Abstract

Green innovation serves as a pivotal force driving high-quality economic development and facilitating the achievement of environmental objectives. As a crucial instrument for regulating firms’ environmental practices, the environmental protection tax exerts a central role in fostering green innovation. Using Chinese A-share listed companies from 2011 to 2019 as the research sample, this study employs DID model to empirically examine the impact and underlying mechanisms of the environmental protection tax policy on firms’ green innovation. The results indicate that the environmental protection tax effectively promotes firms’ green innovation activities through the dual mechanisms of innovation compensation and environmental legitimacy pressure. Specifically, executive pay stickiness exerts a positive moderating effect, and the incentive effect of the environmental protection tax is more pronounced in firms with higher pay stickiness. Further analysis reveals that the promotional effect is significantly stronger in key pollution-monitored enterprises and SOEs compared to other types of firms. This study sheds light on the roles of executive pay stickiness, environmental regulation intensity, and nature of property rights as key boundary conditions. It also broadens the understanding of the microeconomic consequences of environmental tax policies, thereby establishing a reference-worthy framework for emerging economies in terms of legalization, differentiation, and local attribution of revenue in environmental tax system reform.

Plain Language Summary

Using Chinese A-share listed companies from 2011 to 2019 as the research sample, this study employs DID model to empirically examine the impact and underlying mechanisms of the environmental protection tax policy on firms’ green innovation. The results indicate that the environmental protection tax effectively promotes firms’ green innovation activities through the dual mechanisms of innovation compensation and environmental legitimacy pressure. Specifically, executive pay stickiness exerts a positive moderating effect, and the incentive effect of the environmental protection tax is more pronounced in firms with higher pay stickiness. Further analysis reveals that the promotional effect is significantly stronger in key pollution-monitored enterprises and SOEs compared to other types of firms. This study sheds light on the roles of executive pay stickiness, environmental regulation intensity, and nature of property rights as key boundary conditions. It also broadens the understanding of the microeconomic consequences of environmental tax policies, thereby establishing a reference worthy framework for emerging economies in terms of legalization, differentiation, and local attribution of revenue in environmental tax system reform.

Introduction

The intensification of global ecological challenges has prompted governments and the international community to accord greater priority to environmental protection and sustainable development. President Xi Jinping has emphasized that “green development constitutes the very foundation of high-quality development, and modern productive forces are inherently synonymous with green productive forces.” This strategic framing positions green development at the core of the national development agenda. Amid intensifying global competition in the green economy, green development has emerged as an indispensable prerequisite for achieving high-quality economic growth. The promulgation of the Environmental Protection Tax Law in 2018 represented a major turning point in China’s environmental governance system. It replaced the previous pollution discharge fee system with a statutory tax mechanism grounded in the rule of law. Grounded in the “polluter pays” principle and the internalization of external environmental costs, the legislation applies differentiated regulation across four categories: Air and water pollutants are taxed based on pollution equivalent values, covering only the top three to five categories; solid waste is taxed based on net discharge volume; And noise is taxed based on the number of decibels exceeding the standard. A differentiated adjustment mechanism is implemented, meaning “the more you emit, the more you pay; The less you emit, the less you pay; and if you emit nothing, you pay nothing.” It follows the principle that higher emissions incur greater charges, lower emissions incur reduced charges, and zero-emission operations are exempt from taxation. Notably, the policy’s primary objective is not to generate fiscal revenue but to incentivize firms to curtail pollutant emissions and accelerate green innovation. In the context of the “dual carbon” goals, corporate green innovation has become the micro-foundation for high-quality economic growth. Given the inherent complexity of green innovation, enterprises frequently encounter substantial barriers to succeeding independently and thus critically depend on environmental regulatory instruments (G. Wang et al., 2024).

The relationship between environmental regulations and corporate innovation has long been a central concern in both environmental and industrial economics. Nevertheless, existing literature has yet to reach a consensus regarding the specific link between environmental taxes and green innovation. Proponents, drawing on the Porter hypothesis, argue that environmental taxes can stimulate firms to generate greater green innovation through a cost-driven mechanism, thereby creating an “innovation compensation effect” (Porter & van der Linde, 1995; Su et al., 2023; X. Zhao et al., 2023b). For instance, Rubashkina et al. (2015) found that environmental taxes promoted technological innovation in the U.S. manufacturing sector. R. Zhou and Segerson (2012) further noted that such taxes yielded not only a “green dividend” but also a “blue dividend.” In contrast, opponents adhere to the cost-constraint hypothesis, asserting that environmental taxes directly increase firms’ operational burdens, divert resources from research and development, and consequently suppress green innovation (van Leeuwen & Mohnen, 2017; L. Zhao et al., 2023a). Tian and Yae (2024) and Wagner (2007) revealed that environmental taxes reduced patent applications in U.S. and German manufacturing industries. Krass et al. (2013) further argued that high tax burdens increase production costs, lower marginal returns, and thereby stifle green innovation. Although empirical research has made progress, conclusions remain inconsistent due to differences in environmental regulations, tax policies, and sample characteristics.

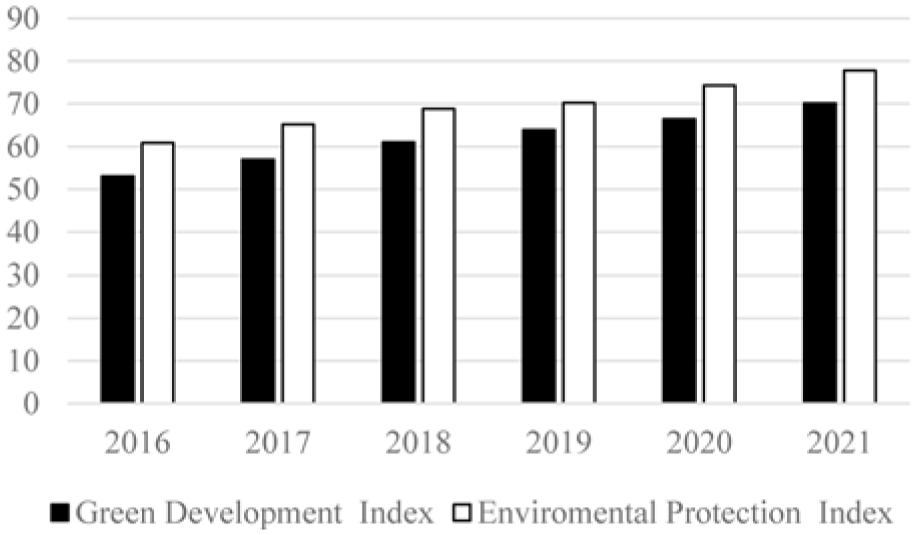

As China’s transition to a market economy deepens, traditional command-and-control environmental regulations—characterized by high implementation costs, limited flexibility, and a propensity to generate efficiency losses—have become increasingly incongruent with the imperatives of green development. Consequently, the environmental governance system is undergoing a gradual transition toward a market-based regulatory model (Jiang et al., 2021; Ren et al., 2018). As illustrated in Figure 1, indicators employed to assess corporate green development and environmental protection exhibit an upward trajectory (Xiong & Zhu, 2023), suggesting that market-oriented environmental regulation has achieved preliminary success. As a primary instrument of market regulation, whether the environmental protection tax system can stimulate green innovation and foster a mutually beneficial scenario for advancing environmental protection and economic development has emerged as a pivotal concern for both academia and policymakers. The enactment of the Environmental Protection Tax Law may be conceptualized as a “quasi-natural experiment,” affording a rare opportunity to examine its real-world impact on corporate green innovation and furnishing a methodological foundation for analyzing this impact. This carries significant practical implications for evaluating policy effectiveness and refining the environmental protection tax system. However, in practice, the environmental protection tax confronts challenges including excessively low tax rates, insufficient collection and administration capabilities, and regional disparities in implementation (Yan et al., 2024); moreover, the boundaries of its effectiveness remain indeterminate. Existing research is still characterized by three critical gaps: Insufficient analysis of transmission mechanisms at the micro-firm level, inadequate attention to the moderating role of internal governance factors such as executive compensation stickiness, and a failure to systematically address the fundamental question of under what conditions the environmental protection tax proves effective. Therefore, grounded in the institutional practice of China’s environmental protection tax, this study adopts an integrated “external policy–internal governance” perspective to systematically examine the boundary conditions and transmission mechanisms through which the environmental protection tax influences corporate green innovation, thereby reconciling conflicting conclusions in the extant literature. The marginal contributions of this paper are as follows:

Trends in green development and environmental protection indicators.

First, it expands the research on the relationship between environmental protection taxes and green innovation by introducing an internal governance perspective. Whereas existing literature has focused predominantly on the intensity of external environment-related regulations (Y. Zhou & Su, 2025) or firm-size heterogeneity (Duan & Rahbarimanesh, 2024), scant attention has been devoted to the moderating role of executive compensation contract design in the transmission of environmental tax policies. Prior studies have examined how executive compensation stickiness influences investment efficiency or general innovation. By contrast, the present study integrates such stickiness into the analytical framework for assessing the effectiveness of environmental protection tax policy. The findings reveal that compensation stickiness, functioning as an implicit incentive mechanism that permits managerial failure, mitigates managers risk aversion and alleviates conservative investment behavior induced by the protracted development cycles and elevated uncertainty inherent in green innovation. Theoretically, compensation stickiness attenuates management’s concerns regarding short-term performance declines, thereby extending their investment decision-making horizon and amplifying the influence of environmental protection taxes in promoting green R&D investment. This study is among the first to validate this moderating mechanism from an integrated “external policy–internal governance” perspective, thereby offering a novel analytical dimension for understanding the micro-level drivers of corporate green innovation.

