Abstract

Brought to fame by a 1994 World Bank report, the idea of pension pillarization has become part of the orthodoxy of pension reform. Yet scholars have neglected both the national origins and the pre-1994 diffusion of the ‘three-pillar doctrine’. This article presents a critical history of the transnational diffusion process that led to the adoption of this concept at the World Bank. My analysis retrieves the Swiss roots of the doctrine during the late 1960s, as well as its gradual adoption and mainstreaming during the 1970s and early 1980s by a transnational epistemic community of life insurers and pension consultants. By 1990, the doctrine was widely used without reference to its national origins: a Swiss trademark had become a generic reform idea that framed controversies on the future shape of old-age provision.

‘Confidence in private pensions is at an all-time low … there have been calls to

move away from mixed pension systems back to an exclusive reliance on public

pay-as-you-go schemes. … This is the wrong way to go. … To prevent a backlash

and the reversal of past reforms, it will be important to restore people’s faith

in private pension saving. … If policy makers do not succeed in making a

convincing case for diversified retirement income systems, combining public and

private, pay-as-you-go and funded, individual and collective elements, they will

be thrown back to square one in their efforts to maintain prosperity in ageing

societies’ (OECD,

2009: 10).

This pessimistic OECD statement spells potential trouble for the ‘transnational campaign for social security reform’ (Orenstein, 2008). After well-publicized forays in Latin America and the former Eastern Bloc, this campaign has reached industrialized countries. The benefits cutbacks, higher retirement age thresholds and less generous indexation mechanisms introduced in the early 1990s in OECD countries mean that future state pensions may decrease by one-fifth (OECD, 2007: 74). Meanwhile, pension funds assets in the eleven countries with the largest pension markets rose from US$14.2 trillion (1998) to over US$24 trillion (2007), before falling precipitously to US$20.4 trillion in late 2008 (Watson Wyatt, 2009). As of early 2011, stock markets had rebounded, giving some breathing space to pension funds, but they have yet to regain lost ground. Although the ongoing crisis may have blunted the appeal of pension financialization, austerity pressures on pay-as-you-go (paygo) pensions are stronger than ever in a context of deteriorating public budgets.

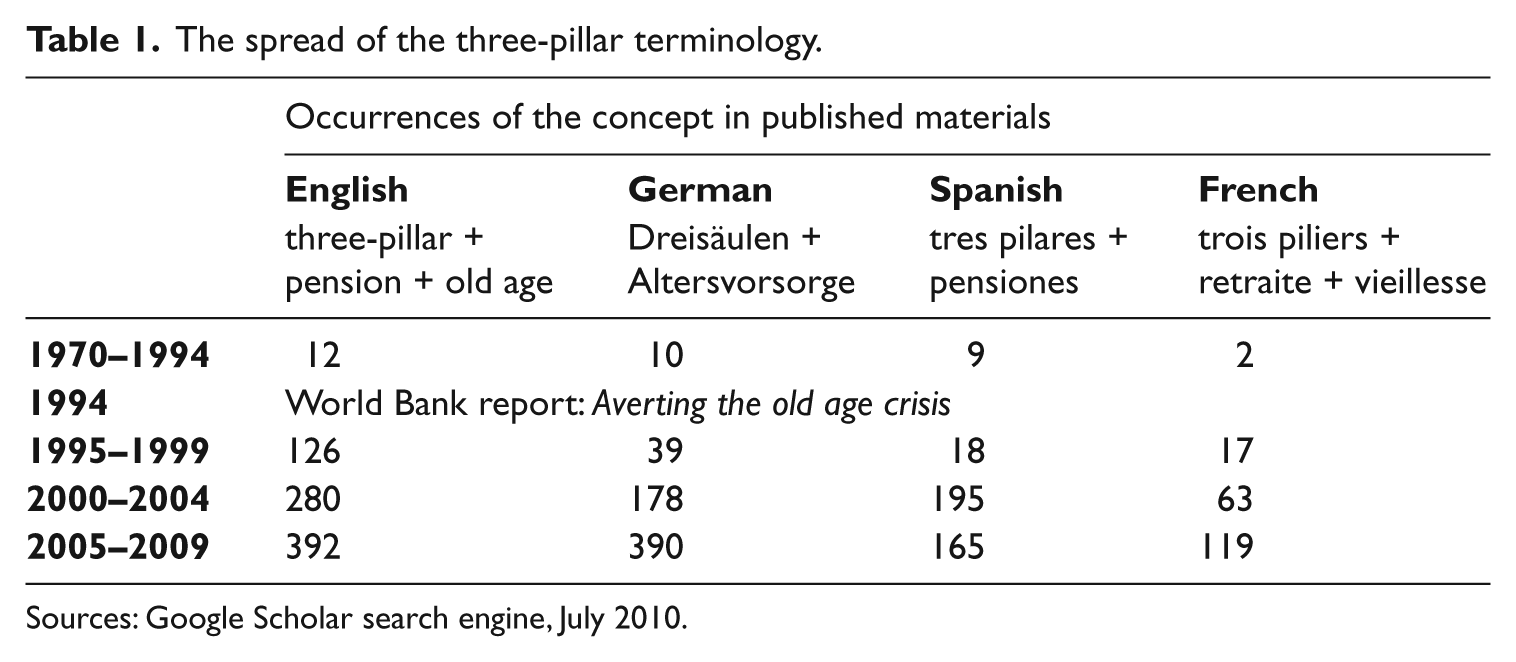

This article proposes a critical examination of the national roots and international diffusion of the three-pillar doctrine, a key reform concept that is implicitly hinted at in the OECD preference for ‘mixed pension systems’ (see above). Brought to fame by the World Bank (WB) report Averting the old age crisis (1994), this doctrine advocates a combination of basic state-based pay-as-you-go pensions (first pillar) and funded occupational and individual supplements (the second and third pillars). This agenda-setting report has become classic. Denouncing the demographic crisis looming over state pensions and economic distortions produced by payroll taxes (notably their burden on wages, their depressing impact on employment and, last but not least, their stifling effect on savings and capital markets), the WB extolled the virtues of privatization, individualization and financialization. These three pillars have been highly controversial (Orszag and Stiglitz, 2001; Tausch, 2002). Described as a neoliberal synthesis (Reynaud, 1996), they have become part of the new pensions orthodoxy (Müller et al., 1999). A basic survey (Table 1) underscores the post-1994 spread of the pillar concept in the academic and policy literature.

