Abstract

This study looks at the main factors influencing mutual fund distributors’ (MFDs’) propensity to distribute funds using digital tools, seeking to assess the adoption of financial technology (FinTech) platforms by these firms and Individual in India. Structured questionnaires were used to gather data from MFDs throughout India as a component of a descriptive research approach. Different statistical methods, such as reliability assessments, Confirmatory factor analysis and Structural Equation Modeling were utilized to evaluate the Research model validity and relationships between the constructs. The results suggest that price value, facilitating conditions, social influence, performance expectancy, and habit significantly affect behavioral intention, while effort expectancy and hedonic motivation have little effect. This study emphasizes the significance of contextual and practical factors for asset management firms, FinTech innovators, and policymakers seeking to improve digital integration and efficiency in mutual fund distribution.

Keywords

Introduction

The Financial services industry has entered a period of fast technological innovation, with Financial Technology (FinTech) emerging as a transformative force altering market dynamics (McKinsey and Company, 2021) (Chen, 2022). This digital transformation impacts every aspect of the sector, including the distribution of mutual funds. Key participants in the mutual fund industry are distributors of mutual funds (MFDs), who serve as a conduit between investors and mutual fund schemes (Sharma S. 2020). These financial experts provide clients with the knowledge, direction, and expert advice they require to effectively manage their finances and select from a range of investment possibilities. To stay competitive and attract tech-savvy clients, MFDs need to integrate FinTech solutions such as robo-advisors, online KYC procedures, data-driven portfolio management, and automated investing platforms. (Bogle, 2018).

FinTech integration offers numerous benefits, such as improved efficiency, transparency, and investor happiness. Nevertheless, there are a number of obstacles to MFD adoption, particularly in emerging countries like India. The transition from traditional, relationship-based approaches to digital platforms is often hampered by behavioral inertia, a lack of training in digital skills, cost concerns, and data security. Long-term adoption and inclusive digital transformation depend on an understanding of these issues.

Despite the pressing need for MFDs to embrace digital technologies, there remains a significant research gap. Most previous studies on FinTech adoption have focused on the perspective of investors or asset management companies (AMCs). There is a glaring dearth of empirical study on MFDs’ particular awareness, adoption trends, and challenges. This study closes this gap by using the Unified Theory of Acceptance and Use of Technology 2 (UTAUT2) model, which is specifically designed to assess the individual behavioral, social, and environmental elements influencing MFDs’ desire to use FinTech. (venkatesh, 2012).

Definition of fintech

Fintech is the term used to describe the sector that employs Utilizing technology to increase financial institutions’ efficiency and the provision of financial services. New business models, applications, procedures, or products that potentially significantly affect financial markets, institutions, and the delivery of financial services can be launched through technologically driven financial innovation. (RBI, 2020).

Definition of mutual fund distributor (MFDs)

Mutual fund companies that go by different names, such as brokers, agents, and distributors (henceforth referred to as “distributors”), sell mutual funds to investors. These distributors have two roles to play. They assist the Asset Management Companies (AMCs) in marketing their schemes by acting as their representatives. Additionally, they serve as counselors to investors, assisting them in selecting the plan that best suits their requirements. AMC buys and sells mutual funds with the assistance of distributors. A distributor may represent one or more AMCs. (2019, Dr. P. Sai Rani).

Platforms utilized by mutual fund distributors

(1) (2) (3) (4) (5) (6)

Literature review

Overview

A key factor in the adoption of FinTech is the knowledge of Mutual Fund Distributors (MFDs). Many MFDs, especially those in Tiers 2 and 3, are still acclimating to digital platforms, according to recent research. Awareness varies widely depending on the distributor’s age, education, experience, and degree of local digital penetration.

According to research, many independent or small-scale MFDs lack in-depth knowledge of the FinTech tools available, whereas larger distributors and registered investment advisors (RIAs) are aware of and regularly use FinTech tools like robo-advisors, mobile-based investment platforms, and customer relationship management (CRM) systems. (NAASCOM, 2020) According to a study by (Agarwal, 2021), even though awareness has increased as a result of marketing and training campaigns by asset management companies. There is still a lack of understanding in the use of cutting-edge technologies like algorithmic advising and portfolio analytics. Mutual fund accessibility and distribution have been greatly impacted by the increasing digitization of the financial services sector. When Financial Technology (FinTech) is integrated into mutual fund distribution, the efficiency, transparency, and investor experience all improve. The use of FinTech tools such as digital platforms, mobile apps, digital onboarding, and automated portfolio tracking by mutual fund distributors (MFDs), important participants in this ecosystem, is essential to the industry’s digital transformation.

