Abstract

This study aims to investigate the asymmetric effects of exchange rates on the growth of the agricultural, industrial, and service sectors in Türkiye, utilizing the Nonlinear Autoregressive Distributed Lag (NARDL) method for time series analysis. The analysis covers the period from 2005Q4 to 2023Q4. The results indicate significant differences in sectoral effects. Specifically, increases in exchange rates do not have a substantial long-term impact on the agricultural sector, while decreases in exchange rates tend to enhance agricultural output over the long term. In contrast, for the industrial and service sectors, increases in exchange rates result in a decline in production, whereas decreases in exchange rates lead to an increase in production. The findings also reveal that the service sector is the most affected by exchange rate fluctuations in Türkiye, as indicated by the coefficients. These results demonstrate that Türkiye, as an emerging market and developing country, experiences the impacts of exchange rate fluctuations on its agricultural sector differently than on its industrial and service sectors in the long term. The NARDL findings underscore the necessity for regulatory institutions to manage exchange rates more sensitively, taking into account the relative importance of each sector in the Turkish economy.

Plain language summary

This study looks at how changes in exchange rates affect different parts of Türkiye’s economy—agriculture, industry, and services—between 2005 and 2023. Using a special method called NARDL, the researchers found that the effects are not the same for every sector. When exchange rates go down, agricultural production tends to increase over time. But when exchange rates go up, there is no strong effect on agriculture in the long run. For industry and services, it’s different: A rise in exchange rates leads to less production. A fall in exchange rates leads to more production. The service sector is the most sensitive to these changes. In short, exchange rate changes affect each sector in different ways. Policymakers in Türkiye should consider these differences when making economic decisions.

Introduction

Theoretically, it has been established that currency devaluation has a stimulating effect on economic activity. It is anticipated that the first spike in the price of foreign goods relative to domestic goods will lead to an excess demand for domestic goods. Moreover, the influence of currency depreciation on the total output levels of an economy has been a subject of debate among economists with diverse perspectives, primarily due to the existing uncertainty.

In its essence, currency devaluation fundamentally enhances exports and encourages a transition from imports to domestic goods, thereby boosting the demand for domestic products. In addition, countries may choose to devalue their currency to achieve competitive trade benefits and stimulate the growth of export-oriented sectors (Dornbusch & Leslie, 1988). This can ultimately propel a country toward a developmental path characterized by increased potential for long-term economic growth and employment (Dornbusch et al., 1994, 1995). As a result, with the aim of benefiting from expansionary aspects of devaluation, widespread devaluation can be seen following the collapse of the Bretton Woods system and through the adjustment policies of the International Monetary Fund (hereafter IMF) in countries such as Greece, Egypt, Argentina, and Türkiye in the years 2010, 2016, 2002, and 1994, respectively.

Although devaluation may originally benefit overall economic performance by boosting aggregate demand, its adverse impacts on the supply side result in an ambiguous outcome in terms of its influence on domestic output. The uncertainty surrounding this issue has captured the attention of development economists, who argue that the initial positive impact of devaluation will be undermined through various channels, such as distributional effects, account deficits, and real money balance effects (Guitian, 1976; Hanson, 1983). This is because the initial effect will not be enough to counterbalance the subsequent increase in import prices, leading to a decline in output (Krugman & Taylor, 1978).

Indeed, for countries like Türkiye, which rely on imported inputs for production and exports, this problem signifies a significant unresolved issue. Furthermore, the Turkish lira was pegged to the British pound and French francs until the Bretton Woods agreement, during which the value of the lira was fixed at 2.8 liras per United States (hereafter U.S.) dollar. Nevertheless, as the Bretton Woods system collapsed and floating exchange rates became increasingly prevalent, the lira experienced significant devaluation in 1960 and 1973. The value of the lira dropped from 2.8 to 9 liras per U.S. dollar in 1960 and further declined to 13 liras per U.S. dollar in 1973. The Turkish economy experienced a significant shift after the political and socio-economic crisis of 1994 to 1999, which ultimately led to the 2001 financial crisis. This crisis not only resulted in distortions of key macro-economic indicators such as output, exchange rate, and unemployment in Türkiye but also brought about the exchange rate to fall to 2.4 million per dollar. The Central Bank of the Republic of Türkiye (hereafter CBRT) has implemented necessary steps in response to the economic crisis, specifically targeting the monetary aspects of the markets, to maintain stability. Moreover, with the introduction of the lira reform, new lira replaced old Turkish lira at a rate of one new Turkish lira to 1 million old Turkish liras.

Following the crises of 2001, 2008, and the most recent COVID-19 epidemic, the CBRT has exerted considerable influence over the exchange rate market. Through open market operations, the CBRT attempted to prevent a sharp devaluation of the Turkish lira, albeit at the cost of depleting the central bank’s exchange rate reserves. Recently, there has been a surge in public statements made by government officials pertaining to the adoption of the “Beijing Consensus” (or Chinese Economic Model) as a means to enhance the competitiveness of the lira, with the ultimate aim of boosting the country’s exports and employment rates. The strong growth rates displayed by many countries with undervalued currencies in the early 2000s (Ridhwan et al., 2024) may have contributed to the adoption of such an approach. However, these tendencies raised inquiries regarding the pass-through of the exchange rate into industrial output and inflation levels in Türkiye. The concerns mainly revolved around the country’s reliance on intermediate goods, current account deficits, and foreign debt, which were already extensively debated.

Although economic theories are grounded in numerical data, countries’ economic systems are fundamentally supported by the social institutions formed by individuals. Consequently, countries with similar economic characteristics may not achieve identical outcomes by adopting comparable policies. Furthermore, the economic effects stemming from the political stability fostered by social structures should not be underestimated. In this context, the discussion surrounding the appreciation of the Turkish lira, often regarded as an undervalued currency, has become increasingly prevalent. Analyzing these effects from various scientific perspectives presents substantial research opportunities. The rationale behind this study is grounded in the previously mentioned reasons, with the aim of examining Türkiye within the context of its internal balances. A model that elucidates the effects of currency fluctuations on sectoral production has significant potential to provide valuable insights for a developing country like Türkiye and other emerging markets. Furthermore, the incorporation of variables such as exports, oil prices, and money supply, factors that substantially influence production across various sectors in Türkiye, offers a comprehensive perspective, enabling the research process to be conducted through a distinctive model.

In this context, the research questions are as follows:

Answering these research questions will significantly contribute to the development of the model, drawing on the theoretical foundation necessary for the research as well as previous similar studies. Additionally, the existing gaps in the literature will provide a compelling rationale for conducting this study.

Theoretical Framework

Building on the conceptual ambiguity surrounding the macroeconomic effects of exchange rate fluctuations, this section develops the theoretical foundations of the study by outlining the key transmission mechanisms through which currency devaluation (depreciation) and revaluation (appreciation) may influence aggregate and sectoral output.

First of all, in the context of the Mundell-Fleming model, a devaluation of the domestic currency results in increased output levels, potentially accompanied by higher interest rates depending on the reaction of monetary policy (Wang, 2020). In an open economy, this shift toward production can also be explained by the expectation of earning valuable foreign currency through exports. Bahmani et al. (2013) explain this situation through the Marshall-Lerner condition. Conversely, in the case of revaluation (appreciation), the opposite effect will be observed (Levy-Yeyati et al., 2013). In this scenario, the belief that export earnings in the local currency will decrease diminishes the incentive to engage in international risks. This perception may lead businesses to concentrate more on the safer domestic market rather than pursuing additional production for exports. As a result, companies might scale back or abandon plans for increased production, as the potential returns from exports may not warrant the associated risks.

Furthermore, recent studies have revisited this framework in light of contemporary challenges, including financial globalization and digital currencies. For instance, Enajero (Enajero, 2021) and Tenderere (Tenderere & Mishi, 2025) demonstrate that the traditional Mundell–Fleming predictions may be altered when economies experience volatile capital mobility and the presence of alternative monetary assets, notably cryptocurrencies. Similarly, Leightner (2024) and Magacho et al. (2022) empirically confirm that the model’s predictions differ across fixed and flexible exchange-rate regimes in small open economies characterized by advanced technology utilization, such as Australia and South Korea.

Additionally, the “J-Curve” theory elucidates that in the short run, currency devaluation will deteriorate a nation’s trade balance, whereas in the long run, after pre-existing trade agreements are alleviated, trade balance will progressively improve (Bremmer, 2007). The short-term deficits described by the J-curve approach, which are offset by long-term recovery, can also be attributed to production aimed at generating foreign currency earnings (Geldner, 2025). The existence of significant exchange-rate volatility not only hinders the recovery phase, undermining long-term advancements in sectors such as agriculture (Trofimov, 2024), but also induces disparities in readjustment across bilateral trading partners (Bosupeng et al., 2024; Montes et al., 2024).

In practice, the real-world effects of a domestic currency revaluation or devaluation on output may not always align with the theoretical predictions. This is a common occurrence in the field of economics where ambiguity often plays a significant role. Nevertheless, the theory’s limitations arise from its failure to consider the sensitiveness of domestic price levels to fluctuations in exchange rates (specifically devaluation in this context). Such volatility might possibly decrease overall demand and translate into substantial economic losses, manifesting as recurrent declines in industrial output and employment levels (Alejandro, 1963; Cooper, 1992). Contrary to Krugman and Taylor’s (1978) assertion that a reduction in demand as a result of devaluation lowers prices, adverse supply shocks completely negate the gains from devaluation and put upward pressure on price levels, depending on the response of nominal wages (Lizondo & Montiel, 2006; Van Wijnbergen, 1986).

