Abstract

This article explores three national news agencies in Europe (Press Association Group in the United Kingdom, Austria Presse Agentur in Austria and Tidningarnas Telegrambyrå in Sweden) in order to find the reasons why these agencies decided to transform themselves from traditional newswires into diversified media businesses. We ask why these agencies are able to operate under market principles, with substantial profit margins, and also to contribute to a sustainable national media system, while agencies in some other countries struggle. We draw on semi-structured interviews with 26 senior managers of the agencies and use several strategic management frameworks, including five forces and dynamic capabilities. We find that, in all three agencies, early crises led to a sensing of news agencies’ weakened bargaining power with media clients and the decline of industry attractiveness and triggered a timely search for new revenue sources through diversification. These successful new businesses are based on a strong news-agency brand, on technological capabilities, and on resources originating from the agencies’ firm relationship with the news media. We argue that, in all three cases, visionary leadership and an ability to orchestrate a new relationship with media owners have been key capabilities created in these early crises.

Keywords

Introduction

How do we make money out of content when so much of it is free?

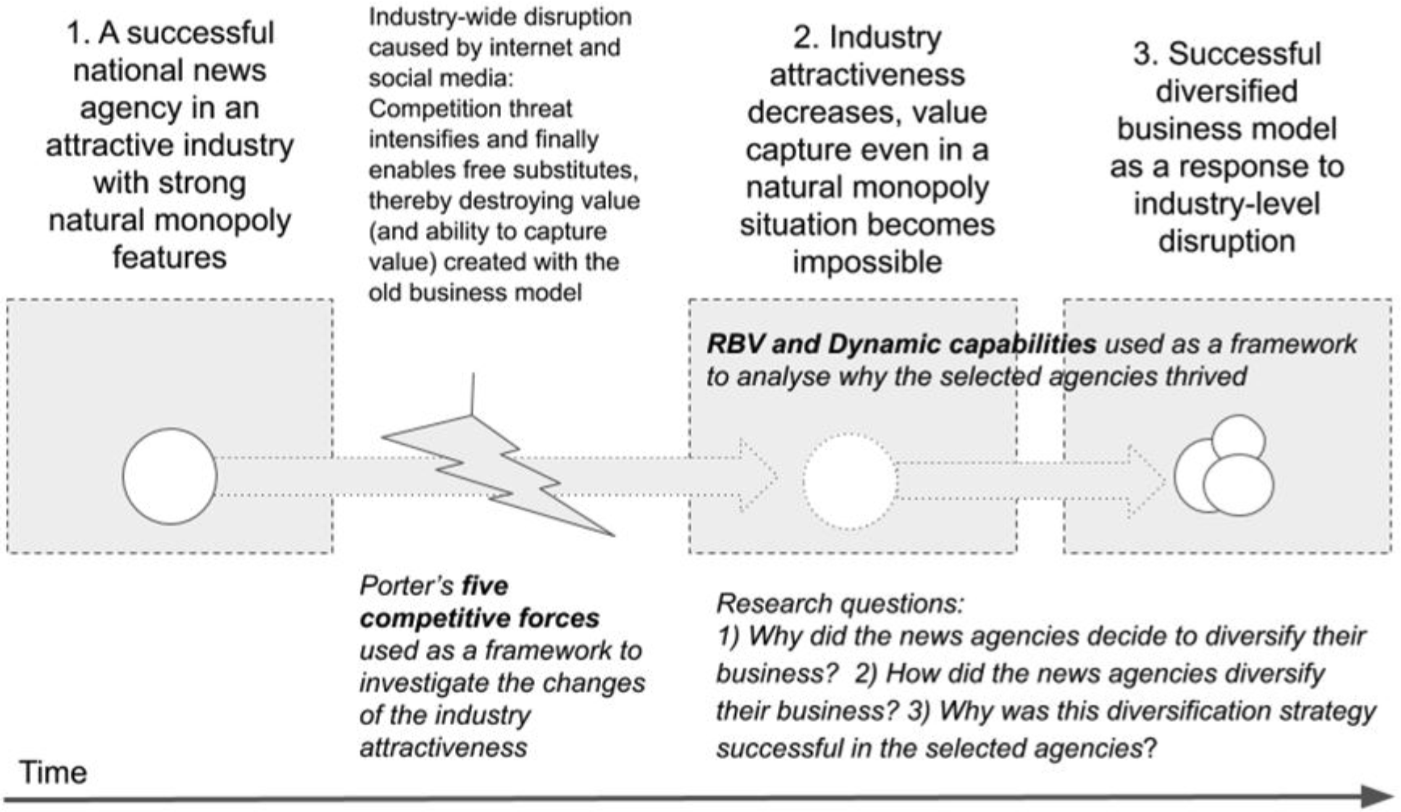

Fresh findings from European national news agencies invite us to analyse more deeply the concept of diversified business models of national news agencies (Rantanen et al., 2019). Although the Internet has fundamentally challenged the viability of the old model of a national news agency as a business, some agencies are still thriving and operating under market principles. An ability to diversify successfully has made it financially possible for these agencies also to maintain a news service and therefore to contribute on a societal level to a sustainable media system. Why and how have these agencies diversified their business? (Rantanen et al., 2019). In this study, these questions are approached by applying first time internal views of strategic management to national news agencies. We first analyse the changes in external competitive forces that initiated a search for a new business model. After this, we use a dynamic capabilities (DCs) framework to identify what led to early and successful moves to business models more fit for the present environment.

