Abstract

Background. Unhealthy food and beverage taxes are gaining global momentum, but implementation complexities at the retailer level are poorly understood. The only such policy in the United States, a 2014 Navajo Nation legislation, applies a 2% tax to unhealthy foods and beverages, while exempting healthy foods and beverages from their 6% Navajo sales tax. In 2019, approximately half of small stores had not implemented both taxes correctly, primarily the tax exemption. Therefore, this study aimed to provide culturally-informed promotional materials to enhance implementation accuracy in these stores and test the impact. Methods. Stores (N = 20) were randomly assigned to receive early promotional materials versus a waitlist group. Three to 6 months later, we visited all stores to purchase healthy and less healthy items, at which time waitlist stores received materials. Implementation accuracy of the junk food tax and exemption were tracked and compared. Results. Overall implementation accuracy of both taxes increased from 0% to 20% at follow-up (p = .013). Tax waiver accuracy increased from 5% to 30% (p = .065). Comparing intervention versus waitlist stores, we observed no difference in implementation of tax exemption and a non-significant increase in accuracy of added tax on unhealthy foods and beverages (90% vs. 70%, p = .284). The study process revealed strengths and barriers to impactful store outreach. Discussion. Grounded in community partnership, we explored a promotional outreach strategy to enhance accurate implementation of Navajo Nation food and beverage taxes. Our findings suggest store outreach and promotional materials could address confusion issues, while barriers related to store capacity merit further exploration.

Keywords

Sugar-sweetened beverages (SSB) taxes, along with unhealthy food taxes, are a growing policy approach, with policies recently implemented in large cities in the United States such as Philadelphia, PA (Hua et al., 2021) and Berkeley, CA (Falbe et al., 2015) and in international settings such as Mexico (Batis et al., 2022; Hernández et al., 2019) and Hungary (Biro, 2015). While prior research has shown relatively high accuracy of tax implementation (El-Sayed et al., 2020; George et al., 2021), taxes aren’t always fully passed through to the consumer, particularly in smaller stores (Falbe et al., 2015) and stores in rural settings (Colchero et al., 2017).

Support to retailers to ensure correct implementation in stores may be particularly relevant for complex policies, such as those taxing both foods and beverages, and for those in which retailers (rather than distributors) are responsible for applying the tax (Chriqui et al., 2021). Challenges from retailer perspectives include concerns about impacts on revenue and complexities of incorporating tax changes (Hua et al., 2021). Stores may have different infrastructures in terms of point-of-sale technology, management structures to train staff, and rolling out changes across an entire store or retail chain. These challenges may lead to hesitancy or confusion among store staff, and ultimately, community concerns or confusion (Falbe et al., 2015). For food tax policies that are passed into law for a trial period or pending permanent reauthorization, stores may be reluctant to invest in significant changes early on.

The Navajo Nation is one of the largest tribal nations in the world and is considered a food desert, meaning that people have limited access to nutritionally affordable foods (Economic Research Service, U.S. Department of Agriculture [USDA], 2022). In 2014, the Healthy Diné Nation Act (HDNA) was passed 2014 and permanently reauthorized in 2020 (Navajo Nation Office of Legislative Services, 2020; Navajo Nation tribal Council, 2014). The law stipulates that a 2% tax be added to all unhealthy food and beverages, including SSB, with revenue allocated to local, self-determined wellness projects (Yazzie et al., 2022). In the same year, the Navajo Nation Council also passed legislation CJA-04-14, exempting healthy foods and beverages from the 6% Navajo sales tax (Office of the Navajo Tax Commission, 2014). For this reason, the Navajo Nation’s food and beverage tax policies are ambitious and complex, applying both added taxes and tax exemptions to different foods and beverages. In 2019, a study found that almost 90% of stores correctly implemented the additional 2% tax on less healthy items, similar to the accuracy of implementation in Cook County, IL (El-Sayed et al., 2020). However, a little more than half of stores correctly waived the Navajo sales tax on healthy items (George et al., 2021), suggesting an opportunity for enhancing accuracy. While there is little literature on retailer interventions to support tax policy implementations, store managers and owners have described the need for information about tax-eligible items, making sure the changes are easy to make, and a desire for culturally-informed, positive promotional materials to communicate effectively with community members (Chriqui et al., 2021; Etsitty et al., 2022).

Therefore, using a randomized waitlist design, the aims of this study were to provide culturally-informed promotional materials to approximately half of the Navajo Nation stores that did not implement both the tax and waiver correctly, and test the impact on implementation accuracy. We hypothesized that stores receiving promotional materials would be more likely to correctly implement the HDNA tax and tax exemption with comparison to stores that did not receive the materials. In addition, we gathered detailed feedback from the outreach team that distributed promotional materials to gain better insight into the feasibility and impact of a store outreach intervention on the accurate implementation of complex food taxes among stores in a rural, tribal setting.

Method

Framework

Conceptually, the study started with descriptive information about the stores and accuracy of taxation, informing the implementation of an intervention, further complemented by insights gained from the field. The underlying framework was the Social Ecological Model, with a recent emphasis on social policies and environmental change initiatives and building partnerships (Golden et al., 2015). The intervention strategies took place at the policy and community (store) levels. Our study also incorporated indigenous perspectives, emphasizing community collaboration, resilience, and traditional ways of living.

