Abstract

The aim of this article is to examine the impact of private standards on the Indian marine export industry. Private standards are standards established by large retailers and supermarkets, primarily in developed countries, that impose stricter compliance requirements on exporters. Adherence to these private certifications has become a de facto necessity for exporters seeking to access certain markets. Using a data set that matches private standards adopted by Indian marine firms, collected through a primary survey, with their publicly available financial statements, we find that firms adopt private standards to secure better prices, access new markets and buyers and enhance quality and branding, despite the additional compliance costs and regular audits. Our analysis finds that firm size plays a key role in the adoption of private certifications, with firms in the third to fifth quintiles of total revenue in our sample being more likely to obtain a private certificate. As a result, certification is associated with improved access to export markets and better firm-level outcomes, but also leads to an unequal distribution of trade benefits, with larger firms disproportionately capturing these gains.

Keywords

Introduction

Non-tariff measures (NTMs), such as public and private standards, have become a determining factor in trade in the agriculture and allied sector in the recent decades. Public standards are rules set by government authorities in the form of Sanitary and Phytosanitary Standards (SPS), such as those related to food quality and safety, which must be followed by law by any exporter wishing to export to these countries (Gupta et al., 2024). On the other hand, private standards are established by large retailers and supermarkets, mostly in developed nations. Private standards are more stringent than public standards and require a higher level of compliance from exporters in order to gain access to the shelves of these retailers. Therefore, meeting these private standards is often a de facto requirement for accessing certain supply chains (Ehrich & Mangelsdorf, 2018; Shepotylo, 2016). Using a data set that matches private standards adopted by Indian marine firms, collected through a primary survey, with their publicly available financial statements, this article demonstrates that larger firms are more likely to adopt private standards. Access to premium markets enables these firms to expand further, thereby widening the gap between larger and smaller firms in this sector.

The growing adoption of private standards in agriculture and allied products can be attributed to several factors. Due to increased competition, retailers and supermarkets use private standards to differentiate their products from those of their competitors. Additionally, legislation in developed nations holds retailers accountable for providing safe and healthy food to consumers. As a precautionary measure, private standards serve as a form of legal defence in case of litigation. Moreover, rising incomes and greater awareness of health and food safety have shifted consumer preferences toward certified food products. Finally, retailers aim to build consumer trust by enhancing transparency in the supply chain. Private standards enable them to enforce strict traceability measures, ensuring clear and reliable information flow throughout the supply chain (Schuster & Maertens, 2015).

The debate surrounding private standards, similar to that of public standards, centres around whether they act as a barrier or catalyst to trade. Private standards impose additional costs on exporters, potentially acting as a barrier to trade (Akoyi & Maertens, 2018; Mitiku et al., 2017; Schuster & Maertens, 2015). Cheptea et al. (2015) found that in addition to upfront audit fees, firms may also incur additional sunk costs to meet desired private standards. Additionally, strict traceability standards, unannounced audits and the adoption of strict quality management systems can lead to significant variable costs. As a result, firms that are unable to afford these high costs may not be able to access premium markets. However, private standards can help bridge information asymmetries in the supply chain and increase trust and transparency, thus increasing exports (Cheptea et al., 2015; Kleemann et al., 2014). For instance, Fiankor et al. (2020) found that the GlobalGAP standard served as a catalyst for trade in the export of apples, bananas and grapes. Andersson (2019) reported similar findings in their analysis of the impact of the GlobalGAP standard on the import of fresh fruits and vegetables to the European Union (EU), discovering a significant positive effect on both the extensive and intensive margins. Additionally, research has shown that private standards can lead to consolidation in the supply chain and concentration of market power (Schuster & Maertens, 2013). This could benefit a few firms that are able to participate in the supply chain, while other firms may be excluded from the market. Therefore, it is particularly important to consider the impact of private standards on developing nations, where institutions may be weaker, and resources may be unevenly distributed (Gupta & Sangita, 2022).

While the existing literature has extensively examined the role of private standards in influencing export performance and market access (Anríquez et al., 2025; Bemelmans et al., 2026; Ehrich & Mangelsdorf, 2018; Fiankor et al., 2020), much of this evidence is based on country-level analyses, often using gravity models or commodity-specific studies. Recent firm-level studies (Dong & Liang, 2023; Meemken, 2021) focus on agricultural producers and examine the impact of certification on farm-level outcomes such as income, productivity and prices. While these studies provide important insights, they largely concentrate on the production side and farm performance, with limited attention to firm-level dynamics in export-oriented industries, particularly in terms of market access, firm performance and industry structure. Evidence from the Indian context is also limited and geographically narrow (Raymond & Ramachandran, 2017). This study addresses these gaps by focusing on marine export firms in India and by combining primary survey data on certification with firm-level financial data to examine both the determinants of adoption and the resulting distribution of trade benefits across firms.