We selected three agencies on the basis of data collected for the research project ‘The Future of National News Agencies in Europe’. All these three agencies have substantially diversified their businesses and we consider them to be successful in terms of the following three criteria:

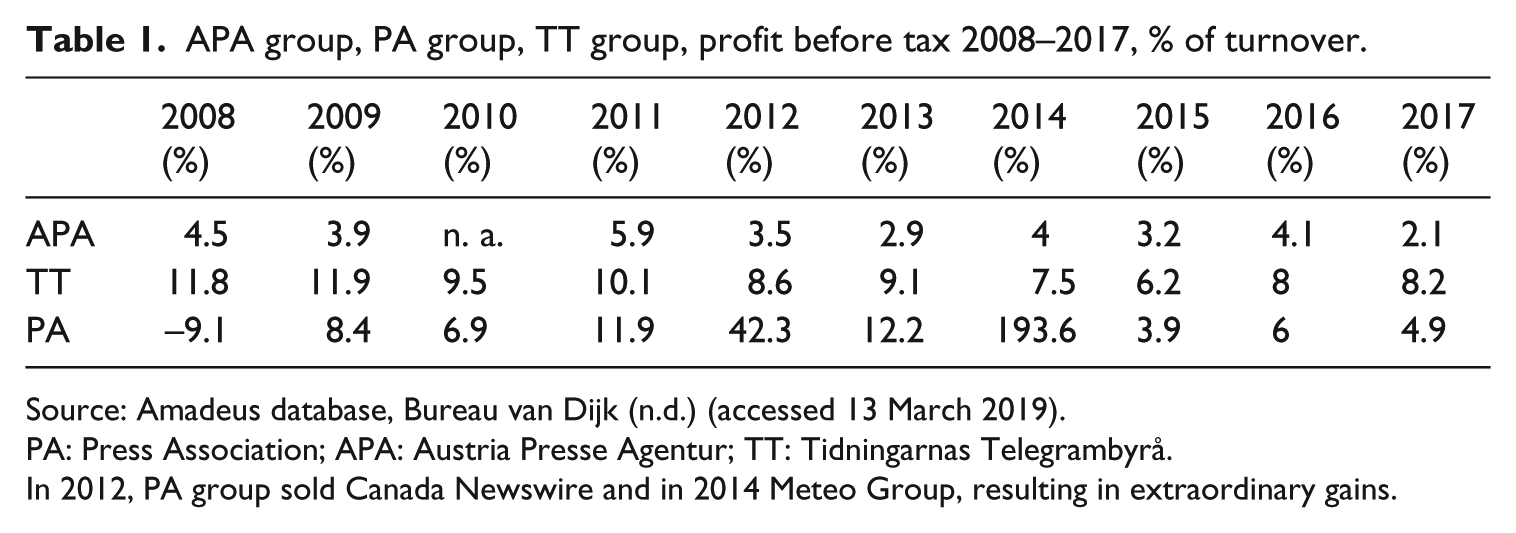

They have shown an ability to operate during recent years with a substantial profit margin and return on capital. From the Amadeus database, we find that Press Association (PA) and Tidningarnas Telegrambyrå (TT) have been able to produce excellent ROE (return on equity) (29% and 32% on average between 2008 and 2017) and ROCE (return on capital employed) (30% and 26%), while Austria Presse Agentur (APA) also reached acceptable levels (13% ROE and 7% ROCE).

APA and PA were identified as role models by more than half of our interviewees (11/20) with European news-agency directors for the project mentioned. They also mentioned in this context TT and ‘Scandinavian agencies’.

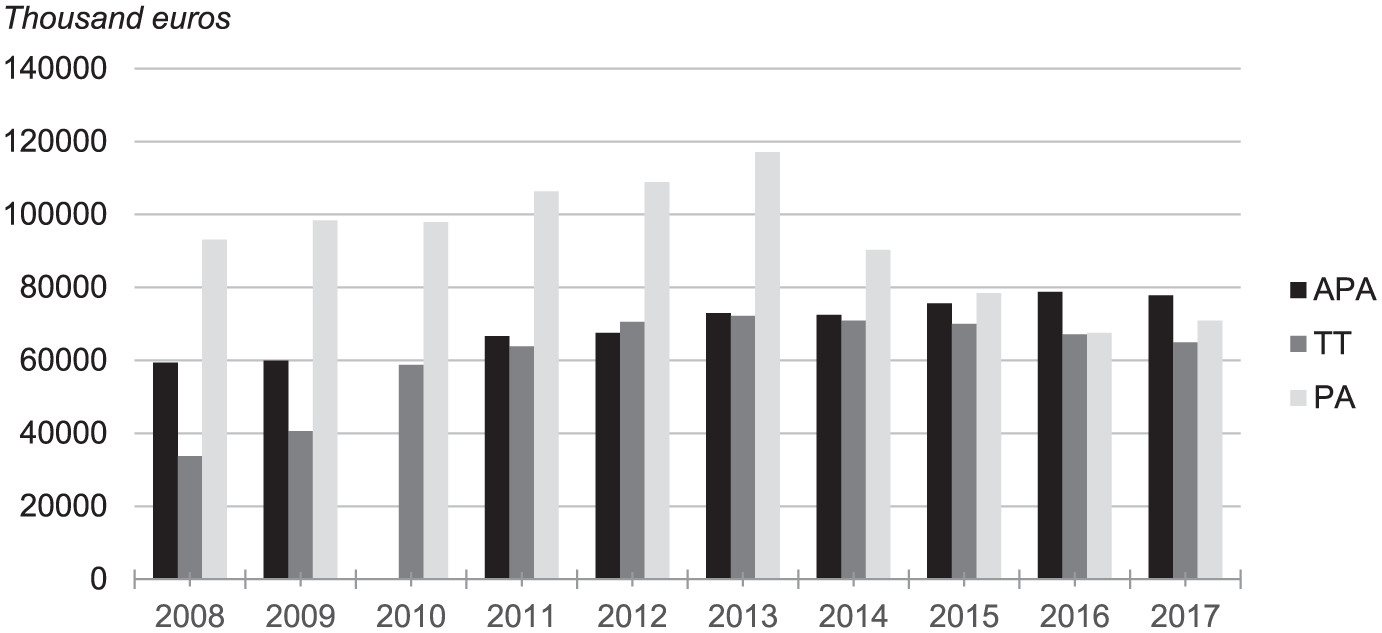

These agencies have been able to maintain a well-resourced and widely used general news service. This has been achieved at a time when the income trend from general news service in Europe is negative and diversification strategies, in general, have not had significant results (Rantanen et al., 2019) (Figure 1, Table 1).

