Abstract

Sovereign creditworthiness within the euro area hinges upon the credibility of the Stability and Growth Pact (SGP). We analyse whether political events that worsen the SGP's credibility result in a shared default risk premium for all euro members, therefore leading to a joint deterioration of creditworthiness. We especially examine the decisions and statements of the Commission and the Council of Economic and Finance Ministers. Analysing daily data through the 1999–2005 period with an ARMA-GARCH model, we find the Commission plays a decisive role in affecting investor evaluations, where its credibility-strengthening decisions decrease volatility and statements signalling a weakening of fiscal credibility spark uncertainty on financial markets. Our results stress the importance of creating credible fiscal institutions that preserve sovereign creditworthiness within the euro area.

Keywords

Introduction

The recent debt crisis in the euro area brings together two developments that, at first sight, appear paradoxical: divergence between member states and the convergence of the euro area. On the one hand, no day passes without the recognition of ‘country spreads’, that is, the divergence of interest rates paid by states with relatively higher and states with relatively lower creditworthiness. On the other hand, the inability of several euro area members to refinance on international capital markets, and the subsequent political reactions, demonstrated the extent to which member states are sitting in the same boat.

We consider diverging yield spreads and common risks to be complementary in nature, rather than contradictory. However, this article focuses on the spillover effects that result from partially integrated fiscal policies, and the subsequent common costs and benefits of the interdependencies in the currency union.

Our contribution builds upon previous research, which saw the Stability and Growth Pact (SGP) as a common good of fiscal policy credibility in the eyes of investors (Mosley, 2004). In this respect, we analyse the question of whether the damage caused to this legal framework resulted in a shared (that is, common) deterioration of default risk for sovereign debt in the euro area. Our basic idea conceptualizes the SGP as a political commitment susceptible to a time-inconsistency problem, with politicians having an incentive to free-ride when it comes to common fiscal prudence. Investors expect such behaviour, which results in higher interest premiums. Consequently, we argue that a lack of credible commitment to the SGP burdens all euro area members with additional financing costs.

We test this claim empirically, investigating political events that violate or adjust the SGP and the consequent impact on the euro area default risk in government bonds. We examine not only relevant political decisions of the European Commission and the Council of Economic and Financial Ministers (EcoFin Council) but also the statements of relevant politicians. That is to say, we investigate whether these two categories of events move financial markets' perception of creditworthiness. Three key results can be reported. First, we find no level effect of decisions and statements by relevant European Union (EU) institutions on the common default risk premium. Secondly, our empirical analysis does, however, indicate that decisions and statements increase volatility in the risk component in public debt. This highlights the importance of credible fiscal institutions within a monetary union and, thirdly, suggests that the Commission – in contrast to the EcoFin Council – seems to be of decisive informational relevance to financial investors.

The Stability and Growth Pact and common default risk

In outlining our theoretical argument, we first recall the rationale of the SGP by focusing on its inherent negative externality problem. Secondly, we detail the official SGP procedures for fiscal laggards within the euro area. Based on this, we look at the problem of credible commitment and how this creates a common default risk component. Finally, we outline testable hypotheses as to how political events that weaken the credibility of the fiscal policy framework increase the common premium.

Monetary union and negative externalities: the political-economic rationale behind the SGP

The European Economic and Monetary Union (EMU) has substantially reshaped economic conditions and political realities in Europe (Beetsma and Giuliodori, 2010; Wyplosz, 2006). Politically, the monetary union has altered the constraints and possibilities of policy makers, as monetary policy became supranational in nature in the European system of central banks, led by the European Central Bank (ECB), while fiscal policy control remained largely in member states' hands. From the perspective of national politicians, the EMU curtails macroeconomic, in particular monetary, policies. Moreover, a centralized monetary policy is devoted to average values of inflation in the euro area, which results in differing economic formation across member countries. This development may even amplify the need for domestic macroeconomic policy adjustments. As Leblond (2006: 984) argues, governments are under pressure to use other macroeconomic tools, with fiscal policies being the decisive instrument.

Increased fiscal spending typically results in heightened debt-financing costs owing to rising government bond yields. One major risk element driving this correlation is the raised default risk component. In fact, there is mounting empirical evidence that such a relationship between fiscal policy-driven default risk premiums and government bond yields exists (Codogno et al., 2003; Hallerberg and Wolff, 2008). As Faini (2006) empirically confirms, there is a fiscal policy interest rate correlation within the EMU. A 1 percent deficit/GDP ratio surge results in a rise of approximately 10 basis points in sovereign bond yields.

Moreover, in a currency union with supranational monetary policies but national fiscal policies, such nationally motivated fiscal policies might lead to supranational externalities (De Haan et al., 2004: 245). Since countries may have an incentive to free-ride by overspending on their budgets, a key challenge for the euro area arises from national fiscal profligacy. An increase in inflation and interest rates induced by public debt might spill over to other members of the euro area through raised debt-financing costs and depreciation of the currency (Faini, 2006). An extreme case would be the necessity to bail out a defaulting member state, financed either directly by the other members or indirectly through the ECB (De Haan et al., 2004). As a result, the costs of financing governmental debt through financial markets might increase substantially if investors demand a relatively higher risk premium because of the perception that creditworthiness has deteriorated. In effect, national fiscal profligacy could come at an economic, and eventually political, cost for other member states of the euro area.

The SGP at work

To mitigate such negative externalities, the SGP was introduced as a commitment to fiscal prudence at the national level. Here, we briefly outline the main mechanism and important historical events (see the web appendix); for a detailed discussion, refer to Heipertz and Verdun (2010). In a nutshell, the SGP can be viewed as a far-reaching political commitment, with substantial supranational competencies that increase the transparency of public debt formation, enabling markets to evaluate policy at the supranational level. At the same time, however, it has also enabled national politicians to behave dishonestly at the expense of the SGP's credibility.

The SGP was designed to substantiate the rather loose Maastricht Treaty stipulations regarding maximum debt levels – 60 percent of gross domestic product (GDP) – and maximum deficit levels – 3 percent of GDP – for member states. Legally, the SGP consists of a European Council resolution and Regulations 1466/97 and 1467/97, which detail the surveillance of budgetary positions and the coordination of economic policies, as well as the implementation of the excessive deficit procedure.

