Abstract

Agency theory is the dominant theory of shareholder activism and argues that activist investors function as external governance monitors. Agency theory predicts that activist investors will tend to target firms who exhibit governance and performance problems. However, given limited resources and time, activist investors must often decide between selecting targets with particularly strong agency and performance problems and those where their activism efforts are most likely to succeed. Social movement scholars point out that, in social movement contexts, the corporate opportunity structure affects when and where activism is likely to arise. We draw on insights from social movement scholarship and agency theory to advance a theory of heterogeneity in shareholder activism. We argue that an activist’s access to power and resources shapes its target selection, particularly the activist’s preference for targeting firms with greater agency problems or where contextual factors favor chances of success. Whereas more powerful activists are able to wield their power as effective governance monitors against firms with substantial agency problems, less powerful activists must strategically select targets of opportunity by choosing firms where contextual factors improve their odds of success. We test these propositions using an innovative relational approach that can simultaneously incorporate firm traits, activist identities, and endogenous dynamics.

Keywords

Introduction

Over the last two decades, shareholder activism has moved from a relatively rare event to a regular occurrence. Shareholders have gained greater power relative to corporate boards and top managers, as investors have become more successful in directly shaping corporate governance (Goranova and Ryan, 2014; Renneboog and Szilagyi, 2011). Consequently, shareholder activism is now a central arena in contests over corporate governance and control. 1 Despite its increased prominence, research on shareholder activism contains many notable ambiguities. Advocates argue that shareholder activism gives investors more of a voice in corporate matters and can curb managerial entrenchment and rent-seeking (Bebchuk, 2005), functioning as an important external corporate governance mechanism (Aguilera et al., 2015). In many cases, shareholder activism has been instrumental in dismissing a sitting CEO, increasing share-buybacks and dividends, or reforming shareholder voting rights. However, critics worry that shareholder activism embroils boards and managers in unproductive and costly distractions (David et al., 2007; Ghazal, 2017; Solomon, 2014) and claim that many shareholder activists are simply aiming to capture notoriety (Duhigg, 2007; Kerber, 2013).

A key reason for this continued controversy is that, until recently, researchers have paid scant attention to the heterogeneity in activists’ goals and resources (Goranova et al., 2017; Goranova and Ryan, 2014). Disagreements over whether and how shareholder activism helps improve governance or performance largely stem from ambiguity in how different types of shareholders use activism to advance their interests. Agency theory informs most research on shareholder activism and highlights how activist investors use various tactics to address performance and corporate governance concerns (Renneboog and Szilagyi, 2011). In this frame, activist investors function as external governance monitors who attempt to intervene when agency problems arise—when a shareholder judges that managers are inadequately attentive to shareholder interests, they may engage in activism aimed at reforming governance and improving managerial accountability.

Given agency theory’s prevalence in shareholder activism research, less research has examined how contextual factors, aside from performance and agency concerns, explain when and where activism is likely to arise. Although a different substantive domain, social movement scholarship highlights how contextual factors and political opportunities shape activism (McCarthy and Zald, 1977; Tilly, 1978). Given limited time and resources, social movement activists often have to decide between targeting firms who have the worst social or environmental records and targets where activists’ efforts are most likely to succeed and have broader impacts. In fact, social movement activists do not always target the worst offenders, often favoring targets of opportunity (Bartley and Child, 2014; Briscoe et al., 2014). The “corporate opportunity structure” describes these contextual factors that open opportunities for activists to press their goals (Briscoe et al., 2014). Activist investors in the finance and corporate governance domain operate in a distinct institutional context, yet they are also likely to incorporate similar contextual factors. Activist investors face a similar decision, having to select between firms with the most entrenched managers, where corporate governance arrangements insulate managers from shareholder scrutiny, and those where their efforts are likely to have an impact.

In this article, we develop a theory of shareholder activism that incorporates agency theoretic motivations but recognizes that other motivations can shape opportunities for activism to emerge, which cannot be explained by agency theory alone. Drawing on theories of stakeholder power, we argue that organizational factors that make firms more susceptible are likely to appeal to distinct activist groups, depending on their relative power to intervene in governance matters. Agency theory emphasizes traits like performance and corporate governance, which we argue are particularly important for powerful activists, such as institutional investors (Ertimur et al., 2010). When facing a decision of targeting the worst offenders or firms where the terms are favorable for success, powerful activists can wield the necessary resources to take on particularly entrenched managers and act as external governance monitors. However, less powerful investors, such as labor unions and individual retail investors, are more sensitive to contextual factors in the corporate opportunity structure. In the absence of formal power and resources, and all else being equal, these activists favor targets of opportunity.

This article makes a number of contributions to research on corporate governance and shareholder activism. First, we theoretically integrate diverse shareholder motivations, drawing on ideas from agency theory and research on social movements. In doing so, we answer recent calls to address heterogeneity in shareholder activists’ goals (Goranova et al., 2017). Second, we go beyond a narrow focus on agency concerns by incorporating ideas from organization theory about status and reputation in organizational fields and how these contribute to firms’ position in the opportunity structure for shareholder activism. Third, to make these concerns empirically tractable, we introduce a novel network approach to analyzing shareholder proxy resolutions and draw on a class of statistical models developed in social network analysis (Lusher et al., 2013; Snijders, 2011). Our empirical approach allows us to represent shareholder activism as a relational field of interacting activist investors and firms, each with their own characteristics and interests.

Empirically, we represent shareholder activism as a bipartite network where nodes are partitioned into two distinct classes representing activist investors and firms; network ties represent shareholder proxy resolutions that link activists to the firms they target. Using a class of statistical network models called temporal exponential random graph models (TERGMs), we predict shareholder resolutions as a function of firm and activist traits. We apply our approach using panel data on shareholder resolutions targeting the S&P 1500 between 2006 and 2013. Our sample includes resolutions that were voted on at the annual meeting as well as resolutions that were withdrawn by the sponsoring shareholder or omitted from the proxy statement by the firm’s appeal to the SEC, capturing a rich collection of shareholder activism events. Our theoretical synthesis and novel empirical approach present new opportunities to consider how corporate governance and political opportunities codetermine the structure and dynamics of the shareholder activism field.

Background on shareholder activism

Most research on shareholder activism focuses on shareholder-sponsored proxy resolutions and the firm characteristics that predict being targeted (see Goranova and Ryan, 2014, for a review). Proxy resolutions have increased in prevalence, becoming a prominent means for investors to voice their concerns in matters of corporate governance (Gillan and Starks, 2000; Goranova and Ryan, 2014). In a typical scenario, an investor submits a proposal to appear in the firm’s annual proxy statement and for shareholder to vote on in the annual meeting. These resolutions can cover a wide range of governance matters, including repealing takeover defenses, altering shareholder voting rules, and reforming executive compensation. Many proxy resolutions prompt private negotiations, leading the sponsor to withdraw the resolution prior to the vote (Bauer et al., 2015). However, when private negotiations fail, or parties have been particularly intransigent, proposals can escalate into contentious engagements (Gantchev, 2013; McCahery et al., 2016). In recent years, shareholder resolutions have become more effective at prompting governance reforms (Ertimur et al., 2010). Although shareholder resolutions are only advisory in nature, and firms are not obligated to adopt resolutions that pass a shareholder vote, managers and directors face reputational penalties, increased activism, and dismissal if they routinely ignore shareholder resolutions (Ertimur et al., 2010). In the corporate finance literature, shareholder proposals serve as a useful indicator of shareholder dissatisfaction and firms’ responsiveness to investors (Renneboog and Szilagyi, 2011).

As a context for investigating activist investor heterogeneity, shareholder resolutions are particularly useful. First, shareholder resolutions offer a low-cost avenue for shareholder engagement. Unlike more costly proxy battles or takeovers, shareholders are only required to hold a minimum of US$2000 in company shares to present a proposal. This low cost means that even minority owners can present resolutions and be heard. Second, proposals do not require private access or personal contact with company management. Although many institutional investors use their private back-channel communications to engage with portfolio firms, less powerful investors rarely have such access. Nevertheless, even large investors present resolutions if private negotiations are ineffective or managers remain intransigent (Gantchev, 2013). Finally, shareholder proposals are public and both the business media and other shareholders witness these confrontations. As a result, both managers and activists must manage public perceptions. Corporate managers often negotiate to have a resolution withdrawn in order to avoid public embarrassment (Bauer et al., 2015). Relatedly, public shaming, reputational penalties, and stock market reactions can determine the odds of success. In sum, shareholder resolutions offer a low-cost, widely available, and public means for shareholders to voice concerns in corporate governance, making it an ideal context to consider heterogeneity in shareholder activism.

Agency theory

Agency theory is the dominant theoretical perspective for research on shareholder activism and corporate governance (Dalton et al., 1998) and suggests that firms who eschew shareholder interests will attract greater scrutiny from investors (Gillan and Starks, 2007). In this formulation, investors (principles) must rely on monitoring and incentive alignment mechanisms in corporate governance to ensure that managers (their agents) will act in ways that serve investors’ interests. Agency theorists propose several internal corporate governance mechanisms to monitor managers and ensure that managers’ incentives are aligned with shareholder interests. These include electing an independent board of directors, maintaining an active takeover threat that keeps managers focused on share price, and performance contingent compensation (Jensen and Meckling, 1976).

As an external corporate governance mechanism, shareholder activism allows investors to voice their concerns if they believe that governance arrangements do not reflect their interests or managers have become too entrenched (Aguilera et al., 2015). In firms with shareholder-oriented corporate governance, investors will be more satisfied and less likely to engage in activism (Renneboog and Szilagyi, 2011). However, when activists become concerned that managers are eschewing shareholder interests, they may attempt to intervene. Ultimately, agency theory posits that shareholder activism gives investors a voice in corporate governance, helping to reduce managerial entrenchment.

