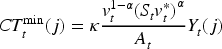

Abstract

Firms routinely invoice their exports in the buyer's currency, absorbing exchange rate risk they could otherwise pass on to consumers. We explain why, in a framework that bridges partial- and general-equilibrium analysis and delivers three results. In partial equilibrium, heavy reliance on imported inputs (α > 0.5) makes local currency pricing (LCP) optimal as a cost-side hedge (Proposition 2). In general equilibrium with complete financial markets, firms invoice in the currency of the most monetarily stable economy, a benchmark result that our general arbitrage condition nests as a limiting case (Proposition 8). Under incomplete markets, formalized as a bond economy, the cost-hedging motive regains primacy regardless of relative monetary stability (Proposition 9). Whether the cost-hedging or the monetary-stability motive dominates, therefore, turns on financial-market completeness. The model yields three testable predictions that link import intensity, monetary credibility, and financial development to observed invoicing patterns.

Keywords

Introduction

Exchange rate pass-through—the transmission of currency fluctuations to the prices of traded goods—has resisted a unified theoretical account in international macroeconomics. A well-documented empirical regularity is the “exchange rate disconnect”: exchange rate movements frequently exceed shifts in underlying fundamentals, yet their pass-through to import and consumer prices is both incomplete and sluggish (Devereux, 1997; Gopinath & Stein, 2021; Obstfeld & Rogoff, 1995). This disconnect gave rise to the pricing-to-market (PTM) literature, in which firms with market power set different prices across destination markets (Dornbusch, 1987; Krugman, 1987). Under nominal rigidities, PTM typically involves stabilising prices in the buyer's currency (Local Currency Pricing, LCP), which decouples consumer prices from exchange rate movements and can amplify exchange rate volatility in response to monetary shocks (Betts & Devereux, 2000; Chari et al., 2002).

Yet most of this literature takes the invoicing currency as given. So why does a firm take on exchange-rate risk, pricing in the buyer's currency when it could shift that risk onto consumers instead? Far from a mistake, the decision is a deliberate operational hedge. Earlier studies tie it to three things in turn: the exporter's market share and the elasticity of substitution it confronts (Bacchetta & Van Wincoop, 2005); the relative monetary stability of the two economies (Devereux & Engel, 2001; Devereux et al., 2004); and the part international currencies play in financing trade (Gopinath & Stein, 2021; Liu & Lu, 2019). The gap is that no model yet joins the hedging motives that global value chains create to these macro and financial forces, and none pins down which force wins out.

Global value chains sharpen the question. A firm reliant on imported intermediate inputs watches its production costs track the exchange rate one for one. Invoicing, meanwhile, is highly concentrated—more than 80% of world trade is settled in dollars or euros (Boz et al., 2025), currencies that serve as vehicles even between partners who use neither domestically. Our concern is the interaction itself: how firm-level production choices meet aggregate monetary conditions, and how the completeness of financial markets governs that meeting. The stakes are both theoretical and policy-relevant.

We make three contributions. In partial equilibrium, we show that the optimal invoicing currency is governed by import intensity α: firms with α > 0.5 prefer LCP as a cost-side hedge, while firms with α < 0.5 prefer PCP (Proposition 2). This result is absent from the prior general equilibrium literature, which assumes marginal costs are independent of the exchange rate. In general equilibrium with complete markets, we derive a general arbitrage condition (Proposition 6) from which the monetary-stability result of Devereux and Engel (2001) emerges as a special case under three restrictive auxiliary assumptions (Proposition 8). The contribution is the general condition itself, which nests the monetary-stability result alongside the cost-hedging channel and identifies the assumptions under which each dominates. We then extend the model to a bond economy with incomplete financial markets and show that the cost-hedging channel regains primacy irrespective of relative monetary variances (Proposition 9), establishing that financial market completeness mediates between the two channels.

We see our framework as a companion to Gopinath and Stein (2021), not a subset of it. Theirs—the “banking view”—operates on the demand side of financial markets, through safe-asset premia and the collateral constraints banks face. Ours operates on the supply side, through a firm's cost exposure to the exchange rate via imported inputs. Each captures something the other does not. What links the two is Proposition 6: one arbitrage condition, tractable enough to take to data, that holds import intensity α, the variance of the exchange rate, and the full covariance structure tying the exchange rate to economic fundamentals.

The argument unfolds across the remaining sections. Section 2 situates it within the literature; Section 3 sets up the partial-equilibrium model; Section 4 takes the model to general equilibrium and then to the incomplete-markets case; Section 5 develops the testable predictions; and Section 6 closes.