Turnover of APA group, PA group and TT group 2008–2017.

APA group, PA group, TT group, profit before tax 2008–2017, % of turnover.

Source: Amadeus database, Bureau van Dijk (n.d.) (accessed 13 March 2019).

PA: Press Association; APA: Austria Presse Agentur; TT: Tidningarnas Telegrambyrå.

In 2012, PA group sold Canada Newswire and in 2014 Meteo Group, resulting in extraordinary gains.

Originally formed in 1868 as a co-operative, the PA group operates as a private limited company owned by a number of UK media companies. As early as 1869, there was a co-operation agreement with Reuters: PA submitted UK news to Reuters, while Reuters provided news from around the world to PA. PA was for a period of time a main owner of Reuters, before the latter became a publicly traded company and was later sold to Thomson Group (Moncrieff, 2001; Silberstein-Loeb, 2014).

APA was founded in 1849 and nationalized in 1859, becoming the first state-owned news agency in the world. During the Second World War, the agency operated under state control. It was re-founded as a co-operative agency owned by newspapers and by the Austrian public broadcaster. In contrast to the other two agencies in this study, the group company of APA still operates as a co-operative, while other two are stock companies with client-media organizations as shareholders (Vyslozil, 2014: 360–361).

The Swedish TT was founded in 1867 and purchased in 1893 by three Swedish newspapers. Since 1921, the agency was in a form of ownership similar to that of a co-operative, as a corporation with some 170 newspapers each owning one share. Since 1999 the two largest media groups in Sweden, Bonnier and Schibsted, have each acquired a controlling 30 per cent shares of TT (Vyslozil, 2014: 372–373).

Literature review

There have been attempts to diversify the revenue base of global news agencies throughout their history and diversification strategies at least since the 1980s (Boyd-Barrett, 2000: 12–13) and in European national news agencies since the 1990s (Boyd-Barrett and Rantanen, 2000). Previous research on news agencies, however, has largely revolved around international agencies and the political economy. In Boyd-Barrett’s comprehensive review of theory development in relation to news agencies, he notes that the scope of studies had been dominantly characterized by the dependency discourse (Boyd-Barrett, 2012; Boyd-Barrett and Rantanen, 1998). Within the trajectory of this, many studies have examined in depth the role and activities of international news agencies (Headrick, 1981, 1991; Hills, 2010; Read, 1994; Winseck and Pike, 2007). This research has mainly addressed the relationship between news agencies and states, ownership issues, content analyses and the role of news agencies as agents in a globalized age (Boyd-Barrett and Rantanen, 1998). Relatedly, locating national news agencies in the context of soft power as a tool of international relations has been depicted as a remarkable endeavour (Cheng et al., 2016).

However, as Boyd-Barrett (2012) points out, research on national news agencies as ‘an industry or genus’ was neglected to a great extent until the 2000s (p. 336). Boyd-Barrett and Rantanen (2002) pioneered the study of how the Internet would influence global and national news agencies, evaluating opportunities and threats in this new age. Following that initial work, Boyd-Barrett (2008, 2010) and Rantanen (2009) continued. However, existing research provides limited insight into how the ecosystem of news agencies has changed. Boyd-Barrett (2012: 347) calls for future research that would examine how far the Internet had reformulated news-agency business models. However, the responses of news agencies to all these digital disruptions have still not been specifically studied or viewed through a theoretical lens in order to understand and explain the root causes of the changes.

A business model is defined as the description of how a firm creates, delivers and captures value in relation to its network of exchange partners (Massa and Tucci, 2014). Who captures the value is dependent on the bargaining power of the exchange parties (Bowman and Ambrosini, 2000). While business model is a term describing a logic centring on value, strategy is a term describing the choices and decisions that a firm makes (Casadesus-Masanell and Ricart, 2010).

By diversification we mean spreading the base of a business, in order to achieve improved growth and reduce overall risk by addressing news products, services, customer segments or geographic markets (Chan-Olmsted and Chang, 2003: 214). Such diversification typically means using a firm’s surplus physical and intangible resources – or new, specifically acquired, resources. Diversification strategies are classified on the basis of (1) direction (product, geographic or product-geographic diversification) or (2) relationship with core and target markets (related/non-related diversification) and (3) mode (acquisitions/internal expansion) (Chan-Olmsted and Chang, 2003; Chatterjee and Wernerfelt, 1991; Montgomery, 1994).

Boyd-Barrett and Rantanen briefly discussed diversification strategies in the early 2000s, describing these but considering the issue mainly in the context of national identity. From their perspective, diversification was one of two strategies being examined by news agencies and was ‘limited only by the willingness of shareholders to provide news agencies with the freedom to be entrepreneurial’ (Boyd-Barrett and Rantanen, 2000: 103–104). Moreover, Boyd-Barrett identified the key features of this defensive ‘new model’ (Boyd-Barrett, 2002: 93–94) and argued that agencies all over the world were ‘converging towards a new business model’ (Boyd-Barrett, 2008: 166). Picard (2015) noted briefly that exclusivity, now lost, used to be a basis of a successful business model for AP. However, the diversification practices and policies of news agencies have not previously been specifically examined by dedicated research, or frameworks of strategic management applied to these diversification attempts.

Furthermore, Bakker has studied how news agencies historically tried to profit from selling news during different types of crisis situations and ‘how they gradually developed new business models in response’. However, his research has mostly focused on the 19th century (Bakker, 2014).

