Abstract

This study investigates the key determinants of voluntary tax compliance among Category “A” taxpayers in Hawassa City, Ethiopia, with a particular focus on the mediating role of public trust. Drawing on the Slippery Slope Framework and Deterrence Theory, the research examines how economic, psychological, cultural, and institutional factors shape taxpayers’ willingness to comply. Data were collected from 308 businesses using structured surveys, and the analysis employed structural equation modeling to test direct and indirect relationships. The findings reveal that while institutional and cultural factors have strong direct effects on compliance, economic, and psychological factors influence behavior indirectly through public trust. Public trust emerges as a critical mechanism, translating perceptions of fairness, transparency, and accountability into voluntary compliance. The study highlights the importance of designing tax policies that not only ensure enforcement but also build confidence in government institutions. Policy implications include enhancing transparency, leveraging local cultural networks, linking tax payments to visible public services, and tailoring outreach strategies to different demographic groups. By emphasizing trust-building alongside effective administration, the study provides actionable insights for fostering sustainable voluntary tax compliance in developing-country contexts.

Plain Language Summary

This study examines why some Category “A” taxpayers in Ethiopia voluntarily comply with tax regulations while others do not, using data from 308 business owners. The analysis demonstrates that compliance behavior is shaped by multiple factors, with public trust in government, perceptions of fair and consistent enforcement, and cultural norms exerting the strongest influence. Economic conditions and individual attitudes also contribute, but to a lesser extent. Using Partial Least Squares Structural Equation Modeling (PLS-SEM), the study identifies not only direct effects but also the mediating role of public trust in translating perceptions of fairness and legitimacy into actual compliance behavior. The findings emphasize that effective tax policy should integrate transparent governance, culturally relevant outreach, simplified procedures, and targeted taxpayer education. By doing so, authorities can foster voluntary compliance and support sustainable national development.

Introduction

Voluntary tax compliance is a complex phenomenon shaped by institutional, economic, psychological, cultural, and social factors. Research across different countries demonstrates that compliance is influenced not only by enforcement mechanisms but also by perceptions of fairness, legitimacy, and trust in government institutions. In Organisation for Economic Co-operation and Development (OECD) countries, studies have highlighted that taxpayers are more likely to comply when tax authorities combine strong enforcement with customer-oriented services, transparency, and procedural fairness (Kirchler et al., 2008; Sulestiyono et al., 2024). In Latin America, institutional trust and perceptions of corruption are key determinants, with compliance declining in contexts characterized by weak accountability and mismanagement of public funds (Daude et al., 2013). In Asia, psychological and cultural dimensions, such as social norms, religiosity, and collective values, play significant roles in shaping taxpayers’ willingness to comply beyond financial calculations (Chau & Leung, 2009; Loo et al., 2010). Meta-analyses reinforce this multidimensional view, showing that deterrence alone is insufficient and that psychological, institutional, and socio-cultural factors often exert stronger effects on voluntary compliance (Alm, 2019; Kirchler, 2017).

Ethiopia presents a particularly compelling case within this global context. Unlike OECD or Asian countries with mature tax systems, Ethiopia faces challenges including limited administrative capacity, low levels of public trust in institutions, and a highly diverse socio-cultural environment. These challenges underscore the importance of understanding not only how enforcement measures affect compliance but also how public trust mediates the relationship between institutional, economic, psychological, and cultural factors and taxpayer behavior. Public trust acts as a key mechanism, translating perceptions of fairness, transparency, and legitimacy into actual compliance decisions.

Raising adequate tax revenue to finance essential services such as healthcare, education, and infrastructure remains a persistent challenge in Ethiopia. Despite years of reform, the tax-to-GDP ratio has stagnated around 12%, below the African average of 16% (Adem et al., 2024). Low voluntary compliance contributes significantly to this shortfall, with many taxpayers paying only when enforcement compels them to do so. Encouraging voluntary compliance is therefore essential for sustainable revenue mobilization (Abdu & Adem, 2023; Kenno, 2020).

This study focuses on Category “A” taxpayers businesses with annual income exceeding one million birr because they are legally required to maintain formal records, submit regular returns, and pay key taxes such as Value-Added Tax (VAT) and business income tax. These businesses form the backbone of Ethiopia’s formal tax base but frequently underreport or fail to meet their full obligations (Kumi et al., 2023; Oktaviani & Triyani, 2023). Understanding the factors that encourage or hinder compliance among this group is critical for designing effective tax policies and enforcement strategies.

Several studies have highlighted the uneven nature of tax compliance in Ethiopia. A World Bank (2023) survey reported that nearly 70% of small and medium business owners in Addis Ababa avoided taxes, largely due to low trust in government and concerns about corruption. Conversely, visible public investments, such as the Addis Ababa Light Rail Transit, were associated with a 15% increase in compliance (Kassahun, 2020). Similarly, participatory infrastructure programs in the Amhara region, which allowed communities to vote on local priorities, enhanced taxpayers’ sense of ownership and trust, boosting compliance (Kassa, 2021; Tarekegn, 2015). In Hawassa, many businesses remained informal due to complicated registration procedures, high compliance costs, and fears of unfair treatment (Admasu & Shallo, 2018). Even among registered Category “A” taxpayers, compliance decisions depend on multiple factors, including clarity of tax rules, perceived fairness of audits, trust in officials, and cultural practices such as iddir, a traditional mutual support system (Biru, 2020; M. Tilahun, 2018; A. Tilahun & Yidersal, 2014).

The global literature emphasizes that voluntary compliance arises from a mix of external enforcement and internal motivations. Economic theories conceptualize taxpayers as rational actors weighing the risks of detection against benefits of evasion (Allingham & Sandmo, 2018; Manaye et al., 2020). Psychological perspectives highlight fairness, civic responsibility, and perceived legitimacy as drivers of behavior (Braithwaite, 2009). Social and cultural frameworks point to peer influence, collective norms, and community identity as key influences on compliance decisions (Richardson & Lanis, 2007). Empirical evidence increasingly supports a combined approach, suggesting that education, fair treatment, and strategic enforcement are more effective than punitive measures alone (Alm, 2019; Le et al., 2024; Thomas et al., 2024).

Within this framework, public trust serves as a mediating mechanism, linking perceptions of institutional fairness, economic and psychological conditions, and cultural norms to actual tax compliance behavior. For instance, even when enforcement mechanisms are present, taxpayers’ willingness to comply is strengthened when they perceive the government as fair, transparent, and accountable. Trust can therefore amplify the effect of economic incentives and psychological motivations, providing a pathway through which cultural and institutional factors translate into voluntary compliance.

Given these considerations, this study aims to examine how economic, psychological, cultural, and institutional factors influence voluntary tax compliance among Category “A” taxpayers in Hawassa City, Sidama Regional State, while explicitly testing the mediating role of public trust. By focusing on this taxpayer group, the study contributes to the broader understanding of compliance in developing countries and provides actionable insights for tax authorities seeking to improve revenue mobilization through policies that enhance both enforcement and legitimacy.

Theoretical Foundation

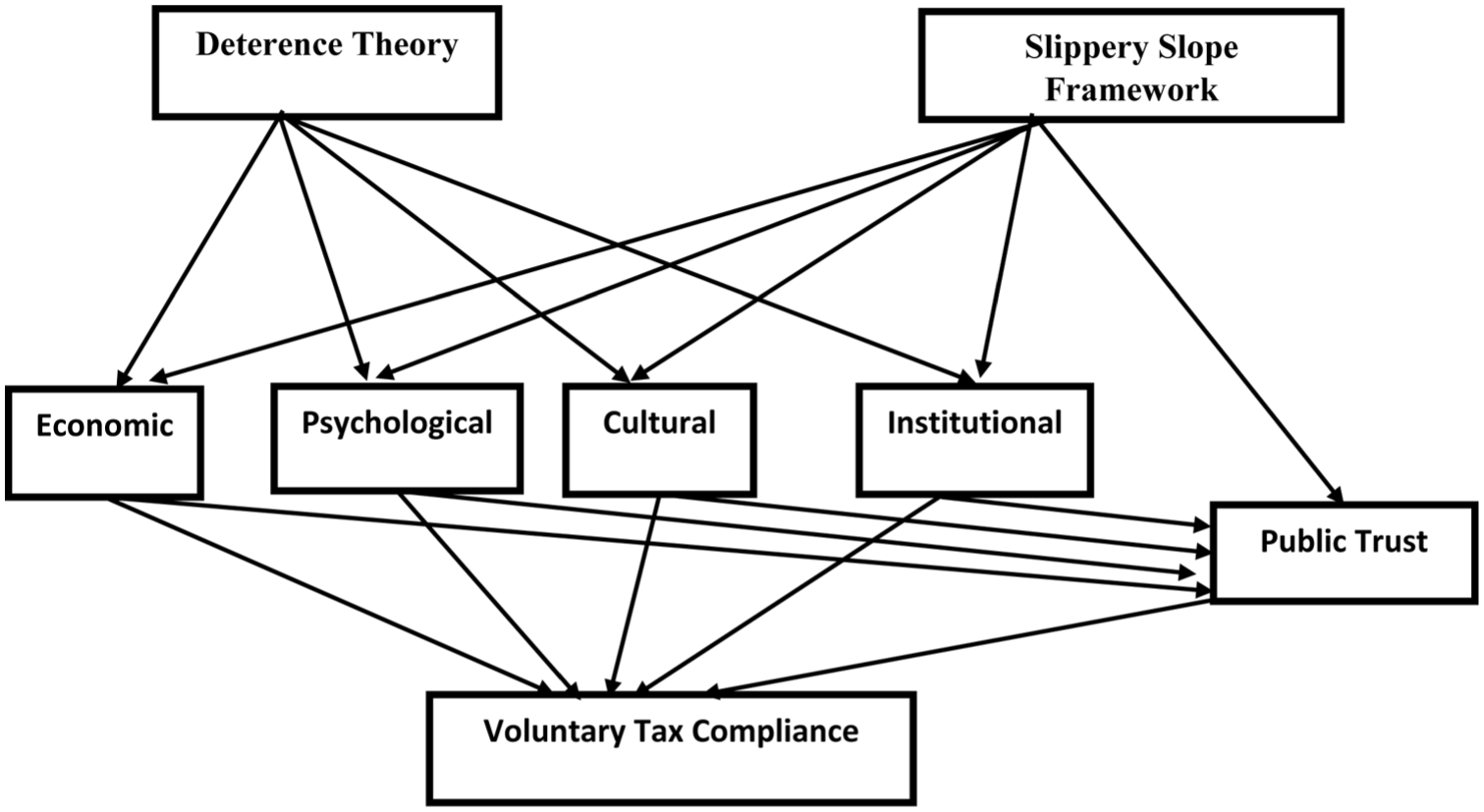

Voluntary tax compliance is a complex and multifaceted phenomenon influenced by economic, institutional, psychological, social, and demographic factors. Understanding these influences requires an integrated conceptual framework that reflects both the role of enforcement and the importance of trust. Two complementary theories offer valuable insight: Deterrence Theory and the Slippery Slope Framework (Figure 1).

Research model based on literature review.

Deterrence Theory views taxpayers as rational actors who weigh the costs and benefits of tax evasion. From this economic perspective, individuals are likely to comply when the risk of being audited and penalized outweighs the financial gains of non-compliance (Mwandu et al., 2024; Vibol, 2023). On the other hand, the Slippery Slope Framework explains compliance not only through fear of punishment but also through trust in authorities. When taxpayers believe that the government is fair, transparent, and uses tax revenues responsibly, they are more likely to comply voluntarily (Fauziati et al., 2020; Yahaya et al., 2023).

