Abstract

We investigate the role of consumer-oriented media influence on their purchase intentions, how this influence changes from a stable economic situation to a recessionary period and what are its repercussions on marketers’ media selection. We use survey data from the US in the clothing category for the 2008 economic recession to investigate the individual and synergy effects of Promotional and Informational Media and how this evolves with the economic cycle. In line with Construal Level Theory, we find that consumers are in a low-level mindset during recessions and hence value the feasibility of a purchase important, whereas they are in a high-level mindset during stable economic times and focus on the desirability of a purchase. This results in positive media synergy (across multiple media) during stable times, however during recessions, influence of individual media is stronger. We provide robustness checks with electronics and groceries categories. Insights from this research provide marketers with an approach for strategic media selection during economic fluctuations using survey data, that is robust across categories and hence can be implemented across other recession scenarios.

Keywords

Introduction

Before the Coronavirus pandemic-induced economic challenges, no other recent crisis has seen a greater impact on the global economy than the financial crisis of 2008. The drastic economic impact of 2008 financial crisis and the Coronavirus pandemic were driven by the changes in behavior of both consumers and markets.

While macroeconomic contractions have significant impact on consumer behavior, firms also need to adjust their marketing activities to adapt to the changing economic landscape. Effective adaptations require understanding of consumer orientation, with respect to consumers’ media consumption patterns. In this research we identify how marketers can employ strategic media choice based on a consumer-oriented approach, during economic fluctuations, using survey data, as media synergy influences purchase behavior. With evidence from the recession that affected the US economy in 2008 following the financial crisis, our insights can provide industry-specific guidance (consumables vs. durables). The recommendations for single vs. multiple media choice are especially useful for future recessions, like the economic challenges in the aftermath of the Coronavirus pandemic.

For marketers, one of the important decisions during recessions is the allocation of limited marketing resources across alternative advertising media. There is evidence that decreased advertising is not necessarily the most prudent strategy during economic downturn and studies have found the positive impact of advertising on firm’s financial parameters (Frankenberger & Graham, 2003; Srinivasan et al., 2005; Van Heerde et al., 2009). Proactive advertising during economic downturns, i.e. targeted spending on specific advertising media (addition/substitution/omission of a particular media) for each category is a better approach than rationing advertising.

Additionally, marketers cannot simply direct their advertising messages towards consumers through their chosen media. Consumers play an important role in deciding what media to use, either for information search or for actual purchases. In the case of high involvement products, consumers are more likely to focus on media that provides product-related information. For low involvement products, promotional media might be more effective. Also, with different media sources influencing consumers’ decisions simultaneously, exposure to multiple media either reinforces advertising messages or creates conflict across messages.

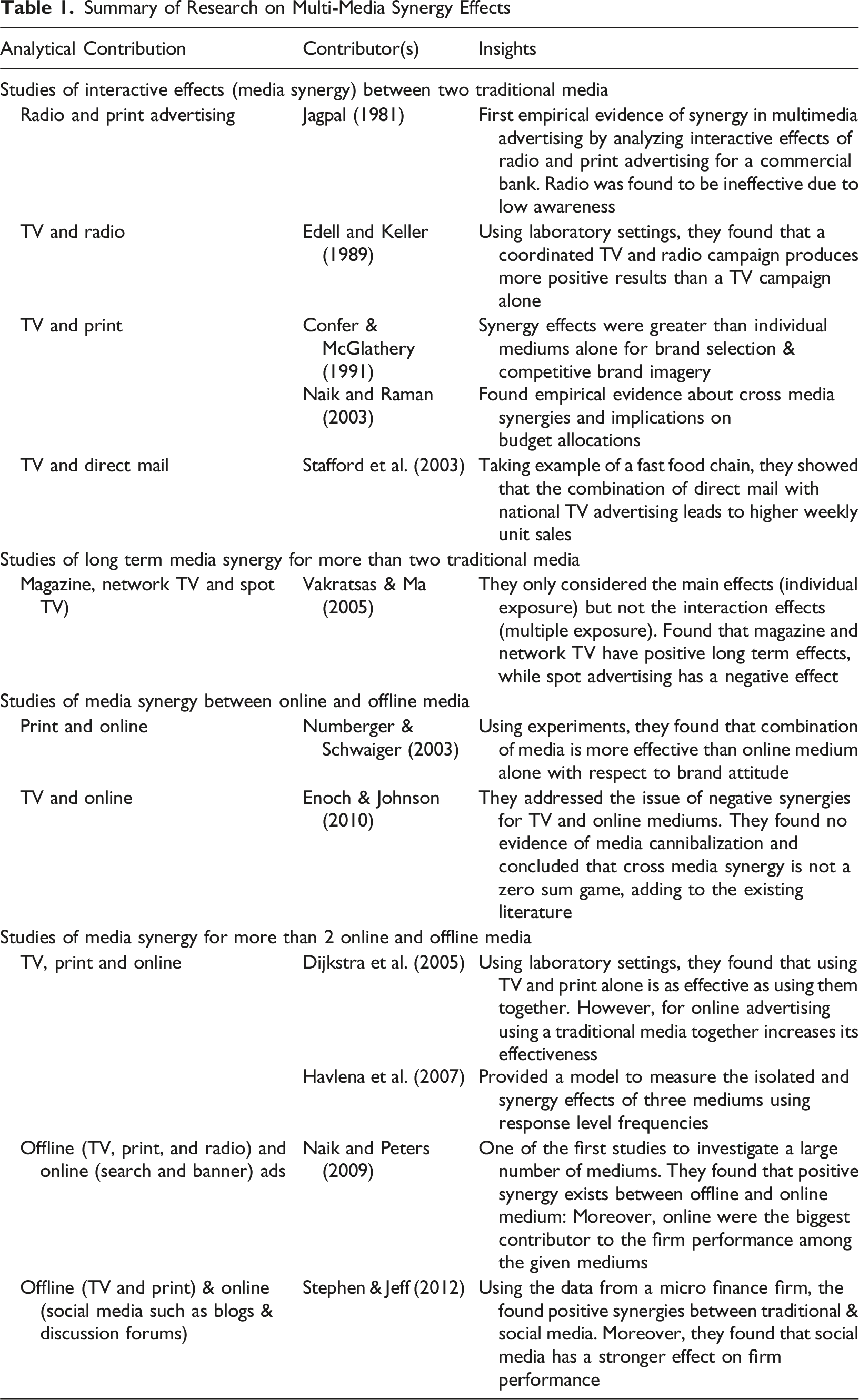

The literature on media synergy in marketing mainly focuses on the interaction effects of two or more advertising media to understand which media have a positive influence, which ones have negative influence or are effects of multiple media neutral. Researchers have studied media synergy effects on consumer behavior and resulting firm performance – e.g. radio and print advertising (Jagpal, 1981); TV and Radio (Edell & Keller, 1989); TV and print (Naik & Raman, 2003); offline and online (Naik & Peters, 2009).