Study Design and Store Selection

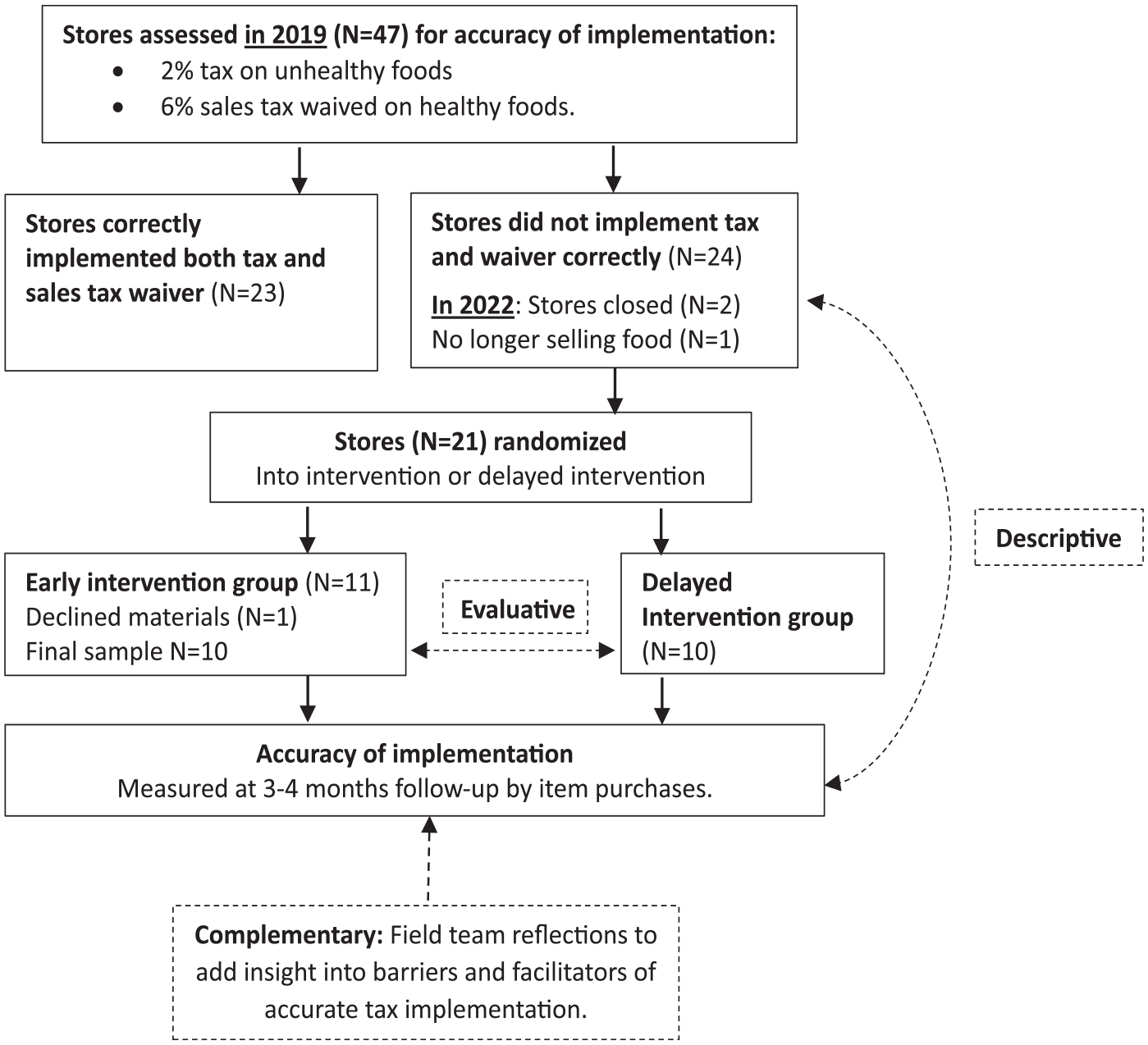

This prospective controlled study was conducted in follow-up to a 2019 assessment of tax implementation in stores located on Navajo Nation (George et al., 2021). Of the 47 stores assessed in 2019, 24 did not apply the HDNA tax and tax exemption correctly (See Figure 1). These 24 stores were engaged in this study for a store outreach intervention to help promote accuracy and to promote consumption of healthy foods. In 2022, two stores were no longer operating, and one was no longer selling food. Of the remaining 21 stores, using computer-generated randomized assignment, half (n = 11) were assigned to early distribution of promotional materials and the remaining (n = 10) to waitlist distribution. One store in the early group declined the materials (requiring headquarters approval), leaving 20 remaining stores.

Conceptual Design Overview of Study Components

The wave of early distribution of promotional materials to stores took place from November 2021 to January 2022; assessment of accurate tax implementation was conducted in March 2022 through May 2022; and the waitlist stores received their promotional materials at the time of the data collection visit.

