Abstract

This teaching case examines the challenges of platform governance, accountability, and trust in India’s Open Network for Digital Commerce (ONDC). Focusing on RetailSathi, a seller-side startup onboarding small grocery retailers, the case highlights tensions between decentralization and service reliability. It explores how ONDC’s unbundled architecture affects customer experience, especially when responsibilities are fragmented across actors. Through the lens of Unified Theory of Acceptance and Use of Technology 2 (UTAUT2) and Service-Dominant Logic, the case prompts discussion on technology adoption, value co-creation, and the feasibility of open digital ecosystems in replicating the trust mechanisms of traditional e-commerce platforms.

Keywords

Case narrative

Late one evening in Lucknow, Aditi Sharma, founder of RetailSathi, was alerted to a viral complaint on social media. A customer’s grocery order via ONDC had leaked in transit, ruining the contents. The buyer app deflected the issue, ONDC lacked direct support, and RetailSathi was blamed publicly. Though the fault lay with a careless kirana store, Aditi chose to refund the customer immediately to contain reputational damage—an all-too-familiar dilemma in ONDC’s decentralized structure. The next day, during a training session with new kirana prospects, skepticism was evident. Shopkeepers raised concerns about trust, delivery reliability, and how they could compete with fast, established players. One asked bluntly: “If something goes wrong, who fights for us?” Aditi explained ratings, low commissions, and customer proximity advantages, but many remained unconvinced. Digital literacy gaps and fear of returns added to their hesitation. Despite these hurdles, RetailSathi’s order volume in Lucknow grew. A promo campaign with PhonePe sparked a surge in demand, but also exposed weak spots—inventory mismanagement, delayed deliveries, and overwhelmed sellers. Support lines were flooded. The promise of scale was becoming a challenge of coordination. Later, Aditi pitched at an ONDC workshop, sharing a seller success story. But soon after, a potential investor flagged poor service in test orders, questioning RetailSathi’s ability to deliver consistent customer experience on a scale. That night, Aditi and her team debated: should they grow fast or tighten operations first? Ideas ranged from exclusive logistics partnerships and app improvements to vetting sellers and even running a support hotline. But such measures risked turning RetailSathi into a de facto platform—seemingly at odds with ONDC’s open ideals. Torn between rapid expansion and building trust, Aditi drafted two strategies: one prioritizing growth and the other emphasizing quality control and customer assurance. At the heart of her dilemma was a core question: In a decentralized network with no central authority, who ensures the customer is truly cared for?

Introduction

India’s Open Network for Digital Commerce (ONDC) is an open e-commerce network launched by the government in 2021 to unbundle and decentralize digital commerce (Islam et al., 2024). Unlike traditional marketplaces that tightly control seller onboarding, logistics, and customer service end-to-end, ONDC is a protocol-based network where multiple specialized participants (buyer apps, seller apps, payment, and logistics providers) interoperate to fulfill a single order. The goal is to democratize online commerce by lowering entry barriers for small sellers and breaking platform monopolies (Jefferies, 2022). ONDC’s architecture is often likened to UPI for e-commerce—any buyer app can discover products from any seller on the network, much as any UPI payment app works with any bank.

This decentralized, interoperable design is a cornerstone of India’s digital commerce push. It holds promises for millions of kirana (corner grocery) stores and small vendors to go online without depending on a single large platform (Kapoor and Sivadas, 2023). However, it also introduces a user experience dilemma: In a traditional platform like Amazon, a unified entity is accountable for customer satisfaction, whereas in ONDC, the responsibility is fragmented (CUTS Centre for Competition, Investment & Economic Regulation, 2023). If a delivery is delayed or a product is faulty, who is answerable? Early analyses warned of a “lack of clarity on accountability” for customer complaints and returns in the ONDC model. Without a central authority ensuring service quality, there is a risk that poor experiences erode user trust. This paradox of trust in a decentralized marketplace frames the challenge facing Aditi Sharma and her startup, RetailSathi. As ONDC gains momentum, Aditi must decide how to build customer trust when logistics, seller quality, and problem resolution are largely outside her direct control. The stakes are high: ONDC’s success and RetailSathi’s growth hinge on whether a federated network can deliver a reliable experience that earns user confidence.

