Abstract

This paper examines the various challenges facing competitive electricity markets as they transition not only to systems based more on renewable energy, but also to generation sectors that become more competitive. In doing so, it examines how the reform of the South West Integrated System electricity market in Western Australia has affected returns, prices, and concentration in the electricity sector, particularly in the wholesale generation market. In doing so, this paper considers the lessons from the reforms that have taken place in Western Australia, both for the jurisdiction itself and more broadly for the Australian electricity sector as a whole.

Keywords

Introduction

Research into the nature and effects of reform of the electricity sector in Australia has tended to focus primarily on the establishment and development from the 1990s of the National Electricity Market (NEM), which operates across the south-east of the country, and encompasses multiple state and territory jurisdictions. Over the same period, however, parallel reforms of the electricity sector have occurred in other discrete electricity markets across the nation – in particular, in the state of Western Australia. The state of Western Australia is the largest in Australia, spanning 2.5 million square kilometres and ranking as one of the world’s largest sub-national jurisdictions. The power supply system in Western Australia consists of a series of separate supply areas that operate as independent systems. By far the largest of these is the one in the south-west part of the state, the South-West Interconnection System (SWIS), centred on the state capital and largest city, Perth, with smaller isolated systems existing in the Pilbara, and in several isolated towns where relatively small plant is operated. In addition, there are a few privately owned power stations that exist primarily to supply isolated, individual mines or mineral processing installations (Western Australia, 2024).

The experience of electricity sector reform in Western Australia differs from that of the NEM because the structural and regulatory changes have all occurred within a single jurisdiction, without the complicating impacts of interconnections with other regions/markets, and without multi-jurisdictional management. This means that it is possible insigght into the role of the government in r4eforming the electricity industry without these complications as is the case when the reform of the NEM is studied.

The wholesale market in the SWIS has been operating since 2006, when the vertically integrated, government-owned power company was broken up. Since then, several concerns have arisen in the running of this market, including the degree to which the government generator company that still operates in it exerts market power, the degree to which the regulatory regime encourages an overinvestment in infrastructure, and the degree to which the market is truly competitive (McHugh, 2012). Additionally, there are issues associated with the shift of generation capacity from coal-fired plants, first to natural gas-fired plants, and then to renewable energy, as well as rising prices in both the wholesale and retail markets. One aspect of the transition of electricity markets from being based mainly on fossil fuels (such as coal and natural gas) to renewable energy (mainly wind and solar) is that the nature of economies of scale has also changed. Whereas the optimal scale of a coal-fired power generation unit is around 500 MW, a combined cycle natural gas plant is typically around 50 MW, and a wind generator is usually around 1-2 MW. Switching from one fuel source to another not only changes the underlying costs of the industry, but also the generation profile of the industry, because of these differences in scale economies.

Focusing on the case of the SWIS in the state of Western Australia, the purpose of this paper is to look at the various challenges facing competitive electricity markets in transitioning not only to systems based more on renewable energy, but also on generation sectors as they become more competitive. Utilising long-term data, this paper analyses the impact of both the disaggregation of the vertically disintegrated electricity company in the south-west of Western Australia, as well as the impact of lower levels of generation concentration. To do so, this paper is structured as follows. In “History of Electricity Provision in Western Australia” section, the paper briefly outlines the historical development of the energy sector in Western Australia. This is followed by a section that details the nature of the reforms that have occurred from the 1990s onwards. “Effects of Reform of the Western Australian Electricity Sector” section then considers how these reforms have impacted returns, prices and concentration in the electricity sector, in particular in the wholesale generation market. The paper then concludes with consideration of the lessons of the reforms that have taken place in Western Australia, both for the jurisdiction itself and more broadly for the electricity sector in Australia as a whole.

History of Electricity Provision in Western Australia

The first demonstration of electric lighting in Western Australia took place in 1888, when Government House in Perth was lit with electricity supplied by the Western Australian Electric Light & Power Company. The commercial supply of electricity followed in 1894, when the Perth Gas Company began to install electric lighting in Perth, and private companies in several other municipalities supplied power for electric lighting and trams. In 1912, the Perth Gas Company was acquired by the City of Perth, including its electricity undertaking. In Perth, in addition to the Gas Company’s supply, a private tramways company had a small power station that supplied electricity to both its trams and some parts of the city. The tramways company was taken over by the Western Australian Government in 1912, and its power station was subsequently replaced by the newly built East Perth power station, which opened in 1916. The Government Railways Department, which subsequently operated the tramways and major Perth power stations, supplied much of Perth’s electricity for the next thirty years, providing bulk supplies to the councils of Perth, Fremantle and Midland. Its coverage was extended to other councils - Subiaco in 1920, and Claremont in 1924 –and new distribution networks were built to supply electricity to other parts of Perth. In other regions of the state, responsibility for the supply of electricity was assumed by local government councils and/or by gold mines which operated their own plant (Boylen et al., 1994; Edmonds, 2000).

The disaggregated nature of the electricity industry in Perth helped to contribute to the higher costs and prices in Perth compared to the major Australian cities in the eastern states (Abbott & Cohen, 2023). To help overcome this problem, in 1945, the State Electricity Commission of Western Australia was formed as a state government-owned utility and took over both the state government and, in 1948, the Perth City Council’s electricity assets. Over the next twenty years, the State Electricity Commission took over other power assets in other parts of the south-west region of Western Australia, extending its delivery area to much of this region of the state. The State Electricity Commission aimed to create a larger distribution area that supplied a greater number of people and businesses, which in turn meant that larger-scale generator units could be utilised. With larger generator units, it was hoped that average unit costs could be lowered, which in turn would lead to lower electricity prices for consumers.

Generation and transmission were gradually centralised and expanded over this period, including the establishment of coal-fired power stations supplied by the Collie coalfields, conversion of AC power to the national standard of 50 Hz, the construction of high-voltage transmission lines, and eventually the introduction of natural gas-fired power plant.

The State Electricity Commission was reconstituted in 1975 as the State Energy Commission of Western Australia to take over responsibility for the distribution and retailing of natural gas as well as electricity. Much of the plant built by the Commission in the 1970s and 1980s was coal-fired plant, a trend encouraged by the oil price shocks of that decade, which made the previously installed oil-fired plant less competitive. By the early 1990s, the discovery of natural gas in Western Australia, along with the construction of transmission pipelines and improvements in combined cycle natural gas units, led to a shift in the installation of new plants to natural gas. Between 1955 and 1994, the State Electricity Commission and then the State Energy Commission aimed to break even, and so provided no returns to the government, although the tendency was for prices in constant $ terms to fall, as was the case in the rest of the country (Electricity Supply Association of Australia, 1955). The intended greater economies of scale of the unit plant and declining transportation costs of materials helped achieve these lower electricity prices (Abbott & Cohen, 2021).

Reform of the Western Australian Electricity Sector From the 1990s

Reform of the Western Australian electricity sector from the 1990s took place in two distinct phases – from 1990 to 2006, and then from 2006 onwards. This section briefly outlines the structural and regulatory changes that occurred over both periods, having regard to the broader reform processes occurring in Australia during this time.

Reform From 1990 to 2005

Reflecting the experiences in other Australian states, cost overruns in the construction of power projects in the 1980s in Western Australia led to an accumulation of debt by the State Energy Commission, and at the same time, it was also criticised for overmanning of its operations (Booth, 2003). The monopoly state utility faced the classic problems of a lack of competition, which led to incentives for the Commission to over staff, both in the construction and the operation of the plant. Through the 1950s and 1960s, these effects were more than counterbalanced by the afore mentioned achievement of economies of scale, which had lowered average unit costs. However, by the 1970s, the scope for further economies from this source was diminishing.