This article focuses on the significance of private standards in the Indian marine export industry, a globally important sector. According to Food and Agriculture Organization (FAO) (2022), State of World Fisheries and Aquaculture Report, aquatic products account for 11% of global agricultural trade and 1% of total merchandise trade. India is one of the world’s largest exporters of marine products, with exports reaching $7.38 billion in 2023–2024, representing 4.5% of global marine trade and serving over 100 countries (MPEDA, 2022). The adoption of private standards among exporters has been steadily increasing, with many firms obtaining certification in one or more standards (Raymond & Ramachandran, 2017). Given the importance of the Indian marine industry, understanding the impact of private standards on this sector is essential.

This article has two primary objectives. First, it aims to investigate the role of private standards in the Indian marine export industry. Second, it seeks to identify the specific characteristics that enable Indian marine firms to adopt private standards. In this study, we conducted a primary survey of 209 Indian marine firms that are registered as manufacturer-exporters on the Marine Product Export Development Authority (MPEDA) portal. The survey was designed to collect detailed information on the types of private standards adopted by firms, as well as their experiences with certification, including associated compliance challenges, and perceived benefits, over the period 2014–2020. To augment the collected data, financial information from the Ministry of Corporate Affairs (MCA) portal was matched to create a unique data set to undertake analysis.

Furthermore, this article employs two distinct methods to examine the role of private standards in the Indian marine industry. First, a descriptive analysis is conducted to identify broad patterns and trends in the adoption of private standards within the industry. Second, a panel data econometric analysis is used to assess the specific characteristics that influence Indian marine firms’ likelihood of adopting private standards. The findings of the study revealed that despite the additional compliance costs and regular periodical audits, firms cited benefits such as better prices, access to new markets and buyers and improvements in quality and branding as reasons for adoption of private certifications. The analysis revealed that firm size was a dominant characteristic that enabled firms to adopt private certificates, with firms in the third to fifth quintiles of total revenue in the sample being more likely to hold a private certificate. The study highlights that the unequal access to markets has led to an uneven distribution of benefits from trade, contributing to a higher level of inequality among firms.

This study contributes to the literature in three important ways. First, due to the lack of publicly available data on firm-level adoption of private standards, the literature on the topic is limited. While the study by Raymond and Ramachandran (2017) only examined the impact of food standards in the state of Kerala, this study conducts a comprehensive survey of firms located in all eight states along the peninsular India and covers 30% of all firms registered with the MPEDA as manufacturer-exporters. Second, by combining data on private standards with financial data available on the MCA portal, this study is one of the few that associates audited data from balance sheets and profit and loss statements with data on private standards. These unique panel data allow for the examination of causal links between firm characteristics, such as size, and the probability of firms certifying themselves with one or more certifications.

The proceeding for this article is as follows: the next section, ‘Private Standards and Evolving Supply Chains’, provides stylized facts on private standards. Section ‘Data’ explains the data, and section ‘Patterns and Benefits of Adoption of Private Standards’ describes the methodology. Section ‘Determinants of Adoption of Private Standards’ presents the empirical results. Lastly, the final section, ‘Conclusion and Policy Recommendations’, concludes.

Private Standards and Evolving Supply Chains

One of the primary reasons behind growing popularity of private standards is the complexity of supply chain of marine industry (Ehrich & Mangelsdorf, 2018; Henson & Humphrey, 2010; Schuster & Maertens, 2013). As mapped by Raymond and Ramachandran (2017), marine products move through several stages within the supply chain before finally being exported from processing plants (see Figure A1 in Appendix). Unprocessed marine products could potentially originate from two sources – aquaculture ponds and wild capture. In case of aquaculture, food safety and quality standards are mainly dependent upon the water quality, feed quality and aquatic health maintained at farms (Marschke & Wilkings, 2014). While in case of captured marine products, food safety and quality are influenced by the sanitary conditions maintained in fishing vessels, health of aquatic life in water bodies and processes followed in landing harbours (Sebastian, 2019). Though MPEDA, the agency responsible for export of marine products from India, regulates the supply chain through various approvals and certifications, these standards are significantly lower than those followed internationally (Henson et al., 2004). Therefore, maintaining food safety and quality throughout the supply chain, as desired by the consumer food safety laws in developed nations, is challenging for exporters (Henson & Humphrey, 2010; Mitiku et al., 2017). Due to this arbitrage in standards, private standards have been increasingly demanded from exporters in countries in developing nations such as India, which would like to access markets of developed nations. Hence, it is important to understand the implications of this trend, that is, the rising adoption of private standards, on the Indian marine industry.