Theoretical foundation: The UTAUT2 model

(venkatesh, 2012) Thorough framework is offered by the Unified Theory of Acceptance and Use of Technology 2 (UTAUT2) people’s behavioral intentions and actual technology use. Price value, habit, and hedonic motivation are some of the new components that UTAUT2 adds to the original UTAUT model. It is therefore extremely pertinent to the research on MFDs’ adoption of FinTech. Distribution patterns, investor interaction, and compliance protocols have all changed result of the mutual fund Financial technology, or FinTech adoption. Even though tech-savvy investors and asset management companies (AMCs) have welcomed these digital tools, mutual fund distributors (MFDs), especially in emerging nations, face a number of obstacles when it comes to incorporating FinTech into their everyday operations. Long-term adoption and inclusive digital transformation depend on an understanding of these obstacles.

Challenges and barriers to FinTech adoption

Under the categories of technological, behavioral, regulatory, infrastructure, and financial constraints, this section examines the different issues that MFDs encounter. Lack of knowledge of new technology and digital skills is one of the main obstacles to the adoption of FinTech. Many MFDs, particularly those in semi-urban and rural areas, lack formal training in the use of digital tools, according to studies by (Mehta, 2021). Behavioral inertia is a well-known barrier to FinTech adoption. The long-standing operations of many MFDs have been built on personal connections and paper-based procedures. The shift to digital platforms is perceived by many as disruptive and impersonal. Inadequate helpdesk, educational, and practical guidance support leads to poor onboarding and underuse of the offered resources.

Technological and security constraints

Since FinTech platforms usually require MFDs to handle and keep sensitive client data, data privacy and cybersecurity are significant issues. Distributors may be reluctant to use cloud-based platforms to store client KYC, investment trends, or personal financial information. Analyses by (Chatterjee, 2021) illustrates how MFDs are deterred from relying only on FinTech technologies due to concerns about hacking, data breaches, or system failures, particularly when those tools are provided by questionable third-party service providers. Cost remains a significant barrier, especially for small or independent distributors. FinTech solutions provided by third-party platforms may incur transaction, setup, or subscription fees. (Menon, 2021) AMCs assert that paywalls usually block access to more advanced products (like as CRM integration or AI-driven suggestions), despite the fact that they provide basic digital tools. It could be difficult for MFDs with small profit margins to defend such investments in the absence of a clear, measurable return.

(Kumar, 2019) Note that having tools does not guarantee that they will be used effectively, and stress the importance of focused education and AMC-led training in closing this awareness gap. According to their findings, incentives and support networks are required to motivate MFDs to engage in digital transformation.

Significance of study

The use of financial technology (FinTech) in mutual fund distribution is a crucial study since it clarifies how India’s distribution landscape is evolving due to digital transformation. It highlights the current level of mutual fund distributors’ (MFDs’) awareness and use of FinTech tools, outlines the primary barriers to adoption, and looks at the potential benefits of digital integration. The study’s analysis of these variables can help distributors, FinTech developers, lawmakers, and asset management companies better understand market dynamics, increase operational efficacy, and develop strategies that encourage wider technological adoption and, ultimately, build a more transparent, accessible, and investor-friendly mutual fund ecosystem.

Objectives

(1) To assess the awareness of financial technology application among mutual fund distributors. (2) To analyze the adoption of Fintech in mutual fund by mutual fund distributors. (3) To analyze the challenges and Problems facing by mutual fund distributors in financial technology.

Research Gap

Despite the rapid adoption of FinTech by India’s financial sector, mutual fund distributors (MFDs), crucial intermediaries in the distribution process, have not received much attention in studies. Little is known about MFDs’ awareness, adoption trends, and challenges, such as issues with digital literacy, behavioral resistance, infrastructure constraints, and data security, because the majority of research to date has focused on investors or asset management organizations. Additionally, this study attempts to close a clear gap: FinTech uptake among MFDs in India has not been adequately examined using the UTAUT2 paradigm.

Research Questions

(1) To what extent do mutual fund distributors (MFDs) now understand the applications of financial technology (FinTech)? (2) How much do mutual fund distributors (MFDs) use FinTech in their distribution operations? (3) What are the primary challenges and problems MFDs are facing while implementing FinTech in the distribution of mutual funds?

Research Methodology

Research design

To understand the present situation, obstacles, and motivators of FinTech adoption in distribution. A descriptive research design is employed in study. To give a complete picture of FinTech adoption trends among mutual fund distributors, the study combines qualitative and quantitative data.