Company and context background

ONDC, a non-profit initiative incubated by India’s DPIIT, was launched in December 2021 with pilots beginning mid-2022 across five cities (Jefferies, 2022). Instead of functioning as a single platform, ONDC connects buyer and seller applications via an open protocol. This architecture unbundles digital commerce into distinct services—discovery, ordering, fulfillment, and payments—handled by different entities (CUTS Centre for Competition, Investment & Economic Regulation, 2023). While ONDC maintains the registry and protocol, it does not oversee individual transactions.

This model holds special promise for India’s 12.7 million kirana stores, which contribute nearly 90% of grocery retail sales but remain largely offline. Digital penetration in the grocery sector is still negligible (around 0.2% of a $400 billion market). Most kirana owners operate with manual methods, and digital adoption has been limited—only about 15,000 stores had joined aggregator platforms by 2021. Barriers include not just costs and infrastructure, but also behavioral inertia and mistrust of online systems. ONDC seeks to address this by offering small retailers a low-cost, interoperable alternative to large platforms, free from high commissions or restrictive contracts (Modi and Gupta, 2022). By July 2024, it had onboarded over 630,000 sellers and service providers across 600+ cities, handling 12 million orders monthly, 1.4 million of which were groceries (Online Bureau, 2024).

Lucknow, a Tier-2 city with nearly 3 million residents, exemplifies ONDC’s target market. While online retail adoption is rising in such cities, quick-commerce players have limited presence here, creating room for local solutions. Founded in 2023, RetailSathi helps local grocers digitize inventory and join the ONDC network. The startup offers a seller app, onboarding support, and integration with ONDC’s logistics and buyer apps.

Aditi Sharma, who left a job in Bengaluru to launch the venture in her hometown, was inspired by ONDC’s mission. Starting with 20 stores in Aliganj, RetailSathi expanded to over 200 grocers in Lucknow and Kanpur by mid-2024. Operating on a low-fee, asset-light model, it connects stores to buyer apps like Paytm and Pincode. National-level ONDC promotions further boosted visibility for local sellers (Bain & Company and Flipkart, 2025).

Still, the model depends heavily on trust. While ONDC expands reach, RetailSathi must ensure the overall experience, delivery, packaging, and accuracy meet customer expectations. In a decentralized system with distributed responsibility, maintaining this trust remains its biggest challenge.

Key challenges

RetailSathi operates within ONDC’s decentralized model, where order fulfillment involves multiple independent actors—buyer apps, seller apps, kirana stores, and logistics providers. While the startup manages seller onboarding and order processing, it lacks control over warehousing, packaging, and delivery. This fragmentation creates a central tension: how can a brand build trust and scale when it cannot guarantee consistent service? • Service quality control: RetailSathi cannot enforce uniform service standards across the small retailers it onboards. Issues like poor packaging, outdated stock listings, and inconsistent store hours are common. Unlike centralized platforms that penalize underperforming sellers, RetailSathi can only train and encourage compliance, often with limited results. • Logistics and delivery: Approximately 70% of RetailSathi’s deliveries in Lucknow are handled by FastKart, an ONDC-integrated courier. But without contractual control, delivery lapses such as no-shows during bad weather go unresolved. Customers blame RetailSathi or ONDC, even though neither directly manages the drivers. • Customer support and grievance redressal: ONDC’s policy designates the buyer app as the first point of contact for complaints. However, these apps often lack visibility into fulfillment status. In one case, a package disappeared in transit, with no party accepting responsibility. The incident required formal mediation and highlighted how ONDC’s distributed accountability leads to delayed, opaque resolution processes. • Reputation and ratings: While ONDC offers network-wide ratings and badges, accountability remains diffused. A poor review could result from any actor in the chain. RetailSathi’s reputation is shaped by others’ actions; errors by shops or couriers reflect poorly on the brand. As Aditi notes, trust is “co-created” but also “co-destroyed.”

