Abstract

This teaching case presents a strategic dilemma faced by Ajay Pradhan, General Manager of the Cloud Management Business Unit (CMBU) at VirtuWorld—a global enterprise software provider transitioning from a perpetual license-based business model to a cloud-first, subscription-based Software-as-a-Service (SaaS) model. Amid this transformation, Ajay is tasked with balancing two competing priorities: accelerating new customer acquisition for re-engineered SaaS offerings and retaining existing customers for legacy and cloud-native products. The situation is further complicated by VirtuWorld’s recent $450 million acquisition of CloudDen, a fast-growing SaaS platform focused on cloud cost optimization, which brought in a mature customer base and a SaaS-trained salesforce. The case is constructed using modified data based on real-world market dynamics and organizational strategy. While the company and names have been fictionalized, the scenario draws closely from actual business model transitions in the enterprise technology sector. The case provides learners with the opportunity to analyze the implications of moving from Enterprise License Agreements (ELA) to subscription pricing, and investment trade-offs between acquiring new customers versus retaining existing customers, with the organizational, operational, and go-to-market shifts that accompany such a change.

Keywords

Introduction

Ajay Pradhan, General Manager of the Cloud Management Business Unit (CMBU) at VirtuWorld, sat contemplating a critical inflection point in the company’s transformation journey. As VirtuWorld accelerates its shift from a traditional on-premises software provider to a modern, multi-cloud Software-as-a-Service (SaaS) enterprise, the transition is beginning to show promising signs—SaaS and subscription-based revenues have grown by over 14% year-on-year. However, Ajay is increasingly aware that the very practices that once made VirtuWorld a market leader in legacy software may no longer suffice in a subscription-driven ecosystem. The new model demands not just changes in product delivery, but a fundamental reorientation of customer engagement strategies. Continuous value delivery, proactive customer success, and usage-driven expansion are now essential for sustaining growth. As the company doubles down on its SaaS-first ambition, Ajay faces a pressing strategic dilemma: should he prioritize acquiring new customers to scale the business rapidly, invest in deepening relationships with existing customers to reduce churn and drive expansion, or adopt a blended approach that balances both imperatives? The answer carries significant implications—not only for revenue growth and customer satisfaction but also for VirtuWorld’s long-term positioning in an increasingly competitive SaaS landscape.

VirtuWorld

Founded in 1996, Redwood City, California, VirtuWorld has been a pioneer in enterprise virtualization and cloud infrastructure solutions, enabling organizations to optimize IT resources, enhance operational efficiency, and accelerate digital transformation. Known for its flagship virtualization technology, VirtuWorld helped redefine how data centers operate by abstracting computing resources and enabling scalable, software-defined environments. Over the years, the company expanded its portfolio to include multi-cloud management, networking, security, and modern application development platforms—serving a global customer base across industries. As the enterprise IT landscape shifted toward subscription-based and cloud-native delivery models, VirtuWorld embarked on a strategic transformation to become a SaaS-first company. This transition represents not just a change in how technology is delivered, but a reimagining of the company’s customer relationships, revenue models, and value creation mechanisms in an increasingly competitive cloud ecosystem.

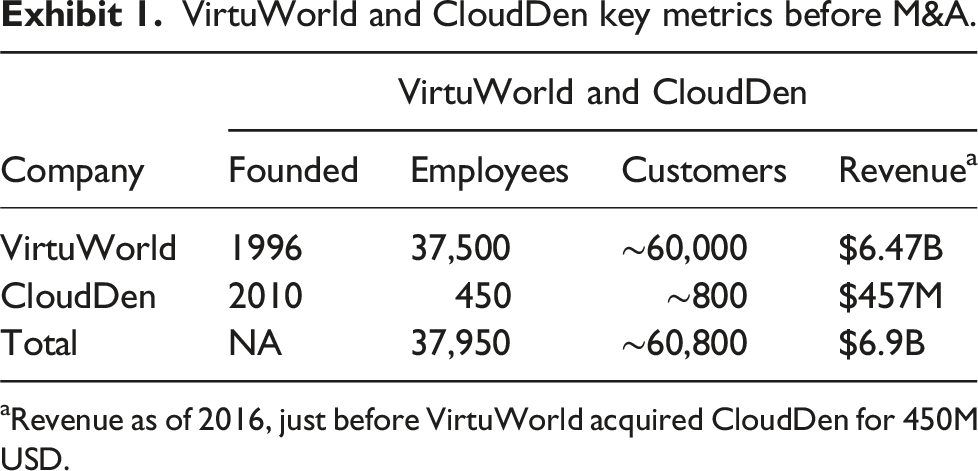

VirtuWorld and CloudDen key metrics before M&A.

aRevenue as of 2016, just before VirtuWorld acquired CloudDen for 450M USD.

