Abstract

Financial exploitation (FE) is among the most commonly reported forms of elder abuse, with older people living with dementia facing a heightened risk due to various vulnerabilities. Given its high prevalence and deleterious impact, limited research has specifically addressed this critical issue, such as the lack of studies examining risk factors and intervention strategies. Guided by the methodological framework of Arksey and O’Malley, this scoping review aims to summarize the existing literature enhancing current knowledge and raising awareness about FE in this vulnerable population. Following a structured and systematic approach based on established scoping review protocols, we systematically searched 4 scientific databases (Ageline, Medline, CINAHL, and PsycINFO) for peer-reviewed articles published in English up to July 2024, identifying 21 articles for inclusion (14 quantitative and 7 qualitative). A comprehensive data extraction process identified seven key themes, including the prevalence of FE, the relationship between FE and cognitive function, case descriptions, risk factors, warning signs, strategies to address FE, and barriers (e.g., unclear professional responsibilities) and facilitators (e.g., strong advocacy services) to safeguarding. The findings emphasize the necessity for multilevel strategies to prevent and address FE at the individual, professional, institutional, and systemic levels. Research in this field is thematically diverse yet fragmented, with limited studies directly addressing the intersection of FE and dementia. These insights underscore the need for future research (e.g., adverse effects), policy-making (e.g., mandated reporting), and intervention development (e.g., caregiver education) to better support and protect this at-risk population.

Introduction

Financial Exploitation of Older Adults

The global population aged 60 and older is growing faster than any other age group and is estimated to more than triple from 605 million in 2000 to 2 billion in 2050 (United Nations, 2017). In the United States, one in five people is expected to be 65 or older by 2030, with the older population becoming increasingly ethnically and racially diverse (Colby & Ortman, 2015). The prevalence of financial exploitation (FE) is expected to rise with the growing aging population and the recent exponential increase in reported cases (United Nations, 2017; U.S. Financial Crimes Enforcement Network, 2019). FE, defined by the National Center on Elder Abuse (2023), refers to the illegal, unauthorized, or improper use of an older person’s resources for monetary or personal benefit, profit, or gain.

At the global level, based on 52 studies from 28 countries, Yon et al. (2017) reported a pooled prevalence rate of 6.8% for FE. In the United States, current estimates suggest that 5% to 11% of older adults experience FE (Acierno et al., 2010; Beach et al., 2018; Laumann et al., 2008; Lichtenberg et al., 2016). A meta-analysis of 12 studies reported that as many as 1 in 18 community-dwelling older adults are affected by financial fraud and scams every year (Burnes et al., 2017), with FE accounting for 55% of recent nationwide hotline calls (Weissberger et al., 2020a). Additionally, a recent online survey found that 66% of older adults reported being targeted by a COVID-19-related fraud attempt (Teaster et al., 2023). Reports of FE in older adults have been growing exponentially within the last 10 years (U.S. Financial Crimes Enforcement Network, 2019), and the situation has worsened since the COVID-19 pandemic. Thus, a scoping review of related literature is necessary to address this growing challenge.

Financial losses resulting from FE are substantial, with older adults in the United States losing an estimated 28.3 billion dollars annually to FE, including abuse, scams, and fraud (Gunther, 2023). The harm extends beyond financial (e.g., reduced funds for essentials) to include relational harm to relationships (e.g., loss of trust and broken relationships) and emotional scars (e.g., shock and embarrassment; Nguyen et al., 2021). It is linked to physical health declines, including chronic conditions, difficulties with activities of daily living (ADLs; Wong & Waite, 2017), poor self-rated health (Acierno et al., 2019), and increased rates of hospitalization (Dong & Simon, 2013a) and long-term care admission (Dong & Simon, 2013b). Psychologically, it is associated with loneliness (Wong & Waite, 2017), depression (Acierno et al., 2019; Lavery et al., 2020), generalized anxiety disorder (Acierno et al., 2019), post-traumatic stress disorder (Acierno et al., 2019), and trauma symptoms (Lavery et al., 2020).

Older adults face numerous risk factors for FE, such as older age (James et al., 2014), racial minority status, particularly being African American (Beach et al., 2010; Laumann et al., 2008; Peterson et al., 2014), lower household income (Peterson et al., 2014), lower health and financial literacy (James et al., 2014), lower financial satisfaction (Lichtenberg et al., 2013), greater number of chronic physical health conditions (Hall et al., 2022), greater physical frailty (Axelrod et al., 2020), impairments in ADLs (Peterson et al., 2014), poor sleep (Weissberger et al., 2020b), worse psychological well-being (James et al., 2014), greater symptoms of depression (Lichtenberg et al., 2013; Weissberger et al., 2020b), more stress (Hall et al., 2022), lower social needs fulfillment (e.g., fewer people to turn to; Lichtenberg et al., 2013), higher interpersonal dysfunction (e.g., social dissatisfaction; Lim et al., 2023), a higher number of non-spousal household members (Peterson et al., 2014), less social support (Hall et al., 2022), and lacking a spouse or romantic partner (Laumann et al., 2008; Peterson et al., 2014). However, no reviews have summarized this literature related to cognitive impairment.

One of the most consistently indicated risk factors for FE in older adults is worse cognition (Boyle et al., 2012; Han et al., 2016). Scam susceptibility was associated with poorer global cognition, episodic, semantic, and working memory, as well as perceptual speed (James et al., 2014). Han et al. (2016) found that older adults diagnosed with mild cognitive impairment exhibited greater susceptibility to scams than cognitively unimpaired individuals, and this disparity was driven by poorer episodic memory and perceptual speed. In a longitudinal study of older adults without dementia, global cognitive decline over a 5.5-year study period was associated with worse decision-making abilities and increased scam susceptibility (Boyle et al., 2012). This vulnerability may stem from age-related changes in brain structures and functions, particularly within frontostriatal networks, which impair fluid cognitive abilities (e.g., poor attentional capacity and planning; Samanez-Larkin, 2013). These abilities are crucial for learning and decision-making in novel situations, and disruptions in these neural networks can increase susceptibility to FE by limiting individuals’ ability to make sound decisions in uncertain environments. These findings suggest that cognitive declines may impair decision-making abilities, leading to heightened financial vulnerability in aging populations.

Based on prior studies (Dessin, 2000; Hafemeister, 2003; Langan & Means, 1996; National Committee for the Prevention of Elder Abuse, 2001; Rush & Lank, 2000), Rabiner et al. (2004) summarized that potential signs of FE among general older population includes unpaid bills or eviction notices; unusual or unexplained bank activity; suspicious signatures on documents like checks; missing bank statements or canceled checks; inadequate care of an older person given their resources; changes to wills or insurance; caregiver who expresses excessive interest in the older adult’s finances; new “best friends”; missing belongings or property; overcharges for or failure to deliver caregiving services; changes in spending patterns; misuse of legal documents such as powers of attorney; and family members who refuse to pay rent or coerce the older adult into unpaid caregiving.

