Abstract

We take stock of theory and explanation in financial geographies between 2001 and 2020. Our analysis confirms the lone ascent of financialisation to the status of leading theory and shows that economics, particularly the financial variety, has been gradually pushed away from financial geographies in a shift that accompanied the decline of quantitative research approaches. We explain how these developments are interrelated and argue that they pose challenges to the role of explanatory theory, particularly in terms of its practical adequacy, understood as analytical robustness in explaining empirical outcomes, and usefulness for the practice of positive social change. We propose that these challenges need to be addressed by strengthening relationships between financial geographies and varieties of economics. We illustrate opportunities for such engagement in three broad areas: quantifying financialisation, sustainable finance, and decentralised finance.

Introduction

‘By our theories you shall know us’, wrote Harvey (1969: 486) in his book, Explanation in Geography. Thirteen years later, he published The Limits to Capital, offering a geographical theory of capitalism with money at the centre. In the 1990s, the geographies of money and finance became distinguished as a subdiscipline (Leyshon, 1995; Martin, 1999a), which continued to develop in the 2000s (Clark and Wójcik, 2007), but a big boom in financial geographies came with the global financial crisis of 2008. The number of publications has multiplied, and so has the membership of the Global Network on Financial Geography (FinGeo) (Gibadullina, 2021). Finance & Space was launched as a new journal dedicated to financial geographies (Wójcik et al., 2024). But, do people know financial geographies and financial geographers by their theories? Is there a financial geography theory? How much attention do financial geographers pay to theories? Thinking about the future of financial geographies, how should we respond to David Harvey's 55-year-old call?

The time seems ripe for financial geographers to address these issues. We are reminded of Harvey's statement by Yeung's new book, which starts with the same quote, works its way through the minefield of theories in critical human geography, and ends with his own motto for geographers: ‘By our explanatory mid-range theories you shall know and learn from us’ (2024: 266). This article addresses both Harvey's and Yeung's challenge by reflecting on their application to financial geographies. We acknowledge that Yeung's book offers a (not the) perspective on theory and explanation in geography, and in Cresswell's words in the book online endorsement, ‘geographers will be inspired and/or infuriated by Yeung's arguments in this provocative and cogently argued call to theoretical arms for many years to come’ (Wiley, 2024). While we are mostly inspired, we apply Yeung's arguments critically to emphasise what we think is most prescient to financial geographies in Yeung's call, but also to highlight what is potentially problematic or missing. We use Yeung's arguments as a starting point of our hopefully provocative call to financial geographers.

Before we move on, let us clarify what we mean by financial geographies and why we use the term in plural. We refer to financial geographies as the study of the spatiality of money and finance as well as its implications for economy, society, and the environment. The first part refers to geographies of money and finance, focusing on the spatial production of finance (e.g. the spatial structure of banking systems) (Martin, 1999a). The second refers to using an understanding of money and finance as a lens to study other geographical phenomena, including, but not limited to, housing, mobility, development, sustainability, etc. (Aalbers, 2018). As such, the second part complements the first by focusing on the financial production of space. While financial geographers mostly use financial geography in the singular, we use it in the plural to emphasise the diversity of the field. Financial geography is often considered a subdiscipline of economic geography, but financial geographies in the plural remind us of the relevance and connections with cultural, environmental, political, social, and other types of geography, and open-ended interactions of financial geographies with other social sciences, including broadly defined social studies of finance. Though how open-ended financial geographies are and in what directions and how closed in other directions will also be a matter of discussion.

Our argument is two-fold. First, we make a case for an explanatory theory in financial geographies. Explanatory theories are in use in financial geographies, but there are gaps in terms of theories and modes of explanation prevalent in the field. In this article, we back the call for explanatory theory in geography at large that Yeung (2024) advances. Second, we argue for reinvigorated engagement of financial geographies with economics, which we consider essential to develop more explanatory theory in financial geographies. In doing so, we claim that there is much less difference between theory and explanation that Yeung (2024) advocates, and what economics partly is, and what it aspires to, than most geographers think.

Our intervention is intended as a combination of a literature review and agenda setting. To develop the diagnostic component of the paper, we take stock of theories and explanation in financial geographies as robustly as we can. To this end, we conduct a bibliometric analysis using Web of Science to identify all articles (other than editorials) that contain the terms ‘finance’ or ‘money’ (and their variations like ‘financial’ or ‘monetary’) in keywords, published between 2001 and 2020 in geography, urban studies, and urban and regional planning. We go beyond narrowly defined geography since all these fields focus on space by definition, in contrast to economics, management, or sociology, which were not included. Hence, while our sample of financial geographies is broad, it is consistent, and we highlight this breadth by using the term financial geographies in the plural. As publishing authors, we routinely consider journals in urban studies and urban and regional planning in addition to geography as potential outlets for our financial geographical work, and our experience suggests that this approach is common. The resulting list of 984 articles was reduced to 449 to include those cited at least 10 times as of the end of May 2021 when we collected the data. Cited almost 17,000 times in total, the selected papers account for approximately 90% of all citations of the full sample. The sample is diverse, with articles published in 35 different journals, with Geoforum, Journal of Economic Geography, Housing Studies, and Regional Studies accounting for 30 or more each. The review is limited to publications in English.

We recognise the limitations of this bibliometric exercise. Reducing the sample to more cited publications in English, we underplay the significance of work published towards the end of the sample period and the voices less heard, possibly reinforcing the biased production of knowledge in financial geographies and beyond (Rosenman et al., 2020). However, our focus on more vocal research is consistent with our critical approach and our goal to identify gaps rather than reify the existing structures of knowledge production through celebratory rankings. The goal of our bibliometric exercise is not to paint a definitive picture of the field, but to generate insights for a debate. We should also recognise our positionality upfront. Both authors have PhDs in economic geography and have experience working in the financial industry. Both are invested professionally in financial geographies and deeply interested in their success. This gives us a particular perspective and motivates our interest in both explanatory theory and engagement with economics in financial geographies. As we stressed before, this paper diagnoses a problem and offers a solution, with emphasis on indefinite, not definite, articles.

The rest of the paper follows the two-fold argument we make. First, we reflect on how theorising and explaining are done in financial geographies and the role of explanatory theories in these processes. Next, we explain the need to strengthen the relationship between financial geographies and economics. Lastly, the article concludes with a discussion of the broader ramifications of our arguments.

Theorising and explaining in financial geographies

We follow the economic sociologist Swedberg in defining theory as ‘a statement about the explanation of a phenomenon’ and agree with him that ‘an explanation represents the natural goal of theorizing and completes the process of building out a theory’ (2014: 17 and 98). Theory needs to be concerned with both ontology as ‘theory of reality and existence’ and epistemology as ‘theory of our knowledge of reality and existence’ (Yeung, 2024: 37), but ultimately both need to aim at explanation. Theorising without explanation has an important place in research, but imbalance and disconnect between theory and explanation impoverish research. This issue is expressed in Yeung's call for ‘theory not only as an abstract representational device or rhetorical-descriptive apparatus, but more importantly also a causal explanation of socio-spatial change and outcome’ (2024: 95). Put metaphorically, as the cover of Yeung's books does, the seesaw of theory and explanation functions only with balance and movement between the two. In agreement with Yeung's argument that theory and explanation should be the raison d'être of human geography, we believe it should also be the raison d'être of financial geographies.

An explanatory theory in Yeung's view ‘requires causal explanations to specify their attendant mechanism in relation to general processes and the operating contexts of these mechanisms in relation to historical and geographical contingency’ (2024: 95). Furthermore, according to Yeung, such theory needs to pass three tests: normative concerns, socio-spatial contexts, and practical adequacy. First, a researcher needs to think for whom and on whose behalf theorising and explanation are undertaken. Second, theory and explanation have to be grounded in different socio-spatial contexts. Yeung rejects the idea of grand theories of social change. There are ‘no such things as universal or all-inclusive causal mechanisms’ (Yeung, 2024: 108). Instead, ‘mid-range theories addressing specific empirical phenomena and yet broad enough to apply across a wide range of socio-spatial settings’ (Yeung, 2024: 108) are his favourite, though not the only, solution. Finally, practical adequacy refers to analytical robustness in explaining empirical outcomes (i.e. adequacy to researchers), and usefulness for the practice of positive social change. Following Schatzki (2019), the ‘so what’ and ‘how can this make positive change and transformation in the material world possible’ questions are much more important to theory and explanation than its conceptual elegance and sophistication.

