Abstract

Background:

Saudi Arabia introduced one of the most significant beverage taxes globally (50% on sugar-sweetened drinks and 100% on energy drinks). This provides a unique opportunity to investigate the impact of taxes on perceptions and attitudes toward sugary drinks and whether consumers are substituting taxed beverages with healthy alternatives.

Methods:

A qualitative study using semi-structured interviews with university students in Riyadh, Saudi Arabia. Interviews were analysed using thematic analysis.

Results:

A total of 27 participants were interviewed. Four themes were identified from the data: Health is beyond personal choice, The role of food companies in promoting health behaviour, What is excise tax and why do we need it? and The impact of taxation on consumer behaviour. Social factors and the availability and prices of healthy and unhealthy products often restrict the ability to follow a healthy diet. Food companies have a role in facilitating access to nutritious products, and policies should be in place to regulate the process. Many participants needed to be made aware of the implementation of the excise tax and often confused it with the value-added tax. Participants who perceived themselves as light consumers of sugary drinks reported minimal impact of the taxation on their consumption. Those who perceive themselves as heavy consumers have reported being affected by taxation.

Conclusions:

This study strengthens the idea that people’s perception of the impact of taxation on their purchasing behaviour was influenced by their views regarding their consumption. A comprehensive approach is needed to reduce sugary drinks, including promoting healthy substitutes and enhancing understanding of public health interventions to maximise benefits.

Introduction

Obesity is a complex problem caused by multiple factors, such as increased energy intake, reduced physical activity levels, increased sedentary time (1) and a global shift towards cheap and highly processed food high in calories, sodium and added sugar (2,3). There is no simple solution to prevent weight gain, and no country has reversed the obesity epidemic yet. However, systematic reviews and meta-analyses show a strong link between increased intake of added sugar—especially through Sugar-Sweetened Beverages (SSBs)—and the global obesity epidemic, as well as higher risks of type 2 diabetes and cardiovascular diseases (4–7). Consuming SSBs is linked to unhealthy behaviours; such individuals eat fewer vegetables and spend more time on screens like televisions, phones and video games (8–10). Therefore, limiting sugary drink consumption can help people maintain a healthy weight and dietary patterns (10).

The World Health Organization recommends reducing SSB consumption by considering policy-level instruments, such as taxes (11). Evidence from several countries, including Mexico, the United States and Saudi Arabia, shows SSB taxes effectively reduce consumption rates (12). Additionally, evidence from economic and epidemiological models suggests that reducing SSB consumption will significantly reduce the incidence of obesity and type 2 diabetes (13–15). This evidence demonstrates the promising potential of taxation in reducing the consumption of these types of beverages.

While taxation might influence SSB consumption, its long-term behavioural effects are unclear. Studies show that consumers, especially youth, prioritise taste over health, though prices matter (16). People know SSBs impact health, but see it as irrelevant personally (17). Eykelenboom et al. (18) reviewed public and policymaker acceptance of the SSB tax, finding that many believe taxation affects purchasing because price influences decisions. However, some think it has little effect on heavy consumers, people with obesity and affluent people (18). The review also suggested that over half distrust government motives, viewing policies as revenue-driven rather than health-focused (18).

Saudis are the fifth-largest consumers of daily calories from SSBs worldwide (19). Additionally, the most recent national surveys indicate that obesity is a significant public health problem, with 57% of males and 61% of females being considered either overweight or obese (20), figures to which SSB consumption has likely directly contributed. The Saudi government has launched obesity-fighting programmes promoting the prevention of health risks and, by 2030, Saudi Arabia aims to reduce the obesity rate by 3% (21). In 2017, Saudi Arabia introduced a 50% tax on SSBs and a 100% tax on energy drinks, expanding to all SSBs in December 2019. This offers a chance to assess Saudis’ awareness and the tax’s impact on their behaviour.

Young adults in Saudi Arabia represent the primary consumers of SSBs (8,22). This study investigates young Saudi adults’ perceptions of SSBs and how a tax might influence their consumption, crucial for designing effective health promotion programmes that encourage healthy beverage choices and improve public health.

