Abstract

This paper econometrically analyzed 5868 Internet insurance-related literature published between 2004 and 2024, examining annual publication trends, countries studied, and research institutions. It found that the number of Internet insurance literature increased by 37% in 2018, reaching its highest level in nearly a decade in 2022, highlighting the booming global Internet insurance sector. Research organizations in various countries have invested their efforts to provide strong support for the healthy development of the sector. Additionally, a systematic review of 30 selected papers was conducted, comprehensively defining Internet insurance and its related concepts, and highlighting its virtual, interactive, convenient, and economic advantages over traditional offline insurance. The development of the Internet has promoted the deep integration of Internet insurance and traditional insurance, accelerated the provision of universal insurance services, and promoted fair competition in the insurance market. However, the paper also revealed the product and operational risks as well as moral hazard challenges faced by Internet insurance. To promote sustainable development, the study proposed optimizing products, strengthening credit assessment mechanisms, and establishing risk early warning mechanisms. This paper is the first to explore the impact and sustainability of Internet insurance using econometric analyses and systematic review methodology, aiming to inspire further in-depth research to promote the sustainable development of Internet insurance and provide greater value and protection for consumers, the industry, and society.

Introduction

Since the end of the 20th century, the rapid development of information technology, especially Internet technology, has had a profound impact on the daily production and living patterns of the public. This technological revolution has not only overturned the way we know and understand the world but is also gradually reshaping the landscape of traditional industries, among which the insurance industry, which has a long history, is also one of them.

Against this background, the perfect combination of Internet technology and insurance business has given birth to the new business model of “Internet insurance.” It is not only an innovation in products and services but also a comprehensive innovation in business processes and business models. Through the Internet platform, insurance companies can reach potential customers in an unprecedented way and provide them with more convenient and personalized insurance services. At the same time, consumers can more easily compare various insurance products and choose the most suitable protection plan for themselves.

In addition, the introduction of Internet technology has greatly enhanced the operational efficiency and service quality of the insurance industry. Using advanced technologies such as big data analysis and artificial intelligence, insurance companies can more accurately assess risks and develop more reasonable premium strategies. At the same time, the automated claims process has also significantly shortened the waiting time of customers, further enhancing customer satisfaction. 1

However, the development of Internet insurance also faces many challenges, such as data security, privacy protection, and risk prevention and control of Internet technology. Internet insurance, as a product of the combination of information technology and insurance business, represents the future development direction of the insurance industry. It will not only change our insurance consumption habits but also promote the whole insurance industry to achieve transformation and upgrading towards a better future.

This paper systematically reviews the relevant literature in the field of Internet insurance and deeply analyses its connotation, development history, status, and sustainability. By summarizing and concluding the existing studies, this paper aims to reveal the research hotspots, methods, and development directions in the field of Internet insurance, and to provide a comprehensive and in-depth understanding and reference for the academia and the insurance industry. This has a positive role to play in promoting the further maturity and development of the Internet insurance industry and optimizing the quality of insurance services, which cannot be ignored.

Methodology

To write this systematic review paper, we have carefully developed a rigorous set of criteria, parameters, and research quality assessments from which we have developed a review protocol that draws heavily. These criteria were the cornerstone of our literature review and ensured that the research process was rigorous and scientifically sound.

First, in the literature search phase, we focused on the core keywords of Internet insurance, Online insurance, Web insurance, Cyber insurance, and Digital insurance. Extensive and in-depth literature collection was conducted through Google Scholar, Researchgate.com, and Citexs, which are authoritative academic platforms and comprehensive databases of literature. We rigorously screened academic resources closely related to the topic to ensure the accuracy and reliability of the research.

Second, to ensure the quality and authority of the literature, we selected only journal articles and published conference papers as the research database. Journal papers and published conference papers usually contain the latest research results and cutting-edge academic ideas. These pieces of literature not only reflect the current research hotspots and development trends in the field but also provide us with rich data and case support. By studying this literature, we can gain a more comprehensive understanding of the current state of the research field and explore the research issues in greater depth, thus presenting more insightful views and conclusions.

Third, to further deepen our research horizon, we conducted an extensive collection of articles related to Internet insurance in the last decade. The period of this literature research began in January 2014 and continues until January 2024, covering all the latest research findings in the field of Internet insurance during the last decade. To ensure the international and generic nature of the research, special attention was paid to those articles written in English. As a globally accepted academic language, English is more representative and influential in terms of research findings. Therefore, we have collected 5868 articles in English. These articles cover a variety of research topics, methods, and findings related to Internet insurance. We did a bibliometric analysis of these articles and analyzed in-depth the annual trend of Internet insurance publications, countries studied, and research institutions. They provide a rich source of material and reference for our study.