In political terms, each Regulation serves a specific objective (together, they are often referred to as the ‘two arms’): 1466/97 details the desired supranational transparency of domestic budgets and establishes the early warning mechanism (EWM); 1467/97 establishes the excessive deficit procedure (EDP), a mechanism for possible sanctions. The EWM (or surveillance mechanism) standardizes the transparent reporting of expected and achieved national budgets, thereby establishing an important monitoring mechanism led by the European Commission. Moreover, it enables a private channel of control, where public spending in the EMU is put under the intensified scrutiny of investors (Leblond, 2006). Meanwhile, the EDP portion of the SGP is targeted at clarifying the sanctions mechanism dealing with member states that have sustained deficits and have failed to remedy them. In principle, it stipulates that, 10 months after a state has failed to redress a deficit position, the EcoFin Council can impose sanctions – first in the form of an interest-bearing deposit, later as a fine (De Haan et al., 2004: 237).

To offer a clearer picture of the political process, we briefly outline the steps of the potential procedure leading up to a fine. Should the Commission – within its regular budget-monitoring task and based on both national forecasts and its own macroeconomic forecasts – detect an existing (or a very likely future) infringement of the stability criteria, it recommends to the EcoFin Council the opening of an EDP (or alternatively an EWM) against the violating country. In the following procedural step, the EcoFin Council then has to confirm the validity of the recommendation, which would lead to the opening of a procedure. In both instances (EDP and EWM), the country is obliged to take immediate measures (within three to four months) to bring its budget back into line with SGP requirements. In subsequent stages, the procedural steps are repeated, but the consequences for a country that remains non-compliant become more severe. The second round would lead to an edict by the Commission about what measures have to be taken to return to a balanced budget. A potential third round could lead to sanctions if the member state stays in abrogation (first in the form of a deposit, later on as a fine).

Even though the SGP can be viewed as an outstanding supranational tool in dealing with such an influential macroeconomic policy instrument as fiscal policy, especially in relation to other international commitments, it is frequently seen as problematic owing to its discretionary nature (for example, De Haan et al., 2004; Wyplosz, 2006). The SGP's problem is its susceptibility to political moral hazard once the monetary union is successfully established. As a ‘soft law’ commitment, it is not automatically enforceable and the sanctions mechanism in particular is exposed to political discretion (Leblond, 2006: 974). At the same time, the governments that the SGP ought to constrain are the authorities that decide the application of the procedures and rules. They therefore cannot be expected to employ the criteria of the SGP objectively. Moreover, only a qualified minority is needed to block the adoption of the Commission's recommendation to impose sanctions (Leblond, 2006: 971–3). As a result, the lax political nature of the stability criteria and the associated monitoring mechanisms, in combination with the altered macroeconomic options of national governments, create an incentive to free-ride. In other words, domestic macroeconomic necessities weigh more heavily when compared with SGP-related intergovernmental fiscal obligations.

Mounting evidence of renewed loose fiscal policies under the SGP's regime feed this expectation. As Mink and De Haan (2006: 207) argue, political budget cycles reoccur after euro membership, simply because ‘the short-term gains at the national level of higher deficits outweighed the systemic costs involved in violating the rules. This contributed to the erosion in the “political ownership” of the discipline rules after the Maastricht convergence period’ (Buti and Van Den Noord, 2004: 754).

How then is it possible that the SGP was considered a relevant and functional institution at any time? We claim that it was regarded as a credible commitment, as long as the member states prudently adhered to the fiscal framework. However, when political events damaged the reputation of the SGP, the potential institutional weaknesses entered actors' calculations and their valuation of sovereign debt from the euro area. Given this setting, a potential time-inconsistency problem exists (Leblond, 2006: 974) and the question of whether the SGP is seen as a credible commitment becomes crucial.

The emergence of a common default risk

As Kydland and Prescott (1977) demonstrate, policy choices suffer under a time-inconsistency problem. This applies to instances in which rational economic actors are forward looking and do not believe in the credibility of a political commitment to a declared policy. In such a case, the economic actors at whom the policy is targeted do not believe that the policy maker will adhere to its commitment in the future. This induces strategic behaviour and undermines the success of policy measures. A credible commitment is the key to sufficiently disabling political discretion, thereby building trust among firms and consumers. This resulted in the widespread trend toward independent monetary authorities (Bernhard et al., 2002) and laid the groundwork for the SGP: the risk to be prevented here is that financial markets anticipate (the incentives for) fiscal profligacy, which would decrease the currency's value and lead to demands for higher government debt risk premiums (Hallerberg and Wolff, 2008).

Time-inconsistent fiscal policy will emerge once a national government evaluates the added value from fiscal expansion to be higher than the additional gains from sticking to the SGP rules. Such free-riding on fiscal credibility becomes highly attractive if a member state's own actions are expected not to weaken the SGP in the long run. From their point of view, it is then completely rational to increase public spending in order to win an upcoming election. Unless euro area member states credibly commit to fiscal prudence in a transparent manner, financial markets will demand higher risk premiums on a member state's sovereign obligations (Hallerberg and Wolff, 2008). From the investor's perspective, the SGP – by increasing transparency (through the EWM) and control (through the EDP) – becomes a benchmark for preventing fiscal profligacy and reducing default risk by constraining the impact of national fiscal policies on the euro area as a whole (Mosley, 2004). However, with reference to the research that touches on credible international commitment (for example, Simmons, 2000), the major question is whether investors regard the SGP as a credible signal of true intentions in an environment of incomplete information (Gray, 2009). An international commitment would be credible in constraining policy choices if investors can trust that politicians will make their future decisions in compliance with the agreement. Investors have to observe that credible obligations to follow fiscal prudence are made. Consequently, by outlining clear rules and benchmarks of fiscal prudence, the SGP acts as an international institution that regularizes investor expectations about the future behaviour of states in an uncertain environment (Gray, 2009: 935–6). However, if investors lose confidence in the credibility of the SGP's commitment, they will correct their economic expectations accordingly. The credibility of the SGP then becomes a relevant element for the evaluation of euro area government debt. Empirical evidence also supports the benchmark role that the SGP plays (Mosley, 2004).

Moreover, we conjecture that regime-switching trends characterize investor behaviour (Freeman et al., 2000: 450); that is, they alter their risk evaluation as they conceive of different regimes of fiscal credibility. As long as financial markets consider the SGP to be a credible commitment, the demanded yields should be relatively lower. If subsequent events negate this trust, the SGP will lose credibility in the view of investors, with risk-sensitivity soaring as a consequence. This could mean that rational investor expectations regarding the credibility of the SGP will change over time. Although the SGP may have been considered a credible commitment towards fiscal prudence, investor expectations may shift towards a new regime in terms of realizing that the SGP does not protect against fiscal profligacy.

Similarly, Bernoth et al. (2004: 18) make a state-contingent argument, highlighting that EMU membership reduces the linear effect of debt on default risk premiums but increases the non-linear, marginal effect. Accordingly, EMU members enjoy a lower risk premium than before, but this benefit declines as the size of public debt increases. In other words, although all euro area member states benefit from their membership in the form of reduced interest rate payments and particularly reduced default risk, they are subject to heightened market scrutiny, which might lead to soaring debt-financing costs if the SGP is perceived to be incapable of constraining fiscal profligacy.

