Abstract

Keywords

Caves, Tatos, and Urschel (Caves et al.) emphasize that I declined to share my dataset, but the context of that decision warrants further elaboration. All three authors have a clear connection to the plaintiffs in the active antitrust case, Le et al. v. Zuffa LLC (UFC Lawsuit), and two of the authors – Dr. Caves and Mr. Urschel – consulted for the plaintiffs and may yet provide future support. 1 I have zero financial interest in the case and felt it improper to provide data to individuals with an obvious interest in either side of an ongoing, multibillion-dollar lawsuit. This was my personal “barrier to data disclosure.” In addition, all data used in my analyses are publicly available and both sides have significant resources at their disposal.

Caves et al. advance two primary lines of criticism: (1) concerns regarding comparisons of marginal revenue product (MRP) and compensation in the presence of fixed Ultimate Fighting Championship (UFC) revenues and (2) concerns regarding my use of Google Trends search interest data as a proxy for UFC fighter popularity. I leave it to readers to form their own conclusions regarding the authors’ conflicts of interest and address their two substantive criticisms below.

MRP, Compensation, and Fixed Revenues

My paper, Gift (2020), was initiated following a February 2018 court filing in which it was evident the expert witnesses on both sides of the UFC Lawsuit agreed MRP was the relevant compensation metric for what workers would receive in a competitive labor market (Le et al. v. Zuffa, LLC, 2018).

At first glance, it appears Caves et al. take issue with the model presented in Table 4, Column 2, raising concerns with the manner in which fighter MRPs were estimated due to the presence of fixed revenues. Upon closer examination, they, in fact, acknowledge that my analysis utilized variable revenues exclusively. Their concern seems to be that comparisons of MRP and compensation in my Figure 5 “ignores the admonition of Berri et al. (2015)” (p. 3).

As an initial matter, any fixed-revenue criticism is inapplicable to the analyzes of Figures 1–4, Tables 1–4, and the middle column of Table 5 in Gift (2020) as they only include observations from pay-per-view (PPV) main card fighter-bouts; i.e., those with variable content revenues. 2

This is a key distinction between Gift (2020) and Berri et al. (2015). In their early analysis, Berri et al. (2015) utilize total team revenues derived from a mixture of variable- and fixed-revenue sources. With the UFC during my sample period, variable content revenues were easily disaggregated from fixed-revenue sources – all PPV main cards had variable content revenues while PPV prelims and non-PPV events had content revenues which were fixed. 3

Utilizing fighter-bouts from only PPV main cards, I estimated fighter MRPs in a world of variable content revenues. In this world – in which the framework of Berri et al. (2015) does not apply – it was still found that 20 percent of fighter-bouts during the sample period did not have an MRP significantly different from zero and 23.3 percent had a numeric MRP estimate below the fighter's calculated compensation. Thus, even in a world of purely variable revenues, one-fifth of UFC fighters, selected by management to appear in high-profile fighting slots (PPV main cards), did not have statistical support for generating any incremental content revenues and roughly one-quarter of fighters, in the language borrowed from Berri et al. (2015), would be considered “overpaid” by traditional economic standards. 4