Assessing the state of theory and explanation in financial geographies is an almost impossible task. Given at least a four-digit stock of publications on financial geographies in existence, as our bibliometric exercise suggests, a comprehensive review would go beyond the scope of a single book, not to mention a paper. What compounds the challenge is the fact that identifying theory and explanation, and how they are done in a publication, can be difficult in itself. The method we applied was to search the contents of a publication for the term theory, look for theory and concepts in keywords, scan literature reviews for the key theoretical influences, and analyse methodology and results sections to ascertain the mode of explanation used. While we think it is a robust method given the circumstances and resources of two authors spending hundreds of hours each on analysing the sample, and believe it represents original effort not undertaken before, we admit the caveats. Our analysis can only show broad and proximate patterns, influenced by our own positionality and interpretations. At the same time, we read theories, key concepts, and modes of explanation from – not into – the sample papers, and our results are based on explicit references rather than our impressions.

Only 121 articles (27% of the sample) do not have a single mention of the word theory, theories, or theoretical, and, on average, a paper mentions any of these words four times. For 95 (21%) papers, despite effort, we were unable to pinpoint the theoretical framework used. There are themes (e.g. taxes or land finance, but the theory underpinning a paper may still remain vague. For other papers, we identified the key theory or (if an explicit theory is missing) concept present in the article. Our judgement of what is ‘key’ was based on the reading of each paper to identify the most prevalent or guiding theory or concept. In sum, despite limitations of the sample and necessary judgement involved, this gives us a reasonable starting point to see what the key theories and concepts in financial geographies are and how they evolved over two decades. With the growing popularity of financial geographies, the number of papers increased with time, and our temporal comparisons divide the whole period into the first decade, 2001–10, and two five-year periods in the second decade, 2011–15 and 2016–20, with 123, 174, and 152 publications, respectively.

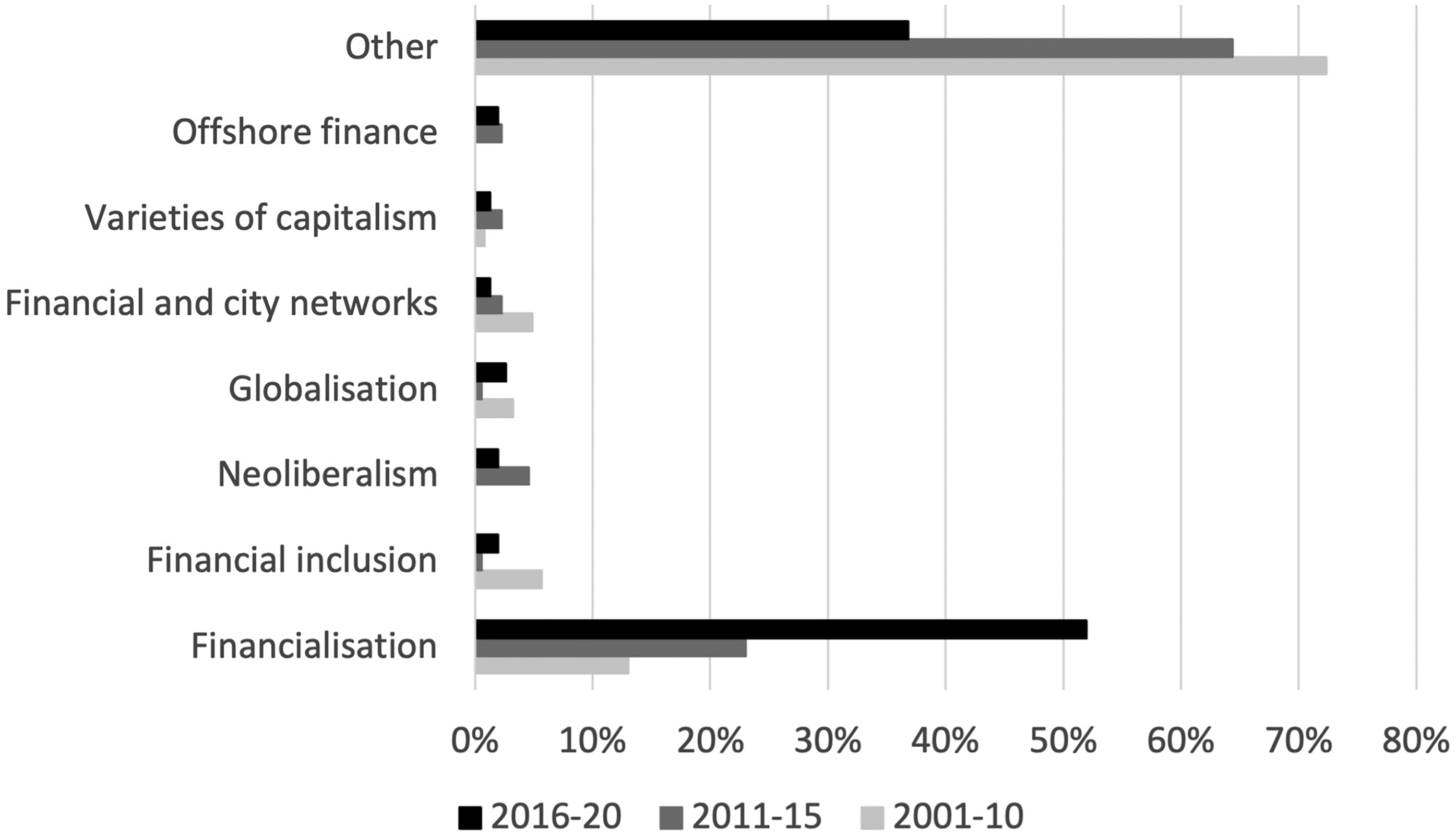

Figure 1 shows the results. Only seven theories and concepts could be identified in five or more papers over the whole period, and they all feature in the figure. There are papers that focus on conceptual overlaps among the seven, such as globalisation and city networks, and varieties of financialisation, but this does not change the general patterns emerging. The absence of grand theories, such as Marxist, feminist, or post-structuralist, in Figure 1 may be surprising, but these simply do not feature explicitly enough in the sample papers to make the cut. Recall that our method was bottom–up rather than top–down. We did not start with a list of theories as a scheme for classifying papers. Instead, we followed whatever the authors referenced as part of their theoretical and conceptual frameworks. In summary, our results suggest that financial geographers rely predominantly on mid-range theories and concepts.

Theories and concepts in financial geographies. Source: Authors.

The rise of financialisation as the key theoretical and conceptual framework in financial geographies is clear and loud. Its share of influential papers rose from 13% in 2001–10 to 23% in 2011–15, and then claimed a majority of 52% of articles in 2016–20. As Christophers (2015a) notes, financialisation has become the third of the big -isations after globalisation (the buzzword of the 1990s) and neoliberalisation (2000s), which have deeply influenced the whole of human geography of the last 30–40 years. As we show here, in financial geographies, financialisation has become by far the biggest of the three -isations. It is financialisation that has made geography of finance and money into financial geography, a transition marked symbolically by the name of the Global Network on Financial Geography launched in 2015, and the first Progress in Human Geography report called financial geography, not geography of finance. As Aalbers (2018: 916) writes in that report: [t]his denotes a shift from money and finance as an object of geographical analysis to finance as a lens through which one can look at other issues. This shift is embedded in an understanding of financial geography not merely as a sub-discipline of economic geography, but as an approach couched in and relevant to virtually all sub-disciplines of human geography: economic, political, urban, historical, social and cultural, and related to other intersectional lenses such as development, global and legal geographies.