Cloud computing market landscape

The emergence of cloud computing in the early 2000s fundamentally reshaped how organizations approached IT infrastructure and digital innovation. A key inflection point came in 2006, when Amazon launched Amazon Web Services (AWS), introducing scalable, on-demand computing resources through offerings such as Elastic Compute Cloud (EC2). This model allowed businesses to move away from capital-intensive, on-premises infrastructure toward a flexible, utility-based operating expenditure model. The reduction in upfront costs enabled a wave of “born-in-the-cloud” startups to rapidly innovate, scale, and focus on their core competencies without the burden of managing physical infrastructure.

By the mid-2010s, cloud adoption had broadened beyond startups to become a central pillar of enterprise IT strategy. A notable shift occurred around 2016, as cloud platforms evolved from being merely developer-friendly to developer-driven. Application developers increasingly leveraged cloud-native tools, APIs, and services for rapid prototyping and deployment, prompting cloud providers to tailor their offerings toward developer needs. The COVID-19 pandemic further accelerated cloud adoption, as organizations rapidly digitized operations to enable remote work, online collaboration, and e-commerce. Looking ahead, the cloud computing ecosystem is expected to be shaped by the growing emphasis on automated data governance, compliance with evolving regulatory standards, and the integration of AI-driven capabilities—all of which present both opportunities and strategic challenges for technology providers like VirtuWorld as they pivot toward subscription-based service delivery models.

Against this backdrop of rapid ecosystem transformation, VirtuWorld’s strategic pivot from on-premises software to a SaaS-first model is not merely a shift in delivery architecture—it signifies a fundamental redefinition of how value is created, captured, and sustained. In a market where speed, flexibility, and customer-centricity increasingly determine competitive advantage, Ajay Pradhan must navigate a high-stakes decision: should the Cloud Management Business Unit prioritize acquiring new customers to capture emerging demand in the cloud-native market, invest more heavily in retaining and expanding relationships with existing enterprise clients, or pursue a hybrid approach that balances both imperatives? The answer is far from obvious. While new customer acquisition fuels top-line growth and market share, customer retention drives profitability, stability, and deeper engagement—especially in a subscription-based business model. With finite resources and rising pressure to demonstrate impact in a fast-moving industry, Ajay’s choice will shape not only the trajectory of his business unit but also VirtuWorld’s relevance in a cloud-first world.

VirtuWorld business model & delivery model

As public cloud adoption gained momentum in the early 2000s, VirtuWorld—a long-standing leader in on-premises enterprise software—faced increasing pressure to evolve. To remain competitive in a rapidly digitizing market, the company began pivoting its product portfolio to address the emerging need for cloud infrastructure monitoring, cost optimization, and usage visibility. This shift was more than technological; it marked a fundamental change in both the delivery model and the business model. In the cloud economy, Software-as-a-Service (SaaS) has become the dominant delivery model—software is no longer installed on customer infrastructure but is accessed on demand via the cloud. Complementing this is the subscription-based business model, which enables customers to pay recurring fees (monthly or annually) for continued access, rather than making large, upfront capital investments. While all SaaS offerings are delivered via subscription, not all subscriptions imply SaaS—some may involve on-premise or even non-technical products. For VirtuWorld, the transition from perpetual license sales to consumption-driven revenue marked a major departure from its historical model, where revenue was recognized at the point of sale, regardless of actual usage.

Ajay Pradhan, General Manager of the Cloud Management Business Unit (CMBU), was tasked with leading this transition. His strategic directive from the CEO focused on three priorities: (1) capturing the multi-cloud enterprise market by offering choice and flexibility, (2) operating as a consumption-obsessed SaaS organization delivering rapid time-to-value, and (3) fostering a unified, customer-centric culture across business units. Yet the journey was anything but simple. It is key to understand why VirtuWorld is under pressure due to its legacy business model. VirtuWorld’s traditional workforce—particularly its sales teams—was deeply entrenched in selling long-term enterprise license agreements (ELAs), often spanning three to 5 years. Under the ELA model, customers were contractually locked in and heavily incentivized through discounts, but the value delivered post-sale often went unmeasured. In many instances, products became “shelfware” once customer engagement dropped, with little impact on short-term revenue—until renewal time revealed the fallout.