The Department of Health and Human Services has made several policy recommendations to address FE of older adults, including improving understanding risk factors for victimization, gaining insight into characteristics of perpetrators (e.g., motives and methods), collecting high-quality data on the incidence and prevalence of FE, examining the impact of FE (e.g., on physical and mental health), evaluating the effectiveness of money management programs, public awareness campaigns, and prevention messages, identifying key elements leading to successful prosecution of financial crimes, reducing the misuse of powers of attorney, improving the process of appointing and monitoring guardians and other fiduciaries, establishing restitution programs and increasing the likelihood that victims receive restitution and support, assuring that in-home service programs adequately safeguard older adults, providing multidisciplinary training on FE for professionals (Rabiner et al., 2004).

Common FE protective strategies include fraud awareness training, fraud awareness messaging (e.g., encouraging potential victims not to rush financial decisions), immersive training (e.g., simulated scam calls or phishing emails used to assess vulnerability of FE), technology-based solutions (e.g., call blockers), specialist training for professionals working with older adults, and social prescribing (referrals to nonclinical services to reduce isolation and mental health risks; Button et al., 2024). In their extensive review, however, Button et al. (2024) emphasized that research on FE protective strategies remains limited in terms of rigorous evaluation. The existing literature has largely focused on describing the scope of the problem, analyzing victim and offender characteristics, and examining opportunity factors, with very little empirical evidence to support the effectiveness of prevention efforts.

A recent study by Lichtenberg and Hall (2025) employed a pre–posttest design to evaluate the effects and acceptability of a three-session FE prevention intervention for older adults, which included content such as FE vulnerability and techniques used by scammers. The study found significant improvements in financial literacy and reductions in financial vulnerability from baseline to post-intervention, representing a promising direction for future research on protective strategies. Given that prior research has primarily focused on the general older population, our scoping review is particularly important for mapping the evidence and highlighting unmet needs among older people living with dementia (PLWD), a group with distinct vulnerabilities that has received limited attention in existing research.

Financial Exploitation Among Older People Living with Dementia

FE is one of the most prevalent forms of abuse among older PLWD (Vida et al., 2002). Dementia refers to a group of conditions characterized by a progressive decline in cognitive functioning, self-care abilities, and physical independence (Alzheimer’s Association, 2016). Common types of dementia include Alzheimer’s disease, Parkinson’s disease, vascular dementia, and dementia with Lewy bodies. The risk of developing dementia increases dramatically with age, affecting approximately 2% of individuals aged 65 to 70 and rising to 20% among those over 80. PLWD often experience cognitive decline, impairing decision-making, problem-solving, memory, reasoning, and judgment (Alzheimer’s Association, 2020). These cognitive deficits increase their susceptibility to FE (Boyle et al., 2012; James et al., 2014). For instance, Rogers et al. (2023) reported that FE was significantly more common among older PLWD (47%) compared to those without (39%). The economic burden of FE is further complicated by the burden of dementia, with an estimated annual cost of $818 billion worldwide, representing 1.1% of the global gross domestic product (World Health Organization, 2017a, 2017b). Total spending on healthcare, long-term care, and hospice services for dementia patients aged 65 and older in the United States was estimated at $305 billion in 2020. Thus, supporting the need for a scoping review on the available literature related to FE of PLWD.

Examples of FE in PLWD include a daughter and son-in-law who depleted over $200,000 from an older PLWD’s accounts and sold her property, resulting in criminal convictions (Lawrence et al., 2022), and home care workers stealing money and valuables from PLWD in senior housing settings (Jang et al., 2023). Factors such as reduced ability to assess risks and living alone can further increase their vulnerability, while dementia itself can obscure the detection of FE (Alzheimer’s Society, 2011). Systemic challenges exacerbate these risks. For example, cultural barriers within professional groups and organizations often hinder the reporting of abuse, as some health professionals perceive it as outside their duties. Banking procedures frequently fail to address the specific needs of PLWD, and a lack of dementia awareness among service providers, together with inconsistencies in applying safeguarding laws, further worsen older adults’ vulnerabilities. The process for Lasting Power of Attorney (LPA) and Court of Protection applications was also criticized as being too slow (Alzheimer’s Society, 2011). These challenges underscore the need for a comprehensive understanding of the research to support the development of more effective strategies to protect this at-risk population.

FE in PLWD often goes unnoticed due to victims’ reduced cognitive capacity to recognize and report abuse (Borza et al., 2011), fear of retaliation or losing support (Burgess & Phillips, 2006), and neglect or oversight by potential interveners (Alzheimer’s Society, 2011). This invisibility further complicates efforts to assist this vulnerable population. A scoping review can provide a clearer understanding of FE in PLWD, enhance knowledge and awareness, and identify gaps in the literature.

The Current Study

To our knowledge, no review has comprehensively mapped the literature on FE among older PLWD. This may be due to the low reporting rates of findings for PLWD in the literature, including studies that may include this population as a subset but do not differentiate findings, as well as barriers to obtaining consent for PLWD, particularly those at more advanced stages of their diagnosis. As a result, we propose to conduct a scoping review to address our research questions. A scoping review is a study that captures a broad range of literature on a given topic, typically guided by a broader research question (in contrast to other systematic review types, which may have more specific research questions or use different methods; Arksey & O’Malley, 2005). Our scoping review aims to address this gap by exploring the extent, range, and nature of studies in this field, thereby improving our current knowledge and highlighting areas for future research, policy-making, and intervention development. Additionally, we seek to raise awareness among the public and professionals about the issues surrounding FE in the context of dementia by summarizing key signs, risks, and guidance for recognizing and addressing it, with the goal of preventing victimization and identifying effective protective interventions for PLWD. This review may also inform practice, such as helping professionals identify individuals at risk and support caregivers in implementing protective strategies. Based on Peters et al.’s (2020) and Riva et al.’s (2012) guidance, the research questions are as follows: (a) What topics related to FE among older PLWD have been studied in the existing peer-reviewed empirical literature and (b) What gaps exist in the current literature on FE among older PLWD that suggest directions for future research, policy, and development of protective strategies. Our study strives to summarize the existing evidence and provide a foundation for evidence-based decisions to better care for this vulnerable population.

Methodology

This study was guided by a scoping review methodological framework (Arksey & O’Malley, 2005; Peters et al., 2020), which is designed to examine the extent, range, and nature of existing literature, identify research gaps, map key concepts relevant to the research focus, and summarize findings for dissemination. Key themes were charted, and the results were analyzed to reveal structural themes related to FE among older PLWD.

