Abstract

Debt management is crucial to achieving financial well-being among young employees, particularly as they enter the workforce. With rising living costs, student loans, and easy access to credit, young employees need to handle debt effectively. Thus, this study examines how young employees understand and manage debt by analysing the learning process that shapes financial literacy and behavioural indicators influencing personal financial management capabilities. A qualitative research design was employed, utilising purposive sampling, which involved semi-structured interviews with six young employees from one of the economically underdeveloped states in Malaysia. The data were analysed through a thematic synthesis approach, supported by NVivo. Consequently, two major themes emerged, namely learning in financial literacy through both formal and informal channels, and financial literacy indicators that influence debt management practices, including budgeting behaviour, credit awareness, self-control and use of digital financial tools. Accordingly, the findings emphasise the critical role of digital and experiential learning in shaping financial capability among young employees in less economically developed regions. Also, this study contributes contextual insights into the micro-processes of financial literacy among Malaysian young employees and offers policy recommendations for enhancing financial education and digital interventions.

Introduction

Young Malaysian employees, particularly those in the early stages of their careers, face significant financial challenges due to limited financial literacy and ineffective debt management practices (Awanis & Chi Cui, 2014; Mad et al., 2024). These structural conditions combine with rising living costs, stagnant wage growth, easy access to credit, and poor financial decisions at an early career stage can have long-term consequences, affecting major life aspirations such as homeownership, education, and retirement savings (Park, 2021). Globally, youths are recognised as a financially vulnerable group due to limited work experience (Lusardi & Messy, 2023). Many young workers are employed in socioeconomic environments characterised by low average income and scarcity of financial education (Loke, 2016; Dwivedi et al., 2021).

For the record, young population in this study refers to the generation definition made by Beresford Research (2025), comprising younger Millennials (Gen Y) who were born between 1995 and 1996 whereas Gen Z are those who were born between 1997 and 2007. Empirical evidence shows that Malaysian youths disproportionately struggle with budgeting, impulsive spending, high-interest credit and limited exposure to formal final education. The statistics from the Malaysian Department of Insolvency revealed that there are 33,388 cases on bankruptcy for period from 2019 until February 2023, and 6,361 cases or 19.05% of them are presented by young adults (Abdullah & Shukor, 2024).

However, existing research predominantly focuses on the urban population or employs quantitative approaches. Thus, leaving a gap in understanding how young employees interpret and manage their debt in everyday life (Institute of Labour Market Information and Analysis, 2017). Furthermore, the lack of understanding of financial literacy programmes during early employment contributes to poor debt management practice, indebtedness with high-interest loans and impulsive spending behaviours (Hamid & Loke, 2021). This behaviour can disrupt common life goals, especially home ownership, education and retirement planning.

Addressing these challenges requires a nuanced understanding of financial management, habits, and external factors influencing financial behaviour. Despite the availability of digital financial tools such as budgeting apps and fintech solutions, their effectiveness is limited when financial education is lacking (Kass-Hanna et al., 2022; Yang et al., 2023). Moreover, limited research explores youth financial behaviour in economically less diversified states such as Kelantan, one of the states in Malaysia, where income, opportunities, and financial exposures differ from the urban context (Zain et al., 2024).

Therefore, this exploratory study aims to fill this gap by examining how young employees in Kelantan understand and manage debt, focusing on the learning process that shapes their financial literacy and the indicators influencing their financial decisions.

Literature Review

To establish the conceptual basis for this study, this section synthesises previous relevant literature.

Financial Literacy and Debt Management

Numerous definitions of financial literacy exist, but the most lucid and comprehensive is provided by the Organisation for Economic Co-operation and Development (OECD). Financial literacy encompasses the awareness, information, skills, attitudes, and behaviours essential for making informed financial decisions and attaining personal financial well-being (OECD, 2020). Those equipped with financial decision-making skills typically demonstrate high confidence in budgeting, managing debt, and financial planning (Carpena & Zia, 2020). Lusardi and Messy (2023) emphasise that financially literate young adults may have positive long-term implications for their financial well-being, including career development, mortgage security, and retirement security.

