Abstract

This study investigates how women’s inclusion in leadership positions affects financial risk in China’s hotel industry, integrating gender role theory with agency theory. Test results of dynamic panel regressions with the two-step SYS-GMM estimation reveal three key insights, providing empirical evidence that strategic gender diversity in leadership can serve as a financial risk management tool. First, both women’s inclusion in executive (EWI) and board (BWI) positions significantly reduce firm-specific risk but have no impact on market-wide risk. Second, the study identifies a U-shaped relationship, with firm-specific risk minimized at optimal inclusion levels of 29.21% (EWI) and 24.20% (BWI). Third, the risk-mitigating effect of EWI and BWI is asymmetric, specifically stronger during economic expansions than recessions, reflecting the hospitality sector’s cyclical nature. The study contributes theoretical value by bridging theories with financial risk analysis in hospitality contexts and offers practical guidance for hotel firms in optimizing leadership structures.

Keywords

Introduction

In recent decades, the importance of gender diversity in leadership has gained significant recognition within the hotel industry (Chen et al., 2021). This is particularly relevant given the sector’s high proportion of female employees and service-oriented character. Despite this, women remain markedly underrepresented in senior roles, especially in China. According to the China Stock Market and Accounting Research (CSMAR) database, only 18.2% of executive positions and 9.7% of board directorships in Chinese hotels are held by women. This imbalance is striking considering that women account for nearly 60% of the hospitality workforce in China, yet face structural barriers to career progression. Industry reports further indicate that China hotel market is undergoing rapid transformation, with heightened demand for international-standard governance, sustainability practices, and digitalized operations (China Hospitality Association, 2023). Such disparities highlight the urgency of addressing gender imbalance not only to advance equity but also to promote sustainable development in line with Sustainable Development Goal 5 (gender equality) and Sustainable Development Goal 8 (decent work and economic growth).

Within this context, advancing gender diversity by increasing women’s representation in leadership is increasingly viewed as a strategic imperative. The hospitality sector has indeed witnessed a notable rise in women occupying senior roles in recent years (Chen et al., 2021). These leaders provide valuable insight into the experiences of front-line female employees and act as role models, fostering greater motivation and engagement across the workforce. Appointing more women to executive and board positions enhances a hotel company’s capacity to respond to evolving guest expectations and strengthens organizational cohesion. This contribution is particularly evident in key areas of competitive differentiation such as sustainability, wellness, and digital transformation. In China, for instance, where domestic tourism recovered to 90% of pre-pandemic levels by 2023 amid aggressive expansion by luxury hotel chains, female leaders have been instrumental in shaping service innovation and customer engagement strategies (China Hospitality Association, 2024). These industry observations are supported by empirical research linking female leadership to superior organizational outcomes, including higher profitability, greater market share, and improved governance (Chen et al., 2021; Jensen and Meckling, 1976; Kang and Lee, 2014; Menicucci et al., 2019; Song et al., 2020; Zhu et al., 2025).

The benefits of gender-diverse leadership in the hotel industry are well-documented. Research demonstrates that increased female representation at executive and board levels correlates with enhanced profitability and market share (Chen et al., 2021; Song et al., 2020). These outcomes stem from several factors, including female directors’ ability to foster organizational cohesion and improve corporate governance (Kang and Lee, 2014; Zhu et al., 2025). Furthermore, greater female participation on corporate boards can help mitigate agency problems (Jensen and Meckling, 1976) and has been associated with broader organizational benefits, including increased sales and employment growth (Menicucci et al., 2019).

Despite growing recognition of gender diversity’s importance in corporate governance, research has yet to systematically investigate its impact on risk management within the hospitality sector. The existing literature has predominantly focused on the general relationship between gender diversity and firm performance, largely overlooking risk as a critical dimension of organizational sustainability. Furthermore, while studies have established a link between female representation and profitability, the specific mechanisms through which female leadership influences financial risk management remain poorly understood. This gap is particularly salient in service-intensive industries like hospitality, where inherent exposure to external market fluctuations makes risk management paramount. Consequently, there is a pressing need for a comprehensive framework to elucidate the role of women in mitigating financial risk within hotel organizations.

The hotel industry faces substantial financial and operational risks due to its capital-intensive nature (Chen, 2010), with heavy investments in fixed assets increasing exposure to financial risk. As a labor-intensive sector, it also grapples with chronic challenges like high employee turnover, which compound operational risks. Studies indicate that the hospitality industry experiences higher levels of unsystematic (firm-specific) risk compared to many other sectors, making it a volatile environment for investors (Chen, 2013). Against this backdrop, the composition of corporate boards, especially the degree of women’s inclusion, plays a critical role in shaping financial decision-making related to risk-return tradeoffs.

Research suggests that diverse boards approach investment opportunities with a broader set of perspectives, leading to more balanced risk evaluations (Adams and Ferreira, 2009). Women presence on boards has been linked to stronger monitoring and more prudent financial strategies, which can mitigate excessive risk-taking while still enabling growth. Existing studies indicate that women often adopt more cautious, risk-averse decision-making approaches (Brooks et al., 2019; Eagly, 1987). Beyond individual decision-making styles, female leadership has been associated with cultivating positive corporate cultures, improving work environments, and enhancing employee satisfaction (Chen et al., 2021). These qualities contribute to lower turnover rates and reduced operational risk, while women’s vigilance in monitoring strengthens governance and enhances financial resilience.

To address the research gap, this study develops a novel theoretical framework grounded in gender role theory to investigate how female leadership shapes financial risk mitigation. Gender role theory emphasizes that behavior and decision-making are socially constructed and shaped by gendered expectations (Eagly, 1987). For instance, women tend to emphasize autonomy and self-fulfillment, while men often prioritize status and external rewards (Bernardi and Arnold, 1997). Women are also generally more risk-averse, with fear serving as a deterrent to high-risk decisions (Lerner et al., 2003). By integrating these behavioral tendencies with organizational perspectives, this study provides deeper insights into how gender dynamics influence risk management in hotels.

Moreover, existing literature has largely overlooked the potential for nonlinear relationships between women’s representation in leadership and firm outcomes. While gender role theory posits that greater diversity correlates with reduced firm risk, suggesting women may prioritize shareholder interests (Jensen, 1993), an excessive diversity of viewpoints could also introduce a wider range of strategic preferences, some of which may be riskier (Poletti-Hughes and Briano-Turrent, 2019). Building on established evidence of threshold effects linking female representation to profitability in the hotel sector (Chen et al., 2021), this study investigates whether analogous thresholds exist for financial risk. This inquiry addresses a significant and previously underexplored gap in the research.

Furthermore, the cyclical nature of the hotel industry exposes firms to varying levels of financial risk across business cycles. Previous studies have acknowledged heightened risks during recessions (He and Leippold, 2020), but few have examined how gender dynamics intersect with these fluctuations. Given that women may adopt more pessimistic outlooks during high-risk conditions (Lerner et al., 2003), their inclusion may have asymmetric effects depending on the macroeconomic context. This study addresses this neglected dimension by analyzing how women’s representation influences hotel financial risks during both expansionary and contractionary periods.

Finally, while financial risks are often treated as a single construct, little attention has been given to the distinction between market-wide and firm-specific risks in the hospitality sector. Drawing on the Capital Asset Pricing Model (CAPM; Sharpe, 1963), this study separates these two risk categories to examine how women’s inclusion affects each. This dual approach moves beyond conventional performance metrics, offering a more granular understanding of how gender diversity contributes to organizational resilience in the hotel industry.

The remainder of this paper is organized as follows: Literature review represents relevant literature and develops research hypotheses. Data and Variables describe the data sources and variable definitions. Methodology and empirical results include the methodology and empirical results. Discussion and implications analyze key findings and their implications. Section 6 addresses study limitations and suggests directions for future research.

Literature review

Hotel financial risks

Financial risk in the hotel industry is typically categorized into two distinct types: market-wide (systematic) risk and firm-specific (unsystematic) risk (Chen et al., 2022). Market-wide financial risk, which affects all firms in the market, is a critical determinant of firm valuation and the cost of equity capital. As Copeland et al. (2005) demonstrate, heightened market-wide risk increases the cost of equity, thereby depressing firm value. This type of risk, driven by systematic factors like inflation and business cycle fluctuations (Chen et al., 2022), cannot be eliminated through diversification (Bodie et al., 2024). In the Chinese context, firm-specific characteristics such as debt leverage, company size, and state ownership have also been shown to influence a hotel’s exposure to this systematic risk (Chen, 2013).

In contrast, firm-specific financial risk pertains to uncertainties unique to an individual company, such as management changes or supply chain disruptions (Chen et al., 2022). This component of total risk is independent of general market movements and can be mitigated through a diversified investment portfolio (Bodie et al., 2024). Empirical evidence suggests that larger hotel firms generally exhibit lower levels of firm-specific risk (Chen, 2013), and that corporate philanthropy can also serve as a mitigating factor (Chen et al., 2022). While these studies provide a foundational understanding of financial risk determinants, a significant gap remains: the influence of gender diversity in leadership on firm-specific financial risk within hotel companies is largely unexplored.

