Abstract

This study examines the time-varying Granger causality relationship between geopolitical risks and economic policy uncertainties with energy and food prices using the time-varying Granger causality procedure proposed. The global geopolitical risk index (GPR) and the global economic policy uncertainty index (GEPU) were associated with the FAO food price index (FFPI) and global energy price index (GEPI) variables representing the basket prices of traded agricultural and energy commodities. According to the findings obtained with the recursive evolution procedure, no evidence was found for the existence of time-varying Granger causality between GPR-GEPI and GPR-FFPI. The findings obtained from the recursive evolving procedure, which is a current approach, differ from the findings of previous studies based on the rolling window method. The study presents evidence of causal relationships between GEPU, FFPI, and GPI. However, these causalities are valid for short time intervals. In addition, as a result of the causality test conducted for the relationship between GEPI and FFPI, evidence in favor of time-varying bi-directional causality between the variables is determined. The results suggest that global geopolitical risks are not a precursor to fluctuations in food and energy commodity prices. In this respect, it is argued that food and energy commodities can be safe instruments for investors in periods of geopolitical risk. There is evidence that economic policy uncertainties Granger-cause food and energy prices in some limited periods. To protect investors during periods of global economic policy uncertainty and prevent pass-through to domestic inflation, uncertainty-resistant long-term trade agreements, agricultural production support, tax advantages in international trade, and more investment in renewable energy alternatives that reduce foreign dependency are recommended.

Plain Language Summary

This study examines the time-varying causality relationship between geopolitical risks and economic policy uncertainties with energy and food prices. The global geopolitical risk index (GPR) and the global economic policy uncertainty index (GEPU) were associated with the FAO food price index (FFPI) and global energy price index (GEPI) variables representing the basket prices of traded agricultural and energy commodities. According to the findings, no causality in any direction was determined between GPR and FFPI during the period examined. The causality between GPR and GPI can be confirmed bi-directionally only with the findings obtained from the rolling window approach in certain months of 2008. The recursive evolving procedure does not provide evidence for the causality between GEPI and GPR. The findings obtained from the recursive evolving procedure, which is a current approach, differ from the findings of previous studies based on the rolling window method. The study presents evidence of causal relationships between GEPU, FFPI, and GPI. However, these causalities are valid for short time intervals. In addition, as a result of the causality test conducted for the relationship between GEPI and FFPI, evidence in favor of time-varying bi-directional causality between the variables is determined. The results of the study allow the inference that fear, and panic caused by geopolitical risks are not important in terms of commodity prices at the global level and that agricultural commodities, in particular, can provide investors with protected alternatives during geopolitical risk periods

Introduction

The world’s economy has been becoming increasingly integrated through global trade and financial flows (Trung, 2019). While this creates effects in each of the dimensions of globalization, it also increases the complexity of the network of relationships that are analyzed in a single dimension by the concept of economic globalization. Thus, globalization arises as a high degree of integration in the behavior of economic units and in the pattern among the economic variables. Increased integration level improves the living standards of people and societies absolutely and relatively through channels such as greater trade flexibility, flow of goods and services, physical and human capital transfer, foreign investment, and technology transfer (Coulibaly et al., 2018). However, the process does not always operate in the form of positive externalities. Increasing level of integration also increases the transitivity of risks and uncertainties across economic variables and countries (R. Li et al., 2024). Since the early 1990s, the economic effects of geopolitical risks and political uncertainties that emerged during the period of high integration, which is called hyperglobalization (Subramanian & Kessler, 2013), and their transitivity across economic agents and variables have become more debated. This period includes many political fluctuations such as the Gulf War, the Bosnian War, the September 11 attacks, the Iraq War, the Arab Spring, the Russo-Ukrainian tension and war, and the Iran-US tensions. These fluctuations are referred to as geopolitical risks. Geopolitical risk (GPR) is defined as the threat, realization, and escalation of events such as wars and tensions between political actors and terrorist activities (Caldara & Iacoviello, 2022). Another dimension of uncertainty comprises economic policy uncertainty (EPU) which refers to the cases with the absence of defined government policies and regulatory frameworks (Al-Thaqeb & Algharabali, 2019; Hoang et al., 2023) for the near future. The Russian crisis (LTCM), the 2000 US elections, the global financial crisis, the Eurozone crisis, the Brexit process, the 2016 US elections, China-US trade tensions, and the Covid-19 pandemic are some of the periods of heightened economic policy uncertainty in the last 30 years. It has also been confirmed that geopolitical risks cause economic policy uncertainty in various periods due to the damages (Chortane & Pandey, 2022; Umar et al., 2022) they can cause to economic and financial systems (Shen & Hong, 2023).

Geopolitical risks and economic policy uncertainty are multidimensional indicators affecting many economic variables and the link between the variables. The effects of geopolitical risks and political uncertainties on the primary sectors of the economy such as tourism (Shahzad et al., 2022), transportation (Drobetz et al., 2021; Kotcharin & Maneenop, 2020), industry (Y. Li & Bai, 2023), agriculture (I. Abid et al., 2023), mining (Rumokoy et al., 2023), and finance (Demir & Danisman, 2021; Z. Wang et al., 2023) have been confirmed. Accordingly, the possible effects of risks and uncertainties on each economic variable have emerged as research hypotheses. The relationship between geopolitical risks and uncertainties and key economic variables such as inflation (Athari et al., 2022; Bouri et al., 2023), unemployment (Caggiano et al., 2017; Yalçinkaya & Daştan, 2020), exchange rates (A. Abid, 2020; Iyke et al., 2022), interest rates (Ashraf & Shen, 2019), and economic growth (Bannigidadmath et al., 2024; Jha et al., 2024) has been confirmed by many studies. However, the main interest is on the direct and indirect effects of geopolitical risk and economic policy uncertainty on commodity markets and prices. Commodities have the quality to be both inputs in production processes and final consumer goods. In this respect, the supply-demand balance in commodity markets and commodity prices are important for sectors and consumers. Moreover, commodity supply-demand and commodity prices can be considered as input variables for many other economic variables. Therefore, analyzing the effects of risks and uncertainties on commodity markets allows for inferences about the transmission ways of risks and uncertainties to many other economic variables. Moreover, given the fact that some commodities are natural resources, or their production is concentrated in certain regions, the effects of geopolitical risks on commodity markets are of particular interest. For example, the outbreak of war in 2022 between Russia and Ukraine, which is one of the world’s major wheat producers, posed significant threats to the wheat trade. The price of wheat, which is an agricultural commodity, increased by about 35.5% in 2022 compared to 2021. Similarly, natural gas supply fluctuations, such as the cut-off of natural gas flow to European countries by Russia during the war, caused natural gas prices to increase by approximately 105% in 2022 compared to the previous year (IMF, 2024). The impact of economic policy uncertainty on commodity prices is also shaped by the extent to which commodities are regarded as alternative investment instruments. Investors are expected to optimize their portfolios and adopt diversified investment strategies during periods of economic policy uncertainty (Du & Zhang, 2024). Thus, commodities, both goods and financial assets, are positioned between the real economy and financial markets and are expected to be affected by economic policy uncertainties (Hou et al., 2020; Xiao et al., 2022).

The relationship between geopolitical risks, economic policy uncertainties, and commodity prices functions through several different mechanisms, both direct and indirect. The transmission from risks and uncertainties to commodity prices functions through channels such as the effect of deterioration in confidence on prices, supply-demand fluctuations, financial channels and volatility transmissions across markets (L. Wang et al., 2021; X. Wang et al., 2023). Increased economic policy uncertainty leads to fluctuations in commodity markets through decreased production motivation and increased demand uncertainty (Song et al., 2022). Moreover, financialized commodities are influenced by policy uncertainties through financial channels as alternatives (Zhu et al., 2020) that investors use to avoid risks through portfolio diversification against political uncertainties. One of the reasons for changes in commodity prices during periods of economic uncertainty is trade fluctuations caused by political uncertainties (Wen et al., 2021). Geopolitical risks may have direct effects on commodity prices, such as supply-demand, investor behavior, and supply chain, as well as indirect effects through political uncertainties. Geopolitical risks have impacts on commodity supply and supply security, particularly in the energy sector (Mo et al., 2024; Zhang et al., 2024). Moreover, geopolitical risks affect expected returns and cash flows and constitute one of the components of the demand channel in commodity market transitivity (L. Wang et al., 2021).

This study aims to investigate the effects of geopolitical risks and economic policy uncertainties on energy prices, which is a basket price of energy commodities, and food prices (FAO, 2024), which is a measure of the basket price of traded agricultural commodities. The effects of agricultural and energy commodities on the economy are multi-dimensional. Agricultural and energy commodities provide alternatives for investor portfolios as components of commodity funds. They can also be used as raw materials and intermediate goods in production processes. Moreover, energy commodities are directly used to meet households’ basic needs, such as heating and transportation, while agricultural commodities are directly used to meet households’ nutritional needs. Thus, agricultural and energy commodities can be simultaneously labeled as investment instruments, raw materials-intermediate goods, and consumer products. This expands the economic span of supply-demand and price fluctuations in these commodity markets. This multidimensionality of agricultural and energy commodities strengthens the motivation for this study on the relationship between geopolitical risk and economic policy uncertainties.

