” view (Palmer et al., 1995). While environmental initiatives in the HT business often entail high implementation and maintenance costs, as well as long payback periods (Moneva et al., 2020), they can be considered an additional cost that negatively affects financial performance in the short term. In a similar vein, the Covid-19 pandemic weakens the effect of ESG initiatives because it transforms insurance-like benefits into cost-intensive obligations. For example, while 70% of business owners increased their companies’ social responsibility initiatives amid the pandemic (Carroll, 2021), mandatory quarantines and travel restrictions severely limited the consumption of tourism-related services, resulting in high costs with minimal returns. The similar findings from the service firm sample further support the uniqueness of the HT businesses, even in a homogeneous industry context. Compared to other service sectors such as healthcare and personal care, HT firms may not benefit as substantially from implementing ESG programs and are more vulnerable to economic turbulence.

Remedy strategies are discovered by analyzing the moderating effect of four corporate governance measures. The findings suggest that the relationship between ESG performance and bankruptcy risk becomes stronger as the percentage of institutional owners decreases. Institutional owners typically have a negative impact on ESG performance, as they view ESG programs as direct costs that reduce profits (Barnett and Salomon, 2006). Unlike Rossi et al. (2021), which found a positive effect of board size on the association between CSR practices and firm financial performance, this study showed that board size weakens the correlation between ESG performance and the likelihood of bankruptcy. A natural explanation is that larger boards exercise stronger control and oversight of sustainability practices, which may lead to underinvestment in ESG initiatives when firms experience financial distress. Quite surprisingly, board gender diversity is found to attenuate the association between ESG performance and bankruptcy risk, contrary to studies that support the positive influence of female leaders on the relationship between ESG and firm performance (Kahloul et al., 2022). One possible explanation is that females care more about the philanthropic aspects of sustainability practices (Ibrahim and Angelidis, 1995). A gender-diversified board may invest more in discretionary practices that do not yield sufficient financial returns (Freeman, 2010). For firms across all industries, CEO duality weakens the relationship between ESG performance and the risk of bankruptcy. However, this moderating effect is not observed within service firms, where CEO duality has a non-significant effect on the ESG-bankruptcy risk relationship. Compared to non-HT firms, the negative moderating effect of institutional ownership and board size on ESG performance is stronger for HT firms, suggesting that ESG initiatives in the HT industry may be more sensitive to the influence of corporate governance attributes.

Theoretical implications

The findings of this study contribute to the finance and HT literature in several ways. While previous research tried to understand the effect of ESG performance on the topline financial performance of HT firms (C.D. Chen et al., 2022; Y. Lin et al., 2023; Uyar et al., 2022), the current study shifts the focus from financial success to the probability of financial distress. To the best of our knowledge, the current study is the first to examine the ESG performance and bankruptcy risk while highlighting the uniqueness of the HT industry. In line with previous studies (Boubaker et al., 2020; Cohen, 2023), this research evidences that companies with high ESG ratings have a lower risk of bankruptcy. This finding supports the risk mitigation view rooted in stakeholder theory, which posits that investing in sustainability practices enables firms to develop moral capital and goodwill, providing insurance-like protection for the firm (Godfrey et al., 2009). More importantly, the current study contributes to the body of research by demonstrating that the effect of ESG on reducing bankruptcy risk varies across industries, even within the service sector, which encourages the consideration of industry characteristics in investigating the impact of ESG initiatives. Unlike other services that revolve around tangible products, the HT service centers on intangible experiential offerings, making innovation a critical driver for business success (Peng et al., 2024). However, the HT sector’s typically thin profit margins make it difficult for firms to absorb the associated costs, potentially limiting the effectiveness of ESG initiatives.

In terms of bankruptcy risk reduction, HT firms benefit from ESG performance to a lesser extent after the Covid-19 outbreak, which is consistent with prior research findings on the negative effect of the Covid-19 pandemic on firm performance. In addition, this study fills a gap in the literature by addressing corporate governance measures as potential moderators of the ESG performance and bankruptcy risk nexus. The current research provides the first empirical evidence that CEO duality weakens the connection between ESG performance and lower bankruptcy risk across industries in general and has a non-significant moderating effect within the service industry. This finding contrasts with prior research, which found that CEO duality enhances the effect of CSR performance on tourism industry development (Uyar et al., 2022). Contrary to existing research findings (Alodat and Hao, 2024; Savio et al., 2023), this study finds that board gender diversity has a negative influence on the relationship between ESG performance and firm bankruptcy risk.

Practical implications

The current research provides important implications for hospitality managers and investors. From the investors’ perspective, strong ESG performance signals financial health, positioning high-performing firms as relatively safer investment options. From a human resources perspective, fostering a company culture that values ESG practices is essential. From a managerial perspective, ESG initiatives can protect companies against financial distress; however, the magnitude of this positive influence depends on the overall economic condition and industry characteristics. While hospitality managers can mitigate bankruptcy risks by implementing ESG programs, they must carefully weigh the costs against the benefits during economic downturns. As evidenced by this research, in financial crises resulting from events that significantly impact operating revenues, such as the Covid-19 pandemic, managers must assess how ESG costs may affect profitability. This argument aligns with the trade-off theory, which suggests that firms must use their resources for core business activities. Facing declining operating revenues, business managers could be better off initiating ESG projects that benefit their operational performance to offset associated costs.

Regarding corporate governance mechanisms, HT firms can enhance the effectiveness of ESG initiatives in reducing bankruptcy risk by having a greater proportion of individual investors. Another strategy for HT managers to mitigate the negative influence of institutional ownership is to document cost-benefit analyses of ESG projects and prioritize investments that align with core business activities, thereby garnering greater support from institutional investors. Given that larger boards may diminish the effectiveness of ESG performance, shareholders may favor the formation of more modestly sized boards. Companies should avoid board oversizing and consider appointing directors with expertise in sustainability to enhance ESG oversight.

Limitations and future research

The limitations of this research suggest the direction for future studies. First, as the analysis focuses exclusively on publicly traded U.S. firms, caution should be exercised when generalizing the findings to other markets. Cross-country comparisons are encouraged to explore the impact of ESG performance across diverse business environments. Second, the only crisis period examined in this study is the Covid-19 pandemic. Future research could investigate other health or financial crises using alternative ESG metrics and contribute to the evidence on how different types of crises may influence the ESG-bankruptcy risk relationship. Lastly, future studies may explore the moderating effects of other corporate governance attributes to provide additional insights.

Supplemental Material

Supplemental material - ESG performance and bankruptcy risk in the hospitality and tourism industry: Moderating role of the Covid-19 pandemic and corporate governance attributes

Supplemental material for ESG performance and bankruptcy risk in the hospitality and tourism industry: Moderating role of the Covid-19 pandemic and corporate governance attributes by Wenjia Han, Ozgur Ozdemir and Ezgi Erkmen in Tourism Economics

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data used in the current research is available upon reasonable request.

Declaration of generative AI in scientific writing

The authors report that AI and AI-assisted technologies were not used in this paper.

Supplemental Material

Supplemental material is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.