Recent global studies further highlight the psychological mechanisms relating literacy to financial well-being. For example. Mitra and De (2024) demonstrate that financial self-efficacy partially mediates the relationship between financial literacy and the overall satisfaction of rural households with lower incomes, both directly and indirectly. In the Malaysian context, past literature reveals that many studies show young workers struggle with debt management, controlling spending, and understanding financial products (Masrom et al., 2022; Pahlevan et al., 2020). Financial literacy remains consistently imbalanced, especially between urban and rural regions, contributing to persistent debt challenges (Czech et al., 2024).

Behavioral Influences and Theoretical Foundation

It should be noted that behavioural factors also significantly influence financial decision-making. The Theory of Planned Behaviour (TPB) provides a useful insight into understanding how debt-related actions are influenced by attitudes toward borrowing and saving. Meanwhile, subjective norms, including peer pressure or family expectations, are posited as having the strongest influence (Boonroungrut & Huang, 2021; Johan, 2018; Renanita, 2013; Xiao & Wu, 2008). In addition, perceived behavioural control, reflected in financial confidence and self-control, affects an individual’s ability to regulate spending and manage debt effectively, thereby influencing whether financial intentions are successfully translated into actual behaviour(Johan et al., 2020).

Similarly, self-control, impulsivity, and financial self-efficacy are vital in determining whether individuals manage debt effectively or fall into financial distress (Boonroungrut et al., 2020). As a result, individuals with high financial self-efficacy are more likely to adopt proactive financial strategies and avoid excessive borrowing (Jumady et al., 2024). These behavioural frameworks directly link to the study’s aim, including financial literacy indicators and debt management attitude.

Socioeconomic Determinants of Debt Behaviour

Debt management is also influenced by socioeconomic factors, including access to financial resources, job stability, and income levels (Fitch et al., 2011; Lee & Mori, 2021). Economic instability, conversely, exacerbates debt problems, leading to increased financial stress and a decline in confidence in financial judgment (Cwynar et al., 2019; Pérez-Roa & Ayala, 2020). On the contrary, better financial decisions resulted from perceived behavioural control is enhanced by stable employment and income (Abdullah et al., 2019; Cloutier & Roy, 2020).

Family and peer pressure also influence financial habits. According to studies, people are more likely to adopt sound financial practices around peers and family who are financially responsible (Mohd Alwi et al., 2023). On the other hand, financial strains and social pressures could encourage careless borrowing and excessive spending (Hassan et al., 2018).

Digital Financial Tools and Informal Learning

The rise of digital platforms, such as YouTube, Instagram, and TikTok, has been phenomenal, transforming financial learning among young people. Fintech applications, for example, budgeting apps and e-wallets, help a lot for them to facilitate daily financial management (Kass-Hanna et al., 2022). Many young employees particularly Gen Z easily integrate digital financial tools into their routines (Alaeddin et al., 2018; Nwoke, 2025). Thus, this informal digital learning environment aligns strongly with the study’s findings and reflects a broader global trend, especially in financial activities and development.

Research Methodology

Research Design and Sampling Strategy

A purposive sampling method was employed to gain in-depth insights into understanding debt management among young employees in Kelantan, specifically those aged 18-30 (Rey-Ares et al., 2021). Informants from various backgrounds were interviewed. The informants met the study criteria, which included at least holding a bachelor’s degree, employment in any sector, work experience, and residency in Kelantan. Kelantan was selected because the diverse socioeconomic background is strategic, providing fertile ground for exploring varied perspectives on debt management, especially from one of Malaysia’s least developed states with a low composite development index (CDI) (Yusof & Kalirajan, 2021).

To broaden informants’ access, snowball sampling, involving six informants, was applied as shown in Table 1, where existing informants recommended additional informants. Although small, the sample is suitable for exploratory qualitative research that focuses on depth rather than generalizability. Additionally, a survey of various sites found that six or fewer interviews were sufficient to identify common themes with relatively homogeneous groups (Hagaman & Wutich, 2017). On top of that, this aligns with qualitative methodological literature, which states that thematic saturation can occur within six to 12 interviews for homogeneous groups (Constantinou et al., 2017). The point of view is that data saturation (mainly for validity purposes) is rooted in a qualitative research background (Alam, 2020). Hence, for this study, evidence was observed after the sixth interview, where no new codes or insights emerged.

List of Informants.

