Abstract

Presenteeism refers to a situation in which an employee performs less optimally due to problems such as poor health, job dissatisfaction, family conflicts, and financial difficulties. This often leads to decreased productivity, which is detrimental to employers. The main objective of this research is to examine the role of financial well-being in mediating the relationship between financial literacy and presenteeism and the relationship between financial behavior and presenteeism. To investigate the issue, we used data collected through a survey of 175 employees at a government agency in Indonesia and then conducted partial least squares structural equation modeling (PLS-SEM) regression technique. We find that financial behavior directly and negatively influences presenteeism, suggesting that presenteeism can be reduced if the employees maintain good financial behavior, which can eliminate financial difficulties as one of the sources of presenteeism. We also find that financial well-being, although it has no direct role in reducing presenteeism, can significantly mediate the effect of financial literacy on presenteeism. Employees with good financial literacy, in our case, cannot directly reduce presenteeism, but financial literacy will decrease presenteeism only if the employees have good financial well-being. Our finding recommends employers to increase their employees’ financial literacy and behavior to minimize presenteeism.

Plain Language Summary

In this article, we investigate the factors of why employees perform less optimally or known as “presenteeism.” In fact, they are present at the office, but they are not productive. In our research, we examine whether financial literacy, financial behavior, and financial well-being could become factors that can reduce presenteeism. We find that people with good financial behavior tend to have a lower probability of presenteeism. We also find that people with good financial literacy could also have a lower chance of presenteeism if they have good financial well-being.

Introduction

The issue of individual financial well-being, particularly among workers, has recently become a prominent topic for companies. The Covid-19 pandemic and several global issues (for example, war in Ukraine, Palestinian conflict, and the United States’ reciprocal tariff) have affected society’s financial well-being. Financial problems not only affect personal life but also affect an individual’s work life (Joo, 1998; Kim et al., 2006; Wei et al., 2024). Previous studies have ascertained that financial well-being (or financial stress) is the one factor that has an impact on work productivity, primarily through absenteeism and/or presenteeism (Lohaus & Habermann, 2019). Absenteeism is a phenomenon in which one is not present in their scheduled work, while presenteeism refers to one who is at their workplace but performs less optimally (Joo, 1998; Kim et al., 2006; Kim & Garman, 2003; Merrill et al., 2012; Miraglia & Johns, 2016; Sabri & Aw, 2020; van Vuren et al., 2018).

The main objective of this paper is to see whether financial well-being and some other employees’ financial aspects such as financial literacy and financial behavior can play a role in mitigating employee presenteeism. Rather than absenteeism, in this paper we focus on presenteeism because the latter has recently received more attention globally mainly due to its substantial impact on organizational performance, especially in influencing work productivity (Lohaus & Habermann, 2019; Miraglia & Johns, 2016). Although both absenteeism and presenteeism lead to a decrease in productivity, presenteeism has recently received more attention as it has also become the main factor affecting organizational performance (Lohaus & Habermann, 2019). Moreover, the average disruption of working hours and the impact of economic losses due to presenteeism have been proven to be greater than those of absenteeism (Uribe et al., 2017; Wee et al., 2019). In addition, absenteeism occurs relatively infrequently compared with presenteeism. Employees are more likely to attend work rather than be absent, even when their performance is reduced. This is due to the fact that absenteeism is more noticeable to the employer and can directly affect an employee’s job security (Kim et al., 2006). Employees who are absent are more likely to receive punishment, wage reduction, and other consequences of absenteeism (Lohaus & Habermann, 2019).

The 2022 United States Employee Financial Wellness Survey revealed that 42% of employees who are stressed about finances admit being bothered at work by personal financial problems, 76% of employees who are stressed about finances stated that financial worries have a negative impact on their productivity, and 55% of employees who are bothered by personal financial stress spend 3 hr each week at work to deal with their financial problems (PwC, 2022). Furthermore, this could lead to losses for the employer due to decreased employee productivity (Prater & Smith, 2011). The monetary value of productivity losses due to absenteeism and presenteeism is estimated to be US$840 million in middle-income countries (Uribe et al., 2017).

Both absenteeism and presenteeism disrupt operations, reduce productivity, and are economically detrimental. Therefore, it is important for employers to solve these problems. Improving financial well-being is one solution. For example, welfare can bring about a higher level of productivity; employees who exhibit higher levels of welfare tend to report higher work productivity. On the contrary, a decline in several aspects of welfare is associated with decreased productivity (Isham et al., 2021). Employees who are satisfied with their financial well-being will have fewer financial distractions at work, which can help them become more focused and productive at work (van Vuren et al., 2018). In addition, the role of financial well-being and stress in influencing absenteeism and presenteeism has also been widely demonstrated (Kim et al., 2006; Kim & Garman, 2003, 2004; Merrill et al., 2012; Miraglia & Johns, 2016; Prater & Smith, 2011; Sabri & Aw, 2020). Subsequently, fostering employees’ financial well-being contributes to increasing their work productivity by reducing both absenteeism and presenteeism.

In the context of developing countries such as Indonesia, the level of a society’s financial well-being has not been fully realized. According to the results of the 2020 International Survey of Adult Financial Literacy by the OECD, when viewed in terms of financial reserves, 46% of respondents stated that they could only survive for less than 1 month (without resorting to additional borrowings or being evicted from their homes) if they lost their main source of income. Only 8.6% of the respondents stated that they would be able to survive for more than 6 months (Indonesian Financial Service Authority, 2021). This indicates that many Indonesians still do not possess sufficient financial management skills, especially in emergency fund management, to face challenges associated with financial security. The inability of society to manage its finances, especially when dealing with unexpected emergencies, attests to the fact that society’s financial well-being has not been achieved in Indonesia.

This paper examines the moderating role of financial well-being, particularly in the relationship between financial literacy and presenteeism, as well as between financial behavior and presenteeism. According to contemporary economic views, someone with better financial literacy will be more likely to survive and succeed (Yordudom et al., 2024). A decent level of financial literacy is highly correlated with a better ability to handle emergency expenditures and other economic shocks (Prakash et al., 2022). One of the main causes of financial problems is the lack of knowledge on how to manage, save, and invest money (Parcia & Estimo, 2017). Previous studies found strong evidence that workplace financial education leads to improved financial well-being among employees (Garman et al., 1999; Kim & Garman, 2003; Sajid et al., 2024; Taft et al., 2013). Companies are willing to offer financial education for the following reasons: (a) improving the financial health of employees, (b) reducing worker stress, and (c) increasing productivity in the workplace (Garman et al., 1999). Financial education can safeguard employees who are experiencing financial difficulties, as they can discern useful information to improve their financial well-being and arrest the decline in productivity (Joo, 1998).