The spread of the three-pillar terminology.

Sources: Google Scholar search engine, July 2010.

The role of multilateral financial organizations as diffusion channels for global pension reform after 1994 has been well documented, with authors scrutinizing the WB’s role in Eastern Europe (Müller, 2003), Latin America (Brooks, 2009; Madrid, 2003) or the global stage (Blackburn, 2002; Minns, 2001; Orenstein, 2005, 2008). Pension reform has indeed become a textbook case for scholars analysing transnational ‘waves of institutional change’ (Weyland, 2008: 284). During the last decade, the ‘language of pillars and tiers’ (Immergut et al., 2007: 21–23) has also become common in comparative social policy handbooks. The concept is even used, somewhat anachronistically, to describe the pre-1990 development of supplementary pensions in Western Europe (Ferrera, 2005: 118–119).

While this extensive literature identifies ‘Averting the old-age crisis’ as a landmark, it fails to apprehend the pre-1994 history of the three-pillar doctrine. Indeed, most accounts designate the 1981 Chilean pension reform as the key national example upon which the ‘global drive to commodify pensions’ (Blackburn, 2002) and to ‘retire the state’ (Madrid, 2003) has been based. The international connections of the policy entrepreneurs who enacted the 1981 reform and then promoted it on a global stage with the support of influential Chicago school economists (Valdés, 1995) and international financial organizations (WB, IMF) has been recounted many times. Yet, if the Chilean express road towards privatization offers a clean-cut transition from statist paygo to individualized funding, the pervasive pillar metaphor definitely comes from elsewhere.

In 1993, economist Dimitri Vittas (Vittas, 1993) underlined that WB reform blueprints should be described as ‘Swiss Chilanpore’. In other words, a synthesis between Chilean individual retirement accounts, Singapore’s national provident fund and the Swiss three-pillar architecture (in particular, its mandatory occupational pensions, or second pillar). As provident funds rely on strong state steering, they have not attracted much attention from pro-market reformers. Nevertheless, as I will argue below, retracing the growing international reputation of the Swiss solution before 1994 helps us understand the later global success of the three-pillar doctrine.

If the Chilean reform constitutes a radical path towards privatization, the pillar metaphor offers a more gradual, and seemingly balanced, path. Instead of retiring the state, the three-pillar doctrine features several components, each of them working together to support a strong pension architecture, sometimes even represented as a genuine temple of provision (Figure 1). Yet this harmonious depiction is misleading: the different pillars have neither the same role nor the same weight in retirement provision. In fact, the three-pillar concept is highly normative and ideologically laden: it aims to both contain the scope of paygo and to entrench funded solutions at the core of retirement. In this sense, speaking of pillars instead of tiers (or layers) is far from innocent. On the contrary, unpacking this semantic choice reveals a pervasive ideational reform agenda.

The holy temple of old-age provision (2004).

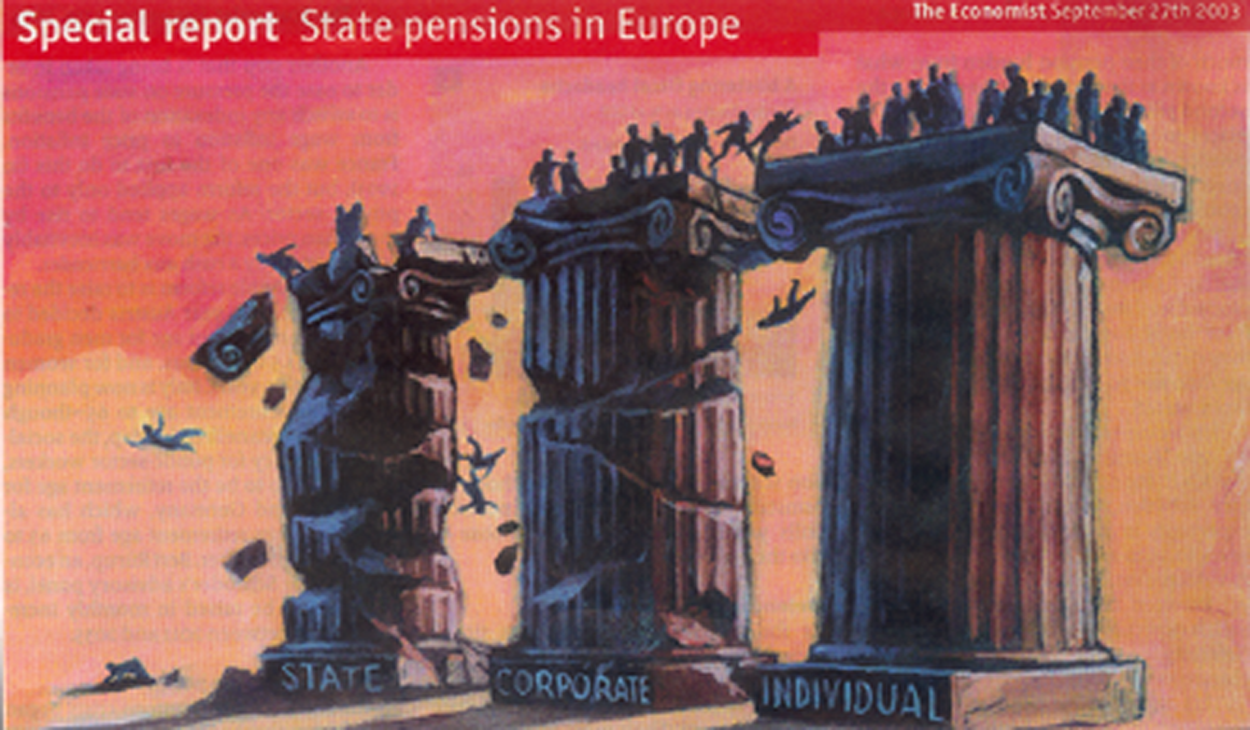

A cartoon illustrating The Economist’s pitch (2003) on Europe’s ‘crumbling pillars of old age’ may help clarify this statement (Figure 2). The distinguished financial weekly not only offered a graphic representation of the state, corporate and individual pillars, but also advocated governments to ‘cut back on the promises of the state pension system’ and to introduce ‘an element or two of compulsion’ to foster individual savings accounts. This cartoon highlighted the policy horizon of neoliberal pension reform, namely the third individual pillar, the solidity of which supposedly offered a safe haven in an age of uncertainty. Not incidentally, this article came out as the European Union was issuing new guidelines on pension funds. These directives, which I will return to below, represented the ‘first time the division (of old age provision) in pillars was explicitly integrated in EU law’ (Coron, 2007: 268). Yet, the cartoon only signalled the last stage of a long-term diffusion process that will be analysed in this article.

