Abstract

This article assesses the effect of political institutions on stock market performance in 14 African countries for which stock market data are available for the period 1990–2010. The estimation technique used is a two-stage least-squares instrumental variable methodology. Political regime channels of democracy, polity and autocracy are instrumented with legal-origins, religious-legacies, income-levels and press-freedom qualities to account for stock market performance dynamics of capitalisation, value traded, turnover and number of listed companies. The findings show that countries with democratic regimes enjoy higher levels of financial market development compared to their counterparts with autocratic inclinations. As a policy implication, the role of sound political institutions has important effects on both the degree of competition for public office and the quality of public offices that favour stock market development on the African continent.

The evolution of politics in Africa vis-à-vis the investment climate and financial market development can be discussed in two main stages, notably, (1) before the fall of the Berlin wall that marked the advent of multiparty politics and (2) the post-1989 era that is characterised by multiparty politics and the growth of stock markets. According to Yartey and Adjasi (2007), there has been substantial progress in stock markets in Africa since the 1990s. Before 1989, there were only eight stock markets in the continent: three in North Africa and five in sub-Saharan Africa. Today, there are 29 stock markets representing 38 countries. With the exception of South Africa, between 1992 and 2002, stock market capitalisation doubled in most countries, increasing from US$113.423 million to US$244.672 million. Unfortunately, these developments have not moved hand-in-glove with maturity in stock markets. This is essentially because in many of the stock markets, trading still occurs in a very limited number of stocks which make up a substantial part of the total market capitalisation. Moreover, vital issues in disclosure, information-sharing and supervision that are related to the overall institutional quality are affecting the development of these stock markets. Such institutional concerns are closely related to the quality of government.

The emergence of London as a major financial centre in the world can be explained by its tradition of fairness in the settlement of judicial matters (Asongu, 2012a). According to the narrative, the experience of Russia has shown that foreign investors are more likely to invest in environments that are characterised by limited expropriation risk and sound political institutions.

The growing depth and breadth of financial markets in developing countries (IMF, 2006; Mosley, 2008) have unfortunately been accompanied by deteriorating levels of political governance in recent decades (Asongu and Nwachukwu, 2016b). While the bulk of political science literature has focused on mechanisms by which globalisation in finance and trade influence government policy choices and economic outcomes (Friedman, 1999; Obstfeld and Taylor, 2004), as far as we have reviewed, little is currently known about how political regimes affect the health of financial markets. We fill this gap by assessing the effect of political regimes on stock market performance in Africa.

Consistent with Simplice Asongu (2012a), the intuition behind the inquiry is that the process of enhancing the value of stock markets is contingent on policies which are the result of institutional processes. Hence, it is relevant to examine how political regimes influence stock market performance on the continent for at least two reasons. First, the African business literature has substantially documented the need for other forms of investment because privatisation and liberalisation projects have failed to deliver the much needed foreign direct investment (FDI) (Asongu, 2013; Rolfe and Woodward, 2004). Second, there is a growing stream of African stock market literature showing that the stock markets of the continent substantially depend on the quality of institutions (Asongu, 2012a).

With the above facts in mind, the political climate in Africa over the past decades has been characterised by political strife, violence and a plethora of governance issues, notably, the Kenyan 2007–2008 post-election violence, Nigeria’s 2008 marred transition, the 2011 Arab Spring and negative externalities across North Africa, Côte d’Ivoire’s unfortunate political transition in 2011, the South-Sudanese political crisis that began in mid-December 2013 and has displaced hundreds of thousands of citizens and the Burundian failing political transition since April 2015, which has been caused by President Pierre Nkurunziza’s decision to seek a third term in office.

