Abstract

The paper studies fraud conceptualization at different levels that motivate criminal behavior. Accounting fraud literature is analyzed using the grounded theory approach to find new themes and inconsistencies concerning fraud conceptualization. According to our analysis, fraud conceptualization in literature is divided into two-tier levels; micro and macro, which include individual and environmental factors. These factors are derived from five well-known fraud conceptualization papers in accounting literature. These five journal articles were analyzed, and factors were generated using an open and axial coding methodology. According to the coding mechanism of grounded theory, literature fails to include the gap between the individual fraud offender and the institutional governance and departmental control mechanisms, which are considered meso variables in our study. Hence, based on the review of a well-carved-out piece of literature on accounting, a meso-tier level that incorporates departmental factors is derived that integrates the micro and macro factors into a three-tiered model. The theoretical model is then applied to the Carillion fraud case to comprehend and legitimize the meso-level theory.

Introduction

Fraud research has long been shaped by disciplinary silos. While criminology has historically paid limited attention to fraud, accounting scholarship has come to dominate the field, often framing fraud as behaviour that moves directly from individual misconduct to institutional failure (Cooper et al., 2013; Lokanan, 2018; Morales et al., 2014). Such framing has privileged micro-level explanations focused on individual intent and macro-level analyses centered on governance, regulation, and control systems, while largely overlooking the organizational and departmental dynamics that connect these levels. Consequently, meso-level factors—those operating within groups, departments, and organizational subunits-remain under-theorized in critical accounting fraud research (Fine, 2012).

Across disciplines, fraud is generally understood as intentional deception resulting in financial or economic harm. Accounting research conceptualizes fraud primarily in terms of financial misrepresentation and control failures, emphasizing prevention, detection, and compliance within financial reporting, auditing, and forensic contexts (Cooper et al., 2013; Jones, 2011; Lokanan, 2015; Power, 2013). In contrast, criminology and sociology examine fraud as a form of white-collar crime shaped by social, psychological, and environmental conditions, focusing on motivation, opportunity, rationalization, and broader social consequences (Becker, 1968; Cressey, 1953; Piquero, 2018; Sykes & Matza, 1957; Tillman, 2009).

Despite shared recognition of fraud as an intentional act involving deception, integration across these perspectives remains limited. Accounting research has tended to prioritize financial and institutional outcomes, whereas criminological approaches emphasize individual and social dimensions (Cooper et al., 2013; Lokanan & Sharma, 2023; Power, 2013). Such bifurcation has contributed to analytical gaps, particularly in explaining how fraudulent behavior is enacted and sustained within organizational settings. Sociological theory distinguishes among micro-level interactions, macro-level structures, and meso-level group dynamics (Fine, 2012; Lokanan et al., 2018; Morales et al., 2014), yet critical accounting studies have largely confined their analyses to the micro–macro continuum (Cooper et al., 2013; Dellaportas, 2013; Lokanan, 2018; Lokanan & Aujla, 2021; Power, 2013).

Neglect of the meso-level analysis obscures the organizational mechanisms through which fraud becomes normalized, coordinated, and sustained. Group-level dynamics—such as departmental pressures, shared rationalizations, internal alliances, and professional identities—can mediate the relationship between individual intentions and institutional structures (Fine, 2012; Lokanan, 2018). Absence of explicit attention to these dynamics’ risks overlooking the contextual conditions that give rise to systemic misconduct. A more comprehensive understanding of fraud, therefore, requires focused examination of meso-level processes that link individual behavior to organizational and institutional outcomes.

The primary objective of this study is to develop a meso-level conceptualization of fraud that bridges micro-level individual behavior and macro-level institutional forces. Specifically, the paper seeks to theorize how collective processes operate within organizational subunits, such as departments, teams, and professional groupings, mediate the relationship between individual intentions and structural conditions. By foregrounding meso-level mechanisms, the study advances fraud research beyond individualistic or purely structural explanations and offers a more integrated, process-oriented account of how fraud emerges within complex organizations.

To achieve this objective, the study adopts a qualitative, theory-building research design informed by grounded theory principles. Rather than employing grounded theory in its classical form as an inductive method derived from a large primary empirical dataset, the study uses grounded theory as a sensitizing analytical framework to identify conceptual gaps, generate categories, and develop theoretical relationships. The research design unfolds in two interrelated phases. The first phase involves systematic coding and analysis of five highly influential papers on accounting fraud studies to examine how fraud has been conceptualized at the micro and macro levels and to identify the absence of a clearly articulated meso-level framework. The phase functions as a structured theoretical foundation rather than an exhaustive literature review.

In the second phase, the study applies the emergent meso-level constructs to an in-depth case analysis of the Carillion collapse. Drawing on parliamentary inquiry transcripts and official documentary evidence, the case study is used to examine how meso-level mechanisms—such as groupthink, collusive behavior, social capital, and group identity—operate in practice to connect individual actions with institutional failures. The case is not treated as a source of statistical generalization but as an analytical setting through which the explanatory value and coherence of the proposed meso-level framework can be demonstrated.

The two-phase design enables progression from conceptual gap identification to theoretical development and empirical illustration in a logically sequenced manner. The contribution of the study lies not in the introduction of new detection techniques or the reapplication of established fraud models, but in the development and operationalization of a meso-level framework that integrates behavioral and structural dimensions of fraud. Such an approach responds directly to longstanding calls within critical accounting and criminological scholarship for more multilevel, organization-sensitive explanations of fraudulent behavior (Lokanan & Sharma, 2023; Morales et al., 2014).

The remainder of the paper is structured as follows. The analysis begins with the first methodological phase, which employs a grounded theory–informed approach to identify gaps in the literature through analysis of five well-known accounting fraud studies. The discussion then turns to a literature review of micro- and macro-level analyses of fraud, drawing on factors derived from the initial coding process. Subsequently, the second phase of the research methodology is presented, employing the grounded theory approach to identify emerging patterns and developing a theory for the meso-level analysis of fraudulent behavior. Grounded theory, originally introduced over five decades ago, remains a methodological approach that many researchers find challenging to operationalize effectively (Makri & Neely, 2021). To apply the grounded theory methodology, a case study approach is employed based on the suggestions of Makri and Neely (2021) to analyze the meso-level theory in the context of fraud research. The Carillion fraud case is utilized as a case study for the application and analysis stage of the theory. The final section of the paper highlights potential areas for future research and discusses the limitations of the study.

Methodology – Phase 1

Grounded Theory, introduced by Glaser & Strauss in 1967, is a systematic and iterative process involving data collection and code generation, which aims to identify relationships within the data (Makri & Neely, 2021). The paper follows the research strategies of Luca et al. (2022) and Wolfswinkel et al. (2013) by applying grounded theory to influential scholarship focused on understanding the conceptualization of fraud. The primary objective of this approach is to gather information and develop a theoretical model regarding the phenomenon being studied (Charmaz, 2014; Corbin & Strauss, 2015; Geiger & Turley, 2003; Makri & Neely, 2021; Mills et al., 2006; Ralph et al., 2015). The grounded theory approach is frequently employed to explore the complexities and nuances of observed phenomena through initial coding stages and the exploration of relational dimensions. By utilizing this approach, the iterative process of data collection and analysis continues until any identified gaps in the dataset are addressed, leading to a comprehensive understanding of the phenomenon under investigation (Charmaz, 2014; Corbin & Strauss, 2015; Makri & Neely, 2021; Mills et al., 2006; Ralph et al., 2015). Through the creation of connections between codes, the grounded theory approach ensures that data collection and coding are guided by a theoretical contribution rooted in the data itself (Charmaz, 2014; Corbin & Strauss, 2015; Mills et al., 2006; Ralph et al., 2015). In this study, the grounded theory approach was used to collect data related to various theoretical propositions employed in elucidating fraud within critical accounting research, with the primary objective of identifying gaps in the existing literature. By employing grounded theory, this study facilitated the systematic collection and analysis of data, enabling the identification of gaps in the current literature on fraud in critical accounting research. The approach ensured that the analysis was grounded in the collected data rather than predetermined notions or assumptions, thereby enhancing the credibility of the findings.

The study adopts a constructivist grounded theory approach (Charmaz, 2014; Mills et al., 2006; Ralph et al., 2015), emphasizing the co-construction of meaning between researcher and data rather than the discovery of an objective reality, as in classical grounded theory (Glaser & Strauss, 1967). The constructivist stance is appropriate given the interpretive nature of fraud research and the goal of theorizing about underexplored meso-level mechanisms. The process followed the systematic grounded theory principles of theoretical sampling, memo writing, constant comparison, and saturation (Corbin & Strauss, 2015). Although the data corpus consisted of secondary literature, theoretical sampling was applied iteratively, where emerging categories from the initial coding guided the inclusion of complementary works that elaborated or challenged preliminary themes. Memo writing was used throughout all stages to document analytical reflections, track the evolution of core categories, and link emerging patterns between micro- and macro-level dimensions. Saturation was reached when additional coding produced no new theoretical insights or relationships among categories, after repeated comparison across the five papers and supplementary literature. Coding was performed by the lead researcher and reflexivity was maintained through analytical memos that documented the researcher’s positionality as both an academic and practitioner in the accounting field, acknowledging how this background informed interpretive decisions. The expanded methodological account underscores the systematic rigor and transparency of the grounded theory process, reinforcing its value in developing a meso-level perspective of fraud that bridges behavioral and structural dynamics.

Data Collection

Data Source 1: Documentary Evidence and Case Data Collection

The first sources of data came from evidence heard during the parliamentary inquiries into the collapse of Carillion plc. Carillion was a major British multinational construction and facilities management company that entered compulsory liquidation in January 2018 following years of financial mismanagement, aggressive accounting practices, and mounting debt. The collapse resulted in the loss of thousands of jobs, the termination of public sector contracts, and significant financial harm to pensioners and suppliers. Parliamentary investigations conducted by the Work and Pensions Committee and the Business, Energy & Industrial Strategy Committee examined the causes of the company’s downfall, focusing on failures in corporate governance, auditing oversight, and executive accountability. These inquiries produced extensive written and oral evidence, including testimonies from Carillion’s directors, auditors, regulators, and other key stakeholders, offering critical insights into the institutional and departmental factors that enabled systemic misconduct.