Beyond financialisation, none of the other six discernible theories or concepts rose in significance. We can even posit that financialisation partly subsumed some other frameworks. Financial inclusion (and exclusion), for example, rather than being mobilised as a leading theory or concept, can be approached as an aspect of financialisation, in which inclusion can take on a much more pejorative meaning (Lai and Samers, 2021). This is seen in work explaining expanded financial inclusion through FinTech as digital financialisation ‘undergirded by an infrastructure that harvests citizens’ data, which companies can monetise and governments can use for political surveillance’ (Jain and Gabor, 2020: 1). We should also note that the residual category in Figure 1 remains large, accounting for 37% of articles in 2016–20. Among theories and concepts that do not make it to the top seven and hence do not have individual labels in the figure are financial ecologies, state rescaling, marketisation, securitisation, political ecology, and entrepreneurial ecosystems.

Let us highlight the difference between our analysis and that of Gibadullina (2021). While she uses a sample of financial geography publications and a separate sample of publications on financialisation, irrespective of the discipline in which they are published, we look at financialisation as a key theory within a sample of literature on financial geographies. Gibadullina (2021) does not offer numbers on the rise of financialisation studies in relation to financial geography research, and her statement on the ‘financialisation turn’ in financial geography is based on the share of financialisation as a keyword in financial geography articles and on qualitative evidence based on interviews. Gibadulina's key focus is co-citation networks and clusters of authors and journals. Ours is theory and explanation in financial geographies.

To delve further into the nature of theory in financial geographies, for each article for which we could identify a key theory or concept, we also identified up to three main source references for this theory or concept. Including up to three references allowed us to accommodate cases when it was difficult to decide which one or two references were most important. Put differently, in this way, we were less likely to miss a key reference. The result is significant diversity, which we think highlights the non-canonical nature of the field, even within financialisation studies. Seventeen works were key theoretical references for five or more papers, and they feature 113 times in total. While we could not name any theories identified in Figure 1 as grand theories, the influence of Harvey and Arrighi illustrates the salience of Marxist roots in some financial geographies, with Harvey's Limits to Capital (1982) and Arrighi's Long Twentieth Century (1994) appearing as key theoretical influences in 19 and five articles, respectively. In fact, almost all of the articles with Harvey or Arrighi as the key reference are concerned with financialisation as a key theory or concept, often using Marxist political economy to explain phenomena referred to as financialisation (Christophers, 2017; Guironnet et al., 2016). There are seven other works present as a key source of theoretical references in financialisation studies. These are by geography and urban scholars (Aalbers, 2008, 2016; Weber, 2010), sociologists (Krippner, 2005, 2011; Martin, 2002), and an economist (Epstein, 2005). We will return to the significance of their disciplinary affiliations later.

How would financialisation, the leading and rising, if not already dominant, theory in financial geographies perform according to Yeung (2024) criteria of explanatory theory? Parts of his book discuss Marxist theory in geography, which he considers too deterministic, mechanistic, and reductionist to be sufficiently grounded in socio-spatial contexts and to be practically adequate. Unfortunately, his book mentions financial geographies and financialisation only in a footnote. We address this omission here.

Financialisation as practiced in financial geographies passes the normative test. It represents critical social science, with its critical stance pointed at finance, its excesses, and impacts on socio-spatial relations. The origins of financialisation research in financial geographies and some of the key theoretical references mentioned above predate the global financial crisis of 2008, adding to the credibility and reputation of the concept. Financialisation studies did not just jump on the bandwagon of criticising finance after it blew up in 2008. As practiced in financial geographies, financialisation research rarely focuses solely on theorising, and typically aims at explaining financialisation and its impacts in specific contexts (e.g. French et al., 2011; Sokol, 2013). In this respect, we would argue that there is a sound geographical confidence in this body of research, with little ‘philosophy envy’ and theorising for the sake of theorising, which according to Yeung (2024) is pervasive in human geography. There is certainly room for improvement in terms of voices represented in financialisation studies. Over 80% of articles using interviews use expert interviews only (Wójcik, 2022). This percentage applies across financial geographies to both financialisation research and other publications. Furthermore, the experts being interviewed are typically white males in financial centres and other big cities (Wójcik, 2022). Notable influential exceptions from this pattern within our sample include interviews with tenants in Brooklyn (Fields, 2017), rural households in northeast England (Coppock, 2013), families in Palestine (Harker, 2017), and microfinance clients in Nepal and Vietnam (Rankin, 2008). To demonstrate normative concerns, financial geographers need to make sure that their embrace of close dialogue as a method (Clark, 1998) is radically opened up rather than becoming a closed dialogue.

Studying and grounding financialisation in socio-spatial contexts are a central focus of financial geographies. While real estate, land, and housing are by far the leading topics of financialisation studies in financial geographies, other topics range widely, including agriculture, family, infrastructure, nature, and urban development. Socio-spatial contexts are studied at all scales, from the body (Borch et al., 2015) through households and organisations to cities, regions, and countries. Van der Zwan (2014) highlights this multi-scalar approach by distinguishing between financialisation as a regime of accumulation in capitalism and institutional change, the corporate strategy of shareholder value, and financialisation of the everyday. In doing so, she also highlights the multiple strands of financialisation research, with their theoretical roots and vocabularies in economics and political economy, business studies, and sociology and cultural studies, respectively, a remarkably diverse range to which we will return later. The Global North dominates as empirical focus, but there is a growing number of studies on subordinate financialisation in the Global South (Fernandez and Aalbers, 2020; Green, 2019) and Eastern Europe (Büdenbender and Aalbers, 2019). Subject to further improvement in geographical coverage, financialisation passes the second of Yeung's tests.

This takes us to the final test of practical adequacy, which combines analytical robustness in explaining empirical outcomes (i.e. adequacy to researchers) and usefulness for the practice of positive social change. In a critique of financialisation, Christophers (2015a) argues that financialisation has been stretched so much that it borders meaninglessness, is not a proper theory, unlike Harvey's Marxist concepts on which it often relies, and that the ‘financialisation of everything’ wave of research has diverted attention from the geography of money. The danger he sees is that with financialisation studies focusing on how finance changes everything else (organisations, cities, capitalism, etc.), we remain in the dark about how finance itself works. His verdict is that ‘[t]he limits are sufficiently substantive, and their implications sufficiently material, to warrant a tempering of enthusiasm, if not a turn away from the concept altogether’ (Christophers, 2015a: 184). In a rejoinder, he reasserts that ‘work on financialisation has had the perverse effect of black boxing “finance” and crucial dimensions thereof’ (Christophers, 2015b: 229).

Like Yeung (2024), we believe in the value of mid-range explanatory theories as a way to address complex and unpredictable social reality. Financialisation offers a wide range of explanations. Just to give a few examples, it shows how homes become real estate (Smith, 2015), how more and more organisations, including universities, start to behave like corporations (Engelen et al., 2014), how climate change is managed through the expansion of financial markets (Knox-Hayes, 2016), and how these processes impact people and the environment in specific contexts. We think that studying financialisation is compatible with opening the black box of finance. On a methodological and empirical level, financialisation studies can use interviews with both those affecting financialisation (e.g. finance professionals or landlords) and those affected (tenants, borrowers, etc.), hence shedding light on how finance, with its instruments and narratives, works. We stress that studying the spatial production of finance is compatible with studying the financial production of space, and financial geographers often do both at the same time. But, we agree with Christophers (2015a) that more effort is necessary to strengthen the geographies of finance leg of research. Such effort would help a more balanced theory and explanation in financial geographies. Here, we echo Ouma (2015) call for more study of operations between M and M′, which ‘matter as the glue that keeps things together’ (228). We also second Poovey (2015: 220) that it is ‘crucial to analyse the institutional and mathematical infrastructure of finance in any treatment of financialisation’. This infrastructure, she stresses, ‘includes theoretical treatments of finance in the academic literature of economics’ (Poovey, 2015: 221). As we shall argue in the next section, critical engagement with economics is a major ingredient for improved practical adequacy of explanatory theory in financial geographies.