The crumbling pillars of old age (2003).

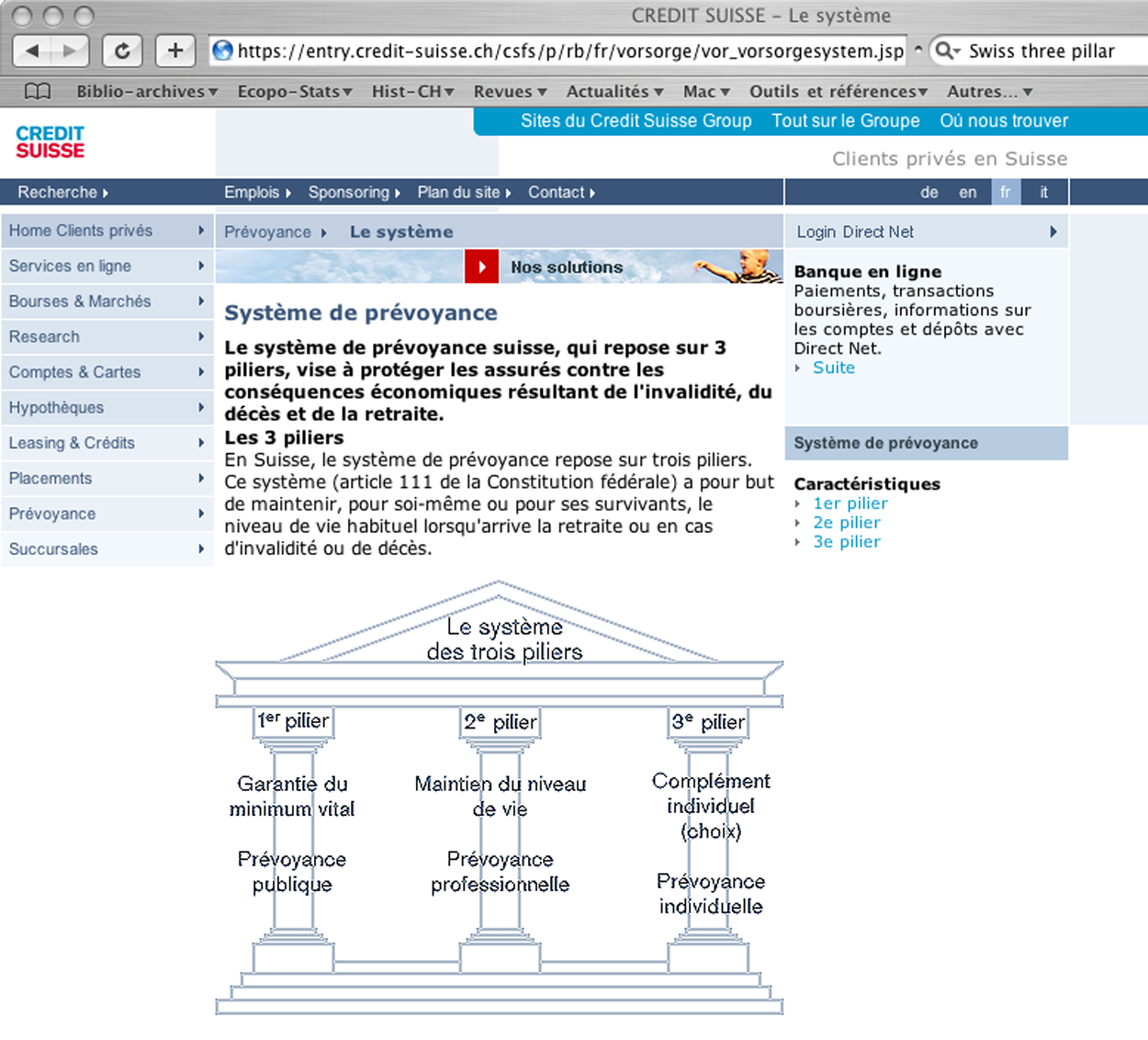

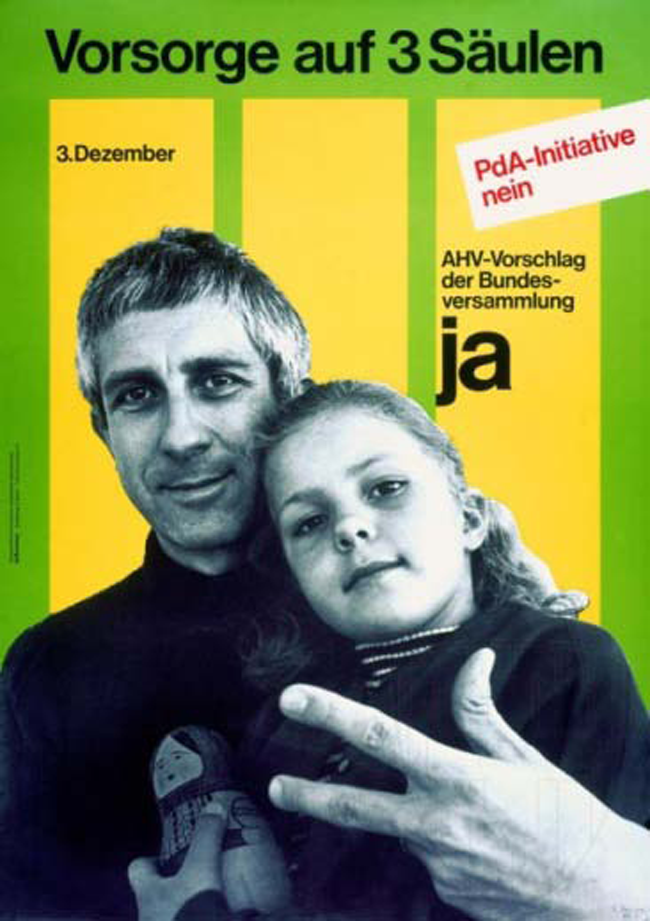

The normative use of the pillar metaphor had first crystallized a generation before, during a controversial pension debate in Switzerland in 1972 (Figure 3). Before this date, graphic representations of the Swiss pension system had been more diverse (Figure 4). The first section of this paper goes back to this domestic controversy. It analyses how the three-pillar doctrine became the quintessential ‘Swiss solution’, and how this doctrine was used to promote the twin aims of restraining the development of paygo and bolstering pension funds. By the 1980s, the three-pillar doctrine had become a genuine national trademark: it has been used ever since to market private pensions in Switzerland (see Figures 1, 5 and 6). The second section retraces a parallel trajectory, namely the transnational circulation, translation and adoption of this Swiss model among insurance and business networks during the 1970s. This process heralded the gradual transformation of a national trademark into an international generic model for pension reform. The third section presents how experts inside the OECD and the European Commission adopted the three-pillar metaphor around 1990. It confirms that the multi-pillar perspective was already known within international, and especially European, policy circles before the WB made it prominent in 1994.

Old-age provision on three pillars (1972).

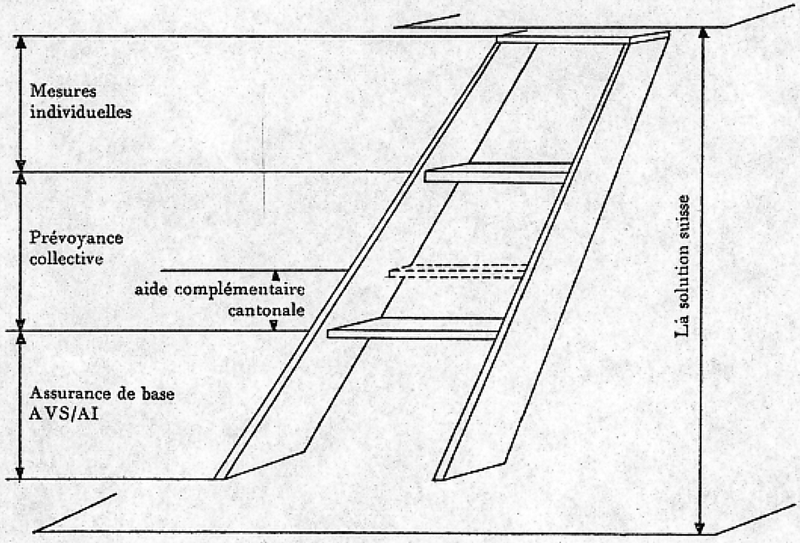

The ‘Swiss solution’ as a stepladder (1965).

Marketing the second pillar (1983).

Marketing the second pillar (1983).

The contemporary ubiquity of the pillar metaphor can be better understood if we connect the national origins of the concept with its early international diffusion and mainstreaming. Using a variety of archival sources and published materials, my analysis highlights the diffusion channels of the doctrine, the structures of the transnational networks that contributed to its aura of success, as well as the translation processes that subtly reshaped the national trademark into a potent generic in the space of a generation. Such historical approaches of ideational diffusion have not been at the centre of the rapidly expanding literature on transnational policy diffusion. While underscoring that ‘ideational processes constitute a key aspect of the impact of transnational actors’, a recent literature review (Béland and Orenstein, 2010: 1) only acknowledged in passing the input of historians to this domain. Yet, historical research is necessary to map the ‘circulation and appropriation of concepts beyond the borders of the national or linguistic community’ (Conrad, 2011: 228). This is all the more true if such processes take place in transnational communities and networks, such as the business and professional circles presented below. Indeed, these are not usually studied by social scientists focusing on more visible forums of transnational activity such as NGOs and international organizations.