Literature Review

Currency invoicing, as Section 1 framed it, is a response to exchange rate risk—and the determinants of that response have been examined along four mostly disconnected lines: cost-based hedging, relative monetary stability, financial structure, and strategic interaction. We treat each one here and argue that no single model has yet tied them together. A sensible starting point is the exchange rate disconnect (Gopinath et al., 2010; Obstfeld & Rogoff, 1995). Throughout the OECD since the end of Bretton Woods, the disconnect appears in nominal and real rates, both, and the data show real exchange rates swinging persistently, with half-lives on the order of four to five years (Devereux, 1997; Hinterhuber & Liozu, 2017).

Two explanations compete. One, going back to Balassa (1964) and Samuelson (1964) and recently extended by Egorov and Mukhin (2023), points to international differences in the prices of non-tradable goods. The other, which matters more for the large industrialised economies, turns on departures from the law of one price among traded goods (Drissi & Boukhatem, 2020; Mukhin, 2022)—departures that imply genuine segmentation of international markets.

Segmentation of this kind motivated the “pricing-to-market” (PTM), or local currency pricing (LCP), models. There, firms with market power charge different prices in different destinations (Dornbusch, 1987; Krugman, 1987), and a later body of work has worked out what this implies for exchange rate dynamics (Betts & Devereux, 2000; Chari et al., 2000; Nagengast et al., 2021; Obstfeld & Rogoff, 1995). When prices are nominally rigid, PTM typically leaves them sticky in the buyer's currency. Consumer price indices then move only loosely with the exchange rate—a violation of the law of one price (Kollmann, 2001) that can also magnify how monetary shocks feed into exchange rate volatility.

Even so, this body of work tends to assume away the very choice that interests us—the decision to price in the buyer's currency in the first place. A prior question remains: why would a rational exporter retain exchange rate risk under LCP rather than pass it to the buyer under producer-currency pricing (PCP)? We think that choice warrants a formal treatment, and we supply one.

At the micro level, the drivers are well established. A bigger market share for the exporting country, together with a higher elasticity of substitution, tilts the choice towards PCP (Bacchetta & Van Wincoop, 2005; Devereux et al., 2004); strategic complementarities between competing firms add a further pull. The macro side is more straightforward—exporters tend to settle on the currency of the country whose monetary policy is steadier (Devereux et al., 2004).

A different line of work connects invoicing to the architecture of global finance. In the “banking view” of Gopinath and Stein (2021), a currency's grip on invoicing is strengthened by its function as a safe store of value within financial intermediation. Liu and Lu (2019) treat invoicing and finance contracts as jointly chosen, and they show how bank intermediation and collateral constraints can push a vehicle currency towards dominance, potentially divorcing the choice from the trading partners’ direct macroeconomic fundamentals. Assuming complete financial markets, then, can distort the predictions, since it takes perfect hedging for granted.

There is also the matter of how much invoicing contributes once a firm has other hedges available. The toolkit is broad—forward contracts and options, balance-sheet matching, natural hedges from adjusting where inputs are sourced, and trade-finance structures that embed the currency risk (Liu & Lu, 2019). Usage, though, is far from uniform. Big, globally active firms in well-developed financial markets favour FX derivatives (Ito et al., 2016), whereas smaller firms in emerging markets fall back on operational hedges, invoicing being one (Boz et al., 2025). The lesson is that invoicing matters most for hedging where financial markets are thinnest—precisely the interaction Propositions 6 and 9 formalise. So we treat invoicing not as the sole or even principal hedge, but as the residual one, whose value depends on how far financial instruments can substitute for it.

Fragmented production along global value chains brings a further consideration. A firm dependent on imported intermediates feels exchange rate swings directly in its costs, and that vertical structure pushes it to manage cost uncertainty through invoicing—typically by leaning towards LCP or pricing in the currency of its main inputs. This cost channel has theoretical roots in Bacchetta and Van Wincoop (2005) and Devereux and Engel (2003), and is empirically linked to dominant currency pricing (Cravino, 2017; Gopinath & Stein, 2021). Recent evidence confirms the stability of dominant currency patterns, with the US dollar as the global vehicle currency and the euro as a regional anchor, though emerging geopolitical tensions are now examined as a potential disruptive force (Boz et al., 2025; Brüggen et al., 2025).

Our paper extends this line by tracing market incompleteness through the supply side of the production process rather than the demand side of financial markets; the complementarity with Gopinath and Stein (2021) is set out in Section 1 and revisited in Section 4.5.

