Abstract

Over the past decade, housing prices in many regions of the United States have increased precipitously. This is especially true in the San Francisco Bay Area, a region that has experienced an influx of highly paid tech workers and a tightening of the housing market. Against this backdrop, this article examines the strategies and compromises that a racially and socioeconomically diverse group of Bay Area residents use to maintain housing. Drawing on survey and interview data, the article finds that both homeowners and nonhomeowners described feeling “stuck in place” as prices rose around them. Yet nonhomeowners made greater compromises to maintain housing, including (1) living in structurally inadequate housing; (2) moving in with friends and relatives; and (3) accepting legally precarious living arrangements. Although research on housing often focuses on why families move, this article reconfigures immobility as a deliberate process, documenting the trade-offs families make to keep their homes.

In many regions of the United States, wages lag behind housing prices, making it harder for the average worker to afford a home (Aurand et al. 2021; Schmidt 2022). The lack of affordable housing poses immense challenges to families making decisions about where to live. Much of the research on housing decisions focuses on mobility, including both voluntary and involuntary moves (DeLuca, Garboden, and Rosenblatt 2013; Desmond 2016). Such moves are important, especially considering that housing instability can negatively affect health and well-being (Burgard, Seefeldt, and Zelner 2012), social relationships (Desmond 2012), employment (Sard and Waller 2002), and children’s educational outcomes (Crowley 2003).

Comparatively less research has investigated those who stay in their housing (Clark, Duque-Calvache, and Palomares-Linares 2017; Rosen 2017; Shakespeare 2022). Yet examining why and how people stay in their housing, including the compromises they make to do so, is important for understanding the full consequences of rising housing prices. Indeed, many families, including those who are economically disadvantaged, manage to stay in place for extended periods (Clark et al. 2017; Hanson 2005; Rosen 2017), though it is not always clear whether they do so by choice. Drawing on survey and interview data, this article examines the strategies that a racially and socioeconomically diverse sample of San Francisco Bay Area residents use to maintain their housing in one of the nation’s most expensive housing markets.

Prior literature on housing affordability understandably focuses on low-income families (Desmond 2016; Edin and Lein 1997; Stack 1974). Yet in some regions of the country, including the Bay Area, even middle-income families struggle to find affordable housing (Solon 2021). Furthermore, research on housing mobility tends to focus on cities where vacancy rates are relatively high and/or housing costs are low. This study takes a different approach by considering how families across the income spectrum make decisions about housing in a high-cost housing market where vacancy rates are low and housing options are limited (U.S. Census 2021). This multimethods project draws on survey data with over 3,000 Bay Area residents and in-depth interviews with a subset of 50 respondents. Together, these data offer insight into why and how Bay Area residents stay put in an increasingly expensive region.

The data reveal stark inequalities by race and income in the living conditions of Bay Area residents. Black respondents are more likely to face housing hardships, including eviction and homelessness. Survey data also suggest that many respondents, especially Asian and Latinx residents, live with friends and family. Interview data then shed light on how respondents experience these arrangements and make decisions around housing. Most respondents lamented the rising housing costs in the Bay Area, and, with some notable exceptions, described feeling “stuck” in their current housing arrangements. Staying in place is often seen as beneficial, as longer tenures are equated with more stable housing (Frederick et al. 2014). Housing stability, in turn, is generally associated with positive outcomes for physical and mental health (Bures 2003). Yet residential immobility is not always positive, especially when it keeps families in low-resource neighborhoods or inadequate housing (Sampson 2012; Sharkey 2013).

This article suggests that a lack of mobility can be perceived as constraining for families who feel locked into undesirable housing arrangements. Many respondents described compromises they made to keep housing in the Bay Area, yet these compromises differed between homeowners and nonhomeowners. Homeowners noted that they often made trade-offs to stay in homes that were no longer the right size for their family. They were also more likely, however, to describe their housing situations as secure. Nonhomeowners felt notably less secure and described a host of additional trade-offs including (1) living in structurally inadequate housing; (2) moving in with friends and relatives; and (3) making do with legally precarious living arrangements. Together, this research adds to recent scholarship (Coulter, van Ham, and Findlay 2016; Shakespeare 2022) that reconfigures immobility as an intentional process, documenting the trade-offs that families across the economic spectrum make to maintain their housing.

Background

Disparities in Housing Arrangements

Before considering why people move (or do not move), it is useful to take stock of the different housing arrangements families find themselves in. Americans overwhelmingly prefer to own their homes rather than rent (McCabe 2018) and homeownership is integral to ideas of citizenship and the American Dream (Jang-Trettien 2021). Yet homeownership remains out of reach for many. Homeownership rates have declined over the past 15 years as asking prices increased (Joint Center for Housing Studies, Harvard University 2015; U.S. Census 2021).

Decades of research documents racial disparities in homeownership rates. White Americans are more likely to own their homes than other racial groups. Black Americans continue to face barriers to homeownership (Connolly 2014; Massey and Denton 1993; Taplin-Kaguru 2022), ranging from discrimination in the housing market (Korver-Glenn 2021; Krysan and Crowder 2017) to persistent racial wealth gaps (Oliver and Shapiro 2006). White Americans benefit from greater generational wealth along with tax subsidies and access to credit that help them afford homes (Robinson 2021). Nationally, 73 percent of White Americans own their homes, compared to just 42 percent of Black Americans (U.S. Census 2019). Homeownership in the Bay Area is somewhat depressed, given the high cost of housing, with 63 percent of White residents and only 34 percent of Black residents owning their homes (Bay Area Equity Atlas 2021).

Renting is already a precarious arrangement but has become more so as rental costs have grown faster than wages (U.S. Census 2021). Compared to homeowners, renters accumulate less wealth over time, limiting economic mobility (Arundel 2017). Most guidelines recommend that families spend less than 30 percent of their incomes on housing (Linneman and Megbolugbe 1992). Families who spend more than 30 percent are considered “cost-burdened.” Yet growing numbers of Americans spend far more than that percentage. By 2018, 47.5 percent of renters in the United States were cost-burdened (Airgood-Obrycki, Hermann, and Wedeen 2021), compared to 22.5 percent of homeowners (Robinson 2021). More than half of poor families who rent spend over 50 percent of their incomes on housing, and Black and Latinx families disproportionately carry rent burdens (Robinson 2021). Cost burdens are becoming increasingly common among families with moderate incomes as well. Between 2003 and 2013, the proportion of cost-burdened renters with incomes ranging from $30,000 to $45,000 increased from 38 to 45 percent (Harvard University, Joint Center for Housing Studies 2015). Housing cost burdens have also been linked to homelessness. Recent evidence suggests that homelessness increases sharply once the median cost of rent surpasses 30 percent of median incomes (Glynn, Byrne, and Culhane 2021). In these situations, middle-income families may begin renting units that were once reserved for low-income families, leaving few options for poorer families (Glynn et al. 2021).

When housing is unaffordable, many people rely on friends and family for support (Clampet-Lundquist 2003; Edin and Lein 1997; Harvey 2022; Stack 1974). Doubled-up households are defined as those “that include an adult who is not the householder, spouse or cohabiting partner of the householder” (Mykyta and Macartney 2011:3). These households often involve young adults moving back in with—or never leaving—their parents’ homes (Berlin, Furstenberg, and Waters 2010). Doubling-up may represent a way of coping with economic insecurity, allowing people to pool resources, benefit from economies of scale, and access added childcare assistance (Desmond 2012). The number of households doubling-up increased in the years following the Great Recession and was most common among younger adults (Mykyta and Macartney 2011). But although doubling-up is necessary in many situations, research suggests that it may carry negative consequences. Doubling-up can strain economic resources in families and result in overcrowding (Clampet-Lundquist 2003). These housing arrangements can also be unpredictable and uncertain (Kalil and Ryan 2010). Research on preferences for doubling-up suggests that people would prefer not to double-up if financial resources allowed (Sassler and Miller 2017). Yet doubling-up may be an important strategy for those facing housing instability or living in high cost of living areas like the Bay Area. While many housing studies focus on either renters, homeowners, or those who double-up, this study includes respondents across these housing arrangements to better understand the housing challenges and strategies of different groups.