The Western Australian Government review of the industry in the early 1990s, known as the Carnegie Report, advocated not only separation of the State Energy Commission into electricity and gas companies but also separation into generation, and transmission/distribution companies, which was occurring in the eastern states at this time and took place after the Australian Government’s Industry Commission report of 1991 on the energy sector (Abbott & Cohen, 2021; Australia, Industry Commission, 1991; Western Australia, Energy Board of Review, 1993).

The state government accepted the split into two organisations – AlintaGas (natural gas, and subsequently privatised) and Western Power (electricity, remaining in government ownership) in January 1995, but did not vertically separate the electricity component at this time. A key driver for retaining a vertically integrated electricity industry was that it enabled the then Coalition government in Western Australia to maintain the cross-subsidisation of city for country supplies, which it wished to do in order to promote regional development and placate its rural and regional supporters (Booth, 2003; Edmonds, 2000).

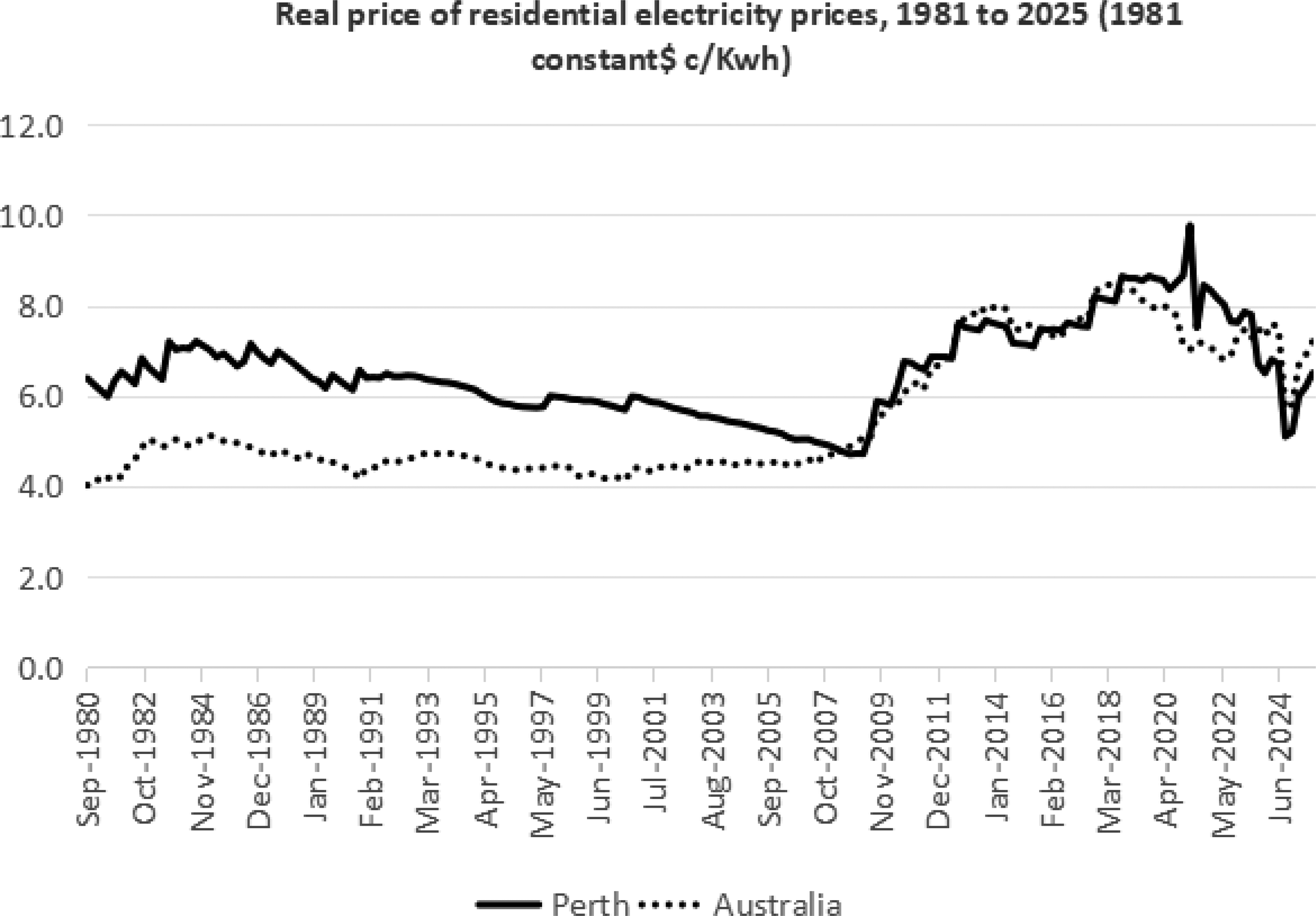

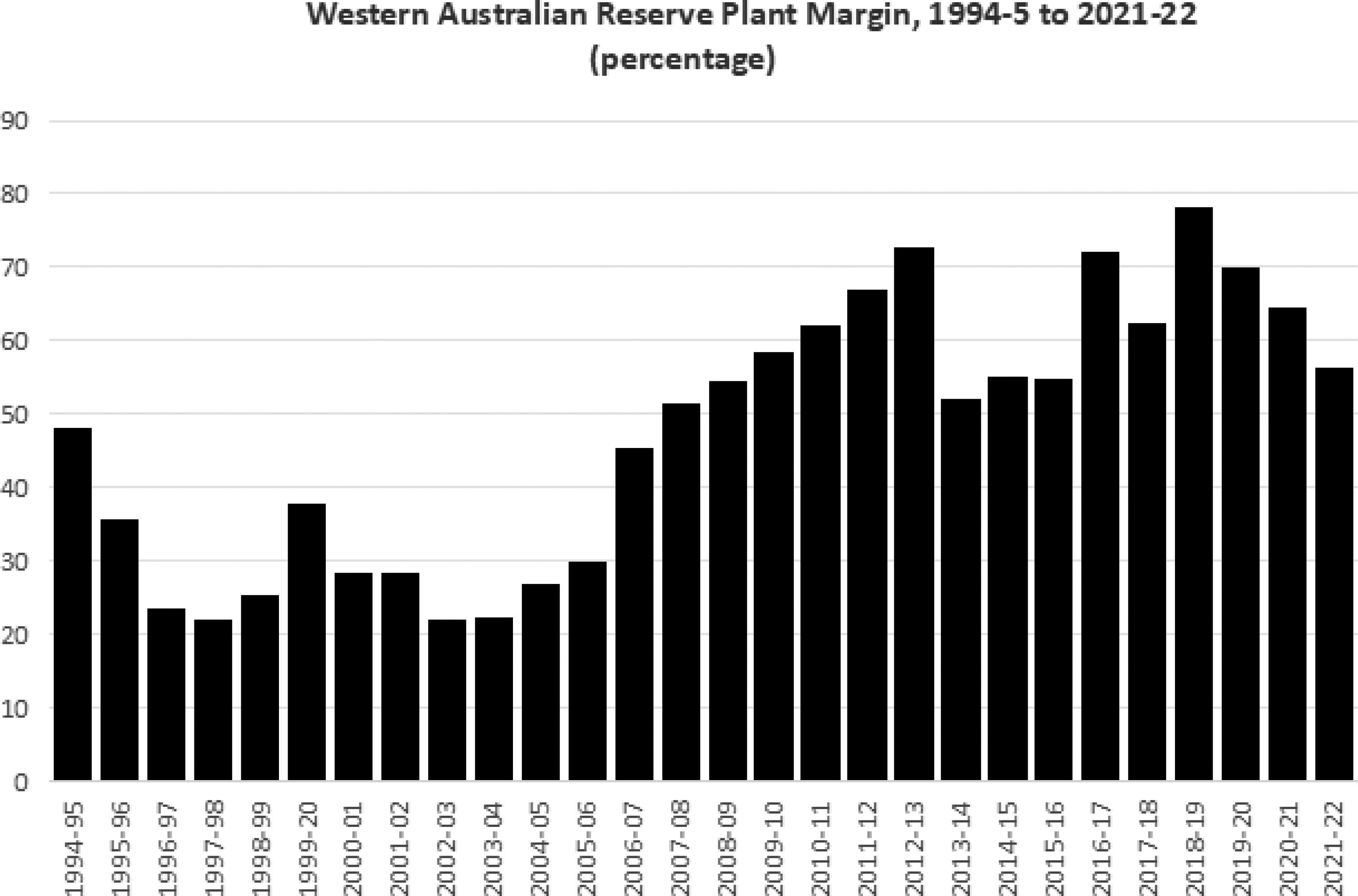

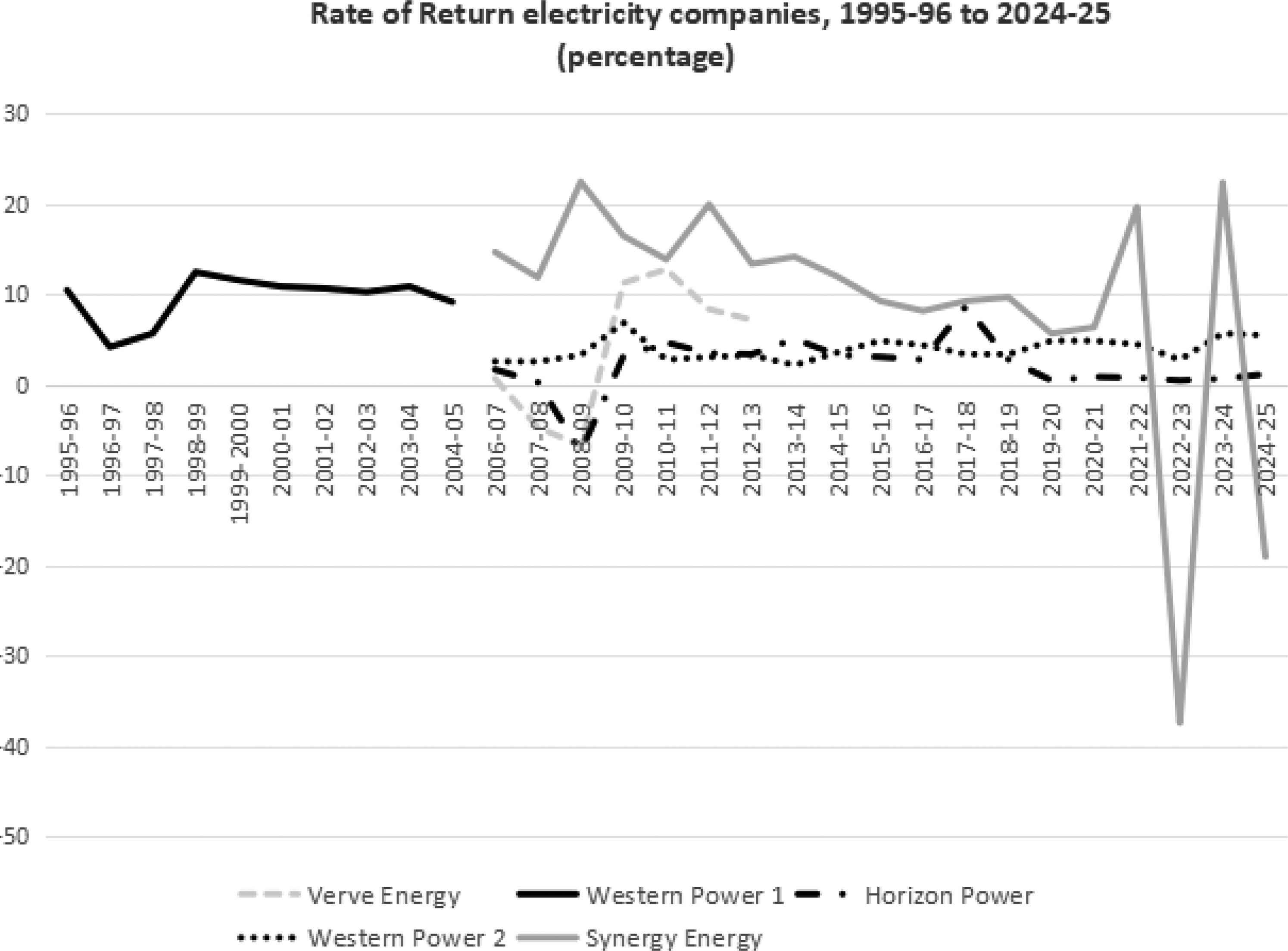

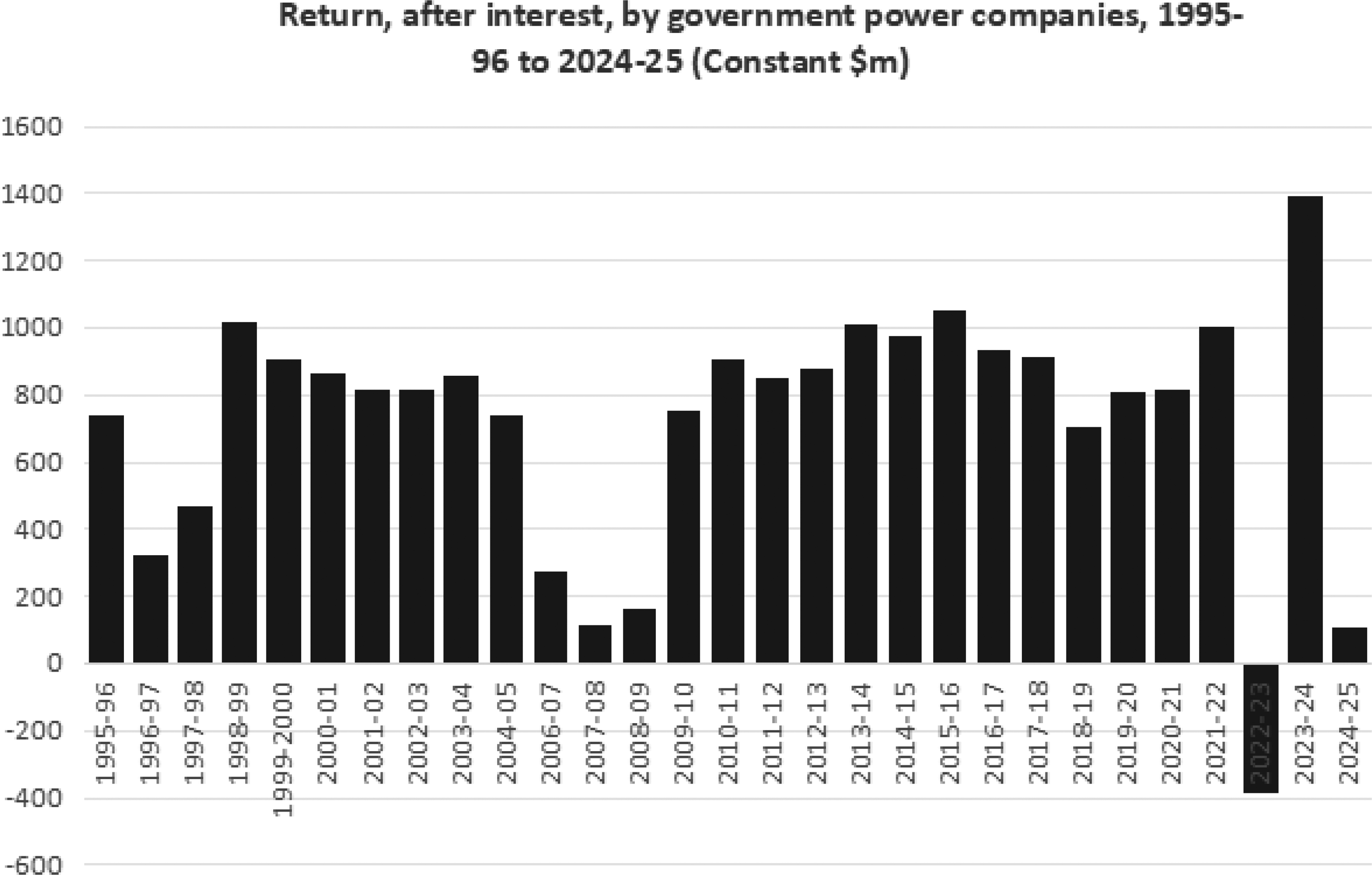

Western Power subsequently operated as a corporatised, government-owned entity, under a board of directors, with commercial objectives including target rates of return imposed on it. It provided electricity services across the state and acted as a vertically integrated company operating power stations, transmission and distribution networks, and retail sales. At