Data Collection

Data were collected through semi-structured interviews, which lasted between 15 and 20 minutes. The interview guide was developed based on a thorough review of existing literature on financial behaviour and debt management, ensuring relevance and alignment with the study’s objective (Biplob et al., 2022).

The interview content included understanding debt and financial responsibilities, as well as sources of financial knowledge. In addition, the informants were asked about their experiences with budgeting, credit, and, lastly, the challenges they faced in debt management. All interviews were audio-recorded, and participation was voluntary with all informants provided informed consent. Confidentiality was maintained in accordance, and their identities would not be revealed in any publication as per Malaysia’s Personal Data Protection Act 2013 and audio files were stored securely (Yan Ping, 2021).

Data Analysis

This study applies the steps checklist by Cruzes and Dyba (2011), who proposed to perform a thematic analysis. The checklist is made up of five steps (as described in Figure 1); commencing with the initial reading and familiarization with interview transcripts (extraction), identification of meaning unit in specific segments across all transcripts, labelling of segments of text (coding), translation of codes into themes, and creation of the model and assessment of the model's trustworthiness (Cruzes et al., 2015).

Thematic synthesis process adapted from Cruzes and Dyba (2011).

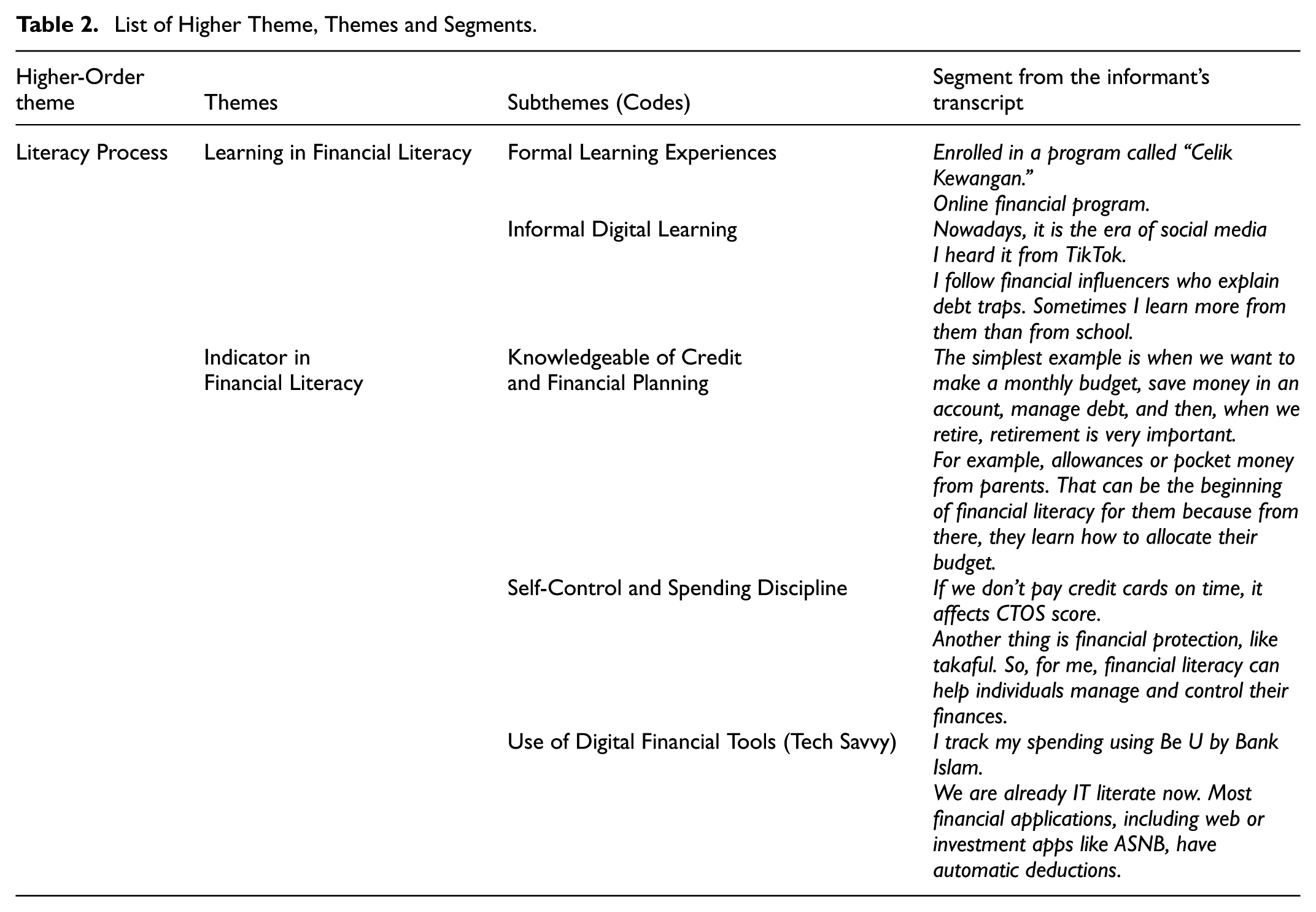

The reading and data extraction contained transcripts of interviews with informants. This study utilised NVivo 14 software, which identified the text containing insights into debt management in the transcript. Similarly, during the coding process, as illustrated in Figure 1, a total of 11 text segments were extracted. Two themes were abstracted after considering the commonalities and differences in the segment’s quotation, as per Table 2. For each theme, the possible repetition of meaning from respective informants was retrieved (Alam, 2020). The meaning and the quotes from these segments were all related to the more abstract concept of understanding debt management among young employees.

List of Higher Theme, Themes and Segments.

To reduce researchers’ bias and enhance credibility, this study employed peer debriefing with another researcher to review part of the coding. At the same time, the researcher documents all coding decisions in NVivo to ensure an audit trail is in place. Furthermore, this research includes direct quotations in findings to preserve informant’s voice (Lim, 2025). Thus, these steps strengthen the reliability and transparency of the results.