Search Strategy

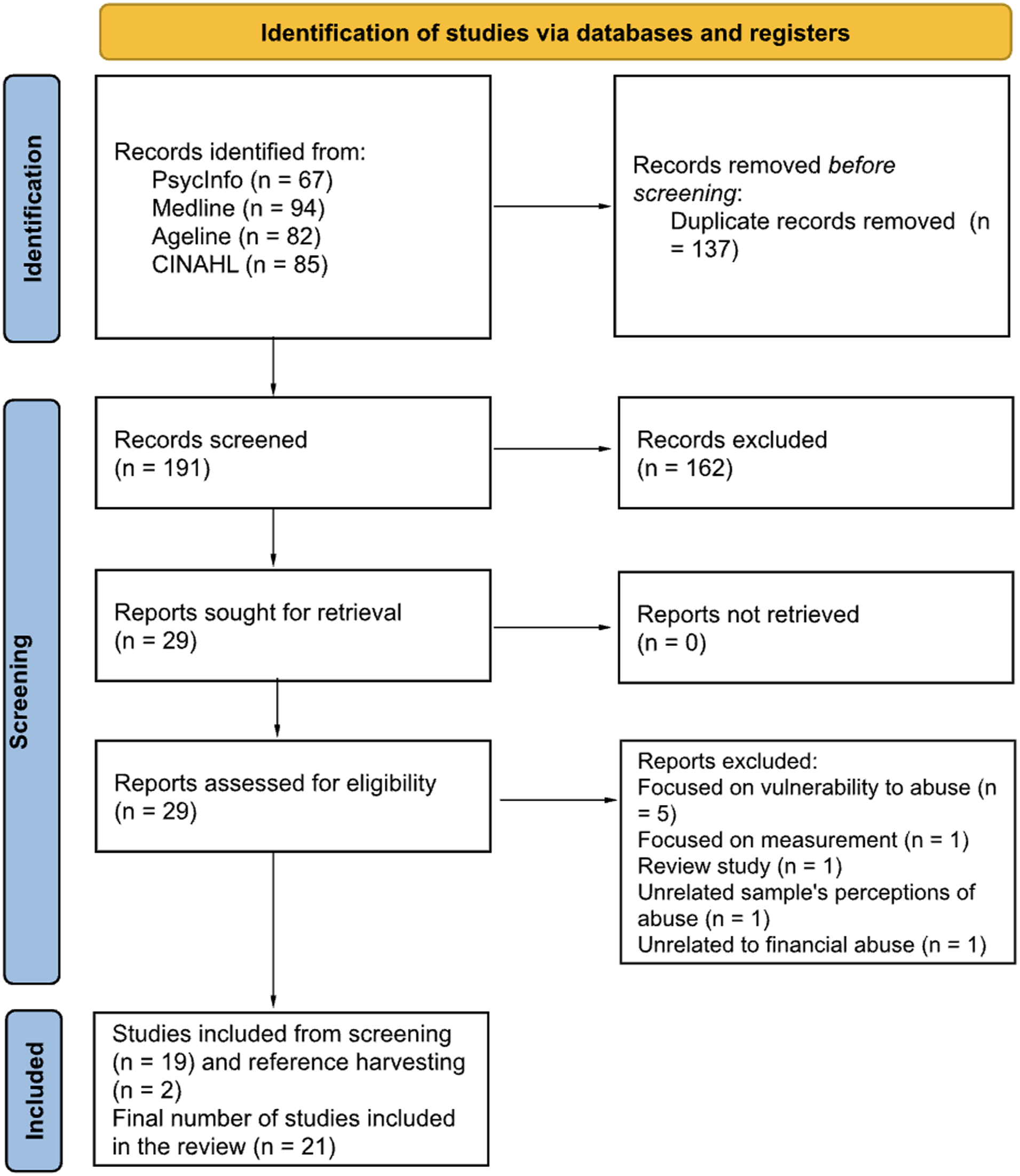

This scoping review adhered to the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) guidelines (Liberati et al., 2009). With consultation of university librarians, we finalized search terms and searched the following electronic bibliographic databases: Ageline, Medline, PsycINFO (American Psychological Association), and the Cumulative Index to Nursing and Allied Health Literature (CINAHL). These databases were chosen to find relevant peer-reviewed articles across several disciplines, such as social welfare, psychology, medicine, and nursing, to construct a comprehensive picture of FE in older PLWD. The search string used for the database was: (“scams” or “fraud” or “financial exploitation” or “financial abuse” or “economic abuse” or “identity theft” or “identity-theft” or “impersonation” or “phishing” or “catfishing”) AND (“aged” or “older adults” or “older people” or “elder*” or “geriatric” or “senior citizens” or “over 60” or “over 65”) AND (“dementia” or “Alzheimer’s” or “cognitive impairment” or “memory loss” or “neurocognitive disorders”). The search was completed in July 2024, and outcomes were reported using the PRISMA flow diagram (see Figure 1).

PRISMA 2020 flow diagram (Page et al., 2021).

Inclusion and Exclusion Criteria

The inclusion criteria were: (a) the article is about FE; (b) the article includes older adults; (c) the article includes PLWD; (d) the article is empirical. To maximize the number of included articles, no limitation on publication date was applied as studies on the FE of PLWD are scarce. This broader timeframe allowed us to examine the phenomenon more comprehensively, capturing a wider range of research and insights across contexts. A historical perspective helps provide a fuller understanding of FE as a persistent and evolving issue, highlighting patterns, gaps, and shifts in how it has been studied and addressed over time. The exclusion criteria were: (a) the publication type is a systematic review/scoping review/meta-analysis/literature review/editorial/book chapter; (b) the article is gray literature or not empirical; (c) the article is not in the English language. For review studies, screeners retrieved and harvested references for potentially relevant articles. Studies were limited to peer-reviewed empirical literature to aid comparison of findings and ensure that the included studies were methodologically rigorous. We chose to include any peer-reviewed empirical study, including case studies, to capture a broad range of the literature. Articles not written in English were excluded due to the research team’s linguistic capabilities.

Screening and Data Extraction

After removing the duplicates, two screeners (WW and SB) independently screened the titles and abstracts based on the inclusion and exclusion criteria. The full text was reviewed when eligibility could not be determined from the abstract. If the full text was not available, Screener 1 obtained the full text through assistance from the University librarians. The initial interrater reliability was calculated using Cohen’s kappa coefficient (Viera & Garrett, 2005). Screeners 1 and 2 were able to reconcile any coding disagreements through discussion and consensus on the final codes. Screener 1 sifted, charted, and sorted material from each included article independently, systematically extracting key information. The extracted data were entered into Supplemental Table 1, which includes details such as study participants, data sources, study design, measures, and findings. Screener 2 reviewed the table, providing feedback to ensure accuracy and comprehensiveness. Both screeners then discussed and finalized Supplemental Table 1 collaboratively. Together, the screeners identified key issues and themes based on recorded data. The Mixed Methods Appraisal Tool (MMAT) version 2018 was used to assess the quality of articles (Hong et al., 2018). Scores were summed to generate an overall quality rating for each article on a scale of 1 to 5, with 5 being the highest quality. The range of publication dates of the screened articles is from 1983 to 2024, with the 21 articles included from 1999 to 2023.

Results

Search Results

A total of 328 articles were identified across the 4 databases (see Figure 1). After removing the duplicates, 191 citations were screened. After screening and reconciling by Screener 1 and Screener 2, 162 articles were excluded because they did not meet the inclusion criteria, leaving 29 for inclusion. The interrater reliability of the article screening process, as measured by Cohen’s kappa coefficient, was substantial at .82 (Viera & Garrett, 2005). During the full-text screening, 10 articles were excluded because they were outside the scope of the review (see Figure 1 for details). We extracted references from 7 review articles among the 191 citations, identifying 2 additional relevant articles. In total, 21 articles were included in the review.

