Abstract

This case study examines the competitive trajectories of Teradata and Snowflake within the data warehousing sector against the backdrop of a rapidly shifting technological paradigm toward cloud computing. It outlines the strategic challenges and market dynamics that influence the evolution of their business models in an industry undergoing digital transformation. The narrative probes into Teradata’s efforts to pivot from its traditional on-premise stronghold to cloud solutions, juxtaposed with Snowflake’s rise as an innovator in cloud-based data warehousing. The case aims to elucidate the complexities faced by these companies, including market competition, technological upgrades, and regulatory compliance. By dissecting their strategies and operational hurdles, the case provides insights into crafting resilient business models in the data-intensive landscape of today’s economy.

Keywords

Introduction

Data Warehousing, often called DWH, encompasses the various techniques, technologies, and approaches employed to store and administer large datasets for analysis and reporting. As a critical component of business intelligence, DWH allows companies to amalgamate data from diverse sources, offering a comprehensive perspective that facilitates enhanced decision-making processes. It is the backbone for analyzing trends and patterns and making strategic business decisions. 1

The evolution of DWH has been a remarkable journey of technological advancements and adaptations to changing data landscapes. The evolution of DWH has traversed several transformative eras, beginning in the 1960s with the Mainframe Era, where the foundations for data storage and simple query executions were laid despite the limitations of the technology at the time (Poljak et al., 2017). The 1980s marked a significant advancement with the rise of relational database management systems (RDBMS), revolutionizing data storage and retrieval by introducing structured, efficient management of large data volumes, enabling complex queries, and improving data organization (Schmid, 2019).

Entering the early 2000s, the advent of Big Data introduced a range of challenges that stretched the capabilities of traditional Data Warehouses (DWHs) to their limits. On-premises DWHs struggled to keep up with rapidly growing data volumes due to limitations in vertical scalability. Adding more computing power and memory to a single machine proved expensive and inefficient compared to modern distributed systems. DWH’s dependence on batch extract, transform, and load (ETL) processes further hampered the ability to deliver real-time or near-real-time analytics. DWHs were unable to process streaming data quickly enough, introducing substantial latency and outdated insights. DWHs were optimized for structured data and faced difficulties handling the diverse formats of unstructured and semi-structured data, such as images, logs, and social media feeds. Their strict schema requirements required costly and time-consuming transformations, making it impractical to adapt to Big Data’s evolving nature. These challenges highlighted the need for more flexible, scalable, and real-time data processing architectures, necessitating the development of advanced DWH solutions capable of handling complex analytics and the growing data demands (Mehmood and Anees, 2020).

The most recent shift towards cloud computing has further revolutionized DWH by offering unmatched scalability, flexibility, and cost efficiency, making data warehousing more accessible to organizations of all sizes and opening new possibilities in data analytics and business intelligence (Kaur et al., 2012). This journey highlights the continuous innovation and adaptation within the DWH landscape, responding to the evolving data storage and analysis needs. DWH plays a pivotal role in enhancing business operations and strategic decision-making. It serves as a comprehensive data repository, which is crucial for businesses to derive strategic insights, identify trends, and make well-informed decisions. This centralization and integration of data from various sources streamlines business processes, leading to improved operational efficiency (Ghosh et al., 2015). Furthermore, leveraging a DWH can provide a significant competitive advantage to businesses. It enables a deeper understanding of market dynamics and customer preferences, which is essential for staying ahead in the competitive landscape.

Business models

Business models in the realm of data warehousing have evolved to adapt to the changing technological landscape and organizational needs. One traditional approach is the On-Premise Licensing model, where organizations make a one-time purchase of the software and install it on their hardware. While this approach offers complete control over the data warehouse, it comes with a few limitations, such as high initial costs and the need for in-house maintenance and updates. In contrast, the Cloud-Based Subscription Models represent a modern approach. These models are characterized by scalability, lower upfront costs, and outsourced maintenance. They provide better customer support and regular updates, contributing to their growing popularity. This model’s flexibility and cost-effectiveness make it an increasingly preferred choice for many businesses (Pereira, 2023).

Additionally, Managed Services offers a comprehensive solution that includes the software and complete management of the DWH by the service provider. This model is particularly suitable for organizations that lack the necessary in-house expertise. It provides a hassle-free experience, as the service provider handles all aspects of the DWH, allowing the organization to focus on its core activities. Each of these business models offers distinct features and benefits, catering to the diverse requirements of organizations in managing and utilizing their data effectively.

The evolution of Data Warehousing from mainframe systems to sophisticated cloud-based solutions mirrors the growth and complexity of data itself. Today, DWH is not just a storage mechanism but a strategic tool that drives decision-making, operational efficiency, and competitive advantage across various industries. With diverse business models, from traditional on-premise licensing to flexible cloud-based subscriptions and managed services, DWH technologies continue to adapt, offering scalable and efficient solutions to meet the ever-evolving data needs of organizations worldwide.

Macro-environment

The DWH industry, a pivotal segment in data management and analytics, has witnessed a significant transformation in recent years. This industry’s market size and growth trajectory are remarkable, with forecasts indicating a continued upward trend. This growth is primarily fueled by the increasing demand for data-driven decision-making across various business sectors. The worldwide data warehousing market is substantially expanding. Based on multiple research reports (Intelligence, 2024; Linker, 2024), it is projected that the size of the active DWH market will likely reach approximately USD 30 billion by 2029. Throughout the forecast period, from 2024 to 2029, this increase is anticipated to have an average compound annual growth rate (CAGR) of approximately 12%. The core value proposition of DWH solutions revolves around their capacity to facilitate enhanced data integration, storage, and analysis. With the use of these platforms, companies may efficiently conduct thorough analyses by combining data from several sources into one repository. This consolidation aids in generating deeper insights, fostering informed decision-making, and ultimately contributing to improved business outcomes.