Moreover, recent empirical research supports that the extent of exchange rate pass-through to domestic price levels is neither constant nor uniform across various economies (An et al., 2021; Beirne et al., 2024; Bhat et al., 2025). Consequently, the magnitude of pass-through evolves and fluctuates according to monetary policy credibility, inflation expectations, and structural characteristics of production (Colak et al., 2024; Lama et al., 2025).

Further, when the regional context is taken into consideration, the implementation of a strategy of competitive devaluation in an emerging economy might result in negative regional spillovers due to the “neighborhood effect” (Calvo & Reinhart, 1996; Rose & Glick, 1999). In a globally interconnected economy, when a country’s export competitor experiences devaluation, it can deteriorate the trade balance of the partner country. This can potentially trigger a speculative attack on the partner country’s currency, causing an excessive fluctuation of the domestic currency (S. Kim & Roubini, 2000). Should a country’s trader competitor resort to the “tit for tat” strategy as a policy response, the attempt to “beggar thy neighbour” (Smith, 2007, p. 377) via competitive devaluation may not necessarily yield a desired outcome.

The contemporary studies on foreign exchange spillovers reveal considerable interconnectedness among major and emerging-market currencies, implying that depreciation episodes in one economy can propagate volatility to others (Ha et al., 2025; Huynh et al., 2023). Additionally, the global monetary environment intensifies these effects, as expansionary policies in advanced economies or crisis-related depreciations, such as those observed during the COVID-19 period, can produce implicit pressures on exchange rates and capital flows in developing regions (Bhatia & Tuteja, 2024; Dées & Galesi, 2021).

In their study on the relationship between exchange rates and financial fragility, Eichengreen and Hausmann (1999) highlight the inability of developing economies to borrow (domestic or abroad) using their domestic currencies, regardless of the duration of the loan. This lack of ability is commonly referred to as the concept of “original sin,” leading to probable financial fragility and a currency mismatch for domestic investments. In a recent report by the United Nations Trade and Development [UNCTAD] (2023) organization, it was revealed that approximately 54.7% of short- and long-term external debt in developing economies is denominated in US dollars. This represents the highest level ever recorded since the outbreak of the COVID-19 pandemic, underscoring the significant impact of currency devaluation on the “balance sheets” of the banks in developing economies. The repercussions of the “balance sheet” effect will counteract the anticipated advantages of currency devaluation, and substantial unhedged exposures to short-term foreign currency debt will arise. This will culminate in widespread domestic credit rationing, an elevated amount of non-performing loans (NPLs), and a credit crunch for industrial producers (Hutchison & Glick, 2000).

Moreover, the aforementioned industrial producers with elevated foreign-currency exposure encounter substantial reductions in investment subsequent to depreciations, and banking systems with dollarized liabilities face increased non-performing loans and tighter lending standards (Bruno & Shin, 2017; Hofmann et al., 2022; Seraj & Coskuner, 2021). This mismatch between currency composition of assets and liabilities constrains monetary policy autonomy and heightens systemic risk, making exchange-rate flexibility less effective as a stabilization tool (Chakrabarti & Sen, 2023; International Monetary Fund [IMF], 2022).

In addition, Fernandez-Arias and Hausmann (2001) characterize short-term debt as unfavorable, drawing an analogy to “bad cholesterol,” owing to the fact that riskier countries attract less capital but receive a higher proportion of it in the form of speculative foreign direct investment (FDI). The susceptibility of developing economies to speculative attacks, exacerbated by structural problems, contributes to concerns regarding the potential reversal of the early advantages of moderate devaluation. This reverse effect can serve as a trigger for major capital outflows and ultimately bring about a complete economic collapse due to credibility concerns, possibly sparking a large-scale speculative attack. Krugman (1998) claims that the response of markets to devaluation strategies differs across developing and developed nations on account of problems surrounding “credibility.” These problems can cause a subsequent decline in the currency’s value, generating a vicious cycle of crisis-induced devaluation, scarcity of available funds, and financial bankruptcy for organizations and enterprises. According to Shang-Jin and Wu (2002), contractionary devaluation in developing countries is a result of “poor” governance, which is closely tied to the aforementioned credibility aspect.

Recent empirical research reinforces the potency of these credibility and debt composition channels. It is documented that emerging economies with larger shares of short-term foreign-currency debt are particularly prone to experience abrupt capital outflows and currency crises during periods of global stress (Bernoth & Herwartz, 2021; Dalgic, 2024; S. Liu et al., 2024; Zhang et al., 2024). Several analyses further show that investor skepticism pertaining to policy credibility amplifies speculative pressures, particularly when short-term debt is rolled over through foreign-denominated instruments (Chowdhury & Sundaram, 2023; Dhar, 2021; Inoguchi, 2025).

The theories presented indicate that the impact of exchange rate fluctuations on real output dynamics is significantly context-dependent, contingent upon trade openness, financial depth, and policy credibility. These interactions are particularly pertinent for emerging economies that rely extensively on imported inputs and foreign-currency borrowing, conditions that characterize Türkiye’s economic structure. The following section, therefore, surveys the related literature and identifies the empirical gaps that motivate this study.

Literature Review

Several studies utilizing Vector Autoregressive (VAR) frameworks document that exchange-rate depreciations affect output dynamics through trade, price, and financial channels, yet the sign and magnitude are context-dependent. In emerging markets, flexible exchange rates can either cushion or amplify shocks depending on external vulnerabilities and policy settings (Babubudjnauth & Seetanah, 2021; Fisera, 2024; Montane et al., 2021). Models that include control variables such as inflation, employment, trade, capital flows, and money supply observe heterogeneous impulse responses across countries and time periods, underscoring that structural features shape the transmission from exchange rates to Gross Domestic Product (GDP; Ahmed et al., 2023; Souza & de Mattos, 2022). Evidence from small open economies and commodity-dependent regions further shows that the interaction between exchange-rate movements and price formation (terms-of-trade and pass-through) is crucial for short-run output responses (Chen & Ward, 2025; Manopimoke et al., 2024). While the samples and variables examined vary, the findings also demonstrate variability. This further underscores the necessity of analyzing exchange rate fluctuations from different perspectives, as outlined in the theoretical framework. Similar situations are also observed in other studies within literature.

Studies utilizing the Vector Error Correction Model (VECM) have underscored the significant impact of exchange rates on economic growth and sectoral production in various research studies that differentiate between developed and developing countries (Kandil, 2019; Moses et al., 2020; Zengeni & Mahonye, 2019) . Notably, contrary to earlier studies, recent investigations incorporate the oil price variable into their models (Ben Salem et al., 2024; Chatziantoniou et al., 2023). Further, evidence demonstrates that in countries that have substantial export capacity, depreciation may enhance growth, whereas in economies depending on imported inputs or foreign-currency debt, it can lead to contractionary consequences owing to rising production costs and inflation pass-through (Bigerna, 2023; Ha et al., 2020). Overall, these findings justify a country-specific empirical assessment that explicitly models trade and cost transmission together.

Research conducted using the Generalized Method of Moments (GMM) has examined the relationships between exchange rate fluctuations, economic growth, and production across various models focusing on high-, middle-, and low-income countries (Demir & Razmi, 2022; Ebrahimi et al., 2020; Ferrara & Yapi, 2022; Gabriel et al., 2020). In addition, Bussière et al. (2020) report that exchange rate depreciation dampens growth in financially dollarized countries due to increased balance-sheet pressure. In the context of commodity exposure, Mous and Maznan (2024) find that exchange rate volatility diminishes industrial production during periods of elevated energy prices.

When examining various studies that have employed different panel regression models, researchers have identified the impact of exchange rate fluctuations on sectoral production in several contexts. For instance, Hardy (2023) documents that exchange rate volatility significantly weakens the credit capacity of firms in emerging economies by deteriorating their balance sheets, ultimately constraining investment and productivity. Caballero (2021) argue that exchange rate shocks are transmitted from firms to the broader macroeconomy through credit constraints, amplifying systemic risk in financially dollarized sectors. Evidence from Salomao and Varela (2020) further suggests that sectors with high import dependence exhibit stronger output contractions following currency depreciations, confirming that exchange rate dynamics are central to the transmission of external shocks into domestic production. Ramoni-Perazzi and Romero (2022) demonstrate that exchange rate depreciation raises input costs and inflationary pressures, disproportionately affecting manufacturing firms that are exposed to global value chains. These findings collectively indicate that the exchange rate is not merely a nominal variable but a key determinant of sectoral performance through its influence on cost structures and financial stability.

Studies examining the relationship between currency devaluation or exchange rates and economic and sectoral growth using Autoregressive Distributed Lag (ARDL) methods have included samples from various regions. For instance, Bahmani-Oskooee and Arize (2020b) provide evidence that exchange rate depreciation in African economies brings about asymmetric growth responses, emphasizing the relevance of structural vulnerabilities and the degree of import dependence. More recent studies, such as Nusair (2022) and Nosheen et al. (2023), show that exchange rate misalignments create persistent output fluctuations in Asian countries by affecting trade balances and capital flows. Ali et al. (2022) reveal that while depreciation pressures in Pakistan could contribute to short-term benefits in net exports, they ultimately pose challenges for long-term growth as production costs soar. The instability of the exchange rate, according to Sharaf and Shahen (2023), undermines the confidence of investors and, thereby, erodes fiscal space in Egypt.

