Abstract

Exit from international agreements can severely damage a state’s reputation and hinder prospects for future cooperation. Nevertheless, governments sometimes withdraw from treaties and subsequently seek new agreements with the same partners. This article examines why dissatisfied states exit treaties in the context of international investment agreements, where unilateral withdrawal and renegotiation have become increasingly common. Although existing explanations highlight the importance of domestic political benefits of increasing governments’ ability to regulate foreign investments, they are unable to explain the diverse strategies they employ. Evidence from theory-building case studies and interviews with cabinet ministers in Indonesia and Ecuador suggests that exit was considered as the best way to catalyse renegotiations of their investment agreements. Yet they had to carefully balance between domestic political benefits and international reputational costs of exit when pursuing the strategic benefits. The findings contribute to a more refined understanding of strategic and political dimensions of treaty exit.

Keywords

Introduction

Many states have unilaterally withdrawn from international treaties and exited from international organisations (IOs; Helfer, 2005; von Borzyskowski and Vabulas 2019). Yet exit from international agreements is costly: it can damage a country’s international reputation, undermine diplomatic relations, and complicate future cooperation. Why, then, do governments unilaterally exit from international agreements, incurring the reputational costs?

Existing explanations for exit from international commitments focus on dissatisfaction with the terms of cooperation, sovereignty constraints, and domestic backlash against globalisation (Thompson et al., 2019; von Borzyskowski and Vabulas, 2025; Walter, 2021; Wojczewski, 2024). While these accounts explain why states can become incentivised to withdraw from international agreements, they cannot fully account for variation in governments’ exit behaviour: not all dissatisfied states exit, neither do all exits entail retreat from international cooperation. Frequently, governments first exit specific agreements while remaining committed to the broader regime – and often successfully re-engage under revised terms.

This variation suggests that exit may serve purposes beyond simple disengagement. I argue that governments can employ strategic exit: unilateral withdrawal used as leverage to renegotiate the terms of cooperation. When partner states are unwilling to revise the terms of international cooperation, exit can function as a bargaining tool to compel renegotiation (Verdier, 2021), and even catalyse reform in the wider global governance regime (Schmidt, 2024). Rather than necessarily represent rejection of international cooperation, exit can merely be a strategy within ongoing cooperation.

This research presents a theory-building study of the international investment treaty regime, where questions of exit and renegotiation have become highly salient. Since the 1990s, thousands of bilateral investment treaties (BITs) have been signed to promote and protect foreign direct investment (FDI) by codifying the property rights of foreign investors in host countries (Büthe and Milner, 2008; Elkins et al., 2006), 1 and by providing foreign investors access to international investor–state dispute settlement (ISDS) (Bonnitcha et al., 2017). These treaties have, however, generated controversy. Some governments increasingly worry about the threat of disputes with investors that entail expensive litigation and possible financial compensation, limiting the ability of states to regulate investment for the protection of their economies in the event of financial crises (Park and Samples, 2017), public health (Moehlecke, 2020; Uribe and Danish, 2021), and the environment (Wehrmann 2021).

The consensus in the literature on investment treaties holds that states seek more regulatory space via terminating or renegotiating BITs (Haftel and Thompson, 2018; Peinhardt and Wellhausen, 2016; Thompson et al., 2019). Yet governments adopt diverse approaches towards investment treaties. While some states such as India decided to unilaterally exit from their BITs, others such as Argentina have not terminated any despite having faced some of the most high-profile disputes with foreign investors (Calvert, 2018; Haftel and Levi, 2020; Peacock and Joseph, 2017). Emerging economies have also been particularly active in abandoning old BITs, suggesting changes in the bargaining power dynamics between developed and developing countries (Haftel et al., 2021; Hopewell, 2017; Huikuri, 2023).

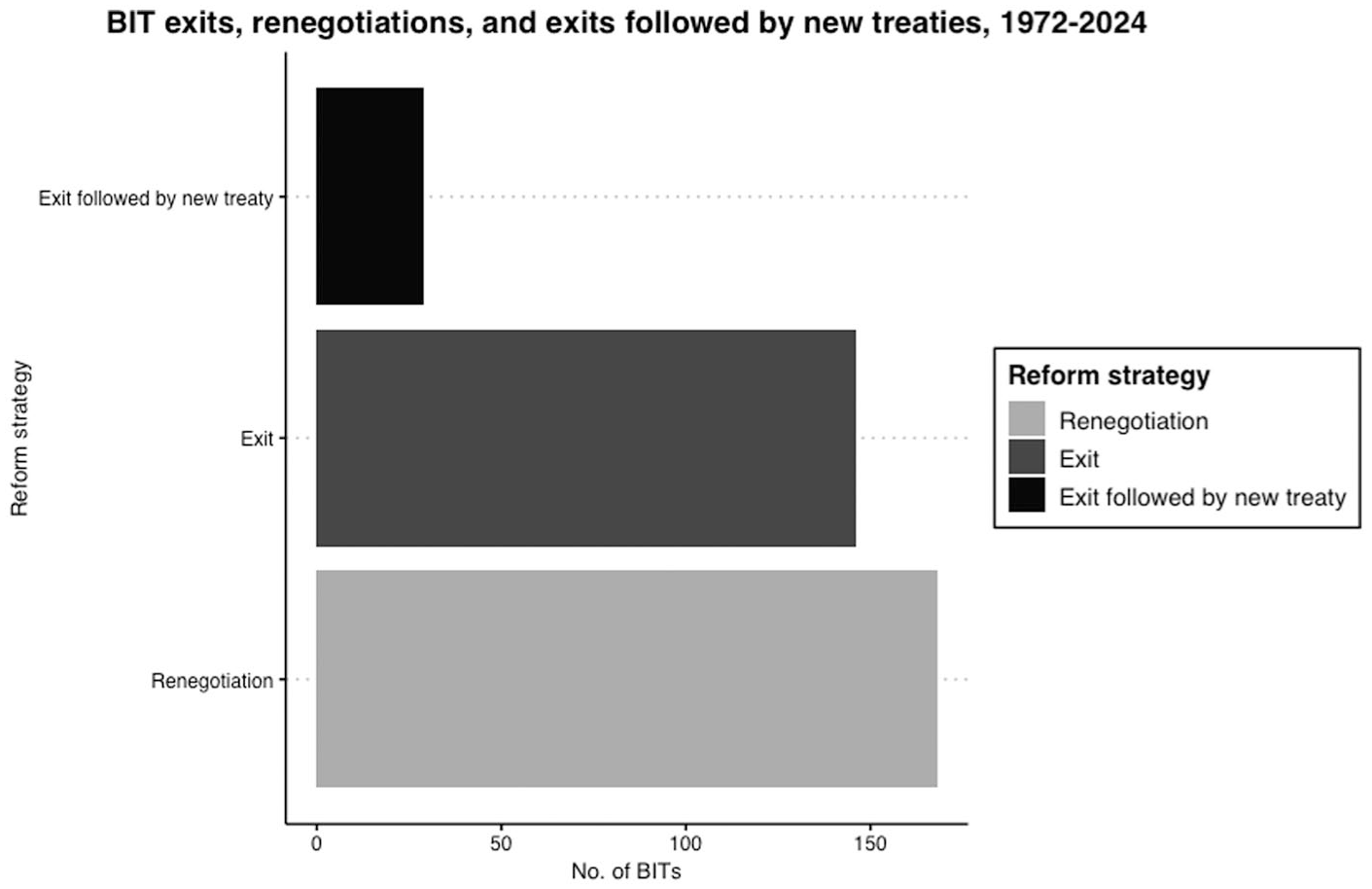

Furthermore, many countries renegotiate the treaties, and a small proportion of BITs have been first unilaterally terminated by one state before a new treaty was signed between the same partner states (Figure 1). What explains these diverse pathways to investment treaty reform?