However, most media synergy studies use firm level advertising exposure or spending data. This presents a limited view on media synergy as the consumer’s perspective is not considered. It is important to consider how consumers decide on combining media forms as opposed to how marketers choose to combine them in their campaigns. Additionally, it is important to measure the cumulative or relative effects of different advertising media along with their individual effects. When consumers’ media consumption and purchase decisions change during economic fluctuations, it also becomes to investigate whether media synergies persist during economic stability and do they synergies carry over during the recessions.

During recessions, there is not only change in purchase behavior of consumers, but media influences also evolve. There is a potential gain from strategic media allocation during recessions when resources are scarce. Also, when firm-level advertising exposure or sales data is not available, there can be value of self-reported survey data on media influence and purchase intention to determine these media synergies. Based on these challenges, we intend to address the following research questions: (1) For a given product category, what advertising media are the most prominent influencers of consumer purchase behavior during economic stability vs. economic downturns? (2) Do the chosen media provide a positive synergy and do these synergies change during economic volatility compared to stable economic conditions? (3) Can marketers make a strategic choice in their selection between individual and multiple media when they are faced with recessions with an approach that is not limited to specific recession episode? (4) Can we use survey data from multiple sources having different frequencies and without identifiable respondents to provide generalizable conclusions about media synergies?

We conduct our research in the context of the clothing category, with robustness checks done for electronics & groceries, which cover the spectrum of high to low involvement products. The consumer purchase data is extracted from a US based monthly survey called Customer Intentions and Actions (CIA) (Source: Prosper Foundation Insight Center). We have combined this data with another US based bi-annual survey of media exposure called Simultaneous Media Usage (SIMM) (Source: Prosper Foundation Insight Center). Our analysis covers 36 months of data, starting from January 2008 up to December 2010 which includes the build-up period of the recession that hit the US economy in September 2008, the critical period that lead to the failure of financial institutions and the period in the aftermath of the recession. We follow the definition of recessions proposed by NBER and use fluctuations in US GDP levels (Source: US Bureau of Economic Analysis) to create a dummy variable representing economic fluctuations. We also include a variable on economic outlook of consumers and investment confidence to reflect individual perceptions of economic fluctuations. Further we used socio-demographic variables such as Gender, Education and Marital Status to control heterogeneity in purchase behavior.

The rest of the paper is organized as follows. First, we discuss the literature on the impact of advertising investments during recessions and highlight how our research adds to the understanding of targeted advertising spending. Further, we discuss the literature on media synergy and its impact on firm performance. We also provide a theoretical explanation for the changing influence of individual vs. multiple media during recessions. We then describe the data used for our analyses and proceed with a brief specification of our model (O-Probit). The discussion of our main findings based on the model estimation follows along with the multi-category analysis. We conclude by discussing the implications of our study, data and model limitations and suggesting directions for future research.

Literature Review and Theoretical Background

In the marketing literature, researchers have investigated how multiple media usage in advertising campaigns can affect media synergy. However, we emphasize the importance of understanding the changes in media influence on consumer behavior during recessions relative to stable conditions and investigate marketers’ rationale behind choosing individual versus multiple media during the economic cycles.

Firms’ Strategic Adjustments During Recessions

There is considerable variation in firm performance in response to recessions. Though economic logic suggests that decreased consumer spending during recessions might automatically lead to cuts in firm’s advertising budgets, researchers have provided counter-intuitive evidence (Van Heerde et al., 2009). Dhalla (1980) shows that firms can increase their advertising to get more consumer attention and improve their performance. Kamber (2002) gives further evidence of a positive impact of advertising on product sales during recessions.

However, the focus of researchers has been confined to the role of advertising expenses across different media sources during recessions at an aggregate level. Even though there is a strong recommendation towards targeted advertising during recessions, it might well be the case that some media are more effective than others during economic cycles for individual consumers.

Consumers’ Responses when Resources are Limited

Dutt and Padmanabhan (2011) observe adjustment in spending across durables, non-durables and services during recessions and Millet et al. (2012) showed a shift in spending from products and services with positive outcomes (e.g. gambling) to those with negative outcomes (e.g. insurance). In a related study, Kamakura and Du (2012) show that consumers tend to consume less discretionary products and more necessary products, even without any changes in their allocated budget. While contractions usually lead to downward adjustments on durables (discretionary) spending instantaneously, during subsequent expansions, spending on durables do not immediately adjust upwards (Deleersnyder et al., 2004).

Media Synergy - a Marketer’s & Consumer’s Perspective

Summary of Research on Multi-Media Synergy Effects

Most of the research explores synergy between different media using firm level advertising data, inherently analyzing the choices of media made by the marketer. However, consumers of today are flooded with advertising messages, and this information overload might lead them to overlook information conveyed through certain media. Consumers choose the media that facilitates their purchase decisions based on their specific needs. Schultz et al. (2009a, 2009b) uses CHIAD analysis and consumer-oriented media influence data to identify potential synergies between media in a multi category analysis. This topic was further developed by Schultz et al. (2012) where they provide a methodology to understand consumer-oriented media synergy between traditional and online media.

