Abstract

We find that corporate access to the executive in the United Kingdom fails to deliver financial benefits to firms. We use two measures of access for the United Kingdom’s largest 2049 firms between 2013 and 2019: (1) all meetings between corporate representatives and ministers and (2) all state non-executive directorships held by the employees of those firms. Both meetings and non-executive directors (NEDs) skew dramatically towards a group of large firms that have regular access to government, overwhelmingly the Department of Business and the Treasury. Once we correct for endogeneity, we show that various versions of the NED and meeting measures are not consistently associated with seven financial outcomes. By contrast, using a matching exercise, we observe that elite firms with giant market values and weekly interactions with the government gain relative to peers. Since so few corporate executives get regular access to government, their occasional meetings may serve to aid policymaking without distorting it or distracting noticeably from a business leader’s principal duties.

Introduction: Are meetings worth it?

Is access to ministers worth it? Would business executives be better off attending to their companies instead of chatting about policy with politicians? If executives accept a position on a state board, does it benefit their commercial employer? Can the value of access be isolated and calculated? In this paper, we find that access to the UK government does not deliver substantial benefits to companies. This applies to both meetings with ministers and directorships in executive bodies. This null finding applies to the average firm in our dataset after we account for possible endogeneity in the relationship between access and financial performance. By contrast, we provide suggestive evidence that access gives an edge over less-connected peers to elite firms with large stock market values and previous, regular access to senior politicians.

Previous contributions have tended to concentrate on access to legislatures (Aizenberg and Hanegraaff, 2020: 182; Chaqués-Bonafont and Muñoz Márquez, 2016; Cross et al., 2021; De Bruycker, 2025) and/or sample surveys (Hansen and Rødland, 2025), with the important exception of a study of visitors to the White House (Brown and Huang, 2020). In the UK context, an emerging literature on access (Alonso and Andrews, 2022; Andrews and Fahey, 2025; Barbakadze, 2024; Dommett et al., 2017; McKay and Wozniak, 2020) has not yet studied how multiple types of access impact firm performance. We present a population study of access to the UK executive from 2013 to 2019. We study all meetings between the 2049 largest publicly traded firms in the United Kingdom and government ministers, as well as all appointments of their staff to central-government and state-agency boards. We show that both forms of access fail to deliver value across a range of seven financial outcomes, although it may be useful for some large firms. Descriptively, we demonstrate a symbiosis between some firms and the state: meetings are so frequent and non-executive directors (NEDs) are so numerous that these firms are intertwined with the UK executive.

We begin by placing our work in the context of the access literature, with a particular emphasis on the channels from access to financial benefits for firms. We begin our empirical section by reflecting on how access fits into the UK’s political system and how it is regulated there. Next, we report descriptive results, including discussions of the types of firms that get the most meetings, have staff represented on the most boards, and get the most private meetings, as well as the politicians and government departments that have held the most meetings with business representatives. Then, we present two-stage least-squares (2SLS) models of access and seven distinct financial outcomes, where we fail to find a consistent relationship between the two. We further employ a matching exercise which suggests that access does provide a financial advantage for elite firms. Finally, we conclude with implications for the potential for comparative studies and further work on the United Kingdom.

Access and corporate gains

Our work is located at the intersection of three sometimes overlapping, but often separate, literatures, rooted originally in public administration, economics, and political science. In public administration research, good governance is often associated with stakeholder consultation, which legitimises (Braun and Busuioc, 2020; Brummel, 2025; Bunea and Lipcean, 2024) and potentially improves public policy and regulation (May, 1992). Viewed through this lens, corporate access to the executive is a good thing. By contrast, the political economy literature on the gains to politics tends to regard corporate access as rent seeking. It originally neglected process to focus on the association between offices and connections and financial outcomes (Fisman, 2001). Later research in finance and political science used reported lobbying expenditures to explain financial outcomes (Alexander et al., 2009; Hill et al., 2013; Kelleher et al., 2009). Recently, a handful of works have tested the impact of access on firm performance more directly (Alonso and Andrews, 2022; Andrews and Fahey, 2025; Chalmers and Macedo, 2021). Political science has tended to adopt a more agnostic view on the merits of corporate access. Access is generally understood as part of an exchange between policymakers and lobbying actors (Halpin and Fraussen, 2017), such as policy reforms for campaign finance (Claessens et al., 2008; Liang and Renneboog, 2017) or a legislative subsidy between like-minded politicians and firms (Hall and Deardorff, 2006). It tends to be studied as a dependent variable and/or as part of a process (Coen et al., 2021). In what follows, we draw on elements of all three. From public administration, we incorporate the concept of legitimacy into our theory and we focus on a governance innovation, the boards to which independent businesspeople are appointed. From economics, we take the concern with financial outcomes and how to infer them. From political science, we embrace access as a key concept that connects process and outcome.

The financial benefit from lobbying depends on the political outcome, which, in turn, depends on the who, what, where, and how of the lobbying. Who relates to the lobbying actor; what is the aim of the lobbying actor; where is the access; and how adept is the political craft of the lobbying actor. We do not discuss this last term. Instead, our analysis assumes a reasonably high level of realism and competence. The following informal equation represents our theory of the process connecting corporate access to financial benefits:

We begin by considering the political outcomes and related financial benefits of corporate lobbying. There are three basic sorts of goods for which firms lobby. First, there is information. A better understanding or advance warning of policy and implementation can give a firm an advantage over its competitors. Second, there is the policy itself. Minor variations in policy can be enormously beneficial or damaging for firms. Firms can influence policy by shaping policymakers’ understanding of the policy area through the provision of information on how the firm does business and how policy affects it. Policies generally affect classes of firms, often very large ones, but sometimes they can be so specific that they only matter to a handful of firms or even just one. Third, and finally, there are government contracts, in which the government becomes a customer of the firm. The three outcomes vary in respect of how easy they are to study. Information exchanges are hard to observe. Although official consultations, especially with legislatures, can be studied, we cannot know what is said in private meetings. Policy changes can be observed, but given the complexity of the policy process, it is difficult to associate them with lobbying without very intense qualitative research, which cannot be done for a large sample like ours. Governments provide data on public procurement, but this represents only a small proportion of the state’s overall effect on business.

Each of these political outcomes is associated with financial benefits for the firm. Nevertheless, the extent to which they are translated into financial benefits depends on whether the firm has correctly calculated the relationship between their business and the political outcome and a host of other factors outside their control. For example, a firm could lose money fulfilling a government contract because of an increase in the cost of inputs provided by other entities. There is a range of indicators of financial success for a firm. Most obviously, there are profits, both before, and after, tax. The indicator most directly linked to the state is the amount of tax paid. Capital efficiency matters: how much money does the firm make relative to its capital? Turnover, the amount of money moving through the firm, can be seen as a performance indicator, independent of profits. Finally, the market capitalisation indicates the present value of the firm, which, crucially, takes into account predictions of its future profits. We calculate the extent to which firms benefit across this range of financial outcomes, regardless of through which political good they were produced.

We now turn to ‘where’, the access itself. We will adopt a slightly modified, wider version of a useful definition of access (Binderkrantz et al., 2017), by replacing ‘group’ with ‘actor’ and ‘arena’ with ‘venue’. ‘Group’ and ‘arena’ reflect the literature’s tendency to study interest groups and legislatures. The revised definition of access is: Instances where an actor has entered a political venue passing a threshold controlled by relevant gatekeepers.

It is often assumed that the more access a lobbying actor has the better, but it may be the quality of the access really counts. We define quality of access as the opportunity afforded to the firm to gain benefits from the interaction. Much of the quality of access can be understood by an interaction of the privacy of the meeting and the power of the decision-maker:

The privacy of venues varies enormously. Legislative meetings are public in their content and who attends. Executive meetings tend to report who is present but not what was said. Meetings with politicians outside representative bodies tend to be more or less secret: there is no legal obligation to report who was there; what was said; or that the meeting even happened. The power of political interlocutors also varies enormously. Ministers tend to be more powerful than legislators. Party politicians are often indirectly powerful: they can act as brokers between lobbyists and decision-makers.

Finally, there is ‘who’. The actor’s characteristics comprise the structural power, informational resources, legitimacy, and the decision-maker’s obligation towards the actor. Structural power is a function of the impact of a firm’s decisions on the wider economy and its sensitivity to political choices (Lindblom, 1977). By contrast, the other three characteristics are contextual and can vary radically from one venue to another. Therefore, we will discuss how a lobbying actor’s informational, legitimacy, and social obligation resources can vary across venues.

