Abstract

The purpose of private internal investigations by fraud examiners is to reconstruct the past by identifying past events and sequences of events. In this article, work by fraud examiners is studied in terms of maturity; introduce a five-stage model for investigation maturity: chaos, mess, disclosure, clarification, and investment. Based on student term papers in a financial crime class, six investigation reports are allocated to levels in the maturity model. The average score for the investigation reports is a level 3 disclosure, where the investigation is problem-oriented and often limited by the mandate. Based on the low average score, this article discusses the privatization of law enforcement, secrecy of investigation reports, lack of disclosure to the police, competence of private investigators, and limits of the investigation mandate.

Introduction

Stages of growth models for maturity levels can be used to assess and evaluate a variety of phenomena (Röglinger et al., 2012; Solli-Sæther and Gottschalk, 2015). In this article, we use the concept of maturity levels to evaluate private internal investigations by fraud examiners (Brooks and Button, 2011; Button and Gee, 2013; Button et al., 2007a, 2007b; Schneider, 2006; Williams, 2005). The purpose of this article is to develop the characteristics of investigations at different maturity levels.

This research is important because reports of private investigations tend to be kept secret and never disclosed to the media, the public or even law enforcement (Gottschalk and Tcherni-Buzzeo, 2017). Exceptions in the United States include Valukas’ investigation at Lehman Brothers (2010) and at General Motors (2014).

Based on publicly available investigation reports completed in 2016 and 2017 in Norway, a class of business school students was asked to evaluate maturity levels in their term paper in spring 2017. Student evaluations are presented to illustrate the diversity of maturity levels in private internal investigations.

This article starts with a review of the literature on internal investigations and stages of growth models. Six sample investigation reports evaluated by students are then presented. Student evaluations of the reports are discussed in terms of a five-stage maturity model. Finally, problems related to internal investigations are discussed.

Internal investigations

The purpose of private internal investigations by fraud examiners is to reconstruct the past by identifying past events and sequences of events. The past may be an event or a series of events in which, for example, someone did something to somebody. Previous events are typically negative and have caused some damage. The goal of the investigation is to uncover the facts in a particular situation; the truth of the situation is the ultimate goal. A private investigation mainly occurs after the facts, with the goal of determining what happened and how a negative event occurred, or indeed whether the suspected action occurred at all. The goal may also be to prevent a situation from occurring in the first place, or to prevent it from happening again.

Private fraud investigators are not in the business of law enforcement; they do not to find private settlements when penal laws are violated (Schneider, 2006). Their task is to reconstruct the past as objectively and completely as possible; they should not be in the blame game.

When there are rumors, suspicions or accusations of misconduct and financial crime based on media reports, whistleblowing (Liu and Ren, 2017) or other sources, the affected organization has to react in some way. If management decides to report incidents only to the police, then the case may get out of hand for the affected organization (Gottschalk and Tcherni-Buzzeo, 2016). Therefore, many organizations prefer to hire private detectives to reconstruct past events and sequences of events (Brooks and Button, 2011).

The business of private internal investigations by fraud examiners has grown remarkably in recent decades. Law and auditing firms are hired by both private and public organizations to reconstruct the past when there is suspicion of misconduct and potential financial crime. A criminal investigation is initiated when there is a need to study negative incidents and events that happened in the past. Unlike the police, regulators and other investigative agencies, private financial detectives practice legal flexibility (Brooks and Button, 2011; Button and Gee, 2013; Button, Frimpong et al., 2007; Button, Johnstone et al., 2007).

Internal private investigations examine facts, events sequences, and the causes of negative events, as well as those responsible. Depending on what the hiring party asks for, private investigators can either look more generally for possible corrupt or otherwise criminal activities within an agency or company, or more specifically for those committing potential white-collar crime. In other situations, it is the job of the private investigator to look for potential opportunities for financial crime, so that the agency or company can fix any problems and avoid future misconduct.

Internal investigations include fact-finding, causality studies, change proposals, suspect identification and the assessment of financial irregularities. An inquiry aims to uncover unrestricted opportunities, failing internal controls, abuses of position, and any financial misconduct such as corruption, fraud, embezzlement, theft, manipulation, tax evasion and other types of economic crime (Cebula, 2012; Yearwood and Koines, 2011).