Tiers, layers, stools, pyramids and pillars: the perplexing nomenclature of supplementary pensions

Well-versed connoisseurs of social policy might argue that pension pillars are hardly a unique Swiss occurrence. Indeed, multi-tiered retirement systems with basic paygo state pensions topped up by mandatory or voluntary supplements set up by the state and/or private providers on an occupational or individual basis have long been operating in countries such as the Netherlands, Sweden and Denmark, not to mention the USA and the UK (Rein and Rainwater, 1986; Rein and Turner, 2002; Reynaud et al., 1996). So why designate Switzerland as a model? Another objection might be that ternary metaphors have also been used in other national contexts. In 1950, Wilbur Cohen of the Social Security Board depicted US pensions as a ‘three-layer cake’ composed of federal, occupational and individual components: ‘The first layer being minimum subsistence; the second layer providing a more adequate standard supplemental to minimum subsistence; and the third ‘luxury’ layer being primarily a function of what the individual can do for himself’ (quoted in Klein, 2003: 188). The previous year, Reinhard Hohaus, a Metropolitan Life executive, had also coined the term ‘three-legged stool’ to describe the US pension mix:

‘The first in order of time is individual insurance … the second, a variety

of employee benefit plans of which Group insurance is an outstanding American

contribution; and the third, social security – designed by the government

for the well-being of our fellow citizens … Each has its own function to

perform and need not, and should not, be competitive with the others. When

soundly conceived, each class of insurance can perform its role better

because of the other two classes. Properly integrated, they may be looked

upon as a three-legged stool affording solid and well-rounded protection for

the citizen.’ (quoted in DeWitt, 1996)

Hohaus’ reversal of the order of old-age provision (in today’s parlance, from third to first pillar) underscored insurers’ preference for individual and occupational solutions. A generation before, Emile Marchand, director of the Swiss Life Insurance and Pension Company (Swiss Life), had already suggested a strikingly similar portrayal of the interdependence between state and private pensions. Speaking at the International Congress of Actuaries, he argued that ‘state pensions will only represent a supplement which will add itself to the savings accrued from one’s own work as well as, especially for wage workers, the sums which will have accrued from provident institutions set up by their employers’ (Marchand, 1927: 57).

Insurers’ preference for mixed pension structures has a long tradition. As we will see below, the proximity between insurers and the pillar metaphor constitutes a red thread of the international diffusion of the three-pillar doctrine. Before retracing this process, however, a brief portrait of Swiss occupational pensions will bring answers to the two objections mentioned above and clarify the motivations that underlay the international reputation of the Swiss pension system.