One of the parameters for measuring the level of financial literacy is “attitude and behavior in decision-making and financial management” to achieve welfare (Indonesian Financial Services Authority, 2021). The inability to transfer financial knowledge into sound financial behavior practices does not result in improved changes (Sabri & Aw, 2020). Financial literacy and financial behavior have a significant positive impact on financial well-being. Additionally, financial behavior was found to have a mediating role in the relationship between financial literacy and financial well-being. Individuals with superior financial knowledge tend to show better financial behavior, lower financial fragility, and higher financial well-being (Prakash et al., 2022). The link between financial literacy and financial behavior and its effect on improving financial well-being has been widely studied (Adee et al., 2024; Brüggen et al., 2017; Falahati & Sabri, 2015; Fan & Henager, 2021; Kuutol et al., 2024; Oquaye et al., 2020; Osman et al., 2018; Parcia & Estimo, 2017). Emphasizing these three variables is vital in anticipating absenteeism and presenteeism, which could harm productivity (Sabri & Aw, 2020).

Many studies have investigated “the relationship between financial literacy, financial behavior, and financial well-being” and “the relationship between financial well-being and presenteeism.” However, studies on the link between financial literacy and financial behavior toward presenteeism, especially when they are moderated by financial well-being, are still limited. Several previous studies have found that financial literacy has an insignificant influence on presenteeism. However, it has been found that there is a mediating role that significantly influences both variables, that is, through financial behavior and financial well-being (Hwang & Park, 2023; Lone & Bhat, 2024; Sabri & Aw, 2020). To the best of our knowledge, there has yet to be research investigating the relationship between financial literacy, financial behavior, and the mediating role of financial well-being on presenteeism in the Indonesian government sector.

The Indonesian government sector is a good example to study presenteeism because the inefficient governance system can impact employees’ behavior and motivation during their work in the office. Bureaucracy in Indonesia struggles with inefficiency and corruption even after 20 years of reform (The Jakarta Post, 2021). This problem is further exacerbated by the many cases of illegal fees (pungli) (Pertiwi, 2023), embezzlement, absenteeism (Utami et al., 2021), and leaving during working hours. Indonesian government employees are often reported that they come to the office but do not work productively.

Based on data released by the state civil service agency (Badan Kepegawaian Nasional-BKN), in 2022, the number of government employees reached 4.25 million, with 91% being civil servants, while the rest is employees with agreement (Pegawai Pemerintahan dengan Perjanjian Kerja-PPPK) (Litbang Kompas, 2023). This number is still relatively small compared to the proportion of the Indonesian population, which is only two government employees per 100 people (Booth, 2021). In terms of education level, only 2% are still qualified below high school, and more than 60% have a bachelor’s degree (Booth, 2021). Starting from this phenomenon, we want to investigate the determinants of why many government employees in Indonesia engage in presenteeism by focusing on financial aspects such as their literacy, behavior, and well-being. Moreover, to the best of our knowledge, this may be the first study to examine the influence of financial literacy, financial behavior, and financial well-being on presenteeism, especially in the scope of Indonesian government employees whose performance is considered less productive, and it is indicated that presenteeism occurs based on financial factors.

The remainder of this paper is organized as follows. Section “Literature Review and Hypothesis Development” reviews the literature and develops our hypotheses, and section “Methodology” reviews the methodology. Section “Results and Discussions” presents the results, and the last section concludes.

Literature Review and Hypothesis Development

Maslow, Content, and Process Theories

Presenteeism can be explained through several theories which are actually closer to the field of psychology, like the job demands model (Deery et al., 2014; McGregor et al., 2016). According to Johns (2010), the causes of presenteeism can be explained through two main approaches: content theories and process theories. The former theory focuses on exploring what motivates employees to come to work even in less-than-optimal conditions (intrinsic and extrinsic factors), while the latter theory refers to why employees decide to come anyway (future consequences). Our research tends to be closer to the approach of “content theories” based on the theory of needs stated by Maslow (1943). Financial well-being is closely related to physiological and safety needs. Physiological needs include primary needs that are met, whereas safety needs include having a retirement account, health insurance, and similar safeguards. Achieving financial well-being motivates a person to fulfill the highest hierarchy of needs, namely, the need for self-actualization. At this level, an individual’s highest creativity can be expected (Maslow, 1943), and maximum work productivity can be achieved.

However, organizations need to know how to achieve this goal. This concept emphasizes the importance of intervention (or extension) in the employer’s responsibilities to meet employees’ needs, which can improve their welfare (Nielsen et al., 2017). In addition to providing salaries, employers are responsible for educating their employees in managing their financial resources effectively. In the absence of these support mechanisms, employee stress levels can become more intense, leading to low productivity (Prakash et al., 2022). Meta-analysis research conducted by Miraglia and Johns (2016) also revealed that individual financial difficulties are one of the factors causing employee presenteeism.

Financial Literacy and Presenteeism

Presenteeism has received much attention globally because of its impact on organizational performance, especially in influencing work productivity (Lohaus & Habermann, 2019; Miraglia & Johns, 2016). In contrast to absenteeism, which is generally seen as the phenomenon of not being present for scheduled work, presenteeism is a phenomenon in which a person is present at work but operates at less than their full capacity or less optimally (Isham et al., 2021). Many factors can cause presenteeism, including health problems, job satisfaction, family conflicts, and financial difficulties (Lohaus & Habermann, 2019; Merrill et al., 2012; Miraglia & Johns, 2016).

Previous studies suggest counseling and financial education to reduce presenteeism (Merrill et al., 2012). Other studies advocate effective financial education to increase employees’ financial knowledge (or literacy), reduce their financial problems, and increase work productivity (Kim, 2000; Kim & Garman, 2003, 2004). Even in developed countries, financial knowledge is regarded as a basic competency for fulfilling needs as conceptualized by Maslow’s theory. Financial literacy is a crucial competency for success and survival based on contemporary economic views ( Yordudom et al., 2024). The Indonesia Financial Services Authority defines financial literacy as “knowledge, skills and beliefs that influence attitudes and behavior to improve the quality of decision-making and financial management in order to achieve welfare” (Indonesian Financial Service Authority, 2017). On the other hand, Parcia and Estimo (2017) define Financial literacy as “individual knowledge about managing financial resources for life satisfaction” (Parcia & Estimo, 2017).

Institutional factors play a role in contributing to the level of financial literacy of employees (Banerjee, 2011). One of the reasons companies are willing to provide financial education to employees is to increase productivity in the workplace (Garman et al., 1999). Similar to other training programs, financial education programs in the workplace can affect employee performance (Kim, 2000). Financial education can serve as a buffer for employees who are experiencing financial difficulties, as it can assist them in dealing with their financial problems (Joo, 1998). Employees with deep financial literacy will increase their self-confidence (Amagir et al., 2018), and the ability to organize finances which will have a positive impact in the long term both at the individual and organizational level (Van Nguyen et al., 2022). Consequently, they will feel more comfortable and maximal in working, and therefore, presenteeism will decrease. The first hypothesis is consequently written as follows.