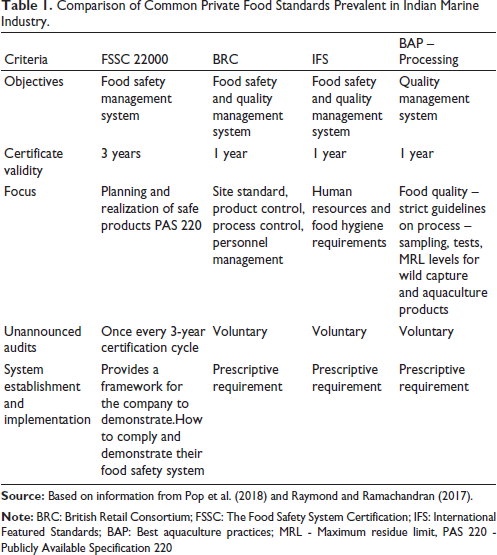

While standards such as ISO 22000 and CODEX Alimentarius are uniform across geographies, retailers and trade associations in specific geographies have developed their own sets of standards that they collectively follow. For instance, members of British retail trade associations follow the British Retail Consortium (BRC), while members of French and German retailer associations follow International Featured Standards (IFS). This means that the exporters interested in serving these geographies need to be certified with the required geographical standards. However, compliance with private standards is burdensome and requires significant commitment by senior management of firms. Table 1 compares a few private standards commonly adopted by exporters of the Indian marine industry. Standards were developed to achieve distinct objectives. First, for instance, while the Food Safety System Certification (FSSC) 22000 was established to achieve a food safety management system, BRC and IFS seek to achieve efficient quality management system along with food safety. Hence, BRC and IFS also focus on product and process control, site standards, food hygiene conditions and human resource management. Therefore, broadening the objectives increases the scope of rules and regulations associated with each standard, leading to higher cost of compliance for exporters (Fontaine et al., 2018; Pop et al., 2018; Raymond & Ramachandran, 2017).

Comparison of Common Private Food Standards Prevalent in Indian Marine Industry.

Second, in general, certifications are valid for a year, and renewal is dependent upon re-audit. Moreover, any certified facility, during the year, can be audited without prior notice. Since guidelines are prescriptive in nature, and key responsibility of the senior management is to ensure continuous monitoring of the processes followed at the facility. Adherence to strict guidelines requires appropriate training of unskilled labour, trained middle-level managers who completely understand desired regulations and detailed documentation, thus resulting in a long-drawn, time-consuming exercise.

Lastly, in addition to food safety and quality, private standards also impose environmental and social regulations. BAP, which is popular in the United States, requires facilities to maintain labour standards set by the International Labor Organization (ILO) instead of labour standards followed in host countries (Kruijssen et al., 2021). Moreover, to mitigate overfishing, catch certificates are to be documented while sourcing wild-captured marine products to prevent Illegal, Unregulated and Unreported (IUU) fishing (Andre, 2013). Therefore, exporting to premium markets involves significant additional sunk costs on behalf of the firms. Besides hefty certification cost, firms also incur compliance cost, that is, additional cost incurred to match desired standards from current levels followed by the firm. Compliance cost could be in the form of training of personnel, readjustment of production lines, improving documentation and others and can vary across firms. According to Cheptea et al. (2015), IFS certification requires firms to undergo a two-and-a-half-day audit, which requires upfront audit fees of €3,500. Since IFS recognizes each production line within a facility as an independent line, firms that wish to certify numerous products or production units pay higher audit fees. Bar and Zheng (2019) analyzed the decision-making process of manufacturers when it comes to obtaining certifications, using data from the BRC’s Global Standards programme. The study found that manufacturers tend to obtain certifications from bodies that they perceive to have the most lenient standards, as well as from organizations that are located closer to them geographically.

A commonality among all private standards is the regulation on traceability. Traceability builds trust between producers (exporters) and buyers (importers, usually large retailers and supermarkets), assuring that necessary steps were undertaken to comply with food safety and quality standards. Though levels of traceability can vary with the type and objectives of a standard, the ability to trace a food product is a major concern for the food industry in developed nations. BRC, for instance, requires facilities to maintain a traceability system of in-house processes. In particular, it also requires documentation of quality and hygiene conditions while manufacturing food packaging materials. On the other hand, BAP mandates certified units to establish ‘one up and one down’ traceability by using Trace Registers, an end-to-end transparency platform that allows each final product to be traced back to its origin pond and inputs fed. However, full traceability requires free information flow and extensive documentation of inputs and outputs throughout the supply chain, which is usually not easily available due to weak institutions in the developing countries. Hence, tracing food back to its origin requires effort and substantial control of the supply chain (Andre, 2013).

In addition, not all private standards are applicable to a unique end user; instead, they are applicable at different stages of production (see Figure A1 in Appendix). BAP certifies every step of the production chain, that is, hatcheries, farms, feeds and processing plants, while BRC, IFS and FSSC are only applicable to the processing plant. Such certifications eventually lead to a consolidation of supply chains, wherein processing plants are induced to source their raw materials from either certified farms, processing plant-controlled farms or independent farms that are able to maintain desired safety and quality. Trifkovic (2014), in the Vietnamese pangasius (a type of fish) sector, found that processing companies preferred to vertically integrate by choosing to control primary production rather than contracting to a third party. Hence, consolidation of supply chain may lead to unequal distribution of benefits among firms in the industry.