The characteristics of a private investigation include a serious and unusual event, an extraordinary examination to find out what happened or why it did not happen, develop explanations, and suggest actions towards individuals and changes in systems and practices. A private investigator is someone hired by individuals or organizations to undertake investigatory services. A private investigator (PI) also goes under the titles of a private eye, private detective, inquiry agent, fraud examiner, private examiner or financial crime specialist. A PI carries out detailed work to find the answers to misconduct and crime without playing the role of a prosecutor or judge. The PI stops the investigation before passing any judgment on criminal liability.

An internal investigation is a goal-oriented procedure for reconstructing past events. It is a way of creating an account of what has happened, how it happened, why it happened, and who did what to make or let it happen. An internal investigation does this by collecting information, developing knowledge and presenting evidence (Osterburg and Ward, 2014).

Investigations into white-collar crime are a specialized knowledge industry; Williams (2005) refers to it as the forensic accounting and criminal investigation industry. It is unique, set apart from law enforcement, due to its ability to provide “direct and immediate responsiveness to client objectives, needs and interests, unlike police who are bound to one specific legal regime” (Williams, 2005: 194). The industry provides flexibility and a customized plan of attack according to client needs.

Investigations take many forms and have many purposes. Carson (2013) argues that the core feature of every investigation involves what we reliably know. The field of evidence is none other than the field of knowledge. There is an issue of whether we can have confidence in knowledge; this occurs when knowledge emerges in terms of evidence. A PI accumulates knowledge about what happened.

Stages of growth models

An internal private investigation can be evaluated by applying the maturity model given below, which represents theorizing about how the investigation could be improved through management-controlled or random development. A model has the same function as a theory, because the model provides a simplified picture of reality. The steps, stages or levels of the model are: (1) sequential in nature, (2) grow in a hierarchical progression that is difficult or impossible to reverse, and (3) involve a wide range of organizational activities and structures (Röglinger et al., 2012; Solli-Sæther and Gottschalk, 2015).