Financial Behavior and Presenteeism

Maslow’s theory mentions that a person’s level of needs will shape their financial behavior. Needs are assumed to be a motivator for a person to behave (Rojas et al., 2023). A person is considered to have good financial behavior if they are able to map their needs correctly. Good financial behavior also plays a role in reducing presenteeism. Financial behavior is defined as any behavior relevant to financial management, such as thrifty behavior, planning for retirement, and investing (Fan & Henager, 2021). Financial behavior includes basic financial behavior such as budgeting skills, debt reduction, and financial goals (Parcia & Estimo, 2017). Someone with good financial behavior will not easily experience financial stress that threatens their condition while working. They will also be mentally and physically healthier (Fu et al., 2020; Raišiene et al., 2020), thereby enabling them to optimize their performance at work.

Meanwhile, poor personal financial behavior is defined as “personal and family money management practices that have detrimental consequences and have a negative impact on person’s life at home or work” (Garman et al., 1999). These include lavish spending, excessive abuse of credit, and lack of an emergency fund. A person with low financial behavior is vulnerable to facing financial stress and threatening their mental health (Shek, 2005; Xia et al., 2025). In general, employees attempt to overcome problems related to their financial difficulties.

It is important for employers to be aware that these employees experience distressing financial events that may negatively impact their work. Previous studies revealed that personal financial setbacks stemming from imprudent financial decisions directly and negatively impact employee productivity (Garman et al., 1999; Joo, 1998; Luther et al., 1997; Williams et al., 1996). Other findings have shown that employees who exhibit inferior financial behavior tend to have lower productivity levels (Joo & Grable, 2000). Joo (1998) also concluded that superior personal financial behavior and financial satisfaction are positively related to performance and negatively related to absenteeism. Furthermore, recent studies have established that financial behavior has a significant effect on increasing productivity by reducing the extent of presenteeism (Sabri & Aw, 2020). Based on this description, the following hypothesis is proposed.

Financial Well-Being and Presenteeism

Financial well-being is a condition in which a person can fully meet their current financial obligations, has made preparations to meet future financial needs, and can make choices that allow them to enjoy life (Consumer Financial Protection Bureau, 2015). As mentioned in the previous section, financial well-being significantly impacts employee productivity. Employees with high levels of well-being tend to demonstrate an increase in work productivity and vice versa (Joo, 1998; Kim et al., 2006; Merrill et al., 2012; Miraglia & Johns, 2016; Sabri & Aw, 2020; van Vuren et al., 2018). Socioeconomic factors, particularly in low-income groups, can contribute toward higher stress levels and financial problems, lower job satisfaction, irregular working hours, and higher levels of presenteeism (Wee et al., 2019).

Presenteeism arising from personal financial problems occurs because financially stressed employees spend more working time dealing with personal financial matters, thereby reducing their effective working time (Kim et al., 2006; Kim & Garman, 2004; Merrill et al., 2012; Sabri & Aw, 2020). They are preoccupied with various problems, such as feeling that they do not have enough money to cover their living expenses, worrying about high debt, and dissatisfaction with their poor savings. This, in turn, has a negative impact on their attitudes and behaviors at work (Kim & Garman, 2004). Prolonged financial stress can also have detrimental effects on individual welfare, as low financial well-being has been shown to increase presenteeism (Kim, 2000). Thus, increasing organizational commitment toward employee welfare, which has an impact on lowering presenteeism levels, is essential (Wee et al., 2019). Based on this description, the following hypothesis is proposed.

The Mediating Role of Financial Well-Being

Financial well-being has been widely associated with various aspects of daily life, including presenteeism. However, past research has shown that simply adding more money to an employee’s salary does not necessarily increase well-being or financial satisfaction (Joo & Grable, 2000). Meanwhile, based on the literature on determinants of financial well-being, financial literacy and financial behavior have been determined as the main predictors. This suggests that increasing financial literacy and behavior could lead to financial well-being (Joo & Grable, 2004; Sajid et al., 2024). It is difficult to achieve financial well-being without a person having sufficient financial literacy.

Financial literacy refers to the level of financial knowledge required to control and manage a personal financial situation, which in turn impacts individuals’ financial well-being (van Vuren, 2015). Efficient financial education can also improve financial health (Garman et al., 1999). A significant positive relationship between financial literacy and well-being has been widely demonstrated. The higher the level of financial knowledge, the better their financial well-being is (Darmawan & Pamungkas, 2019; Joo, 1998; Oquaye et al., 2020; Prakash et al., 2022; van Vuren et al., 2018). Therefore, it is important that financial literacy be imparted to employees to improve their financial well-being.

Previous research has revealed that the direct effect of financial literacy on presenteeism is insignificant (Sabri & Aw, 2020), indicating that high financial literacy does not directly affect workplace productivity. Therefore, a mediating influence is required, and one of the possible mediating variables is financial well-being, which has been empirically proven to be a mediator (Sabri & Aw, 2020). Previous research has demonstrated the effectiveness of financial education in the workplace for improving employees’ financial well-being, which leads to growth in employees’ productivity (Joo & Grable, 2000). In addition, a person’s ability to use financial knowledge to manage financial resources can lead to fewer financial problems, leading to better financial well-being (Parcia & Estimo, 2017). Fewer financial problems reduce the amount of time spent on personal financial problems (Joo, 1998). They will work more comfortably and focus so that presenteeism will decrease accordingly. Based on these explanations, we propose the following hypothesis:

Furthermore, financial behavior is an act of managing personal and family financial resources to achieve financial success (Joo, 1998). Financial behavior practices, such as cash management, credit management, budgeting, financial planning, and money management, generally have a large impact on an individual’s level of financial satisfaction. Someone with positive financial behavior tends to be more financially satisfied than those with negative financial behavior (Halim & Astuti, 2015). Other studies have also established a significant and positive effect of financial behavior on financial well-being (Darmawan & Pamungkas, 2019; Oquaye et al., 2020; Prakash et al., 2022).

People with planned financial goals have a higher level of financial satisfaction (Darmawan & Pamungkas, 2019). Furthermore, individuals with sound financial management behavior can fulfill their financial obligations, be secure about future finances, and make worthwhile choices (Oquaye et al., 2020). In turn, healthy financial practices will reduce poor financial decisions and financial stress, which can ultimately lead to increased productivity in the workplace because less time is spent dealing with personal financial problems (Sabri & Aw, 2020). Although the direct effect of financial behavior on presenteeism has been found to be significant, the interrelationship between financial behavior, financial well-being, and presenteeism is also interesting for further testing. Thus, the following hypothesis is proposed:

