Abstract

In the beginning of 2025, Amy Wong, the Director of Rooms at the Whistler Blackcomb Hotel (WBH), is facing a crossroads in the operation of the business. WBH, despite being in the prime location in the heart of Whistler Village, has seen continuous decline in room revenue and share from 2022 to 2024. The main problem is the decrease in occupancy and revenue per available room, leading to decreased revenue in the Rooms division. The other issues facing the business are increased costs, underperforming contracts, and weakening brand loyalty. Amy is asked to address the dilemma of choosing between maintaining high-quality, sustainable business practices and premium eco-friendly suppliers, or adopting cost-containment strategies to ensure the profitability of the business. The case presents an opportunity for students to examine the data from the past 36 months, including ARI, MPI, and RGI, to determine if the decline in the business is due to pricing, age of the product, cost, or inefficiency. Ultimately, students must assume Amy’s role to present a data-driven action plan for revenue optimization and market differentiation to strengthen WBH’s position against its competitive set.

A Critical Turn for WBH

Amy Wong is the Director of Rooms at WBH with over 15 years of experience in hospitality operations; including a strong focus on cost control, revenue optimization, and operational efficiency. Since joining WBH in 2019, she has led the Rooms segment, where she achieved early progress but is now facing intensifying competition and a decline in profitability.

WBH’s profitability significantly declined between 2022 and 2024 particularly due to the rise of both traditional and P2P competitors like Airbnb and vacation rentals as well as evolving customer preferences, and post-COVID travel trends. In addition, rising labor and supply costs have increased operational pressure, especially as the hotel has attempted to preserve service quality. The Rooms segment has been particularly affected by short-term rental platforms which are now offering a more than 3,300 accommodations in Whistler (Airbnb Property Management in Whistler: Custom Revenue Report, n.d.).

As a result, WBH faces a complex challenge to regain lost profitability within its Rooms segment while responding to new guest expectations and aggressive competition. Given its limited capacity for capital investment, the hotel must focus on operational improvements and low-cost, high-impact strategies.

This case invites students to assume Amy’s role and conduct a structured evaluation of WBH’s historical, monthly, and competitive performance data to assess the Room segment’s financial and operational results. With limited capacity for major capital investment, students should examine a range of strategic and operational levers including pricing and distribution strategies, supplier contract negotiation, cost efficiency initiatives, technology integration, labor management, and service delivery improvements to address WBH’s performance gaps. While doing so, they must also evaluate the repercussion of their decisions, balancing short-term margin requirements such as cost savings versus guest experience with long-term brand integrity.

The Peterson Legacy and the Whistler Market

Whistler Blackcomb Hotel was originally built in 1994 by the Peterson Hotel Group and operated as Aurora Hotel until 2006 when it was suddenly it for sale. Capitalizing on this rare opportunity, local Lawson family group acquired the hotel for 75 million and rebranded it as Whistler Blackcomb Hotel. Due to their prior experience in the hospitality industry, they were able to retain the hotel’s 4-star property rating, positive customer reviews and profitability.

To remain competitive, the hotel underwent a major renovation in 2015 to enhance overall offering – primarily targeted at modernizing the interior and enhancing guest comforts. Some major upgrades included modern colors, furnishing, as well as a technology refresh that included Smart TVs, LED lights, and premium appliances. The 150-room property now includes 105 standard rooms, 37 suites, and 8 VIP apartments, all equipped with smart-card locks, high-speed internet, and premium in-room amenities. The rooms are further complemented by amenities such as a restaurant, spa, swimming pool, meeting spaces, and a fitness center.

Its location within the core of Whistler Village places the hotel within a short walking distance of world-class skiing, biking, and outdoor recreation opportunities. However, this beneficial location has created a challenge for the hotel in that its proximity to the slopes makes the hotel very sensitive to Whistler’s fluctuating seasonal demand patterns. During the peak winter and summer months, the village experiences its highest foot traffic, while the spring and fall periods are characterized by a quieter atmosphere.