Most research in this tradition suggests that corporate governance arrangements that entrench managers will attract greater shareholder activism. Evidence indicates that firms with abnormal CEO compensation, takeover defenses, and limited shareholder voting rights are more likely to be the target of shareholder resolutions (Ertimur et al., 2010; Goranova et al., 2017; Renneboog and Szilagyi, 2011). Conversely, mechanisms that align managers’ incentives with shareholders, like higher levels of CEO ownership and a stronger link between CEO pay and performance, reduce activism (Bizjak and Marquette, 1998; Ertimur et al., 2010). Unsurprisingly, some research also indicates that poor operating and financial performance increases activism (Ertimur et al., 2010; Goranova et al., 2017); however, this evidence is more mixed (Cai and Walkling, 2011; Ferri and Sandino, 2009).

Corporate opportunity structures

While agency theory largely focuses on how performance and corporate governance characteristics attract activism, it is also likely that other contextual factors play an important role in determining when and where activism is likely to arise. We borrow from research on social movements for insight into how certain contextual factors operate. Social movement scholars have long acknowledged that social movement activists must often decide whether to target particularly deviant firms, with particularly poor social and environmental performance, or target firms where activism is more likely to succeed and help shape broader social norms. The “corporate opportunity structure” refers to the “attributes of individual firms that make them more (or less) attractive as activist targets” (Briscoe et al., 2014: 1786). Importantly, these attributes are distinct from the characteristics that primarily attract activists’ concern, such as a poor social or environmental record. While social movement activists primarily focus on reforming social or environmental behaviors, the corporate opportunity structure refers to the other contextual characteristics that make particular firms attractive targets. As Briscoe et al. (2014) argue, as activists “consider mobilizing to press their demands against a given company, they must calculate whether the effort and risk is likely to pay off” (p. 1878). When and where the odds are more favorable, companies are likely to be targeted (Soule, 2012). Organizational scholars have identified a number of dimensions that make firms more attractive targets, including top managers’ political ideologies (Briscoe et al., 2014), the firm’s visibility in the corporate community (Rowley and Moldoveanu, 2003), and the potential for threatening the firm’s reputation (Bartley and Child, 2011; King, 2008).

Although the corporate opportunity structure concept was originally developed to describe how social movement activists select target firms, we borrow this concept to theorize about how activist investors incorporate ideas about firms’ relative vulnerability into their activism. Clearly, activist investors are distinct from social movement activists, given the prevalence of shareholder value norms in the United States. Nevertheless, firms vary in their vulnerability to activist investors’ demands. We argue that, like social movement activists, activist investors are sensitive to contextual factors that help determine whether activism efforts are likely to pay off and have broader effects. We delineate three firm characteristics that, we argue, comprise components of the corporate opportunity structure in shareholder activism: visibility, reputation, and status.

First, highly visible firms are particularly likely to attract activists’ scrutiny for a number of reasons. More visible firms are those that are widely followed by relevant audiences, including market analysts, media, peer firms, and investors. More visible firms often attract greater scrutiny from relevant audiences, increasing firms’ susceptibility to institutional pressures (Okhmatovskiy and David, 2011). Targeting highly visible firms may allow activists to capture greater attention from the public and business press, thereby increasing pressure to conform to activist demands (Marquis et al., 2016). Activists may seek to use this attention to gather greater shareholder votes or exert public pressure on the firm, increasing the chances of success (King and Soule, 2007). Visible activism can also reach broader audiences, magnifying an activist’s ability to shape societal norms beyond the targeted firm. Successful reforms at a high-profile firm are more likely to trigger spillover effects where non-targeted firms preemptively adopt reforms (Brandes et al., 2008; Rowley and Moldoveanu, 2003). In general, visibility allows an activist to leverage public scrutiny in the absence of alternative sources of pressure.

Second, corporate reputation can be a powerful magnet of attracting activists’ attention (King, 2008: 409). Reputation refers to an informal signal of a firm’s quality that outside audiences, such as consumers or investors, use when making evaluations (Chandler et al., 2013; Sorenson, 2014). Firms who have established reputations for strong quality and superior performance rely on these signals to distinguish themselves from competitors. As such, reputation offers an important source of competitive advantage. Although positive reputations may dissuade scrutiny, activists may seek to threaten a firm’s reputation as a means of exerting greater pressure. For example, Bartley and Child (2014) argue that firms with greater reputation are more “shamable” than others, arguing that firms’ “deep investments in image, reputations, and social standing can quickly be tarnished” in the spotlight (p. 662). When a firm’s competitive advantage rests on a strong reputation, threatening that reputation can be a powerful lever for activists (McDonnell and King, 2013).

Finally, status may attract activists’ attention. Status and reputation are similar, in that both serve as informal signals for external audiences (Podolny, 2005; Sorenson, 2014). However, unlike reputation, status stems from a firm’s relative social position in a field and is valuable precisely because of its scarcity. Whereas reputation serves as a signal for quality, status is valued in its own right as a marker of distinction and social rank (Chandler et al., 2013; Sorenson, 2014; Washington and Zajac, 2005). Status can also serve as a prominent dimension in the corporate opportunity structure for two reasons. First, although status can confer a “halo-effect” in audiences’ evaluations, high-status actors tend to attract greater scrutiny, making them attractive targets of denigration (Hahl and Zuckerman, 2014; Kovács and Sharkey, 2014). As a result, high-status actors often experience harsher reactions when they are viewed as deviant (McDonnell and King, 2017). Second, targeting a high-status firm may help an activist gain prominence. Just as status “leaks” across network ties (Podolny, 2005), targeting high-status firms can allow an activist to establish themselves as a prominent shareholder rights advocate, willing to take on major players in the field.

Similar to social movement tactics like boycotts and protests, shareholder activism often aims to identify and publicize firms that violate prevailing norms of corporate governance and shareholder value maximization. Activists’ claims about excessive CEO pay, unresponsive boards, or excessive managerial entrenchment can provoke public image threats, particularly among financial analysts and investors. Shareholder activism rests on drawing attention and sympathy from other shareholders in order to build supportive voting blocs, leverage pressure, and exert penalties through financial market reactions (Ertimur et al., 2010). Consequently, activists may be more successful in achieving corporate governance reforms if they can attract attention from the media, financial market analysts, and other investors.

Integrating agency theory and corporate opportunity structure

As noted earlier, given limited time and resources, activist investors must often decide whether to target firms who have greater performance and agency problems or firms where visibility, reputation, and status support activists’ goals. Drawing on research on investor heterogeneity (Desender et al., 2016; Goranova et al., 2017), we argue that the extent to which activists focus on agency problems or rely on the corporate opportunity structure is likely to vary across distinct shareholder groups. On the one hand, powerful investors are best able to press their interests and engage with firms through their sizable portfolios. On the other hand, the corporate opportunity structure is likely to be especially important for activist groups that lack powerful means of influencing an organization. More marginal activist groups tend to favor particularly aggressive and innovative tactics (Bearman and Everett, 1993; Wang and Soule, 2016). However, to be clear, we do not claim that less powerful investors completely eschew these agency concerns. Rather, compared to powerful activists, they will be more likely to press for governance reforms when the opportunity structure is conducive. In other words, an activist’s power shapes how they select corporate targets.

In this article, we focus on the three most prolific groups in corporate governance activism: institutional investors (investment and pension funds), unions, and individual retail investors. We chose these groups for theoretical and empirical focus because they capture the bulk of the variation in activist power and it is most clear how they use activism to advance shareholder interests. Research shows that these activist groups vary in terms of portfolio size and power, as well as voting support, implementation, and success (Gillan and Starks, 2000; Goranova and Ryan, 2014). In the following sections, we discuss each of these investor groups in turn, outlining their varying levels of power and predictions for activism.

Institutional investors

Given their size, expertise, and ownership concentrations, large institutional investors, including public pensions and other investment funds, are the most powerful activist investors. Institutional investor ownership concentration has grown extensively in recent years, affording them considerable power over managers at the firms where they invest (Davis, 2009). Institutional investor concentration helped institutionalize shareholder-friendly corporate governance norms (Davis and Thompson, 1994), and their activism typically draws greater voting support and is more successful (Ertimur et al., 2010). Most institutional investors extend their power even further by participating in coordinating institutions, such as the Council of Institutional Investors, that advance their collective interests (Ward et al., 2009). Given their size and expertise, researchers generally view institutional investors as more effective governance monitors than other classes of investors (Connelly et al., 2010; McNulty and Nordberg, 2016). In general, there is little question that institutional investors wield greater power than other types of investors in the contemporary context of concentrated financial intermediation (Davis, 2009).

Given their power, institutional investors can be reasonably sure that managers and other shareholders will respond to their demands. We argue that institutional investors are more likely than other groups of activists to conform to traditional agency theoretic predictions, selecting targets with entrenched managers and poor performance. In addition, institutional investors have a clear incentive to focus on reforming governance and performance concerns, even in the absence of a favorable opportunity structure, due to the potential for sizable returns and strong odds of success. Based on these arguments, we predict that entrenched managers and poor performance attract greater attention from institutional investors.

Hypothesis 1a. Compared to less powerful investors (individuals and unions), institutional investors (pensions and investment funds) are more likely to target firms with entrenched managers.

Hypothesis 1b. Compared to less powerful investors (individuals and unions), institutional investors (pensions and investment funds) are more likely to target firms with poor performance.

Individual investors

Individual retail investors wield considerably less power than institutional investors. Individual activists typically own very small ownership stakes and rarely have access to management or governance expertise comparable to institutional investors. Individual activists are commonly dismissed as “gadflies,” or small irritants that distract from legitimate matters—for instance, in 2014 four companies sued John Chevedden and attempted to block his resolutions from appearing in their proxy materials, arguing that he “abuses the proxy process” with wasteful distractions (Ackerman, 2014). Individual-sponsored resolutions rarely pass a shareholder vote and are viewed skeptically by many observers (Renneboog and Szilagyi, 2011).

