Abstract

With a long history, studies have investigated how remittances affect development. In doing so, a few studies have looked at the impact of remittances on the recipient countries’ financial development. This comparative study aims to address the lack of a specific study that would identify the impact of remittances from highly- and low-skilled groups on financial development. The instrument variable approach (IV) was used in this investigation. Findings were mostly produced using secondary data from the World Development Indicators, while primary data was also used to support the talks. According to research, remittances typically improve recipient nations’ financial development. We also point out, nevertheless, that remittances from migrants with comparatively low levels of education have significantly boosted financial inclusion in the host nations. Both inshore and offshore laws and regulations for overseas employment and investment possibilities would be loosened—an implication—to guarantee a larger and longer-term impact of remittances from both groups on financial growth.

Introduction

Remittances, or the money migrants bring home, have a major positive impact on the economies of the nations from where either they have migrated or have settled. The entire amount of remittances increased from roughly $2 billion in 1970 to $131 billion in 2000. Furthermore, many economies are still struggling to recover from the Global Financial Crisis (GFC) of 2008–2009. Despite this and the COVID-19 financial crisis, the remittance flow curve remains higher. In 2023, for example, remittances reached $669 billion, up from $430 billion in 2010 (World Bank, 2023). Both highly- and low-skilled migrants might have contributed to this flow of remittances. Yet a study is to be conducted to understand by comparing the contribution made by these two groups while producing highly skilled migrants costs more education funds of home countries.

Traditional saying that ‘education is the backbone of a nation’ doesn’t appear to apply in the age of globalisation (Alam et al., 2020; Veugelers, 2020). The function of education has expanded significantly since its inception (Alam et al., 2020; Tight, 2021; Veugelers, 2020). Therefore, by creating a dependency theory, education should ideally play a bigger part in international growth, which could come at the expense of national development (Forhad & Alam, 2021; Horner, 2019). In a similar vein, higher levels of education would contribute to more remittances in receiving nations. By comparing the incomes of highly- and low-skilled migrants, this study investigates whether remittances have an impact on the financial development of the recipient nations.

Unquestionably, education increases a person’s productivity and skill level, which accelerates both an individual’s and a country’s income (Alam et al., 2020; Veugelers, 2020). This is a crucial developmental strategy. It is unknown if the remittance flow from receiving nations is impacted by the migrants’ higher income (Alam & Forhad, 2023). Since the county of origin has invested more in the education of these migrants, the increased revenue should ideally aid in its development (Alam & Forhad, 2023).

These family members are more inclined than their counterparts to settle in countries that welcome immigration, even while their relatives back home demand remittances for charitable reasons. As a result, immigrants who work in nations that welcome immigration plan to start the procedure and send money. Different reactions result from the fact that a higher proportion of highly educated individuals reside in immigration-friendly nations than in other nations. This study looks at the various ways that highly skilled immigrants’ remittances impact recipient nations’ financial development.

Since naturalisation-friendly migration policies have separated educated migrants from their country of origin, they have integrated into the economic and social life of the host nation (Veugelers, 2020). This could limit the highly skilled migrants’ ability to make a substantial contribution to the remittance flow, which would reduce the return to education in the destination countries—the idea that motivates this study.

Remittances have recently emerged as a more reliable source of foreign income than portfolio equity flows, private loans and international developmental aid (Carling, 2008; World Economic Forum, 2018). Even if the COVID-19 pandemic has generated an imbalance in the flow of remittances, developing nations still receive over 70% of all remittances worldwide (Alam & Forhad, 2023).

The impact of remittances on recipient countries’ development was the subject of numerous studies. Remittances, for instance, improve socioeconomic conditions (Acosta et al., 2006; Masron & Subramaniam, 2018; Mundaca, 2009; Vacaflores, 2018), lower poverty (Acosta et al., 2006; Adams & Cuecuecha, 2010; Anyanwu & Erhijakpor, 2010; Azizi, 2021; Samaratunge et al., 2020), enhance exchange rate and export earnings scenarios (Acosta et al., 2006; Adams & Cuecuecha, 2010; Kim, 2019; Lopez et al., 2007; Morad & Sacchetto, 2021; Patler, 2018) and raise educational attainment (Askarov & Doucouliagos, 2020).

Additionally, remittances alleviate financial constraints for small- and medium-sized business owners (Kakhkharov, 2019; Vaaler, 2011; Yavuz & Bahadir, 2022) and improve health conditions (Amuedo-Dorantes & Pozo, 2010; Antón, 2010; Djeunankan & Tekam, 2022; Jaschke & Kosyakova, 2021; Kanaiaupuni & Donato, 1999; Mansour et al., 2011; Shor & Roelfs, 2021). Only a small number of studies, meanwhile, investigated how remittances affected the financial development of the nations that received them. Economic growth would be accelerated by financial development and increased remittance inflows because remitters may be encouraged to contribute more to their family through an effective remittance transaction.

In a recipient nation, remittance inflows may also lead to the growth of additional financial institutions (Aggarwal et al., 2011; Fromentin & Leon, 2019; Gupta et al., 2009; Mundaca, 2009; Sobiech, 2019). Conversely, others contended that poor remittance management can potentially have a negative impact on financial development (Demirgüç-Kunt et al., 2011). For instance, a financial services industry that is uncontrolled or improperly regulated may result in higher service fees for remitters, discouraging them from using official channels (Aggarwal et al., 2011). There might be a reverse causation in such a scenario. We employ the Instrument Variable (IV) technique to deal with the reverse causality. The weighted Gross National Income (GNI) of the remittance-sending nations serves as the IV.

Although there are some differences between our study and others, its main goal is to distinguish the unique impact that remittances from two types of migrants—those with higher and lower levels of education—have on the economic growth of the host nations. To investigate two research questions, namely (1) whether remittances contribute to the financial development of recipient countries and (2) whether remittances from highly- and low-skilled migrants significantly impact such development, the total amount of international remittances received is not considered. Instead, they are divided into two sources, namely from low- and highly-skilled emigrants.

Since education has a positive correlation with abilities, this study used educated migrants interchangeably with skilled migrants. We primarily divide skill sets into two categories: low and high. High school graduates and those with less education are viewed as low-skilled or low-educated, whereas those with more education are viewed as highly skilled or highly educated.

Since sending nations must spend more money to produce highly educated migrants, the main goal of this comparative study is to find out if the money sent home by highly skilled migrants has a greater impact than that sent home by their less educated counterparts. Furthermore, highly skilled people are presumed to be more knowledgeable about financial systems, their responsibilities (individualist and nationalistic) and investment opportunities than those without a good education because a higher level of education should ideally guide its recipients to react wisely. For instance, it is a propositional assumption that migrants with higher levels of education and wealth should generally save more money and make investments in their new nations, thus promoting financial development.

