Abstract

Robo-advisor is an artificial intelligence (AI) driven professional financial service that suggests financial portfolios and offers personalised investment recommendations to clients. Since the services are high in credence properties where financial results only become manifest over time and clients typically have difficulty assessing outcomes even after consumption, client psychological comfort is vital for service adoption. Drawing on the unified theory of acceptance and use of technology (UTAUT), information economic theory and the self-service technology (SST) literature, this study investigates a mediating role of psychological comfort, antecedents of psychological comfort and possible boundary conditions. Thailand (an emerging economy with sophisticated financial systems) was selected as our research context. Data were collected through a mixed method approach involving in-depth interviews with investors followed by a structured survey administered to 548 current and potential investors. The findings revealed clients’ key psychological characteristics (performance expectations, suspicion of human financial advisors) and boundary conditions that drive psychological comfort. Performance expectations and suspicion of human advisors are associated with psychological comfort, which subsequently fosters intentions to use and percentage of investment through robo-advisors. Client confidence in ability to search for financial information and need for human interaction have small but distinct moderating effects. This study extends the SST adoption and AI-enabled professional service literature. It reveals psychological comfort as a key mediator between client psychological characteristics and robo-advisors usage.

Keywords

Introduction

Technology driven by artificial intelligence (AI) and machine learning (e.g. service robots, chatbots, e-health, ChatGPT and other sophisticated automated systems) represents a ‘game changer’ in many service industries (van Esch & Stewart Black, 2021), especially professional financial services (Bughin & van Zeebroeck, 2017) where AI fundamentally complements human decision making, alters the form of interactions between clients and service providers and improves the customer experience (Hollebeek et al., 2021; Larivière et al., 2017). This research is timely as the financial advisory industry still reels from the effects of damaging revelations of corrupt, incompetent and self-interest behaviour in a number of countries (Bank of Thailand, 2022; Hayne, 2018). Many service firms strive to encourage clients to migrate from previous high-touch service encounters towards self-service technology (SST) (e.g. mobile banking, online medicine, frontline service robots, airport check-in kiosks) (Lu et al., 2020). In the financial services sector, robo-advisors are replacing human financial advisors in managing clients’ investment portfolios. These technologically sophisticated, computer-generated financial advisory services analyse clients’ profiles, allocate their portfolios and recommend investments based on individual client’s risk profile and financial goals, with little or no reliance on human involvement. Online questionnaires, self-reporting and quantitative modelling methods replace in-person interviews (Jung et al., 2018). Their appeal has prompted substantial venture capital investments (Deloitte, 2015; Jung et al., 2018). Thus, robo-advisors represent a major disruption to the long-standing, financial advisory industry.

Unlike static, low involvement SSTs (e.g. ATMs, rental car and airport kiosks, supermarket self-service checkout) that represent automated technologies at one end of a continuum, and sophisticated humanoid service robots (e.g. waiter robots, airport passenger aiding robot, hotel service robots, chatbots) with social-emotional and relational capabilities at the other end (Lu et al., 2020), robo-advisors are AI-based services lying on this continuum closer to social robots. They are more complex, customised and apply more sophisticated algorithms than typical SSTs (Xu et al., 2020), but deliver lower social or relational assistance compared to service robots. Prior research has modelled client acceptance of low involvement, non-smart SST with antecedents such as perceived usefulness (Curran & Meuter, 2005), ease of use (Chen et al., 2021), enjoyment (Rosenbaum & Wong, 2015) and convenience (Wang et al., 2013), but not with high involvement, sophisticated, highly customised, professional services such as robo-advisors. Furthermore, research on sophisticated service (humanoid) robots has by and large been conceptual with no studies empirically modelling customer acceptance. Uncovering drivers of robo-advisors acceptance, from clients’ perspective, is also a concern raised by prior research (e.g. Belanche et al., 2019; Hohenberger et al., 2019; Lourenço et al., 2020) due to an urgency by marketers and policy makers in successfully attracting clients to robo-advisory services. Previous studies address technical and design issues that could affect client acceptance (e.g. Baker & Dellaert, 2018), but few address client psychological characteristics that might be a key driver. Clients with a finance background and investment proficiency; those who are confident in technology usage; and risk-takers may tend to adopt robo-advisors (Epperson et al., 2015). However, most clients express more trust and expect to receive better financial performance from human financial advisors, despite robo-advisors’ ability to execute unbiased, superior forecasting accuracy and faster services (Zhang et al., 2021). This is consistent with the notion of algorithm aversion (Dietvorst et al., 2015) and a preference for social rapport, affective relationships and perceptions of human advisors’ superior ability to personalise advice (Hildebrand & Bergner, 2020). Therefore, client psychological characteristics could determine their affective response to robo-advisors, an influence that has not been sufficiently addressed in prior literature. The current study attempts to fill this gap.

Professional services represent offerings that are high in credence properties, in that clients have limited ability or skills to evaluate the technical service quality and value confidently (i.e. financial returns), even after the service provision (Darby & Karni, 1973; Frey et al., 2013; Park et al., 2021; Sampson, 2021). Financial advisory services feature high product complexity, require customisation and exhibit information asymmetry between clients and service providers, all of which can increase clients’ anxiety and perceived uncertainty (Alford & Sherrell, 1996; Schuster et al., 2015). Moreover, the outcomes of the core service (e.g. financial returns relative to alternative investments) only unfold over time, prompting additional anxiety, risk and uncertainty (Auh et al., 2007). Therefore, clients need to feel psychological comfort when considering robo-advisors (Roongruangsee et al., 2022; Spake et al., 2003). Psychological comfort produces feelings of ease (Simmons, 2001), security, peace of mind (Scitovsky, 1992) and decreases anxiety (Daniels, 2000).

The purposes and contributions of this study are: first, to explore the role of client psychological comfort as a potential mediator between the antecedents (client psychological characteristics) and intention to use robo-advisors based on the information economic theory. Second, to extend the relevance of the unified theory of acceptance and use of technology (UTAUT) model, including its antecedents and facilitating conditions, in a complex, AI-based SST service context. Third, to extend previous studies of the drivers of client acceptance of robo-advisors, particularly on clients’ inclination for human advisor proficiency (e.g. Zhang et al., 2021). Forth, to extend prior SST adoption and AI-enabled service literature by investigating client psychological characteristics (performance expectations, suspicion of human financial advisors, technology readiness) in driving psychological comfort and intention to use robo-advisors. Finally, to explore potential boundary conditions on the influence of the antecedents on psychological comfort. That is, we examine not only what drives psychological comfort and so intention to adopt, but rather under what contingency conditions the drivers will have stronger or weaker impact. In doing so, this study responds to prior research (e.g. Atwal & Bryson, 2021; Zhang et al., 2021) that calls for examination on potential antecedents of intention to use robo-advisors.

The study employed a mixed-method research design. We first conducted qualitative, in-depth interviews to verify and supplement previous studies in SST adoption, as well as to gain insights into the constructs relevant in the adoption of robo-advisors. We utilise the interview findings to develop our hypotheses and conceptual framework, in conjunction with a literature review. Then, as a second stage, we employ a quantitative approach using a structured survey informed by the literature review and interviews to empirically test the relationships among the variables relevant to psychological comfort and robo-advisors adoption.

We commence with a conceptual background and hypotheses development, followed by a description of the methodology.