Inclusion of women mitigates hotel financial risks

Gender role theory provides a valuable framework for understanding how women’s inclusion in leadership positions may influence financial risk management in the hotel industry. According to this theory, individuals’ behaviors and emotional responses are shaped by societal and cultural expectations based on gender (Eagly, 1987). The theory suggests that women tend to prioritize self-fulfillment and independence in their professional careers, while men are more likely to focus on achieving higher status and external rewards (Bernardi and Arnold, 1997). Building on Maslow’s hierarchy of needs (1943), research indicates that female managers often reach higher levels of self-actualization compared to their male counterparts.

Furthermore, studies have demonstrated that women in management positions typically exhibit higher levels of ethical development (Bernardi and Arnold, 1997). This heightened ethical sensitivity enables female managers to more readily identify unethical behaviors and maintain stricter moral standards in business practices. As a result, the presence of women in leadership roles has been associated with reduced unethical practices and better risk management in internal auditing and corporate governance (Larkin, 2000).

When examining decision-making patterns, research shows that female executives tend to be more cautious and deliberate than male executives when addressing ethical issues such as financial disclosure and corporate integrity (Doan and Iskandar-Datta, 2020). In high-pressure situations, psychological studies reveal that men are more likely to experience anger, which may drive them toward high-risk, aggressive decisions. In contrast, women are more inclined to feel fear in such circumstances, which typically serves as a deterrent against excessive risk-taking due to concerns about potential negative outcomes (Lerner et al., 2003). Empirical studies using U.S. data have consistently found that women adopt more cautious, risk-averse approaches to financial decision-making compared to men (Jianakoplos and Bernasek, 1998). While men may perform better in highly competitive, high-risk business environments, women generally display less overconfidence and prefer more conservative strategies (Lamiraud and Vranceanu, 2018).

The risk-mitigating effects of female leadership have been documented across various industries and geographical contexts. Perryman et al. (2016) found that female executives in non-financial Fortune 500 companies contributed to lower overall corporate risks. Similarly, Palvia et al. (2020) demonstrated that women in executive positions significantly reduced default risks in U.S. commercial banks. Studies of UK-listed companies by Nadeem et al. (2019) revealed that female board representation was associated with reductions in all three major risk categories: market-wide financial risk, firm-specific financial risk, and total risk. Parallel findings have emerged from research on Chinese (Khaw et al., 2016), Norwegian (Yang et al., 2019), and Vietnamese (Hoang et al., 2019) companies, suggesting that the risk-reducing effect of gender diversity in leadership may be a universal phenomenon.

This study extends previous research by examining how women’s inclusion affects both market-wide and firm-specific financial risks in the hotel industry. Market-wide risk encompasses macroeconomic factors such as inflation and general business uncertainties that affect all market participants (Chen et al., 2022). These systemic risks are beyond the control of individual firms and cannot be mitigated through internal management strategies, including changes in leadership composition. In contrast, firm-specific risk relates to internal company factors and events that affect individual firms or small groups of companies, such as the gender composition of executive teams (Chen et al., 2022). Unlike market-wide risk, firm-specific risk can potentially be reduced through appropriate diversification strategies and management approaches. Therefore, we expect that increasing women’s representation in executive and board positions will primarily influence firm-specific risk rather than market-wide risk.

Based on this theoretical framework and empirical evidence, we propose the following hypotheses: Hypothesis 1a: The inclusion of women in top management positions reduces firm-specific financial risks in China’s hotel industry. Hypothesis 1b: The inclusion of women in top management positions does not affect market-wide financial risks in China’s hotel industry.

Nonlinear effect of women inclusion on hotel financial risks

The relationship between women’s inclusion in leadership and hotel financial risks is not necessarily linear. Gender role theory suggests that the risk-mitigating effects of female executives may be most pronounced in hotels with initially low levels of gender diversity in management. When female representation is limited - operationally defined as having at least one woman in executive positions - women tend to assume primarily monitoring roles within the management team (Adams and Ferreira, 2009). Critical mass theory (Kanter, 1977) explains that when the number of female executives falls below a certain threshold, women face significant challenges in influencing business strategy and decision-making processes. In such situations, limited representation confines women’s roles to oversight functions rather than active participation in strategic decision-making. Gender role theory suggests that women’s natural risk aversion and higher ethical standards lead them to exercise strict oversight to protect shareholder interests (Eagly, 1987). Consequently, in the early stages of increasing gender diversity, the presence of women in leadership positions is expected to contribute to reduced financial risks.

However, when women’s representation exceeds a critical threshold, agency theory predicts that female executives may begin to engage in greater risk-taking behavior (Poletti-Hughes and Briano-Turrent, 2019). Specifically, as women surpass this threshold, they gain more substantial influence and autonomy in decision-making processes, with less constraint from male colleagues (Kogut et al., 2014). As women break through the “glass ceiling” and achieve more significant leadership roles, they may feel increased pressure to match or exceed the competitiveness and assertiveness of their male peers (Adams and Funk, 2012). Agency theory suggests that female executives, in their pursuit of maximizing shareholder value, may become more willing to undertake calculated risks to capitalize on profitable opportunities (Poletti-Hughes and Briano-Turrent, 2019). Therefore, as women’s representation grows beyond the critical threshold, their influence on hotel risk profiles may shift, potentially leading to increased risk-taking.

Compared to firms with all-male executive teams, gender-diverse leadership introduces a wider range of personal experiences and professional resources, which expands the spectrum of available strategies and investment opportunities (Poletti-Hughes and Briano-Turrent, 2019). This diversity may ultimately increase a firm’s risk exposure by encouraging the pursuit of more ambitious projects designed to enhance overall performance (Ward and Forker, 2017). Additionally, Poletti-Hughes and Briano-Turrent (2019) argue that greater gender diversity in top management improves decision-making quality. Female executives tend to closely monitor managerial behavior to protect shareholder interests, which can improve the success rate of strategic initiatives undertaken by gender-diverse leadership teams (Chen et al., 2017).

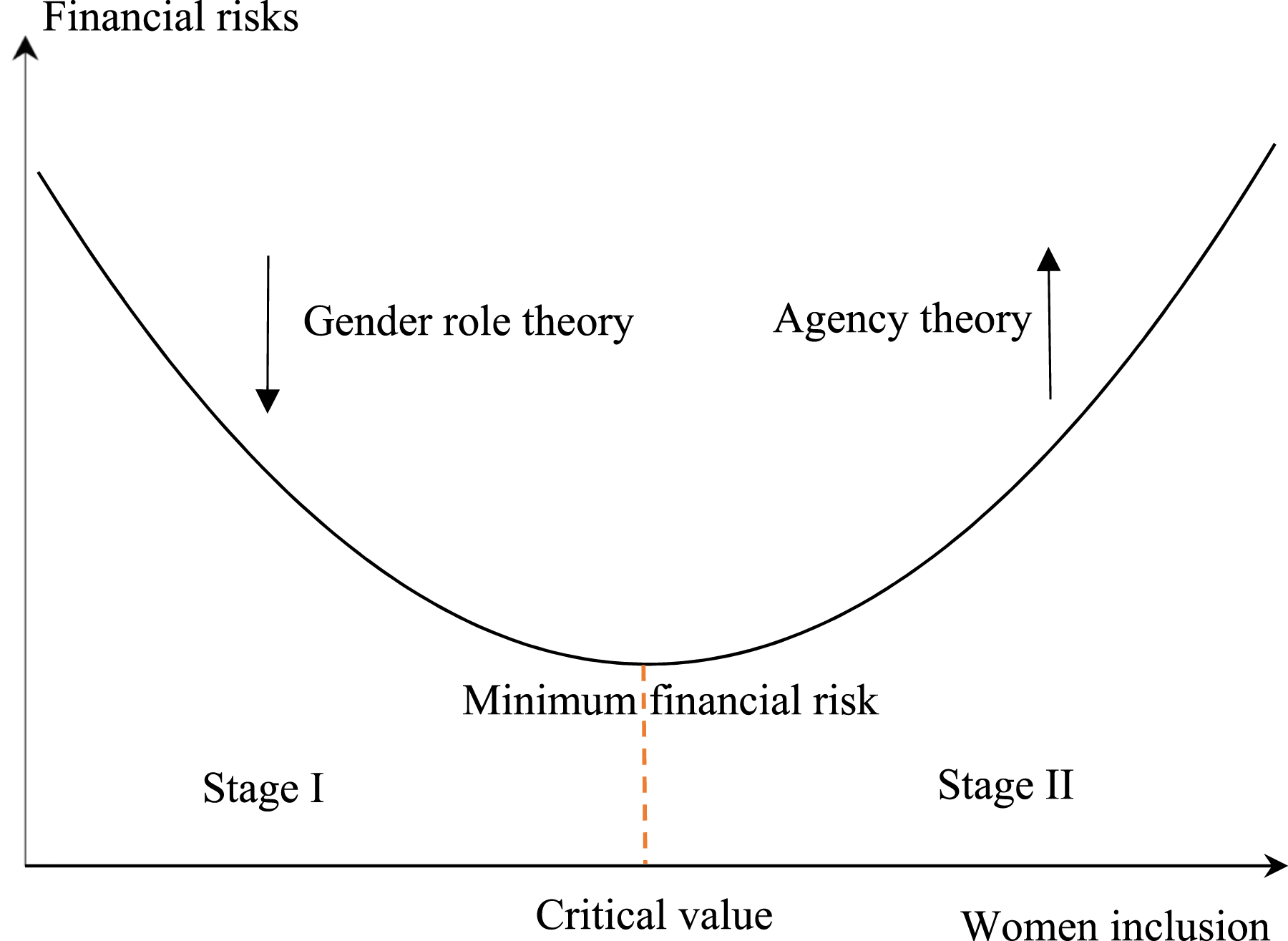

By integrating insights from both gender role theory and agency theory, this study makes an important contribution to the hotel literature by examining the nonlinear relationship between women’s inclusion and financial risks. We propose that the effect of women’s inclusion on hotel financial risks varies depending on the level of representation, following a U-shaped pattern. As is shown in Figure 1, there exists a critical threshold where increasing women’s representation below this point reduces hotel financial risk (consistent with gender role theory), while exceeding this threshold leads to increased financial risk (consistent with agency theory). Based on this theoretical framework, we propose the following hypothesis: Hypothesis 2: The relationship between women’s inclusion in top management and firm-specific financial risks in China’s hotel industry follows a U-shaped pattern, with risk levels initially decreasing but eventually increasing as women’s representation grows beyond a critical threshold.