Housing Mobility

Research on how people make housing decisions often focuses on why people move. Early theories of housing search decisions (Cadwallader 1993; Rossi 1980; Tiebout 1956) frame the housing search as an “ordered, multistep process whereby families decide to move, then collect information about available homes in neighborhoods with desirable amenities. . . and finally select housing units within those neighborhoods” (DeLuca, Wood, and Rosenblatt 2019:559). This research focuses implicitly on “voluntary moves,” which often improve housing or neighborhood quality, help people access more space, or bring people closer to work (Phinney 2013). While research warns against the negative consequences of housing instability more broadly, voluntary moves are viewed as less problematic. Indeed, voluntary moves into higher quality housing or neighborhoods are more likely to improve health, safety, and well-being for movers (Leventhal and Brooks-Gunn 2003).

In reality, not all moves are voluntary (DeLuca et al. 2019; Desmond 2016; Evans 2021). While higher income families may engage in lengthy purposive searches, those with lower incomes often cannot afford to do so (DeLuca et al. 2019; Harvey et al. 2020). Scholars document social class and racial differences in the housing search process, finding that not all families engage in the same ordered housing searches (Clark and Flowerdew 1982; Krysan and Crowder 2017). Low-income families tend to have higher rates of residential mobility in general (Ihrke and Faber 2012) and are more likely to experience forced or involuntary moves (DeLuca et al. 2019; Desmond 2012; Siskar and Evans 2021). In a longitudinal study of low-income Black families, DeLuca and colleagues (2019) found that 70 percent of moves were prompted by issues with landlords, housing quality, or violence. Housing unit failure—including electrical problems, collapsed ceilings, mold, and other issues—was the leading cause of “reactive” moves (DeLuca et al. 2019:565). Recent research also shows how housing dilapidation can displace homeowners, especially low-income Black women (Bartram 2023).

Forced or reactive moves can have important consequences for families, leading them into lower quality housing units (Desmond and Shollenberger 2015; Evans 2021). Evictions, perhaps the most salient form of forced moves, can have devastating effects on the families who experience them. Evictions are linked to material hardship, psychological issues, and job loss, and can make it more difficult to access government housing assistance in the future (Desmond 2016; Evans 2021).

Previous research has therefore examined how low-income families make housing decisions, finding that they often make reactive decisions to escape their current housing problems rather than proactive decisions toward better opportunities (DeLuca et al. 2019; Desmond 2012; Harvey et al. 2020). Yet many of these studies focus on areas with “loose” housing markets, where other housing options are available. The Bay Area, however, presents a different situation and offers insight into how people think about housing in a context where there are often few affordable alternatives (U.S. Census 2021).

Housing Immobility

Complementing research on housing mobility, a smaller body of research examines people who stay in their housing arrangements (Clark et al. 2017; Desmond, Gershenson, and Kiviat 2015; Huang, South, and Spring 2017; Rosen 2017). In the past, researchers largely assumed that nonmovers were sufficiently satisfied with their housing circumstances (Speare 1974). More recently, however, scholars have taken a more explicit focus on the constraints that prevent families from moving, including the lack of financial resources (Coulter et al. 2016; Coulton, Theodos, and Turner 2012). These researchers argue that we should consider immobility “an active process that can be a desired choice or a response to restrictions and constraints” (Coulter et al. 2016:353). Research shows that people who do not move are also important for understanding neighborhood processes. Huang and colleagues (2017) used the term “in situ change” to describe how neighborhoods change around nonmobile Black and White families, arguing that such change “may be at least as important as racial differences in residential mobility in driving neighborhood racial disparities” (p. 1820). While many people who are dissatisfied with their housing ultimately move (Speare 1974), others are therefore unable to do so. This suggests that just as there are “voluntary” and “involuntary” moves, there are “voluntary” and “involuntary” stays.

In recent years, researchers have begun to examine who these nonmovers are. Studying “immobile” renters, Desmond and colleagues (2015) hypothesized that they tend to fall in the economic middle—between low-income families who are forced to move frequently and higher income families who are free to move wherever they please. Coulton and colleagues (2012) explored heterogeneity among populations that do not move. They characterize 22 percent of households who did not move as “dissatisfied stayers,” who were more likely to stay in their housing situations due to constraint rather than choice (Coulton et al. 2012:72).

In a study of middle-income renters in New York City, Shakespeare (2022) found that renters make trade-offs to remain in desirable neighborhoods, units with below-market rent, or situations with positive landlord relationships. Other research focuses on why low-income residents stay in their housing. Drawing on data with low-income Baltimore residents, Rosen (2017) found that many “craft narratives to make sense of how they live and survive in their communities despite the perils they face” (p. 271). Yet these narratives can be disrupted by incidents such as neighborhood violence, which, in turn, prompt families to move to restore some semblance of safety (Rosen 2017). In related research that draws on a sample of low-income mothers, Phinney (2013) found that “dissatisfied stayers” are more likely than other groups to experience problems with housing quality and neighborhood safety.

The present study builds on this small body of research about why people stay, finding that many renters (and a surprising number of homeowners) feel unable to move even when they would prefer to do so. As rental and housing prices rose in the Bay Area, many respondents felt “stuck in place.” Rather than discussing potential moves, respondents instead discussed how and why they stayed in their housing arrangements. Respondents believed that they would be unable to find new places to live that were affordable. As a result, renters, in particular, remained in undesirable and sometimes hazardous living arrangements. This article therefore reveals the compromises that Bay Area residents make to live in one of the nation’s most expensive housing markets.

Methods

To examine the housing strategies of Bay Area residents, I draw on data collected through the Taking Count project, a multimethods project that combines survey data (N = 3,100) and in-depth interviews with 50 survey respondents. The telephone survey was conducted in 2018 in the six counties that make up the San Francisco Bay Area (Alameda, Contra Costa, Marin, San Francisco, San Mateo, and Santa Clara). These counties are home to 6.5 million residents. Compared to the nation, the region is racially diverse, and has particularly high percentages of Latinx and Asian residents (though a lower percentage of Black residents compared to the nation’s average of 13.6 percent; U.S. Census 2022). The San Francisco Bay Area is currently 42 percent White, 24 percent Latinx, 23 percent Asian, and 6 percent Black (Bay Area Census 2023).

The Bay Area is a useful site to study housing. The region has experienced a sharp rise in housing prices, due, in part, to the recent influx of highly paid tech workers (Solon 2021). In August 2019, the median price of a single-family home in the Bay Area was $900,000 (California Association of Realtors [C.A.R.] 2021). Cities like San Francisco and San Mateo boasted even higher prices of about $1.5 million in 2019 (C.A.R. 2021), with recent reports of houses selling for up to $1 million over their asking prices (Solon 2021). Median rents in the Bay Area hover around $2,000 a month (U.S. Census 2020), with median rents in San Francisco rising to $2,850 for a one-bedroom apartment in 2022 (Kolomatsky 2022). In addition to high housing costs, the Bay Area has an extremely tight housing market. California has the lowest rate of housing unit vacancy in the country, and the six counties circling the San Francisco Bay have some of the lowest vacancy rates in the state (U.S. Census 2021). The Bay Area therefore offers insight into how families make decisions about housing in a region where housing options are constrained.

The high costs of housing and low vacancy rates in the Bay Area make it difficult for residents across the income spectrum to afford a home. Recent estimates show that there are only 35 affordable units for every 100 extremely low-income households 1 in the Bay Area (Aurand et al. 2021). One-in-three Bay Area residents—or 1,524,600 people—are considered “very low-income” and may struggle to find affordable housing (Ross and Treuhaft 2020). In fact, considering the high costs of living in the region, even those with middle-class incomes may face difficulties securing housing. While the official poverty measure identifies a family of four as poor if their income falls under $26,000, the supplemental poverty measure places the cut-off at $40,000 for the region (Austin 2020). Others argue that in cities like San Francisco, even families making $140,000 per year cannot afford the cost of housing (Woetzel et al. 2016). Data from the Bureau of Labor Statistics (2022) find that Bay Area residents spend nearly 42 percent of their household budgets on housing (compared to 34 percent nationally). Rather than focusing exclusively on low-income residents, this study examines Bay Area residents across the income spectrum, from those earning less than $25,000 a year to those earning nearly $1 million. The sample includes renters, homeowners, and those living with friends and family to offer a more comprehensive portrait of how people maintain housing.