Investment treaties that have been renegotiated, exited, or replaced by new treaty following exit, 1972–2024. Categories are mutually exclusive.

To answer the research question, I conduct two theory-building case studies of BIT exit and renegotiation processes by the governments of Ecuador and Indonesia. Both Ecuadorian and Indonesian governments exited from several of their BITs between 2008 and 2021, with mixed success in investment-related negotiations afterwards. With evidence from 19 interviews with leading politicians and bureaucrats at the time in the two governments, I process-trace the decision-making processes to either keep, attempt to renegotiate, or exit from BITs.

The theoretical insights grounded in these empirical contexts contribute to the study of reform in the investment treaty regime and beyond. The findings demonstrate that the governments considering adjustment of their international commitments must balance between international reputation costs of exit and the domestic political benefits from increased policy autonomy. When the domestic political climate turns negative towards international cooperation on the given issue area, political elites can gain popular support and electoral benefits by withdrawing from the relevant treaty. In the case of investment treaties, popular demands to regulate multinational corporations (MNCs) and to ensure that FDI benefits the host countries tilted the governments in favour of seeking investment treaty reform.

However, the international reputational costs of exit can hinder decisive efforts to adjust treaty commitments. Exit from investment treaties can risk scaring away foreign investors and damaging relations with the partner states (Hartmann and Spruk, 2022; Schmidt, 2023). Therefore, when these reputational costs are particularly high, the dissatisfied governments will rather seek to renegotiate or mutually terminate the agreements cooperatively. Reputational costs of exit are, however, not uniform across states or over time, and governments that perceive minimal additional reputational consequences are likely to pursue exit to achieve the domestic political benefits.

Importantly, exit can present a negotiation advantage at later negotiations. Once a government withdraws from the treaty, former partners will need to reassess whether they would benefit from agreeing to concessions in a new agreement, instead of having no treaty in place at all. This can help especially parties with less bargaining power to initiate new negotiations (Fisher and Ury, 1981; Lax and Sebenius, 1985). The case evidence shows that the successful conclusion of replacement treaties has been most likely in partnerships where reputational damage from exit were effectively minimised, and when gains from continued, treaty-based investment cooperation continue to exist.

This research contributes to understanding the efforts of especially weaker states to renegotiate international investment treaties in particular and international agreements more generally. By examining the two governments facing different kinds of contradicting pressures and incentives in detail, I provide an insight into their decision-making processes with regard to investment agreements they wanted to adjust with interview evidence from cabinet ministers at the time.

Furthermore, theory-building grounded in close investigation of empirics is a valuable contribution to theorising about broader dynamics of international treaty negotiations (Glaser and Strauss, 1967). While the politics of investment treaties have their idiosyncratic characteristics, the domestic political benefits and international reputational costs of any treaty exit can help to explain governmental decision-making when balancing between the two, also in relation to other kinds of agreements.

The rest of this article proceeds as follows. I first introduce the domestic and international contexts of investment agreement negotiations, before I discuss the concept of strategic exit based on past scholarship on states’ strategic adjustments in membership to international organisations and agreements. I explain why unilateral exit can provide a strategic benefit for some states in pursuit of improved treaty terms. Second, I introduce my research methodology and the logic of theory-building case studies to examine the dynamics of strategic exit in practice, before providing evidence from the interviews. Finally, I present the theoretical framework explaining why weaker governments choose to keep, attempt to renegotiate, or exit the international agreements with more powerful partners when they are unsatisfied with them. I conclude by discussing the scope conditions and generalisability of the presented theoretical insights, and implications for institutionalised international cooperation at the time it is increasingly threatened.

Domestic and international politics of investment agreements

BITs are international agreements that have their origins in highly unequal negotiations. The home countries to major investors and MNCs were in a stronger bargaining position in comparison to potential host countries to foreign investment due to dynamics of competition for FDI among developing countries (Bonnitcha et al., 2017; Elkins et al., 2006; Guzman, 1998; Salacuse, 1990; Simmons, 2014). However, since the onset of the regime, many host countries to FDI have improved their material capabilities, strengthened their domestic rule of law, changed their capital importer–exporter status, and diversified their alternatives for attraction of capital and finance (Haftel et al., 2021; Zeitz, 2024). These changes in the underlying power relations between states have coincided with changes in the investment treaty regime (Huikuri, 2023).

Furthermore, many governments have learned about the risks of investment agreements after facing investor–state dispute settlement cases (Poulsen and Aisbett, 2013). Argentinian efforts to mitigate the economic crisis of the 2000s (Park and Samples, 2017) and the Netherlands’ decision to ban coal use in energy production (Wehrmann 2021) are examples of government regulation which were met by large compensation claims by foreign investors. Governments become more likely to pursue exits and renegotiations of investment treaties when they find their regulatory space limited by investment treaties. Importantly, although the general public is generally not aware of BITs nor ISDS, these high-profile disputes with foreign investors have attracted wide news coverage and also increased the political salience of investment treaties as a result. Many people also hold strong skepticism towards MNCs and foreign investment generally, which has presented opportunities for elites to politicise their concerns (Vries et al., 2021).

Despite the changing power relations and increasing political salience of investment treaties, concrete progress to cooperative reform of BITs has been slow. Many governments continue to consider investment agreements and investor–state dispute settlement as an important tool for facilitation and attraction of FDI, even though the empirical evidence on the ability of BITs to attract foreign investment is mixed at best (Arias et al., 2018; Hallward-Driemeier, 2003; Hartmann and Spruk, 2022). Fundamentally, governments must balance between keeping their international commitments towards foreign investors in place, and increasing state regulatory space to cater to the domestic demands to regulate multinationals (Huikuri and Shim, 2025). Because governments’ preferences and priorities differ, little systematic reform has so far been accomplished at multilateral negotiations on investment treaty reform despite systematic efforts (UNCTAD 2024).