Disengagement with economics

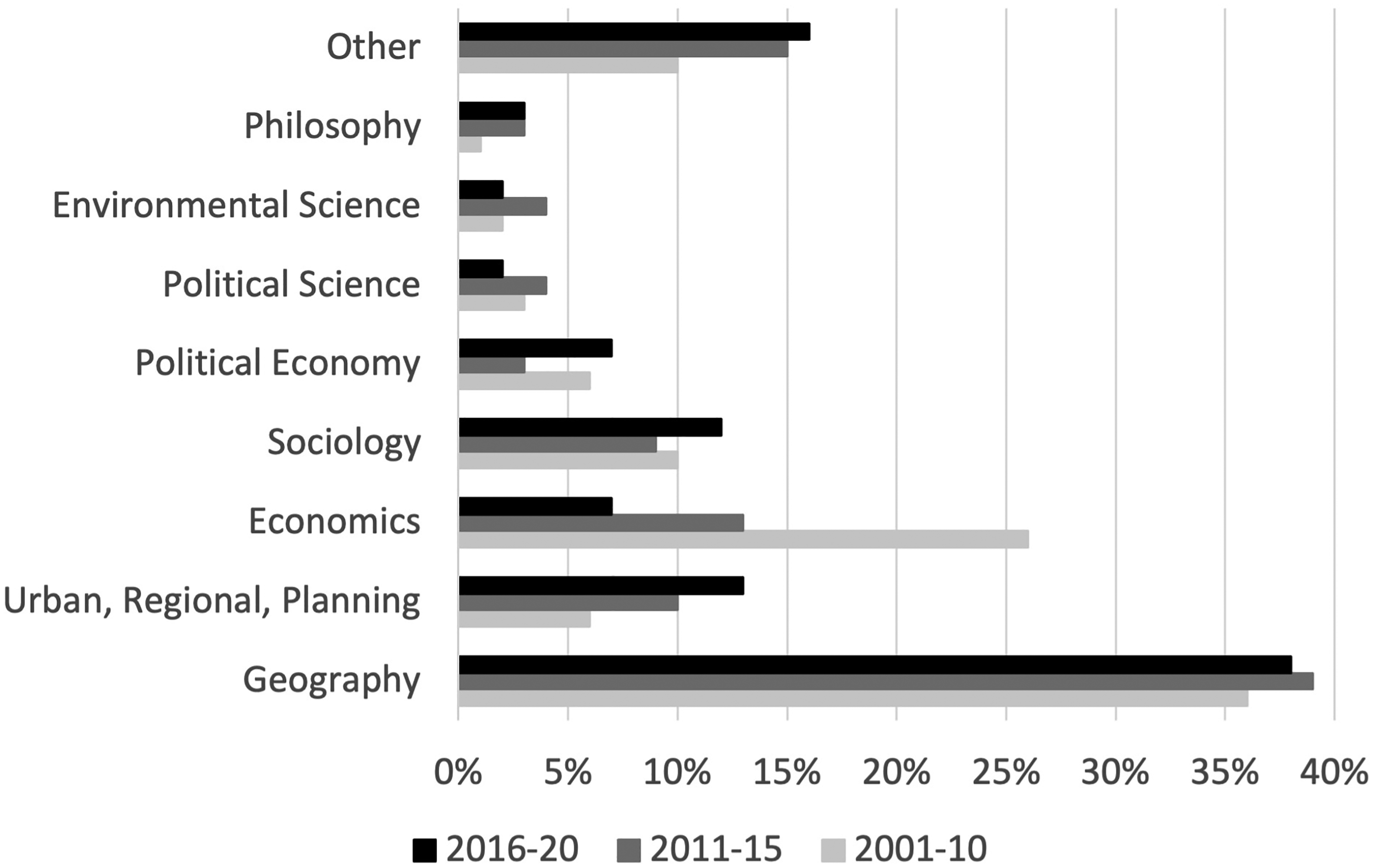

To deepen our analysis of theory and explanation in financial geographies, we need to understand where financial geographers draw their theoretical inspiration. To do so, we classified all theoretical references, including books and working papers, by discipline or subdiscipline. For journals and working paper series, we were guided by the main remit of the journal or the series. For books, we were guided by the main subdiscipline of the author/s based on their current affiliation and self-description on their website. The results are shown in Figure 2.

Main sources of theory and concepts in financial geographies. Source: Authors.

Given that our sample of financial geographies covers geography, urban studies, and urban and regional planning, it is not surprising that the main sources of theoretical references are from exactly those fields. Geography provides 38% of major theory references over the whole period, and its share is quite stable over time. Urban, regional, and planning studies have become the second most significant source over time. If we add this group to geography, their total share is about 50%, with the other half representing a genuine external influence on financial geography. This aligns with Gibadulina's finding that ‘the interdisciplinary nature of the field is highlighted by the fact that almost half of cited journals emanate from outside of geography and urban studies, showing that financial geography draws almost as much inspiration from outside the discipline as it does from within’ (2021: 159).

The origins of external influence exhibit a major shift, which we do not think has been uncovered before. While in the first decade of the century, economics, including financial economics, frequently influenced theory in financial geography, its use in the second decade faded away. We find 55 key theoretical references from economics in 2001–10 and 50 in 2011–15, yet there were only 26 in 2016–20. Note that economics here includes any economics, orthodox or heterodox, though it excludes political economy, which is considered in a separate category. Particularly remarkable is the meagre influence of financial economics, by which we understand any type of economics focused specifically on finance, whether it stems from publications in journals or reports of international economic and financial organisations. Although any financial economics, defined broadly, was present as a key theoretical or conceptual source in 5% of papers in 2001–10, in the second decade, this share fell to a paltry 1% (e.g. Fingleton et al., 2015; Sokol, 2013). In fact, in 2016–20, there were more theoretical influences in financial geography from rural studies (part of the other category) than from financial economics.

The main growth in external influence has come from a wide range of disciplines classified as ‘other’, followed by sociology. In 2016–20, sociology became the most important external influence on financial geographies. A major reason is the financialisation turn, with many of its key theoretical sources in sociology, as discussed above. Financialisation has also elevated the influence of urban and housing studies and accompanied the revival of political economy in financial geographies. Disciplines classified as ‘other’ primarily include anthropology, cultural studies, rural studies, management, real estate studies, and science and technology studies. Their growing share may be seen as evidence of the growing interdisciplinarity of financial geography, but with a caveat that it is an interdisciplinarisation away from economics and financial economics in particular.