Techniques for gathering data

Sampling methods

Data analyis & interpretation

Interpretation

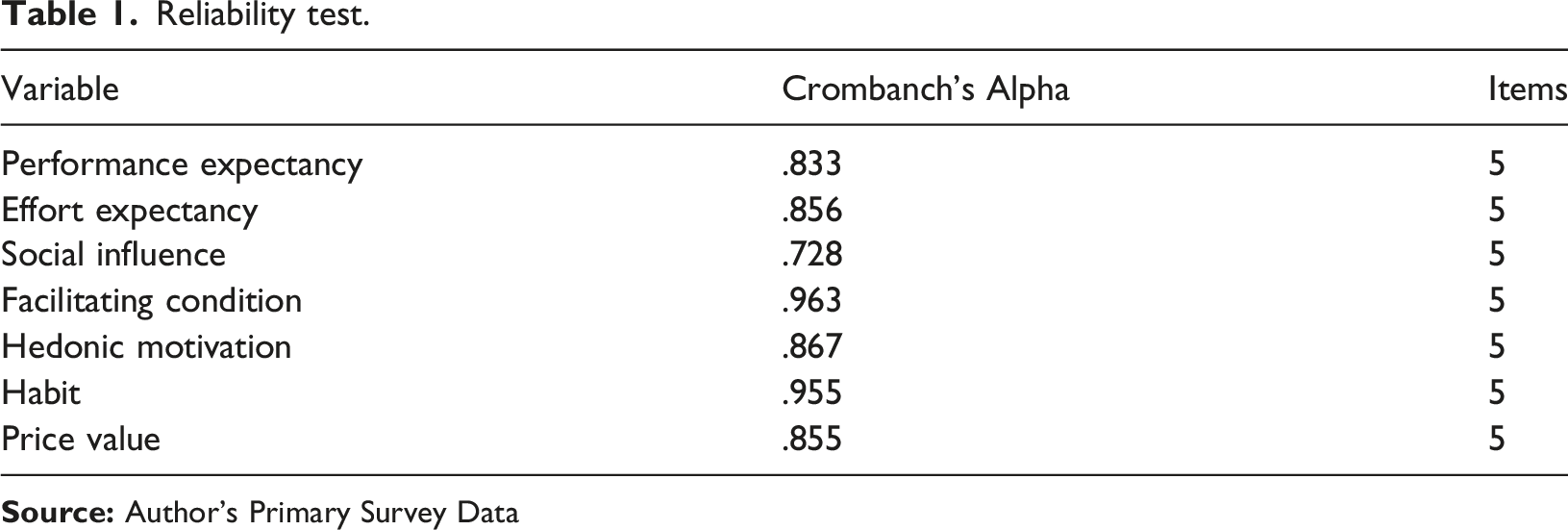

Reliability test.

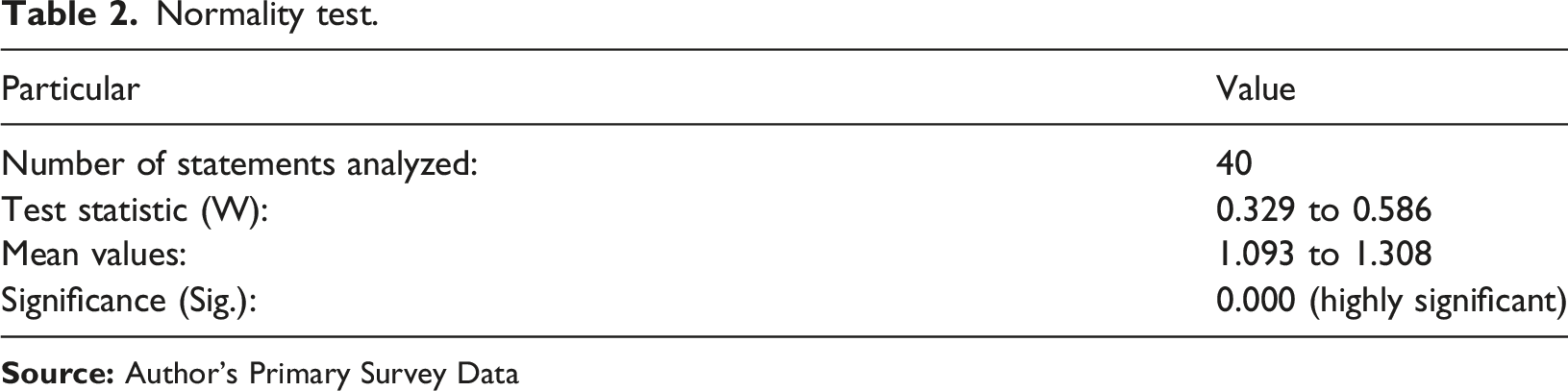

Normality test

Interpretation

Normality test.