Furthermore, the transitivity of possible fluctuations in these commodity markets due to geopolitical risks and uncertainties or other factors can also be mentioned. It is known that commodity prices have the potential to affect each other through many different channels. The relationship between energy prices and agricultural prices is said to work directly through the bio-fuels channel and indirectly through the input channel (Ciaian & Kancs, 2011). In fact, this situation can also be explained as a supply-and-demand-driven situation. Energy is one of the important inputs of agricultural production. Therefore, agricultural product prices are exposed to supply shocks stemming from increasing energy prices (Tiwari et al., 2021). On the other hand, it is known that biofuels are used as oil substitutes, and the raw materials of biofuels are various agricultural products. Therefore, demand for biofuel alternatives increases against any increases in fossil fuel prices that may emerge based on geopolitical risks and uncertainties. Therefore, agricultural product markets are subject to demand-side changes based on the oil substitution feature of biofuels (Tiwari et al., 2021). Any fluctuations in agricultural product prices are reflected in energy prices through biofuel prices. Thus, the effects of risks and uncertainties on energy or agricultural commodity prices may also lead to the interaction of these commodity prices among themselves. Considering this multidimensional pattern among the variables that are taken into account, the study also analyzes the relationship between food prices and energy prices.

Geopolitical risks, economic policy uncertainties, energy prices, and food prices are analyzed together in this study, which is important for the analysis of the interactive structure among variables. The impact of geopolitical risks or economic policy uncertainties on commodity prices may need to be assessed simultaneously. For example, C.-W. Su et al. (2021) suggested that political crises would increase oil prices in their study on the relationship between energy prices and geopolitical risks. However, they stated that decreases in geopolitical risks would not decrease oil prices. In the study, this is justified by the fact that there may be increases depending on the financial or economic conditions of the period. In this case, it is considered significant to evaluate geopolitical risks and economic policy uncertainties together.

In the study, the relationships between geopolitical risk, economic policy uncertainty, and energy and agricultural commodity prices were analyzed based on Granger causality. Granger causality allows for the identification of precedence relationships between variables under study. This allows for the identification of price changes that follow geopolitical risks or economic policy uncertainties. Thus, the study findings are expected to provide evidence for the pass-through of economic policy shocks or geopolitical risks to energy and food prices through channels such as deterioration in the confidence environment, supply-demand fluctuations, financial channels, and inter-market volatility.

Considering that the relationship between variables considered in the study may change over time, a time-varying Granger causality approach is used. Standard Granger causality tests assume that the VAR model parameters used in the testing process are constant. Possible structural breaks in variables often lead to violations of this assumption. Including structural breaks in the model with dummy variables by researchers may lead to pre-test biases (Nakhli et al., 2022; Nyakabawo et al., 2015). The nature and pattern of geopolitical risks, economic policy uncertainties, and food and energy prices raise doubts concerning the success of standard causality tests. This judgment is supported by some previous studies. Degiannakis et al. (2018), who examine the relationship between oil price shocks and uncertainties, argued that static frameworks do not show the relationship dynamics between the variables. The study provides strong evidence that uncertainty responses to price shocks are heterogeneous both by time and by different price shocks. Similarly, many studies on the relationship between risks and uncertainties and commodity prices (Ben Haddad et al., 2021; Chen et al., 2019; E. Dogan et al., 2022; Gao et al., 2019; He & Sun, 2024; Huang et al., 2022; T.-T. Sun & Su, 2024; Yang et al., 2022) have emphasized the time-varying nature of the relationship. In this study, we use the time-varying Granger causality approach introduced by Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) to test the causal relationships between variables based on the variable structures with many structural breaks and the widespread acceptance by previous studies.

Literature Review

This study analyzes the relationship between geopolitical risk and economic policy uncertainty and the prices of agricultural and energy commodities. This section summarizes some previous studies on the subject. The relationship between geopolitical risk and economic policy uncertainty and agricultural and energy commodity prices has been tested many times for different commodities and commodity groups using various methods. The results provide extensive evidence for dynamic correlations and volatility spillovers between geopolitical risks and economic policy uncertainty and these commodity prices. In addition, some of the examined studies provide inferences about the interaction mechanism between the variables under consideration.

The relationship between geopolitical risks and economic policy uncertainties and agricultural commodity markets has been confirmed by many studies (Frimpong et al., 2021; Jana & Ghosh, 2023; Micallef et al., 2023; T.-T. Sun et al., 2021; T.-T. Sun & Su, 2024; Wu et al., 2023). However, there is no consensus on the direction and nature of the effect. T.-T. Sun and Su (2024) suggested a time-varying bidirectional Granger causality relationship between geopolitical risks and food prices. In the study, it is stated that high geopolitical risk will increase food prices, while the effects of geopolitical risks on supply and demand conditions in global food markets are emphasized. In another study that provides inferences on the effects of geopolitical risks on food supply-demand conditions, Deng (2024) analyzed the effects of geopolitical risks in two different ways as internal and external risks. It was shown in the study that country-specific risks negatively affect domestic production, while external risks reduce food imports. It was also reported in the study that countries with low output levels are more easily exposed to geopolitical risks. Indeed, it has been argued that policy uncertainties in developed countries have relatively significant impacts on less developed countries. Oshodi and Olasehinde-Williams (2025) confirmed the impact of US trade policy uncertainties on Nigeria’s participation in the global value chain. In another study that examines these relationships within the context of development, F. Su et al. (2023) affirmed the effects of economic policy uncertainty on food markets and stated that the negative effects of economic policy uncertainty on food security are lower in developed countries. Suggesting that policy uncertainty will increase agricultural commodity prices, T.-T. Sun et al. (2021) assert that transitivity is demand-driven. They also emphasize that governments increase the demand for agricultural commodities to prevent food security risks against policy uncertainties and that increased demand creates upward pressures on agricultural commodity prices. Some studies examine the relationship between risks and uncertainties and agricultural commodity prices for specific products. Hudecová and Rajčániová (2023) provide evidence of the asymmetric impact of geopolitical risk on rapeseed, sugar, sunflower oil, and wheat prices, while commodity prices such as corn, cotton, milk, oats, and soybeans show no long-run link with geopolitical risks. Micallef et al. (2023) tested the effects of geopolitical risk on the prices of 10 agricultural commodities classified as soft commodities and cereals. The results confirmed the effects of geopolitical risks on wheat and oats. This was associated with the war between two major agricultural commodity producers, Russia and Ukraine. In another study (Zhou et al., 2023) on food security problems during this war, commodity networks other than the barley trade network were found to have a relatively consistent ability to recover and prevent damage against war and global panic. This conclusion is supported by Ahmed and Sarkodie (2021), who analyze the effects of economic policy uncertainty on commodity prices in the context of the COVID-19 pandemic. In this study, Ahmed and Sarkodie (2021) analyze the responses of the most widely traded commodity prices to uncertainty and find that agricultural commodities respond less negatively to exogenous variables. In a study testing the relationship between Russia’s increased geopolitical risk during the war period and European food prices, Sohag et al. (2022) suggested that geopolitical risk decreases food prices in Eastern Europe in the short run and increases food prices in Western Europe in the long run. Considering the characteristics of agricultural commodities as alternative investment instruments in times of risk and uncertainty, Jana and Ghosh (2023) relate geopolitical uncertainties to agricultural commodity investments. They found that uncertainty affects investments in agricultural spot markets in the medium term and futures markets are less sensitive to geopolitical risks than spot markets. Akyildirim et al. (2022) affirmed the effects of economic policy uncertainty on agricultural commodity returns and investor sentiment. Thus, it can be stated that empirical evidence has been provided regarding the channels of supply-demand conditions and investor behavior in the relationship between risks and uncertainties and agricultural commodity markets. In some other studies examining the relationship between food prices and risks and uncertainties, Kirikkaleli and Darbaz (2022) reported that economic policy uncertainty is a long-term and persistent cause of food prices, while Wen et al. (2021) reported that the effect of economic policy uncertainty on food prices is asymmetric and only short-term. The studies that provide evidence of unidirectional causality from risks and uncertainties to food prices (Chowdhury et al., 2021; Saâdaoui et al., 2022) provide inferences about the importance of economic and political stability for commodity markets. Establishing the bidirectional relationship between risks and uncertainties and commodity prices, T.-T. Sun and Su (2024) emphasize the power of food markets to reflect the geopolitical environment.

