Abstract

This study aims to resolve theoretical ambiguities concerning the impact of digital transformation (DT) on Environmental, Social, and Governance (ESG) performance within the unique institutional context of an emerging economy. It specifically investigates the mediating role of green innovation as a key mechanism in the DT-ESG nexus in Vietnam. The study utilizes a balanced panel dataset of 400 enterprises listed on Vietnamese stock exchanges from 2019 to 2024. We construct novel composite indices for both digital transformation and green innovation using Principal Component Analysis (PCA) on data from corporate annual reports. To address endogeneity and dynamic panel bias, the analysis employs a System Generalized Method of Moments (SGMM) estimator, with the mediation pathway tested via a cluster-bootstrap analysis. The findings reveal that digital transformation has a positive and statistically significant impact on corporate ESG performance. Green innovation is confirmed as a crucial mediating mechanism, translating digital capabilities into enhanced sustainability outcomes. This effect is heterogeneous across industries, with the technology and energy sectors showing the most pronounced positive impacts. Firm size and supportive national policies are also found to amplify these effects. This study contributes to the literature by providing one of the first empirical examinations of the DT-ESG relationship in Vietnam. It offers a synthesized theoretical framework and develops context-appropriate, non-patent-based measures for digital transformation and green innovation. The findings provide actionable insights for managers and policymakers in emerging markets on leveraging digital transformation as a strategic driver for sustainable development.

Keywords

Introduction

The relationship between digital transformation and corporate sustainability performance constitutes a critical theoretical puzzle in contemporary organizational scholarship. While established theories suggest technological capabilities should enhance organizational performance across multiple dimensions (Bharadwaj, 2000; Teece, 2007), the mechanisms through which digital transformation influences Environmental, Social, and Governance (ESG) outcomes remain theoretically underdeveloped and empirically contested (Dubey et al., 2019; George et al., 2021). This theoretical ambiguity intensifies in emerging economy contexts, where institutional voids, resource constraints, and divergent development trajectories may fundamentally alter the digital-sustainability nexus (Khanna & Palepu, 2010; Marquis & Raynard, 2015).

Vietnam exemplifies this theoretical puzzle with particular acuity. The nation’s digital economy expanded at 29% compound annual growth from 2019 to 2024, reaching US$23 billion and positioning Vietnam among Southeast Asia’s fastest digitalizing economies. Yet this rapid digitalization trajectory sharply diverges from nascent ESG maturity. Only 38% of listed enterprises disclosed formal ESG reports in 2024, with average ESG scores lagging regional peers by 17 to 23 percentile points despite comparable digital infrastructure investment. This paradoxical divergence (advanced digital capabilities coexisting with underdeveloped sustainability institutionalization) generates a critical empirical context for examining whether and how digital transformation translates into ESG performance when formal institutional supports remain nascent.

Existing scholarship exhibits pronounced geographic and institutional bias, with three critical gaps impeding theoretical advancement. First, the institutional void paradox remains unresolved. Institutional theory posits organizational practices reflect isomorphic pressures from regulatory, normative, and cognitive institutions (DiMaggio & Powell, 1983; Scott, 2014), yet emerging economies exhibit weak sustainability institutions that theoretically should attenuate the digital-ESG relationship. Whether digital capabilities can substitute for institutional supports or whether institutional voids fundamentally constrain sustainability impacts remains theoretically contested. Second, innovation pathway mechanisms are inadequately theorized for non-patent contexts. The prevailing logic, that digital transformation enhances ESG through facilitating green innovation, relies overwhelmingly on patent-based measures developed in contexts with strong intellectual property regimes, systematically mischaracterizing innovation in emerging economies where green innovation manifests through informal process improvements and incremental modifications rarely captured in patent databases (Fu et al., 2011; Zanello et al., 2016). Third, the dynamic capabilities-institutional context interaction lacks empirical grounding. While Dynamic Capabilities Theory suggests digital transformation enables organizational adaptation (Teece, 2018; Vial, 2019), whether dynamic capabilities remain effective under institutional constraints or whether resource constraints create unique pathways through which digital capabilities influence sustainability represents a critical theoretical frontier inadequately examined in existing scholarship.

This study advances understanding through three interconnected contributions. Theoretically, we develop an integrated framework synthesizing Resource-Based View, Dynamic Capabilities Theory, and Institutional Theory to explicate how digital transformation influences ESG performance under institutional underdevelopment, explicitly theorizing institutional voids as boundary conditions fundamentally altering mechanisms through which digital capabilities translate into sustainability outcomes. Methodologically, we advance innovation measurement by developing a composite Green Innovation Action Index derived from systematic content analysis, triangulating multiple innovation dimensions through Principal Component Analysis to provide contextually appropriate operationalization beyond patent-based metrics. Empirically, we provide the first systematic examination of the digital transformation-green innovation-ESG pathway using longitudinal data from Vietnamese listed enterprises, employing System GMM estimation to address endogeneity and simultaneity concerns, providing evidence regarding whether digital capabilities can autonomously drive sustainability improvements in institutional void contexts or whether institutional development remains prerequisite.

Literature Review

Theoretical Debates on Digital Transformation and Organizational Performance

Scholarly discourse on digital transformation’s sustainability implications reflects a fundamental theoretical tension between technological optimism and critical skepticism, generating contradictory empirical findings that this study seeks to resolve. This theoretical polarization manifests across three dimensions: the nature of digital transformation’s effects, the mechanisms through which effects occur, and the contextual contingencies moderating these relationships.

Technological optimists, anchored in the Resource-Based View and capability-based theories, posit that digital technologies constitute strategic resources enabling superior environmental monitoring, stakeholder engagement, and sustainability governance (Bharadwaj, 2000; Warner & Wäger, 2019). This perspective emphasizes digital transformation’s enabling functions: real-time data collection facilitating resource optimization (Y. Chen et al., 2014), enhanced transparency strengthening stakeholder accountability (Gholami et al., 2013), and analytical capabilities improving sustainability decision-making (Brynjolfsson & McElheran, 2016). Empirical studies in developed economies predominantly support this optimistic view, documenting positive associations between digital capabilities and environmental performance (ElMassah & Mohieldin, 2020), social responsibility indicators (Srivastava & Shainesh, 2015), and composite ESG scores (Benner & Tushman, 2015; Feroz et al., 2021; C. Xu et al., 2024).

Critical skeptics, conversely, highlight potential negative consequences and paradoxical effects. This perspective, drawing on institutional theory and critical technology studies, emphasizes that digital transformation may increase organizational complexity, disrupt existing capabilities, and generate substantial environmental costs through energy consumption and electronic waste (Belkhir & Elmeligi, 2018; Lange et al., 2020). Moreover, critics argue that digital technologies primarily drive efficiency-oriented innovations that may not align with broader sustainability objectives, potentially creating rebound effects wherein efficiency gains stimulate increased consumption that offsets environmental benefits (Böhringer et al., 2012). Empirical investigations supporting this skeptical view document weak or non-significant digital transformation-ESG associations in certain contexts (Bendig et al., 2018; Liu et al., 2024), negative relationships under specific conditions (P. Chen & Hao, 2022), and substantial heterogeneity suggesting that contextual factors fundamentally moderate the relationship (Feroz et al., 2021; H. Wang et al., 2022).

Emerging economy contexts amplify this theoretical tension. While both optimists and skeptics develop arguments based primarily on developed economy evidence, the institutional environments, resource constraints, and innovation systems characteristic of emerging economies may fundamentally alter the digital-sustainability dynamics. Recent studies examining Asian and Latin American contexts yield particularly heterogeneous results—some demonstrating strong positive effects (Li et al., 2016), others finding weak associations (L. Zhou et al., 2023), and still others identifying non-linear relationships suggesting threshold effects or contingency factors (Singh et al., 2020; L. Zhou et al., 2023). This empirical heterogeneity suggests that the digital transformation-ESG relationship may be institutionally contingent, with mechanisms and boundary conditions varying systematically across economic contexts (Gan, 2025; Luo & Child, 2015; Wright et al., 2005).

ESG Performance: Measurement Challenges and Theoretical Foundations

The conceptualization and measurement of ESG performance remain theoretically contested despite widespread adoption by practitioners and policymakers (Christensen et al., 2022). Stakeholder theory provides the dominant theoretical foundation, suggesting that organizations must balance multiple stakeholder interests to achieve long-term value creation (Freeman, 1984; Harrison et al., 2010). However, critical perspectives challenge the coherence of ESG as a unified construct, arguing that environmental, social, and governance dimensions may involve fundamentally different logics and potential trade-offs (Bansal & Song, 2017; Delmas & Blass, 2010).

Measurement challenges compound theoretical ambiguities. The proliferation of ESG rating methodologies has produced substantial divergence in assessments, with correlations between major rating agencies ranging from .38 to .71 (Berg et al., 2022; Chatterji et al., 2016). This divergence reflects not merely technical measurement issues but fundamental disagreements about what constitutes sustainability performance and how different dimensions should be weighted (Dorfleitner et al., 2015; Gibson Brandon et al., 2021). Furthermore, the validity of ESG metrics in capturing actual sustainability impacts remains questionable, with studies documenting substantial gaps between ESG scores and environmental or social outcomes (Busch et al., 2022; Lyon & Montgomery, 2015).

The institutional embeddedness of ESG practices introduces additional complexity. Institutional theory suggests that organizations adopt ESG practices not solely for performance benefits but also to gain legitimacy and conform to institutional pressures (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). This raises critical questions about whether ESG performance represents substantive organizational change or merely symbolic compliance (Bromley & Powell, 2012; Marquis et al., 2016). The decoupling of ESG policies from practices has been documented across contexts, with particular prevalence in emerging economies where institutional enforcement mechanisms remain weak (Jamali et al., 2017; Yin & Zhang, 2012).

Recent scholarship examining ESG measurement and conceptualization challenges has intensified these debates. Berg et al. (2022) demonstrates that rating divergence across agencies exceeds previous estimates, with implications for empirical research validity. Christensen et al. (2022) provides evidence that ESG performance measures may systematically misflag emerging economy firms due to Western-centric evaluation criteria, while C. Xu et al. (2024) documents substantial sectoral heterogeneity in ESG metric validity that prior research inadequately addresses These methodological concerns compound theoretical ambiguities, suggesting that observed digital transformation-ESG relationships may partially reflect measurement artifacts rather than substantive organizational phenomena.

Green Innovation: Conceptual Ambiguities and Empirical Contradictions

The green innovation literature reveals fundamental conceptual ambiguities regarding the definition, measurement, and drivers of environmentally beneficial innovations (Schiederig et al., 2012; Tariq et al., 2019). While early conceptualizations focused narrowly on end-of-pipe technologies and pollution control innovations (Kemp & Arundel, 1998), contemporary frameworks encompass process innovations, organizational innovations, and system-level transformations (Adams et al., 2016; Carrillo-Hermosilla et al., 2010). This conceptual expansion, while theoretically justified, complicates empirical investigation and comparison across studies.