Confirmatory factor analysis

Explanation

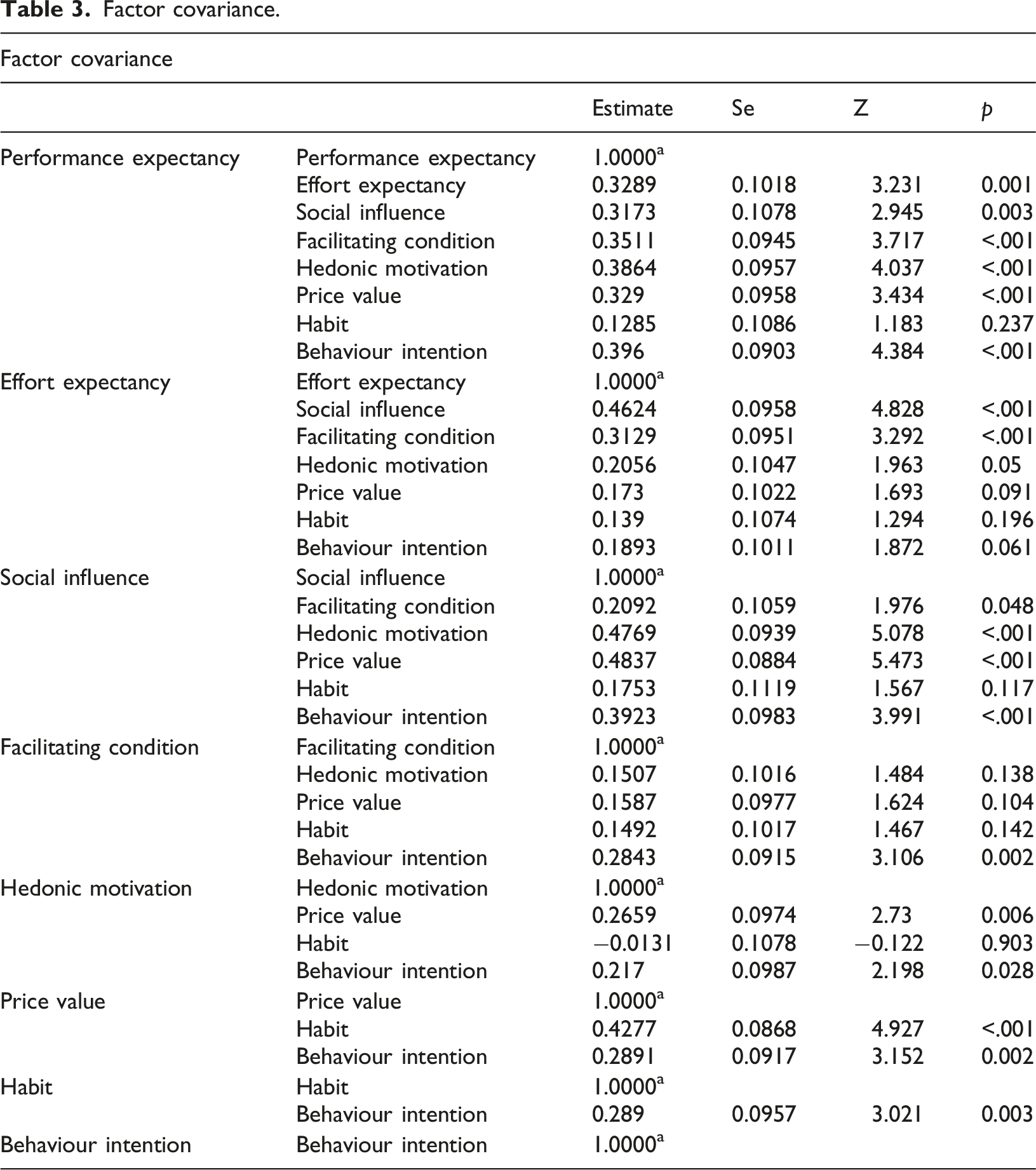

Factor covariance.

Model fit.