Nevertheless, despite their limited power and scant odds of success, individual investors are very prolific, regularly sponsoring the majority of all resolutions targeting public firms (Renneboog and Szilagyi, 2011).

From an agency theory perspective, it is somewhat unclear why these investors are such prolific activists or what drives their target selection, given that they stand to earn negligible returns from their activism. Some scholars propose that individual activists are more motivated by ideological concerns or use activism as a means of identity expression (Rowley and Moldoveanu, 2003). Critics suggest that individual activists are “annoying attention seekers,” more interested in increasing their own notoriety and fame (Duhigg, 2007; Solomon, 2014). For instance, Evelyn Davis, a very prolific activist investor, has sponsored several proposals a year targeting very prominent firms, like IBM, but only stood to earn negligible returns from her small ownership stakes. It turned out that Mrs Davis was earning an income of up to US$600,000 per year selling copies of a newsletter based on her notoriety as an activist investor (Duhigg, 2007). It seems clear that such motivations favor targeting highly visible and prominent corporations.

In other cases, individual activists appear to recognize how a firm’s visibility aids their activism efforts. One activist told a reporter that the attention has given him “entrée into a world [he] otherwise couldn’t access” (Duhigg, 2007). John Chevedden, another prolific activist, clearly recognizes the value of visibility and the potential for reputational penalties, telling a reporter that his efforts put “management on its toes and prevents it from lapsing into complacency” (Solomon, 2014). Individual activists recognize that they typically would not have the power or resources to mount a salient activism threat against corporate targets. However, by leveraging public scrutiny, individual activists may be able to capture corporate executives’ attention and press for reforms that corporations would otherwise ignore.

As discussed above, visibility, reputation, and status are distinct theoretical constructs, yet we expect that they will operate in similar ways: less powerful investors may target firms with greater visibility, more positive reputation, and higher status because these contextual factors make firms more conducive targets. While agency theory argues that activists are likely to be somewhat homogeneous in their concerns about firm performance and corporate governance, we suggest that individual investors are likely to be more sensitive to a corporate target’s vulnerability and visibility. Targeting more visible firms allows activists to draw greater visibility to their activism efforts. Similarly, firms with a positive reputation in the corporate community may be more vulnerable to reputational threats via activism (Bartley and Child, 2014). Finally, higher status firms attract greater scrutiny and harsher penalties from external audiences (McDonnell and King, 2017), making them attractive targets for activists with limited power. In the absence of formal power, individual activists may seek to leverage public scrutiny by targeting firms that attract a wider audience.

Hypothesis 2a. Compared to more powerful activists (unions and institutional investors), individual investors are more likely to target firms with greater visibility.

Hypothesis 2b. Compared to more powerful activists (unions and institutional investors), individual investors are more likely to target firms with positive reputations.

Hypothesis 2c. Compared to more powerful activists (unions and institutional investors), individual investors are more likely to target firms with greater status.

Unions

Shareholder activism by union pension funds has drawn comparatively less research attention but is no less important. As compared to institutional investors like public pensions and private mutual funds, union pension funds are much smaller and less powerful. In recent years, unions have increasingly presented shareholder resolutions addressing corporate governance topics. Many observers suggest that union shareholder activism is motivated by political goals, rather than agency concerns (Jacoby, 2008; Matsusaka et al., 2016). For instance, some critics argue that unions use shareholder proxy resolutions as part of contract negotiation or organizing strategy (Agrawal, 2012; Jacoby, 2008; Matsusaka et al., 2016). However, as compared to individual investors, union pension funds are more powerful because of their greater size and organizational capacity. Surprisingly, unions’ proxy resolutions typically win considerable voting support from other investors, suggesting that union resolutions support prevailing corporate governance norms (Ertimur et al., 2010; Thomas and Martin, 1998).

Therefore, we argue that labor unions occupy a middle ground between institutional investors and individuals. In deciding between targeting firms with greater agency problems or more vulnerable positions in the opportunity structure, labor unions aim to strike a balance. Compared to individual investors, unions exercise greater power allowing them to act as external governance monitors focused on reforming managerial entrenchment performance. However, as compared to other institutional investors, unions wield less power, making them more strategic in selecting targets where they can leverage the corporate opportunity structure. Thus, we argue that unions may not go after firms with the worst agency problems (as institutional investors do) but are more willing to take on these firms than individuals. However, unions are more similar to individuals in their reliance on the corporate opportunity structure.

Hypothesis 3a. Compared to less powerful investors (individuals), unions are more likely to target entrenched managers and poorly performing firms.

Hypothesis 3b. Compared to more powerful investors (institutional investors), unions are more likely to target visible, reputable, and high-status firms.

Data and methods

The analysis focuses on firm and activist antecedents to shareholder activism targeting large and midsized public corporations between 2005 and 2013. The sample comes from Institutional Shareholder Services (ISS) data on shareholder proxy resolutions targeting S&P 1500 firms and includes resolutions that came to a vote at the annual meeting as well as those that were omitted from the proxy materials and were withdrawn by the sponsoring shareholders. 2 Because resolutions are highly correlated with firm size, the S&P 1500 sample captures a substantial majority of shareholder resolutions in the United States. The ISS data include the identities of the target firm as well as each of the sponsoring shareholders, or proponents. Our analytic sample includes all firms and activists in the ISS dataset that were involved in at least one proxy resolution between 2006 and 2013; the 2005 wave provides the prior year’s activism control for the first wave in 2006 to facilitate our lagged design.

We analyze annual panels of bipartite networks constructed from all shareholder resolutions in the ISS data designed to reflect shareholder activisms’ relational structure. This approach offers an empirically tractable method of incorporating activist identities and firm traits into a single modeling framework. In a bipartite network, nodes are partitioned into two distinct classes—in our case, firms and activist investors. Bipartite networks have long been used to reflect the relational structure of social systems where two entities are connected through their shared affiliations at some event or setting—such as socialites attending the same parties (Davis et al., 1941) or corporate directors serving on the same boards (Benton, 2016; Koskinen and Edling, 2012). Ties are allowed between nodes in different partitions but not between nodes in the same partition; that is, an activist can target a firm but not another activist.

More formally, for a set of n activists and m firms, we define a set of variables

To construct our networks, we used the following procedure. First, we expanded the proxy resolution list from ISS so that each sponsor–firm pair represents a unique observation and resolutions with multiple cosponsors can be represented. 4 Second, we hand-checked the sponsor identity information provided in the ISS data to ensure consistent spellings and assigned unique identifying numbers to each activist in the sample. Third, we expanded the panels so that firms (and activists) that did not receive (or submit) a resolution during a given year are represented in the matrix as isolates, indicating the absence of activism. Finally, we matched the firm observations with data from business databases (described below) and adjusted the network panels to reflect firms that join or leave the sample during the observation period—firms may join the sample if they go public or are spun off from another firm, while firms may leave the sample if they delist their securities, go bankrupt, or are acquired by another firm. The final sample includes 522 activist investors sponsoring 4329 resolutions targeting 1243 firms. The sample includes 7480 firm-year observations, including firms that were targeted and not targeted in a given year.