Finally, after carefully reading and evaluating the abstracts of the showcased articles, we selected 30 representative papers with high citation scores and impact factors as the basis of this Internet insurance literature review. These papers are not only closely related to our research topic but also have high academic standards and research value. This selection ensures the depth and breadth of this study. Through these articles, we can gain an in-depth understanding of the research dynamics and sustainability trends in the field of Internet insurance over the past decade, providing a solid theoretical foundation for our study.

Findings

The research on the literature review of Internet insurance has formed a series of achievements focusing on the Bibliometric Analysis of Internet Insurance, Internet Insurance Connotation, and Sustainability development of Internet insurance.

Bibliometric analysis of internet insurance

Annual publication trends in the internet insurance literature

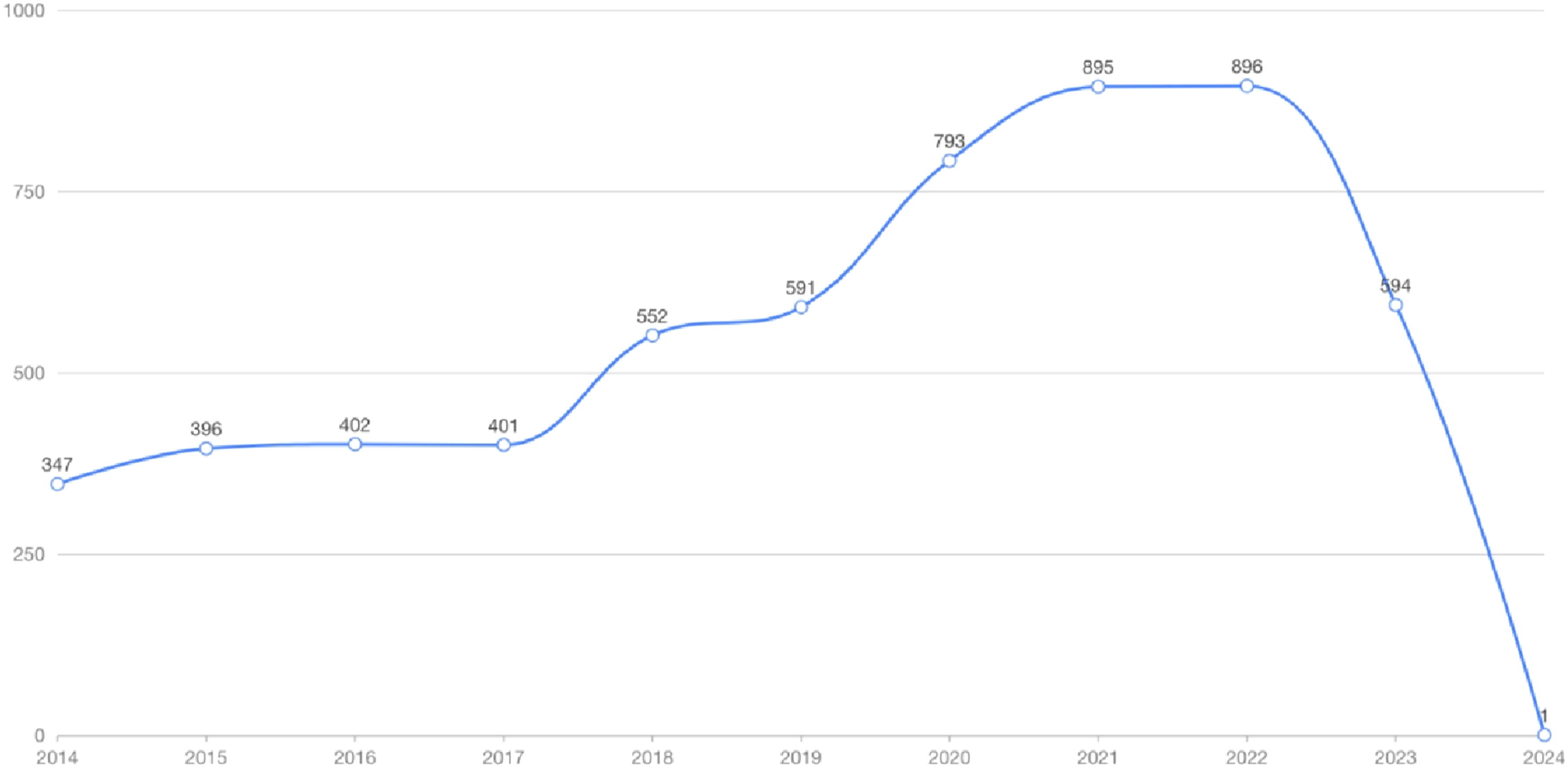

Due to the rapid advancement of information technology, Internet insurance, a key branch in the field of financial technology, is gradually revealing its unique attractiveness and great potential for development. After a comprehensive search of academic literature on Internet insurance, Online insurance, Web insurance, Cyber insurance, and Digital insurance between January 2014 and February 2024, we found that the total number of research literature in this field is as high as 5868 articles, with an annual average of 534 publications. This data not only highlights the heat of Internet insurance research but also predicts the continuous growth of its research field.