Second, this study systematically identifies the boundary conditions under which environmental protection levies drive green innovation, thereby addressing the fundamental question of under what conditions the policy proves more effective. Whereas Lu and Zhou (2023) examined exclusively the direct effects of environmental protection taxes on green innovation, the current research further investigates the moderating roles of ecological regulatory intensity and ownership structure. Theoretically, more stringent environmental regulation heightens firms’ compliance pressure, rendering the coercive effect of the environmental protection tax more salient. Moreover, non-state-owned enterprises (non-SOEs), confronted with more constrained financing and weaker political ties, exhibit heightened sensitivity to tax signals. Existing studies have primarily examined the impact of external regulation on information disclosure or general technological innovation, with limited inquiry into its differential moderating effects on the relationship between environmental taxes and green innovation. Through interaction analysis, this study reveals the context-dependent nature of policy effectiveness, thereby providing empirical evidence pertinent to the refined design of differentiated environmental taxation regimes.

Third, by employing micro-level firm panel data, this study identifies the specific transmission mechanisms through which environmental protection taxes influence corporate green innovation, thereby offering actionable policy implications for emerging economies. In contrast to Deng et al. (2023) and earlier studies that relied exclusively on macro-level data at the industry, regional, or provincial levels, this study utilizes micro-level databases of listed companies (e.g., CSMAR and CNRDS) and manually collected data on actual corporate environmental tax burdens. Causal relationships are identified using either a multi-period DID approach or instrumental variable methods. Mechanism tests reveal that environmental protection taxes ultimately prompt an increase in green technology disclosure filings by encouraging firms to channel greater resources into green initiatives and equipment, allocate additional personnel to green R&D, and phase out high-pollution production capacity. Within the institutional context of China’s 2018 implementation of the Environmental Protection Tax Law and the concomitant transition to market-oriented environmental governance induced by the “fee-to-tax” reform, this study distills three replicable policy lessons: Linking tax rates to pollution equivalents, facilitating data sharing between tax authorities and environmental protection departments, and aligning tax incentives with emission reduction performance. These design features may serve as a reference for other emerging economies in formulating market-based environmental regulation policies.

Theoretical Analysis and Research Hypotheses

Theoretical Background

The regulatory effect of environmental protection tax on corporate behaviors is inherently rooted in the basic logic of externality theory. The negative externalities of environmental pollution prevent firms from internalizing the full societal costs of their emissions. Consequently, private marginal costs remain below social marginal costs, rendering market mechanisms insufficient to achieve spontaneous pollution abatement (Dasgupta & Ehrlich, 2013).The primary function of environmental protection taxes is to internalize these external costs by imposing a tax liability for each unit of pollutant emitted. This price signal modifies firms’ cost-benefit calculations, creating an incentive for abatement whenever the cost of emission reduction falls below the corresponding tax liability (Wei et al., 2023).In response to environmental protection taxation, firms may adopt one of several strategies: First, treating the tax as an operating cost; Second, implementing end-of-pipe control measures, such as installing pollution control equipment; Or third, pursuing green innovation to reduce pollutant emissions at the source or through process improvements (Chen & Zhou, 2025).These three approaches exhibit markedly different cost structures. The first two generate immediate outcomes in the short term but fail to produce sustained competitive advantages. By contrast, green innovation can fundamentally lower long-term compliance costs, though it entails high upfront investment, lengthy implementation cycles, and uncertain returns. A firm’s decision to pursue green innovation ultimately depends on management’s intertemporal assessment of costs and benefits, as well as its risk tolerance (Peng et al., 2023).Extending this logic, Chen and Zhou (2025) proposed that appropriately designed environmental regulations can induce an innovation compensation effect, through which firms utilize technological innovation to enhance production efficiency and reduce compliance costs. This effect may offset—or even surpass—the short-term cost burden imposed by environmental regulations, ultimately yielding concurrent ecological and economic benefits.

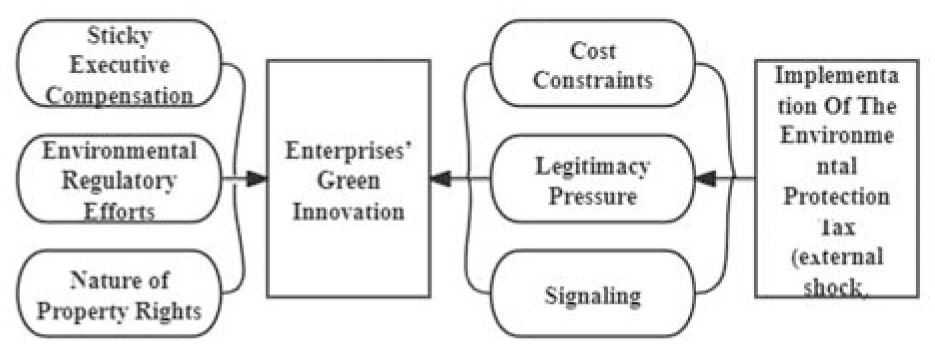

An enterprise’s internal governance system and external regulatory environment profoundly shape this trade-off process. From the perspective of internal governance, the separation of ownership and control in modern corporations implies that managers’ personal interests are not fully aligned with the firm’s long-term value (Gao et al., 2023). The risk of failure associated with green innovation investments may damage managers’ professional reputations and compensation, leading risk-averse managers to shy away from such investments (Mielke & Steudle, 2018). The design of executive compensation contracts plays a crucial role in this context: Compensation stickiness refers to the phenomenon whereby compensation rises more with performance increases than it falls with performance decreases—that is, “easy to increase but hard to decrease” (Jackson et al., 2008). Existing research suggests that compensation stickiness provides executives with institutional protection against failure, alleviates their excessive anxiety regarding innovation failures, and enhances their willingness to take risks (Zu et al., 2025). When firms face cost pressures from environmental taxes, executives with high compensation stickiness—whose compensation is less vulnerable to performance declines—are more willing to allocate resources toward green innovations that offer long-term returns. Conversely, executives with low compensation stickiness may opt for low-cost compliance measures, such as paying fines or implementing end-of-pipe treatment, to avoid compensation losses arising from short-term performance fluctuations (Gu & Chen, 2025).From the perspective of external regulation, firms designated as key pollution monitoring targets face stricter administrative inspections, information disclosure requirements, and public scrutiny. In this context, the economic constraints imposed by the environmental protection tax combine with regulatory pressures to produce an additive effect (Guedhami et al., 2025). This significantly reduces firms’ room to evade emission reductions, thereby rendering the motivation for green innovation structurally more effective. From the perspective of ownership structure, state-owned enterprises (SOEs) are tasked not only with profit objectives but also with policy mandates such as green development. Benefiting from preferential access to resources (e.g., low-interest loans and government subsidies) and greater policy enforcement rigidity, SOEs often respond more proactively to signals from eco-taxes. By contrast, private enterprises rely increasingly on exchange-oriented input–output return evaluations. Although their green innovation decisions may be more sensitive to tax signals, they are also more easily constrained by short-term profit pressures (Zheng & He, 2022).These internal and external conditions collectively determine whether environmental protection taxes can effectively transform cost pressures into a driving force for corporate green innovation. The technical roadmap of this paper is presented in Figure 2.

The technical roadmap.

The Correlation between the Environmental Protection Tax and Corporate Green Innovation

The Environmental Protection Tax Law aims to improve environmental quality and reduce pollutant emissions. As a primary market-based regulatory instrument for advancing green development, it promotes ecological conservation and facilitates the green transition of enterprises through a dual mechanism of incentives and constraints.

Prior studies have predominantly explored how environmental regulations affect green innovation through cost-pressure and policy-incentive channels. Some scholars confirm that stringent environment-related regulations can encourage firms to increase R&D investment and promote innovative output (Martínez-Zarzoso et al., 2019). Conversely, other studies have argued that environmental regulations may exert a cost burden that crowds out corporate innovation, thereby inhibiting technological upgrading (Y. Cao et al., 2025).Overall, although the extant literature has extensively examined traditional environmental regulatory instruments, micro-level research on the impact mechanisms of the Environmental Protection Tax Law—a policy characterized by both legalization and marketization—remains relatively scarce. In particular, systematic analyses integrating the combined effects of cost internalization, legitimacy pressures, and signaling within a unified framework remain limited.

From a theoretical perspective, the implementation of environmental protection taxes internalizes pollution costs, substantially increasing compliance burdens and operational pressures on high-pollution, energy-intensive enterprises, thereby disrupting the cost-benefit equilibrium of their conventional extensive production models (Dong et al., 2024). Green innovation can reduce pollution emissions and per-unit environmental costs at the source, thereby achieving long-term cost reductions and efficiency gains through enhanced resource utilization. When the economic and compliance costs associated with pollution exceed the long-term investments required for green innovation, rational firms tend to intensify their investments in energy-saving technologies and environmentally friendly processes to mitigate cost pressures and sustain their competitive advantage (L. Yang et al., 2026).

Furthermore, environmental protection tax effectively prevents firms from evading environmental obligations through cross-regional relocation or other avoidance strategies. The institutional arrangement that allocates tax revenues to local governments further strengthens local authorities’ regulatory incentives and enforcement capabilities, thereby exposing firms to heightened pressure regarding environmental legitimacy. To achieve regulatory compliance, firms are compelled to reallocate R&D expenditures and human capital toward green technology innovation, thereby strengthening their innovation capabilities. Moreover, the policy pressure generated by the environmental protection tax draws significant attention from external stakeholders. As officially recognized indicators of technological innovation, green patents serve as credible signals to regulators, investors, and the public regarding a firm’s green transition. Consequently, firms subject to environmental protection tax pressure are motivated to increase their green invention filings to secure legitimacy and obtain potential tax incentives (T. Zhang & Xi, 2025).