this time, the only independent power producers tended to be simply cogeneration plant attached to industry or small plant owned by mining companies. During the period when the vertically integrated company existed (1995-2005), the regional and Pilbara sections of the industry continued to operate at a loss (after interest payments on capital expenditure), effectively cross-subsidised by the urban-based section of the industry (Western Power, 1996-2005). Through this period, Western Power was under pressure to both reduce prices to consumers and to meet its government-imposed target rate of return. These two goals could only be achieved by reducing costs; therefore, there was an incentive for the government-owned entity to improve its level of efficiency. Overall, in this period, efficiency gains and the fuller use of the new generation capacity built in the 1970s and 1980s meant that average costs and Perth residential consumer prices were reduced (in real terms between June 1995 and June 2005 by 6%: see Figure 1; Australian Bureau of Statistics, Consumer Price Index; Electricity Supply Association of Australia,1987-2004). From Figure 2, it can also be seen that reserve margins fell throughout the period, as the plant was more fully utilised (Electricity Supply Association of Australia, 1987). Western Power, through these years also generated a financial surplus of around ten per cent on assets after interest payments (see Figure 3). Residential prices in real terms (constant $ terms) were declining in Perth up until 2008, so there must have been efficiency gains in the Western Power integrated period that underpinned this. It is posited that feather bedding, in terms of over