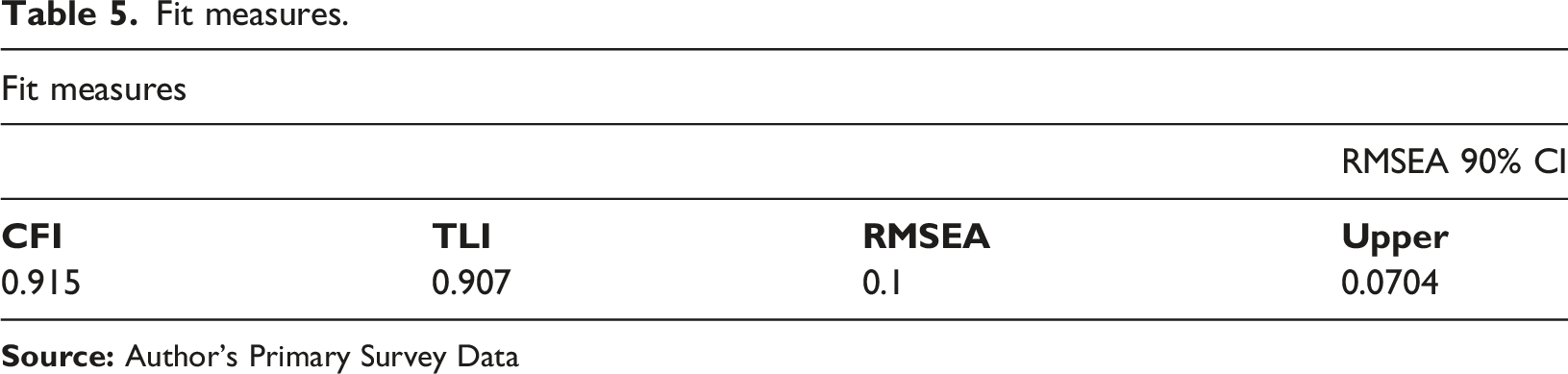

Fit measures.

