Abstract

This article examines spatial fixes and their dialectical relationship with poor forms of flexible work, positioning touristification as a key contemporary form of capital's spatial fixes. Drawing on a multi-scalar methodological framework that integrates Gross Fixed Capital Formation with employment data, it offers a systematic account of shifting patterns of capital allocation between sectors and across regions of Greece, tracing how these may signal the consolidation of new spatial fixes. Findings confirm the Greek economy's enduring mechanism of extracting value primarily from the built environment, although post-2009 recovery has seen the emergence of new fixes pertaining to tourism-oriented structures in contrast to prior ones pertaining primarily on housing construction. In this context, labour markets adapt by intensifying labour devaluation, evident in the expansion of part-time and temporary employment in key sectors such as tourism and construction. Cross-regional variations indicate complementary expressions of a unified accumulation regime rather than divergent development paths. The article argues that spatial fixes and labour devaluation operate as intertwined crisis-management strategies. While tourism-led growth may temporarily bolster profitability, it does so by entrenching precarity and reinforcing uneven geographical development, thereby underscoring the limits of spatial fixes.

Introduction

Among southern Europe's peripheral economies, few illustrate the contradictions of post-crisis restructuring as sharply as Greece, where decades of construction-led growth absorbed surplus capital from manufacturing downturns and left a durable imprint on the built environment (Kokkinou and Psycharis, 2004; Antonopoulou, 1987; Vetta, 2014). This model produced a fragmented labour market marked by widespread self-employment and entrenched informality, rendering precarity structural rather than cyclical (Papadakis et al., 2020). After 2008, the spatial fixes that had absorbed labour surpluses through successive slumps in manufacturing and construction were dismantled (KEPE, 2018; IOBE, 2025; Gourzis and Gialis, 2019), and tourism emerged as the central arena of accumulation – expanding from island and rural destinations into urban regions and deepening reliance on flexible, low-paid and precarious labour (Gourzis and Alexandri, 2026).

These recent shifts in Greece's economic geography can be fruitfully interpreted through critical and Marxist geography conceptualisations on how capital responds to crises by reorganising its spatial and sectoral composition. A central notion in this body of work is the spatial fix, introduced by Harvey (1982) to describe how capital temporarily addresses crises of overaccumulation by redirecting investment across space and production. This mechanism has been linked to the circulation of capital between what Harvey calls the ‘primary’ and ‘secondary’ circuits of accumulation – a process of capital switching from direct production to investment in the built environment, such as infrastructure and housing (Christophers, 2011; Kutz, 2016; Gourzis and Gialis, 2019). Recent studies argue that new waves of spatial fixes have emerged in the aftermath of the global financial crisis, as states and investors channelled capital into real estate, tourism and digital infrastructures (Christophers, 2022; Wijburg et al., 2024). These processes are especially visible in southern European and other peripheral economies, where the built environment becomes a crucial site for managing economic instability and reproducing precarity and inequality (Cocola-Gant et al., 2025; Pettas et al., 2024; Vandarakis et al., 2023). This article contributes to this ongoing endeavour by providing a novel, theoretically informed empirical analysis of spatial fixes and associated capital switching in Greece, a peripheral country of advanced capitalism (Mavroudeas, 2014). In this respect, it offers a valuable vantage point for examining how new forms of investments, spatial organisation and labour recomposition emerge through such spatial fixing attempts.

Against this backdrop, we scrutinise three key research questions. First, drawing upon earlier geographical political economy accounts (Christophers, 2011; Kutz, 2016), we seek to identify the consolidation of spatial fixes in Greece's built environment over the past 30 years. Second, we examine the transition from construction-driven to tourism-dependent models within the secondary circuit during the past 15 years, studying different types of fixed investment in Attica and South Aegean – the region of metropolitan Athens and the island region comprising internationally famous destinations, respectively. Third, drawing upon earlier relevant work (Gourzis and Gialis, 2019), we explore how the identified capital switching relates to labour turnover, focusing on the changing analogies between part- and full-time and temporary and permanent waged employment in these sectors and regions.

Addressing the above, we extend current knowledge in three main ways. First, we establish a concrete framework conceptualising touristification as a spatial fix, showing that in the Greek case, post-crisis restructuring and the partial recovery of construction activity have mainly relied on investments in tourist accommodation rather than residential expansion. Second, we provide theoretical grounding and empirical evidence on the links between spatial fixes, capital switching and work, documenting that poor forms of flexible work are an integral part of tourism-driven accumulation and not a residual effect. Third, we contribute to current accounts of touristification as a process affecting both rural and urban contexts, in contrast to the dominant narrative that confines touristification to the urban arena.

In the next section, we outline the article's conceptual framework. We then present its methodology before moving to the empirical section, which explores the links between spatial fixes, capital switching and labour in the selected sectors and regions. In the final section, we discuss the findings and their broader implications.

Capital switching, spatial fixes and labour flexibilisation: A conceptual framework

Investment in the built environment has mainly been understood as a necessary process for supporting industrial productivity through essential infrastructure or as a response to lucrative opportunities (e.g., in residential or commercial real estate) resulting from low values in favourable locations – coined as ‘rent gaps’ (Smith, 2010). Harvey's work shows that such investment functions as a structural mechanism for addressing looming crises of overaccumulation by redirecting capital from industrial production (the ‘primary circuit’) to the built environment (the ‘secondary circuit’), providing a primarily temporal fix by absorbing surplus capital during periods of declining profitability in the primary circuit (Jessop, 2006). Beauregard (1994), studying the post-war US, empirically traces the corollary, whereby investment in manufacturing recedes as construction and property speculation rise. This capital switching signifies broader transitions between growth models, prompting extensive spatial restructuring, with capital being revalorised through its relocation across space (Ekers and Prudham, 2017). Landscapes are constructed only to be dismantled and rebuilt, while capitalist relations are reconstituted at the global scale, linking spatial fixes with imperialism and colonialism (Harvey, 2001). Yet fixes are unevenly distributed, since planning regimes, interest rates, labour institutions and other political–institutional factors shape where and how they materialise (Morgan, 2011). As Christophers (2011) notes, such transitions are also mediated by institutional investors (e.g., pension funds) channelling surplus capital into real estate.

This strategy is inherently crisis-prone, as capital switching is often triggered by overaccumulation and at the same time seeks to resolve it (Harvey, 2001). Christophers (2011) offered a particularly persuasive empirical account, showing a systematic reorientation of private investment from production to the built environment in mature economies before the 2007/08 crisis. Kutz (2016) extended this thesis, repositioning sectoral and geographical switching as twin dynamics through which overaccumulated capital is spatio-temporally fixed – across both circuits of accumulation and uneven geographies. For example, infrastructure may become obsolete due to technological change or less attractive under shifting geopolitical conditions. Similarly, investment in buildings gradually loses value through physical deterioration or as part of the broader downgrading of urban areas (Gotham, 2009). This tendency towards devaluation is closely linked to capital's drive to reduce turnover time and to search for faster-circulating outlets (Harvey, 2014). Yet the gradual or abrupt devaluation of spatial fixes also creates conditions for their subsequent revaluation, as uneven development opens ‘valleys’ of profitable reinvestment in the built environment – rendering capital's movement a ‘locational seesaw’ (Smith, 2010).

The devalorisation of fixed capital then creates a new necessity for restoring profitability within the secondary circuit (Harvey, 2001). This can be pursued through, among other means, labour devaluation in the form of underemployment, wage suppression, labour intensification, subcontracting and the general extension of precarious labour (Herod, 1997). Labour flexibilisation is a central aspect of this strategy, though not all flexible work is precarious. In this context, flexibilisation refers to replacing stable employment with variable arrangements in working time (e.g., part-time), contract duration (e.g., temporary), contractual dependence (e.g., subcontracted or agency work) and place of work (e.g., shifting locations or remote work) (Eurofound, 2020). These arrangements enable firms to adapt quickly to changing market conditions (Standing, 1989) while also facilitating surplus-value extraction, especially when coupled with processes of labour precarisation (Wilson, 2020).