Asymmetric effect of women inclusion on hotel financial risks

This study further contributes to the literature by investigating whether the impact of women’s inclusion in top management on firm-specific financial risks varies across different phases of the business cycle, particularly during economic expansions versus recessions. As Bodie et al. (2024) emphasize, the hotel industry is highly cyclical and particularly sensitive to macroeconomic fluctuations. Moreover, hotel companies typically have relatively small market capitalizations and require substantial capital investments to maintain operations, making them heavily dependent on bank financing (Chen, 2013). During economic downturns, credit conditions tighten significantly, especially for less creditworthy hotel firms, leading to greater earnings volatility across the industry (Chen et al., 2022). Consequently, the hotel sector tends to experience elevated risk levels during recessionary periods (He and Leippold, 2020).

However, female executives may face particular challenges in managing the extreme risks that emerge during economic contractions. Gender role theory suggests that in highly competitive, high-risk environments, men typically demonstrate greater competitiveness and confidence than women (Lamiraud and Vranceanu, 2018). Lerner et al. (2003) found that women tend to adopt more pessimistic outlooks than men when confronting risky situations. During recessionary periods, when risks are substantially elevated, women may experience heightened fear responses that could undermine their confidence in effectively managing these risks (Lerner et al., 2003). As a result, female executives may have reduced capacity to influence hotel financial risk management during economic downturns, or may derive fewer benefits from their risk management strategies in such conditions.

Conversely, during economic expansions, the hotel industry generally operates in a more favorable environment characterized by greater financial stability and sustainable operational conditions, resulting in more manageable risk levels (Chen, 2013, 2015; Kim et al., 2005). In these periods, hotel companies encounter a broader range of growth opportunities across different quality segments, along with their associated risks. This environment provides executives with greater flexibility in decision-making and may create opportunities to pursue more ambitious projects. Gender role theory suggests that women in top management positions tend to favor less risky corporate strategies, often emphasizing careful operational monitoring due to their higher ethical standards and commitment to protecting shareholder interests (Doan and Iskandar-Datta, 2020). Consequently, female executives are likely to have a more substantial impact on hotel risk management during periods of economic expansion.

Previous research on the hotel industry has documented differential performance across business cycles, revealing asymmetric effects depending on economic conditions (Yang et al., 2020). Specifically, during expansionary periods, increases in tourist arrivals significantly drive hotel industry growth, but this relationship weakens considerably during recessions, underscoring the importance of business cycle analysis in hotel management research (Yang et al., 2020). Building on these findings, we predict that women’s inclusion in top management will have an asymmetric impact on firm-specific financial risks, with a stronger effect during economic expansions than during recessions. This leads to our final hypothesis: Hypothesis 3: The effect of women’s inclusion in top management on firm-specific financial risks in China’s hotel industry varies across the business cycle.

Data and variables

This study analyzes a sample of 14 publicly traded Chinese hotel companies using the same dataset as Chen et al. (2021). While their research focused on general performance metrics, our study specifically investigates how women’s inclusion affects financial risk in the hotel sector. The analysis covers the period from 1999 to 2021, utilizing unbalanced panel data that yields 254 annual observations. All data were sourced from the reliable China Stock Market and Accounting Research (CSMAR) database, ensuring the robustness of our empirical analysis.

Dependent variables

This study measures financial risk using the single-index model developed by Sharpe (1963), which builds upon the Capital Asset Pricing Model (CAPM). The model distinguishes between two types of financial risk that affect hotel company stocks. Market-wide financial risk represents the systematic risk that cannot be diversified away, measured by a stock’s beta coefficient. This reflects how sensitive a hotel company’s stock is to overall market movements. Firm-specific financial risk captures the idiosyncratic risk unique to each company, measured by the variance of error terms in the regression model. This component reflects risks stemming from company-specific factors that investors could potentially mitigate through diversification.

The single-index model is specified by the following equation:

In this equation, HRi,t represents the daily stock return of hotel firm i on day t and is calculated as

Market-wide financial risk is estimated using the beta coefficient (β), allowing hotel firms to assess their exposure to systematic market fluctuations. Firm-specific financial risk, derived from the variance of the regression error term (σ 2 (ε)), captures idiosyncratic risks independent of broader market movements. Specifically, hotel firms use firm-specific risk to evaluate the potential impact of unexpected events.

We first calculate daily returns for each hotel company and the overall market index and estimate equation (1) for each firm-year combination to obtain the beta coefficient and error variance. These annual risk measures enable us to analyze how women’s inclusion in leadership affects different dimensions of financial risk in the hotel industry.

Independent variables

This study investigates two primary measures of women’s inclusion in leadership positions and their impact on financial risk in the hotel industry. Executive Women Inclusion (EWI) represents the proportion of female executives across all senior management roles, including board directors, CEO, CFO, CHRO, CMO, general managers, secretaries, and supervisors. Board Women Inclusion (BWI) specifically measures the percentage of women serving as board directors. This distinction allows us to examine whether different levels of female representation in organizational hierarchies have varying effects on financial risk outcomes.

The measurement of these variables follows the methodology established by Ye et al. (2019), employing a straightforward ratio calculation:

These measures capture the relative representation of women in decision-making positions, acknowledging prior research findings that suggest women in leadership roles may exhibit different risk preferences and management approaches compared to their male counterparts (Adams and Funk, 2012; Farag and Mallin, 2017). The binary gender classification ensures clear operationalization while recognizing the potential complexity of gender dynamics in organizational settings.

Control variables

To isolate the effect of women’s inclusion on financial risk, we incorporate several well-established control variables from the finance literature, including return on assets (ROA), financial leverage (LEV), firm size (FS), firm age (FA), and the percentage of state ownership (SOP). ROA is calculated as net income divided by total assets, this profitability metric may influence risk through two potential mechanisms. Effective management leading to higher ROA could correlate with lower risk (Borde, 1998), while aggressive strategies generating higher returns might simultaneously increase risk exposure.

LEV is measured as total debt to total assets ratio, leverage consistently demonstrates a positive relationship with firm risk in empirical studies (Faccio et al., 2011). Higher debt levels typically amplify both potential returns and risk exposure. FS, the natural logarithm of total assets, is used to account for size effects. Larger firms often benefit from economies of scale and more stable cash flows, potentially reducing their risk profile (Boubakri et al., 2013).

FA, calculated as the natural logarithm of years since stock exchange listing, captures organizational maturity. Established firms may develop more conservative risk management practices compared to younger, potentially more aggressive competitors (Poletti-Hughes and Briano-Turrent, 2019). SOP, measured as the proportion of state-owned shares, significantly influences corporate risk-taking behavior. Firms with greater state ownership tend to adopt more conservative strategies, reflecting both risk aversion and political considerations (Boubakri et al., 2013; Khaw, 2016).