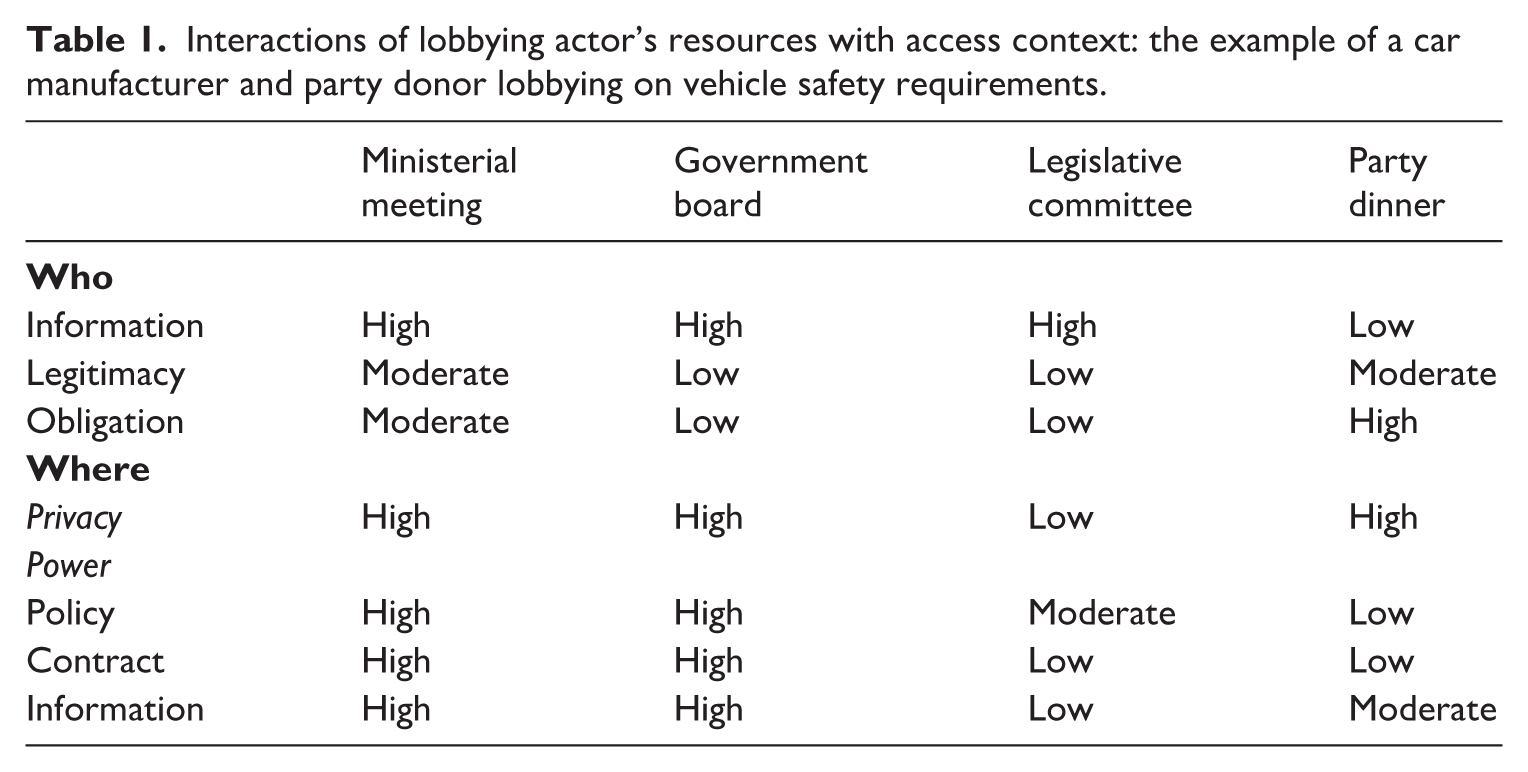

We take the hypothetical example of a car manufacturer and donor to the governing party lobbying in four different venues. In a meeting with the relevant minister, the decision-maker’s need for technical information from the manufacturer is very high. This is an instance of the frequent informational asymmetry between business and government (Bernhagen, 2007). Firms do not vote, so it is difficult to think of them as ever highly legitimate in a democratic system, but, in this context, where politics is ‘quiet’ (Culpepper, 2010), the minister should see them as legitimate actors, since the firm will have to implement any changes to the law. In her capacity as a minister, the politician does not, and should not, feel any obligation towards the firm. However, as a party politician, she will be aware that the firm is, or potentially is, a donor. If an employee of the firm sits on a government or corporatist board, the state’s need for information will again be high. However, the legitimacy of the firm employee to lobby for their firm’s interest and the state’s obligation towards the firm will both be very low. A variety of interests will be present and the purpose of the meeting will be to make or implement policy for a sector, not to entertain narrow lobbying. If the same firm appears before a legislative committee, the need for its information will again be high. Its legitimacy will be low, since the politics of a legislative committee hearing is noisier than the executive, with many stakeholders to hear, consider, and placate, as well as the possibility of media coverage and an increase in political salience. The obligation towards the donor will be low, even, or maybe especially, for politicians from the party the firm supports. When politics happens in the open, it is particularly important to be seen to value citizens’ votes over donors’ pounds. Our last example is where a firm representative attends a party dinner and the need for information is low, partly because the politicians present will be in no position to process technical information, and partly due to the inappropriate nature of the venue. The legitimacy of the firm will be moderate: their invitation to the dinner is an acknowledgement of their legitimacy as a supporter of the party that can expect an opportunity to talk about policy. Finally, the obligation towards the firm is high in this context. The party is the recipient of the donation and must be seen to consider the donor’s position.

The venues vary in their potential to deliver the three types of political outcome. The ministerial meeting is private and the decision-maker is very powerful in relation to information, policy, and procurement. Similarly, a government or corporatist committee will often have important information, as well as an influence over policy and procurement. The legislative committee meeting is shared with many other stakeholders and is reported openly, while the committee may only have a moderate impact on the final legislation. The legislative committee has little inside or advance information to share with the firm and it has no role in awarding public contracts, although it may oversee their implementation. Finally, at the party dinner, the donor’s representative is unlikely to be sitting beside somebody with any direct influence over decisions. Instead, this is perhaps an opportunity to connect with a broker, who can then arrange a meeting with the minister or somebody else who has valuable information, control over a decision, or a role in public procurement. This interaction of the who and the where is summarised in Table 1.

Interactions of lobbying actor’s resources with access context: the example of a car manufacturer and party donor lobbying on vehicle safety requirements.

We also need to discuss the quantity of access. The relationship between the amount of access and lobbying success is understudied. Most work assumes a linear relationship: another meeting increases the chance of success by the same amount regardless of whether it is the actor’s first or hundredth meeting. The large literature on insiders and outsiders implies that another meeting matters little for insiders: those who already enjoy a lot of access will not improve their outcomes by gaining more access. By contrast, there is a threshold that transforms an outsider into an insider and delivers substantial benefits. The signalling theory holds that most of the gains from access are won by moving from no access to a little access. Valuable information for policymakers is communicated in the first meeting; thereafter actors have little to offer the decision-makers and there are no gains to further meetings (Berkhout et al., 2025).

We have discussed the micro level at some length. The meso level relates to particular policy areas or policy communities. In the context of business, the meso level is usually defined by sector, which we will control for in our equations and account for in more detail in a matching exercise. The macro level is the political system and we turn to it next.

Access to the UK executive

We study the famously powerful executive of the United Kingdom. The cabinet is the apex of the executive, with relatively mild constraints from the judiciary, sub-national governments, and international institutions. It also controls the legislature, again with comparatively weak inputs from legislative committees, the upper house, and even backbench parliamentarians in the governing party. Since we focus on the United Kingdom and its executive, we therefore investigate a very different politics of access to the frequently researched legislatures of the European Union (Chalmers, 2014; De Bruycker, 2025) and the United States.

The United Kingdom is a low corruption context, notwithstanding a series of recent alarming developments (David-Barrett, 2022). Corporate donations are legal and unlimited, but, due to good corruption control, inexpensive politics (Fisher, 2000), the transparency of donations, and obligation to periodically obtain shareholder approval to make political donations, any exchanges between politicians and those seeking access need to be subtle (McMenamin and Power, 2023). Golden parachutes are likely to be the main material benefit politicians can expect (Eggers and Hainmueller, 2009; Weschle, 2022). Nevertheless, the sale of access to the UK executive has been embedded in the political system for many decades. The most direct channel is to make a very large donation to a party in return for a private meeting with a minister, or even the prime minister. This is a channel managed by party fundraisers, loyal to the leader, and, therefore, outside the party’s bureaucracy, never mind the government. 1 A less direct channel is for party donors to seek an official meeting with government. Notwithstanding the sale of access, the largest firms in the United Kingdom, which we study, rarely donate to political parties or candidates (De La Torre et al., 2025; McMenamin, 2011: 1032).

The UK lobbying legislation is ‘medium-robust’ (Chari et al., 2020; Keeling et al., 2017). Consultant lobbyists, that is, those who lobby on behalf of others, have to register and provide client lists, but actors lobbying on their own behalf do not. All meetings between UK ministers and outside interests are reported on government websites (Dommett et al., 2017; McKay and Wozniak, 2020). There have been 76,495 meetings between 2012 and 2020. Ministers are not required to report all their meetings, only all their meetings in their official capacity as ministers. So, the list undoubtedly omits where a minister meets actors from outside government in their capacity as party politicians: in one notorious formulation, ‘You’d be meeting David Cameron, not the prime minister’ (Boffey and Siddique, 2012). Only meetings with the very top decision-makers are reported. Ministerial special advisers and senior civil servants do not report their meetings. This may be why many registered consultant lobbyists do not appear to meet ministers (McKay and Wozniak, 2020: 113). Notwithstanding its limitations, the meetings’ data provide an unusually detailed and comprehensive source on access to the apex of an executive. Furthermore, this represents a conservative test of the effects of access on firm performance; were data of more ‘private’ meetings made available, we anticipate finding larger effects. In a study of procurement in the UK defence industry, Andrews and Fahey (2025), show that meetings were associated with greater contract value. Barbakadze (2024) argues that meetings with UK ministers can reduce political risk for firms under some conditions. We see these results as examples of the interactions in our informal model explaining the outcome of lobbying. These scholars study two of the three main types of benefit from access: Alonso and Andrews focus on government contracts and Barbakadze targets information.

The classic lobbying exchange consists of policymakers collecting information from firms to make better policy, while firms get an insight into likely policy developments and have a chance to shape policymakers’ view of policy choices. This means that valuable access is not necessarily just provided when firms meet a minister. Equally, there may be opportunities for firms when they are invited to join the policymaking system itself. The United Kingdom is anything but corporatist, but since 2010, a governance innovation has brought businesspeople into agencies and government departments as Non-Executive Directors, or NEDs. These individuals are therefore legally committed to work for the interests of the government entity to which they are appointed, but these positions pose an opportunity to pursue the interests of their sector and/or firm. Brown and Huang (2020: 424) include meetings with executives on ‘advisory boards’ in their study of the US White House. These are traditional consultative boards, rather than a role within the executive itself, like the British NEDs (Andrews and Fahey, 2025). Likewise, the NEDs are not stakeholders.

