Abstract

Incumbent postal operators (POs) are particularly challenged with rapid technological developments and especially with digitalization which substitutes their letter mail, yet generally boosts parcel volumes. As a consequence, they have to rethink their strategy, especially for their post office network. The article presents potential strategies and discusses the main trends in postal network evolution among incumbent POs, focusing in particular on the examples of Australia, New Zealand, Switzerland, the United Kingdom, Italy, and the United States, and assesses these strategies against a set of key performance and development indicators.

Introduction

Incumbent postal operators (POs) face major challenges and opportunities, especially in light of technological progress. 1 Electronic communications, indeed, impact all POs’ businesses. Traditional letter mail can be and is being substituted by various electronic means. At the same time, POs benefit from growing e-commerce and see their parcel volumes rising despite the economic crisis in 2009. According to the International Post Corporation (IPC 2016), global parcel volumes have doubled between 2005 and 2015. Pitney Bowes (2016) forecasts volumes to grow at rates of 5–7% per year in the near future. POs have reacted differently to those changes in both the letter and the parcel segments of their business as well as in the development of their postal networks.

Many POs have improved end-to-end transit times, for example, by improving delivery times (Saturday delivery, Sunday delivery, evening delivery, selectable time slots) and (faster) delivery speed. Similarly, sender and recipient services have been improved as well (track and trace, collection at home, flexible delivery points, parcel lockers, returns, etc.). Furthermore, POs have developed their post office networks into different directions. Traditional post offices have often been replaced by agencies where basic postal services are provided at third-party retail outlets, notably grocery stores. Other measures include outsourcing or franchising of post offices to third parties and leveraging their post office infrastructure to enter new markets, for example, financial services, insurance services, or high-value retailing.

Incumbent POs have chosen different combinations of the measures mentioned above. Consequently, they are developing into different directions. For example, Poste Italiane has become a much diversified group with postal services accounting for less than 15% of revenues, whereas the US Postal Service (USPS) focuses on its traditional mail and parcel business. Those different developments and solutions are not the least attributable to differences in regulatory frameworks among countries.

This article explores the different options for a future post office network—POs’ post office network strategies—and qualitatively assesses its interplay with broad strategic orientations in the light of the POs’ regulatory background. It is structured as follows: The “Previous research” section provides a brief literature review of incumbents’ strategies. The “Current status and trends in post office development” section summarizes the current status and trends. The “Options for general strategic orientation and network development” section introduces the possible post office network strategies and gives an overview of different broad strategic orientations. The “Selected country studies” section discusses the situation in different countries by focusing on the incumbents’ strategic decisions and the regulatory framework. The “Analysis and conclusion” section concludes.

Previous research

Several authors have studied the strategies of incumbent POs before substitution, generally in the context of their liberalization. However, the literature is sketchy and especially weak when it comes to incumbent POs’ strategies vis-à-vis their post office network. The following section summarizes the few available papers on post office networks and the most important literature regarding general strategies.

Petrović (2006) recognizes the role of the state in influencing the strategies of incumbent POs by setting the regulatory framework in which they must operate. Buser et al. (2008) discuss the role of the post office in the marketplace and aim to contribute to a better understanding of post office network optimization and to identify key strategic issues in light of the regulatory framework. Bailly and Meidinger (2013) conclude that in view of the decline in the traditional core business of incumbent POs, diversification is the best way forward to find new sources of revenue and guarantee their sustainable economic development. Greening et al. (2013) analyze the options of POs to enter the area of telecommunications as a natural complement to the traditional postal business and briefly compare the strategies of different POs in this field.

In 2012, the IPC and the Boston Consulting Group published a report on the future perspectives of the postal sector, indicating that building a new compelling position for incumbent POs requires many fundamental changes and that POs need to move from an evolutionary to a revolutionary transformation in order to face the revenue decline resulting from increased substitution and to seize the window of opportunity in e-commerce.

More recently, the Universal Postal Union (2014) published a book on development strategies for the postal sector in which it considers specific features of postal markets in developing countries and traces the emergence of new legislative and regulatory frameworks in sub-Saharan Africa. The book also presents the role and strategies of post offices in the delivery of basic financial services to all citizens. Additionally, the authors state, quite optimistically in our view, that exploring and making growing use of big postal data, particularly at the international level, will empower postal stakeholders, enabling them to take control of the future of the postal sector, unleash untapped potential, and reinvent postal services for the 21st century.

Borsenberger (2014) argues that accessibility and proximity in connection with the postal universal service obligations (USO) should also contain a “virtual” dimension regarding progress in information and communication technologies. Online services which complement and extend physical postal services might be a solution to reduce the economic and social costs of the USO.

Jaag et al. (2016) explore various approaches to network development by means of selected case studies as well as by an overview of performance indicators. Such indicators reveal particularly successful strategies, namely, the ones that leverage infrastructure, reputation, and competencies. Based on these results, generic strategies are derived. Special attention is paid to the legal and regulatory environment that critically affects the POs’ abilities to adopt successful business strategies.

Current status and trends in post office development

To recall, the post office network performs various functions: As a physical infrastructure, it serves to collect and deliver mail items (letters and parcels) and it constitutes the main tool for cash transactions. Additionally, it is the posts’ main sales channel and the POs’ most important customer interface. The post office network is complemented by a broad range of other access points such as mailboxes, unattended parcel machines, delivery services as well as websites and social media. The postal network is of particular importance in rural areas. Boldron et al. (2008) show that in France, services such as pharmacies or bank branches are less accessible than postal offices. Further, the authors argue that postal services generate positive demand externalities and spillovers for commercial services that lead to further development of the local economy as well as to growth of wealth and population living in the region (Bernabdelmoumène and Borsenberger, 2014; Boldron et al., 2008).

NERA (2009) and Ellison et al. (2016) discuss another aspect expressing the social importance of the postal network. They find that customers’ willingness to pay for the existence of a post office as a whole exceeds their willingness to pay for the sum of the individual services provided by it. The additional willingness to pay for the postal network itself can have several reasons: For example, it could be due to the fact that it “binds the nation together” (Boldron et al., 2008) or it could be related to the attributed importance of the public service function of the postal network.

Originally, the post office network was set up to handle physical postal services. Is it still up to this task and, more importantly, is it still necessary for doing so? Indeed, today there are already more cost-efficient alternatives for the collection and delivery of mail items. Parcel drop-off and pick-up locations are relevant examples (Royal Mail, 2016). In some countries, cash transactions have become the main rationale for continuing to operate traditional postal offices. Borsenberger (2014) reports that changes in postal services usage have induced a decline in over-the-counter activities. In 2000, around 28 million British customers visited postal branches each week. By 2006, this number has fallen to 25 million, and by 2013, it stood at just under 20 million. Likewise, customer visits to USPS brick-and-mortar locations are decreasing rapidly: Whereas there were 1.26 billion customer visits at USPS points of sale in 2003, this number fell to 877.4 million in 2016 (US Postal Service, 2017). In Switzerland, the mail and parcel volumes handled over counters in the postal retail network have declined by 65% and 46%, respectively, over the 2000–2016 period. Over the same period, cash transactions have declined by 40% (Swiss Post, 2017a).

Consequently, POs have strongly transformed their networks and will continue to do so. A general trend in post office development is the replacement of traditional post offices with postal agencies. For example, Swiss Post forecasts that its network size will increase from 3700 to 4200 access points over the 2016–2020 period (Swiss Post, 2017b). The decrease in the number of traditional post offices, which is expected to fall from 1400 to around 800 by 2020, will be offset by the rapid growth of 24-hour-a-day locations (such as myPost24) and business customer points, which are expected to nearly double in numbers over the same period. Thus, post office networks may undergo transformation in the future rather than being replaced or abolished altogether. This view is supported by the results of a study conducted by the Office of Inspector General (2017). Interestingly, their study shows that millennials visit post offices more often than older generations. However, they differ in how they use post offices: Millennials check post office boxes and pick up free shipping material more frequently than older generations, but they complete counter transactions less frequently.

The transformation of traditional post offices into agencies is implemented either by franchising or by outsourcing. Consequently, the PO no longer owns its network. In addition to lower costs for the PO, the advantage of such agencies is that they are much closer to customer needs than the traditional post offices, notably in terms of location (closer to the customers, whereas traditional post offices’ locations date from the period even before the Second World War) and opening hours. However, the development could also come with negative consequences from a social point of view. For example, in some rural areas where other shops have closed, postal offices represent the last remaining physical retail points.

The pace and the very nature of this transformation is determined by the regulatory environment. As will be shown in section “Selected country studies”, many incumbent POs fulfill a USO and/or offer services of general economic interest (SGEI). The extent of these regulations has an impact on the degree of commercial freedom that is given to the incumbent POs.

Not only is the organizational form part of this profound transformational process but also the product range. Typically, the product range offered at the post office has been expanded to nonpostal products (financial, telecom, government). But again, the nature of the products offered is chiefly determined by the regulatory environment or the degree of commercial freedom of the incumbent, respectively.

In terms of the financial burden of operating a dense network, there exists a big variety among incumbents, owing mainly to the incumbent’s commercial freedom which is determined by the institutional framework (especially, ownership and regulation). This will be illustrated in section on “Selected country studies”.

Overall, the challenges are different for the incumbents having full commercial freedom and the ones who do not (ownership and regulatory constraints). Business models of incumbent POs are strongly affected by their regulatory framework (see Petrović, 2006). For those with full commercial freedom, challenges mainly pertain to optimal network design as a combined function of customer demand and network costs. For those without full commercial freedom in terms of numbers and ownership of access points as well as product range offered at these points, challenges are primarily political and regulatory in nature. We will focus exclusively on the latter ones in this article.