The energy sector is more affected by geopolitical risks and economic policy uncertainties than other sectors (Foglia et al., 2023; Mo et al., 2024). Risks and uncertainties that arise in countries with high levels of fossil fuel reserves or in nearby regions affect energy markets, especially through channels such as supply-demand fluctuations and supply security, and these effects have been confirmed in many studies (B. Doğan et al., 2023; Duan et al., 2021; Kara & Gök, 2022; Khurshid et al., 2024; C.-C. Lee et al., 2021; Liu & Chen, 2022; Mei et al., 2020; Tissaoui et al., 2024; L. Wang et al., 2021; Zhu et al., 2021). Jin et al. (2023) affirm that tensions between Russia and Ukraine, which has the largest natural gas reserves, caused two large geopolitical risk shocks in energy markets in 2014 and 2022. Furthermore, it was suggested in the study that the frequency-dependent spillover effects are more pronounced at higher frequencies. These results are consistent with the studies of B. Li et al. (2020) who found that a co-movement between geopolitical risks and oil prices is present only at high frequencies. This shows that any phenomenon that can be considered as a geopolitical risk factor can have immediate effects on energy markets. Foglia et al. (2023) who revealed that the Russo-Ukrainian conflict is one of the most important geopolitical risk shocks, affirmed the impact of geopolitical risks on energy markets and emphasized that risk transmission depends on geographical proximity to the source of the risk. In another study assessing the relationship between energy commodities and geopolitical risks in the context of the Russia-Ukraine conflict, Shahzad et al. (2022) affirmed the importance of geopolitical risk for energy markets. Cunado et al. (2020), Muğaloğlu et al. (2023), and Uddin et al. (2018) reported that geopolitical risks and economic policy uncertainties cause supply shocks and have a positive impact on energy prices through changes in supply and demand conditions. Moreover, the effects of risk and uncertainty on investor behavior and financial stability are affirmed (Qi et al., 2022). In their study examining the effects of the COVID-19 period, which is a period of significant uncertainty, on stocks, Chien-Chiang et al. (2022) revealed a co-movement between infections and stock price indices. Thus, inferences about the transitivity from investor behavior to energy markets are also possible. This inference can be supported by the results of other studies that emphasize the role of risks and uncertainties in the relationship between oil prices and stock prices (Gao et al., 2019; Hoque et al., 2019). The trade dimension of energy supply security is one of the important factors in the emergence of the effects of geopolitical risks on energy markets. F. Li et al. (2021) affirm the negative effects of geopolitical risks on energy trade (based on the result that the effects on exports are larger than the effects on imports) in their study of 17 emerging economies. In another study, Zhang et al. (2024) suggested both positive and negative (pre- and post-Covid-19) effects of economic policy uncertainty and geopolitical risks on energy trade. However, it can be stated that the effects of economic policy uncertainty on energy markets are more limited. Suggesting that the effects of economic policy uncertainty on the oil market vary in direction and strength over time, Chen et al. (2019) reported that the spillover effect between oil prices and uncertainties is weak in the short run, but becomes stronger in the long run. In another study presenting similar results, X. Sun et al. (2020) suggested in their analysis of G7 countries, China, Brazil, and Russia that there is no causality relationship between economic policy uncertainties and oil prices in the short run, except for the US. It is stated in the study that causal relations emerge in the medium and long run. Confirming the effects of economic policy uncertainties on energy markets, Scarcioffolo and Etienne (2021) stated that these effects decreased after 2010. In their study estimating the income and price elasticities of gasoline demand, C. Lee and Olasehinde-Williams (2021) confirmed the effects of economic crisis periods on elasticities. Besides, some studies provide evidence that volatility in energy markets may lead to geopolitical risks and economic policy uncertainty. Zhu et al. (2021) reported a positive short-term effect of oil prices on economic policy uncertainty. In another study, Y. Wang et al. (2022) stated that oil prices have heterogeneous effects on economic policy uncertainty, meaning that the effects differ across countries. He and Sun (2024) suggested that in most cases, oil supply shocks have a negative effect on geopolitical risk, while demand shocks have a positive effect and the effects are time-dependent.

Another dimension of the relationship between geopolitical risk and economic policy uncertainty and energy and agricultural commodities is the volatility spillovers across commodities. There is ample evidence that energy and agricultural commodity prices are affected by geopolitical risk and economic policy uncertainty. In addition to this network of relationships, many studies provide strong evidence of the interaction of agricultural and energy commodities (Adeosun et al., 2023; Ciaian & Kancs, 2011; Kang et al., 2019; Shiferaw, 2019; C. W. Su et al., 2019; Tiwari et al., 2018). Sohag et al. (2022) emphasized the relationship between geopolitical risks and energy prices with agricultural commodities and suggested the effects of risk events and global energy prices on food inflation. Confirming the long-run asymmetric relationship between energy prices and food prices (Alnour et al., 2023), stated that economic policy uncertainty and energy prices shape food prices. Shiferaw (2019) suggested that the dependence between agricultural commodities and energy prices is a dynamic relationship varying by time, while Adeosun et al. (2023) stated that the relationship between commodity prices is bidirectional and consistent with economic policy uncertainty. Vu et al. (2019) affirmed the cost-push effects of different agricultural shocks on oil prices through the bio-fuel channel. Zmami and Ben-Salha (2023) affirmed the sensitivity of food prices to oil prices and emphasized the critical impact of geopolitical risk on food prices under different market conditions. Results obtained from the studies of Fowowe (2016), Kaltalioglu and Soytas (2011), and Nazlioglu and Soytas (2011) suggest that agricultural commodity prices are neutral to changes in energy prices. Affirming the strong co-movements in agricultural and food markets, Tiwari et al. (2021) stated that the relationship emerges in the form of negative correlations. Thus, it can be stated that agricultural commodities may act as a shield for energy commodity returns that are negatively affected by geopolitical unrest.

Data

This study assesses the relationship between geopolitical risk and economic policy uncertainty and energy and agricultural commodity prices on a global scale. Instead of representing geopolitical risks and economic policy uncertainties with dummy variables in models, an alternative is to use calculated indices for risks and uncertainties. This avoids the coverage problem that arises from ignoring the magnitude of risks and uncertainties (C.-W. Su et al., 2021). In this study, geopolitical risks (GPR) arising from unpredictable political, economic, and social activities due to geographical location, political system, unstable government, and regions are represented by the GPR index developed by T.-T. Sun and Su (2024), Caldara and Iacoviello (2018). The GPR index is based on the number of articles discussing geopolitical events and risks in the electronic archives of 10 major newspapers (Caldara & Iacoviello, 2018). As a measure of economic policy uncertainty (EPU), we use the global EPU (GEPU) index developed by Davis (2016) based on the EPU index of Baker et al. (2016). The GEPU index is the average of the EPU indices of 16 countries that provide 2/3 of global output. Countries’ EPU indices reflect the frequency of the articles in national newspapers containing the triple term on economics, politics, and uncertainty (Davis, 2016). An increase in the value of this index indicates an increase in geopolitical risks and economic policy uncertainties. The FAO (Food and Agriculture Organization) Food Price Index (FFPI) is used to represent agricultural commodity prices on a global basis. This index is a measure of international prices for a basket of traded agricultural commodities (FAO, 2024). FFPI data were obtained from FAO. The Global Energy Price Index (GEPI), which represents the prices of energy commodities from the IMF Primary Commodity Prices statistics, is used to represent the energy commodity prices variable. This index represents the weighted average of the prices of the same commodity in different parts of the world (IMF, 2024). GEPI data is obtained from IMF statistics.

In this study, the sample period was determined in a manner to ensure maximum observations. Accordingly, the relationship between GPR and FFPI, and GEPI is analyzed for the period 1992M1-2022M10. 1992M1, which is chosen as the starting date, is the first period for which FFPI data is available. The period 1997M1-20022M10 was chosen to test the relationship between GEPU and FFPI and GEPI. This choice is justified by the availability of GEPU data as of 1997M1. The series is included in the study in natural logarithmic form.

Descriptive statistics of the variables are presented in Table 1. Based on these summary statistics, it is noteworthy that the GEPU series has a higher deviation than the GPR series. This can be presented as evidence of a higher level of volatility in economic policy uncertainties. Another important point is the results obtained from the normality test for the variables. The results of the Jarque-Bera test show that the variables included in the model are not normally distributed because the null hypothesis of the normal distribution is rejected for all series.

Descriptive Statistics (Non-Log).

Methodology

When the econometric literature is examined, it is seen that the basis of causality tests used to increase the predictability of time series is based on the pioneering work of Granger (1969, 1980). Granger causality tests focus on estimating bivariate time series within the framework of linear models, accounting for the optimal lag length, and testing the statistical significance of the lagged values of the exogenous variable included in the model (Bozoklu & Yılancı, 2013; Granger, 1980). In its current form, Granger causality consists of determining the antecedent relationship between series. The existence of Granger causality does not require structural causality between variables. This is a limitation of the method in question. This limitation should be considered when evaluating the study findings.

Tests developed based on Granger causality are commonly used in applied studies; they assume that Granger causality relationships between variables remain constant over time. This assumption is based on the premise that these relationships are fixed and do not change. However, Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) have criticized this approach. They argue that the stationarity assumption limits traditional Granger causality tests, making it difficult to capture dynamic processes such as policy changes, economic shocks, and technological advancements. Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) emphasize that causal relationships between variables may vary over time and suggest that examining these relationships over time can increase predictive power.