We can measure the quality and quantity of access via ministerial meetings and NEDs. Meetings are more straightforward, since each provides access to a minister. We guess this is for a period of at least half an hour for each meeting. Meetings can be private, in the sense that no outside actor is present other than the firm. They can also be collective: ministers can meet a number of firms and/or other outside actors. Each outside actor is recorded, so we have an excellent measure of the privacy of meetings.

The quantity and quality of access provided by NEDs is less certain. Ministerial boards are supposed to meet at least four times a year and NEDs are also supposed to have personal access to the minister. If a board meeting takes at least 2 hours and there are four a year as recommended (Cheshire, 2020: 12) and there are two other high-level access opportunities, one NED would get 10 hours of access every year. An advertisement for a lead NED in the Foreign, Commonwealth and Development Office stipulated 20 days of work per annum. Of course, the amount of access could, and undoubtedly is, often much lower or much higher. NEDs are more likely to provide collective access, most obviously at a board meeting where other NEDs and a range of departmental leaders and stakeholders will be present. NEDs of central ministries have access to the most important decision-makers in the realm, but NEDs of agencies may be working with people who implement policy, rather than formulate it. Whereas it is legitimate and, presumably, more or less expected, for a firm to pursue its own interests in a meeting, it is not legitimate for a NED to do so. The NEDs are appointed to contribute to the mission of the ministry or agency, not to represent their own firm. To the extent that a firm NED does so, she must be subtle.

This means it is difficult to directly compare the regression coefficients for meetings and NEDs. A NED refers to a much greater amount of access than a single meeting. A private, one-on-one meeting should provide much higher quality access than a NED and a meeting with tens of outside interests should provide much lower quality access than a NED. Meetings often provide an opportunity to lobby; whereas a NED cannot do so openly. Nevertheless, Andrews and Fahey (2025) find that more NEDs are associated with financial benefits for UK firms. In particular, they report greater benefits for larger firms across a range of indicators, but, crucially, at the expense of profitability.

Our next section begins by describing how we gathered data on meetings and NEDs and merged both sources with financial data on firms. We measure many of the concepts from our theoretical discussion: the financial benefit of access, the quality and quantity of two forms of access, and controls for the characteristics of the lobbying actor and their sector. We hold the macro context constant and note that the low corruption, comparatively inexpensive political finance, high press freedom, and high visibility of ministers means this is a conservative test of access: its actual benefits are likely to be higher, rather than lower, than our estimates. We do not measure the craft or the specific aims of the lobbying actor, but it is reasonable to assume a high level of competence and realism among the largest firms in the United Kingdom.

Data and operational hypotheses

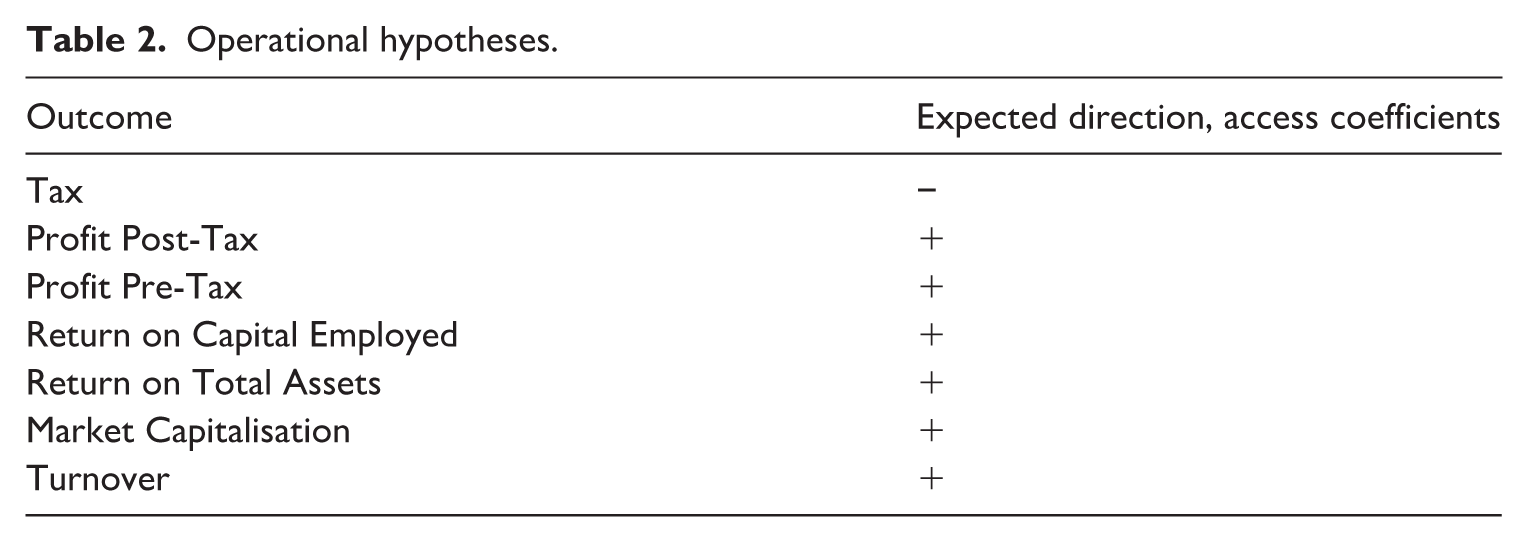

We include our set of hypotheses in Table 2. We anticipate that all of our outcomes – save tax – should be positively associated with access. With tax, we anticipate that more access should result in lower tax.

Operational hypotheses.

We combine a series of datasets including firm-level performance indicators, the number of firm executives who sit on government boards as NEDs (Andrews and Fahey, 2025), the number of meetings that firms held with government ministers, and firm-level indicators from the FAME database. In total, our estimates are derived from an imbalanced panel of 2049 firms from 2013 to 2019. 2 Given the massive increase in reported meetings due to the Covid pandemic and the extraordinary context, we exclude data from 2020 onwards.

We employ seven standard firm-level performance indicators: annual tax paid, post- and pre-tax profits, return on total assets (ROTA), return on capital employed (ROCE), market capitalisation, and turnover. We benchmark changes in market capitalisation against changes in the average value of the whole FTSE (Hill et al., 2013: 943). All seven of these firm-level indicators are transformed twice: first, by standardising within-year using z-score normalisation, and second using the inverse hyperbolic sine transformation to satisfy the assumption of linearity in the parameters (Carboni, 2012). 3 The use of seven dependent variables effectively mainstreams robustness, instead of presenting a relatively weak argument for the priority of one dependent variable and privileging that in our presentation.

We obtain raw-level counts of two firm-level variables as our primary predictors: the number of meetings the firm has held with government ministers and the number of firm executives employed as NEDs in government departments and agencies. 4 Before aggregation to the firm-year, meetings and NEDs are coded as dyads. For example, if both Vodafone and Virgin Media are in a single meeting with the Secretary of State for Business and Trade, we record two separate observations with a common, meeting-level identifier. Similarly, if a firm has executives ensconced as NEDs in two government departments or agencies, we record two separate firm-year observations. There were 19,156 firm-minister dyads and 3018 firm-years where the firm had at least one meeting with a minister. Furthermore, we record 10,042 firm-year NEDs, and 3485 firm-years where the firm had at least one NED.

Unlike meetings, which remained fairly constant throughout the studied time period, firms with NEDs increased from approximately 200 firms in 2013 to just under 275 firms by 2019.