Options for broad strategic orientation and post office network development

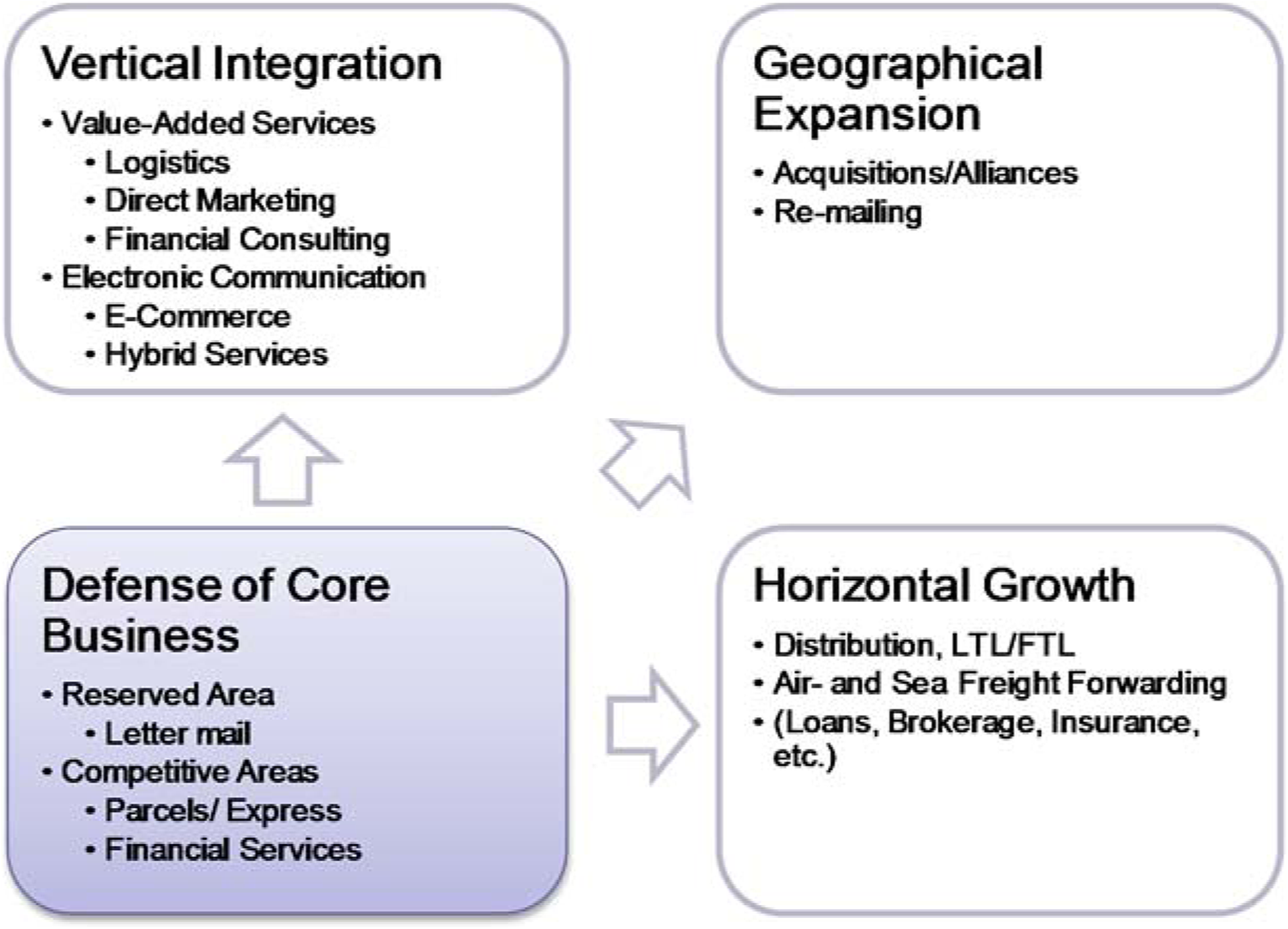

POs have three options to cope with changes in demand for their core products: downsize their operations; defend their core business through product and price differentiation as well as value-added services; or modify or even transform their business model beyond their core business and thereby react more aggressively.

Given the importance of network effects and the cost structure of POs (high fixed costs, low marginal costs), the first of the above options is not economically viable and may result in a vicious circle (e.g. Jaag and Dietl, 2011). The second option, defending the core business, implies an extension of the existing value chain. This likely improves customer retention, spurs demand, and thereby creates additional revenues provided that the new product or service satisfies the consumer needs.

For a more aggressive transformation strategy, there are basically three directions starting from the core business, as indicated in Figure 1. Operators can expand vertically, horizontally, and/or geographically. According to the resource-based view of strategic management, a PO’s strategy has to take the existing resources and capabilities into account. These comprise (besides access to every household, brand reputation, trust, and delivery know-how) especially the postal network. How can POs leverage and develop these resources and capabilities?

Business model transformation. Source: Adapted from Waller (2002). See also Jaag and Dietl (2011).

In section on “Selected country studies”, we will present the concrete evolutions and strategies of six important incumbent POs. All their broad strategic orientations constitute different ways to react to digitalization and thus to a changing demand for their core products.

At least three equally valid broad strategic orientations can be distinguished: provide physical infrastructure, serve as a hybrid intermediary, or exclusively provide digital services.

Post as a physical infrastructure provider: As a physical infrastructure provider, the PO sells network access to various types of service providers, both postal and others. Its strong position in postal markets and its community function make PO entities an interesting platform for a broad range of services and products. The PO leverages its market position in postal services and its function as a community hub to provide physical infrastructure access. As such, the PO benefits from a solid reputation and trust, generally thanks to its local presence. However, the PO limits itself to defending its core business.

Post as a hybrid intermediary: As a hybrid intermediary, the PO manages the discontinuity between the physical and the digital world. Digital services often require some form of physical interaction. A typical example where physical attributes need to be digitized are identification processes. In addition, the hybrid intermediary may produce verified physical objects of digital values or vice versa. Examples include official documents, passwords, or valuables. These services might be provided through physical infrastructure, building again on its geographical presence and customer interfaces. This broad strategic orientation is an example of vertical integration.

Post as a pure digital services provider: The PO shifts to an entirely digital business, for example, by providing e-government services such as eVoting or eHealth. As such the PO builds on the reputation from its physical infrastructure and geographical presence, but gradually moves from the physical postal network to a digital one. This broad strategic orientation is an example of horizontal growth or transformation.

These broad strategic orientations are closely related to the incumbent PO’s ability to transform its post office network, which in turn depends on its political and regulatory constraints as well as on market conditions (e.g. bargaining power of suppliers and buyers).

The incumbent has basically four strategic options to develop its postal network under regulatory constraints. These post office network strategies are:

Network development: The first post office network strategy consists of pursuing (to the extent possible) the same path as the incumbents which enjoy commercial freedom, that is, to replace post offices with agencies or other access points and extend the product range. This implies that their infrastructure needs to be optimized. Under this option, the aim is to gradually reduce the cost of the post office network to the point it becomes fully aligned with the commercial business of the firm.

Network as a commercial service: The second post office network strategy entails the use of existing infrastructure to offer other commercial (nonpostal) products and services. The strategy encompasses the development of products and services that can best be provided through the existing post office network. The strategy is only reasonable if the PO is not able to optimize its post office network, for example, due to legal restrictions. Otherwise “network development” would be a superior strategy.

Network as a government service: The third post office network strategy follows the idea of transforming the post office network into a network for government services and other government-related activities. This strategic option means that government is ready to subsidize or otherwise support the incumbent PO’s post office network so as to make it (somewhat) financially viable.

Handover to government: The fourth post office network strategy consists of isolating the post office network from the rest of the firm (full unbundling) and handing it over to government both in terms of ownership and operations.

The common prerequisite for each of these four options is government support, which of course varies from country to country.

Selected country studies

This section presents illustrative examples from the following six countries: Australia, New Zealand, Italy, the United Kingdom, Switzerland, and the United States. Each of these countries has chosen a somewhat different regulatory framework for postal strategy development. As a result, these country studies represent a wide range of possible network development approaches. The key performance and development indicators concern the size and composition of the network of physical access points, and the development of the POs’ core business (letter and parcel mail) relative to their entire business and their profitability.

Australia Post

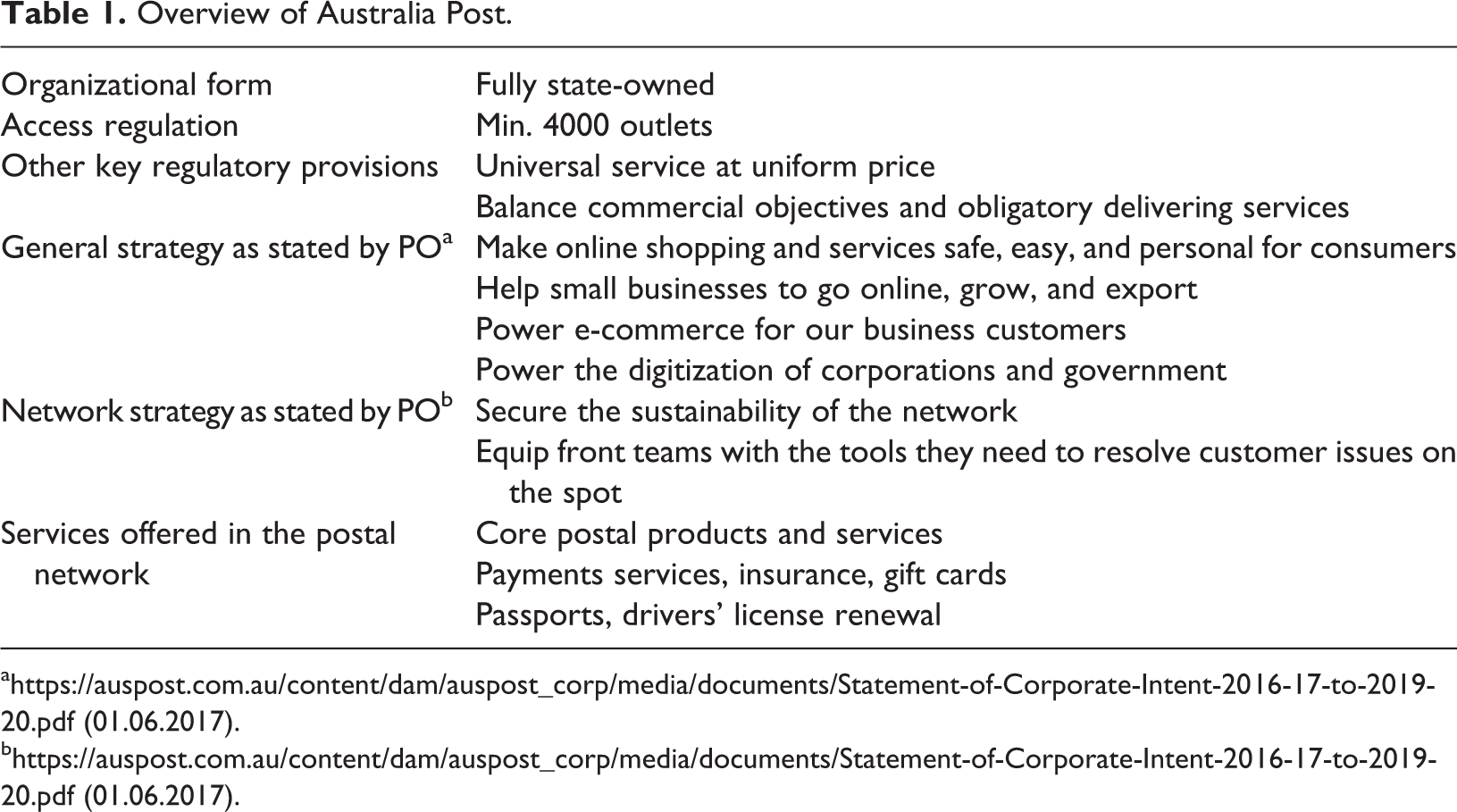

Australia Post is the incumbent PO in Australia and is a government business enterprise, fully owned by the Commonwealth of Australia. As prescribed by the Australian Postal Corporation Act, Australia Post must provide a universal letter service at a single uniform rate (uniform tariff) on an equitable basis. Moreover, the universal service provider (USP), designated by the law, is required to maintain a minimum of 4000 outlets (i.e. post offices or agencies), of which at least 50%, but not fewer than 2500, must be in rural or remote areas. Moreover, the Australia Post is to maintain a network of at least 10,000 letter boxes and provide a mail collection point at each retail outlet (Howard, 2015; Jaag et al., 2016).