Choice Between Individual and Multiple Media Strategies during Economic Cycles

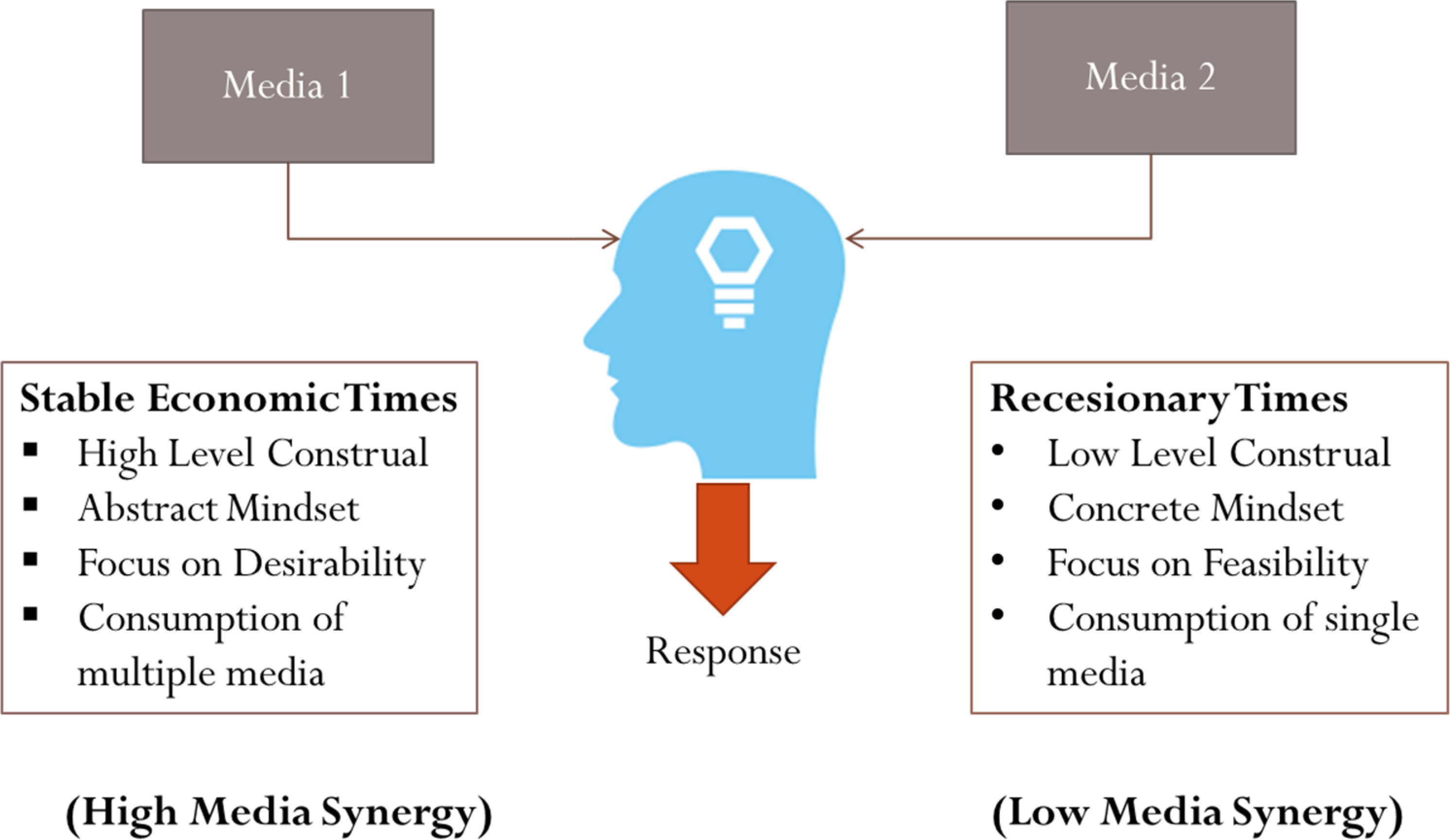

In literature, there is no understanding of the positive or negative synergies which might result from multi-media exposure of consumers and whether these synergies can change during economic downturns compared to periods of economic stability. According to the Construal Level Theory, psychological distance from an event affects the mindset of the consumer. Individual forms a low (high) level construal/concrete (abstract) mindset depending upon the proximity to the event (Liberman et al., 2002). Some researchers have also shown how regulatory focus can affect the construal level. They find that when people are in prevention focus, they are likely to construe information at a concrete level, while the promotion focused individuals are likely to construe information at an abstract level. During stable economic times consumers are likely to be in promotion focus and hence would value the desirability of their purchases more, while during the recessions consumers are likely to be in prevention focus and hence would value the feasibility of their purchases more (Lee et al., 2010; Liberman & Trope, 1998).

Hence, during the stable economic times, consumers would be more willing to get influenced by multiple sources of media (which are complementary) when making their purchases, given their abstract high-level promotion-focused mindset. However, during the recession, consumers would be more willing to focus on individual media sources (which are substitutable) given their concrete low-level prevention-focused mindset.

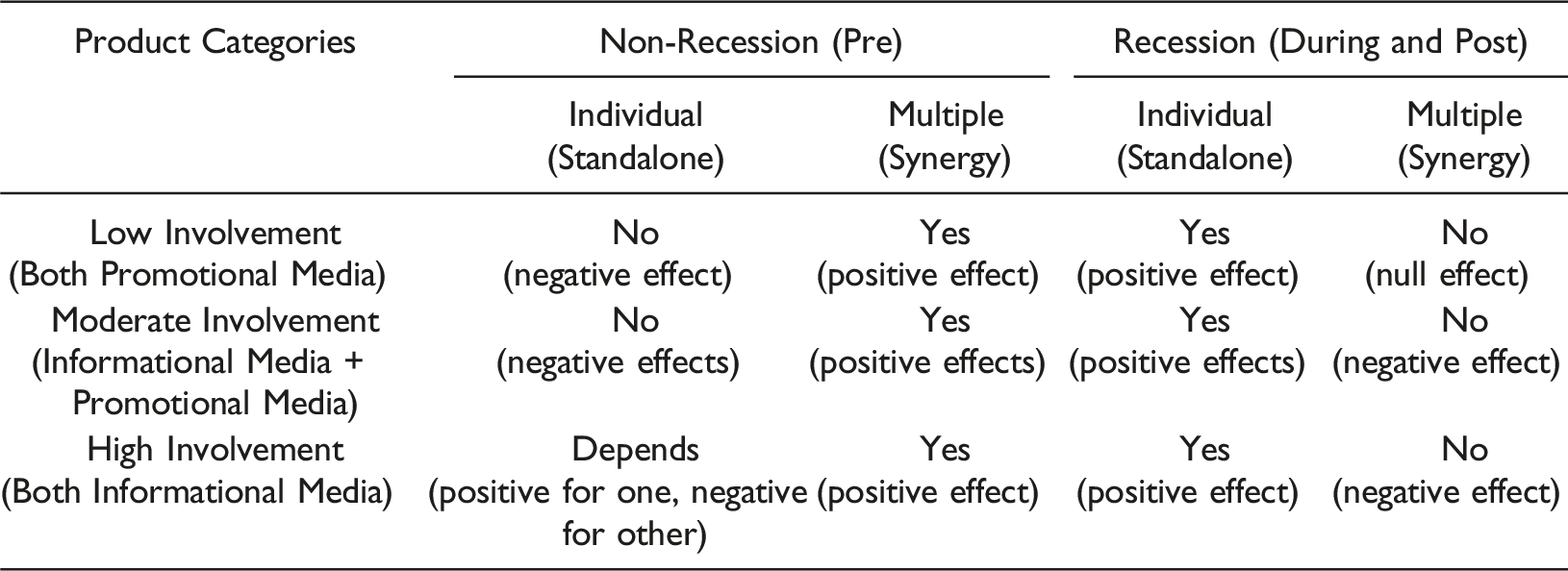

Figure 1 summarizes the impact of economic fluctuations on consumer-oriented media synergy based on Construal Level Theory. Changing impact of media synergy along with the economic cycles

Also, for categories that require moderate degree of involvement (i.e. clothing), consumers might be influenced by both desirability-oriented media (i.e. TV Ads) and feasibility-oriented media (price discounts) during periods of economic stability, but when they encounter recessions, the synergy effects disappear, and individual media, specially those which are prevention-focused, are likely to become more relevant.