Given the cost and the complexities involved in the process of complying with private standards, it is pertinent to understand their impact on different types of firms in the market.

Data

The MPEDA, established by an act of Parliament in 1972, functions as a public authority responsible for regulating, developing, protecting and promoting the export of marine products. All firms engaged in the export of marine products from India are mandated to be registered with MPEDA. Of the 686 exporter-manufacturers listed in the MPEDA exporter directory, financial documents for 209 private and public limited companies are available on the MCA portal. The profit and loss statements of these companies provide valuable data, offering detailed insights into revenue and expenses, while the balance sheets reflect the status of assets and liabilities. According to the Companies (Accounts) Rules, 2014, under the Companies Act 2013, both private and public limited companies are required to upload financial documents. As a result, this analysis focuses on the period from 2014 to 2020. We use this data set to obtain information on revenue, profits, gross fixed assets (GFA), employee expenditure and others (see summary stats in Table A1).

To gather information on private standards, a primary survey was conducted on 209 Indian marine firms registered as manufacturer-exporters on the MPEDA portal. The survey aimed to gather information on the private standards firms complied with and their experiences with certification over the 6-year period from 2014 to 2020. The primary survey was conducted through in-person and telephonic interviews. This survey collected detailed information on firms’ adherence to private standards across multiple years, allowing us to track the adoption of private standards over time. The data obtained from these interviews were then matched with financial statements from 2014 to 2020, creating a unique panel data set for quantitative analysis. Since the primary survey had to be conducted exclusively for firms whose financial statements were publicly accessible, a random sampling strategy was not feasible. Instead, a purposive sampling approach was adopted to ensure relevant firm participation. The survey was carried out between November 2021 and September 2022, with interviews conducted with senior management representatives from the selected firms.

The survey questionnaire included the following key questions: Whether the firm had adopted any private standards in the past. If yes, the year since which the standards have been adopted. Whether the firm perceived any benefits from adopting private standards. If yes, the nature of those benefits. Any additional comments or insights related to private standards.

By collecting data on firms’ adherence to private standards over multiple years, this study provides a comprehensive analysis of the role private standards play in the Indian marine export industry. However, there are certain limitations to consider. First, the data set includes only 209 companies out of more than 600, which may limit the generalizability of the findings. Second, while the study identifies whether firms have adopted private standards, it does not quantify the extent to which these standards influence export growth to specific markets.

Patterns and Benefits of Adoption of Private Standards

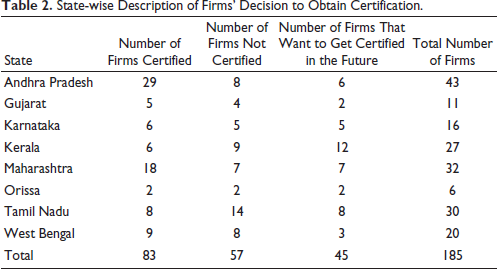

The purpose of our primary survey was to collect and analyze data on private standards of firms, whose historical financial statements were available at the MCA database. Synthesis of such a unique data set would enable us to identify firm-level characteristics that enable adoption of private standards. Table 2 provides a state-wise summary of private standards adopted by respondents. Of 209 firms surveyed, 185 responses were recorded, while 24 firms did not respond. Among eight states across the east and west coast of the Indian peninsular, more than 70% of firms that responded were situated in four states – Andhra Pradesh (23%), Tamil Nadu (16%), Maharashtra (17%) and Kerala (14%). Due to unavailability of agricultural land for aquaculture practices in the states of Kerala and Tamil Nadu, the majority of Indian aquaculture farms are located in Andhra Pradesh and West Bengal (De Jong, 2017). Hence, firms that are involved in aquaculture are located in these states, whereas firms that are dependent on wild capture of marine products are located mainly in Kerala and Tamil Nadu. The highest percentages of firms that are certified were in states of Andhra Pradesh, Maharashtra and West Bengal. On the other hand, 30% of firms surveyed in Kerala wished to get certified in the future.

State-wise Description of Firms’ Decision to Obtain Certification.

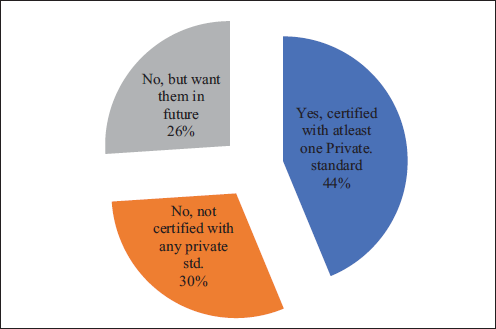

Of 185 respondents, 45% (i.e., 83 firms) have at least one of their facilities audited by one or more private standards during 2014–2020, while 30% did not (see Figure 1). Notably, 26% of the respondents who did not have certificates wished to adopt them in the near future. Most respondents believed that the relevance of private certificates has increased post-pandemic due to the increased demand for certified food in developed nations. Therefore, more firms in the industry desired to get certified in the future.