Vyslozil has pointed out the diversification policies of the Group 39 agencies (TT, NTB, ANP, Belga, Ritzau, STT, SDA and APA) between 2002 and 2012, when they started systematically to modify their policies in response to the dramatic changes in the news market. He shows how the agencies followed a ‘two-pillar strategy’ of providing general news services and diversification services, as a result of which they were generating nearly two-thirds of their overall revenues from diversification by 2012 (Vyslozil, 2014: 298–302).

The research project carried out recently by the London School of Economics can be depicted as the most comprehensive endeavour, having sought answers on different aspects of these issues. Jääskeläinen and Yanatma (2019) examine the business model innovation and business diversification in responding to the challenges of the Internet. They used the framework of competitive forces in analysing the causes of disruption in agencies, which approach we develop in this article.

Diversification as a response strategy

Rumelt (1974) documents his finding that successful diversification strategies were clustered around strengths or resources originating in a firm’s original business. So, diversification around these resources may be a rational response when a firm’s traditional markets decline. The concept of ‘defensive diversification’ applies to firms that operate in markets whose characteristics are constraining their growth or profitability and that are therefore most likely to diversify, and more specifically to diversify into non-related business areas, in pursuit of more favourable markets than those they originally operated in (Christensen and Montgomery, 1981: 338). It has also been noted that unrelated diversification on average is less successful than related diversification (Chatterjee and Wernerfelt, 1991). In general, diversification may be a question of matching a firm’s resources to its market opportunities (Montgomery, 1994).

Porter’s external approach and ‘five forces’

Michael E. Porter’s five competitive forces are a model for explaining the attractiveness of an industry as a field of operations. These forces may change over time, improving or eroding the attractiveness of an industry as a whole (Porter and Millar, 1985). Arguably a national news agency is a natural monopoly, employing a fixed-cost infrastructure, a situation in which typically a single firm tends to dominate a market as joining would incur such a large investment that it disincentives competition. In these scenarios, it is simply more cost-effective for one company to produce a product or service than for multiple firms to do so (Baumol, 1977: 810). In this natural monopoly scenario, the industry’s overall attractiveness may ultimately define whether it is possible to run a news-agency service at a profit at all.

Therefore, we find it useful to use Porter’s theory by analysing changes in the competitive forces over time and explaining the dramatic changes in the news marketplace that are finally challenging the very existence of national news agencies in some countries. Finally, this framework also gives an insight into why the value created may not be available for capture in a business model.

The five forces, according to Porter (1979, 1985, 2008), are as follows: the threat of new entry, the power of suppliers, the power of buyers, the threat of substitutes and rivalry with existing competitors. Below we explore Porter’s theory in the context of national news agencies.

First, economies of scale can limit the threat of new entry. If buyers of a service are able to enjoy the benefits of more buyers using that same service, known as network effects (Katz and Shapiro, 1994), the willingness and ability of competitors to enter the market tend to be weaker. Incumbents may enjoy several other benefits over newcomers, such as preferential access, brand identity or cumulative experience. The threat of new entry may also be reduced because of the expected strong response reaction of incumbents. This is especially the situation if an industry has high fixed costs and low marginal costs, motivating it to drop prices in order to use its capacity to the full.

Rivalry among existing competitors is especially difficult in these situations. There may be considerable pressure for competitors to cut prices close to their marginal costs, thereby winning new customers while still covering some fixed costs. We observe that on the rare occasions when there has been a competitor in a national news market, media-owned agencies have benefitted from owners who secured for them a major share of the market, financial backing and finally a win in the price war that typically results from a competitive situation in a national news-agency market.

Second, powerful buyers are able to capture value by forcing down prices, demanding better quality or more service. If buyers are able to threaten to produce the service themselves, this also increases their power.

Finally, the threat of substitutes is often hard to recognize and unpredictable in industry transformations. A substitute fulfils the function of the product by different means. Sometimes the substitute may replace the buyer industry’s product, thus reducing demand (Jääskeläinen and Yanatma, 2019: 5). This has largely been the case in the market for real-time news information, where pure information needs may be fulfilled by even by news-agency clients publishing the agency’s content and creating a ‘free-rider’ problem.

Internal approach, resource-based view and DCs

Barney (1991) turned strategy researchers’ focus to the question of why some firms perform better than others in the same external conditions. His seminal paper focuses on two sections of the widely used SWOT analysis template: The Strengths and Weaknesses of a firm. Porter’s school, meanwhile, mainly concentrated on external analysis of the Opportunities and Threats of the firm’s environment. Barney’s paper started a research stream known as the resource-based view (RBV). According to this theory, in order to create a sustained competitive advantage, a firm requires resources that are valuable, rare, imperfectly imitable and not substitutable (Barney, 1991: 106–111).

While RBV looks in detail at the way a company is able to exploit its resources for incremental innovation, and to exploit its resources as a whole, the concept of DCs refers specifically to a firm’s meta-level ability to reconfigure such resources in order to respond to a changing environment (Teece et al., 1997). An organization’s DC to successfully explore and adapt to a changing environment through radical innovations became the centrepiece of the theory that evolved.

In Figure 2, we present the conceptual model used to frame the empirical findings of this research.

Theoretical framework.

Methods

The research questions for this study are as follows:

Why did the news agencies decide to diversify their business?

How did the news agencies diversify their business?

Why was this diversification strategy successful in the selected agencies?

The main methodology of this study was a qualitative analysis based on 26 semi-structured interviews conducted by the two authors between May 2018 and May 2019 with present and past senior managers of the selected three agencies, including five present or former agency CEOs. The interviews were audio-recorded, transcribed and analysed with NVivo software in order to categorize relevant findings in terms of the theoretical framework.

Additional information was collected through document analysis of the Amadeus financial database. The findings may have some bias, since the case study interview data represent only the views of persons who have themselves served the agencies as managers.

