Abstract

Building on the vast literature on technological innovation and new product development, we propose a “strategic organization” framework to inform future research. The framework focuses on two core constructs: “agents” (external stakeholders and internal members of the firm involved in innovation activities) and “capabilities” (activities, systems, and values that retain and unfold organizational knowledge). It also distinguishes between two levels: the “new product development” process (the strategic and organizational sequences of tasks and decisions that compose product development activities); and the “firm” (the strategic and higher-order activities that shape corporate governance, corporate strategy, competitive strategy, and the organizational configuration of the firm). We draw on the framework to highlight how the strategic and organizational management of innovation has moved from a specialized organizational unit, the Research and Development function, to the C-suite. We discuss the implications of this framework for future research and highlight emerging challenges related to short-term financial pressures, sustainability, and digital transformation.

Keywords

Introduction

In the 100 years that separate us from Schumpeter’s (1983 [1934], 2014 [1942]) seminal contributions to the understanding of innovation, research has grown exponentially, developing intercontinental outreach (Fagerberg and Verspagen, 2009). Hundreds of papers have analyzed the activities necessary to ideate and develop new products that can potentially succeed in the marketplace from different disciplinary angles. In this essay, we specifically embrace a “strategic organization” view to disentangle the heterogeneity and richness of these findings and inform future research on the management of innovation. In doing this, we have in mind one of the missions of a strategic organization perspective, that is, “to lead a reintegration of strategy and organization” (Baum et al., 2003: 8). This is particularly crucial for a topic like innovation that presents a strong interconnection between strategic and organizational issues. Our goal is also to unveil some of the microfoundations of company strategy (Felin and Foss, 2006) and, more precisely, focus on the fundamental role of agents shaping and informing innovation decisions.

We argue, in fact, that we are moving from a context in which innovation was relegated to an organizational unit and conceived as an una tantum activity, to a situation where firms must constantly monitor and manage innovation from the C-suite. Overall, we claim that firms to effectively innovate must conceive innovation not only as a process within their R&D function but as a continuous strategic and organizational endeavor of the entire top management team (TMT).

After introducing our strategic organization framework for innovation below, we discuss its implications for three emerging innovation challenges that organizations are currently experiencing (financial short-termism; sustainability, and digital transformation), setting an agenda for future research.