staffing and underutilised capacity from the State Energy Commission days, meant some “low-lying fruit” could be reached to enhance productivity. Real price of residential electricity prices, 1981 to 2025 (1981 constant$ c/Kwh). Source: Australian Bureau of Statistics (1981) Western Australian reserve plant margin, 1994-5 to 2021-22 (percentage). Source: Electricity Supply Association of Australia (1987); Electricity Supply Association of Australia, (2005). Australian Energy Council (2016) Rate of Return electricity companies, 1995-96 to 2024-25 (percentage). Source: Horizon Power (2006). Synergy Energy (2006). Synergy (2014). Verve Energy (2006). Western Power Corporation (1996)

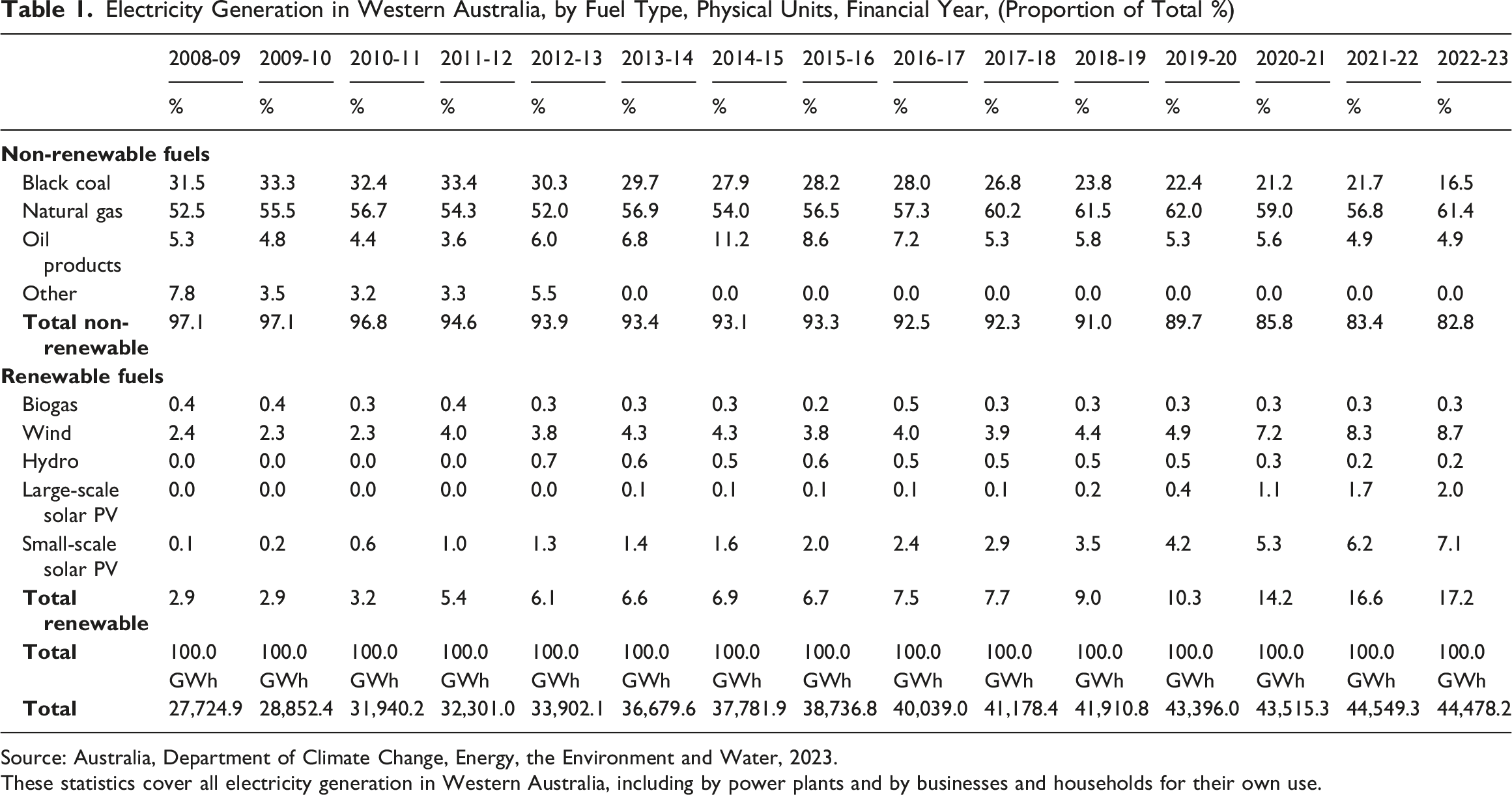

Electricity Generation in Western Australia, by Fuel Type, Physical Units, Financial Year, (Proportion of Total %)

These statistics cover all electricity generation in Western Australia, including by power plants and by businesses and households for their own use.

Reform From 2006 Onwards

Despite the successes that Western Power achieved between 1995 and 2005, in terms of reduced real prices, increasing returns to the government and financing the cross-subsidisation of regional power generation, the vertically integrated structure for electricity was not to survive a change of government. Mirroring changes that had occurred in the NEM jurisdictions across the eastern states, the incoming Labor government reorganised Western Power in 2006 into four separate, government-owned companies: a new Western Power, Synergy Energy, Verve Energy and Horizon Power, with an economic regulator given power to regulate open access to the wires components of the industry.