In addition to studies conducted on various samples using diverse methodologies, it is also beneficial to examine research specifically focused on Türkiye, which is the focal point of this study. Özdemir et al. (2022) demonstrate that exchange rate depreciation does not impose a constraining effect on aggregate production in Türkiye, suggesting that depreciation may bolster tradable sectors via competitiveness gains. Further, Halicioglu et al. (2018), Bahmani-Oskooee and Durmaz (2020a), and Karamelikli and Bahmani-Oskooee (2021) document that exchange rate depreciation enhances industrial activity through augmenting net exports and initiating expansionary monetary effects. However, more recent sectoral studies, such as Ari et al. (2019) and Khalid et al. (2025), reveal that depreciation yields heterogeneous outcomes across industries, benefiting export-oriented manufacturing while adversely affecting sectors with high import dependency due to increased production costs. Complementary evidence provided by Demirkılıç (2021) and Tong and Durmaz (2024) indicates that in periods characterized by heightened financial fragility, currency depreciation reduces output by tightening external financing conditions and exacerbating balance sheet effects.

Literature Gap

The literature review indicates that studies conducted in various countries predominantly focus on measurements based on total production and GDP output. However, it is essential not to overlook the critical sectoral distinctions that are significant for developing countries, despite the fact that many studies concentrate on these nations. Additionally, research specifically conducted on Türkiye similarly tends to focus solely on total or industrial production. Since the sectoral distinctions made in industrial production can also be interpreted through a single sector at the macro level, this literature review reveals a significant gap. Moreover, examining the sectoral effects collectively, not only in terms of addressing different sectors but also regarding the variation of explanatory variables, would provide a substantial contribution to the literature. Furthermore, incorporating both the symmetric and asymmetric effects of the exchange rate into the model allows the study to address these important gaps in the existing literature. Indeed, the research model is supported by the literature through the inclusion of sectoral growth, exchange rates, money supply, exports, and oil prices, while it distinguishes itself by separately measuring and presenting the agricultural, industrial, and service sectors.

Türkiye in Context and Motivation

Türkiye exemplifies a distinctive macro-financial case among emerging economies due to its simultaneous exposure to currency volatility, structural external imbalances, large-scale migration pressures, and unprecedented natural disasters.

The COVID-19 epidemic represented a turning point for the Turkish economy, as the interplay of dwindling central bank reserves and expansionary credit-driven policies precipitated a succession of significant currency depreciations. Furthermore, the massive earthquake that struck 11 cities during the post-pandemic recovery phase caused damage amounting to hundreds of billions of dollars. These extraordinary shocks not only amplified exchange rate volatility but also intensified inflationary pressures and interrupted production networks.

The regional context for Türkiye, like many other aspects, is increasingly complex. In addition to competition, the wars and conflicts in neighboring countries are driving migration to Türkiye, significantly disrupting the balance of demand. Refugees and undocumented migrants from countries such as Syria, Ukraine, Russia, Afghanistan, and others are profoundly affecting the supply-demand equilibrium, which finally affects the monetary issues. This persistent migration-driven demand shock distinguishes Türkiye from other emerging economies, where exchange rate dynamics are typically examined under more stable demographic circumstances.

Türkiye’s macroeconomic fragility is further compounded by its extensive reliance on external borrowing. As of 2024, the country’s total external debt exceeds 550 billion dollars, and a substantial share of this debt is denominated in foreign currency (Central Bank of the Republic of Türkiye [CBRT], 2024).23 This structural attribute renders the Turkish economy particularly susceptible to exchange rate fluctuations, as currency depreciations promptly result in increased debt servicing costs, reduced credit accessibility, and aggravated financial instability. In contrast to studies assessing exchange rate-growth dynamics in countries with limited external debt exposure, Türkiye constitutes a unique instance where devaluation may inhibit rather than augment productive capacity.

The efficacy of the enacted “competitive Turkish lira” policies in Türkiye is disputable given multiple considerations. These obstacles encompass the issues inherent to being a developing country with an open economy, dependence on imported raw materials, concerns over credibility, and the influence of geographical location. Moreover, Türkiye’s reliance on imported intermediate goods for agricultural, industrial, and service production profoundly alters the pass-through of devaluation. Instead of fostering competitiveness, depreciation raises input costs, constrains production, and fuels inflationary spirals, hence challenging the assumptions of traditional growth-enhancing devaluation theories.

Having said these, Türkiye offers a compelling and analytically distinct context in which the effects of exchange rate depreciation cannot be evaluated solely through conventional theoretical frameworks alone. The confluence of external debt exposure, migration-induced demand shocks, natural disasters, and import-dependent production structures renders Türkiye an exceptional case for reassessing the effectiveness of devaluation policies. This study aims to empirically examine whether currency depreciation in Türkiye has adversely affected domestic output in the agricultural, industrial, and service sectors, which are notably susceptible owing to their considerable reliance on imported intermediate inputs and exchange rate fluctuations.

Methodology

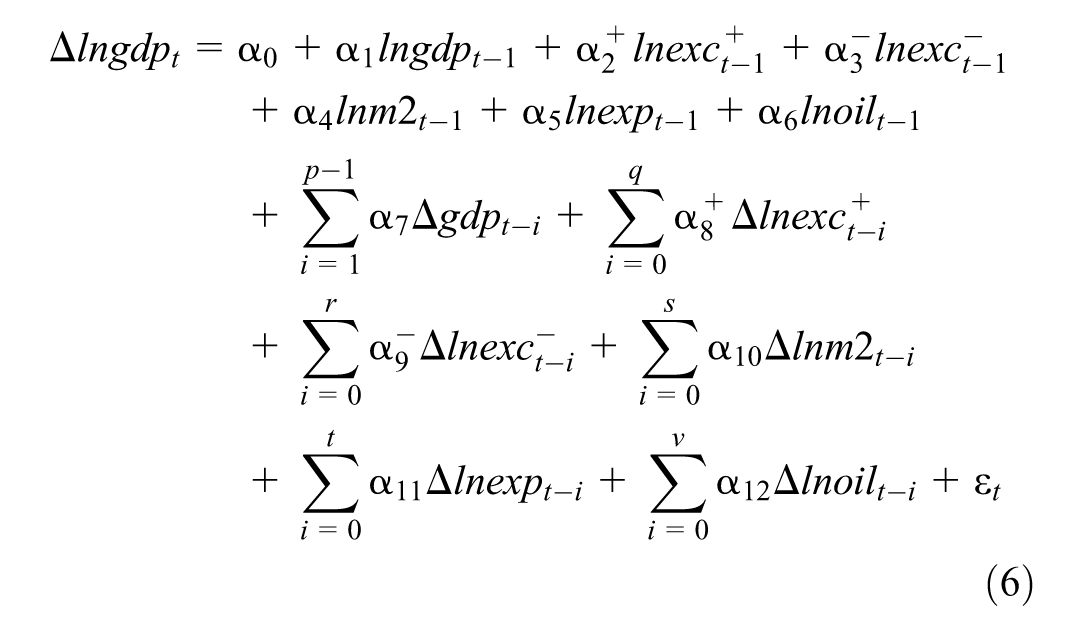

The empirical model employed to examine the effects of exchange rate fluctuations on sectoral production within the Turkish economy is delineated in Equation 1.

In this model, the dependent variable is sectoral production (lngdp). Separate estimations have been performed for production (current, $) in the agriculture, forestry, and fishing sectors, the industrial sector, and the services sector. The primary independent variable in the model is the exchange rate (lnexc), while the control variables encompass sectoral exports (lnexp, and oil prices (lnoil). The exchange rate utilized in the model is the U.S. dollar exchange rate. An increase in the dollar rate (i.e., depreciation of the local currency) may enhance national income by stimulating the country’s exports; however, it may also result in a reduction in production within sectors that heavily depend on imported inputs due to the escalated costs of imports. Among the control variables, lnexp reflects the export levels of each sector, which is essential for the continuity of sectoral production in a globalized economic context. The final control variable, lnoil, is included in the model to account for energy costs, which are a critical input in production. Given that increases in oil prices elevate production costs, they are anticipated to exert a negative impact on production.

As highlighted in the existing literature, while numerous studies have investigated the impact of exchange rates on production within the Turkish economy, the potential nonlinear effects of exchange rates on production levels have been largely neglected. Market distortions, including price and wage rigidities, asymmetric information, and other similar factors, may lead to differential responses of economic variables to positive and negative shocks in another variable. Specifically, fluctuations in exchange rates may exert disparate effects on production levels. This study seeks to investigate the influence of exchange rates on sectoral production through the application of the Nonlinear Autoregressive Distributed Lag (NARDL) methodology, as established by Shin et al. (2014). This approach represents an advanced iteration of the Autoregressive Distributed Lag (ARDL) model introduced by Pesaran et al. (2001). The ARDL methodology presents several advantages; notably, it does not necessitate that the time series be stationary at the same order, allowing for the inclusion of series that are I(0) or I(1), provided they are not I(2). Additionally, this approach facilitates efficient and consistent estimation results, even when applied to small and limited sample sizes. These advantages have contributed to the widespread adoption of the ARDL approach in the exploration of relationships between variables.