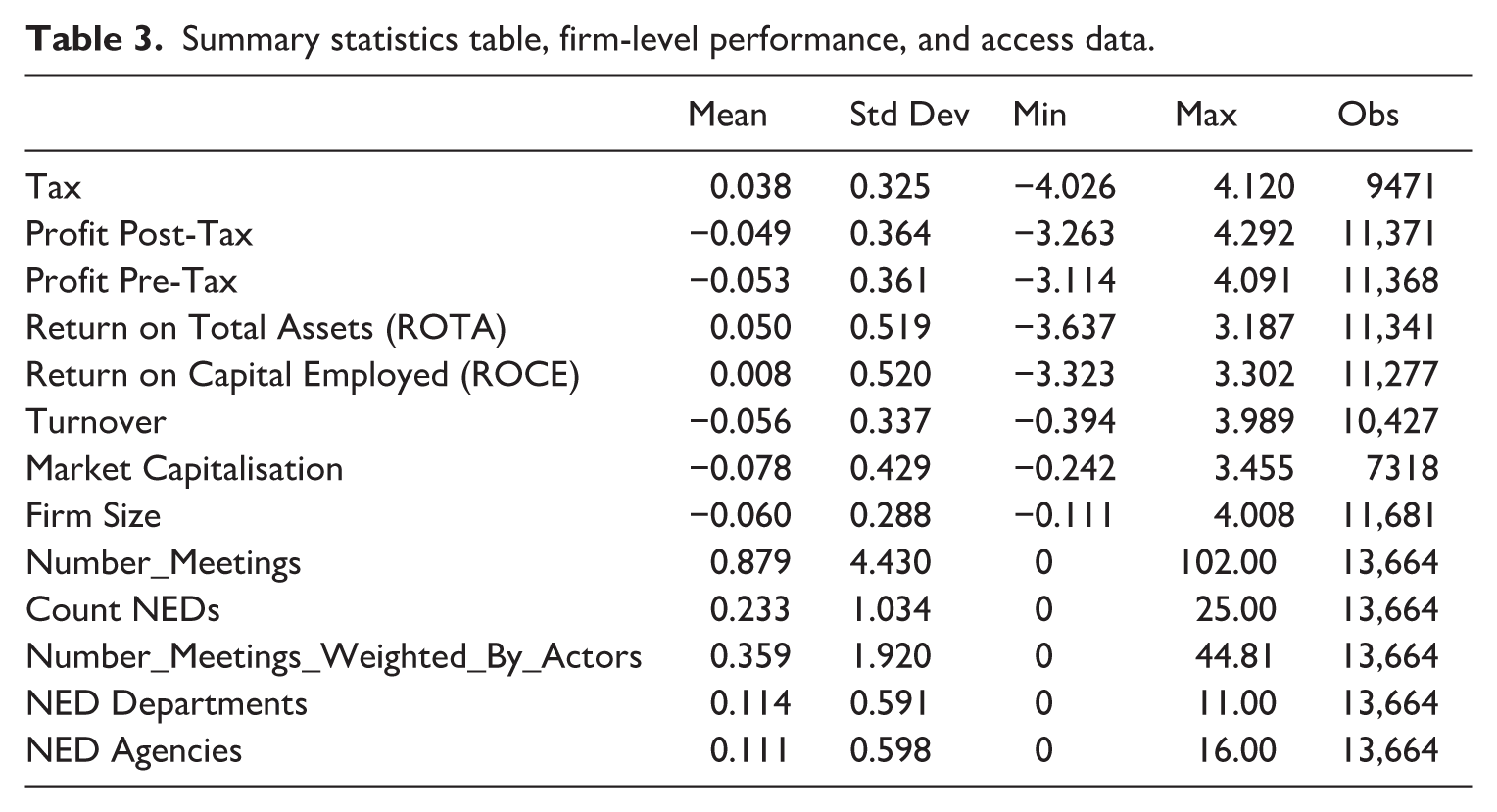

Our measures of access quality are as follows. First, each meeting is divided by the number of outside firm actors present; we then calculate firm-year meeting quality as the mean of this statistic for all meetings in a given year. 5 We measure the quality of NEDs by calculating the proportion of firm-year NEDs in government departments versus government agencies. We include three firm-level control covariates: whether the firm was a member of the FTSE 100 class of publicly traded companies, the age of the firm, 6 and the size of the firm. To account for sectors of the economy that over- or under-perform other sectors, or in individual year over- or under-performance of the economy, we include sector and year fixed effects in all models. Please see Table 3 for summary statistics and the Supplemental Appendix for a discussion of the distributions of our variables.

Summary statistics table, firm-level performance, and access data.

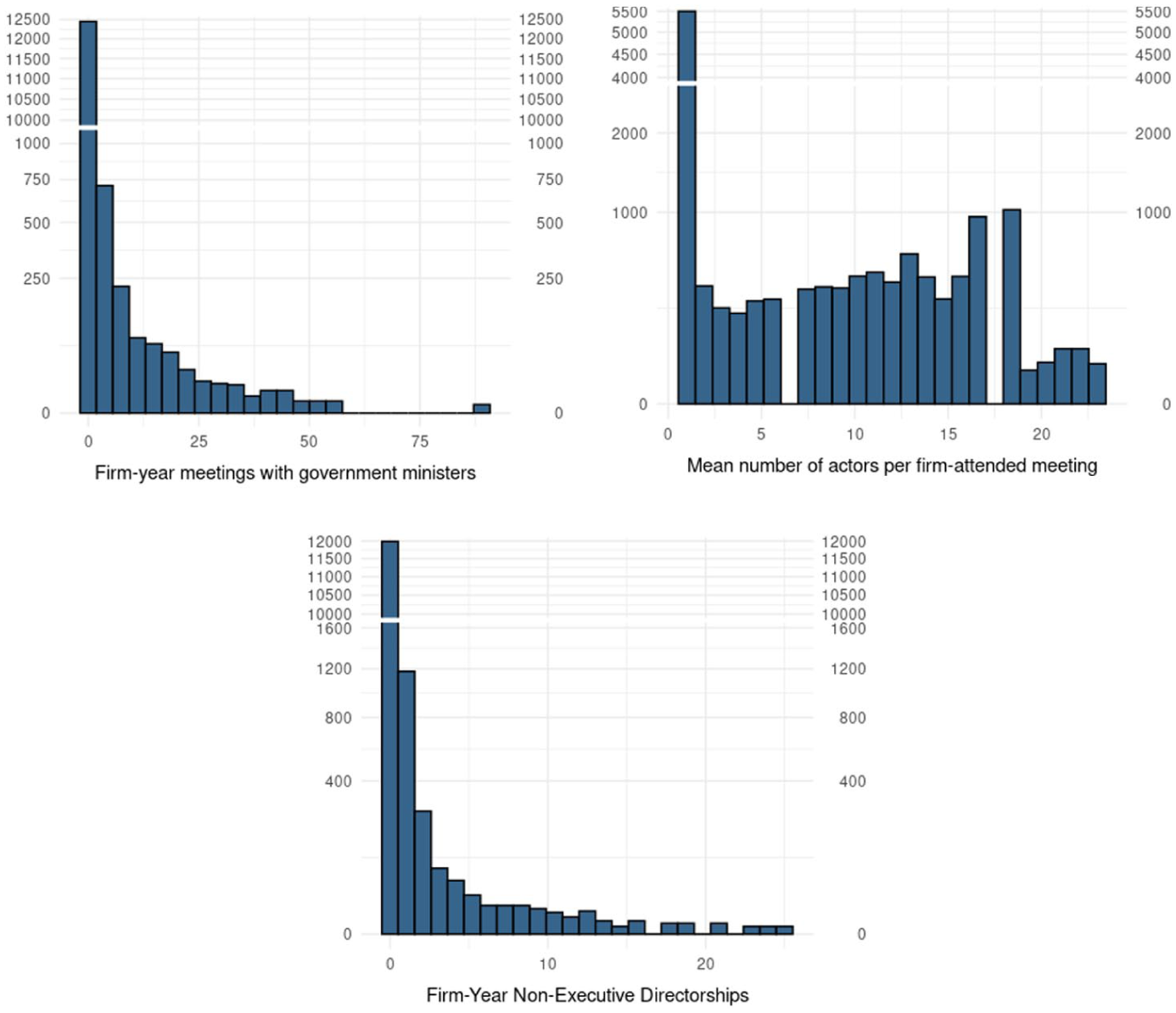

We report the distribution of firm meetings per year, the number of actors per meeting, and the number of NEDs per year in Figure 1. There are a lot of meetings, almost one per firm per year. However, the distribution follows a power law: approximately 80% of firms do not have a meeting in a given year and 1472, or approximately 70%, had no meeting in the 7-year period we study. By contrast, the maximum is over 100: over two meetings a week with ministers. While there are many private meetings, the average meeting contains more than one representative of a company. Like the distribution of meetings, the distribution of NEDs follows a power law. As with meetings, approximately 80% of firms did not have a NED in a given year. Nearly 75% – 1642 – had no NED across the 7 years. A couple of firms averaged over 20 NEDs a year, such as PricewaterhouseCoopers and KPMG, a remarkable contribution by a private company to the political executive. Overall, we can see that many large firms have no access; some have occasional access; others have regular access; and a handful that actually seem to be part of the government itself.

Histograms, access variables.

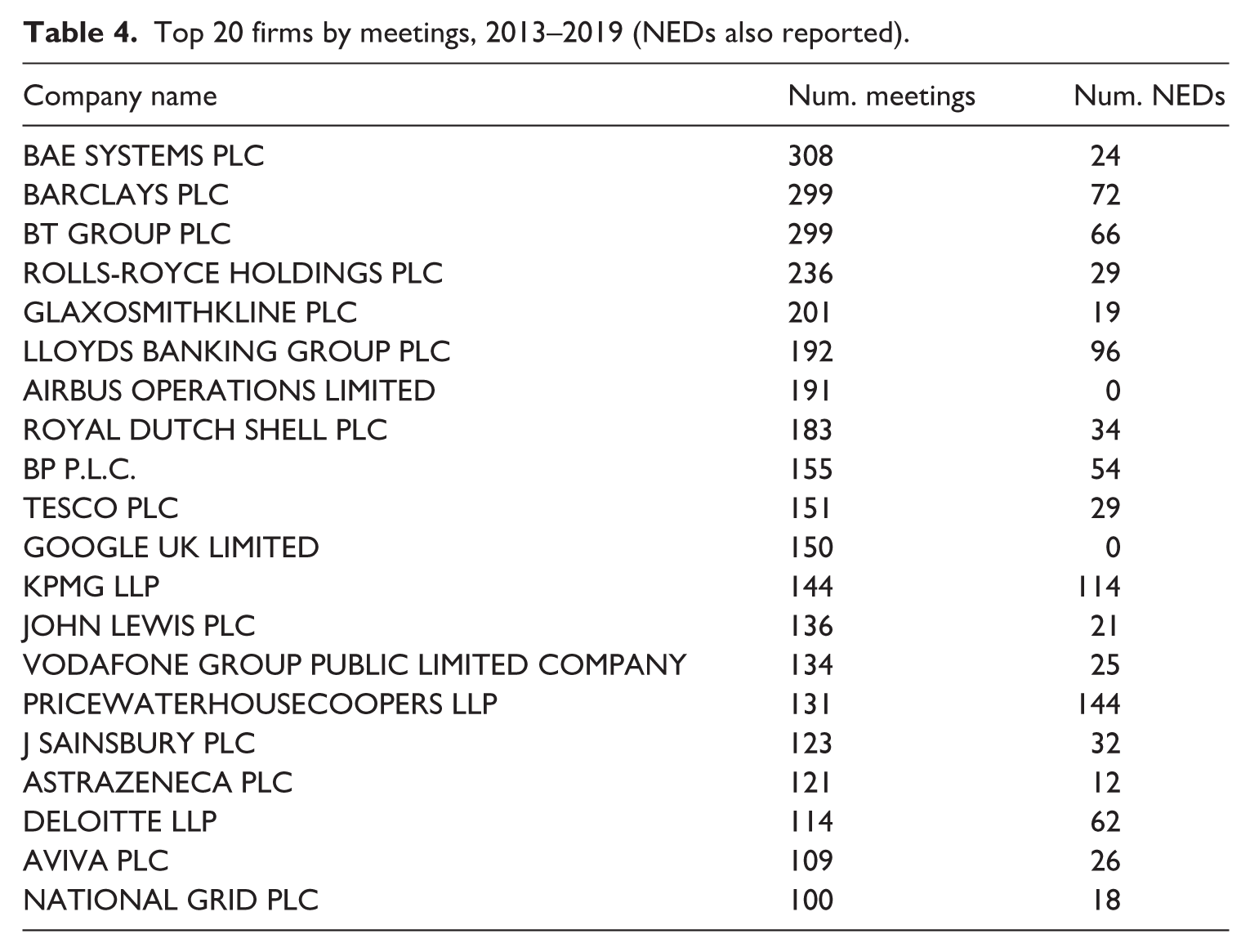

We now proceed, in Table 4, to look at which companies have the most access to the UK’s executive. The maximum (BAE Systems) is over 300 across the 7-year time period, a tremendous frequency of meetings between government ministers and one firm. The functions of the defence firms (BAE, Rolls-Royce, and Airbus) and the national grid are very much entwined with those of the state. The other firms are in the sectors of oil (British Petroleum, Shell), technology (Google), finance (Barclays, Lloyds, Aviva) pharmaceuticals (Glaxo Smith Kline, AstraZeneca), retail (Tesco, Sainsbury, John Lewis), and telecommunications (Vodafone, British Telecom) that are usually regarded as belonging to the market, not the state. The professional services firms (Deloitte, Price Waterhouse Coopers, Klynveld, Peat, Marwick, and Goerdeler) may be a partial exception, in that they often have multiple consultancy contracts that support policymaking and policy-delivery. In this respect, it is relevant to note that KPMG and PWC have more NEDs than any other firm in this table.