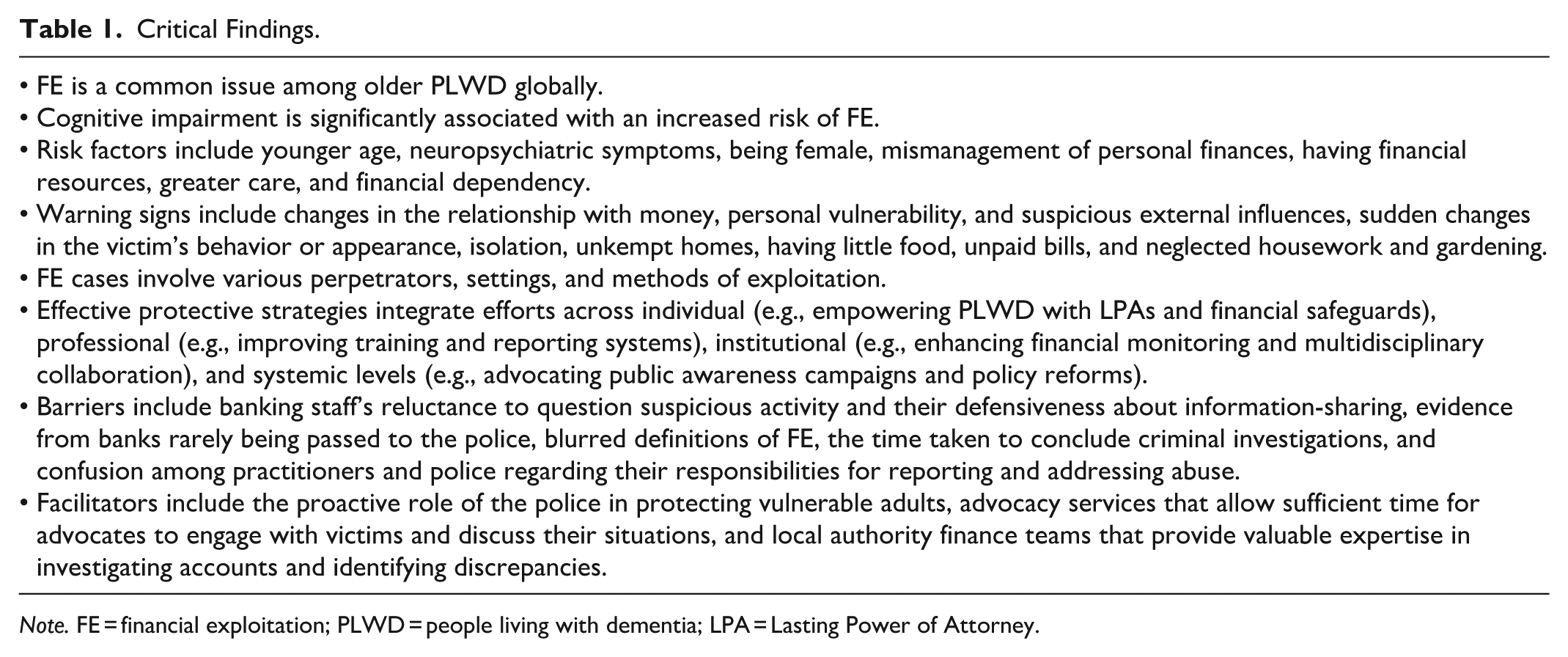

The characteristics of the 21 included articles are detailed in Supplemental Table 1, showing a diverse range of contexts and populations from multiple countries. These countries include the United States, Japan, Norway, China, the United Kingdom, Australia, and Canada. Among them, 20 were cross-sectional, and 1 was longitudinal. The samples varied in origin, with nine using community-based samples, six using facility-based samples, four using administrative data samples, and two using professional-based samples. Some articles utilized samples from the same datasets, including Health and Retirement Study (HRS; Lichtenberg et al., 2013, 2016) and a dataset collected from public hospitals in Guangdong Province, China (Fang & Yan, 2021; Fang et al., 2019, 2023). The review covered articles with various participant groups: six articles included older PLWD (either the entire sample or a portion of it; Chan et al., 2009; Dong et al., 2011; Heath et al., 2005; Koga et al., 2022; Lawrence et al., 2022; Vida et al., 2002), three articles did not specify the proportion with dementia but reported important findings related to cognitive impairment and FE (Lichtenberg et al., 2013, 2016; Moon et al., 2013), three articles included informal caregivers of PLWD only (Harrington et al., 2023; Jang et al., 2023; Steinsheim et al., 2022), four articles included both informal caregivers of PLWD and their care recipients (Anetzberger, 2005; Fang & Yan, 2021; Fang et al., 2019, 2023), two articles included professionals working in adult safeguarding and dementia care (Manthorpe et al., 2012; Samsi et al., 2014), and three articles included older adults with reported or suspected mistreatment (e.g., Choi et al., 1999; Gassoumis et al., 2015; Rogers et al., 2023). See Table 1 for a summary of critical findings.

Critical Findings.

Note. FE = financial exploitation; PLWD = people living with dementia; LPA = Lasting Power of Attorney.

Assessment of Methodological Quality

In general, the articles included in this scoping review demonstrated moderate to high quality, as assessed by the MMAT (Hong et al., 2018). Of the 21 articles reviewed, 1 received a 3-star rating, indicating moderate quality (Anetzberger, 2005). This article had limitations, including the use of data collection methods inadequate to address the research question and a lack of coherence between qualitative data sources, collection, analysis, and interpretation. In addition, 11 articles had a 4-star rating due to concerns such as the risk of nonresponse bias, the representativeness of the sample, the validity and reliability of the measurements, and the discussion of divergences and inconsistencies between quantitative and qualitative results (Choi et al., 1999; Fang & Yan, 2021; Fang et al., 2019, 2023; Gassoumis et al., 2015; Koga et al., 2022; Lichtenberg et al., 2013, 2016; Samsi et al., 2014; Steinsheim et al., 2022; Vida et al., 2002). Nine articles received a high 5-star rating (Chan et al., 2009; Dong et al., 2011; Harrington et al., 2023; Heath et al., 2005; Jang et al., 2023; Lawrence et al., 2022; Manthorpe et al., 2012; Moon et al., 2013; Rogers et al., 2023). See Supplemental Table 1 for details and see Table 1 for a summary of critical findings.

Prevalence of FE

FE among older PLWD has been reported across multiple countries. In the United States, an article with 575 older veterans found that 40% of elder abuse victims with dementia experienced FE (Moon et al., 2013). In the United Kingdom, FE was among the most common forms of elder abuse, reported in 43% of cases, with a higher prevalence among those with dementia compared to those without (47% vs. 39%; Rogers et al., 2023). Additionally, half of 86 Alzheimer’s Society staff reported that PLWD they supported had encountered FE in the past year (Samsi et al., 2014). Adult safeguarding coordinators (ASCs) also frequently identified such cases (Manthorpe et al., 2012). In Norway, 3.9% of 549 caregivers admitted to financially abusing PLWD, while 1.1% reported experiencing FE from them (Steinsheim et al., 2022). In Canada, FE was the most frequently reported form, accounting for 13% of cases among older adults with cognitive disorders (Vida et al., 2002). In China, FE was the second most common form of abuse among 1,002 older adults (79.8% with dementia) and caregivers, with a mutual reporting rate of 33.2% by both care recipients and caregivers (Fang et al., 2019). Fang and Yan (2021) found considerable variation in prevalence, ranging from 17.9% to 40.8%, depending on the reporting sources and operational definition. For example, self-reports by care recipients yielded 40.8% (lenient definition) and 39.4% (restrictive definition), compared with 34.2% and 32.3% for caregiver reports. Care recipients consistently reported higher FE rates than caregivers, which may reflect cultural factors such as familism and face-saving tendencies (Fang et al., 2023). Overall, FE is a significant concern among older PLWD. In some studies, it accounts for nearly half of all abuse cases (Moon et al., 2013; Rogers et al., 2023; Samsi et al., 2014).