The latter arguments imply the existence of effects on the euro area as a whole and are of key importance to our investigation. We argue that establishing the currency union generated a new risk element within EMU government bonds, namely a common risk of heightened default probability if the SGP were to be violated. In other words, whereas the currency union decreased the default risk for individual states (owing to the SGP commitments), it simultaneously creates new risk categories in terms of the SGP's credibility and common fiscal prudence. This does not imply that national differences between member states' debts diminish entirely, but rather that the general difference becomes smaller and is complemented by a shared component of default risk. This common risk element should be mirrored in simultaneous movements of euro area government bond yields. This occurs as a result of political events that signal a deterioration in the SGP's credibility. 1

Although the credible commitment problem in regard to the SGP is hardly a new phenomenon, the concern of a common default risk being shared among the euro area members has been neglected so far. The political lenience (particularly in the course of events between 2002 and 2005) raises serious doubts concerning the credibility of SGP commitments, which should result in the adjustment of investment decisions. We expect this reallocation of investment to come at a common cost to all euro area countries.

This reallocation occurs as financial markets evaluate how political events affect prices. They are expected to react in two ways. If investors are confident about the outcomes of changed political conditions, they will explicitly decide to buy or sell, thus having an enduring impact on the risk level (that is, increasing or decreasing the common default risk). On the other hand, if financial market actors are unclear about political events and their impact on future risks, this uncertainty will result in increased trading volatility.

The two reactions reflect investor evaluations of political events differently. Whereas the effect on the risk level reveals the ‘pricing in’ of political actions into altered euro area debt, increased uncertainty among traders depicts the inability to unambiguously analyse political developments. The latter effect is particularly pronounced in the context of highly topical and unexpected political activity. Whenever political action is perceived to be relevant, market actors will attempt to price it in, which in vague situations will result in heightened volatility with an indeterminate trend. Previous studies have demonstrated the uncertain nature of political events and the volatile market reactions they can cause (for example, Freeman et al., 2000; Prast and de Vor, 2005).

We expect to find both effects as a result of weakened credibility of the SGP's fiscal institutions. First, risk levels should soar as investors detect political events that will visibly decrease the credibility of the SGP. Secondly, volatility should rise in the context of political events that render financial markets uncertain about the SGP's credibility. Building on this framework, two hypotheses will be analysed:

Research design

Investigating the potential influence of SGP-related political decisions and statements on the common default risk premium, as we do in this article, requires a complementary research design. On the one hand, we rely on financial econometric techniques for modelling the dependent variables. On the other hand, we employ a qualitative content analysis approach to capture specific independent variables – that is, our political event data in terms of key actor decisions and statements by various political agents.

The design chosen here consists of estimating a regression model in which the effects of events on particular returns refer to dummy variables. A corresponding dummy variable coefficient usually measures the abnormal return across an event period. In this specific version, rather than modelling abnormal returns as prediction errors from a market model equation for a distinct estimation window, the approach here covers the entire sample period. In doing so, we refer to the ‘parameterizing form of an event study’, which can have several advantages depending on the research question and data (Binder, 1998: 123–5). It is chosen here because this method is particularly compatible with an analysis of multiple events, as is the case in our analysis. Contrary to conventional event data applications, we are able to reduce information loss considerably compared with a design that relies on some arbitrarily chosen estimation window.

Operational definitions of political events

From an empirical perspective, the question arises of whether and to what extent investors perceive political events as signalling a weakening of the credibility of the SGP commitment. In line with related research (for example, Bechtel and Schneider, 2010), we conceptualize the relevant information by looking at pertinent political decisions by key decision makers, as well as public announcements of their intentions:

Actual political decisions within or regarding the legal framework of the SGP, by the European Commission, the EcoFin Council or other SGP-related institutions. Statements by these institutions' politicians that signal future political events concerning the SGP and euro area member states' fiscal policies.

For the empirical analysis, a clear-cut definition of political behaviour that discredits the SGP is needed. We define it as a political decision and/or statement that is (or at least signals a future action that is) incongruent with the current, legally binding rules encompassed by the legal documents constituting the SGP. Consequently, events are categorized as weakening credibility when the SGP is: (a) violated, which refers to all ‘technical’ violations of the SGP's legally binding benchmark values (i.e. when a member state does not comply with the stability criteria); (b) flexibly interpreted, which describes political behaviour in which an infringement of the SGP is not appropriately punished, thus disregarding the SGP; or (c) adjusted, which, in all cases, weakens the SGP's credibility.

In practical terms, the following decisions can be characterized as weakening credibility (see the web appendix for all relevant decisions): the Commission's discovery of violations of the technical measures (combined with announcing an EWM or EDP), 2 the EcoFin Council's divergence from the Commission's recommendation, as well as any decision that alters the legislative framework or its application and thereby weakens the SGP's credibility in preventing fiscal overspending.

With regard to statements, our analysis incorporates announcements that signal either a future violation of the technical measures, flexible interpretations or adjustments of the SGP. In this respect we consider the distinct effects of the key actors, in particular the Commission and the EcoFin Council.

The data

For the purpose of capturing the explanatory political variables, we conduct a content analysis of EU Commission documentation dealing with any official decision-making, as well as various political statements published in two newspapers of great relevance for financial investors, the Financial Times (European edition) and the Frankfurter Allgemeine Zeitung. The resulting binary variables are coded as a decision on days when relevant decisions were made by EU institutions, and a statement is documented when both newspapers simultaneously reported such an event.

To avoid data loss owing to imprecise information-processing, the event windows have been extended by one day prior to and one day after the actual event for decisions, and by the subsequent day for statements. 3 Related studies typically follow such an approach since problems of diffuse information-processing can be circumvented at a comparatively small cost of data dilution (MacKinlay, 1997: 14). In addition, we address concerns regarding investors' propensity to react to statements and particular decisions in different ways. This means that the empirical analysis shows that investor reactions to decisions by the Commission differ from those to decisions by the EcoFin Council. This is reasonable because the Commission – representing the guardian of the SGP – and the EcoFin Council may have different levels of importance and trustworthiness.

Whether political actors reduce sovereign creditworthiness through decisions and/or statements is ascertained by isolating the common default risk component inherent in long-term government debt. Although several indicators have been employed for this purpose, we use interest rate swap spreads (IRSS) (for example, Afonso and Strauch, 2007; Heppke-Falk and Hüfner, 2004; Lemmen and Goodhart, 1999). This indicator isolates the default risk in sovereign bonds by subtracting the interest paid by governments from interest paid for high-quality private sector risk (Lemmen and Goodhart, 1999: 82). It measures the default risk precisely, because its synthetic nature levels all remaining yield and risk components out.