Primary Documentary Sources Used for the Carillion Case Analysis

All documents were retrieved directly from the official UK Parliament website to ensure authenticity and traceability. These materials provided first-hand accounts of regulatory oversight, corporate governance, and auditor conduct related to Carillion’s collapse. Each source was coded thematically using the meso-level categories identified in the grounded theory analysis, groupthink, collusion, social capital, and group identity, to capture the organizational and departmental dynamics underlying the fraud. The use of parliamentary proceedings as the primary data ensured that the analysis was anchored in verifiable institutional evidence and reflected multiple stakeholder perspectives, including those of policymakers, regulators, company directors, and auditors.

Phase 1 – Scholarly Corpus (Micro–macro Coding)

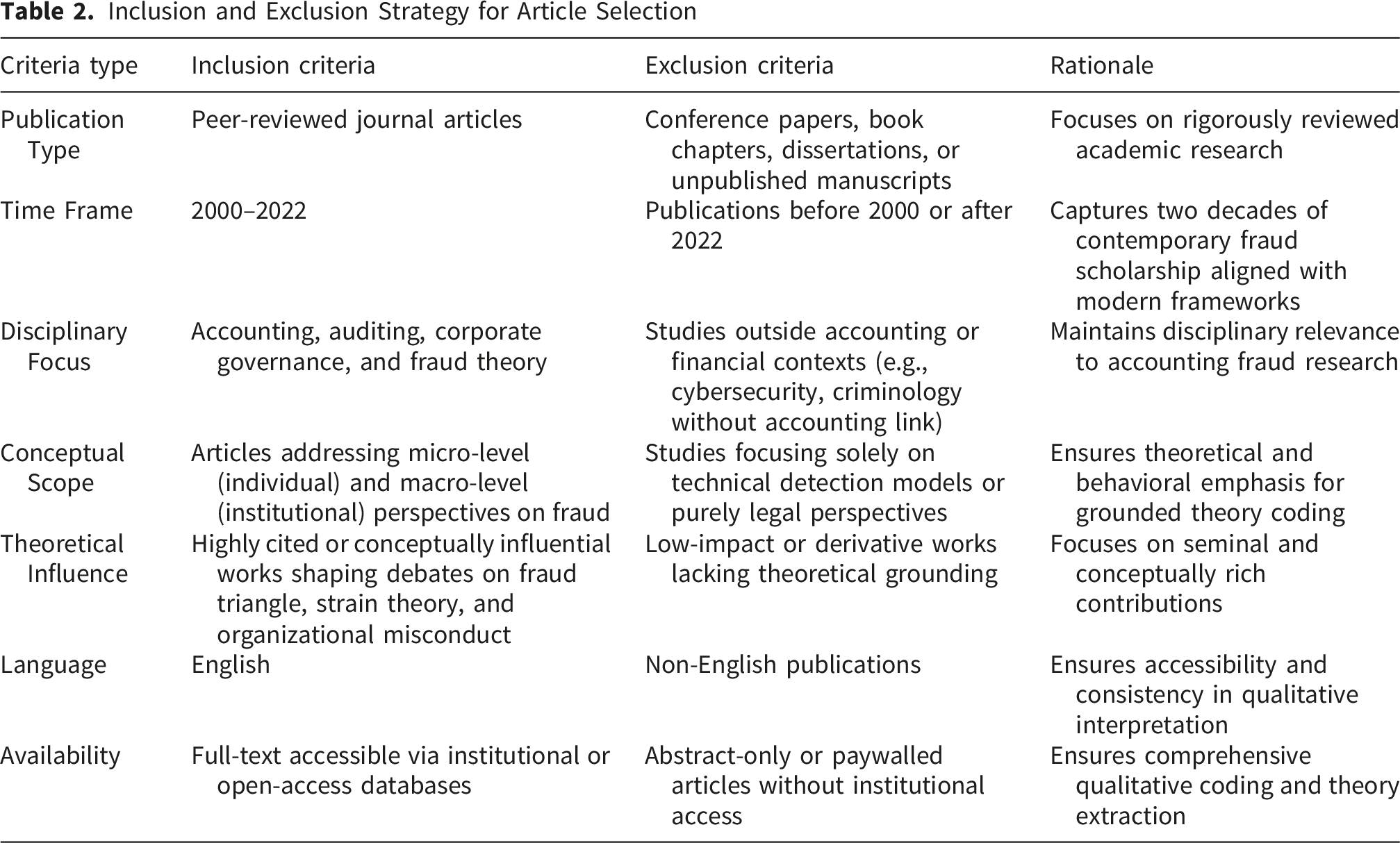

Inclusion and Exclusion Strategy for Article Selection

The selection of the five articles as the Phase 1 corpus requires epistemological justification, particularly given critiques of small-sample grounded theory applications. From a constructivist grounded theory epistemology, the purpose of Phase 1 was not inductive theory generation from a large empirical corpus, but conceptual gap identification through intensive engagement with field-defining texts. The approach aligns with theoretical sampling principles that prioritize conceptual depth over numerical breadth (Corbin & Strauss, 2015; Glaser & Strauss, 1967). In constructivist grounded theory, saturation is achieved not through exhaustive data collection but through theoretical sufficiency, the point at which additional data no longer generate new analytical categories or modify relationships among existing categories (Charmaz, 2014; Corbin & Strauss, 2015). Several methodological traditions support intensive analysis of small, purposively selected corpora. Eisenhardt (1989) demonstrated that theory building from cases often relies on 4-10 carefully chosen papers to develop robust theoretical frameworks. Similarly, in systematic literature reviews using grounded theory, Wolfswinkel et al. (2013) advocate for “deep reading” of foundational texts over broad, shallow coverage when the objective is theoretical refinement rather than empirical generalization. The rationale is that seminal works contain densely layered theoretical propositions that reveal more through iterative, multi-level coding than through aggregation across numerous sources (Locke, 2001).

In the present study, theoretical saturation was achieved through three mechanisms. First, the five selected papers represent paradigmatic positions in accounting fraud scholarship, where each paper introduced or substantially critiqued dominant frameworks (the Fraud Triangle, governance perspectives, and risk-based approaches), ensuring conceptual coverage of major theoretical propositions. Second, coding proceeded iteratively: initial open coding of Cooper et al. (2013) generated 47 preliminary codes; axial coding across all five papers consolidated these into 8 core categories (4 micro-level, 4 macro-level); selective coding revealed no new dimensions after the fourth paper, with the fifth serving as theoretical validation. Third, constant comparison revealed that the five papers repeatedly invoked the same conceptual boundaries, individual versus institutional, without articulating intermediate mechanisms, thereby confirming the absence (rather than presence) of meso-level theorization.

The approach mirrors the methodological strategy employed by seminal grounded theory studies in management and accounting. For instance, Gioia et al. (2013) developed their widely cited methodology by intensively analyzing a small number of foundational qualitative studies to extract meta-theoretical insights. Similarly, Suddaby (2006) demonstrated that theoretical contributions often emerge from deep engagement with conceptually rich texts rather than the breadth of sampling. The present study’s contribution lies not in a comprehensive mapping of all fraud literature but in identifying a systematic theoretical gap, the missing meso level, through critical interrogation of field-defining works. To further validate this approach, supplementary literature (n=23 articles) was consulted during axial and selective coding to elaborate theoretical relationships and ensure the identified gap was not an artifact of the initial sample. However, these supplementary sources did not alter the core categorical structure, confirming that the five papers provided an adequate theoretical foundation for gap identification.

Epistemological Justification for Text Selection

The deliberate limitation to five established and authoritative papers reflects a methodological choice grounded in the distinction between empirical saturation and theoretical saturation (Charmaz, 2014; Corbin & Strauss, 2015). Empirical saturation, common in traditional grounded theory, requires data collection until no new empirical instances emerge. Theoretical saturation, appropriate for literature-based grounded theory, requires sampling until conceptual categories stabilize and relationships among categories become theoretically coherent (Glaser & Strauss, 1967; Thornberg & Charmaz, 2014). The five selected papers were not chosen as a random or convenience sample but as paradigm-defining texts that established, challenged, or extended the dominant theoretical frameworks in accounting fraud research over the past two decades (Kuhn, 1970). Each paper represents a distinct theoretical position: 1. Fraud Triangle lineage (Cooper et al., 2013): Micro-level psychological rationalization 2. Institutional governance critique (Power, 2013): Macro-level regulatory apparatus 3. Moral framing (Morales et al., 2014): Ethical dimensions bridging individual and structure 4. Criminological Integration (Lokanan, 2015, 2018): Attempt to Synthesize Micro-Macro Perspectives

These works collectively define the boundaries of fraud conceptualization in accounting scholarship. Their influence is evidenced by: (1) cumulative citations; (2) adoption in professional auditing standards (PCAOB, 2020); (3) pedagogical dominance in forensic accounting curricula (ACFE, 2022). Methodologically, the study employs what Locke (2001) terms “sensitizing concepts” derived from the five sample texts to guide theoretical development rather than empirical description. The approach has precedents in accounting research: Burchell and his supporting authors’ (1980) influential critique of accounting’s sociological imagination was developed through intensive analysis of five foundational texts, not a comprehensive review. Similarly, Burchell et al. (1980) developed the “accounting in its organizational context” framework by deeply engaging with a small corpus of paradigmatic works. The adequacy of the five-paper corpus for theoretical gap identification was validated through two additional checks. First, a “negative case” search was conducted across 38 additional papers published in top-tier accounting journals (2010-2023) using keywords: “fraud,” “meso-level,” “departmental,” and “group dynamics.” None offered substantive meso-level theorization, confirming the gap’s pervasiveness. Second, the identified micro-macro binary was triangulated against textbook treatments of fraud (e.g., Albrecht et al., 2019; Lokanan, 2018; Power, 2013), which similarly operate within individual-institutional frameworks without meso-level articulation. Critics may argue that five papers cannot represent the entirety of fraud scholarship. The criticism misunderstands the study’s objective: not to comprehensively map the field but to demonstrate that even its most influential and widely adopted frameworks systematically omit meso-level mechanisms. The absence of meso-level theorization in paradigm-defining works is theoretically significant precisely because these texts’ structure how subsequent scholarship conceptualizes fraud (Kuhn, 1970; Suddaby, 2006).