Relationship Between FE and Cognitive Function

Many articles have identified a significant relationship between FE and cognitive impairment. For example, in a sample of 386 older adults reported to Adult Protective Services (APS) in Erie County, the United States, those who were financially exploited tended to be cognitively impaired (Choi et al., 1999). Similarly, in an article of 238 older adults reported for elder abuse to a social services agency in Chicago, the United States, lower levels of cognitive function were associated with an increased risk of FE (Dong et al., 2011). Another article, based on 472 older adults reported for suspected FE in Los Angeles County, the United States, found that suspected cognitive impairment was significantly associated with FE (Gassoumis et al., 2015). In New Jersey, an article focusing on 211 APS clients found that diagnosis of dementia was positively correlated with FE among female clients (Heath et al., 2005). Research in China also suggested that FE was more likely to occur among those suffering from cognitive impairment and dementia (Fang et al., 2019). Importantly, a longitudinal article involving a sample of 12,236 older adults in Japan revealed that participants who experienced FE were 1.53 times more likely to develop dementia than those who did not during the follow-up period of 6 years (Koga et al., 2022).

However, not all articles have observed significant relationships. Analyses of U.S. national data from the HRS found no significant differences in cognitive function between fraud victims and non-victims (Lichtenberg et al., 2013, 2016). In addition, regression analysis indicated that fraud victimization was not significantly related to cognitive functioning (Lichtenberg et al., 2013).

Description of FE Cases

Several articles provided detailed descriptions of FE cases. There were two types of perpetrators identified from FE cases, including close contact (e.g., family and friends) and professional exploitation. In cases of close contact exploitation, Anetzberger (2005) described a family caregiver who exploited her mother’s savings, rationalizing it as compensation for caregiving. The caregiver’s young daughter also misused funds, exacerbating tensions in the caregiving relationship. Harrington et al. (2023) highlighted family members and trusted friends engaging in financial misconduct, such as unauthorized withdrawals, fraudulent checks, and mismanagement of funds under the power of attorney. Moon et al. (2013) documented numerous cases in which friends, neighbors, or family members gained control of and drained veterans’ bank accounts or where power of attorney was sought or granted while the veterans lacked decisional capacity. Three-quarters of these abuses were perpetrated by nonfamily members, such as friends, neighbors, and even casual acquaintances. In Lawrence et al. (2022), a daughter and son-in-law systematically depleted over $200,000 from the accounts of an older PLWD and fraudulently sold her property. Their financially motivated actions were accompanied by severe neglect, ultimately leading to the victim’s death and criminal convictions.

In cases of professional exploitation, Jang et al. (2023) described incidents reported by a spousal caregiver in senior housing, where home care workers stole money or valuables from older PLWD. Chan et al. (2009) described a case where domestic helpers exploited an older adult with Alzheimer’s disease, facilitating financial transactions worth significant sums. Legal interventions, including guardianship, were implemented to protect the individual’s assets. For example, the Guardianship Board of Hong Kong issued recommendations to the public guardian (e.g., reporting the victim’s case to the central elder abuse registry) and to the domestic helpers (e.g., surrendering all personal items belonging to the victim and leaving the victim’s premises immediately). The victim was eventually admitted to a private aged home.

Risk Factors of FE

Four types of risk factors emerged, including cognitive, demographic, social, and economic factors. First, some studies highlighted cognitive risk factors. In a sample from China (79.8% with dementia), Fang et al. (2019) found that FE was more likely among younger elders and those suffering from neuropsychiatric symptoms. In a U.S. sample of informal caregivers for individuals with Alzheimer’s disease or related dementias, Harrington et al. (2023) found that a person’s mismanagement of personal finances due to lack of executive function or memory could lead to FE. Second, in terms of demographic risk factor, Heath et al. (2005) observed that women referred for APS assessment were more likely to experience FE than men in a group of APS clients (62% with dementia) in the United States. Third, a study highlighted an economic risk factor. In a U.K. sample, Manthorpe et al. (2012) noted that having financial resources in old age can increase vulnerability to FE rather than providing protection, as some relatives may be driven by financial gain. Last, another study highlighted a social risk factor. In a U.K. sample, Rogers et al. (2023) found that older PLWD were more likely to be financially dependent on perpetrators, dependent on others for care, and in need of daily care. This finding, combined with their increased risk of FE, suggests that care and financial dependency may increase the risk of FE.

Warning Signs of FE

Manthorpe et al. (2012) identified warning signs of FE. For victims, warning signs included sudden changes in behavior and appearance, and being isolated. In terms of the environment or social situation, warning signs included unkempt homes, having little food, unpaid bills, and neglected housework and gardening. Furthermore, Samsi et al. (2014), in a qualitative article involving Alzheimer’s Society staff, identified three overarching triggers of FE: changes in a client’s relationship with money (e.g., being gradually more confused about money, no longer recognizing the value of money or how much things cost, and diminishing self-protective strategies); a client’s vulnerability (e.g., being alone, offering unguarded access to strangers, confusion about whom to trust, lack of basic provisions, and stopping eating regular meals); and suspicious external interest or influence (e.g., suspicious visitors to a client’s house, an increase in junk or scam mail or telephone calls, unnecessary repairs or home alterations, and changes in financial arrangements).

Strategies to Address FE

Various articles have proposed strategies to safeguard PLWD from FE. Safeguarding adults can be broadly defined as a set of activities aimed at protecting individuals who are unable to protect themselves from abuse, with a focus on the protection of their human rights (Duffy et al., 2025). These strategies integrate efforts across individual, professional, institutional, and systemic levels, each playing a distinct yet interconnected role.

At the individual level, Samsi et al. (2014) suggested that PLWD should take the initiative to safeguard their financial affairs when diagnosed. Measures such as establishing an LPA (Manthorpe et al., 2012; Samsi et al., 2014), setting up direct debits to pay bills (Manthorpe et al., 2012), restricting access to financial details (Manthorpe et al., 2012), and reducing exposure to scams through strategies like barring unsolicited calls (Manthorpe et al., 2012) were identified as practical steps to reduce vulnerability.

At the professional level, safeguarding strategies focus on equipping practitioners with the necessary tools and knowledge to effectively prevent and address FE. This includes prioritizing an individual’s decision-making capacity over the dementia diagnosis when assessing risk, increasing care plan reviews, strengthening audit trails, utilizing services from local authorities, setting up safeguarding plans, building supportive networks (Manthorpe et al., 2012), reporting suspected abuse to local authorities, providing post-diagnosis support to PLWD, and offering training to professionals (Samsi et al., 2014).

Institutional strategies emphasize preventive measures, intervention protocols, and multidisciplinary collaboration. Financial institutions can implement regular monitoring, audits, and improved data sharing with social services to detect and prevent FE (Samsi et al., 2014). Contractual arrangements also help mitigate risks (Manthorpe et al., 2012). Interventions may involve moving veteran victims from unsafe homes into nursing homes and conservatorship arrangements (Moon et al., 2013). Additionally, the role of multidisciplinary teams in identifying and managing abuse cases was highlighted (Chan et al., 2009; Manthorpe et al., 2012; Samsi et al., 2014). For example, Chan et al. (2009) emphasized the important role of geriatrician-led multidisciplinary teams, with frontline hospital workers identifying and providing timely management, psychiatrists assessing the victim’s mental capacity, and the Guardianship Board protecting the victim’s interests. Manthorpe et al. (2012) also highlighted the value of collaborative work with other agencies such as the police, banks, and social services.

