Abstract

Board social capital encompasses two types of relationships: external and internal ties. This study examines the effects of board social capital on firm performance using a sample of the 103 companies listed on The Madrid Stock Exchange (2008). In order to measure board internal social capital, we consider the directors’ co-working experience on the board. On the other hand, to measure external board social capital, we rely on the directors’ ties to other organizations through interlocking directorates. We introduce internal social capital as a necessary variable for a more complete understanding of the external social capital/firm performance relationship. Our results have important implications for corporate governance practices. When firms propose reconsidering the composition of boards, they should not be guided solely by the intention of maximizing external connections. On the contrary, they should really take into account the fundamental role of internal social capital, which (1) intensifies the positive effects of the external capital when its level is low and (2) attenuates the negative effects of an excess of the board’s external social capital.

Keywords

Introduction

Boards of directors have been widely recognized as important governance mechanisms, and much research has centered on figuring out their role in firm strategy (Carpenter and Westphal, 2001; Hendry and Kiel, 2004; Pugliese et al., 2009; Ruigrok et al., 2006) and, more specifically, their influence on performance (Dalton and Dalton, 2011).

In past decades, boards’ influence on firm performance has normally been analyzed using variables linked to their formal composition and structure, but such analyses have usually failed to identify any substantive relationship between these factors and firm performance (Dalton and Dalton, 2011; Dalton et al., 1998). Our work, using a social capital perspective, pays attention to the board’s internal and external connections. Following Kim and Cannella (2008), we understand board social capital as an asset that represents both the relationships and the potential resources arising from the relations. The definition of social capital varies depending on whether the board’s focus is on external ties—external social capital—or on internal ties—internal social capital (Adler and Kwon, 2002). External ties refer to linkages that involve others outside the organization, while internal ties involve interpersonal relationships between directors on the board.

Many studies in this area have analyzed the influence of boards’ external social capital on firm performance (Kim, 2005; Kim and Cannella, 2008; Kor and Sundaramurthy, 2009). The question about whether social external capital can give a firm a consistent advantage is one that scholars have tried to answer. Different studies have argued that the relationships between external social capital and firm performance are positive (Kim and Cannella, 2008), curvilinear (inverted U-form—Kor and Sundaramurthy, 2009), or negative (Goerzen and Beamish, 2005), contending that a board’s external social capital can yield access to important resources (Mizruchi, 1996; Pfeffer and Salancik, 1978), opportunities to cooperate with other firms (Koenig et al., 1979), legitimacy (DiMaggio and Powell, 1983), and information on business practices (Davis, 1991). While many have argued the virtues of external social capital, others have pointed to the risks and/or dangers involved (Adler and Kwon, 2009; Fligstein, 1995; Palmer et al., 1995). In sum, although it has been extensively researched, how a board’s external social capital influences the performance of its firm remains a puzzle (Sullivan and Tang, 2013). Irrespective of the determinants or consequences of a board’s external connections, a widely held view is that highly connected directors on the board are an increasingly widespread phenomenon.

The lack of systematic empirical evidence (He and Huang, 2011) has led many scholars to suggest that to truly understand how boards affect firm performance, research needs to pay more attention inside the boardroom (Carter and Lorsch, 2004; Johnson et al., 1996). Considering the board as a human group (Finkelstein and Mooney, 2003) clearly shows that relationships between directors on the board, as well as those that they have with other external actors, play a critical role in their decision making. We propose that a board’s ability to process information acquired externally through its directors’ social connections depends on the degree of connectedness inside the board, insofar as it favors trust and collaboration between board members, enhancing teamwork and cohesiveness inside the board (Kim and Cannella, 2008). As its central question, this study investigates the following: how does the relationship between internal and external social capital influence a firm’s financial performance? We aim to contribute to this in two ways. First (and perhaps of greater consequence), we introduce board internal social capital as a necessary variable for a more complete understanding of the board external social capital/firm performance relationship arguing that this cannot be interpreted accurately without considering the impact of board internal social capital. While analyzing the relationships between external and internal social capital and firm performance independently, the corporate governance literature (Kim, 2005; Kim and Cannella, 2008; Kor and Sundaramurthy, 2009; Lester and Cannella, 2006) does not consider the possible impact of one on the other, or the potential influence of this interrelationship on firm performance. Furthermore, and taking a step forward from previous works (Kim, 2005, 2007; Kim and Cannella, 2008), our research sets out the disadvantages of an excess of external social capital, with an emphasis on the sources of capital linked to the performance of the board’s tasks rather than its demographic aspects. We argue that a board—like any other human group—needs decision-making abilities (Hillman and Dalziel, 2003), which it gains by encouraging directors to share the resources bridged via directors’ external social capital, and the extent to which they do so will depend on the internal social capital generated by its directors’ internal ties (Tian et al., 2011). The advantages conveyed by high levels of external social capital are conditional on the board being structured in such a way that it can operate in a cohesive fashion as a decision-making body. We therefore develop a framework of board internal and external social capital and firm performance. Second, we examine the board’s social capital as a whole, reasoning—as Kor and Sundaramurthy (2009), Tian et al. (2011), and Haynes and Hillman (2010) do—that the social capital which individual members bring to a group influences the actions of the whole. Many previous studies do not analyze the board’s external social capital in its entirety, but instead they focus solely on outside directors (Carpenter and Westphal, 2001; Kim, 2007; Kor and Sundaramurthy, 2009: Tian et al., 2011). Our research takes a joint view of the internal and external connections of each and every one of board member.

As Kwon and Adler (2014) point, research in social capital can usefully continue to expand on specific aspects and mechanism, as they are relevant to specific topics. In this respect, we would highlight the fact that boards of directors possess distinctive features that give special relevance to the role of internal and external social capital in this type of group.

Our analysis of 1158 directors of 103 firms listed on The Madrid Stock Exchange allows us to test empirically how internal social capital moderates the relationship between external social capital and firm performance, and our analysis provides strong support for our predictions. Our study has implications for research, both about boards and about corporate governance practices, while—in practical terms—our results suggest that boards aiming to improve their productivity should pay attention to the relationship between internal and external social capital inherent in their composition.

Theory and hypotheses

Board social capital

There have been many contributions to the field of social capital since the early 1990s (Adler and Kwon, 2002; Burt, 1992; Coleman, 1990; Putnam, 1993). Starting from Adler and Kwon (2002), Kim and Cannella (2008) apply this concept to boards of directors. They distinguish between external social capital or “bridging” forms of social capital and internal social capital or “bonding” forms of social capital. The bridging view focuses primarily on social capital as a resource that inheres in the social ties tying an actor to other actors outside the organization (external ties), while the bonding view focuses on linkages among individuals within the collective (the board of directors in particular), and, specifically, on those features that enable the board to work effectively as a group and thereby facilitate the pursuit of collective goals (Fukuyama, 1995). We find it most useful to incorporate both perspectives (bridging and bonding) in our study. Most of the research in the board context examining social capital has focused on linkages between firms and the networks that develop from them; however, the role of internal social capital within the board of directors has received much less attention and more recently.

Social capital theory fits the context of board directorship very well. As Pfeffer’s (1973) and Pfeffer and Salancik’s (1978) seminal works on boards point out, network building within and outside their organizations is one of the most important jobs of a director. Boards are decision-making groups that face complex tasks relating to strategic-issue processing. Unlike many working groups, boards function only episodically, there is no continuous working basis, and meetings are only held occasionally. The majority of board members are outside directors, whose primary affiliation is to another organization. They serve on a part-time basis and have limited direct exposure to the firm’s affairs (Forbes and Milliken, 1999). These distinctive features of the board mean that the advantages brought by internal social capital are particularly important for the effectiveness of this governing body. Furthermore, the external social capital gains greater significance in the context of boards of directors. Board members are often selected because of their external connections, in that they contribute to the board’s ability to perform its provision of resources function (Kim and Cannella, 2008). Directors’ external social capital is converted into an attribute that is demanded by firms and its role as a boundary spanner acquires a greater importance than in other working groups.