More importantly, the countries most concerned about bearing the costs of compensation claims from investors have been developing and emerging economies, who often are also the most dependent on FDI for capital flows (Schultz and Dupont, 2014). This underlying power asymmetry in the investment treaty regime has led to perceptions of unequal treaty terms and ‘tendency for the “exploitation” of the small’ (Olson, 1965). Weaker parties to investment agreements tend to have little leverage to voice their concerns and propose renegotiations with rich, capital exporting countries, who usually prioritise promoting their respective model BIT templates in bilateral negotiations (Berge and Stiansen, 2023; Haftel et al., 2023). It can therefore be difficult for the less powerful to convince their partners back to the negotiation table. 2 Investment treaties that were initially shaped by unequal negotiations between the global North and the global South are some of the most frequently exited international agreements to date.

Theorising strategic exit

A strand of international relations research on institutional choice and negotiations has provided insights into when and how states might want to adjust their membership in IOs and agreements (Hirschman, 1970; Jupille et al., 2013; Lipscy, 2017), sometimes strategically (Morse and Keohane, 2014; Slapin, 2009). However, termination of agreements can also be thought of as an intermediate step in a long-term interaction between the parties: a temporary break in negotiations through withdrawal can help one party to achieve concessions in future negotiations, according to a logic akin to labor strikes (Verdier, 2021). In practice, rather than understand treaty exit as the final collapse of cooperation, governments often keep open the possibility to negotiate new agreements at a later stage.

Strategic exit can be particularly attractive for governments that would otherwise struggle to initiate renegotiations of existing agreements. Especially when their more powerful counterparts continue to benefit from the existing terms of cooperation, weaker states may struggle to achieve changes to cooperative agreements with distributional consequences. 3 Even if a weaker state improves its bargaining position via material capabilities or outside options (Fisher and Ury, 1981), the stronger counterparts have little incentive to grant concessions if they continue to benefit from the regime regardless of the cooperation of one member (Gruber, 2000). Exit from the agreement may, therefore, be the only way for the weaker parties to catalyse renegotiations.

However, exit remains relatively rare empirically, because exit from international commitments is a particularly costly way to pursue renegotiations (von Borzyskowski and Vabulas, 2025). Exit creates international reputational costs because withdrawal can be perceived as reneging (or ‘defecting’) from international cooperation by others, and the exiting state will likely be viewed as unreliable (Brewster, 2018; Davis, 2021; Fang and Owen, 2011). Exit can particularly damage the relations with the former treaty partners, as they experience the breaking of commitments directly and bear any material consequences (Schmidt, 2023). Even for states that might otherwise want to seek strategic advantage in negotiations via exit, the reputational costs and uncertainty about future cooperation often prevent them from doing so.

When are governments then likely to consider a strategic exit? In other words, when do especially the weaker governments tolerate the reputational costs of exit and risk the collapse of cooperation in the long term? Exit is only attractive if there are also associated domestic political benefits of terminating international agreements. For international commitments to be credible, they must pose some sovereignty costs or limitations on states’ policy autonomy (Guzman, 2005). Exit from related agreements can result in domestic political benefits when these constraints on policy autonomy are removed: regained policy autonomy can be leveraged to cater to domestic demands for regulation, enactment of policies that would infringe on international legal commitments, or satisfy populist nationalist demands for exit (von Borzyskowski and Vabulas, 2019; Thompson et al., 2019; Voeten, 2020). Domestic political benefits, for example, in the context of election promises, can therefore incentivise governments to exit despite reputational consequences.

Although strategic exit can theoretically provide a negotiation advantage especially for the weaker parties, little research exists to date on whether governments in practice would think of treaty exits in these terms. 4 To study the possibility of strategic exit empirically, the next section presents the logic of theory-building case studies in the context of investment agreements. Through the two case studies, I investigate the extent to which international reputational costs and domestic political benefits faced by governments shaped their exit decisions, and to what extent they were thought to provide strategic advantage in future negotiations.

Research methodology

Theory-building case studies

Building theories through case studies is an inductive approach to theorising about an observed phenomenon, with the goal of constructing new theoretical propositions (Eisenhardt, 1989). Unlike theory-testing research, which seeks to provide evidence for or against specific hypotheses, theory-building research typically aims to address unexplored areas where current accounts provide inadequate or conflicting explanations. Case studies can be particularly useful at the stage of theory building where a magnitude of complex factors are considered (Eckstein, 2000: 119). It is the close connection to empirics that allows the development of valid, testable, and relevant theory (i.e. grounded theory) (Glaser and Strauss, 1967).