Our dependent variable indicator, IRSS, is then calculated as the difference between the fixed leg (i.e. swap rate) of an interest rate swap (IRS) and the government bond yield of the same maturity (10 years). In constructing the government part, we refer to 10-year government benchmark bond redemption yield data provided by Thomson Financial Datastream. This time-series consists of a GDP-weighted index of government bond yields in EMU member states.

Interest rate swaps depict the private sector side: these are contracts between two parties to exchange flows of interest payments in order to hedge interest rate risks (see Bicksler and Chen, 1986; Duffie and Singleton, 1997, for an introduction to this topic). More specifically, an IRS is the exchange of a fixed interest rate payment stream for a floating one at predetermined settlement dates and referenced to a notional principal, here suitable government bonds. 4

The construction of the swap allows for protection from parallel changes in the level of the indexed interest rates. However, the financial positions will be altered if swap and bond rates move in different directions. In this regard, a widening spread, for instance, can be traced back to a drop in bond rates and thus reflects an improvement in the relative financial standing of the sovereign debtor, in our case represented by the entire euro area. In turn, decreasing IRSS reflect a surge in the common default risk component of government bond rates, which points to a worsening of sovereign creditworthiness (Lemmen and Goodhart, 1999: 82). Comparing the relative funding costs of the public sector with those of the private sector makes the inclusion of further control variables in the model specification unnecessary (Heppke-Falk and Hüfner, 2004: 6). IRSS as a proxy are well suited to isolate the financial market perception of sovereign default risk (Lemmen and Goodhart, 1999: 80). A systematic influence on the change in spreads, due to a sole private sector risk variation, is negligible owing to the characteristics of the IRS indicator. First, IRS are traded only among a select group of AAA-rated high-quality dealer banks and corporations and therefore incur very low risks. Second, IRS do not involve an exchange of principal; they are based only on a notional principal, which reduces risk to the replacement risk of the swap. The common default risk component representing our dependent variable is measured in the form of IRSS multiplied by 100. The latter transformation allows for the tracing and interpretation of changes in the common default risk component (measured by basis points). In the following section, we describe why our choice of modelling framework is suitable for testing the outlined hypotheses.

The modelling framework

A ubiquitous problem in dealing with daily data is that such a time-series is often characterized by both serial correlation and heteroscedasticity; that is, periods of lower variance alternate with periods of higher variance. Controlling for such statistical properties requires the application of regression techniques designed to explicitly model the conditional variance process, in addition to the estimation of the financial series conditional mean equation. Econometrically, we therefore rely on general autoregressive conditional heteroscedasticity (GARCH) models (Engle, 1982, and Bollerslev, 1986). This econometric model not only allows us to enquire into the level effects of political events in our IRSS time-series but also deals with volatility phenomena that point to changes in the markets' perceived common default risk in the euro area. The estimation of level changes in the common default risk premium within the euro area is described by the conditional mean equation,

Empirical analysis

The outlined modelling framework is applied to a data set comprising of all trading days between the inception of EMU in 1999 and the end of the year 2005. The latter year is characterized by the neutering of the SGP by considerably softening its legal framework.

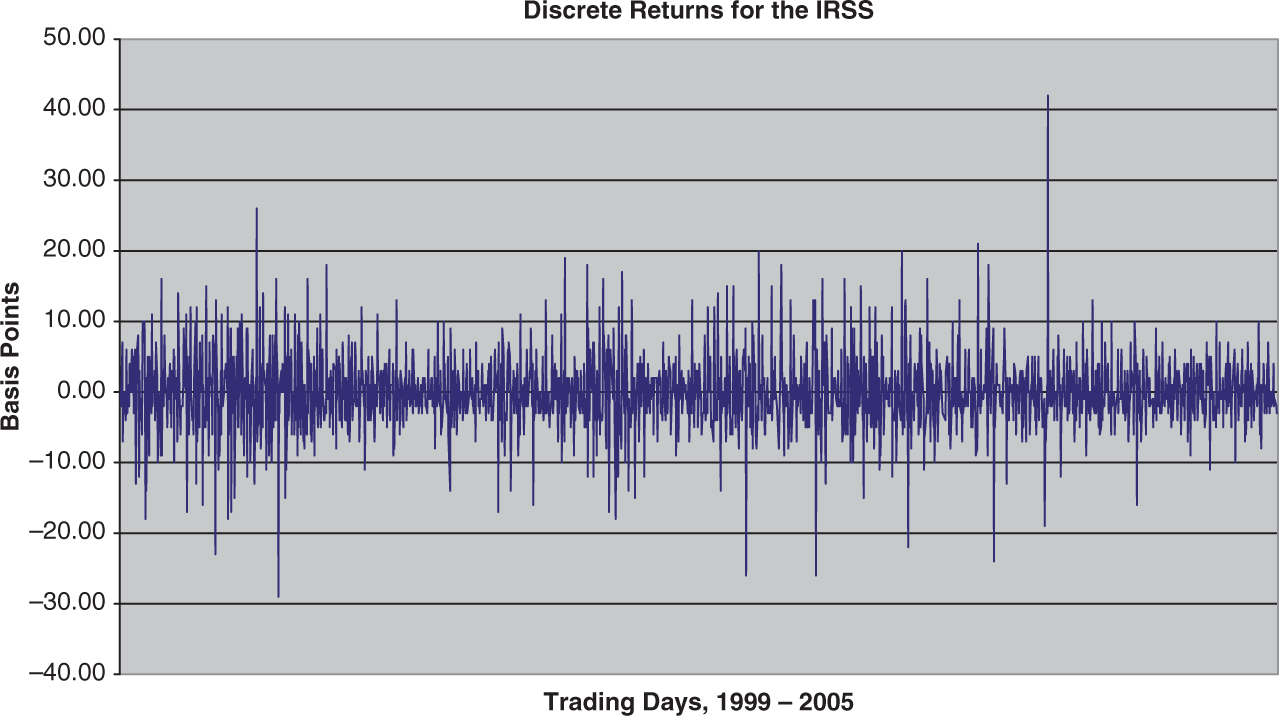

For these reasons we have confined our analysis to a sample covering the period 1 January 1999 to 31 December 2005, comprising a total of 1784 observations (see Figure 1). At the same time, the key political event data on decisions and statements related to the SGP add up to 190 observations, that is, trading days that are marked by a ‘1’ but are otherwise filled with a zero dummy. We start out by presenting the descriptive statistics and the selection of a specific GARCH model. Thereafter, we turn to the impact analysis, including essential post-diagnostic tests.