In summary, the environmental protection tax drives corporate green innovation through a combination of cost constraints, legitimacy pressures, and signaling effects. Based on this, this paper proposes Hypothesis 1:

The Moderating Effect of Sticky Executive Compensation

Principal-agent theory posits that the strategic orientation of corporate innovation is inextricably linked to executive decision-making. The efficacy of environmental protection taxes in driving corporate green innovation is contingent upon executives’ prioritization of resource allocation toward environmental investments and their exercise of requisite decision-making authority within the corporate governance framework. However, green innovation activities typically necessitate substantial investments in human, physical, and financial capital and are characterized by protracted payback periods, thereby precluding the generation of immediate, tangible returns. This substantially heightens the risks and uncertainties confronting firms (Liu et al., 2023). When executives confront adverse outcomes or penalties stemming from failed investments, their rational inclination is toward risk aversion, thereby curtailing investment in green innovation projects (M. Y. Wang et al., 2023).

Against this backdrop, executive compensation stickiness, as an internal governance mechanism, plays a critical moderating role. Compensation stickiness reflects a high tolerance among principals for agents’ investment failures; specifically, firms refrain from excessively reducing executive compensation during periods of poor performance, thereby engendering an incentive structure characterized by “generous rewards and mild penalties” (T. Zhang & Xi, 2025). When executive compensation stickiness is high, the risks and potential personal losses confronted by managers in pursuing green investments are significantly mitigated. This encourages managers to assume greater risks and enhances the likelihood of green innovation investments (Zu et al., 2025). With sustained financial resources and strategic decision-making support, the firm’s level of green innovation will gradually improve.

Admittedly, the efficacy of executive compensation stickiness is bounded; excessive stickiness may induce moral hazard (Tao & Liu, 2024). On balance, however, by affording management institutionalized tolerance for failure, executive compensation stickiness effectively mitigates the perceived risk-related costs of green innovation, thereby reinforcing the positive effect of environmental protection taxes on corporate green innovation. Accordingly, we propose Hypothesis 2:

The Moderating Effect of Environmental Regulatory Efforts

Drawing on externality theory, the environment, as a quintessential public good, is inherently characterized by ambiguous property rights and significant negative externalities (Dasgupta & Ehrlich, 2013). When environmental regulation is absent or penalties for non-compliance are insufficient, the external costs of corporate pollution remain substantially lower than the internalized costs of environmental expenditures, thereby severely undermining the deterrent effect of green taxation. Therefore, the stringency of environmental regulation constitutes a pivotal institutional condition. This regulatory stringency determines whether environmental tax policies can effectively promote corporate green technological advancement.

Within China’s decentralized administrative system, subnational governments bear primary responsibility for ecological governance. The intensity of their supervision directly influences the environmental compliance behavior of firms within their jurisdictions. Tao and Liu (2024) find that when environmental regulation is lax and policy expectations are unstable, firms tend to delay or reduce environmental investments to avoid the risk of sunk costs arising from policy uncertainty, thereby suppressing green innovation. Conversely, Lv et al. (2021) argue that stringent ecological regulation compels enterprises to increase environmental capital investment, thereby enhancing green innovation output. In a highly regulated environment, government mandates for corporate environmental data disclosure enhance information transparency, creating a mechanism that incentivizes firms to allocate greater resources to green innovation projects. Furthermore, when policy tools such as emission standards and emissions trading systems are implemented in conjunction with the environmental protection tax, they produce a more pronounced superimposed effect, establishing stringent external constraints on corporate behavior and compelling firms to internalize environmental protection and green innovation as strategic priorities in their operational decision-making (Han et al., 2026).

In summary, a robust environmental regulatory framework constitutes a critical foundation for the effective implementation of the environmental protection tax system. As regulatory enforcement intensifies, enterprises face mounting institutional pressures, thereby strengthening their incentives for green innovation. As the primary targets of environmental regulation, key pollution-monitored enterprises face substantially greater compliance pressures and policy scrutiny than other enterprises; accordingly, they are more likely to intensify their green innovation activities in response to environmental protection tax incentives. Based on the foregoing analysis, we propose Hypothesis 3:

The Moderating Effect of Nature of Property Rights

Existing literature has extensively examined the impact of environmental protection taxes on corporate green innovation. Nevertheless, scant attention has been devoted to examining how ownership type moderates this relationship. This study posits that, in response to environmental protection tax policies, state-owned enterprises (SOEs) demonstrate a stronger propensity for green innovation than their non-state-owned counterparts.

First, from the perspective of corporate social responsibility, SOEs bear significant social responsibilities, including maintaining economic stability, ensuring employment security, and alleviating poverty (Cheng et al., 2026), and they are institutionally obligated to pursue green development in alignment with national strategies (Z. Y. Zhao et al., 2024). Consequently, SOEs are more inclined to allocate resources toward green innovation to fulfill their environmental responsibilities when confronted with regulatory pressure. Second, drawing on stakeholder theory, senior executives of SOEs are often motivated by political career incentives and thus attach greater importance to non-economic objectives, including environmental performance (G. W. Kong et al., 2021). Consequently, they perceive the pressure from environmental protection taxes as a strategic opportunity for green transformation rather than a mere financial burden. Simultaneously, state-owned enterprises enjoy significant advantages in credit markets, enabling them to secure external financing at lower cost (Huang et al., 2026). This advantage affords state-owned enterprises a robust financial foundation to redirect the burden of environmental taxes toward green innovation investments, thereby enhancing their capacity to reallocate resources effectively in response to environmental tax policies. Third, owing to higher levels of environmental information disclosure (Weber, 2014) and stronger external oversight, SOEs are subject to institutional pressure that compels them to leverage green innovation to improve environmental performance (Z. Y. Zhao et al., 2024). Finally, from the perspective of reputation theory, SOEs are motivated to signal their environmental commitment to the market through green innovation to maintain a favorable corporate image (F. Kong & Zhang, 2014).

Existing empirical evidence also supports this logic: Yu et al. (2019) found that environmental taxes significantly promoted green innovation among SOEs while exerting no significant effect on private enterprises; Y. Zhou and Su (2025) further confirmed that environmental protection taxes exert a more pronounced facilitating effect on green technological innovation among SOEs. Therefore, by leveraging their institutional resources, commitment to social responsibility, and informational transparency advantages, SOEs are better positioned and more inclined to increase investments in green innovation in response to environmental tax policies. Based on these considerations, we propose Hypothesis 4:

Description of the Econometric Model and Variables

Data Source

We use A-share listed companies for the years 2011 to 2019 as the sample, with the following exclusions: (1) ST and *ST companies; (2) financial companies, as their impact on the environment is typically less significant and has different characteristics than other companies; (3) any firm with missing variables is excluded; (4) in 2020, many companies ceased production due to COVID-19 regulations. For guaranteeing the reliability of the empirical data, we restrict sample selection to the period before 2019. Enterprise green innovation data is drawn chiefly from the CNRDS database, for other variables, the CSMAR database of Shenzhen Guotaian Information Technology Co. serves as the main source.

Variable Description

Explained Variable: Firms’ Green Innovation (gi)

Green innovation encompasses any activity that enhances innovation value and novelty while simultaneously achieving environmental improvements and resource conservation. Scholars from different disciplines adopt varying measurement criteria based on their distinct research perspectives. The concept of green innovation in China emerged in the late 1990s and has since become a mainstream theme in the 21st century. Today, green innovation encompasses not only environmental technologies, processes, and products but also organizational, institutional, and managerial innovations. This paper adopts the perspective of Song and Yu (2018). The green patent data in the sample are based on the total number of granted green patents, which effectively reflects enterprises’ current innovation output. Compared with research and development (R&D) investment, patents directly measure innovation outcomes rather than input efforts, and can distinguish between substantive innovation (invention patents) and strategic innovation (utility model patents), making them more suitable for the research questions addressed in this paper.

Explanatory Variables: Policy Intervention Variables

Amount of environmental protection tax collected varies by province. Some provinces set higher tax rates than the earlier pollution discharge fees, and became subject to a strong influence from the environmental protection tax policy. In contrast, policy impact for other provinces that have maintained similar tax rates is less pronounced. Therefore, following the study by Y. P. Wang et al. (2026b), the policy dummy variable (treat) in this paper is defined as follows: If a firm is registered in a region where the 2018 levy standard remained unchanged, it is classified as part of the control group and given a value of 0. For firms located where the 2018 levy standard was raised, they are classified as part of the treatment group and coded as 1. Additionally, we include a dummy variable for time, labeled “post.” If 2018 or a later year is indicated, meaning the sample was collected after the policy was implemented, then POST equals 1; otherwise, it equals 0.

Moderator Variable

Executive compensation stickiness (nx): According to Tsang et al. (2021), compensation contracts should encompass compensation levels, compensation structures, and the correlation between compensation and performance. This paper first discusses the correlation between compensation and performance and then incorporates executive compensation stickiness into existing models. Following the methodology of J. Wang et al. (2022). We first compute, for each year over 2011 to 2019, the chained rates of growth in average executive pay and net earnings. Next, we compute the ratio between the chained growth rate of executive compensation and that of net profit, which reflects the sensitivity of pay to performance changes. Subsequently, we calculate the rolling average of this sensitivity over the previous 4 years plus the current year (a total of 5 years). Finally, To derive the responsiveness of compensation with respect to changes in performance, we compute the proportion of the chained rate of increase of executive compensation relative to that of net profit.