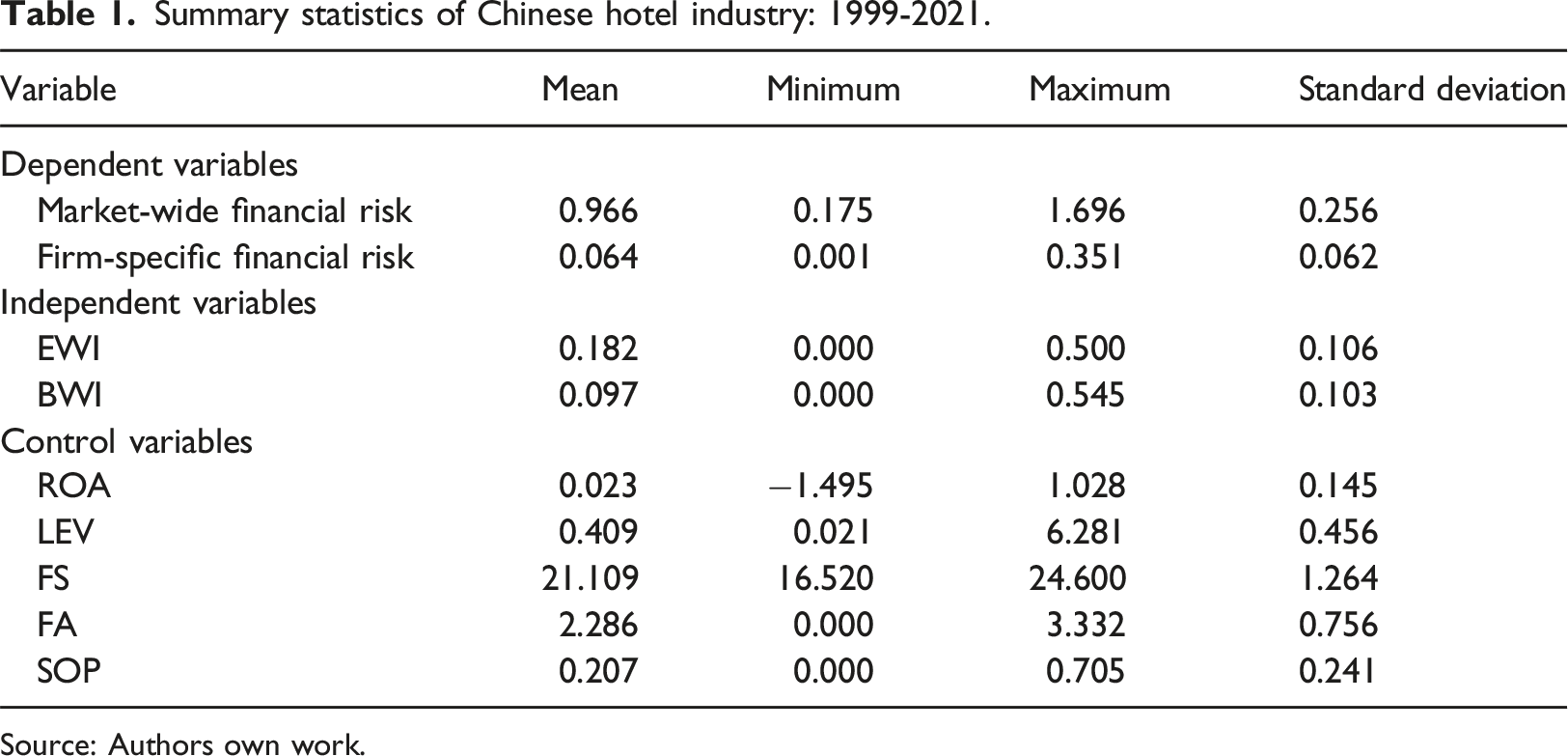

Descriptive statistics

Summary statistics of Chinese hotel industry: 1999-2021.

Source: Authors own work.

The women’s inclusion metrics reveal important industry characteristics. Both EWI and BWI include zero values, indicating periods of complete male dominance in some hotel leadership teams. On average, women occupy 18.2% of executive positions (approximately one in five executives) and just 9.7% of board director seats (roughly one in 10 directors). This gender imbalance highlights significant room for improved female representation in Chinese hotel leadership.

Financial controls show expected variation: ROA averages 0.023 (SD = 0.145), leverage stands at 0.409 (SD = 0.456) with extreme values from 0.021 to 6.281, and state ownership ranges from fully private (0%) to majority state-controlled (70.5%). These ranges ensure our analysis captures diverse organizational contexts within the Chinese hotel industry.

Methodology and empirical results

Models

This study examines the relationship between women’s inclusion in leadership positions and financial risk through three regression models. The baseline linear model (equation (3)) tests the direct effects of women inclusion on financial risk:

In this specification, the dependent variable Risk represents either market-wide financial risk (systematic risk) or firm-specific financial risk (idiosyncratic risk). The key independent variable WI measures women’s inclusion, analyzed separately for executive (EWI) and board (BWI) positions. The model includes several control variables: return on assets (ROA), leverage ratio (LEV), firm size (FS), fixed assets ratio (FA), shareholder ownership percentage (SOP), and the 1-year lag of the dependent variable to account for risk persistence. This specification tests Hypothesis one regarding whether women’s inclusion linearly affects financial risk. Statistical significance of α1 (p < 0.10) would support this hypothesis, with the sign indicating the direction of the relationship.

To investigate potential nonlinear relationships, equation (4) introduces a quadratic term for women’s inclusion:

This specification allows for testing U-shaped or inverted U-shaped relationships. A U-shaped relationship as suggested by two theoretical perspectives (gender role theory vs agency theory) would be evidenced by a negative α1 (initial decrease in risk) and positive α2 (subsequent increase in risk at higher inclusion levels).

Finally, to examine whether the effects of women’s inclusion vary across different phases of the business cycle, we estimate an augmented regression model that interacts our measure of women’s inclusion with a business cycle dummy (BC). The model specification takes the following form:

In this specification, BC represents a business cycle dummy variable that takes the value of one during economic expansion periods and 0 during recessions. The classification of the business cycle is based on data from the Federal Reserve Economic Data (2022). The interaction terms WI × BC and WI × (1-BC) are included to capture the differential impact of women’s inclusion during expansionary and recessionary periods, respectively. This specification retains all control variables from our baseline model.

The model enables us to conduct several important tests of our hypotheses. First, we can test whether women’s inclusion has a statistically significant effect during expansions by examining whether α1 differs significantly from zero. Similarly, we test the recessionary effect by evaluating whether α2 differs from zero. Most importantly, we formally test for asymmetric effects across business cycles by conducting a Wald test of the null hypothesis that α1 = α2. Rejection of this null would indicate that the impact of women’s inclusion on financial risk differs meaningfully between expansion and recession periods.

This empirical approach offers several advantages for our analysis. By interacting women’s inclusion with the business cycle dummy, we can precisely estimate differential effects while maintaining the full sample size and statistical power. The specification remains consistent with our system GMM estimation approach, continuing to account for potential endogeneity through appropriate instrumentation. Moreover, the inclusion of both interaction terms allows for clean interpretation of the marginal effects during each phase of the business cycle.

From an economic perspective, the model parameters have clear interpretations. A negative and statistically significant α1 would indicate that women’s inclusion reduces financial risk during economic expansions, while a significant α2 would show effects during recessions. If both coefficients are negative but α1 is larger in magnitude than α2, this would suggest that the risk-reducing effect of women’s inclusion is more pronounced during expansionary periods. Conversely, if α2 is larger, it would imply greater effectiveness during recessions. Any sign changes between the coefficients would indicate qualitatively different effects across business cycle conditions.

The model maintains all the robust statistical features of our baseline specification. We continue to include firm and year fixed effects to account for unobserved heterogeneity, and cluster standard errors at the firm level to address potential heteroskedasticity and autocorrelation. The system GMM implementation uses the same carefully constructed instrument set as our previous models, ensuring consistency across all results. This comprehensive approach allows us to draw reliable conclusions about how the relationship between women’s inclusion and financial risk varies with macroeconomic conditions.

GMM estimation

This study employs the two-step System Generalized Method of Moments (SYS-GMM) estimator developed by Blundell and Bond (1998) to address the econometric challenges of dynamic panel analysis. The model incorporates a 1-year lag of the risk variable to control for risk persistence, but this introduces endogeneity, as the lagged dependent variable is correlated with the error term. Conventional estimation methods, such as ordinary least squares (OLS) and fixed effects, produce inconsistent estimates in this context due to bias (Nickell, 1981; Sila et al., 2016). Furthermore, purely predictive models are designed for forecasting accuracy rather than causal inference. The SYS-GMM estimator overcomes these limitations by using internal instrumental variables derived from lagged levels and differences of the explanatory variables. This approach provides consistent and unbiased estimates, making it the most appropriate method for examining the causal effect of women’s inclusion on hotel risk.

SYS-GMM estimation integrates equations in first differences with equations in levels, using appropriate lags of the dependent and independent variables as instruments (Arellano and Bover, 1995; Blundell and Bond, 1998). Specifically, in the differenced equation, lagged levels of the variables serve as instruments, while in the level equation, lagged differences are employed. This dual instrumentation strategy improves efficiency relative to the standard difference GMM estimator, particularly in settings where variables display strong persistence over time (Blundell and Bond, 1998). To ensure the validity of our estimation, we implement several diagnostic tests. First, we apply the Hansen (1982) J-test to examine the overall validity of our instruments, where the null hypothesis of instrument exogeneity cannot be rejected (p > 0.10) in all specifications. Second, we conduct tests for autocorrelation in the differenced residuals, finding evidence of first-order autocorrelation (AR(1)) but no significant second-order autocorrelation (AR(2)), which is crucial for maintaining the consistency of our estimates (Blundell and Bond, 1998).

Moreover, given the moderate sample size of Chinese hotel firms in our dataset, we implement two important adjustments to prevent overfitting. Using the xtabond2 command in Stata, we: (1) collapse the instrument matrix to reduce the number of instruments, and (2) limit the lag depth of instruments following the recommendations of Roodman (2009). These measures ensure that our instrument count remains below the number of cross-sectional units, thereby maintaining the power of the Hansen test and avoiding the problem of instrument proliferation that can lead to biased estimates (Cabral et al., 2016).

Therefore, the SYS-GMM estimator proves particularly appropriate for our analysis given its superior performance in finite samples with persistent series (Blundell and Bond, 1998). Our implementation follows current best practices in dynamic panel estimation, including the use of orthogonal deviations to minimize data loss and the application of the (Windmeijer, 2005) correction for finite-sample bias in the two-step variance-covariance matrix. These methodological choices collectively ensure that our estimates are both consistent and efficient, providing a robust foundation for our empirical conclusions.