Study Setting

With more than 400,000 enrolled members (Romero, 2021), the Navajo Nation is one of the largest tribal nations in the world. The land base covers over 27,000 square miles across the states of Arizona, New Mexico, and Utah, comparable to the size of West Virginia. Navajo people traditionally lived a lifestyle characterized by outdoor labor and consumption of healthy, traditional foods such as squash and corn. The diets of many changed with the introduction of Western foods high in sugar and saturated fats (Kopp, 1986; Teufel, 1996), contributing to nutrition-related chronic diseases such as Type 2 diabetes and high blood pressure (Eldridge et al., 2014).

The Navajo Nation only includes 13 grocery stores, which carry a larger variety of produce and staples. Many people rely on convenience stores at gas stations and trading posts, which primarily offer basic food items and processed foods with a longer shelf life and at higher prices compared with off-reservation stores (Kumar et al., 2016). In prior research, Navajo store managers have expressed interest in offering healthier options but describe barriers such as variations in perceived customer demand for healthier items and limited fruit and vegetable choices from distributors (Kumar et al., 2016).

A program that collaborates with stores—Healthy Navajo Stores Initiative (HNSI)—has been operating since 2014 by the local non-profit Community Outreach and Patient Empowerment (COPE); this initiative supports approximately 25% of all Navajo stores, including 10 large stores, 15 gas stations, and three trading posts. HNSI provides technical assistance, promotional materials, equipment and supplies, and other forms of support to stores and has been associated with healthier purchasing behaviors (MacKenzie et al., 2019).