Following this rationale, the data and technique are described in parts two and three, respectively, before the empirical results are reported in section four. The conclusion and limitations are noted in the last section.

Data Sources and Analysis

Because people from the less developed Asian nations, both highly and less educated, try to travel to other places in search of a better future. For instance, a sizable percentage of migrants with high and low levels of education move to Saudi Arabia and the United States, respectively. Given the greater degree of variation in migration and remittances, we gathered the World Development Indicators (WDI) year-by-year macro data for the 1990–2015 period, concentrating on the following Asian nations: Afghanistan, Bangladesh, China, India, Indonesia, Pakistan, Philippines, Sri Lanka, Thailand and Vietnam.

The host nation’s classification is taken into account when assessing the migrants’ educational attainment. Therefore, we selected the GCC (Gulf Cooperation Council) and G7 (Group of Seven) nations to transfer remittances. Table A1 reports the selected countries. Due to their international employment and immigration laws, the GCC countries mostly seek foreign workers with relatively low levels of education. Therefore, we regarded remittances from GCC nations as coming from migrants with low levels of education (Alam & Forhad, 2023). The G7 nations, on the other hand, typically want a workforce that is reasonably highly educated. As a result, we regarded them as highly educated locations for sending remittances (Forhad et al., 2024).

This study makes the simple assumption that educational attainment and skill sets are interchangeable. The dependent variables were market capitalisation, liquid liabilities and private credits, in accordance with Aggarwal et al. (2011), Azizi (2018) and King and Levine (1993). In accordance with the WDI definitions, we also considered private domestic credits as the funding source assisting the growth of the private sector. These credits may take the form of trade credits, loans, various claims for loan repayments or acquisitions of nonequity securities.

Broad money is represented by liquid liabilities, whereas market capitalisation—which is calculated as the ratio of total stock market capitalisation to GDP—indicates the relative size of the stock market. Domestic private credit to GDP and liquidity has a significant impact on the depth of the financial system (Fromentin, 2018; Donou-Adonsou & Sylwester, 2017). We also took the rate of financial system inclusion into account. In this instance, we considered the number of depositors per 1,000 adults who opened a commercial bank account.

Since the chosen nations are developing economies, the financial system’s inclusion rates would provide insight into how remittances impact the possibility of financial inclusion via banking channels. Savings are another measure of financial development used in this study. Here, we take into account the ratio of gross savings to GDP. Gross savings are defined by the WDI as GNI less net transfers and total consumption. In a similar vein, gross domestic savings is calculated by subtracting final consumption expenditure from GDP.

In order to approximate the missing numbers, we used linear interpolation. According to the WDI definition, remittances are calculated as the sum of the personal and employee wage/salary transfers. Trade openness, GDP per capita and inflation rate are the additional control variables. According to WDI, trade openness is calculated as the percentage difference between GDP and the total values of imports and exports. The annual percentage change in the Consumer Price Index (CPI) is known as the inflation rate. Other variables are used in percentage forms, and we use the logarithmic values of the per capita income.

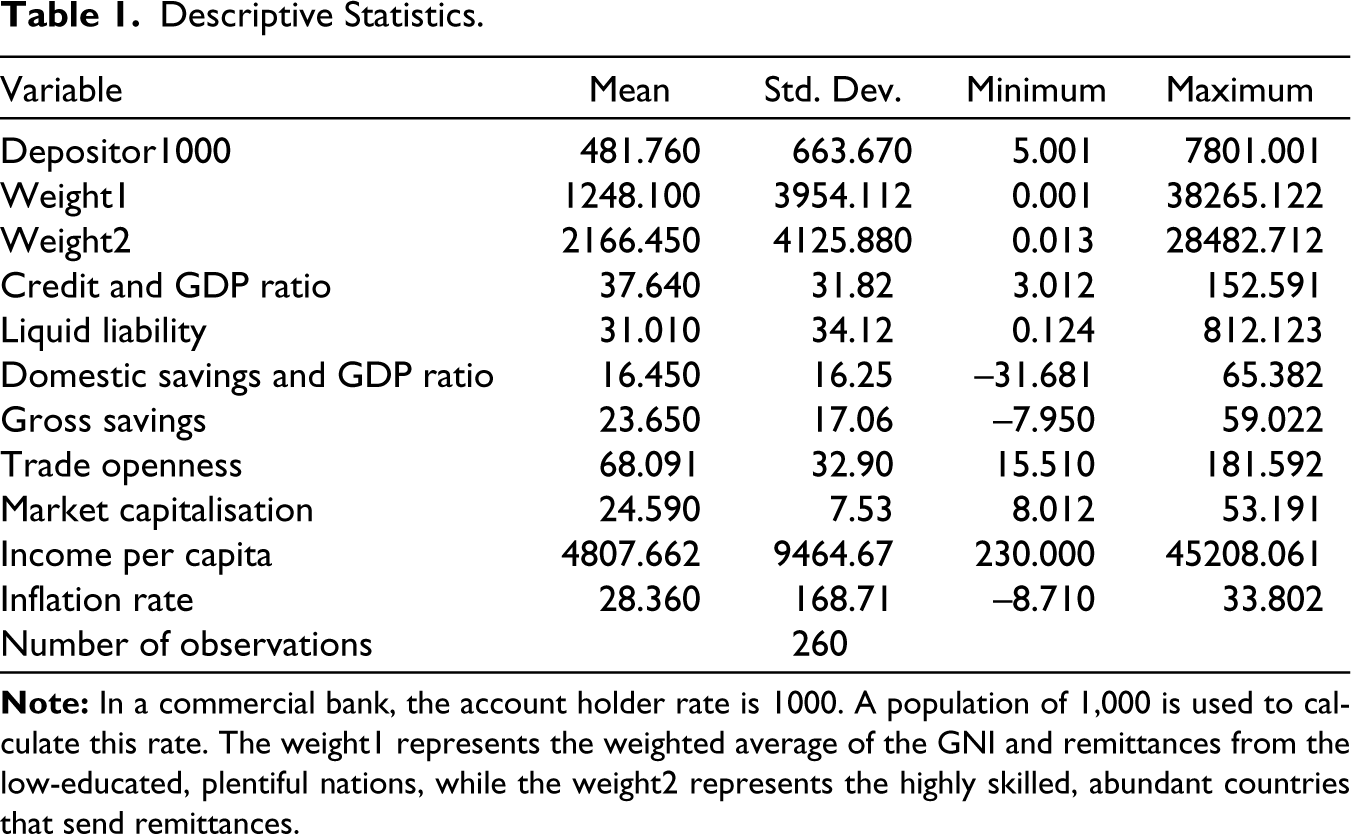

Table 1 presents the descriptive statistics. With a standard deviation of 31.82 and an average domestic credit rate of 37.64%, there is a noticeable difference. There is notable variation among nations, as evidenced by the average saving value of 23.65 with a standard deviation of 17.06. The stock market capitalisation average is 24.60%. Additionally, Table 1 reveals that 481 out of every 1,000 people own a commercial bank account.