Environmental Regulations (regu): In recent times, China has rolled out a succession of environmental rules targeting the fostering of a healthier society. As key market participants, firms are at the center of these regulatory efforts. However, as the economy develops, market failures resulting from factors such as information asymmetry and an imperfect legal framework are inevitable. Therefore, government intervention is essential, and regulation functions as a principal means of safeguarding the environment. The Csmar database contains data on listed companies designated as key pollution monitoring units, environmental incidents, violations of environmental regulations, and environmental complaints. To assess the level of environmental regulation, this paper uses a company’s designation as a key pollution monitoring unit, drawing on Li et al.(2024) study, which employed a difference-in-differences model for investigating the causal link between environmental protection taxes and corporate green technology uptake. We assign 1 as the value for firms listed as key pollution monitoring units, and 0 for those not designated as such.

Nature of Ownership (SOE): Modern corporate theory places considerable emphasis on the moderating role of ownership structure. Within Chinese institutional context, enterprises can be divided into two categories based on the nature of ultimate control: State-owned enterprises (SOEs) and non-state-owned enterprises. SOEs differ markedly from non-state-owned enterprises in terms of resource access, fulfillment of social responsibilities, and responsiveness to policies (Hu et al., 2023; Xu et al., 2022), and they engage in more comprehensive ESG disclosure (Ding et al., 2022; Weber, 2014). These characteristics may influence firms’ green innovation decisions when operating under environmental regulatory pressure. Accordingly, this study introduces ownership nature as a moderating variable, coding 1 for state-owned firms and 0 for non-state-owned firms (Y. T. Zhang & Guo, 2026). The CSMAR database is the origin of the data.

Control Variables

Building on previous research concerning the impact of green levies on internal firm green innovation, this research selects specific economic characteristics of these firms to be used as control variables in the model. Generally speaking, larger firms have higher innovation success rates (X. Yang & Wang, 2023). Drawing on the research methods adopted by G. X. Cao et al. (2024) and Y. Cao et al. (2025), this study measures firm size—denoted as size—using the natural logarithm of the net assets of listed enterprises. Cash holdings equal cash and cash equivalents scaled by total assets; debt-to-equity ratio is used to determine financial leverage; ROA is used for profitability assessment; investment opportunities are evaluated using Tobin’s Q; growth is measured using revenue growth rate; the ratio of equity division is assessed using SEP. The existing equity structure data from CSmart is utilized, with specific variable definitions provided in Table 1.

Variable Names and Definitions.

Model Construction

Constructing a Double Difference Model of Environmental Protection Tax and Corporate Green Innovation

DID is commonly used by scholars to estimate policy effects because it can largely avoid the problem of endogeneity. In empirical testing, endogeneity often poses a significant challenge, particularly since policies are typically exogenous variables for microenterprises. The employment of a double difference model can address reverse causality, making it highly favored by researchers. The conventional DID model includes a multiplicative term that links the treatment dummy (treati) and the period dummy(postt), and the model can be formulated as follows:

Against this context, Yi,t represents dependent variable, with i and t indicating individual and time, μi and λt denote individual and time fixed effects. Xi, t denotes the control variable. The variable “treati” represents the treatment group in this study. One is assigned to the variable if individual i is in treatment group affected by policy shock; 0 is assigned if individual i is in control group unaffected by policy shock. Likewise, the dummy variable postt indicates the treatment period for the treated group, taking 1 for individual i who enters the treatment period for the first time and 0 for individuals who have already been subjected to the treatment. Additionally, including both dummy variable treati and the individual fixed effect μi is not necessary, nor the dummy variable postt and the time-fixed effect λt in the double-difference model, as this could lead to multicollinearity issues if both are included.

The treatment effect is determined by computing the disparity between the treatment group’s before-and-after transformation and that of the control group. To investigate the link between environmental protection levies and firms’ green innovation, we have constructed a model grounded in the previously mentioned equation.

Model 2 is used to test Hypothesis H1. Hypothesis GIi, t is the dependent variable, with i indicating individuals and t represents time. Meanwhile, the variable didi, t denotes treati × postt. Treati is a firm dummy, postt is a time dummy, Xi, t represents the control variables, and μi and λt are firm and year fixed effects. Finally, εi, t stands for model error term. When the coefficient α1 proves significantly positive, this suggests that the enforcement of the environmental levy leads to a marked increase in the level of green innovation within firms, thus verifying hypothesis H1; otherwise, hypothesis H1 is invalid.

Environmental Protection Tax, Executive Compensation Stickiness and Corporate Green Innovation

Model 3 tests hypothesis H2, where GIi,t is the dependent variable and nxi,t is the moderator variable (executive compensation stickiness). Coefficient α1 captures the interplay between executive compensation stickiness in green taxes and its impact on firms’ green innovation. If α1 turns out significantly above zero, it suggests that executive compensation stickiness may act as a positive moderator for the effect of green taxes on corporate green innovation.

Environmental Protection Taxes, Environmental Regulatory Efforts and Corporate Green Innovation

Model 4 tests Hypothesis H3, with GIi,t as the dependent variable and regui, t as the moderator variable (environmental regulation). The coefficient α1 represents the interaction between environmental regulation and the environmental protection tax on corporate green innovation. A significantly positive α1 suggests that the environmental protection tax has a stronger promotional effect on the green innovation of key pollution-regulated corporations. Conversely, if α1 is not significantly positive, Hypothesis H3 cannot be confirmed.

Environmental Protection Tax, Nature of Property Rights, and Corporate Green Innovation

Model 5 tests Hypothesis H4, where GIi, t is the dependent variable, with soei, t serving as the moderating variable (nature of property rights). α1 is a coefficient capturing interaction among environmental protection tax, property rights type, and firm green innovation. A significantly positive α1 indicates that SOEs have successfully implemented the policy, resulting in a marked rise in green innovation. Therefore, Hypothesis H4 holds. Conversely, if α1 is not significant, the hypothesis is invalid.

Empirical Analysis

Descriptive Statistics

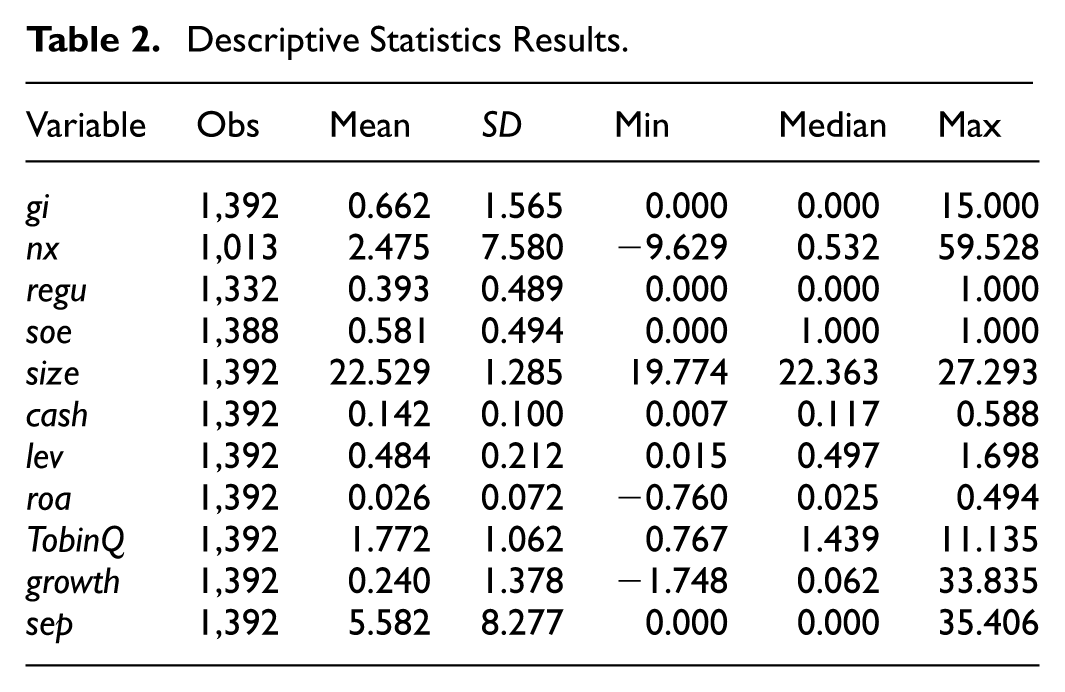

Table 2 sets forth summary statistics of relevant variables. Average value for green innovation variable (GI) equals 0.662, and its corresponding standard deviation amounts to 1.565. This indicates that green innovation prevalence among Chinese firms is relatively low, accompanied by notable variation across firms. The standard deviation of executive compensation stickiness (nx) is 7.580, indicating significant discrepancies in compensation stickiness across enterprises. Additionally, an analysis of the distribution of the sample enterprises revealed that 39.3% are identified as key pollution monitoring units, and 58.1% are state-owned enterprises, pointing to the sample being relatively balanced, comprehensive, and representative in nature.

Descriptive Statistics Results.