RetailSathi must scale rapidly to be viable, but doing so without control over quality risks erodes customer trust. This dilemma reflects a broader issue within ONDC: distributed models diffuse responsibility, making accountability fragile. As one user put it, “ONDC has shifted the responsibilities of Swiggy/Zomato’s customer care onto the customer.” Unless startups like RetailSathi can solve for consistency, users may retreat to closed platforms despite higher costs.

Analysis and discussion

Aditi’s situation with RetailSathi offers rich ground to analyze platform governance, technology adoption, and service co-creation in the context of ONDC’s decentralized marketplace. Several frameworks and theories can shed light on the case’s key dynamics.

Platform governance and accountability diffusion

Traditional e-commerce platforms like Amazon or Flipkart exercise centralized governance: they set the rules for all sellers, manage logistics (or tightly integrate with logistics partners), and provide unified customer service. They can enforce accountability by penalizing or removing sellers/drivers who don’t meet standards, thereby maintaining consumer trust in the platform brand. In ONDC’s networked governance model, such top-down control is absent—no single entity oversees end-to-end execution. ONDC provides protocols and policies, but it’s essentially a facilitator, not an enforcer (Consumer Unity & Trust Society Centre for CompetitionInvestment & Economic Regulation, 2023). This leads to what we observe as accountability diffusion. Responsibilities are spread across multiple actors, each governed by separate contracts and incentives.

In RetailSathi’s case, the buyer app is responsible for front-end customer interaction, the seller app (RetailSathi) manages seller onboarding and order processing, the kirana seller manages fulfillment, and the logistics provider handles delivery. Each has its own governance: RetailSathi can at best deliver a consistently poor seller or stop offering a problematic courier, but it cannot directly train a courier’s employee or dictate a seller’s in-store processes unless it creates its own supplemental rules.

Platform governance frameworks often highlight mechanisms like rules (policies and terms of service), monitoring (ratings and data analytics), and sanctions (suspensions and fines) to ensure compliance and quality. ONDC’s approach is to embed some of these mechanisms in the network protocols, for example, a rating and reputation system visible to all network participants, or an Issue and Grievance Management (IGM) system that is supposed to route complaints to the right party and escalate if not resolved. However, as the case illustrates, these mechanisms are still maturing and can be slow. Enforcement is tricky without a single empowered authority. If a shop repeatedly fails, ONDC relies on RetailSathi (the seller platform) to discipline them; if a logistics partner has high failures, multiple seller apps might collectively stop using them, but there’s no immediate “network ban” unless perhaps ONDC’s central registry steps in after extreme cases.

This absence of a clear governance hierarchy means trust must be achieved through transparency and alignment of incentives, rather than command-and-control. RetailSathi could push for a code of conduct with its sellers as a form of self-regulation – and similarly sign MoUs with delivery partners on expected service levels. Essentially, RetailSathi might create a governance layer atop ONDC for its sub-network of stores. The risk is that this starts to resemble a closed platform if taken too far. Yet, some boundaries might be necessary. For instance, ONDC as a whole might introduce certifications or badging (gold-tier sellers and verified logistics) to signal reliability. Already, network policies talk about publishing performance metrics and possibly taking disciplinary action for unresolved issues. The question is who will enforce compliance—ONDC as a governing body, or the community of participants via market forces?

A real example to compare is how Uber and Airbnb (while companies, not protocols) had to evolve governance measures (like two-way ratings, guarantees, and safety checks) when trust issues threatened their platform. ONDC, by design, lacks the corporate owner to do this, so governance might need to be polycentric, shared among participants or delegated to neutral third parties for dispute resolution. If Aditi pushes for something like an insurance fund or guarantee program for orders (like an “ONDC Buyer Protection”), that might require collective funding or government support, but it could greatly bolster trust. Platform governance theory would suggest that credibly assigning liability in multi-party transactions is crucial for trust. Right now, RetailSathi is discovering that in ONDC, “everyone’s responsible” can feel like “no one is responsible” to the consumer. Effective governance may require rebidding some functions, for example, a unified customer service that handles multi-actor issues in one window, even if behind the scenes it delegates to the culprit.