Conceptual framework and hypotheses development

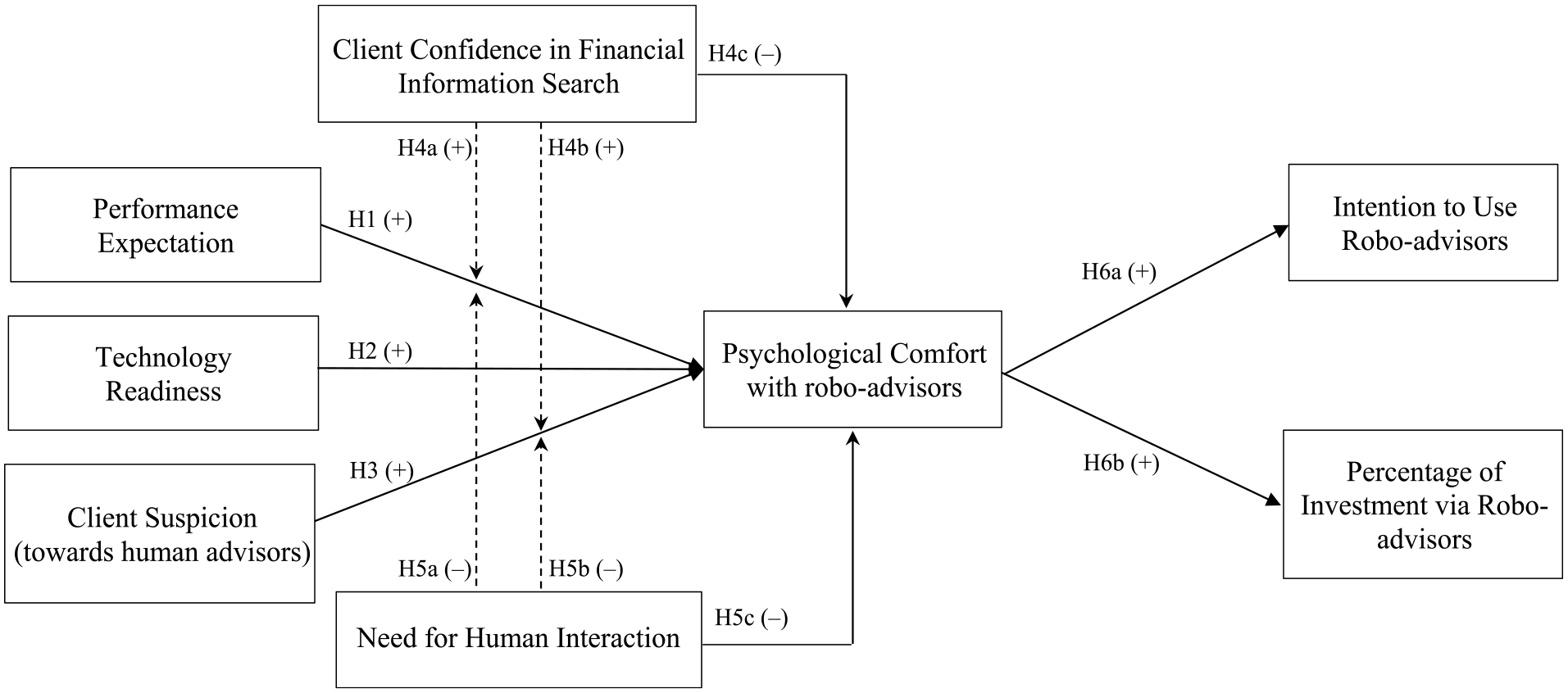

Our conceptual model (Figure 1) is grounded in the unified theory of acceptance and use of technology (UTAUT) (Venkatesh et al., 2003), information economic theory (Darby & Karni, 1973), the self-service technology literature and client interviews. Venkatesh et al. (2003) developed an extension of the general technology acceptance model that built upon the theory of reasoned action and the theory of planned behaviour. The result was the unified theory of acceptance and use of technology (UTAUT) which incorporates relevant social aspects and subjective norms (i.e. individuals’ perceptions) as well as boundary conditions. The model specifically highlights four determinants of use intentions – performance expectancy, effort expectancy, social influence and facilitating conditions. UTAUT has been extensively validated and widely used in examining acceptance of a wide range of generally low involvement, static technologies (e.g. de Ruyter et al., 2005; Wang et al., 2013; Yoo & Huang, 2013; Zhou et al., 2010) such as self-service checkouts, digital kiosks, mobile banking and digital television, to name a few. In the current study, the utilitarian dimension of performance expectancy, as well as social influence and facilitating conditions are considered relevant. When modelling acceptance of front-line service robots – a more sophisticated AI based technology – which requires cognisance of social and relational dimensions, the performance expectancy dimension of UTAUT has been found to be relevant. Further, Amelia et al.’s (2022) study of customer acceptance of service robots in a retail banking context found performance expectations (the robot fulfilled its core service role) and facilitating conditions to be key drivers of acceptance. Moreover, Wirtz et al.’s (2018) sRAM model of service robot acceptance highlights the central role of performance expectations as well as subjective norms and social dimensions.

Conceptual model.

The current study in the context of sophisticated consumer financial services is, to a large extent, different to most previous studies of technology acceptance in that robo-advisors are sophisticated, high involvement services and high in credence properties, meaning clients have difficulty in assessing risk and financial returns, at least in the short term. In fact, investment returns may take months, even years, to become manifest. As such, perceptions and subjective norms in the UTAUT model would seem to be relevant in the current study. Norms rely on social information as a form of social pressure to enact a certain behaviour. Subjective norms are based on interpersonal sources (e.g. peers) and external information sources (e.g. social and mass media) (Bhattacherjee, 2000). One subjective norm relates to the negative publicity surrounding human financial advisors in recent times and consequent perceptions regarding the honesty and integrity of human advisors. It stands to reason that client suspicion of human financial advisors’ motives in giving financial advice be included in our conceptual model.

Confidence in information search and need for human interaction have been shown to be relevant to SST adoption across of range of SSTs. These represent facilitating conditions in UTAUT and therefore included in our conceptual model as moderators (DeCarlo, 2005; DeCarlo et al., 2013; Feng et al., 2021; Parasuraman & Colby, 2015). Furthermore, our initial exploratory qualitative interviews with clients prior to the quantitative stage revealed these constructs were uppermost in their minds when considering adopting robo-advisors for their investment advice. The qualitative approach is further elaborated in the Methodology section.

Psychological comfort

Information economic theory (Darby & Karni, 1973) asserts that product or service attributes fall into one of three categories: search attributes where quality of outcomes can be assessed prior to purchase; experience attributes which a customer/client can confidently assess the quality of outcomes during consumption (e.g. a restaurant meal, a holiday experience); and credence attributes where the quality of outcomes may not be able to be confidently assessed before, during or even after purchase and consumption (e.g. evaluating a psychologists treatment; advice from a lawyer; financial advice from a financial planner or robo-advisors). Hence, clients can confidently evaluate services with search or experience attributes, but not so credence attributes. Therefore, a degree of psychological comfort is needed to entice purchase/adoption. Psychological comfort refers to feelings of security, reassurance, peace of mind (Scitovsky, 1992), reduced anxiety (Daniels, 2000), ease and relief of mental distress (Simmons, 2001). Clients can gain psychological comfort through interactions with service providers (Lloyd & Luk, 2011; Spake et al., 2003), as well as other forms of communication. Research in non-professional services has linked comfort with front-line employees’ service manner, familiarity and even interpersonal similarity (Sampet et al., 2023). It has also been shown to have an influence on perceived service quality (Butcher et al., 2001; Dabholkar et al., 2000), satisfaction, trust, commitment and positive voice behaviours (Spake et al., 2003). However, it is not an end in itself.

In professional services, particularly high involvement financial advisory services using a new technology such as robo-advisors, psychological comfort can be expected to play a central role in client acceptance. Logic alone dictates that, with an emerging technology such as robo-advisors combined with a highly critical, uncertain outcome (i.e. investment returns), client psychological comfort in the form of anxiety and uncertainty reduction would be highly relevant. Research in credence-based professional service settings emphasises reduction of client anxiety and perceived risks, prior to and during service encounters, as key to acceptance and retention (Roongruangsee et al., 2022; Sharma & Patterson, 1999). However, because AI-based robo-advisors lack social and relational features, available in human-provided services, some degree of psychological comfort is required to prompt client acceptance. To illustrate, from our qualitative interviews, psychological comfort emerged as being essential in driving intention to use. An exporter (female, 43 years) stated ‘Feeling comfortable in financial advisory services is about being assured of security in the process’. Also, an entrepreneur (male, 37) stated that ‘Having technology in place could make some people feel comfortable. There is no pressure from a human forcing us to invest or asking us detailed questions’. Hence, psychological comfort with robo-advisors is included as a key mediator of acceptance (see Figure 1).

Influence of performance expectations on client psychological comfort

From our interviews, and consistent with the UTAUT model, it was found that performance expectation was the most salient principle to most participants in choosing a financial advisor, in both cases of human or AI-based advisors. In encountering services high in credence properties, clients assign more significance to their prior knowledge and expectations. According to Patterson (2000) and Stock and Merkle (2018), most clients develop active rather than passive expectations of high involvement service provision, as well as specific expectations of a technology (e.g. social robots and AI) that represents the capabilities of service firms. Successful service outcomes offer an indicator of satisfactory service provision, so clients reasonably rely on their expectations when considering whether to feel secure and use robo-advisors. To illustrate, an actuarial science graduate (male, 27 years) stated that ‘. . .its (robo-advisors’) services are only about the results it generates from managing our investments. Does its performance meet our expectations? I think it’s all about results. . .’. A governmental employee (male, 30 years) also reported that ‘I expect robo-advisors to look after my investment and report their results regularly, answer my inquiries, and watch out for new investments that interest me’.