The macro-environment of the DWH industry is significantly influenced by factors such as regulatory frameworks and technological advancements. Policies such as the general data protection regulation (GDPR) and the California consumer privacy act (CCPA) significantly affect data security and privacy (Haddara et al., 2023). These regulations mandate stringent data handling practices, compelling DWH providers to incorporate advanced security features and compliance mechanisms. Emerging technologies like artificial intelligence (AI), including machine learning (ML) and Internet of Things (IoT), profoundly impact data analytics demands and DWH capabilities. AI algorithms enhance the analytical power of DWH systems, enabling more sophisticated data processing and interpretation.

IoT devices are prolific data generators, producing a wide range of data types such as status updates, automation logs, location coordinates, equipment metrics, and environmental readings. This data may be structured, semi-structured, or unstructured, and can include formats like video and audio streams. Structured IoT data is often processed using real-time analytics to execute aggregations on high volumes of fast-moving data. The amount of data generated by the IoT is astounding. IoT devices are predicted to generate about 80 zettabytes of data per year by 2025, with some sources estimating a daily production of one billion gigabytes. This may result in billions or even trillions of individual data, depending on the frequency of collecting and the amount of information (IDC, 2021). This necessitates the need for DWH systems that can efficiently process and analyze the massive influx of diverse data types in real time, scale seamlessly to accommodate exponential growth, and support advanced analytics and AI-driven insights to drive timely and informed decision-making across industries. The integration of these technologies has led to the evolution of more advanced, intelligent DWH solutions (Datanami, 2023).

Furthermore, the potential for international expansion, particularly in the EMEA (Europe, the Middle East, and Africa) and APAC (Asia-Pacific) regions, offers a vast playground for growth and diversification. Tailoring solutions to specific industries also presents a lucrative path, as vertical solutions development allows for deeper market penetration through highly specialized offerings. Strategic partnerships further augment this opportunity landscape, enabling companies to broaden their offerings and extend their market reach through collaborations. Conversely, the industry is not without its challenges. Intense competition from both traditional providers and innovative, cloud-native entrants underscores the need for continuous innovation and differentiation. The rapid pace of technological changes threatens to diminish the current advantages of established players, making agility and foresight essential traits for survival. If not adequately managed, these factors can harm a company’s reputation and erode customer trust, impacting its market competitive standing.

Market dynamics

The DWH industry is undergoing significant transformations driven by technological advancements, changing customer needs, and new market entrants. Here is a summarized overview of the key competitive dynamics in this industry. There is a marked transition from traditional on-premise DWH solutions to cloud-based platforms led by companies like Snowflake, Amazon Redshift, and Google BigQuery. This shift is motivated by the benefits of cloud services, such as scalability, flexibility, and cost-effectiveness, which are challenging the position of established players like Teradata and Oracle. DWH solutions increasingly incorporate advanced technologies like AI and IoT to improve data analysis and decision-making. Continuous innovation is key to meeting real-time analytics and large-scale data processing demand (Datanami, 2023). Self-service analytics is becoming more popular, allowing people without technical knowledge to handle and interpret data. Data can be ingested, prepared, and managed using services like Microsoft Azure Synapse Analytics, which provides a uniform interface and meets the urgent demands of AI. Given rising data privacy concerns and breaches, DWH providers focus on robust security features and compliance with regulations like GDPR and CCPA. This emphasis is essential for building customer trust and influencing vendor selection.

The DWH market is witnessing a shift in pricing strategies and business models, moving from traditional licensing to subscription-based or consumption-based pricing. The ability to provide cost-effective yet high-performance solutions is a crucial competitive factor, especially for cloud-native providers. Providers offer customized DWH solutions tailored to specific industries, enhancing the relevance and appeal of their products across various sectors. Cloudera data platform provides customized solutions for different industries, including financial services, manufacturing, and telecom. Forming strategic partnerships and developing a robust ecosystem, including third-party integrations and community support, are crucial for expanding capabilities and market reach. To exploit both supply-side economies of scale and economies of scope, providers are broadening their geographical reach, offering localized solutions that cater to specific regional needs and practices.

Critical success factors

The data warehousing landscape is influenced by several crucial factors determining the industry’s growth and success. At the heart of this evolution lies technological innovation. The integration of cutting-edge technologies such as artificial intelligence (AI), machine learning (ML), and the internet of things (IoT) into data warehousing solutions is revolutionizing analytical capabilities and system performance. This integration enables organizations to extract valuable insights from their data, marking a significant leap forward in how data is utilized for strategic decision-making. Another critical aspect in the data warehousing field is compliance and security. The importance of adhering to regulatory requirements and the need to maintain rigorous data security and privacy protection standards cannot be overstated. Ensuring that data warehousing practices comply with legal mandates and secure sensitive information is indispensable for organizations. This commitment to compliance and security is fundamental to maintaining trust and integrity in data management.

Furthermore, the scalability and flexibility of data warehousing solutions play an essential role. Systems must be capable of handling varying data volumes and adjusting to changing business needs. The ability to scale and flex according to demand is crucial for efficient data management, allowing organizations to easily navigate the complexities of data storage and analysis. The user experience also stands as a pivotal factor. A user-friendly interface is key to enabling effective navigation and utilization of the data warehousing system. Organizations can boost user adoption rates and enhance overall productivity by ensuring ease of use, making the system an integral part of their operational framework.