Occupational pension plans – the second pillar – have deep roots in Switzerland. Firm-based and group contracts managed by insurance companies steadily developed from the 1920s onward. By comparison, national Old Age and Survivors’ Insurance (Alters- und Hinterlassenenversicherung, AHV), the equivalent of US Social Security, was only introduced in 1947. By this date, the private pension lobby was powerful enough to contribute to limiting the scope of the paygo AHV so as not to crowd out existing occupational plans. During the post-war growth decades, the pension industry consolidated its positions: more than 15,000 pension plans existed by the late 1960s. This dense thicket included a few hundred large plans set up by private corporations and public administrations, as well as thousands of group insurance contracts. Pension plans assets were substantial and already reached 40 percent of Swiss GDP by 1970 (Leimgruber, 2008: 305). This trajectory diverged on several points from those followed by other European countries.

The early development and strength of the pension lobby thus differed from the situation that prevailed in Scandinavian countries, where second tier pensions had been developed, and mostly managed, by the state from the late 1950s onwards. The fragmentation of Swiss occupational pensions also contrasted with the Dutch configuration, where a few dozen multi-employer plans set up on an industry-wide basis dominated occupational provision. Early occupational plans with fragmented coverage as well as extensive involvement of life insurers in group pensions: all these elements suggest a strong resemblance between the Swiss example and the North American and British divided welfare states. Here are indeed typical examples of systems where basic state pensions have been used as a springboard for voluntary add-ons set up by public and private employers (Babich and Béland, 2007; Hacker, 2002; Hannah, 1986).

These similarities ended with the 1972 introduction of the three-pillar doctrine in the Swiss Constitution. This doctrine was formulated during the 1960s, when the private pensions lobby, and in particular life insurers, feared that the division of tasks between the basic AHV and supplementary funded pensions might be jeopardized by an alternative left-wing project, the so-called people’s pensions (Volkspensionen). The latter envisioned a dramatic expansion of paygo as well as stringent regulation to overcome the shortcomings of occupational pensions (notably their patchy coverage and unequal benefits). As a bulwark against this proposal, the three-pillar doctrine argued for the introduction of mandatory affiliation to occupational plans. Insurers promoted this second pillar as the best defence against a potential curtailment of private pensions, as well as a promising tool to market group contracts. The three-pillar conception emerged as a powerful ideational argument during the political struggle against the people’s pensions and was explicitly circulated for the purpose of strengthening funded provision. The pillar metaphor was of course grounded in the actual situation of the pension system, yet by claiming that this structure represented an ideal ‘Swiss solution’, insurers framed pension debates and achieved a decisive victory, first at the discursive and then at the political level. The three-pillar doctrine entered the Federal Constitution in 1972 after a vote (see Figure 3) that pitted a ‘people’s pensions’ proposal supported by the (communist) Labour Party against a three-pillar counter-project that enjoyed wide political support. Most trade unions, as well as the bulk of the Social Democratic Party, joined forces with business associations and the pension lobby to defeat the people’s pensions (Leimgruber, 2008: ch. 4).

Such support from social democratic and labour unions for the three-pillar doctrine might seem surprising. It was motivated by reformist hopes that, in addition to improving pensioners’ benefits, mandatory affiliation to occupational plans would enable workers’ control of pension plans, the financial reserves of which might then be harnessed for progressive investment. These hopes suffered from a severe miscalculation. Insurers and business owners had no interest in such socialization of pension assets and had designed the three-pillar doctrine as a bulwark to safeguard the pensions industry 1 to ensure business control over pensions assets, to enmesh trade unions in pension plans management, and, last but not least, to contain the development of the AHV. The ‘Swiss solution’ thus consolidated the division of tasks between paygo and funded pensions, to the detriment of the former and the advantage of the latter. While the development of the AHV was de facto frozen, funded plans were now designated as key social policy institutions. In the end, the Federal law on mandatory occupational provision (Berufliche Vorsorgegesetz, BVG), enacted in 1985 after a long delay, largely preserved the autonomy of pension plans. By then, the three-pillar doctrine had become an enduring fixture, both as the inescapable framework of the pension system and as a marketing metaphor for banks and insurance companies (see Figures 1, 5 and 6).

These specific outcomes explain why ternary metaphors have had much less traction in the US and the UK. In the US, ‘three-layer cakes’ and ‘three-legged stools’ have remained catchphrases for specialists without much policy implication. This is due to the fact that the introduction of mandatory affiliation to occupational pensions, briefly discussed during the 1970s, was rapidly shelved at the beginning of Ronald Reagan’s presidency (Hacker, 2002: 145–153). In the UK, the juxtaposition of competing state-based and private pension tiers has led to an inextricable pension mess rather than a clean-cut multi-pillar structure (Pemberton et al., 2006).

The question remains why, when and how the Swiss model was deemed interesting in international venues. The next two sections will address these issues in detail.

The three-pillar doctrine ventures abroad: expert networks and the emerging international pensions industry (1972–1980)

Early international mentions of the three-pillar system were clearly of a descriptive nature. In 1971, during the 5th International Conference of Social Security Actuaries and Statisticians (ICSSAS) held in Bern, sessions dealt with the Swiss ‘three-pillar concept’ as well as supplementary schemes in eleven other nations. One of the ICSSAS experts, Lucien Féraud, underlined that: ‘in recent years it has become customary to make a distinction between three “stages” or “pillars” of social security…’ (ISSA, 1973: A225). The ‘three-pillar principle’ was also mentioned during one of the first meetings of the European Institute for Social Security (EISS), a research outfit founded in 1969 that entertained close links with the Social Security Directorate of the European Commission. In a report outlining a typology of mixed pension systems, Guy Perrin of the International Labour Office (ILO) did not speak of ‘stages’ or ‘pillars’, but rather of the ‘tiers’ of the ‘Swedish pyramid’:

‘These diverse categories combine themselves and form a more or less complex

ensemble. The most accurate example of such ensembles remains the Swedish

pyramid, whose foundations rely on national state pensions, and is

constituted of three tiers corresponding respectively to the state-organized

supplementary pensions, the two inter-professional schemes for blue and

white collar workers, and finally the corporate schemes set up by private

firms for their higher paid managers.’ (EISS, 1973: 156)

In a further study of the International Social Security Association (ISSA), Féraud matched the idea of pension ‘pillars’ with Switzerland:

‘Generally speaking, within the last few decades complementary social

pensions have developed more quickly than general or special schemes and

have become unexpectedly important. In some countries they are comparable in

size to general schemes, both as regards total contributions paid and total

benefits distributed. The present trend is consequently to divide social

protection into three “stages” or sectors – in Switzerland called

“pillars”.’ (Féraud,

1975: 5)

These descriptions neither voiced a preference for multi-pillar pensions, nor urged their adoption. The Swiss case was considered one case among others, and the pillar concept remained an impassioned and descriptive metaphor circulating among a tightly knit group of actuaries and social security experts. The concept only displayed normative traits when European insurers and the emerging international pension industry embraced it.