Methods

This exploratory qualitative study aimed to generate an in-depth understanding of Saudi participants’ perceptions of excise taxes on food and beverages, rather than test hypotheses, making semi-structured interviews an appropriate design. This research method is ideal for investigating perceptions and attitudes toward health policies and interventions (23), providing deeper insights, and examining the Saudi public’s views and reactions to excise taxation implementation. This study was reviewed and approved by the King Saud University Human Research Ethics Committee (Ref. E19 – 4382).

Sampling and recruitment

Potential study participants were recruited from a public university in Riyadh, Saudi Arabia. The study employed purposive sampling to recruit participants from various colleges, age groups and genders. An invitation link was emailed to all students via the Tawasul system, which allows researchers to send emails to all university students and employees.

The invitation explained the study’s purpose, participants’ roles and their right to withdraw. Interested individuals completed an electronic consent and chose a contact method. The team then contacted them to schedule the interview via their preferred communication method.

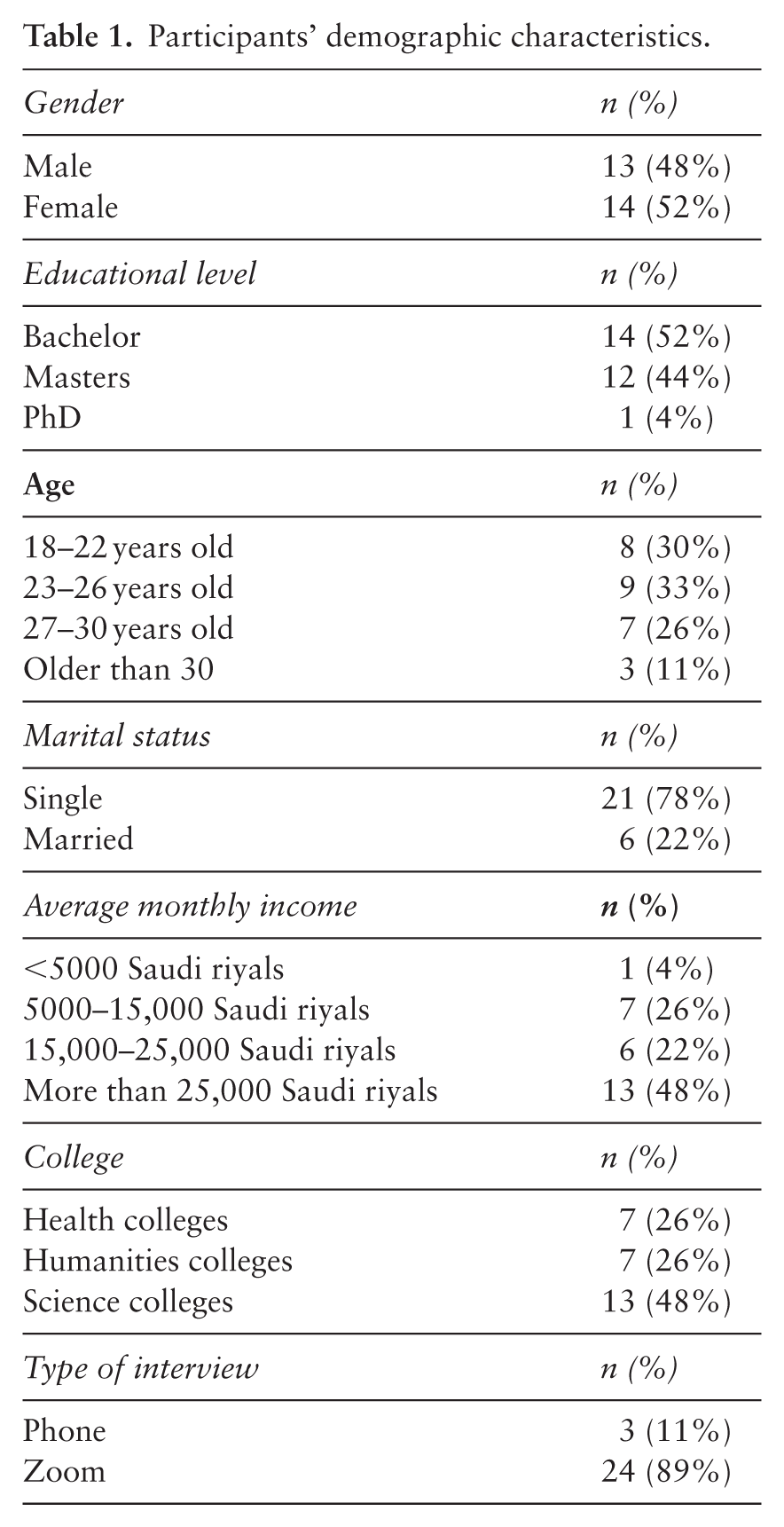

Participants were undergraduate and postgraduate students enrolled in diverse degree programmes across multiple colleges (health, humanities and science) of the university, as shown in Table 1. The sample comprised 52% bachelor students, 44% master’s students and 4% PhD students, representing diverse academic and demographic backgrounds.

Participants’ demographic characteristics.

Interview topic guide

The semi-structured interview guide (Supplemental material File 1 online) was developed based on a review of prior studies exploring attitudes toward SSB taxation (24) and guided by the Theory of Planned Behaviour (TPB) (25). The TPB suggests that behavioural intention is determined by individuals’ attitudes towards behaviour, subjective norms and perceived behavioural control (25). Previous evidence has indicated that the TPB helps explain nutrition-related behaviours, including SSB consumption (26,27).

The initial interview guide consisted of open-ended questions exploring participants’ knowledge, attitudes, subjective norms and perceived behavioural control regarding SSB taxation. To enhance content validity and cultural appropriateness, the guide was reviewed by experts in qualitative research and public health policy who were familiar with the Saudi Arabian public health context. The experts assessed clarity, relevance and contextual suitability. Minor wording modifications were made in response to their feedback. The interview guide was subsequently piloted with one participant to assess clarity, question flow and comprehensibility within the Saudi context. Minor adjustments were made to improve sequencing and wording. The pilot interview was not included in the final analysis.