As shown in Figure 1, the number of publications in the field of Internet insurance research climbed to a peak in 2022, totaling 896 articles. The prosperity in this period is mainly attributed to the extensive application of cutting-edge technologies such as big data, cloud computing, and artificial intelligence, which provide solid technical support for the research and practice of Internet insurance. Meanwhile, with the acceleration of the global digitalization process, Internet insurance is gradually becoming an emerging growth point in the insurance industry, attracting the attention and participation of many scholars and practitioners. Among these years, the growth rate in 2018 was particularly prominent, reaching 37.66%. This growth rate not only highlights the rapid development of Internet insurance research but also foretells the great potential of its research field in the future. During this period, the focus of Internet insurance research gradually shifted from conceptual exploration to practical application, and many innovative research results emerged, laying a solid foundation for the industry’s continued development. Annual trends in publications in Internet insurance literature from 2014 to 2024 Source: Bibliometric analysis was performed using the Citexs Website (https://www.citexs.com/).

Country analyses of research in the internet insurance literature

As shown in Figure 2, in the past decade, the United States has been in the leading position in the global Internet insurance research field, with a total of 1340 articles, accounting for 22.84%. This data fully proves the deep research strength and extensive influence of the United States in the field of Internet insurance. Its strong scientific and technological innovation capacity, perfect financial system, and broad market demand have jointly promoted the booming development of the United States in this field; closely followed by India, with 491 articles, accounting for 8.37%. In recent years, India’s meteoric rise in the field of financial technology has been attributed to its large population base, abundant labor resources, and strong government support for technological innovation. In terms of Internet insurance, India has gradually emerged as an important force in global Internet insurance research because of its unique market advantages and constantly innovative technological strength. China, on the other hand, ranked third with 411 articles published, accounting for 7% of the total. As one of the largest insurance markets in the world, China has great potential for development in the field of Internet insurance. In recent years, with the continuous advancement of technology and the continuous promotion of policies, China’s Internet insurance industry has developed rapidly and become an important player in global Internet insurance research. In addition to the three countries mentioned above, other countries, though with relatively fewer publications, are also actively exploring and promoting research and development in the field of Internet insurance. These countries include developed countries such as the United Kingdom, Germany, and France in Europe, as well as South Korea and Singapore in Asia. The participation of these countries and regions further enriches the content and perspective of global Internet insurance research. Country analysis of internet insurance literature studies from 2014 to 2024. Source: Bibliometric analysis was performed using the Citexs Website (https://www.citexs.com/).