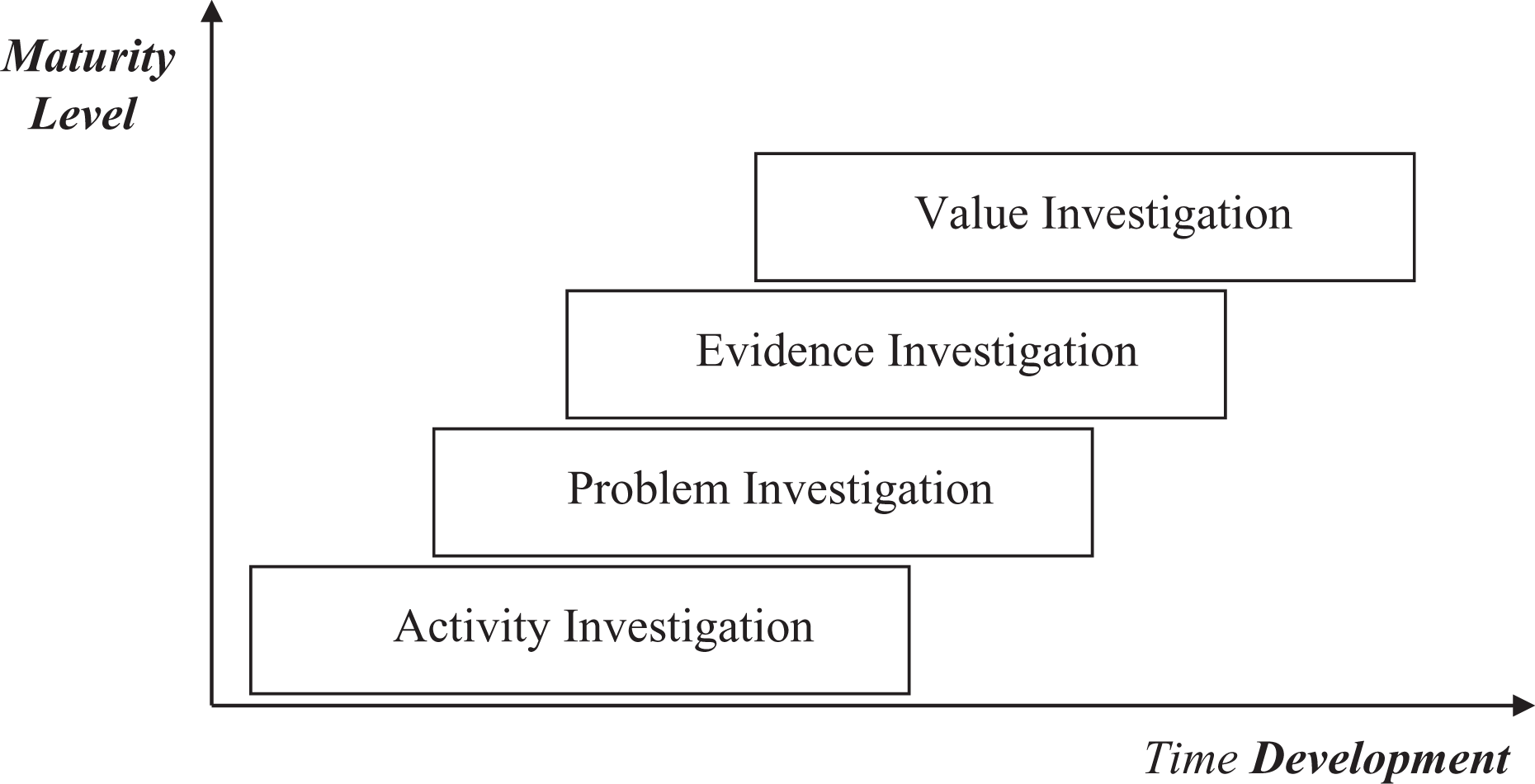

Figure 1 illustrates a potential maturity model for private investigations consisting of four stages, steps or levels.

Maturity model for internal private investigations with four stages.

Level 1 activity investigation

A level 1 activity investigation is focused on activities that may have been performed in a reprehensible way. Examiners are looking for activities in past events and prepare a reconstruction of event sequences. Thereafter, the examiners form an opinion about the activities in terms of whether they are reprehensible. At level 1, auditors and others with accounting and financial transaction knowledge examine and assess activities in terms of assets management. A level 1investigation is usually passive, fruitless and characterized by an unnecessary use of resources; for example, because examiners tend to dig into too many details. At this lowest level, investigators attempt to find answers to the question: What happened?

Level 2 problem investigation

A level 2 investigation is focused on problems and issues that must be solved and clarified. Examiners are looking for answers. When answers are found, the investigation is terminated. It is important to minimize the use of resources in an investigation, which should take the shortest possible time. Appraisal and management are essential for success. The client is faced with an unresolved problem, and the client defines premises for problem-solving. At level 2, there is no room for investigators to pursue tracks other than those that target the predefined problem. At this level, lawyers and others are involved who have a knowledge of the rules and regulations that will identify the facts. Investigations at level 2 are usually passive with trifling results within an agreed cost boundary. At this second level, investigators attempt to find answers to the question: How did it happen?

Level 3 evidence investigation

A Level 3 evidence investigation is focused on revealing something that is kept hidden. Examiners choose their tactics to ensure success in the disclosure of any possible misconduct and white-collar crime. They are looking for the unknown. The investigation steps are adapted to the terrain, where different information sources and methods are used to obtain the most facts. At level 3, detectives, psychologists and other knowledge workers are used to uncover the possible crime. Whereas levels 1 and 2 are focused on predefined suspicions of financial crime, level 3 is focused on the suspicion of there being financial criminals. The focus has shifted from the offence to the offender. There are always criminals who commit crime. Level 3 has a personnel focus, whereas levels 1 and 2 have an activity and legal focus. Level 3 is characterized by the pursuit of responsible individuals, typically executives, who may have abused their positions for personal or organizational illegal gain. This is a more intensive investigation, because suspicions and suspects should be handled in a responsible manner with respect to the rule of law and human rights. Investigations at level 3 are active with significant breakthroughs. New knowledge emerges that was not present in advance of the investigation. The project is conducted in a professional and efficient manner. At this third level, investigators attempt to find answers to the question: Why did it happen?