The relationship between digital capabilities and green innovation remains theoretically underdeveloped and empirically contested. The complementary assets perspective suggests that digital technologies enhance green innovation through improved knowledge management, simulation capabilities, and stakeholder collaboration (Benitez et al., 2018; Melville, 2010). However, empirical studies yield contradictory findings, with some demonstrating positive effects (Singh & El-Kassar, 2019), others finding no significant relationship (Bendig et al., 2018), and still others identifying negative associations under certain conditions (P. Chen & Hao, 2022). These contradictions suggest the presence of untheorized boundary conditions and mediating mechanisms.

The measurement of green innovation through patent data, while offering objectivity and comparability, imposes severe conceptual limitations that remain inadequately addressed in the literature (Haščič & Migotto, 2015; Popp, 2019). Patent-based measures systematically underestimate green innovation in emerging economies where informal innovation, process improvements, and non-patentable organizational innovations predominate (Fu et al., 2011; Zanello et al., 2016). Moreover, the focus on patented innovations privileges technological solutions while marginalizing social and organizational innovations that may be equally or more important for sustainability transitions (Boons et al., 2013; Klewitz & Hansen, 2014).

These measurement limitations have motivated recent methodological innovations. Liu et al. (2024) develops alternative green innovation metrics based on textual analysis of sustainability reports, while Liu et al. (2024) employ machine learning approaches to identify environmental innovations in corporate disclosures. Zhang et al. (2024) provides evidence that disclosure-based measures capture innovation activities with stronger predictive validity for actual environmental performance compared to patent-based metrics in emerging economy contexts.

Synthesis and Research Gap

The literature review reveals three critical gaps that this study addresses. First, existing research lacks an integrated theoretical framework that captures the multi-level mechanisms linking digital transformation to ESG performance under conditions of institutional underdevelopment. While studies examine individual relationships, the complex interplay between digital capabilities, innovation processes, and institutional voids remains theoretically underspecified. Second, the mediating role of green innovation in the digital transformation-ESG relationship has not been systematically theorized or empirically tested using measurement approaches appropriate for emerging economy contexts. Specifically, the prevailing reliance on patent-based innovation metrics systematically underestimates green innovation in institutional environments characterized by weak intellectual property protection, underdeveloped formal R&D systems, and innovation pathways emphasizing incremental process improvements over breakthrough technological inventions. This measurement gap creates a fundamental disconnect: theoretical frameworks developed in patent-rich contexts may inadequately capture the mechanisms operative in emerging economies where innovation manifests differently. Our development of a composite Green Innovation Action Index through systematic content analysis directly addresses this measurement-theory misalignment, enabling more valid examination of innovation’s mediating role in contexts where patents provide incomplete innovation signals. Third, the boundary conditions that moderate digital-sustainability relationships, including institutional voids, resource constraints, and capability gaps characteristic of emerging economies, remain largely unexplored, with existing studies predominantly examining facilitating conditions rather than constraining factors.

Theoretical Framework and Hypothesis Development

Integrative Theoretical Foundation

This study synthesizes three complementary theoretical perspectives to explicate the mechanisms linking digital transformation to ESG performance through green innovation. The Resource-Based View (RBV) provides the micro-foundational logic for understanding how digital capabilities generate competitive advantage and enable sustainability performance (Barney, 1991; Hart, 1995). Dynamic Capabilities Theory extends this foundation by theorizing the processes through which organizations reconfigure resources to address rapidly changing environmental demands (Teece, 2018; Teece et al., 1997). Institutional Theory offers the macro-level framework for understanding how regulatory pressures, normative expectations, and cognitive schemas shape organizational sustainability practices (Scott, 2014; Thornton et al., 2012).

The integration of these perspectives addresses limitations inherent in single-theory approaches. While RBV explains resource heterogeneity and competitive advantage, it inadequately addresses the processes through which resources are reconfigured in response to environmental change (Priem & Butler, 2001). Dynamic Capabilities Theory addresses this processual dimension but underspecifies the institutional forces that enable or constrain capability development (Peteraf et al., 2013). Institutional Theory elucidates these contextual influences but often neglects agency and strategic choice in organizational responses to institutional pressures (Oliver, 1991). By synthesizing these perspectives, we develop a multi-level framework that captures both the strategic and institutional dimensions of the digital transformation-ESG relationship.

Digital Transformation and ESG Performance: Direct Effects

The direct relationship between digital transformation and ESG performance operates through multiple theoretical mechanisms. From an RBV perspective, digital capabilities constitute strategic resources that enable superior environmental monitoring, stakeholder engagement, and governance processes (Bharadwaj, 2000; Wade & Hulland, 2004). Digital technologies facilitate real-time data collection and analysis, enabling organizations to identify inefficiencies, reduce resource consumption, and optimize operations for environmental performance (Y. Chen et al., 2021; Corbett, 2018). Moreover, digital platforms enhance stakeholder communication and transparency, addressing social and governance dimensions of ESG (Gholami et al., 2013; Srivastava & Shainesh, 2015).

Dynamic Capabilities Theory suggests that digital transformation enhances organizational sensing, seizing, and reconfiguring capabilities crucial for sustainability performance (Teece, 2007; Warner & Wäger, 2019). Digital sensing capabilities enable organizations to identify emerging sustainability risks and opportunities through advanced analytics and environmental scanning (Mikalef et al., 2020). Seizing capabilities facilitate the rapid deployment of sustainability initiatives through digital coordination and resource mobilization (Karimi & Walter, 2015). Reconfiguring capabilities enable continuous adaptation of sustainability strategies based on performance feedback and changing stakeholder expectations (Vial, 2019).

However, the institutional context fundamentally shapes these capability-performance relationships. In emerging economies, institutional voids, the absence or underdevelopment of market-supporting institutions, may constrain the translation of digital capabilities into ESG performance (Khanna & Palepu, 1997; Mair & Marti, 2009). Weak regulatory enforcement, underdeveloped sustainability standards, and limited stakeholder activism may reduce incentives for leveraging digital capabilities toward sustainability objectives (Doh et al., 2017; Marquis & Qian, 2014). Conversely, strong state-led digitalization initiatives characteristic of many emerging economies may create unique pathways for ESG improvement through government-mandated sustainability reporting and digital monitoring systems (Child & Tsai, 2005; Peng et al., 2009).

The Green Innovation Pathway: Mediation Mechanisms and Institutional Boundary Conditions

Green innovation constitutes the critical mediating mechanism through which digital transformation influences ESG performance, yet the nature and strength of this mediation pathway depend fundamentally on institutional configurations and organizational capabilities characteristic of emerging economies. This section develops the theoretical logic linking digital capabilities to green innovation and subsequently connecting green innovation to sustainability outcomes, while explicitly theorizing the institutional contingencies that may amplify or attenuate these relationships.

From Digital Capabilities to Green Innovation

The digital transformation-green innovation relationship operates through three interconnected mechanisms grounded in the knowledge-based view and dynamic capabilities theory. First, digital technologies enhance organizational absorptive capacity, which is the ability to recognize, assimilate, and apply external knowledge for innovation purposes (Cohen & Levinthal, 1990; Zahra & George, 2002). Digital platforms facilitate knowledge flows across organizational boundaries, enabling access to diverse sustainability knowledge sources crucial for green innovation development (Nambisan et al., 2017; Urbinati et al., 2020). Big data analytics and artificial intelligence enable pattern recognition and predictive modeling that identify innovation opportunities previously obscured by information complexity (Ghasemaghaei & Calic, 2019; Wamba et al., 2017).

Second, digital transformation enhances innovation capabilities through enabling rapid experimentation, facilitating open innovation and ecosystem collaboration, and supporting evidence-based innovation decisions (Bogers et al., 2018; Brynjolfsson & McElheran, 2016; Nambisan et al., 2019). In the green innovation context specifically, digital technologies reduce the temporal and financial costs of sustainability-oriented experimentation, enabling virtual prototyping of eco-designs, simulation of environmental impacts, and iterative refinement of cleaner production processes without requiring extensive physical infrastructure investment (Ghobakhloo, 2020; Müller et al., 2018).

Third, the institutional environment critically shapes this relationship. In emerging economies, weak intellectual property protection may discourage patentable green innovations while encouraging informal and incremental innovations that digital technologies particularly enable (Phelps, 2010). Limited access to green technology markets and underdeveloped innovation ecosystems constrain commercialization of digital-enabled green innovations (Fu et al., 2011). However, government support for green technology development and digital transformation may create complementary policy synergies that enhance innovation outcomes beyond what either policy domain achieves independently (Gan, 2025; Liu et al., 2015; K. Z. Zhou et al., 2017).

From Green Innovation to ESG Performance: Mediation Mechanisms

Green innovation translates digital capabilities into ESG performance through both technological and organizational pathways, consistent with the natural resource-based view’s extension of RBV to incorporate environmental constraints and opportunities (Hart, 1995; Hart & Dowell, 2011). Technologically, green innovations directly reduce environmental impacts through cleaner production processes, resource efficiency improvements, and pollution reduction technologies (Y. S. Chen et al., 2006; De Marchi, 2012). Organizationally, the green innovation process enhances environmental management capabilities, stakeholder engagement, and sustainability-oriented organizational culture (Albort-Morant et al., 2016; Chang, 2011).

Moreover, green innovations signal organizational commitment to sustainability, enhancing legitimacy and stakeholder support crucial for social and governance dimensions of ESG beyond direct environmental impacts (Berrone et al., 2013; Surroca et al., 2009). This signaling function may be particularly salient in emerging economies where formal sustainability institutions remain nascent, green innovation activities provide tangible evidence of environmental commitment that compensates for weak third-party verification and regulatory enforcement (Marquis & Qian, 2014; Peng et al., 2009).

However, institutional voids attenuate the green innovation-ESG performance relationship through several mechanisms. First, the “liability of emergingness” (resource constraints and capability gaps) limits translation of innovations into performance improvements (Madhok & Keyhani, 2012; Ramamurti, 2012). Second, weak market demand for green products reduces commercialization incentives and revenue generation from innovations (Hoskisson et al., 2013; Sheth et al., 2011). Third, absent regulatory enforcement diminishes performance benefits, as innovations may be developed but not fully implemented or monitored (Peng et al., 2008; C. Xu et al., 2024; L. Zhou et al., 2023).

These theoretical considerations yield a mediation hypothesis acknowledging both the enabling and constraining forces operative in emerging economy contexts:

Research Methodology

Sample Selection and Data Collection

Population and Sampling Frame

The study population comprises all enterprises listed on the Ho Chi Minh City Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX) during the 2019 to 2024 period. As of December 2024, HOSE contained 412 listed firms while HNX contained 384 listed firms, yielding a total population of 796 enterprises. The sampling frame was constructed through a systematic screening process to ensure data quality and methodological consistency.