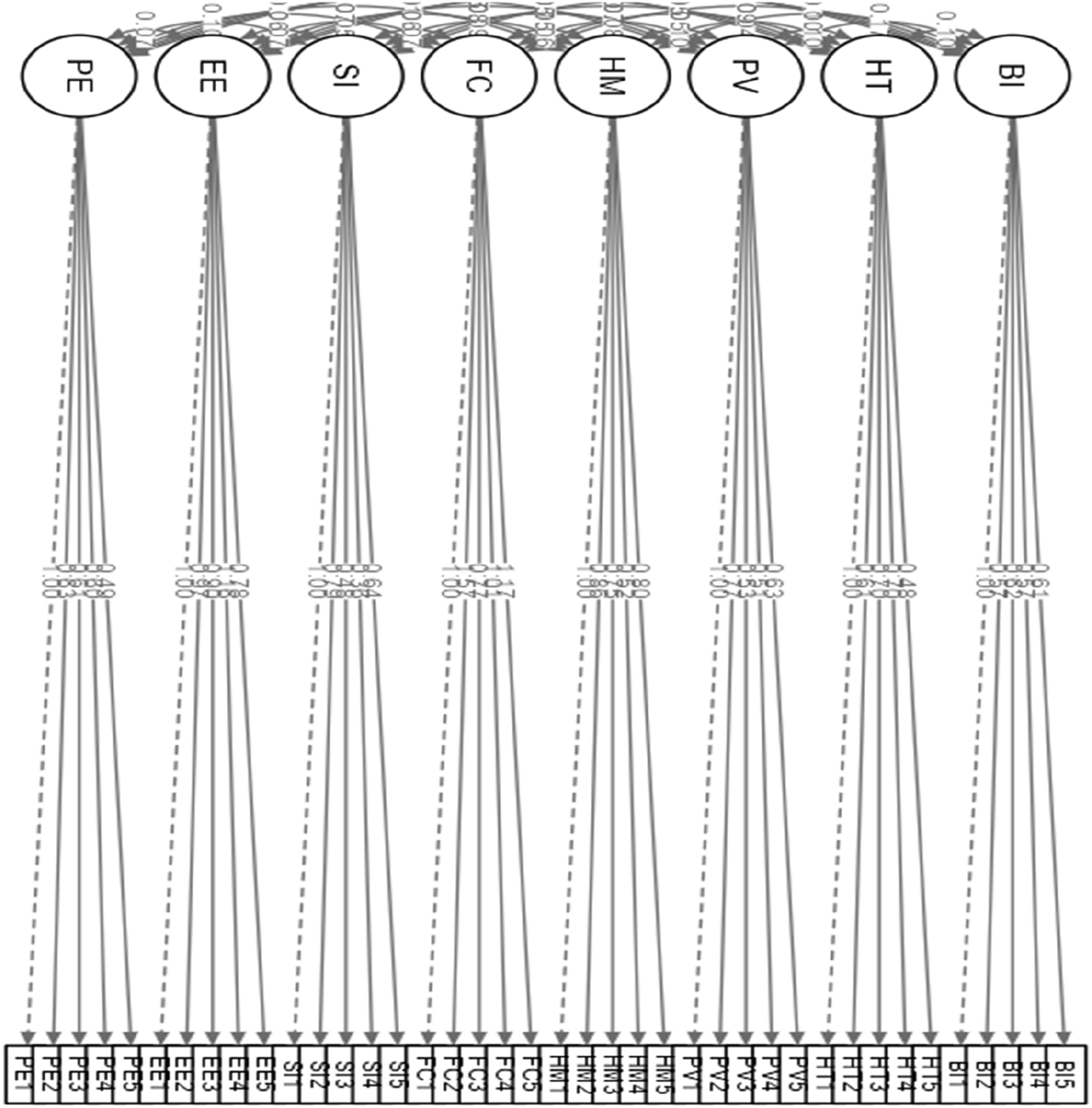

Structure equation modelling

Interprcetation

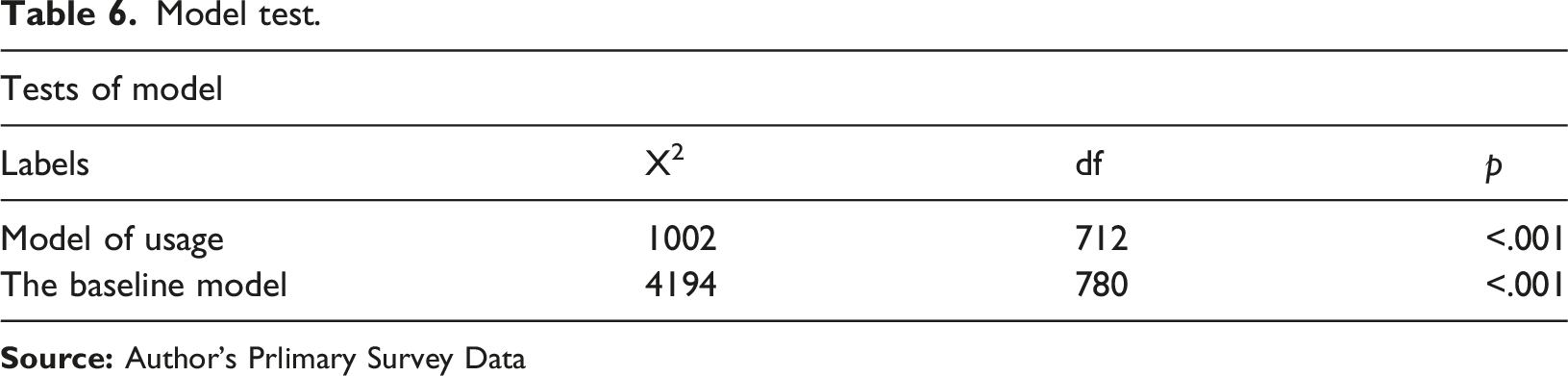

Model test.

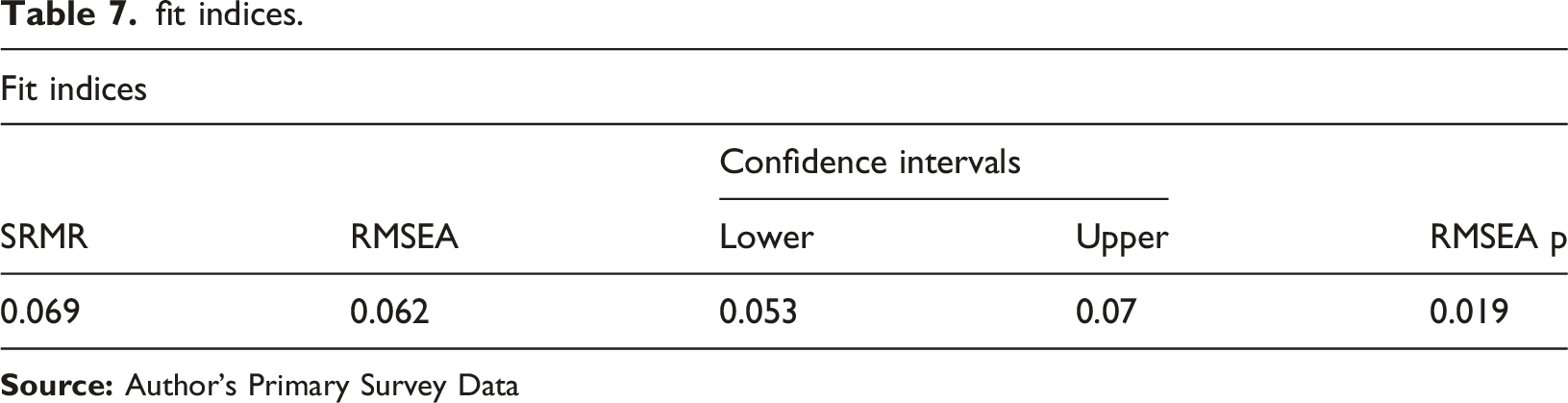

fit indices.

Structural Equation Modelling. Source: Author’s Primary Survey Data (Figure 1, 2023).