Peter Binswanger, director of the Winterthur Life group pensions division, figured among the insurers who played a prominent role in shaping the three-pillar doctrine. As early as 1961, Binswanger had alerted his colleagues about the long-term challenge that the expansion of paygo set for private pension providers. The ‘Binswanger Commission’ had rallied insurance and business interests around the three-pillar doctrine and against the people’s pensions alternative (Leimgruber, 2008: 223–226). Binswanger communicated first-hand impressions of this controversy to European peers, for example in a 1970 memorandum addressed to the British Life Offices’ Association (LOA). 2 British interest for Swiss pensions came in the wake of the June 1970 electoral defeat of the Labour party. This defeat briefly shelved an ongoing controversy on supplementary earnings-related pensions, an issue that had long mobilized British insurers. In this context, much as in Switzerland, the LOA had defended group and individual plans against attempts to introduce state-based earnings-related supplements. Yet, the outcome of British pensions controversies differed from the Swiss ones: instead of a mandatory second pillar, British insurers insisted on contracting out, or the possibility for firms to opt out of the state-organized second pension tier (or State Earnings-Related Pension Scheme, SERPS, that would be finally introduced by Labour in 1978). Binswanger’s nomination in 1971 to the board of Provident Life facilitated further exchanges on this matter. The director of Provident Life, RJW Crabbe, chaired the LOA National Pensions Committee, a task force monitoring governmental proposals (BinswangerFestschrift, 1981: 45, 81, 83). These personal contacts were also facilitated by the fact that, until the 1973 entry of the UK in the EEC, Switzerland and Great Britain were the two most important ‘Non Six’ underwriting markets. Insurance representatives from both countries thus met regularly in ad hoc groups to discuss EEC issues.

Moreover, although Switzerland remained outside the EEC, its insurers worked closely with the Comité Européen des Assurances (CEA), a federation of national insurance organizations. 3 In 1976, a CEA report on comparative pension taxation already designated the ‘three-pillar principle’ as the basic ‘framework’ for harnessing the advantages of paygo and funded pension provision in Europe (CEA, 1976: 3). Elaborated by Swiss Life staff on behalf of the CEA, the study was distributed as a special issue of Sigma, a renowned research newsletter published by leading reinsurer Swiss Re. Despite all these Swiss fingerprints, this report displayed one of the first generic reference to the pillar concept. Swiss insurers’ contacts with their British peers and the CEA signal early evidence of an international diffusion of the three-pillar doctrine beyond domestic borders as well as its use without explicit reference to its national origins.

The birth of a global pensions industry acted as another channel for this early diffusion. Before the 1970s, supplementary pensions had developed in Western Europe along national lines, not least because of the limitations set by domestic insurance regulations. This situation began to change for two interrelated reasons. Firstly, the 1970s witnessed preliminary discussions about the liberalization of the European life insurance market, a process that lasted well into the 1990s (Werner, 2010). Secondly, the expansion of US multinational companies across Western Europe opened new opportunities for private pensions providers. How could a large US company with regional headquarters in Brussels or Zurich, and factories in Belgium, Italy and France coordinate corporate fringe benefits such as pensions for the expatriate managers the firm employed in these different countries?

In 1966, Swiss Life, a pioneer in this field, opened a London office offering cross-border pension contracts to multinational firms (The Economist, 1967, 1970). By the mid 1970s, half a dozen insurance networks set up by North American and European underwriters offered comparable services (Aaronovitch and Samson, 1985: 149). Retirement (as well as health) provision for multinational firms remained a niche market, but it facilitated the emergence of a global pensions industry. In addition to insurance networks, this emerging sector revolved around specialized newsletters (Benefits International, founded in 1971), international conferences for insurance brokers, as well as pensions and fund managers (such as International Benefits Information Services, IBIS, founded in 1969), and the European branches of US and UK pensions and actuarial consultancies (Hannah, 1986: 35–38, 72–33; Sass, 1997: 145–179). These international networks brought the Swiss model to a wider audience of business experts who, unlike the social security actuaries mentioned earlier, were not only interested in understanding the functioning of mixed pension systems but also keen on promoting the development of their funded components. In 1979, a US benefits journal thus designated the three-pillar model as an example to be followed and predicted that mandatory funded provision might well be the ‘wave of the future’, of which pension providers should take advantage (Hanrahan, 1979).

By the mid 1990s, the global pensions industry would act as a key relay for the promotion of the WB multi-pillar concept. Well before this date, however, the International Association for the Study of Insurance Economics, better known as the Geneva Association (GA), was already actively promoting the pillar idea. Founded in 1971, this think tank acted as a meeting point for a tightly knit network of leading insurance executives, first at the European level and later on a global scale (Leimgruber, 2009). Linking executives and academics, the GA set up a ‘State, Social Security and Savings’ research programme in 1976 to review the prospects of European group pension and health contracts. In a 1978 report, Walter Ackermann of the Insurance Institute of the St Gallen Business School designated the ‘three-tier model of old age welfare’, whose implementation was currently discussed in Switzerland (Ackermann, 1978: 12, 34), as the best way to counter the emerging ‘crisis of the welfare state’. Even if he found the pillar metaphor ‘rather unfortunate’ because it evoked schemes standing on their own side by side, rather than complementing each other, Ackermann (1980: 245) supported the normative dimension of the three-pillar doctrine, namely its encouragement of funded provision. During the same period, the three-pillar concept also entered a German encyclopedia of economics, in an article by a scholar who entertained links with the GA (Farny, 1977: 166). In short, European insurance networks had begun to replicate the domestic trajectory of the three-pillar doctrine. First presented as a merely descriptive tool, the concept was increasingly used as a discursive wedge to promote funded pensions and life insurers’ contribution to solving the looming crisis of the welfare state.