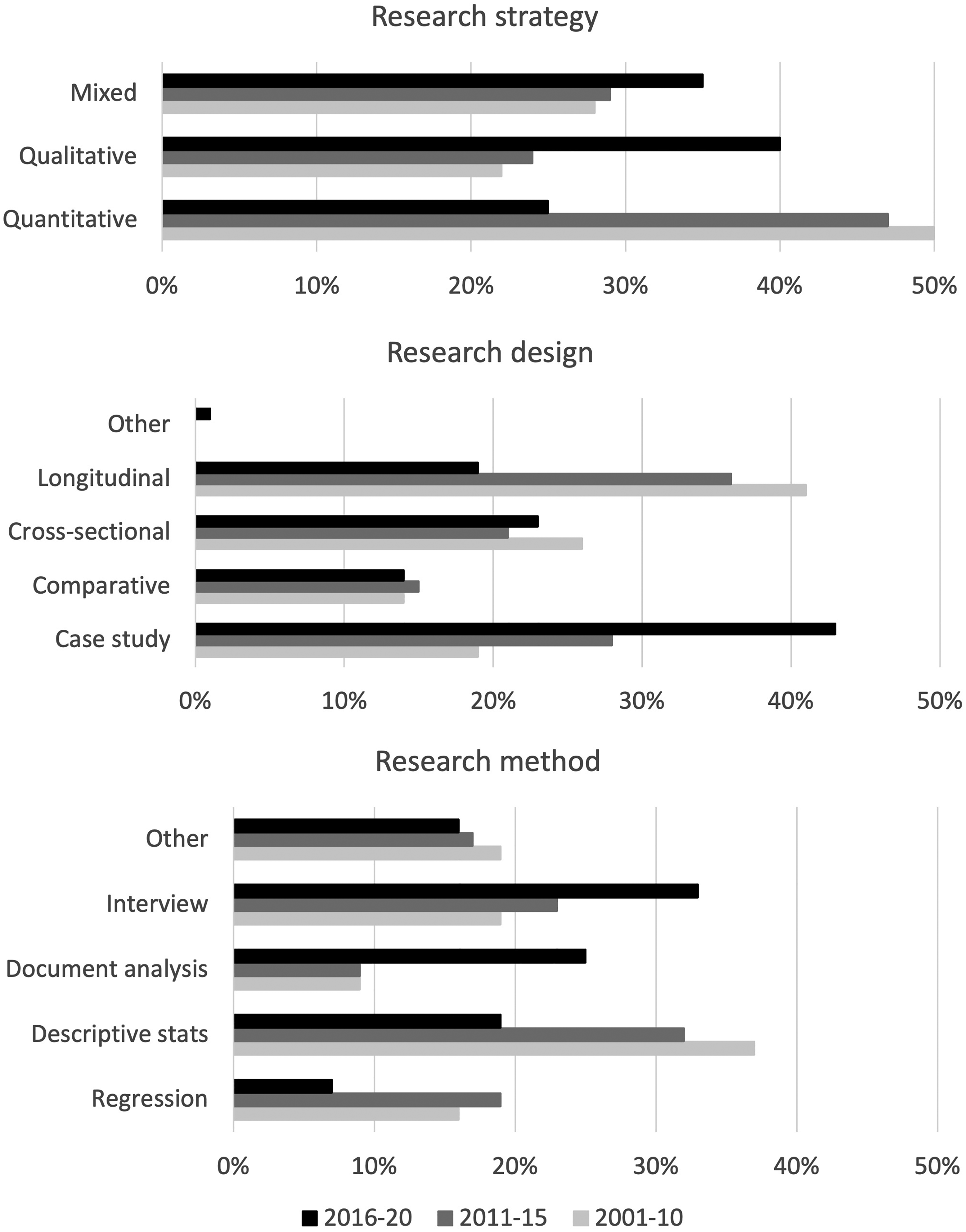

The declining influence of economics and disappearing recognition of financial economics is reflected in the theories and concepts used in financial geographies, but also in how explanation is executed. Figure 3 shows research strategies, designs, and the main methods used in financial geographies in our sample. To construct it, we coded each article that had any empirical analysis (394 out of 449) as belonging to one of the three broad research strategies and one of the five research designs, based on Bryman (2015). We also noted the main method applied in each empirical paper. There are many different methodological classifications, but Bryman (2015) is popular across the social sciences and does the job in highlighting trends in financial geographies (for details of the methods behind the figure, see Wójcik, 2022).

Research strategies, designs, and methods in financial geographies. Source: Authors.

In line with the declining influence of economics on theory and explanation in financial geographies, we see an accelerating decline of quantitative methods accompanied by the rise of mixed and particularly qualitative research strategies. We also see the decline of longitudinal research and rise of case study as the dominant research design applied in 43% of influential works published in 2016–20. Financialisation studies contribute significantly to these trends, with the share of papers following a quantitative strategy falling from 38% in 2001–10 to 23% in 2011–15 and 18% in 2016–20. Qualitative or mixed-methods case studies firmly established themselves as the majority research design in studies of financialisation, relying mostly on interviews and document analysis. Meanwhile, regression analysis is nearing extinction and the use of descriptive statistics is dwindling. Few quantitative and longitudinal studies on financialisation include Wijburg and Aalbers (2017) and Dewilde (2018), the latter of which employs regression analysis. These are notable exceptions, but the fact remains that financial geographies have swung a long way towards qualitative research based on case studies and away from any quantitative methods beyond descriptive statistics. The former certainly can and does contribute to explanation in financial geographies, but in our view, the growing imbalance in the modes of explanation may result in the extinction of any advanced quantitative methods, a neglect of (big and other) data becoming available, and consequently impoverishing theory and explanation in financial geographies as a whole. An additional problem is that many studies in financial geographies, particularly those following qualitative methods, neglect to discuss methods altogether (Wójcik, 2022).

The move away from economics towards more open-ended narrative styles of explanation (and non-explanation) can also be seen in the declining use of hypotheses. To document it, for each paper, we noted whether it used any hypotheses or not, irrespective of whether they were tested with quantitative, qualitative, or mixed research strategy. Our results show that the share of papers formulating a hypothesis was 14% in both 2001–10 and 2011–15, but it fell to 8% in 2016–20. Over these two decades, only 4% of financialisation studies used hypotheses (e.g. Rouanet and Halbert, 2016; Theurillat and Crevoisier, 2013). Describing the processes of financialisation in yet another case study is a contribution to research, but using hypotheses could help financial geographers ask more testable research questions and refine financialisation as a theory. Explanatory theory needs a balance of rule-based and case-based research (Gilboa et al., 2014). Practical adequacy requires both internal and external validities. Case-based research cannot keep ignoring the existence of and need for rules or models that can explain general processes.

Another concern is that while the range of phenomena being explained with financialisation is ever wider, the empirical scope of explanation in financial geographies is getting narrower. Fewer than 5% of articles in the whole sample venture empirically beyond one continent, and even fewer studies are global in scope. Exceptions, Derudder et al. (2011) on banking centres, Lizieri and Pain (2014) on office investment, and Heemskerk et al. (2016) on interlocking directorates. While there are many papers on China, only a handful compare China with any other countries (e.g. Dunford and Yeung, 2011; Lim, 2010; Wójcik and Camilleri, 2015). In contrast to many cross-European studies, cross-national studies for Africa, Latin America, or Asia hardly exist. One notable exception is a study by Fernandez and Aalbers (2020) on financialisation in the Global South. Studying local can, of course, help understand global phenomena, but it does not diminish the significance of studies with global empirical scope. Dominated by case studies, financial geographies risk missing opportunities for addressing the global scale of many problems, including the environmental crisis, and opportunities to use international financial data sources.

In our view, this conjuncture of declining quantitative interests and skills in human geography and the rising interest in financialisation, particularly in the wake of the global financial crisis of 2008, contributed significantly to the state of theory and explanation in financial geographies. Here, we differ from Gibadullina (2021) who highlights the latter, but not the former part of the conjuncture. Here, we also engage with Christophers’ (2015) and Poovey's (2015) observations that research on the spatial production of finance has not developed as much as that on the financial production of space. While lack of engagement with economics affects both strands of enquiry in financial geography, it arguably impoverishes the former in particular. As much as it pains us to write this, economists (broadly defined) had studied the nature of finance for a long time before geographers started, going all the way back to Adam Smith (Ioannou and Wójcik, 2022) and the first formal theories of money in the early 20th century (Bernstein, 2005). Unsurprisingly, the absolute majority of work on finance ever published comes from financial economics. When we put financ* as a topic in Web of Science, we find 518,000 publications, with 202,000 from economics or business studies (including financial economics), 11,000 from geography and urban studies, and 6000 from sociology. If geographers rightly complained about economists appropriating geography through their new economic geography à la Krugman 25 years ago, and about neglecting 100+ years of research in economic geography (e.g. Martin, 1999b), so we should be careful of neglecting decades of financial economics while studying financial geographies. To know what we want to be distinctive from while developing our identity and impact, financial geographers need to maintain their understanding of economics.