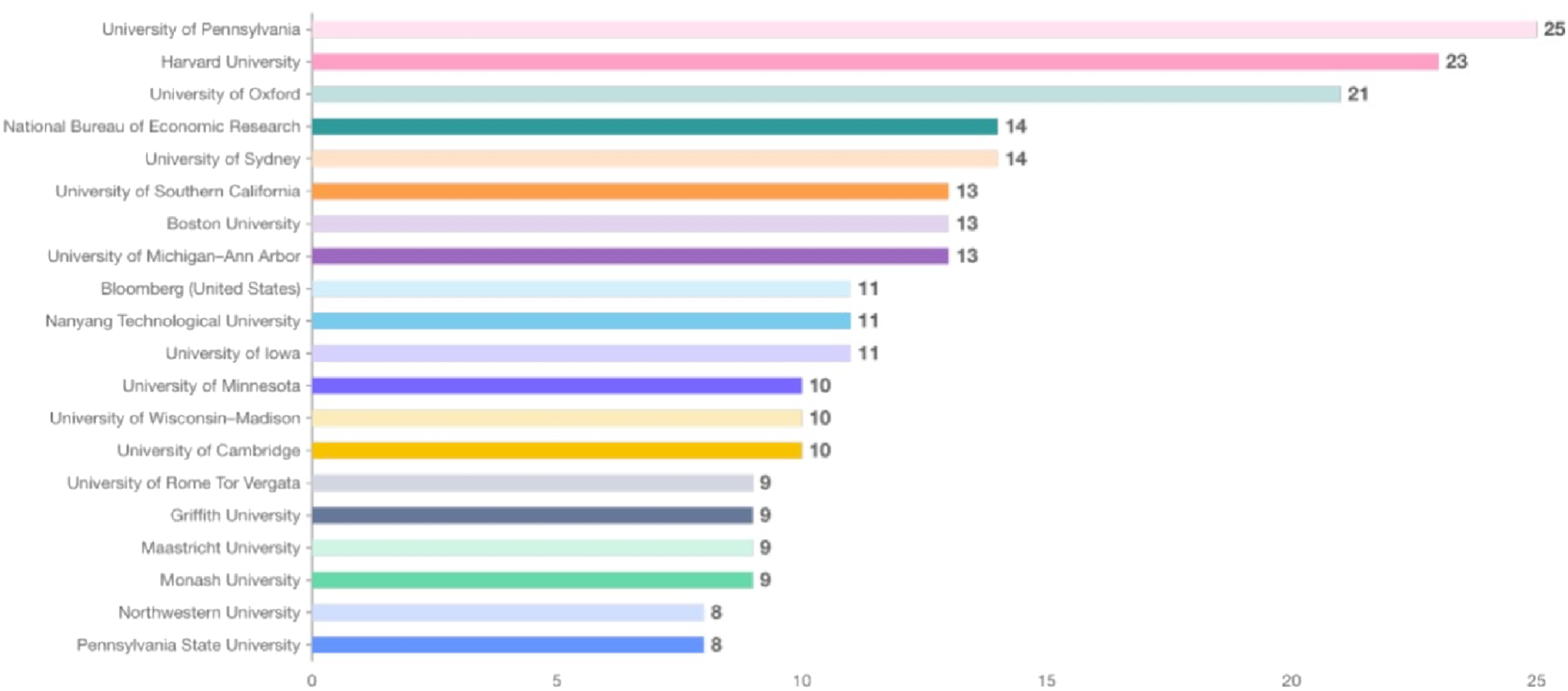

Analysis of internet insurance research organizations

In the decade 2014–2024, global research on Internet insurance has shown a boom. This emerging field has attracted research organizations in many countries and regions to invest in research. By statistically analyzing the results of related research worldwide, we have come up with a list of the top 20 national research institutions in terms of the number of articles published during this period. As shown in Figure 3, the figure illustrates the distribution of academic strength in this field on a global scale, reflecting the diversity and potential for collaboration in academic research worldwide. The research on Internet insurance globally presents a trend of diversification and internationalization. Research institutions in different organizations conduct in-depth studies in their respective areas of expertise, collectively promoting the rapid development of this emerging field of Internet insurance. Analysis of research organizations in internet insurance literature from 2014 to 2024. Source: Bibliometric analysis was performed using the Citexs Website (https://www.citexs.com/).

The University of Pennsylvania and Harvard University occupy the top two positions in terms of publications in the field of Internet insurance research worldwide. The University of Pennsylvania has published 25 research papers, followed by Harvard University with 23. The deep research strength and extensive influence of these two top institutions in the field of Internet insurance can be seen; followed by the University of Oxford (UK), which published 21 research papers, ranking third. The University of Oxford has a long history and excellent research tradition in the fields of insurance, risk management, and financial technology, and its research in the field of Internet insurance is also outstanding; in addition to these three top institutions, the national research institutes that made it into the top 20 also include well-known universities and research institutes from the United States, the United Kingdom, Germany, Canada, Australia, and many other countries. The research of these institutions in the field of Internet insurance covers product innovation, risk management, laws and regulations, consumer behavior, and other aspects, providing strong theoretical support and practical guidance for the healthy development of the Internet insurance industry.

In summary, the global development in the field of Internet insurance research has shown a booming trend, and research organizations in various countries have invested their research efforts to provide strong support for the healthy development of the industry.

Internet insurance connotation

Internet insurance concept

Internet insurance, also known as cyber insurance, online insurance, or digital insurance. There is no uniform definition of the concept of Internet insurance in the academic world. Numerous scholars have discussed the concept of Internet insurance in depth. They argued that the mediating role of e-commerce not only enables insurance companies to reach a wide range of potential consumers more directly, thus reducing operating costs and improving service efficiency but also provides consumers with the convenience of comparing and choosing the products of different insurance companies through online platforms. Eastman et al. in 2002 made a clear division between the narrow and the broad concepts of Internet insurance. In the narrow sense, Internet insurance is defined as the use of Internet technology by insurance companies or Internet insurance intermediaries for the sale and service of insurance products, the networking of the insurance process, and ensuring that the insurance costs are transferred directly to the insurance company’s account through the bank. In the broader sense, the concept of Internet insurance is further expanded, which not only advocates the deep integration with consumers in the business process but also stresses that companies should use Internet technology internally to manage their organizational activities and to cooperate and communicate extensively with other companies.