Findings

Why did the agencies diversify? External view and disruption

First, we looked for the changes in competitive forces to try to analyse what may have caused the search for a new diversified business model. We found substantial changes in both the economic value of a general news service and the ability to capture this value, caused by new technologies and by the new news ecosystem that had brought to the marketplace first new competition and then substitutes for the general news service.

Avoiding competition has been one of the key strategies of agencies since the early years of the news-agency business. Speed was always a means of securing the exclusivity and value of news-agency content (Silberstein-Loeb, 2014). However, the changes sparked by the widespread utilization of the world wide web as a real-time news dissemination method, starting in the mid-1990s, dramatically changed agencies’ competitive position and the value of news in the marketplace.

The news agencies studied here sensed early that their general news business would face significant risks because of the expected disruption of the market due to dramatically lower barriers of competition and free substitutes. Dramatic events in their national markets helped all three of the agencies studied to create the DCs needed and to move from sensing change to an early seizing of opportunities and transformation of their capabilities, and to diversification through innovating new services and through new business models.

The 1990s: early crisis, emerging competition, news-agency wars

By the early 2000s, at the latest, all three agencies had concluded that they needed to diversify their services and products. The key element in sensing the need to change was understanding the strategic importance of new distribution technologies, especially the Internet, for news agencies’ traditional business model.

In Austria, APA had already earlier landed in severe financial difficulties for three reasons: first, the largest newspaper of the country, with some 40 per cent of total circulation, had made a strategic decision not to subscribe to a news-agency service. Second, APA had invested in an office property with expectations of external income that were not realized. Third, cost levels increased, but the media clients controlling the agency’s board refused to increase prices. The new CEO appointed at the beginning of 1982 concluded that in 5 years the agency would face an existential financial crisis. He then started a series of workshops in the company from which the vision of a diversified business model based on media databases and strong IT capabilities evolved (Wolfgang Vyslozil, 2019, personal communication).

In the early 1990s, the other two news agencies, in the United Kingdom and Sweden, noticed changes in their environment and industry.

In the United Kingdom, a number of clients decided to set up their own agencies, aiming for both savings and a better service (Moncrieff, 2001: 263–273). PA thus lost about 40 per cent of its regional newspaper clients for UK News. This ‘was very challenging, but also quite [an] exciting time – we were desperately trying to keep the existing clients on board and see off this competitor. Ultimately, we [PA] won the battle’ (Marc Tucker, 2018, personal communication).

The new competition resulted in significant changes in the culture of the company. New capabilities were created. One interviewee described how ‘PA then started to become customer-focused, rather than deciding that it knew best what its customers wanted. So, I think that was a critical point’ (Clive Marshall, 2018, personal communication). Revenues were hit by the competitive threat, but the quality of services increased (Marc Tucker, 2018). More importantly, the fundamental shift ‘to change it [PA] to a commercial agency’ had started (Ed Ethelston, 2018, personal communication).

In Sweden, TT was exposed to competition in the late 1990s, when regional and local newspapers were similarly trying to challenge the agency. This was a significant alert to the management of TT, who came to the conclusion that they had to reorganize, to shut down stuff, get rid of many of the reporters, head for new contracts with the media clients and some kind of reorganize or redevelop the whole company so the challenger got out of business and TT was restarted. (Per Anders Broberg, 2018, personal communication)

Most significantly, TT learned from the crisis that it needed to review the relationship with clients. In the view of the present TT management, the agency’s conduct towards its customers in the 1990s was poor. They now consider that the competition with Förenade Landortstidningar (FLT) helped TT to become ‘professionalized in a sense’ (Daniel Kjellberg, 2018, personal communication).

In all three agencies the crisis led to serious rethinking of their role in the future markets for news, which were disrupted not only for news agencies, but for media industries overall. The decline in newspaper circulation had a direct impact on news agencies, given that the prices they charged were often calculated on the basis of circulation and frequency of publication.

From 2000 onwards: Internet and social media as disruptors

Another factor that diminished the role of newswire services was the ready availability of the information and content that news agencies used to provide exclusively. The news media and other clients previously had to buy this content from news agencies in order to stay informed about events. Now, information is immediately available, often with the agencies themselves as the source (Picard, 2015; Rantanen, 2009). Anybody can access any agency content their clients publish over Internet, including those organizations to whom the agencies previously sold their service directly. Even if the content cannot be published as it is, the information it contains is immediately available, thus eroding its commercial value: Since the advent of the internet, news information, sports information, entertainment stories – so all of the things which are the lifeblood of an agency – are constantly available in large volumes and almost instantly. (Marc Tucker, 2018)

Social media began a new wave of disruption in the news ecosystem, from which both news agencies and especially their clients have been suffering. Social media has had impacts on the way information and news agencies’ content are distributed. The second major impact of social media has been the lost link between producing news and selling advertising on social media and search engines, a change which profoundly disrupted the business models of the news media and affected media clients’ ability to pay their suppliers.

The managers agree that the agencies have been losing a considerable amount of revenue from the traditional newswire: ‘We don’t get as much money for it as we used to, because print publication is going down, and the willingness to pay much for digital is not so great’ (Göran Westin, 2018, personal communication).

To sum up, looking through the lens of five forces, the competitive environment of media-owned news agencies selling their services has changed fundamentally in several ways:

The threat of new entrants has increased. Real competition emerged in national news-agency markets from the beginning of the 1990s. The increased competition threat weakened news agencies’ bargaining power with their media clients.

Technological development has made it possible for clients to produce real-time news content themselves. This has also weakened the bargaining power of the agencies and increased the power of buyers.

New companies have established services that disseminate real-time information and act as complements to the traditional agency services and have also weakened the toll-good character of news-agency service.

Social media has disrupted news agencies’ clients’ advertising business models, which has weakened their ability to pay for the service and ultimately their ability to earn money from agency content in their own business model.