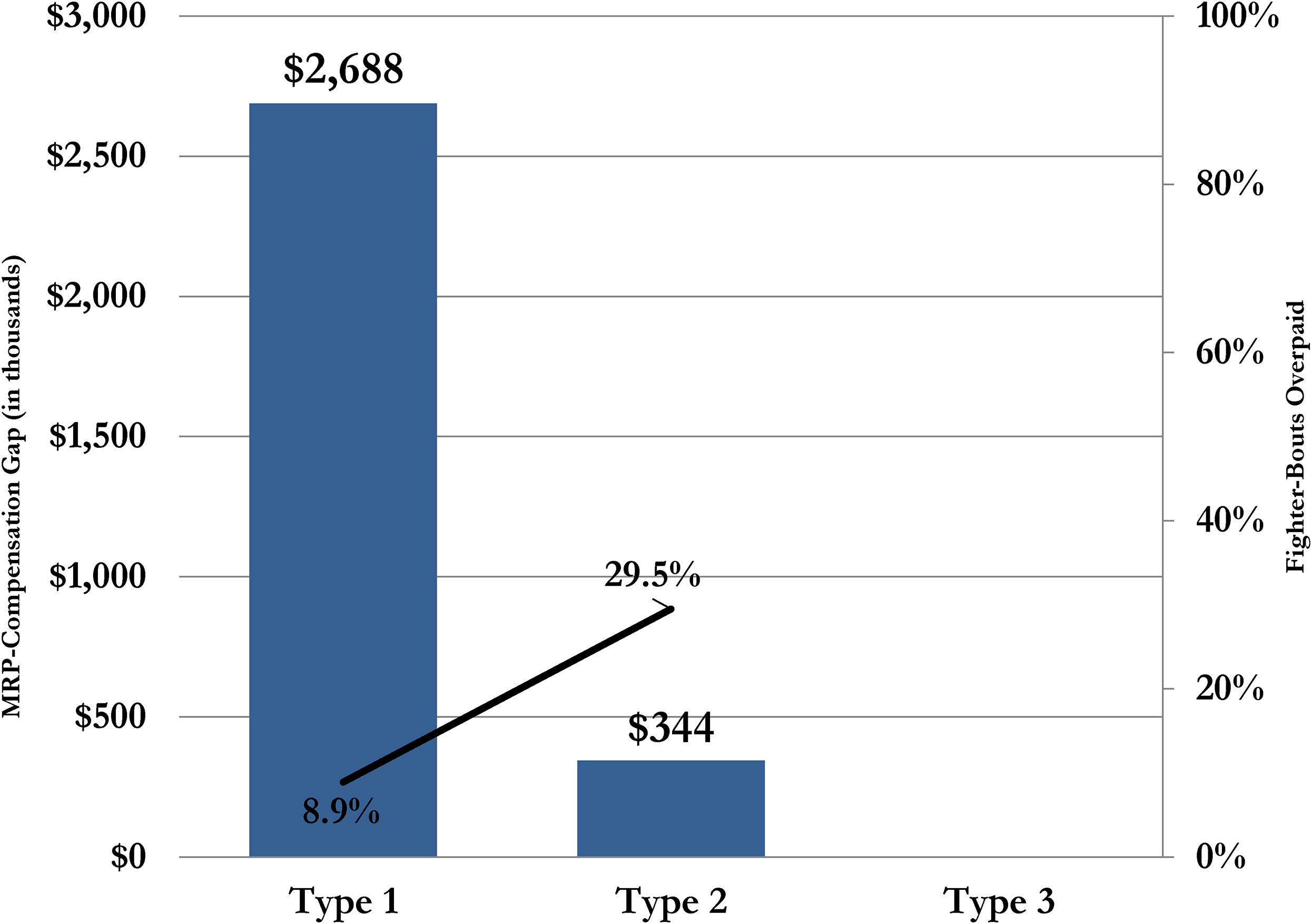

Figure 5 from Gift (2020), which seems to be at issue, can be reconstructed using only PPV main card fighter-bout observations, and is shown in Figure 1 below. The precise numeric values may have changed but the spirit of the findings persists, even in a setting where all content revenues are variable.

Recreation of Gift (2020) Figure 5 using only PPV main card fighter-bout observations.

As Figure 1 shows, Type 1 fighters still have the largest MRP-compensation gaps by a wide margin. This gap declines by 87 percent for Type 2 fighters and their overpayment percentage rises significantly. Type 3 fighters, while not observed in this new analysis, still spend their entire careers on fixed-content-revenue broadcasts and, as such, do not generate content revenue MRP by traditional economic standards. This is not an assumption; it is a conclusion based upon documentary evidence regarding the UFC (see, e.g., Deutsche Bank, 2007, 2013; Moody’s Investors Service, 2013, 2015; Standard and Poor’s Ratings Services, 2013, 2014). “Traditional economic standards,” or a similar phrase to that effect, only appears once in the Caves et al. comment – when quoting Gift (2020) – yet I emphasized it repeatedly in Gift (2020) as well as the present reply.

Gift (2020) did not “ignore” the admonition of Berri et al. (2015), but rather took it quite seriously. In fact, I explicitly agreed with them when I noted, “sports owners are unlikely to make [such] ‘systematic errors’ with respect to overpaying athletes relative to MRP” (Gift, 2020, p. 197). While Caves et al. take issue with the conclusion that counterfactually removing consumer interest in a participating fighter would not change a fixed-revenue television contract, roughly 20 percent of PPV main card fighter appearances also do not change purely variable content revenues. Similar to how Berri et al. (2015) proposed a new way of looking at compensation in such situations that do not make traditional economic sense, I proposed a compensation strategy by which such findings may, in fact, be profit maximizing for the UFC – namely that overpayment of lower-level fighters by traditional economic standards in the continual search for tomorrow's Type 1 superstars could very well be long-run optimal, and therefore inconsistent with systematic poor decision making by UFC management.