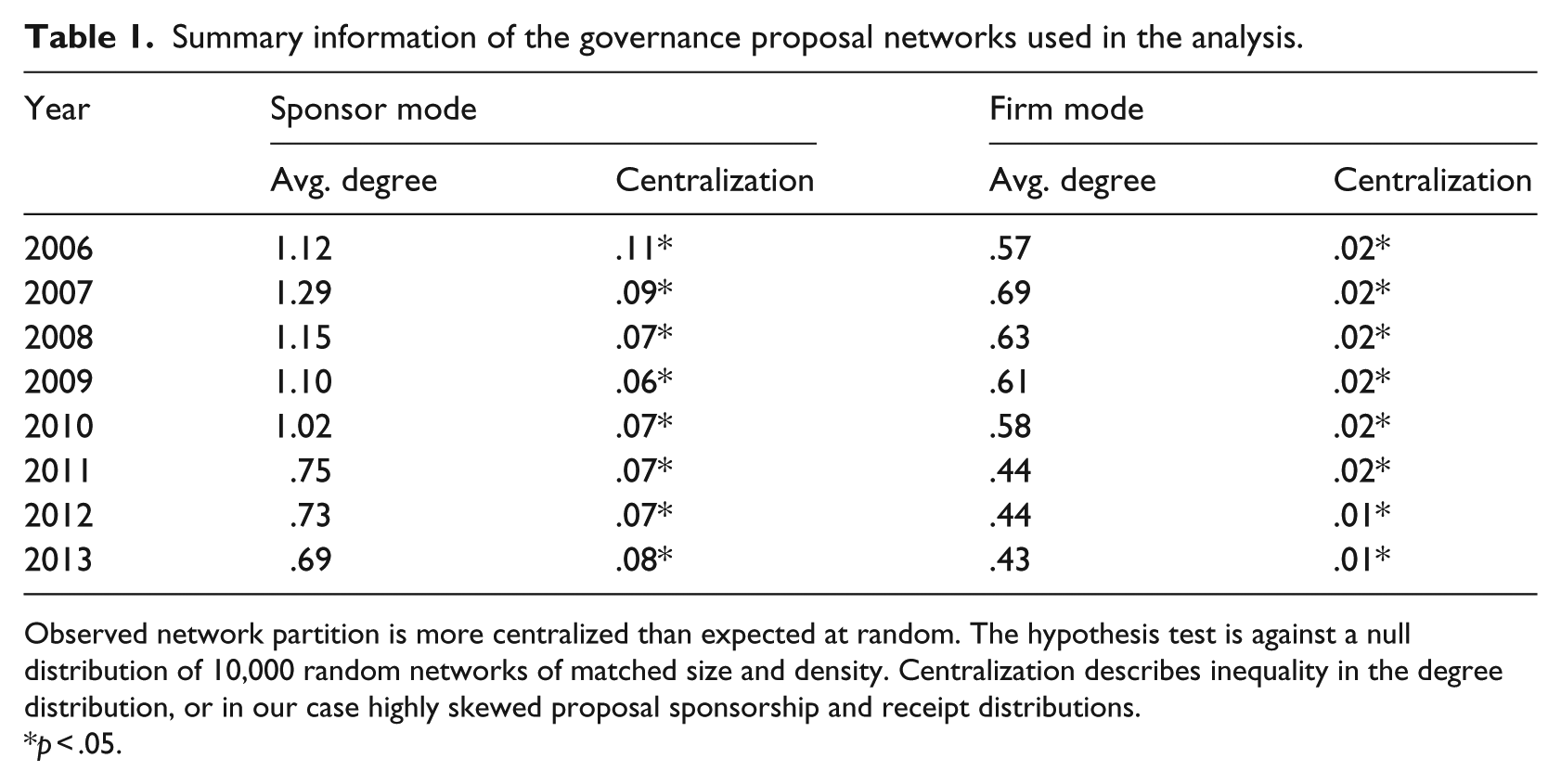

Table 1 presents summary information for each of the annual activism networks. Average degree centrality refers to the average number of ties (resolutions) for nodes in each partition of the network. Centralization describes the extent to which the network has a skewed degree distribution, where a small handful of firms and activists are involved in a disproportionate number of proxy resolutions. 5 Both firm and activist partitions for all observed networks are more highly centralized than expected if ties were random, suggesting that activism disproportionately involves a smaller number of firms and activists. This is consistent with other evidence that a small group of activists and firms are involved in a disproportionate number of proxy resolutions (Copland and O’Keefe, 2015). This suggests that (1) only a handful of activists specialize in sponsoring a large number of proxy resolutions across corporate America and (2) while most firms receive only a small number of proxy resolutions, a small group is perceived as highly ignominious by the activist community and receives a disproportionate number of resolutions (Benton and You, 2017).

Summary information of the governance proposal networks used in the analysis.

Observed network partition is more centralized than expected at random. The hypothesis test is against a null distribution of 10,000 random networks of matched size and density. Centralization describes inequality in the degree distribution, or in our case highly skewed proposal sponsorship and receipt distributions.

p < .05.

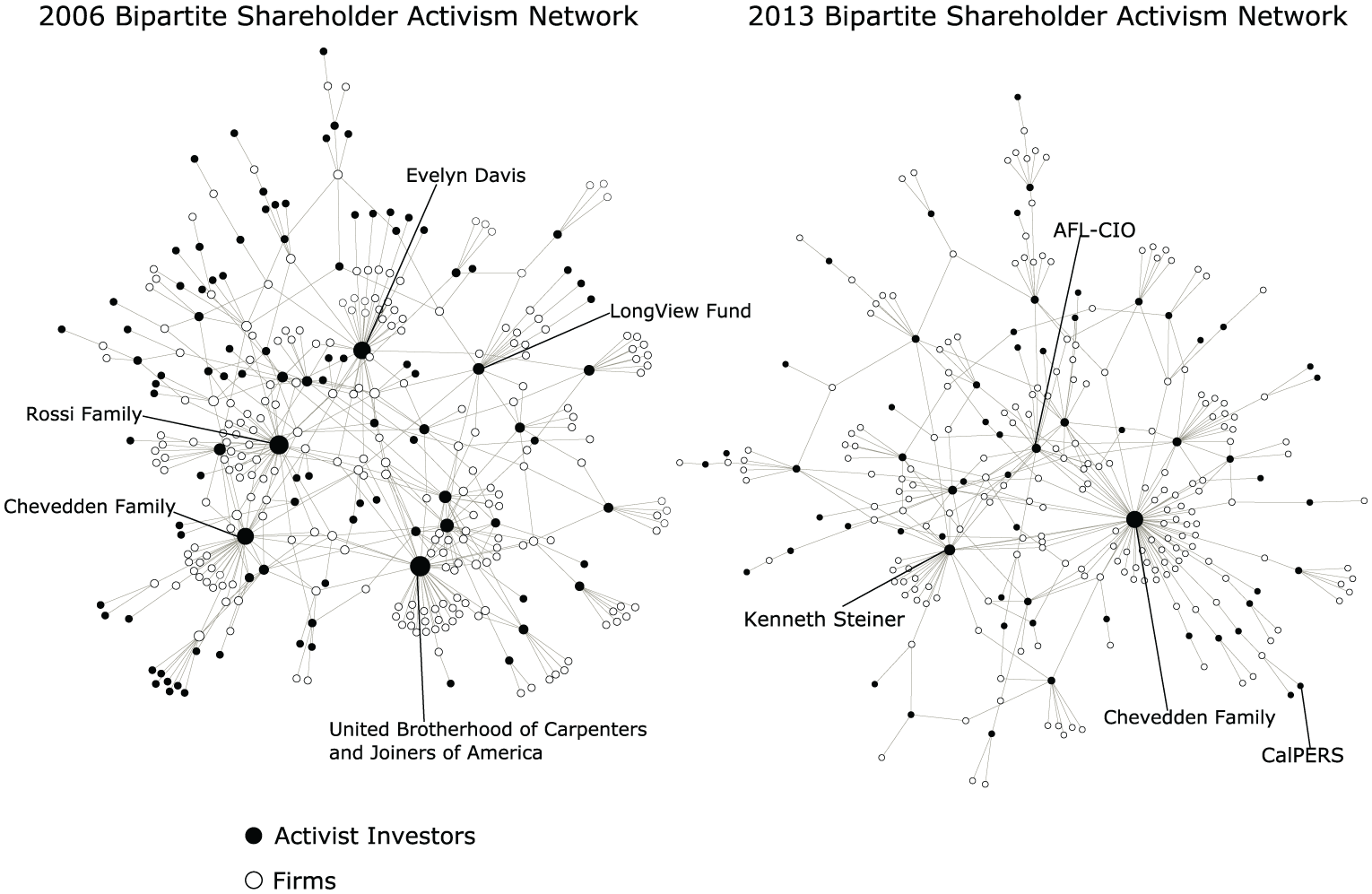

Figure 1 presents the main components (excluding isolates) from the 2006 and 2013 shareholder activism networks. The black nodes represent activist investors (a few are labeled) and the white nodes represent firms. Nodes are sized by their degree centrality, or the number of resolutions they sponsor/receive. Several elements are immediately apparent. First, a handful of activists account for most activism and they target a wide array of firms, many of which are not targeted by any other activists. Second, the most active investors are individuals and unions and these investors are clearly the most visible in the field. With a more formal network modeling approach, we are able to examine how these activists’ targeting decisions depend on the traits and characteristics of the firms in the field.

Shareholder activism networks, main components from 2006 and 2013.

Measures

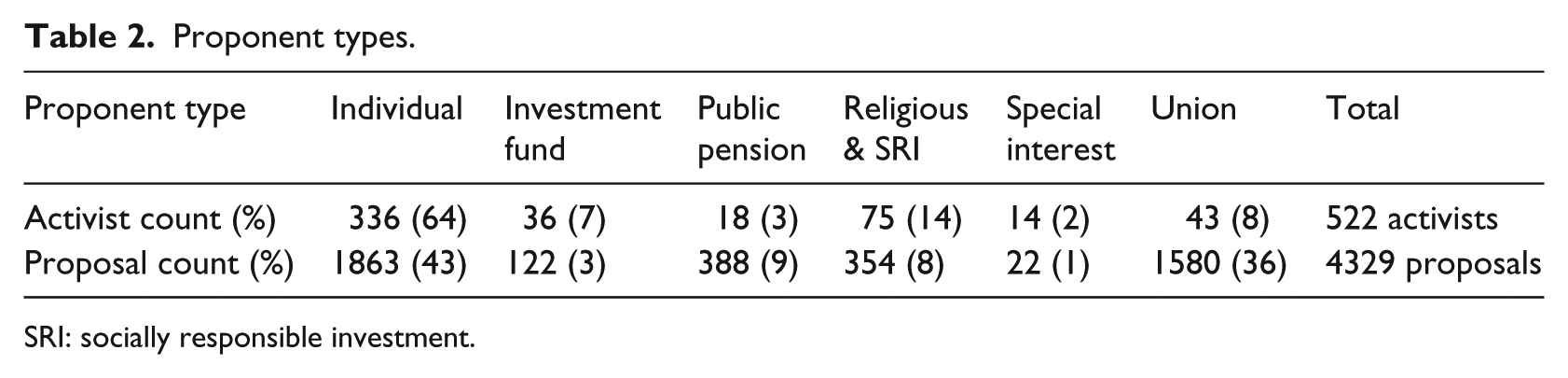

Our analysis includes a number of activist and firm traits. First, activists are categorized according to the ISS labeling scheme and include individual investors (e.g. John Chevedden), investment funds (e.g. mutual funds), public pensions (e.g. CalPERS, NYCERS), religious and socially responsible investment (SRI) funds, special interests, and union affiliated pension funds (e.g. AFL-CIO, Carpenters and Joiners). Our theoretical model focuses primarily on activism from public pensions, investment funds, unions, and individuals. These categories capture most corporate governance–related resolutions and serve as a common indicator of activist power and salience in the literature (Goranova and Ryan, 2014). 6 Table 2 summarizes how the activists and resolutions are distributed across these distinct types.

Proponent types.

SRI: socially responsible investment.