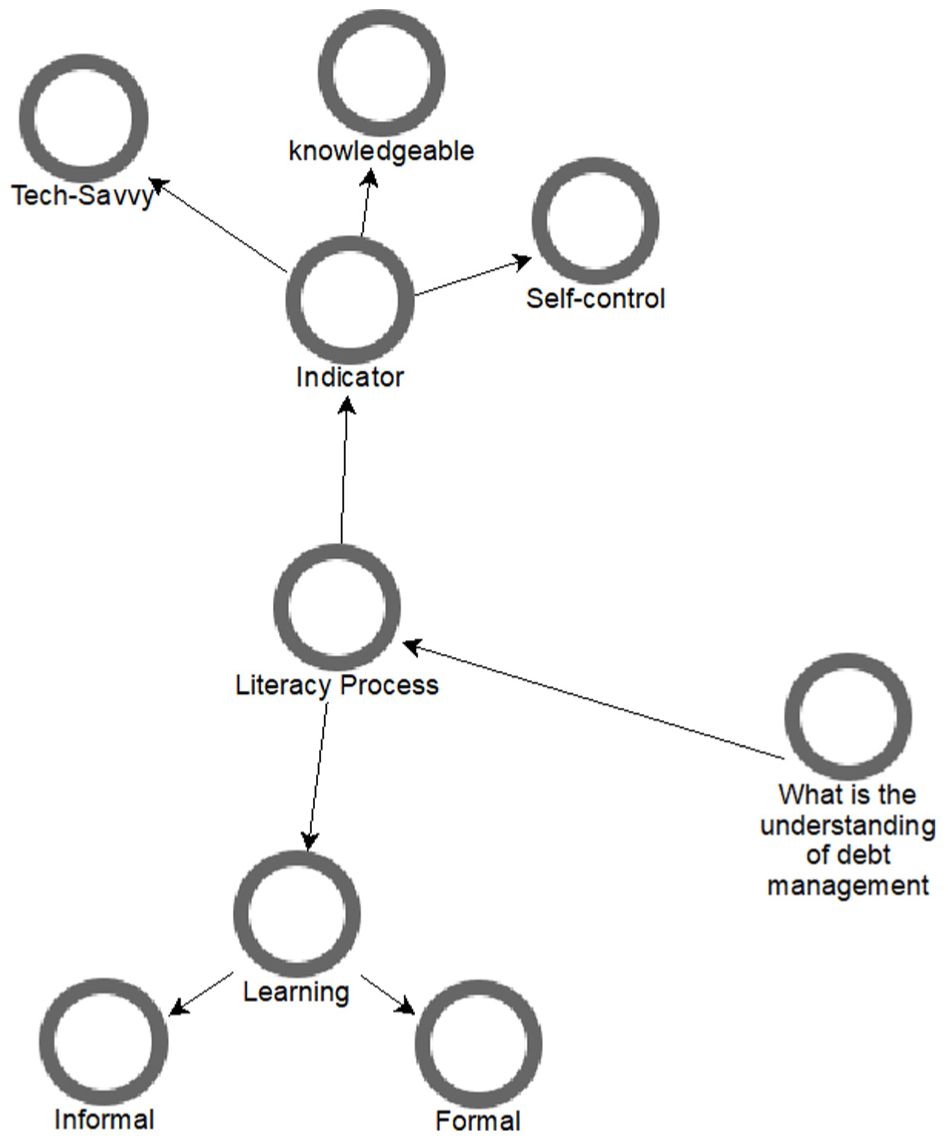

Finally, a higher-order theme model is developed that maps into two themes related to the literacy process in debt management. The final model map is shown in Figure 2. The strength of the conclusion is based on the times mentioned by the informants in the interviews.

Concept model from the thematic synthesis.

Findings

In this section, the study provides answers to the research question, which aims to synthesise the understanding of debt management among young employees. The thematic synthesis method produced a connection in Figure 2 between the higher theme, themes and subthemes in debt management. Furthermore, the empirical data indicate that two major themes reflect how young employees in Kelantan understand and manage debt. These themes closely relate to the research question and illustrate the interplay between the learning process, behavioural- indicators, and personal financial decision making. The themes are learning in financial literacy and financial literacy indicators.

Each theme is presented purely from empirical data, further with example quotes as follows:

Theme 1: Learning in Financial Literacy

Informants described financial literacy as a continuous learning process shaped by formal and informal learning environments. As shown by empirical data, this study found that exposure occurred in institutional or workplace programmes. Meanwhile, informal digital platforms played a significant role in shaping financial understanding.

Formal Learning Experiences

Some informants reported attending financial literacy programmes at school, university, and workplace settings learning context. These structured programmes introduced budgeting, the credit concept and strategies for avoiding bad debt.

That officer once conducted a program called “Celik Kewangan.” He speaks to us about financial literacy, but only does it online. So, when I joined that program, there was indeed a lot of input from well-known individuals, and bank representatives also shared their experiences with debt management, including those who don't pay their debts, among many others.

These platforms deliver accessible and engaging content, making financial understanding more widespread among younger audiences. Nevertheless, they are often criticised for providing only surface-level exposure.