These two theories are not contradictory; rather, they complement each other by highlighting two essential forces that shape tax behavior: power (enforcement) and trust (legitimacy and fairness). Tax compliance, therefore, emerges from the interaction between external control mechanisms and internal motivations based on values, perceptions, and social norms.

Literature Review

Research on voluntary tax compliance spans diverse contexts, reflecting differences in governance systems, economic structures, and cultural norms. Economic factors, such as tax rates, complexity of the tax system, and perceived benefits of public services, have been shown to influence compliance across OECD countries, where studies emphasize the balance between enforcement and service quality (Baba, 2022; Kirchler et al., 2008). Psychological factors, including tax morale, perceived fairness, and attitudes toward authorities, are critical in Latin America, where low institutional trust and perceptions of corruption can weaken compliance (Batrancea et al., 2022; Daude et al., 2013; Jimenez & Iyer, 2016; Vincent, 2023). Social and cultural factors, such as social norms, religiosity, and collective values, are particularly influential in Asian contexts, shaping taxpayers’ willingness to comply beyond purely financial considerations (Chau & Leung, 2009; Dularif & Rustiarini, 2022; Górecki & Letki, 2021; Jibir et al., 2020; Loo et al., 2010).

Institutional factors, including enforcement effectiveness, audit likelihood, and transparency in the use of tax revenues, also play a key role. While these factors can directly affect compliance, research suggests that their impact is often mediated by public trust, which reflects taxpayers’ confidence that authorities act fairly, transparently, and in the public interest (Alm, 2019; Adem et al., 2024; Gobena, 2024). In other words, even well-designed enforcement and procedural systems may not fully translate into voluntary compliance unless taxpayers perceive them as legitimate and trustworthy.

Empirical evidence shows that public trust strengthens the effects of economic and psychological influences on compliance, as taxpayers are more willing to comply when they perceive fairness and accountability in the system (Daude et al., 2013; Kirchler et al., 2008). Social and cultural norms can shape behavior both directly and indirectly through trust, reinforcing collective responsibility and tax morale (Chau & Leung, 2009; Jibir et al., 2020; Loo et al., 2010). In developing countries like Ethiopia, weak institutional performance and historical experiences of corruption can weaken baseline trust, making public trust a particularly critical mediator in translating institutional reforms into voluntary compliance (Batrancea et al., 2022; Vincent, 2023).

Taken together, these findings highlight that voluntary tax compliance arises from the interplay of economic, psychological, social, and institutional factors, with public trust serving as a central mechanism linking these influences to actual compliance behavior (Adem et al., 2024; Alm, 2019; Gobena, 2024).

Ethiopia provides a particularly instructive setting within this global context. Unlike OECD or Asian countries with well-established tax systems, Ethiopia faces challenges such as limited administrative capacity, lower levels of public trust, and a highly diverse socio-cultural environment. These conditions make it important to understand not only the direct effects of enforcement, economic, and cultural factors on compliance, but also how these effects are channeled indirectly through public trust. By examining Ethiopia in this light, the study highlights both universal drivers of tax compliance and the unique institutional, social, and cultural conditions that shape taxpayer behavior in developing countries.

Hypothesis Development

Building on the theoretical foundations and reviewed literature, this study develops a set of hypotheses to explain the factors influencing voluntary tax compliance among Category “A” taxpayers in Ethiopia. Prior research indicates that compliance behavior emerges from a complex interaction of economic conditions, institutional quality, psychological motivations, and cultural norms. The Deterrence Theory underscores the role of enforcement mechanisms such as audits and penalties in shaping taxpayer behavior, while the Slippery Slope Framework emphasizes the importance of trust, legitimacy, and fairness in tax administration. Integrating these perspectives provides a more holistic understanding of compliance, recognizing that taxpayers’ decisions are influenced not only by external enforcement but also by internalized trust and moral commitment.

Within this framework, public trust is conceptualized as a mediating mechanism that links contextual and individual factors to compliance behavior. Trust reflects taxpayers’ belief in the integrity, fairness, and effectiveness of government institutions and their confidence that tax revenues are managed for the collective good. When trust is high, the influence of economic, psychological, cultural, and institutional factors on compliance is likely to be strengthened, fostering a cooperative rather than coercive tax relationship. Accordingly, this study proposes that public trust mediates the relationships between these key determinants and voluntary tax compliance behavior among Category “A” taxpayers in Hawassa City, Sidama Regional State, Ethiopia.

Economic Factors

From an economic standpoint, compliance is shaped by how taxpayers assess the risks and rewards of their actions. Taxpayers may attempt to lower their liabilities by underreporting income, especially if they believe they will not be caught (Njunwa & Batonda, 2023). However, higher risks of audits and penalties as explained in Deterrence Theory can discourage this behavior. Perceptions about the efficiency of government spending and the fairness of tax rates also influence economic decisions (Mwandu et al., 2024; Omary & Pastory, 2022). Thus, economic factors such as audit frequency, tax burden, and perceived utility of taxes play a key role in shaping behavior. Based on the above review, the following hypothesis were framed:

Psychological Factors

The psychological dimension emphasizes how fairness, moral obligation, and emotional responses like guilt and shame influence compliance. Taxpayers who feel the system is unfair may rationalize evasion as acceptable behavior. As noted by Mchukwa and Mbwambo (2024), individuals adjust their behavior when they perceive inequality in tax payments compared to others. Those who are told they pay more than others are more likely to evade, while those who believe they pay less are more likely to comply. These findings align with the trust dimension of the Slippery Slope Framework, which argues that perceived fairness builds legitimacy, encouraging voluntary compliance. Based on the above review, the following hypothesis were framed:

Cultural Factors

Culture and social norms contribute significantly to shaping tax behavior. When communities value honesty and collective responsibility, taxpayers are more likely to comply due to social expectations (Palil & Mustapha, 2011). Compliance is also influenced by how individuals perceive the government’s use of public funds and whether tax practices are aligned with communal values (Chindengwike & Kira, 2022). Kirchler (2017) emphasized the importance of ethical behavior from leadership in reinforcing compliance within organizations. These cultural expectations reflect the horizontal trust component of the Slippery Slope Framework, where mutual trust among taxpayers reinforces voluntary compliance. Based on the above review, the following hypothesis were framed:

Institutional Factors

Institutional trust and credibility play a central role in compliance. When tax authorities are perceived as transparent, efficient, and supportive, compliance increases. Conversely, inconsistent enforcement or weak administrative capacity can erode trust and fuel non-compliance (Chindengwike & Kira, 2022; Skliar, 2021). Access to expert advice and peer behaviors in similar firms also influence how institutions are perceived. This aligns with the vertical trust aspect of the Slippery Slope Framework highlighting the importance of a reliable and fair authority to sustain voluntary compliance. Based on the above review, the following hypothesis were framed:

Public Trust

A growing body of literature underscores the importance of trust in government and tax authorities as a key determinant of voluntary tax compliance. Trust is conceptualized as taxpayers’ belief in the integrity, fairness, and transparency of government institutions, as well as confidence that tax revenues will be used responsibly (Kirchler et al., 2008; Prastiwi et al, 2023). When taxpayers trust that authorities are just and efficient, they are more inclined to see tax payment not merely as an obligation enforced by sanctions, but as a civic duty to support public goods and services (Alm & Torgler, 2006). Empirical studies across different cultural and institutional contexts consistently demonstrate that higher levels of public trust are associated with higher levels of voluntary compliance (e.g., the slippery slope framework research in Ethiopia, Germany, and Indonesia). Based on the above review, the following hypothesis was framed:

Public Trust as a Mediator

Prior studies highlight that public trust plays a vital role in connecting both institutional and individual factors to voluntary tax compliance. Trust represents taxpayers’ confidence that government institutions act fairly, transparently, and responsibly, and that tax revenues are used to support the common good (Nichelatti & Hiilamo, 2024). When people believe the tax system is fair, the economy is managed justly, and public resources are used appropriately, they are more likely to trust government institutions an attitude that naturally promotes voluntary compliance (Kiptum et al, 2024).

From an economic standpoint, perceptions of fairness and the efficient use of public funds enhance citizens’ belief that the government is worthy of their compliance (Batrancea et al., 2022). Psychological influences, including moral values, perceived justice, and personal satisfaction, also help build trust, which subsequently leads to more cooperative tax behavior (Ciziceno & Pizzuto, 2022). Likewise, cultural norms and shared values shape how individuals perceive government legitimacy and collective responsibility, reinforcing trust across society (Gobena, 2024). Furthermore, strong institutional quality expressed through transparent processes, efficient service delivery, and fair enforcement strengthens confidence in public institutions and encourages taxpayers to comply willingly (Kogler et al., 2023). Grounded in these theoretical and empirical perspectives, this study posits that public trust acts as a mediating mechanism between contextual factors and voluntary tax compliance behavior. Therefore, the following hypotheses are proposed:

Methods and Materials

Study Design and Setting

This study employed a quantitative research design to examine how economic, psychological, cultural, institutional, and demographic factors influence the voluntary tax compliance behavior of Category “A” taxpayers in Hawassa City, Ethiopia. As the capital of the Sidama Regional State and one of Ethiopia’s most economically active cities, Hawassa provides a relevant and dynamic setting to explore business tax behavior within a developing country context.

Study Population and Sampling

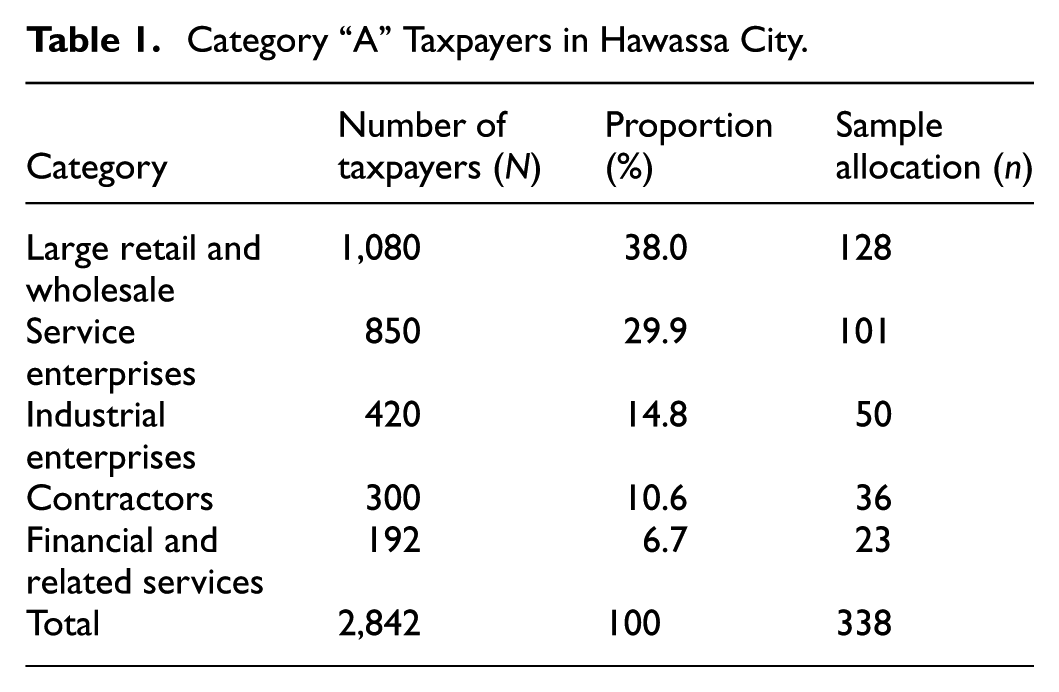

The study focused on Category “A” taxpayers in Hawassa City. According to Ethiopian tax law, this group includes businesses with an annual turnover of at least one million Ethiopian Birr (ETB). Category “A” taxpayers are legally required to maintain proper books of accounts and submit annual tax returns, which makes them a key group for examining voluntary tax compliance. At the time of the study, there were 2,842 registered Category “A” taxpayers in Hawassa City.