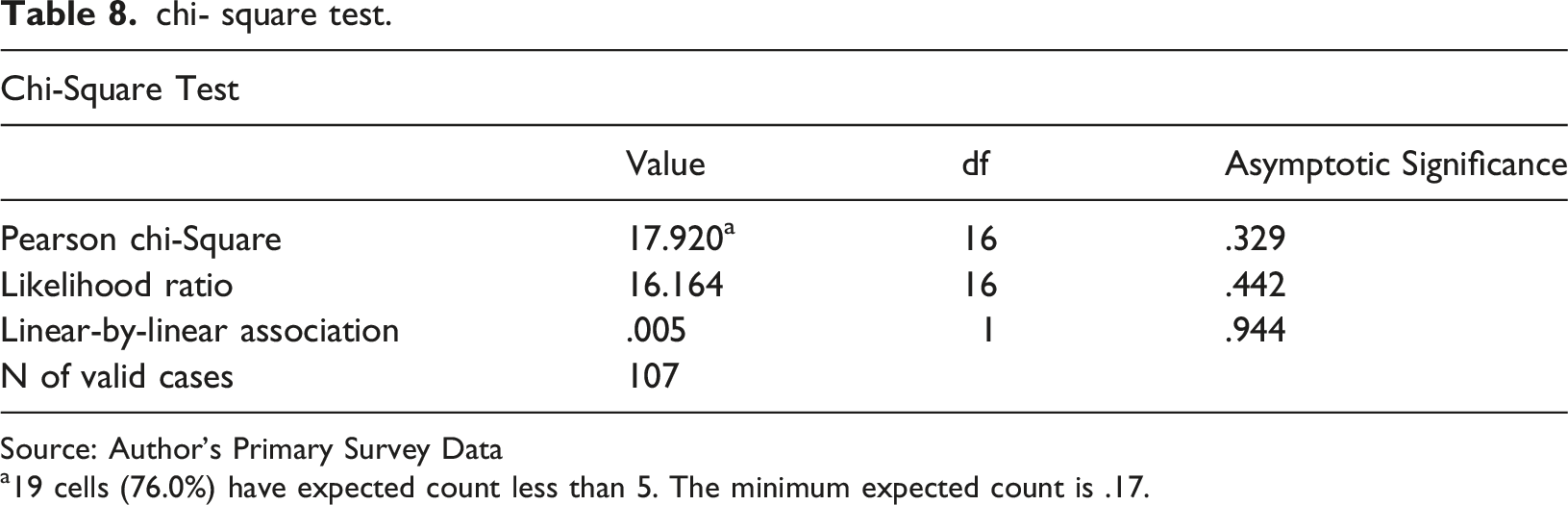

Chi-Square test

1. Evaluating the Relationship between Awareness Level and Age

Interpretation

As per value shows in (Table 8, 2023) the p-value of.329 and the value of 17.920 obtained from the Pearson Chi Square test with 16 df are both greater than 0.05. This implies that there is insignificant relationship between age and awareness level. 2. Evaluating the relationship between experience and awareness level chi- square test. Source: Author’s Primary Survey Data a19 cells (76.0%) have expected count less than 5. The minimum expected count is .17.

Interpretation

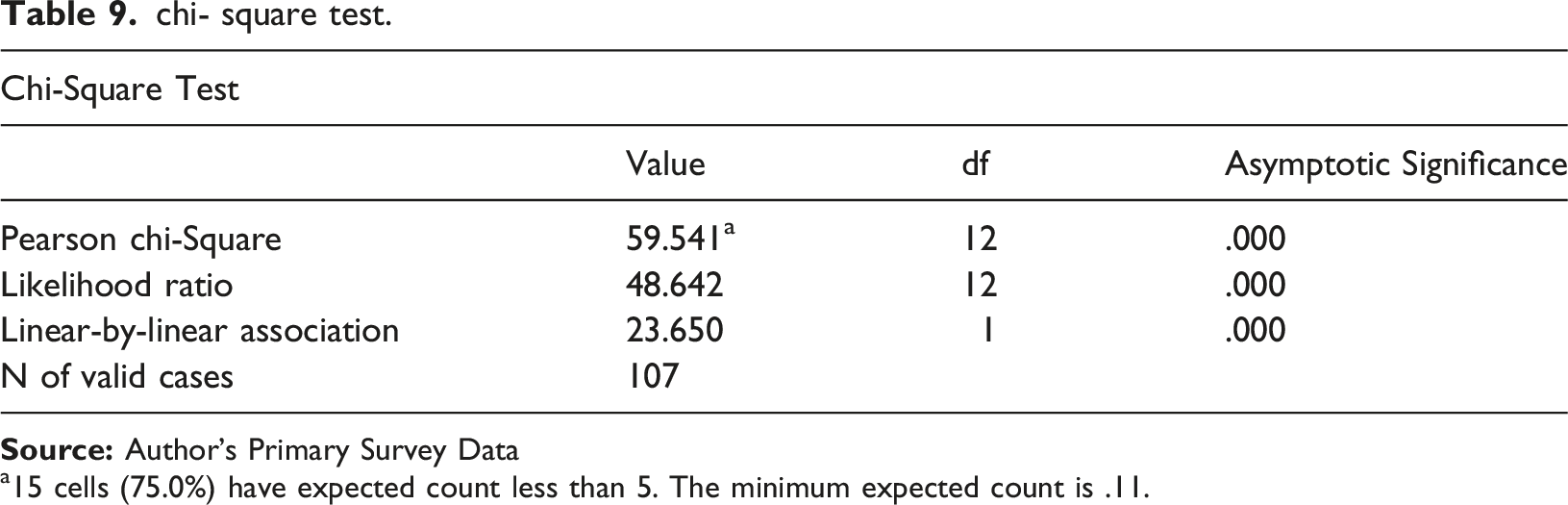

chi- square test.

a15 cells (75.0%) have expected count less than 5. The minimum expected count is .11.