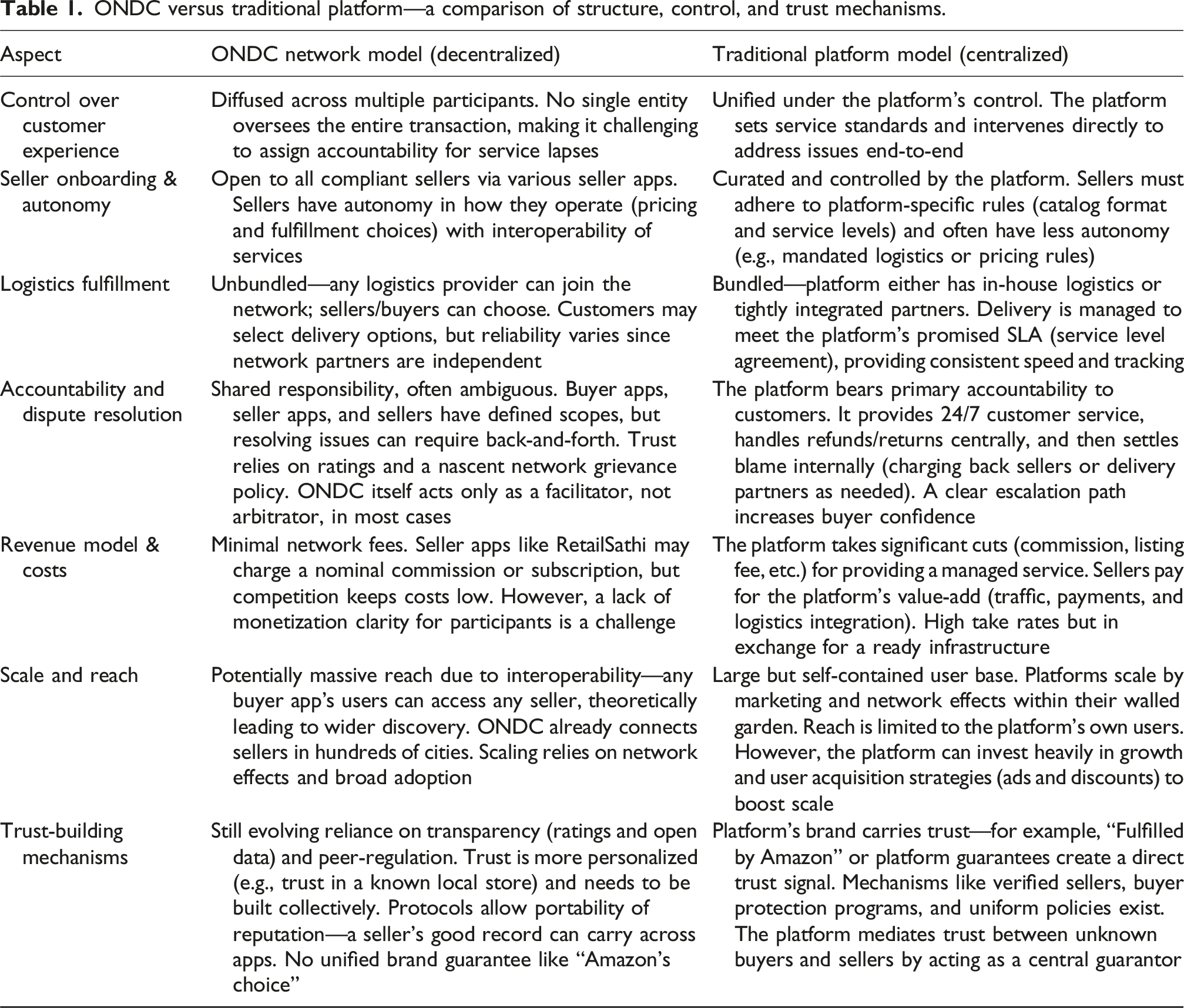

ONDC versus traditional platform—a comparison of structure, control, and trust mechanisms.