External social capital

A board’s external social capital is defined as the degree to which board members have outside connections with the environment and the potential resources arising from those connections, which may be sources of competitive advantage for the firm (Kim, 2005). The primary function of external social capital is that of bridging, or linking the firm to the external environment. Directors may connect to their environment in a number of ways, as there are several sources of external social capital, such as outside directors’ ties to the firms in which they are employed on a full-time basis; seats on the board of other firms; or social capital in the form of the directors’ personal relationships, affiliations, and social standing (Johnson et al., 2013; Kim, 2005, 2007).

Boards with high levels of connections or external ties will have earlier and faster access to critical resources and to more timely information, resulting in better financial outcomes (Carpenter and Westphal, 2001; Kor and Sundaramurthy, 2009; Tian et al., 2011). Kim and Cannella (2008) suggest that, when the business environment is turbulent, directors must engage in creating more external ties, and this notion has led to boards increasing the numbers of their directors who have high levels of external social capital, contributing to raising both the visibility and the complexity of their organizations (Johnson et al., 2011). Firms benefit from their directors’ external social capital in three ways. First, such external social ties can serve as boundary spanners, providing channels for communication back and forth between the external environment (Carpenter and Westphal, 2001; Hillman et al., 2000). For example, firms may be able to reduce the uncertainty associated with new strategies via the information that they gain from interlocks with firms that already have experience in implementing that strategy (Connelly et al., 2011). Second, highly connected directors can play another vital role in the companies they govern by obtaining support from influential agents or external stakeholders that may be critical to the organization’s performance (Hillman et al., 2000; Kiel and Nicholson, 2006). For example, directors with ties to private equity deals will increase the likelihood of private equity deals for the focal firm (Stuart and Yim, 2010). Similarly, connections with industry players (suppliers, distributors, major customers) that result from the directors’ professional experience in the focal industry may encourage the creation of stable relationships with clients and/or privileged access to distributors. Third, the legitimacy of decisions taken by the firm will also be improved by the presence of board members who are highly connected to other organizations with established business reputations (Kiel and Nicholson, 2006). For example, chief executive officers (CEOs) are the most powerful and influential individuals within the business environment and are often invited to join the boards of other firms. The value and worth of the focal firm is confirmed to the rest of the world by having such prestigious individuals as board members (Pfeffer and Salancik, 1978). Legitimacy may also be a prerequisite for securing resources for the firm, because financial institutions or investors may be more willing to provide funding to a firm if it believes that its directors are reputable individuals (Mizruchi, 1996).

Board directors often sit on multiple boards, thus forming connections with other firms, and the aggregate of these “interlocks” can be a major source of a board’s external social capital, and this is the most valued by the literature (Hillman and Dalziel, 2003; Kor and Sundaramurthy, 2009; Tian et al., 2011). Interlocking directorates are thought to have positive impacts on company performance by providing management with access to a variety of key resources in the form of strategic information, learning, and legitimacy. Thus, previous studies on interlocking directorship have shown that such ties play an important part in the dissemination of knowledge and imitation of successful strategies between firms (Burt, 1987; Connelly et al., 2011; Shipilov et al., 2010), in accessing strategic information and opportunities (Carpenter and Westphal, 2001), and in gaining legitimacy for the focal firm (Mizruchi, 1996; Mizruchi and Stearns, 1988; Westphal et al., 2001): since these benefits are complex and difficult to replicate, external directorship ties can amount to an important competitive resource.

However, despite these benefits, there can be associated costs. Serving on many boards—“over-boarding”—can take a toll on a director’s limited time and attention (Harris and Shimizu, 2004; Ocasio, 1997). Being a company director is a prestigious role that provides valuable learning and networking opportunities, so individuals may be tempted to accept invitations to join several boards (Useem, 1982), but then, pressed for time, not attend meetings regularly or fail to prepare for them adequately, which will adversely affect the quality of their contributions (Finkelstein and Mooney, 2003; Harris and Shimizu, 2004; Kor and Sundaramurthy, 2009). The probability of schedule conflicts can increase quickly when directors take on multiple directorships (Harris and Shimizu, 2004), so belonging to too many boards can lead directors to decrease their levels of involvement and commitment to any specific one. Their function as boundary spanners can also distance them from fellow members, a problem that may be exacerbated if they are members of many boards, and which can tend to undermine board cohesion and its nature as a group. A high level of external social capital in a board could therefore lead to a lower involvement from its board members. Once a certain level has been reached, an increase in the number of external ties might create more disadvantages than advantages, with a negative influence on performance.

In summary, while external social capital may contribute to enhancing firm performance, it is reasonable to suggest that an excess of external social capital might be counterproductive:

Hypothesis 1. There will be a curvilinear (inverted U-form) relationship between external social capital and firm performance, such that performance will increase as external social capital increases, but then decline as external capital reaches higher values.

Internal social capital

Finkelstein and Mooney (2003) proposed that “boards are groups” that can improve their decision making by working together as a team. Individual directors may not possess the complete set of skills and knowledge to meet a firm’s advisory and governance needs, but as a group, they can pool their knowledge to fulfill their governance duties effectively (Kor and Sundaramurthy, 2009). Recent studies that have looked at the view of the board as a group have highlighted a critically important issue if directors are going to function effectively as groups and contribute their full potential to firm performance (He and Huang, 2011). Both the number and the length of board meetings are usually limited, so that, unless there are effective ways of guiding the relationship dynamics between their directors, boards are less likely to make specific or key contributions to firm performance (Carter and Lorsch, 2004). Intra-board connectedness can organize or facilitate the directors’ ability to work as a team, with positive consequences for firm performance.

Board internal social capital sources lie in ties and relationships between directors on the board, deploying a bonding function. Internal ties enhance trust between those directors who are connected, which, in turn, facilitates the exchange of valuable information and knowledge (Kim, 2005; Kim and Cannella, 2008; Stevenson and Radin, 2009). Directors may only be willing to share key and critical environmental information with members whom they trust (Kim and Cannella, 2008; Offstein et al., 2005). The relationships between directors serve as informal conduits breaking down the boundaries that tend to undermine the orchestrated activities expected from the board (Leana and Van Buren, 1999; Nahapiet and Ghoshal, 1998). Directors who are close to each other strengthen their ability to work as a team. It is important to recognize that boards should not automatically be assumed to possess such “teamness” (Hambrick, 1994), as they may only meet occasionally—however, any lack of this reduces the ability of directors to work together effectively (Kim, 2005). Connectedness among members facilitates the establishment of norms and values between its members, fostering implicit mutual expectations and behaviors and promoting commitment to collective actions (Offstein et al., 2005). Several authors (Gargiulo and Benassi, 1999; Kim, 2005; Reagans and Zuckerman, 2001) have demonstrated the possibility that too much internal social capital might have negative effects, with the creation of groupthink, cliques, old-boy networks, and other dysfunctions that are the result of “over-chumminess” or homogeneity. However, from our perspective, and given the distinctive characteristics of boards of directors, which have a limited number of meetings per year and have no continuous basis for interaction, internal social capital would have to be extremely high before these negative effects could be generated.

He and Huang (2011) argue that boards—as groups—are specifically responsible for deciding on firms’ strategic issues, and that such decisions—as well as many others they perform as directors—have significant implications for a firm’s financial performance. The complexity of the decisions taken by the board requires a greater cooperation than in other teams to enable a diverse set of directors to apply their various perspectives, knowledge, and approaches to strategic problem-solving. Directors need to communicate, assimilate their cognitive frameworks, and develop shared understandings. On the other hand, the board as episodic decision-making group, and being largely made up of outside directors, will require a strengthening of internal ties in order to break down boundaries and increase the levels of trust and commitment that are required for collective actions.