Customization and integration capabilities further underscore the importance of tailored data warehousing solutions. A unified and effective data strategy must offer customization that aligns with an organization’s specific needs, along with seamless integration with existing business systems and data sources. Lastly, the provision of robust support and maintenance services is critical for the long-term success of data warehousing systems. Access to timely customer support and regular maintenance checks ensures prompt addressing of system issues, minimizing operational disruptions and ensuring the smooth functioning of data warehousing operations. Collectively, these factors underscore the multifaceted approach required for successful data warehousing in today’s business environment, highlighting the dynamic interplay between technology, security, scalability, user experience, and support that drives the industry forward.

Introducing the titans

Teradata

Founded in 1979, Teradata Corporation began as a company focused on developing database management systems. Over the decades, it has evolved into a global leader in the realms of data warehousing and analytics, carving out a niche in big data analytics and data warehousing solutions. Teradata is renowned for its massively parallel processing (MPP) architecture and outstanding data management capabilities, offering a broad spectrum of products and services designed to help businesses harness data for strategic insights (Teradata, 2024a). Teradata’s journey through the years has been a blend of triumphs and challenges. In its dominant era spanning the 1970s to the 2000s, Teradata emerged as the go-to solution for large-scale data warehousing among enterprises and government agencies. However, the 2010s brought significant challenges with the rise of cloud-based data warehousing and heightened competition from rivals like Oracle. This period saw stagnation in Teradata’s revenue and a downturn in its stock price.

In response to these challenges, 2019 marked a period of reinvention for Teradata. The company embraced cloud technology (Teradata, 2019b), forming strategic partnerships with cloud providers such as Amazon Web Services (AWS) (Teradata, 2023b), Microsoft Azure, Google Cloud Platform (GCP) (Teradata-GCP, 2020), and Oracle. They transitioned their flagship Vantage platform to the cloud and introduced innovative hybrid and multi-cloud offerings. This strategic shift began to yield promising results, with a resurgence in revenue growth by 2023. Teradata’s revenue generation comprises software licenses, maintenance subscriptions, and professional services. Software licenses, particularly for their Vantage platform, represent the most significant portion of their revenue. This platform is available for both on-premises and cloud deployments. Maintenance subscriptions provide a steady stream of recurring revenue, ensuring ongoing client support and updates. Additionally, professional services, including implementation, consulting, and training, create supplementary revenue streams for the company (Teradata, 2023a).

Teradata primarily targets large-scale enterprises and specific industries with complex data warehousing and analytics needs. Its product offerings are meticulously designed to cater to these sectors, emphasizing cloud compatibility, advanced analytics, and professional services. The company’s strategic pivot towards cloud-based services and hybrid multi-cloud offerings reflects its adaptation to the evolving market demands and technological advancements (Teradata, 2024b). The company’s offerings include Teradata Vantage, their flagship platform that provides data warehousing, advanced analytics, data lakes, and machine learning capabilities, available in on-premises, cloud, or hybrid configurations. Aster Analytics offers a platform for high-performance analytics and data exploration. Teradata provides Vantage on Azure, Vantage on Google Cloud Platform and IntelliCloud for cloud-based data warehousing solutions. Additionally, Teradata offers a suite of data management tools for data integration, quality, and governance, complementing its core platform (Teradata, 2024a).

Snowflake

Snowflake, established in 2012, starkly contrasts Teradata with its long-standing on-premise legacy. Despite being a newcomer, Snowflake has rapidly ascended the data warehousing arena, challenging conventional market players with its innovative cloud-native architecture and flexible scalability. This ascent, however, has not been devoid of challenges. In its early years (2012–2018), Snowflake quickly captivated the market with its user-friendly, scalable, and cost-efficient approach, marking a significant phase of adoption and growth (Forbes, 2018). The period around its IPO in 2019–2020 was particularly notable. Snowflake’s entry into the public market was met with immense enthusiasm, catapulting its stock price to impressive heights (Bloomberg, 2020). Market volatility soon tempered this initial hype as investors began recalibrating their expectations around the company’s valuation. In the subsequent phase, that is, from 2021 onwards, Snowflake focused on expanding, broadening its customer base, and forging new partnerships. Concurrently, it invested substantially in enhancing its product offerings, introducing advanced features like improved security measures, data lake integration, and machine learning capabilities.

Snowflake’s revenue model is primarily anchored in its pay-as-you-go subscription framework, which is a departure from Teradata’s perpetual license and maintenance approach (Snowflake, 2024). This model allows customers to pay based on their storage and computing resources usage, offering a potentially more cost-effective solution for fluctuating workloads than fixed-capacity models. Additionally, Snowflake supplements its income through professional services, encompassing consulting and training. Targeting cloud-forward businesses and entities that seek contemporary data warehousing solutions for analytics, business intelligence, and data science, Snowflake’s offerings are particularly well-suited for modern enterprises. Its cloud-native structure integrates effortlessly with cloud platforms such as Amazon Web Service (AWS), Azure, and Google Cloud Platform (GCP), rendering it an ideal choice for hybrid and multi-cloud setups. The company’s key offerings include the Snowflake Data Cloud, which forms the backbone of its platform for data storage, processing, and analysis; the Snowflake marketplace, offering an array of third-party data and applications pre-integrated with Snowflake’s system; the Snowflake cloud data exchange, facilitating secure data sharing and collaboration among different (Snowflake, 2024).

Face to face

In the competitive landscape of data warehousing, Teradata and Snowflake stand as prominent players, each with unique strengths and approaches. A head-to-head analysis of these two companies reveals insightful differences and similarities in their offerings and market positions. Teradata is known for its on-premise or hybrid deployments, utilizing MPP architecture that excels in parallel processing, offering high performance for mission-critical workloads (Teradata, 2019a). On the other hand, Snowflake takes a different approach with its cloud-native architecture, emphasizing shared data and elastic computing, making it highly scalable and flexible for modern analytics needs (Dageville et al., 2016).