In the NARDL approach, the effects of positive and negative shocks in the independent variable on the dependent variable are analyzed separately. The asymmetric long-run relationship between the variables is examined through the application of asymmetric cointegration regression, as presented in Equation 2. In this equation,

The model delineated by Equation 1 in this study is articulated in a nonlinear form in equation

In this context, the dependent variable is denoted as

The analysis period of this study encompasses the fourth quarter of 2005 through the fourth quarter of 2023. The selection of this analysis period was influenced by the availability of relevant data. The variables lngdp and lnexp, which have been adjusted for seasonal and calendar effects, were sourced from the Turkish Statistical Institute (TURKSTAT, 2024). The data for lnexc was obtained from the Central Bank of the Republic of Türkiye (CBRT), while the lnoil data, which reflects Brent oil prices, was retrieved from the St. Louis Federal Reserve database. There is a rationale behind choosing these variables. Several recent studies employing ARDL, VAR, and VECM frameworks have highlighted that oil prices are a key exogenous determinant influencing both exchange rates and sectoral output, as energy costs transmit into production and price dynamics (e.g., Ben Salem et al., 2024; Chatziantoniou et al., 2023; Mous & Maznan, 2024). These studies show that elevated energy prices intensify the contractionary effects of currency depreciation, especially in industrial and service sectors dependent on imported inputs. Similarly, exports are widely recognized as the primary channel through which exchange rate movements affect economic growth. Empirical evidence from both cross-country and Türkiye-specific analyses confirms this transmission mechanism: depreciation tends to stimulate export-oriented sectors while constraining those with high import dependence (e.g., Ari et al., 2019; Bahmani-Oskooee & Durmaz, 2020a; Karamelikli & Bahmani-Oskooee, 2021; Khalid et al., 2025; Özdemir et al., 2022). Accordingly, incorporating both oil price and export variables provides theoretical and empirical coherence with the established literature, ensuring that the models capture the trade and cost channels through which exchange rate dynamics influence sectoral growth.

Empirical Results

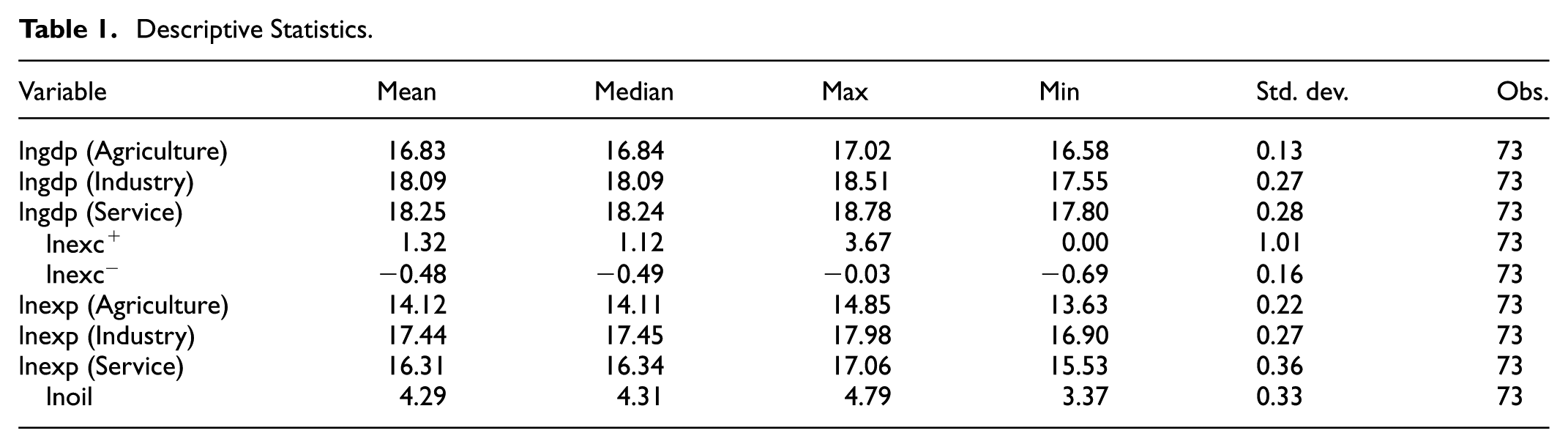

Table 1 presents the descriptive statistics of the data. The results unequivocally demonstrate the disparities in economic magnitude among sectors. The mean lngdp values indicate that during the period in question, the services sector (18.25) had the highest average production level, while agriculture (16.83) had the lowest. Further, an examination of the standard error values of the

Descriptive Statistics.

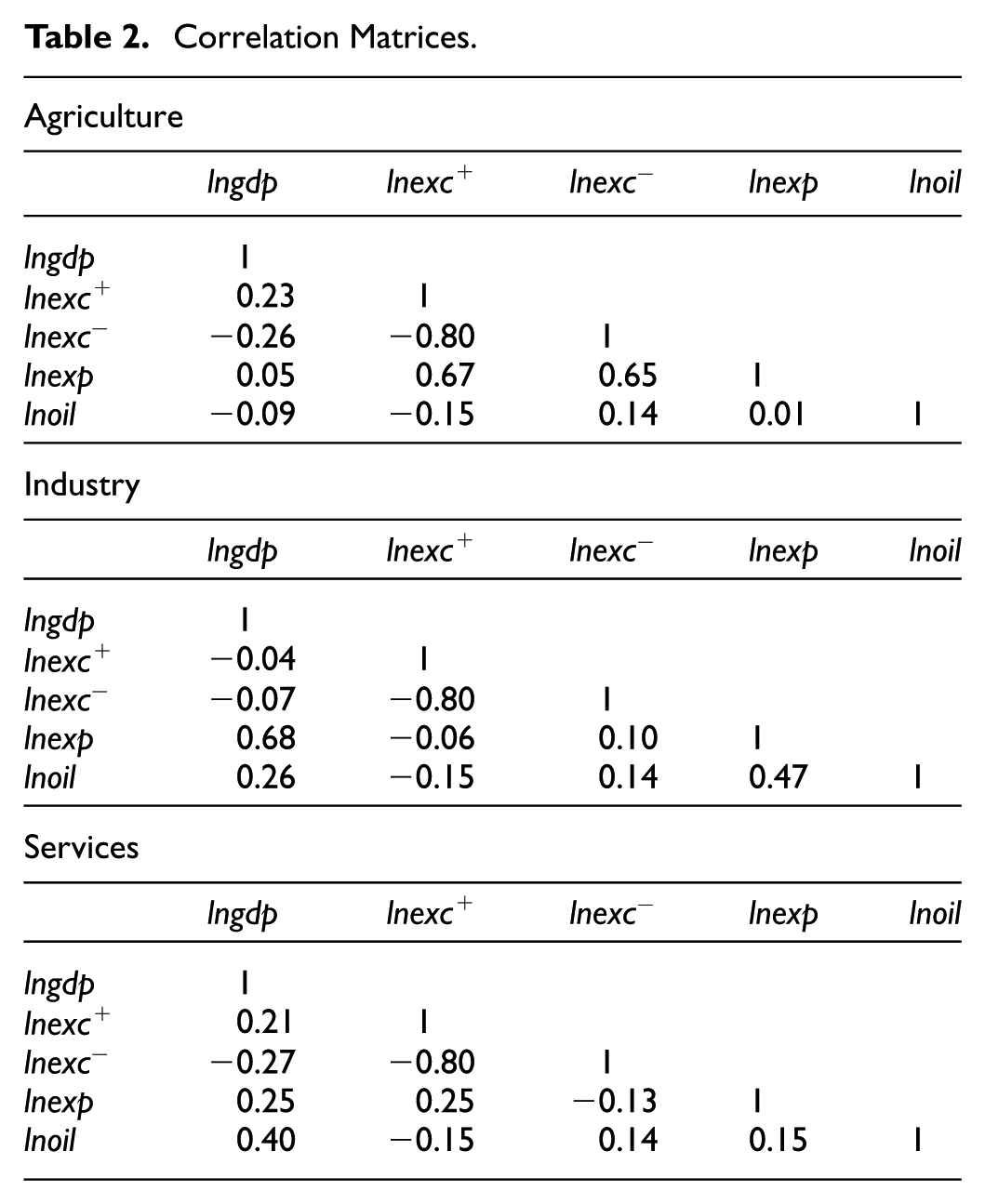

Table 2 presents the correlation matrices for the data adopted in the estimation models. The correlation matrices show generally low to moderate relationships among the variables, suggesting a low risk of multicollinearity. The majority of correlation coefficients between lngdp and other variables are below .7. Although

Correlation Matrices.

There is no evidence of significant linear correlations among other variables, indicating that multicollinearity tends not to be a concern. Therefore, the regression results can be considered reliable, and the independent effects of the explanatory variables can be interpreted with confidence.

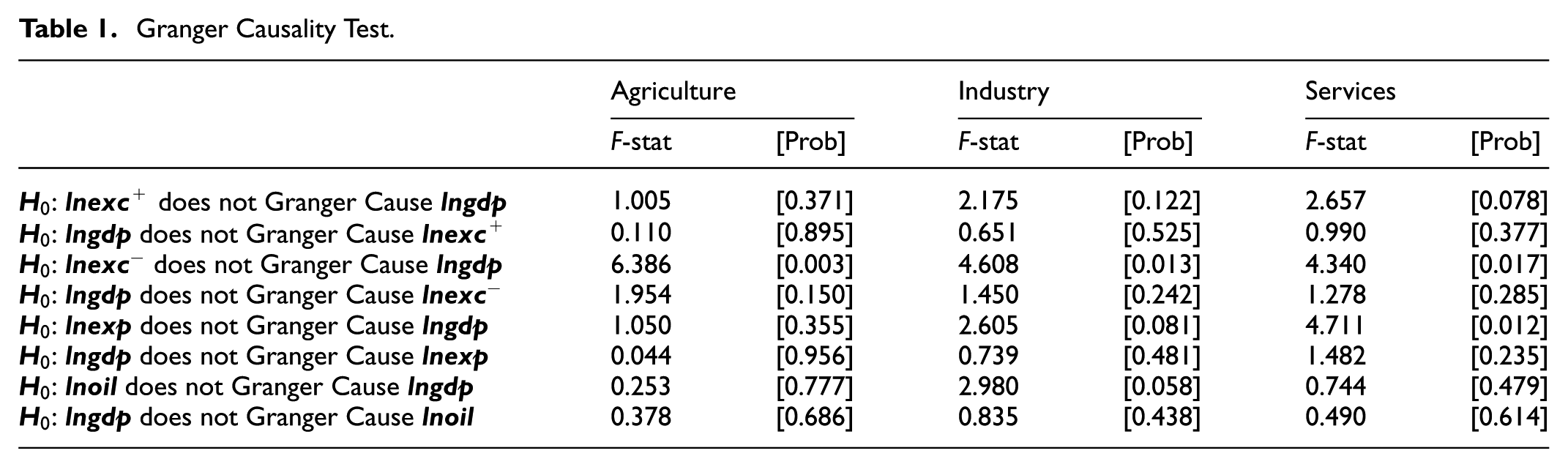

The NARDL method assumes that the variables included in the model are exogenous and represent fluctuations arising from self-adjusting market dynamics. However, considering the sample period covered in the analysis, there is a risk that authorities may have implemented various interventions to ensure economic stability, which could potentially be a source of endogeneity. In this case, a causality analysis was conducted to investigate the direction of relationships among the variables. According to the Granger Causality Test results provided in the Appendix, it was concluded that there is a causality relationship from the independent variables in our model to lngdp at various statistical confidence levels, whereas no significant causality was found from lngdp to the independent variables. These results indicate that the variables are generally exogenous, hence there is no significant endogeneity risk.