Firms Certified with Private Standards.

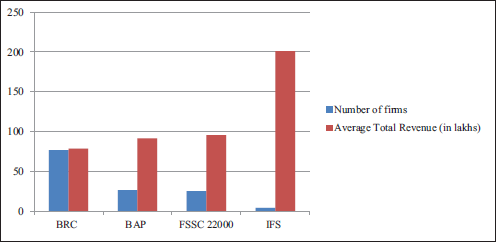

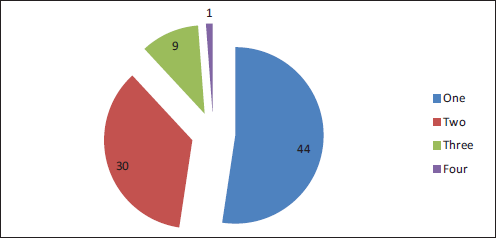

Among the most common private standards certified by exporters were BAP, BRC, FSSC 22000 and IFS (see Figure 2): 77 firms were certified with BRC, 27 firms with BAP, 26 firms with FSSC 22000 and 5 firms with IFS. However, some firms are certified with one or more private standards to access more markets (see Figure 3). Of the firms examined in the study, 52% held certification under a single standard, while 36% held certification under two standards. Additionally, 11% of the firms held certification under three standards, and a small number (1%) held certification under four standards. It is likely that the sunk cost of obtaining and maintaining these certifications increases with the number of certifications held by a firm. However, a higher number of certifications also provides the firms with greater access to markets.

Usual Number of Private Standards of a Firm.

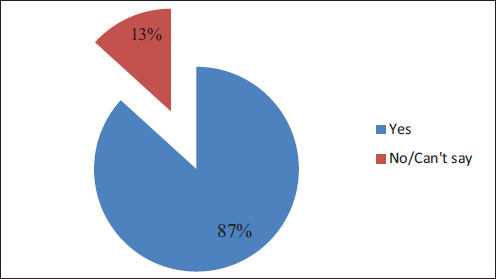

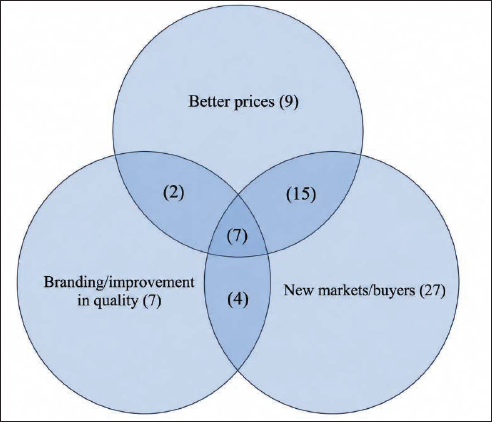

While some respondents mentioned that private certificates are costly and require yearly audits, 87% of respondents believed that private standards have benefitted them despite incurring additional cost (see Figure 4). When asked about the type of benefits experienced, many responded with two or more positives. We classified the benefits into three categories, that is, better prices, access to new markets and buyers and improving quality and branding. According to Figure 5, the ability to access new markets and buyers was the most common benefit experienced by 53 respondents. While 37 respondents mentioned that adoption of private standards helps to find better prices, and 20 respondents found them to improve quality and branding. However, 15 respondents acknowledged the benefits in terms of better prices and access to new markets. While seven respondents found certification to improve quality, access to markets and help in better prices. Similar results were shown by Trifkovic (2014), who found that in the Vietnamese pangasius sector, processors and farmers adopted standards to increase market access to international markets.

Percentage of Firms That Believe Private Standards Have Benefitted Them.

Common Benefits Experienced by Firms from Private Standards.

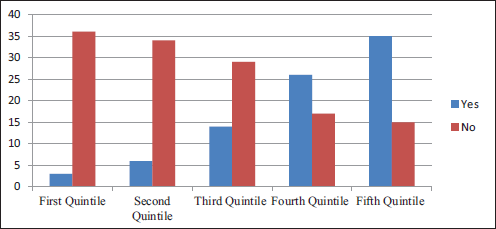

By matching financial statements of firms with their data on private standards, we find IFS to be adopted by firms with relatively higher average total revenue (~20 million INR), as shown in Figure 2. On the contrary, BRC was amongst the popular certifications by firms with relatively lesser average total revenue (~7.5 million INR). While only a few firms were certified with BAP and FSSC 2200, the average total revenue of firms that were certified was relatively higher than that of firms with BRC and relatively lower than that of firms with IFS. This indicates that size (as measured in terms of total revenue) determines the type of standards firms adopt. In addition, on dividing our sample firms into quintiles based on total revenue last reported, we find direct correlation between revenue of the firm and probability of adopting a private standard. As shown in Figure 6, as we move towards higher quintiles, the proportion of firms that have a private standard increases as compared to those that do not. This indicates that larger firms are likely to adopt a private standard, leading to unequal market access among firms.