We are primarily interested in how these activist identities interact with target firm characteristics. Our primary independent variables capture firm-level agency theoretic traits and the corporate opportunity structure. First, we capture corporate governance dimensions using the entrenchment index (e-index), drawn from ISS, as a measure of corporate governance. The e-index includes staggered boards, limits to shareholder bylaw amendments, poison-pills, golden parachutes, and supermajority vote requirements for mergers and charter amendments. The e-index is arranged so that low scores indicate more shareholder friendly corporate governance (Bebchuk et al., 2009). 7 The e-index has been widely used in research on corporate governance and shareholder activism and prior work shows that higher scores on the e-index (more entrenched management) is associated with increased investor activism (Renneboog and Szilagyi, 2011). Second, agency theory emphasizes activists’ focus on firm performance, which we measure as industry-adjusted return-on-assets (ROA) and calculate using Compustat.

Next, we introduce three indicators designed to capture firms’ position in the corporate opportunity structure, measured as firms’ visibility, reputation, and status. Visibility is measured as firm size, defined as logged total assets drawn from Compustat. We anticipate that larger firms make more attractive targets because of their greater visibility in the corporate community (Rehbein et al., 2004). Following prior work in strategy and organization research (Basdeo et al., 2006; Chandler et al., 2013; Staw and Epstein, 2000), we measure firm reputation using Fortune Magazine’s list of the 50 Most Admired Companies. We specify a dummy variable for whether or not the firm appeared in the Fortune list in the corresponding year. Fortune Magazine constructs this annual list by surveying members of the business community about firms that they admire. The measure is the most widely used general indicator of corporate reputation in organizational research. 8 Finally, as an indicator for corporate status, we include the firm’s eigenvector centrality in the S&P 1500 board interlock network, the interfirm network of overlapping board appointments. Eigenvector centrality captures the prominence or importance of each node in a network. Rather than simply measuring the count of network ties (degree centrality), eigenvector centrality captures the extent to which a firm is interlocked with other highly interlocked firms (Bonacich, 1987). Centrality is a useful indicator of corporate status because it captures the firm’s position in the field of intercorporate relations (Sorenson, 2014) and has been used in prior research on corporate status (Chandler et al., 2013; Davis and Robbins, 2005). The interlock data are drawn from the ISS (formerly RiskMetrics) board rosters; networks are constructed using a name matching algorithm and extensive hand-checking. Eigenvector centrality is calculated using the igraph package in R.

Models include additional controls, including market-to-book ratio calculated from Compustat, and the size of the board of directors, and the proportion of outsiders on the board, calculated from ISS. As a final governance measure, we include an indicator of excessive CEO pay, calculated at the natural logarithm of the residual from an annual regression which regresses the log of total CEO compensation on total assets and industry dummies. We include three measures of the firm’s ownership structure; each drawn from Thomson Reuters and supplementary resources. Institutional investor ownership concentration is defined as the Hirschman–Herfindahl index and captures the extent to which the firms’ outstanding shares are held by concentrated block owners. We also control for effects associated with ownership by institutional investors with distinct investment strategies that can affect corporate strategy. Whereas transient institutional investors generally buy and sell broad portfolios based on a strategy of short-term returns, dedicated institutional investors tend to own larger long-term stakes in a few firms (Bushee, 1998, 2004). We use Bushee’s (1998) institutional investor categorization scheme and control for the percent of outstanding shares owned by transient and dedicated institutional investors. 9 Finally, because union activism may be related to union organizing efforts, we control for union membership density in firms’ primary industry using data from the Current Population Survey. 10

Finally, our models control for several endogenous network effects which capture whether and how activists make targeting decisions in the context of other activists (cf. Benton and You, 2017). When a given activist targets a particular firm, this event is likely to be observed by other activists in the field and may shape their own targeting decisions. For instance, activists may seek to target firms in common with other activists. Controlling for these endogenous effects allows us to isolate the role of activist identity from field-level dynamics that may affect targeting decisions. In social network modeling research, endogenous network effects capture self-organizing dynamics whereby actors form networks in the context of other network features (Lusher et al., 2013). We include controls for activity and ignominy, which capture the tendency for some activists and firms to be disproportionately involved in activism. Activity captures the extent to which some activists sponsor a disproportionate number of proposals. Similarly, ignominy captures the extent to which some firms are disproportionately targeted if activists tend to elect to “follow-the-trend” and match their targeting choices with the choices of other activists (Powell et al., 2005). Activity–ignominy assortativity captures the tendency for more active investors to disproportionately target highly targeted firms. Four-cycle closure captures the tendency for activists to cohere around a common set of firms and is the relevant closure effect for bipartite networks (Benton, 2016; Koskinen and Edling, 2012). Finally, homophilous targeting captures the tendency for activists to select common targets with similar activists. We discuss each of these endogenous network effects in Appendix 1. Although we present these endogenous network effects as controls, future research could profitably examine network dynamics in the activism field as a new line of research.

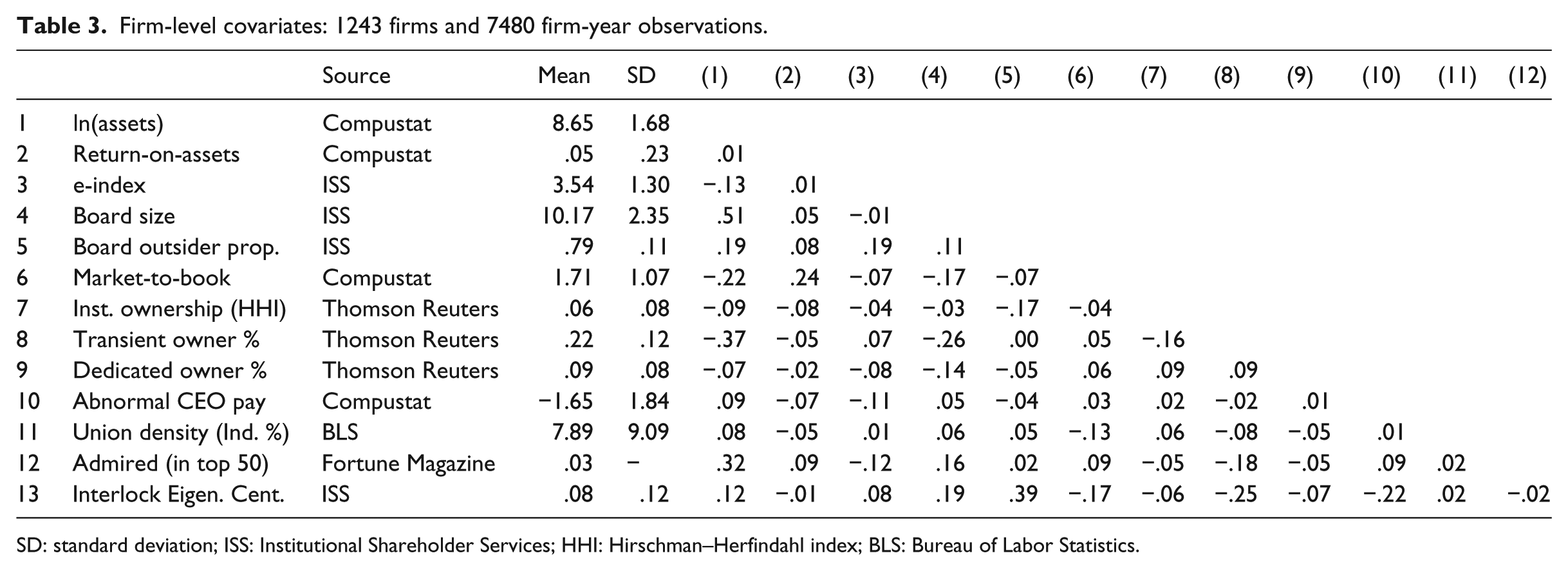

Table 3 presents summary statistics and correlations for each of the variables included in the analysis.

Firm-level covariates: 1243 firms and 7480 firm-year observations.

SD: standard deviation; ISS: Institutional Shareholder Services; HHI: Hirschman–Herfindahl index; BLS: Bureau of Labor Statistics.

Analytic strategy

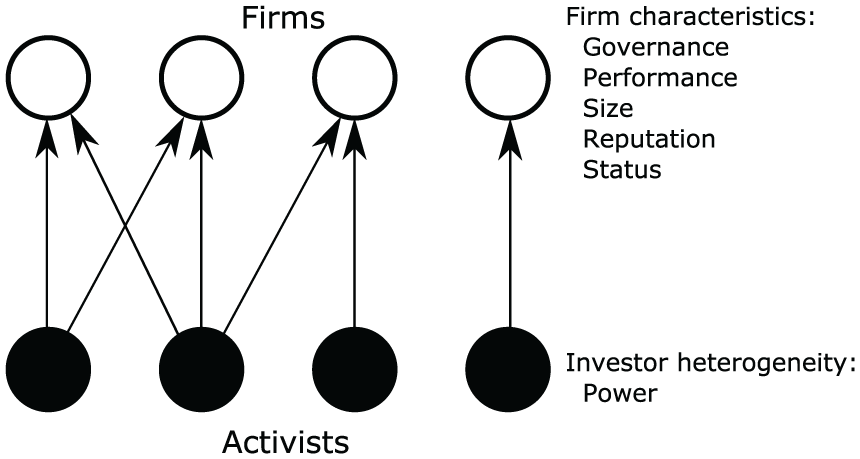

We are interested in examining how different types of activist investors, with different levels of power, select between (1) targeting firms with performance problems (low ROA) and agency problems (high e-index) and (2) targeting firms with greater visibility (large size), positive reputation (Fortune list), and higher status (interlock centrality). Our integrated theory focuses on the interplay between firm traits and activist identities and motivates a novel empirical approach that can model shareholder proposals as a function of both sponsor and target antecedents. Figure 2 presents a schematic representation of our bipartite network approach. Our modeling strategy involves predicting a resolution as a function of firm-level traits and activist type.

Shareholder activism schematic.