Although housing costs are high, the Bay Area offers some legal protections against rising prices for renters. Many cities, including San Francisco, San Jose, Oakland, Berkeley, and Alameda, have some form of rent control or stabilization (Urban Displacement Project 2023). Yet many housing units, including newer buildings and single-family homes, are not covered due to California’s Costa-Hawkins Rental Housing Act (Urban Displacement Project 2023). In the San Francisco Bay Area, where 85 percent of residential land is reserved for single-family housing, this leaves many renters with few protections against rent increases (Menendian et al. 2020). Furthermore, once tenants vacate a rent-stabilized unit, the landlord may raise the rent to market rate, meaning that units often only remain affordable so long as they are occupied (San Francisco Planning 2020).

The Taking Count survey was created to take stock of the hardships among Bay Area residents (for more information see Taking Count 2020). The survey sample was drawn from lists of landline and cellular numbers, stratified by county to ensure roughly equal samples. To produce a racially and economically diverse sample, the sampling strategy targeted low-income households, Latinx and Asian American households, and residents under 30 years. The survey included a module on housing that asked questions about housing costs, living arrangements, length of residence, and a section on hardships that asked specific questions about several housing-related hardships. 2 The survey also collected detailed information about demographics, including income, race/ethnicity, gender, age, and education. Throughout the article, percentages are survey-weighted and representative of the population of the six-county Bay Area in 2018.

In addition to survey data, the Taking Count study included 50 in-depth in-person interviews with a randomly selected subsample of the survey respondents. These interviews were conducted by the author and two other members of the research team between May and September 2019. The semistructured interviews, offered in English and Spanish, ran from 45 minutes to two and a half hours. Respondents were compensated with a $40 gift card. All interviews were recorded and transcribed, and interviewers wrote detailed field notes and respondent profiles after each interview (see Appendix for a Profile of Respondents). This mixed-methods study offers multiple perspectives on housing in the Bay Area. Survey data offer information about a snapshot in time, while interviews provide information about both respondents’ current living situations and their past experiences. Together, these data offer insight into the housing arrangements of Bay Area residents to contextualize the decisions they make around housing.

To analyze the interview data, the research team developed a list of 160 codes, both theoretically informed and based on the interview experience. We tested the coding scheme on a small number of interviews (eight) using Dedoose before fully coding all interviews. While coding, we also added analytic codes to describe themes that emerged in the data. For example, after reading repeated descriptions of respondents feeling stuck in the Bay Area, we added a new code for “feeling stuck” to capture these experiences. Here, I draw primarily on 15 codes that relate to “housing,” which cover topics ranging from discussions of housing situations and strategies to more specific codes about housing quality, stability, and compromises.

Results

Below, I draw on survey and interview data to first describe respondents’ housing arrangements and costs. I then turn greater attention to the in-depth interviews to examine how respondents feel about their housing circumstances and the strategies they use to maintain housing in the Bay Area.

Housing Arrangements in the Bay Area

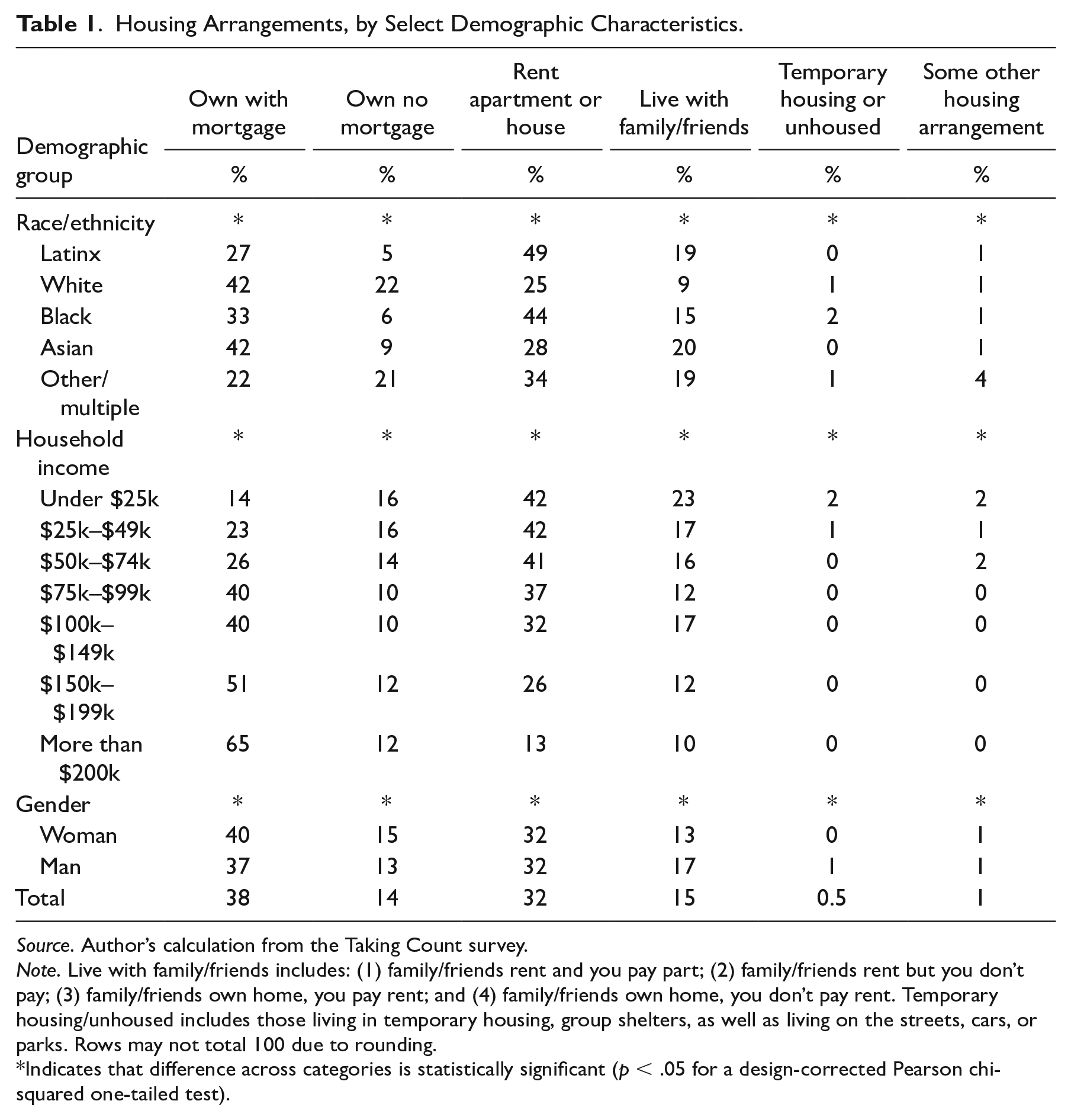

The survey first offers insight into the housing arrangements of Bay Area residents. Fifty-two percent of survey respondents reported owning a home, while nearly a third (32 percent) reported renting. Another 15 percent of respondents lived in a home owned or rented by a friend or family member. Housing arrangements varied significantly by race/ethnicity, income, and gender (Table 1). Mirroring national data, White respondents were more likely to own their homes, and were especially likely to own without a mortgage. Sixty-four percent of White respondents owned their homes compared to 51 percent of Asian respondents, 39 percent of Black respondents, and 32 percent of Latinx respondents. Latinx (49 percent) and Black (44 percent) respondents were more likely to rent their homes compared to White (25 percent) and Asian (28 percent) respondents. Asian (20 percent) and Latinx (19 percent) respondents were more likely to report living with friends or family, especially compared to White (9 percent) respondents. Although the sample captured a small number of respondents who were unhoused or living in temporary shelters, Black respondents (2 percent) were more likely to report these living situations.

Housing Arrangements, by Select Demographic Characteristics.

Source. Author’s calculation from the Taking Count survey.