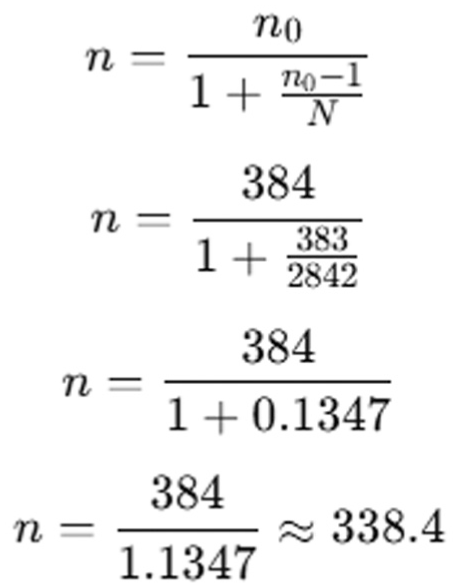

To determine the sample size, Cochran’s (1977) formula for finite populations was applied. Based on a 95% confidence level, a 5% margin of error, and the finite population correction, the required sample was calculated to be 338 taxpayers. The sample was proportionally allocated across business sectors to ensure representativeness (see Table 1).

Category “A” Taxpayers in Hawassa City.

Here to draw the actual sample size, Cochran (1977) formula was used where no denotes the initial sample size for an infinite population, N represents the total population size, and n is the adjusted sample size after applying the finite population correction (Figure 2).

Formula used to find Participant Sample.

The sampling frame targeted business owners and managers, as they are directly responsible for tax-related decisions and financial reporting. A probability-based sampling approach was employed to ensure that different business sectors were appropriately represented.

Data collection took place in January 2025 using a structured, self-administered questionnaire. Of the 338 questionnaires distributed, 308 were completed and returned, yielding a valid response rate of 91.12%. This high rate of participation enhanced the reliability of the findings and reduced concerns about non-response bias.

Data Collection Instrument

The questionnaire aimed to gather both basic background details and the personal views of respondents on the factors influencing tax compliance. To make sure everyone could clearly express their opinions, each item was rated on a five-point scale, from 1 (strongly disagree) to 5 (strongly agree). Questions related to voluntary tax compliance were adapted from Kastlunger et al. (2010), while questions on economic, psychological, cultural, institutional, and demographic factors were based on and modified from the work of Alm et al. (2011). All items were carefully reviewed and adjusted to reflect the Ethiopian context, using feedback from a pretest to ensure that they were easy to understand and culturally relevant. Business-related background details like the age of the business and number of employees were organized using internationally accepted definitions. For instance, businesses were grouped by age into start-ups (less than 5 years), growing firms (5–10 years), and mature enterprises (over 10 years). The number of employees was classified according to Ethiopian and World Bank standards into micro (1–5), small (6–30), medium (31–100), and large (over 100) enterprises. These adjustments were made to ensure that the study’s demographic data were meaningful and aligned with global standards.

Data Analysis

The data were analyzed using Partial Least Squares Structural Equation Modeling (PLS-SEM) in SMART PLS 3.0, a method well-suited for complex models that include multiple latent variables. This approach allows researchers to assess both the measurement of constructs and the relationships between them simultaneously (Chin, 1998). To ensure the measurement model was reliable and valid, several checks were conducted. Internal consistency was evaluated using Cronbach’s alpha and composite reliability, while convergent validity was assessed through the Average Variance Extracted (AVE). Discriminant validity was confirmed using both the Fornell–Larcker criterion and the Heterotrait–Monotrait (HTMT) ratio. These steps ensured that the survey items accurately captured the theoretical constructs and measured distinct concepts.

The structural model was then evaluated to understand how well the independent variables explained variations in voluntary tax compliance behavior. The coefficient of determination (R2) measured how much of the variation in the dependent constructs could be explained by the predictors. Predictive relevance (Q2) was assessed using blindfolding procedures, indicating whether the model could reliably predict outcomes for new observations. Finally, effect size (F2) quantified the relative influence of each predictor on the outcome variables, highlighting which factors had the strongest impact on taxpayer compliance. Taken together, these analyses provided a robust and comprehensive evaluation of both the explanatory and predictive strength of the model.

Ethical Procedures

Ethical approval for this study was granted and participation was entirely voluntary, and oral informed consent was obtained after participants were informed about the study’s objectives, procedures, and their right to withdraw at any time without consequence. Confidentiality and anonymity were strictly maintained, with only de-identified data accessible to the researchers. No minors were involved, and all procedures complied with established ethical standards for research involving human participants.

Results and Discussion

Demographic Profile of Respondents

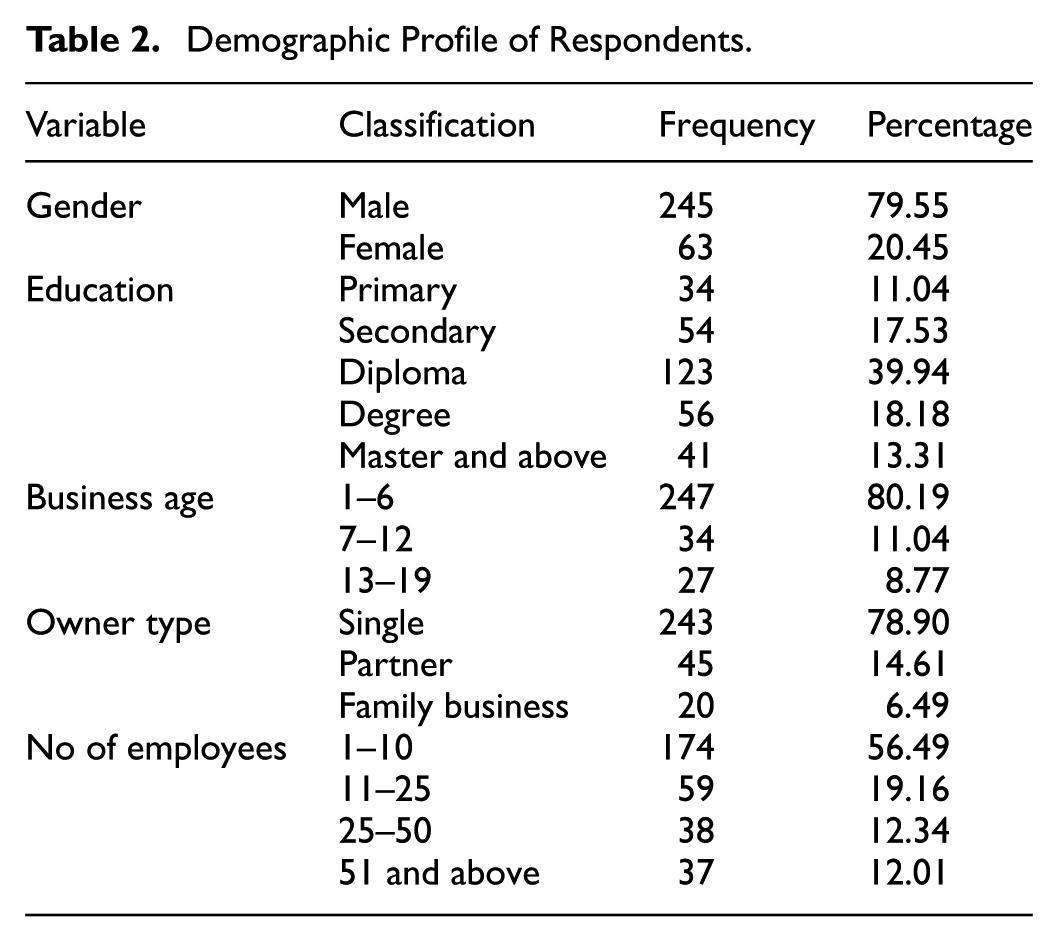

Table 2 presents the demographic attributes of the participants. 245 (79.55%) of the 308 responders are men, and the remaining 20.45% are women. Regarding the respondents’ educational background, the majority (39.94%) had a diploma, 11.08% had a primary education, 17.53% had completed secondary school, 18.18% had a degree, and 13.31% had a master’s degree or higher. Additionally, the results show that 80.19% of Category “A” taxpayers have been in business for 1 to 5 years. The majority of Category “A” taxpayers are sole proprietorships, according to the results of owner type. From 243 (78.90%) of the 308 Category “A” taxpayers that were taken into consideration are sole proprietorships, 14.61% are partnerships, and the remaining 6.49% are family-owned enterprises.

Demographic Profile of Respondents.

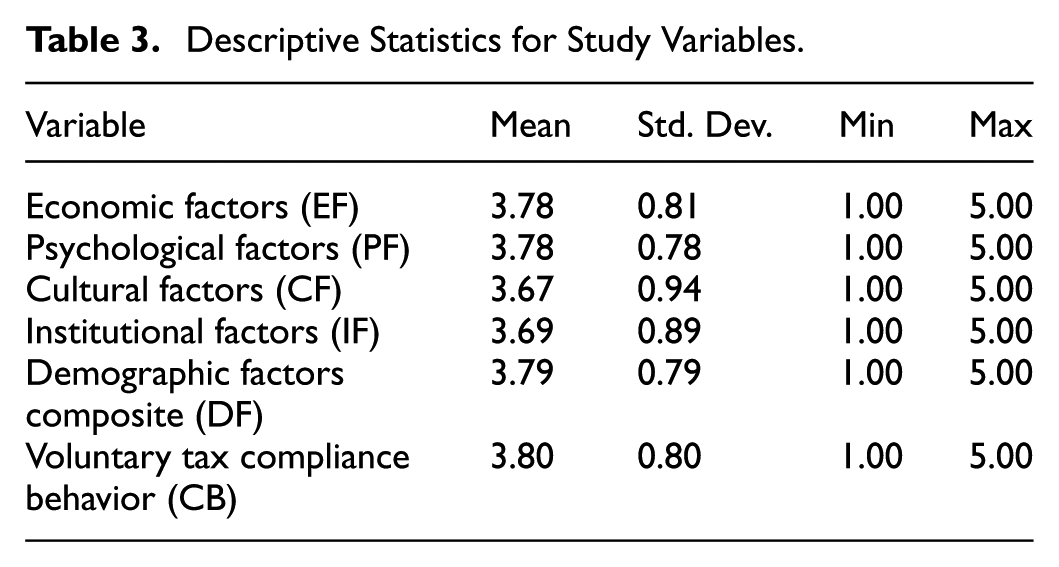

The descriptive results in Table 3 show how respondents generally perceive the main factors that influence voluntary tax compliance. The mean scores for all variables fall between 3.67 and 3.80, which are above the average point of the 5-point scale. This indicates that most taxpayers tend to agree positively with the statements related to each construct. Among the variables, voluntary tax compliance behavior has the highest mean score (3.80), suggesting that respondents generally display a strong willingness to comply with tax obligations. Similarly, both economic factors (mean = 3.78) and psychological factors (mean = 3.78) received relatively high ratings, implying that financial considerations such as the perceived fairness of the tax rate and psychological aspects like moral duty and personal satisfaction are important influences on compliance behavior.

Descriptive Statistics for Study Variables.