The literature has thus developed along these four lines without a model that nests them or identifies when one dominates. Our paper provides such a model, tracing the interaction between market incompleteness and firms’ production architecture through the cost-hedging channel—a mechanism distinct from, and complementary to, the financial intermediation channel of Gopinath and Stein (2021).

We build a dynamic stochastic general equilibrium model in which cost structure, exchange rate uncertainty, financial market architecture, and invoicing currency jointly shape firm behaviour and exchange rate pass-through. Extending the paper of Devereux et al. (2004), we show that a firm's optimal invoicing currency is determined by the relationship between relative monetary volatility, its exposure to exchange rate risk via imports, and the degree of financial market completeness. The central result is a general arbitrage condition that nests these determinants and identifies when the cost-hedging or the monetary-stability channel prevails.

Theoretical Model: Partial Equilibrium

The Firm's Program and Basic Setup 1

Consider a domestic firm operating under monopolistic competition, producing a differentiated good

The firm minimises costs given the domestic nominal wage

Consumer preferences in both countries are of the CES type. The resulting demand for the firm's good in the domestic and foreign markets is given by:

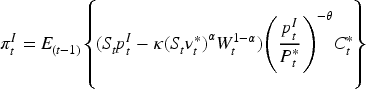

The model omits FX derivatives, balance-sheet hedging, and sourcing adjustments as alternative instruments. This omission is deliberate: the paper focuses on the operational risk management dimension of invoicing, and should be interpreted as analysing the marginal contribution of invoicing under the assumption that other instruments are either unavailable or already optimally deployed. The incomplete-markets extension in Section 4.5 provides the formal justification: when financial markets are incomplete, invoicing regains hedging value that cannot be substituted by financial instruments. We also assume that invoicing in local currency is feasible for the exporting firm. In practice, this may be constrained by buyer bargaining power, industry pricing conventions (e.g., dollar pricing of commodities), or the limited acceptability of the exporter's currency in international transactions. These constraints are discussed in Section 5 as part of the research design for empirical testing, where we note that buyer bargaining power is an important control variable in any empirical test of Prediction P1.

Under market segmentation, the firm maximises its expected profit separately in each market. Nominal rigidities are introduced by assuming prices are set one period in advance (in

In this case, the price of imported factors of production

The optimal selling price is determined by applying a markup to the marginal cost based on the first-order condition.

In the foreign market, the firm must decide both the pricing strategy (PCP or LCP) and the price to be fixed for period t. The reasoning is recursive: for each pricing strategy, the firm determines the selling price that maximises expected profit, then compares the profit levels to deduce the best strategy.

Under PCP, the firm faces demand uncertainty through the exchange-rate-dependent foreign price, which affects both sales volume and revenue.

The first-order condition with respect to

Since the exchange rate is the sole source of uncertainty, this simplifies to:

The firm applies a constant markup to the marginal cost. The law of one price applies: the same good is sold at the same price in both markets (i.e.,

The first-order condition gives:

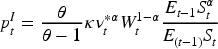

Since the exchange rate is again the sole source of uncertainty, this expression simplifies, and the price ptI that maximises expected profit is:

The firm sets a price in foreign currency by applying a constant mark-up to the expected marginal cost. The law of one price is valid only in expectation, since

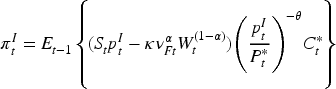

Given the expected profits for each strategy (equations (11) and (15)), Proposition 1 establishes the conditions under which the firm sets its price in one currency rather than another.

A domestic firm in partial equilibrium, which decides the currency in which to fix its export price in period

The firm compares the expected profits under both strategies (equations (11) and (15)):

This result is consistent with the literature (Friberg, 1998; Giovannini, 1988): it is more advantageous to price in the seller's currency when the profit function is convex in the exchange rate. With CES preferences and constant returns to scale, the firm's profits are always convex in S. Thus, exchange rate variability increases profits under PCP more than under LCP.

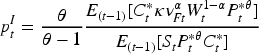

This result changes fundamentally when import costs are denominated in foreign currency. The exchange rate then affects the marginal cost because the price of imported goods is fixed in foreign currency, and the law of one price applies:

The first-order condition gives the optimal price:

Substituting back into (16), the expected profit is:

The optimal price is:

The expected profit is:

Comparing the expected profits in equations (18) and (21) yields Proposition 2.