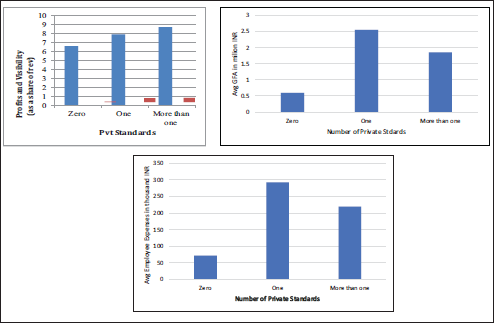

Upon classifying firms based on the number of private standards, we find profitability (profits before taxes as percent of total revenue) and visibility (total exports of a firm as percent of aggregate export of the industry) to be directly proportional to certifications (see Figure 7). The average profitability of the firms that are certified with more than one private standard was 8.7%, relatively higher than firms with one (7.9%) or zero certifications (6.6%). Similarly, average visibility of firms with more than one certification (0.56%) was relatively higher than that of firms with one (0.51%) or zero certifications (0.07%). However, average GFA and average employee expense are relatively higher for firms certified with one certificate as compared to zero, but lower than firms with more than one certificate (see Figure 7). It appears that firms with more than one certificate are relatively more productive, as their profitability and visibility are higher relative to employee and depreciation expenses.

In summary, the survey of firms in the Indian marine industry shows that certification with private standards has been beneficial for most of the firms. The growing interest among firms that are not currently certified to be certified in the future highlights the rising importance of private standards. Despite the added compliance costs and regular audits, firms have cited better prices, new markets and buyers and improved quality and branding as reasons for adopting private certifications. The results showed that certified firms had higher total revenue, profitability, visibility, GFA and employee expenses compared to non-certified firms. In essence, the study confirms the significance of private certification within the Indian marine industry.

Determinants of Adoption of Private Standards

Model

While few studies on certifications have acknowledged that certified firms are generally larger in size than non-certified firms, none, to the best of our knowledge, have quantified this difference (Meemken, 2021; Schuster & Maertens, 2016). Since size of a firm can be broadly measured by various dimensions such as total sales, total assets and number of employees, we seek to understand which among these characteristics enables firms to certify with private standards (Doğan, 2013).

Certification to private standards for accessing developed markets raises sunk costs for firms. As noted in Section ‘Private Standards and Evolving Supply Chains’, firms must upgrade internal standards and pay significant audit fees for third-party certification. However, only firms with certain characteristics can absorb these costs. Melitz (2003) showed that export-related sunk costs reshape industries, with highly productive firms exporting, medium-productive firms serving domestic markets and low-productive firms exiting. This raises a key question: which firm attributes enable firms to bear these additional costs of private standards?

Against this backdrop, this study proposes an empirical strategy that aims to explain the likelihood of firms being certified with private standards as a function of firm-level characteristics indicative of size and other variables such as age and profits of the previous year. To examine the determinants of private standard adoption, we estimate the following empirical specification:

where subscripts

The dependent variable,

Firm size is the key explanatory variable and is proxied using total revenue, GFA and employee expenses. To differentiate firms by revenue levels, we create a categorical variable,

To control for firm-level characteristics that may influence certification decisions, we incorporate two more variables into the model: age and 1 year lagged profits. Age serves as a proxy for accumulated experience, measured by the number of years since incorporation. We expect older firms to be more likely to adopt private standards due to their historical adaptability. Profits, calculated as profits before taxes of the previous year, reflect financial strength and are an indicator of productivity of the firm. Firms with higher productivity are likely to accrue higher profits, and relatively more profitable firms are better positioned to invest in quality improvements and compliance measures.

To address potential multicollinearity, we examine a correlation matrix in Tables A2 and A3 in Appendix. Among the different indicators of firm size, the highest correlation (0.59) is observed between total revenue and employee expenses, while the lowest (0.54) is between GFA and either employee expenses or total revenue. These moderate correlations were expected.