Findings & suggestions

Key findings

(1) All UTAUT2 components with Cronbach’s Alpha scores between 0.728 (Social Influence) and 0.963 (Facilitating Condition) showed good to exceptional reliability. This implies that the measurement items were internally consistent and suitable for further investigation. (2) The Shapiro-Wilk test results showed that none of the items were normally distributed (p < .001 for all). However, parametric analysis is acceptable due to the sample size (n = 107), which makes the Central Limit theorem applicable. (3) Price Value, Habit, Social Influence, Performance Expectancy, and Facilitating Conditions were all significantly associated with Behavioral Intention, and the CFA showed a good model fit (RMSEA = 0.0617, CFI = 0.915, TLI = 0.907). In contrast, Effort Expectancy and Hedonic Motivation had weaker or marginal associations with Behavioral Intention. (4) The CFA results were further supported by the SEM’s good fit indices (RMSEA = 0.062, CFI = 0.915, TLI = 0.907). The behavioral intention to utilize FinTech in mutual fund distribution was highly influenced by the following factors: social influence, price value, habit, facilitating conditions, and performance expectation. Expectations of effort and hedonic drive had less impact. The high standardized loadings of all observed variables (often> 0.7) demonstrated strong convergent validity. (5) This suggests that age has less of an effect on awareness of FinTech than work experience does.

Suggestions

(1) FinTech products should be designed with ease of use, local language support, and seamless integration with existing business procedures in mind. (2) By providing distributors with regular updates, technical support, and a feedback loop, long-term engagement and acceptance will be enhanced. (3) Promote the adoption of standardized digital compliance tools, like e-KYC and online onboarding. (4) Offer distributors that use digital means incentives like recognition programs and reduced audit burdens. (5) Verify that there are clear guidelines for data usage, investor protection, and digital advising services. (6) User-friendliness, multilingualism, and compatibility with distributors’ existing systems should be the top priorities for Fintech solutions.

Limitation of the study

(1) In the mutual fund distribution context, “FinTech” refers to a range of tools and platforms (like mobile apps, robo-advisors, and KYC systems) that not all respondents may have adopted or comprehended equally. (2) Because the study depends on participants’ self-reported attitudes and actions, bias or social desirability effects could be introduced. (3) The sample might not be representative of all distributors of mutual funds in various geographical areas. (4) Subjective impressions may cause respondents to overestimate or underestimate their usage of technology. (5) It might be difficult to get thorough and trustworthy information about FinTech adoption from distributors because of issues with confidentiality, competitive sensitivities, or a lack of organized data collecting. (6) It’s possible that the participant sample isn’t entirely representative of distributors as a whole.

Conclusion

The distribution of mutual funds has changed due to the rapid development of financial technology, which has created new opportunities for efficiency, accessibility, and customer interaction. Industry reports have also shown that mutual fund distribution in India is increasingly shaped by digital platforms, online investor services, FinTech-enabled advisory tools, and changing distributor–investor engagement patterns (Association of Mutual Funds in India, 2022; Deloitte, 2020; EY India, 2021; PwC, 2020). The results demonstrate that social influence, facilitating circumstances, performance expectancy, and effort expectancy play an important role in determining behavioural intention. Through the use of theoretical frameworks like the UTAUT2, the study shed light on the many phases of technology adoption as well as how organizational, technological, and personal aspects affect decision-making. The distribution of mutual funds has changed due to the quick development of financial technology, which has created new chances for effectiveness, accessibility, and customer interaction the results demonstrate how important a role social influence, facilitating circumstances, performance expectancy, and effort expectancy in determining behavior. Digital platforms are more likely to be adopted by distributors and investors when they see obvious advantages, user-friendliness, and sufficient support infrastructure.

The UTAUT2 model is validated in this study in relation to mutual fund distributors’ adoption of FinTech. It emphasizes how important contextual and utilitarian elements are in determining adoption intention, including things like habitual use, cost-effectiveness, social support, usefulness, and available resources. Enjoyment and ease of use, on the other hand, seem to have less of an impact. Since experience has a big impact on awareness, less experienced distributors may benefit from focused awareness campaigns.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.