This pattern of results is likely to be carried forward to high-involvement categories, like electronics, though the media sources might be driven by information gathering motives (i.e. WOM and articles). However, even in this case, while synergies are expected during economic stability as consumers are likely to collect information from alternative sources, they will disappear when recessions hit, as consumers focus on the relevant informational media that maintain their concrete prevention-focused mindset.

For a low-involvement category, like groceries, though the preferred media are likely to be promotional (price-related coupons or nonprice related inserts), consumers are attentive to the desirability of their purchases, are in an abstract mindset and often use these at the same time. But as they encounter economic downturns, they look for specific promotional media that put them in a high-level construal and provide best outcome in terms of feasibility of the purchase (discounts that make the groceries affordable).

These arguments lead us to the following research hypotheses that we intend to verify:

During stable macroeconomic periods, cross-media interactions (synergy) are positive (complementarity)

During recessionary periods, cross-media interaction terms (synergy) either weaken or become negative (substitutability)

These synergy patterns differ in the continuum of high- to low-involvement categories in similarly, albeit the influential media sources differ across categories in predictable ways.

Research Design

Data Description

Our analysis covers 36 periods of data, from January 2008 to December 2010. The reason for considering this time window is to account for the business cycle fluctuations experienced by the US economy during that period, though other recession episodes can be considered as application context. We divided this time window into 3 groups: • ‘Pre-Recession’ corresponds to the period from January 2008 to August 2008. • ‘During-Recession’ corresponds to the period from September 2008 to December 2009. • ‘Post-Recession’ corresponds to the period from January 2010 to December 2010.

In order to distinguish between the 3 periods, our cutoff criterion is based on the definition of recession suggested by NBER, which includes observed fluctuations in the US GDP levels (Source: US Bureau of Economic Analysis) and movements in the US Unemployment levels (Source: US Bureau of Labor Statistics).

Apart from the economic indicators, the rest of the data for our analysis comes from 2 primary sources. For all 3 categories we obtained the self-reported ‘purchase intentions’ of consumers (for following 90 days), demographic characteristics of consumers (gender, education level and marital status) along with consumers’ perspective on the business cycle (economic outlook and investment confidence) from a US based monthly survey called Customer Intentions and Actions (CIA) (Source: Prosper Foundation Insight Center), with around 8000+ respondents on average per month. The data on consumer’s self-stated influence of advertising media on purchase behavior for each category is obtained from another US based bi-annual survey, involving 12000+ respondents on average for each of the 6 bi-annual periods, called Simultaneous Media Usage (SIMM) (Source: Prosper Foundation Insight Center).

In order to link purchase intention data (from BIGResearch CIA data) to media influence data (from BIGResearch SIMM data), we deal with two problems. First, the two surveys are fielded with different frequencies, so we must consider linking SIMM’s bi-annual media use data to CIA’s monthly product purchase data. Second, the two surveys have anonymous respondents, so we should find a way to associate media influence information from SIMM respondents with the category purchase information from CIA respondents.

We adopt two novel approaches to deal with these issues, thereby contributing uniquely to marketing research by suggesting methods to encounter ‘data-fusion’ challenges while using survey data. First, we merge the individual level observations from the CIA database with the ZIP-Code level observations from the SIMM data based on unique socio-demographic profiles from each database. Second, we combined each bi-annual SIMM file with each of the monthly CIA files for the subsequent six months using ZIP-Code to merge the observations for the respondents across the 2 surveys. It is expected that consumers with similar demographic and financial profiles are going to be influenced by similar media sources when making purchases within a category and that the economic fluctuation-induced changes in the media influence patterns are also likely to be consistent. The rationale for combining a SIMM file with the subsequent six CIA files is in line with research in advertising that considers the lagged carryover effects after exposure (Leone, 1995; Winer, 1980). Based on this research domain, we presume that the effects of advertising carry over for at least 6 months.

Model Outline

The dependent measure for consumer purchase behavior in all the categories is spending intention where the responses are an ordinal variable with 3 levels – Less, Same and More. Since our objective is to investigate the influence of advertising media sources on behavior, synergies across alternative media sources and how these effects change over economic cycles, spending intention accurately captures the lagged influence of advertising on behavioral decisions. In our survey dataset, while purchase intention was measured on the same scale as used in our analysis (3 levels) 1 , media influence for each category was captured with respondents allowed ‘free-selection’ of multiple media sources from more than 20 options 2 .

Given that the dependent variable has levels that have natural ordering but the distances between adjacent levels are unknown, we choose to use the Ordered Probit Model (Aitchison & Silvey, 1957) to measure the influence of alternative media sources on purchases (while controlling for economic indicators, demographic profiles and consumers’ perceptions of macroeconomic financial situation). This is because coefficients from this model can provide a comparison between levels by providing a measure of the increase in log-odds for a consumer of being in a higher level of purchase intention relative to a lower level. For clarity, let us consider the following example. In the clothing category, for a consumer influenced by TV and promotions, the probability of spending more relative to same or lower spending changes by a certain r percentage, as the influence of these media changes, either individually or in combination, when the economy evolves from stability to recessions, while we control demographic and financial perceptions of consumers.

Following the model definition above, let us assume

Variable Description

Now we will list the explanatory variables we have included in the specification of the Ordered Probit Model: • Individual Media Types • Interaction of media • Time dummy variables • Interactions of media types with time dummy variables • Financial status and expectations of consumers • Demographic markers 1. Gender: Female (male as baseline). 2. Marital status: Married or with partner (unmarried, divorced, separated or widowed as baseline). 3. Education Level: College graduation and university post-graduation (school matriculation as baseline).