In the literature on econometrics, various methodological approaches to time-varying Granger causality tests have been introduced to examine how factors like policy changes, economic shocks, and technological advancements affect causal relationships. The methodology offers three methods, a forward recursive algorithm, a rolling window algorithm, and a recursive evolving algorithm, to detect change points in causal relationships based on the data without requiring prior knowledge of the trends of the data. Thoma (1994) and Swanson (1998) proposed that causal relationships between variables can be analyzed over time using the forward expanding window and rolling window methods. The first approach employs Wald test statistics and involves continuously expanding the regression equations’ window size based on the number of observations. The second approach, on the other hand, assumes that the window size remains constant throughout all observations. Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) criticized these techniques, arguing that their restrictive assumptions about window size and the number of observations can lead to over- or underestimation of Wald test statistics. In response to these concerns, Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) proposed a new approach that iteratively calculates Wald test statistics using subsamples. In this approach, called the recursive evolving window, Wald test statistics are calculated iteratively by considering all subsamples and their joint significance rather than just a portion of the observations. In this method, the Sup Wald test statistics (SW), which represent the upper norm of the Wald test statistics, are calculated for each observation. This process is repeated for each observation in the sample based on the minimum window size and concludes by associating every observation with the iterative Wald test statistic.

The causality procedure proposed by Shi, Phillips, and Hurn (2018) is used to estimate the time-varying causal relationships between geopolitical risks and economic policy uncertainties and energy and food prices. This procedure, based on Granger causality, allows for detecting and dating changes in Granger causality relationships. The procedure is based on a bivariate VAR model with the null hypothesis that there is no Granger causality between the variables. The time-varying Granger causality test, which is based on the recursive computation of Wald test statistics, can be expressed in the form of a Vector Autoregression (VAR) model for the variables

In Equations 1 and 2, the time-varying causal relationships between the variables

The procedure described so far relies on tests based on the full sample. In this case, it will not be possible to detect the expected changes in causality relationships. However, the nature of the relationship between many economic variables makes time-varying relationships possible. The causal relationships between geopolitical risks and economic policy uncertainties and food and energy prices are also expected to change. Many factors such as the severity of risks and uncertainties, the regions where they arise, and the importance of countries for the global economy are expected to affect the causality relationship between variables. In this case, inferences based on a test statistic such as the one in Equation 3 are based on the average of the sample information and lead to significant information loss. Testing Granger causality for subsamples of the sample that are determined exogenously provides information about the periods under consideration but does not make it possible to identify points of change in the causal relationship. For the detection of possible changes and change points in the causal relationship, Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) introduced a new real-time varying test procedure based on supremum (sup) Wald statistical series following a forward recursive (Thoma, 1994) and a rolling window (Swanson, 1998) and based on a recursive evolving (Phillips et al., 2015a, 2015b) method. In this procedure, the

where

where cv and scv are the corresponding critical values of the

In the time-varying Granger causality test, as suggested by Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020), the test statistics

Results and Discussion

Augmented Dickey-Fuller (ADF; Dickey & Fuller, 1979) and Phillips-Perron (PP; Phillips & Perron, 1988) conventional unit root tests were utilized to determine the degree of integration of the variables before conducting the Granger causality tests between the variables considered in the study. In addition, the stationarity of the series was tested using the Zivot-Andrews (ZV; Zivot & Andrews, 1992), Lee-Strazicich (LS; J. Lee & Strazicich, 2003) and Narayan and Popp (NP; Narayan & Popp, 2010) structural break unit root tests, which do not require a priori information for structural breaks and the break dates are determined endogenously.

The results from the ADF and PP conventional unit root tests are presented in Table 2. According to these results, GEPU and GPR variables are stationary at level. FFPI and GEPI variables, on the other hand, become stationary in first differences according to both ADF and PP test results. The results of the unit root test with structural breaks presented in Table 3 support the inference about the stationarity of GEPU and GPR variables at the level. In addition, the results obtained from the unit root tests with two structural breaks support the stationarity of the FFPI and GEPI variables. When the results were evaluated as a whole, it was concluded that all variables subject to Granger causality relationships are stationary at their level values. At this point, a stance was taken in favor of two-break tests, because structural breaks are likely to occur, given the structure of the variables. Structural changes are observed, particularly in food and energy prices, due to factors such as supply shocks, permanent changes in demand, and fragility in the global competition chain. The tests were conducted with the level values of the variables at which they were stationary.

Traditional Unit Root Test Results.

Note. p (optimal lag length) was determined according to Schwarz information criterion. CV = Indicates critical values at 10% significance level.

indicates stationarity at the 1% significance level.

Unit Root Test Results With Structural Break(s).

Note. p (optimal lag length) was determined according to Schwarz information criterion. CV = Indicates critical values at 10% significance level.

,**, and *** indicate stationarity at the 10%, 5%, and 1% significance levels, respectively.