Test of the Relationship between Environmental Tax and Enterprise Green Innovation

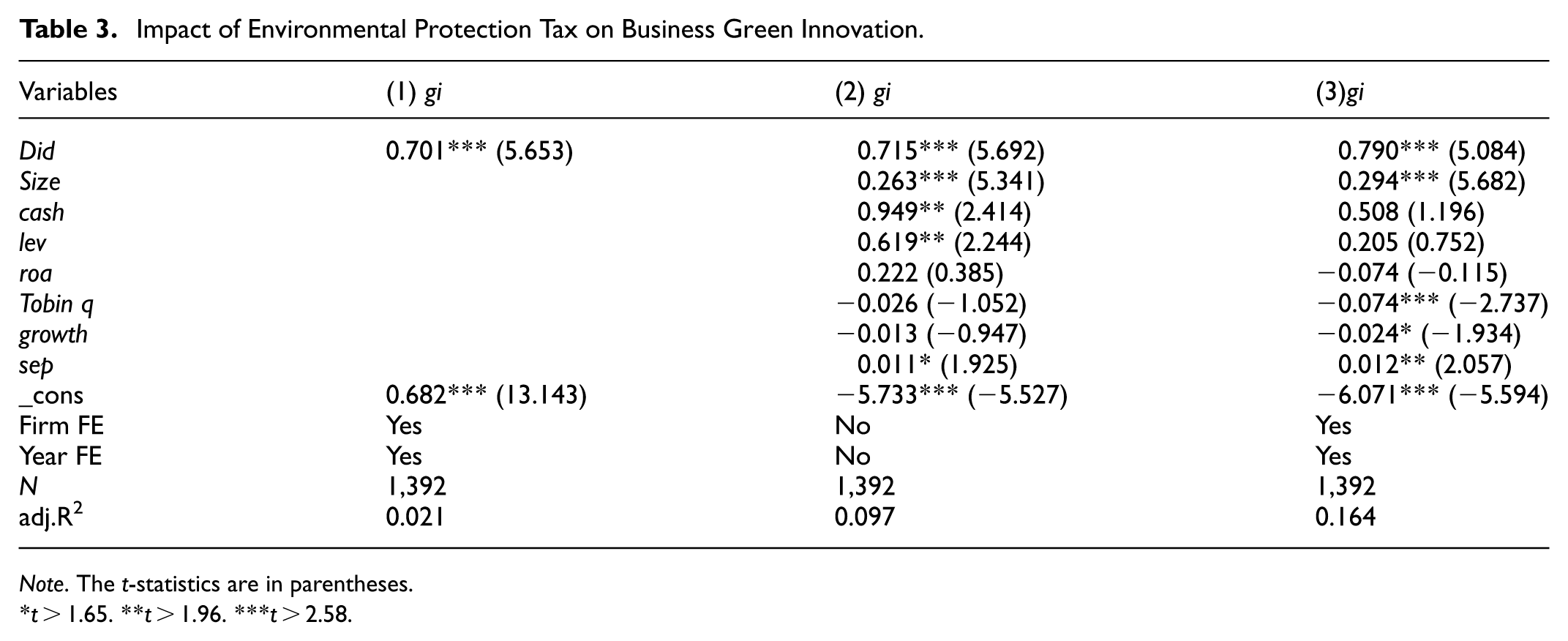

The present study employs a difference-in-differences model to assess whether environmental protection tax promotes corporate green innovation. Table 3 shows the findings of the research. The initial column shows findings lacking control variables or fixed effects. Column two presents findings with control variables, while column three presents findings when fixed effects are added to column two. The coefficients of the interaction terms are all significant at the 1% level. These findings suggest that the environmental protection tax system contributes to enhancing firms’ green innovation. Given the preceding theoretical discussion, environmental protection taxation encourages enterprises to carry out green innovation strategies and to raise their investment in R&D for green technologies and products. Such an outcome is achieved through a mix of preferential policy incentives and regulatory constraints, ultimately leading toward a rise in green innovation. Thus, hypothesis 1 is supported.

Impact of Environmental Protection Tax on Business Green Innovation.

Note. The t-statistics are in parentheses.

t > 1.65. **t > 1.96. ***t > 2.58.