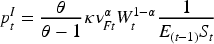

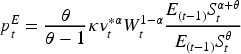

Consider a firm in partial equilibrium that exports its production. The optimal invoicing currency choice depends critically on the share of imported inputs, If the firm's production is less intensive in imported inputs ( If the firm's production is more intensive in imported inputs (

The firm compares the expected profits under PCP (equation (18)) and LCP (equation (21)). The sign of the difference

The threshold

The threshold

This partial equilibrium insight provides a new explanation for low exchange rate pass-through and deviations from the law of one price. Firms highly integrated in global value chains (high α) have a stronger incentive to invoice exports in the buyer's currency to hedge against exchange rate risk.

Proposition 2 establishes that the optimal invoicing strategy switches from PCP to LCP at import intensity α = 0.5. Three properties of this result merit discussion.

Analytical Content

The threshold is derived endogenously from the firm's expected profit maximisation under CES preferences and monopolistic competition. It balances two countervailing forces: the convexity of the profit function in the exchange rate, which always favours PCP (Proposition 1), and the concavity introduced by the cost function when α is large. To find the balance point, we combine Jensen's inequality with the log-moment generating function of a log-normal. Appendix A.2 shows that the qualitative result holds well outside log-normality. Once distributions are described by their cumulants, including skewed and fat-tailed ones, the threshold barely moves, and α and the LCP incentive stay monotonically related across the board. The value 0.5, in other words, is an artefact of the log-normal assumption, not of the economics. The threshold likewise nests in the general arbitrage condition of Proposition 6: set every covariance term to zero, and what survives is ½ Var(s)(2α − 1) ≥ 0 for LCP stability, so the partial-equilibrium result is a true limiting case. The robustness analysis and the cumulant-based derivation of the zone of indifference are in Appendix A.2–A.4.

Practical Limitations

Three frictions, in practice, carve out a zone of indifference around the threshold—a range over which firms hold their invoicing strategy fixed. Menu costs come first: switching the invoicing currency of a contract incurs administrative, legal, and relational costs, and only an expected profit gain that exceeds them justifies the change (Ball & Romer, 1990; Mankiw, 1985). Contractual inertia comes second, because trade contracts typically lock in the currency for the contract's life, sometimes years; the threshold binds only when the contract is renewed. Buyer power and industry convention come third. In sectors with concentrated buyers or settled pricing norms—commodities quoted in dollars being the textbook example, the currency is often dictated by the buyer or by convention, regardless of the exporter's cost structure.

Empirically, the upshot is that a test of Proposition 2 should anticipate a smooth, non-linear increase in LCP adoption as α rises above the threshold rather than an abrupt jump at 0.5. Threshold regressions, or specifications with flexible functional forms, suit the task—a point Prediction P1 (Section 5) takes up. A fuller treatment of the zone of indifference, one that incorporates switching costs, contract length, and bargaining power, is left for future work.

General Equilibrium and Optimal Pricing Strategy

The next step raises the partial-equilibrium analysis into a two-country general-equilibrium setting. Because the exchange rate, prices, and consumption are now pinned down inside the model, we can trace how the optimal invoicing strategy reacts to the way macroeconomic variables move together. We follow Devereux and Engel (2001) and Corsetti and Pesenti (2001) in constructing it.

General Equilibrium Framework

The economy consists of two symmetric countries. Each country is populated by households, a government (central bank), and two production sectors: a perfectly competitive intermediate goods sector and a monopolistically competitive final goods sector. Final goods firms utilise both domestic and foreign intermediate goods in production. Nominal rigidities are introduced by assuming that firms set prices for a period t in period

Household Preferences

The representative household in each country consumes a final consumption basket comprising final goods from both countries. For the domestic household:

Here

The resulting demand functions and price indices are derived from expenditure minimisation.

The domestic household allocates consumption between domestic and foreign goods varieties. The optimal demands for each variety are given by:

These lead to the consumer price index:

Within each variety, the household chooses among differentiated goods. The optimal demand for good j is:

The corresponding price indices are the price indices and :

Money is introduced via a cash-in-advance constraint:

The household's intertemporal program is formulated in the Bellman equation form:

In each period, the household has income from labour

The first-order conditions are as follows:

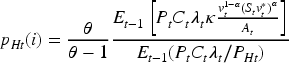

With complete markets, we obtain the international risk-sharing condition:

The central bank increases the money supply through direct transfers to households. The government's budget constraint in each country is:

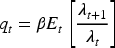

Following Devereux and Engel (2001), we assume the money supply follows a random walk process:

With complete markets, logarithmic preferences, and the random walk assumption, the equilibrium exchange rate is:

This is a deliberately stylised setup—the nominal exchange rate tracks relative money supplies exactly, with no overshooting. The payoff is a clean reading of how exchange rate movements feed into firms’ pricing, and the algebra stays manageable. Technical details are provided in Appendix B.2.