Theoretical Framework

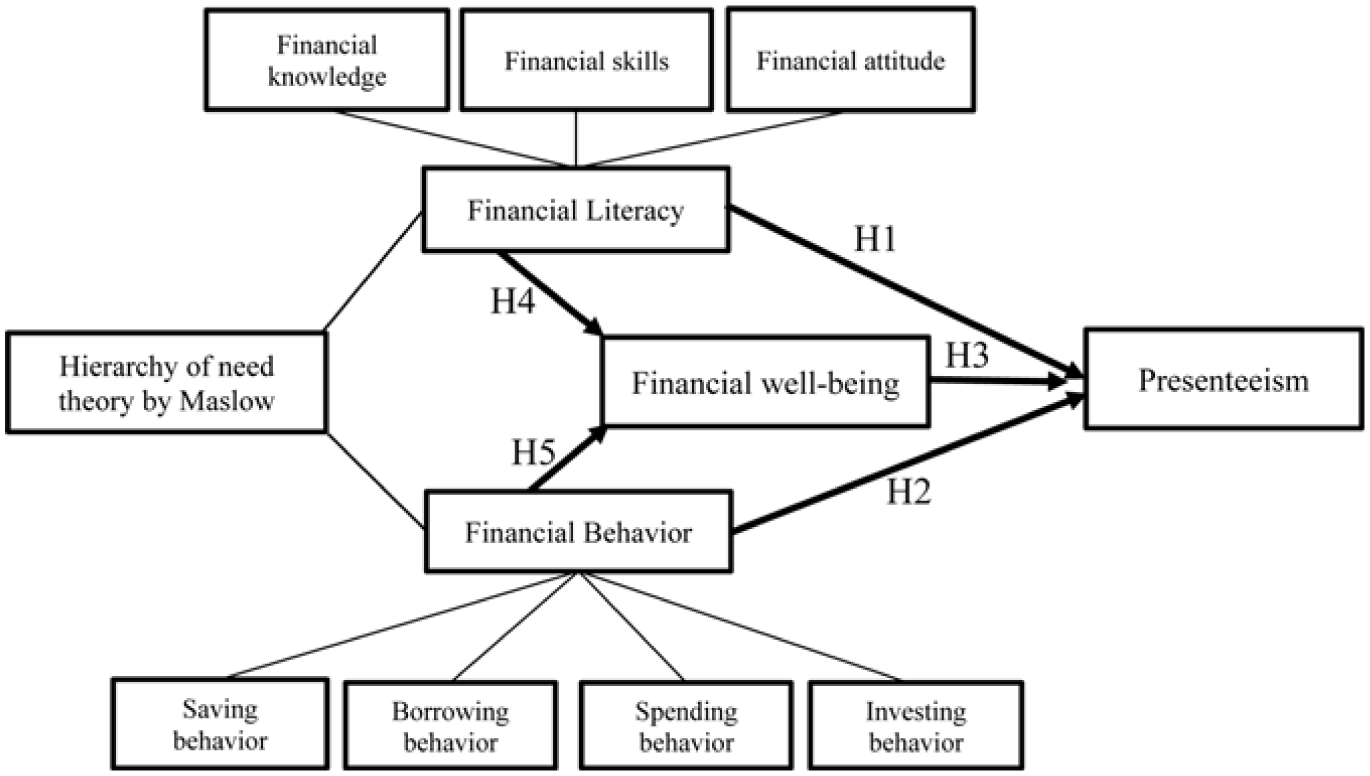

We build a mechanism analysis based on a theoretical framework that connects financial literacy, behavior, and well-being to presenteeism in Figure 1. We predict in H1 that financial literacy will reduce presenteeism. Someone sees financial literacy as one of the basic needs in the priority level that must be met, as proposed by Maslow in the hierarchy of needs, to avoid financial stress. They are assumed to be able to manage their finances better than someone with low financial literacy. Furthermore, they will also be healthier mentally and physically if they avoid stress. As a result, they will be more focused at work, and presenteeism will decrease. In the context of financial behavior (H2), we posit a similar relationship. Maslow’s theory assumes that a person’s level of needs will shape their financial behavior. For example, someone who can classify their needs well will definitely avoid wasteful behavior and debt and prioritize basic needs at first. With a well-organized form of financial behavior, they will also avoid financial stress, resulting in decreased presenteeism. This prediction also extends to H3, which assumes that the higher the financial well-being is associated with lower the presenteeism. Meanwhile, for the indirect effects in hypotheses H4 and H5, we assume that achieving financial well-being requires good financial literacy and behavior. It is almost difficult or even impossible to achieve financial stability without being equipped with sufficient financial literacy. As with financial behavior, someone with good well-being in the financial context will have more opportunities to have emergency funds, future savings, and healthy debt management. Once financial well-being is achieved, they will be free from financial problems that can disrupt their health and they can focus on work to achieve the desired productivity. Therefore, we believe financial well-being will mediate the relationship between financial literacy/behavior and presenteeism.

Theoretical framework.

Methodology

Samples and Data Collection

The sample in this study consisted of permanent and contract workers from an Indonesian government agency. Primary data were obtained through online surveys using a questionnaire designed on Google Forms and distributed to respondents via WhatsApp. In this paper, instead of using probability (random) sampling, we used non-probability sampling by surveying all employees in a government office. By adopting this approach, concerns regarding sample selection bias are substantially minimized, as all members of the population are included. Moreover, sample selection bias usually results from a non-random selection, leading to a skewed or incomplete sample (e.g., only surveying high performers).

Data were collected for 2 weeks, and 175 respondents were obtained. According to Roscoe’s (1975) rule of thumb, sample sizes larger than 30 and smaller than 500 are appropriate for most studies. In multivariate studies (including multiple regression analysis), the sample size should generally be at least 10 times the number of variables in the study.