Although expectations can be defined in multiple ways, such as predictions of future performance (Oliver, 1980), desires or ideals (Spreng & Olshavsky, 1993) or norms grounded on past experience (Cadotte et al., 1987), clients demonstrate their expectation of professional service performance by predicting future services operation (Patterson et al., 1996). Such performance expectations arise prior to the purchase or adoption of a service, in accordance with the UTAUT’s definition of performance expectancy (Venkatesh et al., 2003), or the extent to which clients believe that using a technology will help them achieve their goals.

Performance expectations should influence attitudes, which shape behavioural intentions (Dwivedi et al., 2019). Therefore, clients with heightened expectations of the robo-advisors’ performance might achieve more psychological comfort with regard to robo-advisors, because the expectations grant them greater peace of mind, ease and security. Clients’ expectation that robo-advisors can perform effective analyses, offer prompt responses and notifications and generate acceptable financial returns at some level of risk should affect their degree of psychological comfort (Belanche et al., 2019). Thus, we hypothesise:

Influence of technology readiness on client psychological comfort

Consistent with Parasuraman (2000) and Son and Han (2011), people’s technology readiness indicates their preparedness and willingness to employ new technologies, based on their attitudes and beliefs regarding technology in general. According to Parasuraman (2000) and Parasuraman and Colby (2015), technology readiness consists of four dimensions. First, optimism refers to people’s positive views of technology and beliefs that they can gain controllability, flexibility and efficiency in life by using technology. Optimistic users are open to new technologies, disregard negative outcomes and see new technologies as sources of increased convenience. Second, innovativeness indicates people’s propensity to experiment with new things, such that they tend to be less affected by uncertainty or unexpected outcomes of the technology. Third, insecurity includes doubts about the technology’s security or privacy, prompting distrust in specific aspects of technology-based transactions, not a loss of control over new technologies as a whole. Fourth, discomfort results from perceptions of limited control over technology in general and a sense that technology is excessive. These users develop general fears of services that are technology-oriented, which demand learning costs and appear difficult to understand. As this description shows, the measure of technology readiness thus parallels the UTAUT’s effort expectancy or ease of using the technology (Venkatesh et al., 2003).

In the financial services industry, people with greater technology readiness tend to express positive attitudes towards using a new technology, exhibit more actual usage and adopt innovative technology more extensively (Liljander et al., 2006; Lin & Chang, 2011; Massey et al., 2007). Clients experienced in investing, who also are tech-savvy and risk-takers, are likely to use robo-advisory services (Jung et al., 2018). Furthermore, when they encounter technology-based services like robo-advisors, people with high technology readiness may tend to be more emotionally comfortable with them, due to their innovativeness and optimism.

These views were supported by our interviews. A marketing manager (female, 32 years) stated ‘. . .if clients are not familiar with technology, especially those involved with AI, they could fear of making mistakes when using it, like, what if we accidentally press this button and all the money is gone?’. Hence:

Influence of client suspicion towards human advisors on client psychological comfort

DeCarlo and Barone (2009) assert that some clients express adverse apprehension towards salespeople, anticipating ulterior motives in response to some unexpected, inconsistent, or self-serving situational cue. Such expectations might be reasonable, considering the adverse publicity in recent times that human financial advisors, and the industry generally, have frequently acted in an unethical manner (Maley, 2020). In Thailand, The Financial Consumer Protection Centre reported a growing number of client complaints on services received from human advisors, including their behaviour, incompleteness of financial documents and information, and selling products not suited to client needs (Bank of Thailand, 2022). In Australia, the government faced frequent complaints and evidence of dishonesty and impropriety in financial services (e.g. clients not receiving objective and suitable advice, advisors having undisclosed conflicts of interest, or clients being charged for no advice) resulting in the launch of a Royal Commission of Enquiry in 2017 (Hayne, 2018). This caused resignations of directors, and decreasing client trust in human financial advisors (Janda, 2014).

During persuasive encounters, such suspicions can lead clients to predict the salesperson is about to engage in a ‘hard sell’ or develop other negative views of the salesperson, reducing the likelihood that the encounter results in a sale or other behavioural outcome sought by the seemingly insincere salesperson (Campbell & Kirmani, 2000). In examining client suspicion in professional service encounters, DeCarlo and Barone (2009) found clients assess ulterior motives by gauging the salespeople’s behaviour, comments or opinions. If a service provider displays ulterior motives (e.g. commission-based), it increases client suspicion and negative interpretations of the agent’s actions (Campbell & Kirmani, 2000; DeCarlo, 2005), as well as lowering positive ratings of the sales agent’s sincerity. As noted earlier, this might be regarded as being akin to behavioural norms in UTAUT. Although somewhat similar to distrust (of a salesperson or service provider), distrust refers to negative expectations about another’s motives and a definitive negative judgement (Kramer, 1999), whereas client suspicion implies a process or state of mind that causes clients to seek additional information, which effects the attitude formation process and purchase intentions (DeCarlo, 2005; DeCarlo et al., 2013).

Our qualitative interviews support the contention that client suspicion of human financial advisors plays a substantial role among clients who opt for robo-advisors. An exporting (female, 43 years) reported her feelings towards human advisors as ‘I don’t really want to consult with human advisors. Some of them, especially those advisors of some certain banks, they just offer their bank’s financial products without asking if we really need them or if they suit with our goals’. Clients also questioned human advisors’ knowledge, as an actuarial science graduate (male, 27 years) mentioned ‘Sometimes human advisors are not even that proficient in what they suggest. They encourage us to invest in a particular stock. But, when we ask them the reason, they can’t answer. It is like they are told to sell”’. Moreover, an entrepreneur (male, 37) stated ‘People still see (human) service employee managing investments and insurance very much as a “salesperson” (who offers hard sell). When it comes to lots of money, they need to make clients feel at ease in investments. Don’t use people who could put pressure on clients’.

As some clients anticipate ulterior motives from salespeople through observed behaviour, communications and opinions, robo-advisors on the other hand are not subject to any human judgement biases or analysis errors. They offer superior forecasting accuracy (Jung et al., 2018). that is, they recommend financial investment selections on the basis of a quantitative analysis, with no bias or ulterior motives (Belanche et al., 2019). Accordingly, with recent adverse publicity of the industry in mind, client suspicion with human financial advisors is likely to lead them to prefer and opt for robo-advisors, reflecting their greater psychological comfort. We therefore expect that:

The influence of performance expectations and client suspicion on psychological comfort all may vary across clients’ heterogeneity. In our qualitative interviews participants repeatedly mentioned two themes that represent boundary conditions in gaining psychological comfort with robo-advisors: clients’ knowledge and confidence in making sound investment decisions (Hohenberger et al., 2019) and their preferences for a human touch (Zhang et al., 2021). With the current context in mind, these are regarded as facilitating conditions in the UTAUT model. No compelling argument could be advanced for moderating effects for the technology readiness–psychological comfort linkage. We now explore the two moderating variables.

Moderating role of client confidence in financial information search

Bearden et al. (2001) define confidence in information search as the extent to which a person feels proficient and confident in his or her decisions and behaviour in a marketplace. Such confidence is associated with proactive information gathering and processing, as well as consideration set formation. Client confidence in information search is akin to self-efficacy, or a belief that one can produce expected outputs and achieve success in particular tasks. In turn, it should amplify self-assurance about making sound investment decisions and achieve desirable outcomes, at an acceptable level of risk (Fernandes et al., 2014).