Spatial fixes convert capital devalorisation into labour devaluation in highly uneven geographical terms (Ekers and Prudham, 2017). In weaker institutional contexts, flexibility largely translates into insecurity; therefore, spatial fixes in these contexts are more likely to produce labour precarity. This is the case, for instance, in Southern EU countries, where labour markets have undergone prolonged ‘low-road’ flexibilisation (Gialis et al., 2017). By contrast, stronger welfare states have managed, to some extent, to combine flexibility with adequate labour security – as in ‘flexicurity’ (Sahnoun and Abdennadher, 2019; Richardson, 2025). The result is pronounced cross-regional and cross-national inequalities. These have been further exacerbated in the aftermath of the 2008/2009 crisis, when labour market reforms in Southern EU countries sought even deeper flexibilisation, foregrounding labour cost reductions as a remedy for low competitiveness (Gialis and Leontidou, 2016).

Equally important, these inequalities manifest unevenly across sectors. For example, efforts to maintain profitability within the secondary circuit prompted work flexibilisation and precarisation in the construction sector even before the recent crisis (Gotham, 2009). In essence, this strategy does not differ significantly from those in manufacturing. Since variable capital (i.e., wages advanced to labour) is the component that generates new value, the value of constant capital (machinery, buildings, materials) is instead transferred to the final product and gradually diminished during production. Investment in new spatial fixes raises the organic composition of capital and thus contributes to a general downward tendency of profit rates (Marx, 2019). Consequently, the devaluation of labour, relative to the gradual devaluation of spatial fixes, becomes a central mechanism for maintaining profitability in sectors beyond construction.

More broadly, from the 1970s onwards, capital has persistently sought to confront overaccumulation through geographical expansion and the mobilisation of new social and natural resources. This trajectory has paved the way for what is commonly described as globalisation – not as a single or unified spatial fix but as a multiplicity of successive spatio-temporal fixes (Jessop, 2006). Crucial here has been the role of financialisation, understood as the deepening penetration of financial markets into new fields of accumulation and the proliferation of increasingly complex investment schemes across multiple asset classes (Harvey, 2014). Specifically, financialisation and financial deregulation have delinked real estate capital from construction activity (Beauregard, 1994) and enabled the accumulation of fictitious capital (e.g., derivatives linked to housing loans and real estate investment trust [REIT] shares; Christophers, 2022). This shift has allowed urbanisation to surpass industrialisation as the primary growth model across a wide range of geographical contexts (Harvey, 1982), while simultaneously fuelling major housing bubbles that culminated in the 2008/2009 Global Crisis (Gourzis and Alexandri, 2026).

Touristification as a spatial fix

Touristification can be understood as both a logical continuation and an integral component of the aforementioned regime of accumulation, as the tourism industry has grown in significance in recent decades within contemporary accumulation strategies across much of the Global North (Fletcher et al., 2019). As such, despite being primarily associated as a concept with the urban context, touristification concerns entire economies (Cocola-Gant et al., 2025). Essentially, touristification encompasses the proliferation of tourism-related land uses, for instance, through extensive renovation of existing land uses, new construction and the expansion of relevant infrastructure. Importantly, its material requirements necessitate significant capital investment in the built environment, given that tourism's raw material is (cultivated) physical space (Yrigoy, 2023). In the literature, touristification mainly manifests as the expansion of short-term rentals at the expense of housing, maximising rent extraction, raising property values and ultimately displacing populations (Wachsmuth and Buglioni, 2024). However, it also encompasses the growth of hotels, food and drink and other tourist services, thus involving significant economies of scale (Yrigoy, 2023).

The state has played a crucial role in the co-development of touristified landscapes. Re- and deregulation of labour markets has enabled tourism businesses to rapidly absorb surplus labour, especially from sectors under stress during recession (Mosedale, 2011). Likewise, deregulation of housing markets has accelerated the dispossession and assetisation of housing (Iacovone, 2025), while entrepreneurial planning regimes have favoured tourism-related land uses (Katsinas et al., 2025). Investment-for-residency schemes (e.g., Golden Visas) have also attracted circulating transnational capital into local housing markets (Aalbers, 2019). As in previous rounds of capital switching, financialisation remains central, with the state generally pursuing further deregulation of financial markets. Consequently, housing is increasingly treated as a financial asset, converted into digitally mediated short-term rentals by individual and institutional investors through complex schemes such as REITs, family offices and private equity firms (Cocola-Gant et al., 2025). Similarly, financial capital – often without prior links to tourism – has flowed into the lodging industry (Yrigoy, 2023). Thus, touristification cannot be separated from previous growth models that favoured urbanisation backed by financialisation at the expense of industrialisation (Wijburg et al., 2024).

In contexts such as Southern Europe, this transition unfolded as a reinforcement of accumulation by dispossession (Harvey, 2014). There, construction-driven growth models, sustained in some cases for several decades before the crisis, led mainly domestic capital to territorialise in the form of large accommodation units and transport hubs, cultivating advanced tourism landscapes (Gourzis and Gialis, 2025). As the dust from debt restructuring and shock austerity measures settled, the construction sector lost most of its dynamism, and touristification emerged as a panacea against recession (Mendes, 2018). The extant infrastructure, having lost part of its value during the deep recession of the early 2010s, became an attractive target for transnational capital, whose inflow signified a new round of accumulation (Yrigoy, 2023). The adverse conditions under which labour was absorbed in this process do not constitute an exceptional situation, nor do they relate simply to tourism being a labour-intensive sector. Rather, they reflect conscious efforts to offset fixed capital devalorisation, with touristification formalising precarious labour as a structural component (Bobek et al., 2021). These factors render touristification a key form of contemporary spatial fix (Yrigoy, 2023). Moreover, the process's association with housing crises and real estate or construction bubbles eloquently embodies the contradictory and crisis-prone nature of spatial fixes (Harvey, 2014).

The case of Greece

The above dynamics are highly relevant to Greece's post-war growth model, where construction has played a pivotal role in the regime of accumulation (Kokkinou and Psycharis, 2004). Not only did it drive the country's rapid urbanisation as early as the 1950s (Getimis and Giannakourou, 2014) but after the 1970s Oil Crisis and amid international trends of deindustrialisation, it absorbed overaccumulated capital from a stagnating manufacturing base that relied mainly on multinational subsidiary companies (Vetta, 2014). A central component for construction's growth has been ‘antiparochi’, a practice whereby landowners provide plots to developers in exchange for a share of the newly erected building's units (Leontidou, 1990; Gialis et al., 2025). During the 1980s and 1990s, investment aimed to modernise infrastructure to support industrial development, with the state providing incentives for relocating manufacturing from cities to specially designated industrial areas. Nevertheless, the spatial logic of capital was mainly manifested through urbanisation and suburbanisation (Getimis and Giannakourou, 2014). From the mid-1990s, preparation for the 2004 Olympic Games drove large projects – Athens's new airport, metro and ring motorway system (Sfakianaki et al., 2015) – alongside efforts to rationalise urban space and attract investment in energy, telecommunications, real estate, construction and tourism (Leontidou, 1990; Petroutsatou and Giannoulis, 2022). With Greece's adoption of the common currency and interest rates reaching historic lows in the early 2000s, this model became increasingly speculative; mortgages largely replaced antiparochi, while developers began initiating new projects without having sold previously built units, relying on the continuous appreciation of property values to secure financing and future profits (Sfakianaki et al., 2015).