Level 4 value investigation

The level 4 value investigation is focused on the value for the client being created by the investigation. The purpose of the investigation is to create something that is of value to the client; it may be valuable new knowledge, the settling of disagreements about past events, external opinions, and input to change management processes. The investigation’s ambition is that the result will be valuable to the client. This value may lie in the clean-up, modification or simplification of procedures, innovation and other measures for the future. The investigation should be prudent. Several explicit considerations are identified and practised throughout the examination. The examination is based on explicit choices regarding information strategy (sources), knowledge strategy (categories), methodology strategy (procedures), configuration strategy (value shop) and system strategy (technology). Explicit strategic choices make the investigation transparent and understandable to all involved and any interested parties. Here, it is often investigators in interdisciplinary environments who create value for the client. Investigations at level 4 are characterized by the active use of strategies, with substantial and decisive breakthroughs in the examination. The investigation lays the foundation for learning and value creation within the client’s organization. Detection of deviations and termination of such deviations create value for the client organization. At level 4, detection, disclosure, clarification, analysis and resolution are seen in context. There will be less to uncover in the future if current prevention is strengthened. It will be better in the future if matters are resolved completely. Investigators create value through proper scrutiny. The investigation creates value before, during and after the examination. Before the investigation, an understanding of risks and priorities develops. During the investigation, an understanding of methods and procedures develops. After the investigation, barriers are constructed, holes are blocked, work flows are developed, and continuous evaluations are established. At this fourth and final level, investigators attempt to find answers to the question: How can it be prevented from happening again?

Reports of investigations

We have selected a few publicly available reports of investigations written by fraud examiners during private internal investigations in 2016. We make a short presentation of these reports here, before moving to students’ evaluations of these investigations.

Telenor VimpelCom

Deloitte (2016) investigated the Norwegian telecom company Telenor concerning its oversight and handling of the company’s ownership by the Dutch telecom company VimpelCom. VimpelCom admitted to corruption related to investments in Uzbekistan.

Telenor executives were on the supervisory board of VimpelCom.

Deloitte (2016: 2) identified misconduct, but no crime: Several serious red flags in connection with VimpelCom’s entry into the Uzbekistan telecom market were identified and discussed at a board meeting in December 2005 and at a board meeting in October 2007. Undoubtedly, such red flags should significantly raise the Supervisory Board’s duty of care with regard to the proposed transactions and agreements related to the entry into the Uzbekistan telecom market.

Drammen Municipality

Deloitte’s (2017) review was based on the control committee’s mandate, which essentially deals with organizational conditions. Deloitte had to consider that there was a police investigation going on in parallel. Investigators from Deloitte collected data through document analysis, interviews and the review of 58 building cases, which had been processed in the municipality’s building permit department. Two employees in the department were already charged for corruption by Norwegian police.

DNB Bank

Hjort (2016) carried out a fraud examination into Norwegian bank DNB’s knowledge of and involvement in tax havens such as the Seychelles. Investigators concluded that there was misconduct, but no crime. Investigators suggested that there was misconduct because the bank’s tax haven practice was damaging its corporate reputation. The main perspective applied by investigators was corporate reputation.

Police immigration

KPMG (2016) carried out a fraud examination among executives in the Norwegian Police Immigration Unit based on concerns expressed by whistleblowers. Whistleblowers attempt to disclose information about what they perceive as illegal, immoral or illegitimate practices (Atwater, 2006; Bjørkelo et al., 2011; Vadera et al., 2009; Vadera and Aguilera, 2015). However, management at the immigration unit turned the internal investigation against the main whistleblower. Concerning the working climate, investigators did not blame managers, but suggested instead that there were serious conflicts involving the main whistleblower who was also an ombudsman in the organization (KPMG, 2016: 2): From September 2015 until summer 2016, the ombudsman’s notices, reports and use of media to promote his own views indicate that the accusations against the three were repeated, and that the accusations escalated severely. We have conducted two interviews with the ombudsman, who in June 2016 chose to withdraw his explanations. The ombudsman has thus not wanted to contribute to help investigate matters that he himself had reported. The repeated allegations and patterns of action of the ombudsman are in our view regarded as misconduct. In our view, a major part of the ombudsman’s conduct goes beyond the right to waive and the requirement for proper warning procedures. As of September 2015, this involves serious integrity violations of police employees who are particularly dependent on trust.