When it comes to scalability, Snowflake has an edge over Teradata due to its ability to dynamically grow and compute resources on demand, while Teradata often requires predefined hardware upgrades. Elasticity is another area where Snowflake shines, capable of scaling resources up and down within minutes (Microsoft, 2019), whereas Teradata’s elasticity is more limited and confined to virtual partitions. Both platforms are efficient in query performance, but Teradata particularly stands out in handling complex, long-running queries, thanks to its MPP architecture. Teradata and Snowflake offer advanced analytics capabilities, including machine learning and AI, but Snowflake shows better integration with cloud-based data science tools. In terms of security, both prioritize this aspect, yet Snowflake leverages the multi-layered security typical of cloud environments. The user experience is more modern and intuitive in Snowflake, contrasting with Teradata’s complex and IT-oriented interface.

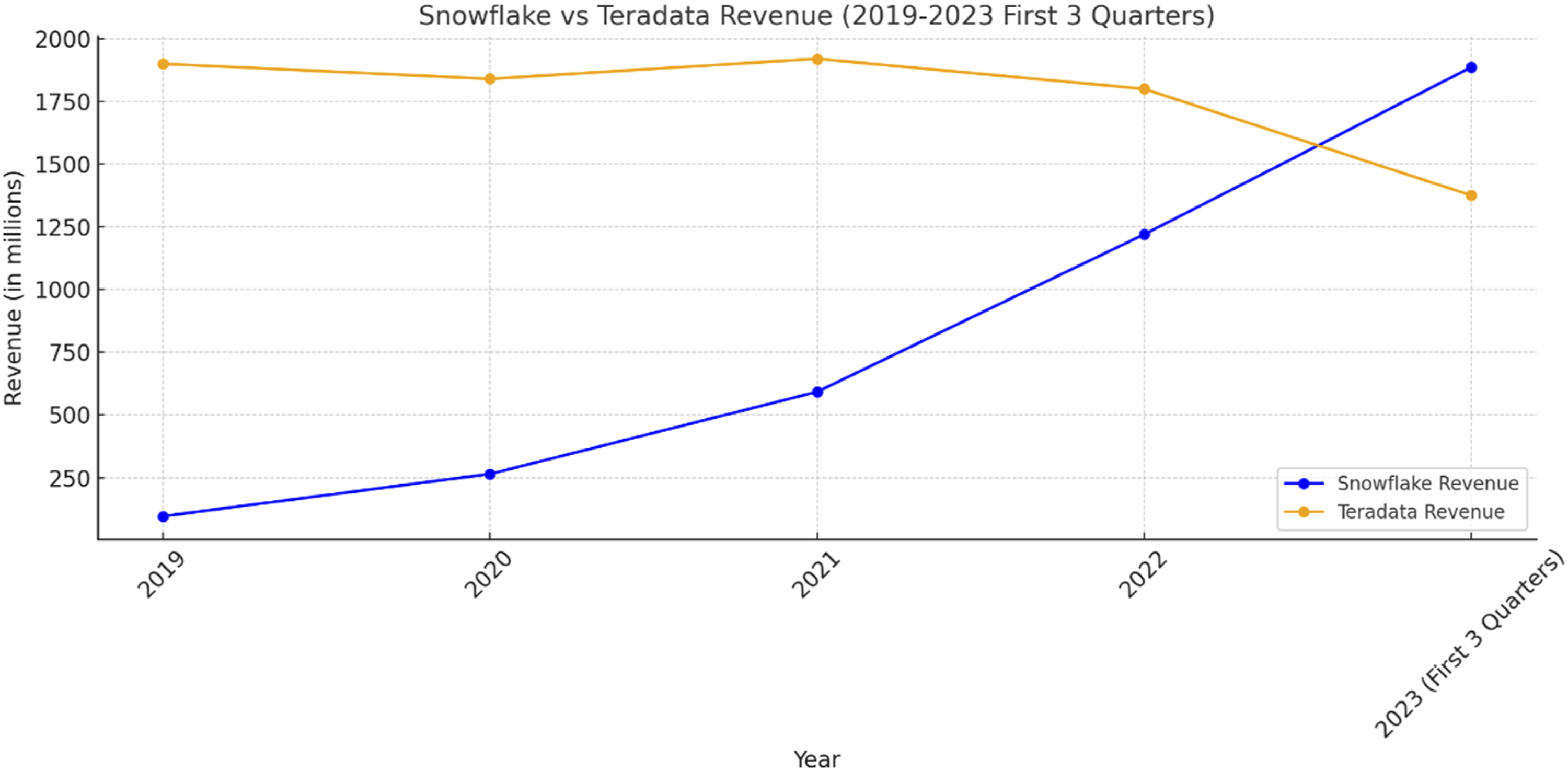

Teradata operates with a model of perpetual licenses and maintenance subscriptions, whereas Snowflake adopts a pay-as-you-go model based on the amount of resources utilized. Snowflake’s elastic nature can lead to optimized resource utilization and potentially lower costs for fluctuating workloads, while Teradata requires more meticulous capacity planning to prevent idle resources. Teradata excels in handling large-scale data enterprises, particularly in regulated industries like finance and healthcare, where mission-critical workloads with high data volumes and complex queries are typical. Snowflake, conversely, is more suited for cloud-first businesses, offering agility and elasticity that cater to modern analytics needs, which is ideal for data exploration, business intelligence, and data science. Historically, Teradata held a dominant market share, but Snowflake is rapidly gaining ground, especially in the cloud data warehousing segment. While Teradata’s revenue remains higher due to large license deals, Snowflake’s revenue growth rate is quickly catching up to Teradata’s. Please refer to Exhibit 1 for revenue growth of Snowflake vs. Teradata from 2019 to 2023. Revenue growth Snowflake vs. Teradata from 2019 to 2023 (in million USD). Source: Authors’ own creation using data from web sources, including Snowflake and Teradata.

