Abstract

The relationship between Short-Term Rentals and home purchase and rental prices is a hot and controversial research topic. This note analyzes the relationship between Short-Term Rentals, Purchase Prices, and Rental Prices of residential properties on the Costa Blanca (Spain). Using panel data techniques, the relationship between these variables is examined across 20 tourist municipalities for the period 2014–2024. The results suggest that the only consistent relationship operating in this context is from purchase prices to rental prices, which is consistent with an asset-pricing mechanism. Also, a short-term reverse causality from rental to purchase prices emerges at 6 months, suggesting an investment channel in which rental yield signals influence acquisition decisions. Conversely, limited evidence of the influence of short-term rental properties is found. These results raise doubts about the effect that regulations on short-term rentals may have on facilitating access to housing in these tourist destinations.

Keywords

Introduction

The relationship between tourism activity and housing markets has attracted growing scholarly attention across diverse geographical contexts, from large urban centers in China (Song et al., 2024; Zhang, 2024) to small tourism-dependent European economies (Vizek et al., 2023, 2024), and from investment-driven Mediterranean destinations (Patsoulis and Deirmentzoglou, 2026) to major global cities where the collaborative economy has reshaped accommodation supply. Within this broader debate, the rapid expansion of short-term rental (STR) platforms has intensified discussion over their effects on housing markets. While evidence for major metropolitan areas is growing (Barron et al., 2020; García-López et al., 2020), sun-and-beach coastal resorts have received comparatively little attention.

In the Costa Blanca, where so-called residential tourism or second-home tourism predominates, there is also widespread controversy about the role that STR play in housing prices and their accessibility to native residents. In this context, Perles-Ribes et al. (2025, 2026) explored the relationship between STR-housing linkages some representative Costa Blanca municipalities through univariate time-series methods, finding a weak correlation between STR and rental and housing prices and highlighting how these relationships are influenced depending on the type of tourism development present in the destination.

This note extends the Perles-Ribes et al. (2025, 2026) exercises by advancing the existing literature along two dimensions. First, expanding the sample to 20 municipalities that span coastal, metropolitan, and inland profiles. Second, moving from individual time-series to panel data analysis, thereby increasing statistical power. The central question is whether a causal relationship exists between STR expansion and housing purchase or rental prices across this heterogeneous panel, and in which direction. To the authors’ knowledge, this is the first exercise of its type carried out for the Costa Blanca as a whole, which represents a novel contribution on the literature on this topic.

Data and methodology

The panel comprises 20 municipalities in the province of Alicante selected on the basis of data availability and territorial representativeness (see Figure 1). Purchase and rental price series (€/m2) are sourced from Idealista; registered STR unit counts are drawn from the open-data portal of Turisme Comunitat Valenciana. The sample period is November 2014 through December 2024 (T = 122 monthly observations). Therefore the sample represents the evolution of the destinations from the end of the last Global Economic and Financial crisis to the present day. The panel is nearly balanced, with 16 missing observations in the rental price series concentrated in four municipalities. Costa Blanca and considered destinations.