As we have highlighted in previous paragraphs, internal social capital derived from intra-board connectedness brings about trust, information exchange, knowledge transfer, teamwork, and cohesiveness—all of which contribute to the board’s ability to function as a team for a common purpose. We therefore propose the following:

Hypothesis 2. There will be a positive relationship between board internal social capital and firm performance.

External and internal social capital

Previous research has largely examined the advantages and disadvantages that firms gain from their directors’ external social capital (Kiel and Nicholson, 2006; Hillman and Dalziel, 2003; Kor and Sundaramurthy, 2009; Tian et al., 2011), but has not explored questions of a possible relationship between external social capital and internal social capital, or of the influence that such a relationship might have on firm performance. We propose that there is, indeed, such a relationship and that it will impact board—and thus the firm’s—performance. Adler and Kwon (2002) concluded that the behavior of a collective actor—such as a board—is influenced both by its external linkages—bridging—and by its ability to work together for communal purposes—bonding—and that these two types of board member relationships are not necessarily mutually exclusive. The most productive boards are those where directors work cooperatively. Furthermore, we propose a multiplicative effect of both types of social capital, in which high levels of internal social capital will intensify the positive effects of external social capital on the firm’s performance, and will cushion its negative effects when the level of director overload reaches very high levels.

Resource dependence theory (Pfeffer and Salancik, 1978) and the social status perspective (Jensen and Zajac, 2004; Washington and Zajac, 2005) indicate that most organizations aim to recruit other directors of known economic and social prestige onto their boards, so as to build up the number and range of resources that they can access. Increasing external social capital provides new resources and capabilities to boards, but its impact on the firm’s performance depends on how these are integrated into the board’s decision-making processes, through internal social capital. As kwon and Adler (2014) proposed, having social capital does not mean necessarily making use of it. In other words, having external ties does not guarantee their mobilization and application to the board’s decision-making process. In this sense, while social network research often assumes that individuals or organizations will take advantage of their network contacts, a recent stream points out that this assumption often fails (Obukhova and Lan, 2013) and it would be useful to make the distinction between potential and mobilized ties. In our case, we believe that a higher internal social capital could further drive the deployment and mobilization of external social capital. Key resources bridged via directors’ external ties may have greater impact on firm performance when the experience, knowledge, connections, and reputation gained are transferred within the board, and this internal dissemination process will be more intense in the case of highly cohesive boards with a high level of internal social capital. In this sense, when the number of external ties is low, high internal social capital will amplify the benefits of external social capital. In this case, the resources provided by external ties will be integrated by intensive co-working among directors. Conversely, low levels of internal social capital may imply that directors with external ties are not able to fully deploy their potential resources to the board’s decision-making processes. A director with valuable ties can provide vicarious experience when it is deployed on the board through co-working. In effect, information and resources travel through directors’ ties, influencing the focal firm’s board. This influence can take the form of new ideas for the focal firm, often to the benefit of its shareholders (Johnson et al., 2013).

Furthermore, internal social capital not only affects the influence of external social capital on firm performance on the increasing side of the slope, but also on its decreasing part. As we explained earlier, increasing the number of these ties can negatively affect the board’s internal working. However, higher levels of internal social capital may cushion the negative impact of “over-boarding.” When boards have a high number of external ties, the negative effects arising from the psychological distance and possible limitations of time and attention of directors with greater external social capital (Kim and Cannella, 2008; Ocasio, 1997) are attenuated by the positive effects of internal social capital. Higher levels of internal social capital mean that boards require less time and effort to access the resources (experience, knowledge, ties, reputation, etc) provided by directors’ external ties. At the same time, the disadvantages of the lack of time and attention available for overboarded directors who sit on a number of boards might be attenuated by the greater commitment that is generated by internal social capital. These arguments are consistent with the results gained from applying group dynamics approaches to firms’ boards (He and Huang, 2011).

Therefore, we argue that when levels of external social capital are low, a high internal social capital will strengthen the increase in knowledge that occurs when new external ties with other boards are incorporated. A high level of internal social capital improves the dissemination of the advantages brought by these new ties, multiplying their effect on firm performance by intensifying the positive effect of external social capital on performance. Conversely, high levels of internal social capital will cushion the negative effects on performance caused by an excess of external social capital, given that communication requires less effort from the increasingly overloaded board members. A high level of cohesion between board members facilitates communication and coordination between them, mitigating the negative effect of overloading caused by their participation on a high number of boards. The negative influence of excessive external social capital on performance will therefore be less intense when internal social capital is higher.

In summary, we propose that the positive impact of external social capital on firm performance will be enhanced by a higher internal social capital. Additionally, the negative effects on firm performance of over-boarding will be cushioned by high levels of internal social capital. In other words, we predict that it will moderate the relationship between a board’s high external social capital and firm performance:

Hypothesis 3. The degree of internal social capital moderates the inverted U-shaped relationship between external social capital and the firm’s performance. Specifically, when board internal social capital is higher, the rate of improvement in the firm’s performance associated with the initial increase in external social capital is more intense, whereas the rate of decline in the firm’s performance, when external social capital is higher, is less pronounced.

Methods

Sample and data collection

Our sample frame was all the Spanish companies listed on The Madrid Stock Exchange in the 2008 financial year, except those classified as financial service firms. We derived a list of 111 such companies from the stock exchange’s official registration files, but eliminated six for which full data about the external directorship ties of their board members were unavailable, and another two for which preliminary data analysis identified as outliers, leaving a final sample of 103 companies. We chose listed companies for our study because the legal requirements on them to publish corporate governance and financial performance information ensured straightforward access to such data, but—in line with previous research (Beverley and Shireenjit, 2009; De Andrés et al., 2005; Fernández and Arrondo, 2007)—excluded financial sector firms because of the specific regulations they work under, and their different balance sheet structures. Spanish companies follow a unitary system of corporate governance (as practiced in the United States, the United Kingdom, Italy, and Portugal), have low percentages of independent directors compared with boards in other countries, have markedly higher proportions of reference shareholders than boards in other countries, and have very high levels of CEO/Chair-duality.

Data on firm performance were gathered from the el Sistema de Análisis de Balances Ibéricos (SABI) database, which provides up-to-date economic and financial information on all listed Spanish companies, while information about board and committee composition was extracted from the National Securities Market Commission—Comisión Nacional del Mercado de Valores (CNMV)—the official body entrusted with safeguarding the transparency of the Spanish stock exchange—whose website lists companies’ annual corporate governance reports. We gathered the names of all board directors of each sample firm from their 2008 corporate governance reports, identifying 1158 directors, together with the dates of their initial board appointments and their memberships of different board committees. We used Axesor, which specializes in using official registers to provide information on companies and their executives, to supply information about individuals’ directorships, and the Official Bulletin of the Mercantile Register (BORME, n.d.) 1 to understand board membership structures, from which we identified all the directorships held by our sample firms’ 1158 directors. Having removed each director’s entry on their focal firm’s board, we were left with a database of 33,519 external directorship ties, which we then refined to avoid duplications caused by firm or board reorganization (retaining the oldest ties), and to remove those no longer valid in 2008, bringing the final total of external directorship ties down to 4841.

Dependent variable

Return on sales (ROS) was adopted as the operating measure of firm performance, as the proxy of profitability most often used in corporate governance and performance research (Geletkanycz and Boyd, 2011; Shrader, 2001; Tuschke and Sanders, 2003): such accounting-based indicators reflect the influence of internal management better than market-based measures, which are more likely to be subject to exogenous economics factors (see a review by Dalton et al., 1999; He and Huang, 2011; Parker et al., 2002). We opted for ROS because it is a profitability measure directly tied to the functioning or running of the company, independent of the level of any investment, and so can be a useful measure of a company’s operational efficiency. The literature on board–firm performance relationships recognizes a time lag effect (Geletkanycz and Boyd, 2011; Haynes and Hillman, 2010; He and Huang, 2011; Kor and Sundaramurthy, 2009; McDonald et al., 2008; Tian et al., 2011), so we employed a 2-year lag between predictors and performance measures using the annual ROS figures related to 2010 (t + 2), to safeguard our results against potential reverse causality, and to also allow for the time it takes for board social capital to influence firm performance (Bono and McNamara, 2011; Brunninge et al., 2007). As kurtosis was initially more than twice the standard recommended value, we transformed the ROS measure using its square root (Hair et al., 2010).