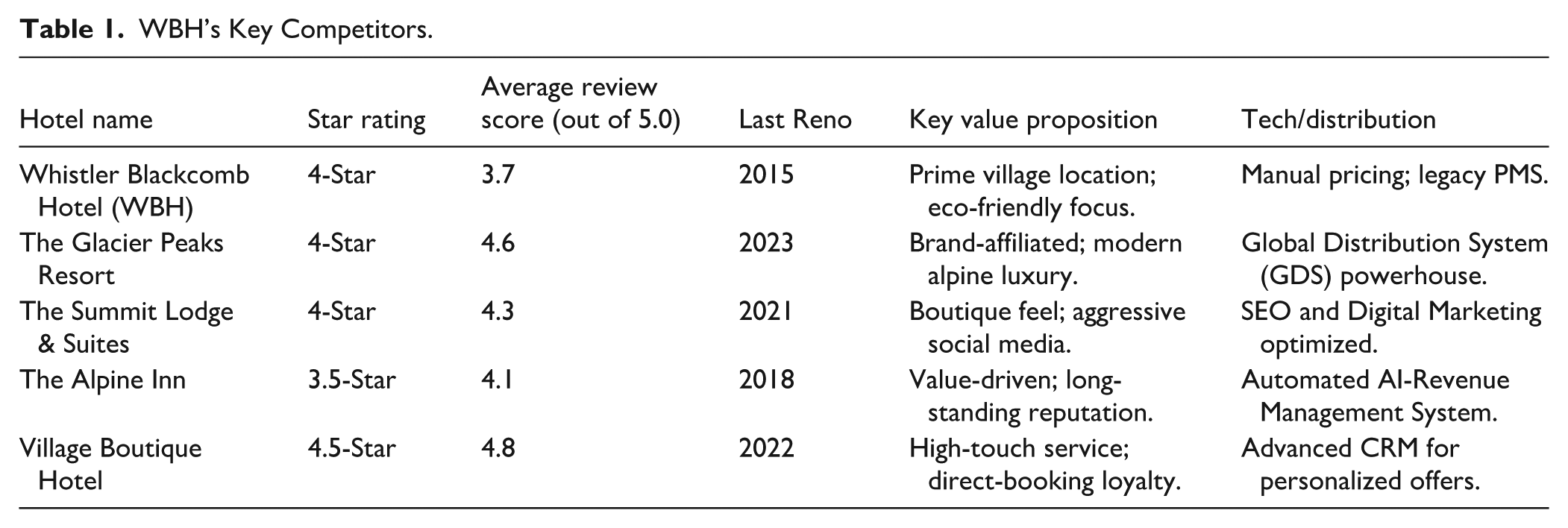

In terms of competitors, WBH primarily measures itself against a group of four main competitor hotels within the Village. They are The Glacier Peaks Resort, a brand-affiliated four-star hotel that completed a full renovation in 2023. The Summit Lodge & Suites, a boutique-style competitor known for their aggressive use of digital marketing, is a rival hotel to WBH. The Alpine Inn, a long-standing competitor, has just installed an automated Revenue Management System, while the Village Boutique Hotel boasts a significant number of loyal, repeat guests (Table 1).

WBH’s Key Competitors.

As Amy prepares for the 2025 strategic review, the contrast between WBH’s legacy status and these shifting competitor profiles has become a central point of internal discussion. While the 2015 renovation initially stabilized the property’s position, the current review scores and recent market shifts have prompted a re-evaluation of whether the hotel’s existing service model and product age can sustain its 4-star standing in an increasingly modernized Village.

A Fragmenting Market

WBH faces increasing competition from nearby three and four star hotels as well as a growing number of high-end Airbnb listings and vacation rentals. The unprecedented growth of alternative competitors – driven by their flexibility, diverse offerings, and all broad price range – is putting extreme pressure on the hotel’s ability to maintain occupancy rates and revenue. In fact, as of early 2025, Whistler has over 3,300 active vacation rental listings with an average occupancy rate of 64% and an average daily rate of $337 (Airbnb Revenue in Whistler, Canada: 2025 Short-Term Rental Data & Insights, n.d.). This supply increase is part of a larger regional trend; for example, traditional hotels in Whistler experienced a 9% reduction in occupancy in January 2024 compared to the previous year.