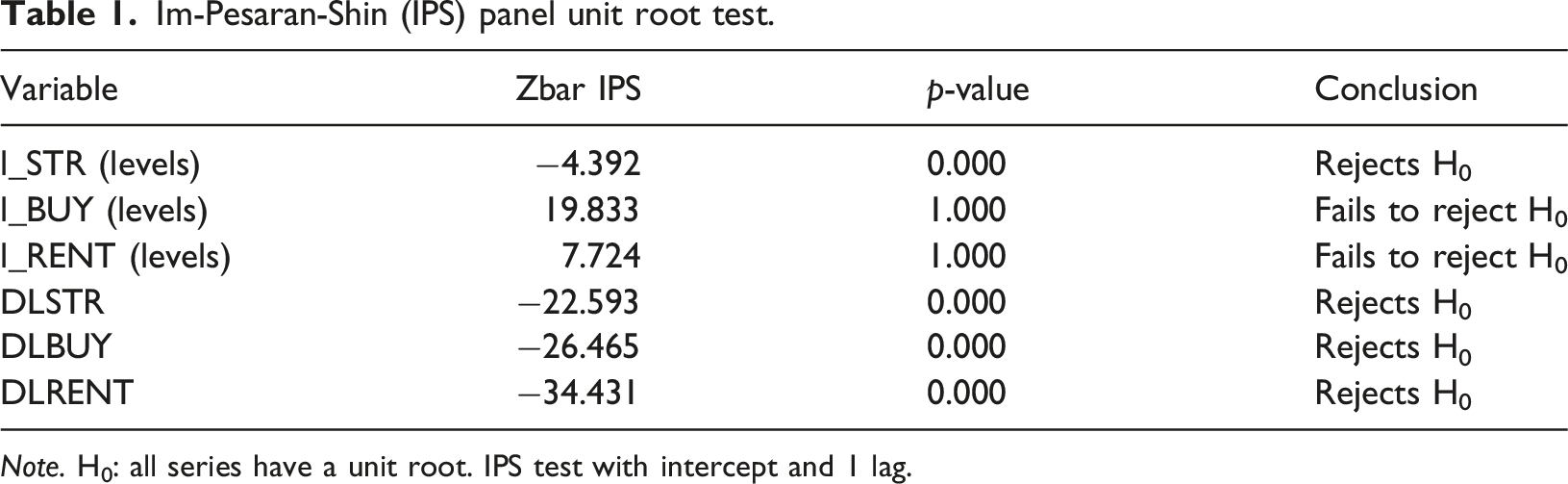

Im-Pesaran-Shin (IPS) panel unit root test.

Note. H0: all series have a unit root. IPS test with intercept and 1 lag.

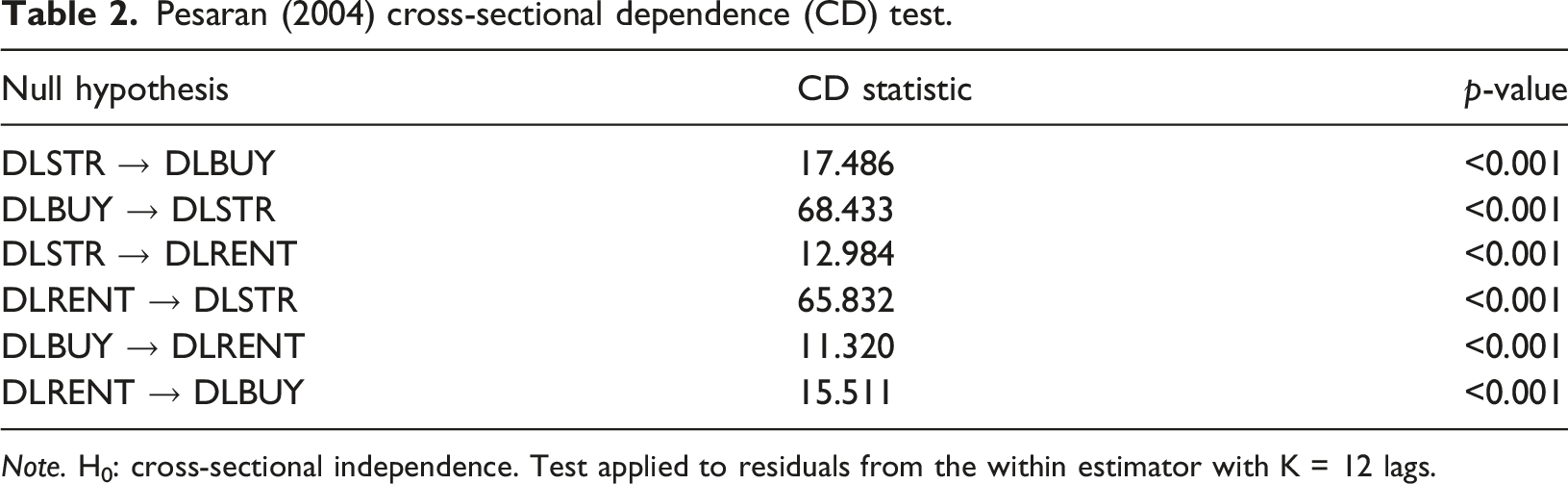

Second, a Pesaran (2004) cross-sectional dependence (CD) test is applied to residuals of the panel estimations. Finally, a Dumitrescu-Hurlin (DH) causality test (Dumitrescu and Hurlin, 2012) is performed employing a wild bootstrap procedure (B = 1000 replications) preserving cross-sectional dependence structure under H0 (López and Weber, 2017).

The DH panel Granger causality test is applied to all six bivariate pairs with a reference lag length of K = 12, corresponding to a full seasonal cycle and the typical duration of residential lease contracts. It is worth noting that SC and HQ criteria favor K = 6; AIC and LR favor K = 24; therefore K = 12 provides a justified trade-off.

Results

Pesaran (2004) cross-sectional dependence (CD) test.