The wholesale market that was established was operated by the Australian Energy Market Operator, a semi-governmental body (60% by the Government and 40% by industry and market participants), which also operates the NEM. In 2006, a centrally cleared day-ahead market was introduced, allowing market participants to adjust their contractual positions by trading with each other. A reserve capacity mechanism was also introduced, through which the market operator procures capacity to ensure that adequate generation and demand-side management capabilities are available to meet demand. In 2023, additional mechanisms were introduced with the competitive gross balancing market operating every half-hour to schedule supply from all generators, as well as a load following ancillary service market, through which the operator can procure frequency regulation services from participants other than Synergy (which previously supplied all of this).

Under the new structure, the reconstituted Western Power operated the electricity grid, which linked the bulk of Western Australians to power producers just in the south-west of Western Australia, including the Perth metropolitan area. Verve Energy became the vertically separated generator company, and Synergy Energy the electricity retailer. The generator market was made competitive to encourage more efficient generation use and to promote private sector investment in new plant. The retail market was made competitive for non-residential consumers, so that commercial users could take advantage of consumer choice. Residential consumers, in contrast were required to purchase electricity from Synergy Energy, and in the absence of competition were protected by government price regulation in this retail segment.

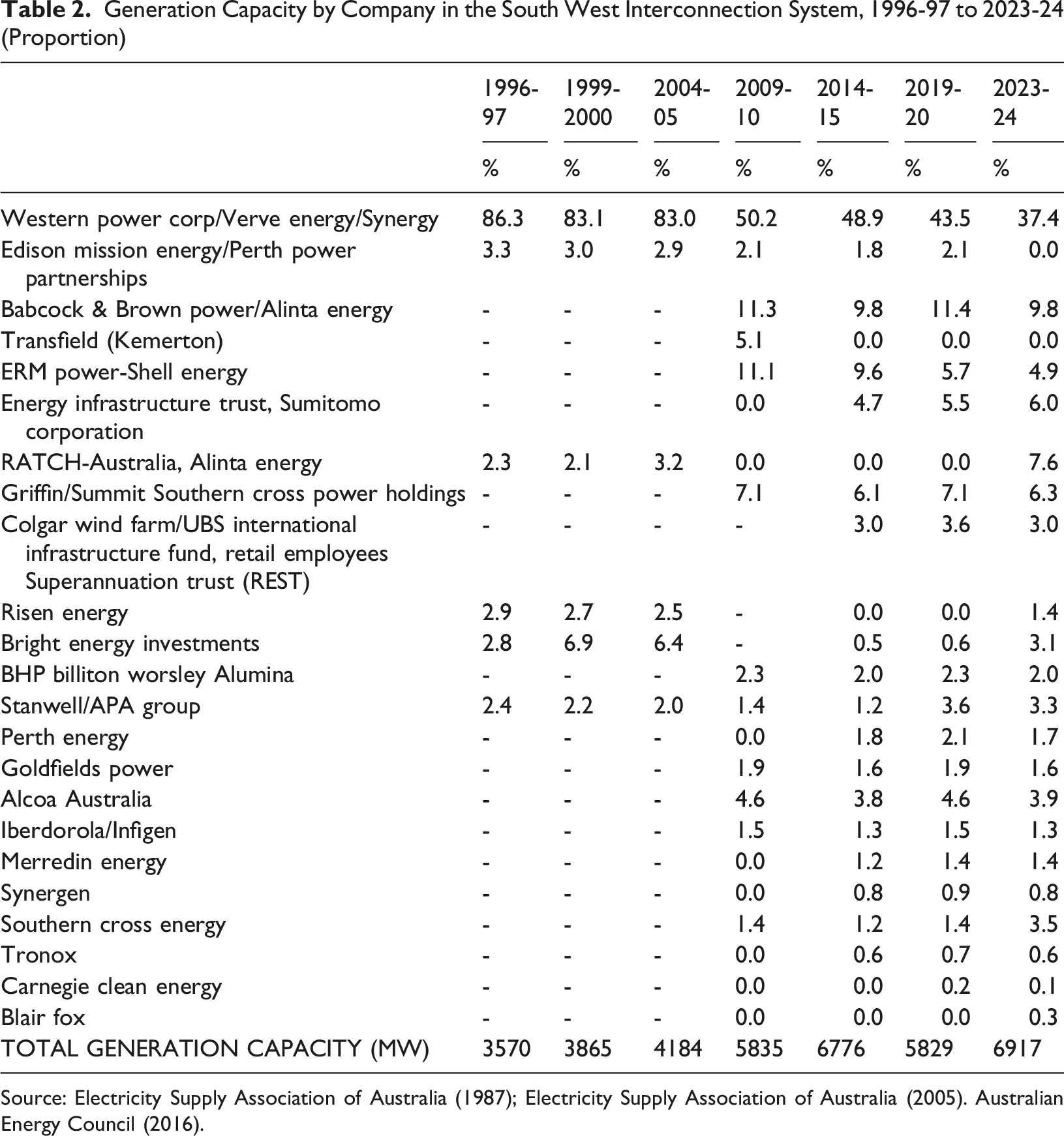

Generation Capacity by Company in the South West Interconnection System, 1996-97 to 2023-24 (Proportion)

Outside the south-west, the state government-owned Horizon Power operated in the Pilbara, Kimberley, Gascoyne/Mid-West, and the Southern Goldfields-Esperance regions of Western Australia. There is a third, small interconnected grid (including the Ord River Hydro Power Station) in the far north of the state, and 34 additional ‘microgrids’ operated by Horizon Energy supplying power to towns in the remoter parts of the state. In each case, Horizon Power’s operations are vertically integrated, unlike in the SWIS, which is due to the small size of each of these markets.

Effects of Reform of the Western Australian Electricity Sector

Together with exogenous changes, such as national climate change-related policies, the changing economic competitiveness, and the ongoing development of the renewable energy sector, the impact of reform in the Western Australian electricity sector manifested in a variety of ways – including on concentration in the wholesale electricity market, prices, and shareholder returns.