WBH’s management team has noted that the rates at which P2P properties are listed with higher nightly rates than traditional hotels. However, this is often due to the fact that the properties are often listed with multiple bedrooms rather than direct equivalents to single hotel rooms. This has sparked an internal debate over the interpretation of market share: whether it should be defined by a vacation rental’s ability to replace multiple hotel rooms, or whether the more important distinction lies in the experience gap between a managed 4-star hotel and a private P2P property.

Thus, WBH must not only compete on price and location but also on guest experience, personalization, and perceived value due to an increasingly diversified accommodation market. While the hotel can adopt selected strategies inspired by short-term rentals such as enhancing flexibility or offering value-added amenities, it’s immediate performance should ultimately be measured against nearby comparable hotels. Accordingly, the case later presents detailed benchmarking and monthly performance analysis to evaluate WBH’s position against its traditional competitive set.

As Amy prepares for the 2025 strategic review, the dichotomy between the legacy status of WBH and the changing market profiles has become a key concern. The rise of modernized traditional competitors and the P2P inventory has led to a review of the prevailing service model of WBH. The question is whether the performance gaps of the hotel are due to market disruptions, internal product misalignment, or a combination of both.

A Look at the Books (2022–2024)

The financial statements of the Rooms segment show a period of transition and increasing pressure for WBH. Since 2022, the property has faced a changing market in Whistler, marked by changing guest preferences and an increase in traditional and alternative accommodation choices. At the same time, rising labor, operating, and distribution costs have placed additional pressure on margins. The 3-year summary (see Table 2) highlights the effect of these factors on the hotel’s performance indicators.

WBH’s 3-year Summary (2022–2024).

Although the hotel was successful in lowering its direct costs significantly from $3,000,000 in 2022 to $2,600,000 in 2024, it was a response to the larger trend of declining revenues. Overall room revenues decreased by $2.5 million over the period due to a combination of declining occupancy rates and Average Daily Rate (ADR).

This imbalance has led to a visible compression of gross margins, as the $400,000 in cost savings proved insufficient to protect the bottom line. Further, the 2024 year-end figures have initiated internal debate on the effectiveness of the “volume-at-all-costs” strategy as nights sold continued to trend downward during the period despite lower rates. While the hotel has become more cost-efficient in terms of Cost per Occupied Room (CPOR), the large decline in GOPPAR has left management questioning whether even the most disciplined cost-control measures can offset the sustained loss of the hotel’s premium pricing power.

To understand if the cause of the decline is a sign of market timing or a fundamental product issue, it is necessary to examine the asset more closely. The inventory levels at WBH have been stagnant since the renovation in 2015. The hotel has 150 rooms, which are heavily skewed toward the mid-market traveler (Table 3).

WBH’s Room Type Mix.

While the standard rooms remain as the workhorse for the hotel by maintaining highest occupancy levels, the premium rooms do not share the same trend. In fact, feedback from the concierge has been that high-net-worth individuals are increasingly opting to stay at one of the newer luxury resorts, or one of the premium multi-bedroom vacation rental options which offer modernized tech suites and a different set of amenities such as privacy and serenity.

The pricing for the eight VIP apartments is at a significant premium, yet these rooms remain largely empty even during periods when Whistler Village is thriving. This failure has led to internal debates within the management team regarding the hotel’s tiering strategy. One perspective suggests lowering the barrier to entry for the suites to drive volume, while another argues that this would further dilute the 4-star brand positioning and lead to further margin erosion.

The 2024 results highlight a significant concentration in mid-tier bookings. Thus, a number of pertinent questions must be asked for the upcoming fiscal year such as if current marketing strategies are effective in capturing the desired premium segments, or if the product offering has become out of alignment with high-end guest value perceptions.

To determine if this reliance upon mid-tier volume is an ongoing struggle throughout the year or an artifact of the natural cycles of the resort, it is necessary to shift from the absolute numbers of inventory to the timing of bookings.