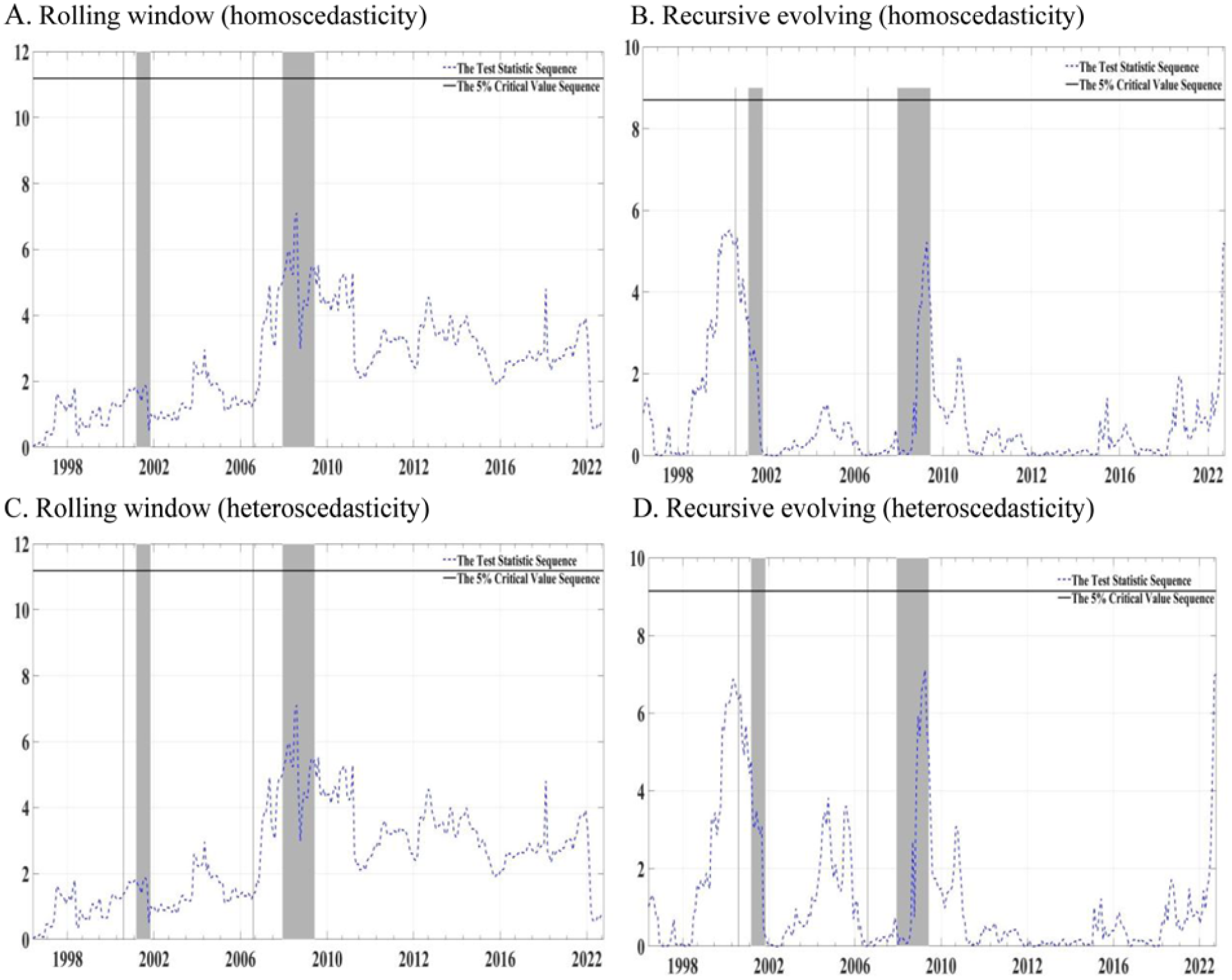

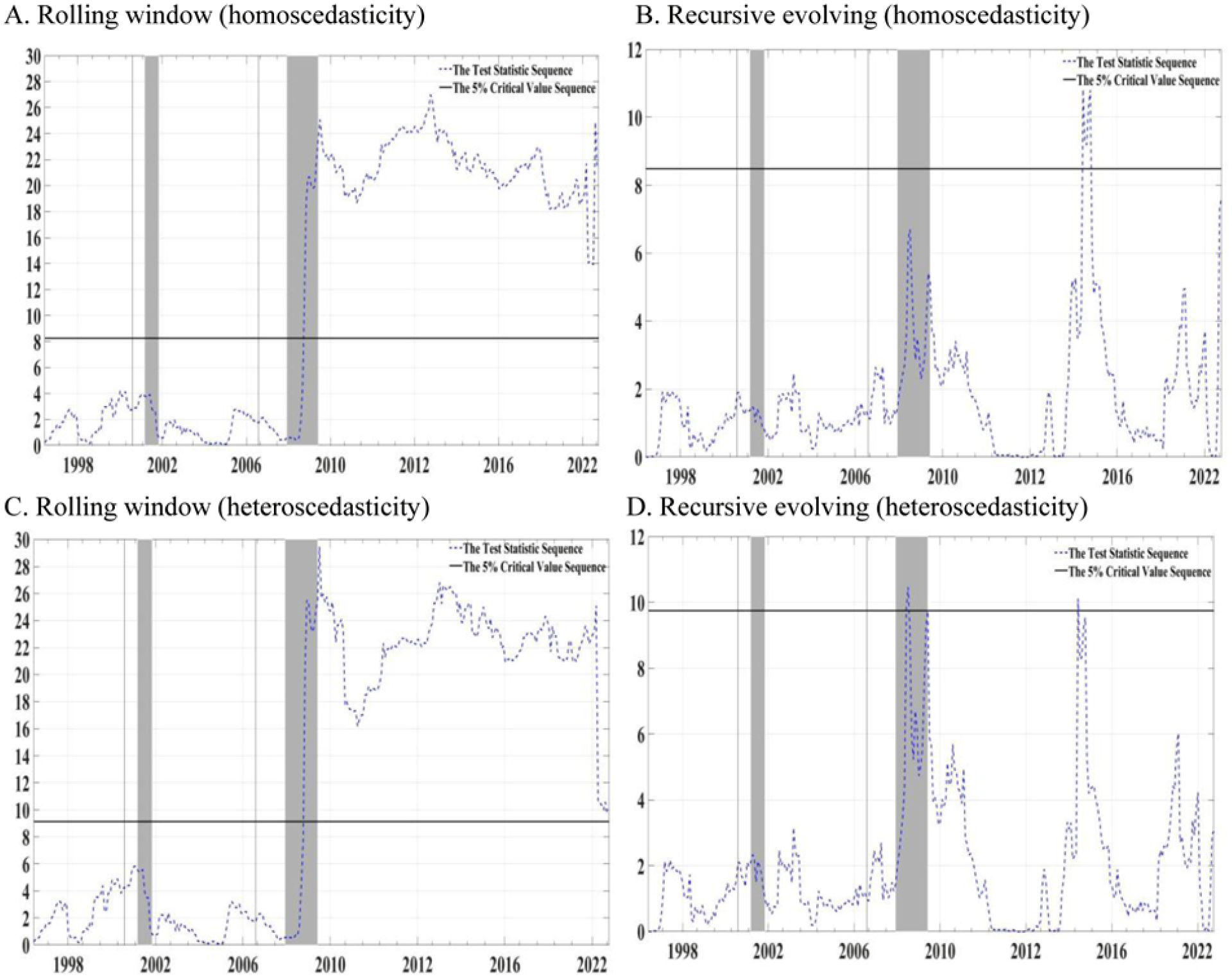

The following figures (Figures 1–10) summarize the test results on the time-varying Granger causality of geopolitical risks and economic policy uncertainties and food and energy prices. The rows in the first column of the figures show the homoscedasticity and heteroscedasticity assumptions of the error terms for the VAR and the results obtained from the rolling window procedure, respectively. The rows in the second column contain graphs comparing the test statistics obtained from their recursive evolving procedures with critical values in the same order. The shaded areas in the graphs indicate the stages of recession according to the dating of the National Bureau of Economic Research (NBER). In the graphs, the black lines parallel to the horizontal axis represent the critical value series at the 5% significance level, while the blue dashed lines represent the Wald statistic series. When the statistical series exceeds the critical value in any period, it provides evidence for significant causal effects.

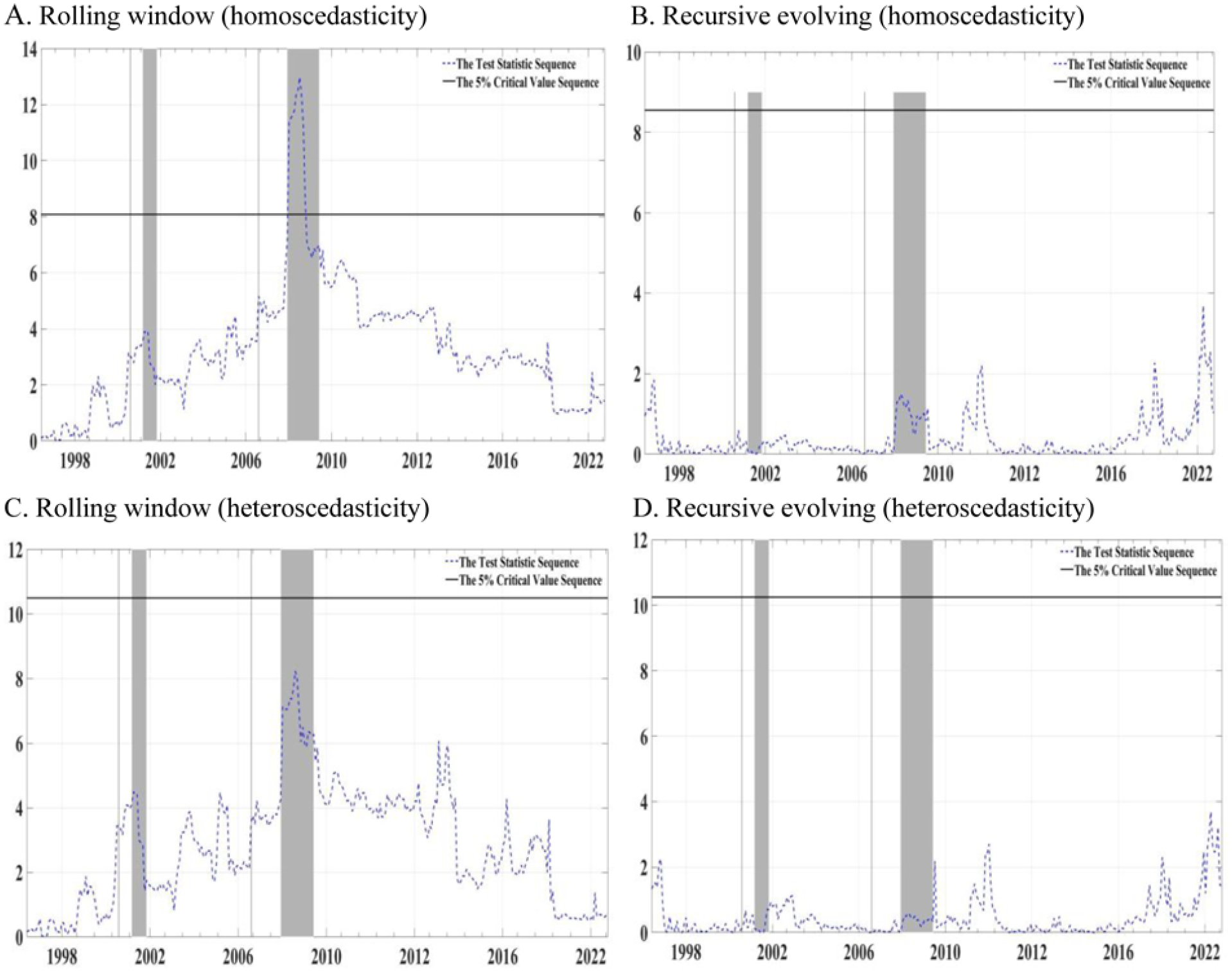

Time-varying Granger causality running from GPR to FFPI. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Time-varying Granger causality running from FFPI to GPR. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