The initial screening applied the following inclusion criteria: (1) continuous listing throughout the study period to ensure panel balance; (2) availability of complete annual financial reports in Vietnamese or English; (3) disclosure of digital transformation-related investments and initiatives in annual reports or supplementary disclosures; and (4) availability of ESG scores from at least one recognized rating agency (Sustainalytics, Refinitiv, or MSCI). Exclusion criteria comprised: (1) financial institutions requiring specialized regulatory frameworks (n = 68); (2) enterprises undergoing major restructuring, mergers, or acquisitions during the study period (n = 43); (3) enterprises with more than 20% missing data across key variables (n = 89); and (4) enterprises classified as penny stocks or under special monitoring by the exchanges (n = 31).

Final Sample Composition

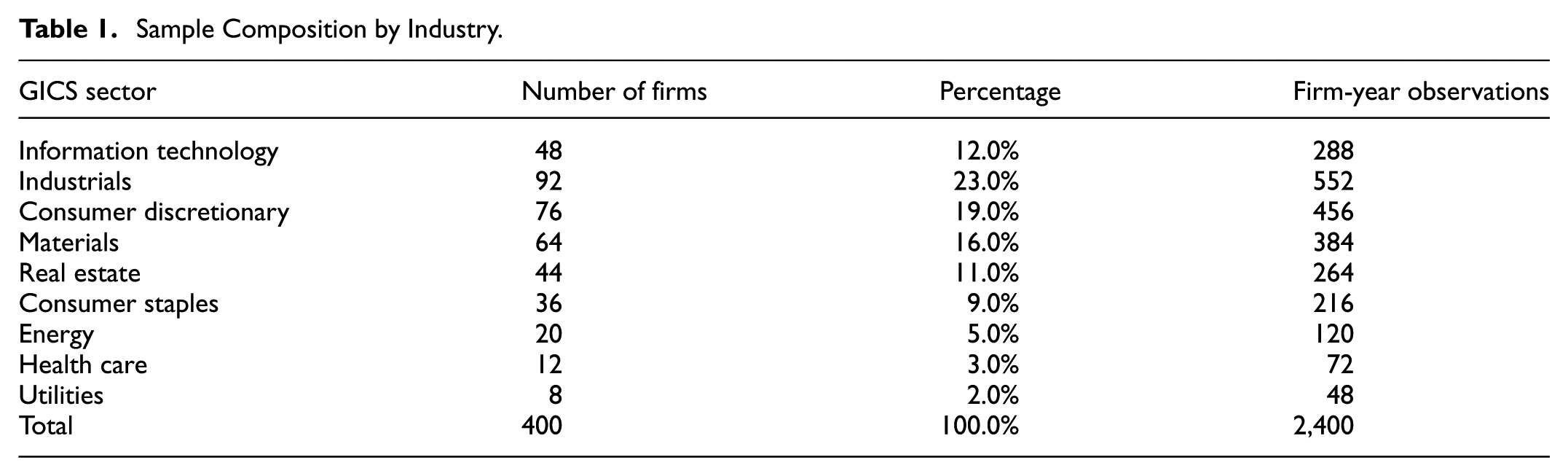

The screening process yielded a final balanced panel of 400 enterprises observed over 6 years (2019–2024), generating 2,400 firm-year observations. Table 1 presents the sample distribution across industries using the Global Industry Classification Standard (GICS).

Sample Composition by Industry.

The sample exhibits reasonable industry diversification, though with expected concentrations in industrials and consumer sectors characteristic of Vietnam’s economic structure. Technology firms, while representing only 12% of the sample, demonstrate higher digital transformation intensity, potentially influencing aggregate relationships.

Selection Bias Assessment

Several potential selection biases warrant explicit acknowledgment. First, survivorship bias emerges from requiring continuous listing throughout the study period, potentially excluding firms that failed due to unsuccessful digital transformation or poor ESG performance. This constraint may upwardly bias estimated effects. Second, disclosure bias favors larger, more internationally oriented firms with superior reporting capabilities, as evidenced by the mean firm size (log assets = 14.3) exceeding the population mean (13.8). Third, the requirement for ESG scores introduces a systematic bias toward firms with greater stakeholder visibility and institutional investor interest.

To assess selection bias magnitude, we conducted Heckman’s two-stage selection correction. The first-stage probit model predicting sample inclusion yielded an inverse Mills ratio with insignificant coefficients in the second-stage outcome equations (λ = .042, p = .31), suggesting that selection bias, while present, does not substantially distort the main findings. Nevertheless, results should be interpreted as applicable to the subset of Vietnamese listed enterprises with relatively mature governance and reporting practices.

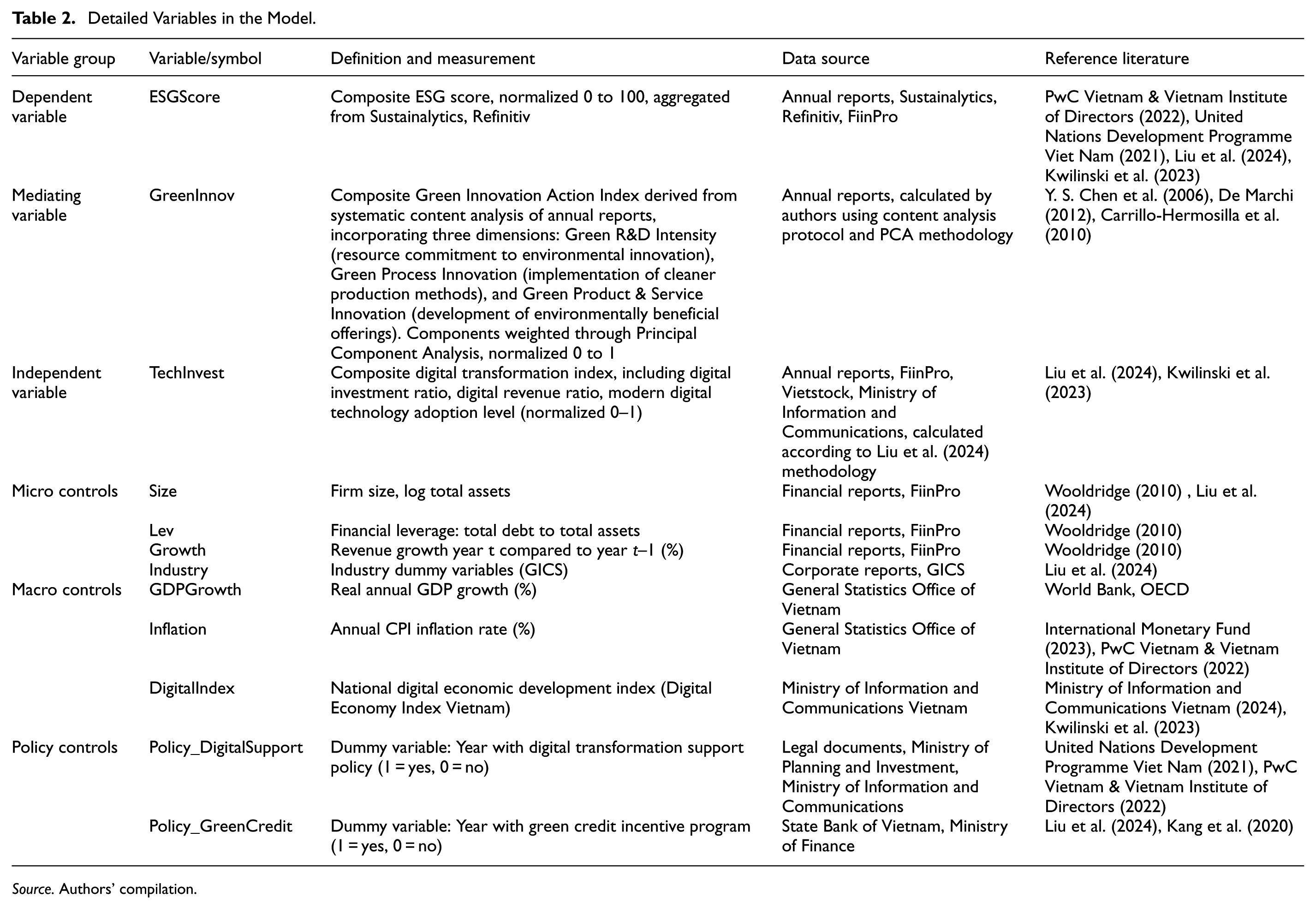

Digital Transformation Index Construction

The digital transformation index (TechInvest) operationalizes the multidimensional nature of enterprise digitalization through three theoretically grounded components. Digital Investment Ratio captures resource commitment to digital transformation, reflecting the input dimension of technological change (Bharadwaj, 2000). Digital Revenue Ratio measures value creation from digital initiatives, representing the output dimension (Vial, 2019). Digital Technology Adoption assesses the breadth of digital technology deployment, indicating the scope of transformation (Nambisan et al., 2019).

Data extraction followed a rigorous protocol to ensure consistency and reliability. For Digital Investment Ratio, we identified digital-related capital expenditures and operating expenses through keyword searches in annual reports (“digital,”“AI,”“IoT,”“cloud,”“automation,”“ERP,”“data analytics”) followed by manual verification. Investments were validated against notes to financial statements and capital expenditure schedules. Digital Revenue Ratio required identifying revenue streams from digital products, services, and channels, cross-referenced with segment reporting where available. Digital Technology Adoption was assessed through systematic content analysis of annual reports, identifying mentions of specific technology implementations (AI/ML, IoT sensors, blockchain, cloud infrastructure, big data analytics, robotic process automation).

Inter-rater reliability testing on a subsample of 50 firms yielded satisfactory agreement (Cohen’s κ = .82 for investment classification, 0.78 for revenue attribution, 0.91 for technology identification). Discrepancies were resolved through consensus discussions and consultation with industry experts.

Rather than arbitrary equal weighting, we employed Principal Component Analysis (PCA) to derive data-driven weights that capture the latent construct of digital transformation. The PCA procedure followed established protocols (Jolliffe & Cadima, 2016):

First, component variables were standardized using z-score transformation to ensure scale comparability:

where

The correlation matrix revealed substantial intercorrelations among components (r = .42–.61), supporting the existence of an underlying factor. Kaiser-Meyer-Olkin measure of sampling adequacy (KMO = 0.73) and Bartlett’s test of sphericity (χ2 = 487.3, p < .001) confirmed suitability for PCA.

The first principal component explained 58.7% of total variance, with loadings of 0.82 (Digital Investment), 0.76 (Digital Revenue), and 0.71 (Digital Adoption). The second component explained 24.3% of variance, while the third explained 17.0%. Following the Kaiser criterion and scree plot analysis, we retained only the first principal component as the digital transformation index:

This PCA-derived index was subsequently rescaled to [0,1] using min-max normalization on the final scores to facilitate interpretation.