Note. Live with family/friends includes: (1) family/friends rent and you pay part; (2) family/friends rent but you don’t pay; (3) family/friends own home, you pay rent; and (4) family/friends own home, you don’t pay rent. Temporary housing/unhoused includes those living in temporary housing, group shelters, as well as living on the streets, cars, or parks. Rows may not total 100 due to rounding.

Indicates that difference across categories is statistically significant (p < .05 for a design-corrected Pearson chi-squared one-tailed test).

Housing arrangements also differed by household income. Fifty percent or more of survey respondents with household incomes above $75,000 reported living in a home that they owned. This percentage reached nearly 80 percent among those with household incomes over $200,000. Among those with household incomes under $75,000, renting was the most common living arrangement. Nearly 2 percent of those in the lowest income group also reported being unhoused or living in temporary housing. Living with friends and family was also a notable strategy across all income groups, but especially among those making under $25,000. Roughly 23 percent of respondents making under $25,000 and 17 percent of those making $25,000–$49,000 reported living in homes owned or rented by friends or family. It is also possible that living with friends and family is slightly underreported in the survey; interviews revealed that some respondents who reported living in homes that they owned on the survey were in fact living with relatives.

Housing Costs and Hardships

According to the survey, 40 percent of residents reported paying over $2,000 a month in housing costs, with 7 percent paying over $4,000. Twenty-four percent of respondents reported no housing costs, though this category represented a heterogeneous group, ranging from those who had paid off their homes to those living with friends and family to those living in shelters. At the other extreme, 15 percent of the total sample reported putting 50 percent or more of their household income toward housing costs.

Respondents making under $25,000 a year reported the greatest housing cost burdens. Fifty-three percent of these low-income respondents reported spending 50 percent or more of their household income on housing costs. Among those making over $200,000 a year, more than a third (34 percent) reported spending only 1–9 percent of their household income on housing and only 2 percent spent 50 percent or more. Results also show significant differences by race. Black respondents reported the greatest housing cost burdens and were more likely to spend 50 percent or more of their household income on housing costs.

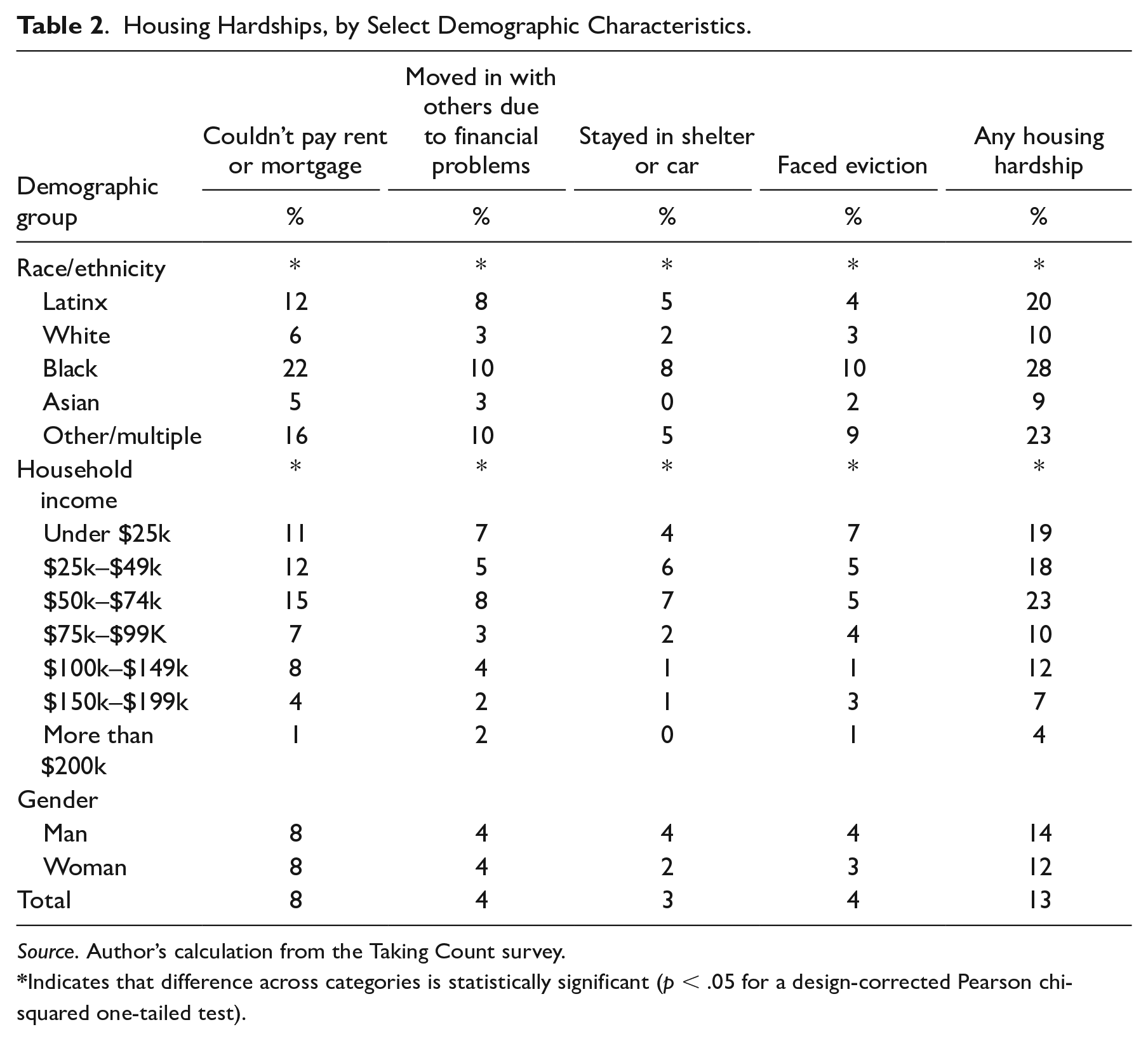

The survey also asked respondents about a series of housing hardships, including whether they (1) couldn’t pay their rent or mortgage; (2) moved in with others due to financial problems; (3) stayed in a shelter or car; or (4) faced eviction (Table 2). Black respondents were the most likely to report all four of these hardships, with 28 percent of Black respondents reporting any housing hardship.

Housing Hardships, by Select Demographic Characteristics.

Source. Author’s calculation from the Taking Count survey.

Indicates that difference across categories is statistically significant (p < .05 for a design-corrected Pearson chi-squared one-tailed test).

Although we might expect low-income respondents to report the greatest housing hardships, those making between $50,000 and $74,000 were the most likely to report any housing hardship, and were the most likely to report specific difficulties including trouble paying rent/mortgages (15 percent), moving in with others (8 percent), and staying in a shelter or car (7 percent). It is possible that respondents in this income bracket made too much to qualify for housing assistance, but too little to keep up with the rising costs of Bay Area housing. Those making under $25,000 were the most likely to report that they faced evictions (7 percent).

During interviews, respondents across the socioeconomic spectrum commented on the high costs of housing—and its consequences—in the Bay Area. When asked the worst things about the Bay Area, over half of respondents immediately brought up the cost of housing, while others discussed housing costs elsewhere in their interviews. When asked to name the worst things about the Bay Area, Shanice (29 years old, Black, renter) explained, “The rent, because it’s not made for everyone to be able to live . . . It’s not attainable for everybody.”

Other respondents mentioned that wages have not kept up with the cost of housing, making it difficult for families to afford a home. Black and Latinx respondents, who reported the largest housing cost burdens in the survey, were the most likely to make the connection between wages and housing. Tiana (57 years old, Black, renter) explained: I get paid $17.15 an hour. But my rent is in the thousands . . . the little people are getting the minimum $15 or $14 an hour, but then they want $2,000 or $3,000 for rent. That’s the only negative thing about that. And that’s what’s sending the people out there in the streets. What else am I supposed to do, sleep in the car?

Tiana’s question is not purely rhetorical, as other respondents (described below) have resorted to sleeping in their cars. Jose (34 years old, Latinx, renter) similarly explained: We can’t keep up with the economy here in the Bay Area . . . where I work, we get a 5% raise increase, at the most, every 2-3 years. I pay rent, I get a 5% increase every year.