One possible approach might be to statistically model the presence or absence of a proxy resolution for all activist–firm dyads using a conventional logistic regression framework where the probability of an individual proxy resolution is modeled as a function of firm and activist covariates. However, this approach is empirically intractable for a few reasons. Network data such as these contain complex dependencies, as when the same activists and firms are involved in multiple resolutions, which renders traditional linear regression inappropriate as the data violate the regression assumption of independent observations (Snijders, 2011; Wasserman and Pattison, 1996). Analysts sometimes use complex random-effects specifications to condition out dependencies. However, this approach is generally not feasible for complex network data. An ideal approach would allow us to explicitly model these dependencies, rather than condition them out, as substantively interesting endogenous activism determinants that contribute to the structure of the network. These endogenous dynamics represent substantively important effects that are worth empirically exploring and controlling for (Goodreau et al., 2009).

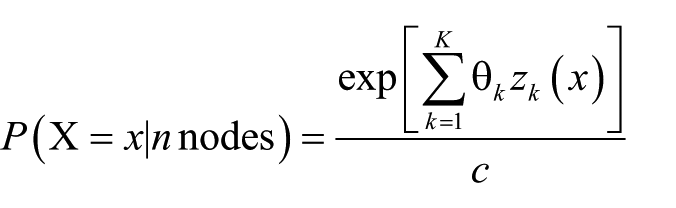

To resolve these problems, we use a class of statistical models for networks called exponential random graph models (ERGMs) and their temporal extension (TERGMs; Cranmer and Desmarais, 2011; Lusher et al., 2013; Robins et al., 2007). ERGMs (or p* models) are suitable for estimating statistical parameters predicting the probability of a tie (shareholder resolution) in a social network as a function of node traits (firms and activist characteristics) and endogenous dependencies (self-organizing dynamics). ERGMs have become popular in several disciplines, including management and organization studies (Kim et al., 2016; Lomi et al., 2013).

ERGMs estimate the conditional probability of observing a given network, x, as

This equation represents the probability that a random network X, with n nodes, has a specific realization, x, conditional on covariates, zk(x). Covariates are a vector of K network statistics calculated on network x. The network statistics are the configurations hypothesized to produce ties in the observed network and can include node characteristics, such as size, performance, and governance, and network configurations such as 4-cycles or ignominy.

Models include proponent type and several firm-level attributes (listed above) as predictors of whether the proponent or firm is involved in an activism event. We examine several interaction effects between activist identities and firm-level traits—these estimates reveal whether different types of investors prefer to target firms with distinct characteristics. Finally, the TERGM models include a dyadic indicator for tie stability—whether the sponsor targeted the firm in the prior year. Many investors sponsor proposals against the same firm year after year so it is important that we control for lagged tie stability. We follow all procedures for assessing model convergence and fit as outlined in the statistical networks literature and we find that the estimated model accurately reproduces structural features of the observed network in simulations.

Results

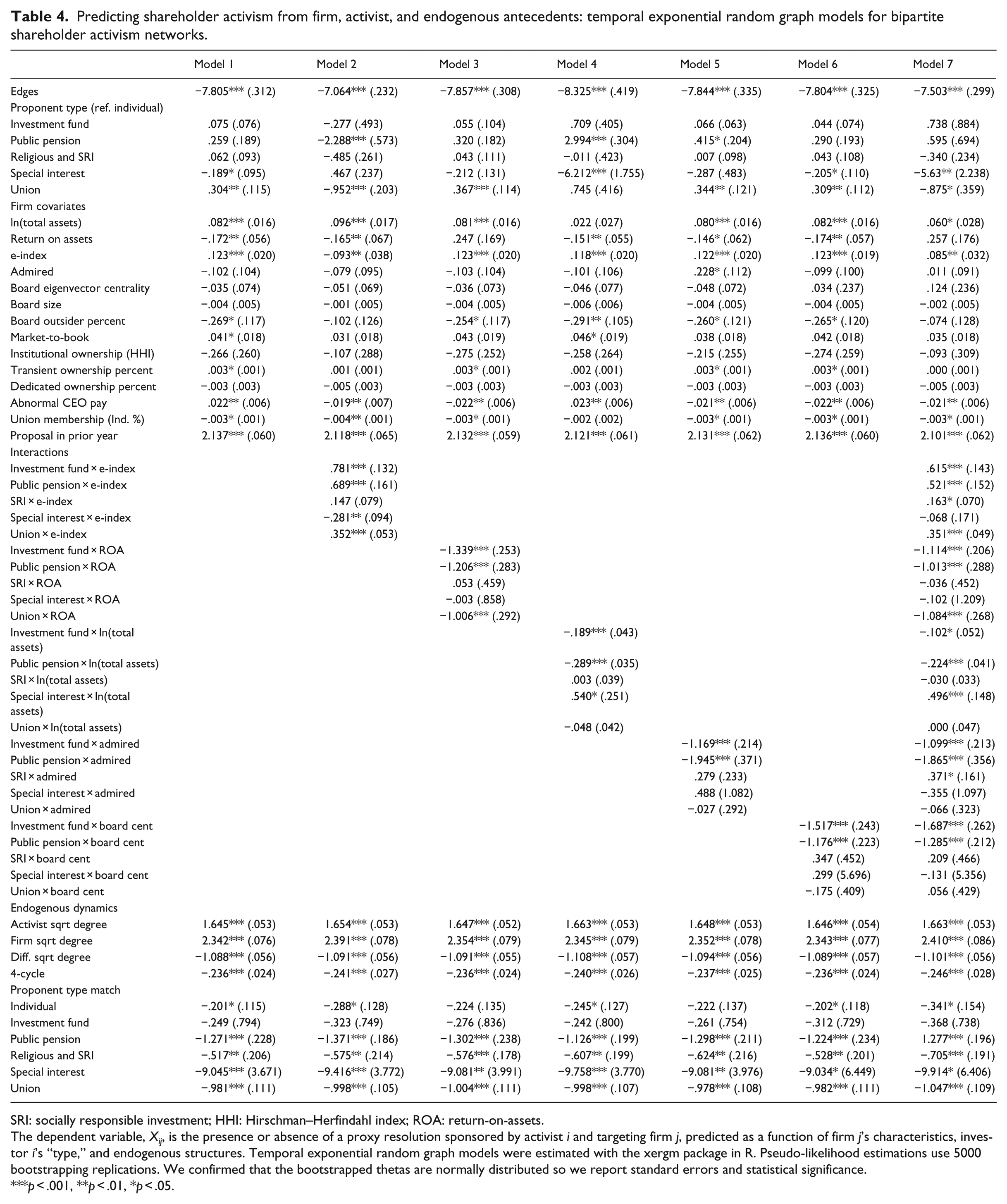

Table 4 presents results from TERGMs, predicting proxy resolutions as a function of firm traits, activist identities, and endogenous dynamics. Recall that the dependent variable in these models is the presence or absence of a proxy resolution in a given year, Xijt, sponsored by activist i targeting firm j in time point t. Predictors are defined as the exogenous attributes of activist i and firm j and network statistics capturing other resolutions involving i and j, which we conceptualize as endogenous dynamics (see Appendix 1). We discuss the results in the order presented above. For intuition, these are interpretable similar to a logistic regression where the dependent variable is the presence or absence of a resolution between a given activist–firm pair.

Predicting shareholder activism from firm, activist, and endogenous antecedents: temporal exponential random graph models for bipartite shareholder activism networks.

SRI: socially responsible investment; HHI: Hirschman–Herfindahl index; ROA: return-on-assets.

The dependent variable, Xij, is the presence or absence of a proxy resolution sponsored by activist i and targeting firm j, predicted as a function of firm j’s characteristics, investor i’s “type,” and endogenous structures. Temporal exponential random graph models were estimated with the xergm package in R. Pseudo-likelihood estimations use 5000 bootstrapping replications. We confirmed that the bootstrapped thetas are normally distributed so we report standard errors and statistical significance.

p < .001, **p < .01, *p < .05.

Model 1 presents the baseline model. The edge covariate controls for the baseline probability of a network tie, or resolution, and is almost always negative in ERGM analyses, indicating the relatively low probability of any one resolution involving a random activist–firm pair and the relatively low density of the networks. The proponent type covariates control for the baseline probability that each type of investor will be involved in a resolution. The positive parameter estimate for union proponents illustrates that unions sponsor a disproportionate number of resolutions, relative to the number of unions in the sample. 12

The estimates under the firm covariates heading capture the effects of firm antecedents on the probability of being targeted by a resolution. Results are largely consistent with prior theory and findings. Consistent with agency theory, better-performing firms (ROA) receive fewer shareholder resolutions, while firms with more entrenched managers (high e-index) receive more resolutions. We also find that larger firms attract more resolutions (total assets), consistent with the prediction that activists target more visible firms. Finally, we do not find a significant direct effect for reputation (admired) or status (board eigenvector centrality). Rather, as the results reveal, reputation and status matter only to specific activists.