Informal Digital Learning

These environments underscore learning beyond traditional classroom settings, with modern activities taking place in the digital realm, where platforms like TikTok, Instagram, and YouTube serve as substantial sources of financial knowledge.

Nowadays, right… it is the era of social media. So, we can use platforms like Instagram, TikTok, and YouTube to spread information about financial literacy.

“I follow financial influencers who explain debt traps. Sometimes I learn more from them than from school.”

These findings align with the profile of Gen Z and younger Millennials (Gen Y), who are actively consuming and creating digital content. For many, digital platforms functioned as daily micro-learning spaces where they gained awareness of budgeting, credit scores, and the implications of overspending.

On the other hand, informants also acknowledge the influence of their parents and family in shaping saving and expense habits, even though this can vary depending on a household's financial practices.

Having financial resources in the form of, for example, allowances or pocket money from parents. That can be the beginning of financial literacy for them because from there, they learn how to allocate their budget. For example, the food budget, as well as the budget for buying books and so on. That might be the typical budget that we can see for our level.

Overall, Theme 1 highlights that young employees’ financial literacy is not primarily obtained through formal education. Instead, digital microlearning plays a significant role in shaping their financial understanding.

Theme 2: Financial Literacy Indicator

The second theme captures informants’ awareness of financial concepts and the behavioural practices they adopt in managing debt. These indicators reveal how financial literacy manifests in every decision-making.

Knowledgeable of Credit and Financial Planning

Several informants demonstrated awareness of credit-related risks, particularly regarding Credit Tip-Off System (CTOS) scores, interest rate and missed payments. Budgeting also emerged as a common financial management strategy.