Clients who possess a slight financial knowledge and acumen regarding financial investments and planning might prompt them to have positive attitudes and accept robo-advisors. According to Fernandes et al. (2014), client confidence in financial information search should increase clients’ self-assurance about making proper investment decisions and reaching desirable outcomes. An expectation of robo-advisors’ performance generates more comfortable feelings when clients feel they are proficient in financial products and in searching for information prior to service adoption. In other words, clients’ performance expectations will have stronger association with comfort when clients have higher (rather than lower) confidence in their information search. Furthermore, as previously argued in H3, suspicion of human financial advisors is predicted to increase client psychological comfort with robo-advisors. In this case, we predict that the positive association between suspicion and comfort will be stronger when clients have higher confidence in their ability to search and evaluate financial information as it reinforces their suspicions about human advisors’ propensity to engage in a hard sell (Campbell & Kirmani, 2000). Finally, we posit a direct negative association between search confidence and comfort because clients having high confidence in their abilities to search for financial information may be less comfortable relying on an AI-based technology for making their investment decisions. As an actuarial science graduate (male, 27 years) stated, ‘Robo-advisors could be suitable to those who have no or inadequate knowledge of financial investment. But, for those who have a certain level of knowledge, they might invest on their own where they can make decisions based on their insights and perceived risks’. Thus, we hypothesise:

Moderating role of need for human interaction

Many professional service encounters, and financial advisory services in particular, feature human interaction that clients come to expect (Collier & Kimes, 2013; Sharma & Patterson, 1999). The personalised nature of a service provider–client relationship can enhance the client’s service experience (Taufik & Hanafiah, 2019). Some clients display a strong need for human contact when searching for information and purchasing technically, complex services, so they seek personalised relationships (Dalla Pozza et al., 2017).

In a technology-based service context, clients’ preference for interacting with a service employee varies. For example, Wang et al. (2013) found that even with a relatively unsophisticated technology (e.g. supermarket self-checkouts), there was a segment that preferred dealing with a human-being at check-outs. Other studies have empirically shown that a high need for human interaction or personal services has been found to diminish clients’ intention to use self-service technology (Taufik & Hanafiah, 2019). These clients feel more comfortable when interacting with humans to reduce perceived risk of making undesirable decisions (Dalla Pozza et al., 2017). Finally, and in a similar vein, the notion of algorithm aversion (Dietvorst et al., 2015) has shown that a large segment of consumers believes humans make better decision than AI, irrespective of the evidence demonstrating AI systematically makes better decisions. Therefore, among clients with a greater need for human interaction, the effect of their expectation of robo-advisors’ performance in driving psychological comfort is expected to be weaker. And in a similar vein, the positive association between suspicion of human advisors and comfort will be weaker for clients who have higher need for human interaction because they likely perceive interactions with human service provider as more crucial (Collier & Kimes, 2013; Dabholkar, 1996).

These views were supported by our qualitative interviews. A marketing manager (female, 32 years) stated that ‘. . .For this kind of services, we want to know the (human) advisor at a certain level. We have to know and trust the advisor well enough. The advisor needs to know our background: how much risk we can take, what kind of (financial) situation we’re in, and be able to guide us in investment. This makes me feel safer than using AI’. Her statement is supported by a business analyst (female, 45) who mentioned that ‘. . .Human advisor makes me feel more contented than AI, even though AI is smarter. With human, we can ask question and get immediate answers. I myself want to ask questions why the outcomes turn out the way it is. The advisor can explain how the risk occurs and for how much, and then let us make the decision. So, they really provide reasons for us and make us feel comfortable and attended”’.

Furthermore, we posit a negative direct effect between need for human interaction and psychological comfort. Logic dictates that clients that have a strong need for human interaction in service encounters would likely feel less comfortable using a complex, sophisticated technology such as robo-advisors to recommend their investment decisions. Accordingly:

Influence of client psychological comfort on intention to use and percentage of investment via robo-advisors

As previously noted, psychological comfort represents feelings of security, reassurance peace of mind and reduced anxiety in choice decisions. Humans actively and constantly seek to enhance and/or sustain feelings of comfort about their environment and decision making (Simmons, 2001). Research has investigated psychological comfort in multiple disciplines including sociology, psychology, humanities and business (Lloyd & Luk, 2011; Spake et al., 2003). Feelings of comfort have shaped clients’ assessment of service quality (Butcher et al., 2001) satisfaction (Dabholkar et al., 2000) and even trust in a financial auditor (Sarapaivanich et al., 2019).

Anxiety is a critical emotional influence with a negative impact on intentions to use (Hohenberger et al., 2019). Decreasing such anxiety instead should enhance these intentions and increase behavioural usage. In the case of robo-advisors, being a high involvement credence service, associated with considerable (financial) risk and associated anxiety, logic and previously cited studies suggest that psychological comfort will reduce anxiety around decision making (Hohenberger et al., 2019) and is therefore positively associated with intentions to adopt robo-advisors. Logic also dictates that clients would invest more of their investment portfolio via robo-advisors when they feel comfortable with robo-advisors. Therefore:

Methodology

A mixed method approach comprising two studies was undertaken to meet the research objectives. We selected Thailand as the research setting, reflecting the rapidly growing number of Thai firms planning to offer robo-advisory services (Pivotal Sources, 2017; World Market Intelligence News, 2017). Thai clients appear strongly interested in employing robo-advisors, whether they are new to investing, or experienced investors (Mir & Ilyas, 2016). Moreover, Thailand is a highly collectivist South-East Asian culture and as such people in general are considerably more risk averse than their counterparts in highly individualist societies (e.g. USA, England, Australia) (Hofstede, 1991), causing challenges to firms offering robo-advisors. Thus, this setting is highly related to our examination of client psychological comfort with robo-advisors, intention to use and percentage of robo-advisor usage.

The first data collection involved qualitative, in-depth interviews with current clients of financial advisory services. The purpose was to verify constructs identified from the literature and gain an understanding and insights concerning other possible antecedents of psychological comfort and intention to use robo-advisors. We sent invitations to 10 interviewees who were clients investing through services offered by human financial advisors and/or online investment banking (non-AI-based) applications. The interviewees must have had experience with at least one financial planning or investment service to qualify for the interview. The sample included six males and four females, aged between 20 and 46 years. They resided in major cities in Thailand (Bangkok and Chiang Mai). None of the respondents had previously used robo-advisors. Their experience with financial planning or investment service ranges from 1 year to over 10 years. Their current financial advisory services included money market funds, fixed income funds, mixed funds, flexible funds, sector funds, equity funds, alternative investment funds, foreign investment funds and stocks. These criteria explain the target clients of most Thai financial advisory firms intending to introduce robo-advisors.