A strategic organization framework for innovation

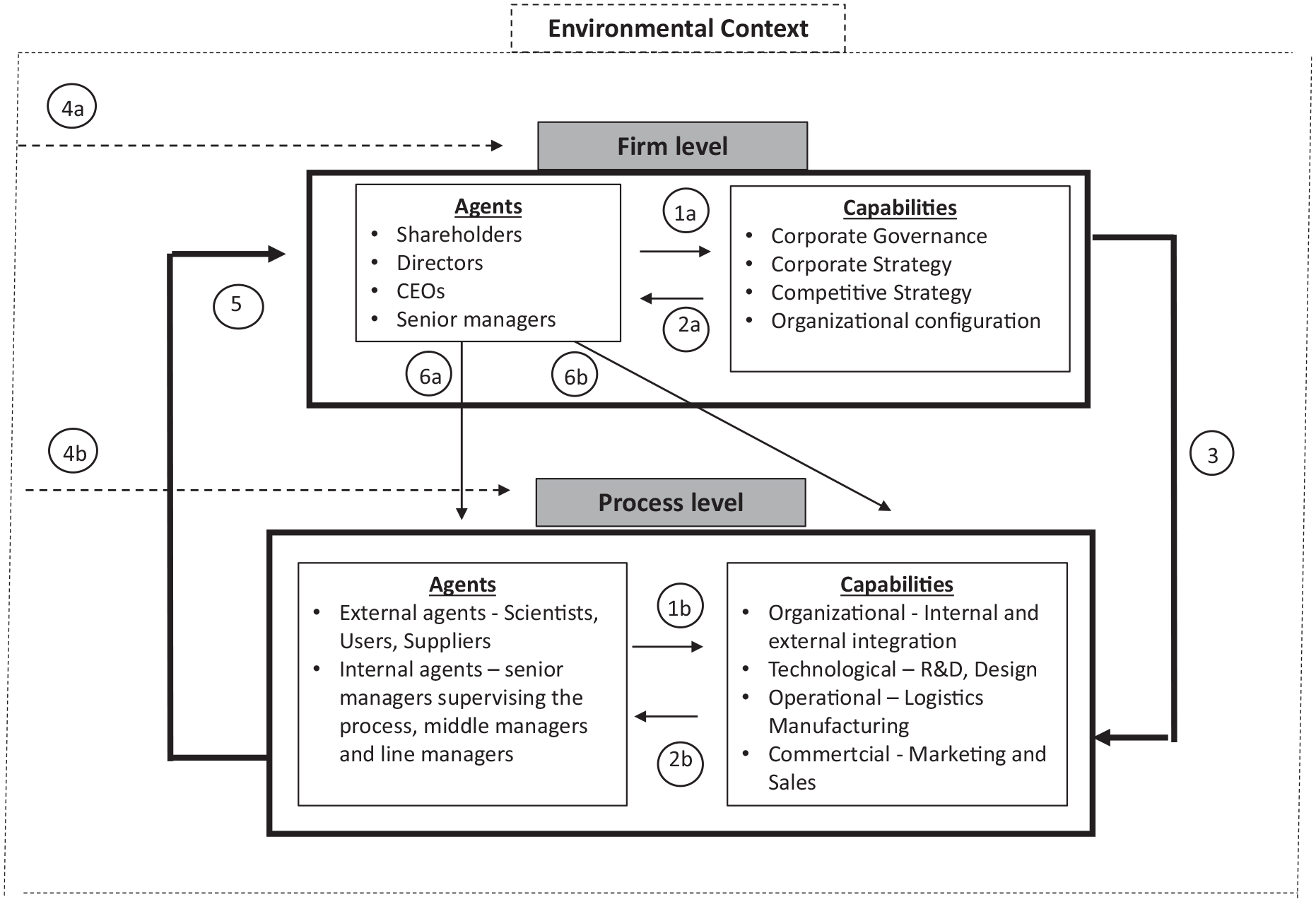

Our proposed framework distinguishes between two core constructs and their interplay at two different levels. The two constructs are agents and capabilities. By agents, we refer to all actors whose knowledge can contribute to innovation activities. By capabilities we refer to the activities, systems, and values that form the basis of organizational knowledge and act as its repositories (e.g. Grant and Verona, 2015; Leonard and Barton, 1992). The two levels at which we consider the interplay between agents and capabilities are the new product development process and the firm. By new product development process level, we refer to the level of strategic and operational tasks and activities needed to ideate and commercialize new products. By firm level, we consider the C-suite’s viewpoint on strategic and organizational decisions. While the two constructs and the two levels are in constant interplay, their separation helps us to structure findings from the literature and deduce their most important consequences (see Figure 1).

A strategic organization framework for innovation research.

We start by noting that agents at the firm level are the CEO and the TMT—that is, the senior managers that oversee functions or divisions within the organization (see, for example, Hambrick and Mason, 1984)—but also the shareholders that influence the executive team through the directors they appoint (Jensen and Mackling, 1976—see left upper box). Agents with their decisions shape and inform corporate governance, corporate strategy, competitive strategy, and the consequent configuration of the firm (Lawrence and Lorsch, 1967; Porter, 1980—link 1a in Figure 1 and the right upper box). The decisions they take produce outcomes that reinforce or falsify their beliefs and their subsequent actions on these decisions (link 2a in Figure 1).

Decisions taken at the firm level include the development of corporate strategy in which innovation can be an important component (Aghion and Tirole, 1994)—other topics of corporate strategy might include diversification, vertical integration, M&A, and so on (e.g. Porter, 1987). Historically, innovation has been organized within a specific unit (Burns and Stalker, 1961; Chandler, 1977; Schumpeter, 2014 [1942]), typically a so-called Research and Development (R&D) function—a function devoted to the creation of patents that serve as innovations to be commercialized (link 3 in Figure 1). The R&D function governs the new product development process that can be broken down into “stages” or “phases” pacing the creation of innovation (see, for example, Clark and Fujimoto, 1991; Cooper, 2011). This configuration at the top defines rules for the interaction of agents and capabilities at the process level.