Time-series of the daily common default risk premium, 1999–2005.

Diagnostic statistics and model selection

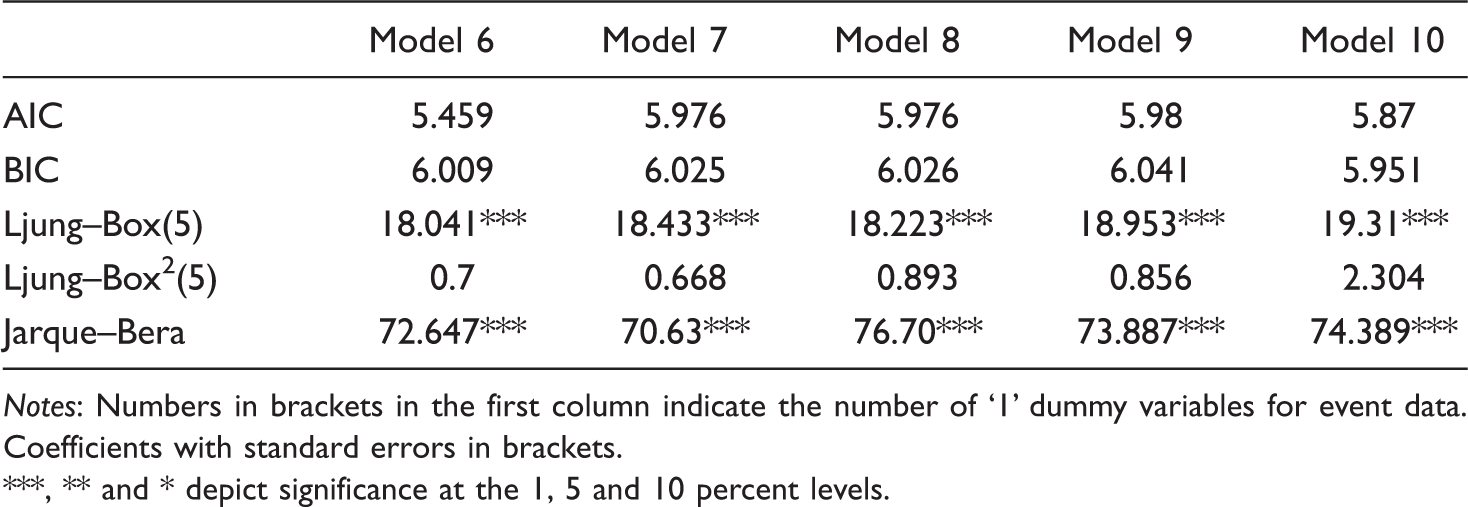

A particular characteristic of high-frequency financial data series (such as daily bond and swap rates) is non-stationarity, which finds its expression in unit roots. Here, the research design – with regard to event data comprising more than one trading day as well as focusing on the common default risk premium in terms of the IRSS – requires the application of discrete returns, which may be appropriate for unit root problems. We have iteratively checked whether the null hypothesis of non-stationarity of the IRSS time-series has to be rejected, with decreasing numbers of up to five lags. At the same time, we have allowed for trend and drift components, respectively, as well as for a suppressed constant in the IRSS time-series. In accordance with the Akaike Information Criterion (AIC), we chose the appropriate model for revealing stationarity. Both the augmented Dickey–Fuller (ADF) test and the non-parametric Phillips–Perron (PP) test clearly reject the null of a unit root in the integrated time-series at all conventional levels of significance. 5

Diagnostic tests

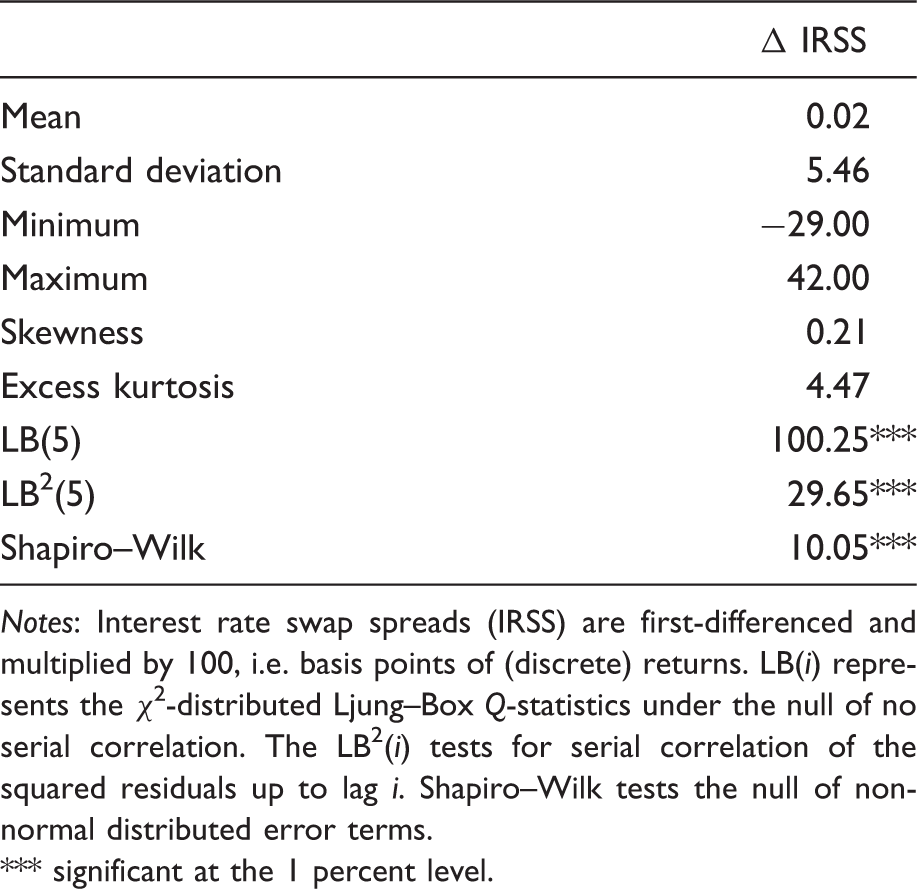

Notes: Interest rate swap spreads (IRSS) are first-differenced and multiplied by 100, i.e. basis points of (discrete) returns. LB(i) represents the χ2-distributed Ljung–Box Q-statistics under the null of no serial correlation. The LB2(i) tests for serial correlation of the squared residuals up to lag i. Shapiro–Wilk tests the null of non-normal distributed error terms.

significant at the 1 percent level.