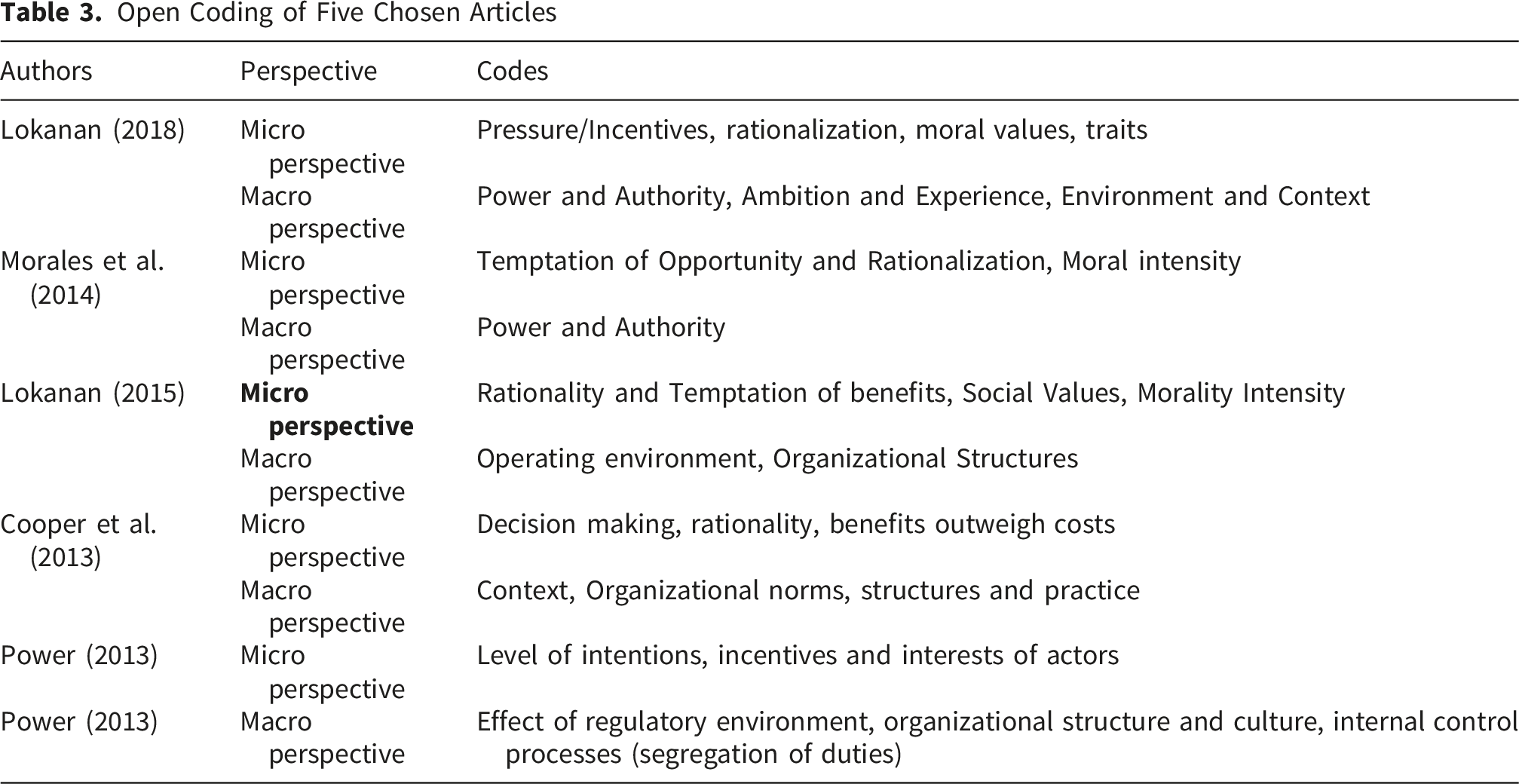

Open Coding of Five Chosen Articles

These five articles underwent the initial open coding process, approaching each paragraph with an entirely open mindset as specified in the grounded theory approach. As depicted in Table 1, during the open coding process, broad categories and codes were developed based on similarities and differences among the paragraphs of the articles. The coding process was facilitated using MAXQDA software. MAXQDA is a computer software program designed to assist researchers in qualitative data analysis. It offers various features that simplify the coding process and can be used for a wide range of research methods, including grounded theory, content analysis, and ethnography. MAXQDA proved particularly useful in this study by organizing data, creating coding schemes for multiple data sources, and enabling the creation of hierarchical coding structures for analyzing data at different levels of abstraction. After creating broad codes for the information in each article using MAXQDA, relational dimensions and connections between the codes were established through axial coding (Corbin & Strauss, 2015). Additionally, we examined other relevant journal articles to gather further insights into the final axial codes and their relationships. This examination allowed us to identify gaps in the existing scholarship.

The study begins by examining a two-tier model of fraudulent activity that illustrates the nature of fraud occurrences. This two-tiered model emerged from the open and axial coding processes conducted on the five papers analyzed for this research. Initially, we position each tier within the context of the fraud literature and then explore the contributions of the five selected articles, along with other relevant literature, in relation to this model. Subsequently, the selective coding step was performed, which is a stage in the grounded theory approach to qualitative data analysis. Selective coding involves identifying and refining a core category that connects all other categories and subcategories derived from the open coding and axial coding processes (Corbin & Strauss, 2015). This step helps identify a core category that captures the essence of literature in a specific area of study. The researcher then examines the literature for gaps where the core category is inadequately addressed or explained (Corbin & Strauss, 2015). Through the selective coding process, we examined the codes and their relationships, identifying gaps in the literature to develop theories regarding the phenomenon under study. The research concludes by developing theories to address these gaps in existing literature. To fill the theoretical gap in the current scholarly literature, a three-tiered model is subsequently constructed.

Literature Review

Micro Level Tier

The micro-level understanding of fraud examines the moral weaknesses of individual offenders and the factors contributing to criminogenic behavior (Lokanan et al., 2018; Morales et al., 2014). This perspective helps us comprehend why individuals behave the way they do within organizational settings (Cooper et al., 2013; Dellaportas, 2013; Lokanan, 2018; Lokanan & Aujla, 2021; Morales et al., 2014; Power, 2013). The accounting literature frames fraud to shed light on the issue, aiming to understand motives while considering the socio-economic context. It portrays criminal behavior as an objective phenomenon, critiquing the micro-perspective in favor of a broader macro-perspective (Cooper et al., 2013). In the following section, we evaluate the themes derived from analyzing the literature on the micro-level occurrence of fraud. The axial coding process was used to build relational dimensions based on the five articles in Table 1. The themes identified as representative of the micro-level analysis of fraud, derived from the coding process, include rationality, temptation, social values, and moral intensity.

Rationality

The decision-making characteristics of fraudulent behavior can be complex. On one hand, the agent-principal relationship examines the interaction between the manager (agent) and the shareholder (principal). On the other hand, the cost-benefit analysis explores the motivations behind individuals’ engagement in fraud. Together, these two schools of thought elucidate how rationality and sources of temptation influence decisions to commit fraudulent activities. The agent-principal relationship is influenced by the agent’s pursuit of personal benefits when the relationship is weak, or by the agent’s commitment to fulfilling the needs and interests of the shareholders as stewards when the relationship is strong (Albrecht et al., 2015; Cooper et al., 2013; Power, 2013; Sundaramurthy & Lewis, 2003). According to Cressey (1953), individuals who engage in fraudulent activities tend to rationalize their behavior in a manner that maintains their personal integrity and a consistent ethical self-image in the eyes of others. Various individual attributes influence the decision to engage in wrongdoing, where the assumption of rationality and cognitive biases act as contributing factors (Cooper et al., 2013; Power, 2013).

The second influence on decision-making for perpetrators of crime is based on cost-benefit analysis. This means that individuals will evaluate the benefits of committing a particular offense against the potential costs associated with it. In analyzing this concept, both tangible and intangible elements are taken into account, where the monetary value is weighed against the risks involved in engaging in criminal behavior and the broader ethical implications (Becker, 1968). By examining such situations, insights can be gained into the motivations behind criminal behavior and the factors that influence decisions about whether to commit an offense (Morales et al., 2014). This idea is widely discussed in the literature on various forms of wrongdoing, including academic dishonesty, financial fraud, and deception. Prominent scholars such as Becker (1968), Greve et al. (2010), and Lokanan and Aujla (2021) have emphasized the significance of cost-benefit analysis in explaining criminal behavior. Individuals who engage in fraudulent activities often attempt to rationalize their behavior to justify misappropriation of resources and breaches of trust. As noted by Cooper et al. (2013), Lokanan and Aujla (2021), and Morales et al. (2014), criminals may perceive the negative consequences of their actions as manageable risks if they believe the potential benefits outweigh them. This mindset contributes to the erosion of moral consciousness, resulting in significant harm to society as people accept criminal activities as acceptable alternatives in certain situations (Lokanan, 2018).

Temptation

Temptation has been identified as a significant contributor to fraudulent behavior, primarily driven by the potential benefits or advantages that cheating or stealing could provide. Scholars Lokanan and Aujla (2021), Lokanan (2018), and Morales et al. (2014) agree that when faced with attractive incentives, individuals may feel more encouraged to engage in fraudulent behavior. Wikstrom and Treiber (2009) found that temptation was the primary influence motivating fraud. These findings suggest that individuals are more likely to commit fraud if the perceived reward is sufficiently high. Temptations can also weaken an individual’s social values and moral frameworks, leading them to choose criminogenic actions (Cooper et al., 2013; Lokanan, 2018).