Agency is in fact particularly crucial at the process level (left lower box of Figure 1). Research has helped identify opposite poles that spur the ideation of new products at the process level, distinguishing, for example, between a “technology-push” perspective and a “demand-pull” view (see, for a review, Di Stefano et al., 2012). According to the former, science is the ultimate source of product development (e.g. Mowery and Rosenberg, 1979) and crucial actors in the creation of innovations are scientists involved in corporate R&D labs, but also those that are located in universities and research centers (i.e. outside the boundaries of the firm). A demand-pull perspective instead emphasized the important role in innovation of demand. Over the years it has been demonstrated that even in business to consumer markets, users can sometimes ideate and manufacture important innovations (Von Hippel, 2005). Indeed, research has shown that external stakeholders (from scientists and users to producers of equipment and raw materials to specialized consultants) and internal stakeholders like senior managers, project leaders, specific functional team members, may all have an impact on successful new product development (Brown and Eisenhardt, 1995).

Agents’ impact operates through their decision making, which shapes new product development capabilities (link 1b and lower right box in Figure 1). Scholars have investigated decisions regarding the organizational nature of the process—for instance, an important decision to be taken is the sequential or concurrent form with which process tasks and activities are configured (see, for example, Ulrich et al., 2020). In the past 20 years they have also debated the degree of openness toward potential complementors. The “open innovation” paradigm has in fact documented the necessity of innovation activity to move beyond company boundaries and involve external actors able to detect technological trajectories of innovation (Chesbrough, 2003; Laursen and Salter, 2006). In addition, engineering and operations research scholars have considered design and manufacturing decisions (Krishnan and Ulrich, 2001), marketing scholars have investigated the role of market research in defining customer needs and managing new products (Hauser et al., 2006), and entrepreneurship scholars have leveraged venturing and finance lenses to study innovation practices (Shane and Ulrich, 2004). The toolkit generated by these interdisciplinary research streams has informed managers working in the various functions involved in the innovation process.

The implementation of these decisions shapes new product development capabilities and outcomes (Verona, 1999). These outcomes, obtained from positive experience of successful innovations but also from mistakes and failures of innovations, reinforce or falsify beliefs and affect overall decision making at the product development level (link 2b in Figure 1). For instance, Danneels (2001) showed how integration of customer competence and technology competence in new product development improves learning cycles. Katila and Ahuja (2002) highlighted a variety of types of search strategies for new products that might either enhance present competences (search depth) or expand them (search breadth). Stadler et al. (2013) showed how heterogeneity in seismic drilling and well drilling technologies in the oil industry favored the quantity of resource access and development. Tzabbar et al. (2008) show how knowledge stocks (i.e. capabilities) developed and deployed in the innovation process can be complementary but also substitutive in an event study of the biotech industry.

In parallel with research on new product development, strategic management scholars became increasingly aware of the evolutionary dynamics of technology (see, for example, Abernathy and Utterback, 1978; Dosi, 1982) and their impact on organizations, reflecting the influence of the environmental context (external dotted box in Figure 1). These dynamics, they observed, can evolve linearly but can sometimes be punctuated by exogenous shocks (Romanelli and Tushman, 1994; Tushman and Romanelli, 1985). Incremental changes or shocks in the trajectory of technology impact innovation at both firm and process levels (dotted link 4a and 4b in Figure 1). This implies that investing in R&D and product innovation is not enough to successfully create new products, because technological discontinuities can sometimes be “competence-destroying” (Anderson and Tushman, 1990; Tushman and Anderson, 1986). While positive learning cycles can strengthen organizational competences in the case of “competence-enhancing” change, in the opposite case of competence-destroying shocks, core competences—namely, the skills but also the organizational structures, values, and systems that shape innovation at the process level—turn into “core rigidities” (Leonard and Barton, 1992).