These examples highlight the early international career of the doctrine. This incubation phase took place among specific epistemic communities of social security experts and insurers. If the former mostly displayed an analytical interest in supplementary pensions, the latter had a vested interest in a terminology that advocated the expansion of funded provision to the detriment of its paygo component. Yet the involvement of insurers in the pension business is not sufficient to explain the international echo of the three-pillar doctrine. This second stage was only reached when the concept had been legitimized by multilateral organizations such as the OECD or the EEC, which boosted both its audience and reputation. The ‘crisis of the welfare state’ controversies that engulfed the West after the advent of Thatcher and Reagan offered fertile ground for pensions reforms based on expanded funding and financialization. Finally, we should not forget that, a decade after the 1972 constitutional change, the actual implementation of the Swiss mandatory second pillar in 1985 bolstered the international legitimacy of the concept. At a time when most other European countries were still improving paygo pensions and introducing early retirement solutions, the policy choices enacted in Switzerland offered a welcome alternative reform path for the business networks that strove to anchor private solutions at the heart of the welfare state.

The three-pillar doctrine goes mainstream (1980–1994)

By the early 1980s, the three-pillar doctrine was well entrenched and designated as a best practice by insurance networks. In a 1982 volume devoted to the ‘world crisis in social security’ published by a conservative American think tank and edited by a French free-market economist, the Swiss ‘three-component’ system and, more generally, funded old-age provision figured prominently among solutions to ‘plan for a lean national future while protecting the income security of the elderly’ (Rosa, 1982: 2, 121–148). Without naming Switzerland, Raymond Barre, a president of the GA before his tenure as Prime Minister of France, reiterated in 1983 the core principles of the doctrine. Emphasizing that states should ‘limit the extension of risk coverage through national solidarity schemes’, he added that they should also ‘facilitate, in addition to the collective protection of fundamental risks weighing on individuals, the development of risk coverage mechanisms based on group and personal insurance’ (Barre, 1983: 85). In 1986, just after the implementation of the Swiss ‘second pillar’, the GA launched a research programme on the ‘four pillars’ of retirement provision: ‘(We have) advocated a strengthening of the second pillar based on funding and a further development of third pillar resources. Our attention has, however, focused above all on the need in future years for a flexible extension of working-life, mainly on a part-time basis, in order to supplement the income of the existing three pillars’ (GA, 2007).

According to Orio Giarini, the long-time secretary of the association (interview with the author, 24 July 2007), the three-pillar concept had become so common among insurers that the GA estimated that it was the right time to develop it one step further. References to the ‘three-pillar system’ had indeed become frequent in German and French insurance publications (Babeau, 1985: 18, 33, 358; Heubeck, 1988; Lambert-Faivre, 1991: 894, 898). 4 The German association of pension funds also routinely used the term (Jung et al., 1987: 84, 99), while the Belgian insurers’ federation explicitly advocated the adoption of this model devoid from ‘either political affiliation or doctrinal content’ (UPEA, 1984: 71). A 1985 meeting of the CEA designated supplementary private benefits as a way to ‘safeguard the future’ of social provision and singled out the ‘three-pillar model’ as the way forward for pension reform. According to German executive G. Laskowski: ‘in most Western European countries, financial provision for old age, disability and early death risks are covered by several parallel systems. In the analyses of the CEA, these various systems are described as the three-pillar concept’ (CEA, 1985: 87, 161–162).

The Swiss ‘three-pillar theory’ had been briefly mentioned in OECD correspondence as early as 1979. 5 This isolated reference surfaced during the preparation of the agenda for the ‘welfare state in crisis’ conference convened in late 1980 by the organization. The OECD’s new involvement in social policy, with the twin objectives of containing (and even better decreasing) state social expenditure and developing private alternatives was a central feature of its new ‘Social Policy Studies’ (Leimgruber, forthcoming). In 1988, the fifth volume of this series singled out the Swiss ‘deliberate three-pillar approach’ alongside US, New Zealand and Japanese pension reforms (Holzmann, 1988: 108). The Austrian economist who had prepared the report, Robert Holzmann, was working at the IMF (1988–1990), where he studied the impact of the Chilean pension reform on financial markets. He would also head the WB Social Protection Department (1997-2000). 6 The stations of this career exemplify the proximity between the multilateral organizations that would become key promoters of the three-pillar doctrine during the 1990s. They also underscore how the pillar doctrine, mixed with the teachings of the Chilean experience, was taking shape before the WB convened the research team commissioned to elaborate Averting the old age crisis in 1992 (Brooks, 2004: 55). (Preliminary WB papers routinely used the pillar terminology, see Davis, 1993; James, 1992.)

While economists advocating pension funding contributed to the diffusion of the pillar metaphor, social security experts who were reticent towards the emerging pension privatization agenda carefully avoided the term. More innocuous concepts such as pension ‘tiers’ or ‘levels’ remained prevalent in contributions on supplementary pensions written by ILO staff (Tamburi and Mouton, 1986: 146–148). Ironically, advertisements paid by insurance companies and banks that used the pillar metaphor to sell pension products also made their way into the promotional leaflet distributed by the Swiss organizing committee for the 1983 ISSA conference held in Geneva (ISSA, 1983) (see Figures 5 and 6). A celebration of the centenary of Bismarck’s social insurance laws, this conference indeed coincided with the implementation of the mandatory second pillar in Switzerland, which opened a thriving market for group and individual pension providers.

These references to the three-pillar doctrine displayed not only its growing international reputation, but also its gradual detachment from its Swiss roots. This denationalization process is a telling example of how national reform trademarks can be repackaged into generic models while retaining their core normative content in the course of ideational diffusion processes. In other words, the pillar concept did not have to be labelled as Swiss to be used effectively. Yet, in all the cases mentioned above, as in Switzerland, it was used as a semantic marker to limit paygo and promote funded provision.