Internet insurance usually refers to insurance products and services that are sold and managed through Internet platforms. It utilizes Internet technology, including online channels, mobile applications, etc., to provide consumers with a convenient insurance purchasing, claims, and management experience. 2 Through Internet insurance, customers can conveniently purchase insurance products anytime, anywhere, without the need to visit a physical shop or communicate face-to-face with an agent, while also being able to enjoy a more personalized insurance service. 3

Zheng et al. specify that Internet insurance is an emerging model that enables a full range of processes such as policy promotion, product transactions, and claims settlement through the Internet. 4 For consumers, the Internet insurance sales service provided by insurance companies is no longer a mere selection process, but an efficient and convenient insurance experience.

The core of this model lies in the establishment of a networked system that enables efficient online communication with customers and allows them to easily carry out operations such as online inquiry, consultation, and purchase, thereby facilitating the electronic transaction of insurance products.

Pan similarly emphasizes the importance of Internet insurance as an innovative insurance sales operation model that covers everything from online advertising, and product recommendation to contract negotiation, product ordering, claim application and policy payment, and other online services in the whole process. 3 This new model not only enhances the efficiency of the insurance business but also brings unprecedented convenience to consumers.

In summary, Internet insurance is not only a major reform and innovation of traditional insurance but also a cutting-edge concept that continues to evolve in line with industry trends, the external environment, and technological advances. It covers an increasingly wide range of areas, from initially making the entire process of traditional insurance business online to today’s personalized and unique product design, each step of which reflects an in-depth understanding and satisfaction of customers’ needs. It not only digitizes and transfers the traditional operational aspects of the consultation, sales, underwriting, and claims handling online but also streamlines operational processes and enhances product innovation through cutting-edge technologies such as big data, the Internet of Things, and blockchain, creating unprecedented new insurance products. These changes have not only led to more standardized and transparent insurance prices and a higher degree of marketization but also brought unprecedented convenience and benefits to customers. 5

Characteristics of internet insurance

In contrast to traditional insurance, Internet insurance has a unique innovative highlight. This innovation is the use of contemporary high-tech to reshape production, operation, and service at a basic level. Through the study and collation of related literature, scholars’ research on the characteristics of Internet insurance mainly focuses on the aspects of virtuality, interactivity, convenience, and economy.

First, virtuality. In Internet insurance, all transaction processes are realized through the Internet platform. Insurance companies use the Internet platform to display their diversified insurance products and services, while policyholders search online to obtain the information they need and use the convenient online payment means to complete the payment of premiums and the signing of the policy. Once the policyholder encounters a risk event, the insurance company will respond quickly and handle the claim through online channels. This transaction model fully reflects the digital nature of Internet insurance and realizes the full virtualization of transaction activities. 6

Second, interactivity. The design of products and services in the traditional insurance industry is often orientated to the business objectives of insurance companies, ignoring the actual needs of consumers. However, under the new model of Internet insurance, consumers are no longer passive recipients, they can communicate directly with insurance companies through efficient online platforms, and jointly construct insurance products and services that meet individual needs. This dynamic communication mechanism between insurance companies and consumers not only encourages insurance companies to innovate and design more diversified and personalized insurance products but also reduces the homogeneity of products to meet the unique needs of different consumers, which in turn enhances their competitiveness and share in the market. At the same time, it also provides insurance companies with the opportunity to provide consumers with timely after-sales service, which enhances consumers’ trust and satisfaction with insurance companies and further strengthens customer loyalty. Under the interaction of the new model of Internet insurance, a good interactive relationship has been built between insurance companies and consumers, forming a mutually beneficial and win-win situation, which strongly promotes the healthy and steady development of the Internet insurance industry.

Third, convenience. The traditional insurance sales model relies heavily on agents visiting door-to-door, limiting consumers’ time choices, and increasing agents' workload. In contrast, Internet insurance offers insurers and consumers more flexible scheduling, allowing insurances and inquiries to be completed online. This shift has improved the convenience of insuring consumers and the operational efficiency of insurers while facilitating the expansion of insurers into international markets. Intelligent Internet insurance business processes shorten customer waiting time, simplify operational processes, enhance user experience, and reshape consumer perceptions and expectations of insurance products.4,7

Fourth, the economy. Technological advances have played an important role in increasing intelligent productivity, and the Internet insurance industry has benefited as a result. Technological advances have lowered the cost of selling Internet insurance, and digital transformation has reduced reliance on offline marketing teams, saving labor costs. In addition, the rise of Internet marketing channels has given consumers more choices and encouraged insurers to develop more affordable products. This trend not only improves consumers’ bargaining power but also pushes the insurance industry towards greater efficiency and transparency. 8

In conclusion, compared with traditional offline insurance, Internet insurance has the characteristics of virtuality, interactivity, convenience, and economy, which enables the Internet insurance market to develop rapidly in a relatively short period, with numerous innovations in products and interaction methods.