In the light of the above, the present inquiry assesses how political regimes of democracy and autocracy affect stock market performance in the African countries for which a stock market exists. The study’s contribution to the current literature is at least fivefold. First, due to the lack of relevant data, the relationship between stock market performance and political regimes has received little scholarly attention. Accordingly, stock markets on the continent for the most part are in their infancy. Second, the growing depth of financial markets on the continent represents an interesting opportunity to assess the role of political regimes in their evolution. Third, we have highlighted above that the continent is in dire need of alternative forms of investment. Moreover, recent African business literature is consistent with the position that institutional arrangements have contributed substantially to affecting the state of capital flows across the continent (Bartels et al., 2009; Darley, 2012; Tuomi, 2011). Therefore, it is relevant to assess the influence of political regimes on stock market development or long-run finance. Fourth, current trends in stock markets on the continent reveal that countries in the French-speaking community have comparatively less healthy stock markets. Given that Africa’s former French colonies have registered more coups d’état than the rest combined since independence (Klah, 2010), findings from the study could provide some insights into why this set of countries are lagging behind their English counterparts. Fifth, despite the wealth of studies in the literature on finance and institutions, there has been only a limited focus on Africa. Paul Alagidede (2008) has argued that the underlying neglect is partly traceable to the institutional environment of Africa. The theoretical underpinning motivating this line of inquiry is the law and finance theory from Beck et al. (2003).

The rest of the study is organised as follows. The next two sections discuss the intuition and theoretical background and the data and methodology. This is followed by a discussion of the empirical analysis and results. The final section concludes.

Intuition and Theoretical Background

The intuition for assessing the relationship between political regimes and stock market development builds on the fact that political institutions are very likely to influence arrangements that regulate stock markets. Within this framework, legal and supervisory bodies that provide order and cohesion in financial markets are shaped by political institutions. The intuition here is broadly consistent with the literature supporting the relationship between political connections and market value (Faccio, 2006; Fisman, 2001; Francis et al., 2009). Hence, it is logical to think that democratic versus autocratic institutions have important and considerable implications on these relationships and dealings between firms and their sources of capital.

According to the World Bank (WB, 2010), (1) ‘institutionalised democracy’ is the presence of procedures and institutions via which citizens can express their preferences about alternative leaders and policies that guarantee civil liberties for all citizens, and (2) ‘institutionalised autocracy’ is the absence of institutions and procedures through which citizens can express their preferences about them. In the latter case, there is an absence of guarantee for civil liberties for all citizens.

In the light of the above, political regimes and financial development are directly linked to political actions which affect financial development. For instance, Philip Keefer (2007) has shown that government actions influence financial development through channels of, inter alia, secured property, financial regulation and contract rights. Hence, such public commodities are sensitive to political incentives. Political economy theories are consistent with the view that where a small elite controls political decisions, financial development can be constrained by the lack of competition. This theoretical underpinning has been confirmed by Girma and Shortland (2008). Given that autocratic regimes are more characterised by a narrow elite that influences political decisions, we expect democratic regimes to influence stock market development more positively. A democratic environment is more likely to increase shareholders’ return by reducing both agency and transaction costs. Moreover, within the framework of financial markets, compared to autocratic institutions, democratic institutions are more likely to enforce the control of corruption which is a source of insider-trading in financial markets. It is interesting to note that insider-trading has been documented to reduce stock market development (Bhattacharya and Daouk, 1999).

Under the assumption that autocratic regimes are less politically stable, political regimes indirectly affect stock market activity through political uncertainty. In essence, political instability negatively affects stock market development because it limits economic growth. This perspective has been confirmed using broad (Alesina et al., 1996) and African-specific (Fosu, 2002) samples. The indirect effect builds on the theory of investment uncertainty which has been confirmed by George Bittlingmayer (1998) within Germany, notably that political uncertainty can simultaneously reduce output and increase volatility.

Data and Methodology

Data

We examine a panel of 14 African countries with data from African Development Indicators (ADI) of the WB for the period 1990–2010 (WB, 2010). The sample is restricted to 14 countries due to data availability constraints. Consistent with recent African stock market literature (Asongu, 2012a, 2013), the dependent variables are stock market capitalisation, stock market value traded, stock market turnover and number of listed companies.

Political institutions variables include democracy, polity and autocracy. Instrumental variables (IVs) are legal-origins, press-freedom, income-levels and religious-domination. These instruments are consistent with African stock market (Asongu, 2012a) and growth (Agbor, 2015) literature. Moreover, they have been substantially documented in the economic development literature (Beck et al., 2003; La Porta et al., 1997; Stulz and Williamson, 2003).