The concept of the “temptation of the moment” has been identified as a driving force behind criminogenic behavior. This refers to an individual’s opportunity to engage in fraudulent activity when they perceive a gap in an organization’s internal control system (Morales et al., 2014; Power, 2013). Gottfredson and Hirschi (1990) and Wikstrom and Treiber (2009) have suggested that this perception of opportunity may enable individuals to cross legal boundaries and deviate from their stated responsibilities. Therefore, recognizing these opportunities for transactional crime is crucial for enforcing existing regulations and deterring future misconduct (Wikstrom & Treiber, 2009Wikström & Treiber, 2009, p. 239).

Recent research has shown that the potential for fraud can be a powerful motivator when individuals are willing to set aside their moral or social values for personal gain (Davis & Pesch, 2013; Lokanan, 2015, 2018). These motivations are not limited to financial greed; desirable emotions such as ego enhancement, pride, and authority can also drive individuals to engage in unfortunate criminal behavior (Davis & Pesch, 2013; Lokanan, 2018; Power, 2013). Furthermore, it has been hypothesized that certain personality traits may contribute to an individual’s susceptibility to temptation (Lokanan, 2015, 2018; Merluşcă & Chiracu, 2018; Morales et al., 2014; Roeser et al., 2016). More recent research suggests that some individuals may be more susceptible than others due to their psychological makeup developed during childhood upbringing (Roeser et al., 2016). For example, individuals with high levels of impulsivity and sensation-seeking tendencies may be more likely to succumb to temptations due to lower levels of self-control (Roeser et al., 2016). Additionally, situational factors such as time pressure, job dissatisfaction, and perceived unfairness can also increase the likelihood of individuals engaging in fraudulent behavior (De Clercq et al., 2021; de Schrijver, 2010; Ermongkonchai, 2010; Ocansey & Ganu, 2017). Finally, social and cultural factors, such as peer pressure, social norms, and cultural values, have been shown to influence individuals’ inclination to engage in unethical behavior (Ermasova, 2021; Ermongkonchai, 2010).

Social Values

Hirschi (1969) proposed that every individual possesses aggressive personality traits, but these traits do not necessarily lead to criminal behavior. Instead, an individual’s social values play a significant role in determining their inclination to engage in crime (Lokanan & Aujla, 2021). Social values are developed through socialization processes and the strength of an individual’s social ties (Lokanan & Aujla, 2021). Individuals with strong social bonds and values are less likely to engage in fraudulent behaviors, while those with weak social bonds and values are more likely to possess criminogenic traits that motivate them to engage in fraudulent behaviors (Cooper et al., 2013; Davis & Pesch, 2013; Lokanan, 2015, 2018; Lokanan & Aujla, 2021; Merluşcă & Chiracu, 2018). These claims are supported by research suggesting that adverse childhood experiences characterized by neglect, insensitivity, and lack of nurturing may increase an individual’s susceptibility to temptation and criminal behavior (Engdahl, 2015; Merluşcă & Chiracu, 2018). Furthermore, cheating is an iterative process of actions and decisions that develop over time, further highlighting the role of socialization and social values in shaping an individual’s behavior (Cooper et al., 2013).

Research on the relationship between social ties and criminal behavior suggests that not only the strength, but also the quality of social relationships can influence an individual’s propensity to engage in fraudulent behavior (van Onna & Denkers, 2019). For instance, previous research has shown that individuals who perceive their organization as unfair or unsupportive are more likely to engage in unethical behavior (De Clercq et al., 2021; de Schrijver, 2010; Ermongkonchai, 2010). Moreover, studies indicate that the presence of deviant peers can increase the likelihood of an individual engaging in criminal behavior (Brezina & Azimi, 2018; O'Donnell et al., 2012). Additionally, cultural factors such as individualism and collectivism in social ties have been highlighted for shaping an individual’s moral decisions and inclination to engage in fraudulent behavior (Ermasova, 2021).

Morality Intensity

The literature on fraud extensively examines the individual characteristics that contribute to an individual’s propensity to engage in fraudulent activities (Cooper et al., 2013; Morales et al., 2014). The degree of moral intensity in an individual’s moral intention and judgment determines the likelihood of engaging in fraudulent activities (Murphy, 2012). The absence or presence of morality plays a critical role in determining the likelihood of fraudulent events. People’s moral characteristics can influence their propensity to engage in criminal behavior. Offenders with weaker moral characteristics may find it easier to rationalize certain activities, regardless of the long-term consequences. These individuals are particularly susceptible to engaging in fraudulent behavior due to the immediate rewards associated with such activities (Lokanan & Aujla, 2021; Morales et al., 2014; Murphy & Dacin, 2011). As a result, these individuals may prioritize immediate gains over long-term consequences, which can lead to the perpetration of fraudulent acts (Kohlberg, 1969). Individuals who are aware of the potential long-term consequences of noncompliance with the law are less likely to engage in fraudulent activities due to their strong moral compass (Kohlberg, 1969; Lokanan & Aujla, 2021; Lord & DeZoort, 2001).

The role of cognitive processes in influencing an individual’s moral decision-making and susceptibility to fraudulent behavior has also been explored. According to the dual-process theory of moral decision-making, individuals can use two different cognitive processes, automatic and controlled, to make moral judgments (Greene et al., 2004). Automatic processes are fast and intuitive, whereas controlled processes are slower and more deliberate. Research has shown that when individuals rely more on automatic processes, they are more likely to engage in unethical behavior (Randolph-Seng & Nielsen, 2007). Additionally, the level of moral disengagement, which refers to an individual’s ability to rationalize or justify their unethical behavior, has also been found to influence the likelihood of engaging in fraudulent behavior (Bandura et al., 1996, 2001; Sykes & Matza, 1957).

Macro Level Tier

The individualistic view of fraud fails to consider the role of institutional and organizational factors in driving fraudulent activities. This one-dimensional analysis overlooks long-standing behaviors and dynamics that may be present in organizations and groups. The micro-level analysis ignores the influence that complex group structures and norms may have on criminality, as well as potential external motivational pressures such as financial goals, competitive conditions, or even greed (Cooper et al., 2013; Lokanan & Aujla, 2021; Morales et al., 2014; Power, 2013). An unbiased analysis makes it clear that a complete examination of fraudulent activities must include an analysis of the contexts that shaped the behavior in question. Without this insight, efforts to reduce such acts will not be effective without a deeper understanding of all contributing factors. Macro-level analysis assesses the broader structural forces that govern fraudulent behavior, including their environment and control systems.

Political and Legal Environment

Organizations are increasingly adopting internal processes that are influenced by external legal and regulatory pressures (Power, 2013). The regulatory environment plays a critical role in shaping an organization’s culture and structure. The proliferation of juridical thinking, processes, and structures has significant institutional implications for organizations (Sitkin & Bies, 1994, p. 21). Organizations respond to the external regulatory environment by implementing fraud risk management standards and creating proof trails for relevant due processes to manage and mitigate fraud risks (Power, 2013). However, the regulatory and legal environment may have weaknesses as they do not always produce relevant and actionable knowledge to prevent and detect misconduct (Lokanan, 2018; Power, 2013). The legislative structure can be a sociopolitical process that may deviate from what most people consider acceptable, making the regulatory environment an inadequate compromised regulatory apparatus (Becker, 1968; Lokanan, 2018; Morales et al., 2014; Power, 2013). Hence, accepted values that are influenced by judgment are more crucial than a robust legislative structure (Morales et al., 2014; Power, 2013). Deviance is not inherent in fraudulent behavior but rather the outcome of applying regulations and legislation to an “offender” (Becker, 1968).

Accounting research is increasingly shifting its focus from a deterrence logic centered on deviant individuals to a compliance logic centered on organizational structures and controls (Lokanan, 2015). Accounting research is evolving as scholars increasingly recognize the critical role of organizational structures and controls in regulating corporate behavior. This newfound emphasis on compliance logic marks a shift from the focus on deterring individuals associated with deterrence logic. These important changes can be seen in several areas, such as financial reporting regulation and fraud detection. In both cases, greater attention is being paid to examining organizations holistically and to designing policies and mechanisms to ensure robust corporate practices and oversight. Lokanan (2015) posits that traditional deterrence-based approaches to accounting regulation are becoming less effective, and there is a shift towards compliance-based approaches emphasizing strong internal controls and ethical behavior within organizations. This shift is driven by the need for more proactive measures to prevent financial misconduct and the recognition of the limitations of deterrence-based approaches. As research continues to uncover more effective ways to prevent misstatements, these compliance-focused approaches will likely continue to dominate the accounting discourse in the future.

Operating Environment

More recent research in the fraud scholarship has moved towards understanding a perpetrator’s interactions at the institutional level. Fraud is often attributed to the interplay between organizations and their socioeconomic surroundings (Power, 2013). Researchers have claimed that environmental design and interactions with these designs influence fraudulent activities (Lokanan & Aujla, 2021; Morales et al., 2014; Power, 2013). The characteristics of fraud occurrences change based on legislative and cultural shifts, as well as economic and political reassessments (Cooper et al., 2013). Moreover, an organization develops and embeds fraud risk prevention systems that must be compatible with the needs and expectations of an institution’s macro-level environment (Castel, 1991; Power, 2013).

The development of fraudulent behavior can be attributed to the conjunction of an individual’s moral deficiencies and the opportunities created by the organizational environment (Lokanan & Aujla, 2021). Lokanan (2018) suggests that the external environment in which an organization operates can influence an individual’s propensity to engage in financial crimes. These settings can lead to the development of individual propensities for such criminal conduct. The absence of alignment between an individual’s morality and the organizational environment is caused by the gap between criminogenic environments and the encompassing structures that shape people’s behavior in structural settings (Cooper et al., 2013; Lokanan, 2018; Power, 2013). Market reactions, capital market expectations, and marketing participant involvement are integral parts of determining these propensities (Cooper et al., 2013; Lokanan, 2018). Consequently, organizations must recognize these misalignments and ensure that their employees adhere to ethical and legal standards.