Note. H0: cross-sectional independence. Test applied to residuals from the within estimator with K = 12 lags.

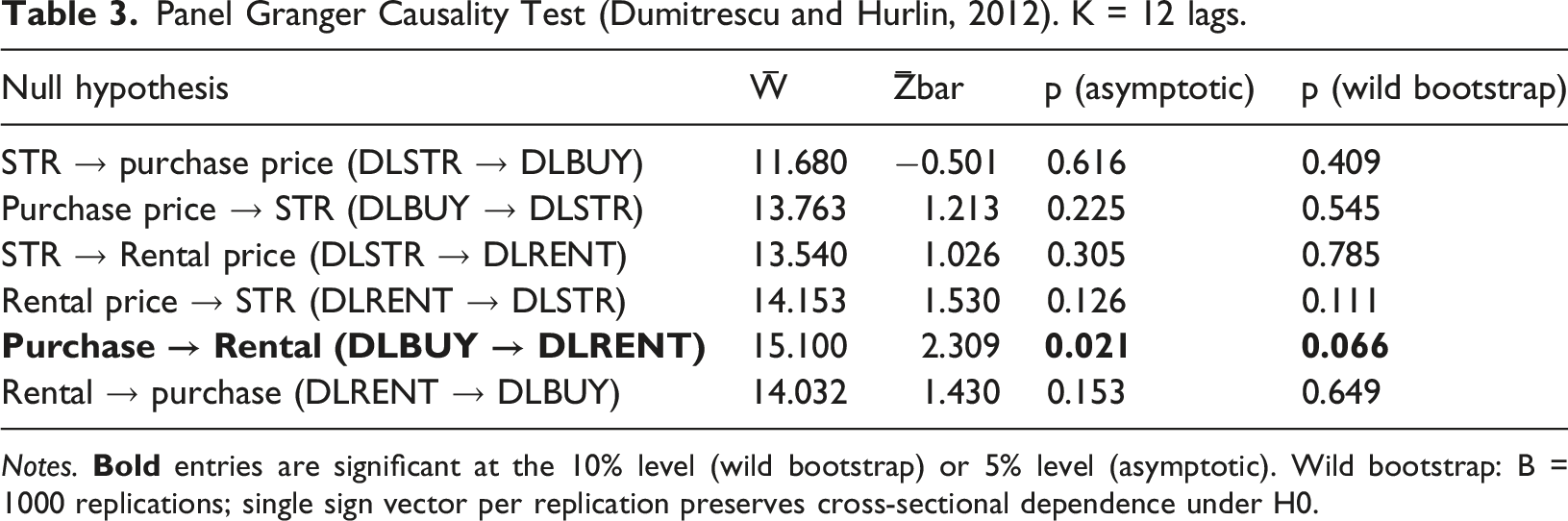

Panel Granger Causality Test (Dumitrescu and Hurlin, 2012). K = 12 lags.

Notes.