Nordea Bank

Mannheimer (2016) investigated Scandinavian bank Nordea, which is headquartered in 19 countries around the world, operating though full-service branches, subsidiaries and representative offices. Nordea international private banking has its headquarters in Luxembourg with branches in Switzerland and Singapore. Nordea is the largest bank in Scandinavia. Nordea has, despite warnings from the Swedish Financial Supervisory Authority, been active in offshore structures in tax havens, as leaked in the Panama Papers. During the period 2004–2014, Nordea in Luxembourg founded almost 400 offshore companies in Panama, the British Virgin Islands and the Seychelles for its customers. The Swedish Financial Supervisory Authority pointed out that there are serious deficiencies in how Nordea monitors money laundering as well as tax havens.

Mannheimer (2016: 11) identified misconduct, but no crime: The investigation has found deficiencies in the procedures regarding renewal of Powers of Attorney (POA). In at least seven cases investigation has shown that backdated documents have been requested or provided during the last six years, which is illegal when it aims at altering the truth. The previous backdating of a POA took place in 2012, and the backdating of a proxy took place in 2014. However, to be convicted of the criminal offence of forgery or of use of forgery, certain conditions need to be met cumulatively. These conditions do not all seem to be met for the cases at hand. At least one of the conditions seems not to be met, which is the clear benefit or illicit advantage of the employee asking for backdating, the bank or another third party or causing prejudice or potential prejudice to a third party.

Grimstad Municipality

BDO (2016) investigated how the largest private supplier of healthcare services to the municipality got all the contracts. The investigation report states that management in the municipality knew of violations of public procurement regulations for several years without doing anything that might correct the deviant practice. Investigators emphasized that the scope of the illegal agreements would never have been known had it not been for a local newspaper’s investigative journalism into the matter. However, investigators did not get to the bottom of the case because the municipality provided very limited funding to the fraud examiners.

Student evaluations

During a financial crime class in a business school in Norway in the spring term 2017, students were asked to evaluate a report from a private internal investigation by fraud examiners. Students had to identify and retrieve a publicly available report that was completed in 2016 or 2017. A total of 93 evaluation term papers were submitted by 190 students who could write their evaluations alone or in groups of two or three students.