As noted with the MRP-compensation gaps, the UFC extracts the most value from its Type 1 stars, by a large margin. Yet identifying, signing, and developing these fighters is a costly process fraught with uncertainty and imperfect information. Paying an efficiency wage (relative to competitors and relative to content revenue MRP) to attract Type 3 fighters and obtain an early opportunity to evaluate their ability and popularity potential could be profit maximizing for the UFC over the long run. 5

Google Trends Data

Caves et al. offer a second line of criticism alleging various concerns with my use of Google Trends search data as a variable of interest.

They start by claiming I overstate the consensus in the literature regarding the use of Google Trends. Their objection itself is overstated. They point to potential caveats from two papers that effectively utilized Google Trends in their research. And in their primary example, they inexplicably claim I “incorrectly” (p. 4) characterized the findings of Zamudio (2016) by presenting a misleading partial quote from Zamudio's abstract.

The complete sentence reads, “Celebrities’ profession (superstar/supermodel) and buzz (popularity on the Internet) moderate the effect of brand personality such that, under certain conditions, celebrity buzz can be detrimental to the endorsement's value” (emphasis added), and addresses the interactions in Zamudio's model. But more importantly, Zamudio's research successfully constructs a Google Trends dataset and employs it in an empirical model as a proxy for celebrity buzz/popularity. In fact, the formulation of my Google Trends dataset utilized a variant of the “benchmark” method described in Zamudio's Appendix B (Zamudio, 2016, p. 425). Zamudio's ultimate finding that companies and endorsers can have positive or negative matching value and celebrity buzz will amplify that value, in either direction, is an irrelevant criticism of my paper. 6

Caves et al. go on to make another vexing claim with no empirical or economic support. Puzzlingly, they allege that in the construction of my consumer interest variables, “the Google Trends proxy is lagged by one month” (p. 7). This is simply incorrect, and thus, their subsequent criticisms are moot. The consumer interest variables used to estimate fighter MPs and MRPs were developed using “_L1” and “_L2” lags representing “the lagged interest in each fighter's most recent or second most recent bout month;” in other words, the interest stemming from each fighter's two most recent bouts when implemented in the model (Gift, 2020, p. 184). 7 These lags were inspired by Berri et al.’s (2015) use of lagged wins, but were adapted for a mixed martial arts setting. It is deeply concerning that the authors would make claims regarding the construction of my consumer interest variables that are patently untrue, especially when the facts of the matter were clearly conveyed in the paper.

When the Caves et al. authors attempt to criticize my use of Google Trends by way of example, their anecdotal references to Zion Williamson and Facebook fall flat and do not substitute for a lack of citation to relevant academic authorities. They also ignore the role of the econometrician, as any reasonable, impartial researcher in such areas would surely note any lack of explanatory power or nonsensical estimates and adapt their research method accordingly. Neither of these occurred in the setting of mixed martial arts (see Tables 3 and 4 in Gift, 2020). 8 The Caves et al. criticism at best suggests that perhaps Google Trends may not be a suitable proxy for consumer interest in their two contrived examples, something which would be discovered during preliminary analyses. Yet their examples are silent on the suitability of Google Trends as a proxy for consumer interest in mixed martial arts.

Additionally, their examples ignore the manner in which my dataset was constructed. This is understandable given their previously noted lack of clarity in this area. The general time trend of the consumer interest variable and any random spikes would not be included in my ultimate dataset. For each observation, only the consumer interest values associated with a fighter's two most recent bout months were included.