Cultural factors have a slightly lower mean value (3.67), showing moderate agreement among taxpayers that cultural norms, shared beliefs, and community expectations affect their tax decisions. The mean score for institutional factors (3.69) reflects that respondents generally view the tax system and its administration as fairly credible and trustworthy. Likewise, demographic factors (3.79) show a consistent pattern, indicating that variations in age, education level, or income may shape individuals’ attitudes toward tax compliance to some extent. Generally, the results suggest that taxpayers hold positive views toward both personal and external factors that encourage voluntary tax compliance. The standard deviations (ranging from 0.78 to 0.94) show moderate variation in responses, meaning that while opinions differ slightly, most respondents share a similar outlook. In summary, the findings highlight that the study participants perceive economic, psychological, cultural, institutional, and demographic factors as meaningful elements that shape their compliance behavior. These insights were further validated through the structural model results. Institutional factors showed the strongest influence on voluntary tax compliance behavior (β = 0.353, p < .001), reinforcing the idea that trust in the tax system plays a central role. Cultural factors (β = 0.248) followed closely, confirming the power of social influences in motivating compliance. Economic factors (β = 0.212) and demographic factors (β = 0.186) also had significant effects, demonstrating that both rational cost-benefit calculations and personal characteristics shape compliance behavior. Although psychological factors had the smallest path coefficient (β = 0.110), they were still statistically significant, suggesting that internal values like fairness and duty are relevant, even if secondary to institutional and social drivers.

Together, these findings paint a nuanced picture of voluntary tax compliance in Ethiopia. Compliance behavior is driven not by a single factor, but by a complex interplay of institutional trust, cultural expectations, economic reasoning, and individual background. Understanding this interplay can help policymakers move beyond punitive enforcement and toward strategies that foster a more transparent, fair, and citizen-centered tax system one that people are willing to support not out of fear, but out of shared responsibility.

Measurement Model Analysis Results

Reliability and Validity Tests

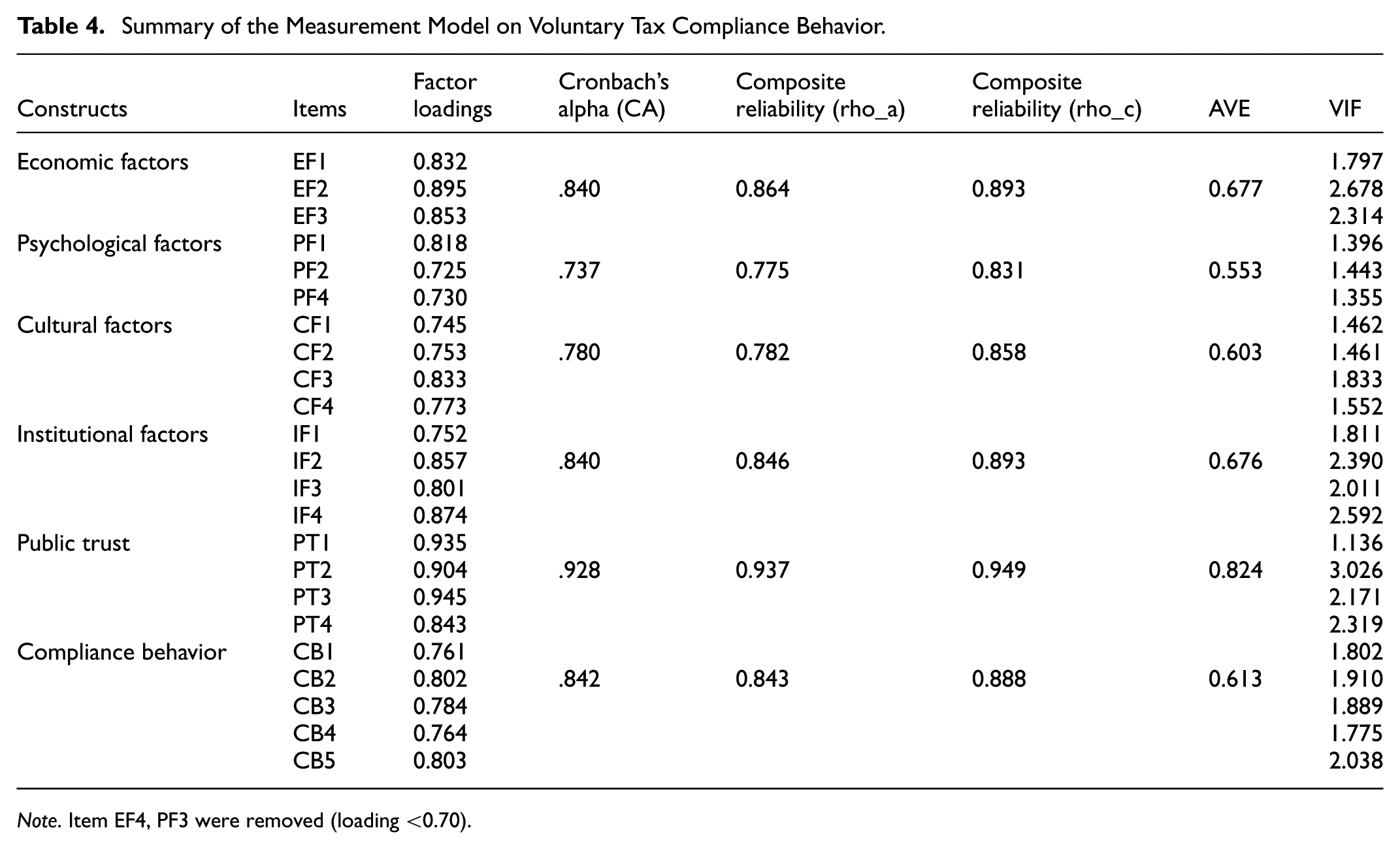

The measurement model was assessed to ensure the reliability and validity of the constructs used to explain voluntary tax compliance behavior. As shown in Table 4, all standardized factor loadings exceeded the recommended threshold of 0.70, except for two items (EF4 and PF3), which were removed to improve construct reliability and model fit. The retained items for each construct demonstrated strong factor loadings ranging from 0.725 to 0.945, confirming that the observed indicators are well-representative of their underlying latent variables.

Summary of the Measurement Model on Voluntary Tax Compliance Behavior.

Note. Item EF4, PF3 were removed (loading <0.70).

The internal consistency of each construct was verified through Cronbach’s Alpha (CA), composite reliability (rho_c), and rho_a, all of which surpassed the accepted minimum value of 0.70. Specifically, Cronbach’s Alpha values ranged between 0.737 and 0.928, and composite reliability values ranged from 0.831 to 0.949 (Figure 3), indicating that the measurement items for each construct consistently reflect the intended concept. In addition, the Average Variance Extracted (AVE) values for all constructs were above the 0.50 benchmark (ranging from 0.553 to 0.824), confirming satisfactory convergent validity that is, the items within each construct share a high proportion of common variance.

Measurement model.