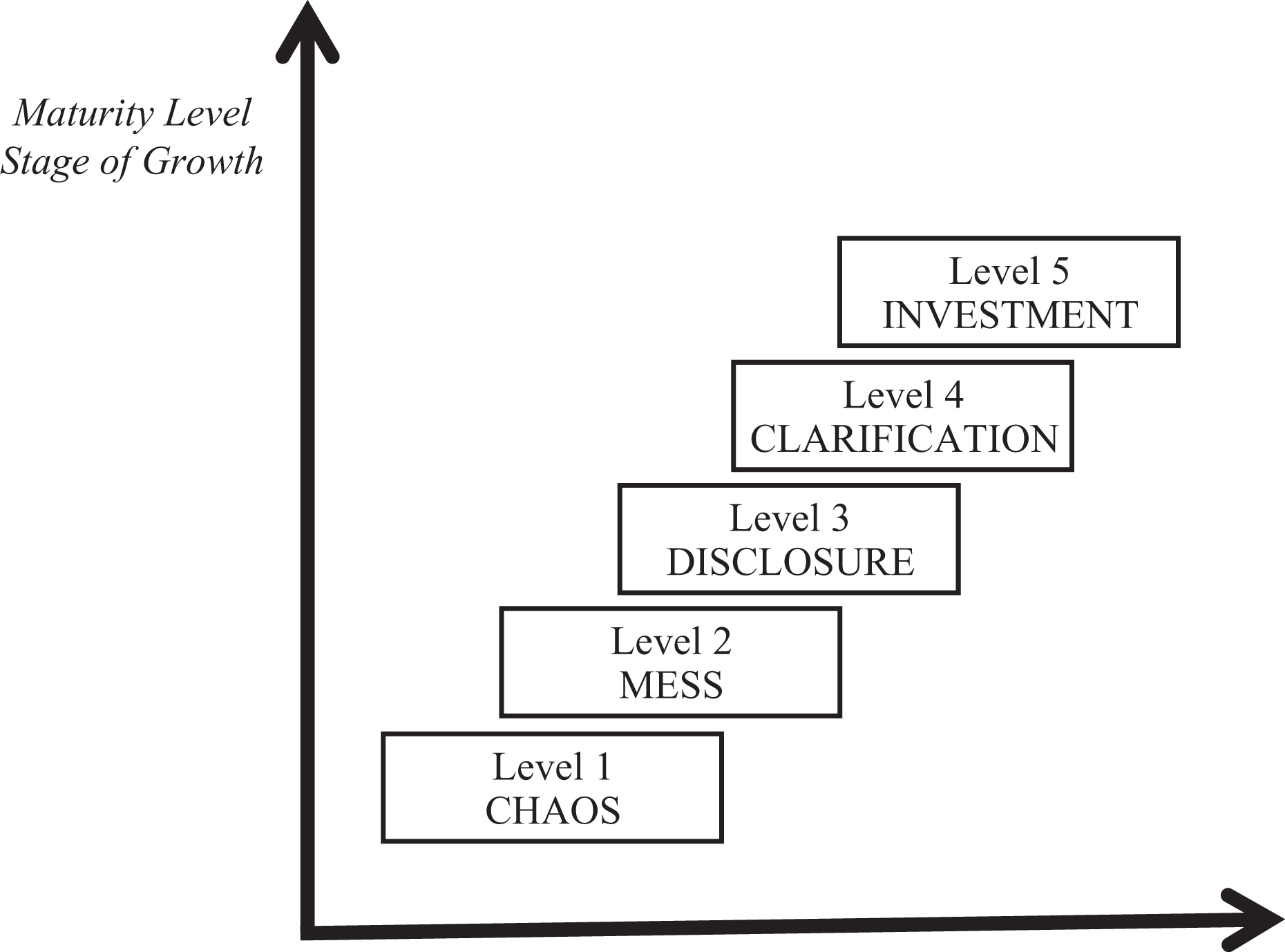

Students were first asked to develop their own maturity models with five stages and then assign their respective investigation reports to one of the levels in the model shown in Figure 2.

Maturity model for internal private investigations with five stages.

The investigation was chaos. The investigation caused more confusion than before the examination was initiated. The investigation was insufficient, inadequate, surface-oriented, a waste of time, useless, passive, unprofessional, worthless, immature, unacceptable, bad, meaningless, fruitless, awful, and chaotic. The investigation was a failure and a disaster.

The investigation was a mess. Nothing came out of the investigation. The investigation was random, amateur, formalities focused, somewhat good, sufficient, descriptive, problem-oriented, neutral, unsystematic, inadequate, activity-oriented, shortsighted, fruitless, deviations-oriented, reactive, questions-oriented, and messy. The investigation lacked scrutiny, was a collection of information without analysis, and was filled with assumptions.

The investigation was a disclosure. Some new facts were identified and documented. The investigation was focused, competence-oriented, average, biased, targeted, systematized, integrated, moderate, indifferent, standard, competent, cause-based, revealing, and disclosure-oriented. The investigation was problem-oriented and limited by the mandate.

The investigation was a clarification. The investigation was able to reconstruct past events and sequences of events. The investigation was responsible, detailed, conscientious, sufficient, professional, neutral, unprejudiced, integrated, proactive, preventive, mature, competent, systematic, professional, explorative, immaculate, expedient, truth-seeking, facts-based, complete, independent, and clarifying. The investigation added value.

The investigation was an investment. The investigation made a valuable contribution to the organization, where investigation benefits exceed investigation costs. The investigation was optimal, innovative, profitable, strategic, extraordinary, outstanding, provident, value-oriented, advanced, learning-focused, valuable, irreversible, truth-based, socially responsible, exceptional, excellent, perfect, exemplary, and a profitable investment. The investigation was a masterpiece and enrichment for the client and society.

The words used above to describe each stage are all derived from the student term papers.