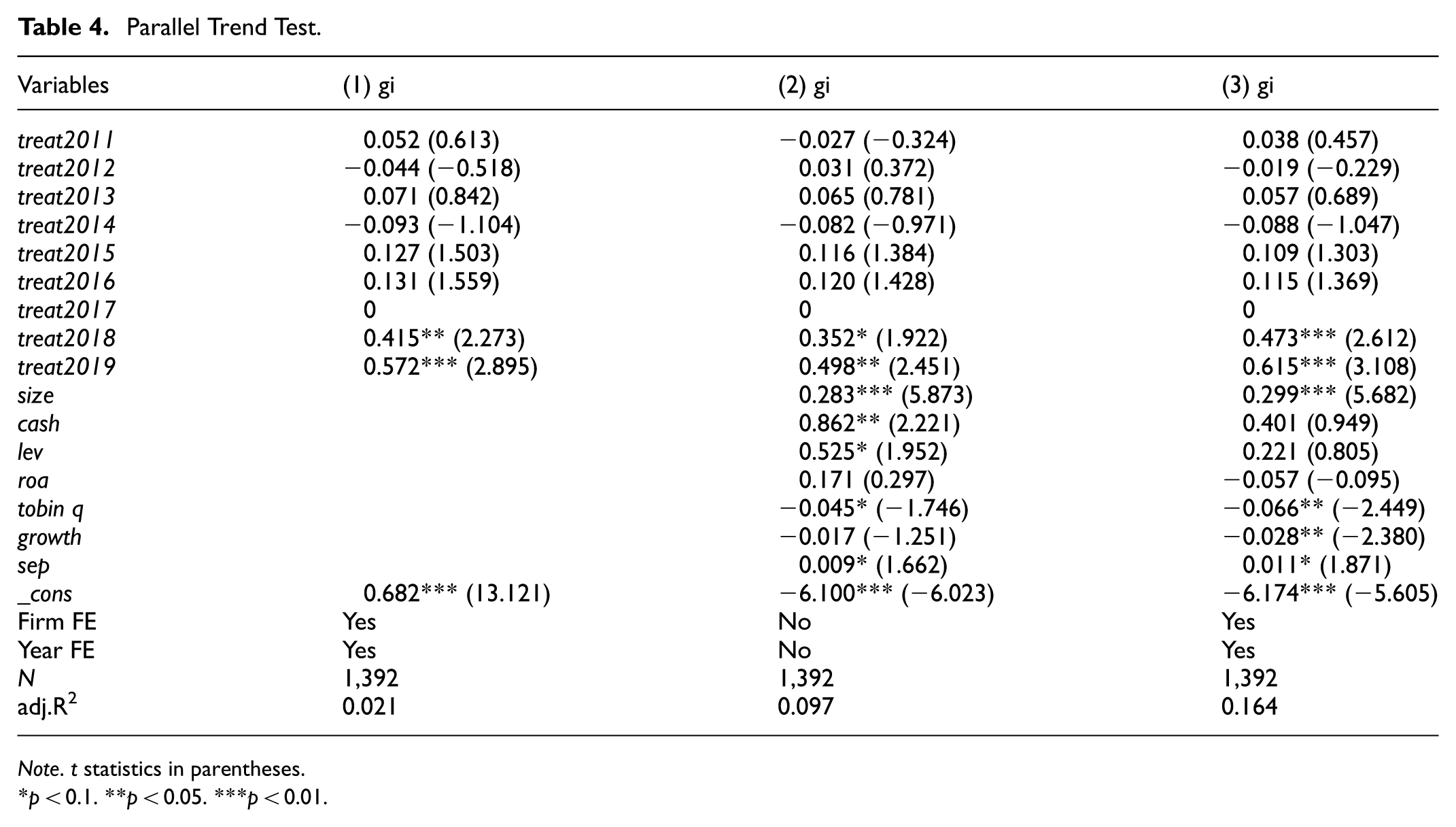

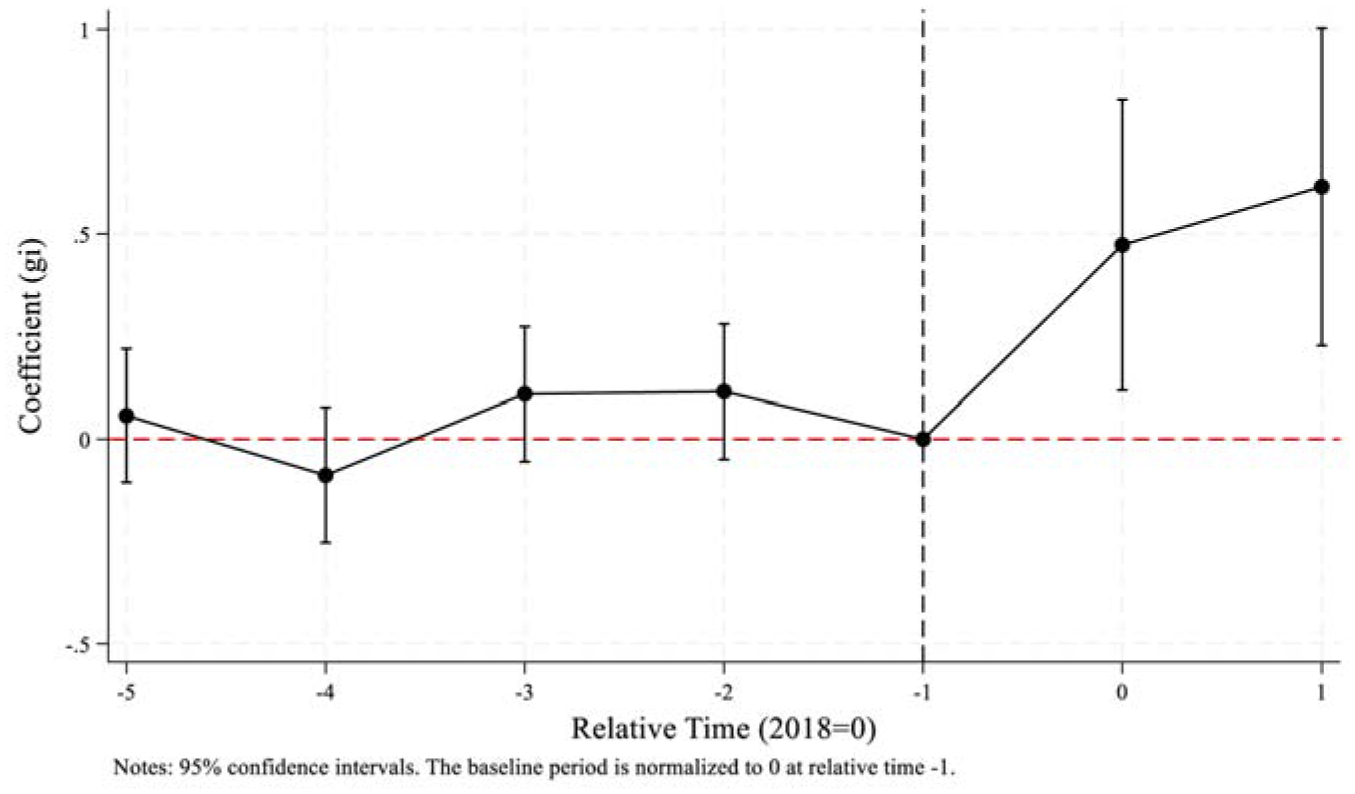

The reliability of the difference-in-differences model lies on the parallel trends assumption. This assumption holds: The dependent variables in the experimental group along with the comparison group must follow common trends before policy implementation. If this assumption does not hold, the difference-in-differences estimator will be biased, which results in an inflated or diminished estimate of the intervention effect. Drawing on the methodology of Roth (2022), this study tests the parallel trends assumption by including interaction terms for each period prior to and subsequent to policy implementation within the regression model. Following standard practice, the year before policy adoption (2017) gets selected for the benchmark period, while each estimated coefficient gets considered as differences in relation to that year. Table 4 provides regression results of event study, while Figure 3 illustrates the dynamic changes in coefficients across periods. As shown in Table 4 and Figure 3, the interaction terms for the pre-policy periods (2011–2016) are all insignificant, fluctuating around zero without significant systematic deviations, and their 95% confidence intervals all pass through the zero line. Based on a comprehensive assessment of the economic significance of the coefficients, their volatility characteristics, and prior sectoral knowledge: The coefficients for the pre-policy periods as a whole show no significant systematic trend, and the treatment and control groups exhibit good ex ante comparability prior to policy implementation, providing empirical support for the identification assumptions of the difference-in-differences model. After policy implementation (2018–2019), the coefficients are significantly positive and continue to rise, confirming the policy’s positive promotional effect on corporate green innovation.

Parallel Trend Test.

Note. t statistics in parentheses.

p < 0.1. **p < 0.05. ***p < 0.01.

Parallel trend test.

Moderating Effect Analysis

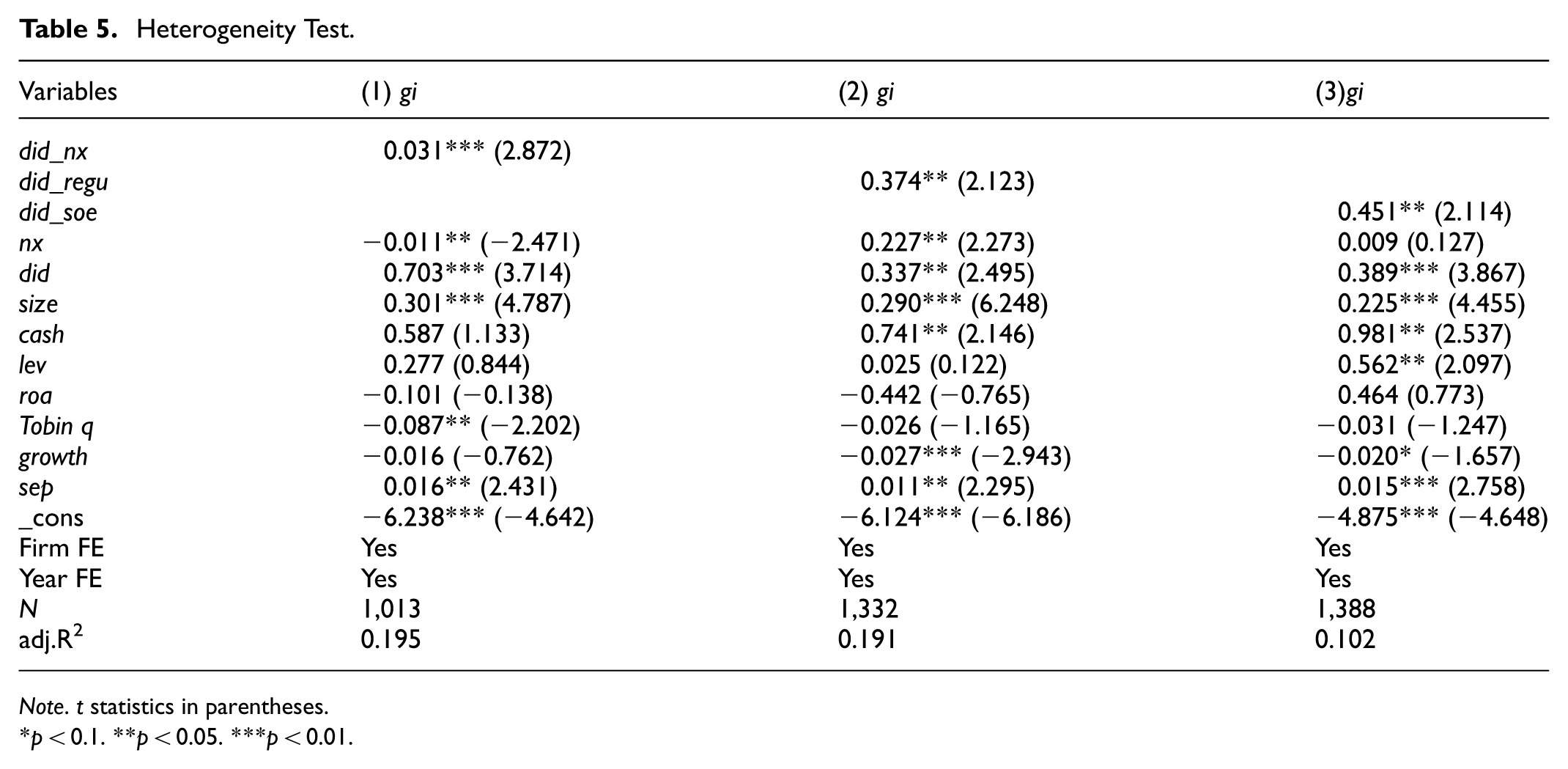

The current work attempts to examine the influence of executive compensation stickiness on the nexus between environmental protection taxation and enterprises’ green innovation. To this end, it introduces executive compensation stickiness as a moderating variable, with a view to elucidating its impact on the aforesaid relationship. The present study employs the model (3) to conduct a regression analysis. The results are presented in column (1) of Table 5, where the coefficient of the cross-multiplication term of did and nx is 0.031. The coefficient is statistically significant and positive at the 1% level, suggesting that executive compensation stickiness has a beneficial moderating effect on this association of environmental protection tax with corporate green innovation. Specifically, the influence of environmental protection tax on corporate green innovation is more pronounced in those, executive remuneration exhibits a high level of stickiness. The cause for this is the increase in executive compensation stickiness provides a certain level of protection for professional managers. Even if the enterprise’s performance declines due to the short-term failure to produce benefits from increasing the capital invested in corporate green innovation, there will be no unfavorable effect. In such cases, companies are more inclined to concentrate on achieving better long-run benefits, which are more evident due to the policy. The regression results confirm the hypothesis H2.

Heterogeneity Test.

Note. t statistics in parentheses.

p < 0.1. **p < 0.05. ***p < 0.01.

Environmental information disclosure has become an increasingly critical aspect of external regulation, attracting significant scholarly attention. Nowadays, the demand is not only for timely disclosure but also for high-quality, transparent reporting to address environmental issues in China effectively. In order to assess the effect from environmental policy upon the experimental outcomes, the paper employs the firm’s designation as a pivotal pollution monitoring unit, utilizing this designation as a dummy variable. As illustrated in tier (2) of Table 5, the regression findings demonstrate this coefficient of the interaction term for did with regu equals 0.374, indicating a notable positive correlation at this 5% degree. The result suggests this positive moderating effect from this environmental protection levy system upon green innovation gets more pronounced among companies classified as major pollution surveillance entities. Consistent with previous theoretical deductions, enterprises within major pollution surveillance entities face more stringent environmental policies, which compels them to give priority to R&D spending and strategic efforts toward green technology, thereby enhancing their green innovation capacity. Thus, Hypothesis 3 is supported.

This paper explores the effect of property rights on the correlation between environmental protection taxation and enterprises’ green innovation. To this end, it introduces the concept of property rights as a moderating variable. Model (5) regression analysis is employed to test the hypothesis, and the results are presented in column (3) of Table 5. This estimate of the interaction term for DID with SOE equals 0.451, which indicates a notable positive correlation at this 5% level, suggesting environmental tax proves more effective at fostering green innovation in SOEs than non-SOEs. As theorized, SOEs are better positioned to implement and enforce environmental protection policies. Additionally, their easy access to capital and innovation resources further stimulates green innovation in these enterprises. Thus, Hypothesis 4 is confirmed.