To offset the strict regulatory framework in which the Australia Post operates, it is given a monopoly in the carriage and delivery of letters, as well as an exclusive right to issue postage stamps.

The strategy for the “postal services” segment is to implement changes that secure the sustainability of the regulated mail services business, such as increasing the basic postage rate or continue to increase the number of providers that sign to use the Digital Mailbox. 2 The strategy for the “Parcel Service” segment is to create a world-class multichannel parcel and freight business to harness the growth in online shopping and e-commerce, by, for example, integrating Australia Post and StarTrack 3 to create a logistics provider that serves both business and consumer markets with a broader range of delivery services (Australian Post, 2016). In this co-branded form, Australia Post benefits both from the trust related to its brand and from the B2B success of the StarTrack brand. The creation of more such co-brandings is stated as an aim by Australia Post (2016a).

Besides the co-branding strategy, the focus is on technological development. For consumers, it is possible to perform many tasks online, such as paying bills, ordering foreign currency, and managing place and time of parcel collection (Annual Report, 2015). This business strategy is to be further reinforced.

Australia Post is still profitable. According to the Financial Report 2016, the profit before taxes was always positive, but in the fiscal year 2015/2016, the amount was only Australian $41 million (compared to the period 2011/2012, where it was at Australian $366.7 million). This caused a negative impact on average operating assets of −8.2%. The loss is due to the accelerated decline in the letter business. The total number of access points was slightly reduced between 2006 and 2016. However, there was a clear shift from corporate offices to community postal agents. Licensed post offices (LPOs) may be run solely as a post office or in conjunction with another business, such as a news agency or convenience store. LPOs must offer a range of Australia Post products and services including mail acceptance and processing, postage stamps, money orders, bill payment, and banking. They may also offer additional products and services including philatelic items, packaging products, stationery, gifts, and post office boxes. Community postal agencies can offer varying mail and postage services. At a minimum, they offer basic postage assessment, stamp sales, and over-the-counter mail acceptance and delivery. They do not offer financial services such as bill payment and banking. Table 1 gives an overview of Australia Post.

Overview of Australia Post.

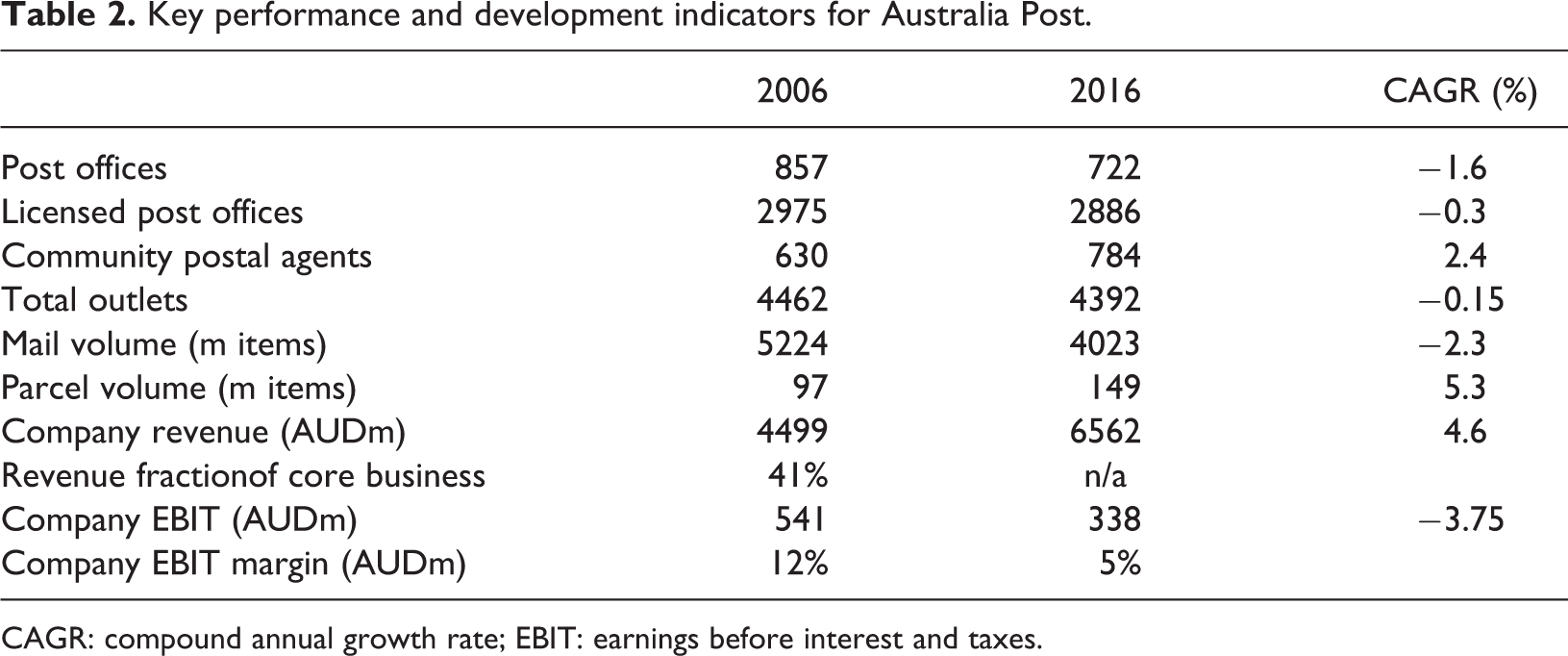

Table 2 shows that Australia Post has been able to grow at an average yearly rate of 4% between 2006 and 2016. However, its earnings before interest and taxes (EBIT) margin has decreased from 12% to 5% during that period of time.

Key performance and development indicators for Australia Post.

CAGR: compound annual growth rate; EBIT: earnings before interest and taxes.

With its broad range of services offered and an almost constant number of postal outlets, Australia Post adopted the post office network strategy “network as a commercial service” to some extent. However, it also follows the strategy “network development” as numerous post offices have already been converted into agencies.

New Zealand Post

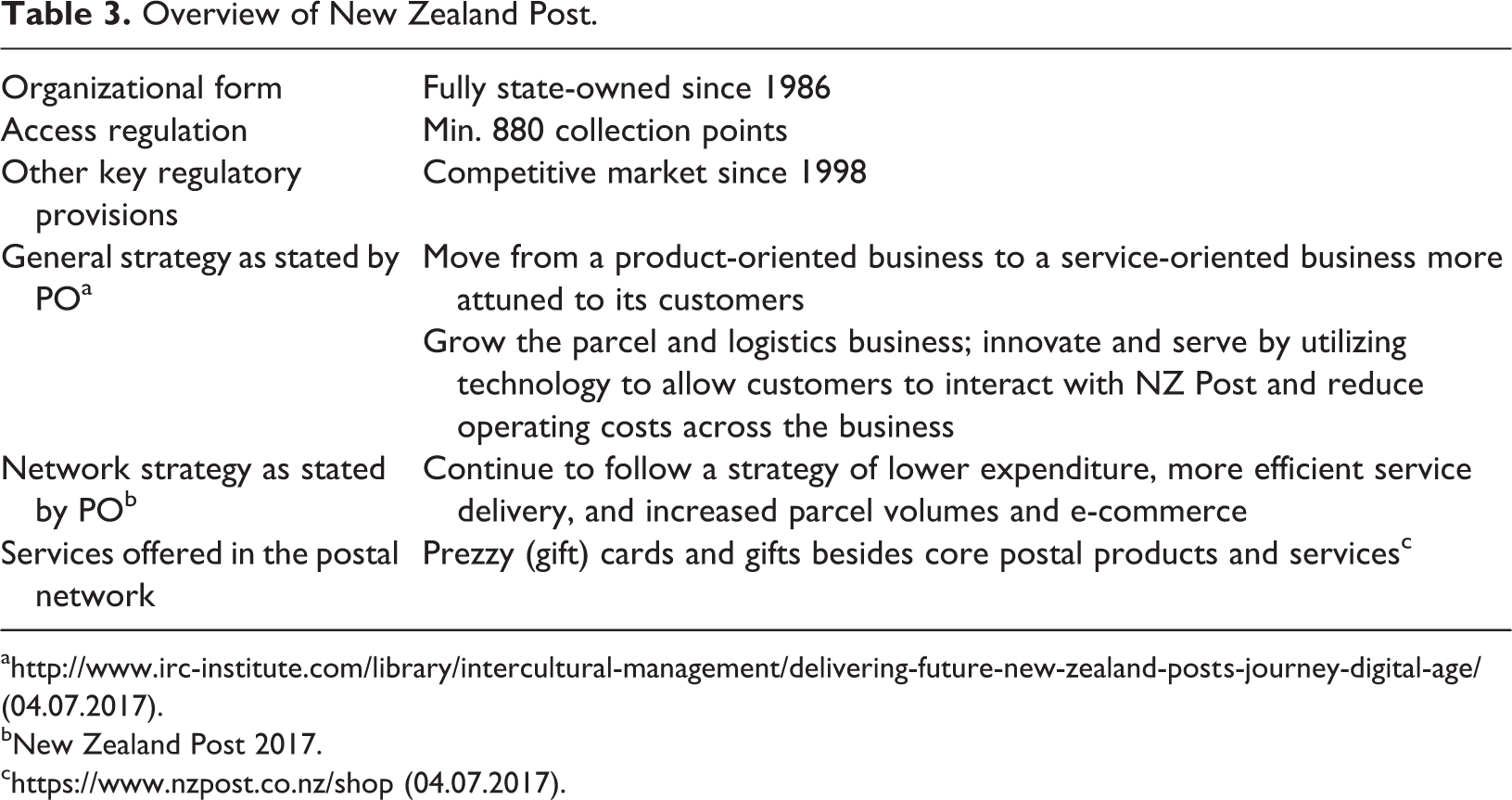

Since 1986, New Zealand Post is a fully state-owned enterprise that is held by the Minister of Finance and the Minister of State-Owned Enterprises and acts as a USP. However, it is not the only player on the market. Competition on the postal market has been permitted since 1998. Since then, about 25 providers take part in the market and there is rather a fierce competition. The USO in New Zealand is defined in the deed of understanding as between the Minister of Communications and Information Technology and the New Zealand Post Group (1998). The USP must operate a minimum of 880 collection points of which at least 240 must provide personal assistance (e.g. postal offices).