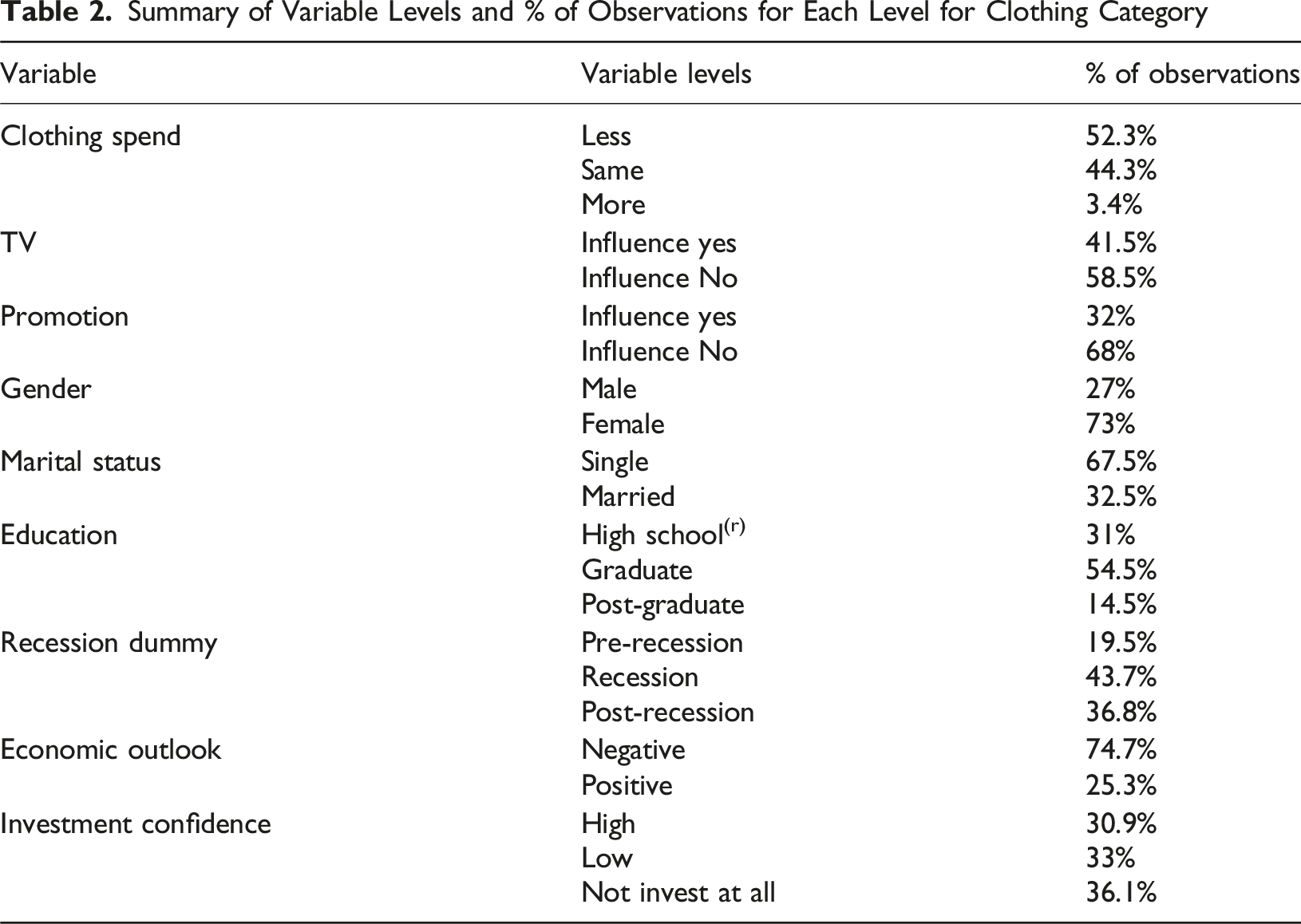

Summary of Variable Levels and % of Observations for Each Level for Clothing Category

Results & Discussion

First, we will provide a quick overview of the sample characteristics for the clothing category. We have a total of 154122 observations for the consumers who reported their clothing purchase intention for the next 90 days. As seen from Table 2, about 52.3% of the consumers want to spend less, followed by 44.3% who want to spend same and only about 3.4% of the consumers want to spend more in the future. The top two media for the clothing category are TV (41.5% respondents for TV ads and banner ads on network and cable TV) and promotion (32% respondents for instore advertising, flyers or coupons). About 20.66% of the respondents are influenced by both TV and promotion.

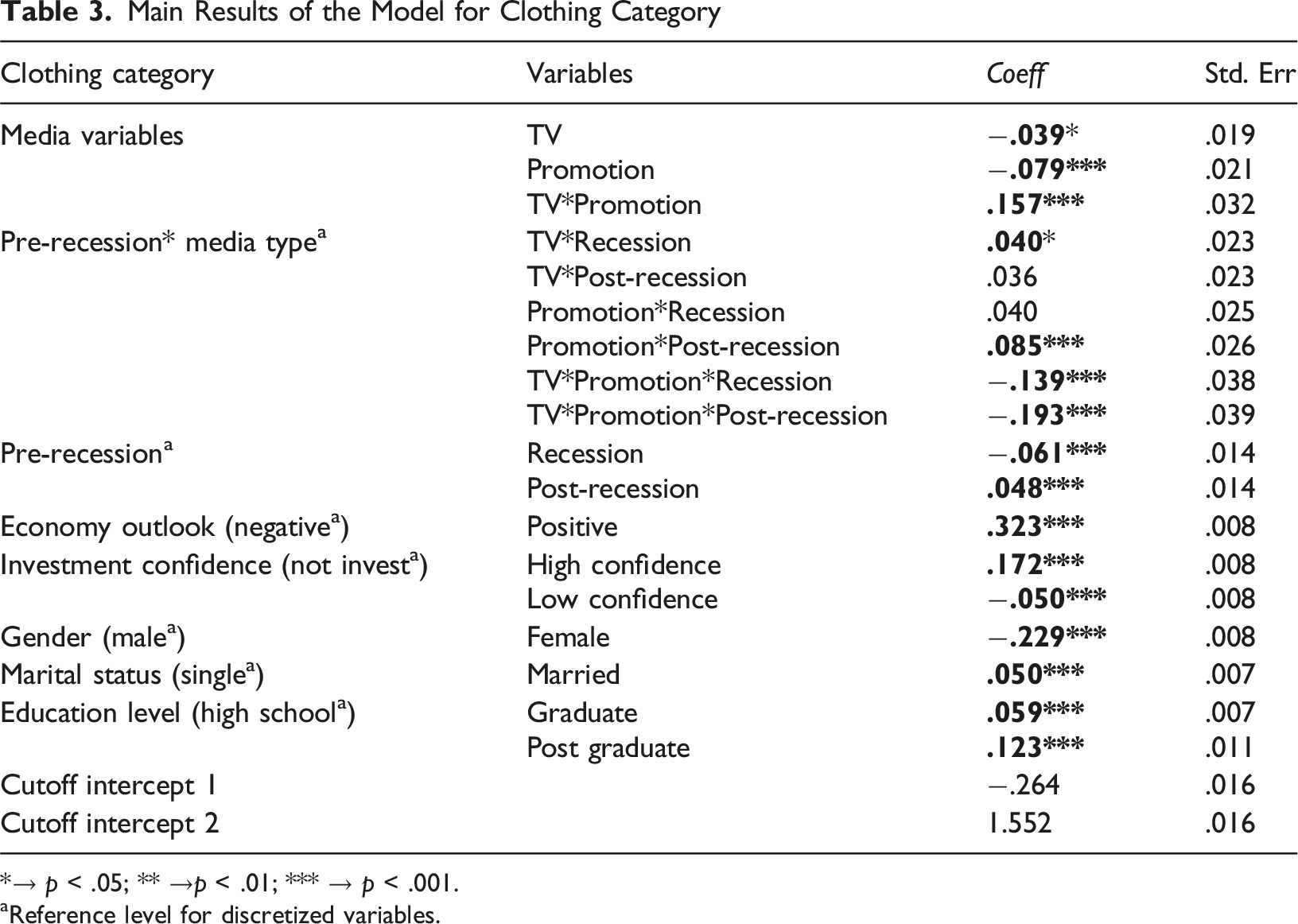

Main Results of the Model for Clothing Category

*→ p < .05; ** →p < .01; *** → p < .001.

aReference level for discretized variables.