Independent variables

Consistent with previous research (Haynes and Hillman, 2010; Kor and Sundaramurthy, 2009; Tian et al., 2011; Wincent et al., 2009), we consider the board’s external social capital as being constituted by the external directorship ties board members hold with other firms. Taking into account that larger boards are naturally more likely to have more ties with others boards, we calculated this variable as the total number of directorships held by a focal firm’s directors with other firms divided by the size of the focal firm’s board (Kiel and Nicholson, 2006)—the higher this quotient, the greater the connectedness of the board to other companies and therefore the greater its external social capital.

Internal social capital refers to the degree to which board members are integrated in the team, reflecting the ability of the board to work together effectively (Forbes and Milliken, 1999). Its source lies in ties and relationships between directors or intra-board connectedness. Internal social capital can be developed through directors’ shared experience of working with each other, which allows them to develop a collectively owned “bonding” form of social capital (Adler and Kwon, 2002). We use as measure for internal social capital the board’s co-working experience.

Board’s co-working experience (co-working) involves a group-level mutual knowledge of the skills, limitations, and idiosyncratic habits of specific board members, enabling the board to function and make decisions effectively as a group (Kor, 2003). Co-working experience is a valuable resource that develops over time, and which has been identified previously in the literature on workgroups and top management teams (TMT) (Kor, 2003, 2006). The amount of time directors spend with the same colleagues results in positive relationship dynamics inside the board. Longer co-working experience facilitates the development of “shared mental models” (Cannon-Bowers et al., 1993) or “mutual knowledge” (Cramton, 2001) about who on the board knows what, and how best to seek and share information for important decisions from and with other board members. We follow previous TMT research (Barkema and Shvyrkov, 2007; Kor, 2006) and board contexts (Tian et al., 2011), in measuring this variable using Carroll and Harrison’s (1998) common historical experience measure, which captures the overlap in tenure or shared experience of board directors as a proxy for their internal relationship dynamics over time in the formula

The measure averages the pair-wise overlap in tenure for all possible pairs of board directors, where N is the total number of pair-wise comparisons and ui the tenure of director i (the number of years between their initial appointment to the board and the focal year 2008). Min (ui, uj) represents the length of the overlap in tenure of directors i and j—that is, the time they have served together on the board. Our analysis used the logarithmic transformation of common historical experience to capture the diminishing effects of members’ interactions over time (Carroll and Harrison, 1998; Cialdini and Trost, 1998): using this logarithmic form reflects the idea that joint tenure has a diminishing marginal effect, consistent with prior research on tenure and socialization that shows that the earlier years of experience lead to greater changes in cognitions and board processes (Katz, 1982; Watson et al., 1993).

Taking into account that the variables used to identify boards’ social capital in this study can be defined as “history dependent”—in that they accumulate over the firm’s and board’s history—our aim was nevertheless to conduct a cross-sectional examination at a particular point in time (2008), with the intention of analyzing how those variables influenced firm performance. We must bear in mind the average 6.5 year tenure of board members (over which period the boards’ internal social capital was forged), as well as the average length of the external ties (4.87 years).

We used straightforward measures of board social capital from publicly available data. Following Tian et al. (2011), our measures are more informative than those previously used by proxies for board composition (e.g. executive vs outside directors). However, we recognize possible limitations. Therefore, regarding external social capital, our measure does not take into account the possible disparity in the number of ties between directors, but it measures the average value of external ties on the board. Moreover, our measures do not directly capture the underlying processes through which board members access, utilize, and synthesize each other’s knowledge. To address this limitation, future research should directly examine the processes that facilitate or hinder board decision making.

Control variables

In line with previous studies on corporate governance, we included a list of control variables at board, firm, and industry levels to monitor the extent to which they might affect the relationships we proposed. Much prior research has considered the positive influence of a board’s size on company performance (Dalton et al., 1999; Finegold et al., 2007; Goodstein et al., 1994; Johnson et al., 1996; Pfeffer and Salancik, 1978). However, this positive effect on firm performance can potentially be counteracted by some large group dynamic problems—where large boards become less participative, less cohesive and more fragmented—so the positive impact could diminish beyond a certain size, indicating an inverted U-shaped association between board size and firm performance (Judge and Zeithaml, 1992; Pugliese and Wenstøp, 2007; Zahra et al., 2000). We therefore included board size—measured as the number of its directors—as a control variable in our analysis.

Boards may be structured so that the CEO also acts as the Board Chairman—so-called “CEO/Chair-duality”—or the two roles may be held separately. Research on the direct performance implications of this duality has produced no conclusive results (Baliga et al., 1996; Dalton et al., 1998), but, given that this structural aspect could affect the informal ties between directors (Stevenson and Radin, 2009), and that a separate Chair could provide additional boundary-spanning relationships (Ruigrok et al., 2006), we have used CEO duality as a control variable in our study, measured as a dummy variable coded 1 if the CEO was also the Board Chairman and 0 otherwise.

The presence of outside directors on the board is consistently recommended in both national and international corporate governance codes (CNMV, 2006; NYSE, 2010; Organization for Economic Co-operation and Development (OECD), 2004), since such directors can present a set of advantages with positive effects for firm performance. Apart from the role that agency theory gives these directors in controlling management (Fama and Jensen, 1983), outside directors are also seen as sources of various and diverse forms of skills: educational, occupational, and organizational, increasing the level of useful cognitive conflict (Forbes and Milliken, 1999; Rindova, 1999; Roberts et al., 2005). Our study therefore controls for the proportion of outside directors on the board, expressed as a percentage of the total number of its directors.

We have accounted for four firm-level control variables: firm size, firm age, past firm performance, and research & development (R&D) investment intensity. In as much as it can affect financial performance, firm size has been seen as an important control factor in much board research (De Andrés et al., 2005; Gabrielsson and Winlund, 2000; Kiel and Nicholson, 2006; Pugliese and Wenstøp, 2007; Ruigrok et al., 2006), and is measured in our analysis by the logarithm of the firm’s total number of employees in the study’s reference year (He and Huang, 2011; Judge and Zeithaml, 1992; Tuschke and Sanders, 2003). In the same way, firm age has been suggested as influencing the level of firm resources, its growth potential, and its performance (Beverley and Shireenjit, 2009; Kim, 2005; Kor and Sundaramurthy, 2009; Pugliese and Wenstøp, 2007), and is measured here as the number of years since the firm’s founding. Past firm performance is a common predictor of future performance (Geletkanycz and Boyd, 2011; Kim, 2005; Tian et al., 2011; Tsai, 2001; Tuggle et al., 2010). Geletkanycz and Boyd (2011) point out that its inclusion as a control variable also helps to mitigate concerns over model misspecification: to the extent that unobserved factors impact a firm’s future performance, prior performance should at least partly capture them. Moreover, poor firm performance may lead the board to take a more active role (McNulty and Pettigrew, 1999; Stiles and Taylor, 2001; Westphal and Fredrickson, 2001). Past firm performance was measured in our model as ROSs for the year prior to our reference year. Finally, we also controlled for R&D investment intensity, which is often considered an important predictor of a firm’s financial performance (He and Huang, 2011), calculated by dividing a firm’s R&D expenditure in 2008 by the firm’s total assets in that year.