When the crisis struck, the fragility of this model triggered a deep recession (Lapavitsas, 2014). Gourzis and Gialis (2019) have shown that capital switching took a ‘disrupted’ form, shorter and more abrupt than in other Southern European economies, reflecting the particular vulnerabilities of a construction-led growth model that had already reached its limits by the onset of the crisis. In response, the state pivoted towards tourism, leveraging existing infrastructure and providing businesses with cheap labour. Work re-/de-regulation became a key component of economic adjustment programmes. Although already deregulated, the Greek labour market was presented as highly rigid, with reforms involving further dismantling of employment protection, lowering wages (e.g., establishing a ‘sub-minimum’ wage for young workers), providing incentives to businesses to adopt more precarious work arrangements (such as internships or publicly funded vouchers) and limiting access to reduced social benefits (Gialis and Leontidou, 2016). The state supported post-crisis touristification by implementing policies to attract foreign investment in real estate, such as the Golden Visa programme, while promoting housing financialisation through mortgage liberalisation and the securitisation of non-performing loans (Bank of Greece, 2024).

Methodology

Below, we employ a multi-scalar comparative analysis divided into three empirical steps. Insofar as spatial fixes are enacted through capital switching between the primary and secondary circuits, and as neither process lends itself to direct measurement through a relevant statistical variable, our empirical approach relies on proxies widely used in geographical political economy (Christophers, 2011; Kutz, 2016; Gourzis and Gialis, 2019). The purpose is not to measure fixes in a deterministic sense, but to detect the material tendencies through which capital becomes anchored in the built environment, and labour relations are reorganised accordingly.

First, we examine Gross Fixed Capital Formation (GFCF) at the national level – the only level such data is available – per main asset type from 1995 to 2024, focusing on total construction 1 and further breaking it down to dwellings 2 and other buildings and structures 3 . Empirically, construction GFCF captures the share of investment directed to the built environment relative to total investment and labour costs. By absorbing idle or devalorising capital, it serves as a proxy for spatial fixes.

To complement this analysis, and drawing from prior studies (Christophers, 2011; Kutz, 2016; Gourzis and Gialis, 2019), we calculate the Building Share index for Greece and the Eurozone by dividing GFCF in total construction by GFCF in all asset types (including total construction, machinery, equipment, weapons systems and intellectual property products) minus cultivated biological resources, plus labour costs. Following Harvey (1978, 1982) and later operationalisations (Christophers, 2011; Kutz, 2016; Gourzis and Gialis, 2019), we read rising construction investment under industrial stagnation (Maniatis and Passas, 2013) not as evidence of an attempt to resolve overaccumulation trends -as this would require a more thorough analysis of difficult to measure phenomena-, but as capital's attempt to stabilise through spatial-temporal displacement, converting liquidity into long-lived assets that defer devaluation. According to this approach, an increase in this ratio suggests a possible reorientation of accumulation from the primary circuit – industrial production – to the secondary circuit of capital – investment in the built environment. As far as these circuits are empirically intertwined, the Building Share functions as a proxy: rising shares may suggest capital switching into the built environment, while declining shares may imply contraction or devaluation in the secondary circuit. It could therefore be read as a signal of shifting accumulation priorities, not as definitive proof of a completed switch.

The temporal scope spans from 1995 to 2024, capturing key phases in Greece's recent economic history: the lead-up to the 2004 Olympic Games, the peak of the country's construction-driven growth model in the mid-2000s, the effects of the 2008/2009 Global Crisis and the economic adjustment programmes 4 upon the country's economy, and the COVID-19 pandemic (KEPE, 2018; IOBE, 2025). This scope aligns with the duration of long investment cycles, which typically last 20–25 years (Harvey, 1982), thus capturing distinct phases of the recent economic cycle. Specifically, it covers Greece's pre-crisis expansionary period (peaking in 2008), deep recession (peaking in 2014), weak recovery (lasting until 2019), an emergent event that largely halted the latter (the COVID-19 pandemic that reached Europe in early 2020) and a post-pandemic period of economic rebound (KEPE, 2018; IOBE, 2025).

As a second step, we examine the regional concentrations of the two most prominent forms of Greece's low-road to flexibilisation (part-time and temporary employment 5 ) vis-à-vis their less-/ non-precarious employment counterparts (full-time and permanent work) in manufacturing, construction and accommodation and catering. 6 This step helps us to scrutinise labour devaluation and its geographical scope is narrowed down to Attica and South Aegean, which are then contrasted with the rest of Greece. Methodologically, we draw from the Location Quotient (LQ) 7 , dividing the proportion of a sector within a given employment type at the regional level by the respective proportion at the national level. 8 This shows the extent to which specific sectors absorb a given type of flexible or stable employment, benchmarking regional distribution against the broader national context. Complementing this methodology, we also examine the shares of the aforementioned employment types within each of the aforementioned sectors and regions. By contrast to the LQ, calculating the shares of part-time and temporary employment within total waged employment shows the extent to which each sector relies upon poor forms of flexible employment.

This step is implemented for four benchmark years – 2008, 2014, 2019 and 2023, which represent turning points in Greece's recent economic cycle. As noted above, labour flexibilisation in the South EU context and Greece in particular has almost always coincided with the expansion of precarious or atypical labour, being realised under adverse conditions that include significantly lower wages, slashed social benefits and labour rights. For their part, Attica and South Aegean serve as illustrative regional cases. Specifically, the former refers to the country's capital region, concentrating the bulk of economic activity and diachronically showcasing the country's growth models. The latter is chosen as the country's – and the EU's – most touristified region (Gourzis and Gialis, 2019, 2025). Similarly, construction, tourism and manufacturing serve as key sectoral cases: the first two uphold a central position in the Greek economy, while juxtaposing them to manufacturing serves as a proxy for instances of capital switching. 9 Notably, they also encompass diverse capital/labour requirements. Construction combines labour- and capital-intensive characteristics, depending on the project type, technology and local conditions. Specifically, large-scale and infrastructure projects require substantial capital investment, while smaller-sized projects and renovations do not; similarly, on-site construction is labour-intensive while the off-site planning and fabrication of materials is mostly capital-intensive (Sibikovskyi et al., 2024). In Greece, where construction projects are mostly small-sized and materials are imported, labour volume and competence of the workforce within the building trades constitute the most crucial components (IOBE, 2025). For its part, tourism is labour-intensive, with core activities relying heavily on customer service, allowing limited opportunities for technological substitution (Sharma et al., 2016). Lastly, manufacturing constitutes a capital-intensive sector, generally articulated through investment in technological upgrading, including automation (Choi and Kim, 2005).

Lastly, the third step of the analysis uses GFCF data per sector (instead of per asset type), focusing on investment volumes in manufacturing and construction, as well as the grouped sector of commerce, storage, transportation and accommodation and catering (the latter as an approximation of tourism-related GFCF 10 ). Specifically, for each of the key sectors and regions under study, GFCF is juxtaposed with flexible employment, allowing us to examine investment patterns in conjunction with the labour devaluation. This, in turn, provides crucial empirical evidence for Greece's recent increase in tourism dependence and deepening touristification. 11

All data has been retrieved from Eurostat; specifically, GFCF from National Accounts and employment data from the Labour Force Survey.