This credit thing has its interest, right? Then there's the annual fee. So, even if we don't use it, we will still be charged. If we play with credit, it's a big risk because if we can't pay, it will affect our CTOS, you know. If you know what CTOS is. CTOS is like each person has their own CTOS score. CTOS score is like a monthly commitment, or it's like a merit.

It is knowledge with the skills to manage finances. The simplest example is when we want to make a monthly budget, save money in an account, manage debt, and then, when we retire, retirement is very important. Another consideration is financial protection, such as takaful. For me, financial literacy enables individuals to manage and control their finances, allowing them to create a meticulous budget.

Informants recognised that mismanaging credit would result in restrictions to future financial opportunities, including hire-purchase or mortgage approval.

Self-Control and Spending Discipline

Self-control surfaced as a significant behavioural attribute influencing debt management. The informants acknowledge that impulsive buying and peer influence often disrupted financial plans.

Sometimes I buy things because I see my friends buying them. It’s hard to control.

If I don’t monitor myself, I tend to overspend, especially online shopping, So I set limits on my e-wallet.

Self-regulation was linked to informants’ awareness of consequences and their commitment to avoid financial burdens.

Use of Digital Financial Tools

The majority of the informants used financial apps, either for banking, investment or daily expense management. They claim that these apps provide real-time financial tracking and help with budgeting habits.

So when we get back to reality now, we are already IT literate now. Most financial applications, including web or investment apps like ASNB, have automatic deductions.

I use Be U By Bank Islam if you've ever heard of it, because in Be U By Bank Islam there are budgets, pockets, and it also has microtakaful, so we can save as much money as we want. Like now there are many financial apps, financial management applications, and banking apps like… Bank Islam, and ASNB which can help us manage our finances and at the same time monitor our spending with the presence of apps like these.

Fintech tools are easy to use among knowledgeable users. Thus, their functions are central to promoting responsible financial behaviour among young employees.

Table 3 showcases the summary of themes. These themes show that financial literacy among employees are deeply connected with digital learning, personal attitudes and daily financial practices.

Summary of Themes.

Discussion

This study aimed to explore how young employees in Kelantan understand and manage debt, focusing on the learning process that shapes financial literacy and the indicators influencing financial decisions. The findings show that debt management is not merely a function of financial knowledge, but rather a dynamic interaction between the learning process and certain behavioural attributes.

Financial Literacy as Continuous Learning Process

Financial literacy is defined as the knowledge, skills, and behaviours related to making financial decisions (OECD, 2020). The findings demonstrate that financial literacy among young employees is a lifelong and evolving process, rather than a one-off educational outcome. Various methods of formal learning are conducted in education. Formal financial education programmes provide foundational exposure. For instance, programmes such as the Celik Kewangan Program (Financial Literacy Program) offer valuable insights from financial experts and provide practical strategies to address financial challenges, as well as valuable lessons on managing finances and dealing with debt-related issues (Azmi & Indriyani, 2023). Ultimately, these formal programs are crucial in enhancing young employees' understanding of strategies for effective debt management (Meyers et al., 2013).

Financial literacy is predicated on three essential components which are financial knowledge, financial behaviour, and attitudes towards money (Abdullah et al., 2022). A financially literate individual should possess a fundamental understanding of essential financial matters and the ability to apply specific skills in financial contexts (Pramahender & Kandpal, 2021). Consequently, they must proficiently address enquiries about concepts such as simple and compound interest, risk and return on investments, and the effects of inflation on financial matters.

The informants also relied more heavily on informal digital learning through social media, enabling individuals to access financial information independently of official educational programs, thereby enhancing the accessibility of financial education to a broader audience (Shi et al., 2025). The study’s findings underscore that these platforms provide accessible and compelling material to facilitate financial management for younger users. Thus, this reflects a generational shift in learning preferences, particularly among Gen Z and younger Millennials (Gen Y), who favour short-term and experience-based context (Laia & Palupiningtyas, 2025). In Kelantan context, the structured financial literacy initiatives are limited (Fadzlyn & Muhammad, 2024), thus digital platforms serve as a compensatory learning mechanism. Importantly, this finding extends the existing financial literacy literature, which shows how informal digital learning operates as a primary literacy channel rather than a supplementary one.