Variables and Measurements

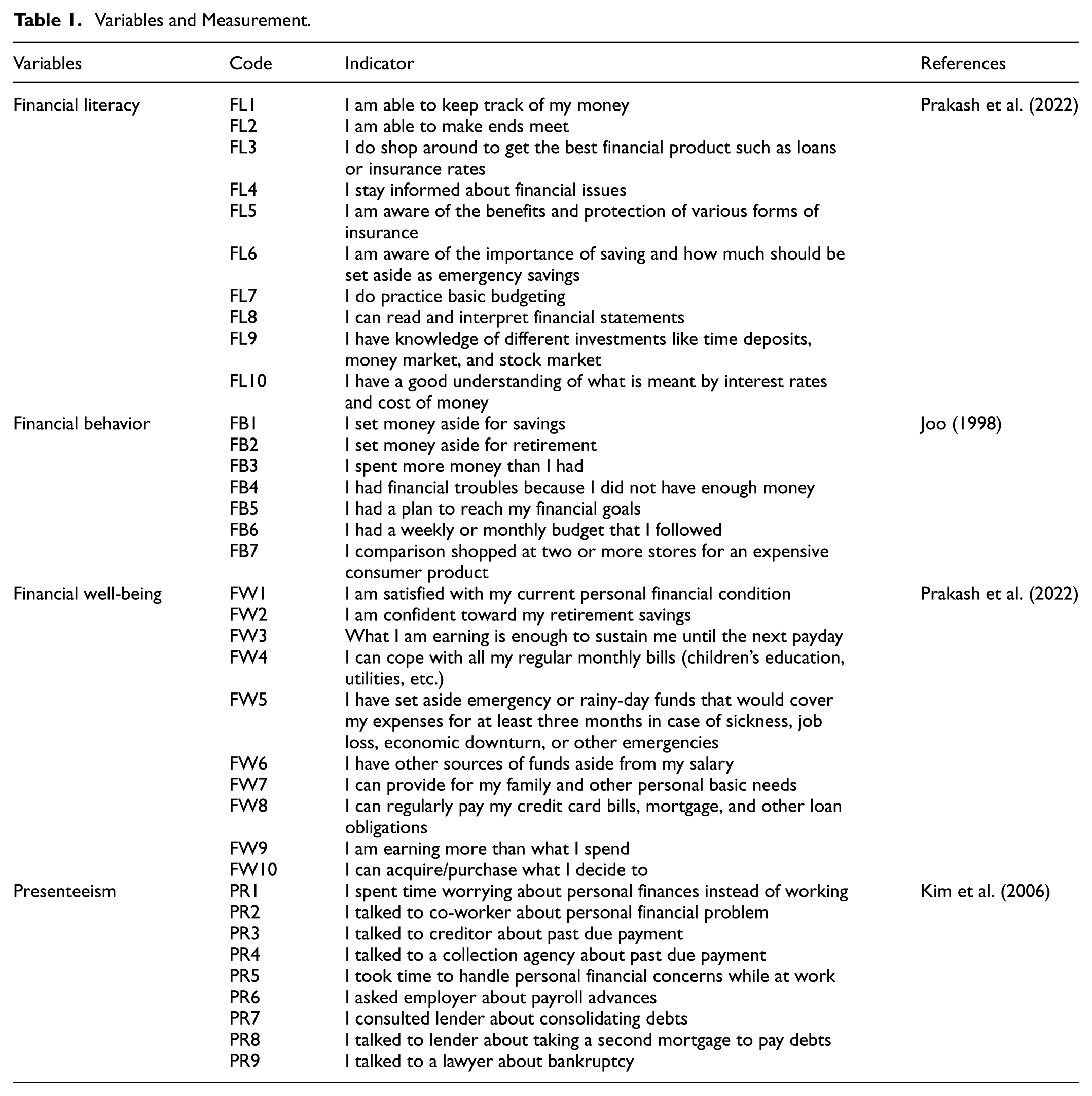

This study examined four variables: presenteeism, financial well-being, financial literacy, and financial behavior. These four variables were measured using a questionnaire with a five-point Likert scale for each question item, which was adopted from previous research (see Table 1). Presenteeism was measured using nine question items related to work time adopted from Kim et al. (2006), which can represent the employee’s work quality. Both financial well-being and financial literacy employ 10 question items adopted from Prakash et al. (2022), while financial behavior uses seven items adopted from Joo (1998). We specifically adopted financial variables question items from a related study that measured employee behavior, for instance, including the questionnaire about debt and salary usage behavior, which cannot be generalized to the individual’s behavior or non-employee.

Variables and Measurement.

Before distributing the questionnaire to a larger sample, a pilot test was conducted to ensure the measurement items adequately represent their respective variables. The results indicate that the internal consistency, as represented by Cronbach’s alpha, is above the threshold of 0.70 (Hair et al., 2016). This result also implies that all of the measurement constructs are valid to be applied in this study.

Method: PLS-SEM

PLS-SEM (partial least squares structural equation modeling) was chosen as the data analysis technique in this study for two reasons. First, this method can accommodate small sample sizes (Widyanty et al., 2024), especially since getting respondents for government employees is not easy because of bureaucratic constraints. Second, many prior studies related to financial literacy, financial well-being, and presenteeism also apply the same analysis technique (Anand et al., 2021; Islam et al., 2024; Respati et al., 2023). PLS-SEM technique divides data analysis into two parts. The first part includes convergent validity, reliability, and discriminant validity of each construct while the second part consists of the conceptual model and hypothesis which are analyzed through path coefficients and specific indirect effects (Yang et al., 2022).

Results and Discussions

Sample Demography

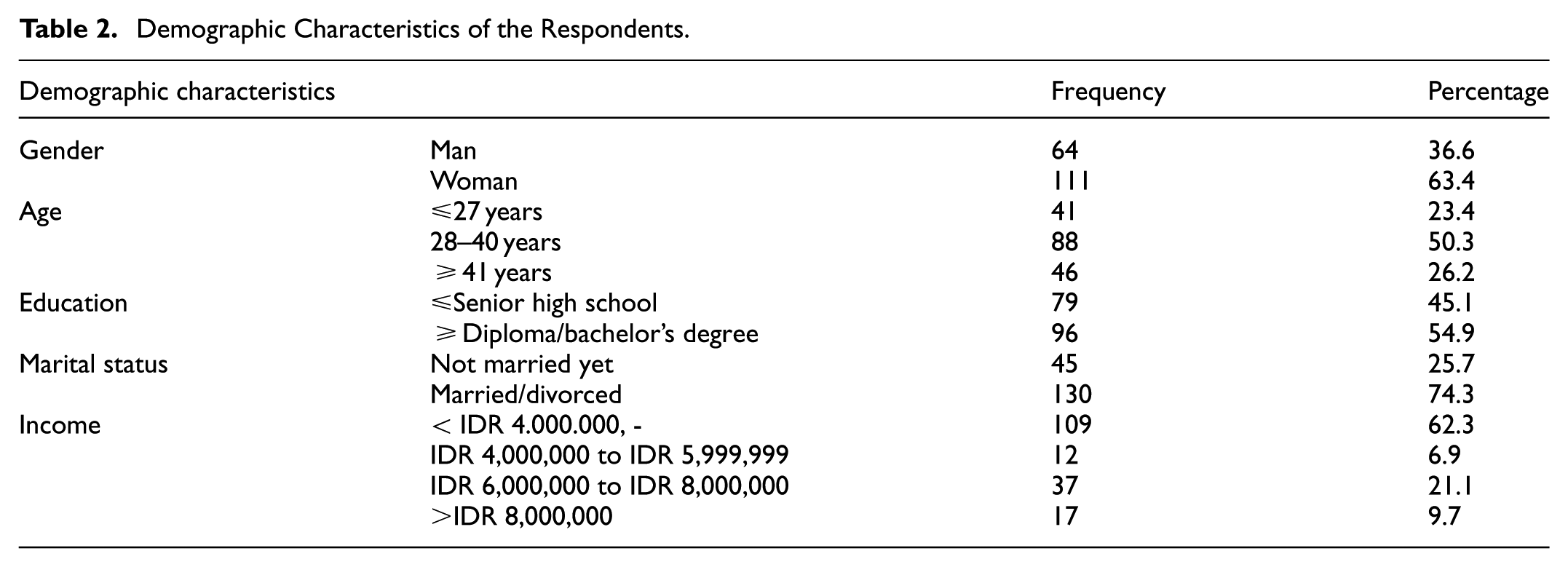

A total of 175 respondents were considered eligible for analysis. Most were women, 111 people (63.4%), and the rest were men. The age of the respondents was divided into 3: under 27 years old (41 people/23.4%), between 28 and 40 years (88 people/50.3%), and over 41 years old (46 people/26.2%). Most respondents earned an income below IDR 4 million (62.3%). Details regarding the demographic characteristics of the research respondents are presented in Table 2. Our respondents have reflected on the population structure of government employees in Indonesia as released by the Central Bureau of Statistics (2026) (Badan Pusat Statistik-BPS), which female has dominated in the Indonesian State Civil Service.