Internal Control Processes

Research on fraud and fraud risks claims that the use of operational controls is vital in mitigating fraudulent behavior within organizations because these controls serve as the primary factor of deviance (Morales et al., 2014; Power, 2013). Scholars have shifted their attention from individual traits of perpetrators to the impact of organizational control systems on fraudulent behavior (Power, 2013). The role of organizational sociology is fundamental in understanding fraudulent institutional misbehavior as a macro factor. The apparatus of fraud risks can be mitigated by adjusting the structure of a business and reprogramming procedures to strengthen control systems (Cooper et al., 2013; Lokanan, 2018; Power, 2013). Additionally, the failure of formal control systems to provide early warning signs of fraudulent behavior allows fraud perpetrators to engage in fraudulent activities (Cooper et al., 2013; Power, 2013). System complexity has been a key factor in many crises caused by fraudulent activities (Cooper et al., 2013; Lokanan, 2018; Palmer & Maher, 2006; Power, 2013). Albrecht et al. (2019) found that a weak internal control system can create an environment where fraud can occur more easily. Similarly, Donelson et al. (2016) concluded that companies with stronger internal control systems are less likely to experience fraud. Rezaee et al. (2018) suggest that an effective internal control system can deter fraudulent behavior, highlighting the importance of enhancing control systems to prevent circumvention through fraudulent activities.

Power

Cooper et al. (2013) suggest that individual offenders who engage in fraudulent activities prioritize short-term gains over long-term consequences. According to Cooper et al. (2013) and Morales et al. (2014), senior management in positions of power and authority are less concerned with the long-term or criminal consequences of their actions, as they hold the ability to influence the organization’s culture. This theory is supported by the LIBOR investigations where senior management fostered an environment of illegal behavior among employees (Lokanan, 2018; Murphy & Dacin, 2011). Furthermore, the ambition of senior management to attain more power and authority at the institutional and societal levels, as well as their expertise in identifying loopholes in an organization’s internal control systems, may amplify the criminogenic traits in the organizational culture (Lokanan, 2018). Piff et al. (2012) found that individuals with higher levels of power often display a greater sense of entitlement, which increases the likelihood of engaging in unethical behavior. Another study revealed that high-ranking individuals exhibit more fraudulent behavior than those in lower positions (Albrecht et al., 2015).

Another study by Conyon and He (2016) found that executives in high-power positions were more likely to engage in fraudulent behavior due to their increased sense of entitlement and reduced fear of punishment. Furthermore, a study by Jávor and Jancsics (2016) found that individuals in high-power positions are more likely to engage in dishonest behavior due to their increased sense of self-interest and reduced concern for others. Similarly, a study by Fleischmann et al. (2019) found that power can lead to both increased and decreased use of deontological and utilitarian reasoning, depending on whether individuals are using their power to serve others or to serve themselves (Figure 1, Figure 2). Two-tiered conceptual model of fraud conceptualization Three-tiered conceptual model

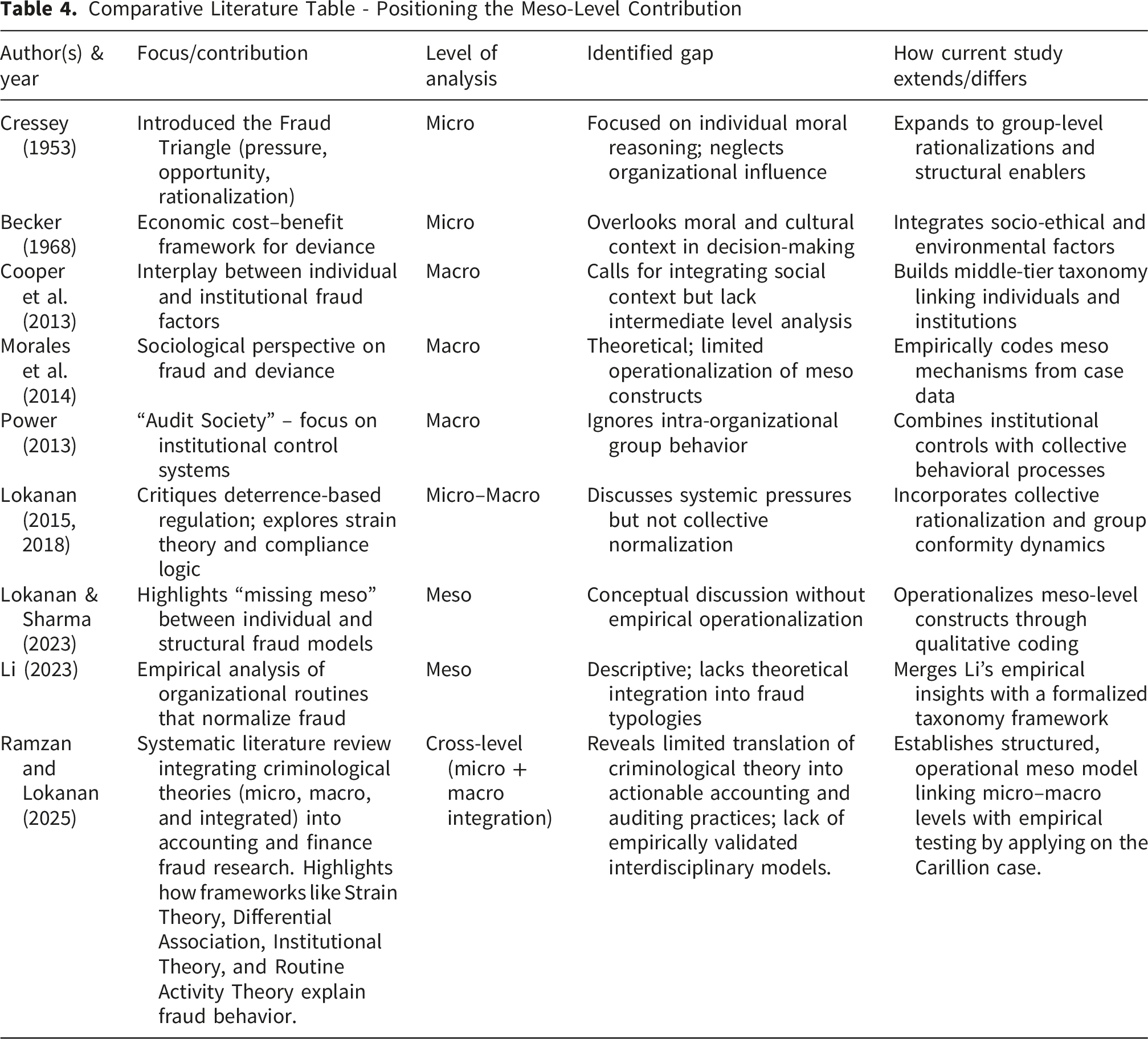

Comparative Literature Table - Positioning the Meso-Level Contribution

Methodology – Phase 2

Data Collection

The second phase of the research study incorporated an inductive reasoning approach. The different themes (factors) of the meso-level of the three-tiered model were derived from sociology literature. We conducted a thorough review of existing literature on fraudulent behavior in organizations and identified common themes related to fraudulent behavior at the meso level of analysis. The following are the themes that were extracted from the literature, contributing to the understanding of fraudulent behavior at the departmental level: 1. Groupthink: Excessive loyalty and rationality are adopted to justify the actions and the performance of these actions by the group (Janis, 1982; Lokanan, 2018; Scharff, 2005) 2. Collusive behavior: Collective action of members of a single group or different groups to attain departmental as well as organizational benefits (Barlow, 1993; Tillman, 2009; Xu & Zhang, 2017; Zhang et al., 2018). 3. Social Capital: Actions to achieve an end outcome such as departmental targets, bonuses etc., for group benefit (Jha, 2019; Khan, 2022; Ruiz-Palomino et al., 2021). 4. Group Identities: To create group identities in the organization, perpetrators build trust and perform unethically (den Nieuwenboer & Kaptein, 2008; Tajfel, 1974; Wang & Dyball, 2019).

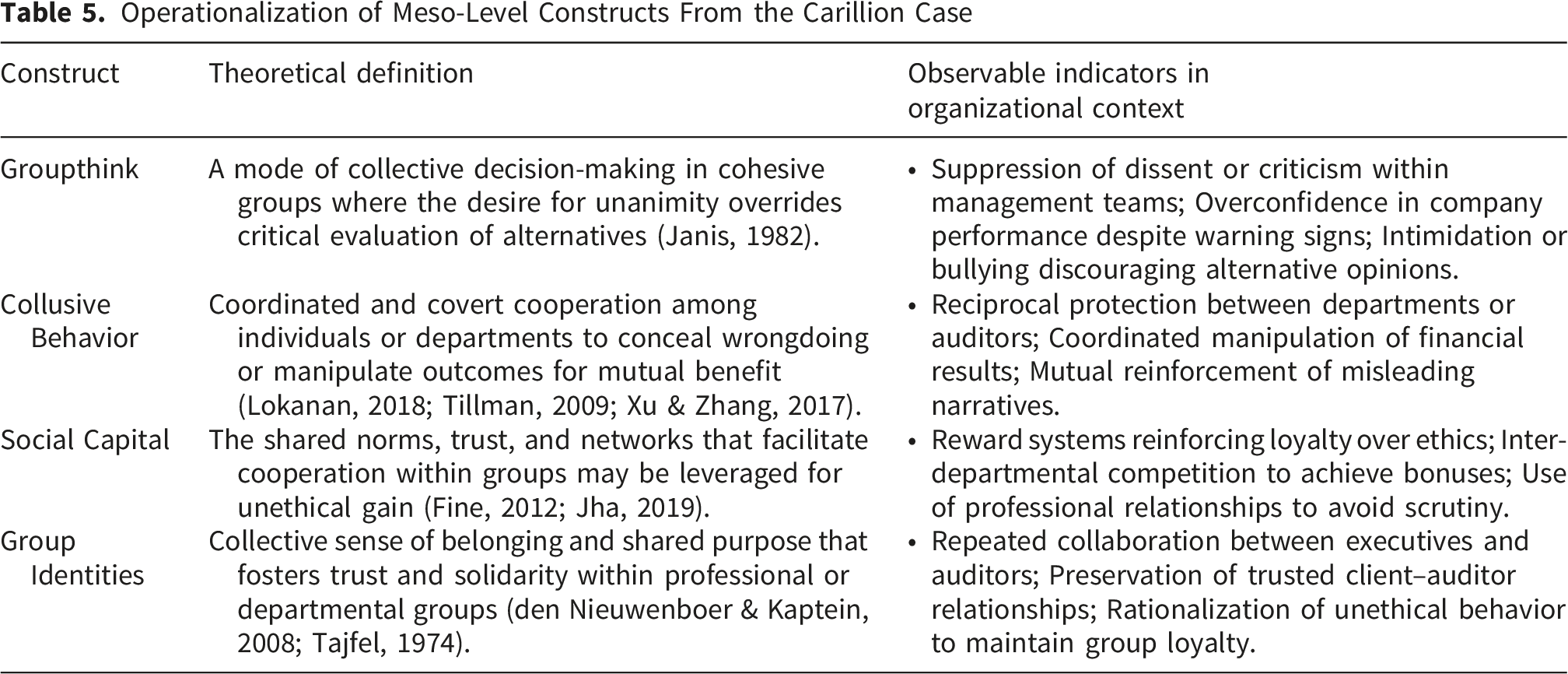

Operationalization of Meso-Level Constructs

Operationalization of Meso-Level Constructs From the Carillion Case

The coding process linked each construct to recurrent themes in the Carillion transcripts. Groupthink codes were derived from segments referencing managerial conformity and risk denial; collusion from interdepartmental cooperation in concealing losses; social capital from statements about competitive rewards and relational advantages; and group identities from repeated emphasis on trust and client–auditor loyalty. By articulating the theoretical definitions, indicators, and direct evidence, the model provides a transparent and replicable foundation for examining meso-level mechanisms of fraud across other organizational contexts.