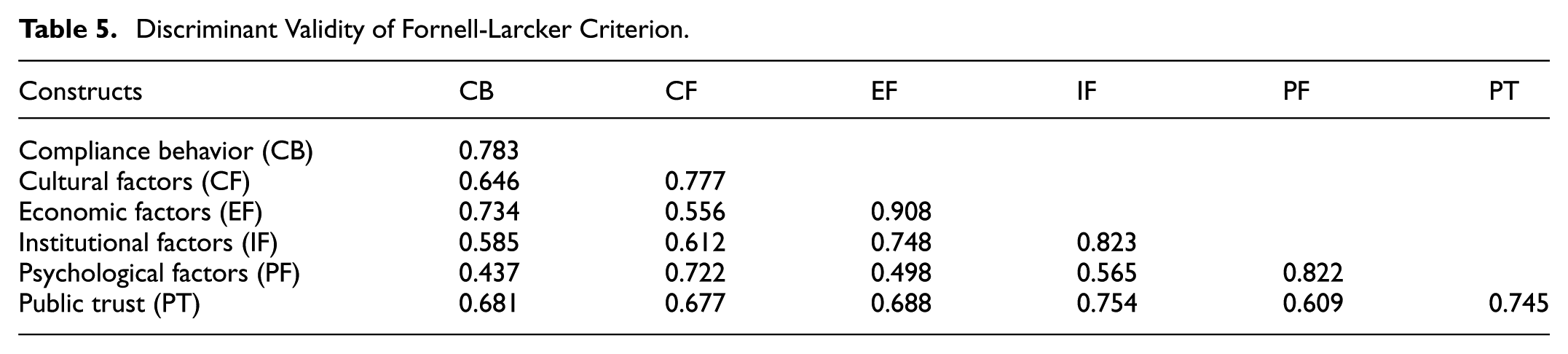

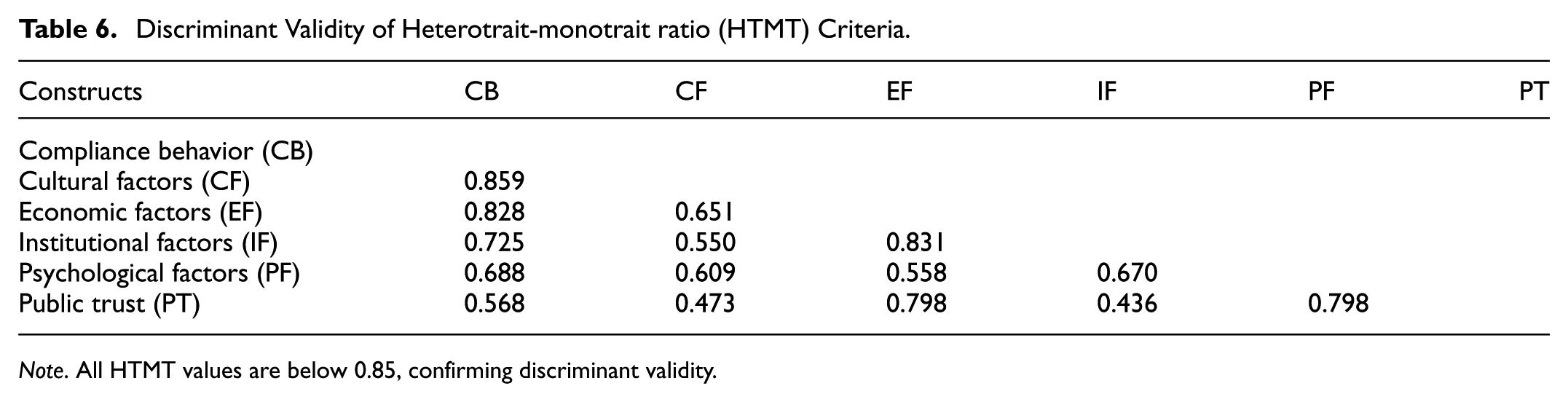

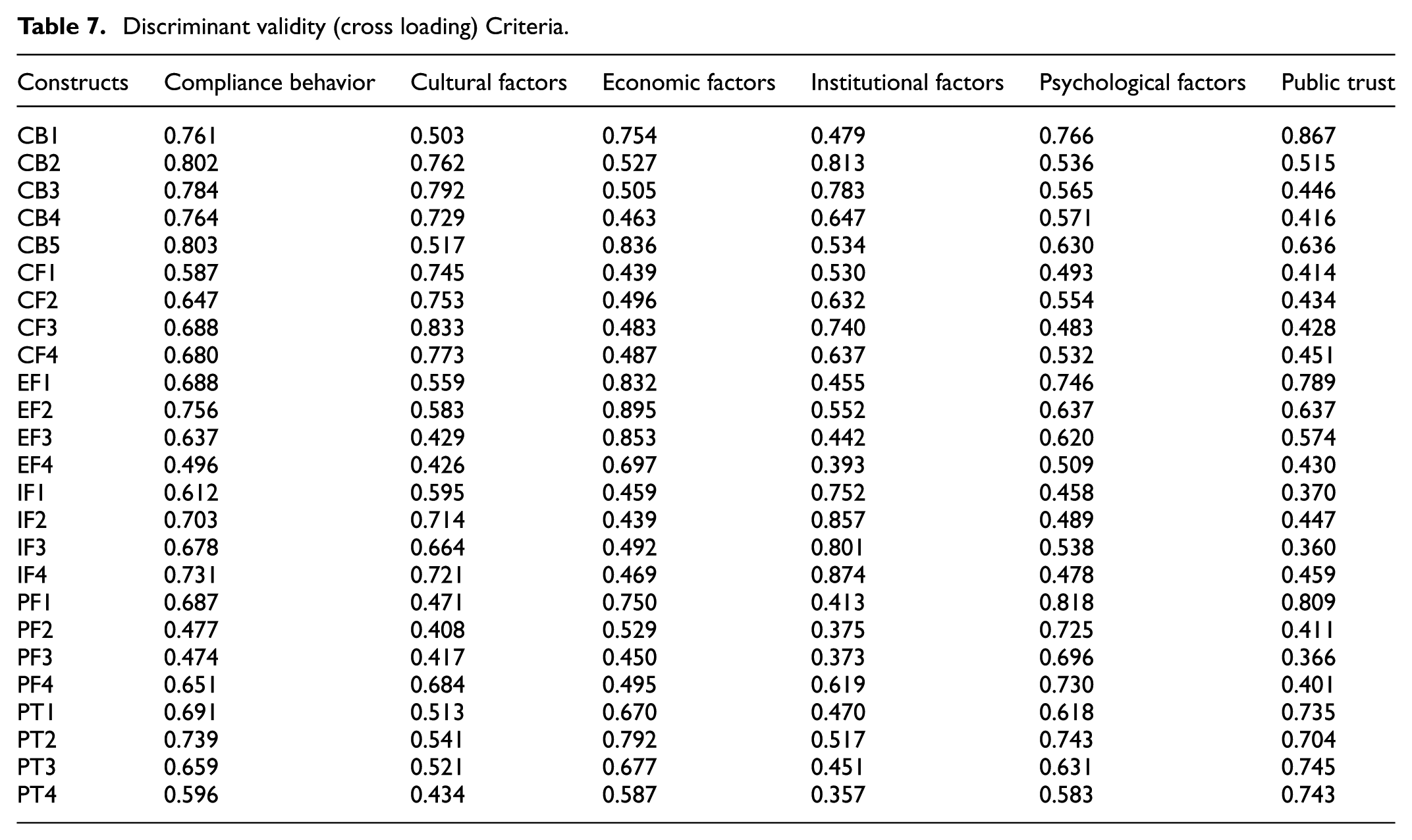

Discriminant validity was examined using the Fornell–Larcker criterion, HTMT ratio, and cross-loading tests. According to the Fornell–Larcker results, the square roots of the AVE values (diagonal elements) were greater than the corresponding inter-construct correlations, confirming that each construct is distinct from the others (Table 5). This finding was further supported by the HTMT ratios, all of which were below the conservative threshold of 0.85, providing additional evidence of discriminant validity (Table 6). Similarly, the cross-loading matrix (Table 7) showed that each item loaded higher on its respective construct than on any other latent variable, reinforcing the conclusion that the constructs are empirically distinct (Henseler et al., 2015). Taken together, these results demonstrate that the measurement model satisfies the necessary psychometric criteria for reliability, convergent validity, and discriminant validity.

Discriminant Validity of Fornell-Larcker Criterion.

Discriminant Validity of Heterotrait-monotrait ratio (HTMT) Criteria.

Note. All HTMT values are below 0.85, confirming discriminant validity.

Discriminant validity (cross loading) Criteria.

The Variance Inflation Factor (VIF) values for all measurement items range from 1.136 to 3.026, which are well below the recommended threshold of 5.0 for assessing multicollinearity in PLS-SEM. Moreover, all VIF values are below the more stringent cutoff of 3.3 suggested by Kock (2015) for evaluating full collinearity and potential common method bias. These results indicate that multicollinearity among the indicators is not a concern, and no evidence of common method bias is detected. Consequently, the measurement model demonstrates adequate indicator independence, supporting the robustness and stability of the estimated parameters. Overall, these results confirm that the measurement model is reliable and valid, providing a robust foundation for testing the proposed moderation effects in the structural model.

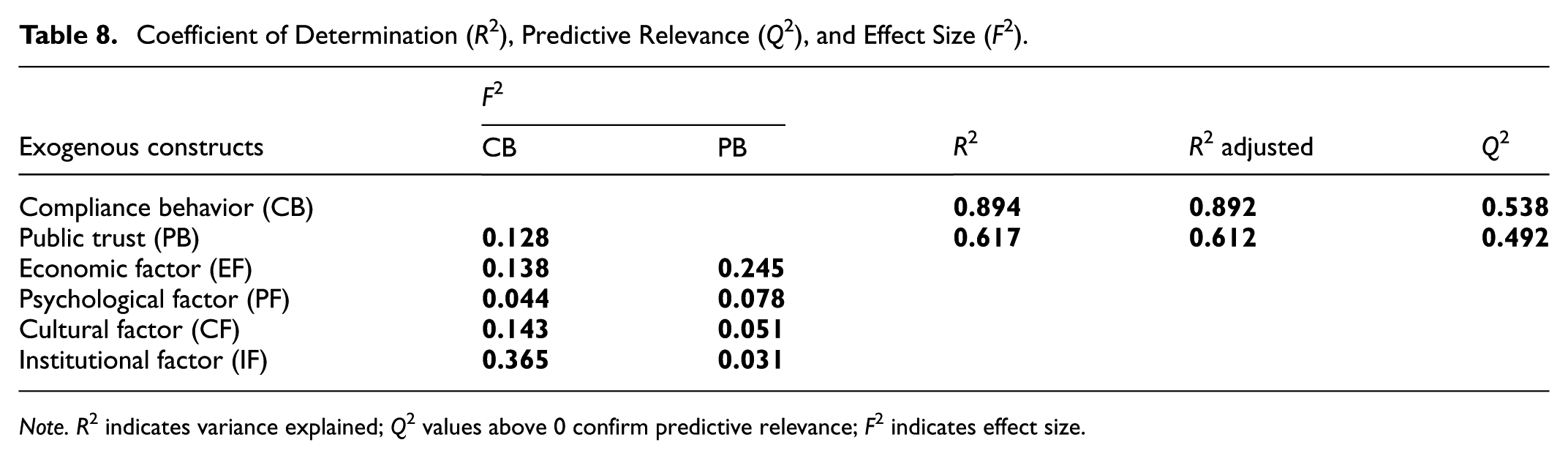

Table 8 presents the results of the coefficient of determination (R2), predictive relevance (Q2), and effect size (F2) for the endogenous constructs in the structural model. The R2 value for Compliance Behavior (CB) is 0.894, indicating that approximately 89.4% of the variance in voluntary tax compliance behavior is explained by the model’s exogenous variables. This represents a very strong explanatory power, suggesting that the combined effects of economic, psychological, cultural, institutional, and public trust factors provide a highly reliable prediction of taxpayers’ compliance behavior. Similarly, Public Trust (PB) recorded an R2 value of 0.617, implying that about 61.7% of the variance in public trust is explained by the selected independent constructs. According to Cohen’s (1988), these values reflect substantial predictive strength, demonstrating that the model fits the observed data well.

Coefficient of Determination (R2), Predictive Relevance (Q2), and Effect Size (F2).

Note. R2 indicates variance explained; Q2 values above 0 confirm predictive relevance; F2 indicates effect size.

The Q2 values further confirm the model’s predictive relevance. A Q2 value greater than zero signifies that the model has acceptable predictive accuracy. The Q2 values further confirm the model’s predictive relevance. A Q2 value greater than zero indicates that the model possesses predictive relevance for a given endogenous construct. The Q2 values of 0.538 for compliance behavior and 0.492 for public trust demonstrate substantial predictive relevance, suggesting that the model has a strong capability to reproduce the observed data through the blindfolding procedure. According to Hair et al. (2019), Q2 values above 0.35 indicate high predictive relevance. Therefore, the results suggest that the model has strong predictive power and practical applicability in explaining and predicting compliance behavior and public trust beyond the sample used in this study.

Regarding the effect size (F2), the results indicate varying degrees of influence among the exogenous constructs. The largest effect was observed for institutional factors (F2 = 0.365), suggesting that improvements in institutional quality, fairness, and transparency have the strongest impact on taxpayers’ voluntary compliance. This finding makes sense in the Ethiopian context, where the credibility of institutions, the fairness of the tax system, and the strength of enforcement are critical for shaping taxpayers’ willingness to comply. Similar patterns have been observed in other developing countries, where weak institutional structures often undermine compliance (Kirchler et al., 2008). Cultural factors (F2 = 0.143) and economic factors (F2 = 0.138) also exhibit moderate effects, highlighting the importance of societal values and financial considerations in shaping compliance attitudes. This suggests that social norms, income levels, perceptions of fairness, and taxpayer characteristics such as education and age all play meaningful roles in explaining why people comply. These results align with earlier studies showing that in developing economies, community values and perceptions of fairness often weigh heavily on compliance decisions (Cahyonowati et al., 2023). In contrast, psychological factors (F2 = 0.044) and public trust (F2 = 0.128) show relatively smaller but still meaningful effects, implying that while moral motivation and trust in government play a role, their individual contributions are comparatively modest. This reflects the reality in Ethiopia and similar contexts, where individual motivation is often overshadowed by systemic issues such as institutional trust and the perceived legitimacy of the tax system (Alm, 2019).

Generally, the results confirm that the model demonstrates strong explanatory and predictive validity, with institutional, cultural, and economic dimensions exerting the most substantial influence on voluntary tax compliance. These findings reinforce the idea that fostering an enabling institutional environment and strengthening trust-based relationships between taxpayers and tax authorities are essential strategies for improving voluntary compliance in the Ethiopian context.

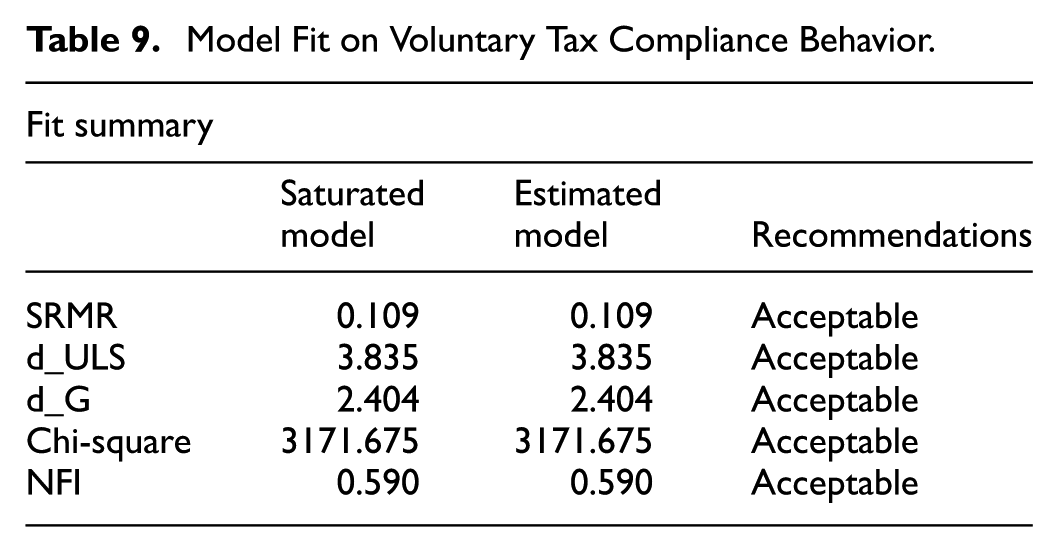

Table 9 shows the overall quality of the structural model, several model fit indices were evaluated. The Standardized Root Mean Square Residual (SRMR) was 0.109, which falls within the acceptable range, indicating that the difference between the observed and predicted correlations is reasonably low. Similarly, both the squared Euclidean distance (d_ULS = 3.835) and the geodesic distance (d_G = 2.404) were within acceptable thresholds, suggesting a good approximation between the model-implied and empirical correlation matrices. The chi-square value of 3171.675, though large as is typical in large-sample structural models was deemed acceptable in the context of Partial Least Squares Structural Equation Modeling (PLS-SEM), where chi-square statistics are often less emphasized due to their sensitivity to sample size. The Normed Fit Index (NFI) value of 0.590, while modest, also falls within an acceptable range for PLS-SEM applications, particularly in exploratory studies. Overall, these fit indices support the adequacy of the model in capturing the underlying relationships among the study constructs and provide confidence in the validity of the SEM results.