Empirical analysis

Capital switching and shifting domestic growth models

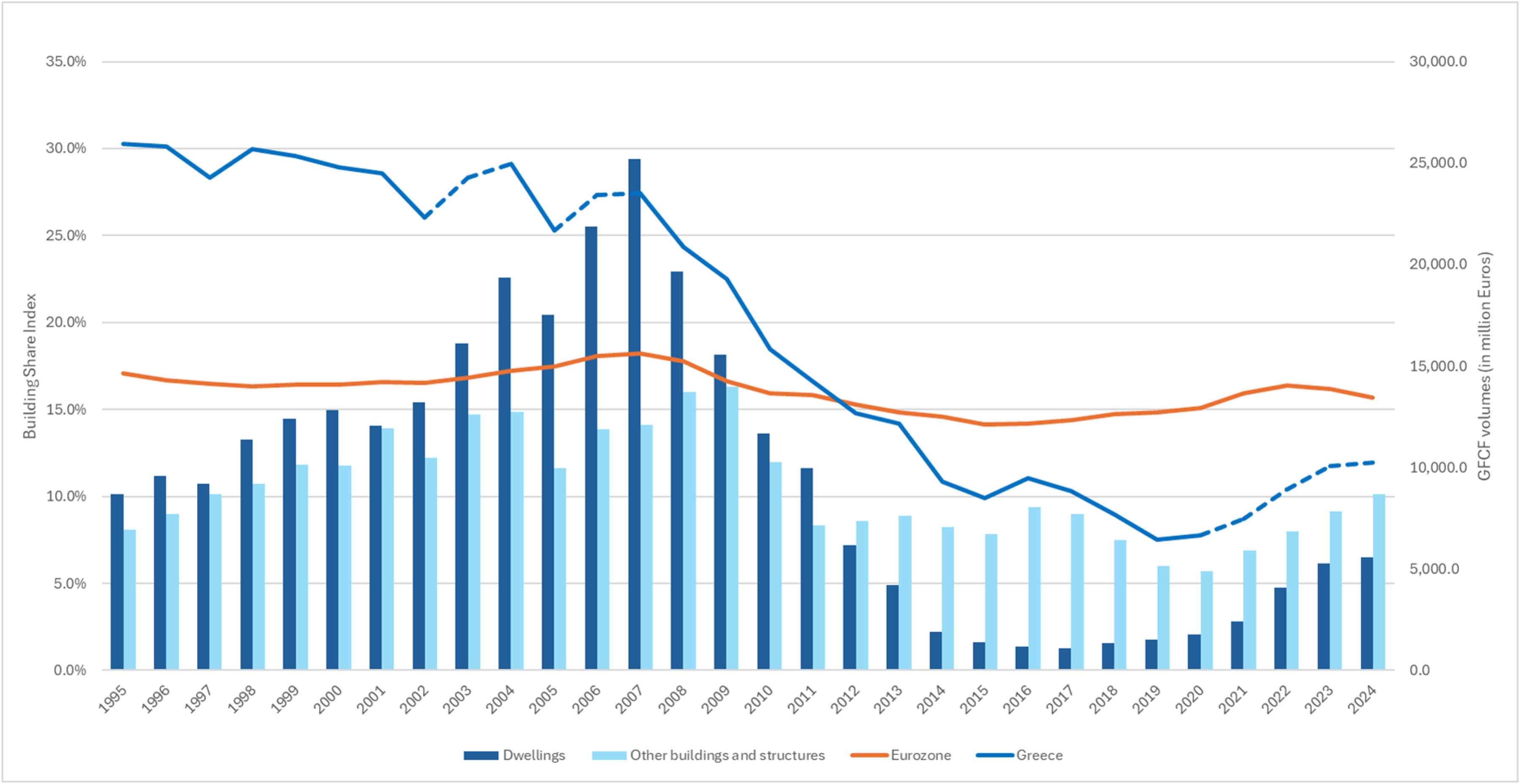

The Building Share showcases that, in Greece, investment in the built environment dominated fixed investment for a long period. Figure 1 shows that this type of investment was prominent in the overall mix already in 1995 (over 30%) and almost double that of the Eurozone (17%). Specifically, after receding temporarily during 2001–2002, a new round of expansion occurred, which, interestingly, was driven by housing construction despite the country approaching the 2004 Olympic Games. In the aftermath of the Olympics and before the onset of the crisis, the index remained relatively stable (above 25%, compared to about 18% for the Eurozone), with housing investment offsetting falling volumes of GFCF in infrastructure and other structures. Therefore, this period did not record a further inflow of capital into the secondary circuit but rather saw attempts of capital switching, which were however, eventually disrupted (also see Gourzis and Gialis, 2019).

The Building Share Index in Greece and the Eurozone, and Gross Fixed Capital Formation (GFCF) volumes in dwellings and other buildings and structures in Greece.

The deep recession of 2009–2014 marked a sharp rupture in the above trajectory, as the index plummeted by 15 percentage points between 2007 and 2015, while it must be noted that this trend commenced before the Greek sovereign debt crisis. Comparing this with broader trends in the Eurozone (there, the index fluctuated around 14%) highlights the uneven effect of the crisis. Namely, core economies kept investment in housing relatively subdued, and despite stagnant wages, managed to protect capital in the secondary circuit (Kotios and Roukanas, 2012).

Greece's weak recovery during 2015–2019 saw the index's values decreasing further (reaching 8%), as opposed to the Eurozone (where it slightly increased to 15%). Importantly, Greece's persistently low values indicate that investment in the built environment even lagged behind labour costs, which were also compressed at that time. Even more importantly, the country's touristification at that time – mainly relying on renovations of previously residential apartments (Pettas et al., 2024) – was not captured at all by the index or investment volumes in housing, as it should be, probably due to the informal character of such building activities in Greece (IOBE, 2025). Overall, the index's retraction in Greece post-2007 is mainly caused by falling investment in housing, with the annual volume of investment in other construction remaining relatively stable between 2011 and 2017. During 2017–2020, however, this trend was somewhat subverted, with the latter type shrinking and investment in housing stabilising and even expanding a bit; nevertheless, the overall index's value kept decreasing.

The post-pandemic recovery of 2020–2023 saw the index's value finally increasing (from 7% to 12%). Notably, for the first time since the 1995–2000 period, the volumes of both types of investment within construction were recorded expanding simultaneously, although this time the volume of investment in other structures was larger than housing investment. This suggests a structural shift, as will be discussed below (IOBE, 2025).