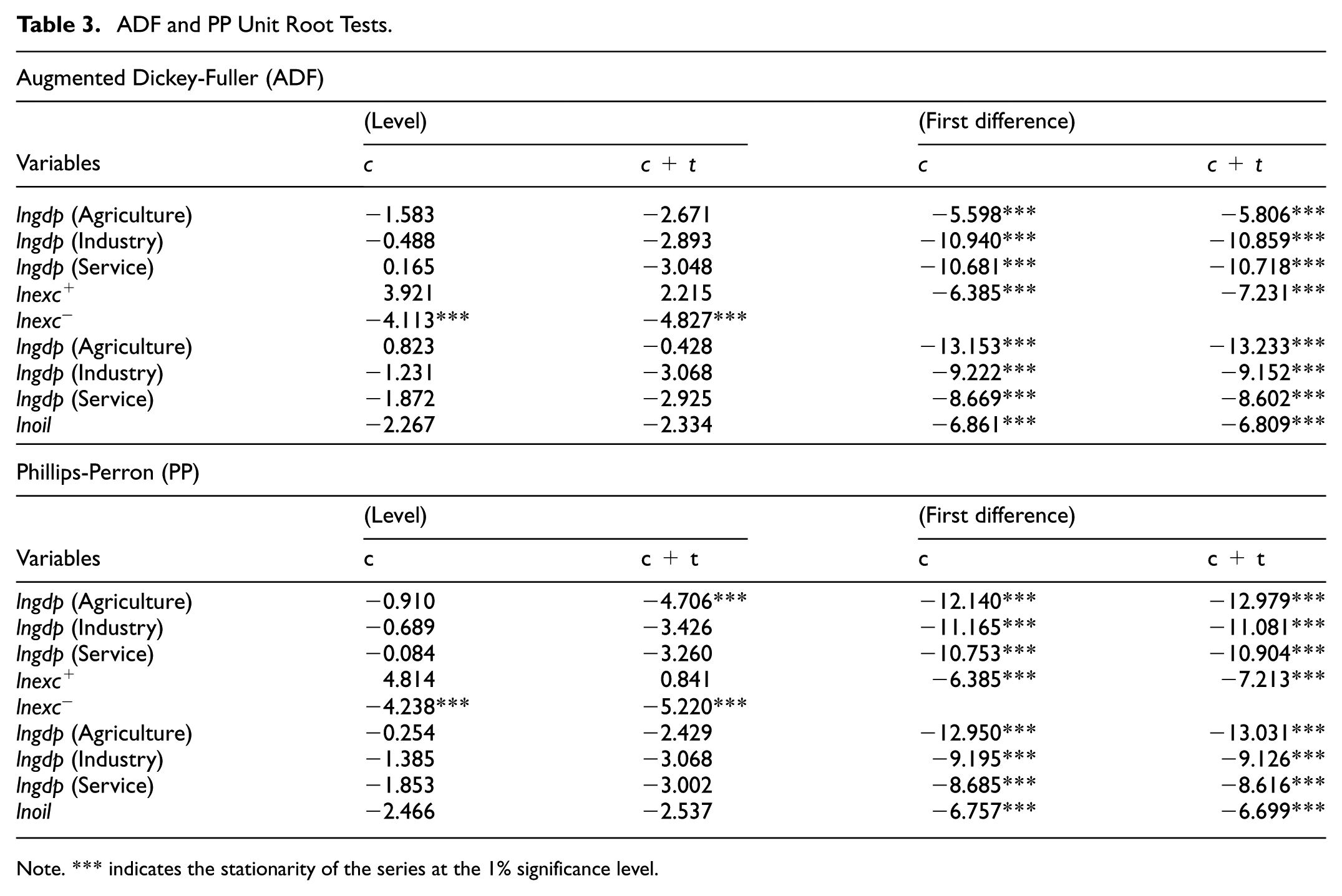

Before proceeding with the NARDL estimation, the stationarity of the time series is assessed utilizing the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests. The findings from these tests are summarized in Table 3. Both unit root tests employed model specifications that included a constant and a constant plus trend. The results indicate that all variables, with the exception of the

ADF and PP Unit Root Tests.

Note. *** indicates the stationarity of the series at the 1% significance level.

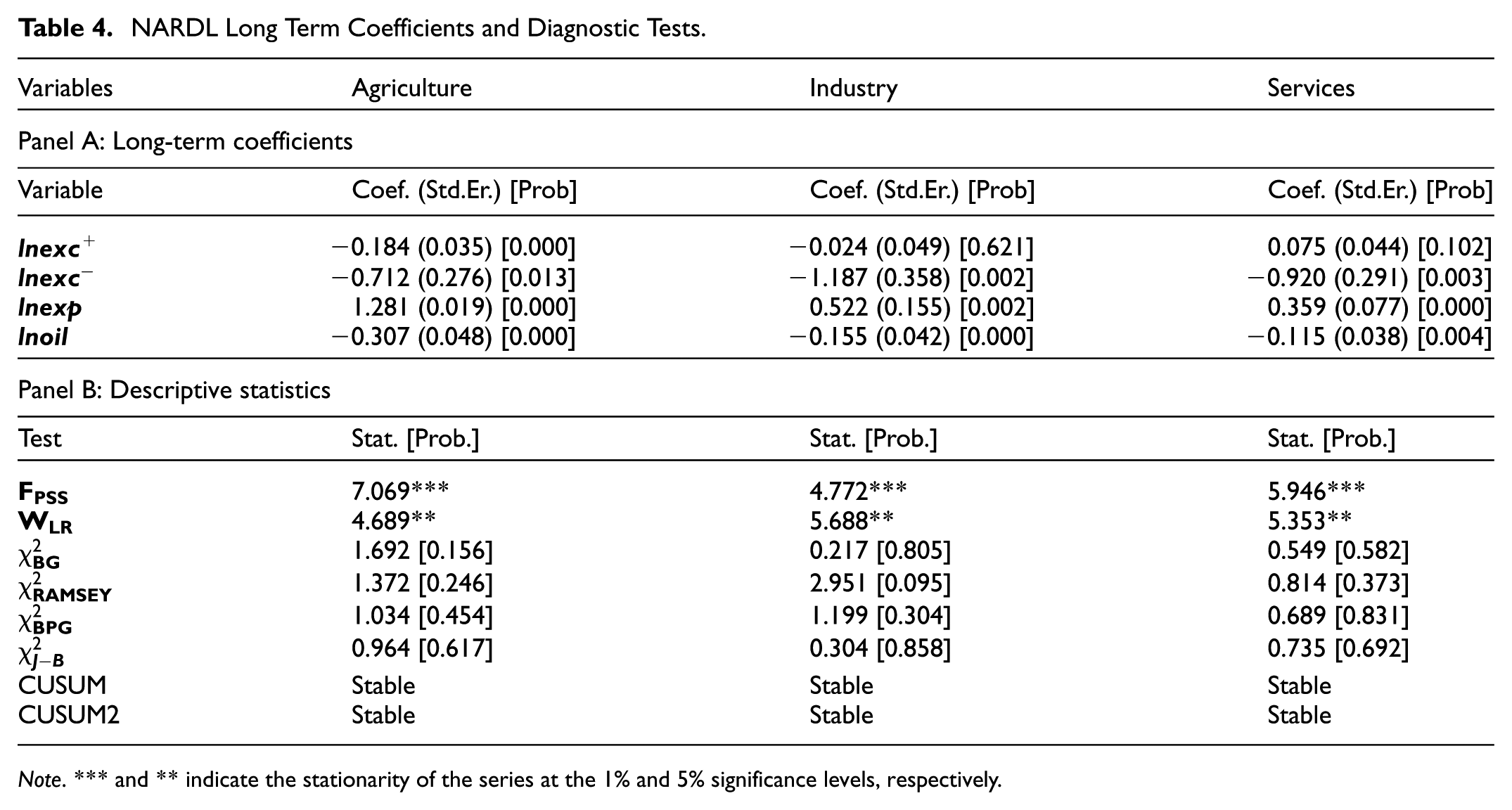

Using data from the agriculture, industry, and services sectors, the model specified in Equation 6 was estimated, and the results are presented in Table 4. Initially, the bound test results (

NARDL Long Term Coefficients and Diagnostic Tests.

Note. *** and ** indicate the stationarity of the series at the 1% and 5% significance levels, respectively.