Selection of the specific GARCH model

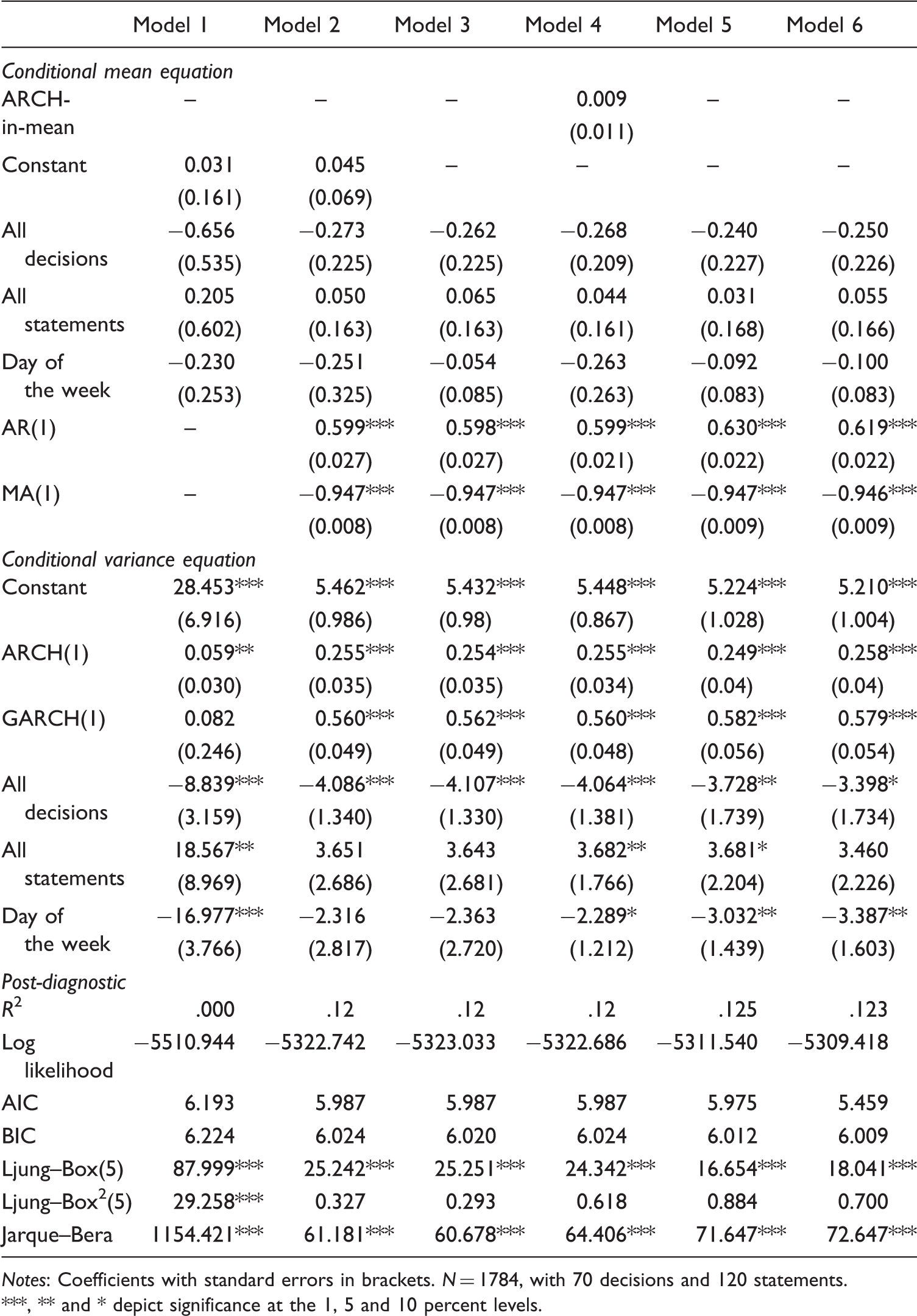

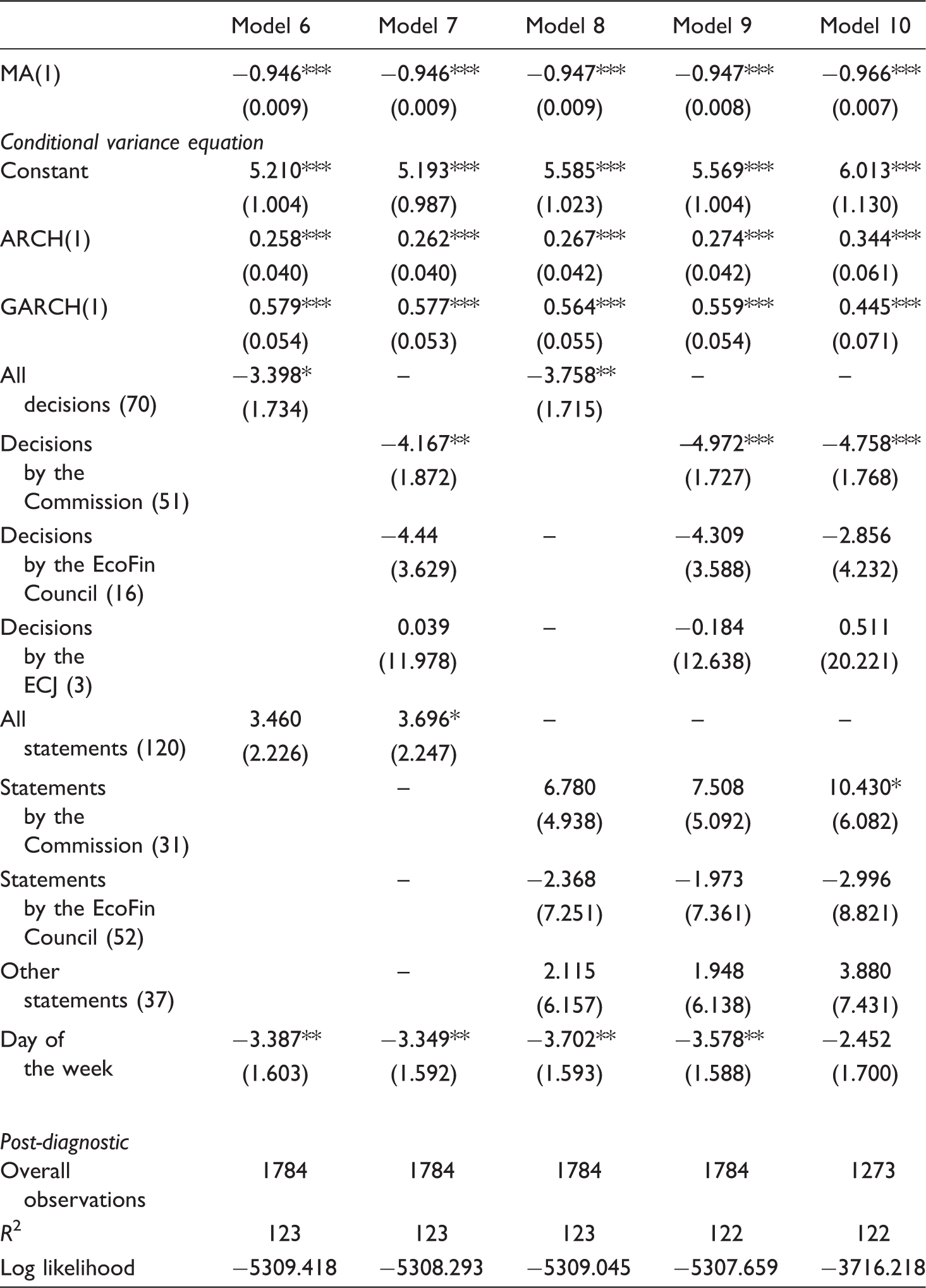

Notes: Coefficients with standard errors in brackets. N = 1784, with 70 decisions and 120 statements.

, ** and * depict significance at the 1, 5 and 10 percent levels.

Model 1 is a ‘plain-vanilla’ GARCH (1,1) that does not capture the conditional variance process in an appropriate way. This is particularly highlighted by the insignificant GARCH term. For this reason, we introduce the suggested ARMA terms in Model 2, which is then characterized by highly significant AR and MA terms for one lagged period. At this stage, the conditional variance process, in terms of non-heteroscedasticity in the post-regression residuals, behaves better according to the Ljung–Box Q2-test statistics. However, the residuals after regression are still not normally distributed. We try to eliminate this problem by suppressing the insignificant constant into the mean equation. The related Model 3 still suffers from very moderate serial correlation in error terms and severe non-normally distributed residuals. Therefore, we employ an EGARCH model, which accounts for the influence that the conditional variance process – that is, uncertainty in financial markets – may exert on the level of the common default risk premium. This model (Model 4) shows that there is no significant ARCH-in-mean effect that helps smooth the variance process. For this reason, we reject the assumption of normally distributed error terms and regress with generalized error distribution (Model 5) and t-student distribution (Model 6). A comparison of the post-diagnostic test