When the economy moves from stability to experiencing fluctuations, consumers not only adjust their consumption, but also change their media consumption patterns. Marketers may also adapt their media strategies by reallocating their budget in other media or adding new media. In order to consider this change in the behavior of marketers and its effects on consumer behavior, in the model we include the interaction effects of TV and Promotion media, with the recession indicator variable.

Relative to the pre-recession period influence, consumers who use a single media viz. TV, show positive spending intention (.040, p < .1) during recession, while the ones who are influenced only by promotion also show positive spending intention during post-recession (.085, p < .01). However, for the group that consumes both media, we see significant negative purchase intention (−.139, p < .01). This suggests that during the recession, consumers prefer to use TV or promotions and not both together, driven by their low-level construal and prevention-focused mindset, with focus on feasibility.

Impact of Economic Factor Controls and Socio-Demographic Controls

During the recession, there is a decrease in the purchase intention (−.061, p < 0.1). However, when the economy goes into recovery in the post-recession period, there is an increase in the purchase intentions (.048, p < .01). Finally, consumers with positive economic outlook tend to spend more than the consumers with negative outlook (.32, p < .01). Consumers with high investment confidence tend to spend more (.172, p < .01) than people who either don’t invest or have low confidence.

Females tend to spend less on clothing than men (−.229, p < .01). We also find that married partners tend to spend more than the single consumers (.05, p < .01). As the education level improves (graduates (.059, p < 0.01) to postgraduates (.123, p < 0.01)), intention to purchase also moves from less to more.

Multi-Category Analysis

We extend our analysis to two more categories: electronics & groceries to understand the similarities and differences in the media consumption between a moderate involvement category (clothing) and a high involvement category (electronics) and differences between a moderate involvement and low involvement category (groceries).

From previous research on consumer involvement in product purchases, we know that consumer decision making processes tend to differ. For purchases with long term consequences of choices such as electronics, consumers tend to be more involved, risk averse and are willing to process more information (Frank, 1985). On the other hand, for purchases with limited long term consequences such as groceries, consumers are likely to process less information, are less involved and willing to make impulsive purchases (Buzzell et al., 1975). Moreover, we also know that consumers react differently to recessions for different product categories as well (Deleersnyder et al., 2004).

Additionally, consumers may be active or passive and limit or extend their processing of advertising messages depending on how involved they are in their category purchase. For groceries, the time consumers devote contemplating is negligible and they are more likely to be impulse purchases, driven by the attractive messaging through advertisements. For electronics, consumers are more likely to be influenced by information-based media, which can be useful for research and visualization.

For the categories we consider, we can see differences in terms of involvement and purchase frequency from Figure 2. For their electronics purchases, consumers are more involved than groceries, while in terms of purchase frequency, groceries are the highest. Clothing lies somewhere between electronics and groceries, moderate in terms of involvement and in purchase frequency. So, we expect the results from electronics and groceries qualitatively similar to clothing, but with differences in the nature of the influential media. Perceived differences in the categories in terms of involvement and purchase frequency

We find that the top two media for the categories are different. They vary from more informational for electronics (WOM, that refers to exchange of product-related information (53%) & product articles, offline or online (44%)) to more promotional for groceries (in-store discount coupons (70%) & non-price advertising inserts offline or in-store (40%)). The average media count for the electronics category is 5.18 while followed by clothing (4.26) and groceries (4.29), implying the higher degree of involvement that electronics purchases require.

Results for Electronics & Groceries

We have a total of 192,342 observations for the consumers who reported their electronics spending intention for the next 90 days. About 51.6% of the consumers want to spend less followed by 40.6% who want to spend same and about 7.8% of the consumers want to spend more in the future. For the groceries category we have 216,426 observations for the consumers who reported their spending intention for the next 90 days. About 19.4% of the consumers want to spend less in the future followed by 71.4% of consumers who want to spend same and about 9.2% of the consumers who want to spend more in the future.