Missing data patterns were analyzed using Little’s MCAR test, which rejected the missing completely at random assumption (χ2 = 143.2, p < .01), suggesting systematic missingness potentially related to firm characteristics. Missing data prevalence was 8.3% for Digital Investment, 11.2% for Digital Revenue, and 5.6% for Digital Adoption.

We implemented Multiple Imputation by Chained Equations (MICE) to address missingness while preserving uncertainty (Rubin, 1987; van Buuren, 2018). The imputation model included all analysis variables plus auxiliary variables (industry dummies, lagged performance indicators, CEO characteristics) to satisfy the Missing at Random (MAR) assumption. Twenty imputed datasets were generated using predictive mean matching for continuous variables, ensuring imputed values remained within plausible ranges. Convergence was assessed through trace plots and the Gelman-Rubin statistic (

Sensitivity analyses comparing complete case analysis (n = 324 firms), single imputation, and multiple imputation revealed that multiple imputation yielded the most conservative standard errors while maintaining statistical power. The digital transformation index demonstrated satisfactory psychometric properties across imputed datasets (Cronbach’s α = .78–.81).

Measurement of Green Innovation and Acknowledged Limitations

Measurement of Green Innovation

The measurement of green innovation presents substantial methodological challenges in emerging economy contexts where innovation pathways diverge systematically from developed market patterns. Traditional patent-based metrics, while offering objectivity and cross-national comparability, capture only formalized, legally protected innovations, excluding incremental improvements, process adaptations, and organizational innovations characterizing sustainability transitions in resource-constrained environments (Govindarajan & Ramamurti, 2011; Zanello et al., 2016). In the Vietnamese context, where formal R&D infrastructure remains developing and intellectual property regimes differ substantively from developed markets, corporate disclosures provide more comprehensive insights into actual green innovation activities than patent databases capturing only narrow subsets of formalized innovations (Fu et al., 2011).

This study develops a comprehensive Green Innovation Action Index (GreenInnov) capturing multidimensional sustainability-oriented innovation through systematic content analysis. The theoretical foundation recognizes that green innovation encompasses not merely technological breakthroughs but also process improvements, organizational adaptations, and incremental modifications collectively contributing to environmental performance (Carrillo-Hermosilla et al., 2010; Klewitz & Hansen, 2014). The index comprises three theoretically grounded components: Green R&D Intensity (GRD) capturing resource commitment to environmental innovation (Y. S. Chen et al., 2006); Green Process Innovation (GPI) measuring cleaner production implementation and resource efficiency improvements (De Marchi, 2012); and Green Product & Service Innovation (GPS) assessing environmentally beneficial offering development (Dangelico & Pujari, 2010).

Data extraction followed rigorous content analysis protocols applied to annual reports. A comprehensive keyword dictionary was developed through iterative refinement based on established taxonomies (OECD, 2009) and pilot testing. The coding procedure involved systematic identification and enumeration of keyword occurrences within substantive disclosure contexts, excluding boilerplate language and aspirational statements lacking implementation specifics. Dual coding by independent trained researchers yielded satisfactory inter-rater reliability (Cohen’s κ = .83 for GRD, 0.81 for GPI, 0.85 for GPS), with discrepancies resolved through consensus discussion.

Principal Component Analysis derived empirically grounded component weights following z-score standardization. The correlation matrix revealed substantial intercorrelations (r = .48–.67), with the Kaiser-Meyer-Olkin measure (KMO = .76) and Bartlett’s test (χ2 = 524.7, p < .001) confirming extraction suitability. The first principal component explained 65.2% of total variance with component loadings of 0.85 (GRD), 0.78 (GPI), and 0.81 (GPS). The resulting composite index underwent min-max normalization to (0,1) interval. Sensitivity analyses comparing alternative weighting schemes demonstrated robust correlations (r >.92), supporting measurement validity.

Missing data (7.2% of observations) were addressed through Multiple Imputation by Chained Equations utilizing auxiliary variables including industry classification, firm size, and prior-year ESG scores. The imputation model satisfied convergence criteria (

Acknowledged Limitations

The disclosure-based measurement approach adopted in this study carries inherent limitations requiring explicit acknowledgment. First, disclosure bias potentially advantages larger, internationally oriented enterprises with sophisticated reporting capabilities, systematically underestimating smaller firms’ innovation efforts despite substantive activities. This aligns with observed patterns wherein mean sample firm size (log assets = 14.3) exceeds population parameters. Second, reliance on self-reported disclosures introduces vulnerability to impression management and greenwashing behaviors. While our coding protocol emphasized substantive implementation evidence, distinguishing genuine innovation from strategic communication remains inherently challenging. Keyword frequency, though providing quantitative comparability, imperfectly correlates with actual environmental impact or commercial significance. Third, content analysis cannot fully capture monetary value, technological sophistication, or environmental efficacy of reported innovations. The index measures innovation activity breadth rather than depth or impact, potentially conflating high-frequency incremental changes with transformative breakthrough innovations. Fourth, temporal dynamics and strategic disclosure timing may influence measurement validity, with firms potentially concentrating innovation-related disclosures during periods of heightened regulatory scrutiny, creating artificial volatility unrelated to actual innovation patterns.

Notwithstanding these limitations, the Green Innovation Action Index represents methodological advancement over univariate patent-based measures for capturing green innovation in the Vietnamese context. The multidimensional construction incorporating R&D intensity, process innovation, and product innovation provides comprehensive coverage of innovation activities characterizing emerging economy firms. Systematic coding protocols and reliability testing enhance measurement consistency, while PCA-derived weighting ensures empirical grounding rather than arbitrary aggregation. Future research should pursue triangulation approaches combining disclosure-based measures with innovation surveys, third-party environmental certifications, and direct environmental performance indicators. Despite acknowledged limitations, the index advances measurement practice by capturing innovation pathways critical to understanding sustainability transitions in emerging economy contexts where formal innovation systems remain nascent.

Dependent Variable: Composite ESG Score Construction

The measurement of Environmental, Social, and Governance (ESG) performance presents fundamental methodological challenges stemming from well-documented divergence among rating agencies’ assessment methodologies, scope definitions, and weighting schemes (Berg et al., 2022; Chatterji et al., 2016). Empirical evidence demonstrates correlations between major ESG providers ranging from .38 to .71, substantially lower than the 0.99 correlation observed among credit rating agencies (Gibson Brandon et al., 2021). This divergence reflects fundamental disagreements regarding sustainability performance conceptualization rather than mere measurement error. Consequently, reliance on single-agency ratings introduces idiosyncratic biases potentially distorting empirical findings.

This study constructs a composite ESG score extracting common variance underlying multiple rating assessments, thereby capturing latent consensus regarding firms’ sustainability performance while mitigating agency-specific methodological artifacts. The theoretical justification derives from classical measurement theory, which posits that multiple imperfect indicators can, through appropriate aggregation, yield more reliable measures than single indicators (Bollen & Lennox, 1991). Principal Component Analysis provides the methodological framework for identifying and extracting shared variance, consistent with established index construction practices in management literature (Dess et al., 1997; Hult et al., 2008).

Data collection encompassed firm-year ESG ratings from three leading agencies: Sustainalytics, Refinitiv Workspace, and MSCI ESG Ratings, selected based on market prominence, methodological transparency, and Vietnamese listed enterprise coverage. For 400 sample firms over 2019 to 2024, coverage rates were 92% (Sustainalytics), 88% (Refinitiv), and 85% (MSCI), with 81% of firm-year observations containing ratings from all three sources. Missing ratings were addressed through multiple imputation procedures maintaining analytical consistency.

Heterogeneous scaling conventions necessitated standardization to ensure commensurability. Sustainalytics’ risk-based scoring (0–100, inverted to align directionality), Refinitiv’s percentile-based scores (0–100), and MSCI’s letter ratings (CCC to AAA, converted following established protocols; Dorfleitner et al., 2015) underwent z-score transformation preserving relative firm positioning while enabling cross-agency aggregation.

Factor extraction appropriateness was confirmed through established diagnostics. The Kaiser-Meyer-Olkin measure (0.75) exceeded recommended thresholds (Kaiser, 1974), while Bartlett’s test rejected the identity correlation matrix hypothesis (χ2 = 512.7, df = 3, p < .001). Correlation matrices revealed positive associations (.68–.76) between agency pairs, supporting common underlying dimensionality while acknowledging agency-specific variance.

Principal Component Analysis on standardized scores demonstrated that the first principal component captured 78.5% of total variance (eigenvalue = 2.36), substantially exceeding unidimensionality thresholds. Second and third components explained 13.2% and 8.3% respectively (eigenvalues <1.0). Component loadings were 0.89 (Sustainalytics), 0.91 (Refinitiv), and 0.86 (MSCI), with communalities ranging from 0.74 to 0.83. The composite score was calculated as weighted sum of standardized ratings, subsequently min-max normalized to 0 to 100 scale preserving relative positioning while facilitating interpretation. The composite ESG score for each firm-year observation was calculated as:

To enhance interpretability and maintain consistency with conventional ESG reporting practices, the raw component scores underwent min-max normalization to a 0 to 100 scale:

The resulting composite measure demonstrated satisfactory psychometric properties (Cronbach’s α = .84), indicating strong internal consistency. Sensitivity analyzes employing alternative aggregation methods yielded correlations exceeding 0.94 with PCA-derived scores, supporting measurement robustness. This methodology addresses single-agency limitations while preserving informational content across multiple assessment frameworks, enhancing both validity and reliability for examining digital transformation-ESG relationships in Vietnamese contexts.

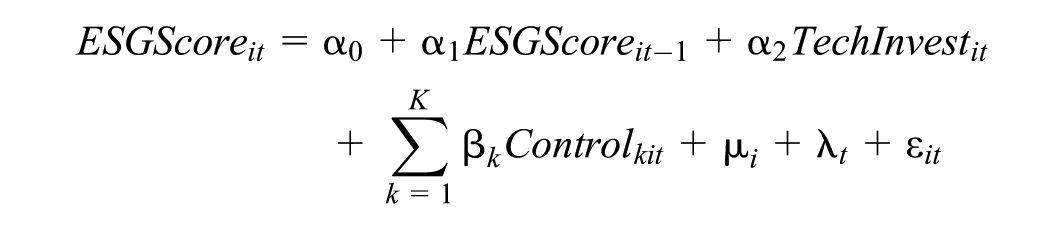

Research Model

The research model evaluates the impact of the digital transformation index on ESG performance of listed enterprises in Vietnam while testing the mediating role of green innovation in this relationship. The study employs panel data from 400 enterprises listed on the Ho Chi Minh City Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX) during 2019 to 2024. Sample selection criteria include: Industry diversification: Technology, finance, manufacturing, energy, consumer goods, real estate; Size representation (large, medium, and small enterprises).