Perfectly competitive firms produce homogeneous intermediate goods using labour:

Here

The law of one price holds for intermediate goods. Profit maximisation yields:

Monopolistically competitive firms produce differentiated final goods using domestic and foreign intermediates:

Cost minimisation yields the unit cost function:

Firms in the final goods sector sell output to consumers in both countries. The firm's production,

Taking the stochastic discount factor

For the export market, the firm chooses between producer currency pricing (PCP) and local currency pricing (LCP) to maximise expected discounted profits

If firm i chooses PCP strategy (pricing in producer's currency), it chooses the price

If firm i prefers LCP strategy (pricing in local currency), it sets the selling price directly in foreign currency

We analyse the scenario where all domestic firms coordinate on the same invoicing strategy. Consider a domestic firm i in isolation. We use the domestic household's marginal utility

If all domestic firms adopt PCP, firm i sets price

In symmetric equilibrium,

The optimal price applies a constant markup to expected marginal cost, weighted by foreign wealth indicators. The coefficient

Symmetric LCP Equilibrium:

Under symmetric LCP, the optimal foreign-currency price is:

In the symmetric equilibrium, where domestic firms choose to price their goods in the buyer's currency, the pricing strategy becomes

The maximum expected profit is therefore:

Equations (58) and (61) deliver an indifference result that should be read with care. The two expected profits match not because the invoicing currency does not matter, but because a lone deviating firm, in a symmetric equilibrium, is too small to shift aggregate price indices. With every other firm pricing in one currency, that currency alone composes the aggregate index. Since P = SP* in the symmetric PCP equilibrium, a firm that moves to LCP faces a price-index comparison it would not face outside symmetry. Indifference is thus a knife-edge property of complete coordination—not a sign that the currency choice is inconsequential. The interesting case is its collapse: contemplate a unilateral deviation and the deviation-incentive conditions of Propositions 3 and 4 emerge, and it is these that determine equilibrium stability.

It is the unilateral deviation that destroys the indifference. An equilibrium holds only if no firm gains by abandoning the strategy the others have settled on.

If all other firms use PCP, we examine whether firm i profits by switching to LCP. The deviating firm's profit is:

The optimal deviation price satisfies:

The expected profit is:

The condition follows from comparing

If all other firms use LCP, the deviating firm's profit is:

The optimal price satisfies:

With all variables log-normal, logging the inequality reduces it to the trade-off underlying Proposition 4. What drives that trade-off is the variance of the nominal exchange rate and its covariance with factor prices

The foreign firms are handled by the same apparatus. With the two countries assumed perfectly symmetric,

A symmetric LCP equilibrium (pricing in domestic currency) is stable if:

A symmetric PCP equilibrium (pricing in foreign currency) is stable if:

The conditions for foreign firms mirror those for domestic firms once the currency roles are flipped: pricing in domestic currency (LCP for a foreign firm) lines up with PCP seen from home, and conversely. The underlying logic is unchanged—the trade-off rests on the variance of the exchange rate and its covariances with factor prices, weighted by the import share α. What differs is the productivity term

The conditions derived in Propositions 3, 4, and 5 form the core of our general equilibrium analysis. They provide a unified arbitrage condition that determines the optimal invoicing strategy by balancing firm-level cost exposure against macroeconomic volatility. Comparing the deviation incentives in Propositions 3 and 4, we can identify the conditions for a stable Nash equilibrium in which all domestic firms coordinate on the same strategy. Proposition 6 states these conditions.

Note that these conditions are complementary: when one holds, the other does not, ensuring a unique symmetric equilibrium. The direction of the inequality depends on whether exchange rate variance or cost-revenue covariation dominates the firm's risk exposure.

This arbitrage condition is the central theoretical contribution of our general equilibrium model. It nests the partial equilibrium result from Proposition 2 as a special case. Specifically, if we assume that only the exchange rate varies (i.e., isolating the partial equilibrium effect by setting

General equilibrium opens a second channel, though, running through uncertainty in factor prices and productivity. Its covariances with the exchange rate reshape the plain threshold rule. A positive covariance between the exchange rate and factor prices

In that condition, the import share α serves as a weight, splitting the influence of foreign against domestic cost shocks. The invoicing choice is not down to any one factor. Three combine to produce it: the firm's cost structure (α), the variance of the exchange rate (Var(st)), and the way the exchange rate moves with economic fundamentals (Cov(st, ·)).