In contrast, the SaaS model required a new mindset. Customer journeys became more agile and outcomes-driven. The business was now only as strong as its weakest customer touchpoint. Customers expected near-instant value delivery, and any lapse in experience could result in immediate churn. With this new reality, VirtuWorld could no longer rely solely on upfront bookings. Instead, sustainable growth would depend on customer retention, consumption, and ongoing value realization.

To expedite its transformation, VirtuWorld strategically acquired CloudDen, a rapidly growing SaaS company founded in 2010, Boston, Massachusetts, for a total of $450 million (Exhibit 1). This acquisition is aimed at accelerating VirtuWorld’s shift to a subscription-based, SaaS-first model, leveraging CloudDen’s expertise and established market presence in cloud cost optimization and multi-cloud management (Refer Figure 1). The acquisition of CloudDen in 2016 marked a turning point in VirtuWorld’s strategy. CloudDen has built a reputation for delivering cloud cost management, governance, and optimization services across Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP)—the industry’s three dominant cloud infrastructure providers. CloudDen’s multi-tenant, AWS-hosted architecture and SaaS-first culture made it an ideal catalyst for change. Its salesforce was already skilled at articulating value in a consumption-led business, and its technology natively addressed the needs of customers operating in multi-cloud environments. Summary of events at VirtuWorld and CloudDen M&A with shift in business model, leading to customer acquisition versus retention investment dilemma.

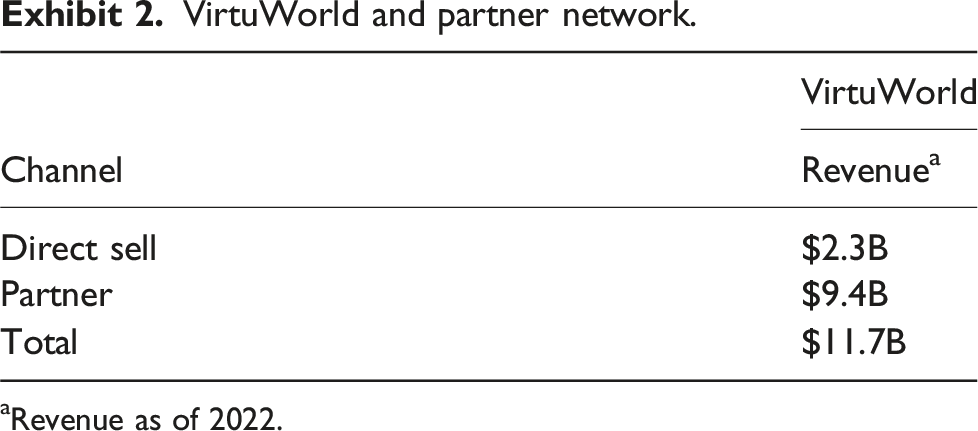

VirtuWorld and partner network.

aRevenue as of 2022.

In the evolving cloud infrastructure and multi-cloud management space, VirtuWorld operates in a highly competitive environment alongside major global players. Industry giants such as Amazon Web Services (AWS) and Microsoft Azure not only provide core cloud infrastructure but have also expanded into native monitoring and optimization tools, increasingly encroaching on independent platform capabilities. Google Cloud Platform (GCP), with its data-driven offerings, is also gaining traction among enterprises seeking advanced analytics and AI integration. Additionally, specialized SaaS providers compete in the cloud cost optimization and IT operations management space, offering solutions that overlap with VirtuWorld’s CloudDen portfolio. As enterprises adopt hybrid and multi-cloud strategies, differentiation through integration, cost transparency, and proactive customer success has become essential for sustaining competitive advantage.