Three regression models are constructed as follows:

Model 1 - Overall impact of digital transformation on ESG performance:

Where ESGScoreit represents the composite ESG score for enterprise i at time tTechInvestit is the digital transformation index, Controlkit are control variables including micro variables (size, leverage, revenue growth, industry), macro variables (GDP growth, inflation, national digital development index), and policy support variables (tax incentives, green credit, national digital transformation programs). μi represents firm fixed effects, λt captures year fixed effects, and error terms are assumed to follow standard distributional assumptions. The lagged dependent variable addresses persistence in ESG performance while partially controlling for unobserved heterogeneity.

Model 2 - Impact of digital transformation on green innovation:

Where GreenInnovit is the composite Green Innovation Action Index for enterprise i at time t, constructed through Principal Component Analysis as specified in Section 4.3, capturing resource commitment to environmental innovation (Green R&D Intensity), implementation of cleaner production methods (Green Process Innovation), and development of environmentally beneficial offerings (Green Product & Service Innovation) (Description of variables are detailed in Table 2).

Detailed Variables in the Model.

Source. Authors’ compilation.

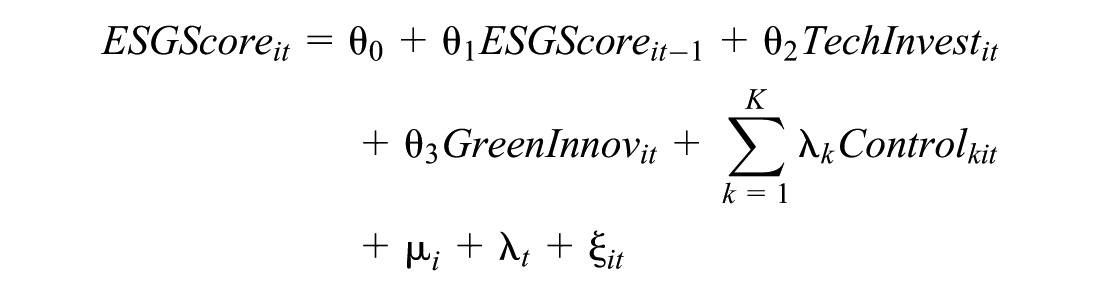

Model 3 - Simultaneous impact of digital transformation and green innovation on ESG performance:

Model 3 aims to test the mediating role of

Model Selection and Testing Procedures

Model Estimation

The study initiates with diagnostic procedures including descriptive statistics, correlation matrices, and variance inflation factor (VIF) analysis to assess multicollinearity. Initial model specification employs Pooled Ordinary Least Squares (OLS) as baseline, though this produces biased estimates when unobserved firm-specific heterogeneity correlates with explanatory variables. F-tests determine whether Fixed Effects (FE) models more appropriately control for unobserved firm characteristics (p < .05 supporting FE selection), followed by Hausman tests distinguishing between FE and Random Effects specifications.

Three critical econometric challenges necessitate System Generalized Method of Moments (SGMM) estimation (Arellano & Bover, 1995; Blundell & Bond, 1998) over conventional panel estimators. First, bidirectional causality between digital transformation and ESG performance, where digital capabilities enhance sustainability outcomes while superior ESG performance simultaneously generates organizational slack and reputational capital incentivizing digital investment, violates strict exogeneity (E[εit|Xit] ≠ 0), rendering OLS and FE estimators biased. Second, inclusion of lagged dependent variables (ESGScorei,t−1), theoretically justified by ESG performance persistence, introduces dynamic panel bias (Nickell, 1981). In short panels (T = 6 years), Fixed Effects’ within-group transformation induces correlation between transformed lagged variables and transformed errors, producing downward-biased autoregressive coefficients persisting asymptotically unless T→∞. Third, the mediating variable (GreenInnov) exhibits potential endogeneity to both TechInvest and ESGScore, creating simultaneous equation systems where standard single-equation estimators yield inconsistent results.

SGMM addresses these challenges by instrumenting endogenous regressors using deeper lags uncorrelated with current errors but correlated with endogenous regressors, satisfying instrument relevance and exclusion restrictions. The estimator combines moment conditions from differenced equations (utilizing lagged levels as instruments) and levels equations (utilizing lagged differences), improving efficiency and mitigating weak instrument problems relative to difference GMM while permitting heteroskedasticity and autocorrelation through orthogonality conditions.

Instrument validity undergoes rigorous assessment through specification tests. Arellano-Bond tests examine whether differenced residuals exhibit second-order serial correlation; AR(1) rejection confirms expected negative first-order correlation while AR(2) non-rejection validates moment conditions. Hansen J-tests of overidentifying restrictions evaluate whether instrument sets satisfy orthogonality conditions (p > .10 indicating validity). Following Roodman (2009), instrument reduction techniques (limiting lag depth to orders 2–4 and collapsing instrument matrices) mitigate proliferation risks that can overfit endogenous variables and weaken Hansen test power in finite samples.

Mediation Analysis Using Bootstrap Method

To test the mediating role of GreenInnov in the relationship between TechInvest and ESGScore, beyond fully estimating models 1, 2, and 3 above, the study additionally applies the bootstrap mediation method (Hayes, 2018; Preacher & Hayes, 2008): Bootstrap is performed with 1,000 resampling iterations with replacement by enterprise clusters (cluster bootstrap) to ensure independence between observations. The indirect effect is calculated as the product of the coefficients of TechInvest’s impact on GreenInnov and GreenInnov ’s impact on ESGScore. The 95% confidence interval of the indirect effect is determined from the bootstrap distribution; if the confidence interval does not contain 0, the mediating effect is statistically significant.

Research Results

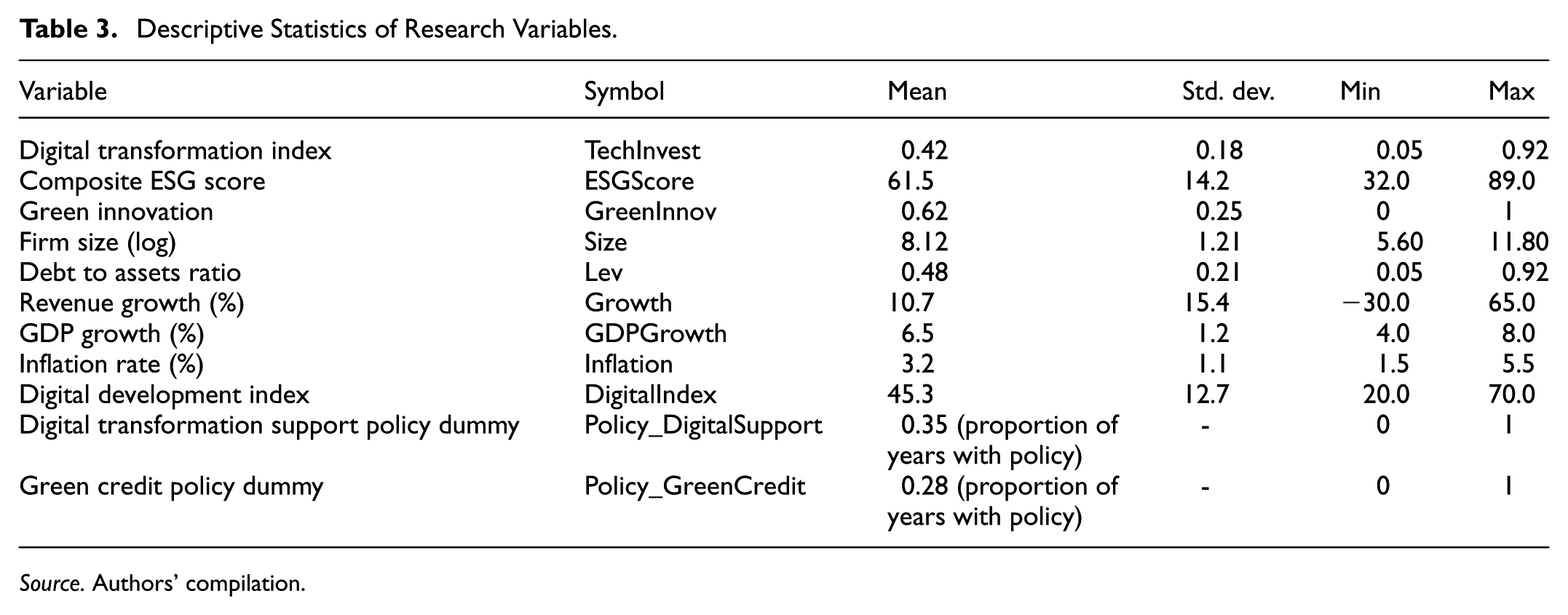

Descriptive Statistics

The descriptive statistical analysis (Table 3) reveals that the main variables in the model exhibit reasonable distributions, accurately reflecting the current state of digital transformation, green innovation, and ESG performance among Vietnamese enterprises. Notably, digital transformation and green innovation levels retain substantial development potential, while macroeconomic factors and supportive policies are gradually being enhanced, establishing a foundation for future sustainable development.

Descriptive Statistics of Research Variables.

Source. Authors’ compilation.

The average digital transformation index of 0.42 on a 0 to 1 scale indicates that digital transformation levels among listed Vietnamese enterprises remain at a low-moderate level, reflecting substantial scope for enhancing digitalization capabilities in the future. The average ESG score of 61.5/100 demonstrates that enterprises have achieved notable improvements in sustainable governance, though they remain distant from leading international standards, particularly in environmental and social domains. Green innovation averages 0.62, indicating limited green innovation action index, reflecting the early stage of green innovation in Vietnam. Average firm size at 8.12 (log total assets) corresponds to medium and large enterprises, consistent with the listed enterprise sample. Average financial leverage of 0.48 indicates moderate debt utilization in capital structure. Revenue growth exhibits high standard deviation (15.4%), reflecting substantial volatility across enterprises and time periods. Macroeconomic variables such as GDPGrowth and Inflation remain within stable ranges, consistent with Vietnam’s economic context during the study period. The average digital development index of 45.3 indicates Vietnam is undergoing digital economic development with substantial growth potential. Policy variables show relatively low proportions of years with policies (approximately 28%–35%), reflecting that digital transformation support and green credit policies have only been implemented in recent years.

Regression Results

The empirical analysis employs System GMM estimation to address endogeneity concerns and dynamic panel bias inherent in the digital transformation-ESG relationship. Formal model selection proceeds through sequential specification tests. The F-test for fixed effects strongly rejects the null hypothesis of zero firm-specific intercepts (F = 12.47, p < .001), confirming significant unobserved firm heterogeneity rendering Pooled OLS inappropriate. The Hausman specification test evaluates Random Effects orthogonality assumptions by testing whether coefficients differ systematically between Fixed Effects (consistent under both hypotheses) and Random Effects (efficient under null only) estimators. The test statistic (χ2 = 43.82, df = 8, p < .001) strongly rejects orthogonality, indicating time-invariant firm effects correlate with regressors (E[μi|Xit] ≠ 0), violating Random Effects identifying assumptions and necessitating Fixed Effects estimation.