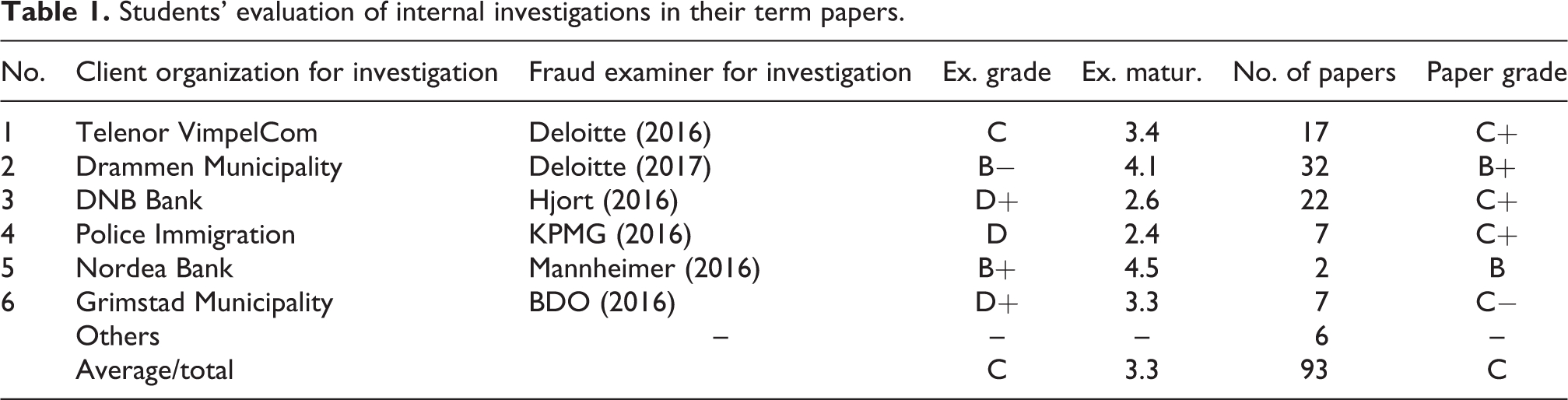

Students were also asked to grade the investigation on a scale from A to F, where A is a top grade and F is a failing grade. There were 4 A, 27 B, 22 C, 21 D and 7 E grades; there were no F grades, and 12 term papers were lacking a grade. Students assigned the best grade A to Deloitte’s (2017) investigation of corruption in Drammen Municipality and to Mannheimer’s (2016) investigation of tax haven practices at Nordea Bank in Sweden.

Similarly, students were asked to place the investigation on the maturity scale from level 1 to level 5. One investigation was placed at level 1 ‘Chaos’, 10 investigations were placed at level 2 ‘Mess’, 23 investigations were placed at level 3 ‘Disclosure’, 21 investigations were placed at level 4 ‘Clarification’, and 6 investigations were placed at level 5 ‘Investment’. Some 32 of 93 term papers were lacking a level indication from the students. Students assigned the highest level 6 to Deloitte’s (2017) investigation of corruption in Drammen Municipality and to Mannheimer’s (2016) investigation of tax haven practices at Nordea Bank in Sweden.

We expected to find strong correlation between grade and maturity, and we did: a correlation coefficient of 0.749** implies that a higher maturity level is strongly correlated with a better grade from students.

It is also interesting to study the correlation between the grades that students received from examiners and the grade students assigned internal investigations. Seventeen student term papers received grade A, and there were 19 B, 22 C, 18 D, 9 E and 8 F grades. Interestingly, the correlation coefficient is −0.276**, which implies a negative evaluation of private investigations by students who wrote good term papers. This result might be explained by the fact that good student answers found several issues in the investigation reports that could be problematized.

The number of students on each term paper could influence student assessments. Correlation analysis indicates that there is no significant co-variation between the number of students and the grade students give to investigations. There is, however, significant co-variation between the number of students and the maturity levels that students assign to investigations. This co-variation is negative with a coefficient of −0.300*, which implies that more students on the term paper are more skeptical of the maturity of internal investigations. This might be explained by more students finding more flaws in private internal investigation reports.

A final correlation analysis might be to study whether groups of two or three students perform better or worse than single students in terms of grades from examiners. A somewhat surprising result is that more students on the term paper caused declining performance as the correlation coefficient between grade and students is −0.215*. The examiner places the same requirements on term papers written by one or several students.

One possible explanation for this somewhat surprising result is that people who join groups tend to expect more from others than from themselves. Thereby, subtasks may fall between two stools and not be picked up by anybody. Another explanation might be that weak students prefer to join groups to make sure that they survive the exam.

We return now to the reports of investigations available to students for their term papers. In Table 1, the client organization for the private internal investigation is listed first, followed by the auditing or law firm that conducted the fraud examination. The next column lists students’ assessment of the investigations in terms of grade. Students found the investigation by Mannheimer (2016) to be the most successful and that by KPMG (2016) the least successful by assigning an average grade of B+ and D respectively. This result is also reflected in the next column, with an average maturity level of 4.5 and 2.4 for Mannheimer (2016) and KPMG (2016) respectively.