Descriptive Statistics.

The remaining percentage was remitted from the destinations of the low-educated counterparts (those in the GCC and beyond), while 40.15% came from the highly educated migrants’ destinations. This disparity in the percentage distribution of remittances suggests that developing recipient countries receive a larger share of remittances from migrants with lower levels of education. Likewise, Table 1 indicates that the average weighted remittance from migrants with higher levels of education is higher. However, the average percentage of remittances from both sending destinations has a wider standard deviation, suggesting that the receiver nations are diverse.

Empirical Model

We mainly employ the following empirical model:

where FD it represents country i’s financial development indicator at time t; Rit– 1 rerepresents the remittance inflows in t period, Rit– 1 is the remittance in period t – 1; X'it – 1 are control variables that could also influence financial developments in remittance recipient countries. We also control for fixed effects, including the time-fixed effect (γt) and country-specific fixed effect (δi).

These fixed effects capture the period and country-specific impacts because different countries may have different fixed effects. α1 is the coefficient of interest. It is anticipated that the estimate will be positive and statistically significant. Remittances greatly enhanced the financial sectors of recipient nations, which is the economic interpretation of this statistically significant beneficial effect. We begin estimating Equation 1 using the pooled ordinary least squares (POLS). The primary obstacle in this situation is endogeneity.

The cause of this problem is the inverse causal relationship between remittances and financial progress. People are discouraged from sending money through formal financial channels since, for instance, sending remittances costs transfer fees. Second, informal avenues may be preferred by migrants. Family members and acquaintances who migrate from developing nations, for instance, are more inclined to send money in this manner. Thus, there may be an endogeneity issue if the official remittance measure is inaccurate or deceptive. The estimated impacts would be skewed as a result.

Most research uses the IV technique to deal with the endogeneity issue. According to certain research, for instance, factors pertaining to nations that receive remittances should be used. In addressing the aforementioned difficulties, this work primarily adheres to Azizi (2018). To meet the relevance requirement, we select an IV associated with remittance. Additionally, the IV must meet the requirements for exclusion.

Remittances may be associated with both sending and receiving countries, since they are thought to be the sum that migrants transfer back to their home countries. One country’s remittance flow would also differ from another’s, and their effects would also change. Therefore, to assess the effects of the remittance-recipient nations, we take into consideration two remittance-sending categories: high and low-educated countries. For the remittances, we employ a weighted average remittance, as per Azizi (2018). Therefore, the weight of country i in year t from remittance-sending country j can be written as follows:

If the weight is 0.09 in 2010 for two receiving and sending countries, the receiving country has 9% of its total remittances from the specified sending country. Multiplying the weight with the per capita GNI of the recipient countries, the weighted average of per capita GNI (yit) can be formed as follows:

where GNI jt is the j-sending country’s per capita GNI. This weighted average of the per capita GNI will be used as an instrumental variable for remittance. As the migration of host countries’ GNI is not directly related to the remittance of the recipient countries, this satisfies the exclusion condition.

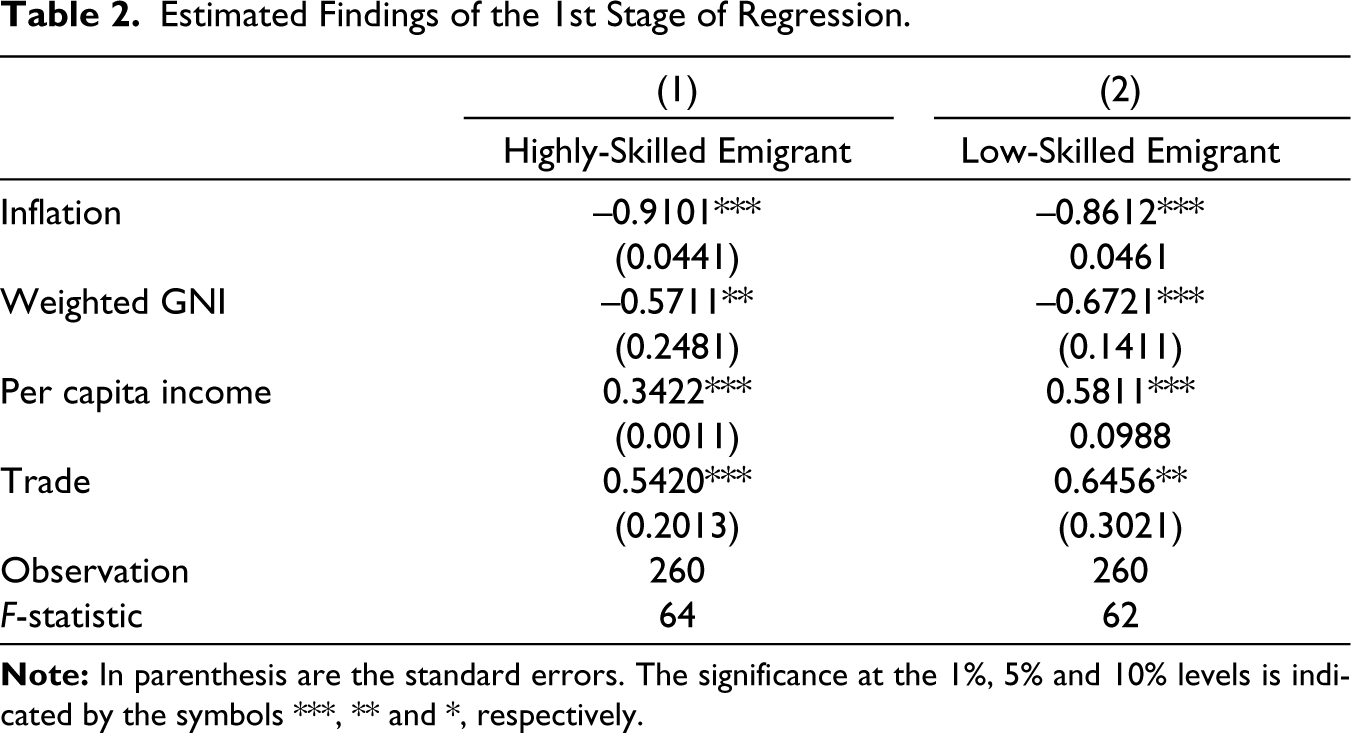

To assess how good the IV is, we performed the first stage regression and presented the estimations in Table 2. While Column 2 displays identical information for the G7 countries, Column 1 reports the estimated effects of the remittances of the low-educated migrants. Table 2 demonstrates that the F-test statistics are greater than 10, indicating that the remittance instruments are not weak. The weighted average GNI is therefore a powerful tool for remittance.

Estimated Findings of the 1st Stage of Regression.