Estimation Findings

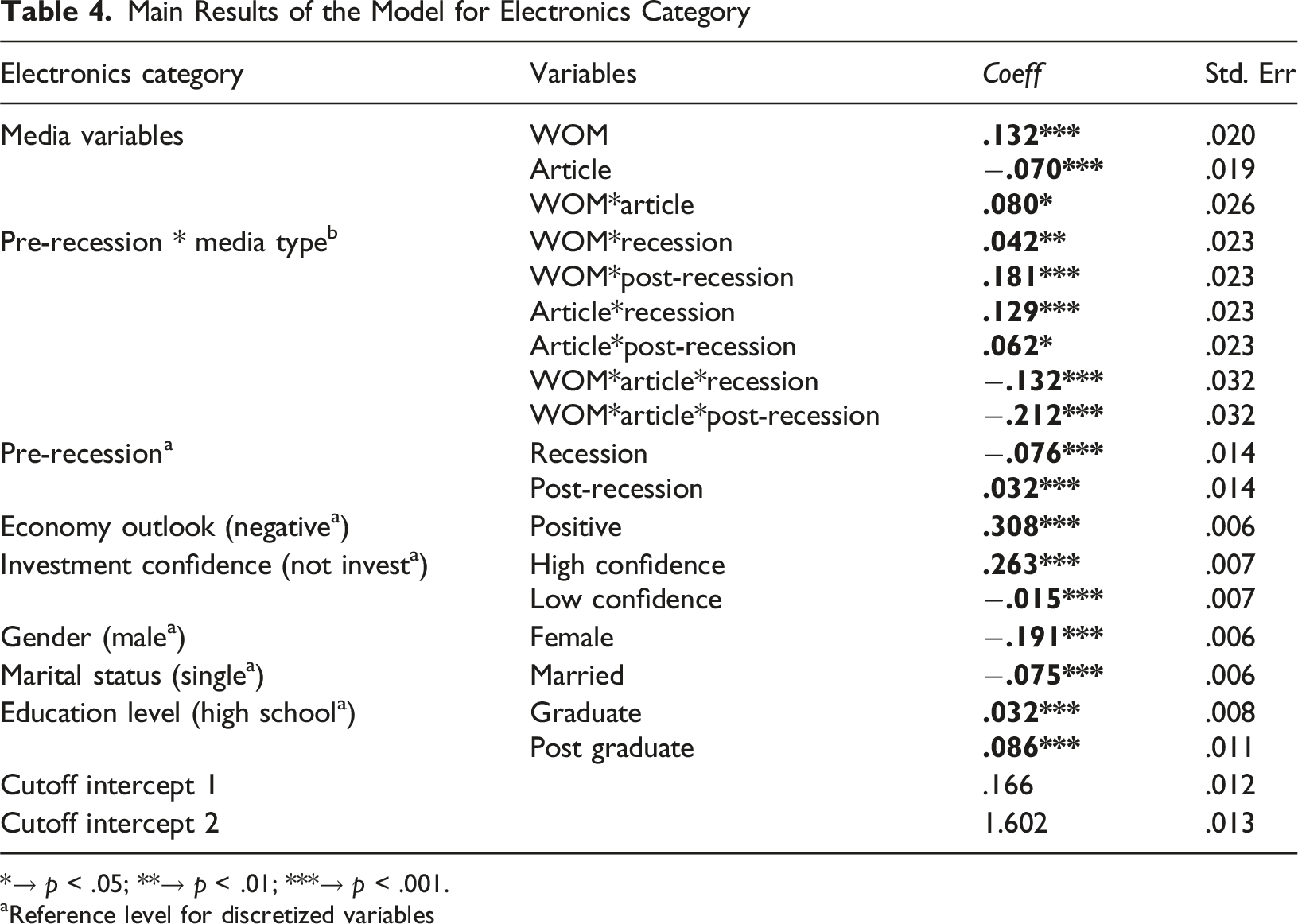

Main Results of the Model for Electronics Category

*→ p < .05; **→ p < .01; ***→ p < .001.

aReference level for discretized variables

Synergy effect of WOM and Article is positive at (.08, p < .01). This synergy result is similar to the result from the clothing category, even though electronics as compared to clothing is a more involved category and surely less frequently purchased.

For interaction results of each media with the recession dummy variable, we see that results are again similar to the clothing category. WOM continues to be an influential media during the recession period (.042, p < .1) and post-recession period (.181, p < .01) as compared to the pre-recession period. Similarly, articles become influential in both the during-recession and post-recession periods. However, when both of them are used together we see significant negative synergy effects (−.212, p < 0.01). Like clothing, for electronics, during the recession consumers are more contemplative about their purchases, focus on feasibility of purchase and would prefer continuing with the most media that provides most effective information, in line with their low-level construal.

We see that during the recession period there is a significant decrease in electronics spending as compared to the pre-recession period (−.076, p < .01), while during the post-recession period we see that improvement in the economy brings back positive spending in the electronics category (.032, p < .01). Consumers who have positive outlook and high confidence in investment tend to spend more than the ones with negative outlook and low confidence in economy. Men tend to spend more than women in electronics. Single consumers tend to spend more than married consumers (−.075, p < .01). As education level increases, spending pattern moves from lower to higher category.

These results help us generalize the results of the clothing category to a high involvement, less frequently purchased goods. In both categories we find that media synergy is positive during economic stability for the top influential media. However, during recessions it is advisable to focus on the media that drives the feasibility of purchase, as multiple media don’t provide any positive synergy due to the concrete mindset of consumers.

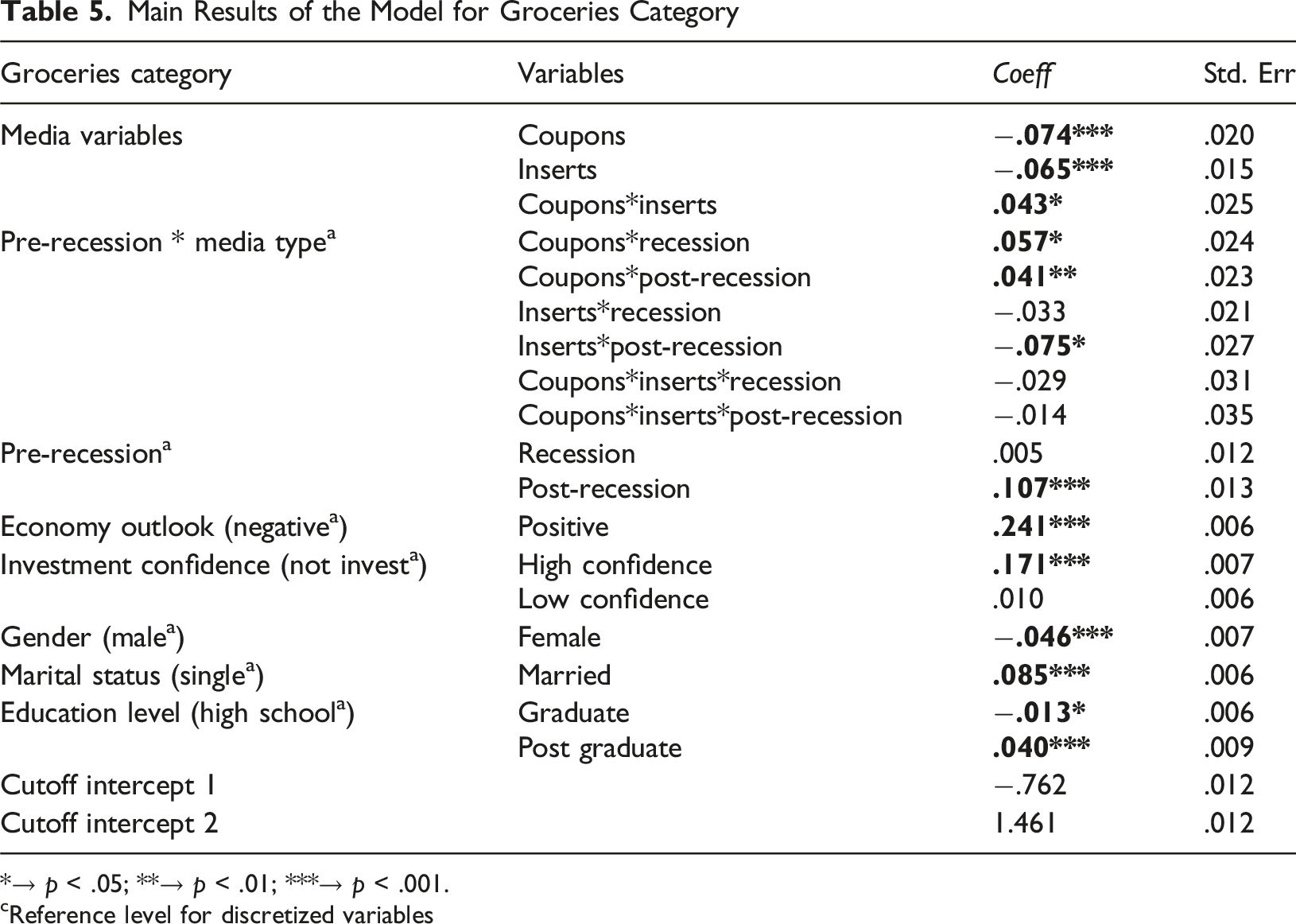

Main Results of the Model for Groceries Category

*→ p < .05; **→ p < .01; ***→ p < .001.

cReference level for discretized variables

We find the main effects of two media, coupons (−.074, p < .01) and inserts (−.065, p < .01) both negative, but the synergy effects to be positive (.043, p < .05), similar to the results of the clothing category.