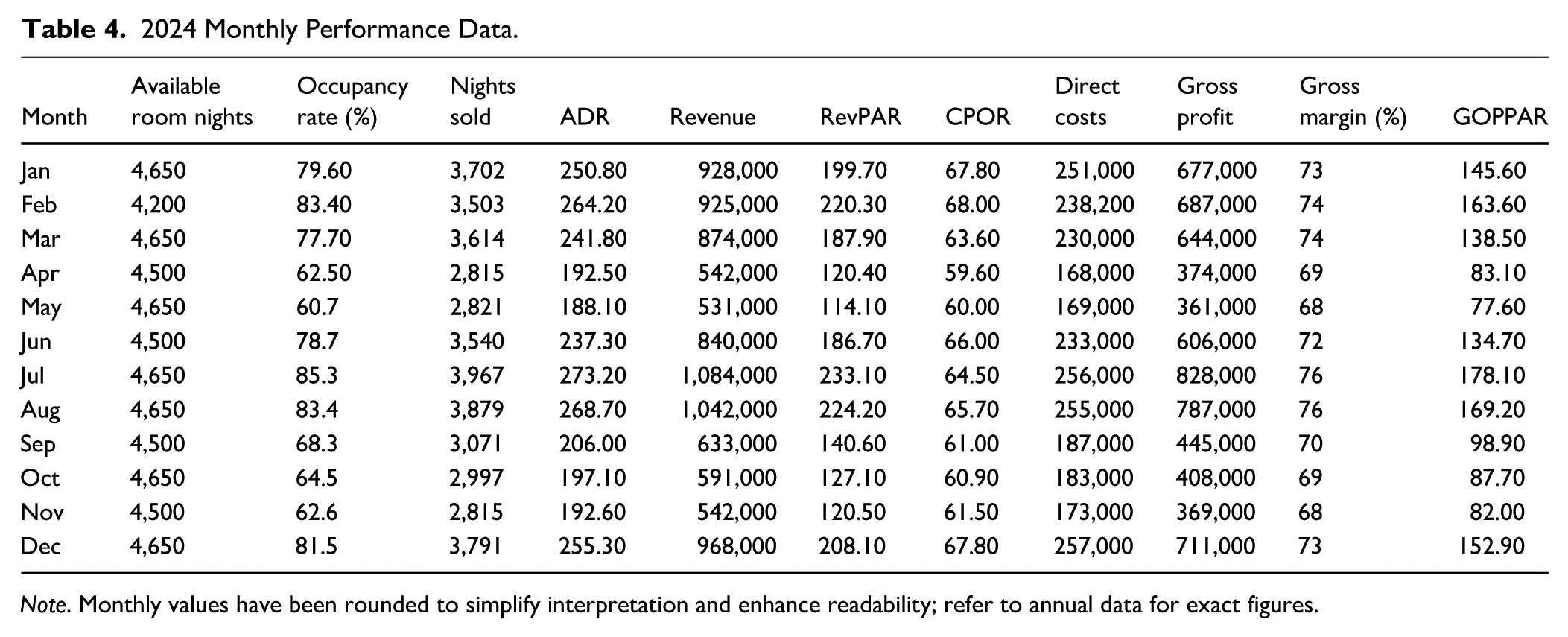

The 2024 monthly performance data (see Table 4) represents the extreme seasonality associated with the tourism market in Whistler. Although the winter and summer months remain the main revenue generators for the WBH, the variability between the peak and off-peak seasons poses a major challenge.

2024 Monthly Performance Data.

Note. Monthly values have been rounded to simplify interpretation and enhance readability; refer to annual data for exact figures.

During the peak of the winter and summer seasons, the occupancy levels consistently sit at 80% to 85%, which allows for a much stronger Average Daily Rate (ADR). However, this trend takes a dramatic shift during the spring and fall shoulder seasons when the occupancy levels drop as low as 60%. These fluctuations are reflected in the hotel’s RevPAR, which experiences its biggest declines during the shoulder months of April-May and October-November. Despite these fluctuations in volume, the Cost per Occupied Room (CPOR) manages to remain consistent throughout the year, indicating a consistent approach to cost management.