Based on our interviews, we found that most European news agencies were not operating a general text service at a profit. If the agencies are profitable, that is in most cases due to high margins in other businesses that the agencies have established through related diversification.

How did the news agencies diversify their business?

Traditionally, the business model of a media-owned news agency was based on the idea of pooling resources and sharing the costs of producing news that most of the media would want to publish. For the reasons described in the previous section, the viability of that business model was quickly eroded.

In the new diversified business model, we find two ways of expanding businesses:

Establishing new added-value services for media clients;

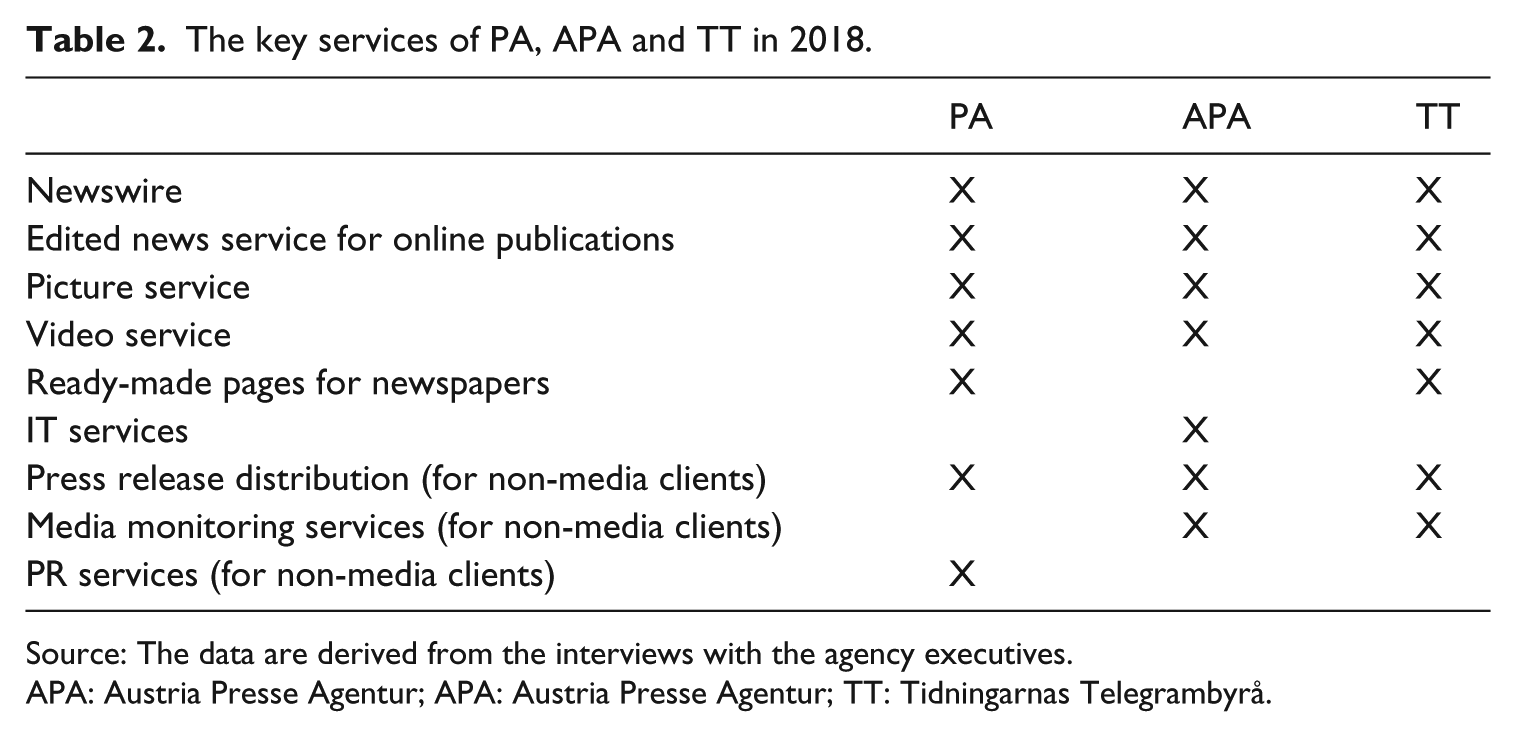

Expanding into new markets outside the media, mostly based on the same competencies needed to serve media clients (Table 2).

The key services of PA, APA and TT in 2018.

Source: The data are derived from the interviews with the agency executives.

APA: Austria Presse Agentur; APA: Austria Presse Agentur; TT: Tidningarnas Telegrambyrå.

All the agencies have used both internal expansion and acquisitions as tools in their diversification. At PA, the acquisition strategy with financial resources created through the successful development and sales of new businesses units has been a key part of the process (Clive Marshall, 2018, personal communication). At TT, the acquisition of the fast-growing media monitoring company Retriever was one of the milestones for the company (Jonas Eriksson, 2019, personal communication).

From the interviews, we drew the following business logic for diversification:

The agencies have identified new needs among their media clients, for example, for more added-value news services or for the enabling of cost savings in clients’ newsrooms.

New services are better protected against the free-rider problem than pure news information, which does not enjoy copyright protection. This protection is based either on a stronger intellectual rights system (pictures, videos, databases) or on better technological barriers (automated publishing or easy-to-use platforms for content).

The media market in general has been on the decline, so agencies have entered other client markets such as corporates and institutions.

The key capabilities used in the new services, illustrating how the diversification can be classified as ‘related’, are as follows:

Using the trusted news-agency brand as an asset in expanding into new markets;

Using the same technological capabilities and round-the-clock, real-time alertness that are needed in news-agency operations;

Using the special relationship with the news media as a way of sourcing unique value components for new services to non-media clients (exclusive access to editorial systems, exclusive access to media content);

Maintaining an organizational and technical capability of super-efficiency in news content production and news service innovation.