Empirical results

The empirical findings provide compelling evidence regarding the impact of women’s inclusion on financial risk in the hotel industry. Tables 2 through 4 present the results of our three model specifications, all of which demonstrate strong diagnostic statistics. The AR(2) tests (p > 0.10) indicate no second-order autocorrelation, and the Hansen tests (p > 0.10) confirm instrument validity. Furthermore, the significant coefficients on lagged risk variables (p < 0.01) validate our dynamic panel specification.

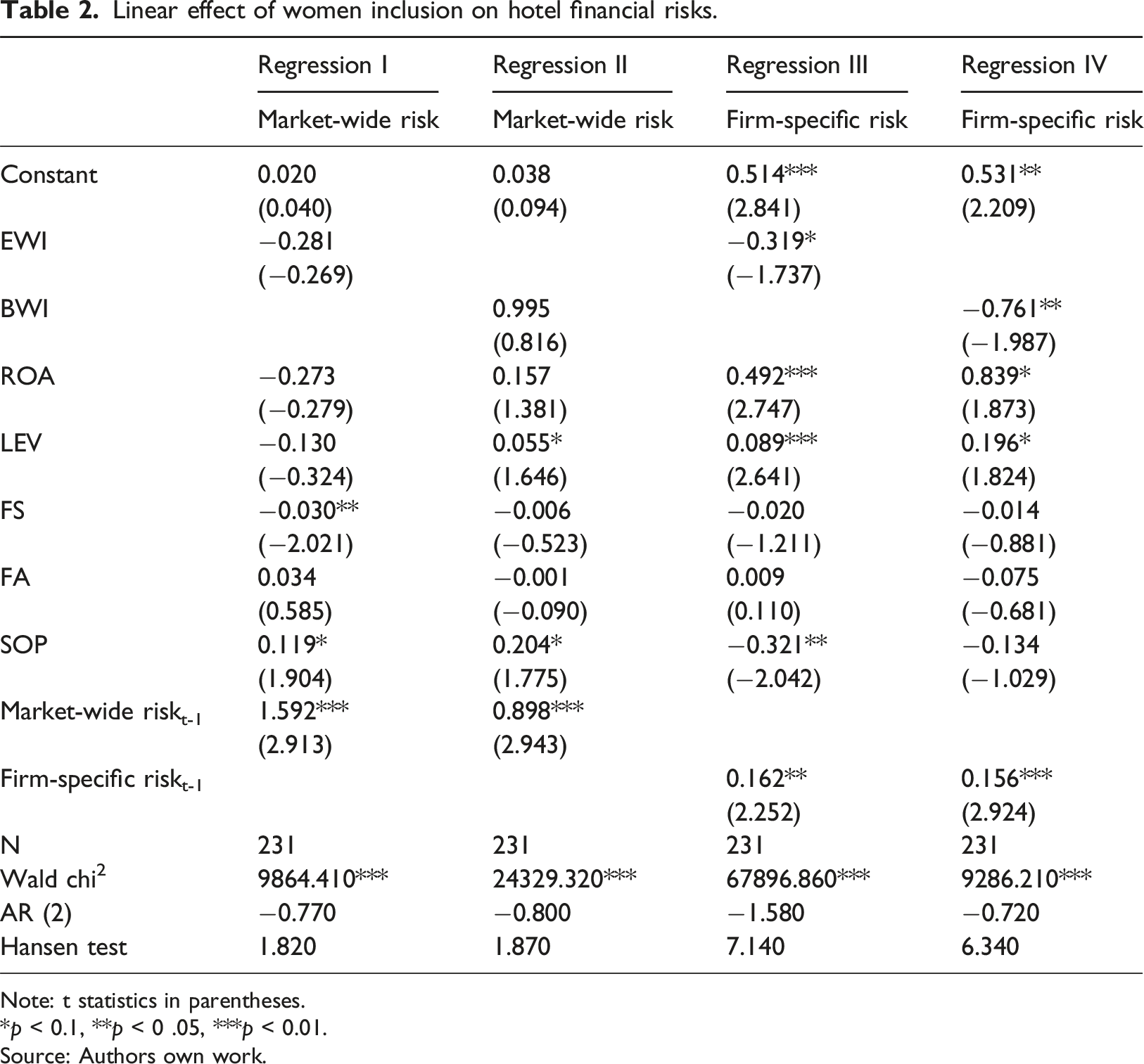

Linear effects of women’s inclusion

Linear effect of women inclusion on hotel financial risks.

Note: t statistics in parentheses.

*p < 0.1, **p < 0 .05, ***p < 0.01.

Source: Authors own work.

Conversely, for market-wide financial risk (Hypothesis 1b), neither executive nor board-level inclusion (EWI and BWI) shows statistically significant effects (p > 0.10) (see Regression I and Regression II). This null finding persists across all model specifications, robustly supporting Hypothesis 1b’s contention that gender diversity affects firm-specific but not systematic risk and aligning with theoretical expectations, as market-wide risks are driven by macroeconomic factors beyond managerial control, such as women inclusion in leadership.

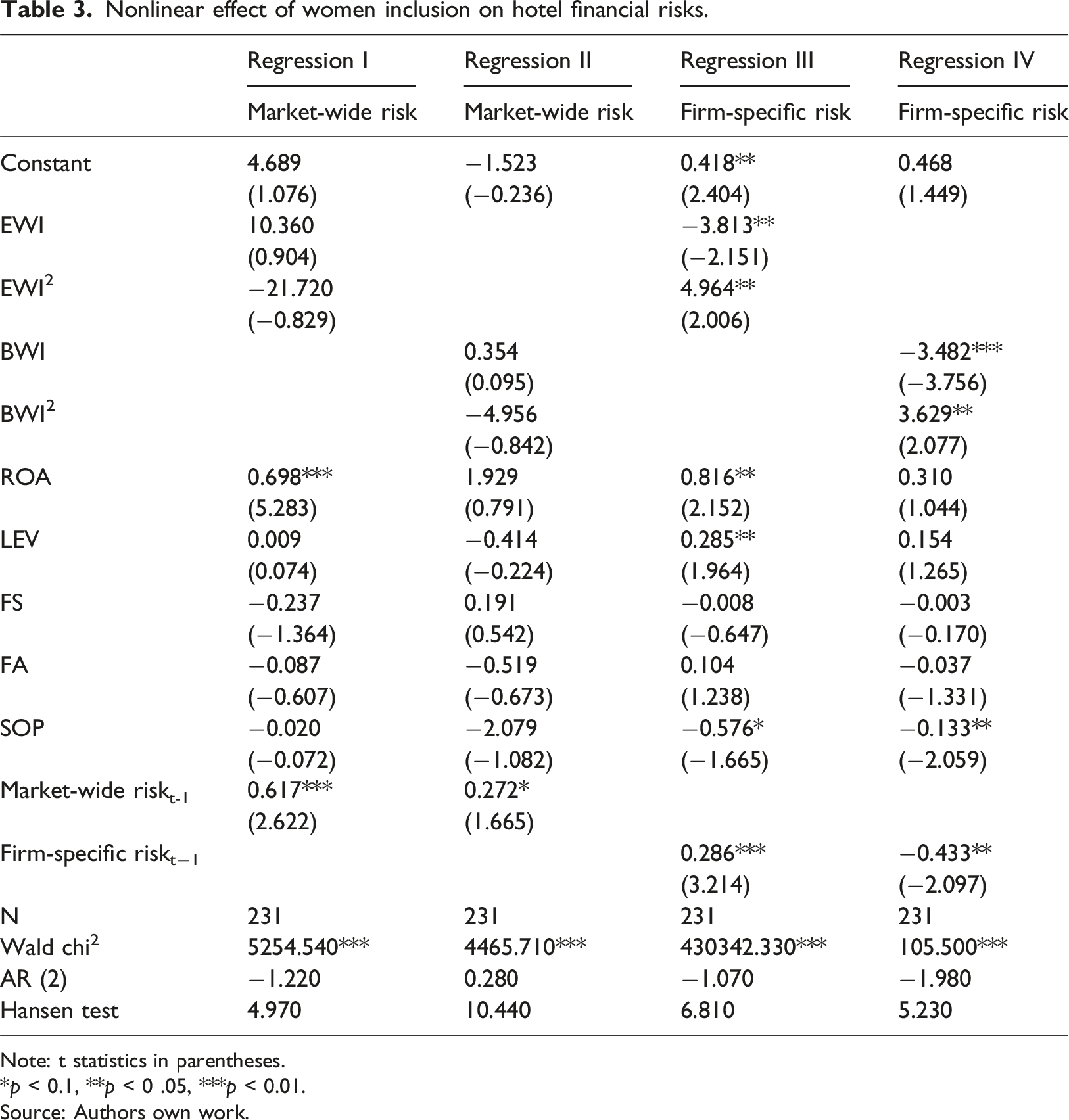

Nonlinear relationship analysis

Nonlinear effect of women inclusion on hotel financial risks.

Note: t statistics in parentheses.

*p < 0.1, **p < 0 .05, ***p < 0.01.

Source: Authors own work.