Given that the board’s performance may be driven by the relationships between the board and its TMT (Kor, 2006), we introduced the percentage of executive directors on the TMT as a control variable (Barroso-Castro et al., 2009). This variable was calculated as the number of executive directors over the size of the TMT. Finally, as our sample includes firms from a variety of industries, we included a control variable to account for any specific industry trends in our results. We adopted the industry classification used by the Spanish stock markets and the financial systems operator, Bolsas y Mercados Españoles (BME), to code the following industry variables: industry 1, Petroleum/Energy; industry 2, Basic materials, Manufacturing, and Construction; industry 3, Consumer goods; industry 4, Consumer Services; industry 5, Real Estate and industry 6, Technology/Telecoms.

Statistical estimations

Table 1 presents descriptive statistics and a correlation matrix for the variables. The variables did not correlate strongly with one another or with the control variables, easing concerns about multicollinearity. Once the dependent variable had been transformed, all kurtosis and skewness values were below the level of twice the standard value taken to indicate a departure from symmetry (Hair et al., 2010). We used ordinary least squares (OLS) to test our hypotheses, as this technique enables the examination of statistical associations for evidence of nonlinearity: nonlinear components were represented by squared variables. Entering the variables in one block and the squared variables in a second enabled us to go beyond linear relationships to determine the significance of curvilinear relationships. Scholars modeling the relationship between external ties and performance have generally employed standard OLS regression.

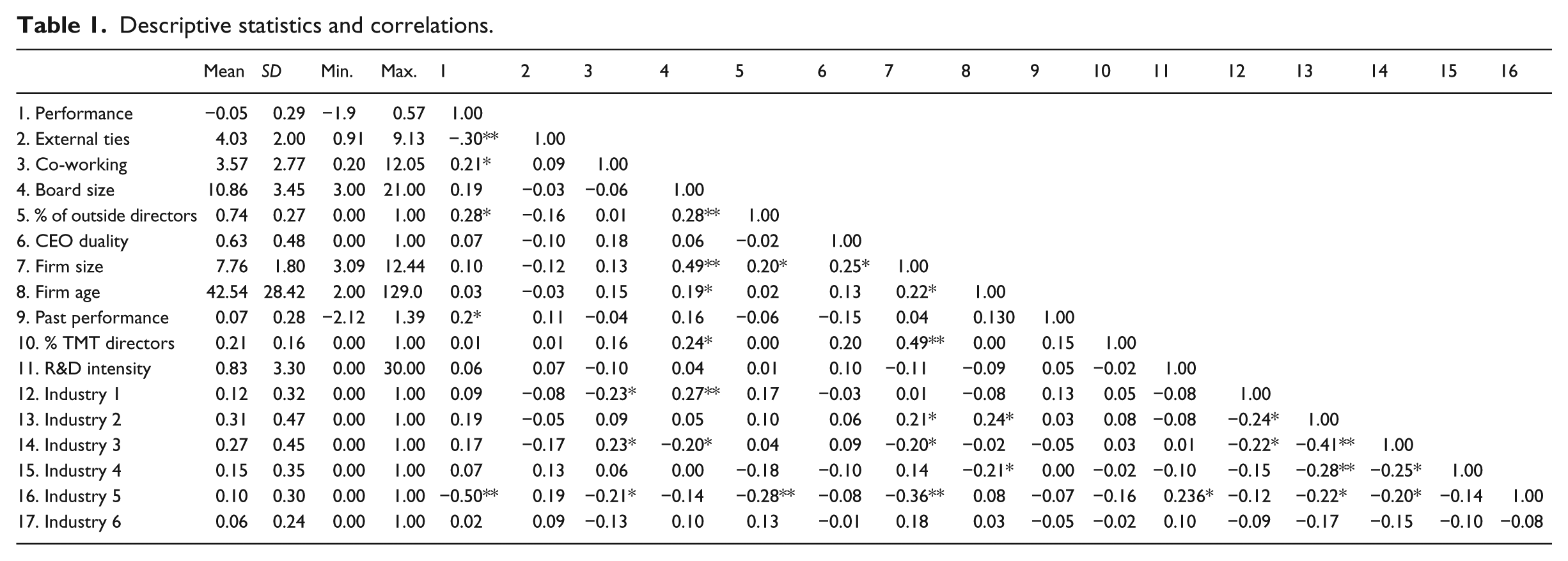

Descriptive statistics and correlations.

However, as the literature clearly indicates, one aspect that complicates the empirical analysis of boards of directors is that many of the variables might be determined endogenously (Boone et al., 2007; De Andrés and Vallelado, 2008; Hermalin and Weisbach, 2003; Johnson et al., 2013; Kwon and Adler, 2014; Linck et al., 2008), that is to say, they are correlated with the error term. The potential for endogeneity between the variables relating to board structure and firm results could be due to the effect of simultaneity, inverse causality, or the omission of important possible variables (Hermalin and Weisbach, 1998, 2003). With regard to the first point, it should be remembered that firm profitability is, among other aspects, the result of the actions of its governing bodies and this in turn is a factor that could potentially influence the choice of future components of these governing bodies (self-selection). In other words, firms may, depending on an improvement or decline in their results, select the structure of their board. Certainly, directors are more likely to stay together when the firm is performing well. Firms’ concerns can also affect who remain on the board, where directors may choose to leave a board if continued memberships might harm their social capital (Johnson et al., 2013). The literature suggests two procedures for analyzing the effect of simultaneity: the use of exogenous “instrumental” variables or the inclusion of “lag effects” as instruments. In the second option, panel data should be used. However, when they are available, carefully chosen strictly exogenous instruments remain the “gold standard” for consistently identifying the effect of an explanatory variable on a dependent variable (Wintoki et al., 2012). With regard to the second question, non-observable heterogeneity arises from the omission of certain explanatory variables from the model (Kor and Sundaramurthy, 2009; Kim and Lim, 2010). This aspect is critical when specifying the model. Obviously, the first step in trying to avoid this situation is to carry out an exhaustive literature review, in order to include all the variables that support the concept that is being studied. For this reason, and following a thorough review of prior studies, our study includes the set of control variables that have been analyzed in the summary above, which take into account board structure, the characteristics of the firm, and the sector in which it is operating. In response to this point, we would point out that one source of endogeneity that is often ignored arises from the possibility that current values of governance variables are a function of past firm performance (Wintoki et al., 2012). We have therefore included this variable in our study as a control variable (Geletkanycz and Boyd, 2011). This procedure comes with the understanding that “at a practical level, it is unlikely that any single study is completely free of endogeneity issues and we therefore argue that the initial consideration should be sought in careful theory construction” (Chenhall and Moers, 2007: 192).

To summarize, it is reasonable to expect that board characteristics, such as the co-working, are endogenous and a function of other “fundamental” characteristics not included in the model. If this endogeneity created an adverse bias in our OLS models, it would be difficult to interpret the association between variables. We therefore used a specification test to investigate the extent of any endogenous bias in a new model (Hausman, 1978). We suggested that the internal social capital (co-working) is associated with “average board tenure” and “number of executive directors.” As Kor (2003, 2006) points out, co-working is a valuable resource that develops over time, enabling the board to function and make decisions effectively as a group. It derives from the amount of time that directors spend with their colleagues, with the direct consequence of a positive relationship dynamic within the board. Therefore, as a board member’s length of tenure on the board increases, the incidence of co-working becomes more likely. Equally, the presence of executive directors, although limiting the board’s independence from the TMT, increases the possibility of directors sharing time together and, as a result, the likelihood of co-working. Before carrying out the relevant analysis, we checked that neither of the instrumental variables correlated to ROS (2010) of the selected firms, and that they did correlate to the co-working variable (0.822** and 0.214* for tenure and number of executive directors, respectively).