In the regressions, we control for voice and accountability and regulation quality in the first stage, but not in the second stage. The control variables from which we expect positive effects are consistent with recent African law-finance literature (Asongu, 2012b). The selective introduction of control variables at the second stage is in accordance with Beck et al. (2003) and Asongu (2012a). The choice of the control variables is also constrained by the degrees of freedom needed for the over-identifying restriction (OIR) test at the second stage of regressions. In essence, given the number of instruments under consideration, control variables at the second stage would either result in exact- or under-identification. This implies that the instruments are either equal to or less than the number of endogenous explanatory variables, respectively.

Definitions and sources of variables are presented in Appendix 1, while the summary statistics are disclosed in Appendix 2. A correlation matrix is provided in Appendix 3, while the categorisation of countries is given in Appendix 4. All the appendices are available in the supplementary information online. Two insights are worth noting from the summary statistics: (1) the variables are comparable from mean values, and (2) the substantial variations imply we can be confident that reasonable estimated linkages will emerge. The purpose of the correlation matrix is to limit potential multicollinearity issues.

Methodology

Consistent with Beck et al. (2003) and recent African development literature (Asongu, 2014; Asongu and Nwachukwu, 2016a), we adopt an IV estimation technique. IV estimates address the puzzle of endogeneity and thus avoid the inconsistency of estimated coefficients by ordinary least-squares (OLS) when the explanatory variables are correlated with the error term in the main equation. The two-stage least-squares (2SLS) technique entails the following steps:

First-stage regression

Second-stage regression

In both equations, X is a set of explanatory control variables. For equations (1) and (2), v and u, respectively, represent the disturbance terms. IVs include legal-origins, dominant-religion, press-freedom and income-levels. In equation (1), ‘PoliticalChannel’ denotes democracy, polity and autocracy. ‘Finance’ in equation (2) represents stock market performance dynamics in terms of (1) stock market capitalisation, (2) stock market value traded, (3) stock market turnover ratio and (4) number of listed companies.

We adopt the following steps in the analysis: (1) justify the use of a 2SLS over an OLS estimation technique with the Hausman test for endogeneity, (2) demonstrate that the instruments are exogenous to the endogenous components of the explanatory variables (political institutions) conditional on other covariates (control variables) and (3) verify that the instruments are valid and not correlated with the error term in the equation of interest through an OIR test.

To ensure further robustness, the following checks are performed: (1) usage of alternative indicators of political institutions, (2) employment of two distinct interchangeable sets of instruments that engender every category of the instruments, (3) usage of alternative indicators of stock market performance and (4) employment of principal component analysis (PCA) to reduce the dimensions of stock market and political indicators.

Empirical Analysis

This section addresses (1) the ability of the exogenous components of political institutions to account for differences in stock market performance, (2) the ability of the instruments to explain variations in the endogenous components of political institutions and (3) the possibility of the instruments to account for stock market performance beyond political institution channels. To these ends, we employ the 2SLS-IV estimations with legal-origin, press-freedom, income-levels and religious-domination as IVs.