Impact of internet insurance

The rapid rise of Internet insurance has had a profound and multi-dimensional significant impact on the traditional insurance industry.

First, it has promoted the deep integration of Internet insurance with traditional insurance. This is of vital significance. The Internet, with its huge information flow, large consumer base, and technological advantages, has demonstrated strong sales potential. If traditional insurance companies can effectively utilize these Internet resources, it will undoubtedly bring them considerable benefits. Nowadays, Internet technology has not only been limited to serving as the background support for traditional insurance businesses but has gradually developed into a brand-new insurance industry, providing a useful supplement to the traditional insurance industry. The two complement each other and mutually reinforce each other, jointly promoting the innovation and development of the insurance industry. 9

Second, it has accelerated the provision of inclusive insurance services. With the networked development of information technology, an online insurance service platform has been constructed, allowing customers to complete comprehensive services such as insurance application, underwriting, policy management, reporting, and claims settlement directly through the Internet platform, effectively breaking through the limitations of time and space. This innovative initiative has greatly solved the problem of insufficient insurance coverage in remote areas, enabling more people to enjoy insurance protection. Meanwhile, the penetration rate of Internet insurance has increased significantly, further promoting the universality of insurance services. The relatively low price of Internet insurance products makes insurance affordable for middle- and low-income groups, realizing truly inclusive insurance services. In addition, Internet insurance products have the characteristics of rapid innovation, short cycle, personalization, etc., which can better meet the diversified protection needs of customers.

Third, it has promoted fair competition in the insurance market. Given the intangible and complex nature of insurance products, insurance companies have traditionally relied on teams of offline insurance agents to recommend and introduce products to customers. However, due to the wide variation in the quality of the agent teams, sales misrepresentation occurs from time to time, which in turn gives rise to a series of problems, including poor customer experience, claims disputes and complaints, and other negative consequences. In contrast, Internet insurance can effectively prevent and efficiently deal with the problem of mis-selling under its unique advantages of high transparency, data-driven nature, super visibility, and traceability of information. This not only helps to improve the overall image of the insurance industry but also promotes the development of the insurance market in a fairer, more standardized, better, and healthier direction.1,4

Sustainability development of internet insurance

To achieve the sustainable development of Internet insurance, it is necessary not only for industry operators to seek a breakthrough in ideological concepts, to re-explore the value of the insurance industry with Internet thinking, and to pay attention to changes in the industry’s intrinsic development dynamics but also for industry regulators to broaden their mindsets, to establish forward-looking regulatory thinking, and to guard against and resolve the new risks of new forms and contents while providing room for error in the development of Internet insurance business. The new form and new content of new risks can be prevented and resolved at the same time.

Embryonic period (late 1990s to early 2000s)

During the period when the Internet was just emerging, some insurance companies began to use Internet channels to sell insurance products. Internet insurance at this stage was mainly based on online sales, where customers could purchase and communicate with insurance products through insurance companies’ websites or emails. However, the Internet insurance market did not achieve large-scale development at this stage, mainly because the Internet was in its infancy and did not form a wide range of popularity; the overall market environment of e-commerce is volatile, and market players do not have enough knowledge of Internet insurance, etc. These factors have hindered the development of Internet insurance to a certain extent. 10

Exploratory period (mid-2000s to early 2010s)

The rise of e-commerce marked the beginning of the exploration period for the Internet insurance market. With the continuous development and popularization of Internet technology, insurance companies began to increase their investment in Internet channels and launched more comprehensive online insurance service platforms. During this period, the Internet insurance industry began to see market segmentation, gradually transforming from pure online sales to a comprehensive service platform that includes online insurance, online claims, online customer service, and other functions. Driven by venture capital, Internet insurance has achieved a great deal of development space. Some Internet insurance companies have begun to adopt innovative sales models, such as direct sales model and partnership model, to actively expand their markets. The government has attached great importance to the development of information technology in the insurance industry and insurance e-commerce. At this stage, the Internet insurance business still has not become the development focus of most insurance companies.