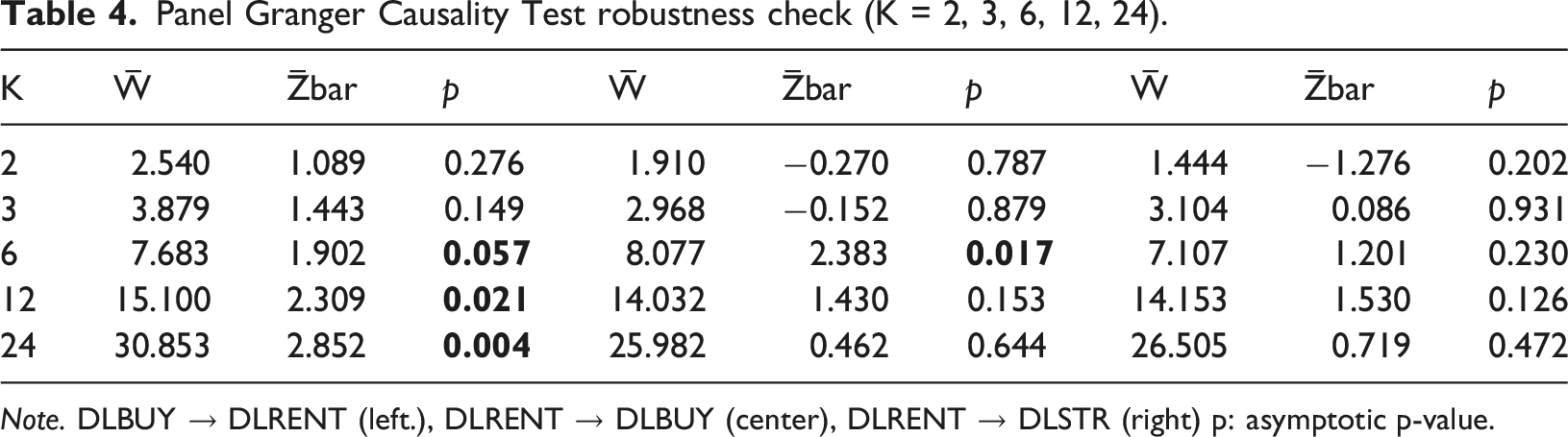

The DH test with K = 12 fails to reject the null of no Granger causality for any of the four pairs involving STRs — neither from STRs to purchase prices nor from STRs to rental prices, in either direction — under both asymptotic and bootstrap inference. This result holds uniformly across all lag specifications (K = 2, 3, 6, 12, 24), confirming that, across this heterogeneous panel, STRs do not constitute a temporal predictor of housing prices at the provincial level.

The only noteworthy result in the reference specification is the causality from purchase prices to rental prices (DLBUY → DLRENT: W̅ = 15.100, Z̅bar = 2.309, asymptotic p = 0.021). However, once cross-sectional dependence is corrected via the wild bootstrap, the p-value rises to 0.066, placing this finding at the 10% threshold rather than the conventional 5% level.

Panel Granger Causality Test robustness check (K = 2, 3, 6, 12, 24).

Note. DLBUY → DLRENT (left.), DLRENT → DLBUY (center), DLRENT → DLSTR (right) p: asymptotic p-value.

An exploratory inspection of municipality-level Wald statistics underlying the aggregate W̅ reveals substantial heterogeneity. Hotel-oriented coastal municipalities — Benidorm in particular — exhibit the highest individual statistics for the STR to purchase price direction, consistent with a market in which rapidly expanding STR supply displaces residential housing stock. In residential-tourism municipalities — Torrevieja, Orihuela, Guardamar del Segura — the pattern reverses. Individual statistics for the purchase price to STR direction dominate, consistent with a yield-driven conversion dynamic. Inland and metropolitan municipalities without direct tourism pressure show uniformly low individual statistics, providing a natural control group.

Discussion

Three substantive findings emerge from this analysis. First, STR activity does not Granger-cause housing purchase or rental prices at the provincial scale, regardless of lag specification or inference method. This contrasts with the bidirectional causality documented for Benidorm and the unidirectional causality found for Calp in (Perles-Ribes et al., 2025, 2026), and suggests that results from intensively touristic, hotel-oriented destinations cannot be generalized to a heterogeneous provincial panel that also includes residential-tourism, metropolitan, and inland municipalities. From a policy standpoint, this argues against blanket regional STR regulations justified primarily on housing-market grounds. The evidence base for price effects in specific destinations does not support extrapolation to the broader territory.

Second, the dominant dynamic in the panel is the transmission from purchase prices to rental prices. The most plausible mechanism is that property owners and investors revise rental rates in response to changes in the market value of the underlying asset, using purchase-price signals as a proxy for opportunity costs and expected capital gains. This asset-pricing channel has implications for rental affordability policy: interventions targeting transaction prices may transmit to rental markets with a lag of 6 to 24 months.

Third, the reverse causality from rental to purchase prices at K = 6 (p = 0.017) is consistent with an investment-channel interpretation. Thus, above-trend rental yields attract buyers, raising purchase prices within two to three quarters. This short-horizon feedback loop, combined with the longer-horizon transmission in the opposite direction, points to a dynamic two-way linkage between transaction and rental submarkets that warrants further research.

Overall, these results suggest that the dynamics of purchase and rental prices in the destination are more closely linked to exogenous factors than to the greater or lesser presence of short-term rentals (STRs). Consequently, a policy based on restrictions on STRs is unlikely to solve the housing affordability problems in this area.

Future work would disaggregate the panel by tourism typology, incorporate macroeconomic controls (Euribor, unemployment, overnight stays), and apply the cross-sectionally augmented IPS (CIPS) panel unit root test to complement the IPS results reported here.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author biographies

She works as a trainee researcher at the Institute for Economic Research and the Institute for Tourism Research, and serves as Technical Secretary of the Institute for Tourism Research (FCE-UNLP). She teaches the course Economics of Tourism I (FCE-UNLP). Her research focuses primarily on employment issues in tourism and job satisfaction, quality-of-life measurements, and public financing, among other topics.