Model Fit on Voluntary Tax Compliance Behavior.

Direct Effects

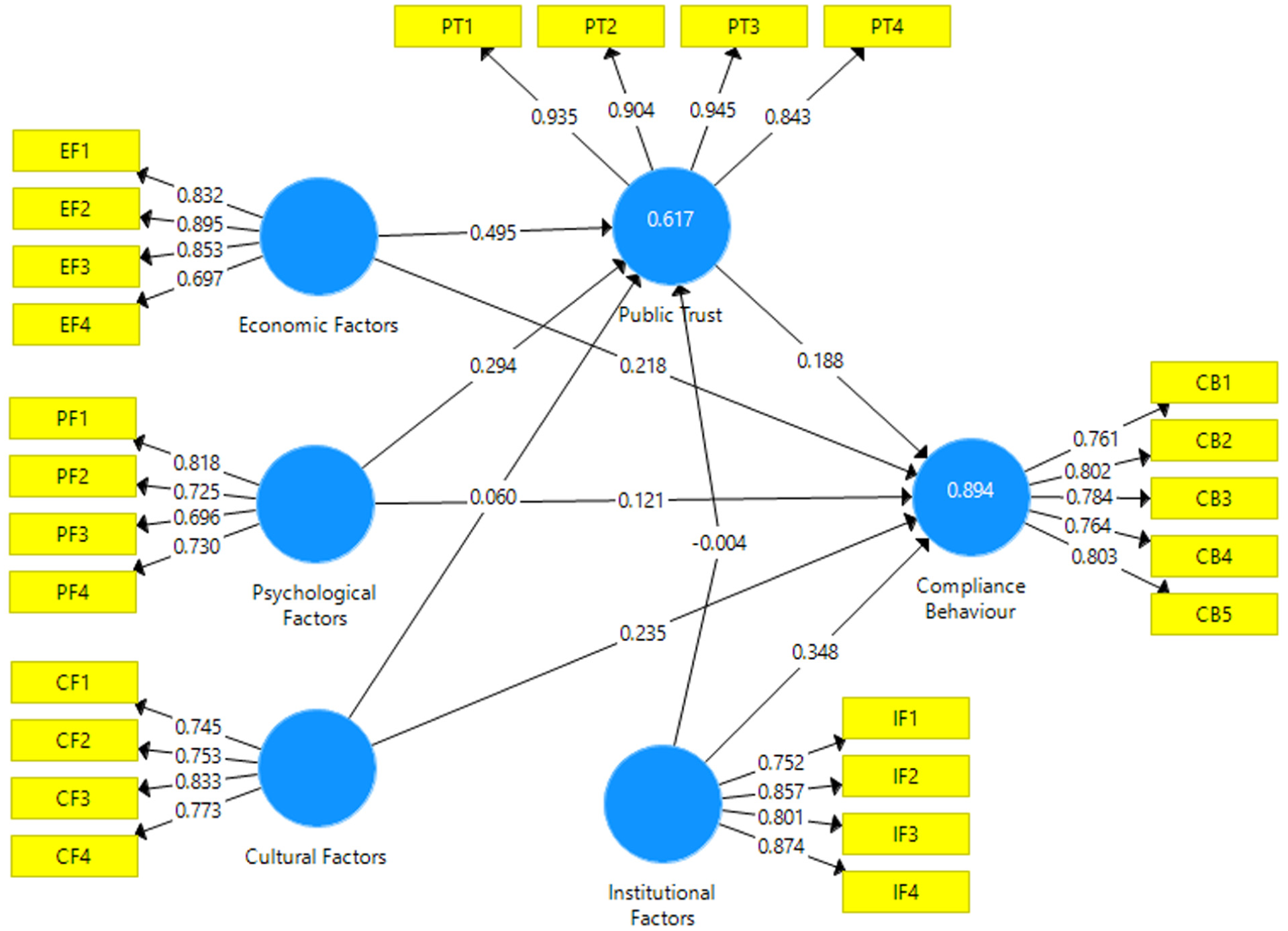

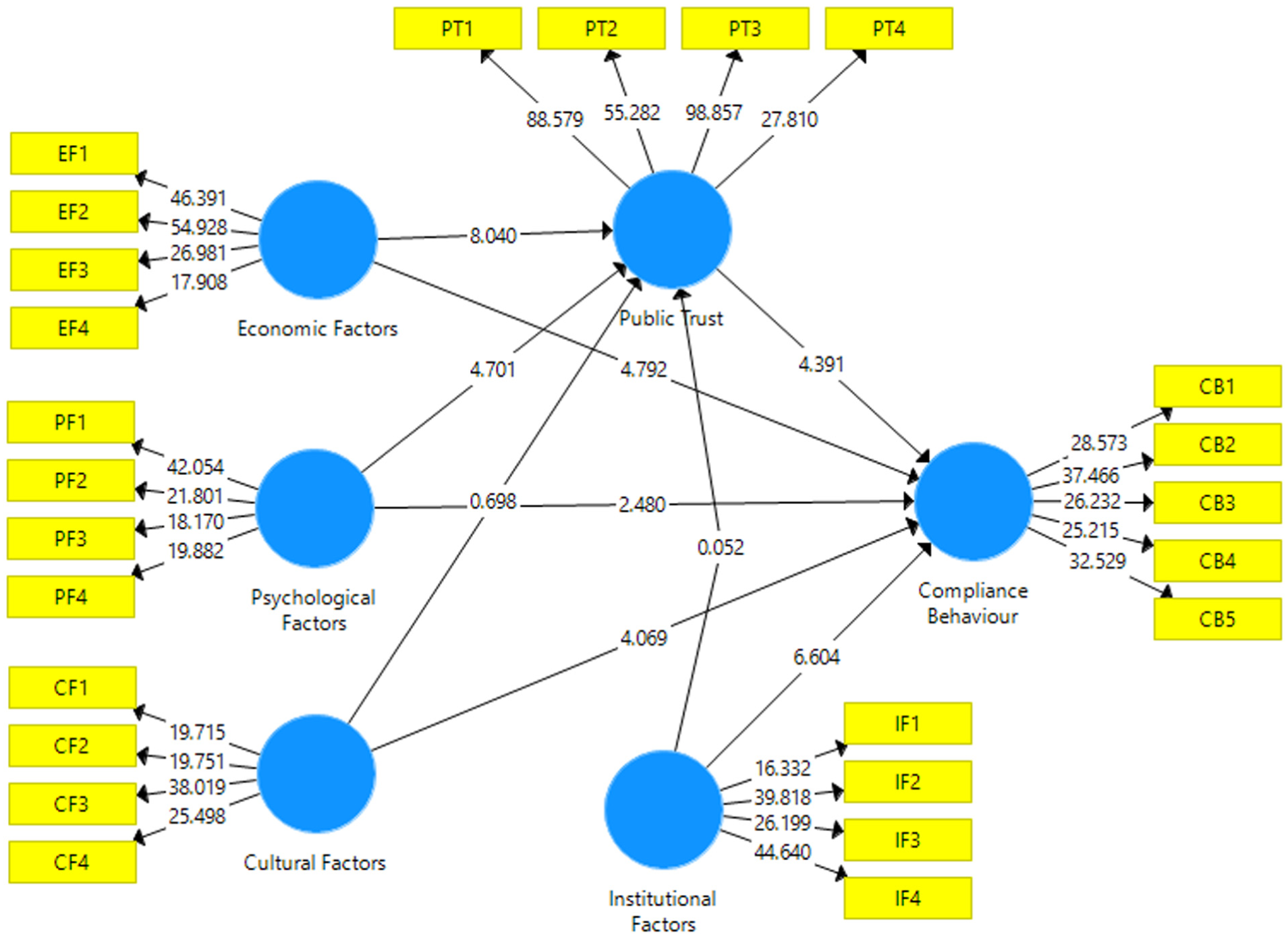

To evaluate the strength and significance of relationships between variables in the structural model, path coefficients were analyzed using the bootstrapping procedure in Smart PLS 3.0. This method involves repeatedly resampling the dataset (5,000 iterations in this case) to generate stable estimates of the coefficients and their confidence intervals. A stringent 97.5% confidence level was applied to ensure precision in assessing the direct relationships, minimizing the risk of Type I errors. As shown in Table 10 and Figure 4, the results provide robust empirical evidence for the hypothesized connections between constructs, confirming whether each proposed relationship is statistically meaningful. This rigorous approach enhances the credibility of the findings, aligning with the study’s earlier validation of reliability and measurement model integrity.

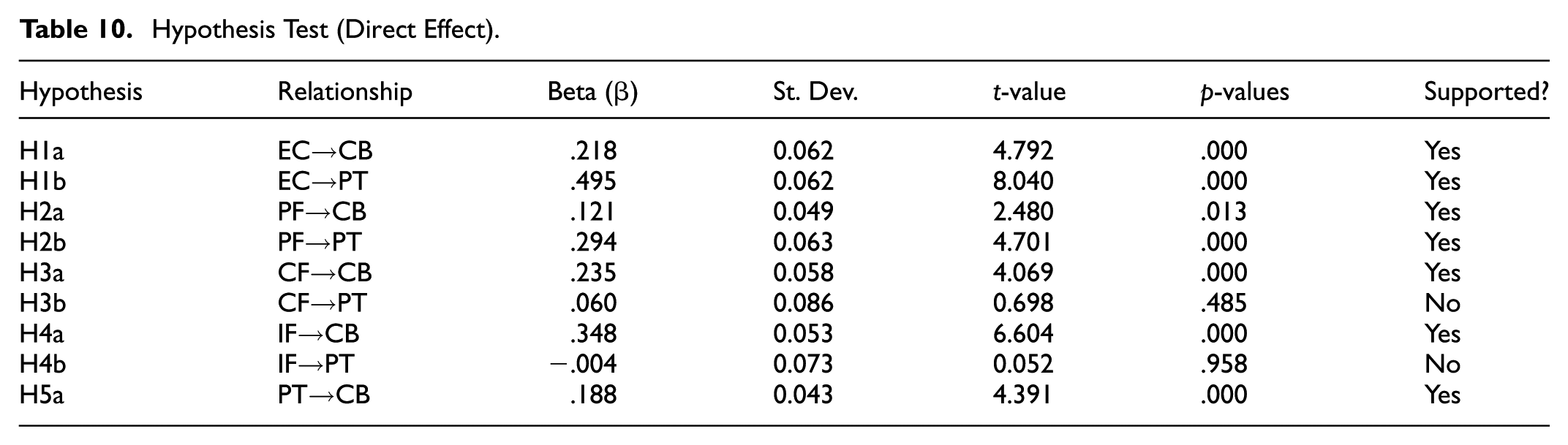

Hypothesis Test (Direct Effect).

Structural model.

Result of the Hypotheses Testing

The structural model as it shown in Table 10 and Figure 4 results reveal that economic, psychological, cultural, and institutional factors all exert significant direct effects on voluntary tax compliance behavior, except for certain paths involving public trust. Specifically, economic factors significantly influence compliance behavior (β = 0.218, p < .001) and public trust (β = 0.495, p < .001), confirming that perceptions of fairness, effective use of public resources, and equitable economic systems enhance both trust in government and willingness to comply voluntarily. Similarly, psychological factors have a positive and significant relationship with both compliance behavior (β = 0.121, p = .013) and public trust (β = 0.294, p < .001), suggesting that internal motivations such as moral obligation and perceived justice foster cooperative tax behavior.