Almost all interviewees agreed that the brand perceptions created by the newswire played a crucial role in introducing new products and services. PA’s Clive Marshall (2018) described how: We don’t envisage a world without that core news service. That’s what we refer to as the beating heart of the business and then we build everything off that. So, our strategy of diversifying – ultimately rests on the agency brand and our trusted journalism.

In TT, media monitoring has been retained under a separate brand in order to protect the integrity of the news agency: If you are going to use the TT brand, or any news agency brand in other businesses you have to do it delicately, so it doesn’t hurt the trustworthiness of the brand of [the] news agency, the core. (Jonas Eriksson, 2019)

We conclude that all the agencies have benefitted from trusted brand even in other businesses than news. There are, however, differences in brand strategies. PA and TT have protected the integrity of their news brand by differentiating the non-news services under separate brand names, while APA has integrated their diversificated businesses in the same brand family with the agency.

Why was it successful? DCs

The agencies turned from cost-sharing co-operatives into profit-seeking media services companies, taking risks and aiming to create a return of capital for the owners. This has fundamentally changed the capabilities needed by the firms (Jääskeläinen and Yanatma, 2019: 5).

The interviews revealed that the mandate of management from owners changed in these three news agencies. The early crises already experienced before the introduction of the world wide web in news dissemination helped to change the culture in these agencies early enough and helped their management to sense, and later to seize and transform, the capabilities needed to succeed in the new environment.

Visionary leadership played a key role

Change capabilities and management capabilities have been key resources in the change. Our findings confirm that the role of visionary management is crucial (Schoemaker et al., 2018). Our interviewees explained that management was the key initiator and led the change process, while owners provided the opportunity by agreeing to the change of mandate.

Changing the business model needed understanding and an ability to predict the main developments in the industry. The cases in our research showed a strong strategic intention.

The carefully planned diversification of APA had already started before the advent of Internet news services. An interviewee from APA described this phenomenon: ‘The system already broke up in the late ’80s. Wolfgang then [stated that] we have to go into the diversification. This was the solid base for all other steps further’ (Clemens Pig, 2018, personal communication). Another interviewee also highlighted the crucial role of the former CEO: ‘There was a very conscious decision by a former CEO, Wolfgang Vyslozil. I think a good one at that. Because I feel back then it put us way ahead of the game’.

At PA, several successful divestments of business units have created substantial financial resources which have been used for further diversification. While strategy was very significant at PA, the British agency also quickly responded to the recent challenges and opportunities (Clive Marshall, 2018). Marc Tucker (2018) explained the position of PA in the last two decades by underlining its evolution as follows: It’s felt like constant evolution at a measured pace. But actually, if you analyse in more detail, that constant evolution is created by the sort of spikes that you’re talking about. It’s just that nothing changes immediately, so the catalysts have been competitors in the market.

In TT, after the crisis, the agency explored the possibility to enter the consumer market. The next CEO changed the plans and decided to focus on diversification on media clients and diversify in that market. The reason was that the CEO at that time did not believe a news agency had the capabilities to compete in a consumer market: I thought that we will never become best in the world in that part and that would be a huge journey to build up that kind of capabilities and as we all know the competition is crazy . . . If you run a company like a business, you must really try to find your role in the value chain, and I think that that was the obvious role. (Raoul Grünthal, 2018, personal communication).

Relationships with owners had to be redefined

We found that the ability to orchestrate relationships with owner-clients in the case of a media-owned agency has been a key requirement for diversification. It has allowed these agencies to gain a mandate from their owners to use resources for investments rather than price cuts, to take risks and expand to other business areas and even gain exclusive rights to their owner-client’s content and access to editorial systems.

As opposed to the original idea of a cost-sharing co-operative, all these agencies are now aiming for profit, especially from their new diversified businesses.

The CEO of TT, Jonas Eriksson, noted the agency’s difference from agencies that still run under tight owner control: ‘They sort of more become cost structures than free and independent news agencies. That’s not the case with TT, but I’m fairly certain that’s the case with quite a few agencies around Europe’ (Jonas Eriksson, 2019).

The boards of news agencies have supported successful and professional management if it has been able to follow a commonly agreed strategy and reach targets. Clive Marshall (2018) described this relationship: Obviously, the confidence was very high with the board. The board were very supportive of the executive . . . So, we have not, I can’t think of any situation the owners have said no in the last eight or nine years.

One part of the new mandate, however, concerns clear lines which agencies cannot cross if they are to avoid a conflict of interest with owner-clients. Several of our interviewees underlined how there had been a clear culture shift: industry leaders were not acting for the benefit of a single owner on the board, but, within explicitly or implicitly agreed limits, for the benefit of the agency. This was expressed in the case of TT and PA, but not as clearly in the case of APA whose news agency still legally operates as a co-operative.

Focus on clients, and on their clients, in order to explore and adapt

After the early crises, the agencies became more alert to how the market was changing, listening to customers far more than they ever had: So that, I think, is a really good example of how we have communicated in a way that we’ve never communicated to that customer set before and it was important in order to execute at that level of change with that market. Really, really important. (Andrew Dowsett, 2018, personal communication)

PA started moving up the value chain from pure content feeds to providing packaged products and ready-made-page products so that customers could start outsourcing that part of their business to the agency. This strategy indicates that understanding the needs and business of its clients was key to PA.

A culture of constant renewal had to be developed

One of the most crucial points stressed was that the agencies need to constantly innovate and provide contemporary products, services and distribution means (Jääskeläinen and Yanatma, 2019: 13): The only thing that is changing really is the pace. When you had a product that lasted 30 years you didn’t have to think that hard. Now we have products that may last a year, and you have to innovate and go again. (Tony Watson, 2018, personal communication)

Changes in customers’ strategies may have a major effect on their needs for an outsourcer. Locking content behind a newspaper’s paywall requires content considered worth paying for and therefore different from that offered free of charge on all news sites, which typically is news-agency content.