Using these results, we carried out the Hausman (1978) test. To do this, we simply regressed the co-working variable using the variables “average board tenure” and “number of executive directors” in our Model 0. The model exhibited significant explanatory power with an adjusted R-square of 86.2% (p < 0.000). We include the OLS residuals obtained from the equation (Model 0) as an additional explanatory variable in the subsequent models (Models 1–5), but the results indicate that the residuals (λ) from Model 0 were not significant in any of the models, suggesting that our results are not affected by an endogenous bias. Following Peasnell et al. (2000), Models 1–5 were also re-estimated via two-stage least squares regression (2SLS), using the predictor variables of co-working as our instrumental variable. The results of the 2SLS are similar to the OLS results in Table 2.

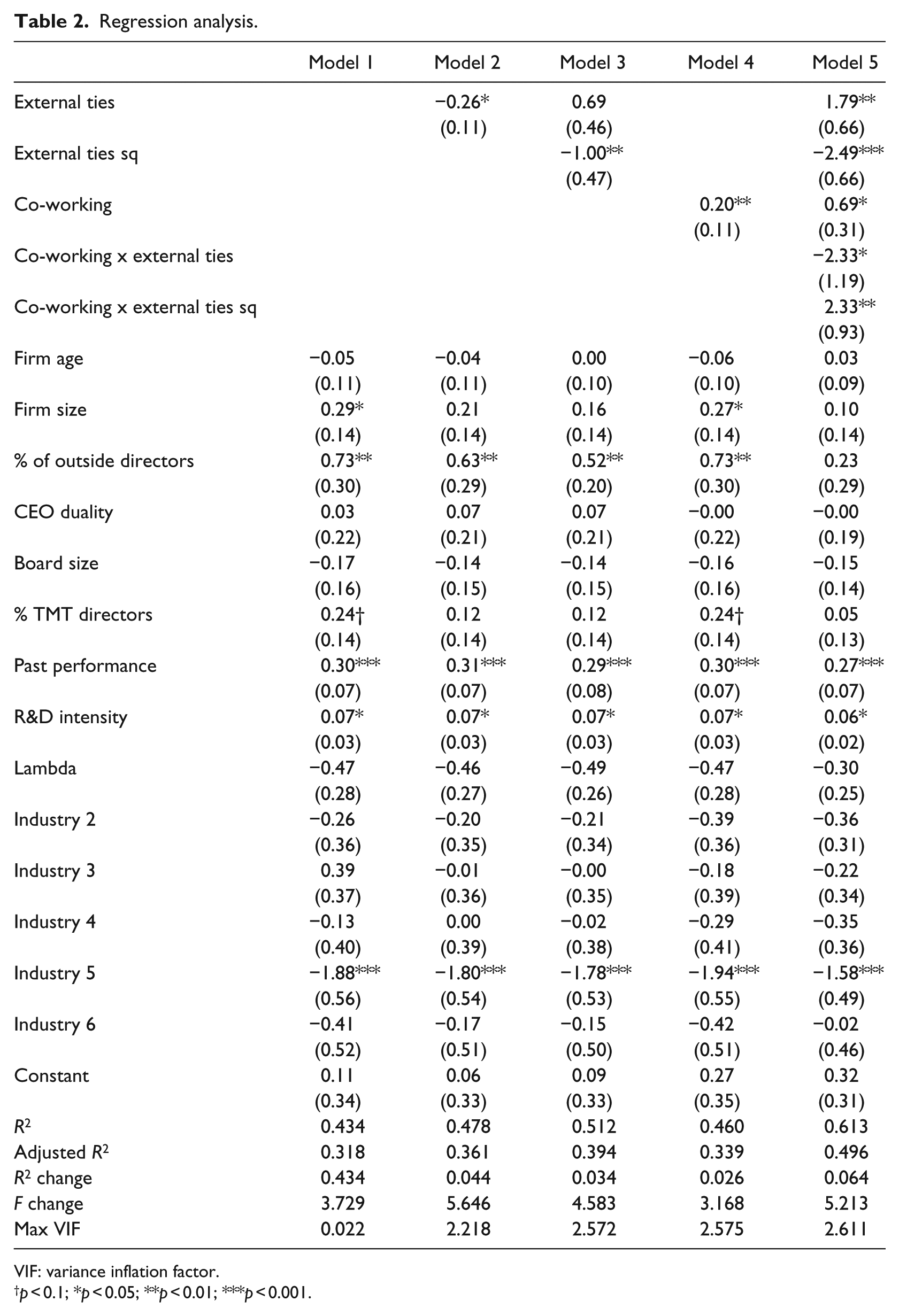

Regression analysis.

VIF: variance inflation factor.

p < 0.1; *p < 0.05; **p < 0.01; ***p < 0.001.

Including two-way interactions and quadratic terms can introduce the possibility of harmful multicollinearity between the variables, producing large standard errors and reducing confidence in the relevant regression coefficients. Following Aiken and West (1991), we mean-centered our variables prior to creating our interaction terms to minimize the distortion due to high correlations between the interaction and higher order terms and the main effects variables. We also applied the residual centering procedure (Jong et al., 2005; Lance, 1988; Zhang and Rajagopalan, 2010) to handle multicollinearity between the interaction term (e.g. X1X2) and its constituent parts (X1 and X2): the two-stage procedure involved first regressing each interaction term on its components, and then using the residuals instead of the original interaction terms in the data analyses (Lance, 1988). The Durbin–Watson test attains a value of 1.89, which, considering the size of our study sample and the number of predictor variables, demonstrates that autocorrelation is not a problem in our case.

Finally, we repeated all the analyses considering Tobin’s Q as the dependent variable, but the results did not differ materially from those reported here, again suggesting that our proposed model was highly robust.

Results

Table 2 presents the results of our regression analysis. Model 1 is the baseline model with all control variables included. In Model 2, the estimated coefficient of external ties was statistically significant, with a negative sign (b = −0.26). To test for curvilinear (inverted U-form) relationships, we added the quadratic terms to the regression equation in Model 3: as the table shows, the squared terms for external ties were negative (b = −1.00) and statistically significant, and the coefficients for the first-order effects remained positive (b = 0.69), but not significant. These results do not indicate the existence of independent curvilinear effects (Cohen et al., 2003) and so hypothesis 1 was partially supported.

Hypothesis 2 suggests that there is a positive relationship between internal social capital and firm performance. In Model 4, the estimated coefficient of co-working experience was statistically significant (p < 0.01) with a positive sign (b = 0.20). Including this variable also significantly improved the model fit compared to Model 1, as indicated by the significant increase in R2 and supporting hypothesis 2.