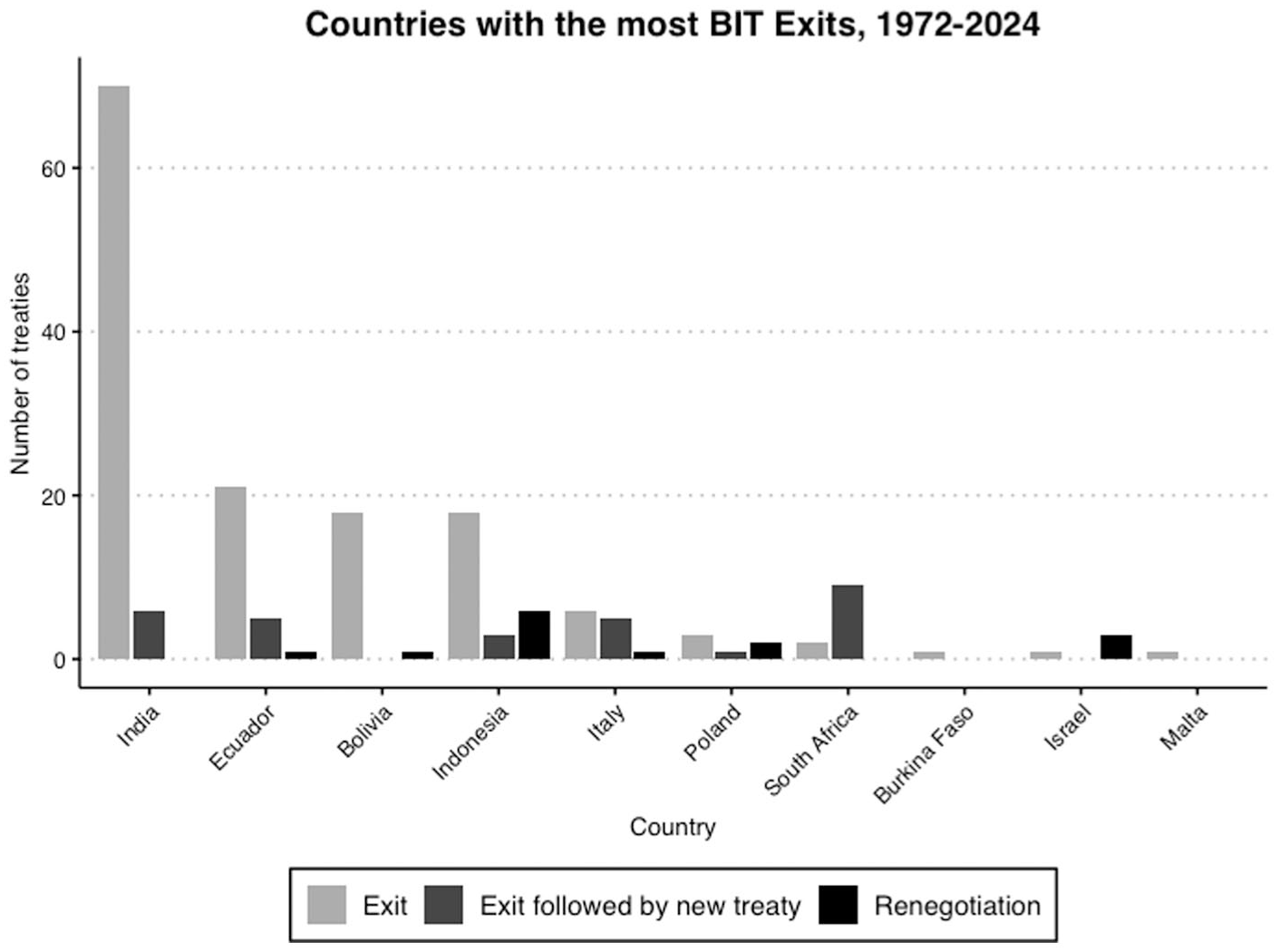

To study the dynamics of strategic exit, I conduct two case studies of governments that have attempted to pursue readjustment of their commitments under their investment agreements. I select the cases from the pool of countries that have unilaterally exited from BITs to identify governments that have become dissatisfied with their treaty commitments. Figure 2 shows the countries that have unilaterally exited from the largest number of BITs. In addition, it shows how many new agreements they have negotiated with the same bilateral partner following the exit as of May 2024, and how many BITs they have renegotiated without conducting exit first.

Countries with the most unilateral exits from BITs, as of May 2024. Mutually exclusive categories. Exits counted by withdrawing state; renegotiations counted for both parties.

Although India has unilaterally terminated from the most BITs due to its blanket policy to withdraw completely from old treaties before initiating new negotiations based on its new model BIT (Hanessian and Duggal, 2017), I focus on Ecuador and Indonesia, who by 2021 had completed their planned exit processes, and successfully concluded at least some new investment agreements with the same partners. This provides an opportunity to examine the possibility that unilateral exit can aid, rather than hinder, new negotiations with the partner states. By investigating the BIT reform processes by Ecuador and Indonesia, I can examine 16% of all unilateral withdrawals, and investigate in detail the handful of the rare instances where exit has successfully led to new negotiations.

The two countries also provide a great comparative case study for examining the negotiation dynamics over BITs. The two governments represent countries in two different regions, differ in the structure and size of their economies, as well as their political and colonial ties. Yet both governments decided to initiate exit from BITs following high-profile investment disputes with multinational corporations. In a set-up resembling the most different systems design, the cases are different in all but the key explanatory factors and manifest in the same outcome – BIT exit (Seawright and Gerring, 2008). I process-trace the sequence of decisions and actions by the governments that led to varying responses from different partners, and eventually, different outcomes of reform in specific BIT partnerships.

Elite interviews

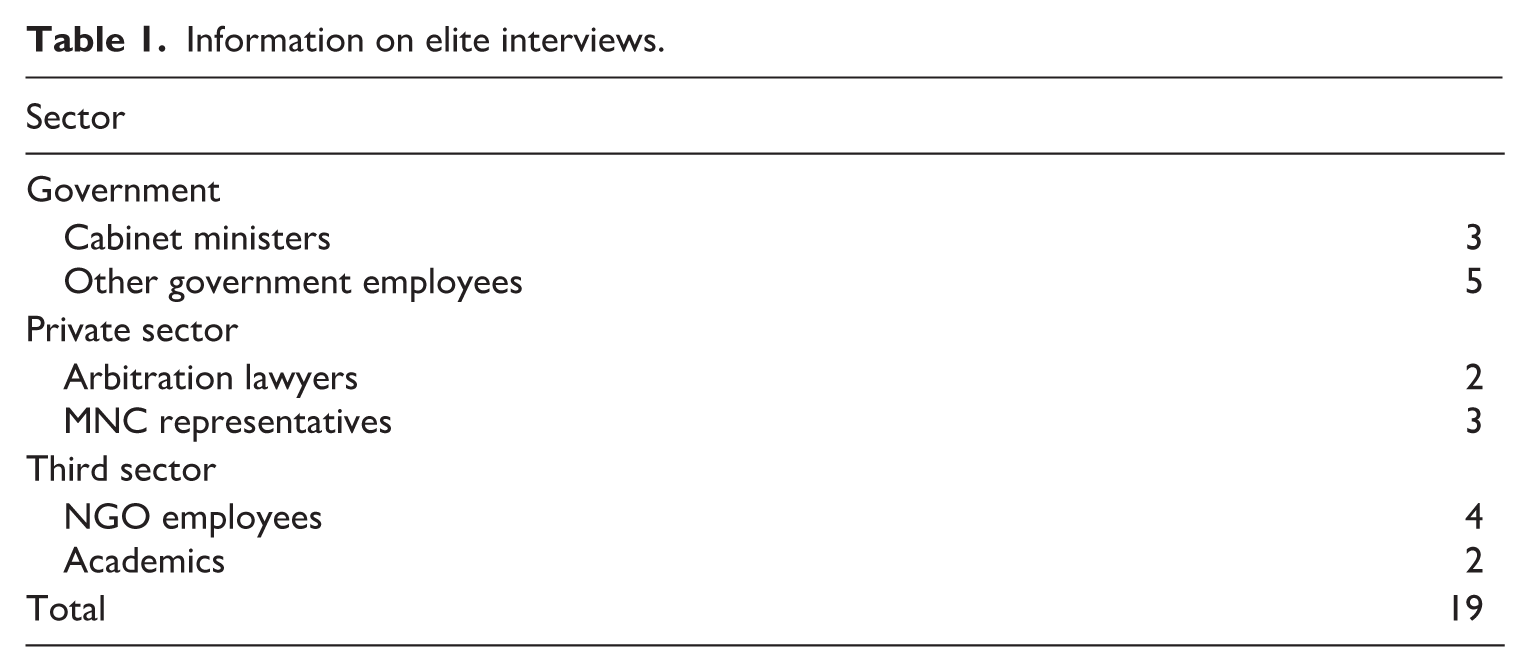

In addition to extensive secondary material from press releases, media reports, and legal and policy analyses, I collect evidence through elite interviews with individuals at the center of BIT reform efforts in Ecuador and Indonesia, as well as representatives of governments with whom the two exited or negotiated investment treaties. Qualitative expert interviews are particularly valuable for the analysis of complex decision-making processes, and for linking macro and micro levels of analysis (Von Soest, 2023). I therefore conducted 19 interviews with individuals who can be defined as elites: individuals with privileged access to power or decision-making regarding the building up to BIT terminations and their aftermath (Lilleker, 2003).