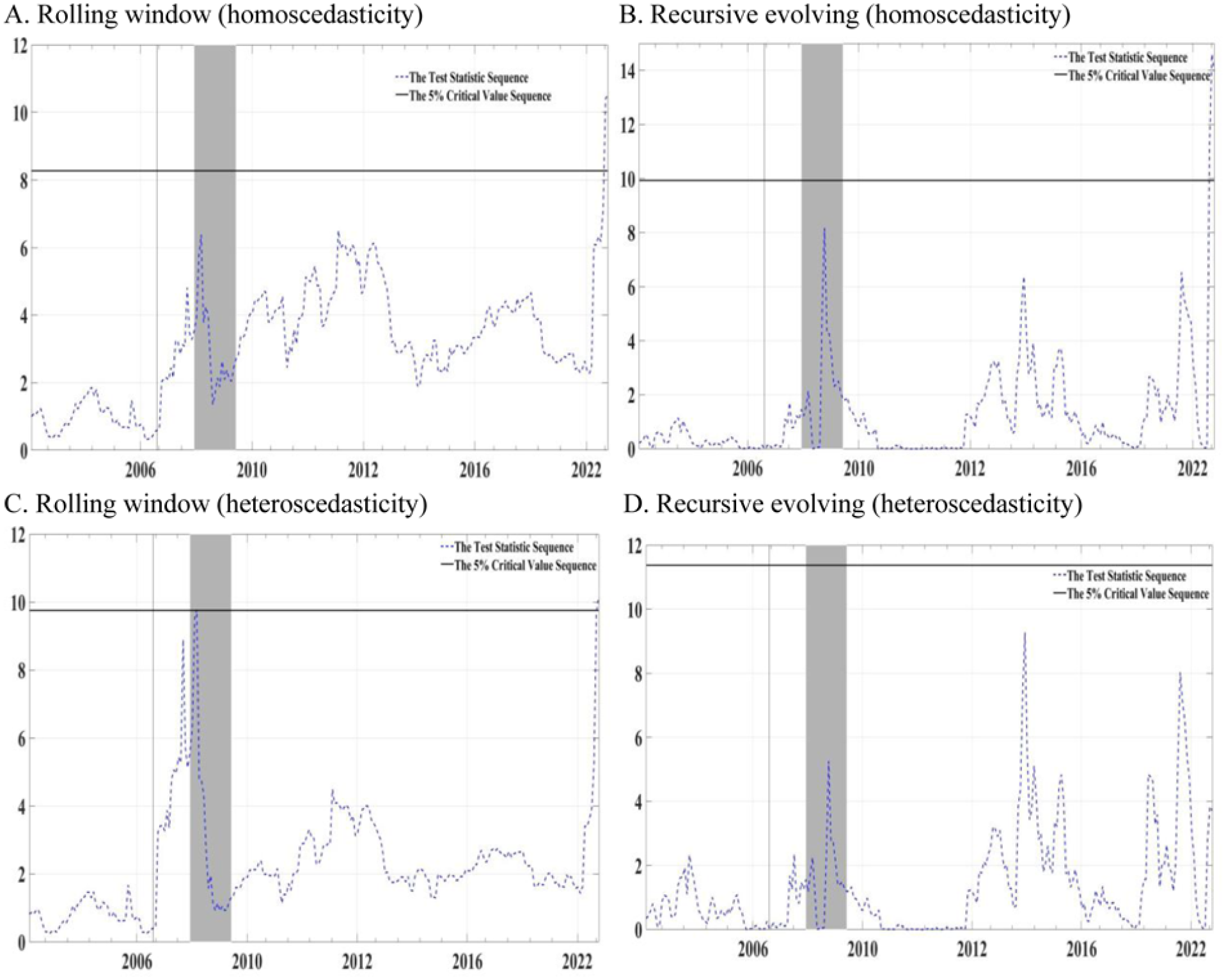

Time-varying Granger causality running from GPR to GEPI. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Time-varying Granger causality running from GEPI to GPR. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

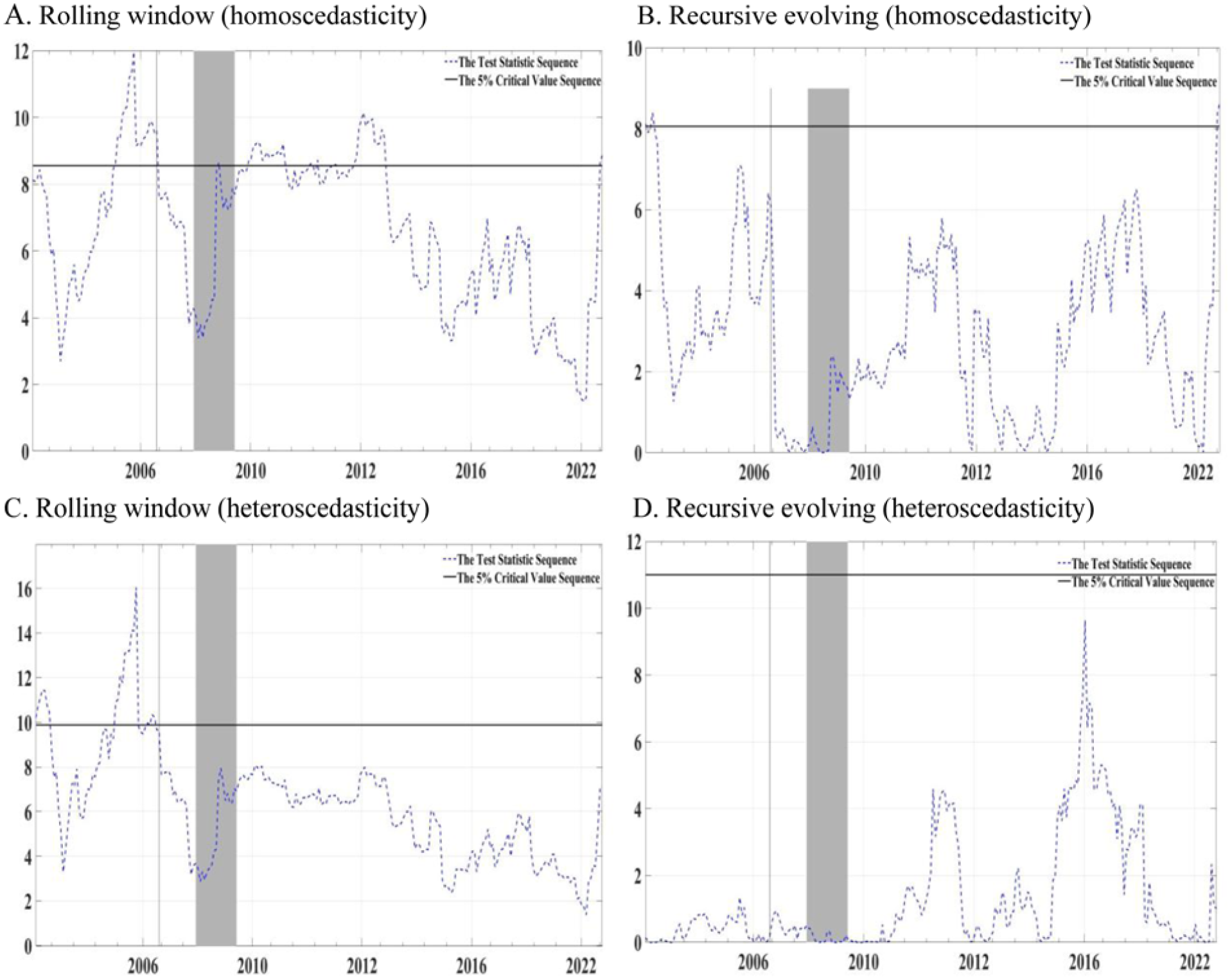

Time-varying Granger causality running from GEPU to FFPI. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Time-varying Granger causality running from FFPI to GEPU. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Time-varying Granger causality running from GEPU to GEPI. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Time-varying Granger causality running from GEPI to GEPU. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