He went on to add that his situation is more fortunate than most, as his unit is rent-controlled. Nevertheless, he has seen his rent increase from $1,200 to $1,900 in the past five years.

The tech industry was a looming presence in conversations about housing. As Rachel (46 years old, White, renter) put it, “All these people in tech are making all this money and it’s driven the cost of everything up.” Albert (52 years old, White, homeowner), who has lived in the Bay Area since the 1980s, described some of the changes that he has witnessed that he associates with the tech industry: It’s gotten so much more affluent, and at the same time, the gap between the haves and have-nots has just become so pronounced. Which really corresponds with the rise of Google and Apple and everybody else, and the phenomenal amount of money Uber, Tesla, all these millionaires. It has changed the city.

These high costs and the presence of the tech industry contributed to a sense among some respondents that they no longer belong in the region. Kevin (33 years old, White, renter) explained that the region is “rapidly showing myself and folks like me that we’re not really welcome here anymore . . . I didn’t choose to be born here. I just was.” When asked about the worst things about the Bay Area, Samantha (25 years old, Latinx, lives with relative) similarly responded: The techies. I don’t have nothing against them, but it’s just like why would you guys come to the smallest cities and try to build these big companies? . . . I feel like they’re trying to get rid of all the people that are not tech people by raising the rent and building new buildings that are not affordable for low-income families.

But despite the feeling that only tech workers could afford to live in the Bay Area, the respondents in this study managed to remain in the region. In the sections that follow, I describe how respondents experienced their living arrangements and the strategies they used to maintain their housing.

Feeling Stuck

Much of the literature on housing instability examines why families move (DeLuca and Jang-Trettien 2020; DeLuca et al. 2019; Desmond 2016). Less research focuses on those who remain and how they manage to do so (Hanson 2005; Shakespeare 2022). Despite this focus on mobility, many respondents in both the survey and interview sample might be more accurately described as immobile. Nearly 60 percent of survey respondents have lived in the same residence for six or more years and 22 percent have lived in the same place for at least 20 years. Only 9 percent of survey respondents have lived in their current residence for under a year. White respondents (33 percent) were more likely to live in their current homes for over 20 years, reflecting higher homeownership rates. Fewer Latinx (13 percent) and Asian (14 percent) respondents reported residing in their homes for over 20 years. Asian (12 percent), Black (9 percent), and Latinx (8 percent) respondents were more likely than White respondents (6 percent) to report living in their current home for less than a year, though the percentages remain relatively small for all groups.

At face value, the respondents in this study represent Bay Area success stories, in that they have managed to find and maintain housing in one of the nation’s most expensive cities. Yet evidence from interviews reveals a deep ambivalence about their housing circumstances. Many interview respondents described feeling locked into their housing situations as the cost of housing rose around them. As Gabriella (42 years old, Latinx, renter) explained: [T]he rent is very expensive. If you want to move out, you’re really stuck because [of the] rent. Not only that, but they sometimes require first month’s rent, the deposit, and last month’s rent . . . It’s like $6,000 just to move plus all the other expenses that come along. It’s very hard.

Rachel (42 years old, White, renter) is currently struggling to find a cheaper place to rent. She explains that the rent on her studio apartment has increased by $700 since she began living there. But she is unsure whether she will find anything less expensive, even if she downsizes from her studio to renting a room in a house. As she explained, “It’s like I’m not saving that much if I move, so, I might as well just stay where I am.”

Some respondents described a double-edged sword of “lucking” into (relatively) inexpensive housing only to feel that it would be prohibitively expensive to leave. When asked if she has considered moving out of San Francisco, Nicole (42 years old, White, renter) explained that her boyfriend is very reluctant to leave their apartment: My boyfriend won’t . . . he’s like, “Well, it’s expensive everywhere now, so it’s not like there’s a benefit to move out of the city, because it’s still expensive.” And he said, “We have rent control.” I said, “Okay, so I’m gonna die in this apartment, aren’t I?” He said, “Probably.”

For Nicole’s boyfriend, the idea of giving up a rent-controlled apartment is unfathomable.

During her interview, Mary (46 years old, White, renter) also described rent control as the main reason she has been able to stay in the Bay Area, saying: they’re only allowed to increase it three percent every year. So, because of that, thankfully, my base rent is like $685 a month . . . That’s the only reason that I can afford to be in the Bay Area.

Despite issues with the home, she noted that it would be difficult, if not impossible, to find a less expensive arrangement today, adding “it does make you kind of stuck.”

Homeowners also described feeling “stuck,” as they felt unable to buy back into the Bay Area if they were to sell their homes. Michael (48 years old, Asian)—who currently lives with his mother in a home that she owns—explained, “Why do I stay here? Because we’re financially stuck. If you sold the house, you could not find a more affordable house.” Other respondents noted that homeowners in the Bay Area may be reluctant to move, as doing so would lead to higher property taxes. Mark (54 years old, White, homeowner) bought his home in San Francisco 26 years ago. Although he feels extraordinarily lucky to have bought when he did, he worries that if he sells, “we’re not gonna be able to afford to buy back in” due in part to the property taxes: That’s probably been a factor for us staying put because our property taxes are pretty low because we bought a long time ago, and it didn’t change. So, in a way, that’s good. But in a way, that’s bad because it kind of locks things down. That’s one of the reasons why we wouldn’t sell is that we lose this low tax base. And even if you could come up with the money to buy some of the houses these days, the amount of money you have to pay in taxes every year is enormous.

There were, however, some respondents who felt less constrained. Many of these respondents worked in the tech industry. Joshua (35 years old, White, renter) works for an artificial intelligence company and has a household income of about $400,000 a year. When asked about the worst things in the Bay Area, Joshua responded: Number one—and I think this is probably the reason why I would ever leave—is it’s just obnoxiously expensive. The cost of living here is insane . . . I do well for myself and I work for a company that takes care of me . . . but it’s not easy. It’s very expensive and I’m beginning to not really justify the amount of rent that we’re paying and I want a place where I can put some roots down, buy a house.

Despite making nearly half a million dollars a year, Joshua feels priced out of the Bay Area housing market and has yet to purchase a home. But he is also in a better position to move elsewhere. Unlike Gabriella, who described how difficult it would be to put together the money required to move, Joshua’s high income makes it easier for him to consider leaving.

Although he currently owns his home, James (50 years old, White, homeowner) is similarly thinking of leaving the Bay Area: We bought just underneath the very peak of the last boom before the rush. I feel the same way right now, which is part of the reason why I want to sell it now. I feel there are economic winds blowing that just don’t feel right. I’m not an economist, but it’s just my instinct telling me that. So, I’d rather get what we can now.

John (37 years old, White, homeowner) is also planning his moves based on economic forecasts. As he explained, “I suspect maybe there will be a recession in the next year or year and a half . . . What I technically should do is wait until all the home values drop, and then I would buy.” Most of these respondents who were seriously considering leaving were transplants to the Bay Area, and did not have family ties in the area that keep others rooted in place. Many were also tech workers, who could afford to relocate and had the flexibility to think carefully about how to strategically time any such moves to ensure they would maximize their profits.

Strategies to Maintain Housing

While some respondents contemplated moving, the vast majority chose to stay put. In the following sections, I examine how these respondents managed to stay in the San Francisco Bay Area in the face of rising housing prices. Interviews reveal that housing strategies differed markedly for homeowners and nonhomeowners. For homeowners, remaining in the Bay Area was largely a matter of retaining their current home, even if it was not a perfect fit for their family. Nonhomeowners, however, were more likely to make additional trade-offs to maintain their housing, some of which carried negative consequences in both the near and long term. These trade-offs included compromising housing quality, doubling-up with friends and family, and living in legally precarious living arrangements.

Staying in the starter

For many homeowners, remaining in the Bay Area primarily involved a decision to put up with what they might have otherwise considered a “starter home.” Amara (39 years old, Indian, homeowner) currently lives in a 1,000-square-foot house with her son and husband. She described her family as “the lucky ones—people not able to move out of their starter homes.” The family recently considered putting an addition on the house because, as Amara reasoned, “we can’t afford to go and buy another house. Let’s try to build.” But she found that demand for contractors is high as “everyone is having the same idea.” In the end, Amara put expansion plans on hold, deciding “we can manage with what we have.”