Store Outreach Intervention

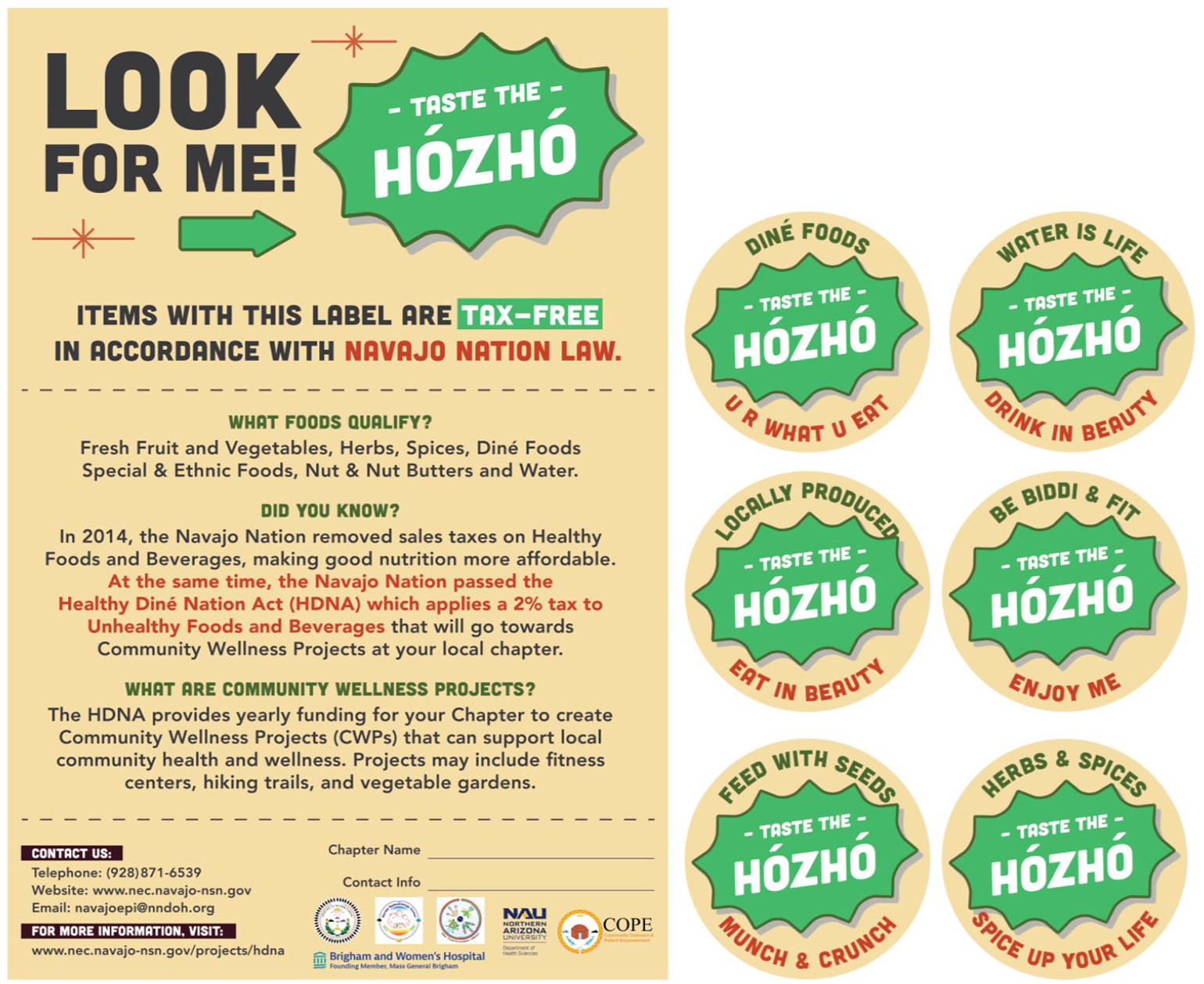

Store outreach materials included a printed list of tax-exempt and HDNA tax-eligible food and beverage items developed by the Navajo Epidemiological Center and Office of the Navajo Tax Commission (printed for cashier use), promotional posters providing information to staff and shoppers about HDNA and tax exemption of healthy foods, as well as shelf stickers, shelf-wobblers and labels for healthy tax-exempt items to be used throughout the store. Promotional materials (see Figure 2) were developed with COPE’s communication team and REACH technical assistance consultant, The Food Trust. The overall theme of the materials was developed with consideration of the local communities. Navajo language and cultural concepts were used to draw attention to and provide a similar context of supporting advice usually provided by an elder. The team decided on the tagline, “Taste the Hózhó,” to lead the campaign. Hózhó is a Navajo term relating to attaining/maintaining balance and harmony (Kahn-John Diné & Koithan, 2015). Feedback was obtained from our Research Advisory Group.

HNSI Promotional Materials Examples

Items were distributed in person by the study team, staggered in two phases (“early” vs. “waitlist” distribution). The study staff included three community members. The materials were tailored to the store type: grocery stores received a mix of larger and smaller posters, whereas smaller stores received small posters to account for limited wall space. A script was developed that explained the materials and provided suggestions on how to effectively use the items (e.g., placement of posters, item labels and shelf wobblers for tax-exempt items), and staff used this script to introduce themselves and materials when speaking to the store manager or owner. The study staff showed the materials to the store manager or employee, describing how each item was designed to be used. They emphasized that the use of these materials was completely voluntary based on the discretion of the store. Of note, in addition to the 23 stores in this study, all other stores located on Navajo Nation received a package of promotional materials as well.

Data Collection

Assessing tax implementation: Trained study staff purchased food items from the selected stores to assess the rate of successful HDNA implementation. Staff purchased a beverage and a food item in each category, usually water plus fresh fruit or vegetable (tax-exempt) and a sugar-sweetened beverage and unhealthy snacks such as potato chips or candy (HDNA tax-eligible). These purchases were made separately to obtain two different receipts. Receipts from each purchase were retained and assessed for HDNA tax implementation.

Key Variables and Analyses

Accurate HDNA implementation was defined as 0% tax on items deemed exempt from the Navajo Nation sales tax, and 2% HDNA tax on items susceptible to the junk food tax. AZ and NM states have 0% sales tax on food, whereas Utah applies a 1.75% sales tax on food. As of July 1, 2018, the Navajo Nation applies a 6% sales tax on food items. Therefore, for this study, we considered correct HDNA implementation as a total sales tax of 7.5% to 8.5% for NM and AZ stores, and a total sales tax of 9.25% to 10.25% for UT stores. These procedures were identical to prior assessments of the implementation accuracy (George et al., 2021).

Receipts were scanned and reviewed, and the following data were entered into an excel file: date of purchase, store name, store type and region, percent tax applied to the healthy purchase, and percent tax applied to the unhealthy purchase. Data were then analyzed using IBM Statistical Package for the Social Sciences (SPSS) Statistics Version 27.0. Analyses first included descriptive statistics and frequency distributions to characterize the HDNA implementation. Then, we used logistic regression analysis to test whether the accuracy of (un-) healthy tax implementation (yes or no) changed from baseline. Next, we tested the primary study question: whether our intervention (receipt of the promotional materials) was associated with accurate tax implementation, using logistic regression with intervention group (early vs. late receipt) as a predictor variable. For any tax error, we used an intercept-only model to test whether the proportion of accurate stores at follow-up was different from zero (since all stores had some error at baseline), and for the other models, we tested whether time (baseline vs. follow-up) was a significant predictor of accuracy. A p-value of 0.05 was used to assess significance.

Field Team Reflections

We gathered feedback from the store outreach team (RA, SS, ME, CG) to reflect on factors contributing to the study success and future strategies. Areas of reflection included the design of promotional materials, store interactions during the outreach process, and broader factors related to the store and community environment.

Ethical Considerations and Community Involvement

The project protocol and procedures were reviewed and approved by the Navajo Nation Human Research Review Board under protocol NNR-15.199. A study advisory group provided feedback on promotional materials and study design; this group included food sovereignty activists, representatives of the Navajo Tax Commission, the Navajo Nation Division of Community Development, and other partners.