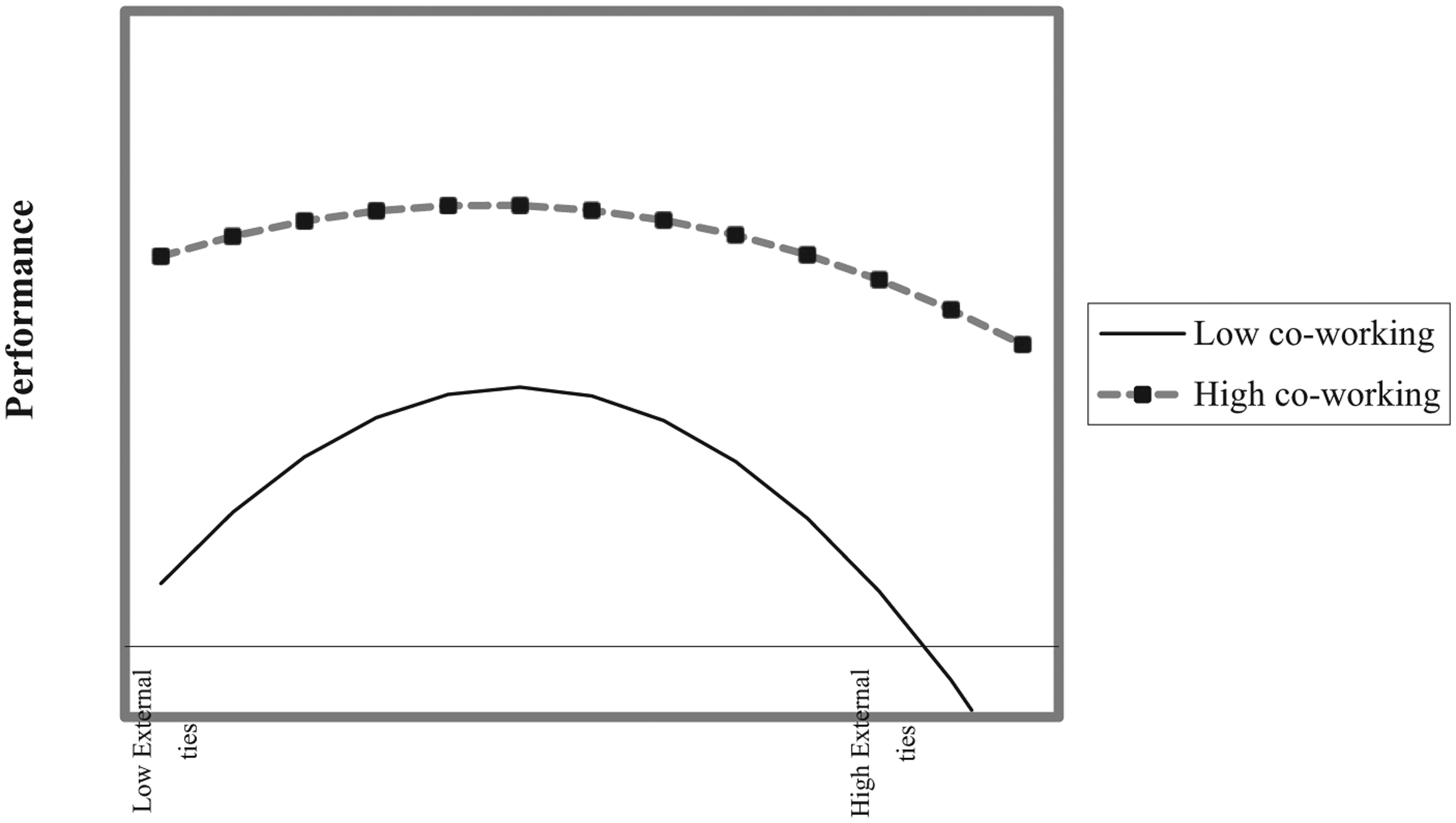

Hypothesis 3 proposes that the degree of internal social capital moderates the inverted U-shaped relationship between external social capital and the firm’s performance. Specifically, when board internal social capital is higher, the rate of the firm’s performance improvement associated with initial increasing of external social capital is more intense, whereas the rate of decline in firm’s performance, when external social capital is higher, is less pronounced. We included (model 5) our board internal social capital measure (board co-working) as moderators of the proposed curvilinear relationship. Using procedures proposed by Aiken and West (1991), we introduced the cross-products composed of the non-squared and squared interaction terms. As Table 2 shows, in Model 5, the estimated coefficient of co-working was statistically significant (p < 0.05) with a positive sign (b = 0.69). Likewise, the squared terms for external ties were negative and significant (b = −2.49; p < 0.001), and the coefficients for the first-order effects remained positive (b = 1.79; p < 0.01). The linear interaction term for co-working and external ties was negative and significant (b = −2.33; p < 0.05), and the squared interaction term positive and significant (b = 2.33; p < 0.01). Including this variable also considerably improved the model’s fit compared to Model 3 (as indicated by the significant increase in R2), suggesting that co-working moderates the linear and curvilinear effects of external social capital on performance and providing support for Hypotheses 3 (see Figure 1).

Effect of co-working at moderating the relationship between external ties and performance.

Discussion and conclusion

This study was designed to refine our understanding of the influence of companies’ boards on their financial performance. We test our proposal that the board’s external and internal social capital determine how productive it is in providing the firm with external resources and facilitating the functioning of the board. More specifically, our perspective is that it is the board’s behavior “as a group” that positively affects firm performance. These proposals are especially relevant for the particular context of board of directors. The distinctive features of the boards, compared to other working groups, pose a different problematic and further emphasize the importance of the joint consideration of both types of capital in order to assess the effectiveness of this governing body. In this sense, the boards are characterized as groups that face complex decisions for the future of the company, involving the need for a detailed analysis process and a wide range of knowledge and previous experiences in this type of decisions. In addition, because boards are elite, episodic decision-making group and are composed of a high proportion of outside directors, its effectiveness is likely to depend heavily on its internal social capital and more specifically, on the interaction between external and internal social capital to bring about a good functioning of this governing body and maximize the resources from the external social capital.

The literature has provided a clear consensus in judging directors’ contributions to their firms as being extremely valuable. Their social capital is seen as one of the most relevant attributes (Hillman, 2005; Stevenson and Radin, 2009). From this, we can conclude that if firms wish their boards to be more productive, they should endeavor to increase their directors’ social capital (Johnson et al., 2011)—although this remains far from simple to put into practice. Resource dependence theory (Pfeffer and Salancik, 1978) and the social status perspective (Jensen and Zajac, 2004; Washington and Zajac, 2005) indicate that most organizations aim to recruit people to increase the number of external ties their boards have. However, we agree with Johnson et al. (2011) in that the story is more complicated. The firms that seek board effectiveness should not simply add more directors with external social capital to their boards. Increasing such numbers of ties can also negatively affect the board’s internal working by undermining group cohesion and by members’ energy and attention becoming divided up between too many such responsibilities. The board will be more productive when it has access to as many resources as possible but can also still work as a compact social group when making decisions. We argue that internal social capital moderates the effects generated by external social capital on the firm’s performance: it intensifies the benefits of external social capital when its level is low, and attenuates the negative effects generated by an excess of external social capital. Our contribution to the literature lies in our analysis of the relationship between these two variables providing valuable new insight in the board context, when the board is considered as a decision-making group.

Our study provides some thoughts into why some firms have more productive boards than others. Our results confirm the relationship between the board’s external social capital and firm performance when we consider internal social capital (He and Huang, 2011; Kim and Cannella, 2008; Tian et al., 2011). These findings have some important implications for both academic research and governance practices.

First, our results show how board internal social capital influences the firm’s performance positively, bearing out recent corporate governance research analyzing boards as decision groups (Gabrielsson and Huse, 2004). This stream of work proposes that efficient and effective group relationships are critical for boards’ contributions to their firms (Huse, 2007; Stevenson and Radin, 2009, Tian et al., 2011): our research clearly shows how intra-board connectedness (Kim and Cannella, 2008; Stevenson and Radin, 2009) affects firm performance. We also suggest a different perspective from the prevailing agency theory. Previous studies of boards and firm financial performance have been criticized for over-relying on these arguments, and have, in fact, generated inconsistent empirical findings (Dalton and Dalton, 2011). Our results help to highlight the importance of internal and external ties, as Pettigrew (1992) has pointed out.

Second, when analyzed in isolation, our results partially confirm the inverted curvilinear U-shaped relationship between the extent of boards’ external connections—in terms of their directors’ ties to other company boards—and the firm results. Nevertheless, the existence of the main effect is not a prerequisite for a moderation effect (Janssen, 2001; Spiller et al., 2013). It could be that two variables do not show any relationships precisely because a third variable is interacting. In our case, when we consider internal social capital as a moderator, we find that the inverted curvilinear U-shaped relationship between external social capital and firm performance is definitively significant. Therefore, our study highlights the effect called “too much of a good thing” (TMGT) (Pierce and Aguinis, 2013) when the influence of internal social capital of the board is taken into account, highlighting the importance of analyzing both forms of capital jointly.

When boards have low numbers of external ties, the positive effects of having directors with access to a variety of key resources (Kiel and Nicholson, 2006) are amplified by the effects of their co-working experience. When boards have high numbers of external ties, the negative effects arising from the distant psychological and possible limitations of time and attention of those directors with greater external social capital (i.e. more outside directorships) towards other members of the organization (Kim and Cannella, 2008) are lessened by the effects of their co-working experience. In our research, the inflection point or the average number of board external ties beyond which they turn counterproductive to firm performance is between eight and nine ties.