In qualitative research, interview guides are flexible and iterative tools rather than standardised psychometric instruments. Therefore, reliability was addressed through methodological rigour strategies, including consistent use of the interview guide, interviewer training, verbatim transcription and systematic thematic analysis. We acknowledge that piloting the guide with one participant represents a limitation; however, given the iterative design of qualitative interviews, no substantial modifications were required following initial data collection.

Data collection

Interviews were conducted via phone or Zoom and lasted between 25 and 50 min. With the participants’ consent, all interviews were audio recorded. The interviews took place from March to June 2021. All interviews were conducted by SA, a Saudi female researcher trained in qualitative methods, with prior experience in public health research. Conducting interviews by a culturally aligned researcher facilitated rapport and contextual sensitivity. Participants also completed an electronic demographic questionnaire to provide descriptive data, including age, gender, educational level and marital status.

We continued the interviews until we reached thematic saturation. Thematic saturation was assessed by SA during data collection and confirmed through team discussions with NA and RA. Saturation was defined as the point at which no new themes emerged across three consecutive interviews, thereby confirming data adequacy. This judgement was supported by continual review of transcripts during the data collection phase.

Data analysis

All interviews were transcribed verbatim by a professional service. Our analytic process adhered to Braun and Clarke’s reflexive thematic analysis (28), emphasising the identification of recurring meanings throughout the dataset rather than analysing discursive aspects and constructions. An inductive approach was used, in which codes and themes were derived from careful reading of the data. SA coded all interviews with ATLAS.ti, while NA, a Saudi public health researcher, coded a random sample. They independently created initial coding frameworks for preliminary themes, then refined them with input from RA, a Saudi researcher in food and nutrition policies. To ensure analytical rigour, intercoder agreement was assessed between the two primary coders on a random subset of transcripts. Discrepancies were discussed and reconciled through consensus. Credibility was further reinforced through team debriefings, maintaining an audit trail of coding decisions and iterative comparison of themes. Multiple researchers analysing transcripts enhance reflexivity and ensure diverse perspectives (29).