Subsequent work helped understand the sources of inertia that prevent firms from continuously innovating with success after competence-destroying change. Some scholars focused on product technology that may require reaching beyond “modular” changes (Baldwin and Clark, 2000) to create an entirely new architectural logic (Albert and Siggelkow, 2022; Henderson and Clark, 1990). Others focused on the absence of complementary assets that might limit the ability to adapt to a changing technological environment (Taylor and Helfat, 2009; Tripsas, 1997). Firms might also be blinded by the needs of current and mainstream customers which trap them into sustaining trajectories that are eventually displaced by technology disruptions introduced by new entrants (Christensen and Bower, 1996). Executives may thus face an “innovator’s dilemma”—whether to sacrifice short-term profit from core markets or nurture longer-term profit in disruptive markets (Christensen, 1997).

Research has also shown that new product development takes place in a social context in which organization and firms may be constrained by their beliefs and identity (Ravasi et al., 2020; Tripsas, 2009). For instance, Tripsas and Gavetti (2000) showed that cognition created an important transformational friction when Polaroid’s managers failed to guide the firm through the technological shift to digital cameras. Danneels (2011) also illustrated how typewriter market-leader Smith Corona faltered during the technological discontinuity of its industry, despite making adequate resource alterations, because it lacked managerial cognition about firm resources.

How can then firms adapt to technological change? Greenwood and Hinings (1996: 1024) comment that radical organizational change “involves busting loose from an existing ‘orientation’ [. . .] and the transformation of the organization.” Balogun and Hope-Hailey (2008) remark that transforming an organization implies changing its organizational attributes. Thus, renewal involves both making strategic choices with long-term impacts and changing organizational attributes to meet new goals (Floyd and Lane, 2000) (link 1a in Figure 1). In order to continuously innovate, firms must therefore develop a higher-level capacity to change (Teece et al., 1997). They must be able to explore new knowledge and competences (March, 1991) while exploiting existing knowledge and competences (O’Reilly and Tushman, 2008). This is why in the past 20 years research has paid increasing attention to these “higher-order” capabilities (Winter, 2000), also called “dynamic capabilities” oriented toward change (Eisenhardt and Martin, 2000; Helfat, 1997; Helfat et al., 2007; Teece, 2007). In our framework, this essentially means that, while a process focus is crucial to producing effective and efficient new products in a specific competitive and technological context, it is specifically a firm-level perspective that sets the stage for the continuous creation of innovation that can overcome the core rigidities of changing technological and competitive terrains (link 5 in Figure 1). It is at this higher level that firms show the capacity to adapt by reconfiguring their knowledge and competence base (Eggers and Park, 2018).

This capacity to explore new knowledge has both “behavioral” and “structural” dimensions. It is behavioral (link 6a) when it points to the ability of senior managers and CEOs to sense, seize, and support the reconfiguration of the organization with specific actions (Teece, 2007). Overall, CEOs have been identified as a firm’s principal decision makers, and evidence has accumulated that CEOs are crucial in risk-taking and innovation decisions (Floyd and Lane, 2000; Herrmann and Nadkarni, 2014). For instance, CEOs who direct their attention toward novel, vivid, and salient information have been shown to introduce more new products (Li et al., 2013). And new products are introduced faster when firms in dynamic environments are headed by CEOs with a low past focus and high future focus (Nadkarni and Chen 2014). Maula et al. (2013) found that CEOs’ diversity of ties through corporate venture capital leads to better recognition of new business opportunities. Cillo et al. (2021) model behaviors of successful multinationals of consumer goods like Gucci, Ducati, and Ferrero, showing that in these organizations the CEO personally finds ways to interact with and learn from specific groups of customers.

In general, top managers play an important role by setting the stage for middle managers to operate (Floyd and Wooldridge, 2000). Indeed, role expectations from middle managers impact their agency and it is therefore important to consider the conditions that allow this agency process to occur and stimulate bottom-up idea generation (Mantere, 2008). Recent studies have shown that TMT diversity is critical to enact a process of change, while middle managers’ diversity impacts the success of innovations and their degree of novelty (Schubert and Tavassoli, 2020). This behavioral capacity of exploration may be enhanced by the presence of dedicated roles like “ambidextrous managers” or “meta-managers,” who support people involved in the new product development activities (Tushman et al., 2010). For instance, the historical case study of Olivetti showed how core agents involved in the transition from mechanical technology of typewriters to electronic technology of personal computers were able to handle a complex process of legitimization of a new technology while de-institutionalizing a previous technology (Danneels et al., 2018).