Endogeneity testing employs the Durbin-Wu-Hausman augmented regression approach, instrumenting potentially endogenous regressors with second and third lags. The test statistic (F = 8.34, p = .003) strongly rejects exogeneity, with supplementary tests identifying TechInvest (t = 2.91, p = .004) and GreenInnov (t = 2.34, p = .020) as endogeneity sources while control variables exhibit no evidence thereof (p > .10). These findings validate theoretical expectations of simultaneity and justify instrumental variable approaches. Given dynamic panel bias from lagged dependent variable inclusion, System GMM represents the appropriate estimator, simultaneously addressing endogeneity, dynamics, and unobserved heterogeneity through combined differenced and levels moment conditions.

Post-estimation diagnostics confirm SGMM specification validity. Hansen J-statistics testing overidentifying restrictions yield: Model 1 (χ2 = 47.32, df = 52, p = .653), Model 2 (χ2 = 38.17, df = 45, p = .741), Model 3 (χ2 = 51.88, df = 58, p = .697). These moderate p-values indicate instrument validity without suspicious weakness. Arellano-Bond tests yield expected results: significant AR(1) statistics (z = −3.42, p = .001) confirm mechanically induced first-order autocorrelation in differenced residuals, while AR(2) tests fail to reject no second-order autocorrelation (p > .147 across models), validating that instruments dated t-2 and earlier satisfy moment conditions. Instrument counts (45–58) remain substantially below panel units (N = 400), satisfying guidelines against overfitting.

Control variables demonstrate theoretically consistent patterns. Firm size exhibits positive significant effects, reflecting superior resource capacity for ESG investment consistent with Vietnamese reporting patterns. Leverage (Lev) demonstrates negative significant impact, indicating financial pressure constrains ESG investment particularly among SMEs facing green capital access challenges. Revenue growth (Growth) shows positive significance, suggesting well-performing enterprises leverage sustainable development advantages. Industry dummies indicate sector-specific ESG implementation heterogeneity, particularly in renewable energy and technology sectors. Macroeconomic variables (GDP growth, inflation) demonstrate expected directional effects, while policy support variables (Policy_DigitalSupport, green credit) exhibit positive impacts, though significance varies, reflecting implementation constraints particularly affecting SME access.

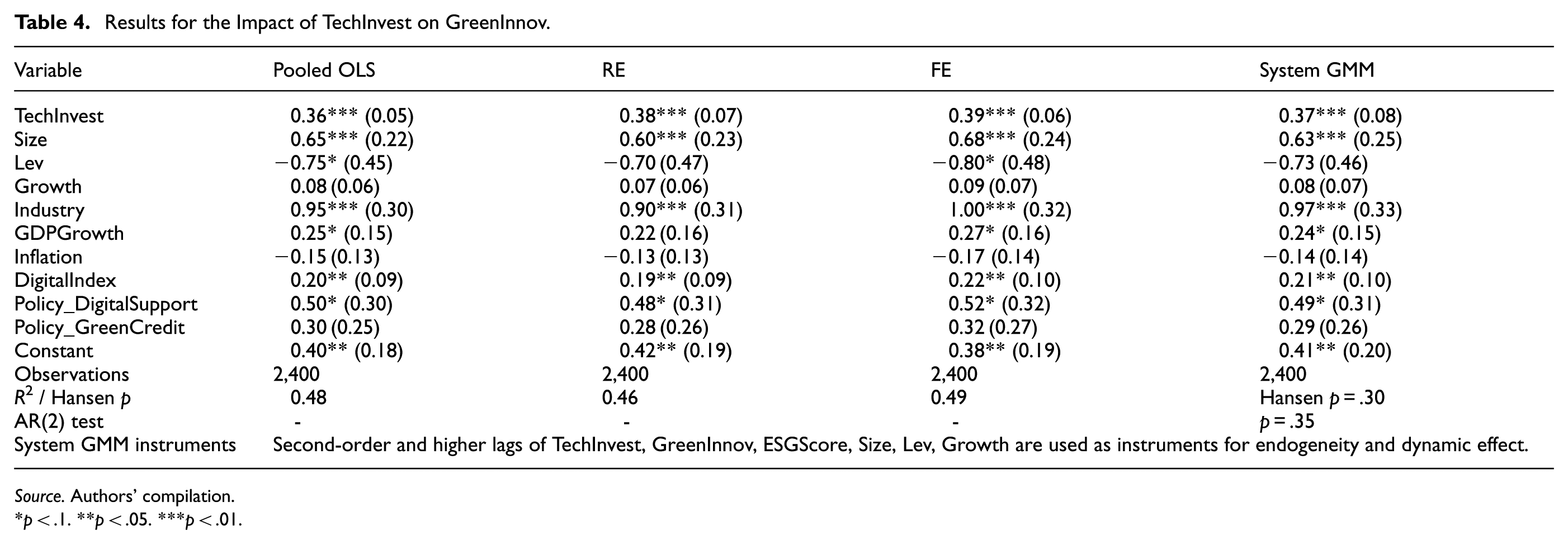

The results presented in Table 4 demonstrate that digital transformation (TechInvest) exerts a positive and statistically significant impact (p < .01) on green innovation (GreenInnov), with a coefficient of .37, indicating that a 1-unit increase in the digital transformation index corresponds to a 0.37 -unit increase in the Green Innovation Action Index. Given the index’s [0,1] normalization, this effect size is substantively meaningful, suggesting that enterprises with more advanced digital capabilities demonstrate significantly broader engagement in green innovation activities across R&D investment, process improvements, and product development dimensions. This finding aligns with Vietnamese practice, where enterprises such as FPT and Viettel employ AI and IoT technologies to develop green solutions, including emission monitoring systems and energy optimization platforms. The substantive magnitude of this coefficient reflects both the enabling role of digital technologies in facilitating diverse green innovation activities and the reality that Vietnam’s green innovation landscape encompasses a broader spectrum of activities beyond formal patenting—including process improvements, organizational adaptations, and incremental sustainability enhancements captured by our disclosure-based measurement approach.

Results for the Impact of TechInvest on GreenInnov.

Source. Authors’ compilation.

p < .1. **p < .05. ***p < .01.

Among control variables, Size and Industry demonstrate robust impacts, indicating that large enterprises and technology sectors possess comparative advantages in green innovation. Conversely, Lev, Growth, Inflation, and Policy_GreenCredit exhibit no statistical significance, partially reflecting the reality that debt pressure, short-term growth, inflation, and green credit policies have yet to substantially influence green innovation in Vietnam. GDPGrowth, DigitalIndex, and Policy_DigitalSupport demonstrate modest positive impacts, consistent with the favorable economic environment and digitalization policies.

These results reinforce the mediating role of GreenInnov in the relationship between digital transformation and ESG performance. Digital transformation enables enterprises to monitor, evaluate, and adjust emission reduction activities in real-time while optimizing production costs and environmental processing, thereby creating distinct competitive advantages. Particularly, digital transformation enhances flexibility in social and corporate governance, strengthening internal connectivity and improving operational efficiency. However, the extent of digital transformation’s impact on green innovation depends on firm size and industry characteristics, as well as support from digitalization and green credit policies. Therefore, enterprises should prioritize digital transformation investment as a foundational strategy to promote green innovation while coordinating with supportive policies to maximize sustainable development effectiveness within increasingly intense international integration and competition contexts.