Moreover, the findings also demonstrate that financial literacy among young employees is a socially embedded learning process. Consistent with Meyers et al. (2013) informal learning was found to take place within family and workplace, in which individuals participate, where individuals acquire financial understanding through observation, experience and interaction. Furthermore, family support cultivates beneficial financial practices (Azhari et al., 2022), as studies indicate that parents offer financial assistance for entrepreneurial endeavours. In some cases, young employees gain advantages from implementing structured budgeting tactics, such as the 50% – 30% – 20% rule (Arnold & Artz, 2019), and utilising technology, including budgeting applications, to improve financial organisation (Javaid et al., 2022). Taken together, these findings suggest that financial literacy development among young employees is shaped by a complex interaction between family socialisation. Informal learning environments therefore serve not only as a source of financial knowledge but also as a social space where financial behaviour is reinforced and challenged.

Financial Literacy Indicators

The findings indicate that debt management among young employees is shaped by a set of interrelated financial literacy indicators, which include knowledge of credit and financial planning, self-control and use of digital content in financial management. These indicators reflect how financial literacy is defined from the understanding into actual financial behaviour.

The study reveals that informants who have clearer understanding of credit mechanisms such as interest charges, repayment obligation and credit reporting system in Malaysia (CTOS and Central Credit Reference Information System which is operated by Central Bank of Malaysia) are more responsible in managing debt.

Beyond credit awareness, financial planning practices, including budgeting and saving, emerged as a critical indicator of responsible debt management. Debt management is an essential component of the financial well-being of young employees (Lusardi & Messy, 2023). This study emphasises the role of financial education and systematic financial planning in promoting prudent debt management. Managing debt is a critical issue for young employees, particularly in the context of Malaysia’s evolving economic landscape. This finding suggests that financial knowledge, when combined with planning behaviour, enhances perceived behaviour control. Hence, it supports prudent financial decision-making.

That is to say, self-control emerged as a significant psychological and behaviour indicator influencing debt management outcomes. The informants acknowledge that impulsive spending and emotional purchases frequently disrupt financial plans. It has been identified as a psychological and attitudinal trait that can influence financial behaviours (Lyons & Kass-Hanna, 2022). A few studies suggest that consumers with higher degrees of self-control are better able to moderate their judgements, regulate their emotions, and resist buying and consumption impulses (Peltier et al., 2016; Rey-Ares et al., 2021).

From a theoretical perspective, self-control corresponds closely to perceived behavioural control within the Theory of Planned Behaviour. Those with stronger self-regulation strategies such as setting spending limit or delaying purchases non-essential items were better positioned to manage debt effectively. Therefore, the findings reinforces that financial literacy extends beyond cognitive knowledge and includes psychological capacities necessary for sustained financial discipline.

The findings further highlight the role of technology as an enabler of financial control. Informants who actively used digital financial tools, such as mobile banking applications, budgeting apps, and automated savings platforms, usually demonstrated greater control over their financial activities (Wandhe, 2024). The prominence of technology in informants’ financial behaviour can be understood within the broader generational context of Gen Y and Gen Z, who demonstrate a high level of digital engagement and technological proficiency. As e-wallets and mobile banking technologies continue to evolve, cashless payment practices have become widely and normalised among younger generations (Aji & Adawiyah, 2021).

Since individuals categorised as Gen Y and Gen Z currently constitute the majority of young employees, their strong digital orientation explains the widespread use of financial applications observed in this study. Consequently, the tech-savvy behaviour exhibited by informants is not by coincidence but reflective of generational norms that shape how financial literacy is operationalised in everyday life. Within this context, digital financial tools serve not only as transactional platforms but also as mechanisms that enhance financial awareness. This finding reinforces the argument that technological proficiency strengthens financial literacy when accompanied by adequate financial knowledge and self-control.

Taken together, the three indicators operate synergistically to shape debt management behaviour among young employees. Financial knowledge shapes one’s decision-making. On the other hand, self-control governs behavioural execution, and technology constantly facilitates implementation.

This integrative relationship demonstrates that effective debt management is not the result of a single factor but rather arises from the interaction of cognitive behavioural and technological dimensions. Thus, this study contributes to a deeper understanding of financial literacy as a multidimensional construct.