Top 20 firms by meetings, 2013–2019 (NEDs also reported).

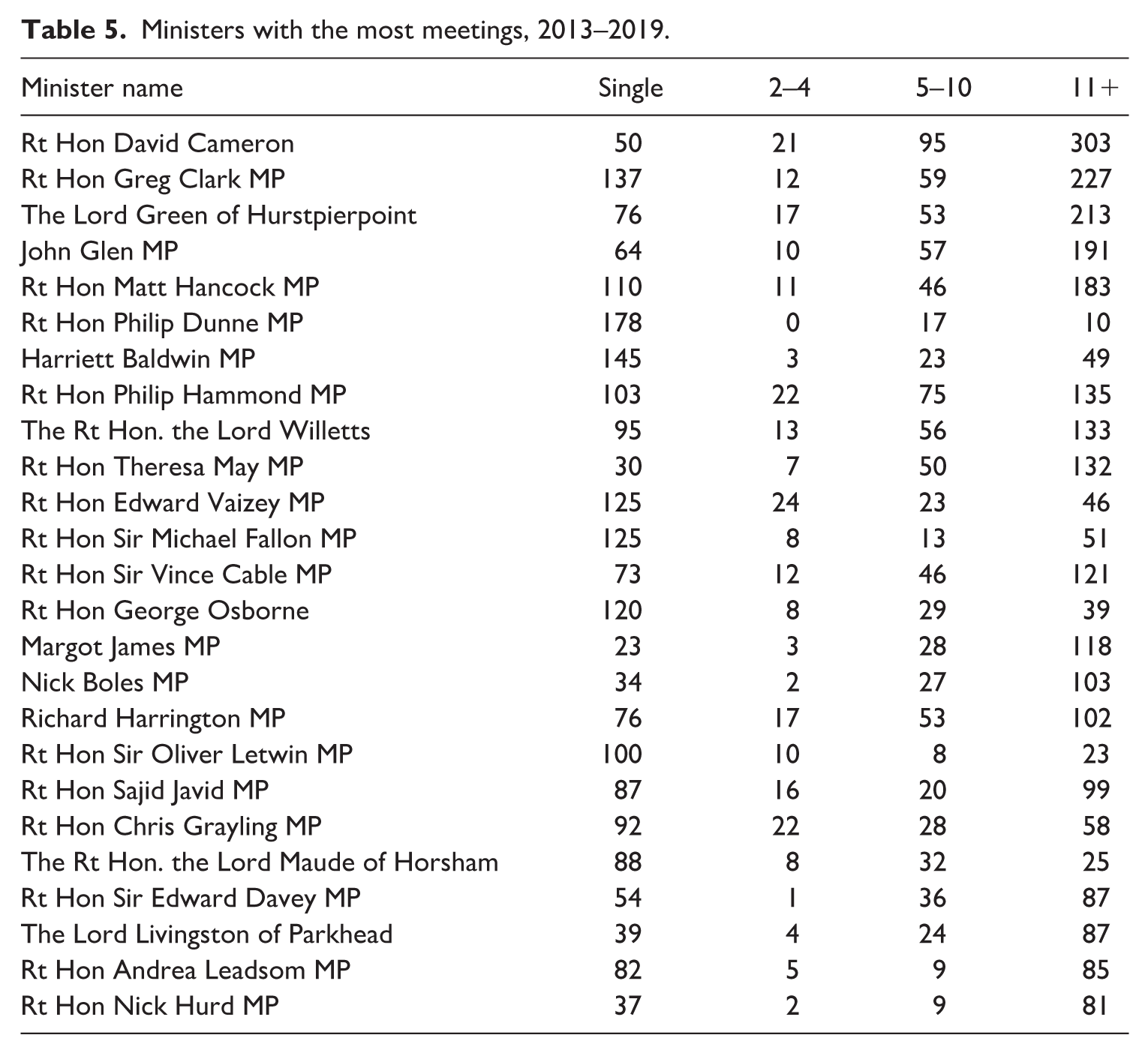

Table 5 looks at who the companies are talking to by listing the ministers who have the most meetings. Almost everybody in the list held a position at the department of business and most also had a background in big business, although the table is topped by David Cameron, who was the prime minister. For the top 25 ministers who took meetings with firms, 35% of these meetings are private, in that they involve one firm, plus the minister and civil servant. If there are five or more firms, there would not seem to be much opportunity to lobby for the interests of a particular firm, as opposed to a type of firm. Nevertheless, nearly 60% of these ‘high-access’ ministers took meetings with five or more firms present. Although the person with the most meetings is extremely well known, not so many will recognise the name of Philip Dunne, who held the most private meetings with firms. He was Minister for Defence Equipment, Support and Technology from 2012 to 2015 and Minister of State for Health from 2015 to 2018. Similarly, the woman with the most meetings is not former prime minister, Theresa May, but Harriet Baldwin, who was Parliamentary Under-Secretary of State for Defence Procurement from 2016 to 2018 and then Minister of State for Africa and Overseas Development from 2018 to 2019. The only Liberal Democrat on the list is former Business Secretary, Vince Cable. The procurement meetings would appear to be very obvious opportunities to lobby, but could also be instances where the government has summoned a firm, which is already providing defence equipment or services.

Ministers with the most meetings, 2013–2019.

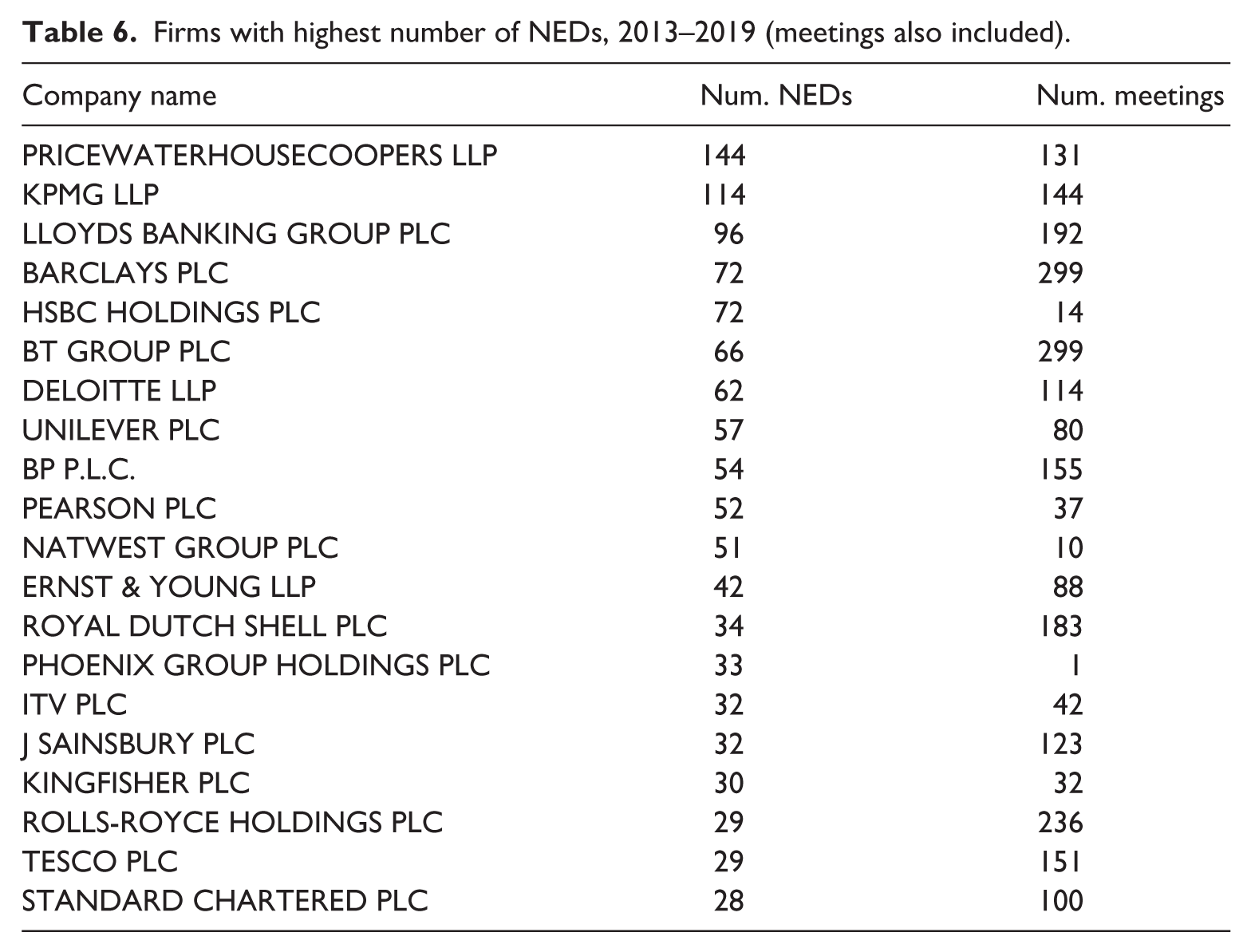

Table 6 lists the firms with the most NEDs. Unsurprisingly, there are some familiar names from Table 4. The predominance of professional services firms makes sense. Their staff are experts in governance and in transferring skills and experience across organisations. A similar functional argument might also be made for the employees of financial institutions and telecommunications companies. We are not sure why so many employees of a broadcaster (ITV), supermarkets (Sainsbury, Tesco, Kingfisher), and oil companies (BP, Shell) were selected to serve as NEDs. Perhaps it was encouraged for the professional development of senior executives or seen as a corporate social responsibility. Some companies did not feature on the list of those with most meetings: Unilever (consumer goods), Phoenix, Standard Chartered, HSBC, NatWest (finance), Pearson (publishing), and ITV (broadcast). Overall, the lists of companies with the most meetings and the most NEDs are similar. The NEDs list is somewhat less diverse, with two of the defence companies disappearing, as well as the telecommunications and pharmaceutical companies and the technology firm. Their replacements increased the proportion of finance firms represented.