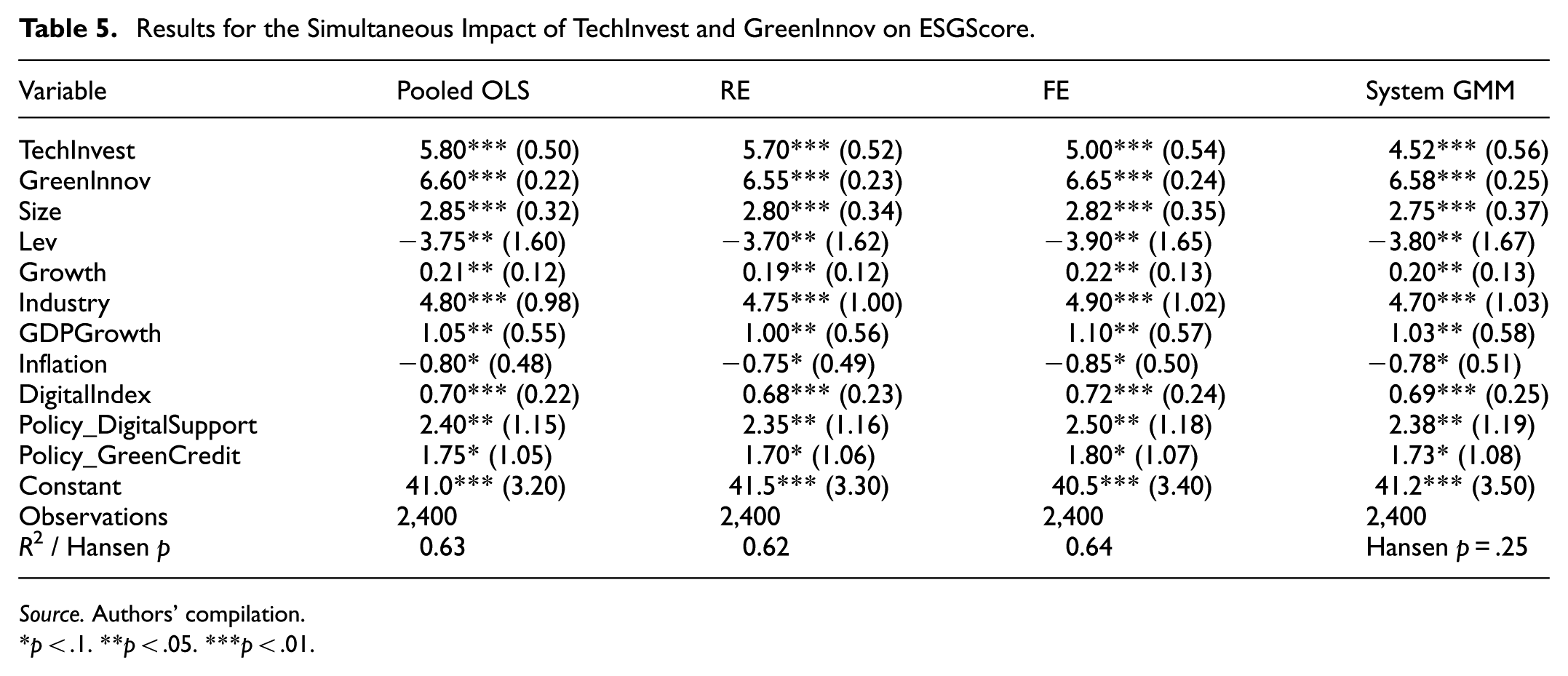

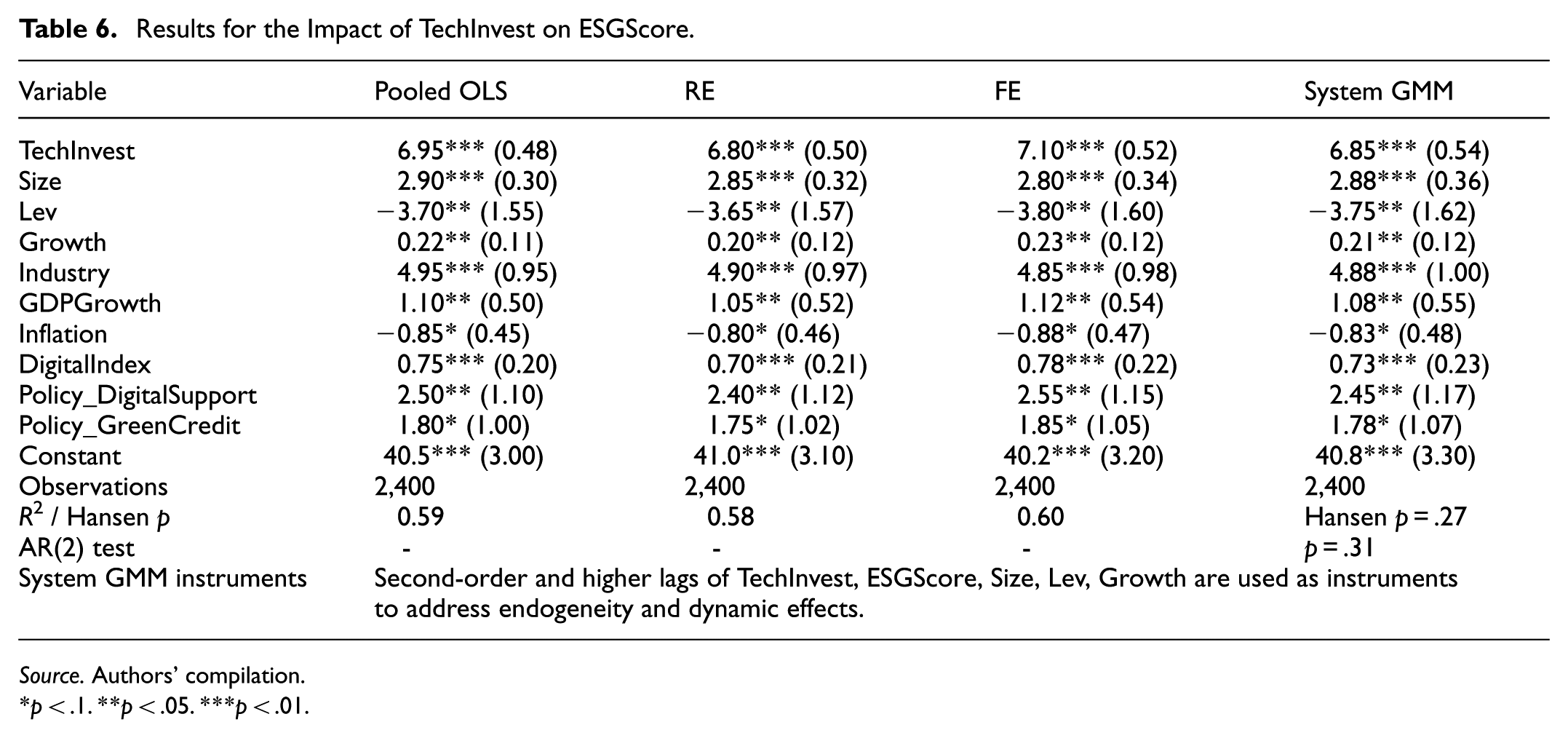

Firm fixed effects (μi) and year fixed effects (λt) are included in all specifications. In this mediation model, the direct effect of TechInvest on ESGScore (β2 = 4.52, p < .01) remains substantial even after controlling for GreenInnov, indicating partial mediation rather than full mediation. The coefficient on GreenInnov (β3 = 6.58, p < .01) indicates that a full transition from minimum to maximum on the Green Innovation Action Index is associated with a 6.58-point improvement in ESG performance. The indirect effect of digital transformation on ESG performance through green innovation can be calculated as: β1(Table 4) × β3(Table 5) = 0.37 × 6.58 = 2.43 points. Combined with the direct effect (4.52), the total effect of TechInvest on ESGScore is approximately 6.95 points (5.75 + 2.43), which aligns with the total effect estimated in Table 6 (β1 = 6.85), confirming the internal consistency of the mediation pathway.

Results for the Simultaneous Impact of TechInvest and GreenInnov on ESGScore.

Source. Authors’ compilation.

p < .1. **p < .05. ***p < .01.

Results for the Impact of TechInvest on ESGScore.

Source. Authors’ compilation.

p < .1. **p < .05. ***p < .01.

Model 3 results demonstrate that both digital transformation (TechInvest) and green innovation (GreenInnov) exert positive and highly statistically significant impacts on enterprise ESG performance. This reflects Vietnam’s practice and sustainable development strategy, where digital and green transformations are viewed as strategic “twins,” playing crucial roles in promoting rapid and sustainable economic growth while transitioning the economy from brown to green. Digital transformation not only creates new resources through data and digital technology but also catalyzes green innovation, helping enterprises optimize production processes, reduce emissions, and enhance ESG governance effectiveness. Green innovation plays an important mediating role, helping digital transformation translate into more concrete sustainable development outcomes, aligning with international commitments and Vietnam’s development orientation. These results also emphasize the role of digital transformation support and green credit policies in creating favorable conditions for enterprises to invest in green innovation and enhance ESG performance. Therefore, enterprises need to synchronously integrate digital transformation and green innovation into development strategies while closely coordinating with national policies to maximize resources and sustainable development opportunities within increasingly extensive international integration contexts.

The mediation test results for green innovation (GreenInnov) in the relationship between digital transformation (TechInvest) and ESG performance are conducted using the bootstrap method (Table 7), a popular non-parametric statistical technique for assessing the reliability and statistical significance of estimated coefficients. Bootstrap results indicate that the indirect effect of TechInvest through GreenInnov on ESGScore has a positive estimated coefficient with a 95% confidence interval not containing 0, and a very small p-value, demonstrating high statistical significance for this effect. This confirms the important mediating role of green innovation, meaning digital transformation not only directly impacts but also indirectly enhances ESG performance through promoting green innovation. This result aligns with theory and practice when green innovation is considered the bridge transforming digital resources into sustainable, environmentally friendly solutions. Bootstrap utilization also enhances conclusion reliability, avoiding bias from normal distribution assumptions or small samples. Therefore, the research recommends that enterprises and policymakers should simultaneously focus on promoting digital transformation and green innovation to optimize sustainable development effectiveness.

Bootstrap Mediation Analysis Results.

Source. Authors’ calculation.

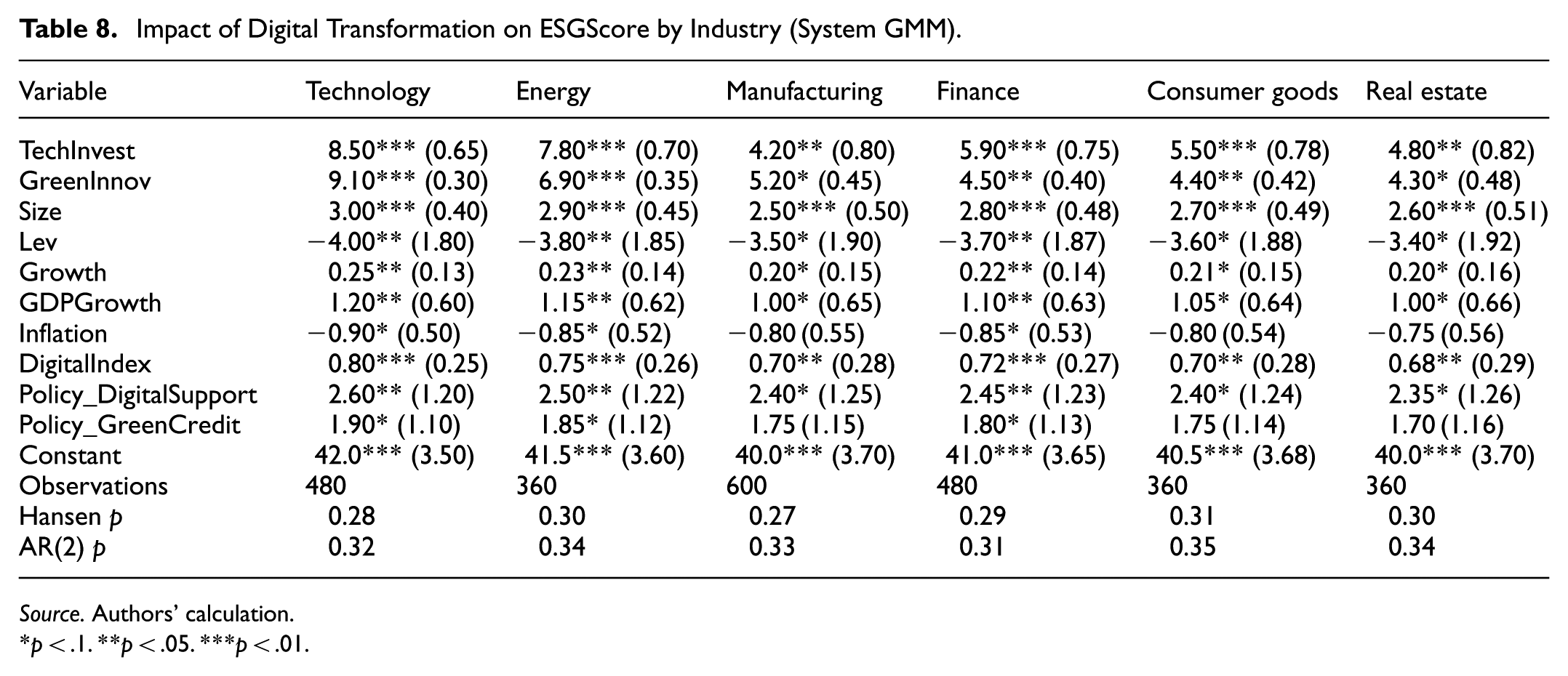

To elucidate the differential impact of digital transformation on ESG performance across industries, Table 8 presents subsample regressions employing System GMM methodology. Industries are classified according to the Global Industry Classification Standard (GICS), encompassing Technology, Energy, Manufacturing, Finance, Consumer Goods, and Real Estate. Control variables are included, utilizing second-order and higher lags of TechInvest, ESGScore, GreenInnov, Size, Lev, and Growth as instrumental variables.