Demographic Characteristics of the Respondents.

Moreover, this domination can influence the differences in financial behavior, financial well-being, and presenteeism, because females generally exhibit a higher level of subjective financial satisfaction than males (Culebro-Martínez et al., 2025). In terms of financial behavior, the female workers have been shown to be more prepared, for instance, in preparation for retirement (Larisa et al., 2021). By contrast, for males, their financial behavior tends to focus on investing in financial market products (Walczak & Pieńkowska-Kamieniecka, 2018). This distinction underscores that females are less risk-taking than males (Schmidt et al., 2021) and is consistent with the empirical evidence that highlights males have a higher level of financial literacy than females (Potrich et al., 2018). However, the male workers also have higher financial stress than females, which can affect work performance (Gardiner & Tiggemann, 1999). Accordingly, the predominance of female respondents in our sample can also influence the direction of the hypothesized relationships.

Validity and Reliability

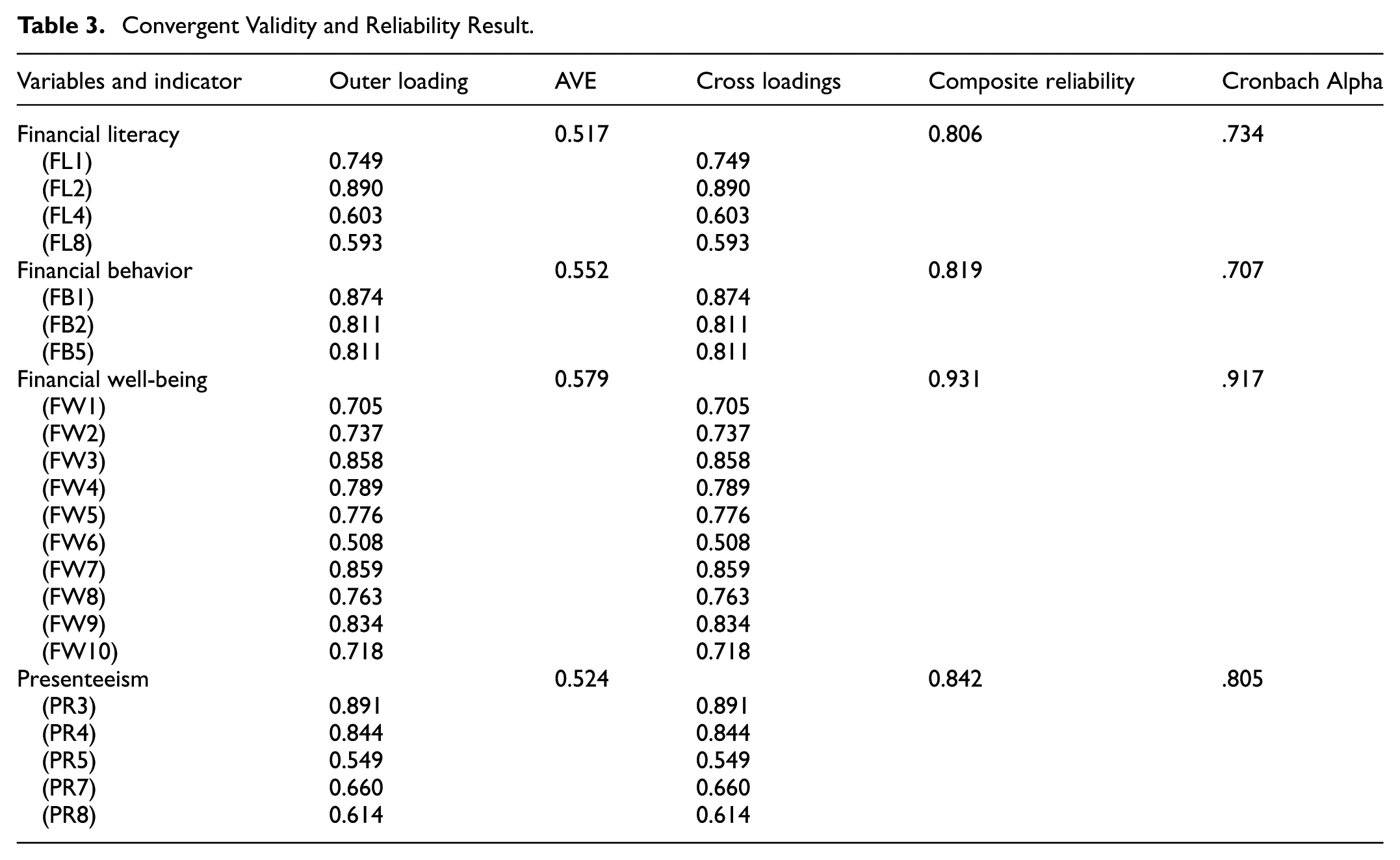

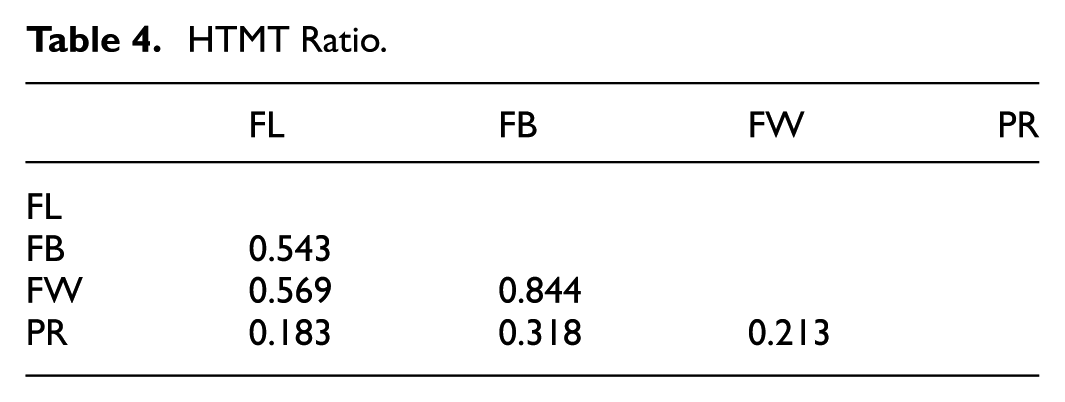

We present Table 3 to show the results of convergent validity, which assesses the extent to which the indicators of each construct correlate with each other. For each construct, the AVE (Average Variance Extracted) value has met the requirements above 0.5 (Yang et al., 2022), indicating that the indicators used are sufficient to explain the construct. In general, acceptable outer loading values exceed 0.7 (or 0.5 in exploratory research) (Hair et al., 2016). Indicators that do not meet the threshold were removed from the measurement model. Lastly, the Composite Reliability and Cronbach Alpha values are both above 0.7, indicating that the model has good reliability (Hair et al., 2009). Discriminant validity was further evaluated using the heterotrait–monotrait (HTMT) ratio. The results presented in Table 4 indicate that all HTMT values are below the recommended thresholds of 0.85 or 0.90, confirming that the constructs are empirically distinct (Hair et al., 2009).