In November 2013, the New Zealand Post Group published a five-year strategy. Similar to Australia Post, one of the strategies pursued by New Zealand Post is the utilization of the existing capacities. Similar to Australia Post, the New Zealand Post aims at strengthening its position in financial services. New Zealand Post service offerings are increasingly colocated within a host business. This promises both greater convenience and longer opening hours (New Zealand Post Group, 2013).

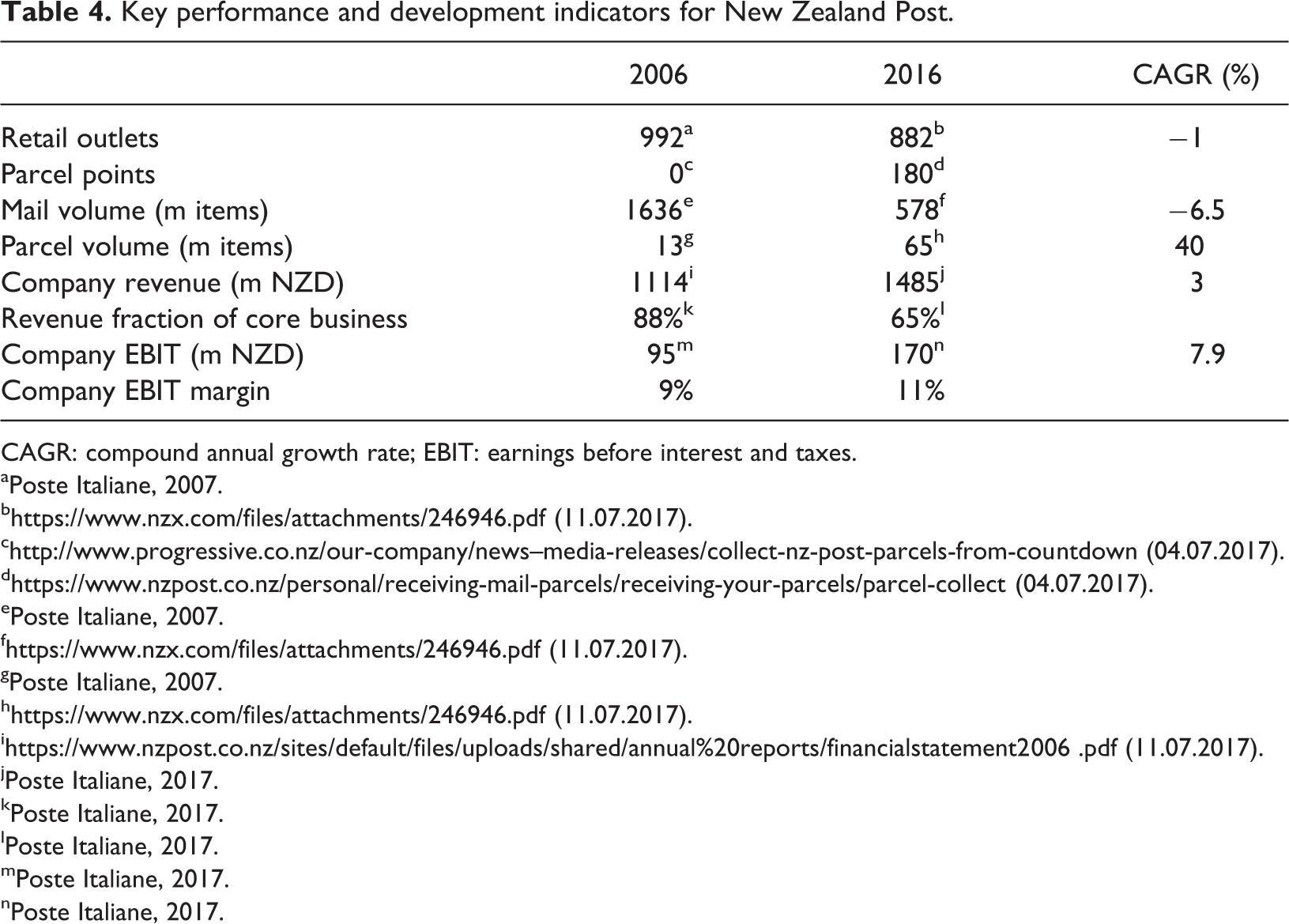

Tables 3 and 4 give an overview of New Zealand Post’s development and performance. The total number of retail outlets (consisting of corporate and franchise PostShop stores as well as PostCentre outlets) has been reduced by only about 1% per year. New Zealand Post’s strategy is a mix between benefiting from the existing postal network and yet transforming it in light of technological change. For example, it furnished 3200 post offices with free Wi-Fi, introduced a new queue management system in more than 1700 offices, and established 23 multi-language counters (New Zealand Post Group, 2016). In addition, New Zealand Post has established new parcel points to benefit from increasing e-commerce. Hence, New Zealand Post pursues the post office strategy “network development.” This resulted in a strong increase in parcel volumes which compensated for the decline in mail volumes.

Overview of New Zealand Post.

ahttp://www.irc-institute.com/library/intercultural-management/delivering-future-new-zealand-posts-journey-digital-age/ (04.07.2017).

bNew Zealand Post 2017.

chttps://www.nzpost.co.nz/shop (04.07.2017).

Key performance and development indicators for New Zealand Post.

CAGR: compound annual growth rate; EBIT: earnings before interest and taxes.

aPoste Italiane, 2007.

bhttps://www.nzx.com/files/attachments/246946.pdf (11.07.2017).

chttp://www.progressive.co.nz/our-company/news–media-releases/collect-nz-post-parcels-from-countdown (04.07.2017).

dhttps://www.nzpost.co.nz/personal/receiving-mail-parcels/receiving-your-parcels/parcel-collect (04.07.2017).

ePoste Italiane, 2007.

fhttps://www.nzx.com/files/attachments/246946.pdf (11.07.2017).

gPoste Italiane, 2007.

hhttps://www.nzx.com/files/attachments/246946.pdf (11.07.2017).

Between 2006 and 2016, the fraction of revenues from its letter and parcel business decreased from 88% to 65%, while the company’s EBIT margin increased from 9% to 11%.

Overall, New Zealand Post’s business and network strategy has so far been successful in coping with the declining mail volumes by aiming to reduce the costs and allow post offices to cater to customer needs. New Zealand Post follows the post office network strategy “network development” in our framework.

Poste Italiane

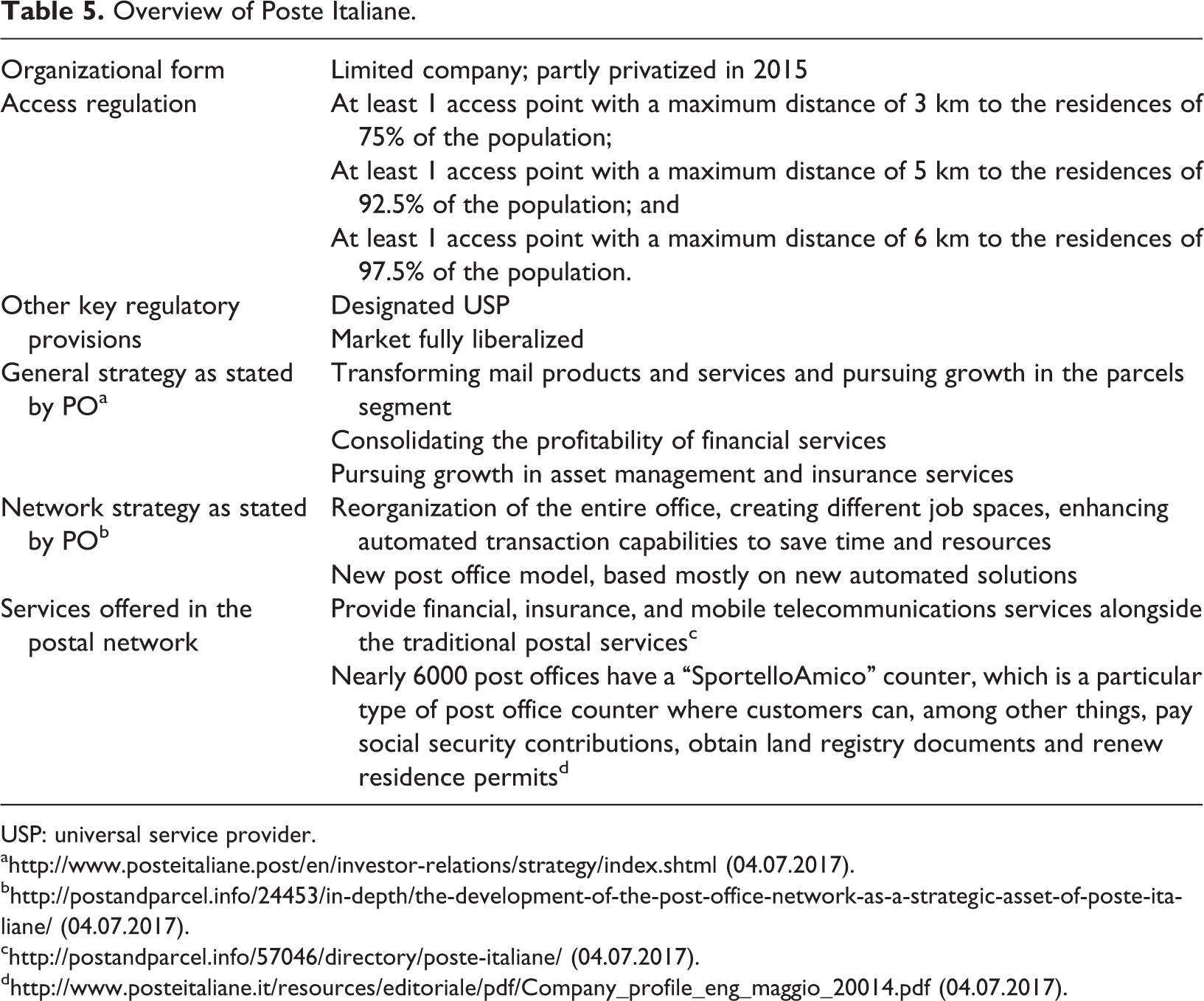

Poste Italiane is a limited public company divided into four operating segments (postal and business services, financial services, insurance services, and other services). Until 2015, it was a fully state-owned company. At the end of 2015, 35% of assets were sold to private investors (Reuters, 2017). Poste Italiane is still Italy’s designated USP. It must ensure that 92.5% of the population has an access point at a distance of less than 5 km from their residence. It is obligated to deliver within a five-days-a-week frequency (with some exemptions for barely inhabited areas).

The mission of Poste Italiane is to consolidate its role as a global operator; drive the development of communications, payment, and logistics solutions; improve the different services provided; and create opportunities for Italy. One of the strategic objectives of Poste Italiane in the “Postal and Business Services” market is to position itself as a provider of high-quality business mail services, providing new shipping and delivery solutions. For letters, however, Poste Italiane tries to achieve relaxations regarding the number of delivery days.