But exploration has also been associated with “structural” arrangements (Gibson and Birkinshaw, 2004; O’Reilly and Tushman, 2013), implying a division of labor with dedicated units such as corporate venture capital divisions or spinouts focusing on new technological paradigms vis-a-vis extant units focusing on exploitation of existing knowledge (see, for example, Christensen and Raynor, 2003–see link 6b). Thus, Lavie (2006) developed a conceptual model showing how capabilities can evolve, be transformed, or acquired in the face of technological change. Burgelman (1994) showed in his study of renewal at Intel that a firm undertakes renewal by pursuing its existing competences while simultaneously exploring new ones. Verona and Ravasi (2003) highlighted how Danish hearing aid player Oticon evolved from analog to digital technology by recombining internal knowledge thanks to processes based on capability integration and reconfiguration driven by a new TMT. Kauppila (2012) showed how structural ambidexterity can be pursued through interorganizational partnerships with different partners focusing on exploratory and exploitative innovation. All of these studies suggest that renewal requires some degree of modification to a firm’s strategy and organization, which are characterized by subprocesses running sequentially or in parallel.

The strategic organization framework we have deduced from the literature offers a historical and functional perspective on innovation. It is functional because it indicates exactly what firms and managers must do at both the macro and the more micro-levels to fuel and streamline innovation and develop a series of new products. But the framework also offers a historical reading because it helps us highlight the increasing complexity that organizations have to face if they want to successfully pursue innovation. Over the years, research has confirmed the transition from an R&D function that has the relatively simple goal to develop patents and introduce new products into stable environments to a more dynamic and complex firm that has to deal with competence-destroying change and to constantly innovate its business models to do that. Overall, the interactions between agents and capabilities at different levels offer a better understanding of the challenges ahead.

Discussion: emerging challenges

The strategic organization framework provides a useful toolkit for theorists and practitioners of innovation that deserves further development. For instance, research on behavioral and structural exploration (links 6a and 6b) is still sometimes anecdotal and industry-specific (O’Reilly and Tushman, 2013). It would be important to generate robust data that would identify potential boundary conditions. Similarly, understandings of the inertial forces that impede adaptation (link 5) may evolve. For instance, Binns et al. (2022) recently provided illuminating cases of the importance of strategic ambition in corporate leaders to stimulate exploration, and even documented the presence of new organizational roles—termed by the authors “corporate explorers”—to coordinate disruptive exploration at the process level. These figures may be capable of breaking the inertial cycles we have documented in the previous section. At a more micro-level, research in different technical fields including marketing and operations has recently developed new “agile innovation” techniques and methodologies for product development that it would be important to explore further in order to update the toolkit for innovation (link 1b).

Future research could also use the strategic organization framework to emphasize some of the challenges and trade-offs linked to new environmental dynamics. We explore three particular challenges below.

Challenge 1: overcoming short-term profitability pressures

When the locus of innovation from the new product development process moves back to the firm (link 5) a first strategic question emerges. Innovation is intrinsically a risky activity and radical innovation contains the highest of risks: how can a CEO who is monitored quarterly by financial analysts organize a company architecture aimed at long-term growth driven by continuous innovation? Research by Benner (2010) on the telecommunication and camera industries demonstrated that security analysts strongly advised incumbents to continue investing in their core technology, leaving them behind startups and other players investing in new disruptive technology. This raises important questions. Are financial markets ready to digest a new management era in which innovation is a core corporate strategy activity as asserted by scholars in the tradition of dynamic capabilities and ambidexterity (link 1a)? Or will innovation remain a process strategy relegated to an R&D function organized to serve una tantum the need for innovation (link 3)?

To the best of our knowledge, the crucial relationship between shareholders and the TMT has not received a great deal of attention in innovation research, but this is an important relationship that is crucial for sustaining an innovative organization. In our framework, we grouped together the “principals” and “agents” of the firm (see upper left box), but future research should probably separate them and dig deeper into potential actions and decisions between the providers of financial resources—including owners—and managers. An exception in this literature gap is the study by Klarner et al. (2020), which focuses on how directors can advise R&D teams on technical topics related to innovation strategy and management. But more broadly, some of the core issues have to do with the commitment to innovate and how to innovate. For instance, Cassiman and Valentini (2009) offered a stylized model showing that separation between principals and agents in the R&D decision making produces different results in terms of how much basic research and open research is done by the firm.