Development period (2010s to present)

After entering the 21st century, with the continuous development and application of new-generation information technologies such as big data, artificial intelligence, blockchain, etc., Internet insurance has experienced explosive growth. Insurance companies have carried out the expansion of the Internet insurance business by using big data to analyze customer behavior, artificial intelligence for intelligent risk assessment, and blockchain technology to safeguard data security, achieving personalized customization of insurance products, risk assessment, and claims processing, and providing customers with smarter and more personalized insurance services. During this period, with the continuous development and maturity of Internet technology, the era of “Internet +” insurance has come. The insurance industry has formed a relatively complete system, including the design and sale of Internet insurance, management and operation, data analysis, and other aspects, thus establishing the basic mode of Internet insurance. Some emerging technology companies have also begun to get involved in the field of Internet insurance, promoting the innovation and development of the Internet insurance industry.11,12

The Internet has had a profound impact on the insurance industry, not only providing a solid technological foundation and extensive platform resources but also promoting the birth and development of Internet insurance as a new business model. Internet insurance, as a major reform and innovation of the traditional insurance model, has been continuously enriched and expanded in terms of its connotation and extension with the evolution of the industry environment, the change of external conditions, and the continuous progress of science and technology.

Limitations of internet insurance development

Internet insurance is facing a series of challenges and problems along with its rapid development.

Moral risks in internet insurance

As Internet insurance has a simple and easy-to-use process and allows for cross-region insurance, this affects the timeliness of underwriting to a certain extent. As a result, it has become more difficult to identify the authenticity of the customer’s insurance information, and loopholes in the review of insurance information may occur, thereby increasing moral hazard. Under such circumstances, policyholders are more likely to breach the principle of utmost good faith. For example, failing to truthfully inform their health status may pose a potential risk in the subsequent claims process. In addition, the virtualized nature of Internet insurance makes it difficult for insurers to accurately judge the eligibility of the policyholder or the “insurance interest” of the insured, which may harm the interests of both parties. 9

The form of Internet insurance has to a certain extent weakened the insurer’s obligation to inform, which may lead to misunderstanding of the “exclusion clauses” by the policyholders. At the same time, insurers may also engage in exaggerated promotions and blur product information to the detriment of policyholders or the insured. Inadequate monitoring of third-party online platforms is a major problem for insurance organizations. Staff may abuse their authority by selling fake policies or making fake claims to gain illegal profits, which undoubtedly increases moral hazard.5,13

Product issues in internet insurance

Awareness and acceptance of Internet insurance products are still lacking. The complexity of the terms and conditions and the jargon covering a wide range of disciplines make it more difficult for consumers to understand, thus inhibiting their willingness to buy. In terms of regulatory enforcement, the current regulation of Internet insurance products is still insufficient. Complaints about Internet insurance have risen significantly in recent years, mainly related to incomplete information in the sales process, bundled sales practices, and insufficient grounds for refusing claims. This reflects that the current regulatory and legal systems are lagging in responding to the new challenges of Internet insurance products, and the protection of consumer rights and interests needs to be strengthened. 3

Operational risks in internet insurance

Internet insurance, as a product of the in-depth integration of the two industries of insurance and the Internet, involves risks that cannot be ignored during its operation. Under the current market environment, the transaction, contract formation, and business management boundaries between different subjects are often blurred, leading to many blind spots in regulation and potential risks. As Internet insurance products involve cross-sector cooperation, including insurance institutions, third-party platforms, financial payment platforms, and other parties, this makes it easy for systemic risks within the financial system to penetrate the insurance industry, which in turn exacerbates the overall risks and may trigger a chain reaction. Internet insurance faces greater fraud risks than traditional insurance. Internet insurance companies and platforms are not infrequently subject to malicious surrender, arbitrage, and insurance fraud. Insurance fraud not only brings huge economic losses to the Internet insurance industry but also harms the interests of bona fide insurance customers and weakens the social function and market trust of insurance products.1,6

Recommendations for the sustainability of internet insurance

Optimization of internet insurance products

We can optimize the product structure, and enrich, and improve the form of Internet insurance products to meet fragmented insurance needs. Traditional insurance products are often large and comprehensive, covering incomplete segmentation needs, but Internet insurance can “fragment” the protection, and should split the complex terms of traditional insurance into independent terms, forming fragmented protection or products, adapting to segmentation scenarios, and meeting personalized needs. Insurance institutions should take advantage of Internet technology to segment the market and innovate universal, customized, and personalized Internet insurance products to promote high-quality development.