Flexible employment within key sectors and regions

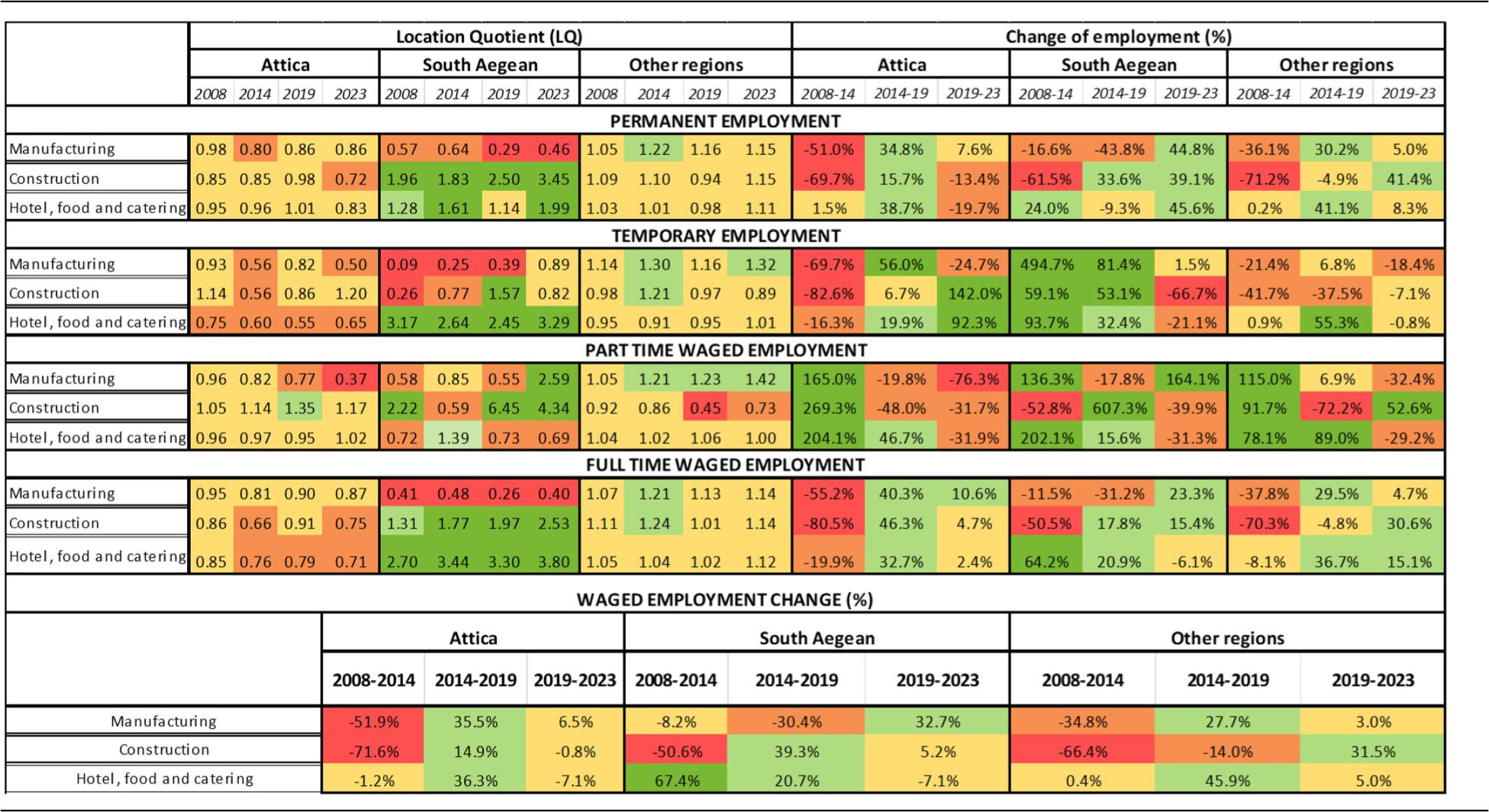

Manufacturing, construction and tourism have absorbed much of the cumulative impact of the successive shocks of the past 15 years, namely, the deep recession of 2009–2015, the lockdown period of 2020–2022 and the subsequent energy crisis (Stathakis and Baltas, 2024). Yet, Table 1 showcases distinct spatio-temporal trajectories of labour underutilisation across these sectors.

Location Quotient (LQ) index and change of employment (%)for part-time and full-time, temporary and permanent waged employment in manufacturing, construction and tourism for Attica, South Aegean and Greece's other regions. 15

In Attica, not only full-time and permanent employment are consistently under-represented across all three sectors but their position recedes over time. On the contrary, construction is the main sector absorbing disproportionate volumes of part-time (LQ value of 1.35 in 2019) and temporary employment (1.20 in 2023) in comparison to the sector's flexibilisation at the national level. Manufacturing and tourism display lower relative concentrations of both part-time and temporary work; this implies that other sectors (e.g., commerce) have mostly absorbed these types, as well as that Attica's flexibilisation in the two sectors pales in comparison to broader trends.

In South Aegean, construction and accommodation-and-catering display high LQ values in all waged employment types. This showcases the dominance of these two sectors within the region's unbalanced labour market – a pattern consistent with the recent, largely uncontrolled tourism-driven urbanisation there (Katehaki, 2025). Specifically, part-time work is over-concentrated in construction (6.45 in 2019), while, as expected, temporary employment is over-concentrated in accommodation-and-catering (3.29 in 2023). Simultaneously, accommodation-and-catering also over-concentrates full-time employment (3.80 in 2023), illustrating the seasonal yet full-time nature of tourism work in Greece's island regions. Interestingly, following the pandemic, part-timerism became prominent in manufacturing (2.59 in 2023), likely linked to the region's small, tourism-oriented secondary activities (Stamatiou, 2024).

In the rest of Greece's regions, part-time and temporary work is similarly over-concentrated in manufacturing. Construction and tourism show no significant over-concentration of specific employment types, suggesting more balanced labour markets compared to Attica and South Aegean.

Turning to changes per type and period, Table 1 shows that during 2008–2014, waged employment contracted in all three sectors under study. Specifically, Attica recorded the steepest losses in construction (–71.6%) due to a collapse of permanent (–69.7%) and full-time (–50.5%) employment therein, while part-time employment was surging (+269%). A decline occurred in South Aegean (–50.6%) as well, albeit not combined with a surge in part-timerism. A similar trend is observed regarding waged work in manufacturing, which contracted nationwide, with Attica documenting the steepest losses (–52%) and combining this with part-timerism's expansion (+165%); South Aegean's manufacturing employment, albeit not contracting significantly, shifted strongly towards temporary jobs (+494%). In contrast to the previous sectors, tourism employment managed to remain stable nationwide and in Attica in particular, while South Aegean saw it expanding by 67.4% in total and part-time work therein by 200%. A similar increase was documented in part-timerism in the sector in Attica (+204%) and Greece's other regions (+78%).

During the phase of recovery (2014–2019), waged employment began to rebound in most sectors, with tourism standing out (+36.3% in Attica, 20.7% in South Aegean). Tourism's boom generated full-time and permanent employment as well, although temporary and part-time employment generally outgrew the latter. Similarly, waged employment in manufacturing expanded in most regions (by 35.5% in Attica and 27.7% in Greece's other regions), with this growth translating mostly into permanent and full-time jobs. Construction also recovered (+31.5% in Greece's other regions and +5.2% in South Aegean), but with contrasting dynamics between South Aegean and Attica: in the former, this stemmed from a surge in part-timerism (+607%), while in the latter from temporary employment (+142%).

During the study's final period (2019–2023), changes in total waged employment were milder across all sectors and regions. Manufacturing in South Aegean stands out (+32.7%), regaining much of its earlier losses, primarily through a sharp rise in part-time (+164%) and permanent (+44.8%) employment. In contrast, in Attica and Greece's other regions, the sector kept relying on stable, long-term positions, despite failing to reach its pre-crisis levels. Conversely, construction remained stagnant in both Attica and South Aegean, with the latter region seeing employment in the sector shifting from temporary and part-time towards permanent work. In contrast, Attica's construction work shifted from permanent and part-time towards temporary employment. Lastly, waged work in tourism stabilised nationwide, with its composition similarly shifting. Specifically, South Aegean saw permanent employment expanding (+45%), while temporary (–21.1%) and part-time work (–31.3%) receded. In contrast, Attica saw temporary positions almost doubling (+92%).