Result Analysis

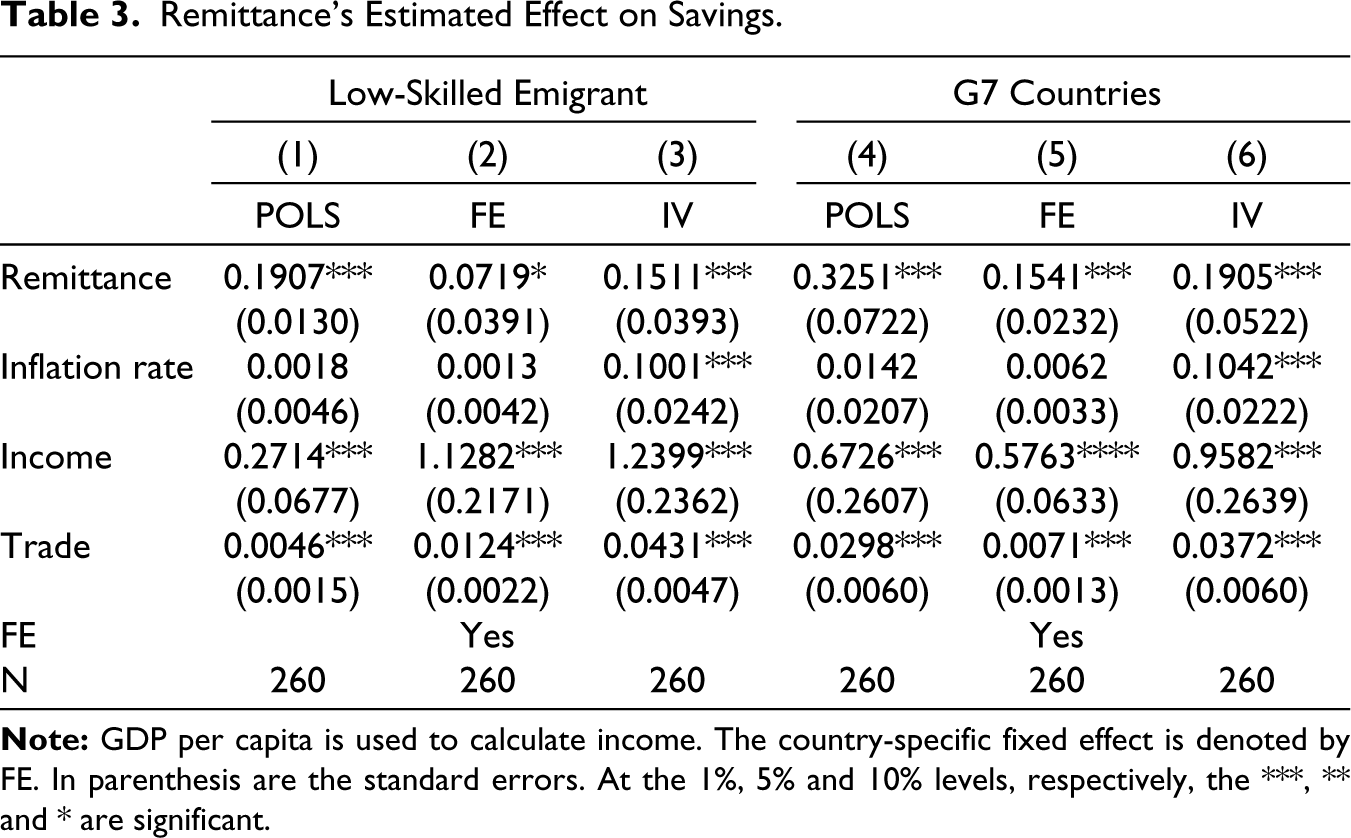

The projected impact of remittances on savings is displayed in Table 3. Using the POLS model, Column 1 displays the implications for the GCC nations. The estimated impact on the savings in this instance is 0.1907, indicating a positive and statistically significant outcome. Column 2 displays the estimated effects of low-educated migrants using the fixed effects model, whereas Column 3 displays the estimates from the IV model. Both the IV and fixed effects models’ projected impacts are statistically significant and positive.

Remittance’s Estimated Effect on Savings.

According to the research, remittances from migrants with low levels of education have a favourable effect on recipient nations’ savings. For instance, the IV’s estimated effect is 0.1511, meaning that a 10% rise in remittances from migrants with low levels of education results in a 15.11% increase in savings. However, the predicted effects of highly educated migrants’ remittances on recipient countries’ savings are displayed in Columns 4, 5 and 6. The estimated effect, for instance, is 0.1905, which is favourably and statistically significant, as shown in Column 6. This suggests that recipient countries save 19.05% more when a 10% remittance is increased.

When compared to migrants with lower levels of education, Table 3 demonstrates that remittances have a greater impact on savings. Additionally, the inflation rate’s predicted effects are statistically significant and favourable. There are also positive and noteworthy consequences from the recipient countries’ anticipated income and trade openness. These results suggest that trade openness and per capita income also boost savings in recipient nations.