Concentration of the Wholesale Generation Market

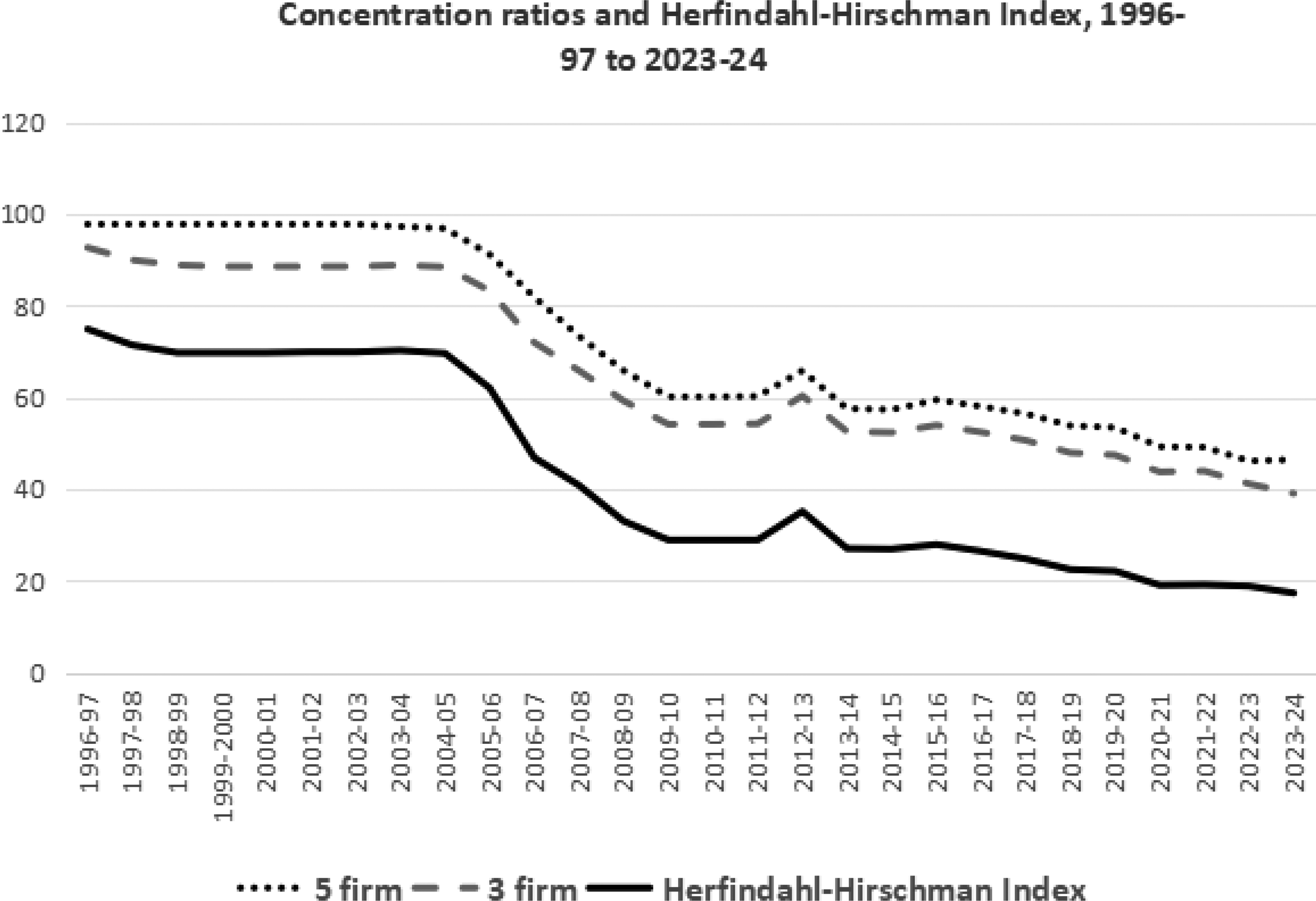

The concentration of generation capacity has changed substantially since the mid-2000s and the breakup of Western Power. Figure 4 shows the dramatic nature of this process in the SWIS. Between 1996 and 2005, the concentration ratios (for the largest three and five firms) remained largely unchanged. Since 2005, these levels have steadily fallen – for example, for the five largest firms, the ratios declined from 97.7 to 46.4%. Concentration ratios and Herfindahl-Hirschman Index, 1996-97 to 2023-24. Source: Electricity Supply Association of Australia (1987), Electricity Supply Association of Australia (2005). Australian Energy Council (2016)

A key measure of industry concentration is the Herfindahl index (also known as Herfindahl–Hirschman Index, HHI, or sometimes HHI-score), which is a measure of the size of firms in relation to the industry they are in and an indicator of the amount of competition among them, the decline has been even more dramatic. The Antitrust Division of the Department of Justice in the United States considers Herfindahl indices between 15% (0.15) and 25% (0.25) to be ‘moderately concentrated’ and indices above 25% to be ‘highly concentrated’ (United States, Department of Justice, 2010; United States, Department of Justice, 2018).

Taking this benchmark would imply that there is still some concentration in the generator market, but far less than was the case in the 2000s. This concentration, however, was further reduced by around 7% of electricity generated and used in Western Australia in 2022-23, which came from small-scale solar PV (Table 1). One could, therefore, conclude that although Verve Energy and then Synergy have some market power from 2005 through to 2020, this is probably no longer the case, and that the generator market is reasonably competitive.

Electricity Prices

Over the period from around 2008 up until around 2017, there was a large increase in retail electricity prices, in both normal and real (constant $) terms, per unit of electricity generated and sold (see Figure 1 for the rise in Perth’s constant $ electricity prices). This is, despite Western Australia’s isolation, in line with price increases that have taken place in the rest of the country. Within the state, these price rises also occurred in government companies operating in the SWIS and Horizon Power, the latter being the regional company not involved in vertical separation. In the latter case, in constant $ real terms, expenses per GWh of electricity generated have more than doubled between 2005 and 2017 (Horizon Power, 2006). This is despite there being no disaggregation of the company as occurred in the south-west of the state. In the south-west, the increase in expenses per GWh has been even higher than the case for Horizon Power. This substantial increase in constant-dollar expenses per electricity generated and sold occurred in the generation segment of the industry, perhaps more so than in the wires segment, with the latter experiencing only around a 15% increase in average expenses per electricity transmitted and distributed (Western Power, 2006). As this increase in expenditures occurred both in the SWIS (vertically disaggregated system) and with Horizon Power, which is vertically integrated, it was likely primarily due in both cases to the replacement of older, less expensive coal-fired stations with first gas-fired and then later renewable sources, rather than to the costs of vertical separation (Horizon Power, 2006-23). It is also due to the substantial build-up of additional generation capacity in the state. From Figure 2, it can be seen that the reserve margins in the SWIS were significantly larger in the 2010s and 2020s than they were in the 1990s, with natural gas, solar, and wind generation capacity being added faster than the older coal and gas plants were retired. In the future, this reserve margin might decline with the retirement of additional, older coal-fired plants, but it will largely remain as greater levels of reserves are needed to manage a system based more on intermittent renewable energy.