Future research could also investigate to what extent continuing investment in exploitation is the solution to funding the exploration of new businesses as core research in ambidexterity suggests (O’Reilly and Tushman, 2013). Or whether strong entrepreneurship capabilities at the corporate level can allow a firm move from one innovation to another, without the necessity of relying on the exploitation of past businesses (link 6b). This seems to be more and more the main trait of multinationals like Alphabet, Meta, and Amazon, among others.

Challenge 2: toward sustainable innovation

The challenge concerning the tension between innovation and financial orientation becomes particularly salient in a world where sustainability is becoming a key goal for society (Henderson, 2020; Kaplan, 2020). Sustainability is redefining the values and strategy of the organization by reframing the trade-offs between short-term financial and future needs (Bansal and Desjardine, 2014). While stakeholder theory has been around for some time (Donaldson and Preston, 1995), we are finally seeing more and more concrete moves that support corporate social responsibility (CSR). These include the massively popular letters to CEOs sent by Blackrock President Larry Fink since 2018, the 2019 commitment toward stakeholders of the Business Roundtable of 250 US executives, but also the fact that in many countries financial regulation is moving toward requirements to adopt a longer-term view. While CSR concerns are increasing worldwide (Matten and Moon, 2008), there is however, broad heterogeneity in terms of its implementation, and specifically in terms of its impact on innovation practices. Are firms really discounting short-term profit for long-term sustainability results?

The increasing presence of activists in the board room to be listened to when a firm is about to develop innovation (upper left box) seems to go in this direction. External pressure groups—boycotts, or collective action orchestrated by social movements—are also increasingly central to strategy (King and Walker, 2014). External or outside stakeholders can clearly play an important role in directing the attention and structures of firms (Crilly and Sloan, 2013). More research that studies how these new voices actually impact the innovation orientation of a firm is clearly needed.

Other challenges of sustainability are related to the ecological transition we have been experiencing in recent years. The environmental voice of the masses is producing brand new shocks that are forcing many industries to change (links 4a and 4b), like in the case of the automotive industry with the current R&D race toward the electric engine which requires a redefinition not only of the organizational competences of the single firm but of the entire industry ecosystems. Ecological transition has also been transforming the product development process and the way we consume innovations (link 1b). For example, producing products that are circular implies thinking ahead about the reuse of each component, in order to extend its lifetime value and reduce waste. One example is provided by Patagonia, a clothing company committed to sustainability since its foundation. Patagonia produces most of its products (72%), garments and equipment, using recycled materials, such as plastic and other fibers that are reused in their production process. In addition, each Patagonia product has a long-life insurance, extending the lifecycle of each product, and the use of recycled materials reduces dependence on oil. More research is needed to explore the principles of circularity and better understand the ways in which new and established companies can transform their innovation processes to promote sustainability.

Challenge 3: toward digital transformation

Increasingly, digital transformation lies at the core of innovation processes, raising the question of how digital technology is likely to impact our framework. While some organizations are still managing digital technology as an organizational function (e.g. the information technology (IT) department), many have understood its disruptive impact and the necessity for broader digital transformation. While digital technology is not itself core to many industries, its impact has apparently oftentimes turned disruptive and competence-destroying (links 4a and 4b). As Greenstein et al. (2013: 110) effectively put it: In less than a generation the costs of storage, computation, and transmission declined by several orders of magnitude, enabling a lowering of cost in a range of activities by a similar order of magnitude, and enabling the creation of an enormous range of new applications.

Digital transformation is forcing all organizations to update their technological architecture. It produces fundamental opportunities for firms offering increased modularity and decreased communication costs (Felin et al., 2017). It also widens the spectrum of the served market and makes available data about buyers’ unmet preferences that can improve product development.

But digital technology is also impacting innovation by creating new potential actors (lower left box). Social movement—like forms of production, as is evident in open-source software—gives rise to new ideation useful for the process of innovation (Lakhani and Von Hippel, 2003). Crowdfunding actors widen the spectrum of financial possibility for startups and individuals (Felin et al., 2017). More recently, research on the sharing economy has conceptualized the emergence of platforms as a network-based meta-organizational model that implies entirely new ways of managing innovation (Kretschmer et al., 2022).