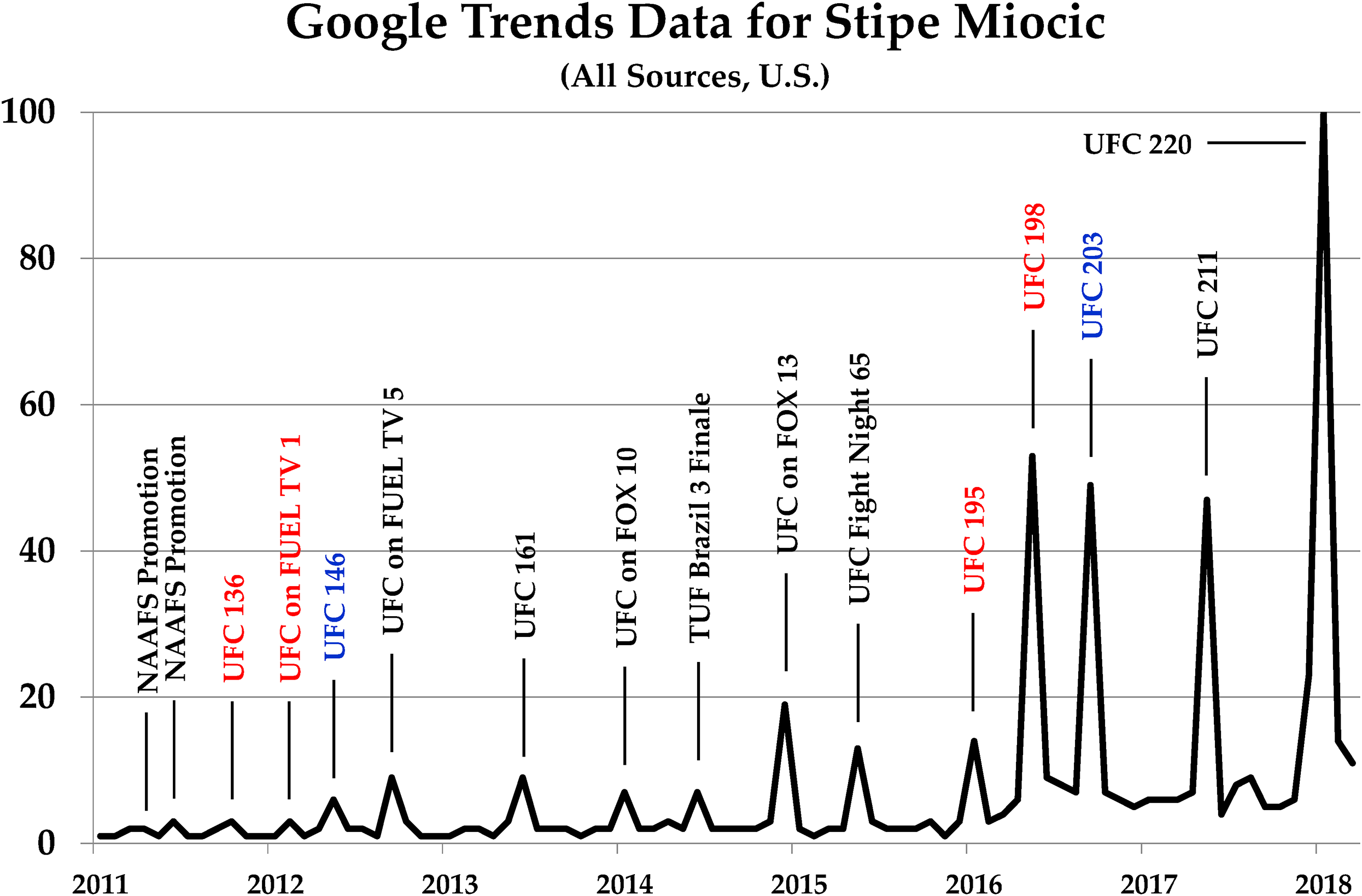

Former UFC heavyweight champion Stipe Miocic is instructive in this regard. His Google Trends chart (Figure 2) is representative of what tends to be seen when working with mixed martial arts (MMA) data: spikes of consumer interest, to varying degrees, during months in which the fighter fights. For any given PPV main card appearance, Miocic's relevant data points came from his two prior promotional appearances. For example, when Miocic made his PPV main card debut at UFC 146, his Google Trends interest from the months of his UFC on FUEL TV 1 and UFC 136 bouts were his relevant data points. Likewise, when Miocic made the first defense of his heavyweight championship at UFC 203, his relevant consumer interest data came from the month of UFC 198, when he upset Fabricio Werdum to win the title, and UFC 195. The chart also helps illustrate what winning a UFC title can do for a fighter's popularity.

Google Trends data for Stipe Miocic (January 2011 through March 2018).

Unfortunately, the content and character of the Caves et al. comment only serve to reinforce my original concerns regarding data sharing with parties affiliated with either side of the UFC Lawsuit litigation. I stand by my decision.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.