Returns

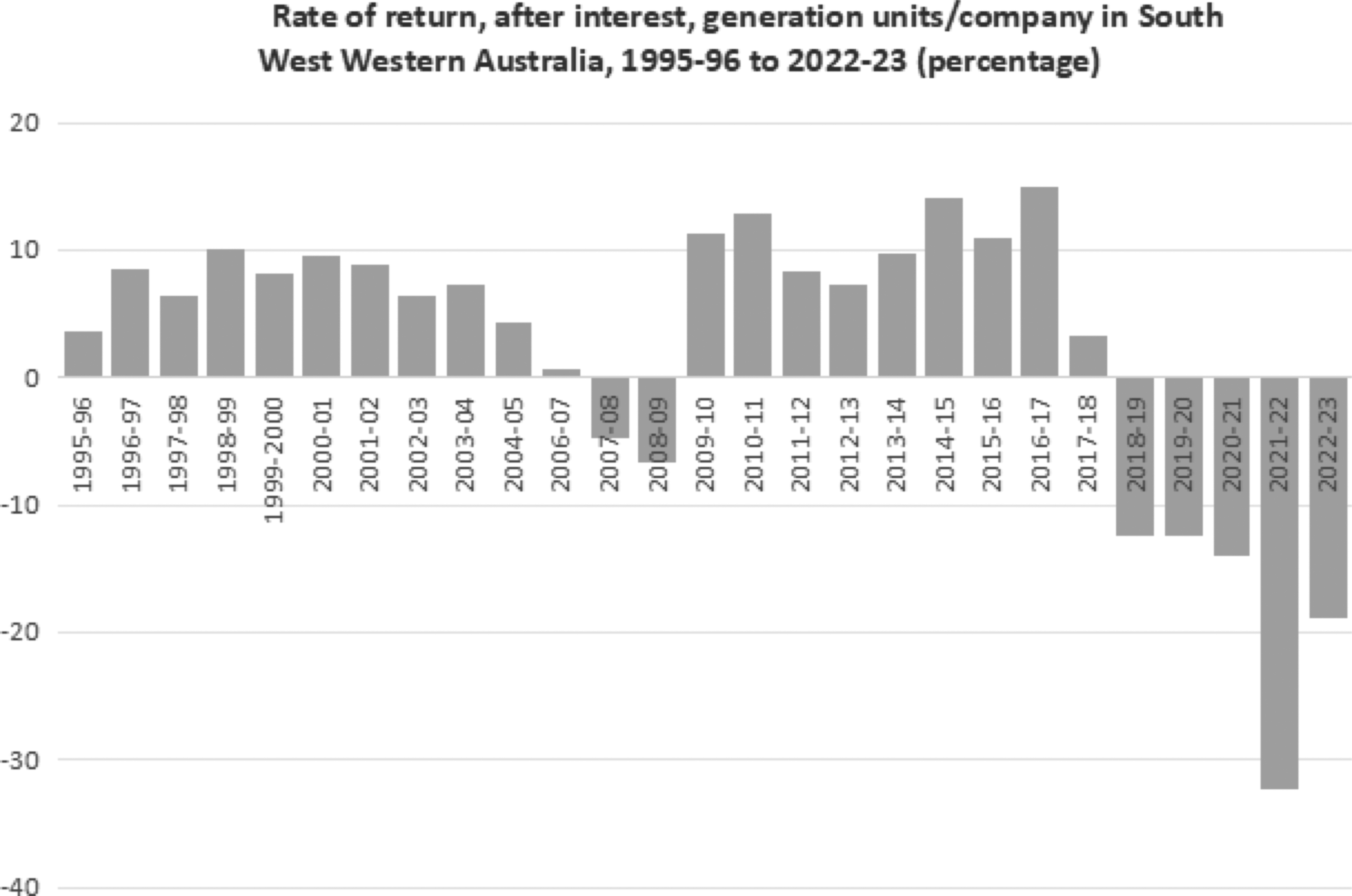

In the case of the state outside the southwest region, both the Pilbara and Regional sections of Western Power operated at a loss (after interest payments) between 1995 and 2006 (Western Power Corporation, 1996-2005). This changed after horizontal separation. As seen in Figure 3, Horizon Power which operated the Pilbara and Regional sections of the industry after separation it generated a positive rate of return from 2009-10 onwards, although in the last few years it has only just broken even. If one of the aims of the restructuring in 2005 was to end the cross-subsidisation of city to country in Western Australia, then this was certainly achieved. As well after 2005 Horizon Power was able to largely eliminate the losses of the Pilbara and Regional sections, although whether this was by lowering costs by improving its levels of efficiency, or simply by raising prices is difficult to say.