In 2000, Poste Italiane set up new value-added services, integrating its clients’ business processes with its own postal and financial services to move into the role as a government service provider (Del Callo, 2014). The main new services provided to Italian citizens through Poste Italiane include integrated notification services managing the entire government official communications process, and the management of immigration permission requests. On behalf of government agencies and third-party utility companies, the post office also became a single point of contact for citizens to manage administrative issues (e.g. passport requests/renewal).

Poste Italiane aims to further diversify its product range, its position in the account and payment systems market, as well as its position in the insurance market. The business unit “Poste Vita,” dedicated to insurance services, has developed very successfully and accounted for over 60% of group revenues in 2013 (Poste Italiane, 2015). 4

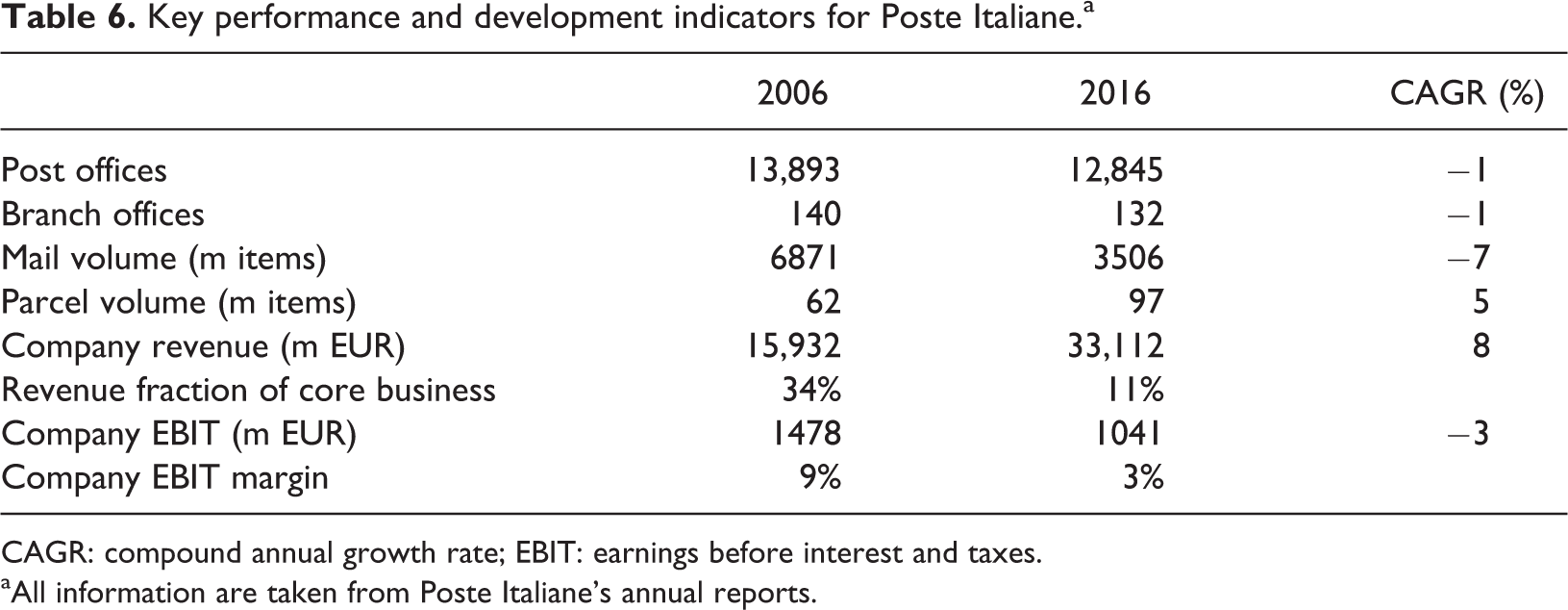

Between 2006 and 2016, the number of both post offices and branch offices (agencies) was reduced only slightly. Poste Italiane was able to strongly increase its revenue through diversification: while the fraction of its core letter and parcel business accounted for one-third of its total revenue in 2006, this fraction declined to one-tenth in 2016. As a result of the strong decline in mail volumes, the company’s profit margin decreased from 9% in 2006 to only 3% in 2016.

Tables 5 and 6 give an overview of Poste Italiane’s development and performance. Compared to other countries, there is a very strict mandate to operate a dense postal network. The postal network currently includes 12,845 post offices and 141,246 employees (Poste Italiane, 2016a). In accordance with its business strategy, Poste Italiane is undertaking investments of €3 billion. The investment is targeted to enforce infrastructure and digital platforms as well as training hours, the aim being to foster the convergence among mail, financial, and logistical platforms (Serafini, 2014). There was further investment in the development of advanced solutions relating to the public system for digital identity management and in implementing the full acquiring service for all the main debit and credit cards. However, the actual company profile states clearly that mail, parcel, logistics, and courier services are important parts of Poste Italiane’s identity. Therefore, Poste Italiane strives for optimizing core services by complementing them and offering them on both physical and electronic platforms (Poste Italiane, 2016a).

Overview of Poste Italiane.

USP: universal service provider.

bhttp://postandparcel.info/24453/in-depth/the-development-of-the-post-office-network-as-a-strategic-asset-of-poste-italiane/ (04.07.2017).

chttp://postandparcel.info/57046/directory/poste-italiane/ (04.07.2017).

Key performance and development indicators for Poste Italiane.a

CAGR: compound annual growth rate; EBIT: earnings before interest and taxes.

aAll information are taken from Poste Italiane’s annual reports.

Poste Italiane provides in its post offices various nonpostal and governmental services. In our classification framework, Poste Italiane is therefore an example for both post office network strategies “network as a commercial service” and “network as a government service.”