For RetailSathi, these differences mean that strategies that work within a closed platform may not directly apply. The case forces us to examine whether decentralization inherently comes at the cost of user trust, or if new governance innovations can compensate for the loss of central authority.

Frameworks for analysis: Technology adoption and value Co-creation

Adoption resistance through the lens of UTAUT2

The narrative of Kirana owners hesitating or struggling to adopt digital commerce is well explained by the Unified Theory of Acceptance and Use of Technology 2 (UTAUT2), an extension of a leading IT adoption model (Bhattacharjee et al., 2024). UTAUT2 identifies several factors influencing technology adoption, many of which we can map to the kirana context. • Performance expectancy: Many kirana owners doubt that using RetailSathi will lead to meaningful business gains. The case shows skepticism about attracting new customers or increasing revenue. Given their thin margins, clear benefits must be shown. Success stories like Meera’s can help build belief in the platform’s value. • Effort expectancy: Digital unfamiliarity makes even simple apps seem difficult. Mr Tiwari’s discomfort using the interface highlights this gap. Despite RetailSathi’s localized design and support, onboarding remains a hurdle. Reducing perceived effort through WhatsApp integration or managed services can ease adoption. • Social influence: Peer feedback and community perception shape adoption. Negative anecdotes and wait-and-watch attitudes deter us, while visible early adopters (like Priya) can motivate others. RetailSathi should encourage community sharing and leverage local social networks to build momentum. • Facilitating conditions: Adoption depends on device access, connectivity, and support. While RetailSathi offers training and a helpline, broader infrastructure gaps persist. Enhancing technical support, including call centers or vernacular assistance, can strengthen enabling conditions. • Hedonic motivation: Enjoyment plays a minor role in this context. Most kirana owners see the platform as functional, not fun. However, gamified features (like achievement badges) might appeal to younger owners and help sustain engagement. • Price value: Low transaction costs support a favorable cost-benefit perception. However, hidden costs like handling returns or complaints can deter adoption. RetailSathi must ensure that financial value remains positive, possibly by absorbing initial losses to reduce seller risk. • Habit: Offline routines dominate kirana operations. Shifting online workflows (e.g., checking orders regularly) is difficult. Missed orders reflect a lack of habit rather than intent. Scheduled reminders and ongoing handholding can help embed new behaviors over time.

Applying UTAUT2 to RetailSathi reveals that trust, though not explicitly listed in the model, is central to several key adoption factors: trust in the technology, the network, and one’s own digital ability. The trust gap seen in kirana digitalization aligns with low performance expectancy and high perceived risk. Overcoming this gap, especially in the early adoption phase, is crucial and can hinge on a few seamless user experiences. External events like demonetization, COVID-19, and now ONDC’s government backing have shaped facilitating conditions and social influence, making digital commerce more acceptable (Kapoor and Sivadas, 2023). Aditi must leverage this momentum while systematically tackling concerns around usefulness, usability, social proof, and habit-building. In short, UTAUT2 shows that adoption isn’t just about tech, it’s about shifting deep-rooted behaviors and beliefs in a tightly knit retail ecosystem.

Service-dominant logic and co-creation of value

The ONDC model and RetailSathi’s role can be examined through the lens of Service-Dominant (S-D) Logic, a perspective from marketing which posits that value is co-created by multiple actors rather than produced by a single entity and delivered one-way. S-D logic emphasizes that all economic exchange is fundamentally an exchange of service—the product is merely a vehicle for service. One of its foundational principles is that value is always co-created by the provider and the consumer (and often other stakeholders), rather than embedded in a product independently (Vargo and Lusch, 2004).