Cultural factors also exhibit a significant direct influence on compliance (β = 0.235, p < 0.001), indicating that shared norms and societal expectations promote voluntary adherence to tax laws. However, their relationship with public trust is not significant (β = 0.060, p = 0.485), implying that cultural values may shape compliance directly rather than through trust in institutions. Institutional factors show the strongest direct effect on compliance (β = 0.348, p < .001), underscoring the importance of administrative efficiency, procedural fairness, and policy consistency. Yet, institutional factors do not significantly predict public trust (β = −0.004, p = 0.958), which may reflect citizens’ skepticism toward institutional performance or past governance challenges. Finally, public trust itself has a significant positive effect on compliance behavior (β = 0.188, p < .001), confirming its pivotal mediating role in fostering voluntary compliance.

The mediation analysis as it illustrated in Table 11 further demonstrates that public trust partially mediates the relationships between economic, psychological, and cultural factors and compliance behavior. The indirect effect of economic factors on compliance via public trust is significant (β = 0.093, p < .001), suggesting that perceptions of economic fairness enhance compliance partly by strengthening trust in government. Similarly, psychological factors exert an indirect effect through public trust (β = 0.055, p = .001), reinforcing the notion that moral norms and fairness perceptions cultivate trust, which in turn encourages voluntary compliance.

Mediation (Indirect Effect).

However, the mediating effect of public trust in the relationships between cultural and institutional factors and compliance behavior is not significant (β = 0.011, p = 0.491; β = −0.001, p = 0.957, respectively). This implies that while culture and institutional quality influence compliance directly, their effects are not transmitted through trust.

Overall, these findings highlight that public trust acts as a crucial psychological bridge linking individual and systemic factors to tax compliance. Economic and psychological drivers enhance compliance both directly and indirectly through trust, while institutional and cultural determinants operate more directly.

Discussions

The structural results show that economic, psychological, cultural, and institutional factors each have significant direct effects on voluntary tax compliance, while public trust itself significantly predicts compliance and partially mediates the effects of economic and psychological factors but not cultural and institutional factors. This pattern points to a nuanced interplay between material, motivational, and contextual drivers of compliance.

First, the strong direct influence of economic factors and their indirect effect through public trust supports the idea that perceptions of fairness and efficient use of public resources both motivate compliance directly and increase trust, which in turn fosters cooperative behavior. Empirical work has documented similar pathways: taxpayers’ perceptions of fairness and service quality increase trust and thereby strengthen compliance intentions (Aktaş Güzel et al., 2019). In addition, economic determinants such as perceived fairness of tax burden, audit likelihood, and government spending effectiveness remain salient. A South Gondar study indicated that audit rate and equity perceptions had positive effects on compliance, albeit with mixed effects for penalties and perceived cost of compliance (Ademe & Simret, 2020). Likewise, literature underscores that taxpayers engage in a cost benefit calculation consistent with deterrence theory where penalties and audit threats can deter evasion if combined with equitable tax rates.

Second, psychological factors (moral norms, perceived justice) exerted both direct and mediated effects via trust in our model. This aligns with behavioral research showing that internal motivations raise tax morale and that trust amplifies this effect individuals who feel morally obliged to pay taxes are even more likely to act when they also trust institutions. Several survey-based and experimental studies report comparable results (Dulleck et al, 2016). In Ethiopian context, prior research in Ethiopia shows that perceptions of equity and fairness shape compliance behavior: individuals who saw discrepancies in payment levels tended to evade more, while those perceiving fairness complied at higher rates (Tumoro & Pandya, 2025). These findings illustrate how subjective attitudes such as moral judgment, guilt, and perceived justice influence compliance decisions.

Third, cultural factors significantly predicted compliance directly but did not operate through public trust in our data. This is consistent with literature that finds culture and social norms often influence tax morale and behavior independently of institutional trust: shared norms can create peer pressure or internalized obligations that prompt compliance without necessarily increasing confidence in government institutions. At the same time, systematic reviews highlight that the effect of culture is heterogeneous across contexts, so direct cultural influences (without mediation by trust) are plausible (Fonseca Corona, 2024). When the Ethiopian context is concerned, the role of social and cultural norms surfaces in numerous Ethiopian studies. In Bahir Dar, perceptions of fairness, communal expectations, and governance ethics significantly influenced compliance behavior while tax knowledge and complexity negatively affected it (Ayele & Bitew, 2019). These findings underline how compliance is not merely enforced but socially constructed, particularly in settings where community norms and leadership ethics matter.

Fourth, institutional quality produced the largest direct effect on compliance but unexpectedly did not significantly predict public trust nor show mediation through trust. This result finds some precedent in the literature showing that institutional features (e.g., efficient administration, enforcement) can yield immediate compliance responses (through reduced opportunity or increased perceived costs) without necessarily shifting citizens’ confidence in institutions especially in contexts where historical governance shortcomings generate skepticism that is slow to change. Other studies also show the relation between institutional features and trust is complex and contingent on how people experience procedures and enforcement (Gobena & Van Dijke, 2016). Consistent with the study by Zewdie et al. (2024), institutional capacity including the effectiveness of tax audits, administrative procedural clarity, and service delivery strongly predicts tax compliance behavior in Ethiopia. Their findings show that institutional factors directly shape audit effectiveness and compliance outcomes. Additionally, Adem et al. (2024) confirm that trust in tax authorities and perceptions of fair institutional power bolster voluntary compliance, echoing the vertical trust pillar of the Slippery Slope Framework.

Finally, the central role of public trust as a predictor of compliance is well supported by cross-country and context-specific studies: trust tends to increase voluntary cooperation and shapes whether taxpayers see payment as civic contribution rather than merely an obligation. At the same time, several works warn that trust rarely acts in isolation its effects interact with authority power, fairness perceptions, and enforcement regimes so simple one-directional models may miss important contingencies (Aktaş Güzel et al., 2019). In line with the study by Zewdie et al. (2024) in Ethiopian context, institutional capacity including the effectiveness of tax audits, administrative procedural clarity, and service delivery strongly predicts tax compliance behavior in Ethiopia. Their findings show that institutional factors directly shape audit effectiveness and compliance outcomes. Additionally, Adem et al. (2024) confirm that trust in tax authorities and perceptions of fair institutional power bolster voluntary compliance, echoing the vertical trust pillar of the Slippery Slope Framework.

The mixed pattern observed in this study where institutional factors strongly predict compliance but show no significant link to public trust aligns with evidence from recent empirical and meta-analytic research. While several reviews emphasize a consistent positive relationship among procedural fairness, trust, and tax compliance, particularly in high-governance contexts, findings from developing countries often reveal more conditional patterns. In such settings, persistent administrative inefficiencies, limited transparency, or historical corruption may weaken citizens’ baseline trust, making it difficult for institutional reforms to generate immediate improvements in confidence toward tax authorities (Hofmann et al., 2017). Thus, our finding supports the argument that institutional quality can influence compliance directly through effective enforcement and service delivery, even when trust remains relatively low.

Similarly, the role of culture in shaping compliance appears context-dependent. Although prior studies consistently highlight the importance of cultural values for tax morale, systematic reviews note that both the strength and direction of this relationship vary across regions and measurement approaches. The direct cultural effect observed in this study without mediation through trust is therefore consistent with the idea that shared norms and community expectations can promote compliant behavior through mechanisms such as social pressure or moral obligation rather than institutional confidence (Fonseca Corona, 2024).

Furthermore, emerging research suggests that the interplay between trust and institutional power may involve interaction rather than mediation effects. Studies within the “slippery slope” framework show that trust can moderate the influence of enforcement, meaning compliance outcomes depend on how these two forces combine rather than act independently. This perspective helps explain why some indirect (mediated) paths, such as institutional factors through trust, were not statistically significant in this context. Taken together, these insights reinforce that both enforcement and legitimacy matter, but their pathways differ by predictor. Economic and psychological factors may build confidence and foster voluntary compliance, whereas institutional and cultural factors may exert more immediate, rule-based effects on behavior. For policymakers, this underscores the importance of balancing credible enforcement with fairness and transparency to sustain compliance in the short term, while gradually nurturing the trust required for long-term cooperative tax behavior.

Policy Implications

The findings of this study provide clear, theory-informed guidance for policymakers and tax administrators. Strengthening public trust is fundamental to promoting voluntary tax compliance. Policies should focus on enhancing transparency, procedural fairness, and respectful treatment of taxpayers. While clear and consistent enforcement supports the deterrence dimension, institutional responsiveness reinforces the trust dimension of the Slippery Slope Framework, fostering compliance that is motivated by confidence rather than fear alone.

Cultural and social norms also play a crucial role in shaping compliance behavior. Community institutions such as iddir, business associations, and local trade networks can act as intermediaries between taxpayers and the state, reinforcing social expectations and collective responsibility. Embedding compliance within culturally recognized practices aligns with the horizontal trust pillar of the Slippery Slope Framework and enhances voluntary adherence without overreliance on coercive enforcement.

Linking taxation to visible public outcomes is another important strategy. When taxpayers see that their contributions fund tangible community improvements such as roads, schools, and healthcare facilities they gain confidence in government institutions, which strengthens legitimacy and trust. At the same time, consistent enforcement ensures that compliance is perceived as both expected and beneficial, creating a complementary interaction between deterrence and trust.

Tailoring engagement strategies to demographic characteristics further enhances effectiveness. Younger taxpayers may respond more readily to digital tools and mobile platforms, whereas older or less formally educated taxpayers might benefit from in-person guidance or simplified instructions. By demonstrating institutional responsiveness and fairness, trust is reinforced, while structured guidance and reminders maintain the deterrence dimension, creating a synergy between both mechanisms.

Finally, promoting taxation as a civic duty can cultivate intrinsic motivation and moral obligation among taxpayers. Education and awareness campaigns should emphasize the social and developmental benefits of tax compliance, linking individual contributions to national progress. This approach reinforces fairness and legitimacy principles in line with the Slippery Slope Framework, while the deterrent effect of enforcement continues to provide structural compliance boundaries. Jointly, these policy measures illustrate the practical integration of Deterrence Theory and the Slippery Slope Framework: enforcement and institutional power establish the boundaries for compliance, while trust, legitimacy, and social norms encourage voluntary cooperation. Policies that simultaneously address both dimensions can increase voluntary compliance, strengthen the social contract, and support sustainable governance and development in Ethiopia and comparable developing-country contexts.

Limitations and Future Research Directions

Like any empirical study, this research has certain limitations that should be acknowledged, which also suggest promising avenues for future investigation. First, the data were collected through a cross-sectional survey, providing a snapshot of taxpayers’ perceptions and behaviors at a single point in time. Tax attitudes and compliance behavior can change in response to shifts in government policy, economic conditions, or enforcement practices. Future research could adopt a longitudinal design to examine how compliance evolves over time and how the relationships among institutional trust, cultural norms, and economic or psychological factors develop.

Second, this study focused exclusively on Category “A” taxpayers in Hawassa City. While this group represents a significant portion of Ethiopia’s formal tax base and offers valuable insights, the findings may not fully capture the experiences of smaller businesses or informal sector operators. Expanding the scope to include other taxpayer categories and regions across Ethiopia would enhance the generalizability of the results and allow for comparisons across diverse economic and cultural contexts.

Third, the study relied on self-reported survey data, which may be subject to social desirability bias, as respondents could overstate their compliance or provide answers perceived as favorable. Future research could integrate mixed-method approaches, combining surveys with interviews, focus groups, or analysis of administrative tax records. This would provide a more robust and nuanced understanding of the motivations, perceptions, and contextual factors underlying compliance decisions.