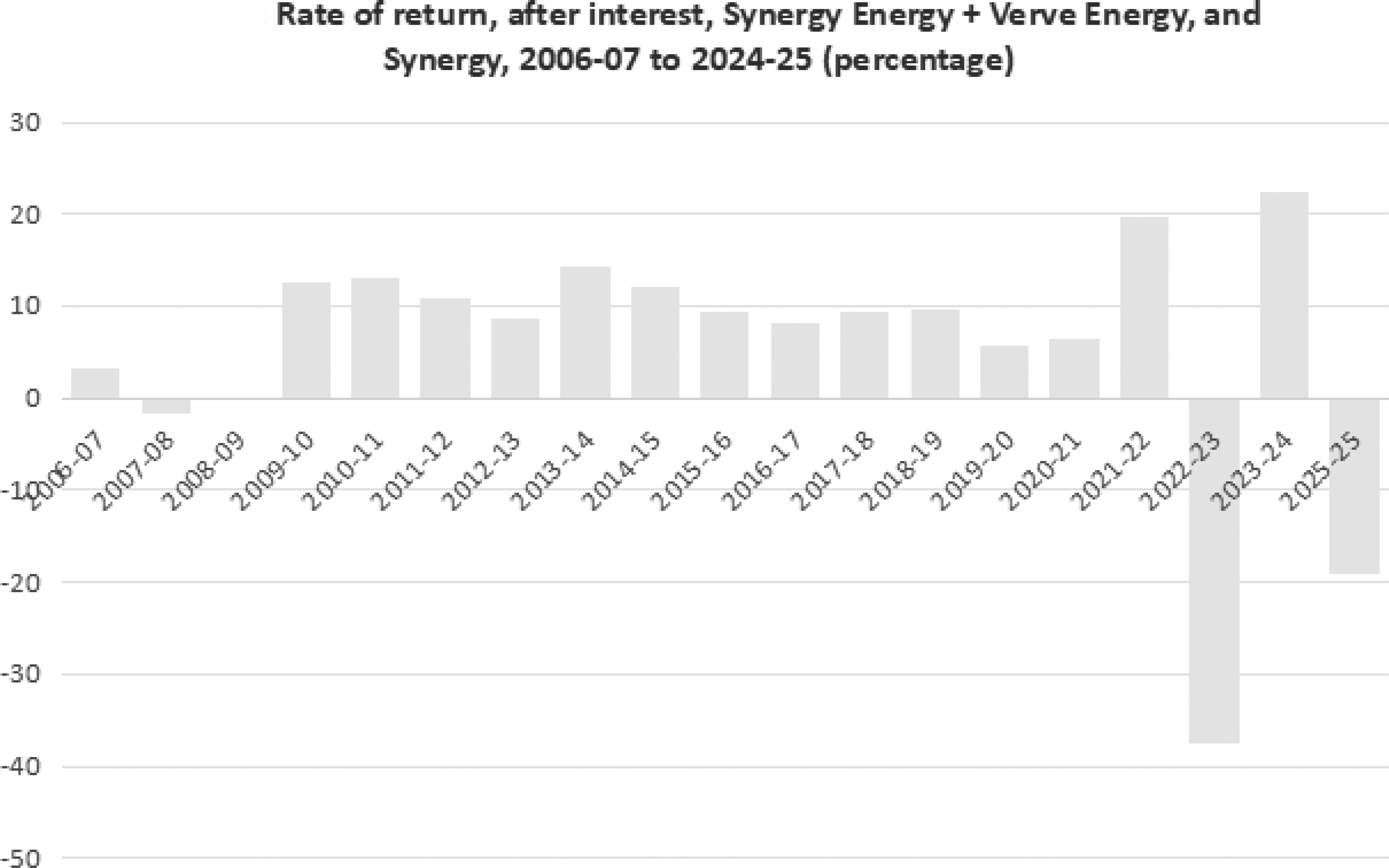

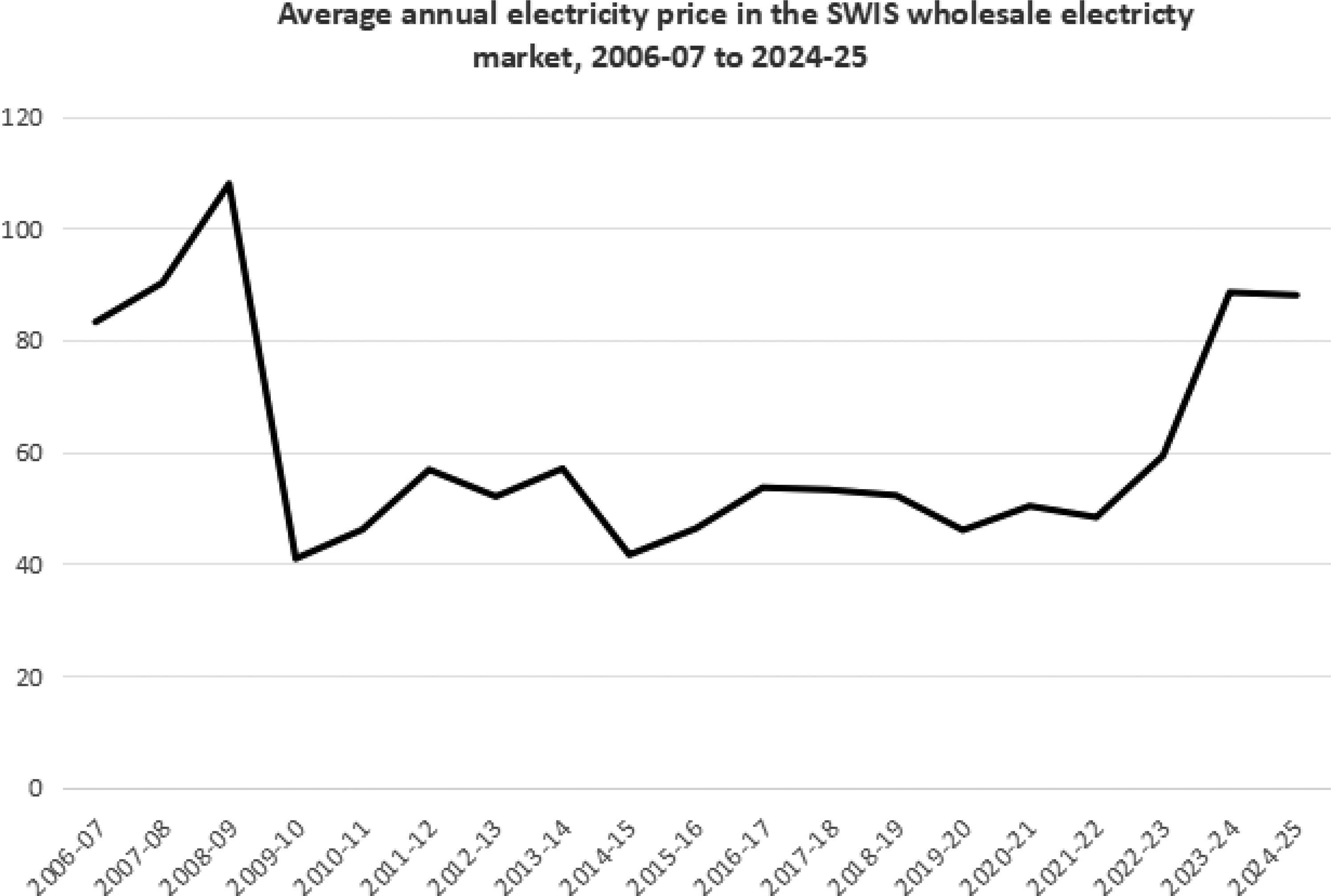

From around 2017 onwards, constant $ real retail prices stabilised and then fell a little (Figure 1), perhaps at least partly because profit margins to the generator and retail companies began to be squeezed by competition. From Figure 3, it can be seen that the rate of return to Synergy declined through the 2010s, with this being true more with the generator section of the company than the retail section. Figure 5 provides the rate of return of the generator section of the company (and Verve Energy before 2013), and it shows that the generation section was in the red by the end of the 2010s. Figure 6 provides data on Synergy Energy and Verve Energy, before 2013, and the combined Synergy after 2013. These figures seem to show a gradual squeezing of the margin. In addition, Figure 7 shows the returns (after interest payments) of all the government electricity companies in constant $ terms from 1995 onwards. Although the overall level of payments to the government appears to be reasonably constant over the period (an exception being the years of the global financial crisis), these returns are on a capital base that is today far larger than it was in 1995, which means overall rates of return have fallen. Wholesale competition in the SWIS seems today to be strong, and wholesale prices have tended to be fairly stable since 2006 (see Figure 8). Synergy, as a retailer, buys a lot of electricity now off other generator companies, and the generation and wholesale parts of Synergy don’t appear to be doing so well. In fact, the retail part of Synergy seems to be cross-subsidising the generation sector. Overall, it seems that the margins earned by Synergy are lower than they were in the Western Power integrated period between 1995 and 2005. Rate of return, after interest, generation units/company in South West Western Australia, 1995-96 to 2022-23 (percentage). Source: Synergy (2014). Verve Energy (2006). Western Power Corporation (1996). 2022-23 is the last year Synergy reports Unit financials Rate of return, after interest, Synergy Energy + Verve Energy, and Synergy, 2006-07 to 2024-25 (percentage). Source: Synergy Energy (2006). Synergy (2014). Verve Energy (2006) Return, after interest, by government power companies, 1995-96 to 2024-25 (Constant $m). Source: Horizon Power (2006). Synergy Energy (2006). Synergy (2014). Verve Energy (2006). Western Power Corporation (1996) Average annual electricity price in the SWIS wholesale electricty market, 2006-07 to 2024-25. Source: Electricity Supply Association of Australia (1987); Electricity Supply Association of Australia (2005). Australian Energy Council (2016)

In the case of the transmission and distribution section of the industry, things have remained more stable over time. As mentioned previously, average real expenses are today around 15% higher than they were in the 1990s (Western Power, 2006). On top of that, the wires company (Western Power) between 2005 and today has made a steady 4-5 per cent rate of return (see Figure 3; Western Power, 2006). As this is determined by the regulator, it is capped, and although it is low, it is on a large capital base (Economic Regulation Authority, 2026).

Conclusion

Overall, it can be said that despite the relatively small size of the Western Australian electricity market, competition in the wholesale market in the SWIS in the 2020s has been fairly strong, unlike it was the case in the late 1990s and 2000s. Synergy still has a legal monopoly on the residential retail market and has some scope to leverage this, but they have lost a lot of money recently on their various contracts with a number of generator companies. In the retail market, the industrial and commercial retail markets are very competitive (in 2024, there were 15 licensed retailers operating in Perth; Economic Regulation Authority, 2024). Greater competition is having an impact by squeezing margins. Not enough to lower prices, however, as large increases in generation costs are also occurring due to the switch from first coal to natural gas, and secondly from coal to renewables.

These outcomes highlight several points relevant to reform of both the Western Australian industry and the broader Australian electricity sector that were occurring at the same time: i. In considering the impact of structural changes in Western Australia relative to those which occurred in the NEM, regard needs to be had not only to the similarity of the changes, but also to how variations in the mix of energy sources may affect the speed and nature of the transition. In particular, the availability of low-cost gas in Western Australia has contributed to a markedly different energy mix from that which is present in the NEM. At the same time, the changing economics of renewable energy, particularly ‘rooftop solar’, has contributed to a growth in its use, although the extent to which this has occurred is less than the NEM (small scale PV in Western Australia accounted for 7.1% of generation compared to 9.4% for the whole country in 2022-23; Australia, Department of Climate Change, Energy, the Environment and Water, 2023); ii. The extent to which reform is made simpler where it occurs in a single jurisdiction, and one in which a significant proportion of the electricity assets are owned and controlled by the government. A concern relating to ongoing public ownership of the electricity sector is that government decision-making may be impacted by the multiple roles played – as policy maker, regulator and asset owner. The experience of Western Australia, particularly in the second stage of reform, is that these competing interests appear to be able to be managed. Further, this appears to have occurred without some of the difficulties that occurred with the introduction of retail competition in the NEM, which resulted in increasing concerns regarding potential abuse of consumers from private sector electricity retailers, and subsequent reintroduction of retail price capping arrangements across the NEM jurisdictions (see, for instance for the state of Victoria: Essential Services Commission, 2024) iii. The consistency of approach which applies to the monopoly “pole and wires” components of the industry, although again, the retention of government ownership has meant less conflictual interactions between asset owners and the regulator. By contrast, in the case of the NEM efforts of private owners of these assets to challenge pricing outcomes determined by designated independent regulators, reform of the appeals processes to remove ‘merit-based’ reviews of regulatory decision making (Competition and Consumer Amendment (Abolition of Limited Merits Review) Act 2017, no. 116, 2016)).

In seeking to examine the reform of the Western Australian electricity sector, the aim of this paper has been to both outline the nature and impact of change that has occurred, and to consider its implications for the broader reforms that have occurred in the electricity sector nationwide. Key lessons that may be drawn are that government ownership does not prevent reform from occurring, either in terms of the introduction of renewables or in terms of vertical and horizontal separation of the industry, rather that its shape and pace may vary. More broadly, in anticipating the long-term energy mix that will operate in any jurisdiction, the extent of access to natural resources plays a key role as ultimately it is the economics of the generation industry that will shape investment in generation capacity. In considering the implications for the expanded use of renewable energy, while government policy may impact the pace and scale of these outcomes, the capital and operational costs associated with the different types of generation plant will be determinative factors over time.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.