Similarly, Mark (54 years old, White, homeowner) originally thought of the house he purchased in the early 1990s as a “starter home.” As he explained: It was a little, tiny place, and I remember thinking, “I’ll be here for five years, and then we’ll do something else.” We never did. I thought about moving down in the peninsula a couple times, but it seemed expensive, and the property taxes go way up. We never had kids, so I mean, it’s 800 square feet, but it’s nice, and it works fine.

Although the home is small, Mark is content with the way his housing situation has developed: I like that it feels secure . . . one of the things that worked for us was we bought it a long time ago. We paid it off a little bit ahead of schedule over the years, in part because we didn’t sell it and keep getting something bigger, and bigger, and bigger. And that was something of a conscious strategy on our part . . . just being happy with what we had has left us in a position where we have it, we own it. It’s modest, but it works and it’s ours.

While both homeowners and nonhomeowners described feeling “stuck” in their housing, homeowners were more likely to characterize their arrangements as “secure.” Despite wanting more space, homeowners like Mark and Amara describe themselves as “lucky” to own their homes in a region where many cannot. Furthermore, because they continue to gain equity in their homes, staying put can be an advantageous strategy for Bay Area homeowners in the long run. Between 2012 and 2019, the average home value in the San Francisco Bay Area increased by 88 percent (Carlisle 2021), suggesting that staying put can literally pay off for homeowners. The same is not true for nonhomeowners. In the next sections, I document the approaches that nonhomeowners took to maintaining housing in the Bay Area and the consequences of these strategies.

Compromising housing quality

Like homeowners, many nonhomeowners doubted that they would be able to find affordable housing if they moved, and instead remained in their current housing situations. Yet their circumstances were notably more precarious, and sometimes meant enduring obvious issues with housing quality. Nonhomeowners often described their housing as “dilapidated,” “falling apart,” or “unsafe.” These respondents traded housing quality for a chance at remaining in the Bay Area. Non-White renters, in particular, noted that they have had difficulty getting problems in their apartments fixed. When asked about her apartment, Shanice (29 years old, Black, renter) explained, “It’s a lot of work to be done. I’ve been here five years. I need a lot of updates.” Brenda (38 years old, Latinx, renter) also explained, “right now, the floor is tearing. The apartment building knows that. I have to be very careful with everything that I do so I don’t damage something.”

Renters often worried that they would be blamed for damaging their apartments if they voiced concerns about housing quality. In many cases, this led renters to refrain from contacting their landlords about housing issues. Renters similarly avoided asking their landlords to make necessary upgrades or improvements to their apartments, such as asking for new floors or appliances, worrying that any requests would be met with an increase in rent. Gabriella (42 years old, Latinx, renter) explained that the “landlord doesn’t really do any fixer uppers unless I really need it. I’ll call him. But if not, I try not to bother him. I’m afraid for him to raise the rent. That’s one of my concerns.” Gabriella detailed several problems with the apartment—ranging from mold to issues with the flooring—but chooses to put up with them rather than involve her landlord or look for housing elsewhere. Yet this reluctance to contact landlords meant that renters endured living in structurally unsound or hazardous conditions. While Shakespeare (2022) found that middle-income renters in New York were more likely to negotiate and form relationships with their landlords to maintain housing, lower-income and non-White renters in the Bay Area preferred to fly under the radar of their landlords. This may suggest racial and class differences in who can successfully build advantageous landlord relationships.

Because many renters were struggling financially, they were also unable to make updates on their homes themselves. Mary (46 years old, White, renter) has had a particularly difficult time affording necessary fixes for her home. Recently, Mary’s heater broke, and she went through the winter without fixing it: I have not managed to get it replaced yet. I’m like, we survived, and it wasn’t that bad. We may go another year without it. Because those things are expensive. I’ll just bundle up with more blankets. Do the laundry at night—I’m running the dryer at night to warm the house up—bake more in the oven, go to bed early, bundle up. And be thankful that we’re in the Bay Area where it doesn’t get too horribly cold. Although there were a few times this last year where we dropped really low.

Research on housing decisions often finds that issues with housing quality prompt poor families to make “reactive” moves (DeLuca and Jang-Trettien 2020; DeLuca et al. 2019). While many low-income renters in this sample experienced these hardships, they largely chose to put up with them rather than risk losing their housing altogether. In an expensive housing market, with few inexpensive rental options, many took a “better the devil you know” approach to housing.

Despite attempts to keep housing in the face of issues, there were instances where these issues led to forced moves. When this happened, respondents were often left in worse circumstances than they started. During her interview, Ava (28 years old, Latinx, lives with relative) described a series of events that ultimately left her unhoused for much of the winter. Her problems started after she reported a stain on the wall of her apartment, which turned out to be a dangerous form of mold. She relocated to another apartment, but after a short while, the heater broke and the indoor temperature dipped into the 40s. Ava explained, “I lost housing at that point because I couldn’t sleep inside when it was so cold . . . I was just like ‘I’m done. I have to leave.’” Ava spent the next few months sleeping in her car parked near a 24-hour Safeway, where she could use the restroom. Reflecting on this period, Ava said, “That was horrible. I wouldn’t wish it on anybody.” After several months, Ava ultimately moved back in with her parents. Ava’s situation was extreme, but puts into context how dire losing housing in the Bay Area can be and why many respondents sought to avoid giving their housing up at all costs.

Doubling-up and family support

Another strategy respondents used to maintain housing in the Bay Area involved receiving support from family. Living with friends and family was a relatively common housing arrangement, used by 15 percent of survey respondents. This arrangement was more common among Latinx (19 percent) and Asian (20 percent) survey respondents. Yet the survey further shows that Black (10 percent) and Latinx (8 percent) respondents were more likely than Asian (3 percent) and White (3 percent) respondents to move in with friends or relatives specifically due to financial problems. While doubling-up often helped respondents remain in the area, many of these situations came with drawbacks and were largely only available to people with family nearby. As I discuss below, there were also notable racial and class differences in the forms of family support residents received.

Many respondents described instances where friends and family provided important housing support. When asked how they found housing in the Bay Area, Alex (25 years old, White, lives with friend) explained, “My sister was going to go traveling for a few months, so she let me stay at her place. So family, basically. That’s how I landed.” After moving out of their sister’s apartment, Alex spent time cycling between friends’ couches.

Others explained that they would not be able to afford housing in the Bay Area had it not been for their family members. Destiny (30 years old, Black) currently lives with her grandmother. During her interview, she noted: I guess with millennials, it’s kind of weird to just be home. But I know a lot of my friends whose family don’t have homes so they are staying in living rooms or staying with different people, so they’re homeless and I’m not.

Destiny’s portrayal of Bay Area housing was borne out in other interviews. Michael (48 years old, Asian) described living in a recreational vehicle for about five years before moving back in with his mother. Interestingly, however, both Destiny and Michael reported that they owned their homes when taking the initial survey when they in fact lived in homes owned by relatives. This suggests that surveys may undercount the number of people who live with family members.

While living with family members was a common solution to the high costs of housing in the Bay Area, it also created tensions. Respondents described overcrowded conditions and disputes that arose from shared housing. Ava (28 years old, Latinx), who is currently living with her parents after a six-month stint of living in her car, feels guilty about her arrangement, saying, “I feel bad for taking space. We kicked my parents out of their room—not on purpose, they did this for us. So they’re sleeping in the family room, my mom and dad. So, I feel so bad.” Although living with her parents is a notable improvement from living in her car, Ava feels uneasy about the arrangement and worries that it will strain relationships with her family. Yet her situation also highlights the importance of having family in the Bay Area. Had Ava not had family in the region, it is unclear where she would have turned for housing support.

Samantha (25 years old, Latinx, lives with relative) recently moved out of her mother’s house and moved in with her boyfriend’s parents and extended family members. Although the arrangement is cheaper than renting their own apartment, she describes it as less than ideal, as other family members tend to monopolize the space: It just sucks. The whole sharing the kitchen and everything because it’s not even really shared, it’s more like it’s [extended family member’s] kitchen and that’s it. I feel like if I go cook, she’ll be like, “Oh, are you almost done? Because I don’t like people in the kitchen when I’m cooking.” And I’m like, “Girl, you’re always in here.”