Among new “actors” at the product development level, algorithms and artificial intelligence are becoming an important adjunct to humans (Lanzolla et al., 2020). Product design has been enriched dramatically thanks to new toolkits made available by digital technologies (Mannucci, 2017), and robotics is playing a wider role in manufacturing and pretesting (Brynjolfsson and McAfee, 2014). In some contexts, firms may begin to undertake privately more of the R of R&D than they used to in the past, where academia were important stakeholders. This is the case in artificial intelligence (AI), as shown by companies such as Meta or Alibaba (Hartmann and Henkel, 2020). Models in which algorithmic machines control organizational actions are also being developed (Schafheitle et al., 2020), with a clear impact on the nature of capabilities (upper and lower right boxes).

Learning loops (links 1b, 2b) will also be enhanced thanks to machine learning driven by digital toolkits (Brynjolfsson and Mitchell, 2017). These will improve thanks to digital technology but will depend a lot on human–algorithmic interaction (Lanzolla et al., 2020), which still needs to be tested case by case. More democratic and bottom-up forms of sensing show promise as a way of harnessing the collective wisdom that (more often than not) latently sits within and among the employees in the firm, and beyond (Felin et al., 2017) (link 6). In addition, digitalization offers unique opportunities for firms to test decisions through quick experiments and learn from them. Economic experimentation has historically been very important but very costly, as documented in the case of the first automotive makers (Pillai et al., 2019). Digitalization can reduce those costs and some authors are proposing a scientific approach to decision making under uncertainty, whereby they encourage startup entrepreneurs to generate and test many hypotheses to reduce potential biases in their decisions by increasing the amount of data available (Camuffo et al., 2019). Also, by providing access to more granular data, digital allows companies to better learn the demand trajectories and to identify new growth paths for their respective businesses, as demonstrated by a recent study on the advent of streaming in the music business (Zanella et al., 2022).

Conclusion

Organizations are at the center of innovation activity, and the managerial processes of innovation and change are central to a strategic organization perspective (Baum et al., 2005). Studies in areas from operations management to marketing have helped us clarify the technical decisions behind successful innovation activity and are continuing to update our understanding of the innovation process. However, it is specifically management research that has helped us identify the forces that inhibit or accelerate innovation at the strategic and organizational level. Within this tradition, innovation has become paramount in business administration research and in business school teaching. Along these lines, our framework bridges a crucial gap in the literature as emphasized by Felin and Foss (2006: 441): “Organizations are made up of individuals [. . .] yet this elementary truth seems to have been lost in the increasing focus on structure, routines, capabilities, culture, institutions and various other collective conceptualizations in much of recent strategic organization research.” Similarly, Baum et al. (2008 116) claim that Under conditions of change and uncertainty, individuals are constrained in their ability to reliably conceive and correctly implement strategic and structural changes that improve organizational success and survival chances. Contemporary research in strategic organization appreciates that it is these very constraints that make the effective strategic management of organizations vital; only in their absence do individuals not matter.

We hope our framework helps emphasize how individuals do matter now and for future research on innovation.

The interplay between agents and capabilities makes us realize that if organizations want to pursue innovation management today, they cannot limit their innovation activity to the process level, but need to reconsider the way they organize innovation at firm level. While technical decision making and capability management at new product development process level is necessary, this is channeled by the way agents at the higher level (e.g. shareholders, directors, CEOs, and senior management) shape governance and strategic decisions and learn from them. Innovative capacity is also threatened by the new challenges posed by digital transformation and sustainability in a post-pandemic world. Addressing these challenges will require more and more interdisciplinary competences that are the focus of other disciplines in business administrations—particularly finance, operations, and marketing. It is crucial therefore that future attempt to build stronger bridges, as we have begun to do in our analysis, in order capture a full 360° understanding of innovation.

Footnotes

Acknowledgements

We are grateful to editor Ann Langley and the anonymous reviewers for helping us improving our original manuscript. Errors remain our own.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.