Challenges

Challenges for Teradata

Teradata, a company traditionally focused on on-premise solutions, faces a significant challenge in adapting to the growing trend of cloud computing within businesses. Teradata faces a complex web of technical, operational, and perceptual challenges. One significant hurdle is the prevailing uncertainty and risk of migrating from on-premises data warehouses to cloud-based solutions. Customers are often apprehensive about the potential for data loss, downtime, and the technical difficulties inherent in transferring large datasets to the cloud. This perception underscores a broader resistance to change, fueled by concerns over security, costs, and the unknowns of cloud technology. Another critical challenge lies in the technical and developmental hurdles of evolving into a truly cloud-native entity. For instance, efforts to adapt existing solutions for the cloud have often fallen short, primarily because the original architectures were not designed with cloud scalability and flexibility in mind. As a result, these adaptations lacked the genuine hybrid and multi-cloud capabilities necessary to meet diverse customer needs, marking a significant learning curve for companies transitioning to the cloud. This challenge is further compounded by the substantial financial investment required to develop a cloud-native solution from the ground up, necessitating considerable resources, workforce, and time.

One of the most daunting tasks for companies traditionally viewed as providers of on-premises solutions is overcoming legacy perceptions. Changing the narrative and being recognized as a forward-thinking, cloud-capable provider requires technological innovation and a strategic overhaul in marketing, customer engagement, and product development. This shift is crucial for remaining competitive in an industry increasingly defined by agility, scalability, and cloud-first strategies. Furthermore, Teradata encounters competitive pressure from emerging cloud-native companies like Snowflake and industry giants like Amazon Web Services. These competitors pose a substantial threat to Teradata’s established market share. Lastly, navigating the complex terrain of data privacy laws and regulations is an ongoing challenge for companies heavily reliant on data, such as Teradata (Iliashenko et al., 2019). Compliance with these regulations while effectively managing and utilizing data assets is crucial in today’s business environment.

Challenges for snowflake

Despite its rapid growth, Snowflake confronts a notable challenge in effectively managing this expansion without compromising the quality of service and customer support it provides (Soni, 2023). Sustaining high standards while scaling up is imperative in maintaining customer satisfaction. In the ever-evolving landscape of cybersecurity, Snowflake must prioritize robust security measures to safeguard against the increasing threat of cyberattacks. As a cloud-based platform handling valuable data, security remains a top concern. Technical scalability is another hurdle for Snowflake as it strives to meet the escalating demands of its customers and accommodate the growing volumes of data (Vuppalapati et al., 2020). Ensuring the platform performs efficiently and scales seamlessly is essential for its competitiveness. Moreover, Snowflake faces stiff competition from established cloud service providers and emerging data warehousing solutions in the market (Maxville, 2022). Staying competitive and innovative is pivotal for Snowflake’s sustained success in this competitive landscape.

Strategic moves for growth

Teradata

In the competitive saga of cloud-based data warehousing, Teradata’s journey stands as a testament to the challenges and triumphs of a traditional powerhouse seeking to reinvent itself in the face of cloud innovation. This tale began in the early 2010s when cloud computing was burgeoning, heralded by Snowflake’s pioneering cloud offering in 2014. Teradata, a titan in data analytics and warehousing, initially viewed the cloud cautiously, hesitant to pivot from its stronghold in on-premises solutions. The narrative takes a turn in 2016, a pivotal year when Teradata, facing the stark realities of stagnant or declining revenues, embarked on a strategic odyssey into the cloud. This journey was neither simple nor straightforward but marked by a series of calculated moves designed to capture the essence of cloud computing’s potential.

Teradata’s embrace of acquisitions was key to this strategic shift, a move that would bolster its technological arsenal. The acquisition of StackIQ, with its prowess in automating cloud installations, and Stemma, known for its advanced data cataloging, signaled Teradata’s commitment to enhancing its cloud data management and integration capabilities. These acquisitions were not mere expansions but a foundational strengthening of Teradata’s cloud services and solutions. Please refer to Exhibit 2 for Teradata’s Growth Strategies. Partnerships also played a crucial role in Teradata’s cloud odyssey. Collaborations with giants like Amazon Web Services (AWS), Google Cloud Platform (GCP), Microsoft Azure, and Nordcloud were not just alliances; they were bridges connecting Teradata to the vast landscapes of the cloud. These partnerships enabled Teradata to offer a seamless, flexible cloud experience, leveraging the global infrastructure and advanced services of these platforms, thereby expanding Teradata’s reach and versatility in the cloud domain. Teradata growth strategies.