Background of Carillion Fraud

This study utilized a theory-driven thematic analysis to apply the identified themes in examining various aspects of the Carillion fraud case. Makri and Neely (2021) advocate for the integration of a case study approach in research to validate the social relationships established through grounded theory. In alignment with this recommendation, the present study employs a case study methodology. Specifically, the Carillion fraud case, which serves as the focal point of this analysis, pertains to the insolvency of a multinational construction services and facilities management firm that occurred in January 2018. The company went into compulsory liquidation after a series of financial difficulties, including a large pension deficit and significant debt, were uncovered. The collapse had a major impact on the British economy, causing job losses and affecting public services. Carillion’s insolvency, regarded as the largest scandal in the UK, resulted in unfunded pension liabilities of £2.6 billion for 27,000 recipients, leaving behind 30,000 unpaid subcontractors owed £2 billion, and 450 service contracts with UK governments in limbo. The estimated cost to ensure continuity of services is just under £150 million (Patil, 2023).

Forensic investigations into the company’s operations revealed a number of issues, including questionable accounting practices and the mismanagement of major contracts. Moreover, it was discovered that Carillion had perpetrated fraudulent activities, which included inflating its profits and concealing its actual financial situation from stakeholders and the general public (Patil, 2023). The Carillion case has sparked debates on the effectiveness of corporate governance, the accountability of corporate executives, and the need for enhanced transparency in corporate reporting, which subsequently stimulated discourse on ethical business practices. The Carillion fraud was enabled by a complex network of collusive behavior, groupthink, and inadequate risk management systems within the company. These issues were not limited to a few individuals but were systemic problems within the organization (Patil, 2023). Therefore, a meso-level analysis is appropriate as it allows for a deeper understanding of the departmental factors that led to fraud, rather than solely focusing on the actions of individual actors.

To analyze the Carillion fraud based on meso-level factors, the transcripts of the “Debate on Lessons from the collapse of Carillion” (House of Commons Library, 2018) were used for the analysis. The debate on the lessons from the collapse of Carillion involved both oral and written evidence. The written transcripts included reports, research briefings, and other official documents, while the oral transcripts consisted of parliamentary debates and hearings, speeches, and interviews with experts and stakeholders. The reviewed material included publicly available transcripts obtained from the UK Parliamentary Archives.

The analysis incorporated testimonies provided by Carillion directors, pension regulators, and KPMG and Deloitte auditors, all of whom were implicated in the fraud. The discussions covered various aspects of the case, such as corporate governance, risk management, public sector procurement, the role of auditors and regulators, and the impact on employees, pensioners, and subcontractors. The aim of the debate was to learn from the Carillion case and identify ways to prevent similar failures in the future.

The transcripts were coded in the MAXQDA software based on the different themes (factors) of the three-tiered model. The meso-level themes generated in phase 2 of the methodology section were applied to the transcripts from the Carillion debate to illustrate that groupthink, collusive behavior, social capital, and group identities were systemic issues within the organization leading to criminal behavior. The study utilized a theory-driven and iterative technique to identify and evaluate categories related to fraudulent behavior using a meso-level analysis.

Discussion

The ontological impact of risk management approaches has been the subject of much research seeking to establish links between micro and macro factors. However, the prevailing understandings of fraud in the accounting and auditing literature remain limited, with many fraud-related terms, concepts, and behaviors yet to be fully explored. These perspectives include the micro-level factors, which focus on the causes of fraud by individual offenders, and the macro perspective, which examines the consequences of illegal behaviors due to institutional issues (Cooper et al., 2013; Lokanan & Sharma, 2023; Power, 2013). Yet parliamentary evidence from the Carillion inquiry revealed that neither level alone sufficiently explains how fraud evolves within complex organizational settings. Testimonies before the Work and Pensions Committee exposed a culture of managerial conformity and intimidation that silenced dissent, reflecting groupthink as a mechanism reinforcing poor judgment at the departmental level. The Joint Committee Report (HC 769-II, 2018) further documented collusive behavior among executives and auditors, who collectively concealed contract losses and exaggerated profit statements to sustain an illusion of stability. Witness accounts highlighted the misuse of social capital, as executives prioritized internal loyalty and personal rewards—such as bonuses and dividend preservation—over ethical reporting. Long-standing auditor–client relationships, notably KPMG’s nineteen-year tenure with Carillion, demonstrated entrenched group identities that compromised professional skepticism and blurred accountability boundaries. These insights confirm that the micro- and macro-level perspectives fail to fully capture the complexity of fraudulent conduct, which should instead be analyzed through the interplay of individual, institutional, and departmental dynamics (Albrecht et al., 2019; Hoffman, 2001; Lokanan, 2018).

The meso-level analysis of fraud remains a critical yet underexplored and often misrepresented dimension within accounting fraud scholarship. Focus is placed on smaller groups within organizations—such as teams, departments, and divisions—and on the relational dynamics that emerge between these units (Albrecht et al., 2019). Evidence from the Carillion parliamentary inquiries underscores the importance of this level of analysis, as testimonies revealed departmental conformity, internal alliances, and coordinated decision-making that facilitated the concealment of financial losses. The Work and Pensions Committee (2018) reported how Carillion’s leadership and auditors operated as interdependent units, reinforcing one another’s actions through shared assumptions and a reluctance to challenge authority—behaviors characteristic of groupthink and collusive cooperation. Furthermore, discussions in the House of Commons highlighted how internal reward systems and loyalty networks cultivated social capital, motivating executives to protect departmental reputations at the expense of transparency. Recognizing these intra-organizational interactions allows for a deeper understanding of how fraud becomes normalized across interconnected groups. The meso-level perspective, therefore, bridges the micro and macro dimensions of accounting fraud, providing a multidimensional view that accounts for the roles of collective behavior, power, and influence in enabling financial misconduct (Gabbioneta et al., 2013; Lokanan, 2018).

The model presented in this study consists of three integrated levels. The first level concerns the micro-level examination of fraud, which centers on the individual characteristics that may contribute to fraudulent behavior, including psychological traits, organizational isolation, and psychosocial factors. The above-mentioned phase is marked by the rationalization of temptations and the desire for personal gain, as well as the influence of social values and ethics on fraudulent behavior. The second tier of the proposed model focuses on the meso level, which delves into the collective actions of departmental and divisional actors who participate in fraudulent activities to serve shared interests and perspectives within interactive spaces. The meso level explores the internal features of an organization that could contribute to fraudulent activities, including its processes, procedures, cultures, and systems. Influences of fraudulent behavior extend beyond individual intentions, incentives, and circumstances and can also stem from a desire among department members to gain trust from managers, colleagues, and peers (den Nieuwenboer & Kaptein, 2008; Wang & Dyball, 2019). The interactions among individuals in a department can be fueled by collusive behavior and groupthink, while the competition to meet targets can create tension and temptation to circumvent the system (Lokanan, 2018; Scharff, 2005; Tillman, 2009; Xu & Zhang, 2017; Zhang et al., 2018). Previous studies (den Nieuwenboer & Kaptein, 2008; Wang & Dyball, 2019) have indicated that this may lead to a collective effort to modify the social environment in which fraudulent activities occur, including its structures, patterns, and beliefs. These modifications can, in turn, facilitate and legitimize fraudulent behavior among individuals involved in criminogenic behavior. The third level, the macro perspective, considers the impact of institutional dynamics on individual and divisional factors, including external economic and social conditions, the political/legal environment, external operating environments, internal environment, and power dynamics at the top levels of an organization. The above perspective acknowledges the variability of fraudulent behavior across contexts and time, due to changes in fraud dynamics and social constructions (Levi, 2008). By integrating these micro, meso, and macro perspectives, this model offers a comprehensive analytical framework that captures the multifaceted nature of accounting fraud and reveals how individual motives, group dynamics, and institutional forces converge to create conditions under which financial misconduct can emerge, persist, and become embedded within organizational practice.

Application

Coding Framework

An examination of the underlying causes of fraudulent behavior is crucial for the development of effective prevention and detection strategies. The application of a meso-level analysis, which focuses on the interactions among departmental and divisional actors who engage in fraudulent activities, can shed light on the factors that enable such behavior within organizations. By understanding these factors, organizations and regulatory bodies can devise measures to deter fraudulent behavior. The meso level approach underscores the significance of contextual and social dynamics in the commission of fraud and is consistent with broader efforts to combat white-collar crime and corporate wrongdoing. Furthermore, an understanding of the meso-level factors that facilitate fraudulent behavior can facilitate the implementation of targeted interventions aimed at mitigating the risks associated with such activities.