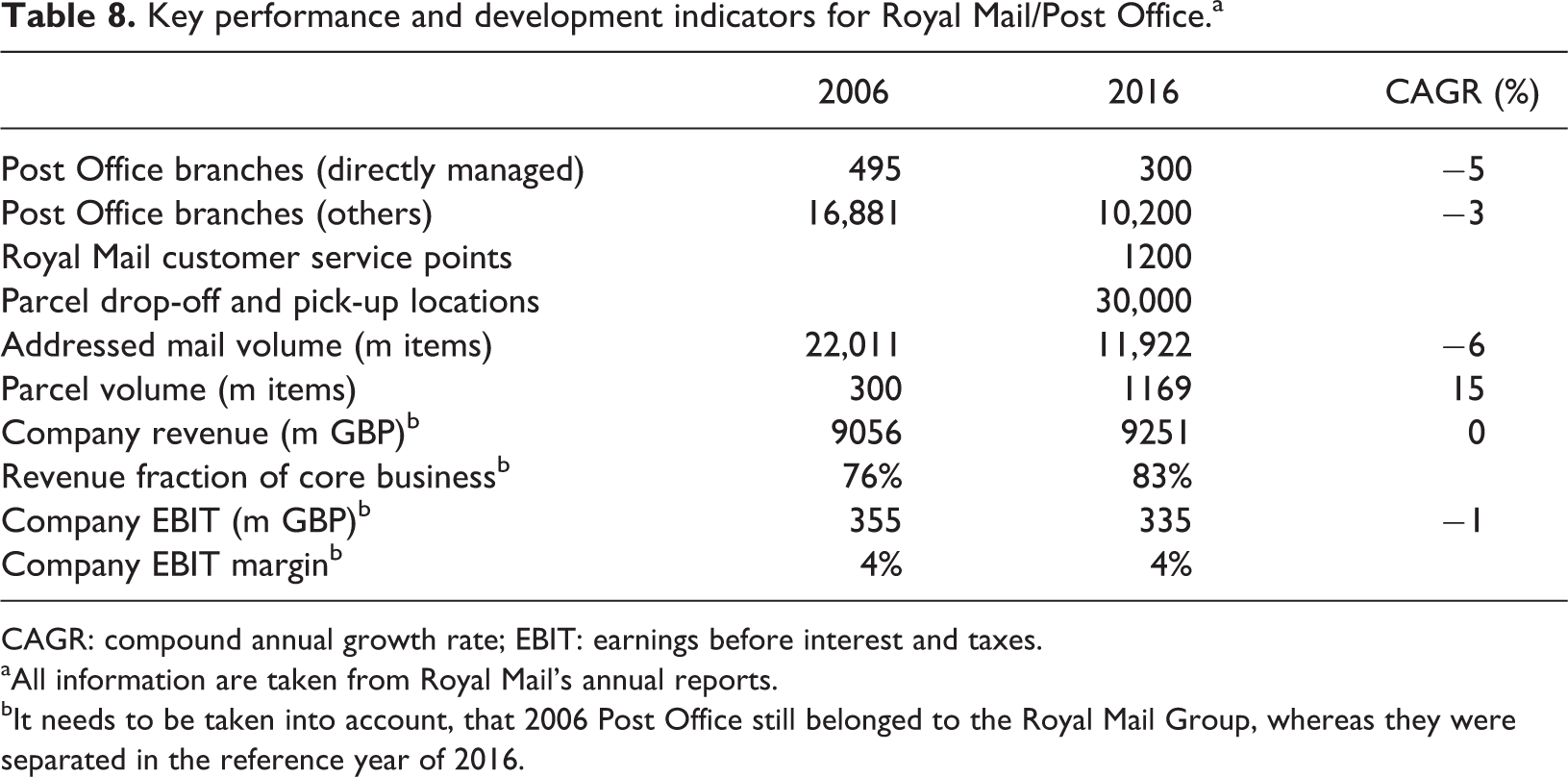

Royal Mail/Post Office

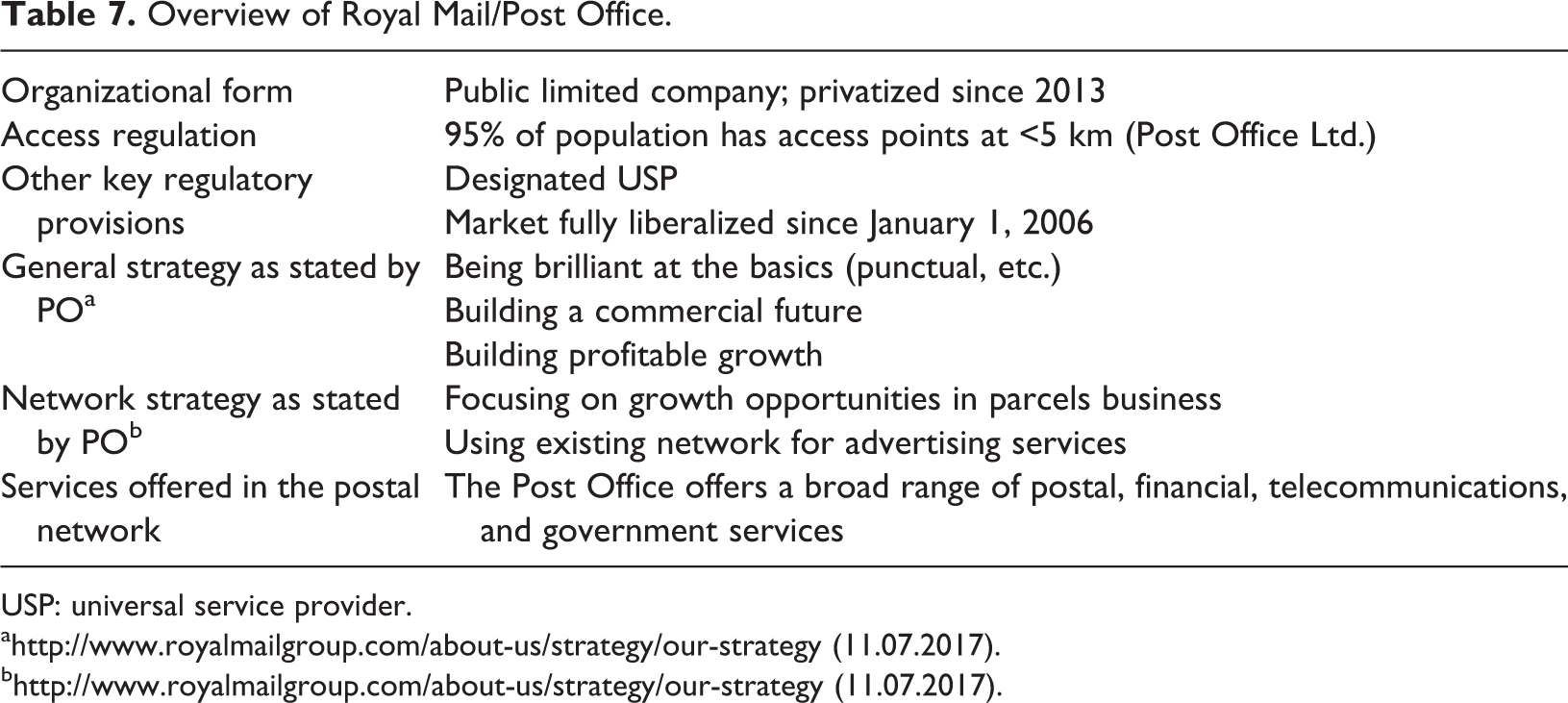

Royal Mail Group Ltd is a limited company owned by the government of the United Kingdom (30%), the company employees (minimum required by law of 10%), and private investors (60% free float). It is designated as the USP. 5 The UK Postal Services Act of 2011 defines the USO requirements for Royal Mail. Letters have to be collected at every access point and must be delivered within 6 weekdays, and parcels within 5 weekdays. Public prices for a postal service must be affordable and uniform. However, most access points are not operated by Royal Mail, but by Post Office Limited. The two former sister companies were separated when the Postal Services Act took effect in 2011. Since then, Post Office Limited is independent of Royal Mail and fully owned by the government. Post Office must guarantee that at least 95% of users are located within 5 km of an access point, capable of receiving the largest relevant postal packages and registered mail and fulfill other regulatory requirements.

Royal Mail is bound to the regulatory requirements described but has no reserved area. The postal market has been fully opened on January 1, 2006. Royal Mail had to adapt its business strategy for being able to stay competitive. It admitted that during several decades, there had been an underinvestment. The only possibility to catch up with their competitors was seen in modernizing the equipment and educating the employees in a way that allowed them to work more efficiently (Royal Mail Holdings, 2007). Since 2002, Royal Mail has increased the prices of first- and second-class stamps for regular letters (up to 100 g) considerably. 6

The vision of Royal Mail is to be recognized as the best delivery company in the United Kingdom and across Europe, by sustaining the continued provision of the universal service in the United Kingdom and by generating sustainable shareholder value.

In 2016, nearly 80% of all citizens are at most 1 km away from the next access point (Royal Mail, 2016). As of 2016, the network consists of 11,700 access points, out of which 10,500 are Post Office branches and around 1200 are Royal Mail customer service points (Royal Mail, 2016). Post Office Ltd. directly manages 283 post office branches. The majority of other branches are either run by various franchise partners or local sub-postmasters or operators, as “sub-postoffices.” Within the whole United Kingdom, there are also 30,000 parcel drop-off and pick-up locations (Royal Mail, 2016). Even though it is strongly declining, the letter market still accounts for about 60% of all revenues (Royal Mail, 2016).

The Post Office has a wide variety of services throughout the network of branches including five categories which are considered by the EU as SGEI, namely, (1) processing social benefit and tax credit payments to the public, (2) processing of national identity and licensing scheme applications, (3) universal payment facilities for public utility services, (4) access to postal services, and (5) universal access to basic cash and banking facilities and government savings instruments, especially for rural customers and those on social benefits (Department for Business Innovation & Skills, 2015). Products and services available vary throughout the network; main post offices generally provide the full range of services. The services offered include postal items and payment on behalf of the two collection and delivery divisions of Royal Mail Group, Royal Mail and Parcelforce. Postage stamps are sold, while applications for redirection of mail are accepted on behalf of Royal Mail. The Post Office (acting as an appointed representative and credit broker) also provides credit cards, current accounts, insurance products, and mortgages since 2015. Personal banking services are offered on behalf of a number of partner banks. These include cash withdrawals, paying in cash and checks, balance inquiries, and check encashment. Some post offices also have cash machines. The Post Office also operates as a provider of a home landline telephone service and has recently added broadband Internet to its portfolio. A passport check and send service is available for passport applications. Other services include lottery games and scratch cards, foreign currency exchange, and sales of gift cards.

Tables 7 and 8 give an overview of Royal Mail’s and Post Office’s development and performance. Since its privatization in 2013, Royal Mail has a strong commercial focus. While Royal Mail’s mail volume has decreased by 6% on average between 2006 and 2016, its parcel volume has strongly increased by 15% per year. As a result, company revenue stayed about constant while EBIT has only slightly deteriorated.

Overview of Royal Mail/Post Office.

USP: universal service provider.

ahttp://www.royalmailgroup.com/about-us/strategy/our-strategy (11.07.2017).

bhttp://www.royalmailgroup.com/about-us/strategy/our-strategy (11.07.2017).

Key performance and development indicators for Royal Mail/Post Office.a

CAGR: compound annual growth rate; EBIT: earnings before interest and taxes.

aAll information are taken from Royal Mail’s annual reports.

bIt needs to be taken into account, that 2006 Post Office still belonged to the Royal Mail Group, whereas they were separated in the reference year of 2016.

With the separation of the Post Office network, the development of the UK post office network can be considered a partial example of the post office network strategy “handover to government.”

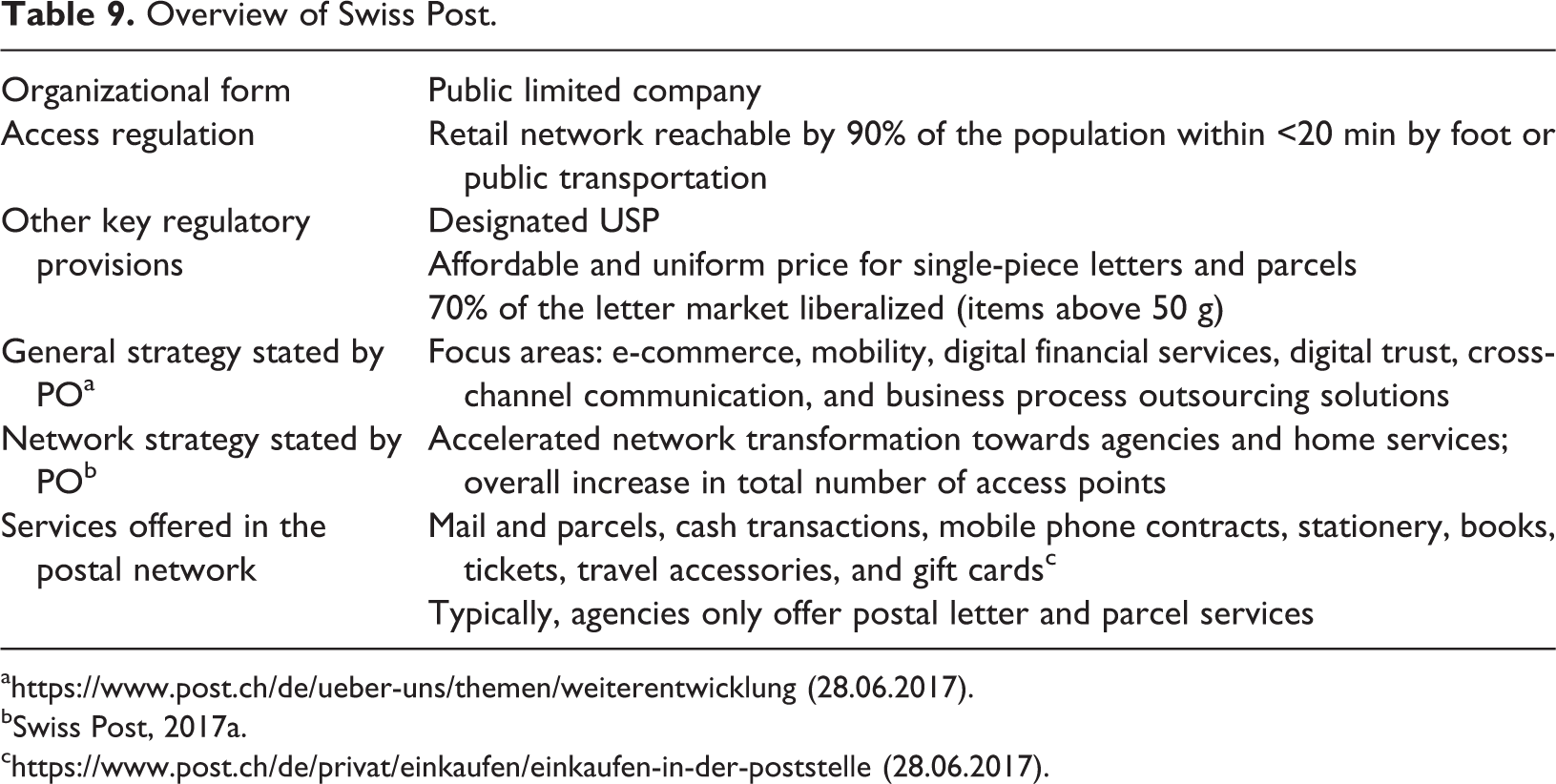

Swiss Post

Swiss Post is a public limited company under special law and acts as the designated USP. It is fully owned by the Swiss state. Revenues from the residual monopoly on domestic letters up to 50 g are one pillar for Swiss Post’s financing of the universal service.