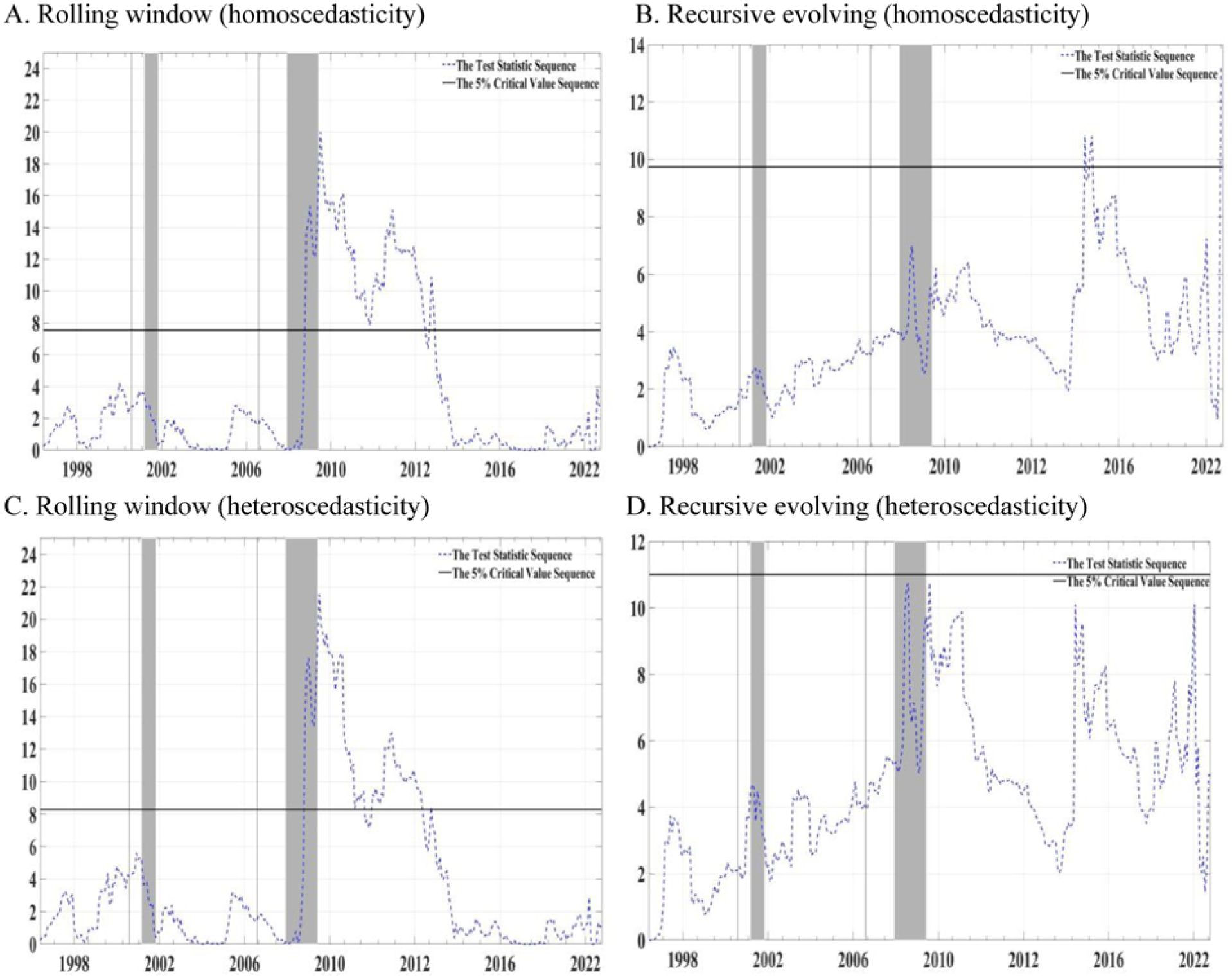

Time-varying Granger causality running from FFPI to GEPI. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Time-varying Granger causality running from GEPI to FFPI. (A) Rolling window (homoscedasticity), (B) Recursive evolving (homoscedasticity), (C) Rolling window (heteroscedasticity), (D) Recursive evolving (heteroscedasticity).

Figures 1 and 2 present evidence on the relationship between geopolitical risks and food prices. It is observed that the test statistics remain below the critical values throughout the sampling period. The results from the rolling window and recursive evolving procedures indicate that the null hypothesis suggesting that there is no Granger causality between the variables over the sample period cannot be rejected for both constant variance and changing variance hypotheses. The test statistics of the time-varying Granger causality analyses examining the relationships between the GPR and FFPI variables, computed for the decennial windows periodically drawn from the study period, are presented in Table S7.

The relationship between geopolitical risks and energy commodities was tested using GPR and GEPI variables. Differences are observed between the results obtained from the rolling window and recursive evolving procedures. The results from the rolling window procedure under the assumption of constant variance presented in Panel A of Figure 3 reveal that the test statistic exceeds the critical value in 2008. Therefore, the null hypothesis stating that there is no Granger causality in this period can be rejected. However, this result is not supported by the assumption of heteroscedasticity and the results from the rolling window procedure (panel C). Furthermore, the test statistics obtained with the recursive evolving procedure are below the critical values for variance under both assumptions (panels B and D). Thus, it can be stated that there is no Granger causality from GPR to GEPI over the sampling period. This conclusion is based on the results (Shi, Hurn, & Phillips, 2020) that the results obtained from the recursive evolving process are more reliable. Figure 4, which analyzes the Granger causality relationship from GEPI to GPR, which is the other dimension of the relationship, shows similar results. Accordingly, only the test statistics obtained from the rolling window process with the homoscedasticity assumption exceed the critical values for the 2008 to 2009 period. In other words, there is a Granger causality relationship from GEPI to GPR in this period and the duration of the effect is longer than the effect of the Granger causality from GPR to GEPI. However, this is not supported by other alternative estimation results (panels B, C, and D). Again, given the assessment of the success of the respective procedures, the inference that there is no Granger causality from GEPI to GPR during the sample period is supported. Considering the results on the relationship between geopolitical risks and other variables, it can be generally concluded that there is no Granger causality between geopolitical risks and food and energy prices over the sampling period. Test statistics for selected periods for the time-varying causality relationships between GPR and GEPI are presented in Table S7. These findings reveal that geopolitical risks are not a precursor to energy and food price fluctuations. This does not mean that theoretically risks do not cause price fluctuations. The findings only allow us to infer that risks and price fluctuations do not follow each other.

Economic policy uncertainties constitute another dimension of uncertainties affecting economic activity. The Granger causality relationship between economic policy uncertainties and food prices is presented in Figure 5. According to the results obtained from the rolling window procedure, the test statistic exceeds the critical values in the September to October 2022 period under both assumptions regarding variance (panels A and C). These results are also supported by the results obtained with the recursive evolving approach under the homoscedasticity assumption (Panel B). Moreover, as can be seen in Panel B, there is a limited Granger causality relationship in mid-2008. It can be stated that the Granger causality from FFPI to GEPU, which is the other direction of the relationship and of which results are presented in Figure 6, emerged in September to October 2022 Thus, there is limited evidence for a time-varying causal relationship from economic policy uncertainty to food prices and vice versa. Test statistics for selected periods regarding the Granger causality test findings visualized in Figures 5 and 6 are presented in the attached Table S8. The alternative Granger causality tests presented in Table 4 do not reject the null hypothesis of no Granger causality from GEPU to FFPI.

Results of the Granger Causality Test Between GEPU, FFPI, and GEPI.

Note. The values in parentheses are the p-values for the Wald statistic, obtained from 1,000 simulations. Column L(F) indicates the optimal delay and frequency length obtained with a maximum of 12 delays and 3 frequency lengths accompanied by SIC.

,**, and *** indicate stationarity at the 10%, 5%, and 1% significance levels, respectively.

Findings of time-varying causality support the idea that economic policy uncertainties can be suggested as a precursor to food price fluctuations.

Figure 7 presents the evidence of the Granger causality from economic policy uncertainty to energy prices. As can be seen in Panel A and B of the figure, the test statistics obtained from the rolling window and recursive evolving procedures with the homoscedasticity assumption exceeded the critical values in some months of 2016. Table S8 contains summary test statistics for time-varying Granger causality between the GEPU and GEPI series. The aforementioned findings can also be read from the associated table. The null hypothesis stating that there is no Granger causality between the variables can be rejected for the sub-sampling period in question. Therefore, there is limited evidence for the existence of a time-varying causal relationship from economic policy uncertainty to energy prices. Figure 8 presents the evidence of Granger causality from energy prices to economic policy uncertainty. In this aspect of the relationship, it is observed that the differences between the results from the rolling window and recursive evolving procedures emerge evident. Panel A affirms the existence of Granger causality between the variables in the 2005 to 2007 period, in various months in the 2010 to 2013 period, and in October 2022. However, only the relationship in October 2022 can be affirmed by the recursive evolving procedure. These inferences are based on the results obtained by assuming homoscedasticity. These inferences are not accompanied by heteroscedastic model results Figure 8 provides limited evidence on the time-varying Granger causality from energy prices to economic policy uncertainties. Thus, it can be stated that there is limited evidence for the existence of time-varying cross-directional Granger causality between the GEPU and GEPI series.

The findings of time-varying Granger causality between economic policy uncertainties and food and energy prices allow us to consider economic policy uncertainties as an antecedent of fluctuations in commodity prices under study. It is anticipated that channels such as investor behavior in the face of uncertainty, news and policy shocks, supply and demand fluctuations may be effective in the transmission of economic policy uncertainties to prices.

Another dimension of the relationships between the variables considered in the study is the Granger causality between energy prices and food prices. Figure 9 contains the results of the Granger causality test from food prices to energy prices. As can be seen in Panels A and C, the test statistics obtained with the rolling window procedure are above the critical values from 2009 to mid-2012. This result is valid for both homoscedasticity and heteroscedasticity conditions. However, as in the previous results, the results obtained with the recursive evolving approach differ from those obtained with the rolling window approach. According to the results from the recursive evolving procedure with the homoscedasticity assumption presented in Panel B, the null hypothesis of no Granger causality from food prices to energy prices in the October 2014 and 2022 periods can be rejected. These findings can also be seen in Table S9, which presents statistics on the time-varying causal relationship between FFPI and GEPI. Table S9 also contains test statistics for the results visualized in Figure 10. Figure 10 shows the causality from energy prices to food prices. The results obtained from the rolling window procedure point to Granger causality from GEPI to FFPI from 2009 to the present. These results are supported by the results obtained from the recursive evolving procedure for the 2014 period. Thus, it can be concluded that there is a bidirectional time-varying Granger causality relationship between GEPI and FFPI series. The results of the alternative causality test presented in Table 6 confirm Granger causality from FFPI to GEPI. The alternative tests conducted do not reject the null hypothesis of no Granger causality from GEPI to FFPI.