Results

Descriptive Statistics

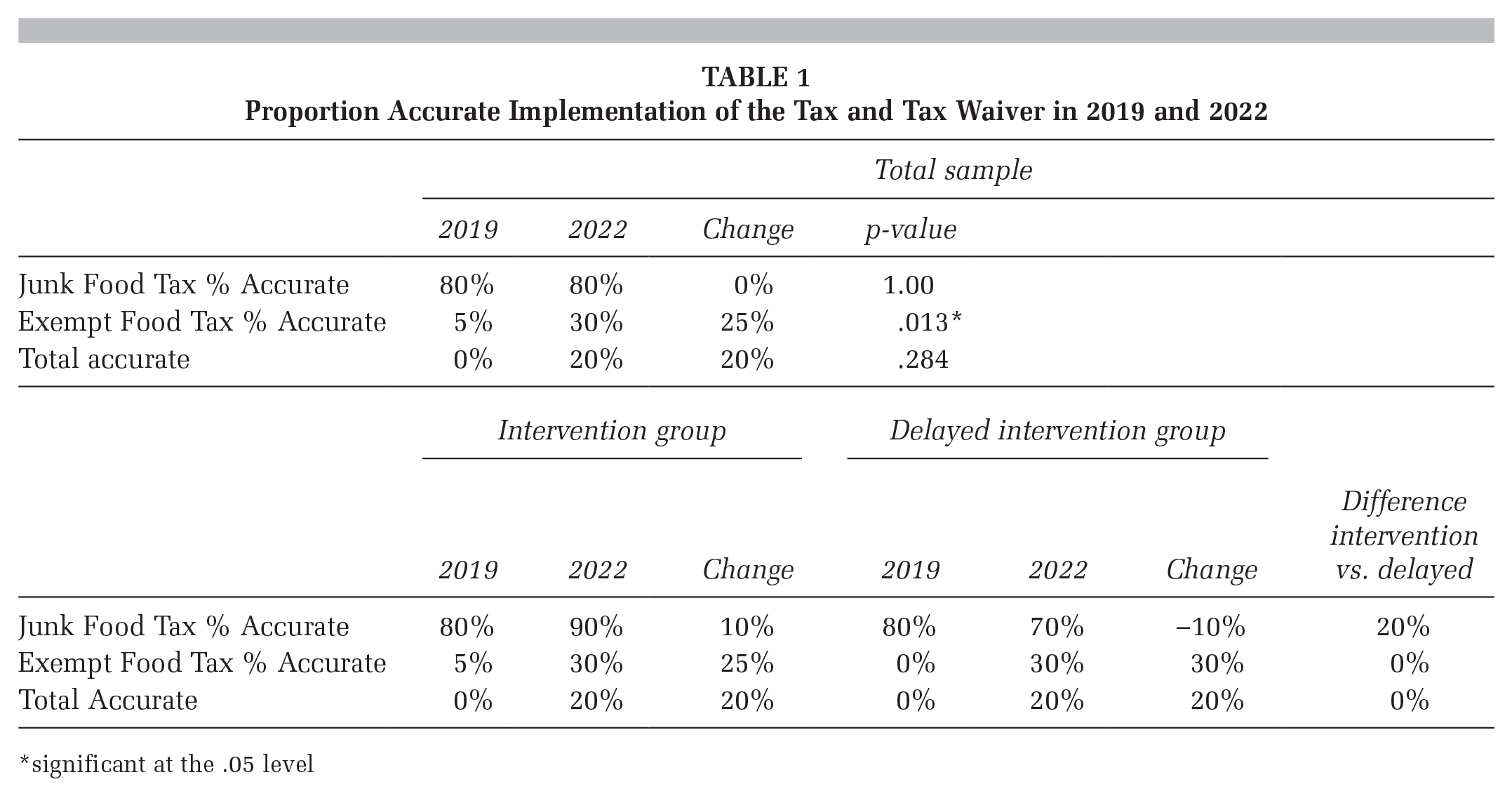

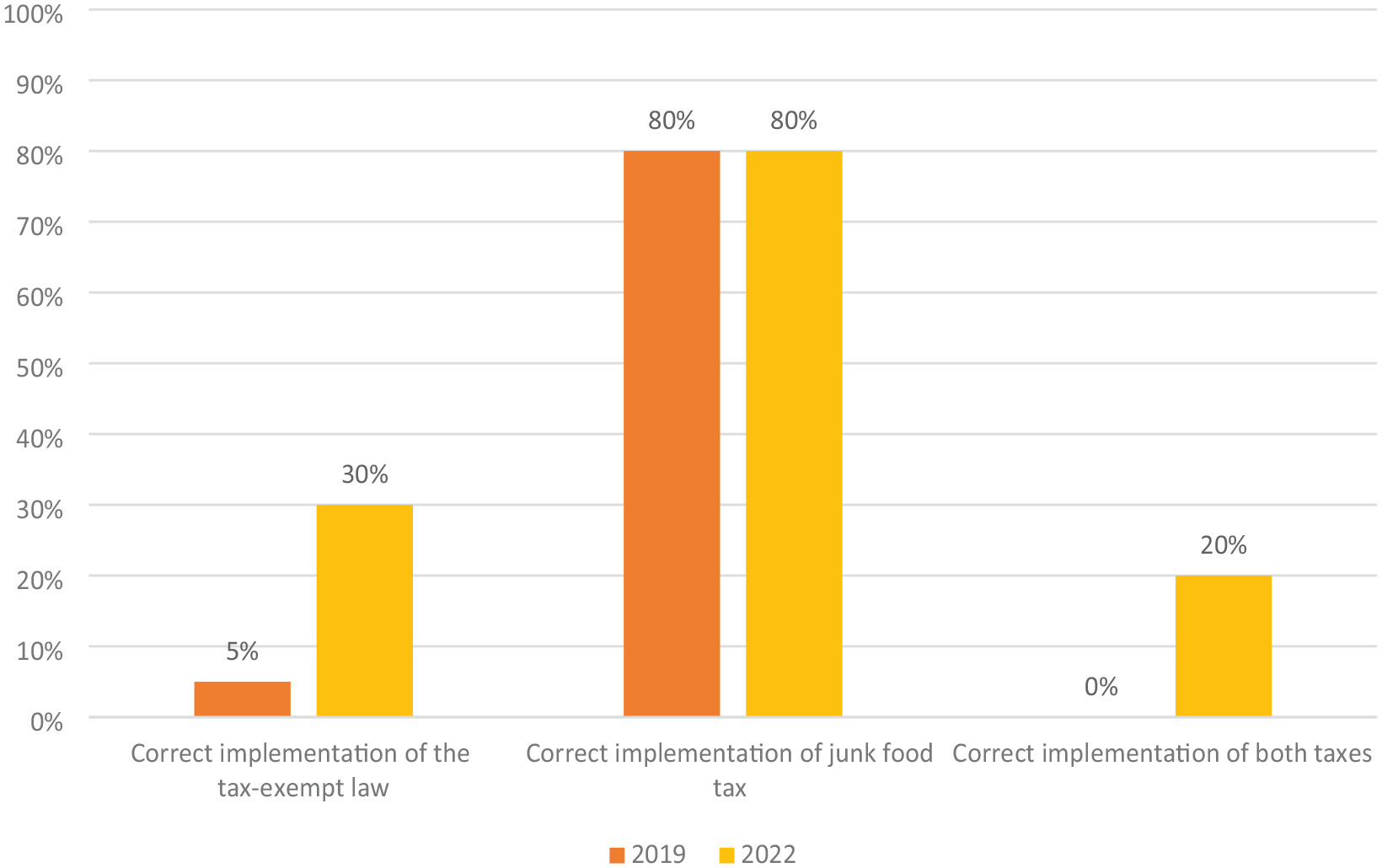

Overall average tax charged was 3.97% for healthy items and 7.00% for unhealthy items (p = .01). We examined the overall tax implementation accuracy across all 20 stores (three grocery stores, one trading post, 16 convenience stores) across three states. In 2019, all stores had at least one implementation error, primarily the tax exempt law. In 2022, 80% of stores implemented the added unhealthy food tax accurately, and 30% implemented the tax exemption accurately. In total, four stores (20%) implemented both taxes correctly in 2022 (Table 1).

Proportion Accurate Implementation of the Tax and Tax Waiver in 2019 and 2022

*significant at the .05 level

Changes in Accuracy of Tax Implementation Over Time

Accuracy improved slightly over the 3-year period (Figure 3). Compared to 2019, the proportion of stores correctly applying both the tax-exempt and added taxes significantly increased (b = 1.39, χ2 (df = 1) = 6.15, p = .013). This was primarily driven by the proportion of stores correctly implementing the tax exemption, which increased from 5% in 2019 to 30% in 2022 (b = 2.10, χ2 (df = 1) = 3.41, p = .065), whereas the proportion of stores correctly implementing the unhealthy tax was unchanged (80% in both time points), but still high.