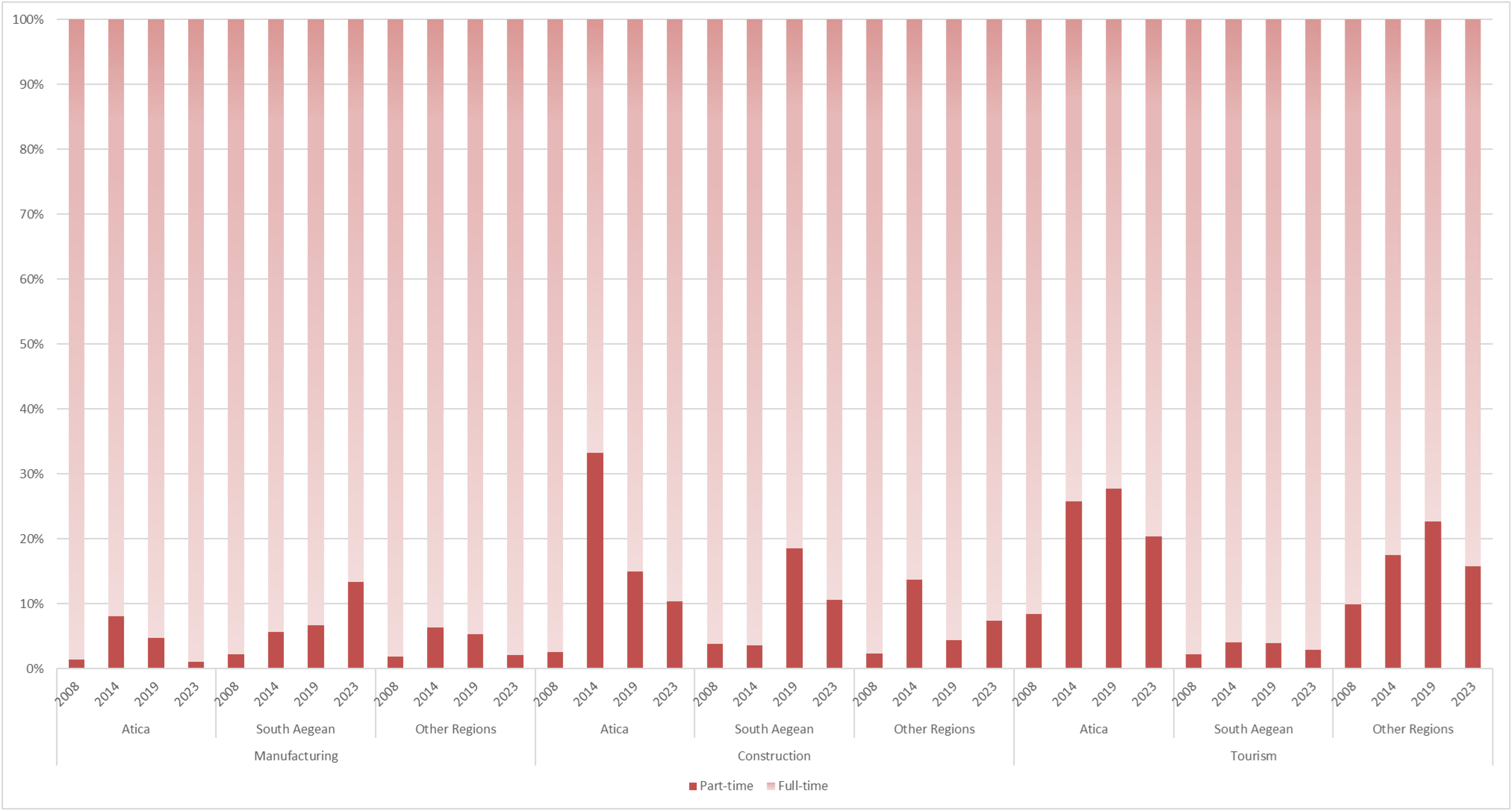

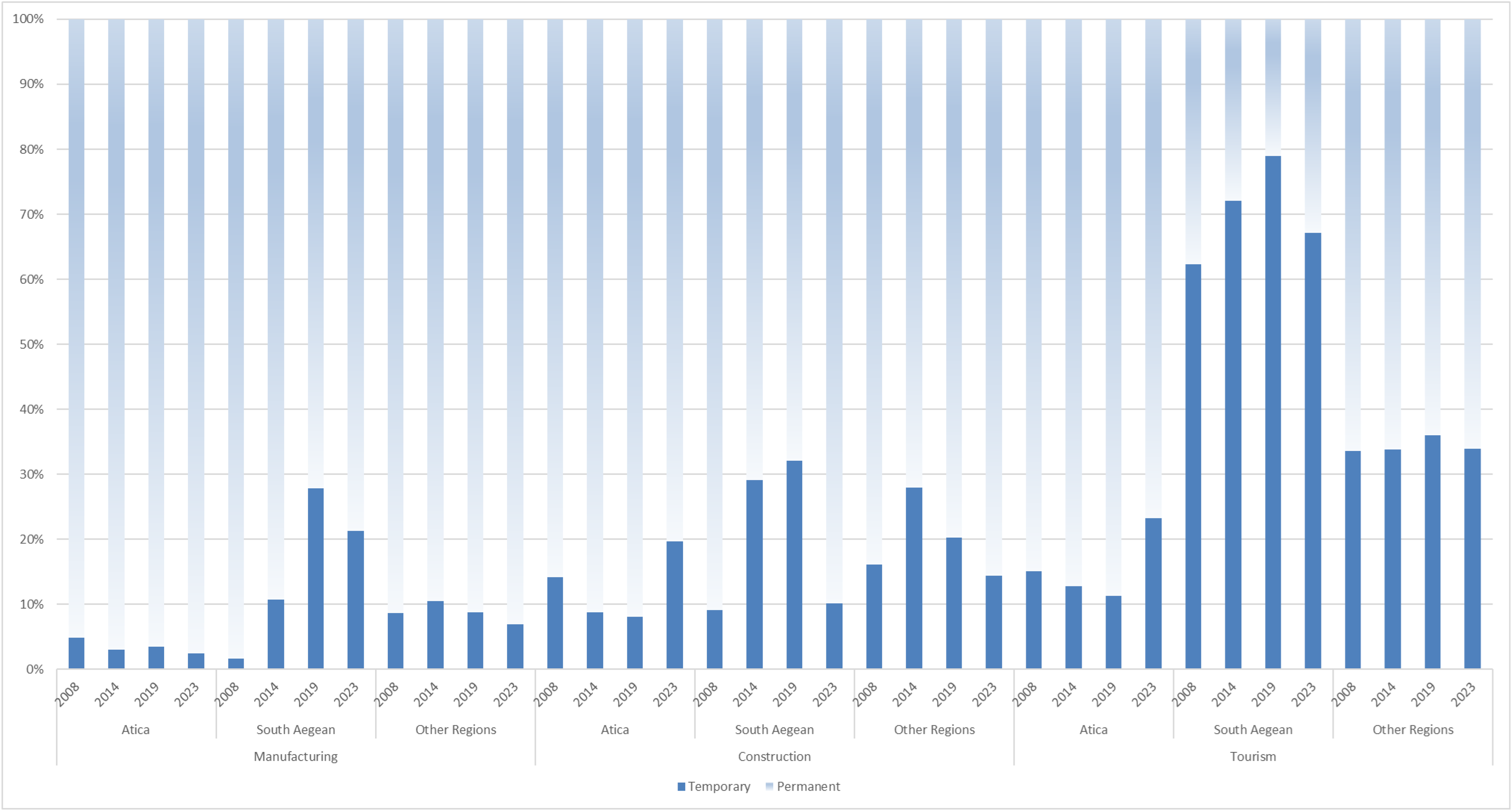

Lastly, looking into the shares of part-time and temporary waged employment, Figures 2 and 3 confirm that both types lag behind their counterparts (full-time and permanent, respectively) – however, there are clear indications of a nationwide shift towards labour flexibilisation. Specifically, waged part-timerism in tourism reached 30% in Attica and exceeded 20% in Greece's other regions in 2019, with this type being less important in South Aegean. As expected, the sector in the latter region is dominated by temporary employment (80% in 2019); in Attica, although this type is less pronounced, it has expanded significantly in recent years (from 10% in 2019 to more than 25% in 2023). In manufacturing, none type of flexible work stands out, except for temporary work in South Aegean (30% in 2019), reflecting the seasonality of most economic activities in island regions. In construction, both regions under study record prominent shares of waged part-timerism (35% in Attica in 2014 and 20% in South Aegean in 2019). Temporary construction work displays similarly high shares in both regions, although in South Aegean it shrunk abruptly between 2019 and 2023 (from 30% to 10%). The short-lived prominence of temporary work in construction relates more to the sector's cycles than to the effect of climate conditions – namely, a halt during winter, as is often the case in central and northern Europe (De Place Hansen and Larsen, 2011). In fact, although construction workers in Greece face serious hazards during the summer months, projects generally resume (Health and Safety International, 2026).

Part- and full-time share in total waged employment in manufacturing, construction and tourism, for Attica, South Aegean and Greece's other regions.

Temporary and permanent share in total waged employment in manufacturing, construction and tourism, for Attica, South Aegean and Greece's other regions.

Sectoral fixed investment vis-à-vis labour flexibilisation

Figure 4 shows the share of fixed investment in manufacturing, construction and tourism, as well as the share of part-time and temporary waged employment within those sectors. Doing so, it reveals the distinct growth profiles of Attica and South Aegean, as well as the way each has integrated labour flexibilisation.

Share of Gross Fixed Capital Formation (GFCF) (in total GFCF) and temporary and part-time (in total waged employment) in manufacturing (a), construction (b) and tourism (c).