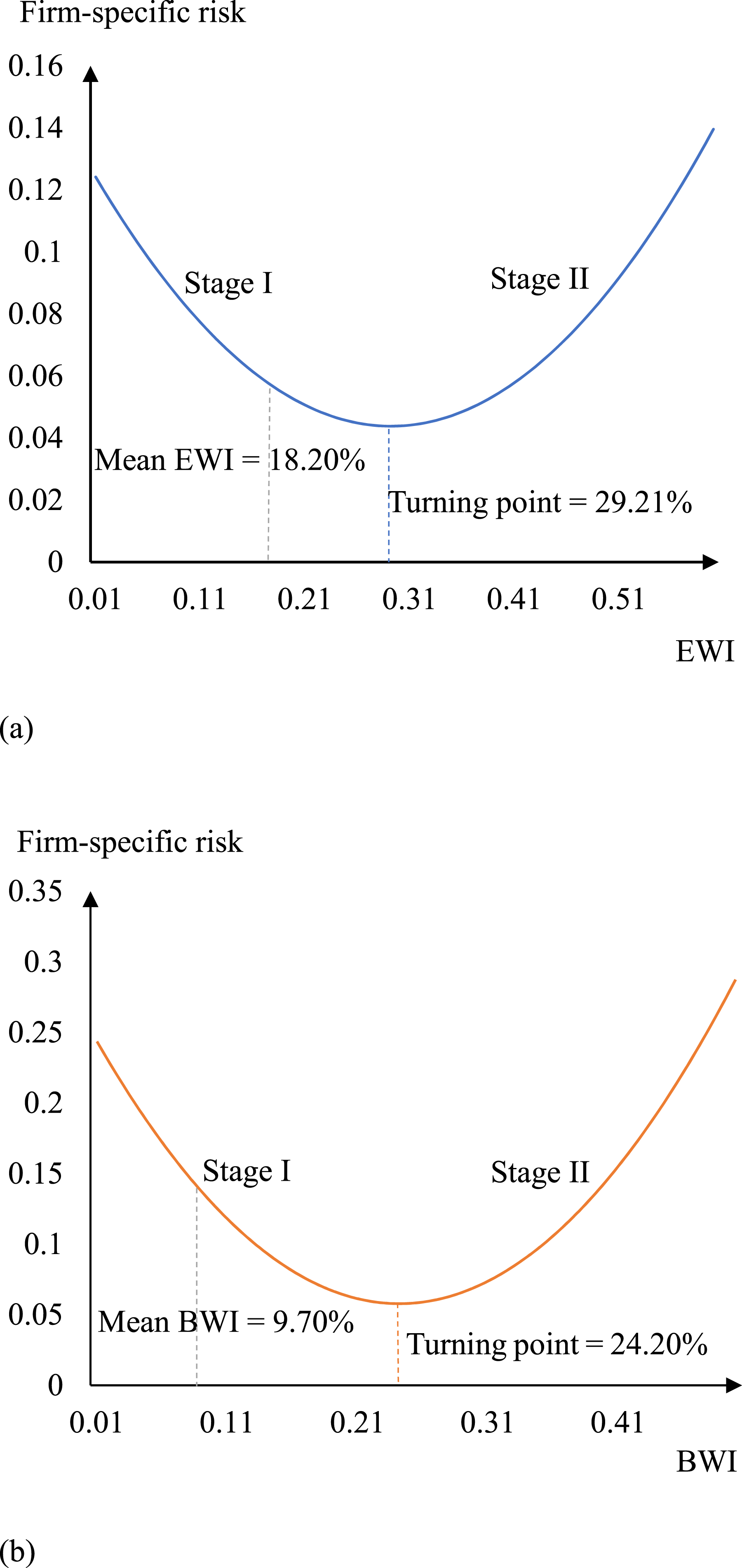

In contrast, firm-specific financial risk reveals a distinct pattern. Regression III shows that the coefficient for EWI is −3.813 (significant at the 5% level), while the squared term EWI2 is 4.964 (also significant at the 5% level). This indicates a U-shaped relationship between executive women inclusion and firm-specific financial risk: initially, greater female representation reduces risk, but beyond a certain threshold, further increases lead to higher risk. A similar trend emerges in Regression IV, where the coefficient for BWI is −3.482 (significant at the 1% level), and the squared term BWI2 is 3.629 (significant at the 5% level). These results imply that moderate levels of women inclusion in executive and board roles are associated with reduced firm-specific financial risk, whereas higher levels reverse this effect.

Thus, the findings provide strong empirical support for Hypothesis 2, confirming a U-shaped relationship between women’s inclusion in leadership and hotel firm-specific financial risk.

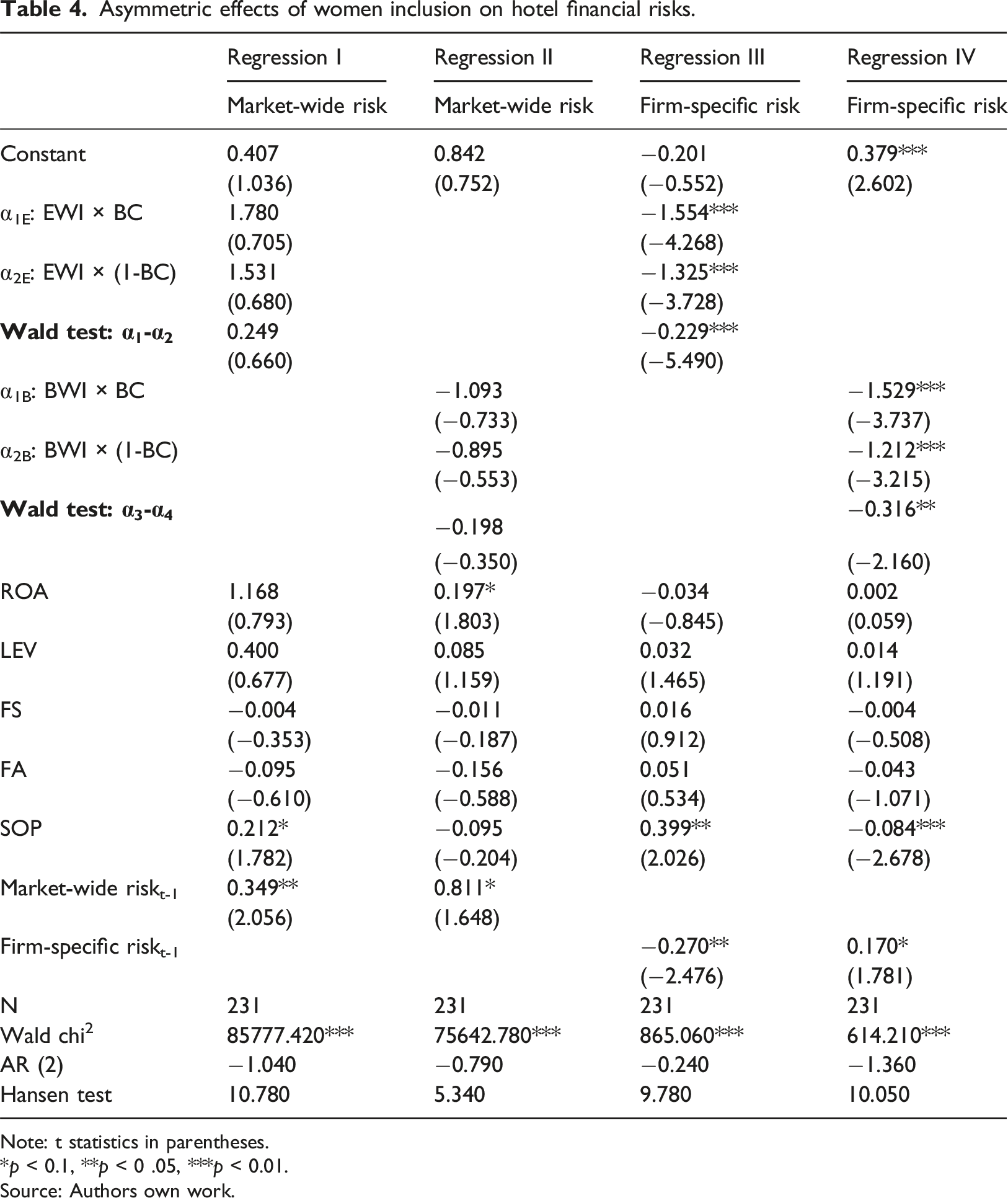

Business cycle asymmetries

Asymmetric effects of women inclusion on hotel financial risks.

Note: t statistics in parentheses.

*p < 0.1, **p < 0 .05, ***p < 0.01.

Source: Authors own work.

For market-wide financial risk, the results show no statistically significant effects from either executive women inclusion (EWI) or board women inclusion (BWI) during either economic expansion or recession periods. This finding suggests that gender diversity in leadership positions does not systematically influence systemic financial risk, regardless of broader macroeconomic conditions. The consistency of this null effect across different economic environments reinforces the conclusion that women’s representation in corporate leadership has limited impact on market-wide financial stability.

The analysis of firm-specific financial risk reveals more nuanced results. The study employs separate coefficients to capture the effects during different economic phases:

Specifically, the data show that both executive and board women inclusion have stronger risk-mitigating effects during economic expansions than during recessions. For executive positions, the coefficient during expansions (

These findings provide robust support for Hypothesis 3, confirming that the financial risk benefits of gender diversity in corporate leadership vary systematically across the business cycle. The stronger effects observed during expansion periods suggest that the strategic advantages of diverse leadership may be more readily realized when economic conditions are favorable, while recessionary environments may constrain the ability of diverse leadership teams to influence firm-specific risk outcomes.