According to Table 4, the significant asymmetric exchange rate effect is pronounced in the agricultural sector, as reflected by the coefficient of

The long-term coefficients derived from the examination of the industrial sector, however, indicate a distinct reaction to currency shocks. Although the coefficient of the

In the context of the services sector, perturbations in

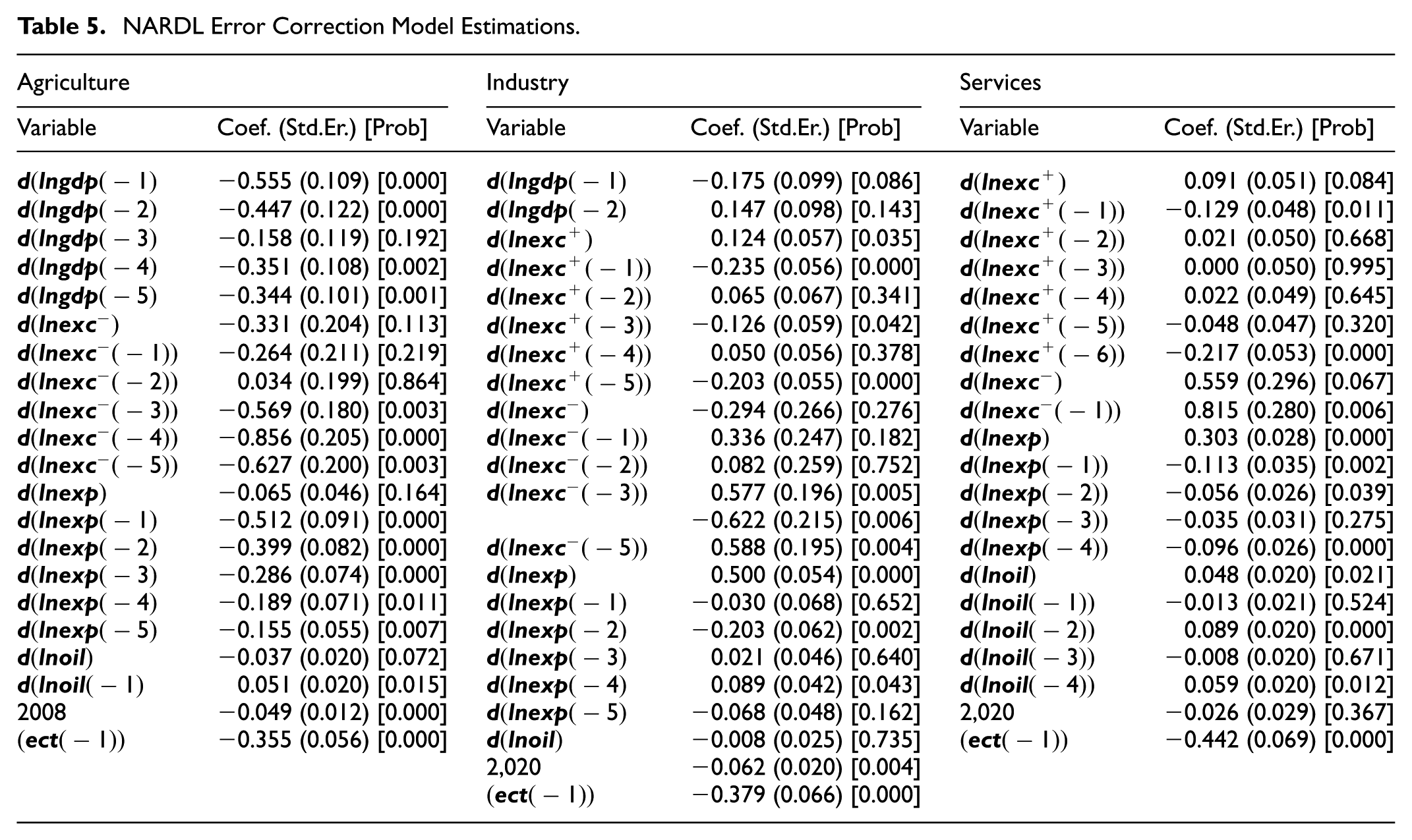

Table 5 displays the estimation results of the error correction model. The coefficient of the error correction term (

NARDL Error Correction Model Estimations.

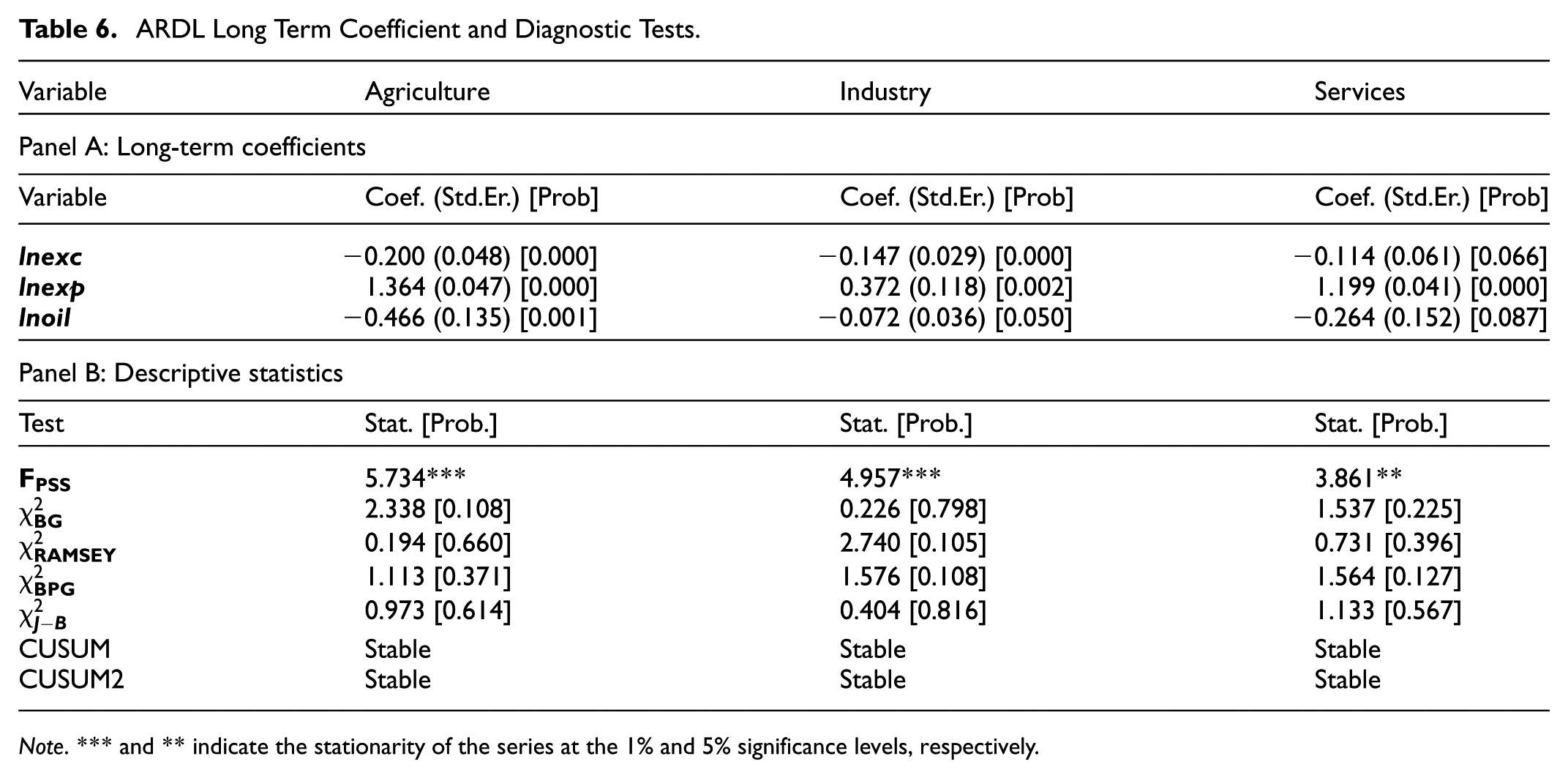

In the last stage of the analysis, the model employed in this study, which was initially estimated using a nonlinear method, is subsequently estimated using a linear approach. Table 6 presents the long-term coefficients and diagnostic test results derived from the ARDL methodology. The results of the bounds test (

ARDL Long Term Coefficient and Diagnostic Tests.

Note. *** and ** indicate the stationarity of the series at the 1% and 5% significance levels, respectively.

An analysis of the long-term coefficients reveals that, the lnexc and lnoil variables display an adverse impact across all three sectors, whereas the lnexp variable exhibits a more profound positive pass-through in comparison with the other variables. The statistical significance of the lnexc and lnoil variables’ influence over the services sector is deemed marginal.