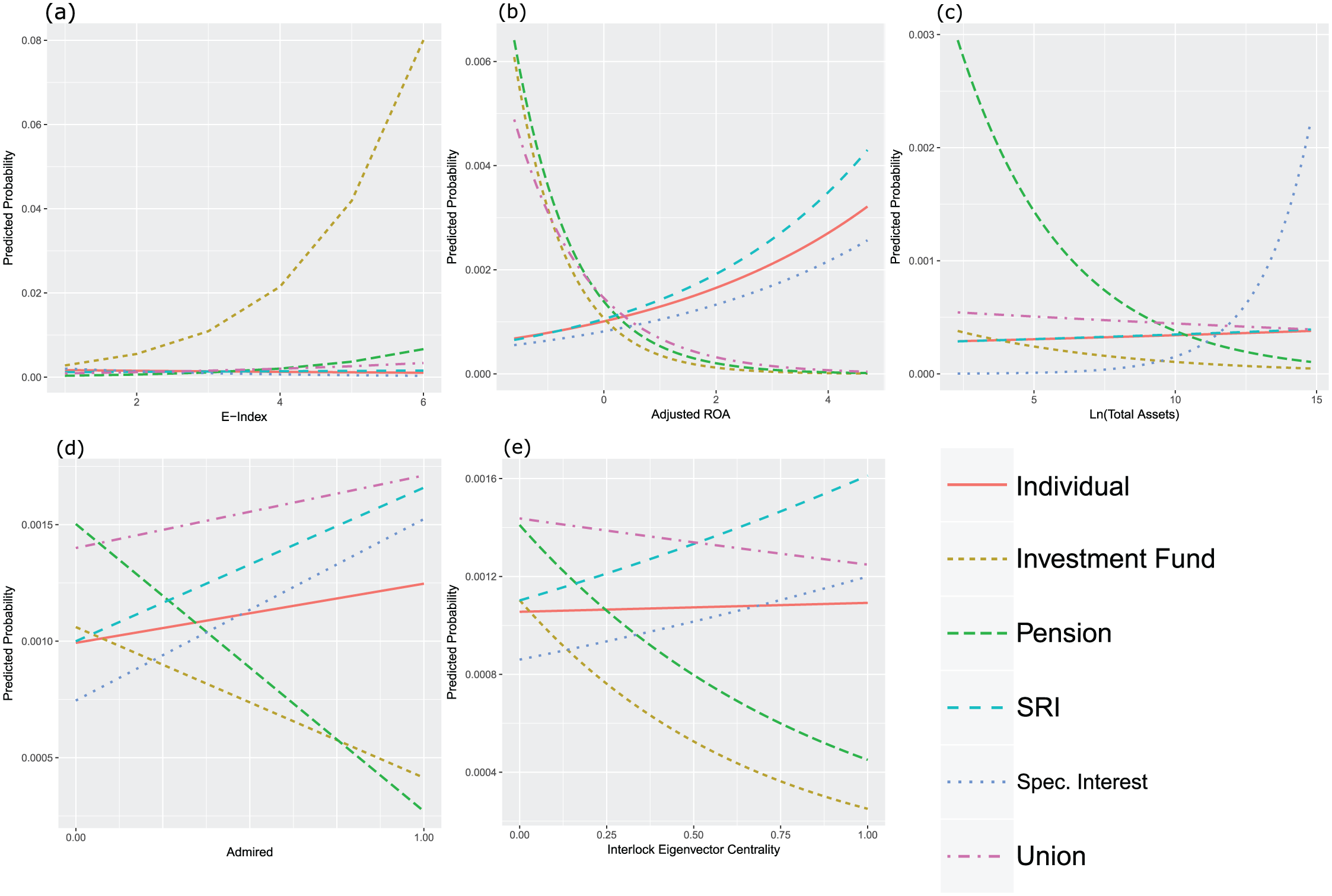

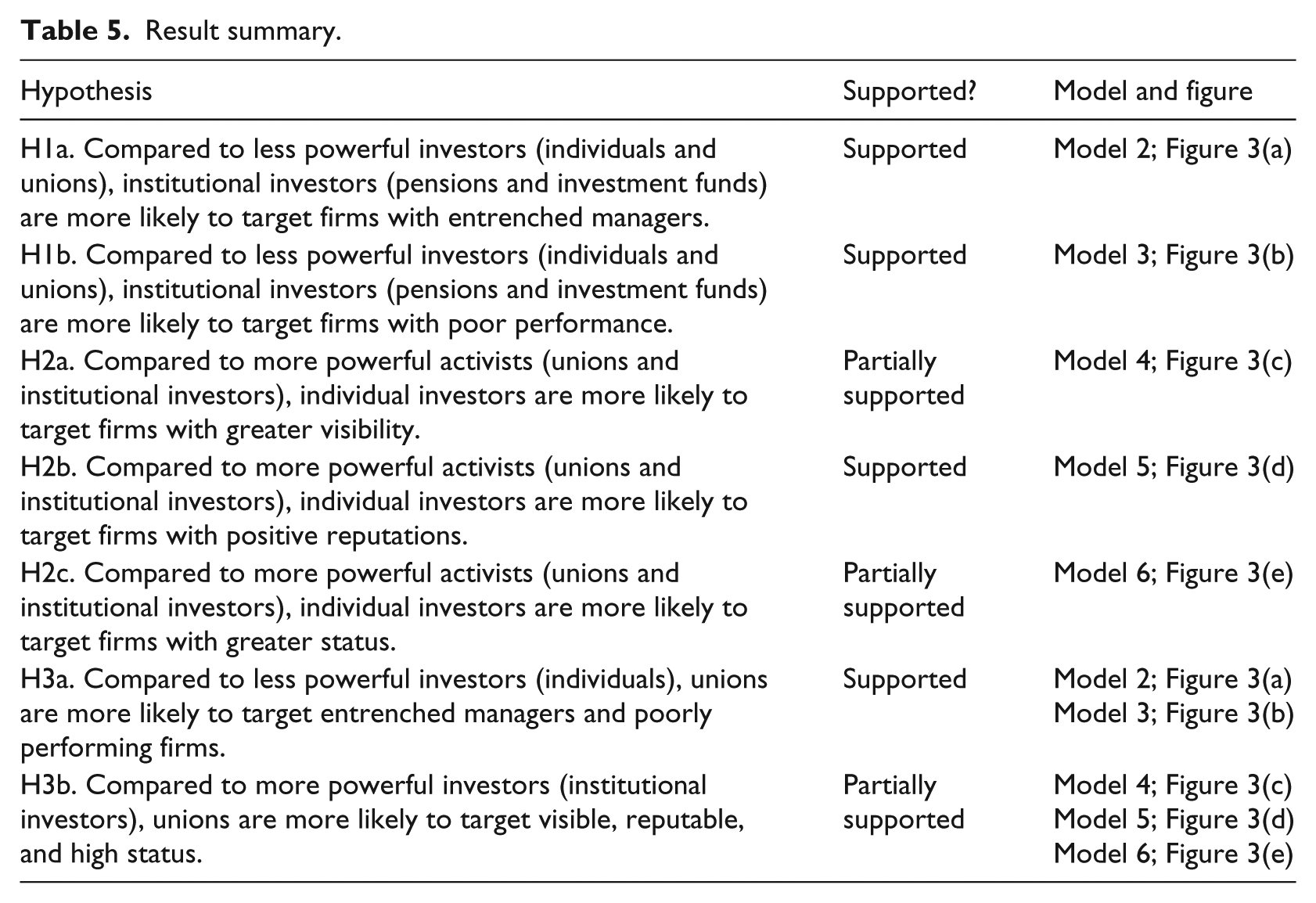

We now turn to a series of models that interact sponsor identity with firm covariates to test our ideas activist heterogeneity and varying levels of power. In Table 4, Models 2 through 6 interact sponsor type with firms’ e-index (governance), ROA (performance), total assets (our measure of visibility), Fortune’s admired list (reputation), and board interlock network eigenvector centrality (status), respectively. Individual investors, as the largest group, serve as the reference category throughout. The panels in Figure 3 plot the predicted probabilities from the interactions, assisting interpretation for investor heterogeneity and firm characteristics. For convenience of interpretation, Table 5 summarizes the main results for each of the seven hypotheses and indicates the model and figure panels that correspond to each hypothesis test.

Predicted probabilities from TERGM interaction effects: (a) e-index, (b) adjusted ROA, (c) ln(total assets), (d) most admired, and (e) interlock eigenvector.

Result summary.

First, we hypothesize that agency theoretic motivations are particularly important for more powerful institutional investors (investment funds and public pension funds), who have the power and resources necessary to act as effective and salient external governance monitors. Hypotheses 1a and 1b predict that, as compared to less powerful investors, institutional investors (pensions and investment funds) tend to target firms with entrenched managers and poor performance. Models 2 and 3 support these hypotheses. The interactions in Model 2 indicate that, as compared to individuals, both investment funds and pension funds tend to preferentially target firms with entrenched managers (high e-index). Both estimates are also significantly greater (p < .05) 13 than the corresponding estimate for union proposals. Thus, investment funds and public pensions are more likely than both individuals and unions to target firms with entrenched managers. Figure 3(a) plots the predicted probabilities from this model. In the plot, investment funds are considerably more likely to target high-e-index firms, as compared to other types of investors, while pension funds are slightly more likely to target high-e-index firms. Unions are also slightly more likely to target high-e-index firms, but this probability is lower than both investment funds and pensions. Taken together, investment funds, pensions, and unions are more likely to target firms with entrenched managers (H1a and H3a).

The interactions in Model 3 indicate that, as compared to individuals, both investment funds and public pensions preferentially target firms with low ROA. However, these estimates are not significantly different from unions. This suggests that investment funds and public pensions are more likely than individuals to target poorly performing firms, but are similar to unions in this preference. Figure 3(b) plots the interactions and shows that pension funds, investment funds, and unions are far more likely to target low-ROA firms while eschewing targeting high-ROA firms. Notably, individuals appear to be more likely to target high-ROA firms. Taken together, pensions, investment funds, and unions are more likely to target poorly performing firms (H1b and H3a).

Next, we draw on ideas about the “corporate opportunity structure” to argue that less powerful investors, particularly individuals and labor unions, are more likely to target firms that are highly visible, exhibit positive reputations, and have greater status. We argue that these characteristics can be leveraged to put public pressure on the firm and potentially yield greater results in the absence of investor power. We rely on firm size, Fortune’s “admired” ranking, and board interlock eigenvector centrality as indicators for these constructs. Model 4 examines the effect for logged total assets and reveals that, compared to individuals, investment funds and public pensions are less likely to target large firms (H2a). However, unions’ propensity to target larger firms is not significantly different from individuals but an additional significance test confirms that it is significantly more likely than institutional investors (p < .05; H3b). Figure 3(c) plots these effects and reveals a surprising pattern. Although unions and individuals are most likely to target larger firms (H2a and H3b), as compared to pensions and investment funds, much of this effect is due to the fact that institutional investors are highly unlikely to target large firms. This suggests that while individual investors and unions are not dissuaded from targeting more visible firms, institutional investors eschew larger targets. We return to this in the section “Discussion and conclusion.”