This shows that the ability to anticipate their clients’ business needs and the flexibility to adjust rapidly are core DCs needed in an agency. Their main customers are media companies, which means they have to analyse and sense changes in their clients’ needs and to be able to adapt to these changing client needs in time.

In order to maintain their cost advantage against clients’ opportunity to produce the content themselves, one of the main areas of future development centre on new technologies like data gathering and artificial intelligence, robot journalism and new production and distribution systems.

Agencies are also required to continuously reconfigure their resources while remaining restricted in a field that they describe as having strong path dependencies. They need staff who can combine editorial services and technology, and IT capabilities have become even more significant. One interviewee from APA stated on this point: I think the biggest challenge that I see from an internal perspective is restructuring the company in a way that the units work together. Because if we do not want only to produce content but we want to enrich the content with technological services, then we can’t separate content creation and technology. (Clemens Prerovsky, 2018, personal communication)

In the eyes of an interviewee from APA, the biggest challenge agencies expect to face is to get the right employees: I think it’s getting the right people for tech services. It’s like all tech companies have problems to get the right people, the coders, the tech architects, to handle all those new tech services, to anticipate them, not to do it always on our own. (Clive Marshall, 2018)

Marc Tucker (2018) of PA also underlines another point: One of the things that keeps me excited is the constant innovation to keep producing new products, but also try and keep the old clients on board or bring them with us and continue to try and satisfy them.

We conclude that clients have been very important in the transformation of these news agencies. They played a key role after competition intensified. In response, the agencies began to dialogue and discuss more with their customers in order to meet their expectations.

Conclusion

The introduction of the world wide web as a news distribution channel has disrupted both news agencies and their media customers’ businesses and made it extremely difficult to create and capture value through the traditional business model of a news agency, thereby challenging the foundations of a media system where privately owned news agencies had media clients as their owners. The crises these three news agencies were already experiencing before the introduction of the world wide web helped them to sense these changes earlier than happened in some other countries, and they benefitted from transforming their capabilities early to meet the new environment.

The key DCs needed in this process were managerial capabilities to sense and seize the changes in the marketplace, and the capability to orchestrate a new relationship with their own owner-clients so that the agencies were given a mandate to take risks, generate and use their financial surpluses to invest in new services and at the same time maintain their special relationship with the news media, on which the new businesses were built. Our empirical findings support an argument that this ability to negotiate a new mandate with owner-clients has been crucial, especially because news agencies’ owners had an interest in limiting the agencies’ freedom to compete with them in the market. Investing in diversification was an alternative means of delivering surpluses back to owner-clients by lowering prices, as practised by some other European agencies, and this choice had to be supported by the owners. The management of the three agencies studied has played a key role in changing this mandate, and their ability to do so has been a key DC.

The agencies have had to develop new business areas in order to thrive financially, as well as new competencies, especially in the field of technology, client-understanding (including understanding their clients’ clients) and an ability to constantly innovate also in their traditional media business on the basis of this understanding. The new business areas were developed on the basis of related diversification strategies, benefitting from trusted brand and an intimate relationship with the news media. Some of the agencies have also diversified into businesses other than news, using the external value of a trusted news-agency brand, but we see variations in how agencies sometimes also protect their news brand by differentiating the new services under separate brand names.

In the totally new business areas using same fixed-cost resources needed for news-agency operations, like media monitoring, press release distribution, media databases or even picture business, profit margins often are substantially higher than in traditional text news operations. Diversification in news agencies therefore makes it possible to produce societally important general news services under market principles, ultimately even if this is at a loss, because it spreads the burden of fixed-cost infrastructure and builds and maintains the agencies’ brand value and special relationship with the news media, which can then be monetized in other, high-margin, businesses with less competition.

However, in the long term, the future of even these three news agencies is still strongly linked to the future of the news media, which remains uncertain. Privately owned news agencies operating without state subsidies in general see the future of their news services as more uncertain than do agencies with the state as an owner or with public institutions as major clients (Rantanen et al., 2019). If one takes the normative stance that a fully private agency is societally a better alternative than a state-owned or state-subsidized one, the means of promoting financial success, or even of continuing to exist, become key elements of the dependency discourse of a national media system.

News agencies, in their original form, only sold news, and media-owned agencies still mainly operate as outsourcers for the news media. In this role, news agencies operating under market principles experience the changes in the economic value of news information in the marketplace almost directly, while in other news media the effects are mixed because of the more complex business models of selling advertising, subscriptions, or both, or because news content is sold as a bundle with several other types of content. The theoretical approach we have applied in this research contributes also to a better understanding of the role of news in the disruption of other news media.

Footnotes

Acknowledgements

The authors would like to acknowledge Prof. Terhi Rantanen for editing this Special Issue and for all her help. They also thank Prof. Ari Jantunen for his valuable feedback on an early draft of this article, the reviewers for their very helpful comments and Jean Morris for proofreading.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the Media Research Foundation of Finland; Jyllands-Posten Foundation, Denmark; the LSE Knowledge Exchange and Impact (KEI) Fund, UK; and the Department of Media and Communications, LSE, UK.

Interviewees

Andrew Dowsett (2018), Chief Operating Officer, PA

Clemens Pig (2018), CEO, APA

Clemens Prerovsky (2018), Head of APA-Medialab

Clive Marshall (2018), CEO, PA

Daniel Kjellberg (2018), Managing Editor, TT

Ed Ethelston (2018), CFO, PA

Göran Westin (2018), Business Development and Sales, TT

Jonas Eriksson (2019), CEO and Editor-in-Chief, TT

Marc Tucker (2018), Commercial Director, PA

Per Anders Broberg (2018), Head of Sales and Business Development, TT

Raoul Grünthal (2018), CEO (2003–2006), TT

Tony Watson (2018), Managing Director, PA

Wolfgang Vyslozil, CEO (1982–2008), APA