Groupthink

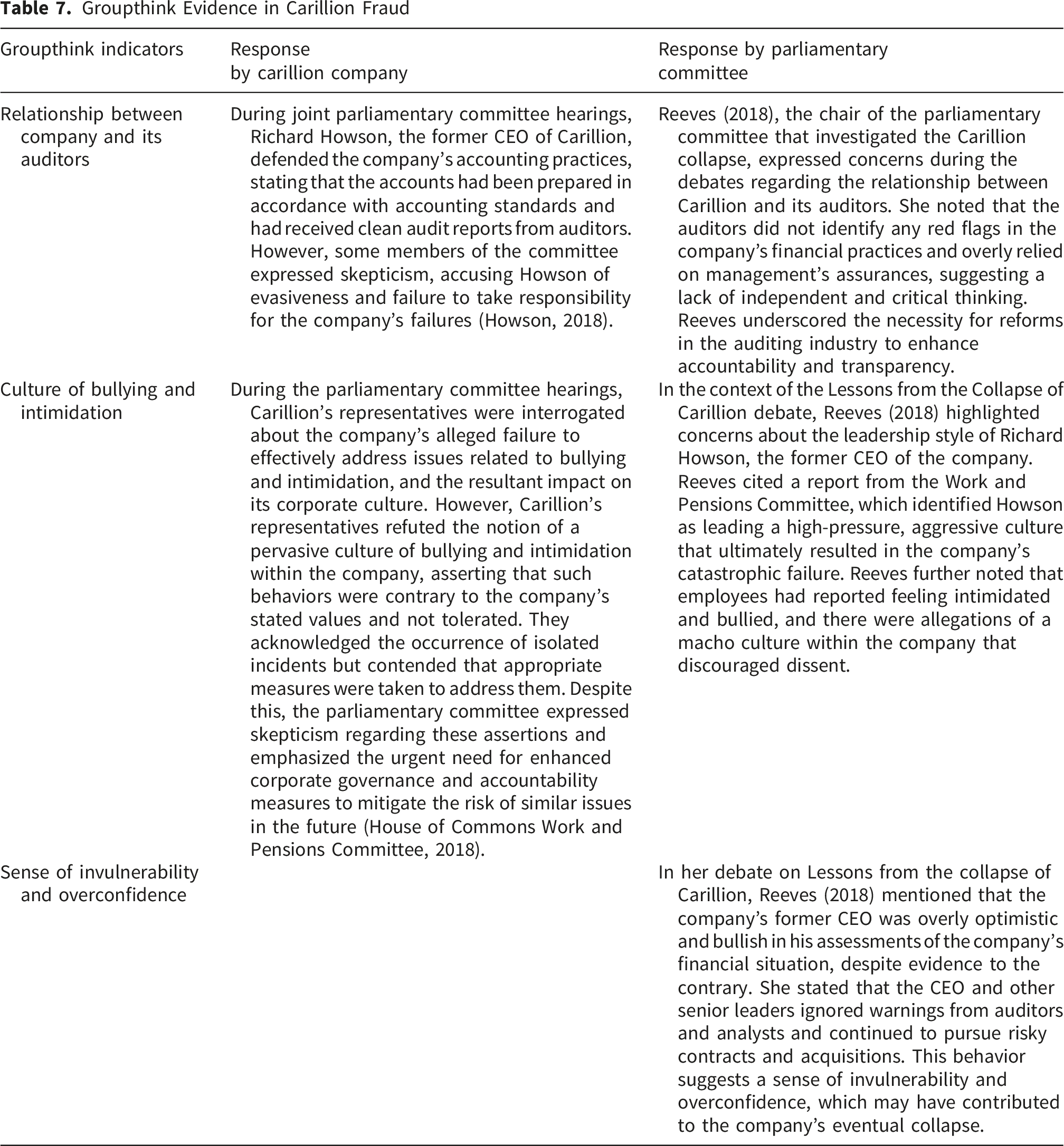

Groupthink is a “mode of thinking that people engage in when they are deeply involved in a cohesive group, [and] when the members’ strivings for unanimity override their motivation to realistically appraise alternative courses of action” (Janis, 1982, p. 9). Groupthink occurs when employees exhibit “arrogance over commitment and excessive or blind loyalty to the group” (Sims, 1992, p. 652). Invulnerability, the ability to rationalize events and actions, a sense of superiority within the group, pressure from the group, self-identity within the group, and unanimity are all motivators of groupthink (Scharff, 2005). Motivators of this kind were evident in the Carillion hearings, where the Work and Pensions Committee identified a corporate culture, characterized as “chronic lack of accountability and professionalism” and references to a “culture of making the numbers” and “willful blindness” among staff that suppressed dissent and discouraged critical evaluation of management decisions (HC 796, 2018, p. 27). The committee also highlights the need for a “cultural audit” and changes to ensure transparency, honesty, and integrity (p. 27). Executives maintained overconfidence in project performance despite repeated financial warnings, while the accounting apparatus “turn a blind eye” to Carillion’s overly optimistic forecasts (p. 42). Patterns of conformity, rationalization, and collective avoidance of criticism observed in the Carillion inquiry illustrate how groupthink operated as a meso-level mechanism that normalized poor judgment and ethical compromise within a tightly bound corporate hierarchy (Lokanan, 2018; Scharff, 2005).

Groupthink Evidence in Carillion Fraud

Another indicator of groupthink is the presence of a dominant leader or figurehead who discourages dissent and promotes conformity. In the Carillion inquiry, the Work and Pensions and BEIS committees observed that “Carillion’s board [was] responsible and culpable for the company’s failure,” presiding over what was described as a “rotten corporate culture” that fostered “recklessness, hubris and greed” (Joint Business, Energy and Industrial Strategy and Work and Pensions Committees, 2018). Such hierarchical control limited open dialogue and reinforced collective alignment around the CEO’s strategic direction. The combination of executive dominance, conformity pressures, and institutional overconfidence demonstrates how groupthink permeated organizational decision-making and contributed to Carillion’s collapse.

Collusive Behavior

Collusive Behavior Evidence in Carillion Fraud

Collusive networks cooperate to create the appearance of genuine profits and justified stock prices at the organizational level. Their behavior can also be observed at departmental levels to portray a successful and profitable department (Barlow, 1993; Jadil et al., 2022; Tillman, 2009). In the context of corporate accounting fraud, the complexity of the scheme requires the involvement of networks of organizations rather than a sole executive, who to varying degrees abets and assists in the distortion of financial statement information (Lokanan, 2018; Morales et al., 2014; Tillman, 2009). This criminogenic behavior can be observed not only among auditors but also among departments, where collusive behavior is utilized to conceal fraudulent activities.

Table 8 provides evidence of collusive behavior in the Carillion case. Collusive fraud is a complex and challenging issue to identify due to the coordinated efforts of colluders to conceal their fraudulent activities (Xu & Zhang, 2017). Colluders work in a highly coordinated manner and collectively alter their behavior to avoid detection, enabling them to develop more hidden and cost-efficient fraud techniques (Lokanan, 2018; Janis, 1982; Scharff, 2005; Xu & Zhang, 2017). The collaboration and coordination of departments, divisions, and teams can lead to heightened fraudulent activities and more advanced strategies, posing challenges in detecting collusive behavior (Xu & Zhang, 2017; Zhang et al., 2018).

The Work and Pensions and BEIS committees concluded that Carillion’s leadership engaged in “a relentless dash for cash, driven by acquisitions, rising debt and exploitation of suppliers,” using “aggressive accounting policies to present a rosy picture to the markets” (Joint Committees, 2018, HC 769, pp. 3–4). The Committees concluded that KPMG failed to exercise—and voice—professional skepticism towards Carillion’s aggressive accounting judgements and “complacently [signed] off the directors’ increasingly fantastical figures.” (UK Parliament, HC 769, 2018a, p. 4). Such coordinated behavior between internal management and external auditors reinforced misleading financial reporting and delayed recognition of losses. Collusive networks cooperated to create the appearance of genuine profits and justified stock prices at the organizational level. Their behavior also appeared at departmental levels, where financial results were manipulated to portray profitability (Barlow, 1993; Jadil et al., 2022; Tillman, 2009). In corporate accounting fraud, the complexity of the scheme often requires networks of organizations rather than a single executive, each abetting and assisting in the distortion of financial-statement information (Lokanan, 2018; Morales et al., 2014; Tillman, 2009).

Social Capital

Competition heightens physiological and psychological activation, preparing the body and mind for greater exertion and promoting excellent performance (Blader & Chen, 2011; Crocker & Knight, 2005; Kilduff et al., 2016; Steinhage et al., 2017). Social capital is created through this sense of competition and the transformation of interpersonal relationships towards desirable ends using shared resources (Fine, 2012). Gao and his supporting authors (2015) found that lower levels of social capital within workgroups were associated with higher rates of employee deviance, which may include fraudulent behavior within a department. High levels of social capital can create a strong sense of shared values and norms within departments, promoting ethical behavior and reducing the likelihood of fraud (Jha, 2019; Khan, 2022; Ruiz-Palomino et al., 2021).

The above outcome occurs because individuals who are embedded in networks of social relationships are more likely to be monitored and sanctioned by their peers, creating a social control mechanism against fraudulent behavior (Brezina & Azimi, 2018; O'Donnell et al., 2012). According to Roeser et al. (2016), these heightened psychological stakes cause people to adopt a more robust performance approach to tackle competition, increasing unethical conduct. For instance, staff at Wells Fargo increased sales by surreptitiously opening millions of illicit bank and credit card accounts, which is an unethical approach that brought long-term consequences for the organization (Steinhage et al., 2017).

The collapse of Carillion exposed fraudulent behavior among the Big 4 auditors, who prioritized gaining social capital through creative accounting practices over fulfilling their responsibilities for good governance. Individuals who are embedded in social networks are more likely to be monitored and sanctioned by their colleagues, thereby creating a social control mechanism that deters fraudulent behavior (Brezina & Azimi, 2018; O'Donnell et al., 2012). In the case of Carillion, the Big 4 auditors engaged in fraudulent behavior to gain social capital. In the written evidence of the debate on Lessons from the collapse of Carillion, Booth (2018, para. 4) noted that: “The sorry saga of Carillion is further evidence that the Big Four accountancy firms are prioritizing their own profits ahead of good governance at the companies they are supposed to be putting under the microscope.”