Yet this transformation came with trade-offs. The subscription model allowed customers to walk away at any time—there was no contractual lock-in and no guaranteed revenue beyond the next billing cycle. This meant that VirtuWorld could no longer rely purely on customer acquisition. It now had to build capabilities around customer success, usage monitoring, and proactive engagement, placing equal—if not greater—emphasis on retention. For Ajay and his team, the question remained: how should VirtuWorld balance its efforts between acquiring new customers and deepening relationships with existing ones in a market where every interaction could make—or break—a subscription?

The investment dilemma: Acquire new customers, retain existing customers, or both?

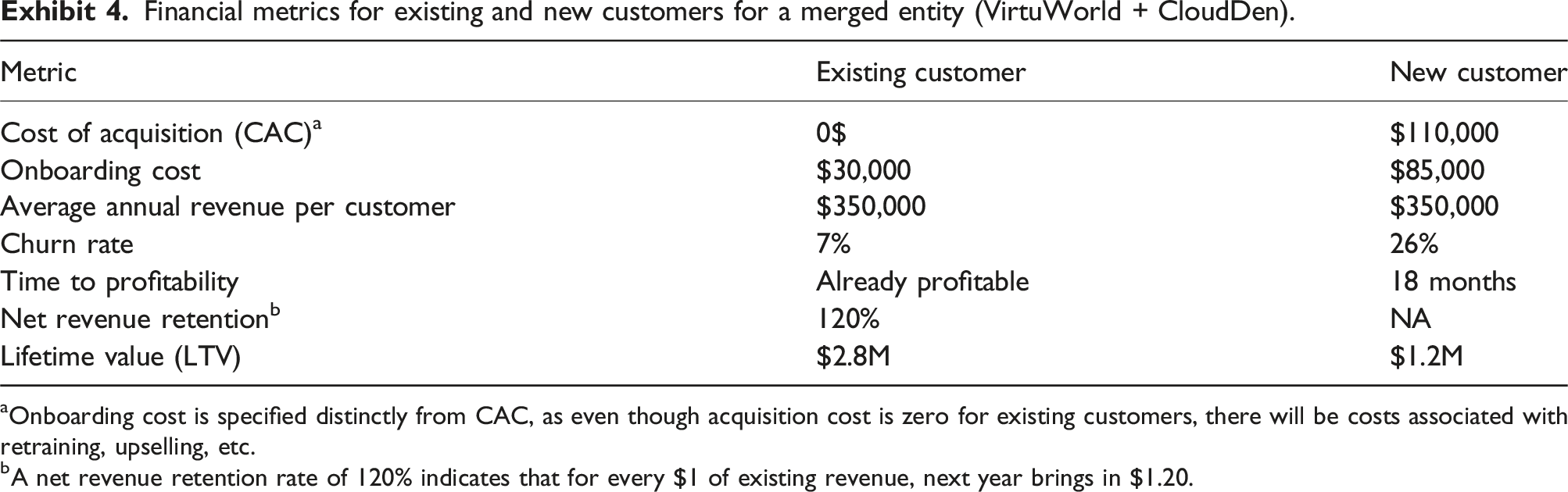

As of early 2023, VirtuWorld accelerated its shift from a perpetual-license Enterprise License Agreement (ELA) model to a subscription-based, Software-as-a-Service (SaaS) delivery model. The focus here should be on a key challenge now emerging: customer churn, and how to strategically manage the trade-off between acquiring new customers versus retaining existing ones in a fast-changing B2B SaaS market. Unlike the legacy model—where customers were contractually locked in for three to five years—subscription customers now enjoy the flexibility to discontinue their engagement at any time, with minimal financial or procedural friction. This introduces a new and pressing risk for the company: the potential for unpredictable and rapid erosion of recurring revenue (Exhibit 4) if retention strategies are not carefully designed and executed.

CloudDen, VirtuWorld’s flagship SaaS platform for cloud cost visibility and optimization, is already facing the consequences of this new reality. As an inherently subscription-based offering, CloudDen depends not only on winning new customers but also on continuously delivering value to retain them. However, the mechanics of churn management are complex. In contrast to customer acquisition, where ROI is relatively direct and quantifiable, retention investments often face attribution ambiguity. If a customer continues their subscription, is it due to the intervention of the retention team, or would they have stayed anyway? Conversely, if a customer churns despite targeted efforts, was the initiative ineffective or simply mistimed? The difficulty in establishing clear causal links makes it challenging to build a data-driven business case for retention initiatives.