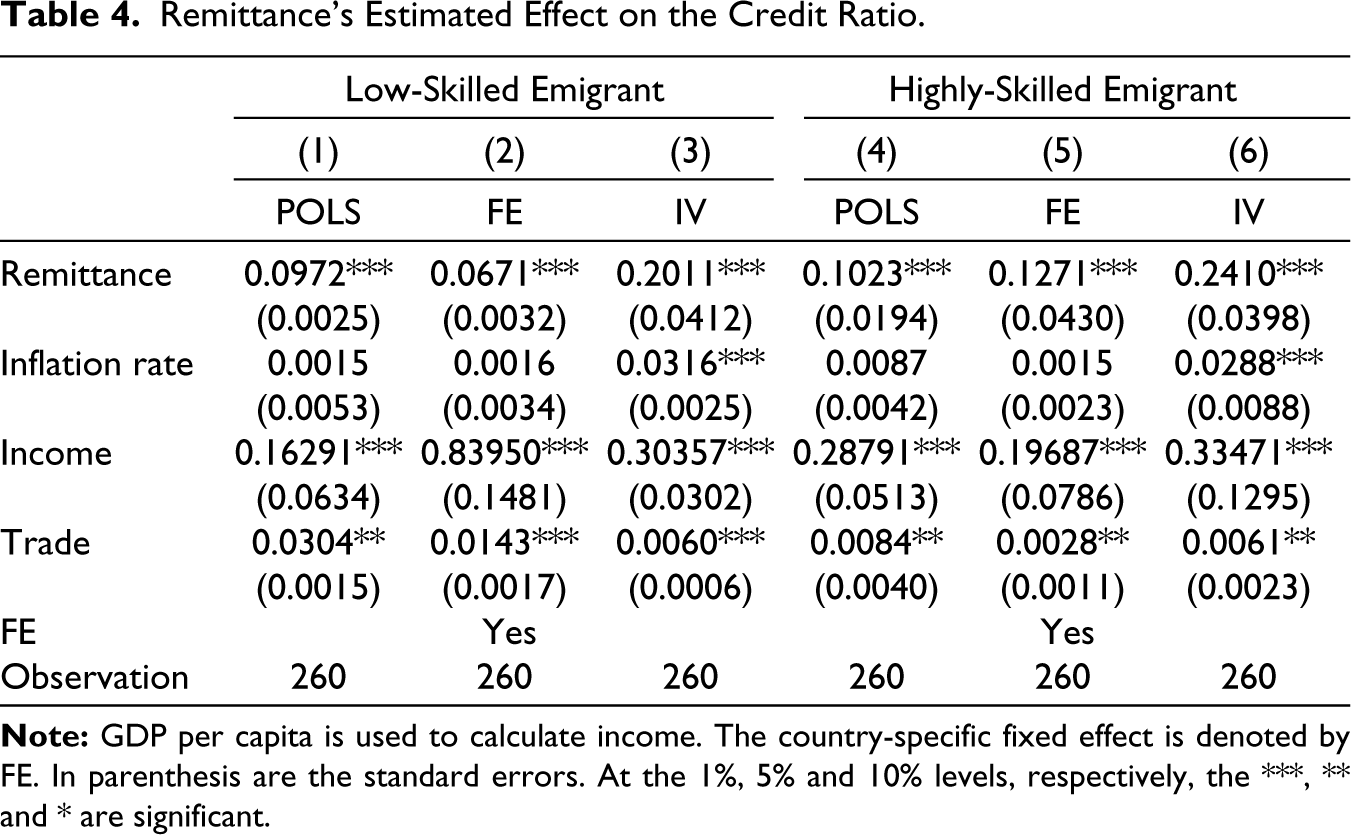

The impact of remittances on the credit ratio in recipient nations is displayed in Table 4. The estimated effects are statistically significant and positive in both cases. As an illustration, Column 3 displays the estimated effect of 0.2011, meaning that a 10% increase in remittances from migrants with low levels of education results in a 20.11% rise in credits. However, for highly educated migrants, it is 24.10%. Like Table 3, the estimated benefits of trade openness and national income are statistically significant and positive, suggesting that they promote financial progress.

Remittance’s Estimated Effect on the Credit Ratio.

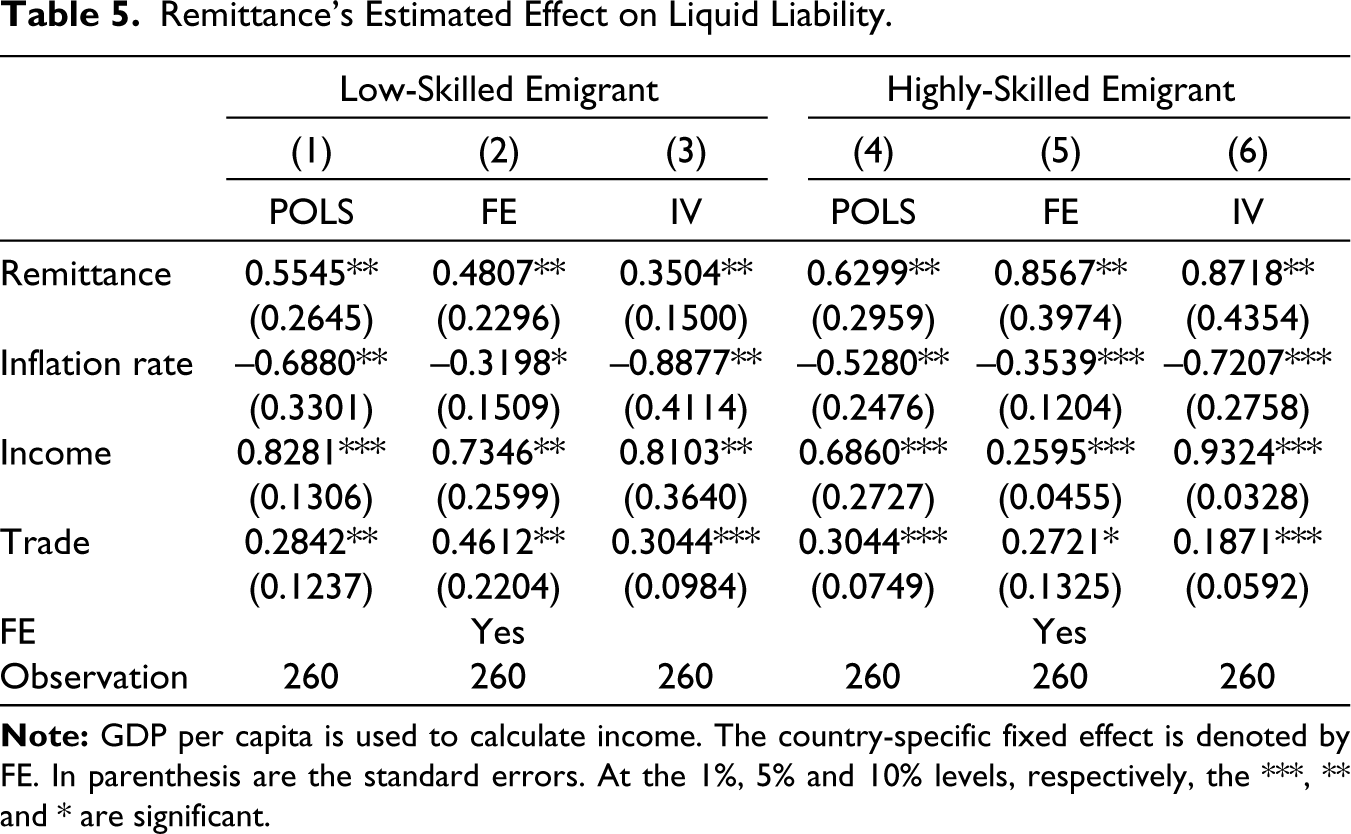

The estimated impacts on the liquid liability are displayed in Table 5. Remittances improve liquid liabilities, as seen by these statistically significant and largely favourable benefits. Remittances from highly educated migrants have a greater influence on liquid liabilities as compared to the projected effects of remittances from low-educated migrants (Tables 3 and 4).

Remittance’s Estimated Effect on Liquid Liability.