Firms with highest number of NEDs, 2013–2019 (meetings also included).

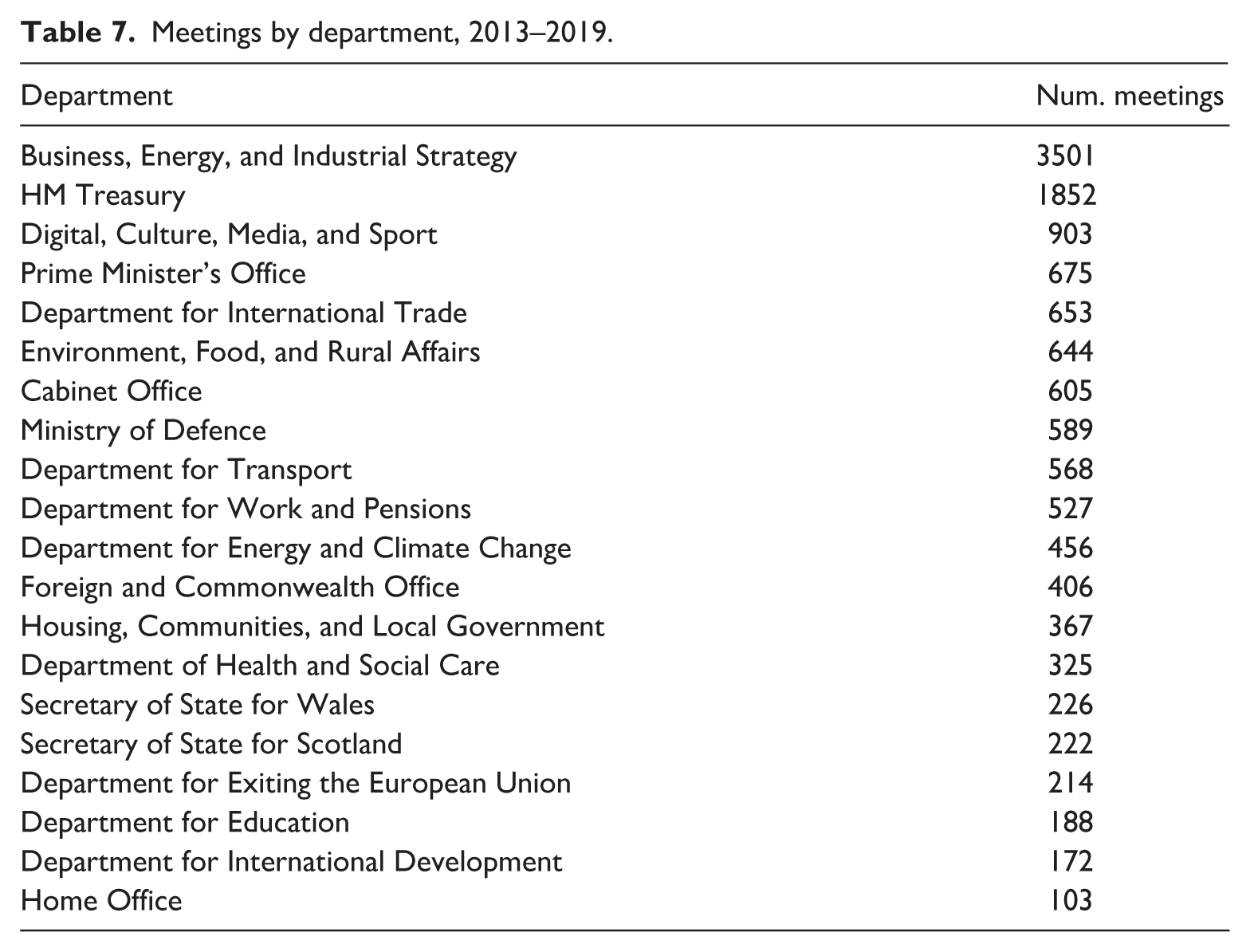

Table 7 shows the frequency of meetings by department. The list is unsurprising and reassuring. Firms are overwhelmingly meeting the department they are supposed to be meeting: the Department for Business, Energy & Industrial Strategy (or its equivalent). It currently has seven political executives: a secretary of state, two ministers, and four parliamentary under-secretaries of state. The total implies 16 meetings a week, which seems like a reasonable load spread across seven ministers. However, the workload for other departments, given that they are not primarily responsible for dealing with business, seems higher: the Treasury averages six meetings a week, the Prime Minister’s office two, and the Cabinet office also two.

Meetings by department, 2013–2019.