Initial coding focused on participants’ knowledge and perceptions of excise taxes, reported behavioural responses, social and cultural influences and perceived economic impacts. These categories were iteratively refined into higher-order themes through constant comparison across transcripts. The research team refined each theme and overall interpretations to enhance the study’s rigour and reliability (23). In Supplemental File 2, themes are linked to participant identifiers to clarify analytic distribution.

Results

The study included 27 participants, 13 males and 14 females, from diverse colleges and age groups (see Table 1 and Supplemental File 3). Four main themes were devised from the data: Health is beyond personal choice, The role of food companies in promoting health behaviour, What excise tax is, and why do we need it? and The impact of taxation on consumer behaviour.

Health is beyond personal choice

Despite being aware of the detrimental effects of SSBs on health, most participants cited various external factors that influenced their consumption. They deliberated on the concept of ‘choice’ about healthier options, noting that the price and accessibility of products significantly shaped their purchasing behaviour. Unhealthy food items, including SSBs, were often regarded as the more affordable and easily obtainable choice across all age groups and socioeconomic backgrounds. Participants emphasised that healthier alternatives are usually pricier and less accessible, constraining individuals’ ability to choose more nutritious food.

It’s an addiction

Participants expressed the difficulty of controlling their consumption of sugary soft drinks, describing them as ‘addictive’ and noting the challenge of changing health behaviours. Some participants explained that they believe sugary soft drinks are addictive because they lead to an increase in adrenaline, attributed to the sugar content, caffeine and other stimulants.

‘I am addicted to it [SSB]; I must have it with every meal. If I have lunch, I must have Pepsi with it . . . but if I go out, it is almost impossible that I will have a meal without a soft drink . . . And I know it is wrong.’ (P15, male, 23–26 years old)

Despite knowing SSB harms, some participants felt the pleasure outweighed health risks. They believed awareness had little effect because most know the adverse effects. Some justified inaction, noting health impacts take time.

‘I mean, the harm does not happen in a short or close period, meaning no one who started eating sugars or drinking sweetened drinks . . . will not get the disease after two or four years. They might get the disease after fifty or sixty years.’ (P23, male, 23–26 years old)

Social influences on consumption

Participants discussed how social factors influence SSB consumption, often viewing these choices as societal norms rather than individual preferences. SSBs and sweets were linked to social occasions, with SSBs playing a significant role in social meals. The availability of unhealthy options strongly impacted consumption, regardless of health awareness.

‘Because it [SSB] has entered into all aspects of life, you will find it in social gatherings, restaurants, and everyday activities. So now there is a connection between consuming it [SSB] and joy and social gathering.’ (P9, male, 18–22 years old) ‘Yes, but I feel it is very difficult. I mean, we are already used to these drinks; how can we change?’ (P20, female, 18–22 years old)

Saudi society’s interconnectedness and family involvement complicate diet choices, with social pressures influencing preferences. Participants suggested that social change is needed. Parents said they struggle to control their children’s diet against family members’ influences, especially in schools and public settings.

‘It’s available to them from the whole community; in school canteens and everything.’ (P23, male, 23–26 years old)

The role of food companies in promoting health behaviour

The influence of food companies on consumers’ health behaviour has been a topic of substantial discussion. It is widely acknowledged that food companies are primarily driven by financial gain and revenue rather than being motivated by the health benefits for consumers.

‘Companies would not care about the percentage of obesity. They only care about profit; they don’t care whether this product harms you or what harms you.’ (P17, female, above 30 years old)

There was widespread distrust of food companies, as many participants voiced concerns about deceptive food labels. For example, numerous SSBs are labelled as ‘no added sugar’ despite the product’s nutrition facts indicating high sugar content.

‘Even if they write that it is free of sugar, and now in front of me a juice, I mean it is free of sugar, but it tastes like sugar; I never expect companies to be credible in the labels written on the cans.’ (P17, female, above 30 years old)

Food companies, including restaurants and delivery services, use strategies like promotions to make unhealthy options more appealing. For example, the ‘Supersized’ option costs only slightly more than a small meal. Similarly, a sandwich’s price is close to that of a meal with sides and a drink, encouraging people to choose the meal.