Interviewees included three senior cabinet ministers from Ecuador and Indonesia when the decisions regarding investment agreements were taken, providing unique insight into the reasoning of the governments’ political leadership at the time. In addition, I interviewed five government officials at relevant bodies of governments, and five private sector individuals, including representatives of MNCs and arbitration lawyers who had represented Ecuador and Indonesia in investment disputes. Because of the crucial role played by civil society activists pushing for BIT terminations, I interviewed six individuals from academia and non-governmental organisations (NGOs) who advised the governments of Ecuador and Indonesia regarding investment treaty reform (Table 1).

Information on elite interviews.

Due to the nature of specific events of interest, I conducted purposive sampling targeting specific individuals involved in BIT politics. 5 All contacts were approached either directly via email or email introduction. The acceptance rate to the request for an interview was 71% for Ecuadorian and 66% for Indonesian individuals. 6 Each interview lasted between 45 and 80 minutes, and they were recorded and subsequently transcribed with the participants’ consent.

Exit and renegotiation of investment treaties by Ecuador and Indonesia

Drawing from the interviews and extensive secondary material, I first discuss the role of domestic political benefits in the decision to attempt to reform investment agreements, and the difficulty of initiating negotiations from a position of historical bargaining disadvantage with more powerful treaty partners. I then address the role of international reputational concerns for the two governments, and how they can explain the overtime changes in the governments’ decisions to exit or renegotiate BITs. Finally, I consider the factors that aided the strategic exit to achieve new agreements.

The overtime changes in what was considered as the best way to pursue reform by the two governments highlight the importance of both domestic and international factors. The domestic political benefits of limiting investment treaty-based exposure to ISDS incentivised both governments to pursue reform of their investment treaties. However, the choice to pursue exit over renegotiations was shaped by the governments’ perceptions over the international reputational costs. Although for Ecuador, the initial hesitation to exit was strongly shaped by concerns over investors and governments’ perceptions and reactions, Indonesia could begin prompt exits due to lower perceived reputational costs.

Importantly, the historically disadvantaged position in investment treaty negotiations made attempts to renegotiate with capital exporting partner states unfeasible initially for both Ecuador and Indonesia. Following exits, however, new negotiations could be initiated with partners for whom the lost gains from cooperation became clear. Although Indonesia was successful in quickly concluding new investment treaties with important regional partners, Ecuador had less success due to its reputation as hostile especially to Western governments and investors following exits and government rhetoric. The cases show the continued existence of cooperation gains along with minimised reputational damage that are necessary for strategic exit to help in achieving improved treaty terms in future negotiations.

Domestic political benefits

Both Ecuador and Indonesia had negotiated extensive networks of BITs during the boom of investment treaty accumulation in the 1990s and 2000s. However, they faced high-profile disputes with foreign investors, enabled by the investor–state dispute settlement mechanism included in their BITs. The disputes shifted domestic public opinion against foreign investors generally, and increased support for politicians that actively took a strong stance against BITs.

In 2002, the oil-rich Ecuador faced its first claim by Occidental Petroleum, a US oil and gas company, when the government of Ecuador cancelled the agreed-on VAT reimbursements in an effort address the 1990s economic crisis.

7

When the dispute escalated to the World Bank institution Institute for the Settlement of Investment Disputes (ICSID), and the claims awarded to the MNC reached an unprecedented US$1.71 billion,

8

the salience of investment disputes and BITs increased among the wider public: The court became literally a bad word in Ecuador . . . CIADI [ICSID in Spanish] was the devil, because that’s where Occidental had initiated the humongous arbitration against Ecuador. (Interview E010)

When Rafael Correa was elected president in November 2006 in Ecuador, he represented the most ideologically radical left and fully identified himself with what was discussed as the ‘left turn’ in Latin American politics at the time (Schamis, 2006). His policies were hugely popular, including raising the tax on oil exports to 99%, doubling the welfare benefits for the poor to US$30 per month, and importantly, pushing through a new constitution explicitly banning investor–state dispute settlement outside of Latin America. He was also openly anti-American, and he actively reached out to new investment partners in Venezuela, Iran, and China. With his 73% approval rating, and a rare majority in government, Correa sent written notice to withdraw from the ICSID Convention in 2009, which was seen as a ‘symbolic break with international governance, linked to the World Bank’ (Interview E008).

Despite the exit from the ICSID Convention, disputes with investors did not cease to proceed because of Ecuador’s various BITs delegating dispute settlement to the World Bank institution (Interview E002). Therefore, in 2008, Correa proceeded to exit BITs with Cuba, Dominican Republic, El Salvador, Guatemala, Honduras, Nicaragua, Romania, Uruguay, and Paraguay. Although these initial exits were largely symbolic due to limited investment coming from these states, Correa’s decisive action against the neoliberal investment instruments was hugely popular, demonstrating the domestic political benefits of the exit from BITs.

Concerns over investment disputes also became salient in Indonesia in 2012, when the British Churchill Mining and the Australian Planet Mining initiated claims against the Southeast Asian country at ICSID (Price, 2017). Although the natural resource rich Indonesia had grown its economy partly due to the surge of FDI into the mining sector following the Commodities Boom of the 2000s, rising resource nationalism was increasing the popularity of policies such as the disputed cancellation of mining licenses in favour of local companies, and President Susilo Bambang Yudhoyono’s (SBY) new mining law, which effectively introduced a ban on the export of raw minerals (Abraham, 2018). The president noted that ‘I do not want those multinational companies to do anything they desire with their international back-up and put pressure on developing countries such as Indonesia’ (Saragih, 2012).

The timing of the exit from the first BIT coincided with strong pre-election nationalism in Indonesia, together with a broader rising sentiment of economic nationalism driven by an expanding economy and a consumer-oriented middle class (Bland and Donnan, 2014). Therefore, when Indonesia sent its first notice to the Dutch embassy in Jakarta of exiting the BIT between the two countries in March 2014, the news was welcomed by domestic news outlets and policy activists (Dwi Armaja, 2015). The incumbent president Joko Widodo went on to win the presidential election in July the same year.

Both governments therefore gained domestic political benefits by actively moving against BITs that resulted in ISDS cases against them and were perceived to unfairly limit the governments’ ability to regulate. The key political figureheads tapped into underlying sentiments and concerns in the wider population, intentionally politicising investment treaties in particular.