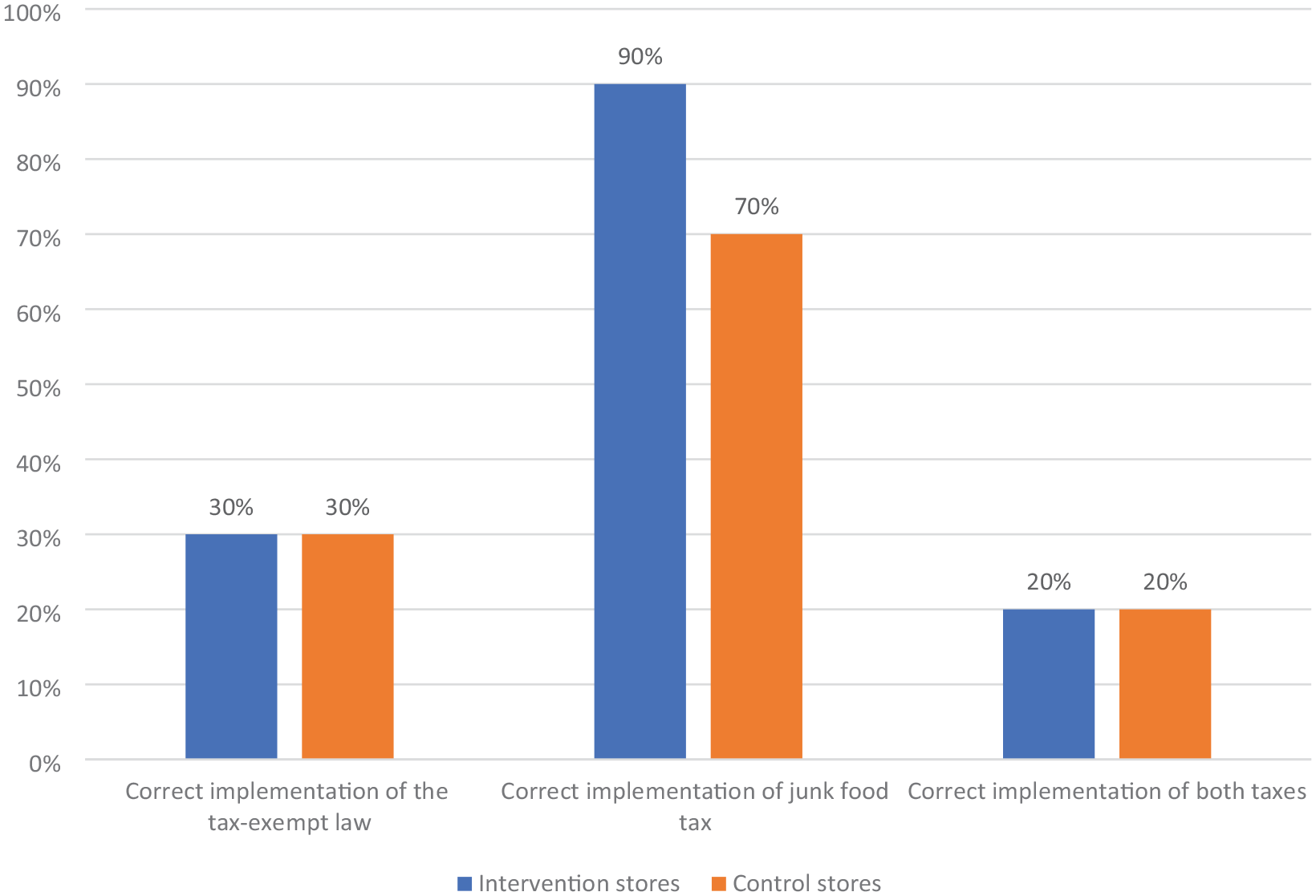

Correct Tax Implementation After Receiving HDNA Promotional Materials, Early Versus Waitlist Stores, n = 20

Intervention versus Waitlist Stores

As shown in Figure 4, comparing stores receiving HDNA promotional materials in the early (intervention) versus waitlist (control) groups, there was no difference in accurate implementation of the tax-exemption law for healthy foods and beverages (30% for both, p = 1.00). Stores that received materials were slightly more likely to correctly apply the additional tax to less healthy food and beverage items (90% vs. 70%), although this difference was not statistically significant (b = 1.35, χ2 (df = 1) = 1.15, p = .284). When looking at combined accuracy of taxes (i.e., both tax exemption and additional tax), there was no difference between store groups (20% correctly implementing both taxes in both groups, p = 1.00).

Change in Tax Implementation Accuracy Among Stores With Baseline Incorrect Implementation, 2019 Versus 2022, n = 20

Study Design and Implementation Process

An important feature of this study was the community-based participatory approach throughout the process. Promotional materials were developed in response to store manager suggestions and required input from multiple stakeholders to ensure accurate and cultural content, reflecting a strength-based approach using Navajo culture and positive empowering choices. When dropping off materials, store managers and staff generally received the materials positively, although some of the stores were unable to accept the larger posters due to the size (e.g., requirements for headquarters approval, lack of wall space). Store staff perceived fewer barriers to using labels, shelf wobblers and small posters, and these materials were anecdotally observed on display when staff returned 3 to 4 months later. Through ongoing discussions and outreach with stores, our team also reflected that smaller stores often described limitations with their point-of-sale technology, making it complicated to assign a tax exemption to healthy items in their cash register system. For some stores, their technology only permitted a single tax percentage, making it impossible to apply correct amounts to both tax-exempt and tax-eligible items in a single transaction. When dropping off items, the outreach team also reported that some store staff voiced confusion regarding which items were healthy (e.g., fruit juices, water) and were hesitant to exempt an item out of concerns of committing an error. Discerning which tax to apply to items was even more challenging when the store’s product inventories changed over time.

Discussion

In this study, we developed culturally-informed promotional materials related to the Navajo Nation’s food and beverage taxes. Materials were designed to reduce confusion about eligible items and enhance awareness and engagement about tax-free healthy choices. Among 20 stores that had not correctly implemented taxes in 2019, stores appeared to be slightly more likely to implement the added tax if they received the promotional materials, compared with stores that did not receive these materials, although the differences did not reach statistical significance. There was no difference in correct tax exemptions among early versus waitlist stores, although overall accuracy of applying the tax exemption to healthy foods increased from 5% to 30% over the study period. The store outreach appeared to reduce overall confusion about tax implementation, although structural barriers remain.

This was the first-ever study that aimed to promote accuracy of complex food tax policy in a rural, Tribal setting. A synthesis of peer-reviewed and selected publicly available studies of the implementation of sweetened beverage taxes in the United States, found targeted education and communication with “on-the-ground” implementers, such as distributors and retailers to be an important component of adopting complex food tax policy (Chriqui et al., 2021). Not only are these stakeholders responsible for ensuring accurate tax application, but also uniquely positioned to communicate food tax policy changes to consumers (Chriqui et al., 2021). Therefore, engaging these stakeholders in targeted education and outreach, such as training, education, and guidance, in the early stages of implementation can increase the accuracy of complex food tax policy.