At the center of the general-equilibrium analysis is Proposition 6's arbitrage condition, valid for any joint distribution of exchange rate, factor prices, and productivity, and for any α. Propositions 7 and 8 are what is left after three additional restrictions: (A1) log utility in consumption, which links the stochastic discount factor to money supplies; (A2) random-walk money supplies, under which relative monetary variances alone drive the exchange rate; and (A3) monetary and productivity shocks that are independent, zeroing out every covariance term. Together, these three reduce the general condition to a contest between monetary variances—reproducing the monetary-stability finding of Devereux and Engel (2001).

Getting closed-form solutions requires imposing some structure—particular functional forms plus a handful of independence assumptions. Remaining within the complete-markets setup, we have money supplies follow random walks:

For the baseline calibrations, we treat monetary and productivity shocks as uncorrelated. This is grounded in evidence: monetary policy and technology shocks seldom move together.

Under complete markets and log-normality, the international risk-sharing condition implies:

However, when monetary shocks dominate and are independent of productivity shocks, the covariance terms vanish because:

The exchange rate Factor prices By independence,

Combining this with the factor price equations derived from optimisation:

With independence imposed, the cumbersome covariance terms in Propositions 5–6 vanish, leaving only the monetary-uncertainty variance terms.

Fix prices in the buyer's currency (LCP) if and only if Fix prices in their own currency (PCP) if and only if

When monetary shocks are independent of productivity shocks and dominate exchange rate movements, the covariance terms in Propositions 3–6 become negligible. The condition simplifies to depend only on relative monetary variances because

If If

Proposition 8 is a limiting case of Proposition 6. Three conditions are jointly necessary: complete financial markets, monetary shocks independent of productivity shocks, and random-walk money supplies. Relaxing any one of the three breaks the simple monetary-variance ranking. What is new relative to Devereux and Engel (DE) (2001) is the general condition (Proposition 6) from which their result is derived, the identification of import intensity α as the structural weight governing the relative importance of the cost and monetary channels, and the formal characterisation of market completeness as the switching condition between the two regimes (Proposition 9, Section 4.5).

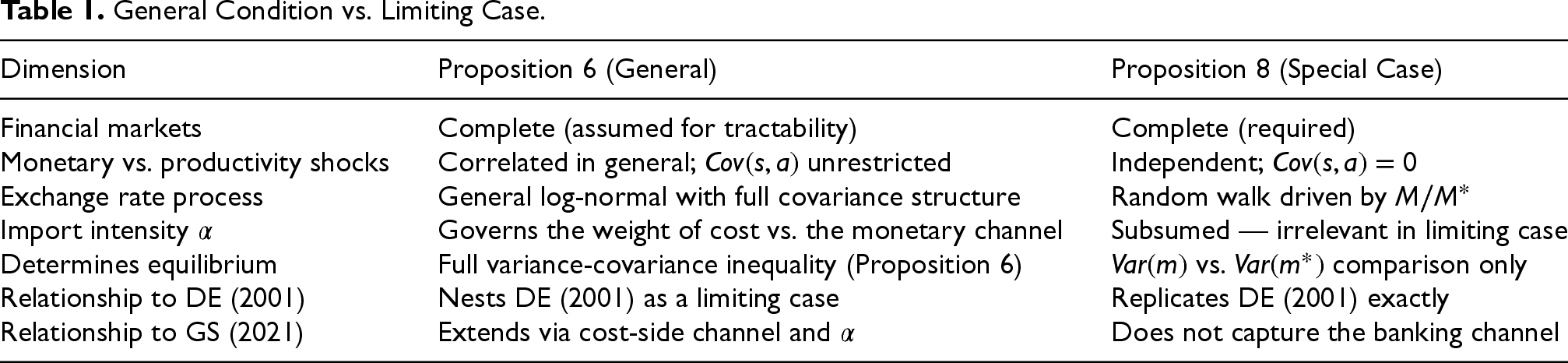

As established in Section 1, our supply-side cost-channel mechanism is complementary to the demand-side banking view of Gopinath and Stein (GS) (2021). When markets are complete, this exposure is fully hedgeable, and monetary stability dominates. When markets are incomplete, the exposure becomes a genuine unhedgeable risk, and the firm's production architecture determines the invoicing equilibrium. A unified framework incorporating both channels remains a productive avenue for future work. Table 1 contrasts the general arbitrage condition of Proposition 6 with the monetary-stability limiting case of Proposition 8.

General Condition vs. Limiting Case.

This result, however, rests on the assumption of complete financial markets. Handy though that is, it presumes firms—or the households behind them—can hedge away the entirety of their exchange rate risk with state-contingent contracts. Markets do not actually work that way. They are incomplete, and the instruments a firm would need are frequently costly or unavailable, all the more so for the idiosyncratic risk it carries at its own level.