We realise that our arguments can be controversial. It is true that the hubris and complacency of economists, and belief in the efficiency of markets and their equilibrating and self-disciplining nature, paved the way to the global financial crisis, as it made regulators and politicians listening to economists blind to critical problems brewing in the economy (French et al., 2009). Arguably, finance is an area of the economy with regard to which economists’ hubris did the most damage to society in living memory. There were dominant economic models saying that global banks were safe and sound, and asset bubbles never happen. There were models blind to the threats posed by bloated financial sector and markets. As a leading economist, Rodrik admits, ‘[w]here economists pushed the logic of the Washington Consensus the furthest, with probably the greatest damage, was in financial globalization’ (2015: 163). Financialisation studies, social studies of finance, and interest in financial geographies boomed largely in response to this damage inflicted by economists (Gibadullina, 2021). Why should we then pay more attention to economics and explanatory theories and models of the kind economists use?

In response, let us re-emphasise five points. First, there is not one economics to engage with, but varieties of economics, with a choice of traditions, theories, models, and methods. It is unfortunate that economics ends with an s, so that in the English language at least, it is difficult to talk about economics in the plural, just as we can talk about financial geographies as plural. Social reality is too complex to be explained with one grand theory. Here, it is useful to quote from Dani Rodrik's view of what economics partly is and should be more like. He states that ‘different contexts – different markets, social settings, countries, time periods, and so on – require different models’ (2015: 228), and that ‘reliance on multiple models does not reflect the inadequacy of our models; it reflects the contingency of social life’ (916). Note that finance is full of practice-oriented journals (e.g. Financial Analysts Journal), not dissimilar from planning journals in geography. Think of the Journal of Portfolio Analysis, where Markowitz published his modern portfolio theory. Given its size, economics focused on finance and finance as a practice are much more diverse than divisions into orthodox versus heterodox schools would make us believe and hence bigger is the scope for engagement and innovation.

Second, a distinction needs to be made between fashions and fads in economic thinking and the toolkit available in economics. Neoclassical economics was embraced in the 1990s not because of the lack of economic theories and models that pointed in directions opposite to market efficiency and self-regulation (Rodrik, 2015). It was a social–political mechanism and historical contingency that made neoclassical economics influential, not necessarily the nature of economics as such. There were economists and theories, not far from the neoclassical tradition, including Shiller (2000) and Rajan (2011), who pointed to the dangers of bloated finance, not to mention the whole tradition of post-Keynesian economics, which focused on them. There was a principal–agent model that should have helped see the problems of bank managers taking excessive risks against the interest of shareholders and society at large. Perverse incentives of rating agencies to approve toxic financial instruments designed by investment banks should have been clear to every economist, given that incentives are a central concept in their vocabulary. It is first and foremost economists, individually and their collectives, who should be blamed when they mistake a theory with the theory, and promote and parade their ideas and ideologies as irrefutable science (Deaton, 2023).

Third, economics is changing. Economists learnt some lessons from the experience of the global financial crisis. The shock was genuine. None of them before experienced such a major crisis in advanced economies in their lifetimes. A model of bank runs and the role of government in preventing them was awarded the Nobel Memorial Prize in Economic Sciences in 2022 (Diamond and Dybvig, 1983). The International Monetary Fund withdrew from the policy of preaching and forcing free cross-border capital flows, instead admitting its dangers and the need for institutional development as a prerequisite for any financial liberalisation (IMF, 2012). Shiller was awarded a Nobel Memorial Prize in Economic Sciences for behavioural economics, though somewhat awkwardly with Fama, the creator of the efficient market hypothesis. Economics has also been stimulated by more data, including the big data variety, with technology enabling quick collection and processing of the data. At the same time, it has tried to respond to the demands of industry strategists and policymakers grappling with rising uncertainty, and diminishing confidence in old-established economic theories. The Economist (2021) has referred to it as ‘third-wave economics’ characterised by more data- and policy-driven, as well as more collaborative, research, following the first and second waves focused on theory and conventional statistics, respectively. Arguably in many ways, over the last 15 years economists have got closer to what geographers were expecting of them (i.e. more bottom-up, inductive research grounded in specific contexts; see Martin, 1999b).

Fourth, neglecting economics misses important opportunities to engage with economists interested in financial geographical questions. When we put financ* and geograph* in a Web of Science topic search on 10 February 2023, we found 11,097 publications, out of which 2022 come from business and management studies and 1724 from economics, followed by environmental studies (1710), geography (1695), and urban and regional studies (981). Political science shows only 211, international relations 181, and sociology 158 publications. As such, 40% of publications that show explicit attention to things financial and geographical at the same time come from geography and related fields, and the next 35% from economics, business, and management studies. There are plenty of papers in financial economics on the role of proximity and spatial networks in finance, both defined in more and more nuanced ways (e.g. Bae et al., 2008; Loughran, 2008; Malloy, 2005). It is not (yet) geographical finance, à la geographical economics of the 1990s, since typically spatial concepts are being added into econometric models rather than being explained, but it illustrates an ongoing ‘spatial turn’ in financial economics. While many are suspicious that economists are horrible at citing non-economists and would hardly ever cite geographers, Gibadullina (2021) shows that economics, business, and finance studies accounted for 38% of citations of her sample of financialisation studies compared to a 6% share of sociology, 5% of political science, and 4% of development studies. There is an audience we are missing by not engaging more with economists.

Fifth and on a related note, economists, whether we like it or not, have the ear of policymakers and strategists, particularly in finance. While practitioners may listen to sociologists with regard to labour markets or political economists with regard to international trade, they tend to treat finance as quintessentially economic. A global study by Lebaron and Dogan (2016) shows that 83% of central bank governors have a degree in economics. Chief sustainability and chief digital officer positions are proliferating in large companies, but chief economists are not going anywhere, and there are no positions of chief geographers. In our view, this is another reason to engage with economics and explanatory theory. We need to be mindful that economists have a proven professional bias and vested interests to profess and defend markets, the financial and business services complex, and financial elites (Deaton, 2023; Rodrik, 2015). But, as Rodrik's account of and for economics illustrates, many economists share geographers' concerns and viewpoints. It is worth engaging with them to influence change wherever and whenever possible.

Boarding boats with economists

As the preceding sections make clear and borrowing from Dicken (2004) reflection on geographers missing the opportunity to drive interdisciplinary research on globalisation, financial geographers certainly did not miss the boat of financialisation. Quite the contrary, geographers have been among the first (Engelen, 2003) and among the leading thinkers of financialisation research (Aalbers, 2015), and should be applauded for that. However, as we argue in this section, the growing disengagement with economics, and particularly financial economics, prevalent in financial geographies, and particularly in financialisation studies, has made financial geographers miss or prone to missing top seats on other boats – phenomena central to understanding finance. Here, we focus on three big issues: quantifying financialisation, sustainable finance, and decentralised finance. We do not claim that financial geographers have not contributed to understanding these issues or have not engaged with economics at all. Instead, we argue that in all three areas more engagement with economics would be beneficial to progress in financial geographies. In our view, financial geographies should indeed rest at the core of discussions on quantifying financialisation as well as sustainable and decentralised finance.

The moribund engagement of financialisation, as a theory practiced in financial geographies, with economics, has little to do with the nature of financialisation as a theory or empirical phenomenon. The kind of financialisation that makes its way into financial geographies should not be taken for granted. Felipini and Palludeto (2018) hint at the strong geography–sociology alliance and anaemic geography–economics engagement in financialisation studies in their 1992–2017 bibliometric analysis, though they never discuss it. A simple Web of Science exercise conducted on 12 February 2023 identified 4464 publications containing terms ‘financialisation’ or ‘financialisation’ in the topic (title, abstract, or keywords). The largest disciplinary category in this sample is economics (1528), followed by geography (680), business finance (537), environmental studies (523), political science (478), sociology (453), and urban studies (408). Publications on financialisation in economics are dominated by heterodox journals, but flagship orthodox journals like the Journal of Finance, Review of Financial Studies, and the Journal of Banking and Finance also feature (e.g. for work on the financialisation of commodity markets, Adams and Glück, 2015). There is nothing intrinsic to financialisation that makes it more social (or political) than economic or more conducive to qualitative than quantitative research strategies. In financial geographies, we find that financialisation is what authors bring to it from a larger body of financialisation studies. They tend to prefer sociology and urban studies to any type of economics and prefer words to numbers. They draw relatively little from the large – larger than the sociology or urban studies – body of more economic and quantitative work on financialisation that has developed in economics. Dymski's (2015) account of the massive uptake of financialisation in heterodox economics and calls for more engagement between geographers and heterodox economists have largely fallen on deaf ears.