At the systemic level, policy reforms are crucial to safeguarding older PLWD. Measures such as making LPAs more accessible and criminalizing FE were identified as critical systemic interventions (Samsi et al., 2014). Public awareness campaigns and strategies for public protection were also emphasized to inform families and communities about FE and the steps they can take to prevent it (Manthorpe et al., 2012). Although many PLWD prefer nonformal resolutions, authorities might still proceed with investigations when necessary to protect the safety of the wider community (Manthorpe et al., 2012).

Barriers and Facilitators to Safeguarding

Manthorpe et al. (2012) identified barriers to safeguarding efforts. Many ASCs noted banking staff’s reluctance to question suspicious activity and their defensiveness about information-sharing. The relationship between banks and the police posed further challenges, as evidence from a bank was rarely passed to the police, and hence, investigations did not proceed or were delayed. Some respondents discussed cultural barriers arising from blurred definitions of FE (e.g., a kindly neighbor overcharging for good service or a carer using her mother’s money for a holiday, claiming it was aligned with her mother’s wishes). In terms of systemic barriers, some ASCs criticized the time it took to conclude criminal investigations and confusion among practitioners and police regarding their responsibilities for reporting and addressing abuse.

Despite these barriers, respondents highlighted some facilitators in safeguarding (Manthorpe et al., 2012). The police were viewed as strong partners in protecting vulnerable adults. Advocacy services were highlighted for their role in giving advocates the time needed to engage with victims and discuss their situations. Additionally, local authority finance teams provided valuable expertise in investigating accounts and identifying discrepancies.

Discussion

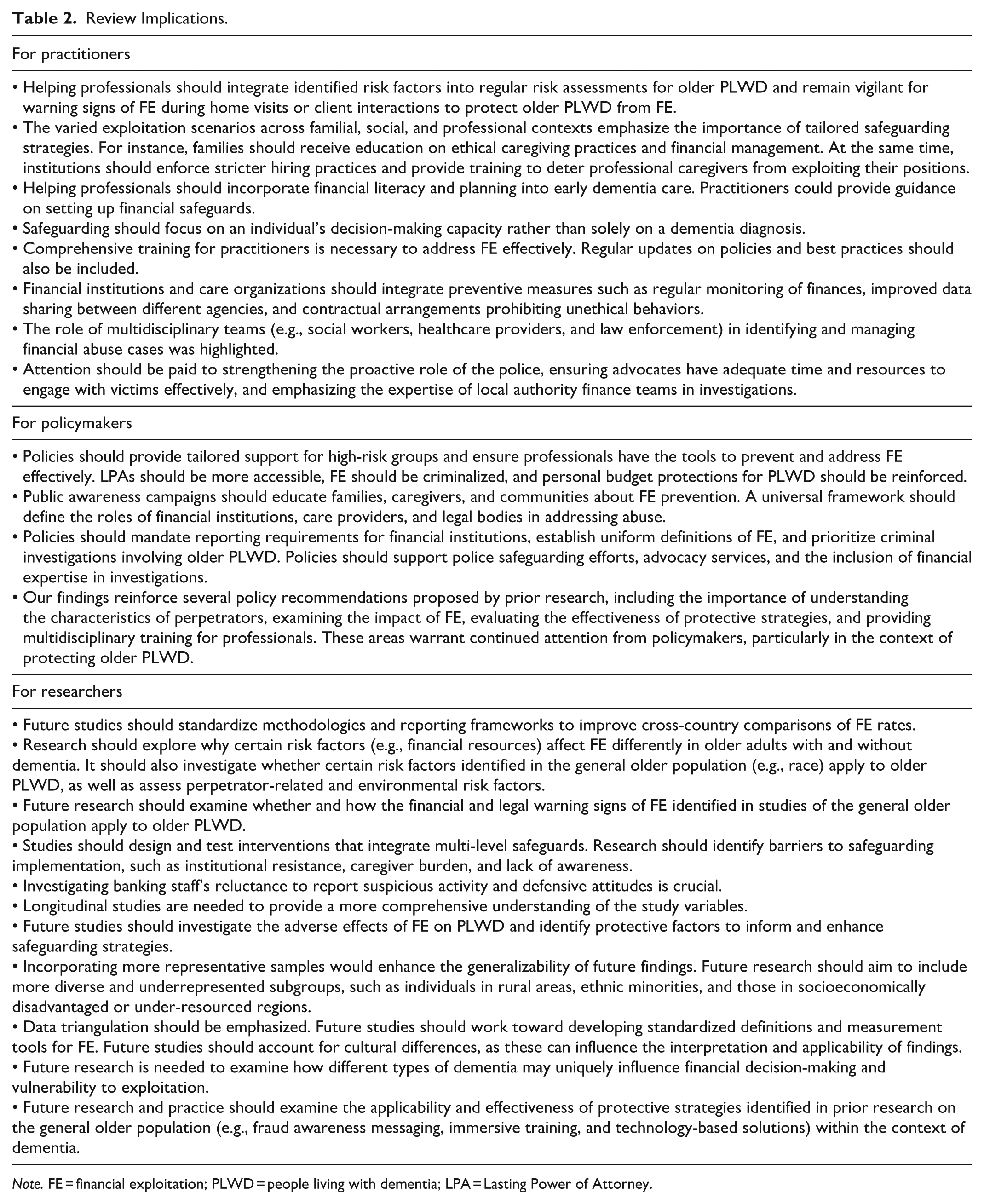

The purpose of this scoping review is to summarize existing literature to enhance current knowledge, raise awareness, and identify research gaps related to FE among older PLWD by examining the extent, range, and nature of studies in this field. Our review is the first to review current literature on this topic. This review contributes to the gap in knowledge in the existing body of literature by identifying seven key themes, including the prevalence of FE, the relationship between FE and cognitive function, case descriptions, risk factors, warning signs, strategies to address FE, and barriers and facilitators to safeguarding. The implications of this review for practice, policy, and research are summarized in Table 2.

Review Implications.

Note. FE = financial exploitation; PLWD = people living with dementia; LPA = Lasting Power of Attorney.

Key Findings and Implications

Our review found that FE among older PLWD was frequently reported as one of the most prevalent forms of abuse in various countries, including the United States (Moon et al., 2013), the United Kingdom (Manthorpe et al., 2012; Rogers et al., 2023; Samsi et al., 2014), Canada (Vida et al., 2002), and China (Fang et al., 2019). It is challenging to compare the rates between articles or previous studies focusing on older adults without dementia due to differences in geographic regions, the proportion of PLWD in the sample, whether the article focused on victims of abuse or not, and the sources of reporting. However, it is evident that the rate of FE remains high among individuals with and without dementia.