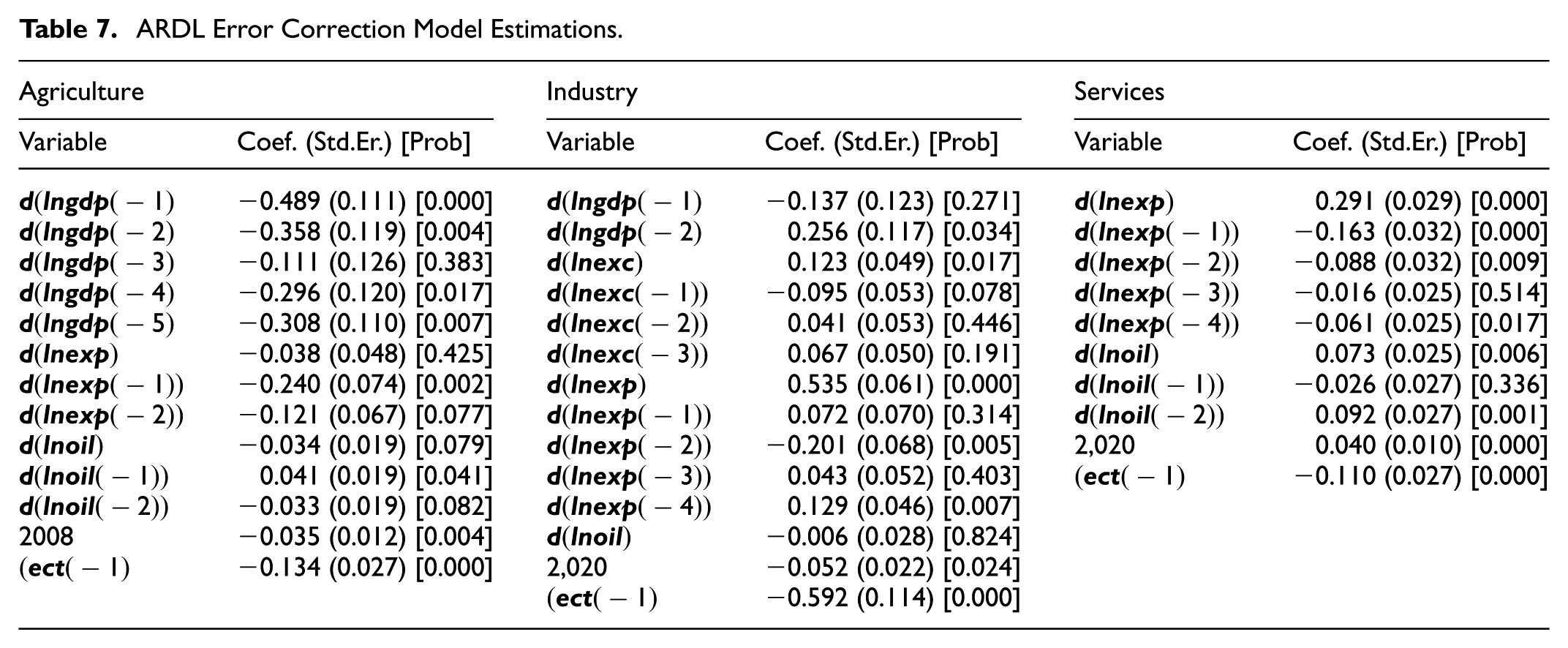

Table 7 presents the estimation results of the error correction model derived from the ARDL approach. The error correction term (

ARDL Error Correction Model Estimations.

Discussion

Upon analyzing the estimation results from NARDL and ARDL models, it is evident that the effects of positive and negative exchange rate shocks on sectoral output exhibit significant variation across the three sectors under consideration. In the context of agricultural sector production, a prolonged depreciation of the currency rate diminishes output levels, whereas an appreciation of the exchange rate enhances output. Conversely, an examination of the industrial and service sectors illustrates that the depreciation of the exchange rate seldom has a major long-term impact on sectoral production; yet it augments sectoral output in the short run for one quarter. This sectoral heterogeneity aligns with classical theoretical expectations derived from the Marshall–Lerner condition and subsequent open-economy extensions (see Bahmani et al., 2013; Levy-Yeyati et al., 2013).

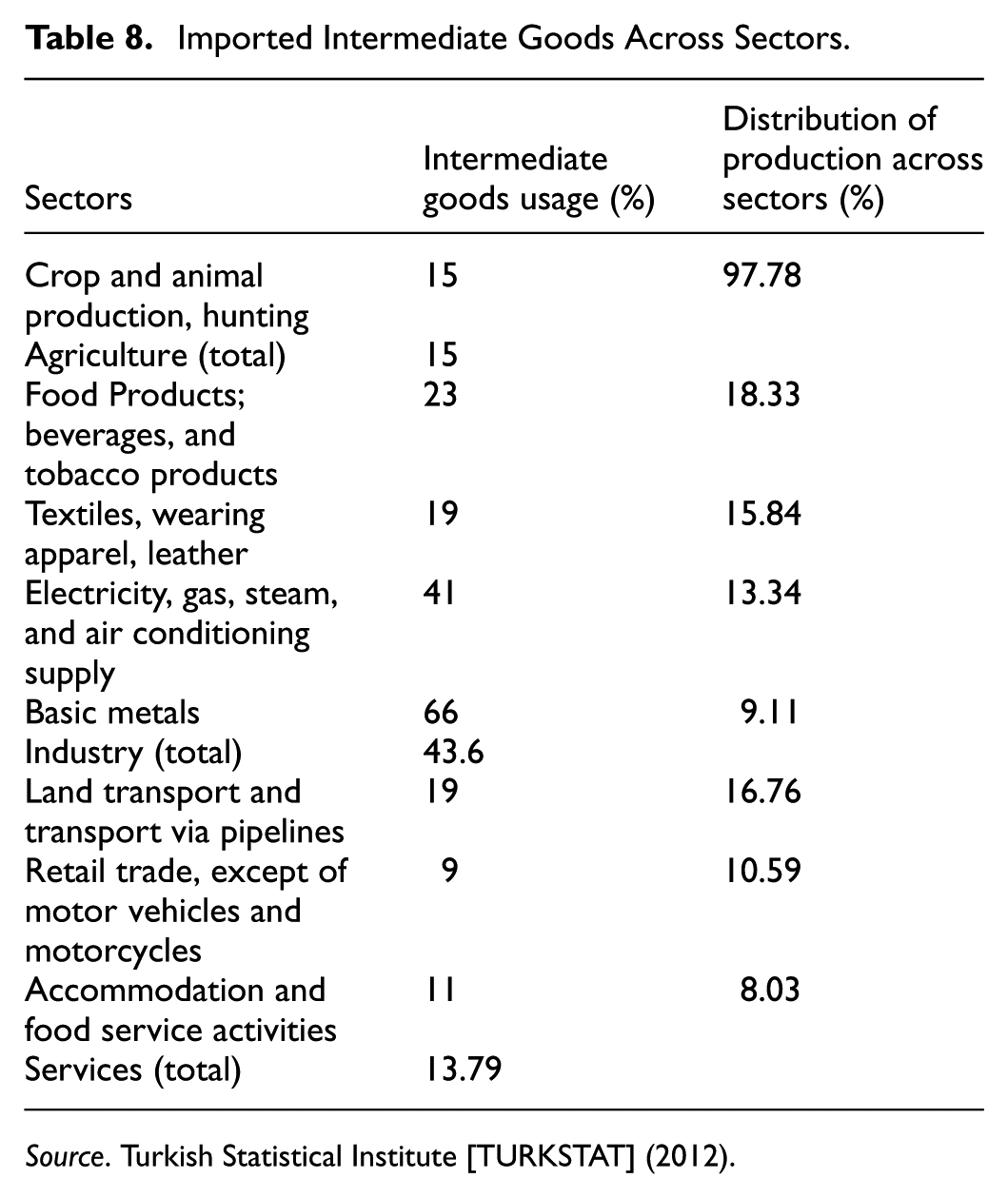

The findings indicate that the effects of exchange rate fluctuations in Türkiye differ between the long-term and short-term perspectives and can be analyzed through two distinct approaches. These findings support the argument that in economies with strong import dependence, exchange-rate appreciation enhances production through the cost channel, whereas depreciation raises input costs, particularly in agriculture (see Ben Salem et al., 2024; Chatziantoniou et al., 2023). Türkiye exhibits a significant dependence on imported inputs for production, as illustrated by the sectoral reliance rates presented in Table 8, which is derived from data obtained from the TURKSTAT. Such results challenge the validity of devaluation-based growth strategies in highly import-dependent economies, echoing concerns pertaining to contractionary devaluation and credibility constraints emphasized in previous studies (see Eichengreen & Hausmann, 1999; Krugman, 1998; Shang-Jin & Wu, 2002). An appreciation depreciation of the exchange rate stimulates sectoral production by lowering the cost of imported inputs, whereas a depreciation elevates the cost of imported inputs primarily in the agriculture sector, thereby influencing sectoral output via the cost channel.

Imported Intermediate Goods Across Sectors.

The empirical results demonstrate that this relationship holds true across all three sectors, with a more pronounced effect observed in the industrial and services sectors. Consequently, variations in the exchange rate, especially appreciation, are beneficial to sectoral production across all three sectors by not only decreasing costs but also mitigating risk and uncertainty. Nevertheless, the transmission of depreciation in the industrial and services sectors continues to be ambiguous. This situation can be interpreted as the positive impact of competitive advantage owing to exchange rate depreciation in exports counterbalanced by the adverse consequences of excessive import reliance, yielding an absence of a discernible net effect.

This finding prompts important questions on the efficacy of devaluation-centric growth strategies in countries heavily reliant on imported intermediate products, such as Türkiye, and indicates that devaluation fails to function as an effective instrument for growth and production. Additionally, the rise in production, recorded during periods of enhanced stability in the Turkish lira, indicates that fostering production in Türkiye is fundamentally reliant on sustaining cost stability and reducing uncertainty.