In Switzerland, the USO includes the daily conveyance of addressed letters and parcels, newspapers and magazines, and outbound international letters, as well as the provision of basic financial services such as bank accounts. Moreover, Swiss Post must ensure that its retail network can be reached by 90% of the population within 20 min by foot or by public transport (see also Jaag and Maegli, 2015).

The vision of Swiss Post is to be “simple yet systematic” and connect the physical and digital worlds, setting new standards with its products and integrated solutions, as well as making it easier for its customers to operate in today’s complex environment. Swiss Post is focusing on maintaining and increasing the value of the company and on achieving industry-standard returns in all markets (communication, logistics, financial services, and passenger transport). It experiences a moderate decrease in income due to lower mail volumes and aims to further tailor its services to the needs of its retail customers.

Besides its core business, Swiss Post is a leader in the provision of secure electronic signatures, eHealth and eVoting services, and business process outsourcing, which is representative for the broad strategic orientation as a “Hybrid Intermediary.” In 2016, the Swiss postal network consisted of approximately 3800 access points. It intends to increase this number up to 4200 access points by 2020. The composition of the planned network is as follows: between 800 and 900 access points are in-house operations (regular post offices) and between 1200 and 1300 post agencies are run together with partners. Another 500 to 700 are complementary service points such as self-service terminals. The remaining 1300 are areas with home delivery services (Swiss Post, 2017b). The main objective behind this network enlargement consists in personalizing and individualizing the postal services for being able to use the network optimally. The services offered in regular post offices include mail and parcels, cash transactions, mobile phone contracts, stationery, books, tickets, travel accessories, and gift cards.

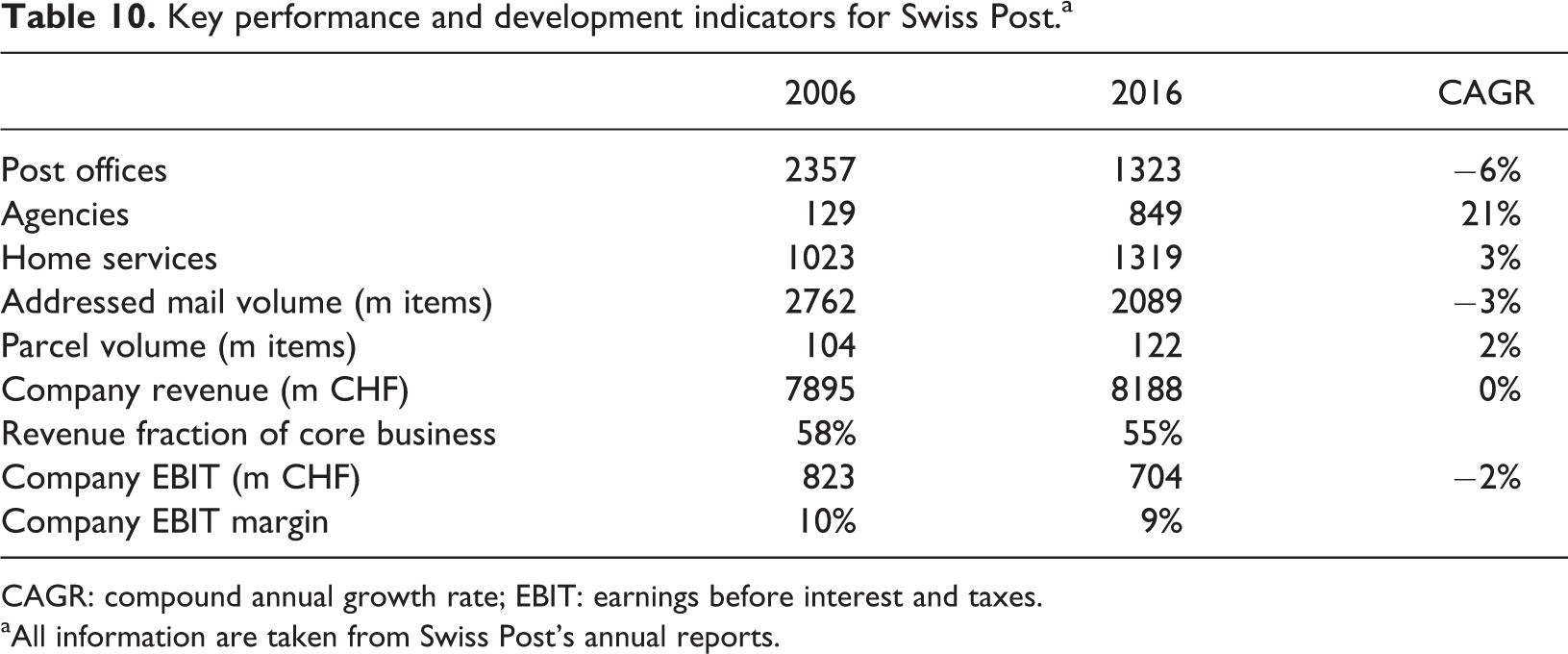

Tables 9 and 10 give an overview of Swiss Post’s development and performance. As a result of regulation and political pressure, Swiss Post operates one of the densest postal networks. Over the years, it has diversified in a broad range of services offered and complemented its physical network by a large online store. Recently, it has started consolidating and better structuring its product range.

Overview of Swiss Post.

ahttps://www.post.ch/de/ueber-uns/themen/weiterentwicklung (28.06.2017).

bSwiss Post, 2017a.

Key performance and development indicators for Swiss Post.a

CAGR: compound annual growth rate; EBIT: earnings before interest and taxes.

aAll information are taken from Swiss Post’s annual reports.

Thanks to its diversification and a moderate decline in mail volumes, Swiss Post was able to maintain its revenues while slightly reducing the fraction of its core mail and parcel services in total revenue. However, the company’s profitability has decreased by 2% per year between 2006 and 2016.

Swiss Post focuses on cost reductions by replacing post offices with agencies or other access points. Therefore, Swiss Post follows the post office network strategy “Network development” in our framework.