In this case, the “service” in question is the delivery of groceries to a customer, a service experience that involves RetailSathi, the kirana store, the logistics driver, the buyer’s app interface, and the customer themselves. Let’s deconstruct the value co-creation in Aditi’s scenario. • Resource integration by actors: Value creation relies on each actor integrating their resources: kirana stores offer inventory and product knowledge, RetailSathi provides digital infrastructure and onboarding, logistics partners handle delivery, and buyer apps manage interface and transactions. Customers also contribute by providing information, placing orders, and offering feedback—making them active co-creators, not passive recipients. • Co-creation vs. co-destruction: Effective coordination across actors leads to successful value co-creation. However, failure by anyone—such as poor packaging or delivery errors—can result in value co-destruction. As S-D Logic highlights, value is subjective and determined by the customer; a negative experience erases collective effort, regardless of intent. • Service ecosystem and institutional arrangements: RetailSathi functions within a service ecosystem requiring coordination among actors. Trust is an emergent property of this system. Each delivery either builds or erodes trust in the network. Institutional support—such as training, rules, and guarantees—can strengthen the system. For instance, a RetailSathi Guarantee can enforce service norms and manage risk across the network. • Value proposition vs. value actualization: While RetailSathi promises reliable local delivery, actual value depends on execution. The gap between proposal and realization is visible when investor test orders fail. Analyzing resource integration breakdowns—such as weak logistics or seller disengagement—can guide system redesign. Investments like free packaging or backup drivers can close these gaps and enhance co-creation capacity. • Customer’s role and co-creation burden: Customers co-create value, but too much involvement (e.g., chasing drivers) can diminish satisfaction. While early ONDC users often accepted these frictions, widespread adoption demands minimal co-creation effort from customers. Solutions include stronger back-end support or a customer-facing helpline to absorb issues. • RetailSathi as resource orchestrator: RetailSathi must go beyond being a platform and act as a network integrator. This involves syncing operations with logistics partners, gathering customer feedback, and supporting sellers with tools and training. It serves both the kirana (enabling digital access) and the customer (ensuring quality service). Aligning with S-D logic, it must propose value and work with the ecosystem to realize it. • Collaborative innovation: Dialog and collaboration across the network are central to value co-creation. RetailSathi’s team discussions and seller engagement are examples of this. Co-designed solutions, like standard packaging ideas from sellers, are more likely to succeed. Shared ownership drives better execution and consistency.

ONDC reflects a service-dominant ecosystem, where all actors contribute to value creation and share risk. RetailSathi’s effectiveness depends on how well it can coordinate and align these actors. Embedding a mindset of shared responsibility for customer experience is key to sustaining value creation across the network.

Conclusion

RetailSathi’s story captures both the promise and the complexity of ONDC’s decentralized model. ONDC aims to level the playing field by opening e-commerce to small retailers, and Aditi’s venture shows how powerful that vision can be, bringing hundreds of kirana stores online in a short time. Unbundled architecture allows flexibility and innovation, but it also blurs accountability.

This openness comes with trade-offs. Without a central player to enforce standards, trust can fray when customers face inconsistent service. Aditi’s dilemma reflects a deeper tension: should RetailSathi remain a lean tech enabler, or take on more responsibility to protect its brand? Either choice has risks.

As ONDC evolves, success will depend on new forms of governance, stronger collaboration across players, and cultural shifts in how trust is built. The case raises a vital question for the future of digital commerce: can an open network deliver reliability without central control? How ventures like RetailSathi answer that will shape what comes next—for themselves and for ONDC.

Teaching questions

1. When an order goes wrong with ONDC, who should be held accountable? In the absence of a central platform, how can accountability be made clear and enforceable? 2. Should Aditi focus on expanding RetailSathi to new cities or strengthen operations and trust in Lucknow first? What trade-offs do each option involve? 3. How is ONDC’s governance different from that of traditional platforms like Amazon? Can a decentralized system work without a central authority? 4. What stops kirana store owners from adopting ONDC? How do UTAUT2 factors like effort expectancy, social influence, or habit shape their decision? 5. How is value co-created among customers, kiranas, and platform partners in the ONDC grocery journey? What happens when this collaboration breaks down? 6. In an open network like ONDC, is it fair to expect customers to solve more of their own problems? What kind of support systems or policies is needed to protect them? 7. Can ONDC build public trust the way UPI did? Will open networks become the future of e-commerce, or will users stick with established platforms?

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.