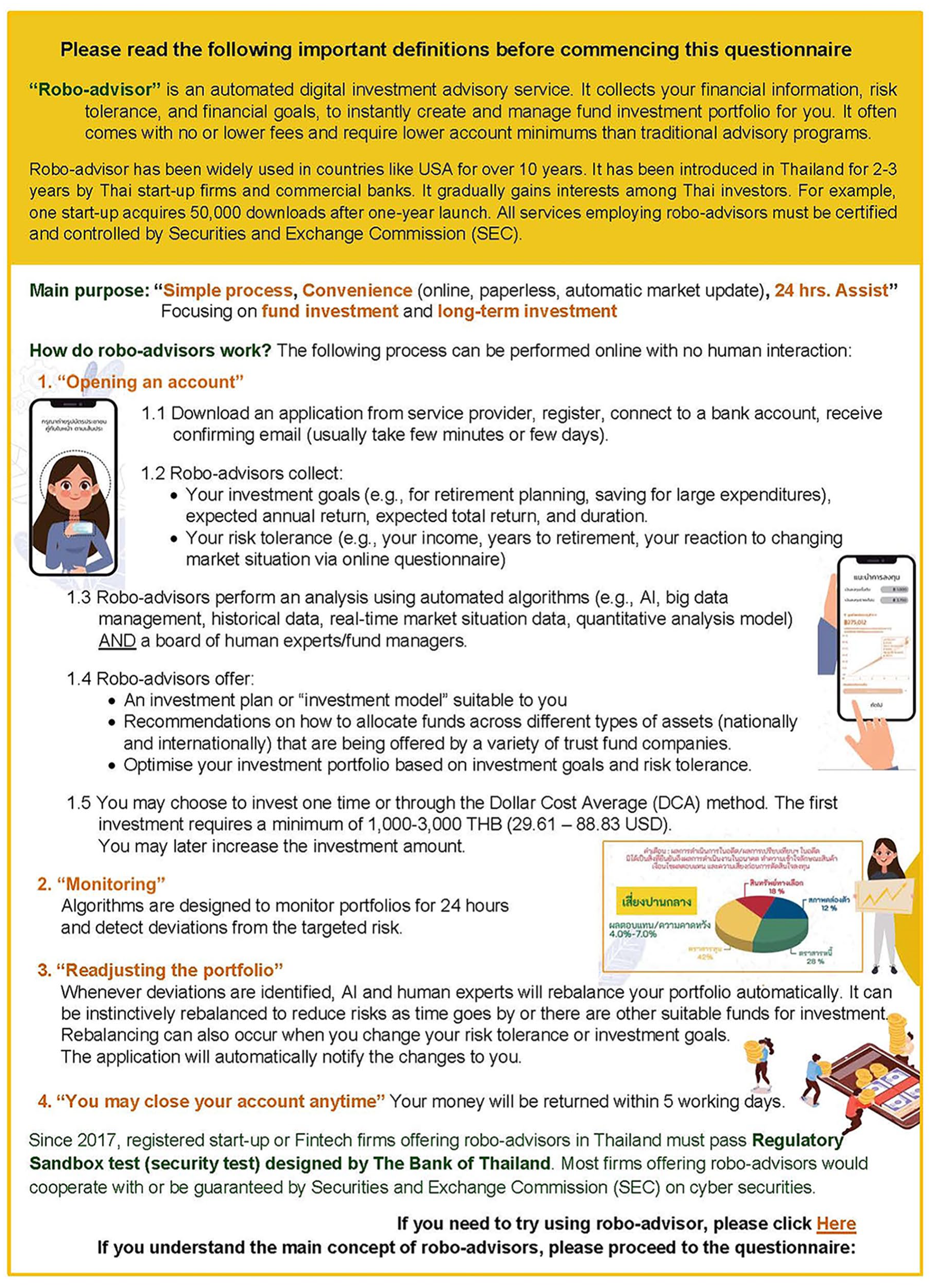

We first provided each participant with a detailed description of robo-advisors and its capabilities (see Figure 2). The interview topics included clients’ perceptions and opinions towards robo-advisory services, covering their capabilities, the differences compared to human advisory services, clients’ feelings towards the services provided by robo- and human advisors, and reasons for choosing or rejecting robo-advisors. Each interview took approximately 40 to 50 min and was recorded. We analysed the data using an inductive thematic analysis to identify themes directed by the content of data, before analysing and reporting the themes (Braun & Clarke, 2006). Since the objective of this study is to glean the antecedents of client psychological comfort and intention to use robo-advisors, thematic analysis offers flexibility and detailed explanation of data. We started with familiarising ourselves with the depth and scope of the interview transcriptions and then developed initial codes, searched for themes and refined the themes found. Finally, each theme was matched with existing variables, based in SST services literatures, that share similar attributes.

Vignette of background and facts of robo-advisors.

The second data collection involved a cross-sectional survey to quantify the impact of client psychological characteristics on psychological comfort, as well as examine the moderating effects of client confidence in financial information search and need for human interaction. Data was collected from clients currently investing or receiving financial planning services from human financial advisors and/or online banking applications (i.e. investing by themselves with minimal assistance from human employees). In addition, we collected data from clients who expressed an interest in investing or engaging in financial planning services in the next 12 months. None of the respondents had previously used robo-advisors. They reside in major cities in Thailand (Bangkok, Chiang Mai, Khon Khaen, Chiang Rai and Lamphang). Their existing financial advisory services included money market funds, fixed income funds, mixed funds, flexible funds, sector funds, equity funds, alternative investment funds, foreign investment funds, stocks, bonds, ETF, derivative warrants, options, futures and cryptocurrencies.

Researchers sought out potential respondents in finance conferences and personal channels, filtering whether they currently invested or used any financial advisory services or were interested in such in the next 12 months. If so, the researcher informed them about the study objectives, questionnaire structure and the required task, namely, spending a few minutes reading a vignette (Figure 2) that described the background, process, features of a robo-advisor and interactions that clients would have with them. The vignette, previously pretested with financial advisory clients, contains pictures and descriptions to ensure clients’ understanding of robo-advisors’ features. After reading the vignette about robo-advisors and indicating they understood their features, respondents started the questionnaire and submitted their answers online through a link provided. The link required completions of all responses before sending.

The 548 responses included 284 current investors or recipients of financial planning services and 264 respondents who were interested in using a financial advisory service in the next 12 months. In addition, 68.1% of respondents were male, and about one-third of them were employed by private companies. In terms of age, 35 to 44 years of age represented 41.6%; in terms of income, 42.2% earned 20,001 to 30,000 Thai baht (620–930 US dollars) per month. Among respondents who were investing or currently receiving financial planning services, the most common length of investment was 1 to 5 years (86.7%), and they mostly made investments themselves through mobile applications or websites (53.7%), rather than relying on a human financial advisor or broker (46.3%). Money market funds, stocks and bonds were the most chosen investments (86.1%). Among respondents interested in financial advisory services, they expected investment lengths of 1 to 5 years (86.5%) and were mostly interested in money market funds, stocks and bonds (77.1%).

Measures

We performed a forward–backward translation procedure (Hambleton, 1993) with the questionnaire. The questionnaire was developed in English, and then two bilingual speakers whose native language is Thai translated the questions. The questions were back-translated by two other bilingual speakers whose native language is English (Brislin et al., 1973). Ten respondents pretested the Thai-language questionnaire to certify the equivalence of the meanings, phrases and words and suggested some modifications (Brislin, 1980). The two versions of the questionnaires also were sent to marketing academics in Thailand and Australia, who assessed their face validity and provided additional feedback on the appropriate wording.

All the measurement scales were sourced from prior literature. We adopted Patterson et al.’s (1996) expectation scale to measure performance expectation, with seven items related to our context, each following a prompt that read, ‘If I was to become a client using robo-advisory services, I expect. . .’. We used Parasuraman and Colby’s (2015) technology readiness index (TRI) 2.0 but limited it to eight items after excluding some items to ensure the appropriateness of the context and avoid redundancy, as suggested by experts during pretesting. The scale still covers four dimensions of technology readiness. For the measure of consumer suspicion, we employed two items from DeCarlo and Barone’s (2009) scale and two questions derived from our in-depth interviews. We also prompted respondents to think about their attitudes about most human financial advisors before answering. Fernandes et al.’s (2014) five-item scale provides the measure of client confidence in financial information search. We measured need for human interaction with a four-item scale from Dabholkar (1996) and Collier and Kimes (2013). All the preceding variables were measured on seven-point Likert scales (1 = ‘Strongly disagree’ and 7 = ‘Strongly agree’).

We adopted Spake et al.’s (2003) six-item psychological comfort scale to measure respondents’ levels of psychological comfort with robo-advisors on a seven-point semantic differential scale with word pairs (e.g. uncomfortable/comfortable, very uneasy/very much at ease, very tense/very relaxed). The questionnaire asked respondents ‘After examining and thinking about robo-advisor, what would be your feelings if you were its client?’, then presented the items. We measured respondents’ intention to use robo-advisory services by asking, ‘After examining and thinking about robo-advisors, what is the likelihood of investing with robo-advisors in the next 12 months?’ and providing a five-point scale (1 = ‘No chance’ and 5 = ‘Certain’). Next, to assess respondents’ percentage of investing through robo-advisors, immediately after they indicated their intentions to use robo-advisors, the questionnaire provided the following item: ‘If you answer 3 (Some chance) to 5 (Certain), what percentage (%) of your investment portfolio would be invested via robo-advisors?’ They could choose one number on a five-point scale (1 = ‘0–25%’ and 5 = ‘76–100%’). The two latter variables were adopted and adjusted from Yim et al. (2012).

As approximately half the sample were currently using a financial advisory service and the other half was seriously considering investing in the next 12 months, we include this (‘client status’) as a covariate in the structural model analysis. As approximately half the sample had no investment experience, it was not possible to include investment experience and mode of investment as covariates. Age and income were included as covariates as they tend to influence financial behaviour (Henager & Cude, 2016). Their inclusion provides a more robust test of our hypotheses.