This trend has created a large concentration of revenue within just 5 months of the year, making the hotel vulnerable to the risks of the off-season. Although the hotel excels at maintaining a high level of “flow-through” efficiency during these peak months, successfully converting a larger portion of every RevPAR dollar into GOPPAR, the trend of falling ADR and volume continues to squeeze the hotel’s margins. The persistence of the 3-year decline has forced a re-evaluation of WBH’s current operational and pricing strategies. While the hotel has managed to hold baseline occupancy levels by reducing the Average Daily Rate (ADR) during the spring and fall, these adjustments have significantly impacted overall room yield and profitability. This has led to a divide within the management team: some advocate for continued blanket rate cuts to maintain volume, while others argue for a more targeted approach that protects rate integrity on high-demand days.

From an operational standpoint, the team has successfully stabilized Cost per Occupied Room (CPOR) through disciplined expense management. However, the continued underperformance during the shoulder months has raised a critical question: has the hotel reached the limit of what cost-cutting can achieve. Some argue that the path back to profitability requires looking beyond the balance sheet to innovate in marketing, distribution, and the guest experience to stimulate demand during Whistler’s quieter periods.

Benchmarking Against the Village (2024)

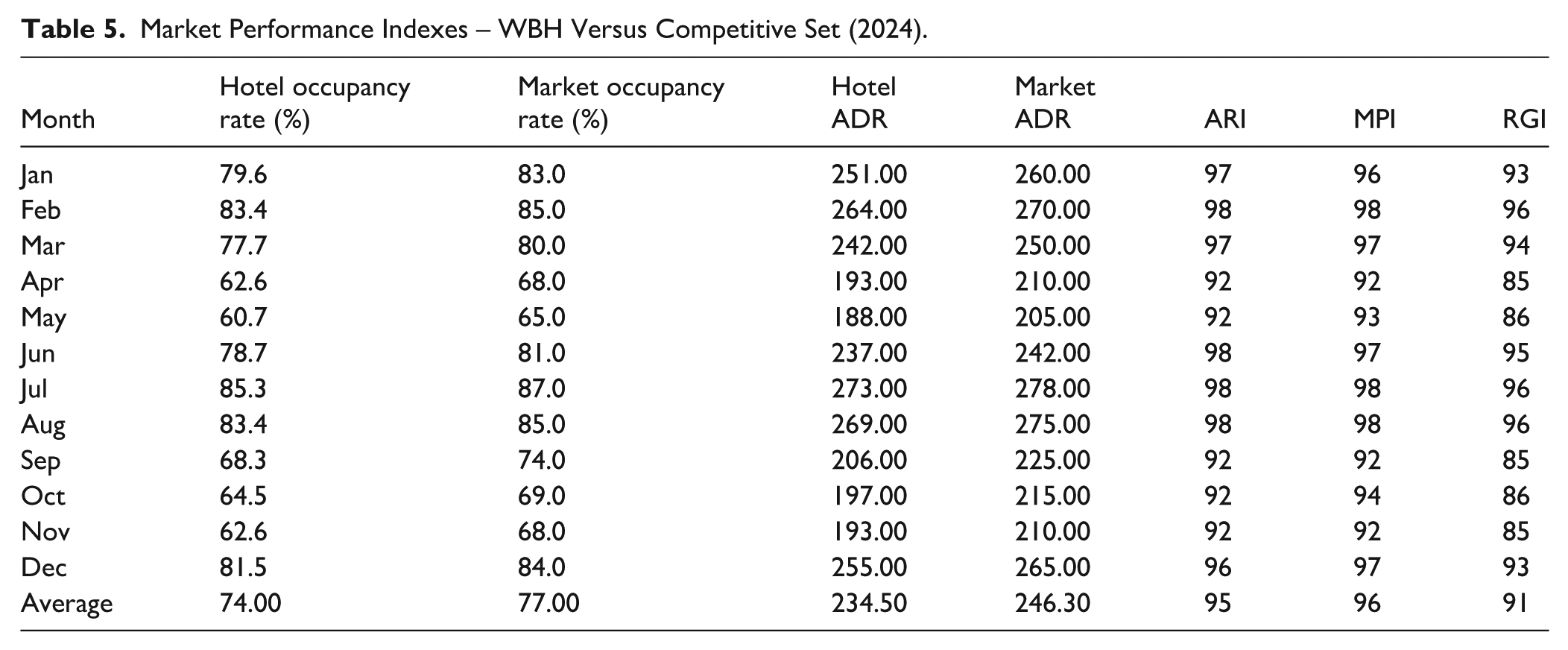

To better understand WBH’s market positioning, the hotel’s performance was compared against competing 4-star properties in Whistler using three industry-standard benchmarking indicators:

These indexes help evaluate the property’s relative pricing, occupancy penetration, and overall revenue competitiveness throughout the year (Table 5).