Convergent Validity and Reliability Result.

HTMT Ratio.

Hypothesis Testing and Discussion

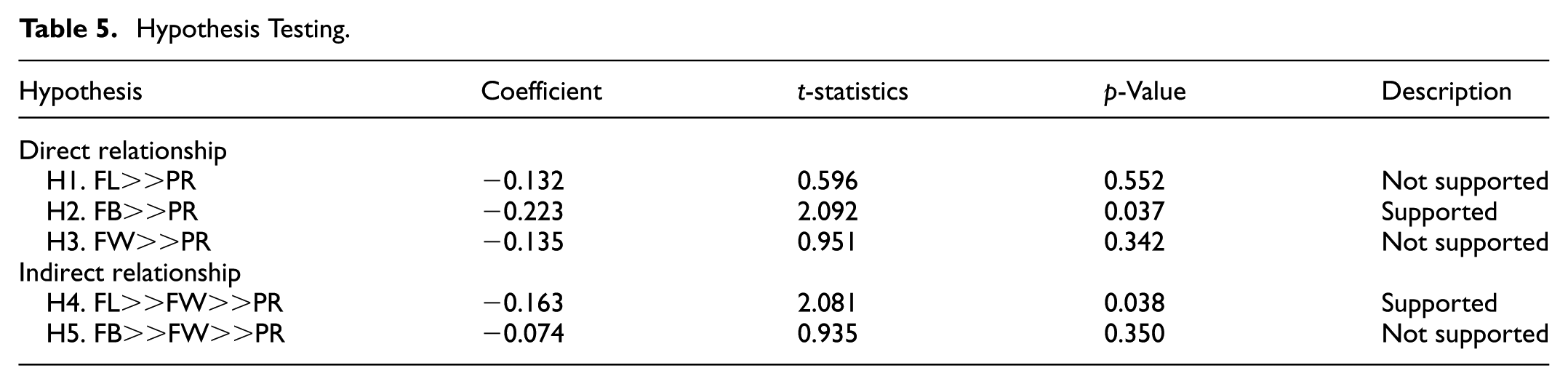

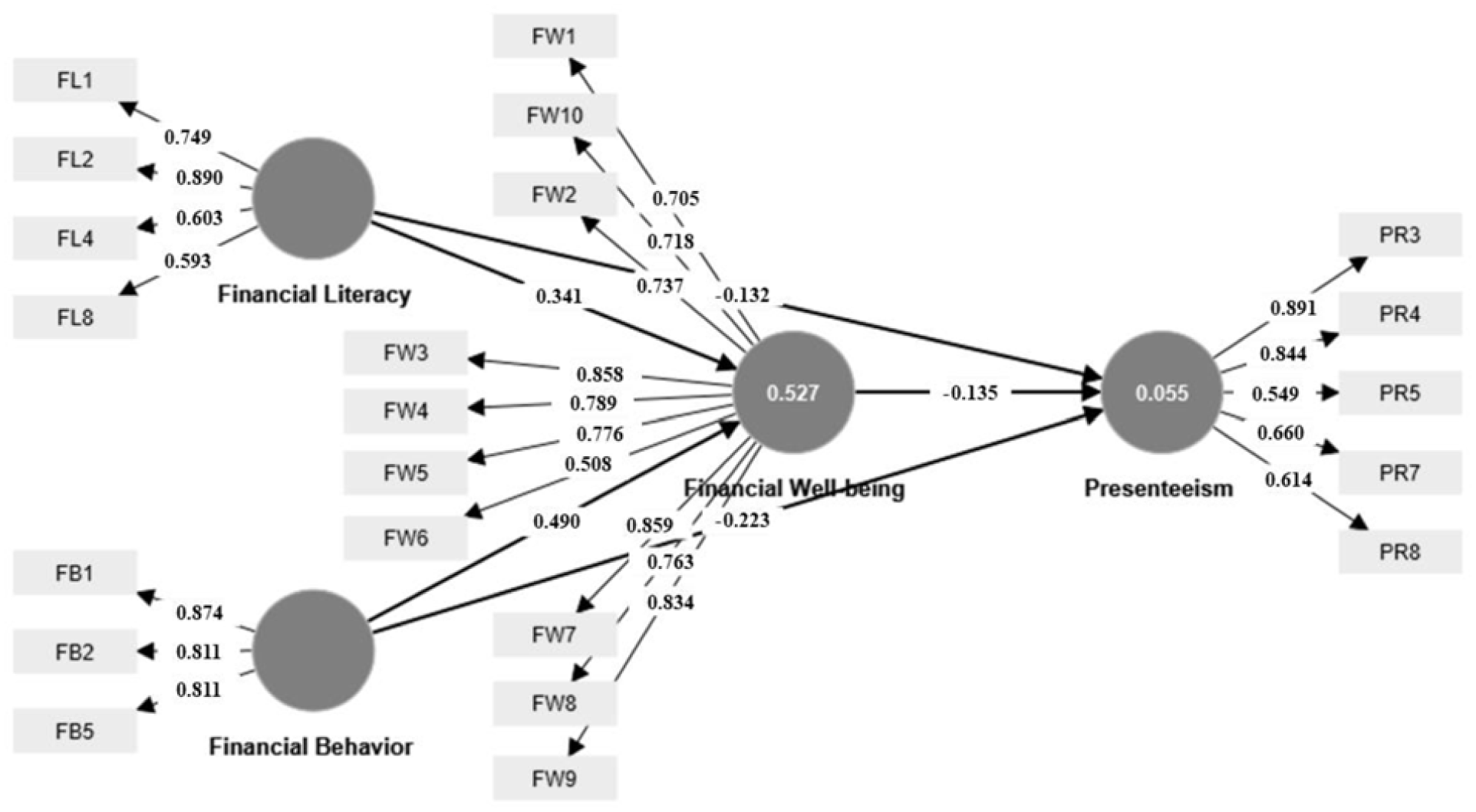

The results of the hypothesis testing of both direct and indirect effects of our independent variables (financial literacy/FL and financial behavior/FB) on presenteeism (PR) are shown in Table 5, while the measurement model is displayed in Figure 2. In the direct effects, the result indicates that the t-statistics and p-value of financial literacy (FL) on presenteeism (PR) do not meet the significance requirements (t = 0.596, p = 0.552). Based on some prior studies (Deacon & Firebaugh, 1988; Sabri & Aw, 2020), we argue that financial literacy cannot directly influence presenteeism. Financial literacy should be mediated by other factors, for example, financial stress, and this association reflects the complexity of personal financial situations and their impact on workplace productivity (Deacon & Firebaugh, 1988; Sabri & Aw, 2020). Financial literacy, in isolation, does not adequately reduce employee presenteeism unless it is complemented by the practical capability to apply financial knowledge in real-life contexts (Sabri & Aw, 2020). Thus, we can conclude that our H1 is not supported.

Hypothesis Testing.

Measurement model.