Future studies should aim to adopt standardized methodologies and implement consistent reporting frameworks to address these discrepancies and enable more accurate comparisons of FE rates across countries, settings, and populations. Addressing methodological inconsistencies, such as differences in sampling strategies, study focus, and population characteristics, would contribute to a more comprehensive understanding of this issue and inform future research and practice. For instance, only one article reported the rate of financial abuse among older adults with dementia in the United States. Future studies should aim to report rates among broader populations, such as community-dwelling older adults. Additionally, only articles from China (e.g., Fang & Yan, 2021) compared the prevalence reported by care recipients and caregivers. Future studies should include information from multiple sources, such as older adults, their caregivers, and professionals. Similarly, only Fang and Yan (2021) examined how different definitions of FE (lenient vs. restrictive) and data collection methods (observation-based instruments vs. self-report) affected reported prevalence, an important consideration for future studies to get a fuller picture of FE. Cultural differences should also be considered. Different cultural contexts can significantly influence perceptions and definitions of elder abuse, particularly in dementia care (Mahoney et al., 2005). Some articles highlighted how cultural factors, such as cultural barriers around blurred definitions of FE (Manthorpe et al., 2012) and familism and face-saving tendencies in Chinese culture (Fang et al., 2023), may influence reporting and perceptions of FE. Future research should further investigate how cultural factors, such as norms, expectations, and stigma, influence the interpretation and applicability of findings.

The current study identified numerous articles indicating that cognitive impairment is significantly associated with FE in the United States (Choi et al., 1999; Dong et al., 2011; Gassoumis et al., 2015; Heath et al., 2005), China (Fang et al., 2019), and Japan (Koga et al., 2022). However, Lichtenberg et al. (2013) found no significant relationship between cognitive functioning and fraud victimization. This discrepancy may be due to the measurement of fraud victimization, which was assessed using a single item: “Have you been the victim of financial fraud in the past 5 years?” with a binary Yes or No response. Such a simplistic measure may limit the ability to capture the complexity of the relationship. Future research should prioritize using reliable and valid measurement tools that better capture the complexity and variability of FE. Contextual and sample differences may also contribute to conflicting findings. Among all the articles conducted in the United States, only Lichtenberg et al. (2013) used nationally representative data. The influence of sample characteristics (e.g., national vs. local) and contextual factors (e.g., geographic region) is crucial for future research to consider.

The detailed case descriptions in the reviewed articles provide critical insights into the multifaceted nature of FE involving older PLWD. These cases involve various perpetrators (e.g., family members, friends, professional caregivers, and casual acquaintances), settings (e.g., home and senior housing), and methods of exploitation (e.g., unauthorized withdrawals, fraudulent checks, misuse of power of attorney, and fraudulent property sales), underscoring the urgent need for adequate safeguards. The varied scenarios of exploitation across familial, social, and professional contexts emphasize the importance of tailored prevention strategies. For instance, families should receive education on ethical caregiving practices and financial management. At the same time, institutions should enforce stricter hiring practices and provide training to prevent exploitation by professional caregivers.

Our review identified several risk factors for FE among older PLWD, such as younger age (Fang et al., 2019), mismanagement of personal finances (Harrington et al., 2023), and having financial resources (Manthorpe et al., 2012). Notably, all these factors are victim-related. Future research should examine other levels of risk, such as those related to perpetrators or environmental contexts. Financial incapacity has been identified in both older adults without dementia (James et al., 2014) and older PLWD (Harrington et al., 2023). However, certain findings conflict. For instance, James et al. (2014) found that older age was a risk factor for scams among older adults without dementia, whereas Fang et al. (2019) found that younger age was associated with an increased risk of FE in a Chinese sample of older adults (79.8% with dementia). Fang et al. (2019) also discovered that chronic illness was associated with a lower likelihood of FE, while Hall et al. (2022) identified a greater number of chronic physical health conditions as a risk factor in the general older population. Additionally, Peterson et al. (2014) identified lower household income as a risk factor for FE in the general older population, while Manthorpe et al. (2012) found that having financial resources could increase the risk factor for FE for older PLWD.

These contradictions underscore that risk factors for FE may present differently among older adults with and without dementia. These examples from our review, in contrast to related literature not focused on PLWD, highlight the importance of further exploring the underlying mechanisms that drive these differences, as PLWD were consistently found to have unique experiences compared to older adults without dementia. These discrepancies also highlight the need for further research to explore why such conflicts exist. Future studies should also investigate whether certain risk factors identified in the general older population, such as race (particularly being African American), physical and mental health, and social support, are applicable to older PLWD. Moreover, our review did not identify articles that explored protective factors against FE among PLWD, which future research should address.

The current review identified warning signs of FE, including sudden changes in the victim’s behavior or appearance, being isolated, unkempt homes, having little food, unpaid bills, neglected housework and gardening (Manthorpe et al., 2012), changes in relationship with money, personal vulnerability, and suspicious external influences (Samsi et al., 2014). These findings highlight the importance of proactive monitoring and assessment by helping professionals during home visits or client interactions. Early recognition and response to these indicators can enable timely interventions. While our scoping review focused on FE among older PLWD, previous research on the general older population has identified additional warning signs that were not found in our review, such as suspicious signatures on financial documents, missing bank statements or canceled checks, changes to wills or insurance policies, and misuse of legal documents such as powers of attorney (Rabiner et al., 2004). These signs, which are largely financial and legal in nature, may manifest differently or be more difficult to detect in PLWD due to cognitive decline. Future studies should explore whether and how these indicators may apply to older PLWD.

The findings from this review highlight the necessity of a multilevel, collaborative approach to preventing and addressing FE among older PLWD. While a multilevel framework of safeguarding strategies has been proposed, most studies did not evaluate the effectiveness or feasibility of these approaches, likely because they were based on case descriptions (Chan et al., 2009) or practitioner opinions (Manthorpe et al., 2012; Samsi et al., 2014). More research is needed to formally evaluate interventions. Only Moon et al. (2013) reported on service engagement, noting that 5 of 31 victims declined services, and 6 neither reconnected with the provider nor could be located. More evidence is needed to determine whether these strategies are effective (e.g., achieving intended goals). These gaps echo Button et al.’s (2024) concern about the lack of rigorous effectiveness evaluation. Our findings support several of the protective strategies identified by Button et al. (2024), which focus on the general older population. For example, our study highlights the importance of raising awareness among caregivers, training professionals to recognize exploitation, and addressing caregiver burden and social isolation. However, other strategies discussed by Button et al. (2024), including fraud awareness messaging, immersive training, technology-based solutions, and social prescribing, were not reflected in the studies we reviewed. Future research and practice should explore the applicability and effectiveness of these approaches among PLWD.

The barriers and facilitators to safeguarding identified in our study offer important guidance for practice, policy, and research. To address these barriers, training programs are required to help banking staff recognize and act upon suspicious financial activities, understand their responsibilities in safeguarding clients, and communicate effectively with law enforcement. Policies should establish clear, legally mandated reporting requirements for banking institutions to share evidence of FE with law enforcement or safeguarding authorities. Uniform definitions of FE across legal, financial, and social care sectors should be implemented to eliminate ambiguity and facilitate consistency in abuse identification and intervention. Additionally, policies should prioritize and expedite criminal investigations related to FE, particularly those involving older PLWD. Research is needed to explore the factors behind banking staff’s reluctance to report and investigate best practices for cross-sector collaboration.