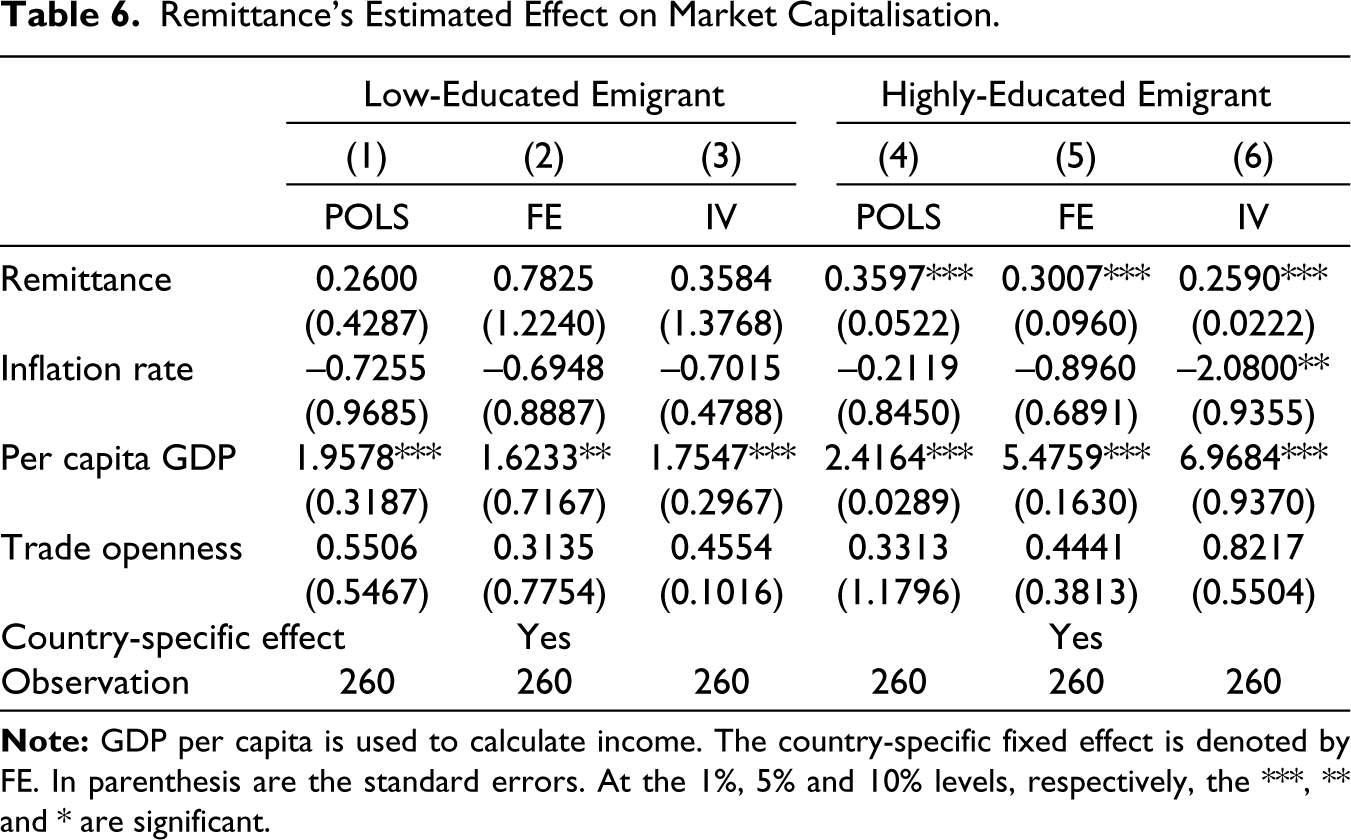

The impact of remittances on the capital market is displayed in Table 6. Columns 1 through 3 display the projected impact of the remittances from the migrants with lower levels of education. The fact that each estimate is statistically insignificant suggests that the stock market in the destination nations is unaffected by the remittances of migrants with low levels of education. However, these impacts are positive and statistically significant for the remittances from G7 nations in Columns 4 to 6. The stock market in receiving nations is greatly enhanced by the remittances sent home by highly educated and professional migrants. Table 7 shows the projected impact of the remittance on gross domestic savings.

Remittance’s Estimated Effect on Market Capitalisation.