To account for unobserved heterogeneity, firm and time fixed effects are included in the estimation. The firm fixed effect,

Results

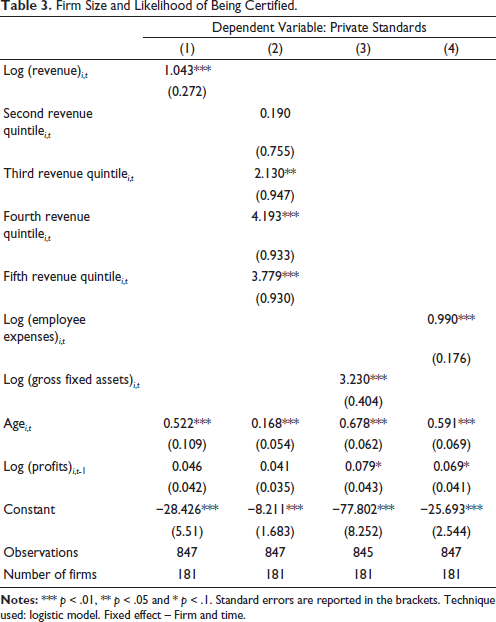

The analysis of the impact of firm size on the likelihood of private standards adoption is presented in Table 3, with corresponding marginal effects detailed in Table A4 and visually depicted in Figure 8. Within Table 3, we explore diverse indicators of firm size, including revenue, employee expenses and GFA, while concurrently considering key control variables such as age and profits of the previous year, across regressions (1)–(4). Regression (1) shows a positive and statistically significant coefficient for revenue, signifying that firms with higher revenue levels were more likely to embrace private certifications. Since revenue is log-transformed, to interpret coefficients we need to transform them into a non-log-transformed variable. 1 The coefficient of log-transformed revenue (1.043) is positive and statistically significant at the 1% level, indicating that larger firms, in terms of revenue, are more likely to obtain private standard certification. Specifically, a 10% increase in firm revenue is associated with a 10.4% increase in the odds of being certified. Similarly, GFA and employee expenses, examined in regressions (3) and (4), also exhibit positive and significant coefficients, reinforcing the role of firm size in certification.

Firm Size and Likelihood of Being Certified.

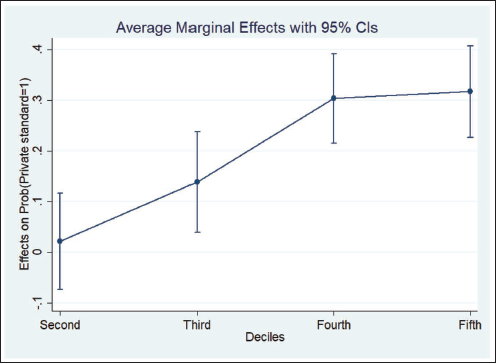

Marginal Effect of Revenue Quintiles of Regression (1) of Table 3.

However, the relationship between revenue and private standard adoption is non-linear, as seen in regression (2), which segments firms into revenue quintiles. Only firms in the third to fifth quintiles show significant positive effects, while the second quintile remains statistically insignificant. Notably, the coefficients for the fourth and fifth quintiles exceed those of the third, highlighting a clear trend: larger firms are more likely to be certified.

As shown in Table A4 and Figure 8, a firm’s probability of obtaining any private certification increases by 13% from the first to the third quintile, 30% from the first to the fourth and 31% from the first to the fifth quintile. These findings highlight firm size as a key determinant in the adoption of private standards.

These findings align with the results of recent investigations on private standards: Schuster and Maertens (2015) surveyed 87 Peruvian firms involved in export of asparagus to assess the impact of private food standards on export performance. They find that certified firms are not only more likely to own both agricultural land and a processing plant than non-certified firms, but also, on average, own substantially larger land (52.86 ha vs 3.6 ha). They also found certified firms to be relatively older, more experienced in terms of export and resilient to exiting international markets. Meemken (2021), using Peru’s National Agricultural Survey, also found sustainability standards to be more common among relatively larger farms. In addition to certified farms being geographically clustered, certifications were associated with higher farm incomes. Moreover, Kleemann et al. (2014) found that larger (in terms of size) and wealthier pineapple farmers in Ghana were more likely to adopt GlobalGAP certification, since it required relatively larger investment in equipment than organic certification.

The control variable ‘age’ consistently shows a positive and statistically significant association across all regressions in Table 3, highlighting its role in private standards adoption. The coefficient on firm age is positive and statistically significant across all model specifications, indicating that older firms are more likely to be certified by a private standard. In Model 1, for instance, each additional year of firm age is associated with a 68.6% increase in the odds of certification, suggesting that experience and maturity may improve a firm’s capacity or motivation to adopt certification. Additionally, profits t –1 exhibits a positive and significant effect in regressions (3) and (4), reinforcing its influence on certification likelihood.

Instrumental Variable Approach

Endogeneity bias in Equation (1) may arise from two sources: omitted variable bias and reverse causality. The inclusion of firm and time fixed effects helps to reduce omitted variable bias by accounting for unobserved firm characteristics that could influence private standards adoption. However, reverse causality may still exist, as firms that adopt private standards may experience growth in size due to increased market access. To address this issue, we employ an instrumental variable (IV) method using two-stage least squares (2SLS) regression.