Reflecting on a time when she lived with extended family, Gabriella (42 years old, Latinx, renter) similarly explained, “sometimes that was hard, because the dynamics of the family situation, sometimes it was a little hard. So, that wasn’t fun to have a house like that.”

In other cases, however, doubling-up had advantages. Living with relatives allowed some respondents to save money for their own homes. This was the case for William (36 years old, White, homeowner). When asked how he was able to afford the down-payment for his home, William explained, “I was able to live with my parents rent-free, which was a huge benefit. I was able to put a lot of money away.” Yet respondents who were able to make the transition from doubling-up to homeownership tended to be those who were racially and economically privileged to begin with. Doubling-up in these situations was often intended from the start as a short-term strategy to save for something bigger—such as a down payment—rather than an indefinite arrangement born of necessity.

While some respondents doubled-up with relatives, others received housing support in other forms including inherited property or financial gifts. Although both the survey and interview data suggest that non-White respondents were more likely to double-up with family members, especially in times of financial hardship, White respondents were more likely to get support from family in these other forms. For instance, Rachel (46 years old, White, renter) currently works part time at a health club in Marin. Although she makes only about $10,000 a year through this work, she lives in a studio apartment that costs $1,750 a month. When asked whether she has a difficult time paying rent, Rachel responded, “No, because I get support. And I will always get support.” Rachel went on to describe the financial support she receives from her parents, saying, “I get $1,500 a month and my rent is $1,750. So, it takes all of that and then I still have to work and come up with $250.” Later during her interview, Rachel mentioned that her parents own two houses in San Francisco (including one that her father inherited from his parents), in addition to the house her father lives in Marin. Her parents rent these houses out, which provides additional income to her parents that they can then pass on to Rachel. In this case, family support and intergenerational wealth were key to keeping Rachel in the Bay Area.

Legally precarious arrangements

Many respondents who lived with friends and family also found themselves in legally precarious housing arrangements, without an official lease. In most cases, these arrangements felt stable to the respondent, as their de facto landlords were friends and family members. But these arrangements could fall through if circumstances changed. Gabriella (42 years old, Latinx, renter) recounted one such situation where plans with extended family backfired, drastically changing her housing circumstances. About five years ago, Gabriella and her husband bought a house with the understanding that her husband’s extended family would contribute to the mortgage payments in the form of rent. As she explained, “the house was just between the dad and us, and the brothers were paying rent.” Ultimately, however, the other family members lost their jobs. Unable to pay the mortgage without the added income from her family, Gabriella lost the house, and the entire family was forced to move.

Other respondents described unofficial arrangements that did not involve their immediate families. When asked about his housing strategies in the Bay Area, Kevin (33 years old, White, renter) explained, “I’ve never been an official on the lease, official tenant, not since 2006.” This strategy has landed him in trouble in the past. A few years earlier, Kevin lived in an apartment that he described as “totally dilapidated,” paying just $600 a month for the “biggest room in the place,” which he considered a steal for the area. Yet Kevin did not have an official lease and his landlord eventually pushed him out of the apartment in favor of more highly paid tech workers. As he described it, “And of course, they’re paying more. The landlord wanted them there more. So, we didn’t technically get evicted, but we got pushed—we got intimidated into leaving.”

Yet Kevin has stuck with this strategy of finding legally precarious housing to keep his rent manageable. He is currently living in a relatively inexpensive room in San Francisco with shared amenities. When asked about this apartment, Kevin explained, “by most people’s standards, it’s a 4 out of 10. By mine, it’s like an 8.” He added that once again: There’s no paperwork or anything. They could just say, “Get out.” And I’ve got to get out . . . My landlord says I can stay as long as I want, and he’ll give me plenty of notice if he plans on anything. He says that. I trust him, though maybe I shouldn’t.

In many cases, these legally precarious arrangements—whether in the form of living with family members or not—provided a low-cost way of living in the Bay Area. But they can be a high-risk solution, leaving respondents vulnerable to housing loss if circumstances change. Paradoxically, these strategies intended to help respondents keep affordable housing in the Bay Area carried a high potential to backfire.

Discussion

Against the backdrop of rising housing costs in the Bay Area, this article provides insight into how a racially and socioeconomically diverse group of residents make housing decisions in a region where housing options are limited. Much research on housing unaffordability focuses on how low-income residents are displaced (DeLuca et al. 2019; Desmond 2016). This project takes a slightly different focus to address how residents across the income spectrum manage to stay in an expensive housing market and the compromises they make to do so.

Survey data first document variation in the living arrangements of Bay Area residents, revealing inequalities by race and income. White respondents and those with higher incomes were the most likely to own their homes. Asian and Latinx respondents were more likely to live with friends and family members, though Black and Latinx respondents reported that they were more likely to move in with others specifically due to financial hardship. Black respondents were the most likely to experience housing cost burdens, and were the most likely to face housing hardships such as eviction or homelessness. Somewhat surprisingly, those with household incomes between $50,000 and $75,000 were the most likely to report a housing hardship, possibly because they make too much to qualify for most assistance programs but too little to comfortably afford housing in the region.

Interview data then shed light on how respondents experience these arrangements and how they navigate housing in the Bay Area. Many researchers see residential consistency as beneficial (Frederick et al. 2014; Wood, Turnham, and Mills 2008). And undeniably, having a reliable place to live is better than not. Yet these interviews reveal much ambivalence among those who were able to remain in the Bay Area. Indeed, many Bay Area respondents felt “stuck” in their housing arrangements and made compromises to maintain their housing. In the case of low-income renters in particular, the housing arrangements residents cobbled together were not necessarily ideal or secure. Yet residents felt the need to keep these arrangements by any means necessary.

To stay in the Bay Area, residents who did not own their homes made several trade-offs including living in structurally inadequate housing, moving in with friends and family, and accepting legally precarious living arrangements. In many cases, renters chose not to contact their landlords about structural issues or potential upgrades, fearing that their rents might increase if they did. While such structural issues might prompt renters in loose housing markets to make “reactive” moves (DeLuca et al. 2019; Harvey et al. 2020), many renters decided to put up with unsound housing rather than face an uncertain housing market. Yet these trade-offs may have harmful consequences for respondents in both the near and long term (Burgard et al. 2012; Desmond 2016). Poor housing quality—including exposed wiring, lead paint, pest infestations, leaks, and lack of heat—is associated with negative consequences for the health and well-being of families and especially children (Leventhal and Newman 2010).

Prior research shows that the lack of financial resources can prevent families from moving (Coulter et al. 2016; Coulton et al. 2012; Hanson 2005). As Desmond and colleagues (2015) wrote, “the lack of affordable housing not only contributes to high rates of forced displacement among the involuntarily mobile, it also prevents the immobile from leaving resource-deprived and dangerous neighborhoods” (p. 254). Here, I show how tight housing markets—and the perception that there may not be other available housing options—create further constraints for families who would otherwise prefer to move. It is therefore important to consider the compromises that even those who manage to stay in expensive housing markets endure, as these represent another consequence of rising prices.

When housing is unaffordable, many people turn to friends and family (Clampet-Lundquist 2003; Harvey 2022). In this study, family members provided an important safety net for those facing housing insecurity. Many respondents, especially Latinx and Black respondents, reported doubling-up with family members due to financial difficulties. It appears that these living arrangements helped to stave off displacement—and even homelessness—among people who would otherwise be unable to afford rent. Yet many respondents also discussed the downsides of these arrangements, suggesting that they are often products of necessity. Although White respondents were less likely to double-up than other racial groups, they received financial help from their family members in other ways, often through inheritances or financial gifts. This support allowed those who could not otherwise afford to live in the Bay Area to remain in the region.