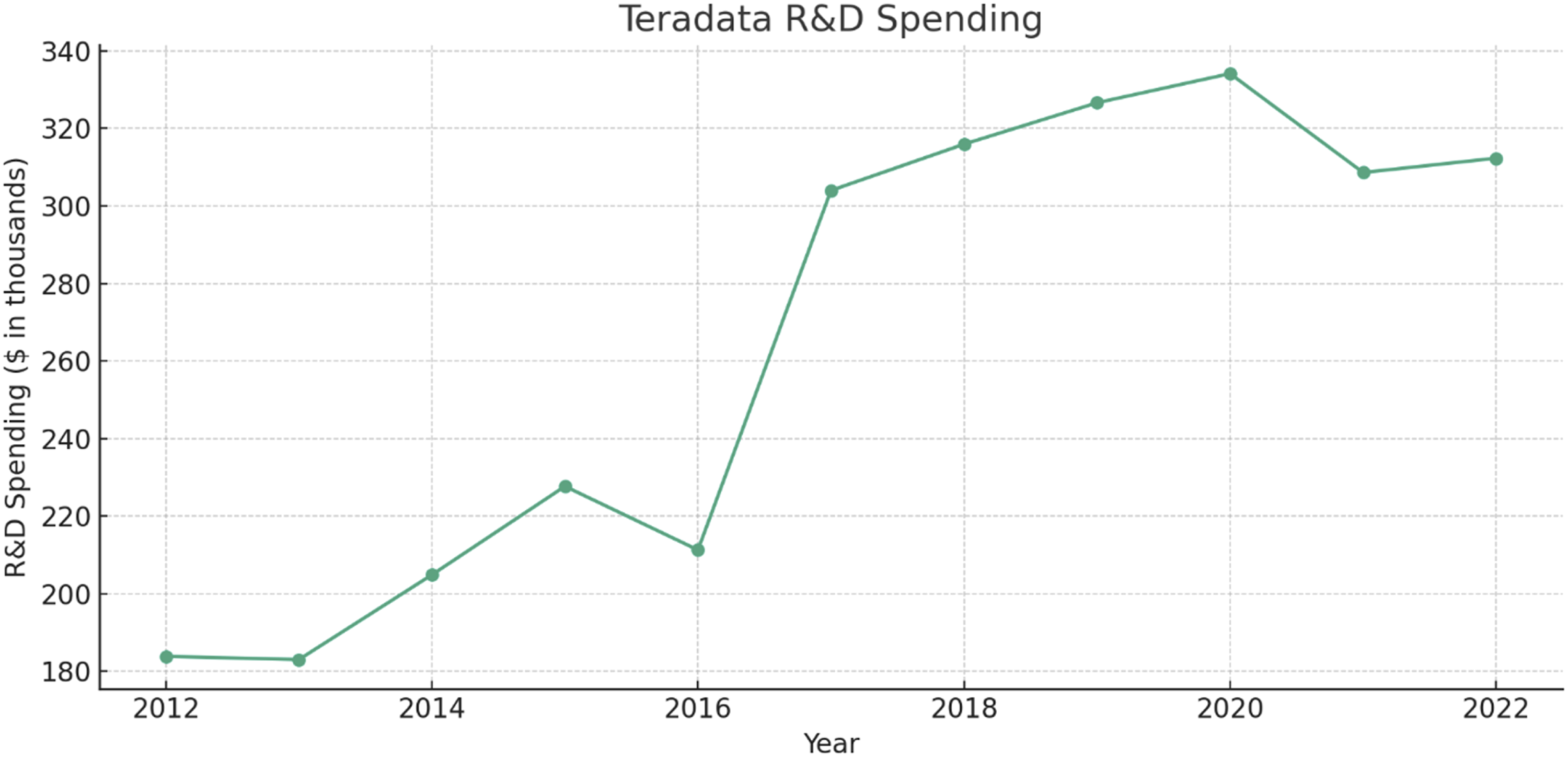

Recognizing that innovation is as much about people as it is about technology, Teradata strongly emphasized talent hiring and retention. This dual approach ensured that Teradata not only preserved its core competencies but also welcomed fresh ideas and expertise essential for navigating the complexities of cloud transformation. Investment in Research and Development (R&D) saw a significant uptick, indicating Teradata’s resolve to lead in cloud analytics, data warehousing solutions, and artificial intelligence (AI) capabilities. Please refer to Exhibit 3 for the Teradata’s R&D spending. This surge in R&D was a declaration of Teradata’s ambition to stay at the forefront of technological advancements and cater to the evolving needs of its customers. Teradata R&D spendings. Source: Authors’ own creation using data from Teradata’s annual reports.