‘It is possibly linked to our frequent visits to restaurants. If we went to a restaurant where Pepsi [refill] is free . . . You can drink 3 cups, four cups. But the juice would cost 22 riyals and be consumed in two sips’ (P23, male, 23–26 years old)

Food companies should actively offer healthier choices and be responsible for providing affordable, nutritious options to promote health. Policies on unhealthy food regulation are crucial. Participants suggest that excise taxes could motivate companies to produce healthier foods by incentivising lower sugar content, thereby improving product quality and benefiting the community.

‘Enforce policies and laws on companies in terms of sugars . . . it is imposed on companies that they reduce the percentage of sugars, replace sugars from processed sugars to natural sugars, you may force them to reduce the percentage . . . and companies can do so.’ (P12, male, 23–26 years old)

What is excise tax, and why do we need it?

Many participants hesitated to share their opinions on taxation for public health purposes because they felt they needed to be more qualified, believing that only experts could offer opinions on public health policies.

‘Frankly, I am not an expert in these matters. I cannot help you a lot in that area; there are certainly people who are more knowledgeable than I.’ (P2, male, 27–30 years old)

Awareness of the excise tax

While some participants could distinguish between excise tax and value-added tax and identify the products to which these taxes are applied, most participants in this study needed clarification about the differences. They also needed to be made aware of the concept of excise tax, its value and the rationale behind its implementation. Participants highlighted the need to share knowledge about the purposes of taxation with the Saudi public.

‘I do not know the percentage that was imposed on sweetened drinks, until now I do not know, but I know that there is a tax on sweetened drinks, but I do not know how much it is.’ (P18, male, 18–22 years old)

Views about the excise tax

Some believe that implementing an excise tax promotes ‘social justice’. They argued that everyone is responsible for improving their health and reducing the strain on healthcare. They see taxation as a way for consumers of unhealthy products to contribute to future healthcare costs.

‘As a matter of social justice, these are harmful things, and we said that they are harmful, and you insist on drinking them. We take a financial benefit from them, in which we support health and other projects to treat them in the long run, at the very least.’ (P2, male, 27–30 years old)

Several participants saw taxation as a form of paternalism that restricts personal choice. While some found it unfair, others accepted the SSB tax mainly because they trusted policymakers’ evidence-based judgments, believing they knew what was best for public health. This trust prevented criticism of the tax.

‘I am sure that there are people who know much more about these decisions than I do, and they studied them extensively before they became a reality. Their impact will be positive in the long run.’ (P2, male, 27–30 years old)

What should we tax?

An important factor in the acceptance of taxation is that taxed products are non-essential and lack nutritional value. Participants suggested taxing other items, like sweets, chocolates, chips, processed meats and high-saturated-fat foods. Many are opposed to or unsure about taxing fast food, which is considered unhealthy but still has nutritional value.

‘Chips, energy drinks, I hope that one bottle of energy drinks would cost 60 riyals, anything harmful, and it does not have any nutritional value.’ (P15, male, 23–26 years old) ‘Applying tax to fast food, no, not necessarily, because sometimes fast food is not as harmful as sweetened drinks.’ (P6, male 18–22 years old)

While it was generally agreed that fast food is not essential, some argued that it might be the only choice for lower-income groups. This raised concerns about growing inequalities, as ‘price’ might outweigh ‘health’ for some populations. Participants emphasised the need to consider tax impacts on the disadvantaged.

‘People who buy fast food are the ones whose financial situation is difficult; this is the only alternative for them, so we tax fast food, this might mean that their financial situation will be worse, which will worsen their health.’ (P19, female, 27–30 years old)

Many participants strongly support higher taxes on harmful products like tobacco, SSBs and energy drinks. Some suggest raising prices by 100% or more to deter consumption and improve public health.