Incompleteness changes everything about the calculus, because a firm can no longer hedge at will through financial instruments. Now the covariance terms in the general arbitrage condition (Proposition 6) matter in earnest: they capture risks that resist hedging and have to be managed by operational means, the currency choice among them. The cost-shock exposure a firm picks up through imported inputs—summarised by α and the covariances—cannot be offset in the market any longer. With that, the microeconomic hedging motive returns to the foreground.

At this point, Propositions 7 and 8, built on complete markets, may no longer hold. Invoicing turns instead on the firm's own cost structure (α) and on the comovement of exchange rates with its input costs—exactly what the partial-equilibrium analysis (Proposition 2) and the general condition of Proposition 6 point to. Our model thus provides a clear theoretical bridge: the dominance of macroeconomic (monetary) factors over microeconomic (cost-structure) factors in invoicing decisions is not universal but conditional on the degree of financial market completeness. This conditional result motivates the formal analysis of incomplete markets that follows in the next Section.

The preceding results depend on the complete-markets assumption, under which households perfectly insure against all idiosyncratic risks through state-contingent financial contracts. This section relaxes that assumption by introducing a bond economy in which only a single non-contingent nominal bond B is traded internationally. This is the simplest form of market incompleteness and the most widely used tractable alternative in the open-economy literature (Betts & Devereux, 2000; Corsetti & Pesenti, 2001).

Structure of the Bond Economy

The household's budget constraint is modified to exclude state-contingent claims:

Under the bond economy, the general arbitrage condition of Proposition 6 continues to hold: LCP is stable iff:

When When

As financial markets approach completeness and risk-sharing improves, Proposition 8's macro-stability result re-emerges as a limiting case—which confirms what it is: a feature of the complete-markets special case, not a general law.

See Appendix C.

The paper's central claim is set out in Proposition 9, and the claim is conditional rather than flat. Financial-market completeness is what determines the outcome. When markets near completeness (ϕ→0), monetary stability (Proposition 8) again dominates; when incompleteness is real (ϕ>0), the full general arbitrage condition of Proposition 6 governs—covariance terms included, terms a monetary-variance comparison cannot make disappear. Under complete markets, state-contingent contracts all but neutralise the cost-side hedging motive, and aggregate monetary stability holds sway. Under incomplete markets, the cost-side exposure measured by α becomes genuinely unhedgeable, and the firm's production architecture—its place in global value chains—takes the lead in the invoicing decision.