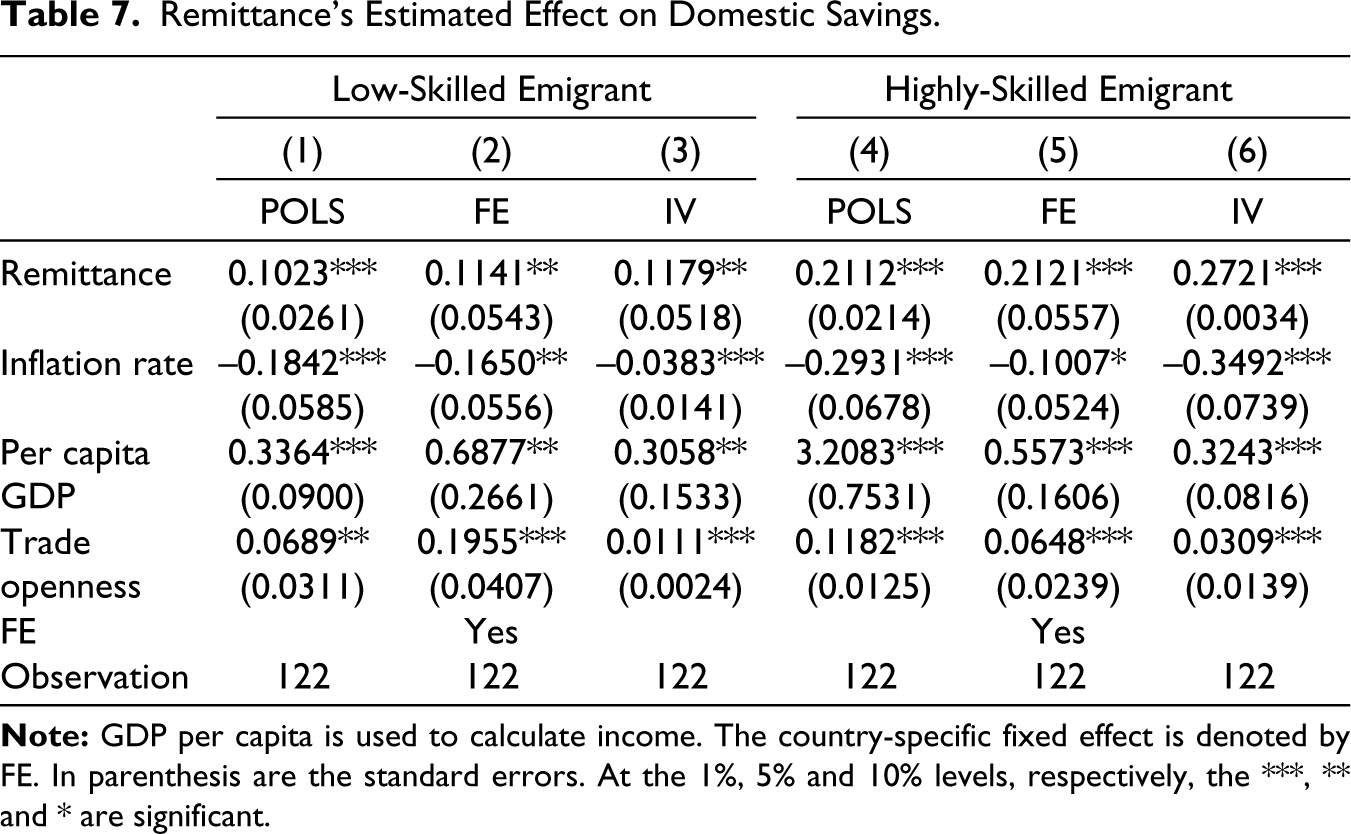

The ratio of gross domestic savings to GNI is one of the dependent variables. Remittances from migrants with low levels of education are predicted to have beneficial and statistically significant benefits. The IV model’s estimate, for instance, is 0.1279. This suggests that a 10% increase in remittances from migrants with low levels of education results in a roughly 10% rise in savings. The same estimated effects of highly educated migrants are also displayed in Table 7. Remittances from migrants with higher levels of education are larger than those from those with lower levels of education. According to these data, remittance recipients from migrants with higher levels of education exhibit much greater propensities for saving than their counterparts with lower levels of education.

Remittance’s Estimated Effect on Domestic Savings.

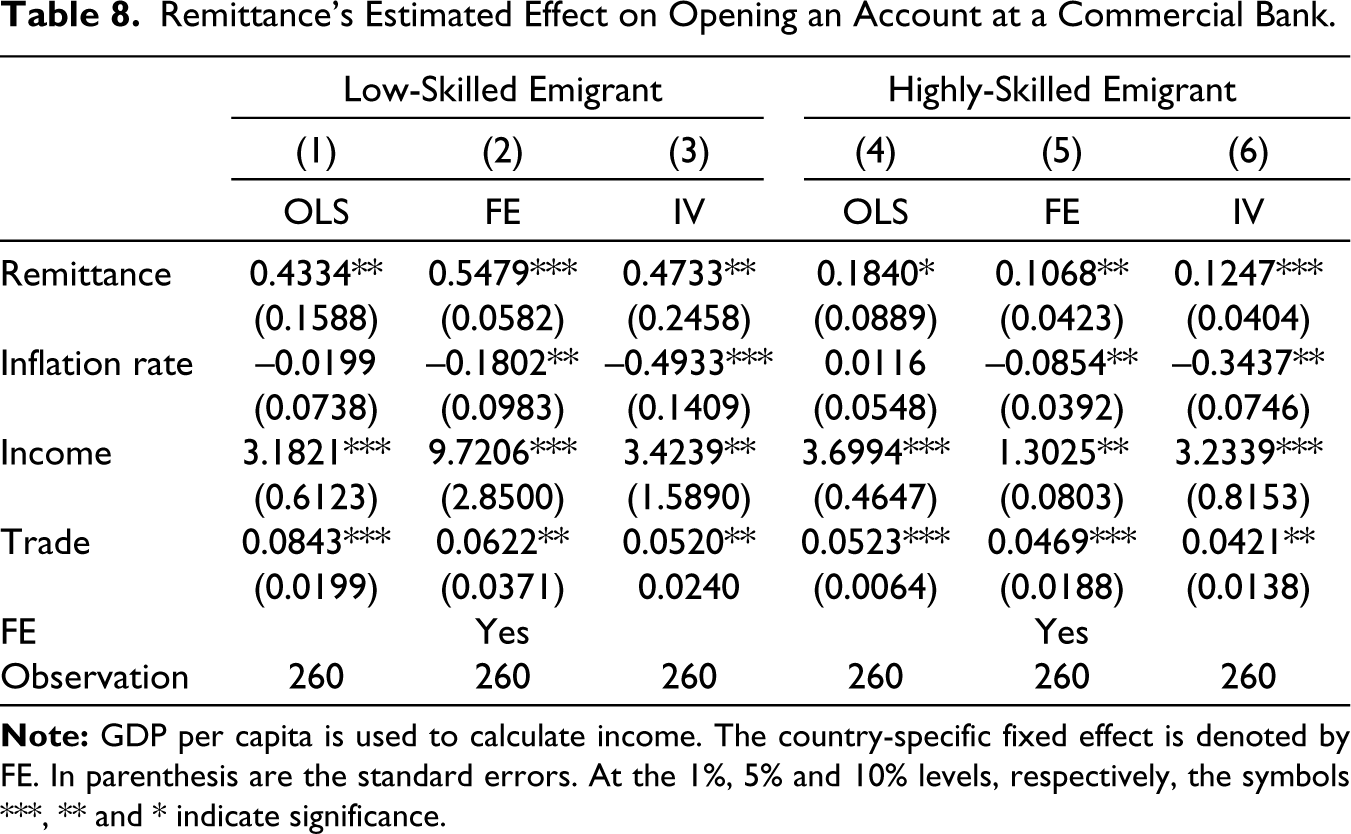

The projected impact of remittances on account opening rates in recipient nations’ commercial banks is displayed in Table 8. These impacts are statistically significant and beneficial in both situations. For instance, Column 3 indicates that the projected effect for the migrants with low levels of education is 0.4733. According to this beneficial and statistically significant effect, the commercial bank opening rate rises by 47.33% for every 10% increase in remittances from migrants with low levels of education. However, the same favourable and statistically significant effects are displayed in Column 6. The estimated effects of highly educated migrants’ remittances are likewise higher than those of low-educated migrants.

Remittance’s Estimated Effect on Opening an Account at a Commercial Bank.

The fact that the majority of migrants who migrate to low-educational migration destinations have comparatively lower levels of education than their highly educated counterparts may be one explanation for the favourable effects on the commercial bank account opening rate. Additionally, these migrants with low levels of education are less likely to own a commercial bank account. For their families, the same situation was evident. To withdraw their remittances to their family, migrants require a bank account. Therefore, it is very likely to have a greater effect on the remittances from migrants with lower levels of education.

Remittances have a favourable and considerable impact on the financial indicators, according to this study’s empirical findings based on the macro data. The estimated effects of remittances between migrants with low or semi-education and those with high education are also compared in this study. The results also show that the opening and savings rates of commercial banks in the destination countries are greatly impacted by remittances from migrants with low levels of education.

These results suggest that remittances from immigrants with lower levels of education have a greater influence on financial inclusion. However, the capitalisation and credits of the stock market are greatly impacted by the remittances from highly educated immigrants. The effects of remittances from two sources—highly and lowly educated migrants—are being compared for the first time. The results contend that the effects on the financial development of recipient nations vary. We provide additional insights into these findings using Bangladesh as a case since this study provides some preliminary ideas on the various implications of remittance.