Model 5 examines activists’ heterogeneity in targeting firms with greater reputation, as captured using Fortune’s list of admired companies. The model indicates that, as compared to individuals, investment funds and pensions are less likely to target high-reputation companies (H2b). Again, a significance test confirms that unions are also more likely than institutional investors to target admired companies and this difference is statistically significant (p < .05; H3b). Figure 3(d) plots the predicted probabilities. While investment funds and pensions are unlikely to target admired companies, individuals and unions are more likely to target these firms. Interestingly, similar to the visibility effect above, institutional investors largely eschew more reputable targets. However, we do observe that individual and union targeting increases with firm reputation. Taken together, individual activists and labor unions are more likely than powerful investors to target admired companies (H2b and H3b).

We also test the effects of corporate status using the firm’s eigenvector centrality in the board interlock network. Model 6 estimates these effects and indicates that, as compared to individuals, investment funds and public pensions are less likely to target central firms (H2c). Unions are also significantly more likely than institutional investors to target central firms (p < .05), but unions are not significantly different from individuals in this regard (H3b). Figure 3(e) plots these effects and reveals that individuals and unions are more likely than pensions and investment funds to target high-status firms. However, as with the visibility effect above, the figure reveals that much of this effect is due to the fact that institutional investors are highly unlikely to target high-status firms. While individuals and unions are not substantially dissuaded from targeting high-status firms, institutional investors largely eschew high-status targets. We contextualize these results below.

While Models 2 through 6 present these activist × firm trait interactions separately, Model 7 presents a fully saturated model with all of the interactions entered simultaneously. The results from Model 7 are generally consistent with the results from the staggered models, indicating that activist investors exhibit considerable heterogeneity in their attention to various firm traits. Consistent with our theory, firms vary in terms of how they select corporate targets with greater agency problems or in more vulnerable positions in the opportunity structure.

Discussion and conclusion

In this article, we set out to examine heterogeneity in shareholder activism and integrate insights from agency theory and social movement research to understand how activist investors select targets (Goranova et al., 2017). While agency theory predicts that firms with entrenched managers and poor performance will attract greater activism (Renneboog and Szilagyi, 2011), social movement researchers note that activists often select targets of opportunity, where their activism efforts will have the greatest impact (Briscoe et al., 2014). Integrating these ideas, we argue that activist investors must often decide between (1) targeting firms who have particularly entrenched managers and poor performance and (2) targeting firms who present favorable targets of opportunity. We theorize that how activists make these decisions depends on their power. All else being equal, more powerful activists target firms with entrenched managers and poor performance. Their power affords them the ability to function as salient external monitors, as predicted by agency theory. However, less powerful activists may be ill equipped to take on entrenched managers in the absence of other contextual factors that aid them in their efforts. As a result, less powerful activists are more sensitive to the corporate opportunity structure, selecting firms where visibility, reputation, and status can help attract greater scrutiny and exert greater penalties (Bartley and Child, 2014; McDonnell and King, 2017).

Although our theory primarily focuses on how investor power shapes targeting decisions, there are other possible explanations. It may be that institutional investors and individual investors simply pursue different goals. While institutional investors focus on increasing the value of their investment, individual investors may be more interested in increasing their own visibility and notoriety. Gregory Lau, a former director at General Motors, spoke to a reporter about John Chevedden’s proposals, saying, “Some of his proposals are good, but you can never talk to him about his positions or his supporting statement. He wouldn’t change them voluntarily” (Kerber, 2013). Lau’s statement reflects the view that some individual activists are less interested in engaging with firms to achieve genuine governance reforms. Notably, however, Chevedden told the reporter that companies were rarely interested in substantial changes when they reach out to him, saying, “They want to talk you to death.” Chevedden’s response reflects his view that corporate leaders are unresponsive to his activism efforts, perhaps because of his lack of power. Such a view is consistent with the premise that less powerful individual activists favor targets of opportunity where they can leverage public scrutiny to their advantage and avoid being dismissed by entrenched managers.

Another possibility is that less powerful investors (i.e. individual investors, unions) are less interested in achieving governance reforms at the targeted firm but are more interested in promoting shareholder-oriented governance norms more broadly. Less powerful activists may choose to target highly visible, reputable, and high-status firms not because these firms are more vulnerable to activist demands, but because these targets may provide less powerful activists with a means to reach a broader audience (i.e. spillover effects) and bring attention to their initiatives. Thus, otherwise disempowered activists may be able to affect broader corporate governance norms with only small ownership stakes by strategically selecting targets that will have a broader impact.

These alternatives suggest that activists may target high-profile firms because (1) they are more vulnerable to activist demands or (2) such activism can have broader impacts. As such, the corporate opportunity structure may shape whether targets are more vulnerable or more suitable for reaching wider audiences. Ideally, we would empirically compare these motivations but data limitations make it difficult to carefully compare the preferences and goals of different investor groups apart from cataloging the targets that activists select. However, adjudicating between competing explanations and activist motivations is a promising avenue for future research.

These findings offer a number of implications for theory and research on shareholder activism, corporate control, and social movements. First, we offer an integrated theory of shareholder activism that joins insights from both agency theory and social movement research. This theorization highlights how activists select targets not only on the basis of agency problems, but also on the basis of the corporate opportunity structure. Moreover, our theorization and empirical approach answers recent calls to focus on heterogeneity in investors’ interests and demands (Goranova et al., 2017). Our study reveals that different types of activists make distinct targeting choices. Consequently, our integrated theory of shareholder activism provides new insights into how activist investors choose targets and the role that activism plays in corporate governance.

Our analysis also advances thinking on reputation and status in organizational fields. Traditionally, scholars argue that reputation and status provide halo-effects that insulate firms from consequences and predisposes audiences toward favorable evaluations. However, following recent evidence in social movement and organization research (Bartley and Child, 2014; King, 2008; McDonnell and King, 2017), we argue that reputation and status can make firms attractive activism targets. Firms are likely to be defensive of their reputation, particularly if it serves as a key source of competitive advantage. Similarly, status can invite greater scrutiny from external audiences and higher status actors often face harsher penalties if they are found deviant from prevailing norms (Hahl and Zuckerman, 2014; McDonnell and King, 2017). For less powerful activists, who lack formal resources for posing a salient threat on their own, leveraging reputational penalties and status-based scrutiny can serve as an important lever for exerting pressures on the firm. In addition, less powerful activists may seek to build their own reputation and status by taking own highly reputable and high-status firms.

Somewhat surprisingly, however, we also find that more powerful investors, including pensions and investment funds, are likely to eschew targeting firms with greater visibility, positive reputations, and greater status, as indicated in the predicted probabilities in Figure 3. While we theorized that reputation and status function as a “magnet” for less powerful activists, the findings indicate that these traits repel more powerful activists and may induce a halo-effect that only affects institutional investors. It may be that more powerful activists are less willing to target these firms because such behavior could threaten their own positions in the field. Investment managers at pension funds and investment funds typically have extensive back-channel access to the managers at the firms where they invest (Gantchev, 2013). This access affords them an opportunity to directly express dissatisfaction over performance and governance matters and to communicate their preferences. However, targeting highly reputable and prestigious firms could threaten institutional investors’ insider access. Indeed, Kenneth Steiner, a prominent individual activist, echoed these ideas, telling a reporter that institutional investors are often unwilling to confront prominent firms “because they can’t lose access to the companies’ management” (Solomon, 2014). Another possibility is that institutional investors’ business practices preclude targeting highly visible, reputable, and high-status firms. Many of these institutional investors provide pension services to the same firms where they hold equity; these business relationships can dissuade institutional investors from confronting management for fear of alienating a customer (Davis and Kim, 2007). Institutional investors may avoid targeting visible, reputable, and high-status firms because such behavior could jeopardize their business ties as pension providers to other firms. Indeed, others have acknowledged the conflict of interest represented in financial intermediation and external monitoring (Davis, 2009), but our results point to a more general status halo-effect that may further exacerbate these problems.

Finally, our analysis introduces an innovative approach to studying activism. Our network-based approach is flexible enough to accommodate numerous firm and activist-centric traits. We hope that future research will adopt our approach but incorporate other activist-level antecedents, like size or portfolio strategy, in an effort to further uncover what shapes activist heterogeneity. In addition, data limitations preclude a more fine-grained analysis of activist power, such as ownership stake in a given firm. More detailed analysis of activist power could help further specify situations when activists select more prominent or problematic targets. However, our network approach could accommodate such an analysis if information on activists’ investment portfolios were to become available. Finally, we hope that our network approach proves useful for research on socially oriented shareholder activism, where activists use proxy resolutions to address corporate social performance. As we noted earlier, our study focuses on corporate governance and finance-related activism, but similar dynamics may shape contention in environmental and social activism fields. Here again, activist heterogeneity can help integrate diverse theoretical perspectives.

Shareholder activism has undergone a notable transformation over the last two decades. Many activists are increasingly prolific and have become more successful at prompting reforms across corporate America. As firms must grapple with the increased costs and scrutiny accompanying shareholder activism, scholars should continue to interrogate whether or not activism serves the interests of all investors, represents idiosyncratic attempts to extract firm concessions, or plainly fails to induce meaningful governance reforms. Investigating the firm-level antecedents that attract investor activism will continue to be a central focus in this scholarly agenda but researchers will need to develop a more holistic and relational conceptualization of shareholder activism that attends to heterogeneity in investors’ resources and interests as well as the opportunities and constraints posed by the increasingly prolific field.

Footnotes

Appendix 1

Acknowledgements

We wish to thank Jiwook Jung, Taekjin Shin, Amit Kramer, Shinjae Won, Dan Wang, and Ryan Lamare for helpful comments on an earlier version of this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.