Implication, Limitation, and Future Research

The findings theoretically support the relevance of the Theory of Planned Behaviour in explaining debt management among young employees, particularly through perceived behavioural control (self-control), subjective norms (family influence) and attitudes toward credit use. Meanwhile, the study has shown the societal impact by demonstrating that informal digital learning and technology-enabled financial behaviour are central components of contemporary financial capability among young adults.

Practically, policy makers and educators should incorporate digital learning approaches into financial literacy initiatives, using platforms familiar to young employees. Financial institutions can enhance debt management outcomes by integrating budgeting tools and credit awareness features into their mobile applications.

It is important to enhance financial literacy and debt management skills among young employees because it may reduce long-term financial vulnerability and support great financial resilience. Moreover, accessible and technology driven financial education can play a key role in promoting responsible financial behaviour and sustainable economic participation among youth.

Past studies have limitations; likewise, this research has its own. As the study prioritizes depth over breadth, the findings are intended for exploratory purposes rather than being representative of a larger population. Hence, future research should expand this study by including more diverse groups of young adults, particularly those from lower-income backgrounds, non-degree holders, and gig or informal sector workers, to enhance generalizability. Furthermore, the study is strictly focused on residents of Kelantan. While this provides specific socioeconomic insights, the results may not apply to young employees in other states with different development indices. Thus, comparative studies across different Malaysian regions or cultural contexts may further clarify the roles of family financial socialization and digital financial education interventions in strengthening debt management outcomes among young adults.

Conclusion

The study sets out to explore how young employees in Kelantan understand and manage debt by examining the learning process shaping financial literacy and the behavioural indicators influencing financial decision making. Using a qualitative approach, the study reveals that debt management among young employees is not solely determined by financial knowledge, but by a combination of learning environments, behavioural control and contextual constraints.

The results show that financial literacy is primarily developed through informal and digital learning channels, with social media platforms and fintech applications playing a central role in disseminating financial knowledge. While formal educational programs provide foundational exposure, young employees rely more heavily on experiential and technology-driven learning to navigate real-world financial challenges.

In addition, the study identifies key financial literacy indicators including budgeting practices, credit awareness, self-control, and use of digital financial tools that shape debt management behaviour. These indicators reflect core elements of TPB, particularly perceived behavioural control and subjective norms, reflecting the relevance of behavioural theory in understanding young employees’ financial behaviour.

By focusing on a less economically developed Malaysian state, this study contributes context-specific insights that extend existing financial literacy and debt management literature, which largely concentrated on urban or national level analyses. The findings underscore the importance of context-sensitive and digitally supported financial education strategies in strengthening financial resilience among young employees.

Overall, the study highlights the need for collaborative efforts among policymakers, educators, employers and institutions to design inclusive and accessible financial literacy initiatives. Furthermore, strengthening debt management capabilities among young employees is essential not only for individual financial well-being but also for broader economic and social sustainability.

Footnotes

Acknowledgements

During the preparation of this work, the authors used ChatGPT in order to generate ideas and to help with writing efficiency. After using the tool, the authors reviewed and edited the generated content as needed and take full responsibility for the final publication.

Ethical Considerations

The study was conducted in accordance with the ICH Good Clinical Practice Guidelines, Malaysian Good Clinical Practice Guidelines and the Declaration of Helsinki. The study adhered to core ethical principles by obtaining informed consent from all participants, ensuring the confidentiality of their data, and minimizing any potential harm. Furthermore, confidentiality was maintained in accordance, and participants’ identities would not be revealed in any publication as per Malaysia’s Personal Data Protection Act 2013 and audio files were securely stored.

Ethical approval was not obtained from Universiti Malaysia Kelantan Research Ethics Committee as one was not yet established at the time of this research.

Author Contribution

M.A. and A.L. conceived of the presented idea. M.A and A.A. verified the methods used. M.A analyzed the data and interpreted it. A.A. encouraged A.L. to investigate and supervised the findings of this work. All authors discussed the results and contributed to the final manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are deeply grateful to Universiti Teknologi MARA (UiTM) for providing the financial assistance.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Research data associated with this article is only available upon request.