Meanwhile, the impact of financial behavior (FB) on presenteeism (PR) is statistically significant, as indicated by the results (t = 2.092, p = .037). The coefficient for this relationship is negative (−0.223), indicating that better financial behavior is associated with a lower level of presenteeism. Employees with sound financial behavior demonstrate organized financial management—such as planning for retirement, prudent spending, and investing—which enhances their sense of financial security (Fan & Henager, 2021). Employees with good financial behavior will also be healthier, both physically and mentally. As a result, they are more focused at work, leading to lower levels of presenteeism. In contrast, individuals experiencing financial concern are more likely to suffer from higher psychological distress (Ryu & Fan, 2023). This supports the results of previous studies (Joo & Grable, 2000; Sabri & Aw, 2020) which found that sound financial behavior is associated with fewer financial problems. Therefore, our H2 is supported.

It can also be observed in Table 5 that the direct relationship between financial well-being (FW) and presenteeism (PR) (hypothesis 3) is not supported (t = 0.951, p = 0.342). Thant and Chang (2021) provide empirical evidence showing that the work environment in the public sector is an essential factor to consider. It has been reported that government employees have relatively good financial well-being because they have fixed monthly salaries, which are relatively higher than those in the private sector. However, because of this reason, government employees may also exhibit lower work efficiency due to the fixed nature of their monthly salaries. They do not have a strong incentive to work optimally because they will also get a similar amount if they work less optimally.

Furthermore, as shown in Table 5, the indirect effect of financial literacy (FL) on presenteeism (PR) through financial well-being (FW) is significant (t = 2.081, p = 0.038, coefficient = −0.163), indicating that FW fully mediates this relationship. It confirms the findings from Sabri and Aw (2020) that financial literacy cannot directly impact presenteeism. Employees with a higher level of financial literacy are better able to manage their finances (Sajid et al., 2024), thereby reducing financial stress and enhancing their sense of financial well-being (Fan & Henager, 2021). As a result, they are more likely to work comfortably and maintain greater focus in completing their tasks, which ultimately decreases presenteeism. This finding suggests that financial literacy is a crucial competency for both survival and success in contemporary economic contexts (Yordudom et al., 2024), a view that is also consistent with Maslow’s hierarchy of needs. Accordingly, these results provide support for H4.

The indirect relationship between FB, FW, and PR (Hypothesis 5) is not supported in this study (t = 0.935, p = 0.350). This implies that financial well-being is not a sufficient component to drive the relationship between financial behavior and presenteeism. We assume that this finding is due to the absence of financial worries among government employees in this study. Although the salaries of government officials in Indonesia are not substantially high, they are considered above average for private-sector employees and can provide financial well-being. Moreover, aspects of financial well-being, such as retirement savings, can promote financial resilience (Adee et al., 2024). In this context, such stability may reduce financial stress to a level where it no longer significantly influences presenteeism.

Conclusion, Implications, and Future Research

Conclusion

Global economic conditions, which are increasingly unstable and can impact financial well-being, can disrupt employees’ performance at work. This is an important reason employers pay attention to their employees’ financial conditions. This study found only financial behavior that has a significant influence on presenteeism. This study also finds that financial well-being significantly mediates the relationship between financial literacy and presenteeism. This analysis shows that effectively reducing presenteeism cannot be achieved by increasing financial well-being alone. Instead, it must be balanced with improved financial literacy.

Practical Implications

This study provides several recommendations for employers to prevent presenteeism in employees in financial aspects, including through financial literacy, behavior, and well-being. The inability to achieve good financial behavior has been shown to increase presenteeism. This can be detrimental to employers because it makes the employees stressed and unfocused and causes worsening health status, decreasing performance, and, ultimately, they will loss of productivity. Although it seems evident that with a high income, one’s financial well-being will be easier to achieve, increasing financial well-being does not necessarily require increasing income. The results of this study prove that financial literacy indirectly and financial behavior directly can decrease presenteeism.

Employers can provide programs to increase financial behavior in the workplace. For example, financial behavior can be achieved by financial coaching of the employees. Providing financial education counseling in the workplace has been shown to significantly improve employees’ financial behavior, leading to decreased presenteeism. In addition to financial education counseling or coaching, with increasingly rapid technological advances, employers can offer many alternatives to increase employees’ financial behavior. For example, offering access to relatively safe financial products such as mutual funds, insurance, or automatic savings options so that employees become accustomed to saving.

Furthermore, the results of this analysis show that financial well-being significantly mediates the effect of financial literacy on presenteeism. In addition to increasing financial well-being, an important step that employers must take is to increase employees’ financial literacy. In many cases, someone cannot achieve financial well-being because of a lack of financial knowledge. They remain trapped in financial behavior that exacerbates their financial well-being and increases presenteeism. Therefore, employers need to help employees improve and evaluate their financial literacy regularly.

Employers need to focus on several factors to improve employees’ financial education, including understanding interest rates, the cost of money, financial products, and knowledge about various investments, such as time deposits, the money market, and the stock market. Some of these topics had a low average score from the respondents’ assessment, meaning their understanding of the topic was minimal. Employees’ financial literacy is as such, even though understanding investment and its practices can help employees achieve various financial goals, such as retirement savings.

Limitations and Future Research

One of the limitations of this study is the relatively small sample size and purposive sampling, which could affect the generalization of the research results. Future research should increase the number of samples and expand the scope of employment types, that is, not limited to workers in the government sector only. Future research should explore other independent variables that influence presenteeism so that presenteeism can be anticipated more precisely.

Footnotes

Acknowledgements

The authors would like to thank the editors and anonymous reviewers for their valuable feedback and constructive comments on earlier versions of this manuscript. In addition, we acknowledge the contributions of our research assistants: Bimo Saktiawan, Inas Nurfadia Futri, and Ahmad Febriyanto. This paper was initially developed while Era Miftakhul Jannah was a master’s student in the Master of Management program at Universitas Sebelas Maret, although it was not part of her thesis. Any remaining errors are the sole responsibility of the authors.

Ethical Considerations

All research procedures were approved by the Research Ethics Committee of the Faculty of Economics and Business, Universitas Sebelas Maret (Approval No. 5409.1/UN27.04/TU/2022) on 10 October 2022. The study was conducted in accordance with the ethical standards of the 1964 Declaration of Helsinki and its subsequent amendments, or equivalent ethical guidelines. The approval covered all components of the study, including recruitment, informed consent, data collection, and data management as outlined in the approved protocol. Any changes introduced after the start of data collection were submitted for institutional review and approval in accordance with established requirements.

Consent to Participate

Informed consent was obtained through an information section included at the beginning of the online questionnaire. Participants were informed about the study purpose, procedures, voluntary participation, data use, and publication of de-identified results. They confirmed that they had read and understood this information and provided consent before proceeding with the survey. Data collection was conducted from 15 October to 15 November 2022. Participation was voluntary, anonymity was ensured, no risks were anticipated, and all data were fully anonymized.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study received partial funding from Universitas Sebelas Maret (International Collaboration Research Grant Scheme No. 460/UN27.22/PT.01.03/2026), specifically to support the publication process.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.