When we check variations of the influence of individual media with economic fluctuations, we see comparable but slightly different results relative to the other categories. Coupons are the main influencers of purchase during recession (.057, p < .05) and post-recession (.041, p < .1). The advertising inserts don’t have any influence on purchases during recession and post-recession. As for the media synergy variations with the economic cycle, we see that the effects are negative but not significant. So, for groceries, even though we do not see negative synergy between the two influential media, we still observe a null effect, as promotional media that facilitates the low-level construal of consumers, determines their purchases.

Although groceries spending during recession marginally goes down, the effect is not significant. Secondly, we see a sharp rise in spending on groceries during the post-recession period when the economy comes back to normal state. Consumers with high confidence in the economy continue to spend more on groceries. However, we see a significant difference for the high investment confidence consumer as compared to the consumers who don’t invest at all, but there is no significant difference between the consumers with low investment confidence and those who don’t invest at all. For groceries, married consumers tend to spend more than single consumers. Graduates also spend less on groceries as compared to people with lower education.

Managerial Implication, Limitations and Future Research Directions

Managerial Implications

This study explores the impact of individual media usage vs multiple media usage on consumer purchase intentions and how this changes from non-recessionary periods to recessionary times, thereby providing recommendations for media selection under economic fluctuations. We provide a consumer-oriented perspective on media synergy which is different from the marketer’s perspective on media synergy. Our study provides guidance on how managers should adapt their strategies based on consumer responses during economic cycles.

Recessions provide an important challenge for marketers since they need to make critical advertising decisions about whether to change advertising spending (increase or decrease) during economic downturns relative to stable economic conditions. Moreover, they have to make decisions regarding which advertising media to invest and whether to adopt an individual media strategy or use the multimedia option. Though our application context is the 2008 recession in the US, its application can be replicated for the economic fluctuations that countries across the globe experienced after the Coronavirus pandemic of 2019 or any future economic crisis. Also, across the 3 categories, the most influential media sources are conventional (i.e. TV and promotions for clothing, WOM and articles for electronics and coupons and inserts for groceries), which has definitely evolved over the last decade. Importantly, given that our approach focuses on identifying the influential media for each category, it is relatively simple to rerun the analysis for contemporary media sources (i.e. social media, mobile, influencers, VR/AR media etc.) for a broader set of categories.

In the 2008 recession context, based on evidence from the estimation results of the clothing category, we can observe that during stable economic conditions, there is positive evidence of synergy between promotion based and information based (TV) media, which should prompt marketers to use both media sources in their advertising campaigns. However, during recessionary times, marketers need to tweak their media strategy and opt for an individual media, as the synergy is negative. It is advisable that the marketer either opts for a promotional media or TV, as consumers in a low-level concrete mindset focus on a medium that retains their prevention-focus.

We also examine differences in the media consumption patterns for a high involvement, less frequently purchased category electronics and a low involvement, highly frequently purchased category groceries. For electronics, information and review-based media channels such as WOM and articles dominate, while for groceries it’s the promotion-based media such as price discount coupons and non-price advertising inserts that are the most influential media. Following CLT, for electronics we find that WOM and product articles have positive synergy during stability but during recessions it is advisable to focus on either of them and not both, as the synergy is negative, once again exhibiting the consumers concrete mindset and focus on feasibility of purchases. Similarly, for groceries, the synergy between coupons and inserts is positive in general while non-significant during recessions, pointing towards a null effect and consumers’ willingness to consider the promotional media which assures feasibility of groceries purchases. Combining price discounts with non-price inserts works during stable economic times, but adapting the strategy to only focus on discount coupons during recession is recommended. These results help us to generalize our findings in the high and low involvement categories, with expected differences in the role of the most influential media in each case.

Unlike previous studies, we have provided a consumer’s side view on media influence and synergy. We have also compared the impact of media across various stages of the economic cycle to identify the strategic media choices and the need for any adjustments, which facilitates better budget allocation across individual media or multiple media simultaneously. Our second contribution relates to the study of the differences between influences of individual media usage and multiple media usage with respect to the changing environmental conditions in the macro-economy and its effects on purchase intentions. This is different from the majority of the studies that only focus on aggregate impact of advertising on organizational level parameters or do not consider the economic scenario when considering individual media sources. Third, our methodology is replicable across other scenarios of macroeconomic fluctuations, and the analyses can be rerun for multiple categories with evolving media sources, that are more influential in consumer purchase decisions in recent times. Finally, methodologically we provide a solution to resolve two pressing challenges in dealing with survey data in market research, namely merging multiple surveys with each having anonymous respondents and with differing frequencies of collected observations. To address the first one, we used profile-based geographic matching and used the lagged effect of advertising as a rationale to combine monthly purchase intention data with bi-annual media influence data.

Limitations

One of the limitations of the paper is the unavailability of usual advertising media usage data and we had to rely on consumers’ self-reported media influence and purchase intention data. Further, due to the lower frequency of the SIMM data (bi-annual) we have to assume that the effect of exposure to advertising has a carryover effect for up to 6 months when merging this data with the monthly CIA data. Respondent anonymity also required us to merge datasets using geographic profiles. Also, we have to take the time of answering the survey question as a proxy for exposure to advertising.

One may further question our choice of periods for the pre, during and post-recession classification based on the most recent recession of 2008, as well. Moreover, there is a significant shift in the sources of media available (traditional, online and new-age technology-rich media) and the way media is consumed today. Our contribution does not lie in finding which media were more effective during the recession under consideration, but providing a methodology supported by a framework to assess each advertising medium in a scenario of multiple media usage and compare that with individual media usage, across different product categories for any period of economic fluctuations.

Additionally, we have not provided any analysis on the content of advertisements, which of course has a great impact on the consumer purchase behaviors. We are only talking about advertising media as not what goes into the making of an advertisement.

Future Research Directions

For future research, we would like to understand the reasons behind the media usage patterns we observe in this study. By gathering data about individual media source ratings and usage patterns we can substantiate our findings and provide a deeper understanding of consumers’ behavioral processes. A second research direction is to explore differences in consumers by profiling them according to the cumulative effects of the advertising media that they are most influenced by. Further on a related domain, it will be interesting to find out whether consumer segments are themselves evolving during recessions compared to the stable or recovery periods. Here the approach will actually involve understanding the changes in consumer mix at the brand level.

Footnotes

Acknowledgments

The author would like to acknowledge the inputs from Dr. Abhishek Nayak (Vin University) in earlier versions of the paper and feedback of faculty members in the Department of Marketing at the University of Auckland Business School.

Ethical Considerations

Since the research uses proprietary third-party survey data from Prosper Foundation Insight Center, no approvals are required.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is not funded by any financial support, but supported by a data grant from the Prosper Foundation Insight Center.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be made available if required, with permission from the data provider.