Historically weak bargaining position

While domestic political benefits can explain why the governments acted towards BIT reform, they do not explain why exit was perceived as the best strategy. Key commonality between the circumstances of Ecuador and Indonesia is their historically weak bargaining position in investment treaty negotiations. This made the initiation of renegotiations with partners difficult: because both developing countries had leveraged FDI attraction towards natural resources as a strategy for economic development, the home countries to MNCs had largely dictated the terms in BITs, including the strong dispute settlement mechanism.

It was the perception in the Ecuadorian government that because the treaties are structured to favour the multinationals, partner states have little reason to agree to renegotiate the features that benefit these key domestic interest groups: [We did] not have the possibility to push the other states to renegotiate or [agree on] mutual termination. We cannot say to the US or to the French government ‘let’s renegotiate’ when it’s a treaty that is established precisely in their benefit, and not our benefit. Then we don’t have to position in the international negotiation [sic]. (Interview E009)

These perceptions together with the asymmetric relations explained why Ecuador and Indonesia did not manage to renegotiate BITs and the dispute settlement features right away, and instead opted to unilaterally exit from them.

9

Importantly, unilateral exit was considered the quickest way for limiting exposure to investment disputes given the notorious sunset clauses in BITs, which keep the treaty terms in place often for decades after termination of the treaty (Huikuri and Shim, 2025). Because the timeline for any potential renegotiations was highly uncertain, exit was considered the best way to ‘start the clock’ (Interview I002). Exit was considered a necessary first step in catalysing change in the treaties, a strong perception held in both governments at the time: To renegotiate BITs, you must have a strategic position to get the two parties on the same table to renegotiate the treaty. If I am Ecuador, and you are the UK, how can I get you on the same table as me to renegotiate the BIT if the BIT benefits you with a lot of issues? If you are ok with the BIT, you don’t want to renegotiate the treaty! So, the first step is to decide to terminate the treaty. You can open the door to renegotiation with a new BIT if you want. That was our strategic reason to terminate and leave that door open to renegotiate later with better terms. (Interview E004)

International reputational costs

Both Ecuador and Indonesia could therefore achieve domestic political benefits and shared perceptions that exit was necessary to overcome their disadvantage in investment treaty relations. However, the decisions and timing of exits were strongly shaped by the governments’ perceptions over the severity of international reputational costs that exits would entail.

Despite the strong resolve of the Ecuadorian government to withdraw from the investor–state dispute settlement system, Correa’s governments’ exit from BITs was delayed because of worsening economic conditions, concerns over the progress of free trade negotiations with the European Union (EU), and the diplomatic pressure especially from the United States. Despite the so-called ‘easy BITs’ having been exited early with the regional partners, Ecuador held up exiting from the most important BITs until 2017 because of concerns over international reputational costs – with the complete exit from the regime lasting over 10 years.

A major commodities decline in the late 2014 hit Ecuador badly, with the price of crude oil plummeting. Year 2015 was also the first year during Correa’s presidency that Ecuador experienced zero growth in its GDP, and 2016 saw negative growth rates of some −1.5% (World Bank 2020). A disastrous earthquake also hit Ecuador on 16 April 2016, with devastating consequences for the local economy, as well as the tuna and banana industries heavily concentrated in the affected region. For Ecuador, ‘pissing off the international community when we most needed particularly the multilaterals to kick in . . . This was the wrong moment’ (Interview E008).

The international diplomatic costs of exits were also apparent in the increasing pressure from the United States, which made clear that exiting the BIT with the United States would have serious consequences: the United States was able to block a pending International Monetary Fund (IMF) loan Ecuador had been negotiating with the IMF (WikiLeaks document 09QUITO973_a, 2009). 10 As a result, the next wave of BIT exits did not target the treaties with the United States or China, which continued to be the most vital home countries to foreign investors, and instead Ecuador exited from BITs with Finland, the United Kingdom, and Germany in 2010, which were considered to carry less heavy international reputational costs. When asked why cooperative adjustment of BITs could not be achieved instead of exits at this stage, the Ecuadorian officials expressed frustration over its impossibility because of the investor-hostile reputation Correa’s government had fostered due to the early exits and the lack of leverage: ‘[in our position] . . . you terminate you get rid of it. And then you start negotiating a different model’ [Interview E003].

Ecuador was only able to exit the rest of its BITs in 2017, after it had mitigated what were perceived as the most negative consequences that exits would entail. It was important for Ecuador to terminate all of the remaining BITs, while at the same time to not appear favouring some partners over others (Interview E003). China was heavily investing into Ecuador at the time through large infrastructure projects, including the over US$10 billion Pacific Refinery. China was less concerned with Ecuador’s hostility towards the Bretton Woods system, and more used to a contract-based model of investment protection. By the time Ecuador exited the BIT with China in 2017, most of the Chinese-funded infrastructure projects had contract-based arbitration coverage in place. 11 Furthermore, Ecuador waited for the Accession Protocol to the Multiparty Agreement with the EU in November 2016 to be executed, and officially joining the EU–Andean Community free trade agreement (FTA) before exiting the BITs with the remaining Western partners in Correas’ last week in office as a president. Ecuador therefore only exited from these BITs after it had effectively mitigated the related international costs.

The perceived international reputational concerns and their mitigation efforts by Ecuador can, therefore, explain the timing of their exit from BITs. However, Indonesia did not perceive as high international reputational costs of exit initially. On the contrary, Indonesia began a swift process of systematically exiting from BITs as their appropriate termination windows approached. However, the Indonesian government was somewhat taken by surprise by the strong international reactions to their exit process, and they changed course from exits as the primary strategy to renegotiations after realising the possible costs of exits – and what eventually turned into a strategic advantage in fresh negotiations with regional partners.

Following the global boom in mining between 2003 and 2014 and after the rising demand from China had increased the prices of commodities dramatically, Indonesia was in a strong economic position and wanted to take an active stance in ensuring that more of the profits of resource extraction would stay in the country.

12

Importantly, the confidence that any exits would not be seriously affected by BIT exits was prominent in the government at the time: Indonesia has become more confident . . . Its natural resources . . . are in such high demand in the rest of the world, that regardless of what the investment dispute resolution mechanism is, foreign investors will still come . . . The prospects for large profits from investing in Indonesian mining projects was so attractive that people were willing to come, regardless of the risks involved. (Interview I005)

Given the Indonesian governments’ confidence over continued foreign investor interest, on 13 March 2014, the Dutch embassy in Jakarta announced that Indonesia had sent notice of their intentions to terminate the BIT between the states. At the time, Indonesia also began a systemic review of its 64 BITs and five investment chapters under FTAs conducted by the Ministry of Foreign Affairs and the Ministry of Investment Coordination Board (BKPM) and proceeded to formulate its new negotiating template for future BITs. 13 Although the exits were not perceived to cause much international reputational damage, already at the time the government of Indonesia strongly signaled that their intention was not to completely exit from investment cooperation: as the responsible minister Abdulkadir Jailani explained, ‘Indonesia has not lost faith in IIAs in general. Indonesia merely intends to modernize and to renegotiate its IIAs with a view to providing greater capacity to regulate in the public interest’ (Jailani, 2015). For Indonesia, it was therefore also important to mitigate any possible reputational damage in the eyes of international business and BIT partner governments.