Students’ evaluation of internal investigations in their term papers.

Those students who evaluated the Drammen municipality investigation by Deloitte (2017) handed in the best term papers (average grade B+), whereas students who evaluated the Grimstad Municipality investigation handed in the worst term papers (average grade C−).

As listed in Table 1, the most popular investigation report among students was the Deloitte (2017) investigation at Drammen Municipality that was evaluated in 32 student papers.

Discussion

Fraud examiners, financial crime specialists and counter-fraud specialists are in the business of private internal investigations for their clients. Six problematic issues related to their roles are discussed: privatization of law enforcement, secrecy of investigation reports, lack of disclosure to the police, competence of private investigators, limits by investigation mandate, and the issue of regulation of the investigation business: Privatization of law enforcement. Ever since Schneider (2006) wrote his classic article on privatizing economic crime enforcement, the potential threat to criminal justice from private rather than public investigation, prosecution and sentencing of individuals in white-collar crime cases has steadily increased. In our context of private investigations, we apply the term ‘private policing’ to capture similarities and differences with law enforcement. Private policing of economic crime can be detrimental to an open and democratic society where the rule of law is to be transparent. The privatization of law enforcement and criminal justice, a current trend in many countries, represents a potential threat to democratic societies because all powers towards citizens in a state should be organized and managed by public authorities under democratic government control, and not by private firms. Schneider (2006) argues that financial crime specialists such as forensic accountants can be viewed as both part of, and distinct from, the larger private policing sector. The focus of the private policing sector seems to stretch from rudimentary disorder and property crime, all the way to complex, highly organized and multijurisdictional criminal and national security problems. Secrecy of investigation reports. Very often, clients and their investigators deny researchers and journalists insight into private internal investigation reports. Investigators argue that reports are the property of their clients, whereas clients argue that there are circumstances that prevent them from disclosing reports. In my search for private investigation reports, I met a variety of reasons why clients and their investigators denied access to investigation reports. The reasons for secrecy fall into three main categories: First, there were reasons important to the investigated organization. Second, there were reasons important for the investigating firm. Finally, there were reasons important for the relationship between the investigated and the investigator. Lack of disclosure to the police. The rule of law and criminal justice work in constitutional states by public prosecution and courts that are open to everyone to observe. If there are suspicions of violations of the criminal law in a country, it is important that knowledgeable sources communicate information about suspects to public authorities such as police investigators and public prosecutors. Disclosure of investigation reports is a necessity in cases of criminal offences. Preferably, investigation reports should not only reach the attention of the police, but also citizens through the media. However, many financial crime specialists consider their reports to be the sole property of their clients, because clients pay for the job and the result in the shape of the investigation report. They consider their work to be a piece of consulting or legal advice, which might be protected by client–attorney privilege. Competence of private investigators. The competence of financial crime specialists and fraud examiners varies to an extent in that it represents a threat to the rule of law, privacy and democracy. Some PIs seem very professional; others are not, as illustrated by the lifting of the lid on a largely hidden world of investigations showing some of the key aspects of cases, key events, and key results. Lawyers in particular suffer the danger of making many mistakes in private investigations, because they are not trained detectives. Limits by investigation mandate. The client defines a mandate for the investigation, which then has to be carried out in accordance with that mandate. The mandate tells investigators what to do. It defines the tasks and goals for the inquiry. The mandate is an authorization to investigate one or several specific issues by reconstructing the past. The mandate may be part of a blame game, in which the client wants to blame somebody while at the same time, diverting attention from someone else. Principles of regulation. In most countries, the investigation business is completely unregulated. Although police investigations are regulated, the private equivalent is not subject to oversight. There may be some guidelines for professionals, such as auditors and lawyers, but the investigation business as such is free of laws, regulations and oversight that could tell them what to do and how to do it.

Conclusion

Based on term papers by students from a financial crime class at a Norwegian business school, maturity levels for private internal investigations by fraud examiners were defined. Sample investigations were assigned to different levels in the maturity model. Student evaluations indicate that fraud examiners have a long way to go before their investigations can be characterized as innovative, optimal, profitable, strategic, extraordinary, outstanding, provident, value-oriented, advanced, learning-focused, valuable, irreversible, truth-based, socially responsible, exceptional, excellent, and perfect.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.