The adoption of the three-pillar doctrine by the EEC confirms this hypothesis. In July 1990, Leon Brittan, the British EEC Commissioner for Competition, advocated the foundation of a single market for pension funds during a speech (Brittan, 1990) given at the annual meeting of the International Pensions Conference (IPC), a reunion of leading pension funds. This agenda had apparently been discussed with the European Federation for Retirement Provision (EFRP), a mouthpiece of the pensions industry (Steward, 1999), and inaugurated a long-term lobbying campaign. In October 1990, a European Commission working paper developed Brittan’s impulse and listed the necessary steps to ‘achieve a single market for private pensions’. Its introduction stated that a ‘three-pillar system’ was ‘in principle’ in operation in ‘all EEC member countries’ (CEE, 1990: 1–2). The report did not mention Switzerland, which was not (and is still not) a member of the EEC. Consequently, this stance is often considered a promotion of Anglo-American funded pensions in Continental Europe. Yet, as the three-pillar concept would not surface in US and UK pension debates until after the 1994 WB report, this working paper should rather be considered as further evidence of the denationalization of the three-pillar doctrine and its increasing generic use. Brittan’s links with milieus that either dealt with cross-European pension funds or knew the Swiss experience through professional or associative contacts adds weight to this hypothesis.

Brittan’s proposal did not lead to immediate results. The first 1991 EEC directive on occupational pensions in the Single Market and its follow up Green Paper on supplementary pensions (1997) were contested in court by Spain and France, as they ignored the peculiarities of their paygo-based supplementary pension schemes. After much political wrangling, a second draft was finally accepted in 2003 (Haverland, 2007; Math, 2001; Pochet and Natali, 2005). According to Gaël Coron (2007: 263), ‘this political process finally enabled the diffusion and the naturalization of the pillarized conception [of the pension system]…’. By this date, this naturalization process had reached far beyond experts’ networks or international organizations (see Figure 2).

The three-pillar doctrine has continued to spread either with or without reference to its Swiss origins. During the last decade, the European Financial Services Roundtable (EFR), established in 2001 on the model of the European Roundtable of Industrialists (Apeldoorn, 2000), has been vigorously advocating multi-pillar schemes. Using the slogan ‘One Europe, One Pension’, the EFR (2002, 2007) has lobbied for portable third-pillar solutions designed for cross-border employees. Once again, financialization and individualization figure at the centre of a generic multi-pillar pension concept. Yet, the Swiss origins of the concept also keep resurfacing. In 2008, OECD expert Monika Queisser urged German politicians to adopt the Swiss three-pillar model as a solution to defuse a looming pension crisis (Spiegel, 2008). Before working at the OECD, Queisser had written in 1993 a paper on Chilean pensions at the Munich Ifo research institute and co-authored a WB report that praised the Swiss system as a ‘triumph of common sense’ (Queisser and Vittas, 2000). As a Swiss Re economist boasted at the turn of the millennium: ‘the Swiss pension system comes off rather well in comparison to the rotten social insurance systems of its European neighbors (and) rightly deserves the high esteem it receives from abroad: its foundations are properly laid’ (Trauth, 2000). More recently, Mercer, a leading international consultancy, even awarded a ‘gold medal’ to the Swiss pension system (NZZ, 2010). In short, we are far from having seen the last iteration of the three-pillar doctrine.

Conclusion

Missing links remain to be uncovered in the diffusion chain leading from the anchoring of the three-pillar doctrine in the Swiss Constitution in 1972 to its adoption by the WB in 1994. Yet, this paper has offered detailed evidence of the early transnational propagation of the doctrine, a necessary phase of incubation, translation and mainstreaming that enabled a further, and much stronger, wave of ideational diffusion. Skeptical readers may still argue that multi-pillar metaphors are merely descriptive. All that comes out of Switzerland, however, is far from being neutral: at the domestic as well as at the international level, the three-pillar doctrine has been used to frame pension debates and to promote funded solutions. In similar ways as the radical Chilean model based on outright pension privatization and individualization, the three-pillar doctrine seeks to entrench private pensions providers, to expand privately controlled funding mechanisms and to open new territories for private insurance. Yet, one of the key advantages of the doctrine resides in the fact that it does not recommend outright privatization, a prospect that is highly controversial in democratic polities with well-developed paygo systems. Instead, under the guise of a mixed pension system, the doctrine promotes a long-term bifurcation towards occupational and individual funding.

This explains why the pillar concept has been so popular among insurers. While the Chilean example is too extreme for Western European realities, the intricate Swiss mix enables a more euphemized, but potent, advocacy of private solutions. The key role of Swiss and European insurers in the diffusion of the pillar doctrine also underscores that the pension privatization agenda has not only Anglo-American roots, and that it is far from being imposed from abroad. On the contrary, this agenda has European promoters and uses European models.

Scholars of transnational policy diffusion have tended to remain at a macro-level, focusing on the role of large international organizations, and have spent less time mapping and retracing diffusion among a variety of sources and documents produced by more informal networks. While the implosion of the USSR and the Eastern Bloc of course opened new opportunities for pension privatization drives, the seeds and core orientations of these campaigns had been planted well before the late 1980s. In this sense, the 1970s should be considered as a central laboratory for these later developments. Selecting ‘1981’ as the Chilean signpost heralding the ‘age of privatization’ (Hu and Manning, 2010) and ‘1994’ and the WB as the second agenda-setting moment distorts our understanding of these controversies.

On a methodological level, the current proliferation of the pillar metaphor among social scientists confirms that the indiscriminate use of ideologically laden concepts may in the end contribute to bolster their credibility at the time when such concepts should be submitted to a thorough critical inquiry. In this sense, the limited case study analysed in this paper has broader implications, and not only because pensions play such a central role in contemporary social policy. The evidence presented here underscores the need for truly historical investigations of contemporary policy concepts. A powerful example of such a research agenda is laid out in Daniel Rodgers’ (2011) exploration of the ‘age of fracture’, or how the reshaping of ideas during the crises and mutations of the late 20th century led to an enduring reorientation of political, social and economic priorities.

Footnotes

Acknowledgements

I would like of thank Dr Marek Naczyk (Oxford) for sharing Belgian sources mentioned in this article.

Research for this paper has been supported by a Swiss National Science Foundation grant (n° PZ00P_121611). Preliminary versions have been presented at the Paris School of Economics and the World Economic History Conference (Utrecht, 2009) as well as the «Made in Switzerland» conference (Neuchâtel, 2010).