Documenting how finance and financialisation transform relationships among people and among people and their environment in specific contexts, which is the forte of financialisation studies in financial geographies, is crucial. But, to pinpoint financialisation and its impacts, we need to quantify them to be able to tell policymakers and others how much of what kind of finance is too much finance. We need both quantitative and qualitative research to identify when a space or place becomes a hotspot of financial instability. These things are matters of qualitative and quantitative relationships and proportions. One method available in heterodox economics, rooted in post-Keynesian theory, is macro-accounting, which focuses on the stocks and flows in key economic sectors: corporate sector, households, government, finance, insurance, and real estate. A typical model consists of a balance sheet of each sector, and a table showing flows of funds between sectors, combined through a series of macro-accounting identities (Godley and Lavoie, 2007). Such a model can cover a whole national economy or individual regions or industries. By focusing on the financial sector, stocks, and flows, it helps identify areas most dependent on credit, and the build-up of unsustainable debt (Bezemer, 2010).

Another example from heterodox economics is post-Keynesian models that link rising inequality and financial deregulation to rising household debt and financial instability, which in turn strengthen the polarisation between debt-led-growth and export-led-growth economies, which fuel even more bubbles and bursts on financial and real estate markets. One of these models was developed by the leading post-Keynesian economist working on financialisation, Stockhammer (2015), whose research does not feature as a key theoretical influence in any paper in our sample. This is unfortunate, as geographers could play a key part in mapping the imbalances between debt-led-growth and export-led-growth economies at both international and subnational scales. There are emerging econometric financial geographical studies on the relationships between financialisation, globalisation, growth, and social and spatial inequality, with global coverage and subnational scale of analysis (Ioannou and Wójcik, 2021a, 2021b, 2023), and those showing that the financial, particularly the real estate sector, has become even more central to the US economy since the subprime crisis of 2008 (Iliopoulos and Wójcik, 2021), but much more work is needed.

The second opportunity for mutual engagement is sustainable finance, concerned not only with environmental, but also social and governance issues (Schoenmaker and Schramade, 2019). As Aalbers (2015) argues, the question of financialisation is not when an economy becomes fully financialised, but how to keep financialisation within limits in ethical, sustainable, and humane terms. According to Aalbers, such limits have already been exceeded. There are many economists, environmental and financial, who agree with this and look for solutions. The potential for financial geographers' engagement is compounded by the fact that sustainable finance research is emerging and booming, but there is no established theory of sustainable finance as such. The environmental side of sustainable finance also offers ample opportunities for collaborations with environmental and physical geographers. In this sense, financial geographies can be as much a force for external collaborations as for advancing integration and realising synergies within geography. There are a growing number of geographical studies that exemplify the benefits of close engagement with economic and financial theory and practice. Christophers (2019), for example, offers insights on how financial actors think and the apparatus they use to measure fossil fuel investment risks. Ouma (2020) uses Orléan's theory of value to account for the assetisation and valorisation of farmland. We argue that more and even closer engagement with financial economics is warranted.

There is overwhelming evidence in financial economics and management studies that stock markets react to a corporation's environmental footprint, punishing eco-harmful and rewarding eco-friendly behaviour (Flammer, 2013). Such research is mostly based on the stakeholder and natural resource-based theories of the firm. The former recognises that companies should consider everyone who can substantially affect or be affected by the company (Agle et al., 2008). The latter proposes that companies fostering resources in favour of environmental awareness are likely to gain competitive advantage and a chance of higher profits (Hart and Dowell, 2011). Financial geographers are perfectly positioned to engage more with this research by advancing analysis on the heterogeneity of companies and contextual factors that affect corporate environmental and social responsibility. Geographers' ability to open the black boxes of the firm and markets geographically could be used, for example, by combining the global production and the global financial network approaches (Coe et al., 2014), explaining how various internal and external configurations of firms relate to their environmental, social, and governance behaviour.

Further on the environmental front of sustainable finance, behavioural economists suggest the introduction of individual carbon scorecards, taking advantage of big data on mobility and energy use, to nudge individuals in the direction of more sustainable lifestyles (Agarwal and Salvo, 2022). At a macro-level, financial economists propose to use carbon credits as a new digital currency (Chen et al., 2017), possibly facilitated by central banks (Dikau and Volz, 2021). At the heart of such proposals is the idea to transform money, as a medium of human–environment relations, to make these relationships more sustainable in terms of energy use and pollution control. This is a quintessentially financial geographical challenge, which needs to be addressed by more qualitative assessments of carbon and climate finance (e.g. Christophers et al., 2020; Knox-Hayes, 2016), but it also requires quantitative engagements with behavioural and financial economics and its models. It also calls for more research on the use of geo-spatial techniques, such as earth observation to track carbon and other greenhouse gas emissions, as well as biodiversity loss at a granular scale (Caldecott et al., 2022). This so-called spatial finance offers potential for engagement between financial and physical geographers and economists.

Elsewhere, on the more social and governance side of sustainable finance, economists lead research and campaigns for more financial transparency and more globally equitable taxation that would reduce tax avoidance and evasion, as well as help fight against illicit economic, social, and political activities, including the drug trade and corruption. This involves a giant forensic exercise of mapping financial flows and stocks that avoid and evade mapping. Tax Justice Network (e.g. Cobham et al., 2015), Zucman (2015), Tørsløv et al. (2023), and others have collated impressive publicly available datasets on such topics over the last 15 years, but, as documented by Aalbers (2018), few geographers have used them or engaged with any tax-related topics before or since (e.g. Janský et al., 2023). Calls for geographies of public finance by Tapp and Kay (2019) and August et al. (2022) underscore this deficit, with the latter proposing engagement with modern monetary theory.

Declining interest in quantitative research is arguably a key reason for anaemic geographies of taxation and public finance, as such topics often require detailed financial economic knowledge of accounting, economics, and law. The challenge, however, opens opportunities for geographers to engage with economics and economists, including law and finance experts. The Anti-Corruption Evidence program offers a positive example in this regard (Haberly et al., 2023). There is a campaign led by economists on introducing minimum taxation rules on a global scale. Ghosh et al. (2023), for example, have criticised insufficient progress made on that front by the OECD as the rich country club and called for the United Nations to take charge of the initiative to give more voice to countries in the Global South. In short, research on financial transparency and taxation reforms represents boats full of economists that should be boarded by more financial geographers. As Knuth’s (2023) analysis of tax credits for renewable energy shows, geographies of public finance are intricately linked with those of sustainable finance.

For the last research area, we highlight – decentralised finance (aka DeFI) – its quintessentially geographical character starts in the very name. Financial geographers have made great strides to examine FinTech as a set of innovations and an emerging economic sector (see Wójcik, 2021a; Knight and Wójcik, 2020, for a review). In doing so, they have applied the conceptual lenses of ecosystems, financial ecologies, global financial networks, and digital platform economies as well as explored the implications of FinTech for financial centres, financial inclusion, inequality, and governance (see Wójcik, 2021b for a review). While financial geographical research on FinTech is still in a nascent stage, DeFi raises the associated challenges and opportunities to a new level. DeFI can be defined as a ‘financial ecosystem built on technology that does not require a central organisation to operate and that has no safety net. It consists of protocols – implemented as “smart contracts” – running on a network of computers to automatically manage financial transactions. Implemented on top of the distributed ledger technology, it does not require banks or other traditional centralized intermediaries’ (Auer et al., 2023: 3). Geographers' reaction should rightly be sceptical, given the history of revolutions that have promised, but failed to decentralise finance, including telephone and internet banking, direct finance through capital markets, and securitisation. However, we should not ignore potential transformations that DeFi can unleash.