Improvement of credit evaluation and information-sharing mechanisms and strengthening of regulation

We can adhere to the principle of market orientation and improve the regulation of Internet insurance so that the market and regulation can play their respective roles. The principle of consumer protection should be highlighted. Protecting consumers’ rights and interests is the eternal responsibility of supervision, especially the prevention of misleading sales. By strengthening the company’s responsibilities, and fulfilling sales obligations and risk tips, consumers are effectively prompted to fulfill their responsibility to protect consumer rights and interests. Insurance regulation should strengthen forward-looking research to achieve a balance between encouraging innovation and preventing risks starting from the similarities and differences between Internet insurance and traditional insurance, and gradually revise and improve the regulatory rules. 12

Construction of risk early warning mechanism to prevent business risks

To effectively identify and respond to risks, a comprehensive risk early warning mechanism should be constructed. By making full use of the Internet and big data technology, potential risky customers are accurately identified, and scientific models are established to assess the probability of fraudulent behaviors such as arbitrage and fraudulent claims by these customers. Once high-risk customers are found, a warning will be issued quickly and corresponding anti-fraud strategies will be formulated to enhance the defense ability of enterprises in the face of risk 8 ; In addition, through the integration of the resources Internet insurance agency platform and the platforms of various types of financial institutions, a “blacklist” of insurance fraud will be established. In addition, by integrating the resources of the platforms of Internet insurance agencies and various financial institutions, a “blacklist” early warning system for insurance fraud can be established, to resist insurance fraud more effectively; finally, at the regulatory level, comprehensive and rigorous laws and regulations should be formulated to plug regulatory loopholes and ensure that business risks can be effectively prevented. This will help to establish a fairer, more transparent, and stable insurance market environment and protect the legitimate rights and interests of consumers. Internet insurance will continue to face challenges from other sources besides insurance regulations. International data flows may be restricted by data localization laws as well as privacy and data protection regulations that restrict the use of data. Therefore, the Internet insurance value chain must be able to be finished electronically, without ever returning to paper documents or wet-ink signatures, for insurance business models to become digital.

Conclusion

This paper provides an econometric analysis of the Internet insurance literature in the past 10 years and finds that the countries that study Internet insurance globally show the characteristics of diversification and broadening. They jointly promote innovation and development in the field of Internet insurance and provide strong support for the healthy development of the industry. In addition, this paper provides an in-depth and systematic review of the relevant literature in the field of Internet insurance. Through 30 selected papers in the past decade, we comprehensively analyze the connotation, development history, status, and sustainability of Internet insurance. The rapid development of Internet insurance has injected new vitality into the insurance industry. The countries that study Internet insurance through the interconnected world present diversified and extensive characteristics.

This study confirms the rise of Internet insurance is not only a major reform and innovation of traditional insurance but also a cutting-edge concept that continues to evolve in line with industry trends, the external environment, and technological advances. Internet insurance covers an increasingly wide range of areas, from the full process of traditional insurance business online to personalized and unique product design, each step of which reflects the in-depth understanding and satisfaction of customer needs. Through cutting-edge technologies such as big data, the Internet of Things, and blockchain, Internet insurance not only digitizes traditional operational aspects but is also able to streamline operational processes, enhance product innovation, and create unprecedented new insurance products. These changes have led to more standardized and transparent insurance prices and a higher degree of marketization, as well as unprecedented convenience and affordability for customers.

The result of this study emphasizes the sustainable development of Internet insurance requires the joint efforts of industry operators and regulators. Industry operators should seek a breakthrough in ideological concepts, re-explore the value of the insurance industry with Internet thinking, and pay attention to the changes in the industry’s intrinsic development dynamics; while regulators need to broaden their thinking space, establish forward-looking regulatory ideas, provide fault-tolerant space for the development of Internet insurance business, and at the same time prepare for and resolve the new risks of the new forms and new contents. In the face of challenges such as moral hazard, product problems, and operational risks, the sustainable development of Internet insurance can be promoted by optimizing products, improving the credit evaluation mechanism, and building a risk warning mechanism. The healthy and sustainable development of Internet insurance will bring more value and protection to consumers, the industry, and society.

Although this study provides valuable insights into the sustainable development of Internet insurance, there are limitations. First, the study data is limited and may not be fully representative of the global Internet insurance market. Therefore, future studies should expand the sample to include data from more countries and regions to enhance generalizability. Second, this study mainly focuses on the macro level of industry development, and micro factors such as consumer behavior are less explored. In the future, more attention should be paid to consumer experience, trust and demand changes, and individual driving factors should be analyzed in depth. Third, with the rapid development of technology, the application of technologies such as artificial intelligence, big data, and blockchain in Internet insurance is still at an early stage, and their far-reaching impact on the industry has not yet been fully discussed. Future research should focus on how these technologies can reshape insurance business models, risk assessment, and customer service. By examining these issues in depth, future research will be able to provide industry practitioners and policymakers with more concrete and practical recommendations, helping the Internet insurance industry achieve healthier and more sustainable development.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.