Indonesia also attempted to mitigate any negative reputational consequences of exits by promoting an image of a technocratic BIT review process. To signal technical competence and objectivity, it was important for Indonesia to follow the exit procedures in relevant BITs, and to exit systematically from treaties with different partners. The systematic exits were thought to avoid any negative political implications or ‘bilateral backlash’ that might undermine Indonesia’s relations with treaty partners (Jailani, 2015). The messaging from the government was vital in communicating Indonesian openness to negotiate new treaties at a later stage and demonstrates their efforts to attempt to mitigate reputational damage.

Despite these efforts to avoid the international reputational costs of exit, Indonesia became aware of the rising concerns abroad over what was perceived as the populist resource nationalism (Abraham, 2018). After exiting from 18 BITs by March 2015, the government of Indonesia changed its approach to BITs by stopping exits and shifting its focus on attempting to renegotiate them. In addition to the concerns of backlash from foreign investors and partner states, the officials learned that the sunset clauses in BITs kept being triggered every time an old BIT was terminated unilaterally and realised the need to find other approaches to eliminate ISDS obligations in them (Interview I002). Indonesia was also better positioned to start renegotiations, as it had developed a new model BIT. 14

Importantly, the exits had created time pressure on the partner states, because any new investment projects would no longer enjoy access to ISDS following Indonesia’s BIT exits. A sense of urgency to negotiate new investment agreements especially for the important regional partners had emerged due to the exits.

Success of future negotiations

The ability of BIT exits to catalyse new negotiations with Ecuadorian and Indonesian partner states were strongly affected by perceptions over continued existence of cooperative benefits that maintaining treaty-based investment protections would bring, as well as the reputational damage done by the exits.

Since signing most of its BITs between 1968 and 2002, Indonesia had dramatically grown its economy and diversified its sources for foreign capital attraction, and the demand for Indonesia’s natural resources abroad had steadily increased. There was a heightened sense in the Indonesian government that ‘foreign investors need Indonesia more than Indonesia needs foreign investors’ (Interview I005), which emboldened the government and gave them leverage when pursuing new negotiations. However, despite investment opportunities, the weaknesses of Indonesia’s institutions had become apparently with widespread corruption and unpredictability of its domestic justice system (Dick and Mulholland, 2016). 15 As a result, investment treaty protections and access to ISDS was crucial for reassuring investors that their property rights and prompt resolution of disputes would be guaranteed. Cooperative gains therefore continued to exist from keeping international treaty protections in place, which would benefit both Indonesia and foreign investors.

In addition to continued cooperative gains from investment treaties, mitigation of reputational damage during the exit processes made a difference to follow-up negotiations. While Indonesia went to great lengths to communicate their intentions to renegotiate the treaties, Ecuador’s exits were largely perceived as fundamentally opposed to the international regime, and especially towards its Western partners. Indonesia publicly repeated that it ‘has not lost faith in IIAs in general’ and that ‘Indonesia merely intends to modernize and to renegotiate its IIAs with a view to providing greater capacity to regulate in the public interest’ (Jailani, 2015) during its exits.

Two important regional partners, Singapore and Australia, concluded new investment agreements with adjustments to the dispute settlement clauses shortly following the initial exits: the negotiations for the Indonesia–Australia Comprehensive Economic Partnership Agreement (IA-CEPA) were concluded in August 2018, while the new Indonesia–Singapore BIT was signed in 2019. In these partnerships, not only would lost gains from investment protections be quickly apparent, but the close channels of communication also aided mitigation of reputational damage from exits.

For Ecuador, because of Correa’s openly hostile rhetoric towards the United States, the Bretton Woods institutions, and Western MNCs, the perception internationally was that Ecuador was principally anti-foreign investment and seeking a clean break from the investment treaty regime (Interview E008). However, mitigation of negative investor perceptions also made a difference to how Ecuador’s BIT exits were perceived by its Chinese partners. Ecuador mitigated Chinese investors’ concerns by negotiating investment contracts with important Chinese firms, thus signaling its continued pro-investment attitude. The compromise was that state–investor contracts still allowed contract-based access to investment dispute settlement, but in Latin American institutions, such as the Santiago de Chile Chamber of Commerce or the Sao Paolo Chamber of Commerce, this alleviated investors’ concerns and was acceptable to the Ecuadorian government, demonstrating that a negotiated compromise was indeed a possibility. This mitigation of investment relations also likely contributed to Ecuador successfully negotiating an FTA with China later in 2023. On the contrary, it is yet to conclude new investment-related agreements with most of the Western partners.

When do governments keep, renegotiate, and exit investment treaties?