Market Performance Indexes – WBH Versus Competitive Set (2024).

The benchmarking data reveal that WBH consistently trails its competitive set throughout 2024, even during peak winter and summer months when market occupancy and ADR reach their highs. With ARI, MPI, and RGI all slightly below 100 throughout the year, WBH captures a smaller share of market demand and pricing power than leading competitors.

The hotel’s underperformance is even more pronounced in the shoulder season (April–May, September–November), where occupancy and rate indices drop to the low 90s. In particular, during peak winter and summer periods, the hotel performs closer to market averages, with RGI values near 96, indicating relatively competitive performance. However, in the spring and fall, both occupancy and ADR decline sharply, driving RGI down to 85–86; thus, leading to an average RGI of only 91 for the year.

While these indexes provide valuable benchmarking insights, they do not capture the growing impact of peer-to-peer (P2P) accommodation platforms such as Airbnb, which now account for a significant share of Whistler’s lodging capacity. Research by Dogru et al. (2019) found that increased Airbnb supply leads to lower hotel occupancy and ADRs, particularly in leisure destinations with limited room inventory such as mountain resorts.

This suggests that WBH’s underperformance relative to its competitive set may not be purely an internal issue, but also a symptom of broader market disruption driven by alternative accommodations. As demand fragments between hotels and short-term rentals, traditional benchmarks should be interpreted with caution, as they may not fully account for these external pressures. Therefore, while market disruption from alternative accommodations is an acknowledged factor in the resort’s evolving dynamics, the question for WBH is whether its current performance is a symptom of these external pressures or a result of specific disadvantages when compared to its traditional comp set.

Efficiency Versus Excellence: The Operational Balance

The year-end review of the Rooms segment revealed an increasing disparity between the performance of standard rooms and premium room offerings. As revenue generated by the hotel still heavily favors the midscale segment, premium product offerings such as suites and VIP rooms still experience occupancy challenges. This has led to internal debate about whether or not the current rate structure of premium product offerings truly reflects the value proposition of modern high-spend travelers, or if the hotel is simply falling behind newer luxury product offerings and upscale vacation rentals in terms of rate competitiveness.

On the expense side, management has continued to emphasize cost containment initiatives in spite of rising inflationary pressures. Current initiatives have successfully stabilized Cost per Occupied Room (CPOR) through diligent oversight of housekeeping and maintenance departments. However, as expenses continue to pressure margins, there has been a rigorous examination of all variable expense categories.

One of the most pressing debates revolves around whether or not further efficiencies can be realized by optimizing staff scheduling, automating processes, or taking a more aggressive approach toward supplier rationalization. Although these operational initiatives provide an opportunity to further reduce expenses, they also pose an important question: when does optimizing these areas begin to compromise guest amenities and services that are critical to maintaining the hotel’s brand identity.