Impact of Digital Transformation on ESGScore by Industry (System GMM).

Source. Authors’ calculation.

p < .1. **p < .05. ***p < .01.

Firm fixed effects (μi) and year fixed effects (λt) are included in all industry-specific specifications to control for unobserved heterogeneity and temporal shocks. Coefficients represent the effect of a 1 -unit change in the digital transformation and green innovation indices (both scaled [0,1]) on ESG performance (scaled [0,100]) within each industry subsample. The substantial heterogeneity in coefficient magnitudes (ranging from β = 4.20 in Manufacturing to β = 8.50 in Technology) reflects genuine differences in how effectively industries translate digital capabilities into sustainability outcomes, driven by variations in technological absorptive capacity and regulatory intensity. These effect sizes are economically meaningful: based on the sample-wide standard deviation (σ = .18), a one-standard-deviation increase in digital capability generates a 1.53-point ESG improvement in the Technology sector (0.18 × 8.50 = 1.53). This substantially exceeds the corresponding effect in the Manufacturing sector, where an equivalent increase yields only a 0.76-point gain (0.18 × 4.20 ≈ 0.76), highlighting the superior efficiency of digital-ESG integration in knowledge-intensive industries.

The specific sectoral results reveal that the Technology (β = 8.50) and Energy (β = 7.80) sectors demonstrate the highest leverage of digital capabilities, substantially outperforming Finance (β = 5.90), Consumer Goods (β = 5.50), and Real Estate (β = 4.80). This differential reflects the capacity of technology enterprises, such as FPT and Viettel, to natively integrate advanced technologies (including artificial intelligence (AI) and the Internet of Things (IoT))to optimize sustainable processes, encompassing real-time emission monitoring and automated corporate governance. Similarly, energy sector enterprises, particularly within renewable energy domains, deploy digital technologies to directly enhance energy efficiency and mitigate environmental impacts, creating a strong, immediate link between digital inputs and ESG outcomes. Conversely, the Manufacturing sector exhibits the most attenuated digital transformation impact (β = 4.20), potentially attributable to the “heavy” nature of industrial assets. Unlike agile service sectors, manufacturers face high capital costs and physical complexities when retrofitting legacy production lines with digital systems, resulting in a slower translation of digital investments into immediate ESG score improvements (Nguyen and Luong, 2024).

Crucially, the GreenInnov variable demonstrates a similar pattern of sectoral divergence, validating the synergistic relationship between digital capabilities and innovation efficiency. The coefficients in the Technology (β = 9.10) and Energy (β = 6.90) sectors are significantly higher than in Manufacturing (β = 5.20) or Real Estate (β = 4.30). This indicates that green innovation activities translate into ESG performance ratings more efficiently in knowledge-intensive sectors. For a technology firm, a full transition from minimal to maximal green innovation intensity (0–1 on the index) yields an estimated 9.10-point boost in ESG score, nearly double the impact observed in the manufacturing sector (5.20 points). This suggests that green innovations in the technology sector (often manifesting as scalable, low-carbon software solutions or efficiency algorithms) are more readily captured and rewarded by ESG rating frameworks than the complex, capital-intensive process innovations required in heavy manufacturing.

Control variables including Size, Lev, and Growth indicate that firm scale and growth trajectories play instrumental roles in supporting ESG performance across all sectors. Notably, financial leverage (Lev) exerts a consistently negative impact, which is most pronounced in the Technology (β = −4.00) and Energy (β = −3.80) sectors. This suggests that high debt burdens significantly constrain the discretionary financial resources required to execute high-risk, high-reward digital sustainability projects in these capital-intensive industries. These findings underscore the imperative for industry-specific strategies: while technology and energy enterprises benefit from a high “conversion rate” of innovation into ESG performance, traditional sectors such as manufacturing require targeted policy support, including tax incentives and preferential green credit, to overcome structural barriers and enhance the efficiency with which their innovation efforts translate into recognized sustainability outcomes.

Conclusions and Recommendations

Conclusions

This study provides robust empirical evidence regarding the positive relationship between digital transformation and ESG performance among listed enterprises in Vietnam. Through panel data regression models and GMM estimation methodology, the results demonstrate that the composite digital transformation index (TechInvest) exerts a positive, highly statistically significant impact on composite ESG scores, even when controlling for micro, macro, and policy factors. Simultaneously, mediation analysis reveals that green innovation, operationalized through the composite Green Innovation Action Index capturing the breadth of sustainability-oriented innovation activities, serves as a crucial mediating mechanism translating digital capabilities into enhanced ESG performance. This finding clarifies the indirect pathway through which digital transformation generates sustainability outcomes—by enabling more comprehensive engagement across R&D investment, process innovation, and product development dimensions. Beyond technological factors, elements such as firm size, growth rate, economic environment, and policy support also play important roles in promoting ESG. Specifically, enterprises with larger scale, higher revenue growth rates, operating in technology or renewable energy sectors tend to achieve better ESG scores. Support policies such as digital transformation incentives and green credit also contribute to enhanced ESG performance within contexts of integration and increasingly intense competition. The research results not only confirm the strategic role of digital transformation in sustainable development but also contribute to refining the theoretical framework regarding the bidirectional impact between digitalization and ESG, while suggesting practical approaches for integrating ESG into Vietnamese enterprises’ digitalization strategies.

Recommendations

For Enterprises: Strategic Integration of Digital Capabilities and Sustainability Outcomes

Vietnamese enterprises should prioritize integrated ESG management systems featuring automated disclosure capabilities aligned with Vietnam’s emerging regulatory frameworks. Rather than maintaining fragmented reporting systems, firms should adopt interoperable platforms compatible with the State Securities Commission’s anticipated 2025 ESG disclosure standards and capable of interfacing with both domestic reporting portals and international rating agencies’ data collection protocols. This integration addresses the prohibitive costs SMEs face in managing multiple stakeholder-specific reporting requirements while positioning enterprises favorably for forthcoming regulatory mandates.

Given Vietnam’s nascent patent infrastructure and the reality that green patents constitute less than 0.2% of national innovation output, enterprises should redirect innovation resources toward comprehensive documentation and disclosure of green innovation activities in annual reports and supplementary sustainability communications. This disclosure-intensive strategy aligns with empirical evidence demonstrating that documentation-based innovation metrics more strongly predict ESG performance than patent counts in the Vietnamese institutional context. Operationally, firms should establish structured protocols capturing environmental R&D expenditures, cleaner production initiatives with quantified impact metrics, and eco-product developments with market performance indicators.

Beyond internal ESG management, enterprises should leverage digital platforms for proactive stakeholder-facing ESG transparency, addressing information asymmetries that systematically depress emerging market firms’ ESG ratings. Strategic deployment of blockchain-verified supply chain systems, real-time environmental performance dashboards, and AI-enabled stakeholder engagement platforms provides cost-effective mechanisms for demonstrating sustainability commitments, particularly critical for export-oriented sectors facing intensified international ESG scrutiny.

For Government and Policy-Making Agencies: Institutional Infrastructure for Digital-Sustainability Synergies

The State Securities Commission should implement comprehensive ESG disclosure requirements mandating digital submission through standardized protocols enabling automated aggregation and public dissemination. This regulatory architecture simultaneously creates institutional pressure for ESG improvement while reducing compliance costs through standardization. A phased implementation, targeting the largest 100 enterprises initially, expanding to all listed firms by 2027, acknowledges differential resource constraints while ensuring progressive market coverage. Coordination between the Ministry of Natural Resources and Environment and SSC remains essential to eliminate duplicative reporting burdens.

Rather than maintaining fragmented incentive structures, Vietnam should develop integrated financial instruments explicitly conditioning tax credits and preferential lending on demonstrated ESG outcome improvements attributable to digital-green investments. A performance-based tiered corporate income tax credit system, with reductions calibrated to composite ESG score improvements coupled with digital investment increases, addresses moral hazard inherent in existing programs that reward announced investments regardless of sustainability outcomes. The State Bank of Vietnam should condition preferential green credit rates on integration of digital monitoring systems, ensuring transparency in green credit deployment.

Recognizing that SMEs lack internal capacity for sophisticated ESG management, the government should support shared service platforms providing subsidized ESG technology and consulting services. Regional ESG Technology Centers, established through public-private partnerships in key industrial zones, should provide access to ESG software platforms, training programs, green innovation documentation support, and facilitation of university-enterprise research collaboration, effectively democratizing ESG capabilities beyond large corporations.

For Investors and Financial Institutions: Risk-Adjusted ESG-Digital Assessment Frameworks

International investors should develop Vietnam-specific ESG evaluation methodologies accounting for disclosure maturity trajectories and digital capability indicators, recognizing that standardized ratings systematically underestimate emerging market firms due to disclosure gaps and Western-centric criteria. Supplementing third-party ratings with proprietary frameworks incorporating digital infrastructure quality indicators, disclosure trajectory analysis, and green innovation intensity metrics enables identification of ESG improvers, which are firms with nascent sustainability performance but strong digital capabilities positioning them for rapid advancement.

Financial institutions should structure sustainability-linked instruments coupling digital transformation milestones with ESG outcome improvements. Dual key performance indicators (annual ESG score improvement and digital ESG management system implementation) with interest rate adjustments create tangible incentives for synchronized digital-ESG investment. Institutional investors should exercise shareholder voice advocating for board-level ESG oversight integrated with digital transformation governance, addressing root causes of weak ESG performance through structural governance reform rather than merely monitoring outcomes.

Footnotes

Ethical Considerations

This study is based on secondary financial and non-financial data from publicly listed companies, as well as publicly available macroeconomic data. All firm-level data were anonymized. As the research did not involve human or animal subjects, ethical approval from an institutional review board was not required.

Consent to Participate

Not applicable. This study does not involve human participants.

Consent for Publication

Not applicable. This study does not contain any individual person’s data in any form.

Author Contributions

Vu Hiep Hoang: Conceptualization, Methodology, Validation, Project administration, Formal analysis, Data Curation, Writing – Original Draft.

Anh Tuyet Nguyen (Corresponding Author): Conceptualization, Methodology, Data processing, Software, Writing – Review & Editing.

Thi Thanh Huyen Nguyen: Investigation, Data Curation, Writing – Review & Editing.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated and analyzed during the current study are available from the corresponding author upon reasonable request. Portions of the raw data were sourced from proprietary databases (including Sustainalytics, Refinitiv, and FiinPro) and are subject to the licensing agreements of those providers. Processed data required to replicate the study’s findings can be made available by the authors.