Analysis

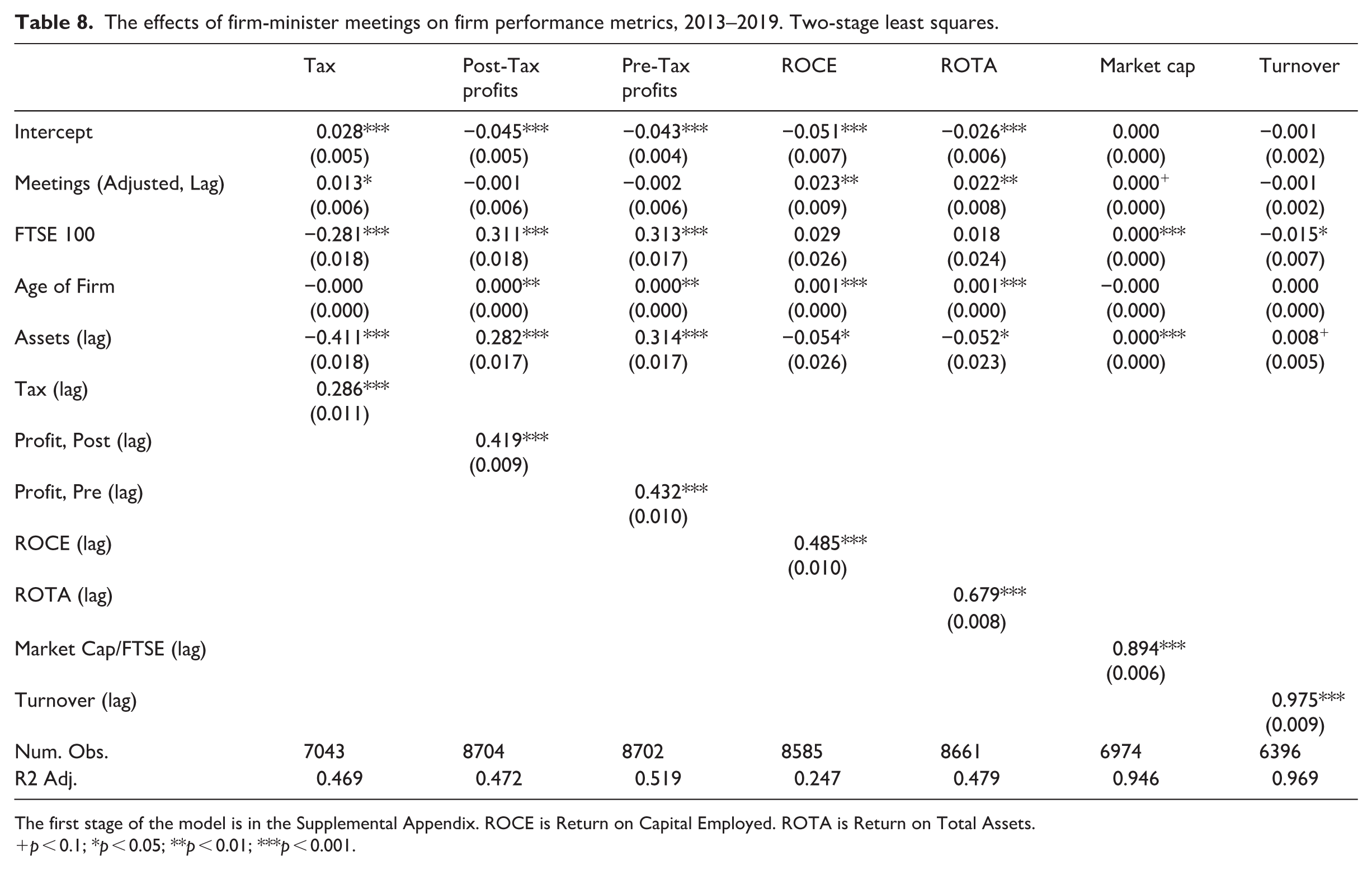

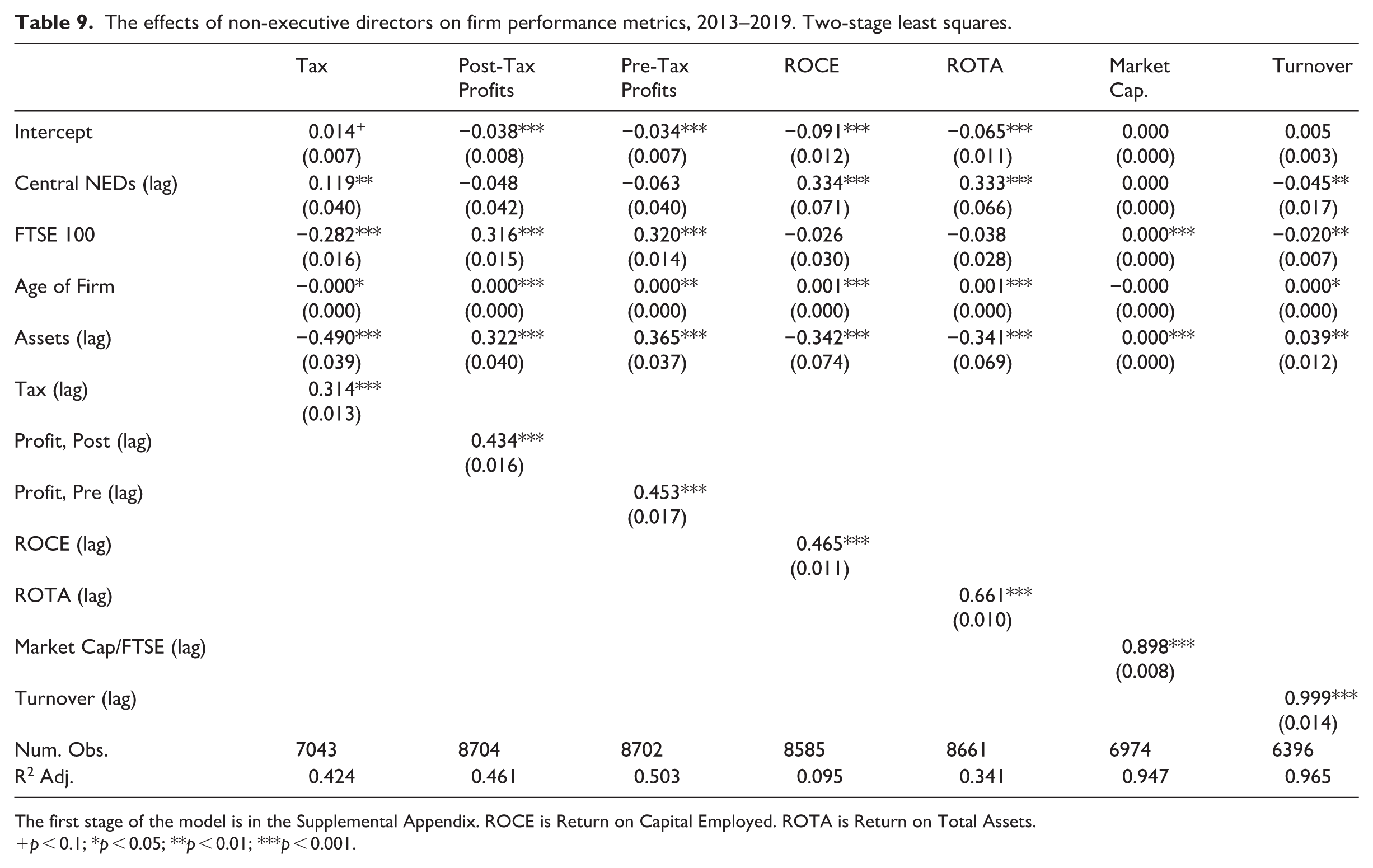

In order to correct for possible endogeneity, we employ a 2SLS approach. This works by separating exogenous and endogenous variation in the first stage, which regresses the number of meetings or NEDs against the number of meetings or NEDs at the sectoral level. Sectoral access is correlated with the access of firms in a given sector, but not with their financial performance (Chalmers and Macedo, 2021: 2001; Liang and Renneboog, 2017: 294–295). In the second stage, we estimate the effect of access on financial performance, net of the endogeneity stripped out in the first stage. There are sectoral and year fixed effects, and firm-clustered standard errors at both stages. We report estimated coefficients from 14 models: 7 where our chief measure of access is the number of meetings (lagged by 1 year), and 7 where our measure of access is the number of NEDs (again, lagged). Note that we rely on lagged measures of our predictors and our outcomes on the right-hand side of the equation, in order to account for several of the threats to inference from an imbalanced panel dataset. Recall from our hypotheses that we anticipate positive coefficients when the outcome variable is pre-tax profits, post-tax profits, return on capital expenditure (ROCE), return on total assets (ROTA), market capitalisation, and turnover, while we anticipate negative coefficients when the outcome variable is tax.

We report the second stage of two sets of models in Table 8 (Meetings) and Table 9 (NEDs). Year and sector effects are included but not shown. They are in the Supplemental Appendix, as is the first stage of the 2SLS. Meetings are associated with a higher tax burden and better ROCE and ROTA. There is also an association between meetings and market capitalisation, albeit not at the conventional 5% level of significance. There is no association between meetings and turnover or profits. NEDs are also associated with an increase in tax and improved ROCE and ROTA. They have no effect on market capitalisation or profits. Finally, NEDs are associated with a decrease in turnover. Out of 14 coefficients, only 4 are statistically significant in the predicted direction; 3 are significant in the opposite direction predicted, and 7 are insignificant. Given the lagged dependent variables, it is unsurprising that the proportion of variation explained is high, except for ROCE. The other financial controls make important contributions to explaining variation: 16 out of 21 coefficients are significant. In the Supplemental Appendix, we report six variations. First, we exclude potentially highly or statistically impactful observations. We calculate DFBeta – the influence of a single observation on regression coefficients – by calculating the difference between the coefficient estimated with all data, and the coefficient calculated when that observation is removed. Then we remove all observations exceeding the conventional threshold of 2/√N for both models when meetings are the outcome, and models when NEDs are the outcome. Second, we include NEDs and meetings in the same model. Third, we include the quality measure of meetings (meetings weighted by the inverse of business representatives present). Fourth, we add the quality measure of NEDs (a distinction between central-government and agency boards). Fifth, we combine NEDs and meetings into an access index (the average of standardised versions of both indicators). Overall, these models are consistent with the findings in Tables 8 and 9.

The effects of firm-minister meetings on firm performance metrics, 2013–2019. Two-stage least squares.

The first stage of the model is in the Supplemental Appendix. ROCE is Return on Capital Employed. ROTA is Return on Total Assets.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

The effects of non-executive directors on firm performance metrics, 2013–2019. Two-stage least squares.

The first stage of the model is in the Supplemental Appendix. ROCE is Return on Capital Employed. ROTA is Return on Total Assets.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

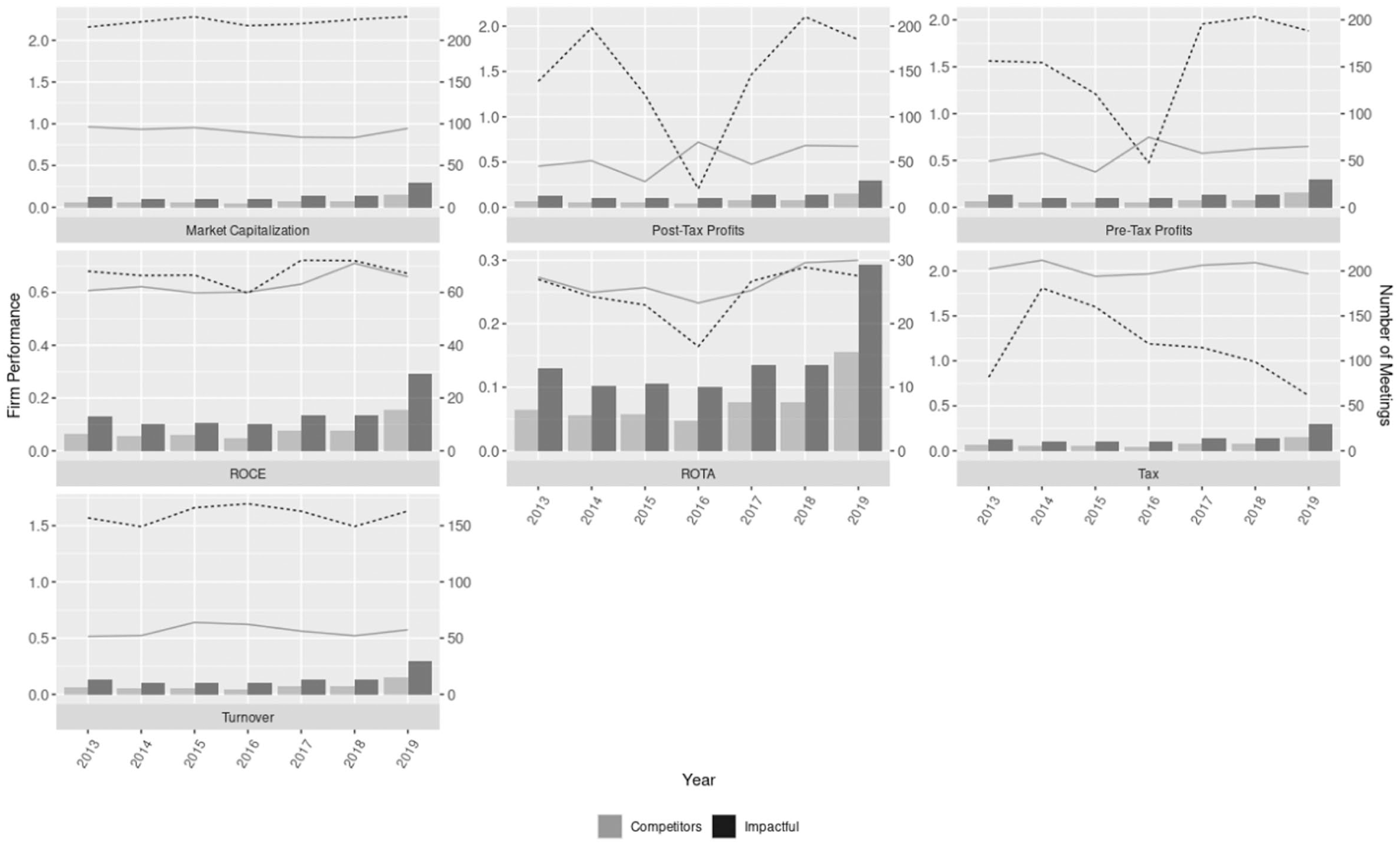

Our descriptive analysis showed that some firms have virtually daily access to the UK executive. We can explore some of these firms further by linking them to the quantitative models above. We noted which firms had statistically impactful observations (according to DFBETA) for each of the 7 years we study. We then identified firms in our sample that are relatively direct competitors; for example, PwC’s main competitors in the international auditing-and-consultancy market are Deloitte, KPMG, and Ernst & Young, the ‘Big Four’ of professional accounting firms. We truncate the sample to all such consistently impactful firms (

Relationships between statistically impactful firms with large numbers of meetings, and their competitors, 2013–2019.