Analysis

Measurement model

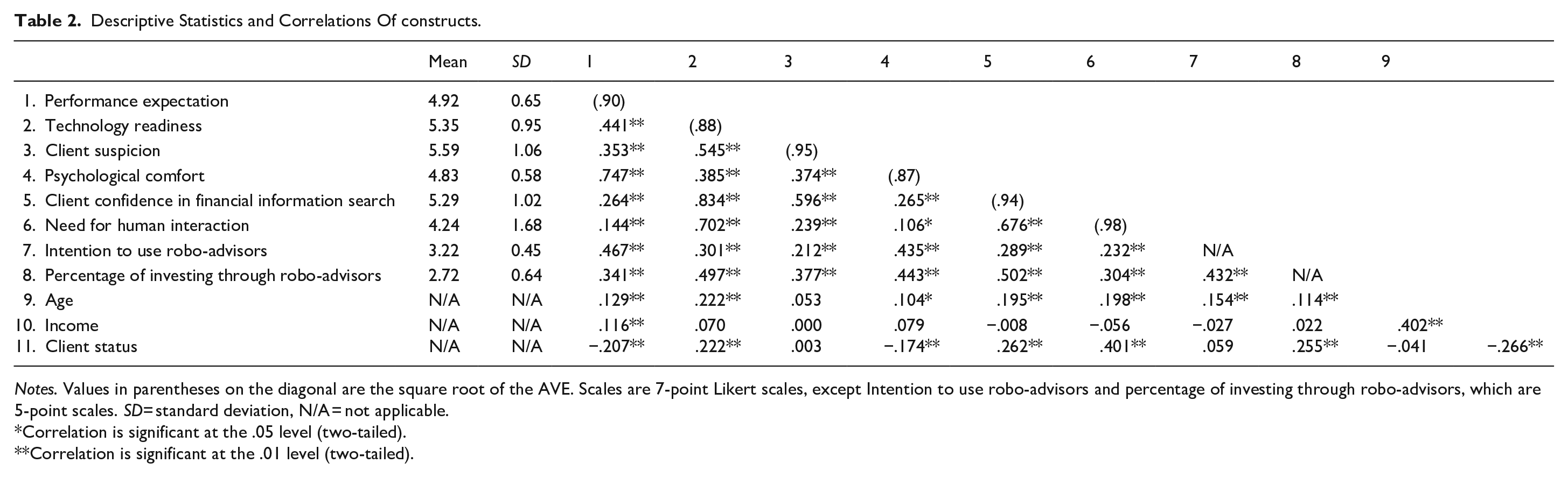

None of the respondents had prior experience with robo-advisors, so we pooled the survey data from current clients of financial planning services with those of interested clients but still controlled for this by including ‘client status’ as a control variable. A confirmatory factor analysis using AMOS v22 reveals that the model fit the data relatively well (Table 1): χ2/df = 3.340, p < .001, comparative fit index (CFI) = .96, Tucker-Lewis index (TLI) = .95, incremental fit index (IFI) = .96, goodness-of-fit index (GFI) = .84, adjusted goodness-of-fit index (AGFI) = .80, root mean square error of approximation (RMSEA) = .065, PCLOSE < .000, and standardised root mean square residual (SRMR) = .04. The CFI, TLI and IFI all surpass the suggested threshold of .90, so the model appears parsimonious. In addition, the items produce significant (p < .001) estimates of more than .50 and thus share high variance within constructs. In Table 3 we report standard coefficients for both the measurement model and structural model. For all constructs, the average variance extracted (AVE) values are above .50, denoting convergent validity. Reliability is satisfactory, with Cronbach’s alphas ranging .96 to .98 and composite reliability above .70 (Bagozzi & Yi, 1988; Hair et al., 2010). The square root of the AVE for each construct is greater than its shared variance with any other construct, indicating discriminant validity for all constructs (Fornell & Larcker, 1981). Table 1 lists the items encompassing each construct, reliabilities and AVE. Table 2 shows their correlations.

Measurement Model Results.

Note. α = Cronbach’s alpha; CR = composite (construct) reliability; AVE = average variance extracted. Loadings are standardised; all t-values are significant (p < .001).

Descriptive Statistics and Correlations Of constructs.

Notes. Values in parentheses on the diagonal are the square root of the AVE. Scales are 7-point Likert scales, except Intention to use robo-advisors and percentage of investing through robo-advisors, which are 5-point scales. SD= standard deviation, N/A = not applicable.

Correlation is significant at the .05 level (two-tailed).

Correlation is significant at the .01 level (two-tailed).

Common method bias

Our online survey-based, cross-sectional approach with single respondents’ data could create some common method bias, so we imposed procedural controls (Podsakoff et al., 2003) and conducted common method variance assessments (Malhotra et al., 2006). As procedural remedies, we ensured that the measurements contain different response formats. Likert scales and semantic differential scales also are separated with various end points. The cover page guaranteed the anonymity and confidentiality of participants. As a statistical remedy, we performed a marker variable assessment (Lindell & Whitney, 2001; Malhotra et al., 2006), with occupation as a marker variable to control for common method variance (rM = .04, p = .50). The mean change in correlations of the eight focal variables (rU – rA) when we partialled out the effect of rM is .02, indicating no significant issue with common method bias.

Structural model and hypothesis testing

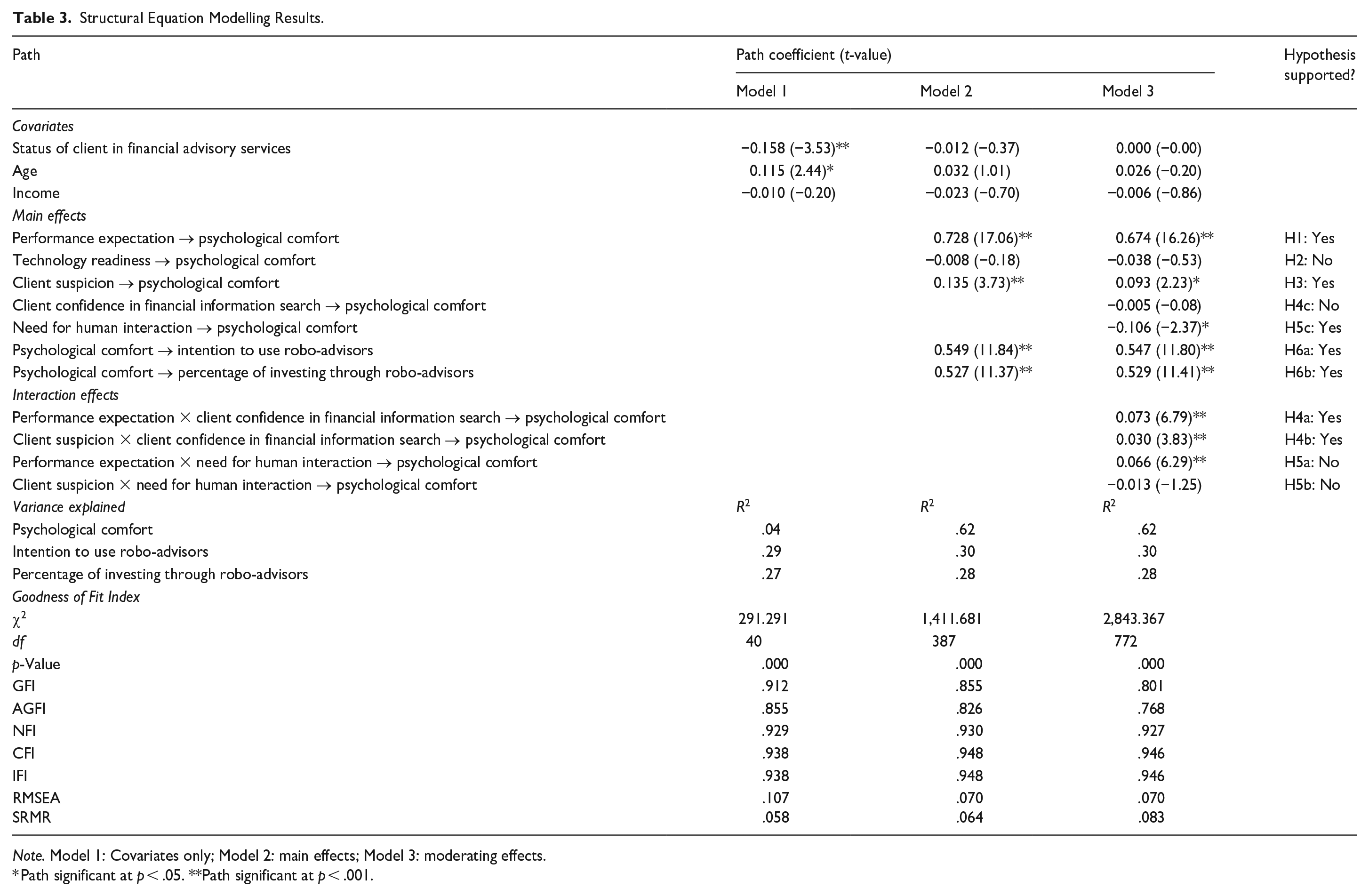

We started by testing the main effects model (Model 2, Table 3), which achieves acceptable fit: χ2/df = 3.648, p < .001, CFI = .95, TLI = .94, IFI = .95, GFI = .86, AGFI = .83, RMSEA = .07, PCLOSE < .000 and SRMR = .06. Performance expectation (β = .73, p < .001) and client suspicion (β = .14, p < .001) have significant positive impacts on psychological comfort. However, technology readiness does not yield a significant impact (β = −.01, p < .854). Psychological comfort in turn exhibits significant positive effects on intention to use robo-advisors (β = .55, p < .001) and percentage of investing through robo-advisors (β = .53, p < .001). The squared multiple correlations of psychological comfort, intention to use and percentage of investing are .62, .30 and .28, respectively.