Political Regimes and Instruments

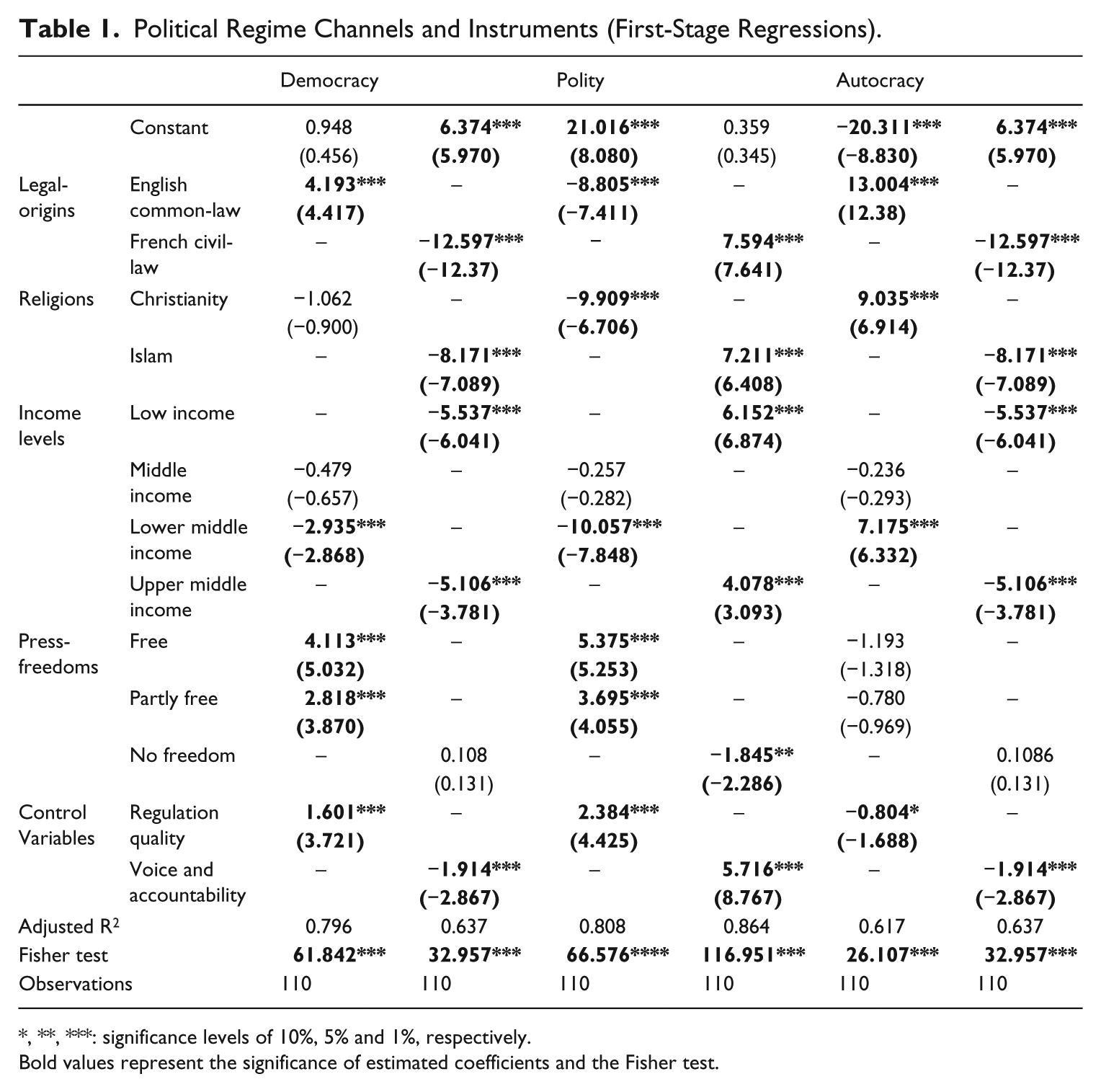

In Table 1, we regress the political regime indicators on the instruments and test for their joint significance. This is the first-stage (requirement) of the IV estimation technique for which the endogenous components of the independent variables must be explained by the instruments, contingent on other covariates (control variables). From the results of the Fisher statistics, it could be established that the instruments are strong, essentially because in the presence of control variables they jointly enter significantly into all regressions at the 1% significance level. Thus, ‘instrumenting’ political regimes with legal-origin, religious-domination, income-levels and press-freedom qualities helps explain cross-country differences in the quality of political institutions. We engage two separate regressions for each political regime: one with the first set of instruments and the other with the second set. Results from both sets of instruments are similar. Based on the findings, the following could be established: (1) consistent with the law-finance (growth) literature (Agbor, 2015; Beck et al., 2003; La Porta et al., 1997, 1998), English common-law countries have higher levels of democracy compared to their French civil-law counterparts, and (2) contrary to Samarth Vaidya (2005) and Henrik Oscarsson (2008), democratic institutions improve with press-freedoms.

Political Regime Channels and Instruments (First-Stage Regressions).

*, **, ***: significance levels of 10%, 5% and 1%, respectively.

Bold values represent the significance of estimated coefficients and the Fisher test.

Financial Markets and Democracy

This section seeks to address two main issues: (1) the ability of the exogenous components of political institutions to explain stock market performance and (2) the ability of the instruments to explain stock market performance beyond political regime channels. To make these assessments, we employ the 2SLS-IV approach.