‘I agree on the issue of tobacco products in general; it is essential, and I would not mind it if it is even a 200% increase, not only 100%.’ (P7, female, 27–30 years old)

The impact of taxation on consumer behaviour

Participants often see their sugary drink intake as minimal compared with past habits and peers, justifying it by comparison or choosing less harmful options like soft drinks over energy drinks. Their views on taxation’s impact on their buying habits are directly linked to their perceptions of consumption. Those who deemed their SSB consumption ‘reasonable’ said taxation did not affect them. Those who perceived themselves as heavy consumers of SSBs admitted to reducing their daily intake owing to taxation. They mentioned strategies like opting for smaller cans or buying in bulk during special offers to avoid the tax.

‘For me, it didn’t make an impact because my consumption before was a fair consumption or even considered below average.’(P3, male, 23–26 years old) ‘Frankly, because I used to buy a lot. But this tax, it reduced my consumption.’ (P11, female, 18–22 years old)

Participants discussed different substitutes for SSBs. Some replaced SSBs with coffee or tea, while others tried water, fresh juices and dairy products. However, some participants remained concerned about replacing carbonated drinks with fresh juices because of their high sugar content.

‘I replaced it with coffee, of course. Coffee does not contain sugar. It can cause addiction, it may cause health problems, but I think that its harms are much less than energy drinks.’ (P4, male, 23–26 years old)

Some participants attributed the limited effect of SSB taxation on purchasing behaviour to the minimal price increase. Some believed Saudi society is ‘privileged’ and unaffected by taxation. Others saw taxation’s limited impact due to poor money management, as many are perceived as ‘big spenders’ regardless of their financial situation.

‘A simple increase in price will not have an effect. Saudis do not check for halalas or riyal or two riyals. But if the change was as large as a 100% increase, it might have an impact.’ (P16, female, above 30 years old)

The impact of taxation was perceived mainly to affect populations with limited resources, such as children and teenagers. The effect of taxation on the younger generation was often deemed justified and accepted.

Knowledge is essential, but not enough

Participants debated whether taxation or health awareness has a greater impact on health behaviours. Most agreed that public health awareness is important, but many favoured taxation as the more influential factor. Taxation does not diminish the importance of health awareness, and many participants needed to understand its purposes. They stressed raising public awareness of policies’ goals, benefits and consequences to shape health policy. They also noted that increasing health awareness fosters a health-valuing society and promotes long-term behaviour change.

‘Raising awareness means that the choice is based on conviction; it becomes stronger than it is a tax, which sounds like something purely monetary.’ (P10, female, 23–26 years old)

Discussion

This study examined the public’s perceptions and attitudes toward SSB consumption and the potential influence of a tax on consumption patterns among young adults in Saudi Arabia. The study identified factors associated with participants’ SSB consumption and opinions on an SSB tax. Participants emphasised health goes beyond personal choice, citing cost, availability and social influences. They felt food companies should promote health over profit. Most were unclear about the excise tax and its implications. Discussions focused on perceived consumption and taxing effects. Participants called for public education on excise tax to better influence SSB intake.

People’s perceptions of taxation’s impact vary with their consumption views. Those with heavy SSB intake are seen as more affected by taxes than moderate consumers. Previous evidence from the United States suggested that price was a key factor influencing beverage selection among young adults, following taste, especially for those with limited resources (16). Several studies suggested decreased SSB consumption due to excise tax-induced price increases (30–32). In Saudi Arabia, carbonated drink sales decreased by 35% (30). Participants who saw their SSB intake as ‘reasonable’ reported no effect from taxation. This may be due to their negative attitude towards SSBs consumption and perceived control influencing their intent to change. Evidence also showed that people believed the tax would not reduce consumption because the price change was too small (24). Future research should assess the perceived and actual effects of SSB consumption on behaviour change related to taxation. This offers insights to optimise taxation’s impact on health behaviour and outcomes.

Participants discussed substitutes for taxed beverages like water, coffee, tea and fresh juices. Evidence from Mexico indicated that people might replace SSBs with homemade drinks (like 100% fruit juices) and water if prices rise (24). To compensate for the impact of increased prices on purchasing behaviour, people may choose multi-purchase offers and brands on sale (33), as observed in the current study. Participants highlight social and environmental factors influencing SSBs intake beyond personal choices. Addressing this requires a comprehensive approach, promoting healthy alternatives, enhancing understanding of public health measures and framing the SSBs tax as part of a broader strategy to improve public health.