Finally, while this study integrates the Deterrence Theory and the Slippery Slope Framework to explain voluntary tax compliance, future research could refine and extend the theoretical model by incorporating additional behavioral and contextual variables. For instance, examining the interaction between deterrence mechanisms such as audit probability and penalty severity and taxpayers’ moral, cultural, or institutional perceptions could offer deeper insights into compliance dynamics. Similarly, exploring how these relationships vary across different economic conditions, administrative capacities, or governance structures would contribute to developing a more context-sensitive framework for understanding and promoting voluntary compliance. Such extensions would not only strengthen theoretical insights but also provide practical guidance for designing more effective and sustainable tax compliance strategies in developing-country contexts.

Conclusion

This study set out to examine the key drivers of voluntary tax compliance among Category “A” taxpayers in Hawassa City, a critical segment of Ethiopia’s formal tax base, with particular attention to the mediating role of public trust. By integrating the Deterrence Theory and the Slippery Slope Framework, the study provides a comprehensive understanding of how institutional, cultural, economic, psychological, and demographic factors shape compliance behavior.

The empirical results indicate that while economic and psychological factors influence compliance indirectly through public trust, institutional capacity, and cultural norms exert more immediate, direct effects. Specifically, taxpayers’ perceptions of audit effectiveness, procedural clarity, and service quality establish the structural boundaries of behavior in line with deterrence principles, whereas trust, legitimacy, and culturally embedded social norms foster voluntary compliance through intrinsic motivation. In other words, enforcement alone is insufficient; citizens are more likely to comply when they perceive the system as fair, responsive, and socially legitimate.

Theoretically, this study extends the Slippery Slope Framework by highlighting the central mediating role of trust in a developing-country context, and demonstrates the complementary relationship between deterrence-based power and trust-based legitimacy. Practically, the findings provide clear guidance for policymakers and tax administrators, emphasizing that sustainable compliance requires balancing credible enforcement with initiatives that build institutional trust and leverage social norms.

While the study offers valuable insights, it is subject to limitations, including its cross-sectional design and focus on a specific regional and taxpayer category. Future research could adopt longitudinal designs, explore other taxpayer segments, and employ multi-source data to strengthen generalizability and robustness. In conclusion, this study offers a nuanced understanding of the mechanisms underlying voluntary tax compliance in Ethiopia, providing both theoretical and practical pathways for improving tax behavior, institutional legitimacy, and revenue mobilization in similar developing-country contexts.

Footnotes

Appendix A

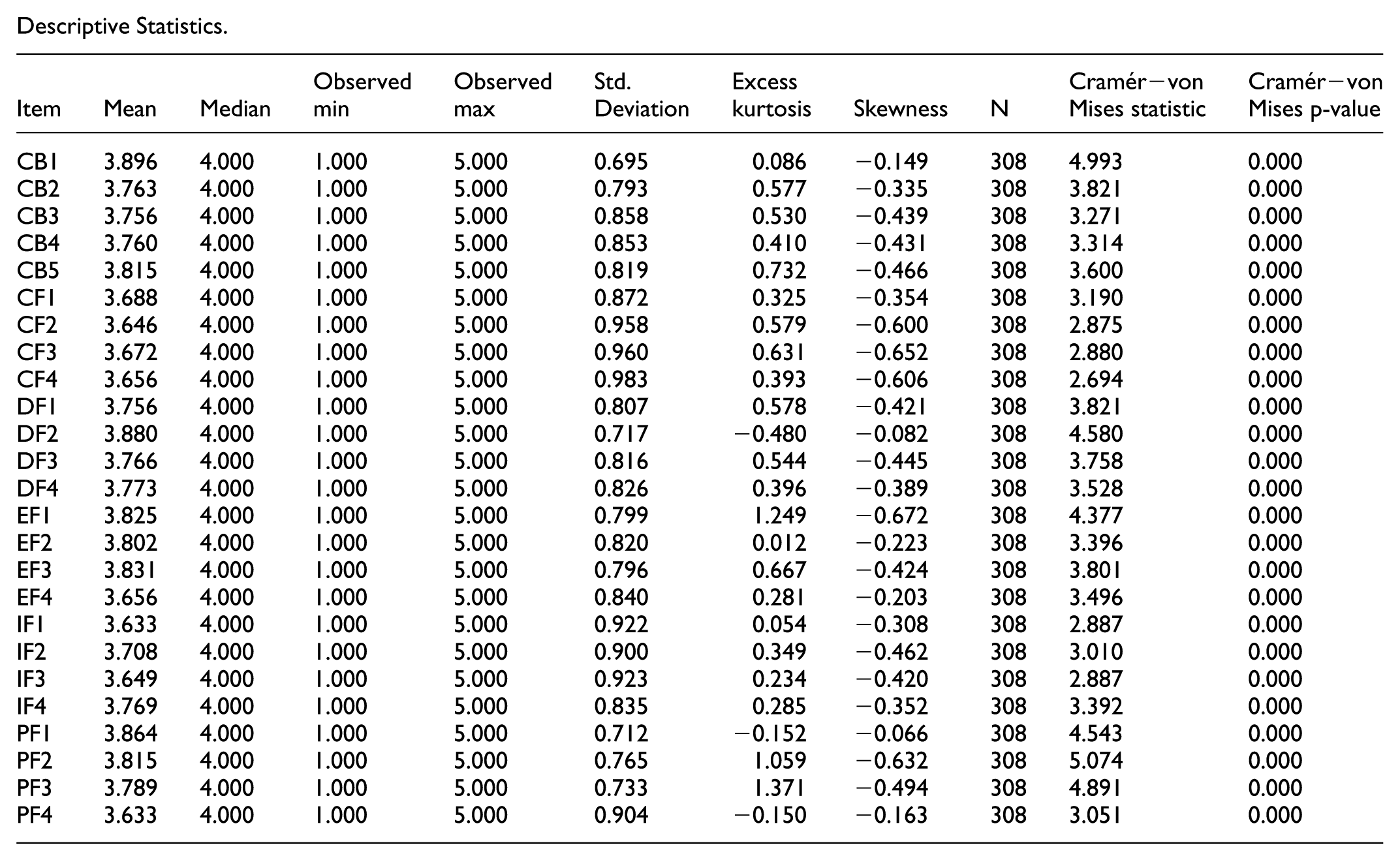

Descriptive Statistics.

| Item | Mean | Median | Observed min | Observed max | Std. Deviation | Excess kurtosis | Skewness | N | Cramér−von Mises statistic | Cramér−von Mises p-value |

|---|---|---|---|---|---|---|---|---|---|---|

| CB1 | 3.896 | 4.000 | 1.000 | 5.000 | 0.695 | 0.086 | −0.149 | 308 | 4.993 | 0.000 |

| CB2 | 3.763 | 4.000 | 1.000 | 5.000 | 0.793 | 0.577 | −0.335 | 308 | 3.821 | 0.000 |

| CB3 | 3.756 | 4.000 | 1.000 | 5.000 | 0.858 | 0.530 | −0.439 | 308 | 3.271 | 0.000 |

| CB4 | 3.760 | 4.000 | 1.000 | 5.000 | 0.853 | 0.410 | −0.431 | 308 | 3.314 | 0.000 |

| CB5 | 3.815 | 4.000 | 1.000 | 5.000 | 0.819 | 0.732 | −0.466 | 308 | 3.600 | 0.000 |

| CF1 | 3.688 | 4.000 | 1.000 | 5.000 | 0.872 | 0.325 | −0.354 | 308 | 3.190 | 0.000 |

| CF2 | 3.646 | 4.000 | 1.000 | 5.000 | 0.958 | 0.579 | −0.600 | 308 | 2.875 | 0.000 |

| CF3 | 3.672 | 4.000 | 1.000 | 5.000 | 0.960 | 0.631 | −0.652 | 308 | 2.880 | 0.000 |

| CF4 | 3.656 | 4.000 | 1.000 | 5.000 | 0.983 | 0.393 | −0.606 | 308 | 2.694 | 0.000 |

| DF1 | 3.756 | 4.000 | 1.000 | 5.000 | 0.807 | 0.578 | −0.421 | 308 | 3.821 | 0.000 |

| DF2 | 3.880 | 4.000 | 1.000 | 5.000 | 0.717 | −0.480 | −0.082 | 308 | 4.580 | 0.000 |

| DF3 | 3.766 | 4.000 | 1.000 | 5.000 | 0.816 | 0.544 | −0.445 | 308 | 3.758 | 0.000 |

| DF4 | 3.773 | 4.000 | 1.000 | 5.000 | 0.826 | 0.396 | −0.389 | 308 | 3.528 | 0.000 |

| EF1 | 3.825 | 4.000 | 1.000 | 5.000 | 0.799 | 1.249 | −0.672 | 308 | 4.377 | 0.000 |

| EF2 | 3.802 | 4.000 | 1.000 | 5.000 | 0.820 | 0.012 | −0.223 | 308 | 3.396 | 0.000 |

| EF3 | 3.831 | 4.000 | 1.000 | 5.000 | 0.796 | 0.667 | −0.424 | 308 | 3.801 | 0.000 |

| EF4 | 3.656 | 4.000 | 1.000 | 5.000 | 0.840 | 0.281 | −0.203 | 308 | 3.496 | 0.000 |

| IF1 | 3.633 | 4.000 | 1.000 | 5.000 | 0.922 | 0.054 | −0.308 | 308 | 2.887 | 0.000 |

| IF2 | 3.708 | 4.000 | 1.000 | 5.000 | 0.900 | 0.349 | −0.462 | 308 | 3.010 | 0.000 |

| IF3 | 3.649 | 4.000 | 1.000 | 5.000 | 0.923 | 0.234 | −0.420 | 308 | 2.887 | 0.000 |

| IF4 | 3.769 | 4.000 | 1.000 | 5.000 | 0.835 | 0.285 | −0.352 | 308 | 3.392 | 0.000 |

| PF1 | 3.864 | 4.000 | 1.000 | 5.000 | 0.712 | −0.152 | −0.066 | 308 | 4.543 | 0.000 |

| PF2 | 3.815 | 4.000 | 1.000 | 5.000 | 0.765 | 1.059 | −0.632 | 308 | 5.074 | 0.000 |

| PF3 | 3.789 | 4.000 | 1.000 | 5.000 | 0.733 | 1.371 | −0.494 | 308 | 4.891 | 0.000 |

| PF4 | 3.633 | 4.000 | 1.000 | 5.000 | 0.904 | −0.150 | −0.163 | 308 | 3.051 | 0.000 |

Acknowledgements

I sincerely thank all the business owners and managers who generously participated in this study. Their time, insights, and willingness to share information made this research possible. I also appreciate the support of Hawassa City tax officials in facilitating access to relevant information, which greatly contributed to the successful completion of the study.

Ethical Considerations

This study was reviewed and approved by the College Research Ethics Review Committee (CRERC), College of Business and Economics (Approval No. CBE-RTT-35/2025). The research protocol complied with institutional ethical standards for studies involving human participants and adhered to internationally recognized ethical principles for social science research.

Consent to Participate

All participants provided oral informed consent before taking part in the study. They were fully informed about the purpose of the research, the voluntary nature of participation, and their right to withdraw at any time without any consequences. Participant confidentiality and anonymity were strictly maintained, and only anonymized data were accessed by the researcher. No minors were involved in the study, and all procedures adhered to the ethical guidelines approved by the College Research Ethics Review Committee (CRERC, Approval No. CBE-RTT-35/2025).

Author Contribution

The author conceived and designed the study, collected and analyzed the data, interpreted the findings, and wrote the manuscript. All aspects of the research, from conceptualization to final drafting, were carried out solely by the author.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The study made use of data, and can be shared upon request.