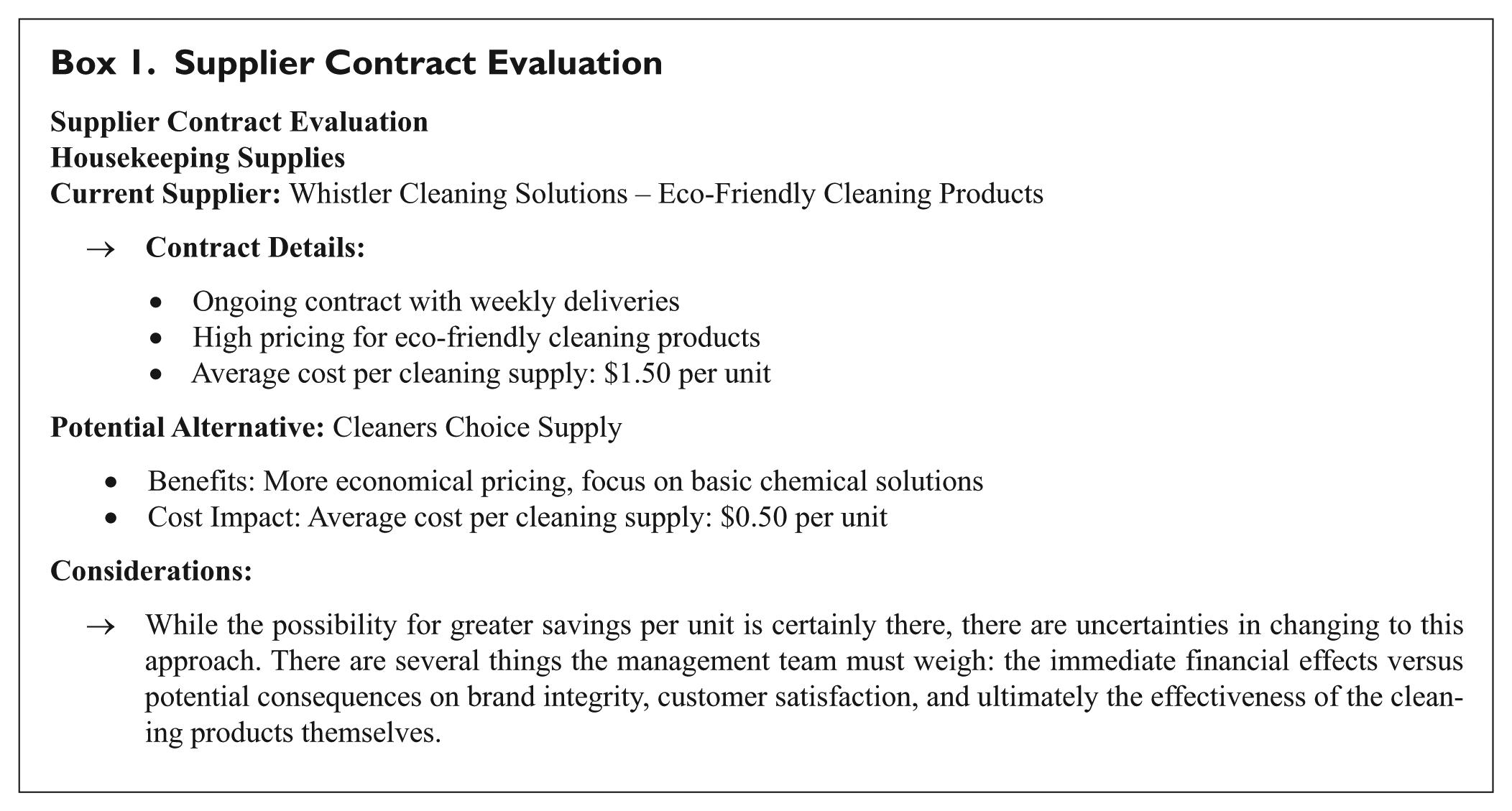

Specifically, one of the most contested cost containment initiatives revolves around the purchase of housekeeping supplies. Although WBH has always placed a high priority on minimizing its environmental footprint, the cost difference between current eco-friendly contracts and industrial-grade supplies has become an important part of the 2025 budget debate (Box 1).

Supplier Contract Evaluation

Mapping the 2025 Strategy

As WBH prepares for the next fiscal year, several internal proposals have been generated to enhance the standing of the hotel and get it out of revenue decrease. These initiatives represent different strategic directions for the property:

Conclusion

Currently, the Whistler Blackcomb Hotel faces a critical crossroads. The continued decline in revenue and market share since 2022 suggests that the new post-pandemic environment requires a more fundamental level of strategic readjustment than that achieved by the incremental changes of previous years. Though the cost discipline has succeeded in driving down the Cost per Occupied Room (CPOR), the increasing gap in competitive benchmarking and the significant level of value gap against its newly modernized competitors are clearly major hurdles for the hotel.