Snowflake

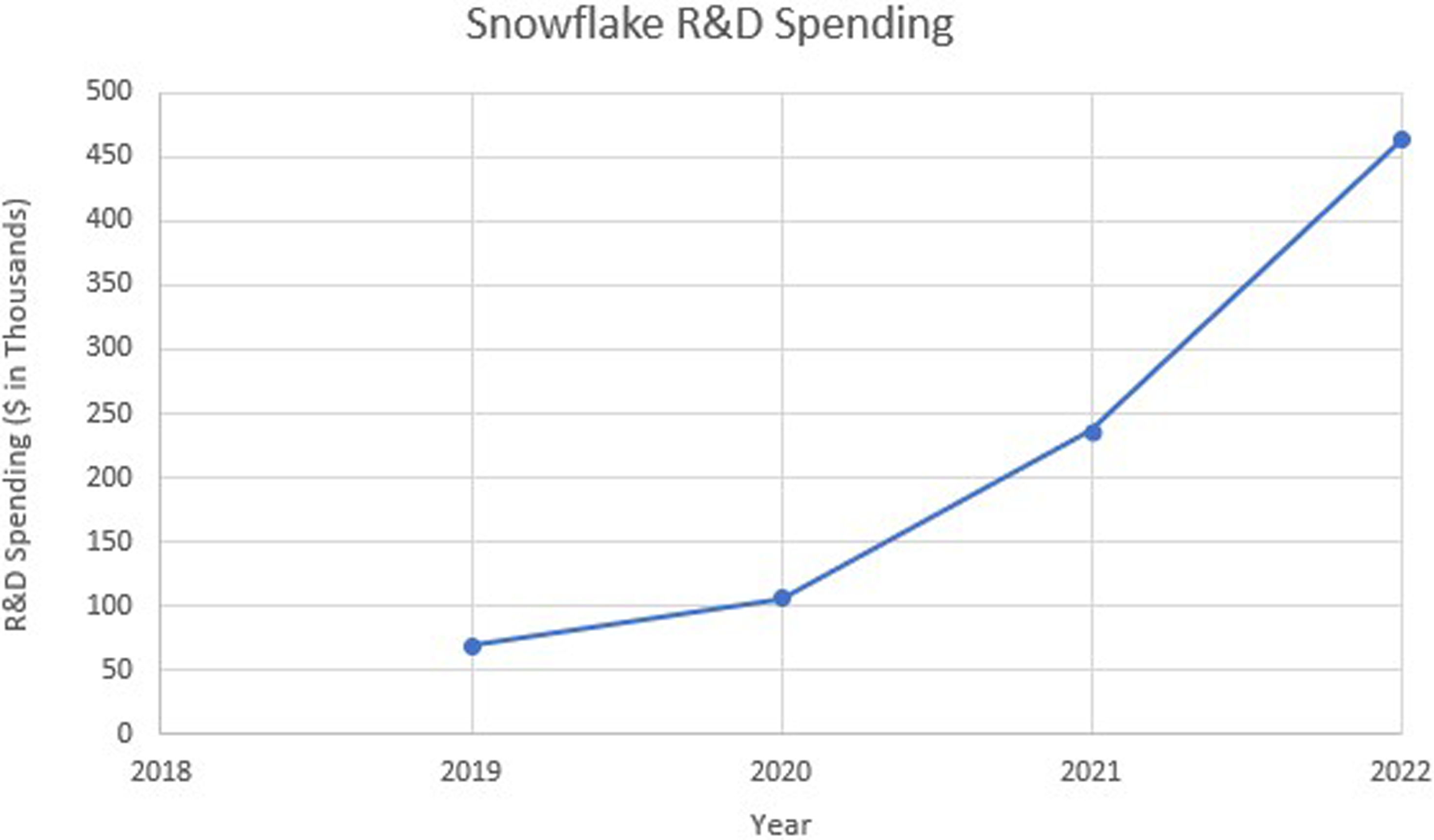

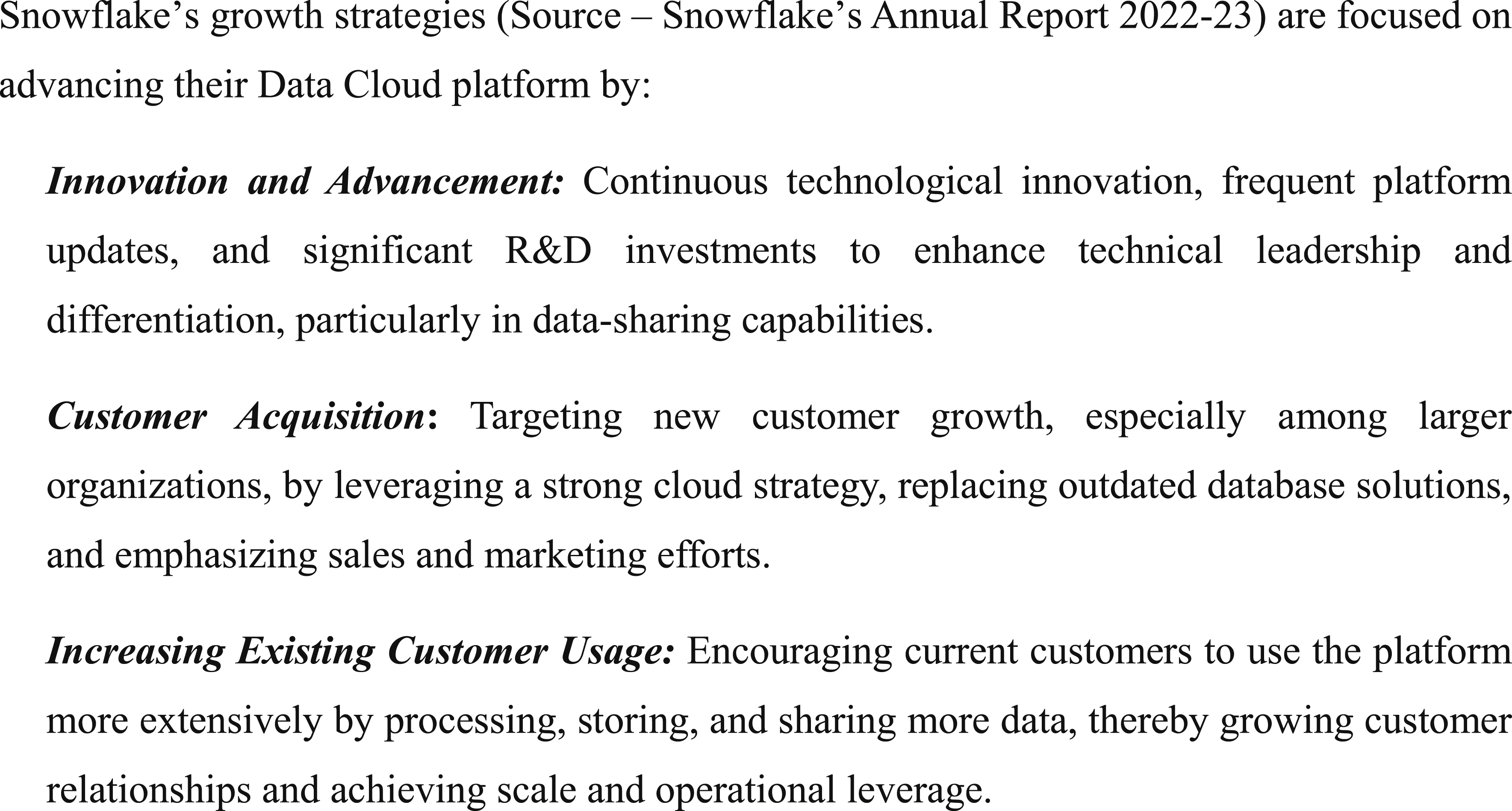

Snowflake’s narrative in the cloud data warehousing landscape is marked by a strategic blend of innovation, global expansion, and ecosystem development. At its core, Snowflake’s commitment to innovation shines through regular feature updates and significant R&D investments, drawing in top technical talent to maintain its edge in cloud-native architecture. Please refer to Exhibit 4 for the Snowflake’s R&D spending. This approach enhances collaboration capabilities and ensures Snowflake stays ahead in technology. Offering a fully managed service, Snowflake removes the complexities of hardware and software maintenance, lowering entry barriers for businesses of all sizes to tap into advanced data analytics. This ease of use makes Snowflake’s platform highly appealing for leveraging cloud-based data solutions. Snowflake focuses on increasing usage among its existing customers to deepen its market penetration. By emphasizing the platform’s benefits and capabilities, supported by targeted sales and marketing, Snowflake aims to boost customer engagement and operational efficiency. Please refer Exhibit 5 for Snowflake’s Growth Strategies. Snowflake R&D spendings. Source: Authors’ own creation using data from Snowflake’s annual reports. Snowflake growth strategies.

Snowflake’s vision extends globally, with strategic efforts to expand its footprint in key regions like EMEA, APJ, and Latin America. This global expansion is fueled by investments across sales, marketing, and customer support, aiming to capture the growing demand for cloud data solutions worldwide. Innovation continues as Snowflake expands data content and fosters collaboration within its ecosystem through initiatives like the Marketplace. This enhances the platform’s value and promotes the data cloud concept, creating a more interconnected community. Lastly, Snowflake is investing in its ecosystem integration, partner network, and community. The Snowflake Partner Network and the “Powered by Snowflake” program are pivotal to this strategy, accelerating platform adoption and enhancing its distribution and platform awareness. Through these multifaceted strategies, Snowflake is not just navigating the cloud data warehousing space but is actively shaping its future, demonstrating a holistic approach to growth and innovation.

The path ahead

In the rapidly evolving data warehousing and analytics landscape, Teradata and Snowflake have carved distinct paths reflecting their strategic priorities and operational challenges. Teradata, a veteran in the industry, is at a critical juncture. Traditionally excelling with on-premises solutions, the shift toward cloud computing has introduced significant challenges, requiring an adaptation of technology and a cultural change within the organization. The company’s late entry into the cloud database market has put it at a competitive disadvantage against cloud-native companies like Snowflake and more prominent players such as Amazon Web Services. On the other hand, Snowflake has leveraged its cloud-native capabilities to race ahead, showing impressive growth as reflected in its revenue trajectory. However, its challenges are typical of a company experiencing rapid growth, including addressing data privacy concerns of larger organizations hesitant to transition to cloud-based solutions. Maintaining service quality, ensuring scalability, and prioritizing cybersecurity are critical to its success. Moreover, Snowflake must differentiate itself in a market crowded with established giants and emerging innovators. Snowflake’s focus on the cloud gives it an edge, but it must continue innovating aggressively to maintain its lead and capture more market share.