At its core, DeFi promises trustless finance, one in which technology deals away with the role of trust (Zetzsche et al., 2020). This would redefine the role of physical, social, and other types of proximity in finance, as well as between finance, other sectors, and government. Consider that, currently, business seeks proximity to finance and vice versa, and that the overlap between the geography of political capitals and financial centres is largely in place because finance and politics need and want to be close to each other. As a result, at least under a radical scenario, DeFi could change financial behaviour, as well as the financial, economic, and political maps of the world. The good news for financial geographers is that economists are as behind in researching such implications as are other social scientists. However, with growing interest among financial regulators, such as the Bank for International Settlements (Auer et al., 2023), behavioural financial economists (Bennett et al., 2023), and proliferating business school courses on DeFI, the time for boarding this boat is running out, too.

Conclusions and implications

Given the booming research on financial geographies, financial geographers should be ready to accept the 1969 challenge of Harvey revisited and reworked by Yeung (2024) on the significance of theory. If financial geographies are to develop and have influence in geography as a whole and beyond, people need to get to know financial geographers by their theories. In this paper, we advanced this point by taking a stock of theory, concepts, and explanation in financial geographies between 2001 and 2020, as well as by reflecting on some of its causes and implications. In line with Yeung's (2024) and Rodrik’s (2015) view of scientific progress in social sciences through multiple mid-range theories, our goal was not to offer a specific ‘go to’ and ‘how to’ explanatory theory for financial geographies. We approached ‘our theories’ as ‘theories we use’ rather than necessarily ‘theories we invented’, so we did not focus on examples of the latter, including variegated financialisation (Aalbers, 2017) or global financial networks (Haberly and Wójcik, 2022). We believe that the openness of financial geographers to external theoretical influences is a virtue. Hence, we were less concerned with whether theories and concepts are ‘imported’ or home-grown, and more with the quality of theories and the explanations they offer.

Our analysis confirms the lone ascent of financialisation to the status of the leading theory in financial geographies. We characterise its ascent as lone and its status as the leading theory, because, as we document, no other theories in financial geographies match its influence and ascendency. Our findings also show that economics, particularly the financial variety, has been gradually pushed away from financial geographies in a shift that accompanied the decline of quantitative research strategies. We do not think that these results are an artefact of our sampling covering publications in geography, urban studies, and regional and urban planning. There is little that prima facie or by nature would push these fields towards growing dominance of financialisation, qualitative methods, and disengagement from economics. If we were to include economics in the sample, we would get more quantitative methods, but we exclude economics for the same reason we exclude sociology and anthropology. What makes the decline of quantitative research even more alarming is that it concerns not only traditional methods involving mathematics and statistics, but also reflects the paucity of research using modern computational methods, such as programming and data scraping.

As we explain, the three developments – the rise of financialisation as theory and the decline of economics and quantitative research – are closely interrelated in the context of the cultural turn in human geography, at least in the UK and the USA, countries that dominate the global landscape of financial geographies in terms of the educational background and institutional affiliation of authors and journals (Gibadullina, 2021). We argue that these developments pose challenges to the role of explanatory theory in financial geographies, and that these challenges need to be addressed by strengthening relationships between financial geographies and economics, among other means. Denial of financial economics based on their caricatures, with efficient markets hypothesis in the lead, may seem comforting to many, but it is counterproductive to financial geographies. In this spirit, we outlined the need for and opportunities of engagement with financial economics in the broadly defined areas of quantifying financialisation, sustainable finance, and decentralised finance, but there is potential in other areas, too.

Arguing that we have potential allies in varieties of economics for both improving the practical adequacy of financialisation and for the development of other mid-range theories, we are not projecting an economics-envy nor calling for a takeover of financial geographies by modes of enquiry typical of economics. The definition of theory we started with comes from sociology, not economics. As authors, we cite and publish both quantitative and qualitative financial geographies influenced by research from a wide range of disciplines beyond geography and economics. The momentum behind financial geographies gives us confidence that financial geographers can engage with economists interested in finance and space on mutually beneficial terms. We are not claiming that explanatory theories and engagement with economics are the only way forward for financial geographies. The rise of qualitative research, which can involve explanatory theory on its own terms, can be seen as a positive contribution of financial geographies to studies of finance as a whole, given that the latter are dominated by quantitative research. Bemoaning this state of affairs in finance, Kaczynski et al. (2014: 127) writes: ‘imagine the benefits to finance if we expand our empirical sources of data to include what people have to say, which then allows us to explore the complex reasoning behind these conversations’. Financial geographies certainly help address this deficit. However, the growing neglect of quantitative research strategies is likely to impoverish the practical adequacy of explanatory theory and explanation in financial geographies.

Explanation can be achieved through qualitative, quantitative, and mixed research strategies and methods. In fact, geography has a long tradition of mixed-methods research that we should be proud of and promote through education. However, as both authors of this article experienced, undergraduate students in geography, at least in the UK, increasingly tend to sort themselves into qualitatively minded human and quantitatively minded physical geographers. As a consequence, it is qualitative geographers who then pick up financial geographies. The end result is imbalanced financial geographies, with disappearing quantitative and weak mixed research, which does not venture beyond basic descriptive statistics. Of course, we are simplifying the picture, but we do so to highlight that restoring balance and improving theory and explanation in financial geographies require reformed training for geographers and are part and parcel of broader challenges facing geography as a discipline.

In our view, one creative way for geographers to revive more balance between quantitative and qualitative approaches to finance leads through financial visualisation, which can be based on data, coding, data scraping, and other mixtures of traditional and novel quantitative methods, just as it can involve drawings of concepts, photographs, or videos. The new Finance and Space journal launched a FinVis section to publish any artwork, quantitative or qualitative, that spatialises finance (Wójcik et al., 2024). Accompanied by a short text, FinVis articles can lower barriers to entry for the development of new ways of presenting and seeing financial phenomena.

Our call for dialogue with economics echoes an established debate in economic geography. Martin (1999b), for example, was sceptical about dialogue between geographical economics (aka new economic geography), as practiced by Krugman and others, and economic geography, highlighting stark epistemological and methodological differences (see also The Economist, 1999). Later, however, he noted possibilities for dialogue, in a statement of much relevance to financial geographies: ‘new economic geography theorists could encourage economic geographers to give much greater attention to the role of market forces, prices, and other basic economic processes that seem to have all but disappeared from the appreciative-theoretic work in proper economic geography’ (Martin, 2011: 66). Peck (2012) intervention was as much a warning for geographers against engagement with orthodox economics as a plea for alliances with heterodox economists broadly defined. He also pleaded that ‘quantitative techniques can (and must) be used for many ends, including heterodox and radical ones… They cannot be allowed to die out, due to disuse…; a qualitative methodological monopoly would be no less problematic than a quantitative one’ (Peck, 2012: 120). The problem in financial geography is that alliances with heterodox economics have been anaemic, and the risk of a qualitative methodological monopoly is looming.

Let us finish with two calls for action. One is for financial geographies, including financialisation studies, to consider more seriously their understanding of and opportunities for engagement with economics and financial economics, whether it is mainstream, heterodox, or any other variety. Second, we wish for research on questions concerning the spatial production of finance to match the dynamism of those on the financial production of space and for more mutual engagement between the two legs of financial geographies. Challenging and profound questions on the spatial production of finance, which await more research, are plenty. How does geography explain the behaviour of investors, including their persistent home bias? How can geography explain the formation of commodity prices (e.g. by mobilising the global financial and production networks approaches)? How does geography matter to the evolution of new financial technologies, including FinTech? How do financial bubbles and crises move in space from one place and sector to another? All of these big questions will benefit from collaboration with economists, and all will require a higher level of numerical literary in financial geography to take advantage of opportunities offered by big data, including financial data.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.