Specifically, Figure 4(a) shows that fixed investment in manufacturing has been particularly prominent in Attica. There, it follows an expansionary trend (peaking at 20% in 2020), being underpinned mostly by stable employment; the trajectory's stark fluctuations can be attributed to the recession of the early 2010s and the lockdown measures of the early 2020s. In contrast, the sector's share of total fixed investment in South Aegean is small, remaining constantly below 5% and being underpinned by rapid labour turnover. As expected, GFCF trajectories confirm that the sector carries more significance in Attica, where larger investment in industrial machinery, IT and transport equipment, plants, warehouses, R&D property rights and other fixed assets indicates better performance and prospects (Abdikeev et al., 2019).

Figure 4(b) confirms that during 2009–2011, construction faced particularly adverse conditions in both regions. Plummeting fixed investment reflects construction firms making no investment in new facilities or transport equipment (Stan and Vintilă, 2021) at that time; however, it must be noted that such investment has been diachronically low in Greece (Petroutsatou and Giannoulis, 2022). After 2011, the two regions followed starkly different trajectories. Attica saw investment rebound until 2013, then plunge again until 2020, before expanding modestly; this trajectory has been supported by permanent and full-time employment, although part-time work exceeded 30% for some time during the deep recession, with temporary contracts stabilising at around 20% of total waged employment. By contrast, investment in South Aegean remained low until 2013, but has been expanding ever since (4% in 2022). During 2013–2016, this trajectory relied heavily on temporary employment (over 40%), while in 2021–2022, part-time work reached similar levels. Nevertheless, both types of flexible employment have since receded, indicating the proliferation of construction firms from within the region and year-round tourism-related construction activity (IOBE, 2025). Indicatively, in 2023, 30% of all building permits issued nationwide for hotels concerned South Aegean (ELSTAT, 2023).

Figure 4(c) showcases the dominance of commerce, transportation, storage and accommodation and catering 12 in the country's total fixed investment. Albeit referring to a wide and diverse spectrum of activities, the above share validates the central role of tourism in the Greek economy. This share was larger in Attica at the beginning of the study period (almost 30%) in comparison to South Aegean (15%), while the latter saw it expanding right before the pandemic (exceeding 40% in 2019). The above does not imply that the South Aegean lacked tourism activity before 2020; rather, tourism enterprises became larger and more investment-oriented (Bank of Greece, 2024). Although the two regions’ trajectories have converged over time (around 25% in 2022), they differ significantly regarding the type of flexibilisation they have integrated. Attica has mainly drawn on part-timerism (30% during 2017–2021), although the two types of flexible work have converged over time at around 20%. By contrast, the seasonal but intense tourism activity in South Aegean has inflated temporary employment (consistently over 60%).

Discussing touristification as a spatial fix

Drawing on the conceptual framework and empirical analysis, two key points emerge. First, the Greek economy extended its dependence upon extracting value from the built environment, shifting its focus from housing to other construction. This, we argue, does not simply further the country's pre-existing tourism dependence, but signifies touristification becoming a new form of capital's spatial fix in the Greek context. Second, that touristification is accompanied by deepening labour devaluation. This, we suggest, does not simply refer to the labour-intensive character of the sector but stems from the inherent devalorisation of capital within the secondary circuit. As part of the above argumentation, we postulate that trends in Attica and South Aegean constitute complementary expressions of a unified accumulation regime.

Already in the first post-war years, the country's growth model was driven by tertiarisation and a spontaneous and rapid urbanisation (Getimis and Giannakourou, 2014). As foreign capital waned – including funds received through the Marshall Plan and subsidiaries of multinational companies (Vetta, 2014) – development shifted from being investment-led to consumption-based (Loizos, 2025). This unfolded within a weak developmental state that avoided structural reform and diverted capital away from productive investment in machinery and technological equipment. As a result, Greek industrial firms remained small, cut off from credit and weak regarding innovation – such shortcomings characterise them to this day (KEPE, 2018). Instead, this model fostered a myriad of small-scale, family-owned firms in construction (IOBE, 2025), although quite rapidly, larger construction companies were established (Antonopoulou, 1987). Similar trends were also observed in tourism (Sarantakou and Terkenli, 2021). Equally important, this type of growth gave birth to a heterogeneous class of rentiers (‘rantierides’). Specifically, within the context of extensive fragmentation of land ownership – as a result of the land reforms of the mid-1920s and early 1950s, along with the country's distinctive insular and mountainous geography – antiparochi provided landowners with multiple apartments in newly constructed buildings (Sarantakou and Terkenli, 2021). Rantierides spanned from the petite bourgeoisie to wealthier social strata, deriving income from rents, bonds and interest (Tsiaras, 2015); in this sense, Greece had developed an idiosyncratic version of rentier capitalism (see Christophers, 2022) as early as the first post-war years. This should not be seen independently of the country's inability to avert deindustrialisation trends after the 1970s Oil Crisis; the latter indicates that significant capital switching occurred in Greece before the onset of our analysis's temporal scope, hence the significantly higher values of the Building Share in comparison to Eurozone's aggregate in 1995.

Then, Greece's spatial fixes of the late 1990s and early 2000s should not be attributed solely to a pre-Olympics construction fever – although this certainly played a key part. Rather, they comprise a long-standing characteristic of Greek capitalism. However, Greece's entrance to the Eurozone eased firms’ access to cheap credit, slashing transaction costs and interest rates, combined with banking liberalisation (Sfakianaki et al., 2015). As such, the growth model of previous decades, which mainly drew on antiparochi, was significantly altered. Specifically, deepening financialisation supported short-term growth (Oltheten et al., 2013), with construction becoming increasingly speculative (Gourzis and Alexandri, 2026). The widespread uncertainty that preceded actual austerity measures around 2008 slowed down housing investment, as reflected in the Building Share's decline. Moreover, such growth proved particularly fragile against Greece's sovereign debt crisis, as construction firms saw their credit flow being cut and many were driven out of business (IOBE, 2025; Sfakianaki et al., 2015). This flagship sector's contraction became systemic (Hardouvelis, 2009), which helps explain the limited presence of construction capital in the country's subsequent touristification – at least until the end of the decade – unlike in the rest of Southern Europe (for Spain, see Yrigoy, 2023).

This period marked a partial restructuring of Greek capitalism under external supervision (Lapavitsas, 2014), although the shrinking share of investment in the built environment does not reflect efforts for industrialisation (KEPE, 2018); instead, a new cycle of accumulation, initially by dispossession (see Harvey, 2014) rather than geographical expansion. Specifically, the founding of the Hellenic Republic Asset Development Fund in 2011 sought extensive privatisations of public property (Katsinas et al., 2025), while the Greek Golden Visa programme sought to attract international investors, particularly in real estate. Moreover, the introduction of a Uniform Real Estate Property Tax in 2014 turned housing from a safety net for the Greek households to a burden. Apart from distressed households losing their primary residence – a trend accelerated by e-auctions being introduced in 2015 – many sought to liquidate their property (Adamopoulou et al., 2025).

Nevertheless, it was only after 2016–2017, when default concerns had receded, that foreign investors – both institutional and individual (e.g., family offices, REITs and funds) – were convinced to enter the market (Gourzis and Alexandri, 2026). Subsequently, an informal short-term rental sector, initially mobilised by Greek households, began to professionalise through the inflow of transnational capital. In this context, the state introduced legal frameworks to facilitate this transformation (Pettas et al., 2024). The above was promptly reflected in the Building Share expanding once again, only this time driven by significant infrastructure that was initiating or being completed at the time (e.g., Thessaloniki's metro network, Athens's metro expansion, key motorway systems and energy infrastructure; Enterprise Greece, 2025), large-scale urban redevelopment (e.g., the Ellinikon Project in Athens’ Riviera) and hotel units (Stamatiou, 2024). Moreover, since the pandemic, investment in housing has begun to follow broader construction trends, reflecting the renovation or development of residences intended for short- or medium-term rentals to accommodate – among others – an inflow of digital nomads (see Wachsmuth and Buglioni, 2024).