statistics with the log likelihood, the AIC and the (Bayesian) Schwarz information criterion (BIC) reveals that an ARMA-GARCH (1,1) with presumed t-student distribution of the error terms is the best-fit model for further analysis. Although the residuals after regression still remain non-normally distributed, the presumed t-student distribution provides for subsequently adjusted standard errors of the coefficients. Heteroscedasticity is not a problem, but significant serial correlation still exists. However, the corresponding coefficients (not displayed) are around 0.02 and mostly negative. This means that the standard errors are rather overestimated, to the point that our baseline model arrives at very conservative estimates. At first glance, neither the variables for all decisions and all statements, nor the day-of-the-week effect exert any significant influence on the level of the common default risk premium. At the same time, our reference model (Model 6) indicates that the variable for all decisions affects the variance process of the common default risk premium. The same applies for the day–of-the-week effect. Regarding the impact of the variable for all statements, a comparison of Model 5 and Model 6 allows us to conjecture that we will probably face difficulties in detecting significant effects for this category of political events. Political event data are therefore subject to a thorough impact analysis.

Impact analysis

Impact analysis

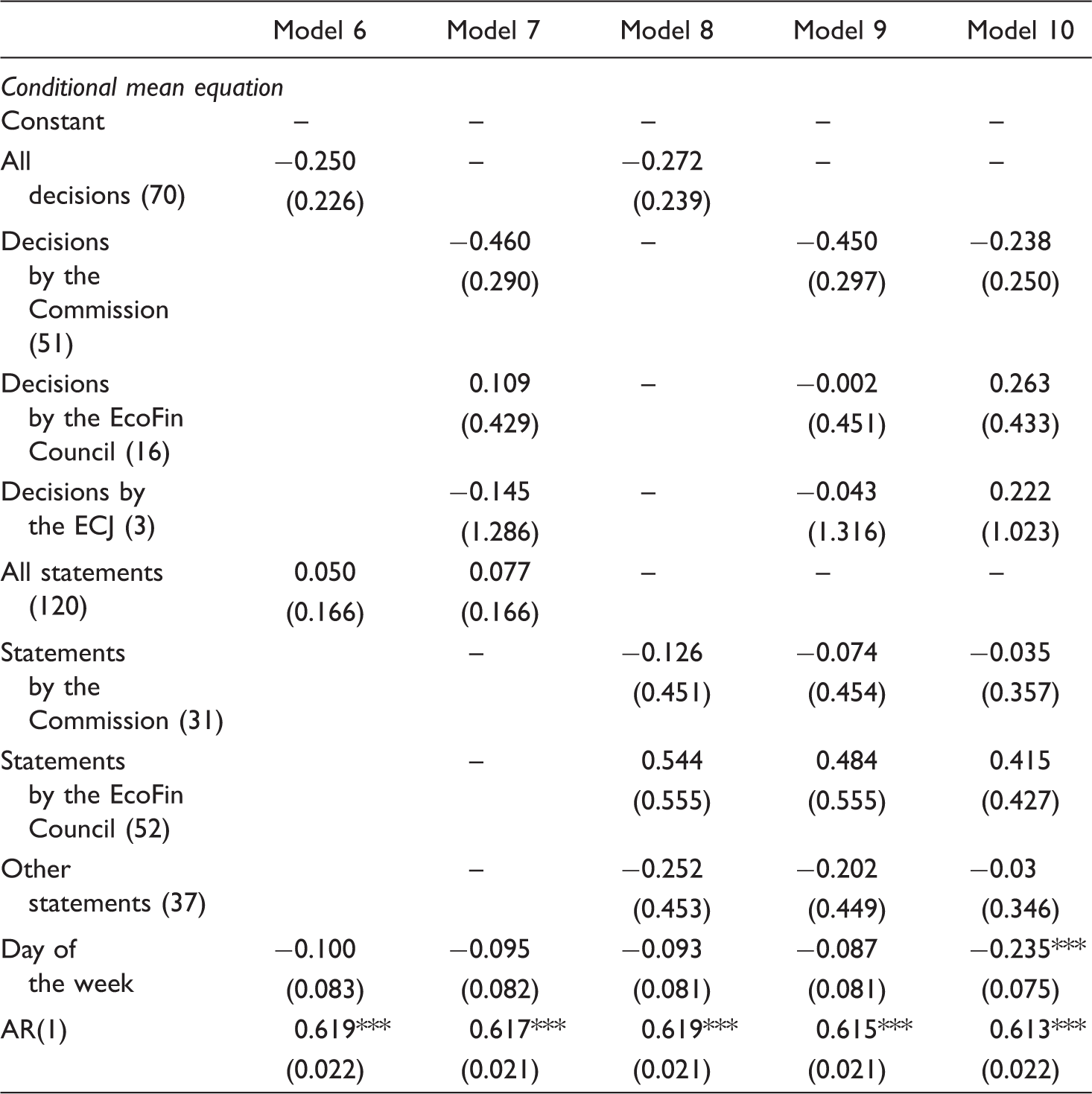

Notes: Numbers in brackets in the first column indicate the number of ‘1’ dummy variables for event data. Coefficients with standard errors in brackets.