Specifically, our research shows that internal social capital modifies the curvilinear form of the relationship between external social capital and firm performance, adopting a more asymptotic form. Thus, internal social capital intensifies the benefits of external social capital when this is not too high and attenuates the negative effects of having a very high number of external ties. This moderating effect provides a relevant contribution to the development of the theory (Pierce and Aguinis, 2013: 325–326).

To improve our understanding of these results, we have analyzed whether the interactive effects of internal and external social capital are greater when boards are more independent of management. That is to say, the social cohesion of the board (internal social capital) might lead to groupthink or social loafing when the board is less independent from the management. To investigate this question, we divided our study sample using the variable, “number of executive directors.” This allows us to distinguish between boards that are more independent of management (there are fewer board members who are also part of the TMT), and boards that are less independent of the TMT. The results confirm our proposal: where boards are more independent of the TMT, the model is highly significant (adjusted R2 = 0.322) and the coefficients of the interactions are much higher than in the general model (Beta co-working x External ties = −4.026**; Beta co-working x External ties sq = 3.412***). In conclusion, and as expected, the effect of the interaction is more pronounced for boards that are more independent of management.

To sum up, we contribute to the literature on corporate governance by looking deeper into the relationship between board configuration and firm performance from an alternative perspective compared to the agency approaches that have underpinned such research for decades. Corporate boards have long been a subject of research; however, there is little consensus as to what a board should look like, or even what kinds of people make the best board members (Johnson et al., 2013). The literature review indicates to us that almost all the works that seek to carry out recommendations about board composition are focused on analyzing demographic characteristics, the skills or abilities of the directors, or economic resources (Castanias and Helfat, 1991; Wiersema and Bantel, 1992), and there are very few works that analyze the possible influence of board social capital in its composition (Kim and Cannella, 2008). All this is despite Pfeffer and Salancik’s (1978) study, in which it was found that the construction of social networks within and outside boards is one of the most relevant tasks for directors.

We agree with Kim and Cannella (2008) when they state that social capital is embodied in board composition. The recommendations made by competent bodies about the composition of boards have traditionally centered on the dilemma between executive directors and outside directors. In this vein, Jensen and Meckling (1976) first theorized about the functions of executive and outside directors on boards. This discussion has modified its focus of interest with the evolving of the functions assigned to the board. In line with this, there are many pieces of research, which propose that outside directors, as well as controlling, are a valuable mechanism to connect the firm with its environment. Thus, they facilitate access to information and resources that promotes the service and advisory roles of these directors in board decision-making processes. Nevertheless, our research proposes that all directors (outsiders and executives) can maintain connections with their environment and that the fruit of these ties is not exclusively present in the outside directors. Thus, we go more deeply into one of the research lines proposed by Kor and Sundaramurthy (2009).

The results of our research reinforce the theoretical conclusions of Kim and Cannella (2008) related to the recommendations about board composition. The firm should seek directors who have network contacts beyond those of any incumbent directors, but not so far outside that the director will be unable to function as part of an effective team. More specifically, our results underline the view that board configuration should be carried out while taking into account both external and internal ties. In this analysis, both executive directors and outside directors must be borne in mind. We must not make the mistake of considering that the possibility of obtaining resources and information, thanks to the connections with the environment, is an option that is exclusive to outside directors. Executive directors can also provide many of these connections. Boards must be sought whose structures imply connection with the environment, without this complicating the possibility of collaboration and joint work as a team. In line with these arguments, in our sample, an average of 21.82% of external ties stems from executive directors; and there are boards in which this value is close to 50%.

Our results have important implications for governance practices. That a board’s internal social capital moderates the inverted U-shaped relationship between external social capital and firm performance suggests a potential avenue for improving corporate governance. The numerous financial scandals of recent years have spurred many countries to begin to design major corporate governance reforms, producing modifications specified in good governance codes with recommendations concerning the structure and composition of this important corporate management agency (CNMV, 2006; NYSE, 2010; OECD, 2004). As He and Huang (2011) have pointed out, these reforms have been centered on the independence of directors from firm management, but their influence so far has been very limited. Our work stresses that board reforms should focus on improving their effectiveness, and that the board’s social capital is a valuable factor here. To sum up, the presence of informal relations and structures facilitate the dynamic of the group’s behavior. The results of this study suggest—as He and Huang (2011) found—that having an “all-star” board may not be conducive to effective board—the relationship between the external and internal ties of the board’s directors may constitute a more important measure for improving board functioning. More specifically, given the advantages that internal social capital provides, forming it is not a question that should be left to chance.

Study limitations

Despite its potential contributions, this study has some limitations, which call for care to be taken in the interpretation of its empirical findings and suggest directions for future research. We decided to measure the extent of boards’ external and internal social capital using the variables most often used in the literature (Haynes and Hillman, 2010; Kor and Sundaramurthy, 2009; Stevenson and Radin, 2009; Tian et al., 2011), but it would also be appropriate to consider other indicators that might benefit a more in-depth analysis. For example, measures linked to directors’ prestige could be applied (D’Aveni, 1990) to gather more detailed information about external social capital, although this might require drawing up lengthy biographies for each director. In terms of internal social capital, variables linked to board relationship dynamics—such as norms of effort, cognitive conflict, or critical focus—could be included (Huse, 2007; Zhang, 2010; Zona and Zattoni, 2007), but again, this would present the challenge of collecting primary data about the workings of individual boards. It would also be of interest to conduct a longitudinal study to support the results that have been attained.

Furthermore, there is another interesting set of questions that has not been considered in this work, and which suggests new lines of research. First, this work is founded on a “board-centric view” and does not take into account—apart from the control variables included in the model—the firm-specific conditions that may explain why external social capital may be irrelevant, good, or bad for the focal firm. This view, which complements the one proposed in our work, and which is focused on the firm, could shed light on the inconsistencies in the results for the external social capital-performance relation, and could therefore lead to a new line of research.

Second, and related to this last issue, it would be interesting to include the strategic perspective and base of expertise provided by the directors’ appointment to other boards as one of the study variables (Carpenter and Westphal, 2001; McDonald et al., 2008), because the value of external social capital could be determined by the strategic relevance of the directors’ experience on other boards.

Third, in our work, we argue that internal social capital has a linear relation to firm performance. In our study, we understand that the positive effects of internal social capital on a work group, such as the board of directors, are more important than the potentially negative. However, as Zhu (2013) proposed, there are some extremely interesting aspects to be studied in the behavior dynamics of teams, such as the possible polarization of specific groups when making particular decisions. We suggest that a new line of research could focus on the analysis of a nonlinear relation between these two variables.

Finally, many of the recommendations of the Spanish Unified Good Governance Code, relating to board composition, structure, and functioning, coincide with the proposals of other international bodies (OECD principles on corporate governance, European Commission recommendations, etc). In the future, it would be interesting to work with samples of boards from different countries and to make possible comparisons, as there is currently very little research of this kind (Johnson et al., 2013).

In summary, our research considers the board as a decision-making group, in a context with very distinctive features, and we show how internal social capital is a vital element in this regard. It has also been widely suggested that a board’s external social capital can be valuable to the firm (Hillman and Dalziel, 2003). We think it is important to ask what the relationship between external and internal social capital should be if boards are going to achieve greater results. Our study shows that internal social capital positively affects firm results, and we both propose and show that this moderates the association between boards’ external social capital and firm performance, and so contributes to corporate governance literature by going deeper into the concept of the board’s social capital.

Footnotes

Acknowledgements

We would like to thank Tim Rowley (co-editor, Strategic Organization) and three anonymous reviewers for this journal for their helpful comments drafts.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Ministerio de Economía y Competitividad, Spain (ECO2013-45329-R).