Structural Equation Modelling Results.

Note. Model 1: Covariates only; Model 2: main effects; Model 3: moderating effects.

Path significant at p < .05. **Path significant at p < .001.

Next, we tested a full model that contains the predicted moderating effects (Model 3, Table 3). It achieves acceptable fit with the data: χ2/df = 3.683, p < .001, CFI = .95, TLI = .94, IFI = .95, GFI = .80, AGFI = .77, RMSEA = .070, PCLOSE < .000 and SRMR = .08. Performance expectation (β = .67, p < .001) and client suspicion (β = .09, p < .025) remain significant, with positive associations with psychological comfort, whereas technology readiness still has no significant relationship (β = −.04, p < .598). We thus find support for H1 and H3 but not for H2. Psychological comfort generates a significant positive impact on intention to use robo-advisors (β = .55, p < .001) and percentage of investing through robo-advisors (β = .53, p < .001), as we predicted in H6a and H6b. The squared multiple correlations of psychological comfort, intention to use and percentage of investing are .62, .30 and .28, respectively.

With regard to the moderators, we find support for H4a and H4b. The positive association between performance expectation and psychological comfort is moderated by client confidence in financial information search (β = .07, p < .001), such that the impact of performance expectation in developing psychological comfort is slightly stronger when clients are more confident in their financial skills. This confidence also positively moderates the effect of suspicion of human advisors on psychological comfort with robo-advisors (β = .03, p < .001), such that the effect of client suspicion is marginally greater when clients are more confident in their ability to search for financial information. However, client confidence in financial information search has no significant direct association with psychological comfort (β = −.01, p < .935). Thus, H4c is not supported. The moderation effects of need for human interaction contradicts our predictions. The positive link between performance expectation and psychological comfort is positively moderated by need for human interaction (β = .07, p < .001), contrasting with H5a. The association of client suspicion of the human advisor and psychological comfort is not moderated by a high need for human interaction (β = −.01, p < .210), so we cannot find support for H5b. The need for human interaction has a negative direct relationship with psychological comfort (β = −.11, p < .018), supporting H5c. Finally, none of control variables (client status, age, income) had a significant impact on psychological comfort.

Mediation analysis

The model in Figure 1 indicates that psychological comfort mediates the relationship between client psychological characteristics (performance expectation, technology readiness, client suspicion) and two dependent variables (intention to use robo-advisors, percentage of investments). With a post hoc analysis, we test formally for the mediating effects, using a bootstrapping procedure with 2,000 bootstrap samples (Hayes, 2013; MacKinnon et al., 2007). In the base model (main effects), we find significant positive, indirect effects of performance expectation (β = .16, p < .001) and client suspicion (β = .02, p < .001) on intention to use robo-advisors, through psychological comfort. Also, there are significant positive, indirect effects of performance expectation (β = .22, p < .001) and client suspicion (β = .03, p < .001) on percentage of investment, through psychological comfort. For the full model with moderating effects, we identify significant positive, indirect effects of performance expectation (β = .15, p < .001) and client suspicion (β = .01, p < .028) on intention to use robo-advisors, through psychological comfort. Also, significant positive, indirect effects of performance expectation (β = .21, p < .001) and client suspicion (β = .02, p < .038) on percentage of investment, through psychological comfort are present. This, by and large, reveals that psychological comfort acts as a full mediator with complete mediation for the relationship between performance expectation, client suspicion and the two dependent variables.

It should be noted that an alternative model with technology readiness, client confidence in financial information search, client suspicion and need for human interaction as antecedents, and performance expectations and psychological comfort as mediators was tested. However, the results did not provide a superior fit to the hypothesised model.

Discussion

Our study is one of only a handful of empirical studies that model customer acceptance of a high involvement, complex, artificial intelligence (AI)-based technology. Robo-advisors are AI-driven professional financial services that offer personalised investment recommendations to clients with little or no human involvement. Most studies of customer adoption of technology have been conducted with low involvement, less sophisticated technologies. Robo-advisors are not only a high involvement service, but also a service high in credence properties where clients’ financial returns only become apparent over time. Hence, clients typically have difficulty assessing outcomes (and risk) before and even after purchase, meaning client psychological comfort is vital for service adoption.

While most of our predictions were confirmed, perhaps the most important finding was the critical mediating role of psychological comfort. Psychological comfort refers to feelings of security, reassurance, peace of mind (Scitovsky, 1992), reduced anxiety (Daniels, 2000), ease and relief of mental distress (Simmons, 2001) which reduces the sense of risk in investing via robo-advisors. In the current context of a high involvement decision, it is a vital affective response that signifies acceptance of robo-advisors. Comfort significantly increases intentions to use, and the percentage of a client’s portfolio invested through robo-advisors. This is in accord with Hohenberger et al.’s (2019) prediction that affective responses (i.e. psychological comfort as opposed to anxiety) can indicate clients’ willingness to use/purchase. It also aligns with Venkatesh et al. (2003) that clients’ attitude affects actual usage behaviour. Hence, psychological comfort emerges as a vital affective response that signifies whether clients who develop expectations about robo-advisors’ performance and have suspicions that human advisors hold ulterior motives will be willing to use and allocate more of their investments to robo-advisors. Clients’ performance expectations of robo-advisors were associated with psychological comfort. Higher performance expectations, were significantly associated with higher levels of client psychological comfort with robo-advisors. Next, clients’ suspicion of human financial advisors (i.e. that human advisors often have ulterior motives when suggesting financial investments) is also associated with greater psychological comfort with robo-advisors. That is, the stronger the suspicion of human advisors, the greater the likelihood the clients would feel comfort and adopt robo-advisors for their investment advice. However, we do not find that clients’ technology readiness generates psychological comfort, although our qualitative interviews indicated clients’ self-perceived confidence in using technology was a consideration for psychological comfort and acceptance of robo-advisors. The analysis suggests that this effect might be dominated by performance expectations and client suspicion. So, to build psychological comfort in an introduction stage of new high-involvement, AI-based SST technology, clients might turn more to their optimistic expectations of the robo-advisors’ performance, rather than their perceived difficulties in using the technology. In other words, clients’ overriding consideration is whether they confidently expect to receive desired financial returns at an acceptable level of risk (Beach, 2020; Natixis, 2017).

The level of confidence the clients have in their ability to undertake financial information search also generates a small but significant moderating effect on the relationship between performance expectations and psychological comfort, such that this link grows stronger among clients who feel assured about their information search and decision making. Moreover, client confidence in financial information search has a significant, but again small moderating effect on the association between their suspicion and psychological comfort, reinforcing this positive association. This is also supported by our qualitative interview findings. In contrast, we find some conflicting results related to the moderating effect of need for human interaction. The positive impact of performance expectations on client psychological comfort is strengthened when clients have a high need for human interaction, opposing our prediction. Although initially seeming counterintuitive, it appears that, among clients with a greater need for human interaction, their reliance on robo-advisors’ expertise, deliberation and effective financial recommendations might be perceived as equivalent to those resources offered by a human financial advisor. Moreover, many firms offering robo-advisors currently provide human interaction/assistance upon clients’ request or demands. Our description of robo-advisors in a vignette (Figure 2) also explains that AI in conjunction with a human expert will rebalance clients’ portfolio automatically. This would seem to explain the unexpected findings of the positive interaction between need for human interaction and performance expectation on psychological comfort. The finding adds to our interview results that, the stronger a client need for human interaction and assistance, the higher they expect robo-advisors to perform correspondingly well to gain psychological comfort. In other words, the impact of robo-advisors’ performance expectations on client psychological comfort becomes stronger. However, the positive influence of suspicion of human financial advisors on psychological comfort is not significantly weakened, even if the direction of the effect is negative, as predicted. Need for human interaction was also shown to have a direct, negative association with psychological comfort. In other words, the greater a client’s preference for interacting with a human in a service encounter, the less likely they were to use an AI based algorithm such as robo-advisors.