In light of the identified facilitators, practice efforts should focus on strengthening the proactive role of the police, ensuring advocates have adequate time and resources to engage with victims effectively, and emphasizing the expertise of local authority finance teams in investigations. Policies should support the police’s role in safeguarding efforts, provide funding and resources for advocacy services, and require the inclusion of financial expertise in safeguarding frameworks to improve investigative outcomes.

Overall, our review addresses several policy recommendations proposed by the Department of Health and Human Services (Rabiner et al., 2004), including improving the understanding of risk factors for victimization and collecting high-quality data on the incidence and prevalence of FE. In addition, our findings reinforce the importance of gaining insight into the characteristics of perpetrators, examining the impact of FE, evaluating the effectiveness of protective strategies, and providing multidisciplinary training for professionals. Future studies should continue to build on these aligned priorities, with a particular focus on addressing the specific vulnerabilities and contextual challenges faced by PLWD. For example, although some prior studies have explored the impacts of FE among older adults, such as difficulties with ADLs (Wong & Waite, 2017) and depression (Acierno et al., 2019), no article in our review has specifically focused on how these adverse effects manifest in older PLWD. This represents a critical gap that future research should address to enhance protections for this population.

Limitations

While our scoping review provides valuable insights, it is essential to recognize that the existing literature presents several challenges that can impact the interpretation of our findings. The included articles exhibited heterogeneity in study design, sampling approaches, data sources, measurement methods, and cultural contexts, making it hard to draw definitive conclusions and apply the findings to different populations and settings. Most of the included articles utilized a cross-sectional design, which limits the ability to establish causal relationships between study variables. Future research employing longitudinal designs would establish the temporal ordering of these variables and provide a more comprehensive understanding of these relationships.

In terms of sampling, many articles used convenience and purposive sampling, which may limit the generalizability of their findings. Incorporating more representative samples, such as nationally representative ones, would enhance the generalizability of future findings. Although the review included samples from various sources (e.g., community-based and facility-based samples), certain subgroups may still be underrepresented, limiting the scope of applicability for the findings. Future research should aim to include more diverse and underrepresented subgroups, such as individuals in rural areas, racial minorities, and those in socioeconomically disadvantaged or under-resourced regions, to provide a more inclusive understanding of FE.

Many articles in this review relied on participants’ self-reported data, which can introduce biases such as recall bias and social desirability bias. Others utilized administrative records or third-party reports, such as data reported by professionals based on their observations or assessments, offering additional perspectives. However, these alternative sources also have limitations in fully capturing the scope of FE. Notably, a few articles in the review triangulated different sources. Only Fang and Yan (2021) and Fang et al. (2019, 2023) reported information collected from both caregivers and care recipients. Future research should aim to triangulate data sources, combining self-reported data, administrative records, and third-party reports. This approach can provide a more accurate understanding of FE, reduce biases inherent in individual data sources, and enhance the reliability of findings.

There was notable variation in how FE and related concepts were defined and measured across articles. For example, some articles employed multiple items from standardized scales (e.g., Fang et al., 2019), while others relied on a single-item measure to assess FE (e.g., Lichtenberg et al., 2013). This inconsistency poses challenges for comparing findings and developing insights across the literature. Future studies should aim to develop standardized definitions and measurement tools for FE. This could include creating universally accepted scales or frameworks that capture both the nuanced and broader aspects of FE, enabling more consistent data collection and comparisons across studies. Contextual factors, such as cultural values and socioeconomic resources, likely shape both the experiences and reporting of FE among older PLWD. However, most studies included in this review did not explicitly examine these contextual influences. Future research should explore cultural and socioeconomic contexts to better understand how these factors may influence FE among older PLWD.

Additionally, no study in our review specifically examined how different types of dementia may uniquely influence financial decision-making and vulnerability to exploitation. For instance, individuals with Alzheimer’s disease may experience memory decline that impacts their ability to recognize financial risks or remember transactions, while those with frontotemporal dementia may struggle with financial planning. Future research is needed to explore these distinctions to better inform strategies tailored to the specific vulnerabilities associated with different dementia types. We discussed the connection between dementia-specific vulnerabilities and FE across several themes in our findings, including risk factors, warning signs, and strategies to address FE. However, due to the limited current evidence, we were unable to thoroughly examine these connections. Future research should address this gap, for example, by comparing barriers and facilitators to safeguarding among older adults with and without dementia.

Moreover, several limitations in our analysis warrant acknowledgment. Gray literature was not included in this study, which may introduce publication bias, as published literature tends to favor positive findings over null results. Future reviews may consider incorporating gray literature to address this bias. Additionally, our review was limited to articles published in English due to the linguistic capabilities of our research team members, potentially introducing language bias and narrowing the scope of our findings. Although the purpose of a scoping review is to summarize a broad range of literature on a topic (Peters et al., 2020), we acknowledge the value of a deeper synthesis of findings. It may be feasible for future researchers to conduct a related systematic review or meta-analysis to investigate specific themes regarding FE among older PLWD. While our scoping review and the included literature have limitations, these should be viewed as opportunities for future research to address gaps and advance our understanding of FE among older PLWD.

Strengths and Conclusion

Despite these limitations, the scoping review has several notable strengths. This scoping review employed the PRISMA guidelines, ensuring a rigorous methodology and enhancing the transparency and replicability of the study selection process. The use of multiple electronic databases increased the comprehensiveness of the literature search, reducing the risk of publication bias. Including two independent reviewers in the article screening process was a robust approach that reduced the potential for errors.

Additionally, the review’s inclusivity of diverse study designs (both quantitative and qualitative) and data sources (including community-based, facility-based, professional-based, and administrative data samples), and geographic contexts (including the United States, Japan, Norway, China, the United Kingdom, Australia, and Canada) enriches the understanding of FE among older PLWD by capturing varied perspectives and experiences. The absence of time restrictions allowed inclusion of articles across a broad historical timeframe. The review analyzed a diverse range of research across 21 articles, providing valuable insights into topics such as the prevalence, risk factors, and safeguarding strategies associated with FE. By identifying seven key themes, the review offers a comprehensive understanding of this critical issue. Furthermore, this review identifies critical gaps in existing literature, such as the need for research on protective factors, adverse effects, and barriers to implementing safeguarding measures. Our findings also emphasize the urgent need to address FE among older PLWD through multilevel strategies. For example, practitioners should be trained to recognize indicators of FE and provide appropriate guidance to PLWD and their caregivers. Policymakers should consider implementing reforms (e.g., expanding legal protections) and launching public awareness campaigns (e.g., educating families and communities about FE prevention and available resources).

In conclusion, this scoping review represents a significant contribution to the field by being the first to summarize existing literature on FE among older PLWD. Our review advances the field by mapping the extent, range, and nature of the existing literature, highlighting critical gaps, and identifying areas for future research. By integrating diverse perspectives and applying a rigorous approach, the review informs practice, policy-making, and the development of targeted interventions, contributing to the improved protection and support of older PLWD.

Supplemental Material

sj-docx-1-tva-10.1177_15248380251383930 – Supplemental material for A Scoping Review: Financial Exploitation Among Older People Living with Dementia

Supplemental material, sj-docx-1-tva-10.1177_15248380251383930 for A Scoping Review: Financial Exploitation Among Older People Living with Dementia by Wenxing Wei and Sarah Balser in Trauma, Violence, & Abuse

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.