, ** and * depict significance at the 1, 5 and 10 percent levels.

The first refined model (Model 7) examines the influence of decisions on the common default risk component, while all statements and the day-of-the-week effect are used as control variables in the conditional mean and variance equations. There are apparently no significant level effects by either the Commission, the EcoFin Council or the ECJ. However, decisions by the Commission considerably reduce uncertainty in financial markets. The volatility of the common default risk premium declines by about 4.1 units of variance here. The day-of-the-week effect also decreases uncertainty by about 3.3 units. Naturally, the opening day of a trading week represents a day off for financial investors because there are still four trading days remaining during which these actors may rebalance their portfolios. This result is confirmed in Models 7 to 9. Most interestingly, the variable for ‘all statements’ in Model 7 indicates that the rhetoric of politicians increases the volatility of the common default risk premium. Model 8 uses ‘all decisions’ as a variable, and the statements are differentiated into those from the Commission, the EcoFin Council (statements by ministers of finance/economics) and all other statements. At this stage, statements have no effect on the mean or on the volatility of the common default risk premium. However, previous regression results regarding the impact of decisions are confirmed. To further refine our analysis, we run the ARMA-GARCH (1,1) for all different types of decisions and statements simultaneously. Again, there are no significant level effects in Model 9. However, for decisions by the Commission, the absolute value of the coefficient in the variance equation slightly increases and turns out to be highly significant.

The final step of our analysis focuses on a restricted time period, namely 2001–5, in which the political destabilization of the legal framework was most prominent. Here, we expect political events to have had strong repercussions. We ran a regression on a smaller sample covering the period 1 January 2001 to 31 December 2005 (1273 observations). The subsequent Model 10 confirms our previous discovery that decisions by the Commission have an impact on the volatility of the common default risk component. In addition, we find that statements by the Commission bear heavily on the conditional variance process. Although there is only a low level of significance, a surge of 10 units in volatility is quite remarkable. At the same time, the small changes in both the (significant) ARMA and GARCH coefficients demonstrate the robustness of our regression results.

To summarize, the impact analysis lends no support to our hypothesis on level effects from decisions and statements. This means that, on average, decisions by the Commission (and the ECJ), which propose enforcement of SGP rules in terms of recommending an EWM and/or an EDP, do not affect the common default risk premium. Concerning the role of the EcoFin Council, our impact analysis indicates that neither decisions nor statements have a bearing on the common default risk component. With regard to decisions, uncertainty effects can be confirmed at very high levels of significance. A further refined analysis shows that this effect can be attributed to decisions by the Commission that decrease the volatility of the common default risk premium. Moreover, regarding hypothesis 2, statements by the Commission also seem to exert some influence on the uncertainty in financial markets, seen by an increase of about 10 points in the volatility of the common default risk component on average. However, statements by other key actors, in particular by the EcoFin Council, do not impact upon the volatility of the risk component. The growing volatility owing to destabilizing political statements by the Commission offers evidence that investors – in their attempt to anticipate certain developments – react strongly to unexpected new information. From a financial market perspective, the Commission seems to be the most important key actor in the context of the SGP. Decisions and statements by all other key actors, such as the EcoFin Council and the ECJ, are seemingly of minor relevance from the viewpoint of financial investors. Considering the EcoFin Council, we conjecture that this is because decisions were anticipated by financial markets and incorporated into the price prior to any official decision.

Conclusion

The analysis carried out in this article demonstrates that specific political events affect the sovereign creditworthiness of the euro area as a whole. Our empirical investigation reveals the significant influence of decisions and statements on the volatility of the common default risk component. In this respect, the SGP framework seems to play a key role in influencing financial investors' evaluations of the creditworthiness of the euro area. Basically, the SGP represents a type of ‘credibility anchor’ designed to ensure sustainable fiscal policies in member states. In turn, financial investors react to political events that undermine the credibility of the SGP. However, the conjecture that EU institutions weaken the creditworthiness of the euro area, in terms of level effects in the common default risk premium, is not supported by our empirical results.

A separate analysis of relevant actors highlighted the importance of the Commission as a provider of information for financial markets. Decisions by the Commission seem to remove some level of the uncertainty that characterizes financial markets. The observable reduction, which can be traced back to reports and recommendations by the Commission, is certainly not at odds with our argument that political events that weaken credibility increase volatility. Rather, the mitigating effect of Commission decisions on uncertainty shows that – from a financial investor perspective – Commission reports and recommendations are an indicator of the credible enforcement of the procedural rules of the SGP. This supports the conjecture that the Commission acts as the guardian of the SGP.

Furthermore, when focusing on the most contested political period, our study indicates that financial investors reacted strongly to signalling statements by the Commission. In this case, financial investors heightened the volatility of the common default risk premium. The reason for this is that statements by the Commission are generally unexpected and therefore depict ‘news’. In addition, the Commission's supranational orientation makes it more likely to uphold a Union-wide perspective (in contrast to the member states). Institutional credibility, therefore, crucially hinges on the Commission rather than on the intergovernmental EcoFin Council, since investors might in certain circumstances expect the EcoFin Council to become blocked by minorities.

The pattern evident in the data is of particular interest for EU politics, because it indicates the existence of a common default risk premium, as well as the considerable influence that EU institutions exert on financial markets in day-to-day politics. A common default risk component seems to add to the government bond yields of euro area members. This highlights the costly externalities caused by the monetary union, though more research is needed to test this claim. Given the weakened rigorousness of the SGP framework and the current sovereign debt crises within the euro area, the credibility of fiscal institutions will be of the utmost importance in rendering the monetary union more stable.

Footnotes

Acknowledgements

We want to thank the three anonymous referees as well as Andreas Busch, Robert Jung, Andreas Kern and Oliver Pamp for their comments. Roman Goldbach gratefully acknowledges the financial support of the FAZIT Stiftung and the Chair for Comparative Politics and Political Economy and Christian Fahrholz gratefully acknowledges the Ernst-Abbe Foundation. For their invaluable research assistance, we also want to express our gratitude to Julian Börner, Cordelia Friesendorf, Thomas Katzschner and Eléna Segalen.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.