As the road to profitability requires complex decisions between short-term business efficacy and long-term brand differentiation, it is crucial that the new strategy identifies those areas of revenue, technology, or supply that will best address the challenge of restoring WBH’s competitive positioning without sacrificing its heritage as a 4-star hotel. With the approaching shoulder season, the focus will shift from simple business discipline to a broader question: How will WBH reclaim its place as a premium resort in an environment that has experienced unprecedented change?

Student Tasks

1. KPI Dashboard

Create a KPI dashboard for the Rooms Segment using data from 2022 to 2024. You are free to use tools such as Microsoft Excel, SimpleKPI, or Google Data Studios. Use the provided data, only calculating additional KPIs as necessary.

ADR, Occupancy Rate, and RevPAR (2022–2024 and monthly 2024). Compare this with a hypothetical incremental ADR Increase of 10% on 2024s value

CPOR and GOPPAR (2022–2024 and monthly 2024)

ARI, MPI, and RGI versus competitive set (2024)

Revenue share by room type (Standard, Suite, VIP)

Visualization of seasonality – monthly/seasonal occupancy, ADR, RevPAR trends

Then, in 1 to 2 short paragraphs, summarize three key insights from your dashboard:

Briefly mention how 2024 compares to 2022 to 2023.

Identify months where occupancy or ADR peaked/dipped and explain why.

Interpret ARI, MPI, and RGI – are they below or above 100? What does that mean for market share and rate competitiveness?

Comment on which room types drive most revenue.

What patterns might guide your strategic choices?

2. Strategic Analysis Tracks

Students should select either Track A or Track B to guide their analysis, or compare both if instructed.

Focus on strategies to increase top-line performance while enhancing WBH’s appeal in a competitive landscape:

○ Examine the impact of dynamic pricing on the Rooms segment, specifically considering off-peak periods.

○ Recommend strategies to improve room occupancy, such as package offerings or targeted marketing to improve occupancy rates, ADR, and revenue.

○ Investigate the potential benefits of upselling strategies, such as offering add-ons or room upgrades at check-in.

Analyze how WBH can improve its margin through supplier evaluation, process redesign, and tech adoption without compromising guest experience:

Consider the impact of switching to a more cost-effective supplier for housekeeping supplies–evaluate cost, brand value, guest satisfaction, and CPOR impact.

Explore possibility of technology integration such as automated check in/check out kiosks and/or internal tools like Property Management System (PMS), and Revenue Management Software that could reduce CPOR without affecting guest experience.

Research how client reviews and feedback can be used through digital marketing to reach new customers.

Consider trade-offs between cost savings, sustainability, and brand positioning

3. Competitive Benchmarking

Using the benchmarking data and market context provided in the case:

Interpret WBH’s ARI, MPI, and RGI values for 2024, what do these indexes reveal about WBH’s pricing, occupancy, and revenue share? How do these indexes correlate with WBH’s Review Score (3.7) and last renovation date (2015) compared to its peers?

Based on the competitor table, identify two specific reasons why WBH is suffering from a “Value Gap” (where both price and occupancy are below market average).

Identify two main reasons WBH trails its comp set and propose one measurable strategy to improve each index.

Suggest how WBH could improve each index through pricing, marketing, or distribution strategies.

Reflect briefly on whether traditional benchmarking adequately captures WBH’s competitive reality given the rise of short-term rentals, or if the quality gap against traditional hotels still remains the primary threat.

4. Memo to Management

Draft a professional memo addressed to management, summarizing:

Dashboard insights (Task 1 highlights)

Strategic recommendations from your chosen track(s)

Competitive benchmarking summary

A short “Action Plan” table (3–5 specific steps, timelines, expected KPI improvements)

Your memo should reflect data-driven reasoning, recognize operational trade-offs, and propose feasible strategies that can improve WBH’s revenue and profitability relative to its comp set.

If you are an ICHRIE member, you can access the Teaching Notes for this case study here: https://ichrie.memberclicks.net/jhtc. If you are not an ICHRIE member, the Teaching Notes will be published in a future Sage Business Cases (SBC) annual collection: https://sk.sagepub.com/cases. For more information, please contact

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.