We also tried to figure out why the skill level of migrants affects how remittances affect financial development. The lack of microdata from the sampled countries led us to explore commercial bank branches in Bangladesh’s rural and urban areas. We gathered data on recipient remittances by conducting a primary survey of account holders. Additionally, the bank transaction record is a supplement. Merely 10% came from migrants with higher levels of education, with the rest portion coming from those with lower levels of education. Furthermore, only 3.5% of the newly opened accounts received monthly remittances from highly educated migrants, compared to nearly 10% from low-skilled immigrants.

Additionally, according to bank management, low-educated migrants account for a larger percentage of deposits than all monthly remittances received. Most of the migrant workers with low levels of education who receive remittances stated that they would rather deposit their funds in banks. Most of the remittance recipients from highly educated migrants, on the other hand, stated that they would rather invest more money in order to create revenue flows. It goes without saying that none of the people who have accounts with rural banks trade stocks.

Compared to their peers, many account holders who receive remittances from low-educated migrants withdraw a smaller share of their money in cash. This indicates that those who receive remittances from migrants with lower levels of education are more likely than their peers to save more. However, only 2% of low-educated migrants who get remittances and live in cities engage in stock market activities, compared to 10% of their highly educated counterparts.

The living expenses and standards for emigrants in industrialised countries are comparatively greater than those of the low-educated emigrants residing in Gulf countries. As a result, migrants with lower levels of education employed in Gulf nations would receive a greater portion of their salary to bring home. In contrast to Gulf countries, the G7 countries provide a welcoming immigration policy for highly educated individuals, facilitating their permanent residency. The majority of highly educated permanent settlers in the G7 countries extend invitations to their family members to become permanent members of their family via the scope of family immigration policy.

Migrants are likely to spend their earnings on the immigration procedure rather than sending remittances because applying for immigration in these industrialised nations demands a significant financial expenditure. Furthermore, the issue of sending remittances becomes irrelevant once the entire family moves to the host nation. Brain drain is the term used to describe the primary migration of highly educated and educated people, particularly from developing nations, like India, Pakistan and the Philippines, to more developed ones (Johnson, 1965; Nguyen, 2014). On the other hand, body drain refers to the phenomenon of people from poor countries temporarily moving to growing economies, particularly those in the GCC, with virtually no education or skills (Alam & Hoque, 2010).

Whereas their ‘body drain’ colleagues are temporary labourers, the brain drain group is supported by a friendly immigration policy in their destination nations, where they can settle with their families. Since the host nation is seen as their ancestral home and the home of their future generations, the brain drain group ideally seeks to support it. In contrast, once their labour contracts expire, the body drain group is required to return to their native nation. Furthermore, in many developing nations, people from lower socioeconomic backgrounds tend to be in the body drain category. They rely heavily on remittances from overseas for their families.

Policy Implication

The results of this study indicate that remittances help recipient nations’ financial sectors grow. Consequently, one policy implication is that governments ought to relax both domestic and international restrictions on a migrant movement. They should also start a banking system that is easy to use and adaptable for the international remittance movement. Furthermore, research indicates that remittances from highly educated migrants have little effect on the financial development of the majority of receiving nations as compared to those from low-educated migrants. To put it another way, remittances from the less educated segment have a greater influence on the financial prosperity of the countries that receive them. The migrants think that residing in industrialised host nations is a safer option than living in the Gulf countries.

However, after their employment contracts end, the majority of migrants to the Gulf countries go back to their own countries. The character of the immigration laws in the host nations may be one factor contributing to these disparate reactions. As a result, both inshore and offshore viewpoints must be applied inclusively to policy dynamics. First, a method that allows brain-drained groups to contribute to their home countries rather than just their host countries can be established. For instance, when migrants work in their new countries, they are required to pay all taxes on their profits. As a result, we advise an international tax policy on the incomes of migrants that would send a portion of the income tax to their home nations.

That is, both the home and host countries ought to benefit from the income tax paid by migrants. For instance, the home nations may receive half of the total income tax, while the host countries would receive the remaining half. The initial financial investment made by home countries in the brain drain group’s human capital development process may be the cause of income tax claims from the host country to the home country. Consequently, home nations ought to receive a portion of the investment’s return.

Second, an international social security program might be suggested by the United Nations (UN). After their employment ends, low-skilled and uneducated migrants feel unprotected and frightened when they return home. Ideally, this plan would provide them with relief and optimism for the future.

Third, human rights, particularly for bodily drain groups, can be guaranteed by ratification under the auspices of the UN. They might also offer programs for these migrants who have returned home to receive retirement benefits.

Fourth, these home-returnee migrants should be employed in their respective fields by their home nations as part of the UN effort. Lastly, the government might provide soft loans, other packages that are favourable to investments, and the necessary training to encourage home-returnees to start their own businesses in their fields of expertise.

Conclusion

This study investigates the impact of remittances from highly- and low-skilled groups on financial development in recipient countries. Using secondary data from the WDI and employing the IV model, the study found that remittances typically improve recipient countries’ financial development. However, remittances from low-skilled migrants significantly boost financial inclusion in host nations. Findings also argue that remittances from high-skilled migrants significantly improve the capital markets in recipient countries. The study suggests more flexible migration policies and regulations for worldwide employment and investment possibilities.

Findings also recommend bilateral and international agreements on migration, remittance, and taxes, which are necessary to ensure that drained brains contribute to their home country. Additionally, findings suggest that policy initiatives should be taken to promote a humane lifestyle for body-drain counterparts after their return to their home country. Financial organisations can also offer investment plans to immigrants, and government rules can promote remittances through official financial transactions.

Potential limitation and scopes for further research

Using macro data, we first assume that the GCC and G7 countries are the main destinations for remittances from migrants with low and high levels of education, respectively. Future research should employ microdata to examine if the variation in migrant skills and education is the reason for the disparate effects of remittances on financial development. Second, the incentive of migrants to send remittances is assumed to be uniform in this study. The results will be influenced by the diverse incentives of the migrants, which is ideal. In a similar vein, recipients of remittances may have differing opinions about how to use the funds or their consumption habits, which may influence how they behave while making financial investments.

Third, the chosen recipient nations do not share borders with the majority of G7 nations. As a result, beneficiaries from these nations are less likely than those from geographically proximate nations, like Mexico, to illegally cross borders into G7 nations and then ‘undercover’ their way to the United States. As a result, there may be a difference in the overall number of undocumented and documented migrants, and the numbers that are listed may not be accurate. Fourth, there may be differences between emigrants from the host country and migrants from the sending country. It is recommended that future research look at how remittances affect financial development at the national level. Lastly, remittance reporting may vary among nations.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Selected Remittance Receiving and Sending Countries.

| Type of Countries | List of Countries |

| Remittance receiving countries | Afghanistan, Bangladesh, China, India, Indonesia, Pakistan, Philippines, Sri Lanka, Thailand and Vietnam |

| Remittance sending countries | Gulf Cooperation Council (GCC) countries Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates The Group of Seven (G7) countries Canada, France, Germany, Italy, Japan, the United Kingdom and the United States. |