These results collectively demonstrate that women’s inclusion in leadership significantly affects firm-specific financial risk through three distinct channels: (1) direct linear reduction, (2) nonlinear U-shaped relationships, and (3) business-cycle contingent effects. The robust findings across multiple specifications, coupled with strong diagnostic statistics, provide compelling evidence for our hypotheses while highlighting the contextual nature of gender diversity’s impact on corporate risk profiles.

Discussion and implications

Discussion and theoretical implications

The mitigation effects of EWI (BWI) on financial risks

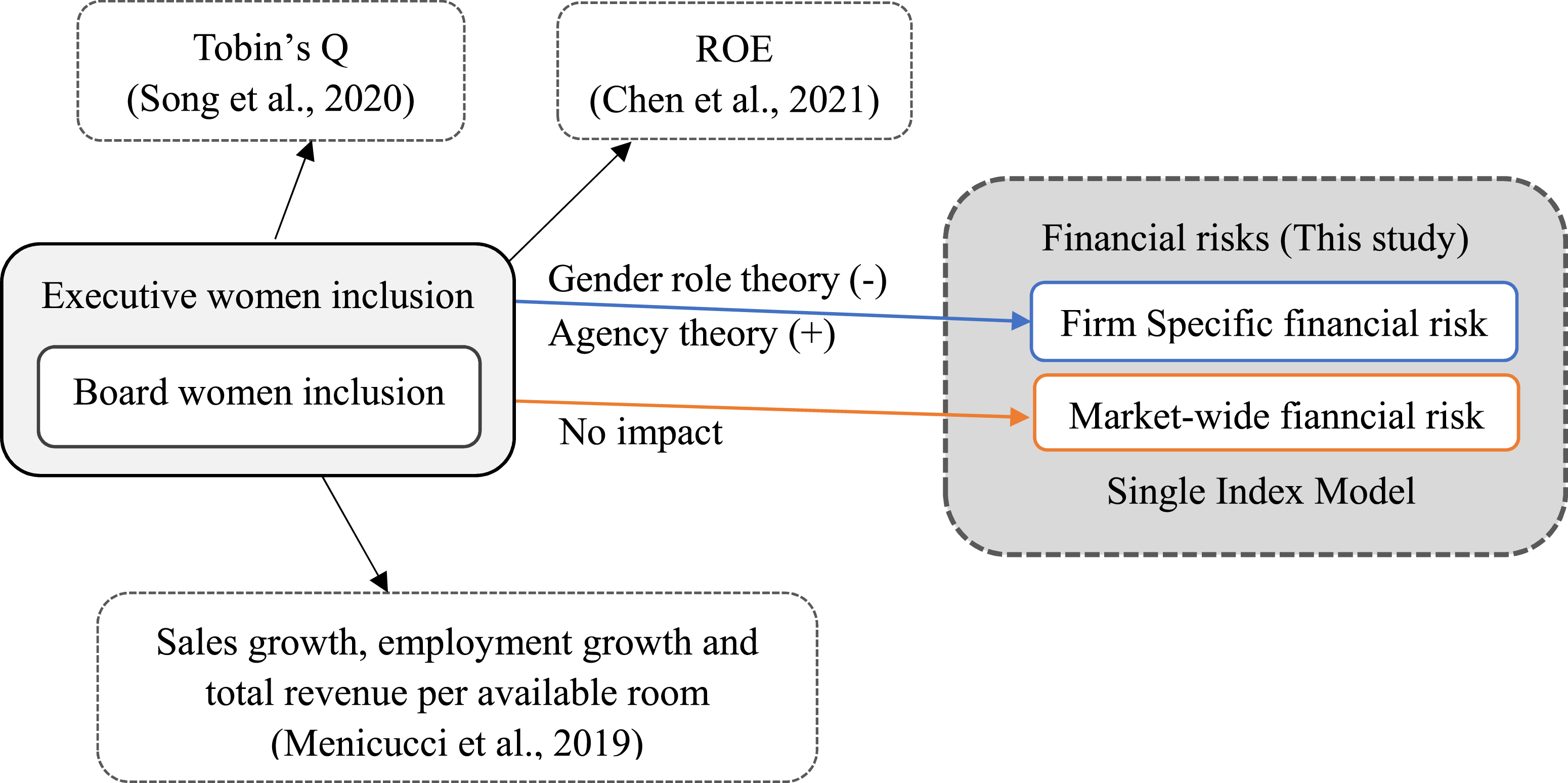

This study contributes to the literature by examining the impact of women’s inclusion through the novel lens of financial risk management (as is shown in Figure 1). While previous research has focused on traditional performance metrics like return on equity (Chen et al., 2021), Tobin’s Q (Song et al., 2020), and growth indicators (Menicucci et al., 2019), our investigation provides compelling evidence that women’s inclusion in leadership plays a crucial role in reducing financial risks. The findings demonstrate significant risk-mitigating effects of both Executive Women Inclusion (EWI) and Board Women Inclusion (BWI) on firm-specific financial risks in Chinese hotels, offering strong empirical support for gender role theory. Theoretical model linking women inclusion and different hotel performance. (Source: Authors own work).

By integrating gender role theory into financial risk analysis, this study deepens theoretical insights by linking its core principles to our findings. The theory posits that women, shaped by socialized expectations of communal and nurturing roles, are more likely to demonstrate caution, ethical sensitivity, and a heightened sense of responsibility (Eagly, 1987). These role-congruent tendencies manifest in more risk-averse decision-making and a stronger inclination to proactively identify and mitigate financial vulnerabilities. Our results confirm that female executives in hotels adopt more conservative financial strategies and display greater vigilance in safeguarding organizational integrity. This alignment strengthens the explanatory power of gender role theory by demonstrating how communal orientations translate into measurable financial outcomes within the service-intensive hotel industry, underscoring that gendered behavioral tendencies exert a tangible influence on organizational resilience.

Furthermore, this study extends gender role theory by revealing a differential impact on various risk types. Our analysis shows that while greater female representation in executive roles significantly reduces firm-specific financial risks, it does not exert a measurable influence on market-wide risks. This distinction highlights the unique contribution of gender diversity compared to other determinants. For instance, firm size influences both risk types, while factors like debt leverage primarily affect market-wide risks (Chen, 2013). In contrast, women’s inclusion specifically mitigates risks originating from internal governance and decision-making. This finding not only reinforces the theoretical mechanisms of gender role theory, such as greater caution and ethical sensitivity, but also clarifies the specific domains where gender diversity has the strongest impact.

The contrasting effects on different risk types can be attributed to their fundamental nature and origins. Market-wide financial risk stems from macroeconomic factors such as inflation rates, global economic uncertainty, and industry-wide shocks that affect all market participants equally. These systemic factors are largely beyond the control of individual companies and their management teams, making them difficult to influence through organizational-level decisions or leadership composition. In contrast, firm-specific financial risks are directly tied to internal operations, strategic choices, and management practices within individual companies. The inclusion of women in executive and director positions appears to enhance risk management through several mechanisms: improved decision-making processes that incorporate diverse perspectives, more comprehensive risk oversight, and the implementation of more conservative financial strategies. These organizational-level improvements can effectively mitigate firm-specific risks while leaving systemic, market-wide risks unaffected.

These findings have important implications for both theory and practice, suggesting that the benefits of gender diversity in leadership may be particularly valuable for managing organization-specific risks rather than broader market fluctuations. The study thus provides a more nuanced understanding of how women’s inclusion contributes to financial stability in the hotel industry, while also highlighting the boundaries of its effectiveness in different risk contexts.

The nonlinear effects of EWI (BWI) on hotel firm-specific financial risk

This study makes an additional contribution to the hotel literature by investigating the nonlinear relationship between women’s inclusion and financial risks, drawing on both gender role theory and agency theory as complementary explanatory frameworks. Our empirical analysis reveals a significant U-shaped relationship, demonstrating that there exists an optimal level of women’s inclusion in both executive and board positions that minimizes firm-specific financial risk. Figure 2 visually presents this nonlinear pattern while providing the theoretical underpinnings for this complex relationship. Theoretical explanation for the nonlinear effects of women inclusion on financial risks. (Source: Authors own work).

The initial risk-reducing effect of women’s inclusion aligns with gender role theory. At lower levels of representation, female executives and directors often have limited influence on core strategy and contribute primarily through enhanced monitoring and oversight. In this early stage (Stage I), traditional gender role expectations promote more cautious, risk-averse behaviors that strengthen governance and reduce firm-specific risks. However, as representation surpasses a critical threshold, agency theory offers a more compelling explanation. With greater numbers, women gain stronger influence, support, and legitimacy in decision-making. This expanded role can foster more competitive, assertive, and risk-tolerant behaviors that, in some instances, may exceed the risk preferences of male counterparts, thereby increasing financial risk (Stage II). Consequently, both theoretical perspectives operate across the continuum of women’s inclusion: gender role theory dominates at lower levels, explaining risk-averse tendencies, while at higher levels, women’s emancipation from traditional roles, fueled by critical mass and the influence of younger cohorts socialized under more egalitarian norms, diminishes these constraints, yielding risk-taking behaviors consistent with agency theory.