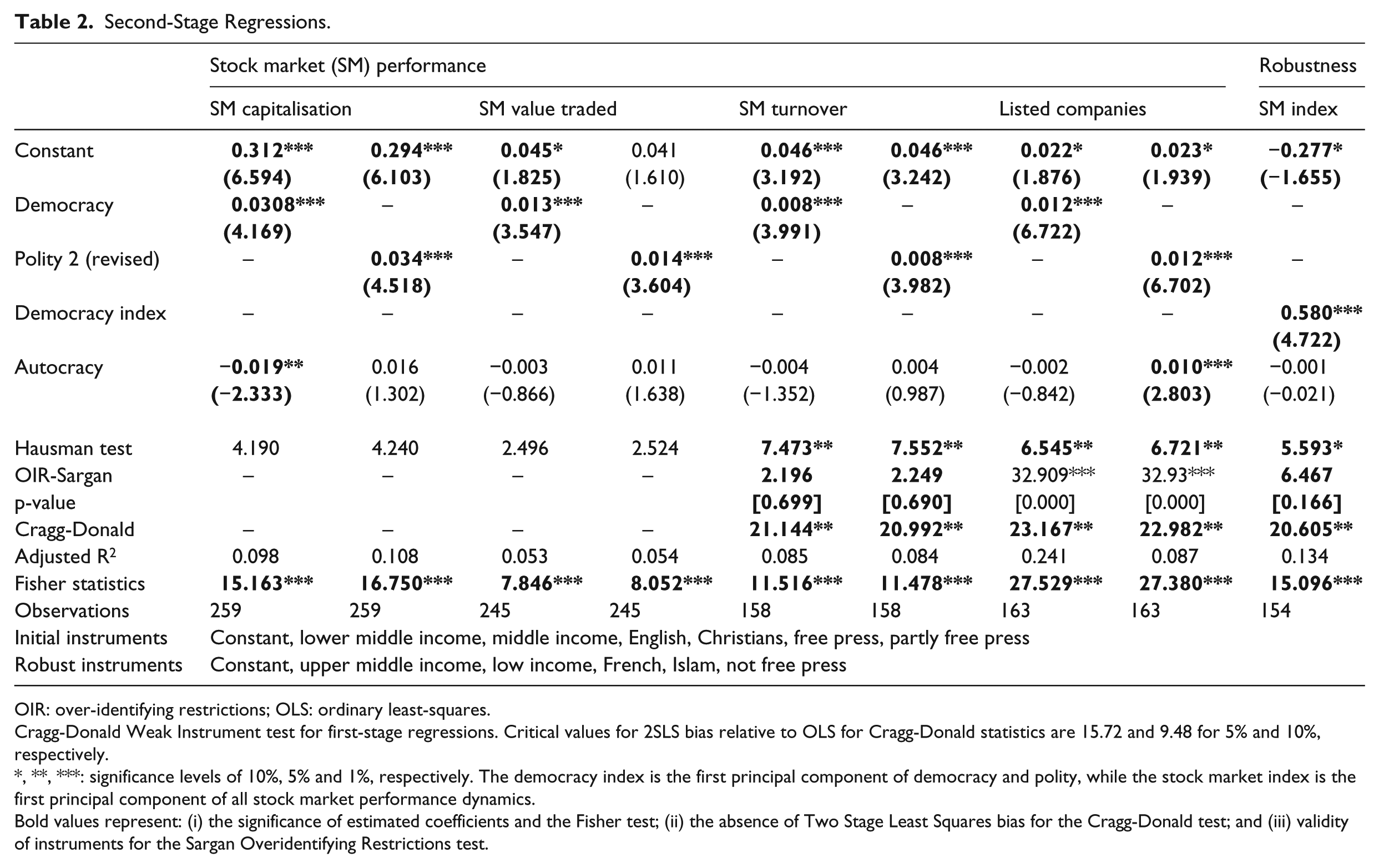

In the second-stage regressions, we first justify our choice of the IV estimation technique with the Hausman test for endogeneity. The null hypothesis of the Hausman test is the position that the estimates from OLS are efficient and consistent. Thus, a rejection of the null hypothesis reflects the presence of endogeneity and hence justifies the choice of our estimation technique. In cases where the null hypothesis of the Hausman test is not rejected (first four columns), regressions by OLS are provided. We also examine the validity and strength of the instruments with the Sargan-OIR and Cragg-Donald tests, respectively. The null hypothesis of the OIR test is the position that the instruments explain stock market performance only through political regime channels. Therefore, a rejection of the null hypothesis is a dismissal of the view that the instruments do not explain stock market performance beyond political regime channels. The Cragg-Donald test is for the strength of the instruments at first-stage regressions. Its null hypothesis is the position that the instruments are weak. Hence, its rejection confirms the strength of the instruments. While the first issue is addressed by the significance of estimated coefficients, the second issue depends on the outcome of the OIR test.