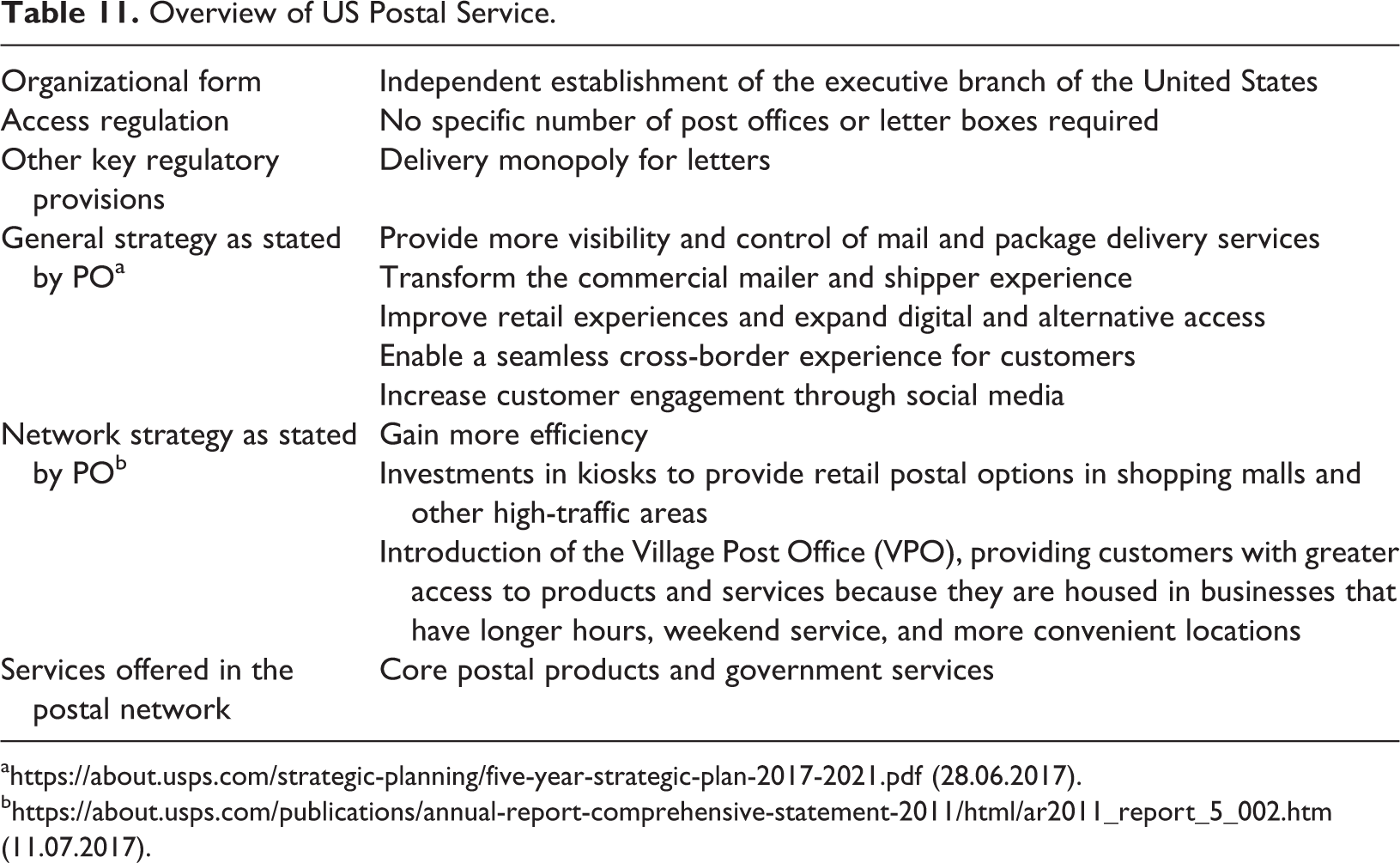

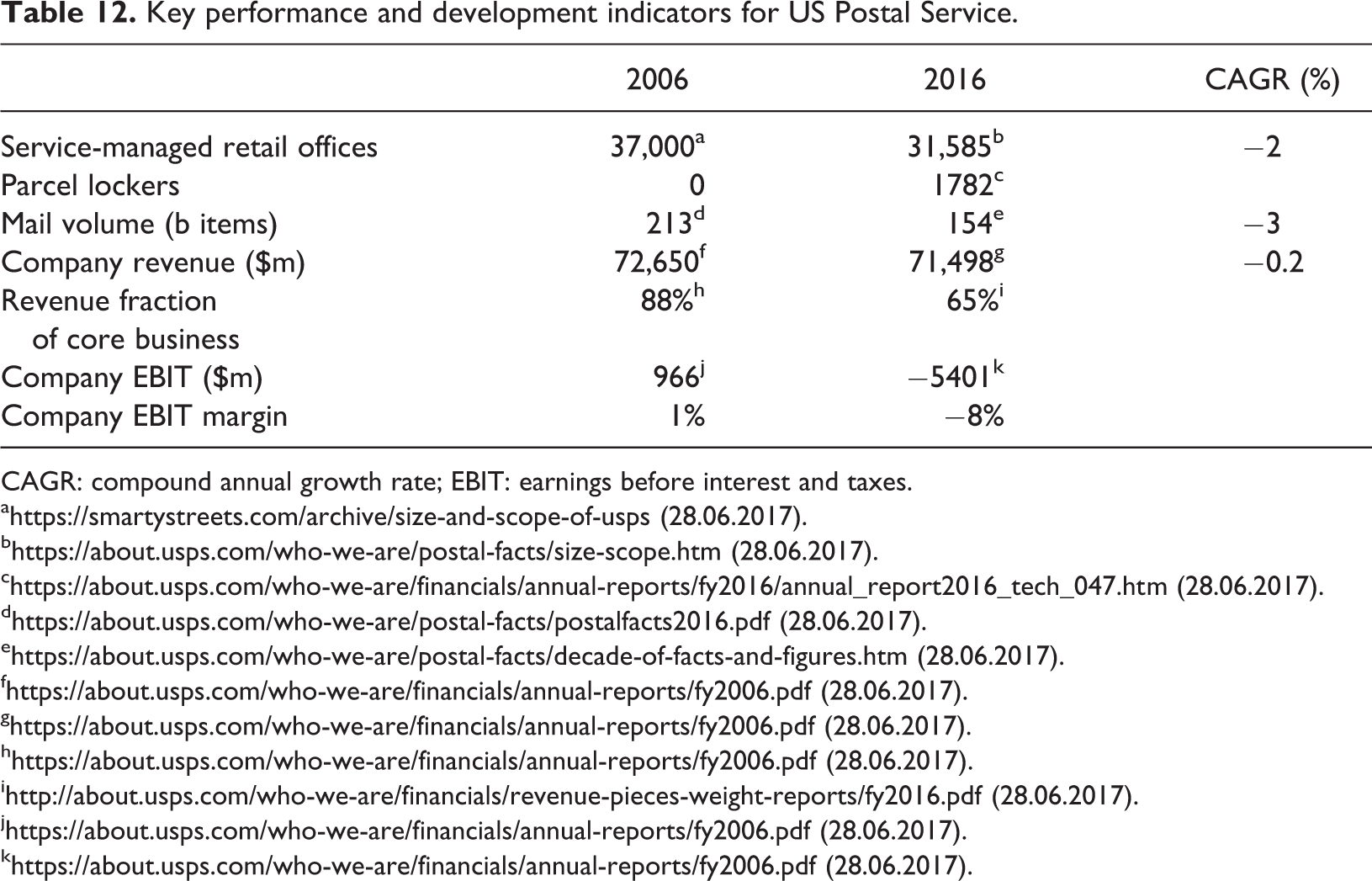

The USPS

The USPS is an independent establishment of the executive branch of the US Government. According to US legislation, USPS must provide prompt, reliable, and efficient services in all the areas; render postal services to all communities; and serve the entire population of the United States.

The corporate vision of the USPS, outlined in its Annual Report 2014, is to improve its services, products, and capabilities so as to adapt to the changing needs of customers in the digital age. Tables 11 and 12 give an overview of USPS’ development and performance. The USPS operates a dense network with a very limited range of products. It has a defined business model imposed by federal laws that does not allow it to utilize its existing asset base to generate additional revenue to offset the recent large mail declines (Crew and Geddes, 2014). Hence, the USPS is forced to restrict its activities to the traditional postal services, such as the delivery of first- and second-class mail, which accounts for over two-thirds of its annual operating revenue, and shipping parcels, which accounts for the remaining operating revenue (US Postal Service, 2014).

Overview of US Postal Service.

Key performance and development indicators for US Postal Service.

CAGR: compound annual growth rate; EBIT: earnings before interest and taxes.

ahttps://smartystreets.com/archive/size-and-scope-of-usps (28.06.2017).

Besides its core postal services, the USPS also offers government services in its retail network: From distributing tax forms to taking passport photos and delivering ballots overseas, the USPS moves toward government services. The USPS is the only delivery service that reaches every mailbox in the United States, including post office box addresses. This is due to the fact that USPS holds a legal monopoly on letter conveyance (18 US Code § 1696) as well as on mailboxes (US Postal Service, 2008). Citizens can apply for their passport at many post offices and the USPS will forward the application to the State Department.

In its Five-Year Strategic Plan 2017–2021 (US Postal Service, 2016), the USPS announced the intention to further develop parcel services so as to compensate the strong decline in mail business. Thereby, the USPS considers a change in the regulatory framework indispensable (US Postal Service, 2016). The USPS also aims to enhance retail and post office box services to leverage its retail stores.

With 88% and 65% of its revenues stemming from its mail business in 2006 and 2016, respectively, the USPS strongly depends on traditional postal services. Between 2006 and 2016, the company’s EBIT has turned into a deficit, which is due to declining demand and payments to its retiree health-care fund which are not directly linked to its operational business.

In our classification framework, due to the regulatory restrictions on its commercial development and its move toward government services, the USPS is an example for the post office network strategy “Network as a government service.”

Analysis and conclusion

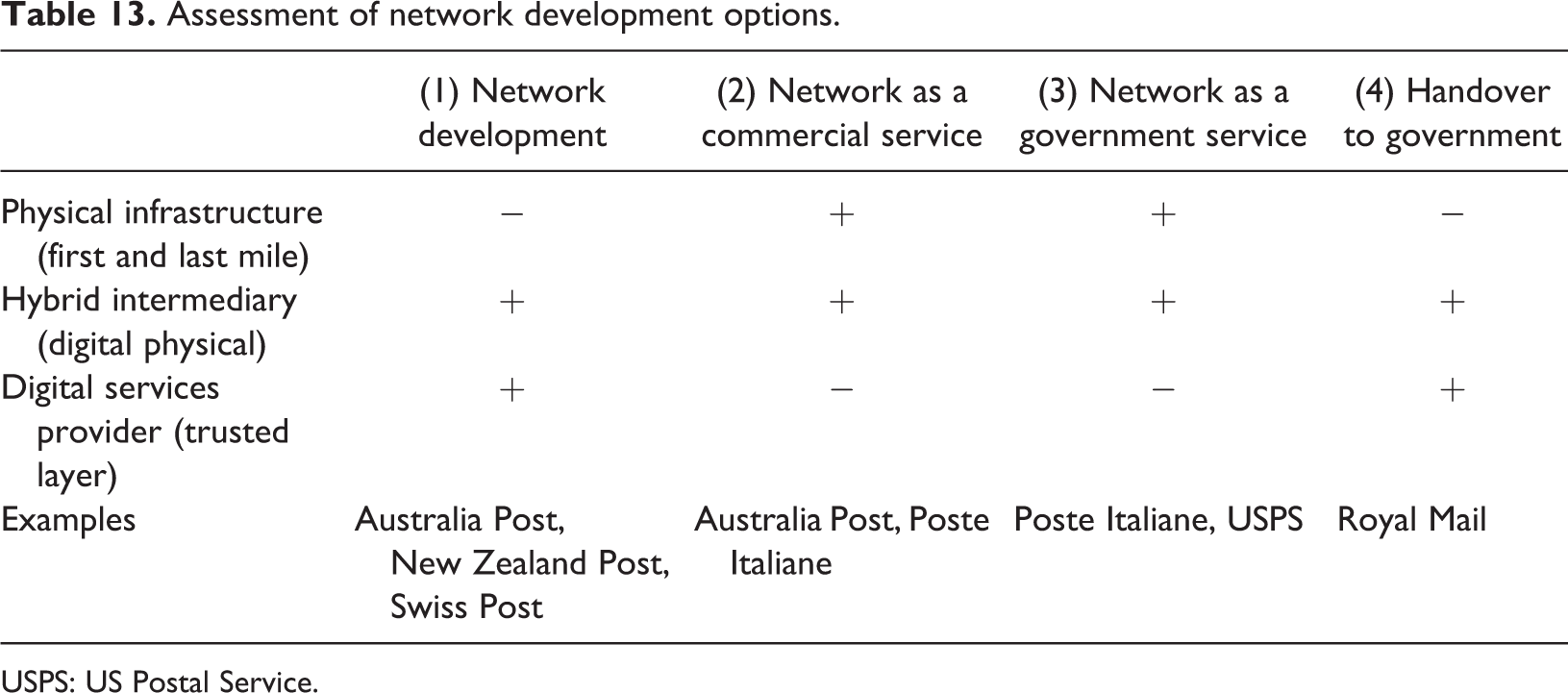

The post office network is part of a greater infrastructure for postal and nonpostal services. Its development is often politically driven such that the observed differences between POs can mostly be associated with the regulatory framework of the respective country. As discussed in the section on “Current status and trends in post office development”, there are four basic options for the future development of the post office network: network development, network as a commercial service, network as a government service, and handover to government. Not all network development options are compatible with all potential broad strategic orientations of a PO.

Table 13 gives an overview of mutual (in)compatibilities and the chosen way forward by the incumbent POs as discussed above: the use of the post office network as a strategic resource, that is, the broad strategic orientation “physical infrastructure provider,” is not compatible with post office network strategies that mainly consist of outsourcing access points to third parties, that is, “network development” or “handover to government.” These strategic choices result in a loss of both customer contact in a PO’s own infrastructure and the PO’s ability to develop the product range in its access points on its own.

Assessment of network development options.

USPS: US Postal Service.

The broad strategic orientation as a hybrid intermediary also requires a strong physical presence to complement core postal services with digital enhancements. However, it is not necessary for the access points to be operated by the PO itself. Hence, this strategy is also compatible with a handover of the network to government or a cooperation with partners to operate franchised counters.

A broad strategic orientation as “digital services provider” leverages the incumbent’s strong reputation, but does not require physical presence. Hence, it is compatible with the post office strategies “network development” and “handover to government.” However, if there is no postal network anymore, it cannot be used to offer commercial nor government services.

Among the incumbent POs covered in this article, Australia Post, Poste Italiane, and the USPS put a strong emphasis on their physical infrastructure, as a result of both their regulatory framework and their broad strategic orientation. They view it as a strategic asset to serve their customers better and use it to serve a broad range of nonpostal products and services. New Zealand Post and Swiss Post focus on developing their post office networks. This is a consequence of their transformation into a hybrid intermediary with strong ambitions both in hybrid and digital services. Royal Mail is a particular case, as its clear separation from the Post Office (network) gives it more flexibility in focusing on its business development without having to deal with post office network development (which is often politically burdensome).

Considering the alternative options, our suggestion is that within the regulatory boundaries, the future of the post office network should be guided by the broad strategic orientation of the PO. Network development and downsizing is a strategic dead end if there is no clear perspective to find new business areas that are independent of the network. Despite declining customer patronage, physical presence and proximity to customers may well prove to be a strategic asset in developing the postal business of the future.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.