This observation is consistent with the high dependency rates on imported inputs in these sectors, as detailed in Table 8. For example, the proportion of imported intermediate goods in total inputs is 43.6% in the industrial sector, escalating to 90% in the manufacture of chemicals and chemical products and 81% in the manufacture of computer, electronic, and optical products. The agricultural and services sectors exhibit relatively similar rates of imported intermediate goods utilization. However, the more significant negative impact of exchange rate fluctuations on sectoral output in the services sector is attributed to the varying capacity to substitute imported inputs with domestic alternatives. Indeed, approximately 25% of the output in the services sector is derived from land transportation and pipeline transport, as well as retail trade, excluding motor vehicles and motorcycles. This segment predominantly utilizes high-tech products or other imported inputs, which often lack domestic substitutes. Conversely, the agricultural sector benefits from the availability of local substitutes for relatively simpler production inputs, and the depreciation period for imported machinery and equipment in this sector is extended. Consequently, it is comparatively easier to mitigate the impact of disruptions on agricultural input imports resulting from fluctuations in exchange rates. Furthermore, classical economic theory asserts that a depreciation (or appreciation) of the exchange rate is expected to confer a competitive advantage (or disadvantage) in exports, thereby resulting in an increase in economic production. However, based on the empirical evidence gathered in this study, this theory appears to hold true only in the short term for the industrial and services sectors in Türkiye during the period under analysis.

When examining the econometric results pertaining to the control variables incorporated into the model, it becomes apparent that the findings largely align with established economic theory. Specifically, exports produce a significant positive influence on output in all industries. Furthermore, shifts in global oil prices, another control variable, negatively influence sectoral production. Beyond the general findings, the models re-estimated with interactive dummy variables provide important insights into the structural differences between crisis and non-crisis periods. During the 2007 to 2009 global financial crisis and the 2020 COVID-19 pandemic, the adverse effects of exchange-rate appreciation on industrial and service sector output became markedly stronger, while the agricultural sector demonstrated relative resilience. These results suggest that exchange rate shocks amplify existing structural vulnerabilities during turbulent periods, particularly in sectors with high import dependency and financial exposure. In contrast, during non-crisis periods, exchange-rate depreciation appears to support production through cost stability and improved expectations, emphasizing that policy interventions should differ across economic conditions. Considering the results obtained, it is evident that Türkiye is negatively impacted by currency depreciation, which contradicts the predictions of classical economic theory. Consequently, it is advisable to implement structural policies aimed at decreasing reliance on imported inputs. Additionally, the findings concerning oil prices further substantiate this situation, highlighting the necessity of measures to mitigate energy costs and reduce dependence on external energy sources. Therefore, structural reforms that reduce import dependence and strengthen policy credibility appear crucial for stabilizing production under exchange-rate volatility (see Chakrabarti & Sen, 2023; IMF, 2022).

Conclusion

This study examined the asymmetric effects of exchange rate fluctuations on the agricultural, industrial, and service sectors of Türkiye over the period 2005 to 2023 by employing NARDL and ARDL models. The findings reveal that the transmission of exchange rate movements to sectoral output is highly uneven. Currency appreciation was found to enhance production in all sectors by lowering the cost of imported inputs and reducing uncertainty, whereas depreciation generally exerted contractionary effects—particularly in the agricultural sector—due to cost pressures arising from import dependence. The results further indicate that the short-term expansionary effects of depreciation on industrial and service sectors dissipate in the long run, suggesting that devaluation does not serve as a reliable instrument for sustained growth in an import-dependent economy such as Türkiye. From a policy perspective, these results underscore the importance of structural measures aimed at reducing production costs and dependency on imported intermediate goods. Enhancing domestic input capacity, improving energy efficiency, and strengthening monetary policy credibility would mitigate the adverse impacts of exchange rate volatility on production. Furthermore, the differentiated effects observed between crisis and non-crisis periods highlight the need for flexible and sector-specific policy responses. In this regard, exchange rate management alone is insufficient to foster sustainable sectoral growth without broader institutional and structural reforms that enhance resilience to external shocks.

Theoretical Implications

The Mundell-Fleming, Marshall-Lerner, and J-curve theories remain applicable to Türkiye, as confirmed by this research, which considers sectoral differences within the industrial and services sectors. This study contributes to the economic theory literature by highlighting these sectoral variations. The theoretical contributions of this research extend beyond this; it effectively addresses a gap in the existing literature. The findings presented have the potential to enhance the scientific impact of the research. The sectoral growth context explored by the research model can pave the way for empirical tests in different countries in future studies. Consequently, it will be possible to observe the effects of exchange rates across various sectors, not only in Türkiye but also in other developing nations. But, specifically in Türkiye, the exchange rate is significantly influenced not only by market dynamics but also by policy interventions. This may be considered a source of endogeneity, which could have affected our estimations. Furthermore, different variables could be incorporated into the research based on the input dependencies of the countries being studied. For instance, oil prices represent a significant input variable for Türkiye due to its considerable external dependence on energy. Additionally, the prices of fuels required for agricultural machinery in Türkiye are directly related to this dependency. Therefore, it is recommended that future studies include variables that may influence sectoral growth levels in countries from social, economic, political, and other perspectives, alongside exchange rates. Finally, the role of exports in the model is underscored by the critical importance of export-based growth for developing countries. Overall, the research assumes a supportive, contributory, and suggestive role for theory, literature, and future models.

Practical Implications

There are several important practical lessons to be drawn from this research for Türkiye, which could potentially be applied to other countries with similar characteristics in the agricultural, industrial, and service sectors. Considering the historical development of Türkiye’s agricultural sector, it can still be said that it holds significant agricultural production potential. Although the percentage of arable land is decreasing due to global warming, it is entirely possible to increase agricultural production through appropriate measures. On the other hand, despite Türkiye’s past agricultural advantages, it currently imports a substantial volume of agricultural products. This situation has led to difficulties for agricultural producers due to competitive pricing. Imported inputs, such as fertilizers and feed, further increase the risk posed by exchange rate fluctuations. The findings of this study explicitly demonstrate that an appreciation in the exchange rate contributes to a rise in sectoral output, whilst a depreciation in the exchange rate results in a plummet in sectoral output, offering a solid framework that underpins the aforementioned situation. These results suggest that a stable exchange rate is crucial for promoting an effective development framework in Türkiye’s agricultural production. Further, it is imperative that long-term policies should be formulated to reduce the agricultural sector’s reliance on imported inputs. Policies ought to concentrate on encouraging the production of agricultural inputs consisting of fertilizers, feed, medicines, and seeds in Türkiye, with a particular emphasis on promoting research and development activities associated with these inputs. Steps to further incentivize and support agricultural production as well as policies that facilitate the work of agricultural producers are crucial. These steps may include reintroducing low-cost fuel policies for farmers, providing maintenance support based on land size, and offering additional incentives based on the production of specialized agricultural products. The combined effect of these measures can further encourage growth in the agricultural sector. In terms of the industrial and service sectors, it is pertinent to recognize that the appreciation of the exchange rate has altered sectoral output to an extent that contradicts Classical Economic Theory. This situation, as previously stated, can be attributed to the significant reliance on imported inputs in emerging economies such as Türkiye. In addition, growth policies that involve devaluing the local currency, especially in the industrial and service sectors, are of inadequate relevance considering their substantial reliance on imported inputs. When examining the industrial and service sectors, the constricting effects of exchange rate increases present significant problems for Türkiye. The country’s social structure largely consists of individuals who have migrated from rural areas to cities, leaving behind agriculture to seek employment opportunities in industry, with many of these workers earning minimum wage. The sustainability of employment opportunities for this workforce is dependent on the expansion and increased production of the industrial and service sectors. However, rising exchange rates pose a major obstacle to this. Economic incentive regimes such as the inward processing regime, which is applied particularly in export-oriented sectors to provide cheaper inputs for industrialists, may not be a viable solution. This is because rising exchange rates increase the cost of inputs for local producers, even if they are tax-exempt. At this point, fiscal measures to stabilize the exchange rate or a focus on domestically substitutable products are necessary. Policymakers should conduct thorough reviews of products that can be sourced domestically and develop new projects that enable industrialists to obtain the inputs they need more affordably from within the country. On the other hand, the high profit expectations of capital also pose another risk, as exchange rate increases lead to a shift from production to exchange rate-based financial investments. This creates a second alternative for capital outflows from production, exacerbated by high interest rates that have been raised to reduce the exchange rate. As seen, additional variables related to social, political, and economic factors necessitate offering different recommendations for the production of Türkiye’s agricultural, industrial, and service sectors.

Footnotes

Appendix

Granger Causality Test.

| Agriculture | Industry | Services | ||||

|---|---|---|---|---|---|---|

| F-stat | [Prob] | F-stat | [Prob] | F-stat | [Prob] | |

|

:

does not Granger Cause |

1.005 | [0.371] | 2.175 | [0.122] | 2.657 | [0.078] |

|

: |

0.110 | [0.895] | 0.651 | [0.525] | 0.990 | [0.377] |

|

:

does not Granger Cause |

6.386 | [0.003] | 4.608 | [0.013] | 4.340 | [0.017] |

|

: |

1.954 | [0.150] | 1.450 | [0.242] | 1.278 | [0.285] |

|

: |

1.050 | [0.355] | 2.605 | [0.081] | 4.711 | [0.012] |

|

: |

0.044 | [0.956] | 0.739 | [0.481] | 1.482 | [0.235] |

|

: |

0.253 | [0.777] | 2.980 | [0.058] | 0.744 | [0.479] |

|

: |

0.378 | [0.686] | 0.835 | [0.438] | 0.490 | [0.614] |

Ethical Considerations

There are no human participants in this article.

Consent to Participate

Informed consent is not required.

Consent for Publication

All authors have approved the submission and publication of this manuscript in this journal.

Author Contributions

The authors have contributed equally to this work. All authors read and approved the final manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.

Disclosure Statement

The authors certify that they have NO affiliations with or involvement in any organization or entity with any financial interest (such as honoraria; educational grants; participation in speakers’ bureaus; membership, employment, consultancies, stock ownership, or other equity interest; and expert testimony or patent-licensing arrangements), or non-financial interest (such as personal or professional relationships, affiliations, knowledge or beliefs) in the subject matter or materials discussed in this manuscript.