The relationship between geopolitical risks and uncertainties and food and energy prices is tested with the time-varying causality test. The results and evaluations about the results can be summarized in several dimensions. No causality relationship was found between geopolitical risks and food prices over the analyzed period. This allows for the inference that events that can be considered geopolitical risk factors do not have the power to determine global food prices. This inference supports the results obtained from the study of Zhou et al. (2023). It also converges with the results of the study of Hudecová and Rajčániová (2023), stating that risks will only affect the prices of some agricultural commodities. This is because the FFPI series used to represent food prices in the study is an indicator calculated based on the basket price of traded agricultural commodities. Therefore, it does not contradict economic expectations that changes in the prices of limited products due to geopolitical risks are not a precursor to the price level calculated for the basket.

The Granger causality relationship between geopolitical risks and energy prices, which is bidirectional, can be affirmed by the results obtained from the rolling window approach only in certain months of 2008. The results from the recursive evolving procedure indicate that no Granger causality emerges between energy prices and geopolitical risks over the sample period. Considering the fact that the inferences (Adeosun et al., 2023; Kara & Gök, 2022; Mo et al., 2024; C.-W. Su et al., 2021) based on the rolling window method are common in previous studies (Cunado et al., 2020; Duan et al., 2021; C.-C. Lee et al., 2021; Zhao et al., 2024) affirming the relationship between these variables and that the relationship between energy commodities and geopolitical risks is usually tested through oil prices, the results of our study are not surprising. This is because, in this study, the effects of geopolitical risks on the basket price of energy commodities are analyzed using a new methodology. The results differ from previous studies due to the variables included in the model and methodological differences. A bidirectional Granger causality relationship between economic policy uncertainties and food prices is affirmed only for the September-October 2022 period. The 2022 period is known to have witnessed an increase in geopolitical risks due to the Russia-Ukraine conflict. Thus, it can be inferred that the transitivity between economic policy uncertainties and food prices becomes more pronounced in periods of geopolitical risk. In this context, it supports the results of Gao et al. (2019) that the transitivity from policy uncertainties to commodities increases during the period of crisis. Evidence for very limited and short-run relationships between economic policy uncertainties and energy prices were found. This confirms the inferences from previous studies (Ben Haddad et al., 2021; H. Li et al., 2023; T.-T. Sun & Su, 2024; Yang et al., 2022; Zhao et al., 2024) about the time-varying nature of the relationship between uncertainties and commodity markets. Evidence in favor of a time-varying bidirectional Granger causality between global energy prices and global food prices was obtained from the Granger causality test for the relationship between global energy prices and global food prices. These results are in line with many previous studies (Adeosun et al., 2023; Ciaian & Kancs, 2011; Kang et al., 2019; Shiferaw, 2019; C. W. Su et al., 2019; Tiwari et al., 2018) that provide evidence for the relationship between agricultural and energy commodities.

Robustness Checks

In examining the relationship between the variables considered in the study, focusing solely on the findings related to the time-varying Granger causality approach proposed by Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) limits the robustness of the results. To overcome these limitations, the Granger causality between GEPU, GPR, GEPI, and FFPI variables was also tested with alternative methods. Granger causality (Granger, 1969), Toda-Yamamoto Granger causality (Toda & Yamamoto 1995), Fourier Granger causality (Enders & Jones, 2016), and Fourier Toda-Yamamoto Granger causality (Nazlıoğlu et al., 2016) are alternative test procedures used. The alternative tests conducted provide inferences about whether the empirical findings are stable under different estimation techniques. In addition, this section examines whether the findings from the time-varying Granger causality framework—which is a relatively recent methodology and sensitive to parameter variability across the testing period—differ from those obtained with the conventional and Fourier-based Granger causality tests.

Table 4 presents the findings from traditional and Fourier Granger causality tests for the relationship between economic policy uncertainties and food and commodity prices. The findings indicate that the null hypothesis of no Granger causality from GEPU to GEPI and FFPI cannot be rejected. The time-varying Granger causality procedure rejects the null hypothesis of no Granger causality from GEPU to FFPI for limited periods in 2008 and 2022. The hypothesis that there is no Granger causality from GEPU to GEPI was rejected in 2016.

Table 5 summarizes the findings of alternative causality tests regarding the causal relationship between geopolitical risks and food and energy prices. These findings support the findings obtained from the time-varying Granger causality test. Accordingly, the null hypothesis of no Granger causality cannot be rejected in any direction between GPR-GEPI and GPR-FFPI.

Results of the Granger Causality Test Between GPR, FFPI, and GEPI.

Note. The values in parentheses are the p-values for the Wald statistic, obtained from 1,000 simulations. Column L(F) indicates the optimal delay and frequency length obtained with a maximum of 12 delays and 3 frequency lengths accompanied by SIC.

Table 6 presents the findings regarding the relationship between FFPI and GEPI. Accordingly, none of the alternative tests conducted can reject the null hypothesis of no Granger causality from GEPI to FFPI. The findings from the time-varying Granger causality procedure confirm the Granger causality from GEPI to FFPI for a limited period in 2014. The Granger causality from FFPI to GEPI is confirmed for limited periods in 2014 and 2022. The Toda-Yamamoto Granger causality, Fourier Granger causality, and Fourier Toda-Yamamoto Granger causality test findings reject the null hypothesis of no causality from FFPI to GEPI for the entire study period.

Results of the Granger Causality Test Between FFPI and GEPI.

Note. For symbols in the table, see Table 4.

Conclusion

The time-varying Granger causality relationships between global geopolitical risks and economic policy uncertainties and global food and energy prices are tested with the procedure proposed by Shi, Phillips, and Hurn (2018), Shi, Hurn, and Phillips (2020) as a new approach to time-varying Granger causality. Food and energy prices are included in the model with the FFPI and GEPI series, which can represent the general price levels of traded agricultural and energy commodities, and the tests are conducted at the global level. The study differs from its peers in terms of the assessments made for the general price levels of agricultural and energy commodities and the use of a relatively new econometric approach. The study also provides inferences concerning the time-varying causal relationship between food and energy prices, which represent the prices of these commodities.

Findings from time-varying Granger causality tests do not provide evidence of a time-varying causal relationship between geopolitical risks and food and energy prices. The results allow for the inference that agricultural commodities may provide investors with sheltered alternatives during periods of geopolitical risk. This inference can also be extended to the relationship between geopolitical risks and global energy prices. The results emerging as a consequence of a holistic analysis of food and energy commodities suggest that the fear and panic caused by geopolitical risks are not important for global commodity prices. At this point, it is important to emphasize that the analyses conducted are global in scope. This situation is expressed as a limitation of the study. In particular, policy design for economies should take into account their proximity to the source of risk as well as their position within international trade networks. Assessing the effects of global and local geopolitical risks on energy and food prices, specific to economies, will guide the policy designs of countries.

Results confirming the causal relationship between economic policy uncertainties and food and energy prices – although quite limited – have been presented in some periods. Therefore, economic policy uncertainties are likely to be accompanied by fluctuations in food and energy prices. It can be expressed that in times of economic policy uncertainty, investors should turn to alternative instruments that provide protection. In addition, global commodity price fluctuations based on risks and uncertainties are a determinant of countries’ domestic inflation levels. Another result of the study that should be noted at this point is the confirmed time-varying Granger causality relationship between food and energy prices. This result presents a pattern with the potential to transition to the domestic inflation level. The results of the study provide policy recommendations that can be used to predict or avoid inflation fluctuations. Policymakers are advised to secure food and energy commodity prices through long-term trade agreements that are resilient to global economic uncertainties. Moreover, governments need to be prepared for situations where supply-demand shocks may cause food or energy price fluctuations, taking into account the causal relationships between energy and food commodity prices. Agricultural production support, tax advantages in international trade, and more investment in renewable energy alternatives that reduce foreign dependency are recommended.

The results also show that the study findings may differ from traditional approaches that approach causality assessments holistically in a time-varying Granger causality procedure. The time-varying Granger causality procedure is an essential alternative for detecting or avoiding the omission of periodic causal relationships between variables. Another point worth emphasizing here is that the study examines the relationship between the variables within the framework of Granger causality. It should be noted that Granger causality does not require theoretical causality but rather establishes a precedent relationship between variables. Thus, the study interprets the findings obtained with these limitations within the framework of economic patterns. The effects of geopolitical risk and economic policy uncertainty on commodity prices are expected to be tested with country samples and different methods. The use of time-varying impulse-response functions in assessing the effects of risk and uncertainty shocks on prices is offered as a suggestion for future studies.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440261420449 – Supplemental material for Do Geopolitical Risk and Economic Policy Uncertainties Affect Food and Energy Commodity Prices? Evidence From Time-Varying Granger Causality Test

Supplemental material, sj-docx-1-sgo-10.1177_21582440261420449 for Do Geopolitical Risk and Economic Policy Uncertainties Affect Food and Energy Commodity Prices? Evidence From Time-Varying Granger Causality Test by Ali Kemal Çelik, Ömer Yalçınkaya and Muhammet Kutlu in SAGE Open

Footnotes

Author Contributions

All the authors were involved in all the research that led to the article and in its writing. All authors read and approved the final manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data used in this research were obtained from various open access databases.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.