While homeowners also described feeling “stuck” in their homes, they reported feeling markedly more secure in their housing arrangements. Furthermore, although some homeowners noted that they decided to stay in their homes to maintain their relatively low property taxes, Proposition 19 (2020) recently made it possible for some homeowners, including seniors and people with disabilities, to transfer the taxable value of their existing homes to a new home (S.F. Gov 2020). While homeowners might still face trouble affording new homes in the Bay Area given rising home prices, this change may make it easier for some homeowners to move in the future. However, this change does little to improve the situation for renters, who often face more profound housing challenges.

This study is not without limitations. The Bay Area features both high housing costs and low vacancy rates (U.S. Census 2020; U.S. Census 2021). The Bay Area also has a particular policy landscape when it comes to housing. At the time of these interviews, many Bay Area cities—including San Francisco, Oakland, Berkeley, San Jose, and Richmond—required a “just-cause” for eviction (Urban Displacement Project 2023). In 2019, the California Tenant Protection Act made just-cause evictions a state-wide policy. California therefore has a lower eviction filing rate (2.2 percent) compared to the United States on average (7.9 percent; Eviction Lab 2023). Furthermore, because the survey sample was drawn from a list of landline and cellular numbers, the study may not reach all Bay Area residents. Although the survey and interview data do capture some unhoused respondents, they are likely undercounted. By design, the study focuses on residents currently living in the San Francisco Bay Area. It therefore highlights those who have found ways to remain in the region, rather than those who have already been displaced (who are another population worthy of study).

While these data were collected in 2018–2019, the COVID-19 pandemic may have increased housing challenges, especially for renters (Airgood-Obrycki et al. 2021). Future research might examine how the pandemic changed the strategies people used to find and maintain housing. These interviews reveal that some respondents find affordable housing in the Bay Area by living in legally precarious living arrangements where they do not have a formal lease. During the COVID-19 pandemic, many Bay Area cities enacted a moratorium on evictions (City and County of San Francisco 2023). While these policies likely helped some Bay Area renters avoid eviction, they may be of limited use to those who did not have a formal lease (also see Decoteau and Garrett 2022).

Although research on housing instability often focuses on families at the bottom of the economic spectrum (DeLuca et al. 2019; Desmond 2016; Harvey et al. 2020), this article takes a wider economic scope. This focus provides insight into the strategies and trade-offs of those who stayed in one of the most expensive housing markets in the country, adding to recent calls to consider immobility as an active process (Coulter et al. 2016; Hanson 2005). In many ways, the respondents in this sample represent a best-case scenario. Despite rising prices in the Bay Area, they all found ways to stay. Yet interviews with these residents suggest that very few felt content in their living arrangements and many—especially those who do not own their homes—made difficult compromises to stay in the region.

Footnotes

Appendix

Profile of Interview Respondents.

| Pseudonym | Age (years) | Race | Gender | Marital status | Children | Housing | Income group ($) |

|---|---|---|---|---|---|---|---|

| Aiko | 30 | Asian | W | Married | Y | Rent | 175,000–199,999 |

| Albert | 52 | White | M | Married | Y | Own with mortgage | 975,000–999,999 |

| Alex | 25 | White | NBi | Partnered | N | Live with relative | 0–24,999 |

| Alexandra | 57 | Latinx | W | Divorced | Y | Own with mortgage | 75,000–99,999 |

| Alice | 45 | White | W | Single | Y | Rent | 75,000–99,999 |

| Amara | 39 | Asian | W | Married | Y | Own with mortgage | 600,000–624,999 |

| Andy | 39 | Asian | W | Single | N | Own with mortgage | 100,000–124,999 |

| Anthony | 50 | Latinx | W | Married | Y | Rent | 0–24,999 |

| Antonio | 37 | Latinx | M | Married | N | Own with mortgage | 250,000–274,999 |

| Ava | 28 | Latinx | W | Married | N | Live with relative | 0–24,999 |

| Brandon | 24 | Black | M | Single | N | Lives with relative | 100,000–124,999 |

| Brenda | 39 | Latinx | W | Single | Y | Rent | 0–24,999 |

| Brianna | 26 | Black | W | Single | Y | Shelter | 0–24,999 |

| Camilla | 41 | Latinx | W | Married | Y | Own with mortgage | 100,000–124,999 |

| Christina | 28 | Latinx | W | Married | Y | Rent | 50,000–74,999 |

| Constance | 55 | Asian | W | Married | Y | Own with mortgage | 425,000–449,999 |

| Daniel | 44 | White | M | Married | Y | Own with mortgage | 100,000–124,999 |

| David | 28 | White | M | Single | N | Rent | 150,000–174,999 |

| Destiny | 30 | Black | W | Single | N | Lives with relative | 300,000–324,999 |

| Eric | 28 | Asian | M | Single | N | Rent | 125,000–149,999 |

| Ethan | 49 | White | M | Single | Y | Rent | 25,000–49,999 |

| Gabriella | 42 | Latinx | W | Married | Y | Rent | 50,000–74,999 |

| Jack | 31 | Asian | M | Married | Y | Own with mortgage | 250,000–274,999 |

| James | 50 | White | M | Married | N | Own with mortgage | 175,000–199,999 |

| Jana | 48 | Asian | W | Married | Y | Own with mortgage | 75,000–99,999 |

| Jasmine | 60 | Latinx | W | Single | Y | Own with mortgage | 250,000–274,999 |

| Jennifer | 57 | Latinx | W | Single | Y | Own with mortgage | 50,000–74,999 |

| John | 37 | White | M | Married | Y | Own with mortgage | 325,000–349,999 |

| Jose | 35 | Latinx | M | Married | Y | Rent | 225,000–249,999 |

| Joshua | 36 | White | M | Married | N | Rent | 325,000–349,999 |

| Kevin | 33 | White | M | Single | Y | Rent | 50,000–74,999 |

| Laila | 32 | Asian | W | Married | N | Rent | 150,000–174,999 |

| Mark | 55 | White | M | Married | N | Own no mortgage | 50,000–74,999 |

| Mary | 46 | White | W | Single | Y | Rent | 25,000–49,999 |

| Matthew | 33 | White | M | Single | Y | Own no mortgage | 0–24,999 |

| Michael | 48 | Asian | M | Single | N | Live with relative | 0–24,999 |

| Michelle | 57 | Asian | W | Married | Y | Owns with mortgage | 325,000–349,999 |

| Nathan | 55 | White | M | Married | Y | Own no mortgage | 200,000–224,999 |

| Nicole | 42 | White | W | Partnered | N | Rent | 125,000–149,999 |

| Peter | 27 | White | M | Single | N | Live with relative | 0–24,999 |

| Peter | 56 | White | M | Married | Y | Own no mortgage | 150,000–174,999 |

| Rachel | 46 | White | W | Single | N | Rent | 0–24,999 |

| Rosa | 25 | Asian | W | Married | Y | Own with mortgage | 75,000–99,999 |

| Samantha | 25 | Latinx | W | Partnered | Y | Live with relative | 0–24,999 |

| Scott | 48 | White | M | Single | N | Owns no mortgage | 0–24,999 |

| Shanice | 29 | Black | W | Married | Y | Rent | 0–24,999 |

| Tiana | 58 | Black | W | Partnered | Y | Rent | 25,000–49,999 |

| Tyler | 58 | Black | M | Married | Y | Own with mortgage | 300,000–324,999 |

| Vivian | 37 | Asian | W | Single | N | Own with mortgage | 75,000–99,999 |

| William | 36 | White | M | Married | N | Own with mortgage | 400,000–424,999 |

Note. W = woman; M = man; NBi = non-binary; Y = yes; N = no.

Acknowledgements

The author thanks Daniel Schneider, Irene Bloemraad, Kim Voss, and Taeku Lee, along with Jamie Austin and Jake Leos-Urbel at the Tipping Point Community, and research assistants Allison Logan, Adriana Ramirez, and Isabel Garcia Valdivia for making this research possible. She extends special thanks to Benjamin Bowyer for expert help with the survey data. She also appreciates Alex Brewer and Matthew Perrigino for their comments on early versions of this article. Finally, she offers her gratitude to the respondents of the Taking Count study for sharing their stories.

Funding

The author(s) disclosed receipt of the following financial support for research, authorship, and/or publication of this article: This research would not have been possible without the financial support of the Tipping Point Community and the University of California Berkeley’s Othering and Belonging Institute.