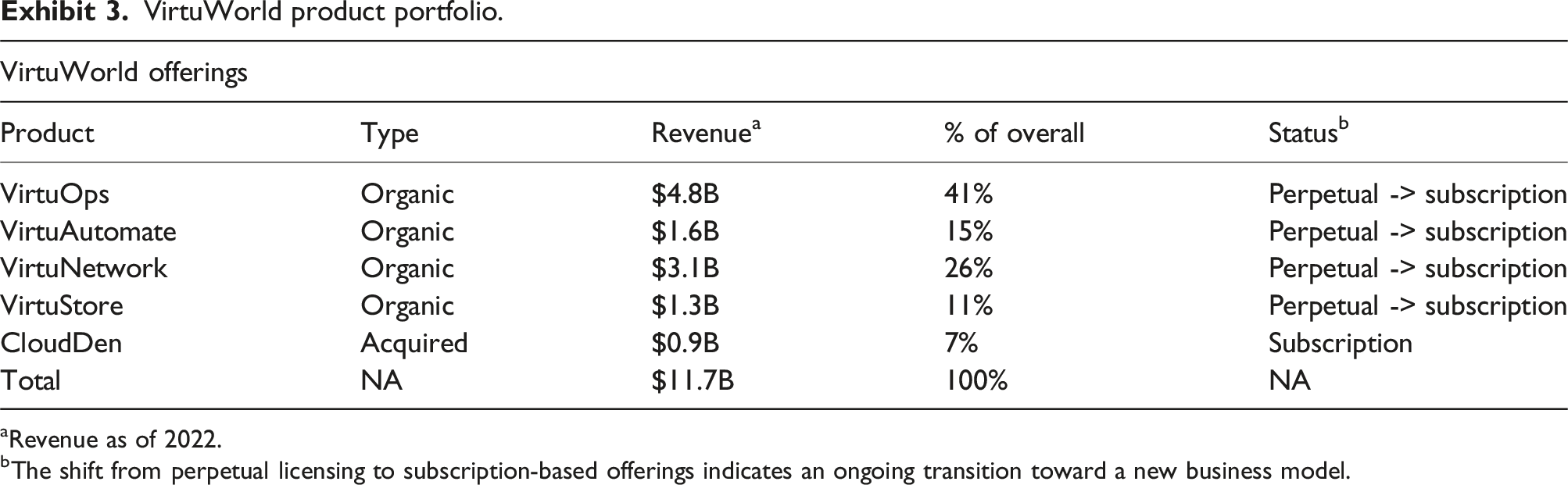

VirtuWorld product portfolio.

aRevenue as of 2022.

bThe shift from perpetual licensing to subscription-based offerings indicates an ongoing transition toward a new business model.

Financial metrics for existing and new customers for a merged entity (VirtuWorld + CloudDen).

aOnboarding cost is specified distinctly from CAC, as even though acquisition cost is zero for existing customers, there will be costs associated with retraining, upselling, etc.

bA net revenue retention rate of 120% indicates that for every $1 of existing revenue, next year brings in $1.20.

As he reflects on the organization’s future, Ajay is reminded of an old proverb: “You can’t sail with a foot in two boats.” The matter keeping him up at night is not whether retention or acquisition matters more, but how to strike the right balance at a time when both feel equally urgent, yet fundamentally different in execution, measurement, and strategic impact. The questions lingering in Ajay’s mind were: (1) Why is the shift of the Business Model from perpetual to subscription critical for VirtuWorld? (2) Why couldn’t VirtuWorld invest organically in building a salesforce that can sell SaaS subscriptions (Instead of M&A with CloudDen)? (3) Which business model (Perpetual vs subscription) is better for the organization? (4) Why VirtuWorld should think deeply in terms of investing in either customer acquisition or customer retention? Why not invest in both? (5) What is the best course of action for me (Ajay) based on the company’s financial data?

Footnotes

Acknowledgments

The author(s) acknowledge the use of OpenAI’s ChatGPT (GPT-4) to assist in rephrasing and refining portions of the manuscript for clarity and academic tone. All substantive content, analysis, and interpretations remain the original work and intellectual contribution of the author(s), based on a modified account of real-life scenarios.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest concerning the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Informed consent

There are no human participants in this article and informed consent is not required.

Data Availability Statement

Data sharing does not apply to this article as no datasets were generated or analyzed during the current study.

Author biographies