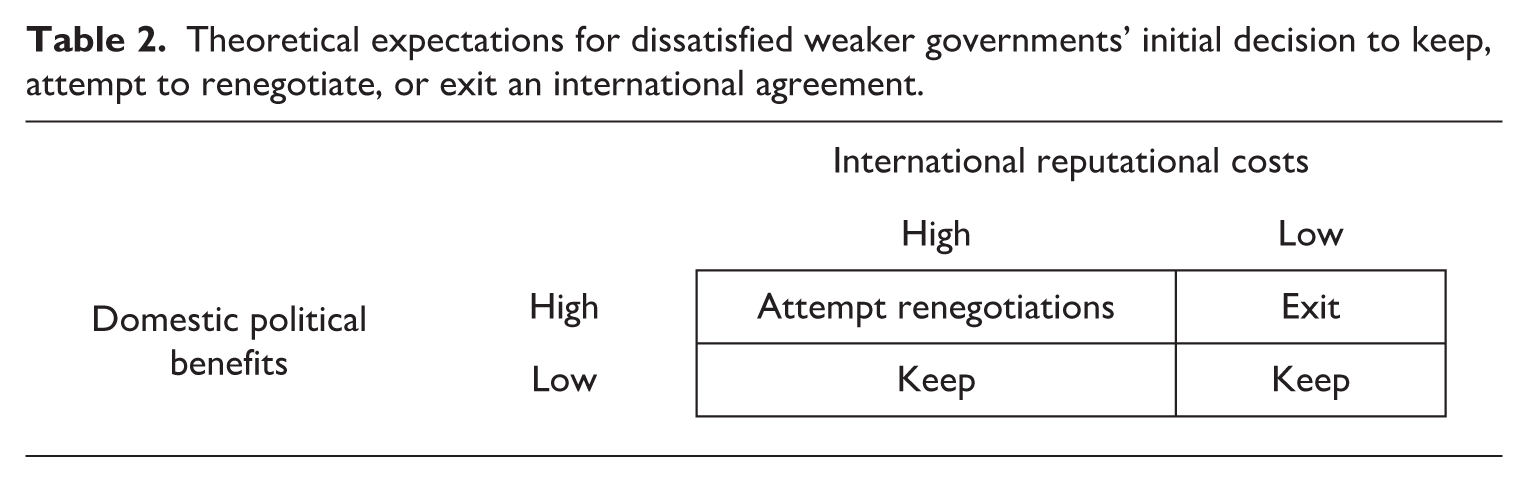

The evidence from the experiences of Ecuador and Indonesia show that adjustment of investment treaties was a careful balancing act between domestic political considerations and the international negotiation dynamic with the partners. These insights provide an opportunity to derive potentially generalisable insights for how states seek to adjust their treaty commitments. Governments which cannot unilaterally force renegotiations, but who yet are dissatisfied with an existing international agreement, must balance between international reputational costs and domestic political benefits when choosing whether to keep, attempt to renegotiate, or exit the treaty (Table 2).

Theoretical expectations for dissatisfied weaker governments’ initial decision to keep, attempt to renegotiate, or exit an international agreement.

When the domestic political benefits of adjusting the international agreement are low, the weaker, dissatisfied state is likely to keep the agreement in place. This is because attempts at renegotiating are often costly, involving time, resources, and diplomatic effort, and may not be reciprocated in the first place if the partner states are not willing to adjust the terms of cooperation. Unilateral exit on the contrary involves the associated international reputational costs and creates uncertainty regarding possibilities for future cooperation. In the absence of domestic political benefits to incentivise the government to act towards the agreement, they are likely to keep the agreement in place.

When the domestic political benefits from adjusting the agreement are high – either because of political salience of the relevant cooperation issues or active elite politicisation – the government is likely to act either by attempting to renegotiate or exit the treaty. The choice over the appropriate strategy depends on the perceptions over how severe the international reputational consequences of exit are. Cooperative adjustment either via renegotiation or mutual termination is preferable when the reputational damage from exits is perceived as high and likely to hinder future cooperation.

However, neither the international reputational costs nor domestic political benefits are constant across countries and over time. Political elites and entrepreneurs can intentionally politicise international agreements and organisations and raise their salience in domestic discourse to foster political benefits of exit (Heinkelmann-Wild et al., 2025; Rixen and Zangl, 2013; Vries et al., 2021; Zürn, 2014). Likewise, international reputational costs vary across states (Brutger and Kertzer, 2018; Downs and Jones, 2002; Sartori, 2002). If states have poor reputations to begin with, the additional damage done by exit is unlikely to prevent their governments from pursuing domestic political benefits through exit. Variation between and over time in governments’ perceptions of domestic political benefits and international reputational costs of international treaty politics can therefore explain the diverse strategies in which governments choose to address their international commitments and their timing.

Once the initial exit has been conducted, the two factors of continued cooperative gains and minimised reputational damage can improve the chances of achieving new, improved terms with the former partners. If the exiting state and the partner state would leave gains to the table by allowing permanent collapse of the treaty-based cooperation, both parties have strong incentives to continue seeking a new compromise. Furthermore, the international reputational damage can be mitigated via skilful diplomacy and communication: if the exiting government expresses its willingness to continue the partnership, the partners are more likely to take seriously its concerns and not presume general hostility towards the partner or the policy area. Afterall, renegotiations are more likely to be successful among likeminded parties renegotiating in good faith (Castle, 2023).

It is therefore a misperception that dissatisfaction with international agreements or populist forces alone can explain treaty exit. Neither can possibility of profit from business relationships nor diplomacy alone predict the success of future negotiations. Instead, governments must carefully balance between the costs and benefits resulting from both international and domestic sources when choosing whether to exit from international agreements.

Conclusion

This research has investigated the possibility of unilateral exit from international investment agreements as a strategic tool to achieve successful renegotiations. By examining the decision-making by two governments, Ecuador and Indonesia, the processes of exit and renegotiation reveal promising theoretical insights for explaining why governments might choose to exit rather than attempt to renegotiate international agreements. Furthermore, the study reveals that exit is costly even when it can result in domestic political gains, and the success of new negotiations with the same partners are not a given.

The insights from the study focusing on strategic exit in investment agreements can possibly generalise to other international negotiations, with important scope conditions. The possible benefits for political gain and international reputational costs are likely always present when considering exit from international agreements. However, their extent will likely differ depending on the salience and politicisation of the related issues in different countries. While BIT politics helps with identification of clear winners and losers of status quo agreements along a single-issue dimension, in many multi-issue or multilateral negotiations the isolation of dissatisfied and disadvantaged parties complicates renegotiation dynamics. Importantly, the foundations of BIT politics are particularly asymmetric, and in more balanced agreements, strategic exit may not provide sufficient benefits for catalysing renegotiations proportional to its costs.

BITs are a hard case for examining the role of the domestic political logic. Because political elites were able to politicise the highly technical investment treaty context and bring it to the public domain, it is likely that exits and renegotiations in other well-known cooperation issues such as the environment or trade also manifest similar dynamics. Since cooperative benefits continue to exist in multiple areas of global governance, possibility of exits to turn into new future agreements cannot be excluded despite reputational costs. Future research on international negotiations can therefore investigate, whether the theoretical insights put forward in this research generalise also to other areas of international cooperation.

The question of strategic benefit of exit for adjusting terms of international cooperation are highly salient at a time when many countries are threatening exit from international organisations while citing unfair practices and uneven distribution of responsibilities (Heinkelmann-Wild, 2026; Panke et al., 2025). The findings of the study, however, show that states may also resort to strategies that may seem uncooperative even when their preferences might be to renegotiate. Considering all treaty exits alike can mask different motivations of exiting governments, distinguishing between exit as regime withdrawal and exit as a negotiation strategy can help us to characterise the extent and nature of challenges to liberal international rules-based order (Lake et al., 2021). By providing more opportunities for dissatisfied states to adjust the terms of cooperation within existing regimes, there is an opportunity to limit the use of the more disruptive strategies such as exit.

Often the study of international negotiations only focuses on bargaining: how much leverage each party has, and the ability of that leverage to achieve favourable negotiation outcomes. However, leverage alone cannot achieve successful renegotiation of an agreement in the absence of skilful diplomacy and communication. While signaling hostility towards the basic principles of international regimes can alienate partners and shut doors to future negotiations, signaling of willingness to negotiate in good faith can help to strengthen international cooperation within the bounds of existing regimes.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has been generously supported by Osk. Huttunen Foundation, The Finnish Cultural Foundation, American-Scandinavian Foundation, and Nuffield College Oxford.