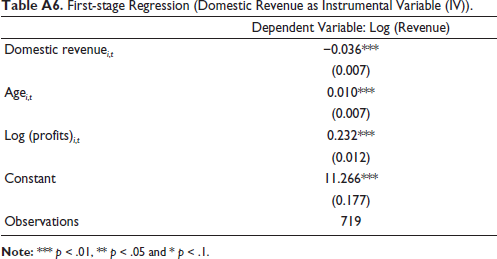

To address potential endogeneity in total revenue, we instrument it using a firm’s domestic revenue in a given year. This choice is justified on two grounds: first, domestic revenue is highly correlated with total revenue (first-stage coefficient = 0.066, p < .01), satisfying the relevance condition (refer to Table A6 in Appendix). Second, since adoption of private standard certifications is primarily driven by export market demands, domestic revenue is unlikely to directly affect certification outcomes, meeting the exclusion restriction. The second-stage results confirm that total revenue remains a strong predictor of certification likelihood, even after accounting for endogeneity (refer to Table A5 in Appendix).

The second-stage results (Table A5) show that log(total revenue) remains positive and significant, confirming our baseline finding that firm size is positively associated with the likelihood of certification. The magnitude of the coefficient (0.293) is somewhat smaller than in the fixed-effects model (1.043), which may reflect the correction for upward bias due to endogeneity.

Importantly, the coefficient on ‘age’ remains positive and statistically significant, indicating that older firms are more likely to adopt private standards regardless of the instrumentation of revenue. This suggests that firm maturity, potentially reflecting accumulated experience or stronger reputational concerns, plays a consistent role in certification decisions. The coefficient on lagged profits, however, turns statistically insignificant, possibly due to multicollinearity or reduced variation after accounting for endogeneity.

Taken together, the IV estimates lend further credibility to the causal interpretation of the positive relationship between firm size and private standard certification.

Conclusion and Policy Recommendations

This study examines the role of private standards in shaping firm-level outcomes in India’s marine export industry using a unique data set that combines primary survey information with firm-level financial data from MCA, Government of India. The empirical results show that firm size is a key determinant of certification. Firms in the third revenue quintile are approximately 13 percentage points more likely to obtain certification compared to those in the lowest quintile, while firms in the fourth and fifth quintiles are about 30–31 percentage points more likely to be certified. The findings also indicate that certified firms are better able to access new markets and buyers, secure better prices and improve product quality and branding. However, these benefits are not evenly distributed. Larger firms are better positioned to absorb the fixed and compliance costs associated with certification and, therefore, disproportionately capture these gains. As a result, private standards exhibit a dual effect: they facilitate market access while simultaneously contributing to an unequal distribution of trade benefits across firms. Moreover, given that the data set skews toward larger firms, as only public and private limited companies are included, the exclusion of small-scale enterprises may be even more pronounced in a broader industry-wide assessment. This underscores the need for institutional reforms and regulatory interventions to create a more inclusive and equitable certification landscape.

In light of the above findings, to promote inclusive growth, the Indian government should consider several policy measures. Financial support for smaller firms can be facilitated through low-interest credit schemes and direct subsidies for certification costs. Additionally, domestic certification frameworks should be strengthened to align with international standards while remaining cost-effective for smaller enterprises. Moreover, digital integration and trade facilitation, such as a national certification portal and streamlined documentation requirements, can improve transparency and reduce administrative burdens. Finally, awareness programmes and capacity-building initiatives should be introduced to educate micro, small and medium enterprises (MSMEs) on certification benefits and processes, ensuring broader participation in export markets.

At the international level, regulatory oversight of private standards is crucial to prevent market distortions and exclusionary practices. The World Trade Organization (WTO) should strengthen governance over private standard-setting bodies, ensuring greater transparency and accountability in certification requirements. Harmonization of private standards through a global certification equivalence framework can ensure uniformity in compliance requirements across markets, preventing unjust trade barriers. Moreover, international organizations such as the WTO, FAO and UNCTAD should provide technical and financial assistance to small exporters in developing countries, helping them meet certification criteria through public–private partnerships and capacity-building initiatives.

Private standards, while essential for ensuring quality and safety in global trade, must not become barriers to market entry that disproportionately benefit larger firms. Addressing these challenges requires domestic policy support to ease certification burdens for smaller firms, alongside global regulatory mechanisms to ensure that private standards do not create hidden trade restrictions. By implementing inclusive certification policies and fostering international cooperation, both India and global trade institutions can work toward a more equitable and competitive trading environment that balances quality assurance with inclusive market participation.

Footnotes

Data Availability Statement

The data that support the findings of this study were collected through a primary survey and from firm-level financial statements. Due to confidentiality agreements with participating firms, these data cannot be shared publicly. Data may be made available from the corresponding author upon reasonable request.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Note

Appendix

| Dependent Variable: Log (Revenue) | |

| Domestic revenue i , t | −0.036*** |

| (0.007) | |

| Age i , t | 0.010*** |

| (0.007) | |

| Log (profits) i , t | 0.232*** |

| (0.012) | |

| Constant | 11.266*** |

| (0.177) | |

| Observations | 719 |