Robustness Test

Placebo Test

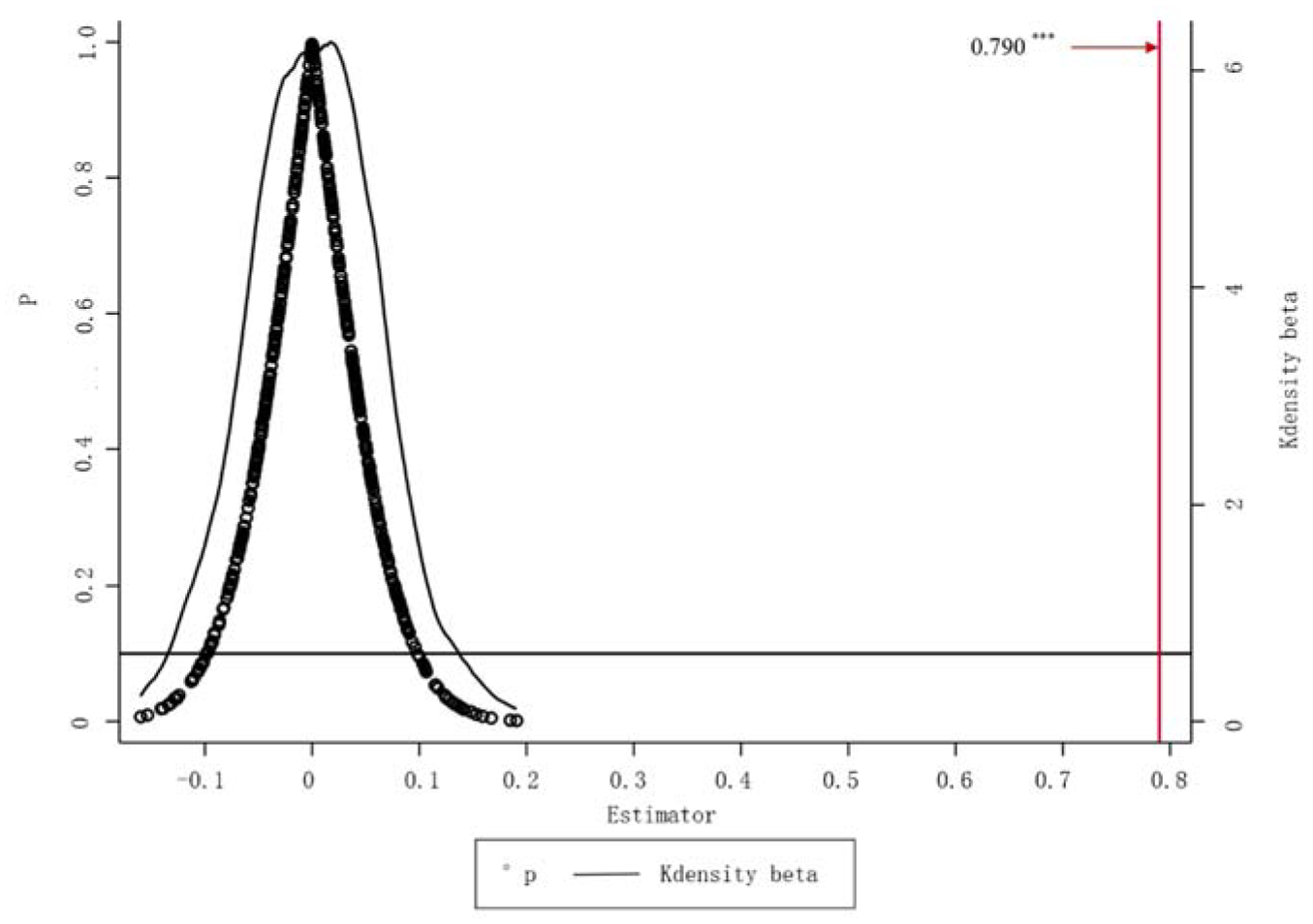

In this work, we follow Cai et al. (2016) methodology to randomly select firms and generate the policy implementation time associated with them. A randomized trial is conducted at both the policy implementation time and firm grouping levels to obtain the randomly assigned spurious interaction term. We regress this interaction term to derive its coefficients and repeat the process 500 times. These estimates and their kernel density plot of p-values get displayed (Figure 4) for assessing these findings’ reliability. The estimated coefficients of the spurious double-difference terms mainly cluster near zero, exhibiting characteristics of positively Gaussian distribution. Moreover, the t-values of the estimated coefficients in the baseline model differ significantly from those of the dummy variable, indicating no serious issue of omitted variables. It can therefore be concluded that the observed growth of enterprises’ green innovation results from implementing the environmental protection tax law. Furthermore, the central findings remain robust.

Placebo test result.

Endogeneity Test

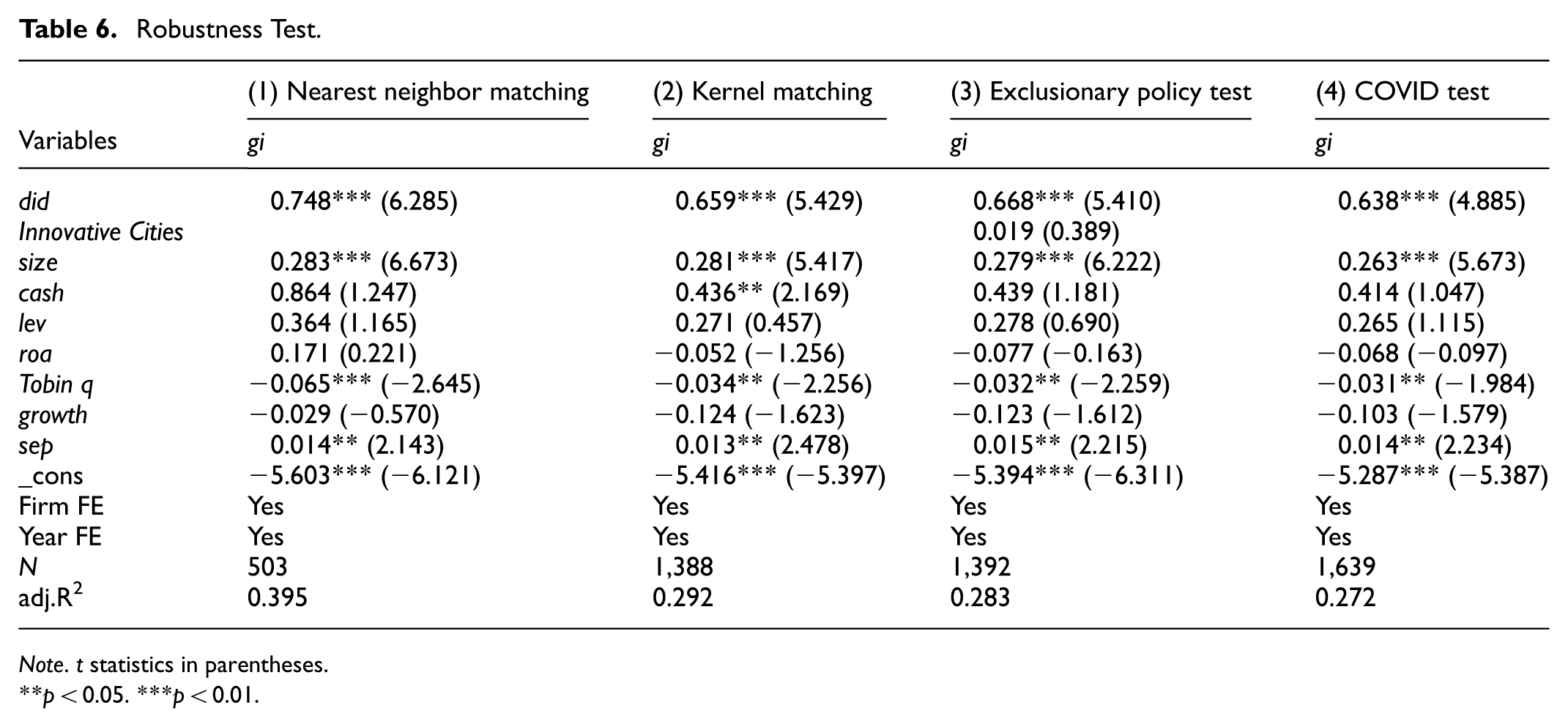

Given that provincial tax burden is influenced by multiple factors, the assignment of the group dummy treat remains non-random, which may raise endogeneity concerns. Following the methodology of C. S. Wang et al. (2026a), this research employs PSM-DID to mitigate endogeneity bias. Specifically, we use both nearest-neighbor matching plus kernel matching so as to obtain matched samples and carry out regression analysis of those samples satisfying the common support assumption. As shown in Table 6, the core DID estimate stays notably positive with 1% significance, reaffirming the stability of the baseline regression findings.

Robustness Test.

Note. t statistics in parentheses.

p < 0.05. ***p < 0.01.