The impactful firms have far more meetings in every year. They also have a superior financial performance across five of the seven indicators: market capitalisation, pre- and post-tax profits, tax, and turnover. There is no difference between their capital efficiency in terms of both Return on Total Assets and Return on Capital Employed. This is the opposite of our main analysis, where we found access was associated with better performance only in relation to ROTA and ROCE. The wide differences between our impactful firms and their competitors stand out. The matching is more exact than what we achieve in our main analysis by controlling for sector, assets, age, and FTSE100 status. However, this exercise does not account for endogeneity like the 2SLS models in our main analysis and, of course, it includes many fewer observations.

Discussion

Overall, we believe our analyses reject the hypothesis that meetings with, and NEDs within, the UK executive deliver financial benefits to firms. There are two alternative interpretations. The first is that access can improve ROTA and ROCE, but not other outcomes. The second is that, while access has no effect for the vast majority of firms, very large and well-connected firms do benefit from their access. We discuss each of these alternatives in turn. We did find that both NEDs and meetings were associated with high returns on total assets and returns on capital employed, but our models also implied that both meetings and NEDs increased the tax burden on firms. While the finding of firm benefits is theoretically, and commonsensically, motivated, there is no literature on the association between increased tax and political access. Firms might seek out access to remedy a high tax burden, but this does not imply an overall association between more access and higher tax. Indeed, if access really did lead to bigger tax bills, firms would refuse to meet ministers and would prevent their staff from accepting non-executive directorships. We are not tempted to dismiss the tax findings as meaningless noise and approve the ROCE and ROTA results as theoretically grounded and empirically verified. Second, our small-N, matching exercise showed that influential firms performed better than their close competitors. We cannot give this finding similar status to the null result for the large-N, 2SLS models.

Failures to reject the null, like rejections of the null, are subject to caveats. We see three. First, the small-n exercise provides a reason to doubt that the null finding applies to the firms with greatest access. Second, if we model firm benefits with ordinary-least squares, more coefficients suggest firms benefit and none imply that firms suffer financial costs from access. 2SLS is an imperfect procedure and our instrument, sectoral access, is relatively weak. Third, as stated at the outset, we expected our estimates to be biased downwards. We believed a positive finding to be a more accurate indicator of the real relationship than a null finding.

Our work contributes a sceptical contribution to the emerging literature on NEDs, meetings, and firms in the United Kingdom. Our employment of an endogeneity correction probably explains the difference between ours and Andrews and Fahey’s (2025) general finding that NEDs deliver benefits. Barbakadze (2024) and Andrews and Fahey (2025), along with Andrews and Fahey’s (2025) findings on insider firms, rely on quite subtle, contextual conditions to identify gains for firms. Our small-N analysis belongs to the same family of arguments. Narrowly specified benefits can be consistent with an overall finding of no gain. Further research has the difficult task of accounting for endogeneity and incorporating more contextual controls into a general study. We have argued that access to the UK executive does not systematically deliver benefits to firms. Although some firms undoubtedly make money from their access, this finding is a reassuring one for UK democracy and governance. When ministers meet business representatives, they hope to gain information and legitimacy for their policymaking, and do so without incurring the democratic and economic cost of thereby financially favouring one firm over another. Similarly, the system of NEDs potentially adds valuable expertise and legitimacy to UK governance, without the worry that officially independent directors are subtly representing their principal employers’ commercial interests. Presumably, then, these directors are motivated by public service and career and network development, rather than an opportunity to obtain benefits for the principal employer. Similarly, the rare instances of meetings for most firms suggest that business leaders are not wasting a lot of time on government business.

It is important to remember that most of the access is retained by a tiny minority of firms. The null finding pertains to the vast majority of the firms, but not the vast majority of the access. It is hard to imagine that if KPMG or British Aerospace were to be suddenly refused all meetings and had all their NEDs removed, they would not suffer a major drop in their financial performance. There may be too little variation in the access afforded to such perennial insiders in our dataset to capture the value of their access. These firms’ close relationships do not reflect fierce market competition or democratic equality. Instead, they demonstrate a symbiosis of a handful of firms and the UK executive, which has been deepened by the introduction of the NEDs.

In their study of American firms, Brown and Huang (2020: 418) find almost exactly the same proportion of firm-years with a meeting as we do. This suggests that large firms in the United States have more access than their equivalents in the United Kingdom, since their data only relate to the president, not the wider cabinet. Perhaps the greater level of access to the executive reflects the more central role of fundraising and the sale of access in the day-to-day life of US politicians. Even in the most centralised institution of its decentralised system, there is greater access for business than in the UK’s much more centralised polity. In the United Kingdom, there is a sharper distinction between the many outsiders and the few symbiotic insiders.

Finally, on the same theme, our work is consistent with none of the three models of access and outcomes presented by Berkhout et al. (2025). Our regressions reject the linear model. The insider–outsider model predicts a threshold after which insiders no longer gain from further access. Our small-N analysis suggests that it is only among insiders that variations in the amount of access matters for financial outcomes. The signalling model predicts that the transition from little or no access to some access is the point at which access delivers outcomes. If this were true, removing the influential outliers would have increased the association between outcomes and access, but it did not. The signalling model is also contradicted by the small-N exercise.

Conclusion

We have conducted a population study of all officially reported meetings with business actors and non-executive directorships in the British government over 7 years. We find that, in general, both meetings and NEDs fail to deliver benefits to individual firms. A small-N matching exercise suggests that variations in access deliver an edge over peers for elite firms, but this finding is more uncertain. Our findings are inconsistent with the rent-seeking approach of political economy. They tend to favour public administration’s emphasis on access as good governance, but do not necessarily falsify the political science emphasis on a resource exchange that can serve both good public policy and narrow corporate interests. The emerging literature on both NEDs and meetings reports benefits for firms, albeit mostly for quite specific outcomes in quite specific circumstances. These results may be consistent with the overall absence of a relationship, as indeed may our small-N finding. The difficult challenge of reconciling these positive results with our overall null is surely high on the agenda for further work on the United Kingdom. Our regression results are somewhat reassuring for UK politics and policy. Lobbying is not associated with a systematic favouring of individual firms. For most firms access is so rare that it hardly represents a waste of senior management’s time. However, the descriptive results are more concerning. While the patterns of meetings and NEDs across ministers and departments are largely defensible, the symbiosis between a handful of defence, finance, and professional services firms and the state is troubling, both democratically and economically. Managers from the firms that enjoy a symbiotic relationship with the state spend a lot of time engaging with the agenda of the executive and there is evidence that their employers may profit from it. Alternative methodologies, such as process tracing and surveys, offer opportunities to shed light on whether meetings and NEDs in fact justify the amount of access given by generating information and legitimacy that improve policy. Our work also compares relatively straightforwardly to a study of the United States and comparisons to the European Commission can also be made. Therefore, like others (Garlick et al., 2025), we believe there is excellent potential for building-block comparative quantitative case studies of corporate access.

Supplemental Material

sj-docx-1-bpi-10.1177_13691481261455520 – Supplemental material for Time well spent? A population study of corporate access to the executive in the United Kingdom

Supplemental material, sj-docx-1-bpi-10.1177_13691481261455520 for Time well spent? A population study of corporate access to the executive in the United Kingdom by Kevin Fahey and Iain McMenamin in The British Journal of Politics and International Relations

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Additional supplementary information may be found with the online version of this article.

Data.

Lags.

Descriptions of Meetings, NEDs.

Table A1: Sample of meetings between firms and ministers.

Figure A1: Frequency of Non-Executive Directorships by Agency and Department.

Correlation Coefficients and Summary Statistics.

Figure A2: Correlation of covariates in main models.

Impactful Cases.

Table A2: The effects of firm-minister meetings on firm performance metrics, 2013–2019. Two-stage least squares. Impactful firms removed from analysis. Clustered standard errors reported in parentheses.

Table A3: The effects of firm-minister meetings on firm performance metrics, 2013–2019. Two-stage least squares. Impactful firms removed from analysis. Clustered standard errors reported in parentheses.

First-stage coefficients corresponding to Table 8 and Table 9 in manuscript.

Table A4: Meetings, first stage.

Table A4: Non-Executive Directors, first stage.

Alternative specifications: Meetings and NEDs together.

Table A5: The effects of firm-minister meetings and non-executive directors on firm performance metrics, 2013–2019. Two-stage least squares.

Access Quality Measures.

A6: The effects of firm-minister meetings on firm performance metrics, 2013–2019. Quality measure of meetings. Clustered standard errors reported in parentheses.

A7: The effects of firm-minister NEDs on firm performance metrics, 2013–2019. Quality measure of NEDs. Clustered standard errors reported in parentheses.

Table A8. The effects of firm-minister meetings on firm performance metrics, 2013–2019. Standardised meetings and NEDs combined into a single measure of influence. Clustered standard errors reported in parentheses.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.