The adaptation of AI technologies, including machine learning (ML), is reaching its zenith, with customers increasingly seeking solutions enhanced by artificial intelligence. Companies in the data warehousing and analytics sector cannot afford to overlook these transformative technologies. While Teradata needs to reinvent itself in the cloud era, Snowflake must fortify its current leadership position. For Teradata, the question is not just about technology but about transforming its business model to be more agile and cloud-centric. For Snowflake, the challenge is to manage its explosive growth while sustaining innovation and competitiveness. Here are a few questions to ponder: How can Teradata leverage its resources and capabilities, including the existing customer base and on-premise expertise, to mitigate the threats and carve out new opportunities in the cloud space? What strategic moves can Snowflake make to maintain its growth trajectory and manage the threats posed by industry giants and cybersecurity risks?

Assignment/Case Discussion Questions:

Perform a SWOT analysis to assess the strengths and weaknesses of Teradata and Snowflake and investigate the opportunities and threats arising from external factors.

Investigate emerging technologies and analyze how Teradata has responded to and integrated these significant changes within the data warehousing and analytics sector.

Assess the growth strategies implemented by Teradata and Snowflake, evaluating their effectiveness.

Examine the potential growth avenues and market capture strategies for Teradata and Snowflake.

Footnotes

Declaration of conflicting interests

The authors declare no potential conflicts of interest concerning the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Disclaimer

Like other cases written solely based on secondary sources, this one also has standard disclaimers such as the following: (1) The case cannot be used as a source of information on the company. (2) The information/facts/statements/mentioned in the case have been taken from secondary sources and are not endorsed by the company, its founders, partners, and other stakeholders. (3) The case is not intended to serve as an endorsement of (in) effective handling of the situation(s). (4) The authors acknowledge that the brand names and trademarks used/mentioned in the cases are owned by respective title holders. (5) All errors are the responsibility of the authors. Upon being notified, the authors will undertake all reasonable efforts to rectify the errors.

Target audience

This case is aimed at B-School post-graduate and executive education participants.

Target courses

This case is best suited for courses focused on Technology, Innovation, and Strategy.

Target teaching modules/concepts

Following modules/ concepts can be taught using this case: macro and industry environment analysis; internal environment analysis; business model canvas and business model innovation; and critically evaluating the customer value proposition and the business model changes.