Impact of Other Policies or Factors

Firstly, this research excludes the effect from innovative demonstration city initiatives. Innovative Pilot Cities necessitate that urban areas improve their scientific and technological innovation capabilities in line with executing the innovation-driven development strategy, which can exert notable influence on corporate green innovation. Eliminate the impact of this pilot policy on benchmark results, this work adds the dummy Innovation Cities (capturing this pilot policy) into the baseline model as a control. The regression results are presented in column (3) of Table 6. Secondly, potential impact from COVID-19 pandemic in 2020 is considered. To strengthen robustness of these research findings, we include 2020 to 2023 data for re-regression, with results displayed in Table 6, column (4). Notably, core explanatory variable estimates remain positive at a notable level after these adjustments, suggesting research conclusions are unaffected by these policies or factors, thereby demonstrating their robustness.

Conclusions

The introduction of the environmental protection tax in China has significantly improved environmental quality and ecosystem stability. In addition to strengthening the emission fee mechanism, the Environmental Protection Tax Law has also heightened public awareness of ecological protection. Beyond its economic significance, this progress plays a pivotal role in mitigating the negative externalities associated with environmental pollution. Accordingly, we treat the enactment of the Environmental Protection Tax Law as a quasi-natural experiment, using Chinese A-share listed firms in Shanghai and Shenzhen over the period 2011 to 2019 as our research sample. We employ a DID approach to empirically examine the effect of environmental protection tax policy on corporate green innovation.

The findings indicate that the implementation of environmental protection tax policies significantly enhances corporate green innovation. On the one hand, environmental protection taxes create incentives for firms to adopt green development strategies and allocate resources to green innovation through preferential policies and R&D subsidies. On the other hand, the tax system compels firms to pursue green innovation by heightening environmental legitimacy requirements, thereby facilitating their green transition and fostering long-term sustainability. Moreover, this environmental tax exerts a more pronounced effect on green innovation among firms with high executive compensation stickiness, those designated as key pollution monitoring units, and state-owned enterprises (SOEs). Our findings offer important insights for governments and firms regarding the use of market-based environmental policy instruments to promote both regional and corporate green development.

Recommendations

Policy Implications

Theoretical Implications

First, this study validates the theoretical pathway through which the environmental protection tax drives corporate green innovation through a three-pronged mechanism encompassing cost internalization, legitimacy pressure, and signaling, thereby providing micro-level evidence for the Porter Hypothesis in the context of China’s transition from a fee-based to a tax-based environmental governance regime. Unlike traditional command-and-control regulations, market-based tax instruments are more effective in internalizing external costs as endogenous decision variables within firms. Simultaneously, the allocation of tax revenues to local governments enhances their regulatory incentives, thereby subjecting firms to greater legitimacy pressures. Furthermore, as officially recognized indicators of technological innovation, green patents serve as credible signals to regulators, investors, and the public regarding a firm’s green transition, thereby creating a positive feedback loop. Second, this study reveals, for the first time, the positive moderating effect of executive compensation stickiness as a “failure tolerance” mechanism within internal governance structures. Highly sticky compensation contracts reduce managers’ perceived risk costs associated with green innovation, thereby amplifying the policy effects of the environmental protection tax. These findings extend the explanatory scope of agency theory within the context of environmental regulation. Third, we identify boundary conditions pertaining to the stringency of environmental regulation and property rights. Key pollution-monitored enterprises exhibit greater policy responsiveness owing to the cumulative effects of regulatory pressure. State-owned enterprises, owing to factors such as their institutional responsibilities and resource access, are significantly more incentivized to engage in green innovation than their non-state-owned counterparts. Our findings address core theoretical questions regarding the effectiveness of environmental protection taxes.

Practical Implications

To begin with, policymakers should strengthen the incentive mechanism of environmental taxation to alleviate financing constraints on corporate green innovation. It is recommended that environmental tax revenues be earmarked for financial support instruments, including interest subsidies on green loans and credit guarantees for green bonds, thereby establishing a dual-drive mechanism of “tax constraint plus capital channeling.” Furthermore, differentiated environmental regulatory strategies should be implemented. Strict enforcement should be maintained for enterprises subject to key pollution monitoring, while incentive-based instruments—such as tax rebates and subsidies—should be moderately expanded for non-key and non-state-owned enterprises, thereby avoiding a rigid “one-size-fits-all” approach that would compromise policy flexibility. Finally, policymakers should foster synergies between environmental and innovation policies. Specifically, environmental tax reform should be integrated with innovative city pilot programs and special green technology R&D projects to leverage cumulative policy effects. Although the robustness tests in this study have ruled out confounding effects from innovative city policies, the potential for policy complementarity remains.

Management Implications

Enterprises should convert environmental tax pressure into a strategic impetus for green transformation. State-owned enterprises should leverage their resource advantages to spearhead green technology R&D, whereas non-state-owned enterprises should capitalize on their market-driven flexibility to forge differentiated green innovation pathways within niche sectors. Furthermore, firms should optimize executive compensation contracts by integrating green innovation performance into long-term evaluation frameworks. Appropriately increase executive pay stickiness—for instance, by introducing clauses that tolerate innovation failures or offering stock option incentives tied to green patents—can mitigate managerial short-termism. Finally, enterprises should establish environmental risk early-warning and internal control mechanisms to ensure the efficient transmission from policy pressure to R&D decision-making and ultimately to innovation output. Key enterprises should proactively integrate environmental protection tax data with green R&D investment records to enhance both regulatory compliance and innovation efficiency.

International Implications

This study provides a replicable proposal derived from the Chinese context for other emerging economies undergoing industrial transformation or confronting environmental governance pressures. China’s institutional transition from pollutant discharge fees to the Environmental Protection Tax demonstrates that market-based environmental regulation is more effective than command-and-control approaches in stimulating endogenous corporate innovation. When undertaking environmental tax reforms, countries should prioritize the rule of law in taxation, the implementation of differentiated tax rates, and the allocation of revenues to local governments. Moreover, this study concludes that the effectiveness of the Environmental Protection Tax is contingent upon both internal and external factors-including executive compensation stickiness, environmental regulation intensity, and property rights structure. This implies that the mere introduction of a tax instrument is insufficient to guarantee policy effectiveness; it is therefore necessary to simultaneously improve corporate governance mechanisms, strengthen regulatory enforcement, and differentiate policy implementation according to enterprise type. Lastly, China’s experience suggests that green patents can serve as effective conduits for transmitting policy signals. It is recommended that other countries incorporate green innovation certification and information disclosure mechanisms into their environmental tax frameworks to mitigate information asymmetry between enterprises and regulators, thereby enhancing the efficiency of the policy in guiding the green transition.

Research Limitations

The sample period is limited to 2011 to 2019. Although this spans the 3 years preceding and following policy implementation, it is insufficient to fully capture the sustained impact of the environmental protection tax or the policy’s performance during the post-pandemic period beginning in 2020. Furthermore, the green innovation indicator is relatively narrow and fails to distinguish between substantive and strategic innovation. Additionally, the assessment of moderating variables remains somewhat simplified: Environmental regulation is operationalized as a binary variable indicating key-monitored-entity status, thereby failing to capture continuous changes in regulatory intensity; similarly, the ownership measure does not distinguish between central and local state-owned enterprises. Finally, despite employing PSM-DID and placebo tests, completely ruling out the influence of unobservable omitted variables, such as heterogeneity in local environmental enforcement intensity—remains challenging, posing a potential threat to causal identification.

Directions for Future Research

First, future research should extend the observation period and employ dynamic difference-in-differences analysis to evaluate the long-term impact of environmental protection taxes on corporate green innovation, incorporating data from 2020 to 2023 to assess policy resilience amid the COVID-19 pandemic. Subsequent studies could further track policy effects 5 and 10 years after the implementation of environmental protection taxation to determine whether these effects continue to strengthen, stabilize, or decline, thereby providing longitudinal evidence to inform policy optimization.

Second, future research should disaggregate green innovation into invention patents and utility model patents as distinct dependent variables to examine whether environmental protection taxes genuinely drive high-quality innovation or induce strategic behavior. If the tax primarily stimulates utility model patent filings, this would suggest that firms may engage in strategic innovation motivated primarily by symbolic compliance rather than substantive technological advancement. Conversely, a significant increase in invention patent filings would indicate that the policy effectively drives substantive technological breakthroughs. This distinction is essential for accurately assessing policy effectiveness.

Third, future research should incorporate additional moderating and mediating variables to deepen understanding of the “external policy–internal governance” transmission mechanism. Mediation analysis could be employed to examine specific transmission pathways, such as tax burden → cash flow constraints → R&D investment, or regulatory pressure → legitimacy requirements → strategic response.

Fourth, it would also be instructive to conduct cross-national comparative studies contrasting China’s environmental tax reform experience with that of EU countries that have implemented carbon taxes (e.g., Sweden and Finland), thereby distilling universal design principles for market-based environmental regulation. Countries differ in tax rate design, collection and administration mechanisms, and complementary policies; comparative research can identify key institutional variables that influence policy outcomes, offering guidance for optimizing environmental tax systems across diverse national contexts.

Fifth, research should extend the analysis to encompass the economic consequences of green innovation, tracking its outcomes in terms of financial performance and carbon emissions reduction to provide a more robust assessment of the Porter Hypothesis’s innovation compensation effect. Whereas existing research has predominantly examined the impact of environmental policies on innovation, future studies should further investigate whether green innovation driven by environmental taxation effectively reduces corporate emission intensity, improves resource utilization efficiency, and enhances financial performance, thereby establishing a complete chain of evidence linking environmental regulation to green innovation and subsequently to corporate performance.

Footnotes

Ethical Considerations

This study did not involve human participants, human tissue, or identifiable personal data. As such, ethical approval and informed consent were not applicable to this research design.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by National Social Science Foundation of China (No. 22BJY035) and Science and Technology Research Project of the Education Department of Jiangxi Province (No. GJJ2505101)

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.