Overall, the above reinforces extant patterns of uneven development, with metropolitan and island regions with mature tourism products benefiting from targeted spatial interventions, while peripheral and industrial regions remaining largely stagnant (Gialis et al., 2017). Moreover, the above outlines a profound touristification, which resonates with the trajectories of many other Southern European countries, such as Spain (Yrigoy, 2023) and Italy (Iacovone, 2025). Nevertheless, Greece has been deeper in terms of spatial and social impact (Gourzis and Gialis, 2025), despite institutional investors still preferring better-regulated contexts like Barcelona's, which has put a cap on the number of licences of short-term rentals since the mid-2010s (Cocola-Gant et al., 2025). Greece's deeper touristification has been attributed to extant spatial fixes facilitating the tourism industry, such as transportational infrastructure in remote locations, as well as areas of secondary residences, which were converted into tourism uses en masse (Gourzis and Gialis, 2025). Equally important, this has to be attributed to a loose regulatory framework, which has favoured tourism investment. Indicatively, large hotel units have exploited memoranda-induced flexible land-use regulation 13 to operate even within nature protection areas (Katsinas et al., 2025). Measures putting tourism development in check have been introduced only recently, including blocking property acquired through the Golden Visa programme from being channelled into the short-term rental market and prohibiting such listings from operating in certain parts of Athens. Policies countering the heavy cost of this model are equally recent, including subsidising low-interest loans for citizens to buy their first home or for owners to renovate their property and rent it long-term. Nevertheless, most of those measures have not only come belatedly but they have often generated opposite-than-intended effects, exposing an inherent contradiction of Greece's current growth model; a decline in property prices would harm homeowners, who constitute a substantial proportion of Greek citizens, as well as investors (Poula, 2025).

The above outline touristification's role as a key form of spatial fix in post-crisis Greece, playing a key role in the revalorisation of capital in the secondary circuit from around 2016–2017 onwards (REMAX Greece, 2017). Initially, this growth model was not reflected in significant new spatial fixes, as extant ones were being repurposed. However, over the course of the last decade, housing and other forms of real estate turned into new asset classes and were embedded in transnational circuits (Wijburg et al., 2024). Despite the country's priorities being reoriented from construction to tourism, it must be stressed that this shift did not subvert a prior underlying spatial/financial logic, whereby value is primarily extracted through the production of the built environment. In contrast to the pre-crisis dominant position of domestic construction capital, however, under this regime of accumulation, value extraction is largely and directly controlled by a transnational tourism-related capital (Christophers, 2022).

Resonating with relevant theory, labour devaluation continues to play a key role in capital accumulation within the secondary circuit (see Harvey, 2001). Indeed, over the past 15 years, the state has emphasised employability at the expense of employment quality, extending pre-crisis patterns of extensive informal employment within the key sectors of construction, commerce and small-scale urban manufacturing (KEPE, 2018). Interestingly, our analysis highlighted traditional forms of informality being replaced by fixed-term contracts and part-timerism. Specifically, amid collapse, the country's prominent construction sector pre-crisis seems to have started integrating part-timerism, a form that is not intrinsic in the building trades (Sfakianaki et al., 2015). Simultaneously, tourism has replaced much of its pre-crisis informality – for instance, reliance on family helpers (Sarantakou and Terkenli, 2021) – by absorbing a large share of the workforce laid off during the deep recession. In a pattern observed across various geographical contexts and over time (Mosedale, 2011), and despite recording surging profits and receiving subsidies through the Recovery and Resilience Facility 14 , the industry has internalised extreme seasonality, long working hours and virtually no days off during the high season, even for highly sought-after workers. The latter conditions are regulated through very precarious flexible forms; at the same time, contract breaching, unpaid overtime and undeclared labour are also documented frequently (Gourzis and Gialis, 2025). Overall, rapid labour turnover amid a tourism renaissance and extensive labour underutilisation amid a renewed construction boom should not be viewed as stabilising mechanisms but rather as manifestations of a structural shift in labour organisation (Sahnoun and Abdennadher, 2019).

It is striking that manufacturing, in contrast, has not internalised such arrangements, despite being under constant stress since the early 2000s (KEPE, 2018). For one, this highlights the labour-intensive character of construction and tourism (Sharma et al., 2016). Moreover, labour devaluation constitutes an enduring organisational mechanism under conditions of uneven and anaemic recovery (Gialis et al., 2017). However, observing tourism and construction functioning as labour reservoirs, periodically absorbing and releasing surplus labour along long economic cycles, renders clear that flexibility and precarity intertwine therein as structural components (Mendes, 2018). This observation retains its hermeneutical value, even though these dynamics exhibit notable spatial differentiation. Specifically, our analysis highlighted the divergent trajectories of Attica and the South Aegean: the former, characterised by a robust service sector and its recent emergence as a standalone urban tourism destination, deepened working-time flexibility. The latter, remaining centred on tourism and incorporating its informal dimensions into transnational circuits, accelerated labour turnover and cyclical workforce mobilisation. Therefore, despite their markedly different economic bases and forms of labour organisation, precarity emerged as pervasive in both, revealing complementary expressions of a shared accumulation regime.

Conclusions

In recent decades, investment in tourism has not only gained significant traction but has also emerged as a central mechanism through which contemporary capitalism reorganises space during periods of crisis (Mendes, 2018). At the same time, housing and the built environment more generally have become key sites of capital accumulation (Wijburg et al., 2024). In this article, we sought to highlight how the adaptation of fixed capital to tourism-related uses and the expansion of labour devaluation constitute closely intertwined processes. Combined, these dynamics consolidate post-crisis models of accumulation grounded in controlled precariousness and entrenched spatial inequality, with tourism functioning as the dominant spatial fix, systematically transferring instability onto labour.

To illustrate the above, we examined the case of Greece. There, construction-driven growth gradually gave way to touristification under the combined effects of successive financial, fiscal and epidemiological crises. State interventions – via spatial planning, labour regulations and targeted funding, among others – have reinforced rather than mitigated the country's pronounced uneven development. Specifically, established metropolitan and island tourist destinations hit rapid rates of development, while other Greek regions are being left behind. We contended that this spatial unevenness does not indicate divergent development paths but rather reflects two facets of the same accumulation regime. Within this framework, the reshaping of labour markets to internalise temporariness and precarity constitutes a structural condition for sustaining profitability. In other words, beyond reflecting the intrinsic tendencies of labour-intensive sectors such as accommodation, catering and construction, this labour devaluation plays a key role in counteracting capital devalorisation pressures within the secondary circuit.

The above highlights the limits of tourism-led growth as a crisis management strategy. On its own, such growth cannot foster lasting social cohesion, as it generates housing crises, labour market instability and territorial polarisation. Moreover, control over the extraction of value lies with entities that typically exhibit highly opportunistic behaviour (Christophers, 2022). Without policies that promote productive diversification, regulate financial markets and strengthen labour protections, multifaceted place-based precarity risks becoming a permanent condition.

In conclusion, the case of Greece shows that capital's attempt to secure profitability through the built environment creates conditions of precariousness in employment and, as evident, in housing. Such dynamics confirm that crises are not external disruptions of an otherwise stable system but arise from and reproduce capitalism's inherent contradictions (Harvey, 2001; Christophers, 2011).

Footnotes

Acknowledgements

This article was written in the frame of the project ‘Skillscapes: Skills Landscapes in Greek Tourism: Multi-level analysis based on real-time labor market data, dynamic forecasts, and consulting using artificial intelligence’. The project is implemented within the framework of the initiative ‘SUB1.1. Partnerships for Research Excellence – SEA’ (OPS code TA 5180519), under Sub-project 1 of the Action ‘Promoting quality, innovation, and extroversion in universities’ (Strategy for Excellence in Universities & Innovation, ID 16289) of the National Recovery and Resilience Plan ‘Greece 2.0.’ This project was funded by the European Union – NextGenerationEU.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the National Recovery and Resilience Plan ‘Greece 2.0’, funded by the European Union – NextGenerationEU, (grant number Skillscapes project).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical consideration

The author(s) declared that ethical approval was not necessary for this study.