With regard to the first concern, the overwhelming significance of political regime effects on stock market performance dynamics indicates that democracy and polity positively affect stock market development, while autocracy (except for ‘listed companies’) reduces it. The signs and significance of these effects are robust to the ‘stock market index’ regressions in the last column of Table 2. With regard to the second issue which is addressed by the Sargan-OIR test, only the instruments pertaining to ‘stock market turn-over’ and ‘stock market index’ regressions are valid since their null hypotheses are not rejected. Hence, we conclude that in addition to political regime channels, the instruments explain the ‘number of listed companies’ through some other channels. Moreover, the instruments do not explain ‘stock market turnover’ and ‘stock market index’ beyond political regime channels. For all regressions that passed the Hausman test (last five columns), the instruments are strong based on the Cragg-Donald test since the critical values for 2SLS bias relative to OLS are 15.72 and 9.48 at 5% and 10% significance levels, respectively. Overall, our findings are inconsistent with Mulligan et al. (2004) because democracies have important effects on both the degree of competition for public office and the quality of public policies that favour stock market expansion in developing countries.

Second-Stage Regressions.

OIR: over-identifying restrictions; OLS: ordinary least-squares.

Cragg-Donald Weak Instrument test for first-stage regressions. Critical values for 2SLS bias relative to OLS for Cragg-Donald statistics are 15.72 and 9.48 for 5% and 10%, respectively.

*, **, ***: significance levels of 10%, 5% and 1%, respectively. The democracy index is the first principal component of democracy and polity, while the stock market index is the first principal component of all stock market performance dynamics.

Bold values represent: (i) the significance of estimated coefficients and the Fisher test; (ii) the absence of Two Stage Least Squares bias for the Cragg-Donald test; and (iii) validity of instruments for the Sargan Overidentifying Restrictions test.

Concluding Implications

This article has assessed the effect of political institutions on stock market performance in 14 African countries for which stock market data are available for the period 1990–2010. The estimation technique used is a 2SLS-IV methodology. Political regime channels of democracy, polity and autocracy are instrumented with legal-origins, religious-legacies, income-levels and press-freedom qualities to account for stock market performance dynamics of capitalisation, value traded, turnover and number of listed companies. The findings show that countries with democratic regimes enjoy higher levels of financial market development compared to their counterparts with autocratic inclinations.

Consistent with the theoretical background, democracy and good governance increase stock market development directly and indirectly by favouring, inter alia, reduced transaction and agency costs, improved corporate governance and investor protection, better enforceability of contracts, improved understanding of the agency problems between shareholders and managers, and fairness in judicial administration of conflicts. It is important to balance this narrative with the possibility that autocracy can also positively affect stock market development in the area of increasing listed firms from the political connections and the firm value literature.

Thus, this positive democracy–financial development nexus may partly elucidate the reasons why many African countries, especially those of Francophone Africa, have financial markets that are comparatively less developed (see Asongu, 2012a). The relative importance of democratic institutions in English common-law countries compared to their French civil-law counterparts also possibly provides insights into why some French-speaking countries (e.g. the Douala Stock Exchange of Cameroon) have not improved much in operational activities since they were launched. It is also interesting to note that in the post-colonial era, as of 2014, countries in Francophone Africa had accounted for much more than half of the documented political coups d’état in Africa, notably 45 versus 22 (Koutonin, 2014).

As a policy recommendation, the role of sound political institutions is crucial for financial development in Africa. Democracies have important effects on both the degree of competition for public office and the quality of public offices that favour stock market development on the continent.

Footnotes

Acknowledgements

The authors are indebted to the editor and reviewers for constructive comments on earlier versions of the article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Supplementary Information

Additional supplementary information may be found with the online version of this article.

Appendix 1: Definitions and sources of variables.

Appendix 2: Summary statistics.

Appendix 3: Correlation matrix.

Appendix 4: Categorisation of countries.

Author Biographies

![]() .

.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.