This dynamic creates an important inflection point in the relationship between gender diversity and financial risk. Our findings indicate that firm-specific financial risk in hotels does not decrease monotonically with increasing female representation. Instead, there exists a critical threshold beyond which the beneficial effects predicted by gender role theory are counterbalanced by the mechanisms described in agency theory. Below this threshold, the risk-mitigating effects dominate, resulting in reduced firm-specific financial risk. However, once female representation surpasses this optimal level, the risk profile begins to increase again.

To precisely identify these threshold values, we conducted regression analyses of firm-specific risk on both EWI/BWI and their squared terms, without control variables. The resulting equations are:

By deriving the first-order conditions through differentiation: The nonlinear effect of EWI and BWI on firm-specific risk. (Source: Authors own work).

Moreover, firms with exclusively female leadership (where both EWI and BWI equal 1) exhibit higher risk levels than those with entirely male leadership (where both indices equal 0). This pivotal finding indicates that while initial inclusion reduces risk, a surplus of representation can ultimately elevate risk beyond levels observed under all-male leadership. This underscores the critical point as the juncture where the advantages of gender diversity are maximized. The U-shaped relationship confirms that firm-specific financial risk is minimized at these calculated thresholds. Notably, the higher optimal threshold for executives (29.21%) compared to directors (24.20%) reflects their distinct governance functions. Executives, engaged in day-to-day management and strategic decision-making, may require greater representation before agency effects emerge, whereas directors, with a primarily supervisory mandate, appear to reach their optimal influence at a lower level.

The critical point, the minimum of the U-shaped curve, offers important theoretical and practical insights. At this threshold, the benefits of women’s role-congruent risk aversion are maximized. Beyond it, these benefits diminish as female leaders gain greater influence and gradually transcend restrictive gender role expectations, causing their risk preferences to converge with those of male counterparts and shifting organizational behavior toward greater risk-taking.

This inflection has significant implications. Theoretically, it demonstrates that women risk behavior is not fixed but dynamic, shaped by context and representation. It effectively reconciles gender role theory and agency theory by showing they coexist along a continuum, with the critical point marking the transition in dominance from one theoretical logic to the other. Practically, it reveals that gender diversity delivers the greatest risk-management benefits at specific, identifiable levels of representation rather than through indiscriminate increases.

For the Chinese hotel industry, this critical point provides a valuable benchmark for corporate governance and managerial policy. Hotels can apply this insight to strategically target female representation levels that optimize risk management and organizational performance, moving beyond merely addressing underrepresentation to understanding the specific conditions that generate the greatest benefit.

The asymmetric effects of EWI (BWI) on firm-specific financial risk

In China’s hotel industry, female executives hold only 18.2% of leadership positions and women occupy just 9.7% of board seats. Both figures fall substantially below this study’s identified optimal thresholds of 29.21% for executives and 24.20% for directors. This disparity confirms that the industry remains in Stage I, the initial phase of women’s integration where their participation demonstrates a measurable risk-reducing effect. Extending this inquiry, our analysis provides empirical evidence of asymmetric effects in this relationship across economic cycles.

The findings reveal that the risk-mitigating benefits of women’s inclusion are substantially stronger during economic expansions than in recessions. This indicates that female leaders exert a more pronounced risk-reducing influence on firm-specific financial exposure under favorable economic conditions. These results are consistent with gender role theory, reinforcing the view that female leaders contribute more effectively to risk management during periods of growth than during economic downturns.

This observed asymmetry can be attributed to several contextual factors. Recessionary periods, marked by higher baseline risk (0.08 in our sample vs 0.05 during expansions; He and Leippold, 2020), tend to trigger universally conservative behavior among all executives, irrespective of gender. This generalized risk aversion during downturns (Lerner et al., 2003) diminishes the distinctive, risk-mitigating impact female leaders exhibit in more stable times. Furthermore, the high-stress environment of a recession may heighten apprehension among female leaders, potentially constraining their decision-making efficacy.

Conversely, expansionary periods create a more conducive environment for female leaders to deploy their risk management capabilities. The stable economic climate and greater strategic flexibility allow women executives to more effectively leverage their well-documented tendencies toward stronger monitoring and higher ethical standards (Doan and Iskandar-Datta, 2020; Eagly, 1987). This enables a more effective alignment of management decisions with shareholder interests (Jensen and Meckling, 1976), culminating in significantly greater risk reduction during growth periods.

Practical implications

This study provides actionable insights for enhancing financial risk management through strategic gender inclusion in the hotel industry. The findings demonstrate that women’s representation in leadership significantly influences firm-specific financial risk, with direct implications for corporate governance and human resource strategies. First, promoting women into executive and board positions serves as an effective risk mitigation strategy. In emerging markets like China, where smaller hotels often operate with limited resources, conservative risk management is particularly vital. The ongoing privatization of China’s hotel sector has created a more competitive landscape where robust risk oversight is essential. Increasing female representation allows hotels to leverage their demonstrated ability to reduce firm-specific risks, thereby strengthening organizational resilience.

Second, the research identifies a clear opportunity to optimize risk management by targeting specific levels of women’s representation. Current figures, 18.2% for executives and 9.7% for board directors, fall substantially below the identified optimal thresholds of 29.21% and 24.20%, respectively. These thresholds represent the points where firm-specific financial risk is minimized. Industry leaders should implement structured diversity initiatives, including leadership development programs, unbiased recruitment processes, and mentorship opportunities. Crucially, significant risk reduction benefits can be achieved even before reaching gender parity, making incremental progress both practical and valuable.

Third, the asymmetric effects across business cycles highlight the need for adaptive leadership approaches. Since women executives exert their strongest risk-mitigating influence during economic expansions, hotels should consider placing them in key decision-making roles during these periods to balance growth with financial prudence. During recessions, when risk sensitivity tends to equalize across genders, a more balanced leadership composition may be optimal. This cyclical approach allows organizations to maximize the benefits of gender diversity in response to changing economic conditions.

For China’s evolving hospitality sector, these findings affirm that gender-inclusive leadership is not merely a social responsibility but a strategic imperative for financial stability. The evidence shows that calibrated increases in women’s representation, combined with thoughtful role allocation across business cycles, can form a core component of a comprehensive risk management strategy.

In practice, hotel organizations should prioritize gender diversity in leadership development, set measurable goals approaching the identified optimal thresholds, and remain mindful of how economic conditions influence leadership effectiveness. By implementing these evidence-based recommendations, the industry can strengthen financial resilience while advancing workplace gender equality. The study’s quantitative benchmarks offer concrete targets for human resource planning, balancing diversity benefits with organizational performance objectives in China’s dynamic market.

Conclusion, limitations, and directions for future research

This study provides important insights into the relationship between women’s inclusion in leadership positions and financial risk management within China’s hotel industry. Through careful empirical analysis grounded in gender role theory and agency theory, we have established several key findings that contribute to both academic literature and practical business applications.

Our research demonstrates three significant conclusions. First, we find strong evidence supporting gender role theory, showing that women’s inclusion in executive and board positions meaningfully reduces firm-specific financial risks. This reduction occurs because female leaders tend to implement more cautious business strategies and maintain stricter oversight of potential financial vulnerabilities. Second, our analysis reveals a nonlinear relationship between gender diversity and risk management, with optimal risk reduction occurring at specific representation levels - 29.21% for executives and 24.20% for directors. These thresholds provide concrete targets for organizations seeking to balance diversity with financial performance. Third, we identify important differences in how women’s inclusion affects risk across business cycles, with more pronounced benefits during economic expansions than recessions.

This study makes several important theoretical contributions to existing literature. By examining both market-wide and firm-specific risks, we provide a more comprehensive understanding of how gender diversity influences different types of financial vulnerability. Our application of both gender role theory and agency theory offers a nuanced framework for interpreting these relationships. Furthermore, our identification of optimal representation thresholds advances the field beyond simple linear assumptions about diversity’s effects.

For hotel industry practitioners, these findings suggest several actionable strategies. Companies should view gender diversity not just as a social goal but as a strategic risk management tool. The identified optimal representation levels provide clear benchmarks for diversity initiatives. Additionally, the varying effects across business cycles suggest that organizations might benefit from adjusting leadership roles and responsibilities according to economic conditions.

While this study provides valuable insights, we acknowledge several limitations. First, our focus on Chinese hotels may limit the generalizability of findings to other cultural and institutional contexts. Second, the binary gender classification in corporate reporting prevents examination of more diverse gender identities. Third, our analysis captures average effects during the study period but cannot account for potential changes over time as societal attitudes evolve.

Several promising avenues for future research arise from our findings. First, comparative studies across countries and cultures could help distinguish which insights are universal and which are context-specific. Second, incorporating more diverse gender classifications would provide a fuller understanding of how gender identity shapes risk management. Third, longitudinal research tracking changes over time could reveal how evolving social norms influence these dynamics. Finally, extending similar analyses to other hospitality sectors, such as airlines and tourism, would test the generalizability of our results.

In conclusion, this study significantly advances our understanding of how gender diversity in leadership affects financial risk management in the hotel industry. By establishing empirical relationships, identifying optimal representation levels, and contextualizing effects across business cycles, we provide both theoretical insights and practical guidance. While limitations exist, these findings create a strong foundation for future research while offering immediate value to industry practitioners seeking to enhance both diversity and financial stability in their organizations.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.