Further strengths of this study included its responsiveness to store feedback to maintain community trust, the emphasis on Navajo culture, positive messaging, and the involvement of multiple expert stakeholders. While the materials may have contributed to greater clarity of which items should be taxed or exempted, additional structural barriers to correct tax implementation were encountered, including point-of-sales technology in smaller stores. This could be particularly salient given retailers, rather than distributors, are responsible for implementing the HDNA tax and tax exemptions. Combined with the fact that store managers have generally voiced HDNA support, our findings suggest that factors contributing to accurate implementation may include infrastructure “capacity” and “confusion,” rather than “compliance” on the part of store retailers.

This is in alignment with prior research, which has documented less accurate implementation or limited pass-through of food taxation in smaller stores (Falbe et al., 2015), rural or semi-rural stores (Colchero et al., 2017), or limited-service stores (El-Sayed et al., 2020). For example, in Berkeley, CA, researchers found that managers of nonchain stores indicated confusion about tax implementation and that changes would take time. “It takes a lot to add [the cost of a] new tax for every item. We’re still going through the process, and it’s June. I think that it would take at least 6 months” (Falbe et al., 2015, p. 2198). Researchers in Cook County, IL, indicated that limited service stores would benefit from additional training and technical assistance, possibly due to the limited availability of support provided with point-of-sale systems (El-Sayed et al., 2020).

Among stores with inaccurate tax implementation in 2019, accuracy did not deteriorate over time and may have even improved in terms of the tax exemption practices. These trends would support the hypothesis that declines in HDNA tax revenue (Yazzie et al., 2020) may be more likely due to healthier purchasing, rather than waning practices of applying correct taxes. Accurate tax exemption was still low, and no differences were observed among stores that did versus didn’t receive promotional materials until later. These findings highlight opportunities to provide continued support and awareness related to the tax exemption component of the legislation, as well as additional opportunities to explore policies and store technology support to increase access to affordable, healthy food and beverages for the Navajo community.

Strengths and Limitations

The study had several limitations. First, the sample size was small given the scarcity of stores located on the Navajo Nation. Second, since itemized receipts were not always available, we purchased unhealthy and healthy items on separate receipts to assess the tax applied to each category (tax-free versus tax-eligible). The accuracy of taxes could have been underestimated in both groups if combined purchases resulted in additional taxation errors; however, our assessment method did not differ across time points or randomized assignment. We did not systematically assess whether promotional materials were used, which could have informed our interpretation of study findings. Finally, this study focused only on stores with previously inaccurate taxation and was not designed to determine if stores with correct taxation in 2019 maintained accuracy or not. Overall, this report describes a unique approach using a collaborative process to gather feedback, develop locally relevant materials, and design an observational approach to understand the impact of these materials on tax implementation accuracy. The study design used an early versus late distribution schedule to allow a comparison group, yet still allowed the sharing of materials with all stores. This model of collaboration could serve as a model for strategies to proactively support retailers and engage community members to facilitate implementation of food and beverage taxes.

Conclusion

This study was carried out to explore a model of store support for a complex policy through public-private partnerships to improve tax legislation accuracy in a rural, Tribal area. Although the findings were not statistically significant, the study demonstrates that a partnership including Tribal government entities, Native community-based organizations, and the network of Navajo stores can facilitate the development and implementation of outreach materials and intervention. This is especially important given the role that retailers and distributors play in adopting complex food tax policies. Overall, the study was guided by our understanding that stores desired additional support to accurately implement the HDNA policy.

Implications for Practice

Health promotion practitioners should consider retailers as active community partners when implementing policies affecting food and beverage sales, such as food and SSB taxes. Ensuring dedicated resources to support front-line retailers can increase accurate implementation of food and beverage taxes. Furthermore, distributing culturally-informed promotional materials to retailers can not only standardize correct implementation in stores, but also play an important role in raising consumer awareness.

Implications for Research

Further research is needed to explore how models of public-private partnerships can maximize the health impacts of food and beverage tax policies and include longer-term follow-up. A particular area of interest is to explore ways to facilitate the accuracy of implementation of tax waivers on healthy foods and complex policies, including both added taxes and waivers. This research will be especially important in areas with populations at high risk for chronic metabolic conditions. In this context, a key area of research includes ways to strengthen long-term community-level public health efforts in rural, Tribal areas.

Footnotes

Authors’ Note:

We would like to acknowledge and thank the HDNA advisory group, including Regina Eddie, Ramona Antone-Nez, Shirleen Jumbo-Rintila. Our deepest appreciation to the individuals who operate stores on Navajo Nation and who have collaborated with our team. Finally, we wish to acknowledge the role of the Navajo Nation, which is responsible for authorizing and implementing HDNA including Navajo Tax Commission, Division of Community Development, and Navajo Epidemiology Center, Data reported in this publication were supported by a cooperative agreement with the U.S. Centers for Disease Control and Prevention (NU58DP006594) and supported by grants from the National Institute On Minority Health And Health Disparities of the National Institutes of Health awards number R01MD013352 and U54MD012388. The content is solely the responsibility of the authors and does not necessarily represent the official views of the funders.