Most participants were unsure of the differences between excise tax and value-added tax, including the rationale of excise tax. However, they trusted policymakers and believed the excise tax served the common good. This contradicts other studies showing public mistrust of SSB tax intentions and concerns about increased income (18,34). Although participants in the current study trusted authorities to implement appropriate health interventions, there is a need to raise awareness of the rationale and benefits of the SSB excise tax. There is a need for clearer, more transparent communication about tax implementation and its purpose.

Strengths and limitations

This study’s main strength is that it offers initial insights into Saudis’ views on the SSB tax and its effects. Its qualitative design provided in-depth information through interviews. Using TPB encouraged discussions of factors otherwise less explored, serving as a useful tool for examining dietary behaviour interventions, including SSB (27). Additionally, a sample of interview transcripts was independently coded by two researchers, which improved the rigour and credibility of interpretations (35).

The findings should be interpreted considering the study’s sample and setting. The use of university student volunteers, likely interested and highly educated, may not reflect the general public’s views. We aimed for a diverse sample across age, gender and specialities. The study was in Riyadh, Saudi Arabia’s capital, and residents’ perspectives may differ from other regions. In our study, telephone and Zoom interviews provided good data, and some found it easier to discuss sensitive topics like weight without fear of judgement. Face-to-face interviews can reveal non-verbal cues but may introduce social desirability bias, as participants might give socially acceptable answers.

Conclusions

This study examined public perception and attitudes toward SSB consumption and how a tax might influence young adults in Saudi Arabia. It found a lack of clarity about the excise tax and its necessity. The perception of taxation’s impact was linked to views on consumption. Health was seen as beyond personal choice. A comprehensive approach is needed to reduce SSB consumption, including promoting healthy alternatives and increasing acceptance of interventions. More transparent communication about tax implementation and purpose in Saudi Arabia is also essential.

Supplemental Material

sj-docx-1-ped-10.1177_17579759261445091 – Supplemental material for Perceptions of sugary drinks within the application of excise tax in Saudi Arabia: a qualitative study among undergraduate and postgraduate students

Supplemental material, sj-docx-1-ped-10.1177_17579759261445091 for Perceptions of sugary drinks within the application of excise tax in Saudi Arabia: a qualitative study among undergraduate and postgraduate students by Reem Alsukait, Noura Alomair, Badriyah Al-Mutairi and Samah Alageel in Global Health Promotion

Supplemental Material

sj-docx-2-ped-10.1177_17579759261445091 – Supplemental material for Perceptions of sugary drinks within the application of excise tax in Saudi Arabia: a qualitative study among undergraduate and postgraduate students

Supplemental material, sj-docx-2-ped-10.1177_17579759261445091 for Perceptions of sugary drinks within the application of excise tax in Saudi Arabia: a qualitative study among undergraduate and postgraduate students by Reem Alsukait, Noura Alomair, Badriyah Al-Mutairi and Samah Alageel in Global Health Promotion

Supplemental Material

sj-docx-3-ped-10.1177_17579759261445091 – Supplemental material for Perceptions of sugary drinks within the application of excise tax in Saudi Arabia: a qualitative study among undergraduate and postgraduate students

Supplemental material, sj-docx-3-ped-10.1177_17579759261445091 for Perceptions of sugary drinks within the application of excise tax in Saudi Arabia: a qualitative study among undergraduate and postgraduate students by Reem Alsukait, Noura Alomair, Badriyah Al-Mutairi and Samah Alageel in Global Health Promotion

Footnotes

Acknowledgements

The authors would like to thank all participants for their participation in this study.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Ethics approval and consent to participate

The King Saud University Human Research Ethics Committee reviewed and approved this study (Ref. E19 - 4382). The research is conducted in accordance with the principles embodied in the Declaration of Helsinki. Participants completed an informed consent form to participate in this study.

Consent for publication

Non applicable

Availability of data and materials

The datasets generated and analysed in this study are not publicly available because they contain individual informants, but they are available from the corresponding author upon reasonable request.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.