She further explains that, “KMPG, PwC, Deloitte and EY pocket millions of pounds for their lucrative audit work – even when they fail to warn about corporate disasters like Carillion.” Reeves (2018, para. 16) claims in her debate that: “Competition in industry is supposed to drive up quality and bring down costs. It is not working in the audit market, where a cozy club of four hoover up huge fees before, during and after any corporate failure, yet their audits and accounts…read like a mystery novel—a fiction, with the reader searching for scant clues on what is really happening.…There are conflicts of interest at every turn.”

Hence, to achieve social capital (departmental targets) and showcase positive divisional performance, employees can perform their duties ethically or unethically (Gao & Greenberg, 2015). Since the Big Four auditors must attain departmental targets (social capital) to gain social acceptance and recognition, as seen in the Carillion fraud scheme, these auditors engaged in creative accounting practices—whether fraudulent or negligent—that helped them secure their financial and reputational standing (Jha, 2019; Khan, 2022). Evidence from the Follow-Up Report on Auditing and Corporate Governance noted persistent concerns that KPMG lacked sufficient professional skepticism and relied too heavily on management representations during its nineteen-year tenure as Carillion’s auditor. Parliamentary debates also criticized the Big Four for “prioritizing their own profits ahead of good governance” and for failing to warn about the impending collapse (Booth, 2018; Reeves, 2018; HC 1392, 2019). The Work and Pensions and BEIS committees found that Carillion’s directors “elected to increase its dividend pay-out every year, come what may,” and that “even as the company very publicly began to unravel, the board was concerned with increasing and protecting generous executive bonuses” (HC 769, 2018, pp. 3–4). These examples reveal how the pursuit of social capital—through loyalty, reputation, and reward systems—encouraged auditors and executives alike to act in ways that preserved group advantage at the expense of ethical responsibility.

Research has shown that higher levels of social capital within an organization are negatively associated with unethical behavior. Bai and their supporting authors (2021) found that higher levels of social capital within an organization were negatively associated with unethical behavior. In the Carillion fraud case, the board of directors received a huge sum of compensation from these Ponzi schemes (UK Parliament, 2018a, 2018b). They created their social capital through collective action to earn compensation and compete in the market with other rivals, which is why these remunerations were never disclosed to the public. As stated by the pension regulators of the UK Parliament, 2018a, 2018b, there was an “absence of clear remuneration terms and performance targets set out for the Special Managers.” Reeves (2018, para. 5), in her UK Parliament debate, explained how Carillion was: “increasing senior salaries and bonuses, ensuring that a dividend was paid regardless of its own health; paying suppliers late, and bidding for contracts that it could not afford to deliver on time or on budget.”

This evidence was not made available by the organization itself but was instead disseminated by the commission. In the debate of UK Parliament, Reeves (2018, para. 7) also pointed out that, “It’s remuneration committee increased payouts on the basis of industry averages, rather than the performance of the business Carillion. A responsible business would see payment by results, not payment by averages.”

These findings show that the firm was creating social capital for group benefits that align with the philosophy of top management. Previous studies have indicated that rewarding top performers can lead to the development of social capital, as exemplified in the Carillion fraud case where departments were encouraged to compete with one another (Beersma et al., 2003; Jha, 2019; Khan, 2022; Ruiz-Palomino et al., 2021). Therefore, incentives offered to high-performing individuals can serve as motivation for fraudulent behavior, leading groups to strive for the acquisition of social capital.

Group Identities

Individual and group identities are cultivated, maintained, and sustained through collective attitudes based on acculturation and common purposes. Identities are shaped via repeated contact within powerful communities (Fine, 2012). Trust is considered crucial in the development of stable working relationships and strong communities within an organization at a departmental level. Gino and Pierce (2010) examine the effect of wealth on unethical behavior and argue that individuals who perceive abundance are more likely to engage in fraudulent behavior, even when they are part of a trusted group. When considering the notion of social identities at the meso level of analysis in relation to the Carillion fraud scheme, the Big 4 accounting firms fail to point out such schemes as they are trying to build group identities to maintain client relationships with firms through trust. Booth (2018) further noted that “[i]t is a parasitical relationship which sees the auditors prosper, regardless of what happens to the companies, employees and investors who rely on their scrutiny.”

For many fraudulent scams and schemes, the initial step that motivates the occurrence of fraud is building trust (Appelbaum et al., 2007) for the purpose of creating group identities. The repeated contacts and mutual trust built between the auditor and client groups motivated communities to engage in fraudulent behavior in the Carillion case. The Carillion report acknowledged that “the dominance of a few giant audit and professional services firms can inhibit competition,” a concentration that weakens independence and reduces the degree of challenge auditors bring to large corporate clients (HC 769, 2018, p. 32). Parliamentary findings highlighted that KPMG’s long and complacent tenure of cursory audits fostered an environment where independence and skepticism were eroded, allowing questionable accounting practices to persist unchecked (UK Parliament, 2018a, 2018b). The inquiry further described the Big Four audit firms as a “cozy club incapable of providing the degree of independent challenge needed,” underscoring how prolonged auditor–client familiarity compromised professional scrutiny (HC 769, 2018). Stephens (2018, para.79) corroborates this argument by stating in the debate that: “Boardroom lifebelts were well and truly secured on this corporate version of the Titanic, with the auditors signing off on their assurances as the SS Carillion steered full speed ahead to the icebergs.”

These findings illustrate how sustained professional relationships and shared identities between auditors and executives contributed to the normalization of unethical practices within the organizational network.

Reeves (2018) argued that the auditors of Carillion failed to disclose the company’s precarious financial situation, despite it being a major corporation on the verge of collapse. According to Reeves, “warning lights should have been flashing when such a big business was on the brink” (para. 3). This failure of auditors to reveal the true state of the company not only concealed the fraud but also undermined the trust that the public and authorities had in their identities. KPMG, the audit firm, was paid £29 million over 19 years by Carillion for conducting audits (House of Commons Work and Pensions Committee, 2018). However, Reeves (2018) criticized the audits conducted by KPMG, stating that they seemed to have been unproductive and futile in providing investors, workers, and the public with accurate assurance. Prioritization of client confidence and group identities by auditors, such as KPMG, in their service provision may indicate their inclination towards maintaining favorable relationships with clients and preserving a sense of group identity within their professional community. This phenomenon has the potential to affect their objectivity in detecting and addressing fraudulent activities during audits. Furthermore, the attribution of higher levels of cognitive trust to the accuser compared to the accused, particularly in the presence of established group identities, suggests that group dynamics and perceptions of trust can influence perceptions of fraud allegations (Fine, 2012; Kennedy, 2015).

There is another circumstance where the accused deliberately commits fraud to gain the trust of their department/division/team (Fine, 2012; Kennedy, 2015). Based on the above analysis, trust in creating group identities is linked to unethical or fraudulent behavior. Employees tend to be influenced by their leaders when it comes to engaging in appropriate or inappropriate behavior (Knoll et al., 2017). Influence on employees can come from observing how leaders themselves behave and from seeing how other employees are either rewarded or punished for their conduct (Appelbaum et al., 2007; Graham et al., 2015; Knoll et al., 2017). For example, if an employee sees deceptive behavior rewarded and builds a group identity due to the benefits attained, the group is tempted to engage in deviant behavior. According to combined stakeholder letters from Chairs in the UK Parliament, 2018a, 2018b regarding the Carillion case, the auditing profession: “is an oligopoly. You can’t be all things to all men and women forever. We have to reduce the level of conflicts and demonstrate why they are manageable and why the public and all stakeholders should trust us” (p. 1)

Based on the excerpts derived from the debate on the Carillion case, meso-level factors have a significant influence on criminogenic behavior in corporations to conceal negative information.

Conclusion

The paper critically highlights the limitations of existing understandings of fraud in the accounting and auditing literature, which predominantly focus on individual and institutional factors while failing to fully capture the complexity of fraudulent conduct. In response to this gap, this study introduces a meso-level tier that encompasses the internal features of organizations that could contribute to fraudulent activities, including their processes, procedures, cultures, and systems. This meso-level perspective of fraud, which examines smaller groups within an organization and considers the relationships between departmental and divisional positions, is identified as a critical area that is often overlooked in accounting research.

The proposed model integrates three levels of analysis: micro-level, meso-level, and macro-level. The micro-level tier examines individual characteristics such as rationality, temptation, social values, and moral intensity that motivate perpetrators to commit fraud. The macro-level tier encompasses a comprehensive set of structural forces that influence fraudulent behavior at the institutional level, including the political and legal environment, operating environment, internal control processes, and power dynamics and authority within an organization. These factors serve as motivators for fraudulent tendencies and shape the overall context within which fraud occurs at the institutional level.

The meso-level tier, which emerges from the identified gap in the literature, encompasses a range of factors that contribute to fraudulent behavior within organizations, including groupthink, collusive behavior, competition among departments, social capital, and the establishment of trust among peers and divisions to build group identities. These meso-level factors provide important insights into the social dynamics and interpersonal relationships that contribute to fraud within organizational contexts and highlight the need for further research in this area.

The grounded theory approach was employed to extract the micro and macro-level tiers from the existing accounting fraud literature and identify the research gap that led to the development of a meso-level theoretical conceptualization of fraud. The gap was identified by drawing insights from the sociological literature on organizational culture, social networks, organizational structure, organizational climate, group dynamics, power dynamics, and white-collar crime. The proposed model was then applied to analyze the case of Carillion fraud. The findings, after applying the meso perspective model to the Carillion fraud, underscore the importance of robust corporate governance, transparency, and accountability in the business sector as preventive measures against similar issues in the future. Additionally, the concerns raised by Reeves (2018) regarding the relationship between Carillion and its auditors, KPMG, as evidenced in the parliamentary committee’s report, highlight the necessity of robust auditing practices, including the exercise of professional skepticism and independence, to ensure the accuracy and transparency of financial reporting in corporations. Further investigation and measures to address potential conflicts of interest and collusion between companies and their auditors may be warranted to mitigate similar lapses in the future.