Theoretical contributions

This study offers several contributions to the literature. First, it adds insights to the professional service literature regarding smart, credence-based SST and AI-grounded technology by showing that psychological comfort to be a critical mediating variable between the antecedents and robo-advisors usage intention, and so supporting information economic theory (Darby & Karni, 1973). Robo-advisors represent a high-credence, professional service that features more technical and information complexity than most traditional SST settings. Being high in credence properties invokes the importance and central mediating role of psychological comfort as a means of reducing a sense of anxiety and stress about whether or not to adopt. This is in stark contrast with services possessing search or experience properties where a client can assess the outcome, value and satisfaction upon purchase and consumption.

Second, while past studies employing the UTAUT model have been around static, non-smart technologies, the current study expands the model’s relevance to sophisticated, AI-based SST. The results enhance, in part, Venkatesh et al.’s (2003) UTAUT model in that performance expectancy for a new AI-based smart technology is a major driver of acceptance and usage of that technology. Further, because of the negative press coverage raising suspicions of human advisors, this construct is akin to Venkatesh et al.’s (2003) normative behaviour. Next, in the current context, the two moderators (confidence in information search and need for human interaction) are in effect ‘facilitating conditions’ in the UTAUT model.

Third, we build on and extend Zhang et al.’s (2021) view of clients’ preference for proficient human advisors over robo-advisors by showing that, in this AI-based, highly customised and complex service, clients will accept robo-advisors if they become suspicious towards human advisors’ motives, and when they possess high expectations of robo-advisors’ performance.

Fourth, we also advance prior studies (e.g. Patterson, 2000; Stock & Merkle, 2018) by establishing that clients who have active expectations in high-involvement, AI-based services, are associated with higher levels of psychological comfort. Its influence on client psychological comfort even overshadows the impact of client technology readiness. Prior studies (e.g. Hildebrand & Bergner, 2020) suggest that clients reject robo-advisors if they are compared with human advisors; we show that if they perceive ulterior motives of human advisors, the perception fosters positive feelings towards robo-advisors and behavioural usage intentions.

Finally, as clients of financial advisors are likely to be heterogeneous, our study reveals two key boundary conditions. In other words, not only do we show the antecedents of comfort and acceptance, but we also show under what contingency conditions these antecedents have a stronger or weaker effect. Our study reveals client confidence in their information search capability and need for human interaction have a small but nonetheless significant impact on the relationship between client psychological characteristics and psychological comfort. In doing so we enhance Fernandes et al. (2014), in an AI-based professional services setting, that clients’ self-assurance about making sound investment decisions and gaining anticipated outcomes stimulates the positive influence of client performance expectation and suspicion towards human advisors on psychological comfort. Clients’ proficiency in financial investment helps reinforce their expectations of robo-advisors as well as examining human advisor’s motives. Moreover, this study shows that clients’ need for human interaction does not weaken the positive impact of expectations on robo-advisors’ performance on psychological comfort. We add a dimension to Dalla Pozza et al. (2017) and Taufik and Hanafiah (2019) that, in encountering technically complex services, clients’ preference for human contact escalates a small but positive effect of robo-advisors’ performance expectation on psychological comfort, instead of diminishing it.

Managerial implications

Specialised robo-advisory service firms or professional service firms using AI in general must acknowledge the essential role of client psychological comfort in order to gain acceptance. Most clients are not sufficiently skilled or experienced in financial analysis to evaluate service outcomes confidently. Delivering this high-risk service by relying on an emerging, technologically advanced tool with limited human touch can create client anxiety and concern. Firms should establish effective advertisements and public relations (e.g. case studies, seminars) to encourage clients’ feeling of comfort and robo-advisors adoption. Service firms in other professional sectors that are increasingly adopting AI-based SST or offering fully digitalised services (e.g. medical services) would be well advised to address client psychological comfort to increase the chances of a successful service encounter.

In encouraging client psychological comfort, managers of the robo-advisory service firms should pay close attention to client psychological characteristics and perceptions. As we show, if clients expect more of robo-advisors or are suspicious of the motives of human advisors, their feelings of comfort are greater, as is their usage intention and percentage of investment using robo-advisors – irrespective of clients’ age, income, or client status. To boost clients’ positive expectations, firms should develop clear advertising strategies depicting robo-advisors’ abilities in effectively analysing clients’ investment options, real-time reporting investment performance, generating better than average financial returns and understanding the industry well. To encourage clients who generally suspect human financial advisors’ hidden motives and behaviours, firms might emphasise this by providing hard evidence to certify that robo-advisors can outperform human advisors in terms of non-biased recommendations, coupled with superior speed of execution. A series of real-life case studies (testimonies) might also highlight the superiority of robo-advisors performance.

Targeting efforts might reflect whether clients are confident in their financial information search and know that they can make good financial decisions and investment returns, along with their need for human interaction. Firms might develop online filtering questions, posed when robo-advisors first start providing services, to segment potential clients according to their confidence in financial information search and need for human interaction. If they are confident (i.e. showing their abilities to identify promising financial investments at the beginning of service encounter), robo-advisors could recommend more investment allocation to clients that expect more of robo-advisors’ performance, because their expectations enhance comfort. Similarly, if the clients also show suspicion of human advisors based on prior experience (i.e. questioning general human advisors’ recommendations and knowledge), robo-advisors could suggest more investment portion. In addition, among clients who exhibit moderate to low need for a human interaction, a recommendation to invest through robo-advisors could be automatically offered.

Still, we caution firms against over-promising robo-advisors’ abilities, especially to client groups that are experienced and skilled in financial investing. Excessive claims or advertisements about robo-advisors’ capabilities might raise doubts among these experienced clients and lessen their psychological comfort. Communication strategies developed to attract potential first-time clients also should be designed carefully by featuring realistic descriptions and logical comparisons with financial advice from human advisors.

Limitations and directions for future research

Several limitations of this study deserve notice. In particular, we measure client psychological comfort at one point in time, immediately after clients read about the robo-advisors’ service offering and background. Thus, we cannot capture the dynamics of psychological comfort that might change over time. Spake et al. (2003) refer to psychological comfort as a stable state, but financial advisory services generally persist for an extended time and involve high risk and uncertainty, such that clients’ perceptions and behavioural responses are likely to evolve over time. For example, earning financial returns from parallel investments (e.g. human advisors, online banking) might evoke comparisons with the robo-advisors and their abilities. Further research should attempt to capture the dynamics that mark psychological comfort over time, as financial returns and risk become manifest.

In addition, we included client suspicion of human advisors as a possible influence on psychological comfort after conducting preliminary interviews with Thai clients and confirmed its role in our data collection. Constant news about financial scams and fraud in Thailand has prompted a generalised suspicion that evokes widespread client anxiety and concerns. The results thus might differ in other countries, such as individualist, Western countries (e.g. United States, UK, Europe) in which clients generally rely less on human professional service providers. Another interesting approach for future research might be incorporating clients from both highly collectivist, Eastern countries (Thailand, Indonesia, Japan) who are generally more risk averse and individualist, Western countries to test their level of psychological comfort with robo-advisors at an individual level, instead of a national level.

Next, the respondents in our survey sample were mostly relatively young (41.6% were 35–44 years of age). This age group would be relatively familiar with new AI-based SST compared to older respondents. Although they were the most interested potential clients to Thai financial advisory firms and we incorporate age as one of our controlled variables, future research should apply our findings with caution. Moreover, researchers could investigate other age groups regarding their stimulus and barriers in adopting robo-advisors.

Finally, due to robo-advisors being at the introduction stage, the data were collected only from respondents who had never used robo-advisors. Nonetheless, they were targeted by most Thai financial advisory firms that start to offer robo-advisors. Additional studies might identify clients that have fully adopted robo-advisors (and limited human advisory services) to conduct more research. Such efforts might concentrate on clients’ attitudes and behaviours in terms of selecting and using robo-advisors, instead of human advisors, such that the researchers can capture clients’ perceptions of switching costs or the attractiveness of alternative options, with limited confounding effects.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Thailand’s Office of the Higher Education Commission, the Thailand Research Fund (TRF) and Thailand Science Research and Innovation (TRSI) through the Research Grant for New Scholar Program [grant no. MRG6280094].