Empirical Implications and Research Design

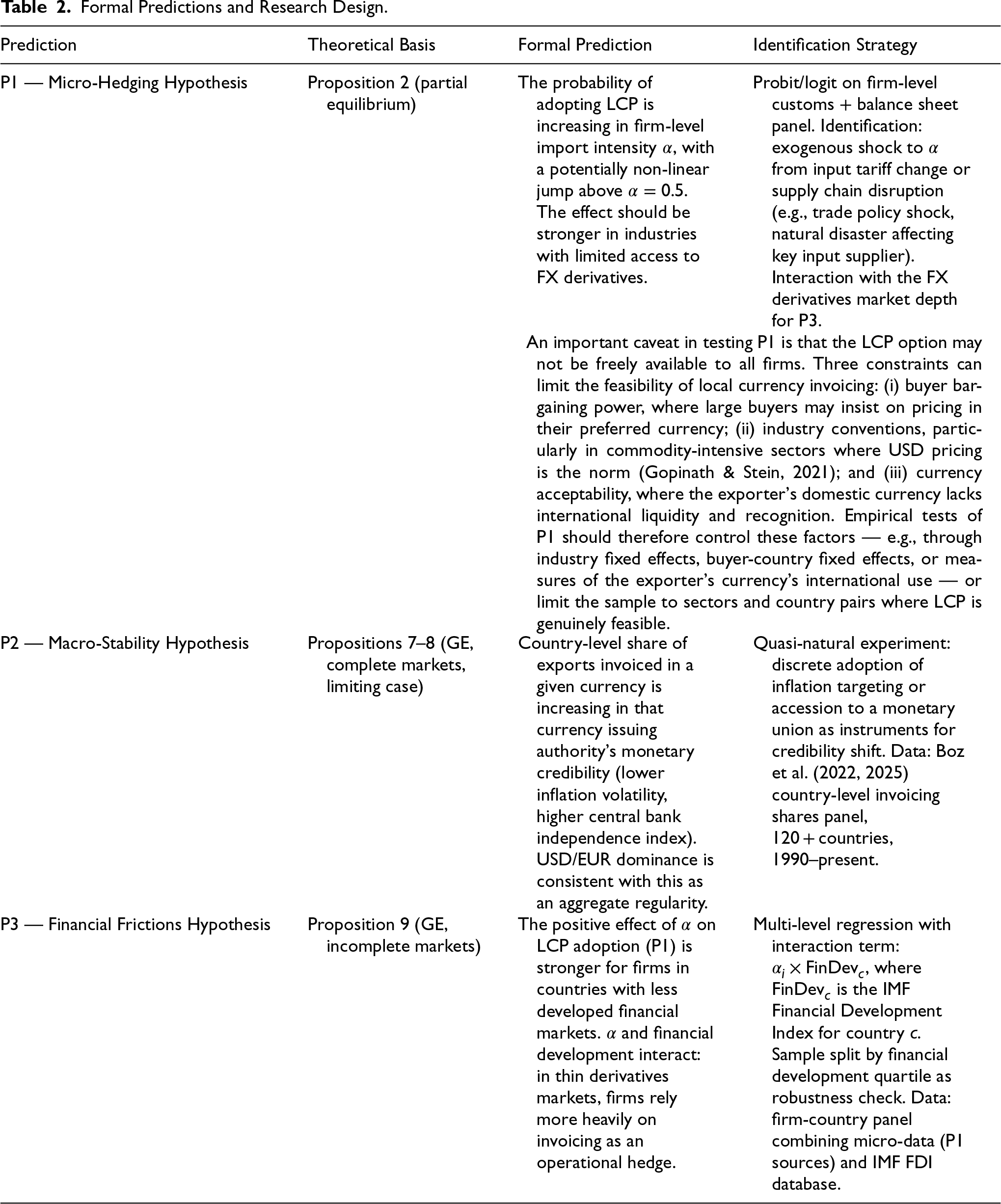

Three falsifiable predictions follow from the framework, each linking observable variables—at the firm and the country level—to invoicing behaviour. For each, we set out the prediction, identify the theory behind it, and propose an identification strategy that the available data could support. Table 2 summaries.

Formal Predictions and Research Design.

Formal Predictions and Research Design.

This paper began with a puzzle: why do firms invoice in local currency if doing so leaves them holding exchange rate risk? The dynamic model developed here, spanning partial and general equilibrium, identifies the answer as operational risk management—a choice molded by the relationship of cost structures, monetary conditions, and the architecture of financial markets.

Three findings stand out. In partial equilibrium, a firm heavily dependent on imported inputs (α > 0.5) is best served by invoicing in the buyer's currency, which hedges the cost-side exchange rate shocks it would otherwise bear (Proposition 2). In general equilibrium under complete markets, firms coordinate on the currency of the country with the steadier monetary policy (Proposition 8), a case that the broader arbitrage condition of Proposition 6 contains, with Devereux and Engel (2001) as a special instance. Make markets incomplete—a bond economy, in our formalization—and the cost-hedging channel takes over irrespective of the monetary-stability ranking (Proposition 9). Financial-market completeness is what arbitrates: when markets are complete, aggregate-stability considerations dominate; when they are incomplete, firm-level cost structures regain primacy.

These results matter in practice. For a risk manager, the worth of LCP as a cost-side hedge hinges on which alternatives—FX derivatives, balance-sheet matching, or sourcing adjustments—are available and at what cost. With deep derivatives markets, Proposition 8's monetary-stability logic is the more useful guide; with shallow ones, LCP supplies an operational hedge that financial instruments cannot match, and the cost-structure logic of Propositions 2 and 9 takes precedence. For a policymaker, monetary credibility raises a currency's appeal for trade invoicing, while financial-development measures that reduce incompleteness reshape the risk-sharing problem firms confront.

Several extensions merit attention. On the theoretical side, integrating the cost channel identified here with the intermediation channel of Gopinath and Stein (2021) would generate a unified framework in which both the demand-side and supply-side dimensions of financial incompleteness jointly determine the invoicing equilibrium. At the firm level, introducing switching costs, contractual inertia, and buyer bargaining power would replace the sharp threshold of Proposition 2 with a zone of indifference whose width reflects the magnitude of these frictions relative to the hedging benefit. Empirically, the model's three predictions can be tested using firm-level data on input sourcing and invoicing choices, with the identification strategies outlined in Section 5. Other productive directions include strategic interactions between central banks when invoicing is endogenous and the influence of geopolitical shifts on the choice of vehicle currencies.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.